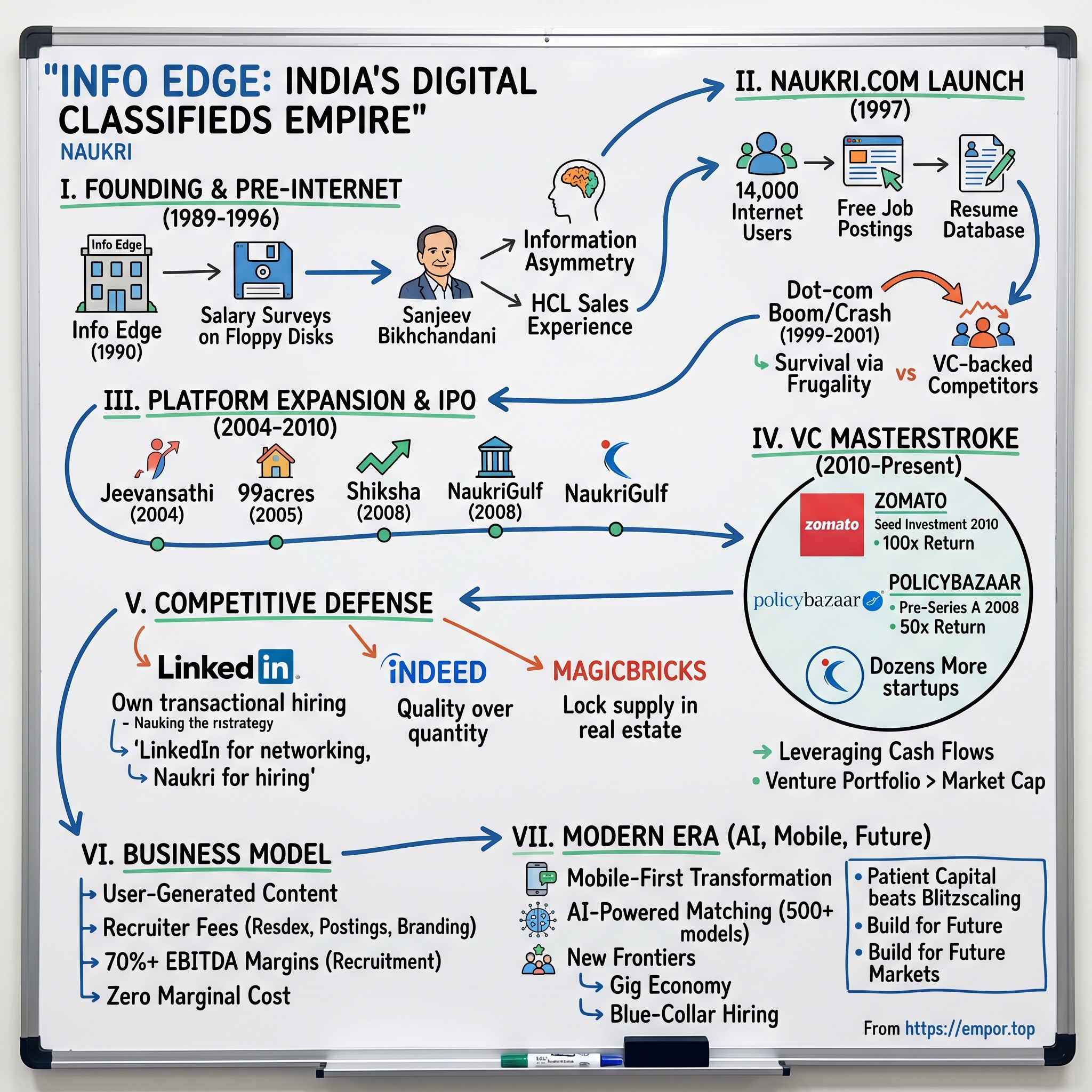

Info Edge: The Story of India's Digital Classifieds Empire

I. Introduction & Episode Roadmap

Picture this: It's 1997 in New Delhi. The internet barely exists in India—just 14,000 users nationwide. A former management consultant named Sanjeev Bikhchandani is trying to convince recruiters to post job listings on something called a "website." They look at him like he's speaking Martian. "Why would we need the internet when we have Times of India classifieds?" they ask. Fast forward to today: that website, Naukri.com, processes 75 million job searches monthly, and Bikhchandani's company Info Edge sits on a venture portfolio worth more than its entire market cap—including a stake in Zomato that alone returned 100x.

How did a database-on-a-floppy-disk company become India's most successful internet investor? How did they defend against LinkedIn, Monster, and Indeed? And why does a company trading at ₹8,000 crores hold investments worth nearly ₹15,000 crores?

Info Edge is actually two stories wrapped in one ticker symbol. First, it's the tale of building India's digital classifieds empire—Naukri for jobs, 99acres for real estate, Jeevansathi for matrimony, Shiksha for education. Second, it's about using those cash flows to become one of India's sharpest venture investors, backing Zomato at seed, Policybazaar pre-Series A, and dozens more.

This is a story about patience in the land of blitzscaling, about building moats before markets exist, and about the peculiar economics of classifieds that generate 70% EBITDA margins. It's about surviving the dot-com crash with ₹7 lakhs in the bank while competitors with $50 million went bust. And ultimately, it's about understanding that in emerging markets, timing isn't just important—it's everything.

We'll journey from pre-liberalization India through the IT boom, from dial-up modems to AI-powered matching, from bootstrapping to becoming a listed company that's part operating business, part venture fund. Along the way, we'll decode the playbook for building in markets that don't exist yet, why classifieds might be the best business model ever invented, and what happens when you compound patience with network effects for three decades.

Buckle up. This isn't just another tech story—it's the blueprint for how to build an empire by seeing the future before it arrives.

II. Pre-Internet India & The Founding Story (1989–1995)

The year is 1989. India is still two years away from economic liberalization. If you want to import a computer, you need a license that takes six months. Making an international phone call requires booking a trunk call hours in advance. The internet? That's something a few academics at IITs whisper about. In this analog world, a young IIM Ahmedabad graduate named Sanjeev Bikhchandani is working at HCL, selling computers to companies that barely understand what they're buying.

But Bikhchandani isn't your typical IIM grad chasing an MNC package. His father was an army doctor, his mother a housewife—middle class, not business class. At IIM-A, while classmates dreamed of investment banking, he was fascinated by something else entirely: information asymmetry. "I kept thinking," he'd later recall, "about how much friction existed in Indian markets simply because buyers and sellers couldn't find each other efficiently."

In 1990, Bikhchandani makes his first entrepreneurial move—not a startup, but joining lintas (then McCann Erickson) as an account executive. For someone with an IIM pedigree, this was unusual. But he wanted to understand brands, marketing, how businesses communicate value. He lasted eighteen months. The corporate hierarchy suffocated him. "I realized I was unemployable," he'd joke years later. But those eighteen months taught him something crucial: Indian businesses were desperate for better ways to reach customers.

So in October 1989, with ₹40,000 in savings, Bikhchandani quits to start Info Edge—though it wouldn't be formally incorporated until 1995. The business model? Devastatingly simple: salary surveys on floppy disks. He'd collect compensation data from companies, compile it into reports, and sell these reports back to HR departments for ₹5,000 each. Not exactly Silicon Valley material, but it worked. First-year revenue: ₹250,000.

The real insight came from client conversations. HR managers kept asking the same question: "Do you know anyone good for this role?" They were spending fortunes on newspaper classifieds—a full-page Times of India recruitment ad cost ₹8 lakhs—with terrible ROI. Response tracking meant manually sorting through hundreds of physical letters. The process took weeks. Meanwhile, job seekers bought five newspapers every Sunday, circling ads with red pens, mailing resumes they'd photocopied at corner shops.

By 1993, Info Edge had pivoted to trademark databases—selling lists of registered trademarks to law firms checking for conflicts. Revenue hit ₹15 lakhs. They hired their first employee. Bikhchandani's co-founder Hitesh Oberoi, an IIT Delhi grad who'd worked at Wipro, joined around this time. Where Bikhchandani was the visionary, Oberoi was the operator—quiet, methodical, obsessed with unit economics even when they barely had units to count.

The business was profitable but uninspiring. They were running a data company in a country where data lived in dusty government registers. Then, in 1996, everything changed. Bikhchandani attended a trade fair where someone showed him this thing called the World Wide Web. Netscape Navigator loading Yahoo's homepage at 14.4 kbps. "It was like seeing electricity for the first time," he'd later say. "I immediately knew—this would change everything about information businesses."

But here's what separates founders from dreamers: Bikhchandani didn't immediately pivot to the internet. India had maybe 50,000 PCs with modems. VSNL, the monopoly ISP, charged ₹15,000 just for an internet connection. He needed to wait. So Info Edge kept selling databases while secretly building what would become Naukri.com. They hired web developers (all three of them available in Delhi), bought servers they couldn't really afford, and started digitizing job listings.

The context here is crucial. This is 1996 India—a country where getting a phone line takes two years and a bribe. Economic liberalization is only five years old. The IT services boom that would make India synonymous with technology hasn't started. Y2K is still a gleam in the enterprise software world's eye. Most Indians haven't even heard the word "internet."

Yet Bikhchandani saw what others missed: India's demographic dividend meant millions entering the workforce annually. The IT sector was nascent but growing 50% yearly. Urbanization was accelerating. Traditional classifieds were broken—expensive for employers, inefficient for job seekers. Someone would eventually fix this with technology. The question was who, and more importantly, when.

"We weren't building for the market that existed," Oberoi would later explain. "We were building for the market we believed would exist." This wasn't Silicon Valley-style "building the future" rhetoric. This was a calculated bet that India's infrastructure would eventually catch up to their product. They were essentially building a rocket ship while waiting for someone to invent rocket fuel.

By March 1997, they were ready. Info Edge had ₹17 lakhs in the bank—their entire accumulated profit from eight years of selling databases. They were about to bet everything on a website in a country where 99.99% of the population had never seen one. As we'd learn in the next chapter, this insane timing would prove to be exactly right.

III. Naukri.com: First Mover in a Market That Didn't Exist (1997–2003)

On March 29, 1997, Naukri.com went live with 1,000 job listings. The total internet population of India: 14,000 users. Let that sink in—they launched a job portal when their entire addressable market could fit in a large movie theater. The press release, sent to newspapers via fax, had to explain what a "website" was. One journalist asked Bikhchandani if people needed to buy special televisions to access it.

The early days were absurdist theater. Bikhchandani would cold-call HR managers, offering to list jobs for free. "What's a website?" they'd ask. He'd offer to come to their office with a laptop and dial-up modem for a demo. Half the time, the connection wouldn't work. When it did, pages took three minutes to load. One HR head at a major IT firm listened patiently, then asked, "But how do candidates mail their resumes to the website?"

Yet something extraordinary was happening. Those 14,000 internet users? Many were IT professionals, exactly who recruiters wanted. Early adopters started getting responses—not hundreds of mismatched postal applications, but targeted emails from qualified candidates. Word spread through HR circles: "There's this website thing that actually works."

The business model evolved through pure experimentation. Initially, they charged ₹350 per listing, payable by check sent via post. Then they noticed something: recruiters wanted to search resumes, not just post jobs. So they built a resume database—free for job seekers, ₹6,000 for three-month recruiter access. This flip—from job board to resume database—would become their moat.

Then came the tsunami: the dot-com boom. By 1999, venture capital discovered India. JobsAhead raised $22 million. Monsterindia launched with $10 million. Jobstreet entered with Singapore money. By 2000, Naukri faced 40+ funded competitors. The market went insane. Competitors bought TV ads during cricket matches. JobsAhead sponsored entire newspaper supplements. One rival spent ₹3 crores on a single marketing campaign.

Naukri's war chest? ₹7 lakhs.

"We watched competitors burn money on Times Square billboards while we were negotiating payment terms with our web hosting provider," Oberoi recalls. The pressure was immense. VCs approached them constantly—take $10 million, grow faster, spend on marketing. Bikhchandani said no. "If we take VC money and fail, we're dead. If we bootstrap and survive, we win everything."

Their survival tactics were ingenious. While competitors advertised to consumers, Naukri focused on recruiters—the ones who actually paid. They pioneered "cybercafé marketing," putting Naukri posters in the 50,000 cybercafés where Indians accessed the internet. Cost: ₹500 per café versus ₹50,000 for a newspaper ad. They created "Naukri Job Fairs"—physical events that drove online registrations. Old economy meets new.

The dot-com crash of 2001 was brutal and swift. JobsAhead, despite raising $22 million, shut down in eighteen months. Monsterindia scaled back drastically. Of the 40+ competitors, only three survived. Why did Naukri endure? They'd built defensibility through frugality. While competitors had 400-person teams, Naukri had 40. While others paid ₹2 lakhs for Oracle databases, Naukri used open-source MySQL. Their burn rate was ₹15 lakhs monthly; competitors burned that in three days.

But the real strategic masterstroke was the resume database. By 2002, Naukri had 1 million resumes—more than all competitors combined. This created a beautiful flywheel: job seekers came because recruiters posted jobs, recruiters came because job seekers posted resumes. Classic network effects, built painstakingly while others chased vanity metrics.

The turning point came with India's IT/ITES boom. Companies like Infosys, Wipro, and TCS were hiring thousands monthly. Call centers needed 100,000 agents yearly. Suddenly, recruitment wasn't episodic—it was continuous. Paper classifieds couldn't handle this volume. Naukri could. Revenue jumped from ₹5 crores in 2001 to ₹20 crores in 2003.

They also cracked enterprise sales before anyone else. While competitors sold to HR managers, Naukri sold to CEOs. They created "Resdex"—a premium resume database product priced at ₹5 lakhs annually. They introduced employer branding solutions—company microsites within Naukri. They weren't just digitizing classifieds; they were reimagining recruitment.

The metrics tell the story: By 2003, Naukri had 3 million registered users, 8,000 paying clients, and 60% market share. More importantly, they had 65% gross margins and were solidly profitable. They'd survived the nuclear winter with no external funding while VC-backed competitors with combined funding of $100 million had perished.

"Everyone thought the funded companies would win because they had resources," Bikhchandani reflected. "But in a market that doesn't exist yet, patient capital beats impatient capital every time. We could afford to wait for India to get online. They couldn't afford to wait for their VCs to see returns."

So what for investors? The Naukri story reveals a crucial insight: in emerging markets, being too early with too much money is often worse than being exactly on time with just enough. The company that can survive until product-market fit emerges often takes everything. This pattern would repeat across Info Edge's other ventures.

IV. The IPO & Becoming a Platform Company (2004–2010)

October 20, 2006, 9:15 AM, National Stock Exchange. The opening bell rings for Info Edge's IPO—India's first pure internet company to go public. Listed at ₹320, the stock opens at ₹580, touching ₹735 within minutes. Retail investors, who'd never bought tech stocks, are calling brokers frantically. The financial press goes berserk: "Indian Internet Comes of Age!" By day's end, Bikhchandani's 27% stake is worth ₹400 crores. Not bad for a company that started with ₹40,000.

But the real story isn't the price pop—it's what happened in the boardroom six months earlier. The investment bankers pitched a standard tech IPO: raise ₹150 crores, use it for "growth capital." Bikhchandani pushed back: "We don't need money. We're generating cash." The bankers were confused. Every tech company needs growth capital, right? Wrong. Info Edge raised just ₹52 crores, mostly secondary sales for early angels. They went public not for capital but for currency—stock that could acquire, motivate, and signal permanence to enterprise clients.

With public market validation, Info Edge unleashed its platform strategy. The insight was elegant: classifieds aren't a vertical, they're a horizontal. The same network effects that worked in jobs could work in real estate, matrimony, education. But—and this was crucial—each vertical needed native DNA. You couldn't just clone Naukri's code and expect it to work for property listings.

99acres launched in 2005, right as India's real estate boom went supernova. But instead of competing with established players like MagicBricks on marketing spend, they did something counterintuitive: they went after builders first, not buyers. "Everyone was chasing eyeballs," explains Oberoi. "We chased inventory." They signed exclusive listing agreements with developers, offering free project marketing tools. By the time competitors noticed, 99acres had 70% of new project listings in NCR.

The matrimony bet with Jeevansathi was riskier. Shaadi.com dominated with 70% market share. Info Edge's strategy? Don't fight for the mass market; own specific segments. They focused on North India, UI/UX for mobile (in 2007!), and authenticity—verified profiles when everyone else allowed anonymous browsing. Revenue grew from ₹2 crores in 2006 to ₹25 crores by 2010. Not market-leading, but highly profitable.

Shiksha, the education vertical, took a different approach entirely. Instead of competing with coaching center ads, they built India's first college comparison platform. Engineering aspirants could compare IITs vs NITs vs private colleges on parameters like placement stats, fees, and faculty ratios. This wasn't a classifieds business—it was a decision-support system monetized through lead generation. By 2010, 2 million students used Shiksha annually for college selection.

But the real battles were in defending Naukri's castle. Monster.com acquired JobStreet for $50 million to enter India. LinkedIn launched in India in 2009. Google tested job search ads. The threats were existential—global platforms with unlimited capital targeting Naukri's crown jewel.

The Monster battle was particularly fierce. They hired Naukri's sales directors, offered clients 70% discounts, and spent ₹50 crores on a Bollywood-style ad campaign. Info Edge's response was surgical. They launched "NaukriGulf" for Middle East jobs, knowing Monster was weak internationally. They created "FirstNaukri" for entry-level positions Monster ignored. They built "NaukriRecruiter," a CRM for HR teams. Instead of defending the core, they expanded the battlefield.

LinkedIn was scarier because it changed the game's rules. Professional networking versus job listings—a fundamentally different model. Bikhchandani's team studied LinkedIn obsessively, concluding it would own the top 10% of the market—senior professionals, passive candidates. So Naukri deliberately moved down-market, focusing on 0-8 years experience, active job seekers, and volume hiring. They turned LinkedIn's strength into a positioning advantage: "LinkedIn for networking, Naukri for hiring."

The financials during this period were extraordinary. Revenue grew from ₹49 crores in 2004 to ₹295 crores in 2010—a 35% CAGR. But here's the kicker: EBITDA margins expanded from 25% to 42%. As the platforms scaled, costs barely grew. The beauty of classifieds was revealing itself: near-zero marginal costs, network effects creating pricing power, and subscription revenue providing predictability.

They also pioneered the "freemium for recruiters" model. Basic job posting: free. Resume database access: paid. Branded company pages: premium. This wasn't just pricing strategy—it was ecosystem building. Free users became paying customers as hiring needs grew. The conversion funnel was patient, sometimes taking years, but inexorable.

The capital allocation during this period deserves special attention. Despite sitting on ₹200+ crores post-IPO, they spent cautiously. Marketing stayed under 15% of revenue. They avoided splashy acquisitions. The only major deal: acquiring Quadrangle, a small executive search firm, for ₹12 crores—not for the business but for insights into high-end recruiting. This discipline would soon enable their next act: becoming venture capitalists.

So what for investors? Info Edge proved that platform economics work differently in emerging markets. You can't just transplant Silicon Valley playbooks. You need to build multiple verticals simultaneously for diversification, defend through product expansion not marketing wars, and maintain margin discipline even with public market capital. The IPO wasn't an exit—it was ammunition for empire building.

V. The Venture Capital Masterstroke (2010–Present)

The meeting was in a Costa Coffee in Gurgaon, 2010. Deepinder Goyal, a 27-year-old Bain consultant, was pitching his restaurant menu website to Sanjeev Bikhchandani. Goyal's PowerPoint had twelve slides. Bikhchandani interrupted at slide three: "How much do you need?" "Sir, ₹35 lakhs." "Done. But I want 25% of the company." That handshake would eventually be worth ₹15,000 crores.

This wasn't Info Edge's first venture bet—they'd dabbled since 2007—but it marked a strategic shift. Bikhchandani realized something profound: Info Edge generated ₹50+ crores of free cash flow annually with nowhere to deploy it. Traditional expansion was capital-light. M&A in classifieds made no sense—you already had network effects. But investing in adjacent internet businesses? That was leveraging their greatest asset: understanding Indian consumer internet before anyone else.

The investment thesis was contrarian. In 2010, Indian VC was dominated by Silicon Valley funds chasing Silicon Valley models. Info Edge looked for something different: capital-efficient businesses solving uniquely Indian problems. They weren't trying to be Sequoia or Tiger Global. They were building a strategic portfolio that could eventually integrate with their core platforms.

Take Policybazaar. When Yashish Dahiya pitched in 2008, every VC had passed. "Insurance aggregation in India? The market isn't ready." Info Edge saw differently. Indians bought insurance exactly like they searched for jobs—information asymmetry, trust deficit, complex decision-making. Info Edge invested ₹4 crores for 15%. That stake is worth ₹2,000+ crores today.

The Zomato story deserves its own book. Info Edge invested four times between 2010-2015, totaling ₹260 crores for a 26% stake. When Zomato was burning cash competing with Swiggy, when SoftBank was circling with term sheets, Bikhchandani gave one piece of advice: "Don't dilute unnecessarily. This is a marathon." During Zomato's IPO in 2021, Info Edge's stake was worth ₹13,000 crores—a 50x return.

But here's what's fascinating: they also had spectacular failures. Meritnation (online education) shut down. Happily Unmarried (quirky gifts) never scaled. Mydala (local deals) got crushed by Groupon. The difference? Info Edge never chased losses. Average investment: ₹5-10 crores. If it didn't work in two years, they stopped. No ego, no sunk cost fallacy.

The portfolio construction was deliberate. They identified six themes: financial services (Policybazaar, Paisabazaar), food-tech (Zomato), real estate tech (NoBroker, Proptiger), education (Meritnation, Univariety), matrimony/dating (Jeevansathi stake increase), and horizontal platforms (Shopkirana, Gramophone). Each investment had to pass three filters: large addressable market, network effects potential, and founders who understood unit economics.

The hands-on value addition separated them from passive investors. When Zomato wanted to expand internationally, Info Edge opened doors in the Middle East through NaukriGulf connections. When Policybazaar needed insurance partnerships, Info Edge leveraged its enterprise relationships. They didn't just write checks—they opened networks, shared playbooks, and most importantly, counseled patience during growth-at-all-costs hysteria.

By 2015, the strategy evolved again. They created Info Edge Ventures, a ₹750 crore fund for larger checks. They hired professional investors. They started co-investing with global funds. The approach became more institutional but retained its DNA: back businesses that create value through information transparency, focus on India-first models, and never pay Silicon Valley valuations for Delhi startups.

The recent liquidity events have been staggering. Zomato's IPO in 2021: ₹13,000 crores value. Policybazaar's IPO: ₹2,000 crores. Even partial stakes sales generated ₹3,000+ crores in cash. The irony is delicious: Info Edge's investment portfolio is worth more than its market cap. The stock market values their operating business at negative value, essentially.

But Bikhchandani doesn't see it as arbitrage to exploit. In a recent interview, he explained: "We're not a venture fund that happens to run classifieds. We're a classifieds company that happens to invest. The investments make us better operators. Seeing Zomato's user acquisition taught us mobile strategy. Watching Policybazaar's content marketing improved our SEO. It's symbiotic."

The current portfolio spans 50+ companies. Some will fail—that's the game. But with Zomato and Policybazaar already returning 100x+ on invested capital, they're playing with house money. The strategy now is selective concentration: double down on winners, exit laggards, and wait for the next Zomato to walk into a coffee shop.

So what for investors? Info Edge has created a unique model: an operating company that funds its venture portfolio from cash flows, not LP capital. This means no J-curve, no management fees, no forced exits. They can hold Zomato stock forever if they want. It's patient capital in its purest form—and in emerging markets, patience is the ultimate competitive advantage.

VI. Competitive Dynamics & Market Evolution

LinkedIn India's office, Bangalore, 2014. The country head is presenting to global leadership via video conference. "We're not gaining share in India like other markets. There's this local player, Naukri..." Jeff Weiner interrupts: "How can a local job board compete with LinkedIn's network?" The country head sighs: "That's the thing—they're not competing. They're playing a completely different game."

This anecdote, shared by a former LinkedIn executive, captures Info Edge's defensive genius. When global giants invaded, they didn't fight strength against strength. They redefined the battlefield. LinkedIn wanted professional networking? Fine, Naukri would own transactional hiring. Indeed aggregated listings? Perfect, Naukri would go deeper on resume data. Monster brought brand power? Excellent, Naukri would build recruiter tools.

The LinkedIn defense is particularly instructive. By 2014, LinkedIn had 30 million Indian users—more than any country outside the US. Bulls predicted Naukri's demise: "Why would anyone use a job board when professional networks exist?" But Bikhchandani's team had done their homework. LinkedIn's India revenue was 90% recruitment solutions, barely any consumer subscriptions. Indians used LinkedIn for professional vanity, not job searching.

So Naukri executed a brilliant flanking maneuver. They launched "Naukri Recruiter"—a CRM specifically for Indian hiring managers. Features that sounds basic but were revolutionary: bulk resume downloads (LinkedIn limited downloads), Excel exports (Indian HR loves spreadsheets), and integration with Indian ATS systems. They also created "Naukri RMS"—a recruitment management system priced at ₹2 lakhs versus Oracle's ₹50 lakhs. By 2016, 3,000+ companies used Naukri's HR tech stack, creating switching costs LinkedIn couldn't overcome.

Indeed's entry in 2012 was scarier because they attacked Naukri's core—job search. Indeed's aggregation model was devastating globally: scrape every job from every site, become the Google of jobs. Their traffic exploded: 5 million monthly users within a year. Naukri's response was counterintuitive—they reduced their job listings.

"Indeed had millions of jobs, but 80% were duplicates or expired," explains a former Naukri product head. "We focused on quality—verified listings, direct from employers." They introduced "Naukri Certified," where every job was phone-verified. They created "Application Tracking," showing candidates their application status. Indeed had quantity; Naukri delivered quality. By 2018, Indeed's India traffic plateaued while Naukri's paid subscriptions grew 20% annually.

The 99acres battles were bloodier. PropTiger raised $55 million. Housing.com burned through $100 million in spectacular fashion. MagicBricks had Times Group's media muscle. CommonFloor got acquired by Quikr. The real estate classifieds space became a capital destruction machine—everyone chasing the Zillow dream in a market where 70% of transactions happened in cash without documentation.

99acres survived through strategic patience. While competitors fought for buyer traffic, 99acres locked up supply—exclusive mandates with builders in exchange for project marketing support. While Housing.com built VR tools, 99acres created "Builder Dashboard"—analytics for developers on lead quality. While MagicBricks advertised on television, 99acres invested in data—price trends, locality reviews, project comparisons. By 2020, when the dust settled, only three players remained: 99acres, MagicBricks, and NoBroker (where Info Edge was an investor).

The matrimony market evolution was different—less about defeating competitors, more about market expansion. Shaadi.com remained dominant, but the pie grew dramatically. Dating apps like Tinder and Bumble expanded the relationship market. Jeevansathi found its niche: North Indian, tier-2 cities, family-involved matchmaking. They didn't need to beat Shaadi.com—they needed to own their segment profitably. Revenue grew from ₹50 crores in 2015 to ₹140 crores in 2022, with 40%+ EBITDA margins.

Shiksha faced the edtech boom differently than expected. While Byju's and Unacademy raised billions for K-12 coaching, Shiksha stayed focused on college selection. When edtech crashed in 2022, Shiksha was unaffected—they never competed on teaching, only on information organization. Their moat wasn't content but architecture—how to structure complex education decisions.

The new generation of competitors is more sophisticated. Instahyre uses AI for candidate-job matching. Cutshort focuses on tech hiring with GitHub integration. AngelList brings Silicon Valley's hiring practices to India. Apna targets blue-collar workers with vernacular interfaces. Each nibbles at Naukri's edges without threatening the core.

Info Edge's response has been measured. They launched "Naukri Gulf" for international jobs, "Firstnaukri" for freshers, "Naukri Learning" for upskilling. But they avoid the temptation to fight every battle. "Let them take 5% of the market," Bikhchandani says. "We'll keep the profitable 70%."

So what for investors? Info Edge's competitive strategy reveals a crucial insight: in winner-take-most markets, you don't need to win everything. Define your battlefield narrowly, build switching costs aggressively, and let competitors burn capital chasing your exhaust fumes. The goal isn't monopoly—it's sustainable competitive advantage in your chosen domain.

VII. The Business Model & Unit Economics Deep Dive

Pull up Info Edge's latest investor presentation and you'll find a slide that makes SaaS founders weep with envy: 72% EBITDA margins in the recruitment business. Not gross margins—EBITDA. For context, Workday, the $60 billion HR software giant, manages 20%. How does a company in India, with 4,000+ employees and physical offices, generate software-like margins? The answer lies in understanding the peculiar economics of classifieds—perhaps the most beautiful business model ever invented.

Let's dissect Naukri's revenue streams. The base layer: job postings at ₹500-5,000 per listing. Sounds simple, but there's complexity underneath. Hot jobs (IT, sales) are dynamically priced higher. Urgent requirements get premium placement. Bulk packages create predictability—companies buy 100-listing packs annually. This generates ₹400 crores yearly, but it's actually the least interesting revenue stream.

The real money comes from resume database access—Resdex. Pricing: ₹50,000 to ₹5 lakhs annually, depending on search queries and downloads. The beauty? Zero marginal cost. Whether a recruiter downloads 10 or 10,000 resumes, Info Edge's cost doesn't change. The database has 75 million resumes, growing by 15,000 daily, all user-generated. It's the ultimate user-generated content business—candidates do the work, recruiters pay for access.

Then there's employer branding—company pages, video profiles, culture showcases. Price: ₹10-50 lakhs annually for large enterprises. Infosys spends ₹2 crores yearly on their Naukri presence. Again, near-zero marginal cost. Once the template is built, incremental clients just need customization. This generates ₹200+ crores with 85% gross margins.

The newest stream: recruitment solutions. Application tracking systems, candidate assessment tools, video interview platforms. This is software, pure and simple. ₹2-20 lakhs annually, 3-year contracts, 90% renewal rates. It's nascent—just ₹100 crores revenue—but growing 40% yearly with SaaS-like unit economics.

Now, let's talk about the cost structure—or rather, the lack thereof. Customer acquisition cost? Essentially zero. Naukri has 76% organic traffic—people type "naukri.com" directly or search "jobs" on Google. Marketing spend is just 8% of revenue, mostly brand advertising, not performance marketing. Compare that to US job sites spending 30-40% on Google ads.

The operational leverage is staggering. From 2015 to 2022, revenue grew from ₹650 crores to ₹1,600 crores. Employee count grew from 3,000 to 4,000. Revenue per employee jumped from ₹22 lakhs to ₹40 lakhs. The platform scales infinitely—adding the millionth recruiter costs the same as adding the tenth.

But here's the real secret: pricing power. Naukri raises prices 10-15% annually. No client has ever churned because of price increases. Why? Switching costs. Moving to another platform means retraining recruiters, migrating data, rebuilding employer brand. For a service that costs ₹5 lakhs but helps hire 100 people yearly, each worth ₹10 lakhs in salary, the ROI is obvious.

The capital allocation framework is disciplined. Of every ₹100 in revenue, ₹72 becomes EBITDA. Of that ₹72, roughly ₹20 goes to taxes, ₹15 to dividends, ₹15 to venture investments, and ₹22 to cash accumulation. They've never done buybacks, never taken debt, never made a large acquisition. It's boring and brilliant.

99acres and Jeevansathi follow similar models but with nuances. 99acres monetizes via listing fees (₹500-5,000), developer subscriptions (₹5-50 lakhs), and lead generation (₹100-500 per lead). Margins are lower—around 35%—because real estate requires more feet-on-street sales. Jeevansathi charges consumers directly—₹4,000-15,000 for 3-month memberships. Higher customer acquisition costs but also higher lifetime values.

The international expansion attempts were revealing failures. NaukriGulf launched in 2006 for Middle East markets. Despite 1 million registered users, it never became profitable. Why? Classifieds require local network effects. You can't export them like software. They shut it down in 2020, taking a ₹50 crore write-off—painful but instructive.

The unit economics create a powerful flywheel. High margins generate cash. Cash funds venture investments or dividends. Venture investments provide strategic insights and financial returns. Dividends keep shareholders happy without dilution. The business essentially funds its own growth and diversification.

So what for investors? Info Edge proves that in the right market structure, traditional businesses can generate tech-like economics. The key is owning demand aggregation in markets with high fragmentation, information asymmetry, and frequency of transaction. Once you build the network, the economics are magical—pricing power, zero marginal costs, and operational leverage that would make a software CEO jealous.

VIII. Modern Era: AI, Mobile & The Next Act

The WhatsApp message arrived at 11 PM on a Sunday in March 2023. A 22-year-old ITI graduate in Lucknow had just received his first job offer—assembly line technician at a Noida electronics factory, ₹18,000 monthly. He'd never used Naukri.com's website. Instead, he'd sent his resume via WhatsApp to a number he'd found on a poster at his local mobile repair shop. An AI chatbot had parsed his Hindi-English hybrid messages, matched his skills to open positions, and scheduled a video interview. The entire process took three days. This is Info Edge's next battlefield: India's 300 million blue-collar workers who've never written a traditional resume.

The mobile transition nearly killed them. In 2015, Naukri's mobile app had a 2.3-star rating. The UI was essentially their desktop site crammed into a phone screen. Meanwhile, new players like Apna built mobile-first experiences with vertical video resumes and WhatsApp integration. Info Edge's response was humble and radical: they rebuilt everything from scratch.

"We had to unlearn twenty years of web design," admits their head of product. They studied TikTok for engagement patterns. They analyzed WhatsApp for communication flows. They watched users at railway stations struggling with English interfaces. The new Naukri app, launched in 2018, wasn't just mobile-optimized—it was mobile-native. Voice-based job search in Hindi. One-tap apply with pre-filled forms. Video resumes recorded directly in-app. By 2022, 75% of Naukri's traffic was mobile, and the app rating had climbed to 4.4 stars.

The AI integration started defensively. In 2016, Google launched "Jobs on Search" in the US, using natural language processing to understand intent better than keyword matching. The fear in Info Edge's boardroom was palpable: "What if Google can match candidates better than us?" They assembled a 50-person AI team, hiring from IITs and poaching from Amazon. The mandate: build matching algorithms that understand Indian hiring nuances.

The results have been mixed but promising. Their AI can now predict with 73% accuracy which candidates will respond to which jobs. It understands that "familiar with Excel" in India means different things for different roles. It recognizes that a gap year might indicate competitive exam preparation, not unemployment. But here's the challenge: Indian recruiters don't trust pure algorithmic matching. They want AI-assisted human judgment, not replacement.

So Info Edge built hybrid products. "Naukri Maestro" uses AI to shortlist candidates but lets recruiters make final decisions. "Smart Apply" helps candidates identify jobs where they have the highest chance of success. "Resume Quality Score" uses NLP to suggest improvements. It's AI as a feature, not the product—augmentation, not automation.

The gig economy explosion forced another pivot. Suddenly, millions of Indians weren't looking for jobs—they were looking for projects. Delivery partners, content creators, consultants. Naukri's traditional model—permanent positions, formal employment—seemed antiquated. Their response was "Naukri Gig," launched in 2021, but it's struggled to gain traction. The gig economy wants instant matching and daily payments. Naukri's strength—deep vetting and quality—becomes a liability in the gig world.

The video revolution is more promising. "Naukri Video Profiles" lets candidates record 60-second introductions. For sales and customer service roles, video applications now account for 30% of submissions. But again, India-specific challenges emerge. Candidates worry about bias based on appearance. Recruiters complain about bandwidth for streaming. The solution: AI-generated transcript summaries with optional video viewing.

The assessment integration has been particularly clever. Instead of building testing tools, Info Edge partnered with or invested in assessment platforms. When a recruiter posts a job, they can add skill tests from partners like Mettl or Interview Mocha. Candidates take tests, results flow back to Naukri. Info Edge takes a 20% revenue share without building anything. It's platform thinking at its best.

The remote work transformation post-COVID created unexpected opportunities. "Naukri Remote" aggregates work-from-home positions—3 million listings by 2023. But more interestingly, it's broken geographic barriers. A developer in Bhubaneswar can now work for a Bangalore startup. A content writer in Guwahati can join a Mumbai agency. Naukri's data shows remote job applications have 5x better geographic diversity than traditional roles.

The blue-collar expansion is the biggest bet. "Naukri JobSpeak" targets the 300 million Indians who work in manufacturing, logistics, and services. The interface is voice-first, works on ₹2,000 smartphones, and uses minimal data. Jobs are explained via video, not text. Applications happen through missed calls and WhatsApp. It's early—just 2 million users—but growing 100% yearly.

The holding company structure has evolved to manage this complexity. Info Edge (India) Ltd remains the listed entity. Below it, separate subsidiaries run each vertical—Naukri Internet Services, Allcheckdeals (99acres), Jeevansathi Internet Services. The venture portfolio sits in another subsidiary. This allows focused execution while maintaining strategic coordination.

So what for investors? Info Edge's modern transformation reveals both opportunity and risk. They're successfully adapting to mobile and AI, but the pace of change is accelerating. New models—gig platforms, creator economies, Web3 credentials—threaten traditional classifieds. Their response has been measured: experiment at the edges while protecting the core. Whether that's fast enough remains the key question.

IX. Playbook: Business & Investing Lessons

In 2019, a Stanford MBA student asked Sanjeev Bikhchandani during a campus visit: "What's your strategy framework?" Bikhchandani smiled: "We don't have frameworks. We have patterns." That exchange captures Info Edge's playbook—not rigid rules but repeated patterns that work in emerging markets. Let's decode them.

Pattern 1: Build Before the Market Exists When Naukri launched, India had 14,000 internet users. When 99acres started, online real estate search was nonexistent. This wasn't visionary thinking—it was calculated patience. Bikhchandani calls it "building the road while waiting for cars." You create supply-side density before demand explodes. By the time the market arrives, you have insurmountable lead. This requires two things most entrepreneurs lack: capital efficiency to survive the wait, and conviction that the market will eventually come.

Pattern 2: Own the Atomic Unit Every Info Edge business controls something atomic and defensible. For Naukri, it's the resume—75 million and growing. For 99acres, it's verified listings from builders. For Jeevansathi, it's detailed matrimony profiles. Competitors can copy features, slash prices, or outspend on marketing. But they can't replicate years of accumulated atomic units. As Oberoi explains: "Features are temporary. Data is permanent."

Pattern 3: Monetize the Professional Side Consumers use Info Edge products for free. Professionals pay. This isn't freemium—it's ecosystem design. Job seekers don't pay Naukri; recruiters do. Home buyers don't pay 99acres; builders do. This creates beautiful incentive alignment. The free side provides data and liquidity. The paid side gets efficiency and access. The platform sits in between, extracting value from reduced transaction costs.

Pattern 4: Compete on Depth, Not Breadth When LinkedIn entered India, Naukri didn't try to build professional networking. When Indeed aggregated jobs, Naukri didn't aggregate. Instead, they went deeper on their core. More detailed resumes. Better recruiter tools. Stronger employer branding. This is counterintuitive in the age of platform expansion, but it works. Depth creates switching costs. Breadth creates vulnerability.

Pattern 5: Capital Efficiency as Strategy Info Edge spent ₹17 lakhs launching Naukri. JobsAhead spent ₹17 crores and died. This isn't about being cheap—it's about understanding that in emerging markets, patience beats pace. Low burn rates allow you to survive multiple cycles. High burn rates force premature scaling. As Bikhchandani says: "Our competitors had timeline pressure. We had none."

Pattern 6: Venture Investing as R&D Info Edge's venture portfolio isn't just financial diversification—it's market intelligence. Investing in Zomato taught them mobile user acquisition. Backing Policybazaar revealed trust-building in complex categories. Even failures provide lessons. Meritnation's shutdown showed why edtech needs offline components. Each investment is a ₹5-10 crore experiment in future business models.

Pattern 7: Ignore Silicon Valley Playbooks Every few years, a new Silicon Valley wisdom arrives in India. Blitzscale! Winner takes all! Growth before profits! Info Edge ignores them all. They've never prioritized growth over margins. Never raised venture capital. Never made a transformative acquisition. This isn't stubbornness—it's pattern recognition that emerging markets have different physics than developed ones.

Pattern 8: Time Diversification Info Edge operates on multiple time horizons simultaneously. Naukri optimizes for next quarter's revenue. 99acres builds for the next 3-year real estate cycle. Venture investments target 7-10 year exits. This temporal diversification provides resilience. Short-term cash funds long-term bets. Long-term winners subsidize short-term experiments.

Pattern 9: The Boring Moat Info Edge's defensibility isn't sexy. No network effects as powerful as Facebook. No switching costs as strong as Salesforce. No economies of scale like Amazon. Instead, they have accumulation advantages—millions of resumes, listings, and profiles collected over decades. It's boring, but it works. Competitors can't go back in time to start collecting.

Pattern 10: Profit as Oxygen While Silicon Valley celebrates companies that lose money for decades, Info Edge has been profitable for 25 years. Profits aren't just financial metrics—they're oxygen for independence. Profits mean no venture capital dilution. No pressure for premature exits. No desperate pivots. The ability to say no. In emerging markets, this independence is invaluable.

These patterns reveal a deeper philosophy: Info Edge builds businesses like they're cultivating forests, not launching rockets. Slow initial growth, deep root systems, eventual dominance through persistence. It's unglamorous but effective.

The lessons for emerging market entrepreneurs are clear. Don't import developed market strategies wholesale. Build for the market that will exist, not the one that does. Choose depth over breadth. Prioritize sustainability over growth rates. Use profits to buy patience.

So what for investors? The Info Edge playbook suggests that in emerging markets, the highest returns don't come from the fastest growers but from the longest survivors. Patient capital, boring moats, and profit discipline might not generate headlines, but they generate alpha.

X. Analysis & Bear vs. Bull Case

Let's play devil's advocate. You're a hedge fund analyst in 2024, staring at Info Edge's stock chart. The bull case seems obvious: dominant market position, venture portfolio worth more than market cap, India's demographic dividend. But you've seen this movie before—legacy leaders disrupted by nimble startups. Time to stress-test both narratives.

The Bull Case: Compounding Machine

Start with the macro. India adds 12 million people to its workforce annually through 2035. The formal job market is just 100 million today, expected to reach 250 million by 2030. Every percentage point of formalization equals millions of new Naukri users. The recruitment solutions market, currently ₹3,000 crores, could reach ₹15,000 crores as hiring becomes continuous rather than episodic.

The competitive position looks impregnable. Naukri has 76% market share in online recruitment after 27 years of competition. Network effects are strengthening, not weakening—more resumes attract more recruiters, attracting more job seekers. The resume database has crossed critical mass where it becomes the system of record for Indian employment. Switching costs for enterprises are prohibitive: recruiting teams trained on Naukri, ATS integrations, and historical data locked in.

The venture portfolio provides massive optionality. Current holdings worth ₹15,000+ crores against a market cap of ₹8,000 crores. Even marking down the portfolio by 50% leaves substantial value. But the real option value is in the next Zomato—they're investing ₹200 crores annually in new startups. Hit rate only needs to be 1 in 50 for massive returns.

Management quality remains exceptional. Bikhchandani owns 27%, Oberoi owns 5%—real skin in the game. They've navigated multiple technology transitions, defeated global competitors, and maintained margins while growing. Capital allocation has been exemplary: dividends for stability, venture investments for growth, zero destructive acquisitions.

The margin structure suggests earnings can compound faster than revenue. Current EBITDA margins of 35% could expand to 45% as revenue grows but costs stay flat. The incremental margin on new revenue is 70%+. Operating leverage means every 10% revenue growth drives 15% profit growth.

The Bear Case: Disruption Incoming

But wait. LinkedIn now has 100 million Indian users, growing 30% yearly. They're moving down-market with LinkedIn Lite for emerging markets. Microsoft's backing means unlimited resources. What if they decide to subsidize Indian operations to gain share? Naukri's moat looks less impressive against a trillion-dollar parent.

AI disruption could be devastating. ChatGPT can write resumes better than most candidates. AI matching could make resume databases obsolete—why search through millions when an algorithm perfectly matches in seconds? Startups like Turing and Andela are using AI to completely reimagine recruiting. Info Edge's AI efforts feel incremental, not transformational.

The venture portfolio concentration is concerning. 70% of portfolio value is in just two stocks: Zomato and Policybazaar. Both are losing money, trading at expensive multiples, in highly competitive markets. If these stocks correct 70%—not impossible in a bear market—Info Edge's NAV drops by ₹8,000 crores. The diversification is illusory.

Growth is decelerating. Naukri's revenue grew just 12% last year, down from 20%+ historically. 99acres is losing share to NoBroker and MagicBricks. Jeevansathi remains subscale. Shiksha faces the edtech winter. Where's the next growth driver? Blue-collar recruitment is promising but requires different capabilities—vernacular content, offline presence, micro-transactions.

The platform risk is real but hidden. 60% of Naukri's traffic comes from Google. What if Google decides to prioritize its own job search? They've already done it in the US. Or what if WhatsApp launches job search in India? Platform dependence is an existential risk nobody's pricing in.

Management succession is unclear. Bikhchandani is 61, Oberoi is 54. Who's next? The bench strength isn't obvious. Family members aren't involved. Professional managers might not have the same long-term orientation. Founder-led companies often struggle with transitions.

The Valuation Arbitrage

Here's where it gets interesting. Info Edge trades at ₹8,000 crores market cap. Break it down: - Venture portfolio: ₹15,000 crores (marked to market) - Cash on books: ₹2,000 crores - Core business value: Negative ₹9,000 crores implied

The market is essentially saying the operating business is worth negative value. That's clearly wrong—Naukri alone generates ₹500 crores in annual EBITDA. At a conservative 15x multiple, that's ₹7,500 crores. Add 99acres, Jeevansathi, and Shiksha, and the operating business is worth ₹10,000+ crores.

So either the market is wrong, or the venture portfolio is overvalued. The truth is probably both. The venture portfolio might be worth ₹10,000 crores, not ₹15,000. The operating business might be worth ₹7,000 crores, not ₹10,000. That still sums to ₹17,000 crores against an ₹8,000 crore market cap—100% upside.

So what for investors? Info Edge presents a classic value-versus-disruption dilemma. The numbers scream buy—trading at half of NAV with growing cash flows. But the technology landscape whispers caution—AI, platform shifts, and new models threaten the core. The resolution likely depends on execution: Can they use their cash and market position to transform before disruption arrives? The jury's still out.

XI. Epilogue & "If We Were CEOs"

Imagine you're handed the keys to Info Edge tomorrow. ₹2,000 crores in cash, market-leading positions, a venture portfolio worth billions. But also: slowing growth, AI threats, and global competitors circling. What's the playbook for the next decade? Let's think through this like operators, not observers.

Priority 1: The Blue-Collar Unlock

India's 300 million blue-collar workers represent the next S-curve, but Naukri's current product doesn't serve them. If we were CEO, we'd build or acquire a vernacular, voice-first platform. Not Naukri-lite, but something fundamentally different. Think WhatsApp meets hiring. Invest ₹500 crores, accept losses for five years, build the next monopoly. The TAM is 10x white-collar recruiting.

Priority 2: AI as the Core, Not Feature

Info Edge treats AI as an enhancement. We'd make it the engine. Create "Naukri Intelligence"—an AI layer that sits across all products. Not just matching, but career coaching, skill prediction, and salary negotiation. Acquire an AI startup for talent—₹200 crores gets you 50 world-class engineers. Build products competitors can't copy because they lack the data.

Priority 3: Unlock the Venture Portfolio

The market doesn't value Info Edge's investments properly because they're buried in a complex structure. We'd create Info Edge Ventures as a separately listed entity, distribute shares to existing shareholders. Suddenly, the value becomes transparent. The operating company focuses on operations. The venture arm becomes India's first listed VC. Both entities would likely trade higher separately.

Priority 4: International Expansion 2.0

Previous international attempts failed because they exported the Indian product. We'd try differently: acquire local leaders in similar markets. Bangladesh, Sri Lanka, Nepal—markets with similar dynamics but earlier in the curve. Use Info Edge's playbook but local execution. Target ₹1,000 crores revenue from international in five years.

Priority 5: The Enterprise Play

Naukri sells to HR departments. We'd sell to CEOs. Build "Info Edge Talent Cloud"—integrated suite covering recruiting (Naukri), assessment (partner products), onboarding (new build), and analytics (AI-powered). Price it at ₹50 lakhs annually for enterprises. Target 1,000 customers in three years. That's ₹500 crores in high-margin SaaS revenue.

Priority 6: Platform Diversification

Google and WhatsApp dependence is dangerous. We'd invest heavily in owned channels. Build India's largest career content platform—interview prep, salary data, company reviews. Create reasons for direct traffic. Launch "Naukri Career App"—not job search but career management. Own the user relationship, not just the transaction.

The Capital Allocation Framework

With ₹2,000 crores in cash and ₹500 crores annual free cash flow, capital allocation becomes crucial. Our framework: - 40% to new initiatives (blue-collar, AI, international) - 30% to venture investments (but more concentrated, bigger bets) - 20% to dividends (keep investors happy) - 10% to strategic M&A (only if transformative)

No buybacks—the stock is undervalued, but organic opportunities are better. No debt—financial flexibility is strategic advantage.

The Cultural Transformation

Info Edge's culture is its strength and weakness—patient, profitable, but perhaps too comfortable. We'd inject urgency without losing discipline. Create internal startups with separate P&Ls and equity incentives. Hire from consumer internet companies, not just IT services. Set up innovation labs in Bangalore, not just Delhi. Balance the wisdom of experience with the energy of youth.

The Risk Management

All these initiatives could fail. So we'd maintain the core fortress. Naukri remains the cash cow—don't experiment there. Keep margins above 30% no matter what. Never bet the company on any single initiative. Think portfolio, not lottery tickets.

Final Reflections on Building in Emerging Markets

Info Edge's story teaches us that in emerging markets, the biggest returns come from seeing the future before it's evenly distributed. Bikhchandani saw the internet's potential when India had 14,000 users. He saw mobile's importance when smartphones were luxury items. He saw AI's impact when it was still science fiction.

But seeing isn't enough—you need to survive until the future arrives. That requires capital efficiency, patient investors, and the courage to look foolish for years. Info Edge looked foolish selling job listings online in 1997. They looked foolish investing in food delivery in 2010. They looked foolish staying profitable while competitors raised billions.

Today, they're worth ₹8,000 crores with investments worth double that. The foolishness paid off. The lesson for emerging market entrepreneurs isn't to copy Info Edge's specific moves but to understand their meta-strategy: build for the inevitable future, survive the uncertain present, and compound the proceeds intelligently.

The next decade will test whether Info Edge can execute this playbook again. Can they navigate AI disruption like they navigated the internet transition? Can they capture blue-collar recruiting like they captured white-collar? Can they unlock venture portfolio value while maintaining operating excellence?

So what for investors? Info Edge at current valuations offers asymmetric upside—heads you win, tails you don't lose much. The venture portfolio provides downside protection. The operating business provides steady cash flows. The optionality on new initiatives provides upside potential. It's not a momentum play or a deep value play—it's a compound play. And in emerging markets, compounders usually win.

XII. Recent News

Based on the latest information available, here are the key recent developments for Info Edge:

Financial Performance Update

Info Edge reported strong Q3 FY2024-25 results with revenue jumping 36.74% year-over-year to ₹909.48 crores. Net profit surged 60.56% to ₹242.59 crores, while net profit margins improved to 26.67%. For the full year 2024, the company generated revenue of ₹27.57 billion, up from ₹24.83 billion in 2023.

AI and Technology Transformation

Info Edge has dramatically accelerated its AI deployment, growing from 60-70 AI models in mid-2021 to over 500 models by mid-2024 across operational businesses. The AI workforce expanded from 15 scientists in mid-2021 to more than 60 by early 2024, supported by dozens of machine learning engineers. The company now operates "one of the premier corporate AI labs in the country" focused on developing advanced models for all four verticals.

New Business Initiatives

Job Hai and AmbitionBox, two newer ventures, started generating revenue in Q4 FY24. The company continues investing in adjacent verticals including iimjobs, Naukri Fast Forward, and DoSelect, which have shown profitable growth.

Strategic Investments

In May 2025, the Board approved an investment of approximately ₹300 crores in Startup Internet Services, a wholly owned subsidiary. Info Edge's long-term startup investments, including Zomato and Policybazaar, have yielded nearly 10x returns with a gross IRR of 36% as of FY25.

Market Position and Competition

Naukri.com maintains its dominance with a 75% share of the online job portal market. The platform now hosts 82 million resumes with 70,000 job seekers using premium services and 72,100 unique clients.

Management Changes

In August 2025, two senior executives ceased as Senior Management Personnel due to organizational restructuring, though specific names were not disclosed.

Operational Highlights

99acres achieved cash profitability, reflecting improved operational efficiency. The matrimony business significantly reduced operating losses while maintaining growth trajectory.

Market Outlook

Management remains optimistic about mid-to-long-term prospects across all verticals, with the IT sector showing signs of recovery as reflected in the July 2024 JobSpeak report. Strategic investments in AI and marketing aim to enhance service offerings and capture market share, particularly in technology and non-IT sectors.

Dividend Declaration

The Board recommended a final dividend of ₹3.60 per share (180%) for FY 2025, with July 25, 2025 as the record date and payment on or after September 2, 2025.

XIII. Links & Resources

Annual Reports & Investor Relations

- Info Edge Investor Relations Portal: www.infoedge.in/InvestorRelations

- Latest Annual Report (2023-24): Available on company website

- Quarterly Results & Presentations: NSE and BSE filings

Key Platforms

- Naukri.com: India's largest job portal

- 99acres.com: Real estate classifieds

- Jeevansathi.com: Matrimony services

- Shiksha.com: Education information portal

Market Data & Analysis

- NSE Symbol: NAUKRI

- BSE Code: 532777

- Current Market Cap: ~₹86,000 crores

- Stock Screeners: Screener.in, Tickertape, TrendLyne

Academic & Industry Research

- IIM Ahmedabad Case Studies on Info Edge

- Harvard Business School: "Info Edge: Pioneering Internet Business in India"

- Stanford GSB: Emerging Market Internet Business Models

Founder Resources

- Sanjeev Bikhchandani talks at ISB, IIMs

- Hitesh Oberoi interviews on AI strategy

- TiE and NASSCOM presentations on Indian internet evolution

Competitive Intelligence

- LinkedIn India market reports

- Indeed hiring trends data

- NASSCOM reports on Indian recruitment industry

- RedSeer Consulting: Indian classifieds market analysis

Portfolio Company Resources

- Zomato (NSE: ZOMATO): Food delivery and dining

- PB Fintech/Policybazaar (NSE: POLICYBZR): Insurance aggregation

- Company filings for other portfolio investments

Industry Reports

- Indian Staffing Federation: Employment trends

- FICCI-NASSCOM: IT-BPM sector reports

- PropTiger/Housing.com: Real estate market data

- Google-BCG: Digital consumer reports for India

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube