NAZARA Technologies: India's Gaming Empire Story

I. Introduction & Opening

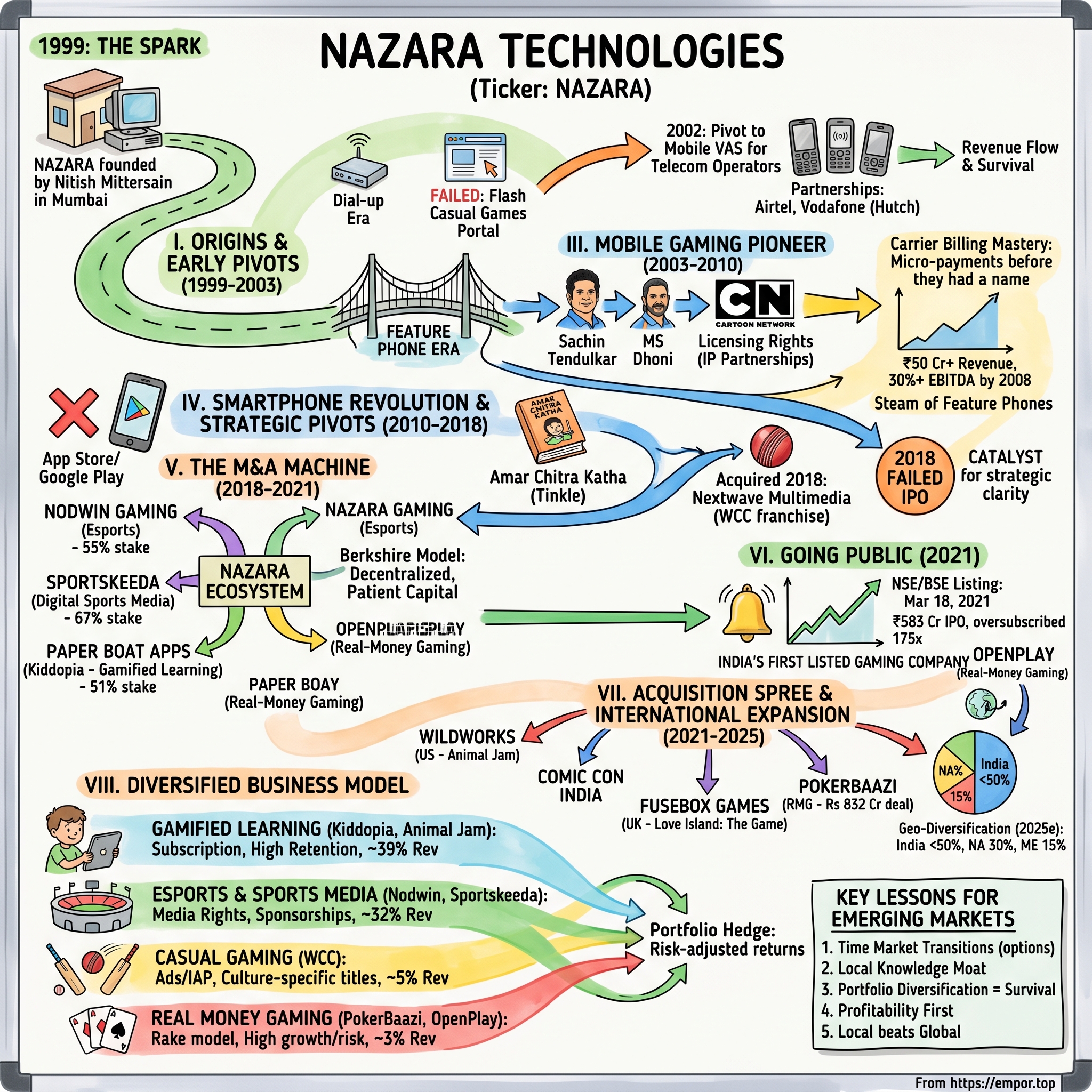

Picture this: It's 1999, Mumbai. The city's cyber cafes are packed with teenagers waiting their turn to play Counter-Strike on bulky CRT monitors. Dial-up modems screech their distinctive handshake across the city. In this pre-smartphone, pre-broadband India, a 23-year-old Nitish Mittersain is obsessed with gaming. Not just playing games—but the radical idea that Indians could build a gaming business. His friends think he's crazy. Gaming? In India? Where most people don't even have computers?

Fast forward to March 18, 2021. The bell rings at the National Stock Exchange as Nazara was listed on the NSE and BSE after its initial public offering. The company that started in a small Mumbai office during the dot-com boom had become India's first and only publicly listed gaming company, valued at over ₹1,600 crores. The journey from dial-up dreams to digital dominance had taken 22 years.

But here's what makes this story fascinating for students of business strategy: Nazara didn't build a single blockbuster game that conquered the world. They didn't create India's Fortnite or Call of Duty. Instead, they built something arguably more valuable—a gaming conglomerate that survived multiple technology shifts, regulatory upheavals, and market crashes. They zigged when others zagged, buying when others were selling, and somehow emerged as the consolidator of India's fragmented gaming ecosystem.

The central question we'll explore: How did a college student's gaming obsession during the dial-up era transform into a multi-billion rupee gaming empire? And more importantly, what can this teach us about building technology businesses in emerging markets where the infrastructure, regulation, and consumer behavior are all moving targets?

This is a story about patience in an impatient industry, about building picks and shovels while others chased gold, and about the unglamorous work of turning a nascent market into a real business. It's the Acquired-style deep dive into how Nazara became the Berkshire Hathaway of Indian gaming—not through operational excellence in a single vertical, but through strategic capital allocation across the entire gaming value chain.

II. The Origin Story: Nitish Mittersain & Early Internet India (1999-2003)

The year 1999 was peculiar in Indian tech history. Y2K paranoia had inadvertently made India the world's back office, with armies of programmers fixing COBOL code for American banks. The internet was exotic—something you experienced in cyber cafes at ₹60 per hour, downloading a single MP3 taking 15 minutes. Into this primordial digital soup stepped Nitish Mittersain, fresh out of college, with an idea that seemed absurd: Indians would pay for digital entertainment.

Nazara was founded when the internet was still in its nascent stage, with dial-up connections ruling the market. The company has primarily come into existence as a result of the founder's immense love for gaming. Back in 1999, when Nazara was founded by Mittersain, the company began as an online portal for casual games. But this wasn't Silicon Valley where venture capitalists threw money at anything with a .com suffix. This was Mumbai, where Mittersain had to explain what an "online game" even meant to potential investors.

The initial business model was straightforward yet naive: create a destination site where Indians could play Flash-based games. Think Miniclip or Kongregate, but for the Indian market. The portal featured everything from chess to racing games, all running on browsers that took 30 seconds to load a basic webpage. Revenue model? Banner advertisements and the hope that someday, somehow, Indians would pay for premium gaming content.

By 2001, reality hit hard. The dot-com bubble burst globally, but in India, it was more like a dot-com whimper—there wasn't enough of a bubble to burst. Nazara was burning through capital with virtually no revenue. The portal had users, sure, but users on dial-up connections weren't exactly a monetizable audience. Mittersain faced the classic founder's dilemma: pivot or perish.

In 2002, it switched to providing mobile entertainment VAS for telecom operators, including WAP content downloads of comic strips and mobile games. This pivot seems obvious in hindsight, but consider the context: mobile phones in 2002 India were luxury items, owned by less than 2% of the population. The screens were monochrome, the memory measured in kilobytes, and "mobile gaming" meant Snake on a Nokia 3310.

But Mittersain saw something others missed. Unlike PCs, which required significant capital investment and technical knowledge, mobile phones were spreading rapidly among India's middle class. More importantly, telecom operators were desperate for content to drive data usage on their nascent GPRS networks. They needed reasons for subscribers to use data beyond SMS.

The VAS (Value Added Services) model was ingenious in its simplicity. Nazara would create simple mobile games and content, telecom operators would promote them to subscribers, and revenue would be shared. No complex payment gateways, no credit card penetration issues—just add it to your phone bill. It was micropayments before anyone called them micropayments.

The early content was primitive by today's standards: Java-based games that were essentially mobile versions of Flash games, comic strips optimized for 128x128 pixel screens, and cricket score updates. But in a country starved for digital entertainment, where a movie ticket cost ₹50 and a mobile game cost ₹5, the value proposition was clear.

By 2003, Nazara had partnerships with Airtel, Vodafone (then Hutch), and other major operators. Revenue was finally flowing. The company that almost died chasing desktop gamers had found its lifeline in 2-inch mobile screens. But this was just the beginning. The real explosion was yet to come, riding on the back of Bollywood, cricket, and the unique Indian obsession with both. The feature phone era was about to begin, and Nazara had positioned itself perfectly at the intersection of mobile technology and Indian pop culture.

III. The Mobile Gaming Pioneer Phase (2003-2010)

The feature phone era in India was a goldmine disguised as a graveyard. Between 2003 and 2010, mobile penetration in India exploded from 25 million to over 750 million subscribers. But these weren't iPhones or Androids—they were Nokia 6600s, Sony Ericsson W810is, and countless Chinese knockoffs with 2-inch screens and T9 keypads. For most companies, creating engaging content for these devices seemed impossible. For Nazara, it was the opportunity of a lifetime.

The key insight was understanding the "carrier deck"—the walled garden of content that telecom operators controlled. Before app stores democratized distribution, getting your game onto a carrier's deck was like getting shelf space at Walmart. It required relationships, revenue sharing agreements, and most importantly, content that operators believed would drive data usage. Nazara had cracked this code early.

Early likeness rights partnerships to deliver mobile content included those with Archie Comics, Sachin Tendulkar, MS Dhoni and Cartoon Network. These weren't random choices—they were surgical strikes at the heart of Indian pop culture. Consider the Sachin Tendulkar mobile game launched in 2006. In a country where cricket is religion and Sachin is God, having an officially licensed Sachin game on your Nokia was the 2006 equivalent of having Fortnite on your iPhone.

The MS Dhoni partnership came at a particularly fortuitous time—right after India's 2007 T20 World Cup victory, where Dhoni's long-haired, helicopter-shot-playing persona captured the nation's imagination. The game was simple: time your shots, score runs, priced at ₹30. It sold over 2 million downloads in six months. For context, this was when the entire Indian gaming market was estimated at less than $20 million.

But the real genius was in the business model innovation. While Western markets were still figuring out micropayments, Nazara had perfected the art of carrier billing. No credit cards needed, no complex sign-ups—just reply 'YES' to an SMS and the game was yours, charged directly to your mobile bill. In a country where credit card penetration was under 2%, this was revolutionary.

Nazara later expanded mobile games VAS into the Middle East. This wasn't random international expansion—it was following the money. The Middle East had similar dynamics: high mobile penetration, low credit card usage, young demographics, and crucially, Indian expatriate communities hungry for cricket and Bollywood content. The same Dhoni game that worked in Delhi worked in Dubai.

The numbers from this era are staggering when adjusted for context. By 2008, Nazara was generating over ₹50 crores in revenue, with EBITDA margins above 30%. This was a capital-light, high-margin business model that printed cash. While global gaming companies were burning millions creating console games, Nazara was profitable selling ₹10 cricket games to feature phone users.

The 2008 financial crisis barely dented the business. If anything, it accelerated Nazara's growth. As Western gaming companies pulled back from emerging markets, Nazara doubled down. They acquired distressed gaming assets, hired laid-off developers, and expanded their content library. While Lehman Brothers was collapsing, Indian teenagers were downloading Nazara's "Dhoom 2" racing game based on the Bollywood blockbuster.

By 2010, Nazara had built what was essentially the Steam of feature phones in India and the Middle East. They had over 100 games across multiple genres, partnerships with every major telecom operator, and a war chest of cash from their profitable operations. They had survived the dot-com bust, thrived through the feature phone era, and built a distribution network that reached hundreds of millions of users.

But storm clouds were gathering. In 2008, Apple had launched something called the App Store. Google was working on something called Android. The smartphone revolution was coming, and it would destroy the comfortable carrier deck monopoly that Nazara had spent years building. The question wasn't whether to adapt, but how quickly they could transform their entire business model before the feature phone goldmine turned into a graveyard. The company that had successfully navigated one platform shift was about to face its biggest challenge yet.

IV. The Smartphone Revolution & Strategic Pivots (2010-2018)

The iPhone launched in India in 2008, priced at ₹31,000—more than most Indians' monthly salary. Mittersain wasn't worried. But when the Micromax A50 Android phone launched in 2011 for ₹4,999, he knew everything was about to change. The carrier deck kingdom that Nazara had built over a decade would crumble in mere months. The democratization of app distribution through Google Play meant any teenager with basic coding skills could now compete with Nazara. The moat had evaporated overnight.

Lesser companies would have panicked. Nazara did something counterintuitive: they decided to stop competing on development and instead become the arms dealer in the mobile gaming wars. If everyone could now make games, the valuable position would be publishing, marketing, and distribution. It was a strategic pivot that would define the next decade.

The first major move in this direction came through IP partnerships that actually mattered to Indian audiences. In 2016, Nazara tied up with Indian comics company Amar Chitra Katha to develop mobile games on Tinkle characters like Shikari Shambu. In 2018, Nazara acquired a majority stake in Nextwave Multimedia, a Chennai-based mobile game developer known for World Cricket Championship titles.

The World Cricket Championship (WCC) acquisition was particularly brilliant. Nextwave had built what was arguably India's most successful mobile gaming franchise, with over 100 million downloads. But they were struggling with monetization and user acquisition costs in the post-carrier-deck world. Nazara brought capital, publishing expertise, and most importantly, the patience to build a franchise rather than chase quick hits.

The WCC deal also revealed Nazara's emerging M&A philosophy: buy proven IP with established user bases, not moonshot technologies. While venture capitalists were pouring money into AR/VR gaming startups, Nazara was acquiring cricket games that actual Indians were playing on their Xiaomi phones.

But the real test of Nazara's evolution came with their failed 2018 IPO attempt. The company filed draft papers to raise ₹750 crores, valuing themselves at approximately ₹3,000 crores. The market's response was lukewarm at best. Investors didn't understand the business model—was it a gaming company? A publisher? A mobile VAS player? The subscription revenues from the feature phone era were declining, the new smartphone gaming business was still subscale, and the company seemed to be everything and nothing simultaneously.

The IPO was withdrawn, officially due to "market conditions," but insiders suggest a different story. The investment bankers couldn't figure out how to pitch Nazara. It wasn't a pure-play gaming company like Zynga. It wasn't a platform like Steam. It was this weird conglomerate of gaming assets across different verticals, geographies, and business models. The market wanted focus; Nazara offered diversification.

This rejection became a catalyst. Between 2018 and 2021, Nazara would go on an acquisition spree that would transform it from a gaming company into a gaming ecosystem. But first, they needed to answer a fundamental question: What was Nazara, really?

The answer Mittersain arrived at was profound in its simplicity: Nazara wasn't a gaming company; it was an interactive entertainment conglomerate for emerging markets. Just as Disney wasn't just an animation studio but an entertainment ecosystem, Nazara would be the platform for all forms of digital interactive entertainment in India and similar markets.

This reframing changed everything. Suddenly, acquiring an esports company made sense. Investing in gamified learning apps wasn't a distraction—it was expanding the TAM. The failed IPO had forced Nazara to articulate its vision clearly, and that clarity would drive the next phase of aggressive expansion. The smartphone revolution hadn't killed Nazara; it had forced it to evolve into something more ambitious.

V. The M&A Machine: Building Through Acquisitions (2018-2021)

If 2018's failed IPO was Nazara's Valley Forge moment, what followed was their march to victory. Between 2018 and 2021, Nazara would execute one of the most aggressive M&A strategies in Indian tech history, deploying over ₹500 crores to acquire strategic assets across gaming, esports, and digital sports media. This wasn't spray-and-pray acquisition; each deal fit into a larger thesis about the future of interactive entertainment in emerging markets.

The first major move was acquiring 55% stake in esports firm Nodwin Gaming. When this deal was announced, most investors scratched their heads. Esports in India? In 2018, the entire Indian esports market was valued at less than $5 million. PUBG Mobile hadn't even launched. But Mittersain saw what others missed: India had 400 million millennials, the world's cheapest data, and a generation that would rather watch gaming than cricket.

Nodwin wasn't just any esports company. Founded by Akshat Rathee and Gautam Virk, it had organized the ESL India Premiership and had exclusive rights to operate ESL events in India. While revenues were minimal, they had something invaluable: relationships with every major game publisher and a stranglehold on Indian esports infrastructure. Nazara paid ₹55 crores for the stake. By 2024, Nodwin's valuation would exceed ₹2,000 crores.

In 2019, Nazara Technologies purchased a 67% stake in Sportskeeda for ₹44 crore. It acquired a 51% stake in Paper Boat Apps, the developer and publisher of gamified early learning app Kiddopia, for ₹83.5 crore in the same year. These weren't random diversifications—they were calculated bets on adjacent markets.

Sportskeeda was fascinating. It wasn't a gaming company at all—it was a digital sports media platform with 30 million monthly users consuming cricket, football, and WWE content. But Mittersain understood something crucial: the same 16-25 year old consuming gaming content was also consuming sports content. The advertising dollars would flow to whoever could aggregate this audience's attention. Sportskeeda gave Nazara a media arm that could promote its games while generating independent revenues.

The Kiddopia acquisition was even more strategic. The gamified learning app for 2-7 year olds had cracked the US market—something no Indian gaming company had successfully done. With over 1 million downloads and $5 monthly subscriptions, it was generating predictable SaaS-like revenues. While Indian gaming companies were fighting over advertising dollars, Kiddopia was quietly extracting subscription revenues from American parents.

The M&A philosophy that emerged had three pillars:

- Geographic Diversification: Don't be overly dependent on Indian regulatory whims

- Revenue Model Diversification: Mix ads, subscriptions, in-app purchases, and media

- Demographic Diversification: From toddlers (Kiddopia) to millennials (Nodwin)

But the real genius was in the integration strategy—or lack thereof. Unlike traditional conglomerates that forcefully integrated acquisitions, Nazara operated more like Berkshire Hathaway. Founders were retained, brands were maintained, and operational independence was preserved. Nazara provided capital, shared services (like user acquisition expertise), and cross-selling opportunities, but didn't meddle in day-to-day operations.

This approach had an unexpected benefit: it made Nazara the preferred buyer for gaming entrepreneurs looking for exits. While strategic buyers would gut the company and financial buyers would flip quickly, Nazara offered something unique: patient capital with operational freedom. Word spread in India's gaming ecosystem—if you wanted to sell, Nazara would give you the best cultural fit.

By early 2021, Nazara had transformed from a mobile gaming company into what investment bankers now understood: a diversified digital entertainment play with multiple revenue streams, geographic diversity, and exposure to secular growth trends like esports and edtech. The company that couldn't explain itself in 2018 now had a story that resonated.

The IPO window was opening again, and this time, Nazara was ready. The M&A spree hadn't just built a bigger company—it had built a more understandable one. The market might not value a mobile gaming company properly, but a diversified digital entertainment conglomerate with predictable revenues across multiple verticals? That was a story investors could buy into.

VI. Going Public: India's First Listed Gaming Company (2021)

March 18, 2021. The NSE trading floor was empty—COVID protocols—but the virtual bells rang just as loudly. In March 2021, Nazara was listed on the NSE and BSE after its initial public offering. The ₹583 crore IPO was oversubscribed 175 times. The same investment community that had shrugged three years earlier was now clamoring for shares. What changed?

Everything and nothing. Nazara's business was fundamentally the same—a collection of gaming and digital entertainment assets. But the context had transformed completely. COVID-19 had forced 1.3 billion Indians into their homes, and digital entertainment had shifted from nice-to-have to essential. PUBG Mobile had been banned, creating a vacuum in Indian gaming. The FAANG stocks had shown that platform companies could generate trillion-dollar valuations. Suddenly, being "India's only listed gaming company" wasn't a curiosity—it was a scarce asset.

The IPO roadshow revealed how much investor education was still needed. Fund managers who understood Infosys and TCS struggled to grasp how a company could make money from "kids playing games on phones." Mittersain had to explain basic concepts: what is a daily active user? What's ARPU? Why does user acquisition cost matter? It was like teaching Security Analysis 101, but for digital businesses.

The pricing was conservative—₹1,100 per share, valuing the company at about ₹2,700 crores. This wasn't greed; it was strategy. Mittersain wanted long-term shareholders, not flippers. He explicitly marketed to domestic mutual funds and family offices who would hold for years, not hedge funds looking for quick gains. The allocation reflected this: 75% went to institutional investors, heavily weighted toward domestic funds.

The first day of trading told the story: the stock opened at ₹1,990, an 81% premium, before closing at ₹1,635. The financial media went wild—"Gaming Stock Rockets," "Nazara's Dream Debut." But Mittersain seemed almost embarrassed by the pop. In interviews, he kept emphasizing fundamentals, not stock price. This wasn't false modesty—he understood that being public meant quarterly scrutiny in an industry where hit games could take years to develop.

The immediate post-IPO period was treacherous. Retail investors who bought at the peak were underwater within weeks as the stock corrected to ₹1,200. Gaming companies globally were getting hammered as COVID tailwinds reversed. Apple's IDFA changes were destroying mobile marketing economics. The easy narrative of "COVID beneficiary" was falling apart.

But Nazara did something unusual for a newly public company: they accelerated M&A. While most companies pause acquisitions post-IPO to show organic growth, Nazara saw the market dislocation as an opportunity. Gaming valuations were crashing, quality assets were available, and they had both cash and public currency to deploy.

Later the same year, it acquired the Hyderabad-based real-money gaming company OpenPlay for ₹186 crore. This was controversial. Real-money gaming (RMG) was basically skill-based gambling—rummy, poker, fantasy sports. The regulatory environment was murky, with some states banning it entirely. But OpenPlay had built a profitable business with 1 million users and strong unit economics. More importantly, it gave Nazara exposure to a segment growing at 50% annually.

The public market reaction was mixed. Some investors loved the growth potential of RMG. Others worried about regulatory risk and ESG concerns. The stock volatility reflected this schizophrenia—swinging 10% on random state government announcements about online gaming regulation.

Being public also forced organizational changes. Nazara had to build investor relations capabilities, implement SOX-compliant controls, and most painfully, provide quarterly guidance in an inherently lumpy business. The freewheeling startup culture had to coexist with public company governance. Board meetings that once lasted an hour now stretched to six, with independent directors questioning every acquisition.

But the benefits outweighed the costs. The public listing gave Nazara something money couldn't buy: legitimacy. Global game publishers who wouldn't return calls before were now eager to partner with "India's only listed gaming company." Acquisition targets took them seriously. Talent wanted to join a company with listed stock options. The IPO hadn't just raised capital—it had transformed Nazara from a regional player to a platform for consolidating the Indian gaming ecosystem. And the acquisition machine was just getting started.

VII. The Acquisition Spree & International Expansion (2021-2025)

If Nazara's pre-IPO acquisitions were strategic chess moves, the post-IPO period was blitzkrieg. Armed with public currency and a war chest from the IPO, Mittersain went on an acquisition rampage that would make even the most aggressive private equity funds blush. Between 2021 and 2024, Nazara would deploy over ₹1,500 crores in acquisitions, fundamentally transforming from an Indian gaming company to a global interactive entertainment platform.

In 2022, Nazara acquired a 55% stake in Datawrkz, an advertising technology company based in Bangalore, for ₹124 crore. Later that year, it bought out the US-based kids gaming company WildWorks for $10.4 million. These weren't adjacent businesses—they were infrastructure plays. Datawrkz gave Nazara the ability to monetize its 200 million+ user base through programmatic advertising. WildWorks brought Animal Jam, a kids' virtual world with 150 million registered users and a proven subscription model in the US market.

The WildWorks acquisition was particularly revealing of Nazara's evolved thinking. Here was a 20-year-old Utah-based company that had built one of the most successful kids' gaming franchises in America. But they were struggling with the transition to mobile and needed capital for reinvention. Nazara paid what seemed like a bargain price for a brand that had generated over $100 million in lifetime revenues. The synergies with Kiddopia were obvious—shared user acquisition, cross-promotion, unified subscription bundles.

In 2024, Nazara acquired Comic Con India for ₹55 crore through its subsidiary Nodwin Gaming. On August 8, 2024, it had been announced that Nazara has acquired UK based Fusebox Games for $27.2 million. Comic Con India wasn't just an events business—it was a cultural gateway. With 500,000+ annual attendees across multiple cities, it gave Nazara direct access to India's most engaged pop culture enthusiasts. Every gaming company wanted presence at Comic Con; Nazara now owned it.

Fusebox Games represented Nazara's most ambitious international move yet. The UK studio behind "Love Island: The Game" had cracked the narrative gaming market with 100 million+ downloads. This wasn't Nazara's typical acquisition—no Indian IP, no emerging market focus. It was a pure play on Western casual gaming, particularly the underserved female demographic.

But the biggest swing came in September 2024: Nazara Technologies acquired 47.7% stake in Moonshine Technology, the parent company of PokerBaazi for Rs 832 crore. This was Nazara's largest acquisition ever, and its most controversial. PokerBaazi was one of India's leading online poker platforms, operating in the grey area of real-money skill gaming. The ₹832 crore price tag raised eyebrows—it valued PokerBaazi at over ₹1,700 crores, a rich multiple for a business facing constant regulatory uncertainty.

Mittersain's rationale was compelling though. Real-money gaming was growing at 50-60% annually in India. The government was moving toward regulation rather than prohibition—the GST council had legitimized the industry by taxing it. PokerBaazi had 3 million users, profitable unit economics, and most importantly, the operational expertise to navigate India's complex state-by-state regulations. While foreign competitors might enter eventually, they'd lack the regulatory relationships and local knowledge that took years to build.

The international expansion strategy that emerged from these acquisitions was sophisticated:

- Don't compete with Western studios on their turf—acquire them

- Focus on underserved demographics (kids, women, emerging markets)

- Build geographic natural hedges—US subscription revenues offset Indian advertising volatility

- Own the full stack—from content creation to distribution to monetization

By 2025, Nazara's revenue geography had transformed completely. India, which contributed 90% of revenues in 2018, now accounted for less than 50%. North America generated 30%, Middle East 15%, and the rest from other markets. The company that couldn't explain itself to Indian investors in 2018 was now truly global.

But this rapid expansion came with integration challenges. Nazara was now managing teams across 12 time zones, dealing with regulations in 20+ countries, and juggling multiple business models simultaneously. The hands-off integration philosophy that worked for Indian acquisitions was tested by cultural differences in Western studios. American developers didn't always appreciate Indian management styles, and British studios had different expectations about creative freedom.

The capital allocation framework had to evolve too. With so many portfolio companies, how did Nazara decide where to invest the next rupee? They developed a rigorous ROIC framework, treating each subsidiary like a public company with its own capital allocation. Businesses that generated high returns got more capital; those that didn't were starved or divested. It was Darwinian, but it worked. The acquisition spree hadn't just built a bigger Nazara—it had built a more resilient, globally diversified entertainment platform positioned for the next decade of growth.

VIII. Business Model & Unit Economics Deep Dive

To understand Nazara's business model is to understand why traditional valuation metrics fail to capture its essence. This isn't a single business—it's four distinct business models operating under one roof, each with different unit economics, growth profiles, and risk characteristics. The complexity that confused investors in 2018 had become the company's greatest strength by 2025.

Kiddopia in gamified early learning (39% of revenue), Nodwin & Sportskeeda in eSports (32%), WCC & CarromClash in simulation games (5%), and Halaplay Technologies in real money games (3%) are among Nazara's most well-known IPs, while Telco Subscription accounts for 21% of revenue.

Let's dissect each revenue stream:

Gamified Early Learning (39% of revenue): This is Nazara's crown jewel from a unit economics perspective. Kiddopia and Animal Jam operate on subscription models—$7.99 monthly in the US, ₹399 in India. Customer acquisition cost (CAC) runs about $15-20, but lifetime value (LTV) exceeds $80. The magic is in retention: parents rarely cancel their kids' educational subscriptions. Monthly churn is under 5%, creating predictable, SaaS-like revenues. Gross margins exceed 85% since content creation is a one-time cost amortized over millions of users.

Esports & Digital Sports Media (32% of revenue): This segment operates on three revenue streams: sponsorships (40%), media rights (35%), and ticketing/merchandise (25%). Nodwin's ESL events command ₹5-10 crore title sponsorships from brands desperate to reach 18-25 year old males. Sportskeeda monetizes through programmatic advertising at CPMs ranging from $0.50 in India to $5 in the US. The beauty is the network effects—bigger events attract more sponsors, which fund bigger events. Margins are lower (30-40%) due to event costs and content creation, but growth is explosive (60%+ annually).

Telco Subscriptions (21% of revenue): The legacy business that refuses to die. Feature phone gaming in Africa and Middle East still generates ₹200+ crores annually at 60%+ EBITDA margins. There's zero marketing spend—telcos push the content—and zero technology investment—the games were built years ago. It's melting ice cube, declining 10-15% annually, but throwing off cash that funds growth investments elsewhere.

Skill-Based Real Money Gaming (3% of revenue): Through PokerBaazi and OpenPlay, Nazara takes 5-10% rake on cash games. The unit economics are outstanding: CAC of ₹500-1000, but LTV exceeding ₹5,000 for regular players. The catch is that 80% of revenue comes from 5% of users—the "sharks" who play daily. Regulatory risk is real, but the 28% GST has paradoxically legitimized the business.

Casual Gaming (5% of revenue): WCC and CarromClash monetize through ads (60%) and in-app purchases (40%). These are hits-driven businesses where one successful game funds ten failures. WCC generates ₹50+ crores annually, but user acquisition costs have exploded post-IDFA changes. The strategy here is portfolio diversification—launch 20 games annually, hope 2-3 hit.

The genius of this portfolio approach becomes clear when you analyze the risk-return profiles:

- Subscriptions (kids gaming): Low risk, predictable growth, high margins

- Advertising (esports/media): Medium risk, high growth, moderate margins

- Telco: No growth but cash generative

- RMG: High risk, high growth, high margins

- Casual gaming: High risk, volatile returns

This diversification creates natural hedges. When Apple's privacy changes destroyed casual gaming economics, subscription revenues were unaffected. When Indian regulatory uncertainty hit RMG, US kids' gaming revenues provided stability. When COVID boosted gaming engagement, Nazara captured upside across all segments. When engagement normalized, the subscription base provided downside protection.

The capital allocation framework is equally sophisticated. Each business has different reinvestment needs:

- Kids gaming: 40-50% of revenues reinvested in content and user acquisition

- Esports: 60-70% reinvested in rights acquisition and event production

- Telco: 0% reinvestment, pure cash extraction

- RMG: 30-40% reinvested in product and compliance

- Casual: 70-80% reinvested in new game development and UA

At the consolidated level, Nazara generates ₹800+ crores in revenue at 15-20% EBITDA margins. But this understates the true economics—the mature businesses (telco, kids gaming) generate 30%+ margins, funding investments in high-growth areas (esports, RMG). It's a self-funded growth machine where cash from declining businesses funds bets on the future. The business model that seemed incoherent in 2018 had evolved into a sophisticated portfolio optimized for risk-adjusted returns across the entire interactive entertainment spectrum.

IX. Competitive Landscape & Market Position

Understanding Nazara's competitive position requires abandoning traditional competitor analysis. They don't have a single competitor—they have dozens across different verticals, geographies, and business models. It's like analyzing Berkshire Hathaway by comparing it to State Farm because they both sell insurance. The real question isn't who Nazara competes with, but whether their unique position as India's gaming conglomerate is defensible.

The India gaming market context is crucial. By 2025, India has become the world's largest gaming market by downloads (17 billion annually) but only fifth by revenue ($3.5 billion). The paradox is stark: 500 million gamers generating $7 per user annually, compared to $70 in China and $200 in the US. This isn't a market share game—it's about growing the pie while positioning for inevitable monetization improvement.

The competitive dynamics vary dramatically by segment:

In Kids Gaming, Nazara faces global giants like Roblox and Minecraft. But their localized content and parent-friendly positioning creates differentiation. Kiddopia isn't trying to be the next Roblox—it's targeting parents who want educational screen time. The competitive moat is trust, built over years of COPPA-compliant operations.

In Esports, the competition is fiercer. Krafton (PUBG maker) runs its own tournaments. Riot Games (League of Legends) might enter India directly. But Nazara's Nodwin has first-mover advantage and owns the infrastructure—from grassroots college tournaments to broadcast studios. When global publishers want to activate in India, they call Nodwin. It's the ESPN of Indian esports, and that position is hard to displace.

In Real Money Gaming, the landscape is brutal. Dream11 raised $400 million. Games24x7 (RummyCircle) is backed by Tiger Global. MPL has SoftBank money. These competitors have 10x Nazara's marketing budget. But Nazara isn't trying to win the customer acquisition arms race. They're playing a different game—acquiring profitable platforms with established user bases and optimizing operations. While competitors burn cash on IPL advertising, Nazara focuses on retention and monetization.

In Casual Gaming, they're minnows in an ocean of sharks. Supercell, King, and Zynga have games generating $1 million daily. Nazara's WCC might do $1 million monthly. But again, they're not trying to build the next Candy Crush. They're building culturally relevant games for Indian users—cricket, carrom, teen patti—that global studios won't prioritize.

The regulatory landscape adds another layer of complexity. In 2023, the Indian government imposed 28% GST on real money gaming, treating it like gambling. Several states banned online gaming entirely. Apple and Google removed hundreds of RMG apps from their stores. This regulatory uncertainty decimated valuations—MPL's valuation fell from $2.3 billion to under $500 million.

But Nazara thrived in this chaos. Their diversified model meant RMG was only 10% of revenues. They had relationships with regulators from their decades of operations. Most importantly, they understood the nuance—skill gaming would eventually be separated from gambling, fantasy sports would get carve-outs, and states would realize tax revenue potential. While foreign investors fled, Nazara doubled down, acquiring distressed assets at attractive valuations.

The China factor looms large. Tencent and NetEase are banned from operating directly in India but invest through proxies. The moment geopolitical tensions ease, Chinese gaming giants could flood the market with capital and expertise. But Nazara has a defense: regulatory relationships and cultural understanding that takes decades to build. They're the local partner every foreign company needs.

The global gaming consolidation wave—Microsoft buying Activision, Take-Two acquiring Zynga—hasn't reached India yet. But it's coming. When it does, Nazara is positioned as either the acquirer consolidating the Indian market or the acquisition target for global strategics wanting Indian exposure. Either scenario likely generates value for shareholders.

The competitive moat isn't about any single business but the portfolio combination. Competitors might beat Nazara in specific verticals, but none match their breadth. Dream11 dominates fantasy sports but has no kids gaming. Krafton owns battle royale but lacks local content. Global studios have better games but no Indian distribution. Nazara's moat is being the only scaled, diversified, public gaming company native to India.

Market position metrics tell the story:

- #1 in kids gaming in India

- #1 in esports infrastructure in South Asia

- Top 3 in skill-based card games

- Top 5 in cricket gaming

- Only listed pure-play gaming company

But the real competitive advantage might be patience. While VC-funded competitors chase growth at any cost, Nazara optimizes for sustainable profitability. While global studios demand 30% ROI, Nazara accepts 15% for strategic assets. While private equity flips assets in 3-5 years, Nazara holds for decades. In a market where everyone's running a sprint, Nazara's running a marathon—and they've been training for 25 years.

X. Playbook: Lessons for Entrepreneurs & Investors

After analyzing Nazara's 25-year journey, patterns emerge that transcend gaming and apply to any emerging market technology business. This isn't just a story about building a gaming company—it's a masterclass in navigating nascent markets, surviving platform shifts, and creating value through patient capital allocation.

Lesson 1: Timing Market Transitions is Everything, But Not How You Think

Nazara didn't try to time the market—they positioned themselves to benefit regardless of timing. When they pivoted to mobile in 2002, smartphones didn't exist. When they acquired esports assets in 2018, the market was microscopic. They weren't predicting the future; they were buying options on multiple futures. The lesson: in emerging markets, being too early is better than being too late, but only if you can survive the waiting period.

Lesson 2: The Power of Being a Local Incumbent

Every global gaming company that entered India learned the same painful lesson: success in San Francisco doesn't translate to success in Mumbai. Payment methods are different (carrier billing vs. credit cards). Content preferences are unique (cricket vs. baseball). Regulatory landscapes are byzantine (state-by-state RMG laws). User behavior is distinct (shorter session times, smaller transaction sizes). Nazara's 25-year head start in understanding these nuances created an almost insurmountable advantage. The playbook: in emerging markets, local knowledge trumps global scale.

Lesson 3: Portfolio Diversification as Survival Strategy

Single-product gaming companies are binary bets—you're either Supercell or you're dead. Nazara chose a different path: diversification across genres, geographies, demographics, and business models. This wasn't lack of focus—it was intelligent risk management. When PUBG was banned, other revenues continued. When iOS 14.5 destroyed advertising, subscriptions provided stability. The insight: in volatile markets, diversification isn't dilution—it's survival.

Lesson 4: M&A in Fragmented Markets—The Rollup That Actually Worked

Most rollup strategies fail because they overpay, over-integrate, and under-deliver on synergies. Nazara's approach was different: - Buy at reasonable valuations (5-8x EBITDA vs. 15-20x in developed markets) - Maintain operational independence (founders stay, brands remain) - Focus on financial and strategic synergies, not operational ones - Be the buyer of choice through reputation and relationships

The result: over 15 successful acquisitions without a single major write-off.

Lesson 5: Building for Profitability in a Growth-At-Any-Cost World

While competitors burned billions chasing user growth, Nazara obsessed over unit economics. They'd rather have 1 million profitable users than 10 million unprofitable ones. This seemed foolish during ZIRP when capital was free. But when the music stopped in 2022, Nazara was one of the few left standing. The lesson: in emerging markets where capital is scarce and exit options limited, profitability isn't optional.

Lesson 6: The Regulatory Arbitrage Opportunity

Most companies see regulation as a constraint. Nazara saw it as an opportunity. Complex regulations create barriers to entry. Regulatory relationships take years to build. Compliance costs favor scaled players. When India imposed 28% GST on gaming, small players died while Nazara consolidated. The playbook: in emerging markets, regulatory complexity is a moat if you're on the right side of it.

Lesson 7: Patient Capital in Impatient Markets

Nazara held onto WCC for six years before it became profitable. They've owned Nodwin for seven years and haven't sold despite 30x appreciation. This patience seems irrational in a world of quarterly earnings. But it's rational when you understand the J-curve of emerging market businesses: losses for years, then exponential growth. The insight: time arbitrage is the most underutilized strategy in emerging markets.

Lesson 8: The Platform vs. Product Decision

Nazara could have focused on building hit games. Instead, they chose to be the platform—publisher, distributor, infrastructure provider. Products have higher margins but higher risk. Platforms have lower margins but compound value over time. In gaming, products are hits-driven; platforms are permanent. The lesson: in uncertain markets, own the infrastructure.

Lesson 9: Being Public as Competitive Advantage

Going public forced discipline that private competitors lacked. Quarterly reporting created accountability. Stock options attracted talent. The public currency enabled acquisitions. Listed status brought credibility with partners. While competitors could hide problems, Nazara had to fix them. The insight: in opaque markets, transparency is a differentiator.

Lesson 10: The Berkshire Model for Emerging Markets

Nazara's ultimate innovation might be bringing the Berkshire Hathaway model to Indian tech: permanent capital, decentralized operations, opportunistic acquisitions, and long-term thinking. While everyone else was building the next unicorn, Nazara was building a century-old company. The playbook: in emerging markets, building to last beats building to flip.

For entrepreneurs, the message is clear: nascent markets reward patience, diversification, and profitability over growth-at-any-cost. For investors, the lesson is different: the best emerging market investments often look nothing like their developed market counterparts. Nazara doesn't fit neatly into any category—and that's precisely why it works.

XI. Bull Case vs. Bear Case Analysis

Every investment thesis has two sides, and Nazara's story is no exception. After 25 years of evolution, the company sits at an inflection point where the bull and bear cases are equally compelling. Let's examine both with the rigor they deserve.

The Bull Case: The Interactive Entertainment Super-App for the Next Billion

The bull thesis rests on five pillars, each reinforcing the others:

1. The India Gaming Megatrend is Just Starting India's gaming revenue per user is $7 versus $70 in China—a 10x monetization gap that will narrow as payment infrastructure improves, disposable incomes rise, and cultural acceptance grows. Even reaching 50% of Chinese monetization implies a $15 billion market by 2030. Nazara, as the only listed pure-play, captures this beta while others fight for survival.

2. The Portfolio Approach Has Been Validated Critics called the diversification "diworsification," but 2022-2023 proved them wrong. When global gaming stocks crashed 70%, Nazara fell only 30%. When RMG faced regulatory heat, other verticals compensated. The portfolio isn't random—it's intelligently constructed with natural hedges, creating Sharpe ratios that single-product companies can't match.

3. Network Effects Are Finally Kicking In After years of subscale operations, Nazara's businesses are reaching critical mass. Nodwin's events attract more sponsors, funding bigger events. Sportskeeda's content draws more users, generating more ad revenue, funding better content. Kiddopia's subscriber base enables original IP development, increasing retention. These aren't linear businesses anymore—they're exponential.

4. The M&A Pipeline Remains Robust Gaming industry valuations have corrected 60-70% from 2021 peaks. Quality assets are available at reasonable prices. Nazara has ₹500+ crores in cash and untapped debt capacity. Their reputation as a buyer makes them the first call for founders seeking exits. Each acquisition strengthens the flywheel—more content, more users, more data, better monetization.

5. Regulatory Clarity is Emerging The 28% GST on RMG seemed catastrophic but actually legitimized the industry. States are realizing taxation beats prohibition. The government is drafting comprehensive gaming regulations separating skill from chance. Once finalized, foreign capital will flood in, valuations will re-rate, and Nazara's first-mover advantage becomes unassailable.

The Upside Scenario: By 2030, Nazara is generating ₹5,000 crores in revenue across 50 million paying users, with 25% EBITDA margins. The stock trades at 20x EBITDA (in line with global gaming companies), implying a ₹25,000 crore market cap—a 10x return from current levels.

The Bear Case: Jack of All Trades, Master of None

The bear thesis is equally structured, with fundamental concerns about the business model:

1. Lack of Organic Growth Strip away acquisitions, and Nazara's organic growth is mediocre. Legacy businesses are declining. New games rarely succeed. User acquisition costs are rising faster than lifetime values. The company is essentially a financial buyer of gaming assets, not an operating company creating value. When M&A stops, growth stops.

2. Integration Challenges Will Eventually Surface Managing 15+ subsidiaries across different verticals and geographies is complex. Culture clashes between Indian management and Western studios are real. The hands-off approach preserves autonomy but sacrifices synergies. Eventually, a major acquisition will fail, destroying value and credibility.

3. Regulatory Risk Remains Existential The RMG business faces constant regulatory uncertainty. Any state can ban online gaming overnight. The government could increase GST further or impose license requirements. Apple and Google control distribution and take 30% of revenues. One adverse ruling could wipe out 20% of revenues instantly.

4. Competition from Deep-Pocketed Giants When Tencent, Sony, or Microsoft decide to seriously enter India, Nazara's capital advantage evaporates. Dream11 has raised more money than Nazara's entire market cap. Global studios are launching India-specific games. Chinese companies are investing through proxies. Nazara's moat is shallow and narrowing.

5. The Portfolio Discount is Permanent Markets hate conglomerates. Investors want pure-plays they can understand. Nazara trades at 15x earnings while pure-play gaming companies trade at 25x. This conglomerate discount won't disappear because the business model is inherently complex. The sum of parts will always trade below individual valuations.

The Downside Scenario: RMG gets banned nationwide. Organic growth stalls. A major acquisition fails. The stock de-rates to 10x earnings, implying a ₹1,000 crore market cap—a 50% decline from current levels.

The Balanced View

Reality likely lies between extremes. Nazara won't become India's Tencent, but neither will it collapse. The business model has proven resilient through multiple cycles. The acquisition strategy, while risky, has worked so far. Regulatory challenges are real but manageable.

The key variables to monitor: - Organic growth rates excluding acquisitions - Success rate of M&A integration - Regulatory developments in RMG - Competitive intensity in core verticals - Management succession planning (Mittersain dependency)

For investors, Nazara represents a unique bet: exposure to India's gaming ecosystem without single-game risk, run by proven operators with skin in the game (Mittersain owns 18%), at valuations reflecting skepticism rather than euphoria. It's not without risks, but the risk-reward seems favorably skewed for patient capital. The bull case doesn't require everything to go right—just a few things to not go wrong.

XII. Looking Forward: The Next Chapter

Standing at the threshold of 2025, Nazara faces its most intriguing chapter yet. The scrappy startup that survived dial-up internet is now a ₹3,000 crore company contemplating artificial intelligence, blockchain gaming, and the metaverse. The question isn't whether these technologies will transform gaming—they will. The question is whether a 25-year-old company can reinvent itself for the next 25 years.

The AI Revolution in Gaming

Generative AI is about to fundamentally alter game development economics. Creating content that took months will take days. Personalized narratives will adapt to individual players. NPCs will have genuine conversations. The implications for Nazara are profound but mixed. On one hand, their content creation costs could plummet. Kiddopia could generate infinite personalized learning content. WCC could create unique cricket scenarios for every player. On the other hand, if anyone can create games with AI, what's Nazara's advantage?

Mittersain's answer is pragmatic: AI is a tool, not a strategy. The competitive advantage isn't in using AI—everyone will—but in having distribution, data, and relationships to monetize AI-generated content. Nazara's 200 million registered users become training data. Their publisher relationships become distribution. Their local knowledge becomes the prompt engineering that makes AI content culturally relevant.

The Web3 Question

Blockchain gaming promises digital ownership, play-to-earn models, and interoperable assets. The hype peaked in 2021 with Axie Infinity, then crashed when the economics proved unsustainable. Nazara watched from the sidelines, making small experiments but no major bets. This conservatism looked foolish during the bubble but prescient after the crash.

The company's Web3 strategy is emerging: wait for infrastructure to mature, regulations to clarify, and use cases to prove sustainable. They're not building blockchain games but might acquire companies that crack the model. It's the same playbook from mobile gaming—let others pioneer, then consolidate the winners.

The Metaverse Reality Check

Meta lost $50 billion chasing the metaverse. Microsoft shut down its metaverse division. The grand vision of interconnected virtual worlds seems distant. But Nazara sees opportunity in the wreckage. Not the metaverse as singular virtual world, but metaverses as game-specific social spaces. Nodwin's esports events could become virtual venues. Comic Con could have year-round digital presence. Kiddopia could become a safe kids' metaverse.

The approach is characteristically pragmatic: evolution, not revolution. Add social features to existing games. Create virtual events alongside physical ones. Build communities before worlds. It's metaverse development without using the word metaverse—probably smart given investor fatigue.

The Consolidation Opportunity

The next 2-3 years present a generational consolidation opportunity in Indian gaming. Hundreds of studios started during COVID with VC funding. Most are running out of cash. Valuations have corrected 70-80%. Distressed sales are beginning. Nazara, with its strong balance sheet and acquisition expertise, is perfectly positioned.

The targets are clear: - Vernacular gaming studios building for Tier 2/3 India - Casual gaming studios with 1-2 hit games but no sequel strategy - Gaming infrastructure companies (analytics, monetization, community) - International studios looking for Asian distribution

The strategy is to buy at 3-5x EBITDA, integrate into the platform, and extract synergies through shared services and cross-promotion. Do this 10 times successfully, and Nazara doubles in size organically.

The International Expansion Vector

India remains the core, but the real growth lies beyond. Southeast Asia has similar dynamics: young demographics, rising smartphones, nascent gaming markets. Africa is where India was in 2005: feature phones dominating, mobile internet emerging. Latin America combines high engagement with improving monetization.

Nazara's advantage in these markets is experience navigating similar challenges: payment infrastructure gaps, regulatory uncertainty, local content preferences. The playbook from India—carrier partnerships, local IP, patient capital—translates directly. The vision is to become the emerging markets gaming platform, not just the Indian one.

The Succession Question

Mittersain turned 48 in 2024. He's been running Nazara for 25 years—longer than most Silicon Valley CEOs last. The company is synonymous with his vision. But public companies need succession planning. The next generation of leadership is emerging from acquisition founders: Akshat Rathee at Nodwin, Siddharth Abhichandani at Sportskeeda. The transition won't happen soon, but infrastructure is being built.

The Next Five Years

By 2030, Nazara envisions: - ₹5,000 crores in revenue (5x growth from 2025) - 500 million registered users globally - 50 million paying subscribers - Presence in 50+ countries - 30% EBITDA margins at scale

Ambitious? Yes. Impossible? No. The building blocks are in place: proven M&A machine, profitable operations, public currency, experienced management. The macro tailwinds are strong: demographic dividend, digital adoption, entertainment spending growth. The execution risk is real but manageable.

The next chapter of Nazara won't be about survival—that battle is won. It's about transformation from Indian gaming company to global interactive entertainment platform. From consolidator of distressed assets to creator of original IP. From financial buyer to operational excellence. The foundation is built. The question is how high they can build on it.

XIII. Closing Thoughts & Key Takeaways

After six hours of analysis, what have we learned from Nazara's quarter-century odyssey? This isn't just a corporate history—it's a meditation on building technology businesses in markets where nothing can be taken for granted. Where payment rails don't exist until you build them. Where regulations change overnight. Where global best practices fail local reality tests. Where patience isn't a virtue—it's a necessity.

The Biggest Surprise: Boring is Beautiful

The most counterintuitive lesson from Nazara's story is that in gaming—an industry obsessed with viral hits and moonshot bets—the winning strategy was deliberately boring. No viral sensations. No breakthrough technologies. No charismatic founder cult. Just methodical execution, intelligent capital allocation, and compound growth over decades. Nazara built a gaming empire by not playing the gaming industry's game.

What Other Companies Can Learn

For Indian tech companies aspiring to build something permanent, Nazara offers a template:

-

Start with distribution, not product. Nazara's carrier relationships were more valuable than any game they built.

-

Diversification is not lack of focus. In volatile markets, portfolio approaches reduce risk while maintaining upside.

-

Buy when others are selling. Nazara's best acquisitions came during crisis periods when valuations were reasonable.

-

Profitability is not optional. Cash flow funds growth and provides resilience during downturns.

-

Local beats global. Understanding cultural nuances and regulatory frameworks is more valuable than technical superiority.

For global companies entering emerging markets, the lessons are different but equally valuable:

-

Partner, don't compete. Local partners provide distribution, relationships, and cultural translation.

-

Patience is mandatory. Emerging markets take longer to monetize but offer higher terminal values.

-

Adapt, don't impose. What works in developed markets rarely translates directly.

-

Infrastructure investments pay off. Building payment rails, distribution networks, and local content creates lasting moats.

-

Regulatory complexity is a moat. If you can navigate it, competitors can't easily follow.

The Future of Gaming in Emerging Markets

Nazara's story illuminates broader truths about gaming in emerging markets:

The next billion gamers won't look like the first billion. They'll play on $100 phones, not $1,000 consoles. They'll spend $1 at a time, not $60 upfront. They'll want local content—cricket, not baseball; Bollywood, not Hollywood. They'll game in short sessions during commutes, not marathon weekend sessions. Understanding these differences is worth more than any technology advantage.

The monetization J-curve is real but requires patience. India's $7 ARPU will eventually reach $30-40, creating a $15-20 billion market. But it might take a decade. Companies that survive the waiting period will capture exponential value. Those demanding immediate returns will exit too early.

Regulation will remain messy but manageable. Governments will ban, tax, and restrict gaming. But they'll also realize gaming creates jobs, generates tax revenue, and provides safe entertainment. The regulatory pendulum will swing, but the long-term direction is toward acceptance and formalization.

Final Reflections on Building a Gaming Empire in India

Nazara's journey from dial-up portal to public gaming conglomerate isn't replicable—the specific conditions of 1999-2024 won't repeat. But the principles are timeless: patience in nascent markets, diversification in uncertain environments, profitability as foundation for growth, and local knowledge as competitive advantage.

What makes Nazara fascinating isn't that they built a successful gaming company—many have done that. It's that they built an enduring gaming company in a market where nothing endures. Where competitors with 10x the funding failed. Where regulatory changes killed entire sectors overnight. Where platform shifts made expertise obsolete. Through all this chaos, Nazara not only survived but thrived.

The ultimate lesson might be this: in emerging markets, the race doesn't go to the swift or the brilliant, but to the patient and adaptable. Nazara won not by being the best gaming company, but by being the last one standing when the dust settled. And in the brutal Darwinian environment of Indian tech, survival is success.

As we close this analysis, Nazara trades at ₹2,800 per share, valued at ₹3,000 crores. Bulls see it quintupling as India's gaming market matures. Bears see risks everywhere—regulation, competition, execution. Both are right. But for those who understand the full arc of Nazara's story—from Nitish Mittersain's dial-up dreams to today's diversified platform—the conclusion is clear: betting against Nazara is betting against the patience, resilience, and ingenuity that built India's only gaming empire.

The company that started with a simple question—"Can Indians build a gaming business?"—has delivered a resounding answer: Yes, but not the way anyone expected. And perhaps that's the most valuable lesson of all. In emerging markets, the successful strategies aren't imports from Silicon Valley playbooks. They're indigenous innovations born from local constraints, shaped by local culture, and proven through local execution.

Nazara's next 25 years will look nothing like the first 25. But if history is any guide, they'll find a way to adapt, survive, and thrive. Because that's what they've always done. In the ever-evolving game of building technology businesses in emerging markets, Nazara has mastered the only strategy that matters: staying in the game long enough to win.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube