Navin Fluorine International: The Fluorochemical Pioneer

I. Introduction & Episode Roadmap

Picture this: In a nondescript industrial complex in Surat, Gujarat, technicians in hazmat suits carefully monitor gauges as hydrofluoric acid—one of the most corrosive substances known to chemistry—flows through specialized Hastelloy pipes. This isn't a scene from Breaking Bad. It's Tuesday morning at Navin Fluorine International, where for over five decades, teams have been quietly mastering some of the most dangerous chemistries on the planet.

Today, Navin Fluorine stands as a ₹24,700+ crore colossus in India's specialty chemical landscape, generating ₹2,551 crore in revenue. But here's what makes this story extraordinary: While most Indian chemical companies were content being toll manufacturers or commodity producers, Navin bet its entire future on fluorine—an element so reactive it can etch glass, so specialized that only a handful of companies worldwide dare to work with it at scale.

The central question we're exploring today cuts to the heart of industrial transformation: How did a 1967 refrigerant manufacturer, born in the license raj era when getting a phone connection took years, evolve into a global CDMO powerhouse that pharma giants trust with their most complex molecules? How did a company making simple cooling gases end up producing advanced materials for AI data centers?

This isn't just a chemicals story—it's a masterclass in technical moat-building, a case study in navigating global supply chain shifts, and perhaps most importantly, a window into how patient capital and deep expertise can create enduring value in industries most investors find too complex to understand.

We'll journey from the founding days when the Mafatlal family first decided to bring fluorochemicals to India, through the refrigerant boom that made "Mafron" a household name, into the specialty chemical pivot that transformed margins, and finally to today's AI-age opportunity in advanced cooling materials. Along the way, we'll decode the strategic choices, the near-misses, and the technical capabilities that separate winners from also-rans in specialty chemicals.

Buckle up—we're about to dive deep into one of India's most underappreciated industrial stories.

II. The Mafatlal Legacy & Founding Context

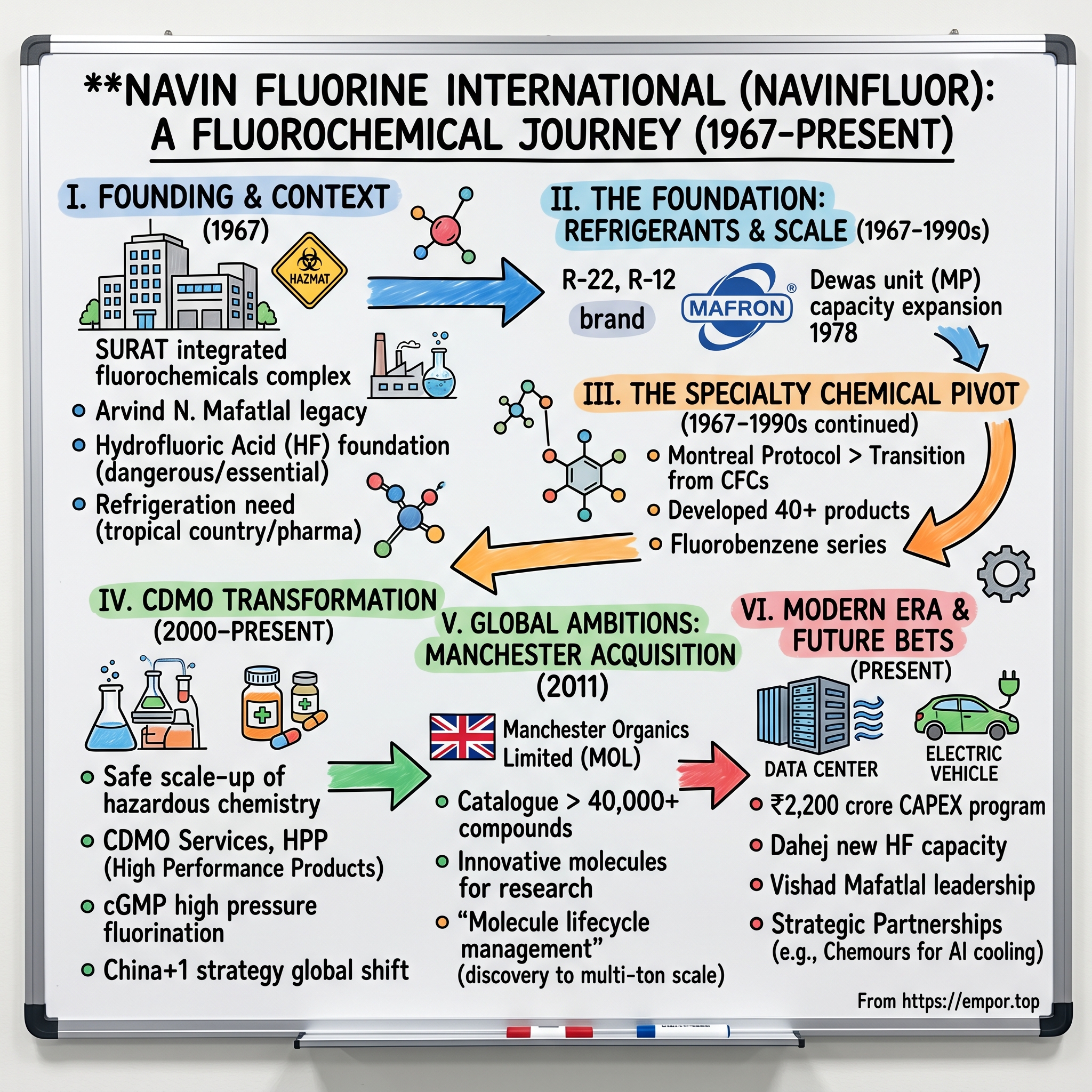

The year is 1967. Indira Gandhi has just become Prime Minister. The Green Revolution is beginning to transform Indian agriculture. And in the industrial corridors of Mumbai, Arvind N. Mafatlal—scion of one of India's most respected business families—is contemplating a radical idea: bringing fluorine chemistry to India.

The Padmanabh Mafatlal Group wasn't new to bold industrial ventures. Since the early 20th century, the Mafatlals had built textile mills, championed indigenous manufacturing, and earned a reputation as builders of institutions rather than mere businesses. But fluorochemicals? This was different. This was dangerous, capital-intensive, and required technical expertise that simply didn't exist in India.

Arvind Mafatlal saw what others missed. Post-independence India was industrializing rapidly. Refrigeration would be critical—for preserving food in a tropical country, for the nascent pharmaceutical industry, for the comfort of a rising middle class. And at the heart of refrigeration lay fluorinated compounds. Every refrigerator, every air conditioner, every cold storage facility would need what he planned to make.

The strategic choice of Surat as the manufacturing location was brilliant in hindsight. Gujarat's entrepreneurial culture, proximity to ports for importing raw materials, and the state government's industrial policies created the perfect ecosystem. But more importantly, Surat offered something crucial: distance from population centers while maintaining connectivity—essential when you're handling hydrofluoric acid that can dissolve glass and cause fatal burns through intact skin. Building that first integrated fluorochemicals complex in Southeast Asia wasn't just about importing technology—it was about creating an entire ecosystem from scratch. Between 1967 and 1969, Navin established what would become the largest integrated fluorochemicals complex in India, starting with the most fundamental building block: hydrofluoric acid (HF).

Think about the audacity of this move. HF isn't just dangerous—it's uniquely terrifying. Unlike other acids that cause immediate burns, HF penetrates through skin and tissue, seeking calcium in bones. A splash the size of your palm can be fatal. Yet Arvind N. Mafatlal founded the company in 1967 with the conviction that mastering this chemistry was essential for India's industrial future.

The timing was impeccable. India's economy was transitioning from agricultural to industrial. The Green Revolution demanded cold storage. The pharmaceutical industry needed specialized solvents and intermediates. Every new factory needed industrial cooling. Navin positioned itself at the intersection of all these needs, becoming not just a chemical company but critical infrastructure for India's modernization.

By 1969, commercial production of refrigerant gases had begun. The "Mafron" brand was born—a name that would become synonymous with cooling in India, much like Xerox became synonymous with photocopying. But unlike many industrial pioneers who remained content with their initial success, the Mafatlals understood something crucial: in chemicals, standing still means falling behind.

III. Building the Foundation: Refrigerants & Scale (1967–1990s)

The Surat facility in 1969 looked nothing like a modern chemical complex. Workers manually operated valves, temperatures were monitored with mercury thermometers, and safety equipment was rudimentary by today's standards. But what they lacked in sophistication, they made up for in engineering discipline and respect for the chemistry.

The company commenced its refrigerant business in 1967 and established itself as a respected refrigerant global brand. The early product lineup was straightforward: R-22 (chlorodifluoromethane) for air conditioning, R-12 for refrigerators, and a handful of other chlorofluorocarbons (CFCs) that powered India's cold chain. These weren't sexy products, but they were essential. Every bottle of milk that stayed fresh, every vaccine that remained potent, every air-conditioned cinema hall—all depended on Navin's output.

In 1978, the company commissioned its Dewas unit in Madhya Pradesh, marking the first major capacity expansion. The choice of Dewas was strategic—central location for distribution, availability of skilled chemical workers, and critically, distance from the coast meant lower land costs while maintaining rail connectivity to major markets.

The 1980s brought new challenges. The Montreal Protocol loomed on the horizon, threatening to ban the very CFCs that formed Navin's bread and butter. Lesser companies might have lobbied against change or milked existing assets. Navin did something different—they invested deeper in fluorine chemistry, expanding beyond simple refrigerants into organic and inorganic specialty fluorides. The 1990s to 2000 marked a pivotal transformation period. Navin Fluorine developed more than 40 products on commercial scale using indigenously built multipurpose plants, expanding into the fluorobenzene series and other specialty fluorinated compounds. This wasn't just product diversification—it was a fundamental shift in capability. Each new molecule required mastering different reaction conditions, handling protocols, and purification techniques.

The transition from refrigerants to specialty chemicals revealed something profound about chemical manufacturing: commodities teach you scale, but specialties teach you precision. By the late 1990s, Navin had learned both. The company was producing everything from simple inorganic fluorides for aluminum smelting to complex organofluorine intermediates for pharmaceuticals.

Economic liberalization in 1991 changed everything. Suddenly, Indian companies could import technology, export freely, and compete globally. For Navin, this meant access to international customers who needed reliable suppliers of fluorinated intermediates. The company built an impressive clientele consisting of several Fortune 500 companies, including five of the top ten global crop protection companies and three of the top ten global chemical companies.

But perhaps the most important development of this era was cultural. The company began to see itself not as a fluorochemicals manufacturer, but as a fluorine chemistry specialist. This subtle shift—from product to capability—would define everything that followed.

IV. The Specialty Chemical Pivot (2000–2010)

The new millennium brought a stark realization to Navin's boardroom: refrigerants were becoming a commodity business. Chinese manufacturers were flooding the market with cheap R-22. Margins were compressing. The writing was on the wall—survive as a commodity player or transform into something more.

In 2008, Navin established its state-of-the-art R&D centre, the Navin Research Innovation Centre (NRIC), followed by the commissioning of a new pilot plant in 2009. This wasn't just infrastructure investment—it was a declaration of intent. The NRIC became the nerve center for Navin's transformation, housing sophisticated analytical equipment, fume hoods designed for fluorine chemistry, and most importantly, a team of PhD chemists who understood both the science and the business of fluorination.

The pilot plant deserves special attention. In specialty chemicals, the gap between laboratory success and commercial production is littered with failed ventures. Reactions that work perfectly in a 250ml flask can become nightmares in a 2000-liter reactor. Heat transfer changes, mixing dynamics shift, impurities that were negligible at small scale become deal-breakers. Navin's pilot plant bridged this valley of death, allowing them to validate processes at 50-100 kg scale before committing to commercial production.

In June 2006, Navin initiated a CDM project to reduce greenhouse gas HCFC 23 with Ineos Fluor as technology partners, receiving UNFCCC approval in March 2007. This Clean Development Mechanism project was more than environmental compliance—it was Navin's first major collaboration with a global fluorochemical giant, proving they could execute complex technical projects to international standards.

The real breakthrough came in Contract Research and Manufacturing Services (CRAMS), now known as CDMO. Global pharmaceutical companies were increasingly outsourcing synthesis of complex intermediates. But fluorinated molecules? Most CDMOs wouldn't touch them. Too dangerous, too specialized, too capital-intensive. Navin saw opportunity where others saw obstacles.

At Dewas, they developed a cGMP compliant site for CRAMS from the very inception. They invested Rs. 65 crores in building a cGMP compliant manufacturing unit to create ton-level capabilities. This became India's only cGMP compliant high pressure fluorination facility.

The numbers tell the story of transformation. By 2010, Navin wasn't just making refrigerants anymore. They were synthesizing advanced intermediates for blockbuster drugs, supplying key building blocks for next-generation agrochemicals, and earning gross margins that would make software companies envious.

But the most important achievement of this decade wasn't captured in any financial statement. It was trust. When a pharmaceutical company hands over synthesis of a critical intermediate for a drug worth billions in annual sales, they're not just buying chemicals—they're buying reliability, confidentiality, and the confidence that their supplier can handle anything that goes wrong at 2 AM on a Sunday.

V. The Manchester Acquisition & Global Ambitions (2011)

In the genteel suburb of Runcorn, near Manchester, sat a small specialty chemical company with an outsized reputation. Manchester Organics Limited wasn't large—barely 50 employees—but in the rarefied world of complex fluorination, they were royalty. Their catalog contained thousands of exotic fluorinated compounds, many unavailable anywhere else. Their chemists had forgotten more about organofluorine synthesis than most would ever learn.

In 2011, NFIL acquired a 51% controlling stake in Manchester Organics Ltd, further enhancing its capabilities to undertake more complex fluorination projects and additionally increase its pipeline of speciality fluoro-organics. For Navin, this wasn't just an acquisition—it was a masterclass in capability building.

When Navin started working with Manchester Organics in May 2011, it had a catalogue of around 8,000 compounds. Today, the number stands at more than 40,000 compounds, including many innovative molecules helping innovator companies in their research efforts.

The synergies were obvious but executing them was complex. Manchester Organics was working directly with innovative pharma companies on milligram to multi kilo research phase, while Navin Fluorine was developing its contract research and manufacturing services division with experience in multi hundred kilos to multi ton production activities. Together, they could offer pharmaceutical companies a complete solution—from discovery to commercial scale.

Cultural integration proved surprisingly smooth. Both companies shared a deep respect for chemistry, an obsession with safety, and an understanding that in specialty chemicals, reputation takes decades to build and moments to destroy. The Manchester team brought sophisticated European customer relationships and cutting-edge synthetic techniques. Navin brought scale, cost advantages, and manufacturing muscle.

In October 2015, Navin acquired the balance equity stake of 49% through their 100% subsidiary NFIL UK Limited. Over the years, they further enhanced the scientific capabilities at the MOL site at Runcorn. This full acquisition marked Navin's evolution from an Indian company with global ambitions to a truly global company with Indian roots.

The Manchester acquisition also brought something intangible but invaluable: credibility with Western pharmaceutical companies. Having a European subsidiary with EU-standard facilities and local technical teams made conversations with Swiss pharma giants and American biotechs much easier. It was no longer an Indian vendor pitching services—it was a global partner offering solutions.

More importantly, the acquisition created a continuous innovation pipeline. Manchester's chemists would work with customers on early-stage molecules, developing synthetic routes and producing research quantities. As molecules progressed through clinical trials, production would seamlessly transfer to Navin's larger facilities in India for scale-up. When drugs received approval, commercial manufacturing could happen at the multi-ton scale in Dewas or Surat.

This "molecule lifecycle management" became Navin's secret sauce—they could partner with a pharmaceutical company from discovery through commercialization, becoming so embedded in the supply chain that switching vendors became almost unthinkable.

VI. The CDMO Transformation (2010–Present)

The conference room in Mumbai was tense. It was 2015, and Navin's board was reviewing the CDMO division's performance. Several high-profile molecules had failed in clinical trials. Millions in development costs—gone. Equipment time allocated to molecules that would never see commercial production. The easy decision would have been to retreat, to focus on the profitable specialty chemicals business.

Instead, they doubled down.

The CDMO business, later branded as Navin Molecular, wasn't just another division—it was Navin's bet on the future of chemical manufacturing. The thesis was simple but powerful: as pharmaceutical companies focused increasingly on drug discovery and marketing, they would need partners who could handle the messy, dangerous, complex chemistry of actually making the drugs.

As part of the Padmanabh Mafatlal group, Navin Fluorine was founded in 1967 with a rich track record in the production of refrigerants, inorganic fluorides, and speciality organofluorides. But the CDMO transformation required different capabilities entirely.

The strategic positioning was clear: "Forward thinking CDMO focused on safe scale-up of hazardous chemistries." This wasn't marketing fluff—it was a precise articulation of competitive advantage. While other CDMOs avoided dangerous reactions, Navin embraced them. High-pressure reactions that could turn a reactor into a bomb? Navin had the equipment and expertise. Reactions requiring hydrogen fluoride that could dissolve glass and bone? Routine work for teams trained since the 1960s.

The business evolved into three pillars:

High Performance Products (HPP): These were Navin's proprietary molecules, developed in-house or in collaboration with customers. Higher margins, longer contracts, deeper moats.

CDMO Services: Custom synthesis and manufacturing for pharmaceutical and agrochemical companies. Lower margins than HPP but steady revenues and strategic relationships.

Specialty Chemicals: The original business, now transformed. Still producing fluorinated intermediates but for increasingly sophisticated applications.

The capacity expansion tells the story of ambition. From 220 kiloliters of reactor capacity, Navin planned to reach over 400 kiloliters by 2025-26. But raw capacity was less important than capability. Each new reactor was designed for maximum flexibility—able to handle different pressures, temperatures, and chemistries. Glass-lined for corrosive reactions, Hastelloy for extreme conditions, stainless steel for standard processes.

The China+1 strategy of global pharmaceutical companies became a massive tailwind. As geopolitical tensions rose and supply chain vulnerabilities became apparent during COVID-19, having a reliable non-Chinese supplier of critical intermediates became strategic, not just economical. Navin was perfectly positioned—lower cost than Western suppliers, more reliable than Chinese competitors, with the technical sophistication to handle complex molecules.

In a recent major win, Navin's Pharma CDMO business signed a multi-year contract with Fermion Oy of Finland for supply of non-fluoro patented commercial intermediates, subject to regulatory approvals, for a minimum period of 3 years starting CY 2025. The volume projections represent a multi-million Euro commercial opportunity.

But the real transformation was organizational. CDMO requires a different mindset than commodity chemicals. Every customer molecule is unique, every project has different requirements, timelines are sacred, and confidentiality is paramount. Navin built separate teams, implemented strict information barriers between projects, and created a culture where customer success was the primary metric.

The validation came from customers voting with their wallets. Repeat business rates exceeded 80%. Multi-year contracts became common. And increasingly, customers were coming to Navin not just for manufacturing but for process development—trusting them to figure out how to make new molecules efficiently and safely.

VII. Current Leadership & Modern Era

The company is currently headed by second-generation entrepreneur, Vishad Mafatlal, who has over 25 years' experience in textile and chemical sectors. Second-generation transitions in family businesses are where empires either evolve or atrophy. Vishad Mafatlal chose evolution. Where his predecessors built a chemicals company, Vishad is building a technology company that happens to make chemicals. The difference is profound. Under his leadership, Navin has committed to a massive ₹2,200 crore capital expenditure program, but this isn't just capacity expansion—it's capability transformation.

The crown jewel of this expansion is NFASL (Navin Fluorine Advanced Sciences Limited), a wholly-owned subsidiary executing five new plants at Dahej—three for High Performance Products and two Multi-Purpose Plants. In March 2023, the NFASL board approved a capital expenditure of Rs 450 crores for setting up a new 40,000 tonnes per annum hydrofluoric acid capacity at Dahej, expanding total HF capacity from 20,000 TPA to 60,000 TPA.

The organizational structure has evolved to match the complexity of the business. Separate verticals for different business lines, dedicated project management teams for major customer programs, and importantly, a significant investment in digital infrastructure. ERP systems that can track batch genealogy across multiple plants, predictive maintenance algorithms that prevent unplanned shutdowns, and data analytics that optimize reaction conditions in real-time.

But perhaps the most significant change under current leadership is the shift from reactive to proactive strategy. Instead of waiting for customer requirements, Navin now anticipates market needs. The investment in battery chemicals for EVs, materials for renewable energy, and most recently, cooling fluids for data centers—all represent bets on future demand rather than responses to current orders.

The company has also professionalized governance while maintaining family involvement. Independent directors with deep industry expertise, audit committees with real teeth, and transparent communication with stakeholders. The promoter holding of 27.1% signals skin in the game without stifling professional management.

The talent strategy has been particularly impressive. Navin has recruited senior executives from global chemical giants, built partnerships with premier Indian technical institutes, and created career paths that retain top talent. The company now employs over 1,000 people, including dozens of PhDs and hundreds of chemical engineers.

The R&D investment has intensified dramatically. Beyond the NRIC in Surat, Navin has built specialized labs for different chemistries, invested in computational chemistry capabilities, and created innovation partnerships with customers where joint IP development happens. This isn't the R&D of the past—copying molecules and optimizing yields. This is fundamental research into new fluorination methods, novel catalysts, and green chemistry alternatives.

Recent performance validates the strategy. Q1FY26 showed 39% sales growth, demonstrating that the investments are translating into revenue. But more importantly, the customer quality has improved. Navin now counts most of the world's top pharmaceutical and agrochemical companies as clients, with multi-year contracts becoming the norm rather than the exception.

VIII. Strategic Partnerships & Future Bets

The morning of May 6, 2025, marked a watershed moment. Chemours announced a strategic agreement with Navin Fluorine to manufacture its Opteon™ two-phase immersion cooling fluid. To understand the significance, you need to understand the AI infrastructure crisis unfolding in Silicon Valley and beyond.

Modern AI chips generate heat densities that would melt traditional cooling systems. A single Nvidia H100 GPU can consume 700 watts—stack thousands in a data center, and you're dealing with megawatts of heat that must be removed instantly. Traditional air cooling has hit a wall. Water cooling helps but requires massive infrastructure and consumes millions of gallons. Enter two-phase immersion cooling—submerge the chips in a special fluid that boils at low temperature, carrying away heat as it vaporizes, then condenses and returns. It's elegant, efficient, and requires fluids with very specific properties.

The company's proprietary Opteon™ fluid offers an ultra-low global warming potential (10), a power usage effectiveness (PUE) approaching 1, and superior performance capabilities compared to traditional or other liquid cooling technologies. Nearly eliminating water use, reducing space requirements by 60%, and lowering energy consumption by up to 40% and cooling energy use by up to 90%.

For Navin, this partnership represents more than a supply agreement—it's validation of their evolution from commodity chemical manufacturer to advanced materials innovator. "Joining forces with Chemours to manufacture their new liquid cooling technology advances our mission to produce high-quality, innovative, and sustainable, high-growth-potential products in the specialty chemicals sector, while helping address a key industry challenge for data centers," said Vishad Mafatlal, Navin Fluorine executive chairman.

The timing is exquisite. As AI computation demands explode, cooling has become the bottleneck. The partnership with Navin Fluorine marks an important step toward commercialization, providing critical capabilities and capacity—beginning in 2026—to support the adoption of two-phase liquid cooling. Navin isn't just manufacturing to Chemours' specifications—they're co-developing the production processes, optimizing for scale, and potentially becoming the sole global supplier of a fluid that could cool the AI revolution.

But the Chemours partnership is just one example of Navin's strategic positioning. Earlier, they had signed their largest contract to date—a ₹2,900 crore agreement for a seven-year period, with Navin investing Rs. 365.50 crores to set up a dedicated manufacturing facility and approximately Rs. 71 crores for a captive power plant at Dahej.

The partnership strategy extends beyond single customers. Navin has built relationships with global pharma majors through their CDMO business, with agrochemical giants through specialty intermediates, and now with technology companies through advanced materials. Each relationship brings not just revenue but knowledge—understanding of cutting-edge applications, exposure to new chemistries, and most importantly, trust that enables deeper collaboration.

The technology focus is deliberate and differentiated. While competitors chase volume in standard fluorination, Navin has built capabilities in the most challenging areas: high-pressure reactions that few dare attempt, toxic material handling that requires exceptional safety protocols, and complex multi-step syntheses that demand both chemistry expertise and engineering excellence.

The semiconductor opportunity looms large. As chip manufacturing potentially shifts from East Asia, specialty chemicals for semiconductor production—etchants, cleaning agents, deposition precursors—all require fluorine chemistry. Navin's existing capabilities in ultra-pure materials and trace impurity control position them perfectly for this market.

Looking ahead, the bets are clear: data center cooling for the AI boom, battery materials for the EV transition, advanced materials for renewable energy, and continued growth in pharmaceutical intermediates as drug complexity increases. Each bet leverages the same core capability—mastery of fluorine—but opens entirely new revenue streams.

IX. Playbook: Business & Investment Lessons

Step back from the specific story of Navin Fluorine, and patterns emerge—lessons applicable far beyond specialty chemicals. This is a playbook for building enduring industrial value in an age that worships software margins and platform effects.

Lesson 1: Technical Moats Are Real Moats

In software, moats erode quickly. Today's breakthrough algorithm is tomorrow's open-source library. But in specialty chemicals, technical moats can last decades. Handling hydrofluoric acid safely at scale isn't something you learn from YouTube tutorials. It requires specialized equipment, trained personnel, regulatory permits, and most importantly, accumulated tacit knowledge—the kind that lives in the heads of operators who've run these reactions thousands of times.

Navin's moat isn't just fluorine chemistry—it's fluorine chemistry at scale, with reliability, meeting pharma-grade specifications, with global regulatory compliance, and customer trust built over decades. Try replicating that with venture capital and a slide deck.

Lesson 2: Complexity Is Your Friend

Most businesses seek simplification. Navin embraced complexity. Each new chemistry they mastered—high-pressure fluorination, organometallic reactions, hazardous material handling—added another layer to their capability stack. Customers don't come to Navin for simple molecules; they come for the ones nobody else will touch.

This complexity compounds. The company that can handle both HF and high pressure can do reactions others can't. The company that can do those reactions at both milligram and ton scale can serve customers others can't. The company that can do all that with regulatory compliance and supply chain reliability becomes irreplaceable.

Lesson 3: Capital Allocation in Chemicals Is Chess, Not Checkers

Every reactor is a bet on future chemistry needs. Build for today's products, and you're obsolete tomorrow. Build too flexible, and you're inefficient. Navin's approach—modular expansion, multi-purpose plants, strategic product dedication—shows masterful capital allocation.

The NFASL subsidiary structure is particularly clever. By housing new capacity in a separate entity, Navin can optimize financing, manage risk, and potentially bring in strategic partners without diluting the core business. The ₹2,200 crore capex program isn't just growth spending—it's portfolio construction.

Lesson 4: Backward Integration Is Forward Thinking

Navin's control of the fluorine value chain from HF production through complex organics provides multiple advantages: cost control, quality assurance, supply security, and importantly, the ability to say yes when competitors must say no. When a customer needs a novel fluorinated intermediate, Navin doesn't need to source fluorinating agents—they make them.

The recent expansion to 60,000 TPA of HF capacity isn't just about selling more hydrofluoric acid—it's about ensuring Navin never has to turn down a high-value project due to raw material constraints.

Lesson 5: Trust Scales Exponentially

In specialty chemicals, trust is everything. When a pharma company shares the structure of a drug candidate worth potential billions, they're betting their entire program on their supplier's discretion and reliability. One leak, one quality failure, one missed deadline can destroy years of work.

Navin built trust slowly and guards it zealously. Separate teams for different customers, strict confidentiality protocols, and most importantly, a track record of delivery. This trust enables deeper partnerships—joint development projects, exclusive supply agreements, early-stage collaboration—that create switching costs far beyond simple commercial relationships.

Lesson 6: Market Transitions Are Opportunities, Not Threats

The Montreal Protocol could have killed Navin's refrigerant business. Instead, they used it to move up the value chain. The shift from CFCs to HCFCs to HFCs to HFOs—each transition required new chemistry, new investment, and scared away competitors. Navin embraced each change, emerging stronger.

Today's transitions—China+1 supply chain diversification, sustainability requirements, AI infrastructure needs—are similar opportunities. While competitors debate whether these trends are permanent, Navin is already building capacity to serve them.

Lesson 7: Geography Is Strategy

Navin's multi-location strategy—Surat for integration and scale, Dewas for cGMP compliance, Dahej for expansion, Manchester for innovation and customer proximity—shows sophisticated thinking about geography as competitive advantage.

Each location serves different purposes: cost optimization, regulatory compliance, customer confidence, talent access. This isn't just manufacturing footprint—it's strategic positioning that enables Navin to serve different customer needs while optimizing costs and managing risks.

The Meta-Lesson: Industrial Capitalism Still Works

In an era obsessed with asset-light business models and software margins, Navin Fluorine proves that old-fashioned industrial capitalism—making complex physical products that require massive capital investment and deep technical expertise—still creates value.

The company trades at 9.11x book value, has generated consistent returns, and faces growing demand for its products. This isn't despite being capital-intensive and technically complex—it's because of it. The very factors that make the business difficult to build make it valuable once built.

X. Analysis & Bear vs. Bull Case

Let's strip away the narrative and examine Navin Fluorine with cold, analytical eyes. At ₹24,700 crore market cap on ₹2,551 crore revenue, the market is pricing in significant growth. Is it justified?

The Bull Case: A Structural Winner in Multiple Secular Trends

Bulls see Navin as perfectly positioned at the intersection of multiple irreversible trends. The pharma industry's shift toward complex molecules requiring specialized chemistry isn't reversing—it's accelerating. Of the new drugs approved in recent years, over 50% contain fluorine. As biologics hit patent cliffs, small molecule drugs with complex syntheses are resurging. Navin's CDMO capabilities directly benefit.

The China+1 imperative has moved from nice-to-have to must-have. COVID exposed supply chain vulnerabilities, geopolitical tensions made them permanent concerns. The recent multi-year contract with Fermion Oy of Finland for supply of non-fluoro patented commercial intermediates, representing a multi-million Euro commercial opportunity, validates Navin's emergence as a trusted alternative to Chinese suppliers.

The data center cooling opportunity could be transformative. If AI compute demand grows as projected, and if two-phase immersion cooling becomes standard for high-density deployments, Navin's partnership with Chemours positions them at the center of a potentially massive market. We're talking about cooling infrastructure for hundreds of billions in AI hardware investment.

The technical moat is real and widening. Each year, safety and environmental regulations get stricter. Each year, the chemistry gets more complex. Each year, customer relationships deepen. A new entrant would need to spend billions and decades to reach Navin's current position—and by then, Navin would have moved further ahead.

Financial momentum supports the narrative. Q1FY26 showed 39% sales growth, demonstrating that investments are converting to revenue. The ₹2,200 crore capex program, while dilutive short-term, positions the company for step-function growth as capacity comes online.

Management quality is proven. The successful transition from commodity to specialty, the strategic Manchester acquisition, the Chemours partnership—these show sophisticated strategic thinking and execution capability.

The Bear Case: Priced for Perfection in a Cyclical Industry

Bears worry that the market is extrapolating peak conditions. Trading at 9.11 times book value implies exceptional returns on capital. But ROE of 13.1% over the last 3 years suggests the business isn't generating returns that justify such valuations.

The CDMO business faces execution risks. Drug development is inherently uncertain—molecules fail, programs get canceled, big pharma changes strategies. Navin could invest heavily in capacity for molecules that never commercialize. The industry graveyard is full of CDMOs that bet wrong.

Competition is intensifying. Chinese players aren't standing still—they're moving up the value chain, improving quality, and accepting lower margins. Indian competitors like PI Industries and Aarti Industries are also expanding into complex chemistries. Navin's advantages are real but not insurmountable.

Customer concentration could be a hidden risk. While Navin serves many customers, a small number of products or programs likely drive outsized profits. Loss of a key molecule or customer relationship could significantly impact financials.

Environmental and regulatory risks are ever-present. One major incident—a leak, explosion, or environmental violation—could shut down operations for months and destroy reputation permanently. The Bhopal disaster still haunts Indian chemical companies' valuations nearly 40 years later.

The capex cycle is concerning. Spending ₹2,200 crore before demand materializes is risky. If growth disappoints, Navin could face overcapacity, margin pressure, and return dilution. The chemical industry is littered with companies that built for demand that never came.

Technology disruption, while unlikely, isn't impossible. Could AI-designed drugs reduce complexity? Could continuous flow chemistry replace batch reactors? Could synthetic biology eliminate the need for chemical synthesis? Low probability, but high impact if they occur.

The Balanced View: Quality Company, Valuation Questions

The truth likely lies between extremes. Navin Fluorine is undoubtedly a high-quality company with real competitive advantages, positioned in attractive markets, with capable management. The strategic initiatives around data center cooling, CDMO expansion, and specialty chemicals make sense.

However, at current valuations, much good news appears priced in. The market is betting on successful execution across multiple fronts—CDMO growth, data center cooling adoption, continued specialty chemical margins, and no major operational hiccups.

The key monitorables for investors: - CDMO revenue growth and margin evolution - Progress on data center cooling fluid commercialization - Capacity utilization of new investments - Customer diversification metrics - Regulatory compliance track record - Competition from Chinese and Indian peers

The risk-reward calculus depends on investment horizon and risk tolerance. For long-term investors believing in India's chemical manufacturing story and Navin's execution capabilities, current levels might prove reasonable. For those seeking near-term catalysts or margin of safety, patience might be warranted.

XI. Epilogue & Recent Developments

As we record this story in late 2025, Navin Fluorine stands at an inflection point. The old business—refrigerants and commodity fluorides—continues to generate cash. The new businesses—CDMO and advanced materials—are scaling rapidly. The future business—data center cooling and whatever comes next—is just beginning.

The company that started in 1967 making refrigerants for a newly independent India now makes molecules that could enable the AI revolution. It's a remarkable transformation, but in many ways, Navin has remained consistent: deep technical expertise, patient capital allocation, strategic customer relationships, and above all, respect for the chemistry.

What would success look like in 5-10 years? Perhaps Navin becomes the global leader in fluorinated pharmaceutical intermediates, the way TSMC dominates semiconductor manufacturing. Perhaps their cooling fluids become industry standard, making them essential infrastructure for the digital economy. Perhaps they discover the next transformative application of fluorine chemistry—in batteries, semiconductors, or something we haven't imagined yet.

The challenges are real. Execution risk on the massive capex program. Competition from China and other Indian players. Regulatory and environmental pressures that only intensify. The cyclical nature of chemical markets. The concentration risk in key products and customers.

But step back, and the larger story is compelling. The world needs more complex molecules—for treating diseases, growing food, storing energy, processing information. Making these molecules requires specialized chemistry. Fluorine, with its unique properties, will be central to many of them. And Navin Fluorine, with its half-century of expertise, stands ready to deliver.

The lesson for entrepreneurs is clear: in industries with real technical barriers, patient capital and deep expertise can build enduring value. The lesson for investors is equally clear: identifying these companies early, before the market fully appreciates their potential, can generate exceptional returns.

As the global economy reshapes around sustainability, supply chain resilience, and technological advancement, companies like Navin Fluorine—bridging the physical and digital, combining old-economy manufacturing with new-economy innovation—may prove to be the real winners.

The story of Navin Fluorine is far from over. In fact, as data centers proliferate, drugs become more complex, and sustainability demands intensify, the most interesting chapters may be just beginning. The company that mastered one of the most dangerous elements on the periodic table is now betting it can master the challenges of the 21st century. Based on their track record, it would be unwise to bet against them.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube