Nazara Technologies: The Indian Capital Arbitrage Machine

I. Episode Introduction & The Roll-Up Revolution

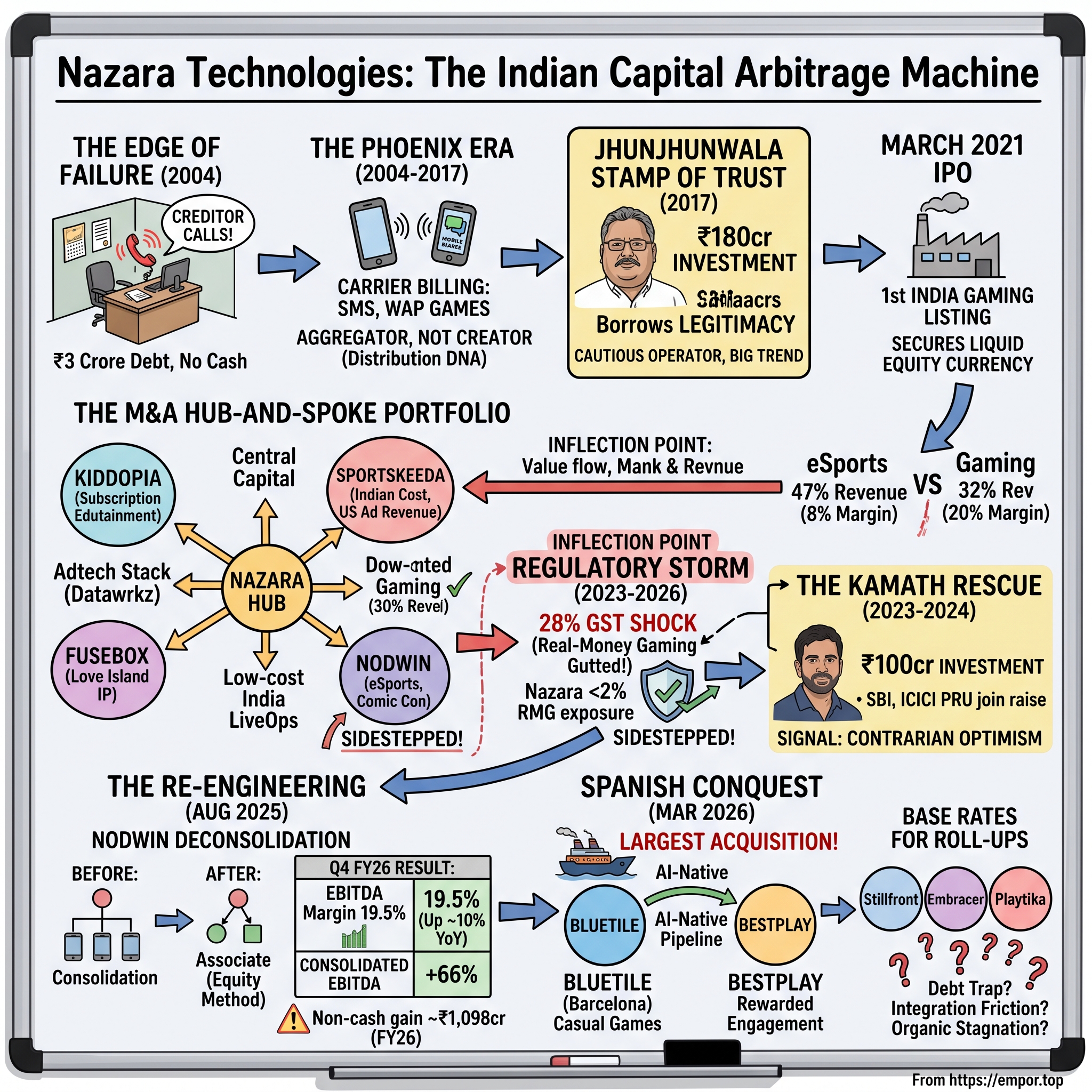

Picture a small office in Mumbai in 2004. The dot-com euphoria that had swept India five years earlier has curdled into a hangover. The phone rings, and it is not a customer — it is a creditor. It rings again. The company on the receiving end, a scrappy gaming portal called Nazara, is sitting on more than ₹3 crore of debt it cannot pay, and its founder is a young man barely out of his teens who had convinced his family to bet on the idea that Indians would one day play games on their phones.

Fast-forward to March 2026. That same company — now Nazara Technologies Limited, trading as NAZARA.NS on the National Stock Exchange of India — announced the largest acquisition in its history: a controlling stake in a pair of Spanish gaming businesses for an upfront $100.3 million in cash, with a total potential price approaching $200 million once earn-outs are counted.2223 The distance between those two moments — the creditor's phone call and the nine-figure cheque wired to Barcelona — is the story of this episode.

Nazara today is best understood not as a game developer but as a capital-allocation machine. It is frequently described, half-admiringly and half-skeptically, as a kind of "Berkshire Hathaway of Indian gaming": a diversified holding company that buys founder-run gaming and sports-media businesses, keeps their founders in place, and layers on central capital, advertising technology, and low-cost Indian operations. Whether that comparison is flattery or a warning is a question this piece will keep returning to.

The title of this story calls Nazara a "capital arbitrage machine," and it is worth defining that phrase up front because it is the lens through which everything else makes sense. An arbitrage, in its purest form, is buying something cheap in one market and selling it dear in another. Nazara's version is subtler: it raises capital in the Indian public market, where investors are willing to pay a rich price for gaming exposure, and deploys that capital to buy gaming businesses in Western markets, where the same kind of cash flow trades for a fraction of the price. The "machine" is the repeatable process that connects the two — the listing, the war chest, the disciplined acquisitions, the low-cost operating base that squeezes more profit out of each asset once it is owned. Whether that machine is a durable engine of compounding or a contraption that only runs while conditions are favorable is the central tension of this entire story.

The financial redesign underway is dramatic. In FY25 (the year to March 2025), Nazara reported consolidated revenue of roughly ₹1,624 crore, split across three engines: eSports at about 47% of the top line, Gaming at roughly 32%, and Adtech at around 21%. The problem hiding inside that revenue mix was margin. eSports — a business of running tournaments and live events — carried an EBITDA margin around 8%, while the Gaming segment threw off cash at roughly 20% margins. Nazara was growing its biggest number, revenue, on the back of its worst business.

Then management performed surgery. Following the August 2025 deconsolidation of its eSports arm, Nodwin Gaming, the FY26 picture (year to March 2026) looks like a different company. Revenue rose 13% year-on-year to ₹1,829 crore, but consolidated EBITDA surged 66% to ₹255 crore — the highest in the company's history — and the Gaming segment's share of consolidated EBITDA jumped from roughly 56% to about 90%.679 Underlying net profit came in around ₹82 crore, though the reported figure was flattered by a large one-time accounting gain we will dissect later.

That single sentence — the highest-margin segment now generates nine-tenths of profit — is the whole thesis in miniature. Nazara deliberately shed a low-margin top-line story and re-emerged as a higher-margin, owned-intellectual-property story. The question for investors is whether this is genuine value creation or a clever act of financial framing.

Here is the road ahead. First, the grueling survival years of founder Nitish Mittersain and the carrier-billing era that kept the lights on. Then the legendary backing of Rakesh Jhunjhunwala and the landmark March 2021 IPO. Next, the regulatory earthquake of India's 28% GST on real-money gaming and how Nazara sidestepped it. Then the arrival of the Nikhil Kamath war chest and the strategic de-subsidiarisation of Nodwin. And finally the European conquest — the disciplined acquisitions of Fusebox Games and, above all, Bluetile. Let us begin where every good survival story begins: at the edge of failure.

II. The Phoenix Era: Surviving the Dot-Com Crash to the Jhunjhunwala Stamp of Trust

In 1999, a nineteen-year-old named Nitish Mittersain did what a great many nineteen-year-olds around the world were doing that year: he started an internet company. What made him unusual was not the age but the obsession. Mittersain had reportedly started coding at age seven, and he was, above all, a gamer — someone who believed in his bones that games were not a fad but a medium.2 He persuaded his family to back a local gaming portal, and Nazara was born into the very peak of the dot-com bubble.

The timing could not have been worse. Within a couple of years the bubble burst, global internet valuations evaporated, and by 2004 Nazara found itself more than ₹3 crore in debt, with creditors calling constantly. This is the moment that defines the entire company, because it is the moment most founders quit. Mittersain did something quieter and, in hindsight, more revealing of his character. He did not file for bankruptcy. He sat down with his creditors and negotiated a payment plan — buying time in exchange for a promise to work the debt off.

The survival strategy was carrier billing. In an India where credit cards were rare but mobile phones were spreading fast, the telecom operator's monthly bill was the only payment rail that reached the masses. Nazara pivoted to SMS-based and WAP-based mobile gaming and content, striking distribution deals with telecom operators — not only in India but across South Asia, including a relationship with Sri Lanka's Dialog Telekom.2 The user did not need a bank; they simply saw the charge appear on their phone bill. It was clunky, low-margin, and unglamorous, and it kept the company alive.

Out of that grind came the insight that still shapes Nazara today. Building games in-house in India was slow, capital-intensive, and risky — a single flop could sink the studio. The smarter role, Mittersain concluded, was to be the ecosystem manager: the aggregator, the distributor, the platform that sat between content and consumer and took a cut of the flow. This is the intellectual DNA of the roll-up strategy that would arrive two decades later. Nazara learned early that it was better at moving other people's games to market than at making its own hits.

For years, this was a footnote business — profitable in a small way, respected by few, and utterly off the radar of India's celebrity investors. That changed in 2017. Rakesh Jhunjhunwala, the trader-investor so revered in India that the financial press routinely called him the country's Warren Buffett, invested roughly ₹180 crore for a minority stake of around 8–10%.1 By his own account of the meeting, Jhunjhunwala was drawn not to gaming hype but to precisely the boring virtues Nazara had been forced to cultivate: limited use of capital, real profitability, and cash generation.13

What did Jhunjhunwala actually see? Not a hit game — Nazara had none to speak of — but a macro trend and a temperament. India in 2017 was on the cusp of a data revolution: the launch of ultra-cheap mobile data had put a smartphone and an internet connection into hundreds of millions of hands almost overnight, and a generation was about to spend its idle minutes on mobile screens. Gaming, Jhunjhunwala reasoned, would ride that wave and become very large.3 But he was a value investor, not a growth tourist, and what sealed his conviction was that Nazara had learned to grow without burning cash — a rarity in a startup world addicted to subsidizing users. He was, in effect, buying a company whose scars had taught it financial discipline, positioned in front of a structural tailwind. That combination — cautious operator, big trend — is the same one every subsequent Nazara backer has claimed to see.

The Jhunjhunwala investment was worth far more than its rupee value. In a country where "gaming" still carried the faint whiff of frivolity and where institutional investors avoided the sector, his imprimatur rewired the market's perception overnight. If India's shrewdest investor was willing to own it, gaming was suddenly a legitimate asset class. This is a recurring pattern worth flagging for investors: much of Nazara's value has historically come from association with credible capital, not just from operating performance.

It is worth dwelling on what happened between 2004 and 2017, because the carrier-billing decade quietly rewired Nazara's whole worldview. A company that lives on telecom-operator billing learns to think like a distributor, not a creator. Its most valuable relationships are not with players but with the carriers who own the payment rail and the customer. Its instinct is to ride whatever platform the masses are already on — first the featurephone and the SMS, later the smartphone and the app store — rather than to build a platform of its own. And its financial temperament becomes almost pathologically cautious, because a business born in debt does not forget the sound of a creditor's phone call. Every later Nazara decision — the aggregator model, the reluctance to chase RMG, the preference for buying proven cash flow over funding moonshots — traces back to lessons absorbed in these lean years.

That credibility set the stage for the milestone that made Nazara a household name in Indian markets. In March 2021, Nazara became the first gaming company to list publicly in India, debuting on the NSE amid heavy oversubscription and a strong listing premium — a coming-out party for the entire domestic gaming industry.2 The company that could not pay its creditors in 2004 was now a public company with a marquee anchor investor.

The listing mattered for a reason beyond the fireworks of day one. By becoming the first pure-play gaming company Indian public investors could own, Nazara secured something more valuable than the cash it raised: a permanent, liquid, and richly valued equity currency. For a business whose entire future strategy would depend on making acquisitions, being publicly listed at a premium multiple was not a vanity milestone — it was the acquisition engine itself. The company had spent two decades learning it was better at buying and distributing than at building, and the IPO finally handed it the tool that made buying scalable. In a sense, everything that follows in this story is Nazara learning to use that tool.

The Jhunjhunwala chapter closed, fittingly, with a large payday. Rakesh Jhunjhunwala died in 2022, and over the following years his widow Rekha Jhunjhunwala steadily pared the family's position, completing a full exit by mid-2025 in staggered sales — a June 2025 tranche alone was valued at around ₹334 crore, capping years of multibagger gains.1011 The legacy investor who had legitimized the story cashed out just as a new set of backers, and a new regulatory storm, were arriving. But to understand why those new backers came, we first need to understand the machine they were buying into.

III. The M&A Playbook: Building the Hub-and-Spoke Portfolio

Every holding company has a theory of itself, and Nazara's is a hub and its spokes. At the center sits the listed parent — the source of capital, the advertising-technology stack, and a shared pool of low-cost Indian talent for live operations, the unglamorous daily work of running a mobile game: tuning difficulty, scheduling events, pushing updates, and squeezing more revenue from existing players. Around that hub orbit the spokes: majority-owned, founder-run businesses that keep their independence and their leadership while plugging into the center's resources.

The logic is deliberately un-heroic. Nazara does not try to conjure the next global hit from a blank page — the strategy it abandoned in the carrier-billing years. Instead it buys businesses that already work, usually taking stakes between 50% and 100%, and leaves the operators who built them in the driver's seat. In theory, the parent supplies three things a bootstrapped studio lacks: cheap growth capital, a centralized user-acquisition engine, and India's structural cost advantage in engineering and content. In practice, the quality of that value-add is exactly what a skeptic should interrogate, because the entire roll-up thesis rests on it.

Consider the core spokes, each of which teaches a different lesson. Kiddopia, from Paper Boat Apps, was the first big swing — Nazara bought an initial 51% stake for roughly ₹83.5 crore around 2019 and later moved to full ownership.4 Kiddopia is a subscription app for gamified early-childhood learning aimed squarely at American parents, and for a while it was a jewel: highly profitable, with an FY24 EBITDA around ₹56 crore on roughly ₹219 crore of revenue — a margin north of 25%. But its growth flatlined, and the reason is a preview of a risk that stalks this entire industry. Apple's iOS privacy changes made it harder and costlier to find new subscribers online, and Kiddopia's user-acquisition math stopped working as well as it once did.

It is worth explaining that privacy shift in plain terms, because it is the single most important structural force in this entire story and it recurs at every turn. For years, advertisers could quietly follow a user from app to app using a hidden device identifier, which let them target ads with uncanny precision and, crucially, prove which ad produced which paying customer. Around 2021, Apple began requiring apps to ask permission before doing this tracking, and most users said no. Overnight, the advertising machine that mobile games depended on went partially blind: it became harder to find the right prospects and harder to measure whether the spend was working, so the cost of acquiring each new paying user climbed. For a subscription business like Kiddopia, whose entire model is spend-to-acquire-then-retain, this was not a nuisance — it was a tax on the core growth engine. Every part of Nazara that touches user acquisition, from Kiddopia to Bluetile to Datawrkz, lives downstream of this single change in Apple's settings menu.

Sportskeeda tells the opposite, happier story. Nazara acquired its parent, Absolute Sports, in stages — a 67% stake for about ₹44 crore in 2019, then step-ups culminating in full ownership in 2024–25.1415 Sportskeeda is a sports-media platform, and its genius is arbitrage of a very specific kind: it uses low-cost Indian content writers to produce reams of articles about high-value American sports — the NFL, the NBA, college football — and monetizes the resulting US traffic through programmatic advertising priced in dollars. It is a business that grew organically, at very high margins, by exporting Indian labor into an American ad market without ever leaving Mumbai. If you want to understand why Nazara believes so deeply in the India-cost-base-serving-Western-revenue model, look here.

Then there is Datawrkz, acquired for around ₹124 crore in early 2022.4 Datawrkz is an ad-tech platform, and inside the Nazara system it plays the role of the house marketing agency — the centralized engine that buys and optimizes advertising across the whole portfolio, so that each spoke does not have to reinvent user acquisition or pay an outside agency's markup. Whether Datawrkz genuinely lowers group-wide acquisition costs, or is simply an in-house cost center dressed as a moat, is one of the KPIs a serious investor should track.

Taken together, the early spokes reveal something important about how Nazara's discipline evolved. The Kiddopia, Sportskeeda, and Datawrkz deals were struck in the 2019–2022 window, when gaming valuations were climbing and Nazara was still assembling the shape of its portfolio. A skeptic could fairly ask whether a company buying an early-learning app, a sports-content site, and an ad-tech firm was building a coherent platform or simply accumulating unrelated assets — the classic conglomerate sin of "diworsification," where breadth substitutes for a strategy. The generous reading is that each acquisition serves the same underlying model: own IP or audience, monetize it with Indian cost structure and Western ad dollars, and route it all through a shared marketing engine. The honest reading is that the coherence became clearer only in hindsight, once management started narrating the portfolio as a single machine rather than a collection of bets.

What changed after 2022 was price discipline. When the funding winter arrived and gaming multiples collapsed, Nazara did not accelerate its buying recklessly; it waited, husbanded the capital it had raised, and then bought only when the numbers were conservative. The clearest proof of that shift was its next deal.

The playbook's discipline showed most clearly in August 2024, when Nazara acquired UK-based Fusebox Games for $27.2 million (about ₹228 crore) in an all-cash deal.1213 Fusebox makes interactive "choose-your-own-story" mobile games licensed from reality-TV franchises like Love Island, and it came with real numbers — 2023 revenue around $10.4 million — and, crucially, a modest price. Nazara framed the purchase at roughly 1.5 times trailing revenue, a strikingly disciplined multiple against the frothy pre-2022 gaming deals that routinely fetched four to five times revenue.13 Mittersain's stated rationale was telling: he wanted global IP that Nazara could support with Indian user-acquisition, data analytics, live operations, and an in-house "AI playbook."13

That is the machine. The strategic question for investors is whether buying cash-flowing assets cheaply and running them from a low-cost base is a durable edge — or whether it merely postpones the day when the acquired games, like all mobile games, begin their inevitable decline. Before we can judge that, we have to reckon with the event that reshaped the entire Indian gaming landscape and, paradoxically, handed Nazara its opening.

IV. The Great Regulatory Storm: The 28% RMG Tax Shock & The Kamath Rescue

For a few intoxicating years, real-money gaming was the hottest corner of Indian technology. Between roughly 2018 and 2022, fantasy-sports apps and online rummy and poker platforms — businesses where users deposit real cash and win or lose real money — pulled in enormous venture funding, splashed cricket sponsorships across television, and minted paper fortunes. Real-money gaming, or RMG, looked like the future of Indian gaming, and money poured toward it.

Then the state brought down the hammer. The government moved to levy a flat 28% Goods and Services Tax on the full face value of deposits made on online money-gaming platforms — not on the operator's revenue or margin, but on every rupee a player put in. The distinction is the difference between life and death for the business model. A platform that keeps, say, ten rupees out of every hundred wagered suddenly owed twenty-eight rupees in tax on that hundred. The industry challenged it, and lost decisively: in May 2026, the Supreme Court upheld the levy — and, devastatingly, upheld its retrospective application stretching back to 2017, reviving tax demands running into lakhs of crores across the sector.18[^27] The GST rate on such activity had already been pushed to 40% in late 2025.19

To grasp the scale of the carnage, look at the casino operator Delta Corp, long the listed poster child for Indian gambling. As the retrospective demands and the punitive rate structure landed, its business case buckled under liabilities it had never provisioned for, and the wider RMG cohort — from fantasy-sports giants to rummy platforms — faced tax bills that in some cases exceeded the total capital they had ever raised. Venture investors who had poured billions into the sector on the assumption that scale would eventually mean profits discovered instead that scale, under a face-value tax, meant a larger bill. An entire investment thesis for Indian consumer gaming was invalidated in a single ruling.

For much of the industry this was an extinction event; rivals exposed to casino and RMG economics saw their business cases collapse. And here is where Nazara's decades-old instinct for capital discipline paid off in the most unexpected way. Nazara's direct RMG exposure — through small assets like HalaPlay and Classic Rummy — was negligible, under 2% of group revenue. The company had, by design, treated RMG as a place to dabble rather than to bet. It even kept its exposure to the poker platform PokerBaazi (via Moonshine Technologies) to a minority stake, deliberately holding the risk off its own balance sheet.

This is what strategists call counter-positioning, and it was more luck-shaped-by-temperament than foresight. Nazara had not predicted the GST ruling; it had simply never been willing to chase the RMG gold rush at the scale that would have imperiled it. The result was that when the storm hit, Nazara stood on dry ground while competitors drowned — and, more importantly, it had the balance sheet and the credibility to go shopping while everyone else was bailing water.

There is a neat symmetry worth pausing on. Just as Rakesh Jhunjhunwala had once conferred legitimacy on Nazara at a moment when Indian institutions shunned gaming, a new marquee name arrived at the next inflection point. Nikhil Kamath — co-founder of Zerodha, India's largest retail brokerage, and by the mid-2020s one of the country's most visible young billionaires and self-styled public intellectuals — is exactly the kind of investor whose participation moves perception. A Zerodha founder buying into a gaming roll-up, in the teeth of a sector-wide regulatory panic, sent a signal that the smart, contrarian money saw opportunity where the crowd saw only wreckage. As with Jhunjhunwala, the endorsement was worth more than the cheque, and investors should be honest that Nazara has repeatedly converted the credibility of its backers into a valuation premium of its own.

Which is exactly what it did. Sensing that industry disruption plus a broader tech-funding downturn had made assets cheap, Nazara raised well over ₹900 crore in late 2023 and early 2024 through preferential share allotments to a new class of backers. The most symbolically potent was Zerodha co-founder Nikhil Kamath, whose entities Kamath Associates and NKSquared put in around ₹100 crore at ₹714 per share.17 Days later, SBI Mutual Fund committed roughly ₹410 crore across three of its schemes at the same price, and ICICI Prudential joined the raise.16 The combined effect took Kamath's footprint to around 3.5% and gave Nazara a war chest precisely when its wounded rivals had none.16

The shareholder register kept shifting in Nazara's favor of narrative but not without complication. In May 2026, a ₹486 crore block deal saw roughly 4.9% of the company's equity change hands at a floor around ₹266 per share, with Kamath (alongside institutional holder Axana Estates) buying while founder Nitish Mittersain, through promoter vehicle Mitter Infotech LLP, sold part of his personal stake.2021 The market cheered the arrival of a marquee buyer, and the stock jumped sharply on the news.20 But an investor should hold two thoughts at once here: a celebrated new anchor was raising his bet, and the founder was selling into the middle of the company's most ambitious expansion. We will return to that tension. For now, note that the war chest raised in the storm's shadow was about to be spent — but first, management had one more piece of financial architecture to build.

V. The Great Financial Re-Engineering: De-subsidiarising Nodwin Gaming

If Nazara had a crown jewel by revenue, it was Nodwin Gaming — the biggest esports organizer in South Asia, holder of coveted ESL tournament licenses, and, after a ₹55 crore deal in early 2024, the owner of Comic Con India.[^16] Nodwin ran the tournaments, the live events, the fan conventions — the loud, visible, culturally resonant face of Indian gaming. In FY25 it contributed roughly 47% of Nazara's consolidated revenue, on the order of ₹763 crore. On the top line, Nodwin was the star.

On the bottom line, it was the problem. Events are a hard business: you rent the venue, fly in the talent, build the stage, and pray the sponsors and ticket buyers show up. Nodwin's EBITDA margin sat around 8%, a fraction of the Gaming segment's. So Nazara's consolidated income statement told a confusing story — a fast-growing revenue line attached to a thin, volatile profit line. Public-market investors who wanted to value Nazara as a high-margin software-and-gaming company kept tripping over Nodwin's low-margin events revenue diluting the blended picture. The biggest number in the accounts was actively depressing the multiple the market was willing to pay.

The solution, executed in August 2025, was a piece of corporate engineering elegant enough to admire and subtle enough to distrust. Rather than sell Nodwin, Nazara allowed it to raise fresh capital independently and, in the process, waived certain controlling and restrictive rights — diluting its effective control below the 50% threshold that requires consolidation. Nodwin stopped being a subsidiary whose full revenue flowed into Nazara's accounts and became an "associate," carried under the equity method, where only Nazara's share of Nodwin's net profit trickles onto the income statement as a single line.

The accounting consequence was, to borrow a phrase, almost magical. In Q4 FY26, Nazara's consolidated revenue "declined" 23.5% year-on-year to around ₹398 crore — but the decline was an illusion of arithmetic, driven entirely by Nodwin's top line vanishing from the tables; adjusted for the deconsolidation, underlying revenue actually grew.58 Meanwhile, with the low-margin revenue gone, the consolidated EBITDA margin leapt to 19.5% in the quarter, nearly ten percentage points higher year-on-year, and full-year FY26 EBITDA rose 66% to ₹255 crore.56 The same operating businesses, viewed through a redrawn corporate boundary, suddenly looked far more profitable.

The market's reaction to all this was revealing in its own right. The financial press dutifully led with the eye-catching numbers — profit "nearly tripling," EBITDA leaping 66%, the highest in company history — while the revenue "decline" was quickly explained away as a technicality of consolidation.59 That is precisely the reception a management team hopes for when it re-engineers a set of accounts: the improvement gets the headline, the accounting cause gets the footnote. A disciplined investor should read those headlines in reverse, treating the flattering framing with more caution than the awkward revenue drop, because the drop was arithmetic while the margin gain was partly choreography. None of this is to allege anything improper; it is simply to note that the same set of facts can be arranged to tell a more or less impressive story, and Nazara arranged them well.

Here the skeptic and the accountant must be invited into the room. FY26's reported profit also included a one-time, non-cash "fair value gain" of roughly ₹1,098 crore, booked when Nodwin was re-valued upon ceasing to be a subsidiary.8 This is a standard accounting treatment — when you deconsolidate, you mark your retained stake to fair value and run the paper gain through the income statement — but it is not cash, it is not repeatable, and it dwarfs the company's underlying operating profit. Strip it out and the ongoing net profit was closer to ₹82 crore. Any investor reading FY26 headlines should mentally separate the operating story (margins genuinely improved because a low-margin business left the consolidation) from the accounting fireworks (a huge non-cash gain that inflates the reported bottom line exactly once).

There is a subtler point about why deconsolidation, and not a simple sale, was the chosen route. Nodwin is not a business Nazara wanted to be rid of — esports and live events are culturally central to gaming in India, and Comic Con India is a genuine franchise with a loyal following. Selling outright would have severed Nazara from that ecosystem and forfeited any upside if Nodwin's economics eventually improve. Retaining a large minority stake accounted for as an associate threads the needle: Nazara keeps its equity in Nodwin's future, keeps a seat at the table, and lets Nodwin raise its own capital and pursue its own ambitions — while removing Nodwin's thin margins from the consolidated profit-and-loss statement that public investors scrutinize. It is a structure that optimizes simultaneously for strategic optionality and for the appearance of the income statement, which is exactly why it invites both admiration and suspicion.

So what does the maneuver actually mean? Two things can be true simultaneously. Operationally, giving Nodwin independent capital and a longer leash may genuinely serve both businesses. Optically, the same move conveniently doubled the headline consolidated EBITDA margin and re-anchored the market's attention on the high-margin Gaming story management wants investors to reward. The honest verdict is that de-subsidiarisation was both a real operational choice and a narrative device, and management's credibility will be tested by whether the margins hold up in the quarters ahead — after the accounting one-timers have washed through. With the income statement re-engineered and the war chest full, the stage was finally set for the boldest move of all.

VI. The Spanish Conquest: Bluetile Games & BestPlay Systems

On March 24, 2026, Nazara announced a deal that made every prior acquisition look like a warm-up. It agreed to buy a 50% controlling stake in two Barcelona-based businesses: Bluetile Games SL (formerly Playvalve) — a casual mobile-game studio — and its in-house rewarded-engagement platform, BestPlay Systems SL.2223 It was, by a wide margin, the largest acquisition in Nazara's history, and it deployed precisely the capital raised from Kamath, SBI, and their fellow travelers.

The terms rewarded a close reading. The upfront consideration was $100.3 million in cash — roughly $88.4 million for half of Bluetile and $11.9 million for half of BestPlay.23 On top sat performance earn-outs of up to $98.2 million, payable over several years and contingent on hitting revenue and EBITDA targets — bringing the theoretical total to around $198.5 million.2223 Nazara also secured a call option to acquire the remaining 50% by 2028 at a fixed 6.6 times trailing EBITDA, with the sellers holding a corresponding put.23 This structure is itself a lesson in disciplined dealmaking: pay a controlled amount up front, tie the rest to results the sellers must actually deliver, and lock in the price of the second half before you buy it.

There is a small irony buried in the names. Bluetile was formerly known as Playvalve, a studio that had quietly built a machine for cloning and modernizing the world's most timeless table and tile games — the digital equivalent of a company that noticed everyone still plays Yahtzee and dominoes and simply built better mobile versions. This is not the frontier of gaming; it is the comfortable, sticky middle, where players are older, more loyal, and less likely to chase the next viral sensation. That is precisely why the cash flows are stable, and precisely why Nazara wanted them.

The scale of the reach was substantial. Across its 17 live titles, Bluetile had accumulated on the order of 375 million lifetime downloads and roughly 22 million monthly active players, while BestPlay's rewarded-play app was pulling in around 1.2 million downloads a month and some 2.2 million monthly actives of its own.2423 In casual gaming, that installed base is the real asset — a standing audience that can be cross-sold new titles without paying the ad platforms to find them from scratch each time.

The numbers behind the assets explain the enthusiasm. For the twelve months to December 2025, Bluetile and BestPlay together generated about $153.6 million of revenue and $27.7 million of EBITDA.2223 At the ~$100 million upfront price for 50%, and against that combined EBITDA, Nazara was buying in at roughly seven times trailing EBITDA — the kind of single-digit multiple that has become normal for cash-generative Western gaming assets in a chastened funding environment, and a world away from the double-digit revenue multiples of the boom. The blunt strategic fact is that this one transaction came close to doubling Nazara's run-rate EBITDA overnight. That is the entire roll-up thesis compressed into a single press release.

It is worth pausing on the structure of the earn-out, because it reveals how Nazara thinks about risk. By tying up to $98.2 million of the price to revenue and EBITDA targets stretching across 2027 to 2029, Nazara did two things at once. It capped its own downside — if Bluetile's cash flows fade, the earn-out simply never gets paid, and the effective purchase multiple falls even lower. And it kept the Spanish founders financially chained to performance for years, converting them from sellers who have cashed out into partners who still have most of their reward ahead of them. The call option to buy the second half at a pre-agreed 6.6 times EBITDA in 2028 completes the design: Nazara has effectively priced its entire path to full ownership in advance, insulating itself from having to renegotiate later at whatever multiple the market then demands. Whatever else one thinks of the deal, its architecture is the work of a careful buyer, not an exuberant one.

But the strategic logic runs deeper than the multiple, and it rests on two ideas worth explaining plainly. The first is the AI-native content pipeline. Bluetile runs 17 live casual titles — games like Yatzy, Domino Legends, and Mahjong Voyage, familiar table and tile games reimagined for phones, with hundreds of millions of cumulative downloads and tens of millions of monthly players.23 Crucially, these titles are built and maintained on an AI-assisted workflow, which in plain terms means the studio uses automated tooling to generate art, variations, and live-operations content at a fraction of the usual human cost. In an industry where the perpetual grind of "keep the game fresh or watch players leave" is the main operating expense, lowering the cost of that grind is a real advantage — if the tooling is as good as claimed, a caveat worth verifying over time.

To make the AI point concrete: a casual game like a Mahjong or dominoes title lives or dies on the steady drip of new content — fresh boards, seasonal events, tweaked difficulty, new visual themes — that gives players a reason to open the app tomorrow. Historically this content was hand-built by artists and designers, and it was expensive precisely because it never stopped. An AI-assisted pipeline lets a small team generate that stream of variations far faster and cheaper, which does two things: it lowers the ongoing cost of keeping each game alive, and it lets a modest headcount run many titles at once. If it works as advertised, it directly amplifies Nazara's India cost advantage — cheap labor made cheaper still by automation. But there is a symmetric risk that deserves stating: if AI tooling this powerful is available to Bluetile, it is increasingly available to every competitor too, which could compress the whole industry's content costs and, with them, the very margins Nazara is buying. Whether AI is a durable edge or an industry-wide equalizer is genuinely unresolved, and it is one of the more important open questions in the whole thesis.

The second idea is BestPlay, and it addresses the single most important structural problem in mobile gaming: the "Apple-Google tax" on finding players. In today's privacy-restricted mobile world, acquiring a new user through Facebook or Google advertising has become punishingly expensive, because the tracking that made targeted ads efficient has been curtailed. BestPlay is an owned "rewarded-engagement" platform — it hands players vouchers and incentives to try games — which functions as Nazara's own distribution channel, with millions of monthly active users.23 Owning that channel means Nazara can, in principle, funnel players across its global portfolio without paying the ad giants for every download. It is the same instinct that made Sportskeeda valuable — controlling distribution rather than renting it — applied to games at global scale.

Whether these synergies materialize is the multi-hundred-million-dollar question, and the honest answer on July 10, 2026, is that it is far too early to know. What can be said is that the shape of the bet is consistent with everything Nazara has done since the carrier-billing days: buy proven cash flow, own the pipes, and run it lean. The strategic pattern is coherent. Now it must survive contact with integration reality — which is precisely the terrain of frameworks built to test durable advantage.

VII. Hamilton Helmer's 7 Powers & Porter's 5 Forces Analysis

Strip away the narrative energy and ask the hard question that frameworks are built to answer: does Nazara possess anything a competitor cannot simply copy? Two lenses — Hamilton Helmer's 7 Powers and Michael Porter's Five Forces — help separate genuine structural advantage from the mere appearance of it.

Start with what may be Nazara's strongest power: counter-positioning. The mechanism is a valuation arbitrage across two disconnected capital markets. Nazara is listed in India, where public investors have historically awarded gaming and technology names rich equity multiples — often 30 to 40 times earnings — treating Nazara's stock as a premium, permanent pool of capital. It then uses that highly valued equity to buy cash-generating Western casual-gaming studios at deeply depressed, single-digit EBITDA multiples, in a Western market where the big consolidators — think of debt-laden, restructuring conglomerates like Sweden's Embracer Group — have been forced into retreat and cannot compete for deals. Nazara is one of the few cash-rich, actively acquiring global buyers left standing. Buying assets at seven times EBITDA using equity the market prices at thirty-plus times earnings is, mechanically, value-accretive with every deal. This is a real edge — but note its fragility: it depends entirely on the Indian market continuing to award the premium multiple. Counter-positioning that relies on your own inflated valuation evaporates the moment the market re-rates you downward.

The second power is scale economies, and here the evidence is more promise than proof. The theory is that centralized tools — Datawrkz for ad-buying, BestPlay for owned distribution — spread across an expanding portfolio of casual games, driving each title's marginal user-acquisition cost below what a standalone studio could achieve. If it works, every new acquisition makes the whole system more efficient, a genuine flywheel. But scale economies in user acquisition are notoriously hard to sustain, because the advertising platforms constantly re-price to capture the surplus. Investors should treat this as a hypothesis on trial, measurable in the portfolio's acquisition costs over the next several years, not as an established moat.

The third power is a cornered resource, and it is the most durable of the three: India's deep pool of low-cost, high-skill engineering, QA, and live-operations talent. This is the same structural advantage that powered Sportskeeda's dollar-revenue-on-rupee-cost model, now applied to running global casual games. A Barcelona or London studio simply cannot match the cost of maintaining a live game from a Mumbai back office. This advantage is real, structural, and shared across all of Indian IT — which is also its limitation: it is available to any Indian acquirer, so it advantages Nazara against Western peers but not against domestic rivals who might adopt the same playbook.

It helps to place Nazara against the global cohort of casual-gaming consolidators, because the roll-up model is not new — it is simply new to India. Sweden gave the world both the cautionary tale and the template. Embracer Group borrowed heavily to assemble a sprawling empire of studios and IP, and when interest rates rose and a mega-deal fell through, it spent years dismantling and writing down what it had built — the definitive example of a debt-financed roll-up that outran its own balance sheet. Stillfront, another Swedish serial acquirer of casual and mid-core studios, spent much of the 2020s nursing a depressed share price as investors soured on the acquire-and-integrate story. Israel's Playtika, a giant of the "forever franchise" casual model, likewise saw its post-IPO valuation compress as growth slowed. The lesson written across all three is the same: roll-ups are rewarded lavishly on the way up and punished mercilessly the moment organic growth stalls or leverage bites.

Nazara's differentiation from that cohort is instructive. Unlike Embracer, it has funded its expansion with equity rather than debt, which removes the refinancing time-bomb that detonated its Swedish predecessor — a genuinely important distinction, because a company that cannot be forced to sell assets at the bottom controls its own timing. And unlike the Western consolidators, it carries a structural cost advantage in operations that they cannot replicate. But it also lacks their scale, their catalog depth, and their years of live-ops institutional knowledge, and it is attempting cross-border integration from a far greater cultural and geographic distance. The comparison cuts both ways: Nazara has learned from the roll-up graveyard, but it has not yet proven it can avoid joining it.

Now turn the Porter lens on the underlying industry, and the picture sobers considerably. The bargaining power of suppliers — specifically the app platforms — is extraordinarily high. Google Play and the Apple App Store are absolute gatekeepers, historically extracting around 30% of every transaction and dictating the privacy rules that make user acquisition expensive. Nazara does not negotiate with these suppliers; it obeys them. The threat of substitutes is likewise high: casual games do not merely compete with other games but with every other claim on a bored commuter's attention — TikTok, YouTube Shorts, Instagram Reels. And the intensity of rivalry is brutal, with thousands of mobile titles launched daily into a hyper-fragmented market where almost none endure.

A word on domestic rivalry, since it shapes how investors should categorize the stock. Within India, the loudest gaming names — the Dream11s and Mobile Premier Leagues of the world — are real-money and fantasy operators, precisely the cohort the GST ruling gutted. Nazara barely competes with them; it deliberately chose a different lane. Its true competitive set is global casual-gaming publishers and the sea of independent mobile studios worldwide, not the Indian RMG champions. This matters because Indian investors sometimes lump all "gaming" together, which can cause Nazara's valuation to swing on regulatory news that barely touches its business. The mispricing runs both ways — sometimes a discount for sins it did not commit, sometimes a halo from a sector it is not really part of — and a clear-eyed investor should insist on valuing Nazara as what it is: a globally-focused casual and IP publisher that happens to be listed in, and staffed from, India.

The synthesis is nuanced rather than triumphant. Nazara operates in a structurally unattractive industry — powerful suppliers, abundant substitutes, savage rivalry — and its defense is not a better position within that industry but a superior capital and cost model layered on top of it: cheap equity, cheap operations, owned distribution. That is a legitimate strategy, but it is a financial and operational edge rather than a product moat, and financial edges are more reversible than product ones. The durability of the whole story therefore comes down to execution and capital discipline — which puts the spotlight squarely on management.

VIII. Management Credibility & The Activist Stress Test

Before assessing the man, it is worth puncturing the label that follows Nazara everywhere: the "Berkshire Hathaway of Indian gaming." The comparison flatters, and it is not entirely wrong — like Berkshire, Nazara is a holding company that buys cash-generating businesses and leaves competent operators in place. But the differences matter more than the resemblance. Berkshire buys durable, low-technological-change businesses — insurance, railroads, consumer staples — whose competitive position tends to strengthen or hold for decades. Nazara buys mobile games, arguably the most perishable consumer product in existence, where a hit can decay in eighteen months and no title is safe from the next viral upstart. Berkshire's edge is a permanent float of insurance premiums; Nazara's edge is a premium stock multiple that can evaporate. The honest reframing is that Nazara is not a compounder of durable moats but an arbitrageur of mispriced, decaying assets — a legitimate and potentially lucrative activity, but one that requires constant re-execution rather than patient ownership. Investors who buy the Berkshire analogy literally are buying the wrong mental model.

The most important asset on Nazara's balance sheet does not appear on the balance sheet: it is the judgment of Nitish Mittersain. A holding company is only as good as the person deciding what to buy and what to pay, and so the fair way to assess Nazara is the way you would assess any capital allocator — by behavior over time, not by rhetoric in the latest press release.

The bull view of Mittersain is genuinely earned. This is a founder who negotiated his way out of near-bankruptcy rather than folding, who spent two decades learning that discipline beats heroics, and who — critically — did not lose his head during the 2021 tech bubble. When gaming valuations were euphoric and easy money was everywhere, Nazara did not torch capital chasing speculative startups at absurd prices. Instead it raised large amounts of equity while public markets were generous, sat on the cash, and then deployed it into profitable, cash-flowing assets like Fusebox and Bluetile only after global valuations had cooled to single-digit multiples. Buying low with capital raised high is the textbook definition of good allocation, and Mittersain has, so far, actually done it. That is a track record, not a slogan.

But a neutral platform owes readers the skeptic's brief, and it is substantial. The first charge is the organic growth deficit. Strip out acquisitions and Nazara's underlying businesses are not obviously vibrant: Kiddopia has been effectively flat for years as iOS privacy costs bite, and older owned titles like World Cricket Championship are aging assets on the natural decline curve that eventually claims every mobile game. A roll-up that grows only by buying is a treadmill — it must keep making ever-larger acquisitions to show growth, and the moment the deals stop, the organic softness is exposed. The single most important thing to watch is whether anything Nazara already owns can grow on its own.

The second charge is financial engineering, and it lands on the Nodwin deconsolidation. Was carving Nodwin out to an associate a genuine operational decision to give it independence — or a well-timed accounting redesign that doubled the headline consolidated margin, added a ₹1,098 crore non-cash gain to reported profit, and re-rated the story for public markets right before the biggest acquisition in company history? The uncomfortable answer is that the move served both purposes, and investors are entitled to weigh how much of FY26's dazzling optics were operating substance versus presentational choice. Management's credibility here will be earned or lost in the plainer quarters ahead, once the one-time gain is behind them and only the underlying margins remain to be judged.

There is also a governance dimension an activist would probe. A hub-and-spoke holding company with dozens of subsidiaries, associates, and minority stakes — spread across India, the UK, and Spain, with founders retaining operating control and earn-outs still running — is inherently complex to audit and easy to obscure. Related-party dealings, intercompany flows, and the valuation judgments embedded in deconsolidations and fair-value gains all require investor trust in management's disclosure. Nazara's reporting has generally been regarded as adequate for a company of its size, but complexity is itself a risk: the more moving parts a structure has, the harder it is for outsiders to verify that the reported margin improvement is operating reality rather than presentation. An investor comfortable with Nazara is implicitly expressing confidence in the integrity of a fairly intricate set of accounts.

The third and most pointed charge is promoter selling. In May 2026, in the very block deal that the market celebrated for bringing in Nikhil Kamath, Mittersain sold a meaningful slice of his personal holding through Mitter Infotech LLP, reportedly for personal diversification.2021 There is nothing inherently improper about a founder trimming a concentrated position, and Kamath's simultaneous buying was read as a vote of confidence. But the pattern deserves close monitoring: a chief executive selling personal shares in the middle of an ambitious, capital-hungry global expansion is a signal an activist would seize upon, and it sits awkwardly beside the message that the best years lie ahead. The charitable and the cynical readings both remain open, and honest analysis holds them in tension rather than resolving them prematurely. Either way, the selling raises the stakes on execution — because if the expansion stumbles, these are exactly the risks that will define the downside.

IX. The Risk Radar & KPIs to Watch

Every roll-up carries a characteristic set of failure modes, and Nazara's are specific enough to name precisely. The point of a risk radar is not to catalog every macro anxiety but to isolate the handful of mechanisms that could actually break this particular business.

The first and most fundamental is user-acquisition inflation and platform dependence. Nazara's entire cost advantage in casual gaming assumes it can find and keep players affordably. But the levers that determine that — Apple's and Google's privacy rules, ad-tracking permissions, and store policies — sit entirely in the hands of two companies that Nazara cannot influence. A further tightening of tracking, or another change to how the app stores handle advertising identifiers, could simultaneously degrade BestPlay's distribution engine, blunt Datawrkz's targeting, and inflate the cost of keeping Kiddopia and Bluetile's players. The whole thesis has a single point of external control, and Nazara does not hold the switch.

The second is cross-border integration risk, which is precisely the risk a roll-up's history warns about. Nazara is now running a UK story-games studio (Fusebox) and a large Spanish casual-games operation (Bluetile and BestPlay) from a corporate center in Mumbai. Time zones, cultures, and the temperament of creative talent do not integrate as cleanly as spreadsheets suggest. Founder-led studios are held together by their founders; earn-out structures keep them motivated for a few years, and then what? Key-talent departures after the earn-outs vest are a classic roll-up failure mode, and they tend to be followed, unpleasantly, by write-downs.

Which is the third risk: goodwill and impairment. Nazara has now spent well over $150 million on recent acquisitions, and a growing share of its balance sheet consists of goodwill — the accounting residue of paying more than the book value of net assets. Goodwill is fine as long as the acquired businesses perform. The moment one of them underperforms its plan, accounting rules force an impairment — a non-cash charge that slices straight through reported net profit and, more damagingly, punctures the market's faith in the roll-up's dealmaking. In a portfolio of assets facing natural mobile decay curves, the odds that something eventually disappoints are non-trivial.

A fourth risk is the most philosophically interesting because it is reflexive — the thesis can undermine itself. Nazara's whole arbitrage depends on its cost of capital staying low, which is to say on its share price staying high. But the premium multiple is not a birthright; it is a belief the market holds about Nazara's ability to keep doing accretive deals. Should sentiment sour — a bad quarter, an impairment, a governance question, or simply a broad de-rating of Indian small-caps — the multiple compresses, the equity currency loses value, and the very deals that justified the premium become harder to finance. A high valuation that depends on continued dealmaking, and dealmaking that depends on a high valuation, is a loop that runs beautifully in one direction and viciously in the other. This is the deepest fragility in the model, and it cannot be hedged, only monitored.

There is also a currency and cross-border dimension worth a brief note. Nazara now earns a growing share of its revenue in dollars, pounds, and euros — Sportskeeda's US ad revenue, Fusebox's Western players, Bluetile's global base — while much of its cost base sits in rupees. In stable conditions this is a tailwind, converting hard-currency revenue against soft-currency costs. But it also means reported results now carry translation effects, and a sharp move in exchange rates can flatter or distort a quarter in ways unrelated to operating performance. It is not a first-order risk, but it is one more reason to read the underlying operating metrics rather than the headline rupee figures.

So what should an investor actually watch? Amid the noise of quarterly headlines, three key performance indicators cut to the heart of whether the thesis is working. The first is organic segment revenue growth — the year-on-year growth of the existing games and platforms, stripped of newly consolidated acquisitions. This is the single cleanest test of whether Nazara can grow what it already owns, or whether it is merely a treadmill that must keep buying. The second is the LTV-to-CAC ratio on the Bluetile portfolio — in plain terms, whether the lifetime value of a player exceeds the cost of acquiring them, and whether BestPlay's owned distribution actually widens that gap over time. That ratio is the live test of the entire scale-economies-and-owned-distribution promise. The third is the consolidated EBITDA margin excluding equity-accounted associates — the proof, quarter after quarter, that the post-Nodwin margin improvement is real operating performance rather than a one-time optical reset, and that it holds sustainably above the high-teens level. Track those three, and you are tracking the actual business rather than the accounting. They also frame the final question: which way does this story break?

X. Bull vs. Bear Case & Epilogue

Every good investment story resolves into two coherent futures, each internally consistent, each supported by real evidence, and the honest work is to hold both in view without pretending to know which wins.

The bull case is the global arbitrage machine running exactly as designed. In this future, Nazara continues to trade at a premium multiple on the Indian market, giving it an enviable currency — cheap equity — that its capital-starved Western rivals lack. It keeps acquiring stable, cash-flowing casual-gaming and sports-media franchises at six-to-seven times EBITDA, migrates their live-operations and back-end to India's low-cost talent base, and cross-promotes them through BestPlay's owned distribution channel to sidestep the app-store advertising tax. Each disciplined deal is accretive; the Bluetile transaction alone nearly doubled run-rate EBITDA. Repeat that a few times, layer on even modest organic contribution, and earnings per share compound into something formidable — Nazara graduating from an idiosyncratic Indian mid-cap into a genuinely profitable global casual-gaming operator. The bull case is not fantasy; the Fusebox and Bluetile deals are exactly the moves it predicts, executed at exactly the disciplined multiples it requires.

The bear case is the roll-up trap, and it is equally grounded. In this future, sluggish organic growth is not a temporary condition but the permanent truth of the portfolio. Acquired assets — Kiddopia, Fusebox, Bluetile — ride their natural mobile decay curves downward, and the treadmill demands ever-larger deals to paper over the decline. Cross-border integration frays; talent walks after earn-outs vest; user-acquisition inflation erodes the very margins the thesis depends on. Then the impairments arrive, hitting reported profits and, worse, cracking the market's belief in management's dealmaking. And here the counter-positioning power inverts on itself: the premium multiple that made the arbitrage possible collapses toward the ordinary holding-company discount that markets apply to sprawling conglomerates. Cheap equity becomes expensive equity, the machine loses its fuel, and the arbitrage quietly stops.

What separates these two futures is not macro luck but execution and discipline — which is why the management assessment and the three KPIs matter more than any single quarter's headline. The frameworks reinforce the point: Nazara's edges are real but financial and operational rather than product-based, and financial edges must be continuously re-earned. Its strongest power, counter-positioning, is also its most reflexive vulnerability, because it is collateralized by its own share price.

It is worth being explicit about the base rates, because history is not neutral on roll-ups. Most serial acquirers eventually disappoint; the graveyard of debt-fueled, integration-challenged consolidators is well populated, and the market's instinct to apply a "conglomerate discount" to sprawling holding companies is earned, not arbitrary. The burden of proof therefore sits squarely with Nazara: the default expectation for a company of this shape is that organic softness and integration friction eventually overwhelm the arithmetic of accretive deals. What tilts the odds in Nazara's favor, to the extent anything does, is the specific combination it has assembled — equity funding rather than debt, a genuine and rare cost advantage, disciplined entry multiples, and a founder with a demonstrated allergy to overpaying. None of those guarantees success, but together they are why the bull case is a serious argument rather than wishful thinking.

The clearest tell in the years ahead will be simple. If Nazara's next moves are financed by an ever-higher share price and justified by ever-larger deals, while the owned assets quietly stagnate, the treadmill is running and the bear case is winning. If instead the existing portfolio starts to grow on its own, margins hold after the accounting noise clears, and acquisitions become optional rather than existential, the machine is real. The company has told investors, through its actions, that it intends to be the former kind of story with the discipline of the latter. Watching whether it can actually be both is the entire investment question.

The through-line from that Mumbai office in 2004 to the Barcelona cheque in 2026 is remarkably consistent: a founder who learned, under duress, that survival comes from owning the flow of capital and content rather than gambling on a single hit. Nazara has turned that lesson into a genuine strategy and, so far, executed it with more discipline than most roll-ups ever manage. Whether it becomes the arbitrage machine or the roll-up trap will be decided not in the press releases but in the unglamorous quarters ahead — in whether owned assets grow, whether acquired players stay profitable, and whether the margins hold once the accounting fireworks have faded. That is the story worth watching, and it is very much still being written.

References

-

Veteran investor Rakesh Jhunjhunwala invests Rs 180cr in gaming company Nazara Technologies — YourStory, 2017-12 ↩↩

-

Nazara Story: Founders, Business Model, Funding, Revenue — StartupTalky ↩↩↩

-

Nitish Mittersain on building Nazara Technologies — Neon.fund Podcast ↩↩

-

Nazara Technologies Ltd: History, Milestones, Subsidiaries — EnrichMoney ↩↩

-

Nazara profit nearly triples in Q4 even as revenue declines 24% — Storyboard18, 2026-05-12 ↩↩↩

-

Nazara FY26 revenue up 13% YoY at Rs 1,829 cr; EBITDA rises 66% to Rs 255 cr — Adgully, 2026-05 ↩↩

-

Nazara FY26 EBITDA Soars 66% as Gaming Drives 90% of Profits — IndianWeb2, 2026-05 ↩

-

Nazara posts 3x jump in profit to ₹47 crore, even as revenue dips 23.5% — Business Standard, 2026-05-12 ↩↩

-

Nazara Reports Highest-Ever EBITDA in FY26 as its Global Gaming Platform Scales — EquityBulls, 2026-05 ↩↩

-

Rekha Jhunjhunwala's Rs 334 crore exit from Nazara Tech ahead of Online Gaming Bill — Storyboard18, 2025-06 ↩

-

Nazara Tech gains as Rekha Jhunjhunwala pares entire stake — India Infoline, 2025-06 ↩

-

Nazara acquires 'Love Island' games creators Fusebox for $27.2M in all-cash deal — YourStory, 2024-08 ↩

-

Nazara acquires Fusebox Games for $27.2M — VentureBeat/GamesBeat, 2024-08 ↩↩↩

-

Nazara Buys Out Absolute Sports, Raises Stake To 100% — Inc42, 2025 ↩

-

Nazara Technologies becomes sole owner of Absolute Sports (Sportskeeda) — G2G News, 2025 ↩

-

After Zerodha's Nikhil Kamath, SBI Mutual Fund to invest Rs 410 crore in Nazara Technologies — Business Today, 2023-09-07 ↩↩

-

Nazara To Raise INR 250 Cr Via Preferential Issue, Kamath Brothers To Infuse Another INR 100 Cr — Inc42, 2023 ↩

-

Supreme Court Upholds 28% GST on Online Gaming — The Quint, 2026-05-27 ↩

-

Retrospective GST on Online Gaming Explained: Tax Shock or Studio Boom? — Republic World, 2026-05-29 ↩

-

Nazara Technologies in Focus After ₹486 Cr Block Deal; Q4 PAT Increases 1,258% — Trade Brains, 2026-05 ↩↩↩

-

Nazara Sees Major Stake Buy As Zerodha And Axana Estates Invest ₹486 Crore — Business Connect, 2026-05 ↩↩

-

Nazara's ~$100m Bluetile & BestPlay Deal Marks Its Largest Acquisition — InvestGame, 2026-03 ↩↩↩↩

-

Nazara buys controlling stake in Bluetile and BestPlay for $100m — MobileGamer.biz, 2026-03-24 ↩↩↩↩↩↩↩↩↩

-

Nazara To Buy Controlling Stake In Spanish Startups Bluetile, BestPlay For $100 Mn — Inc42, 2026-03 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube