Nippon Life India Asset Management: The Transformation of India's Asset Management Giant

I. Introduction & Episode Roadmap

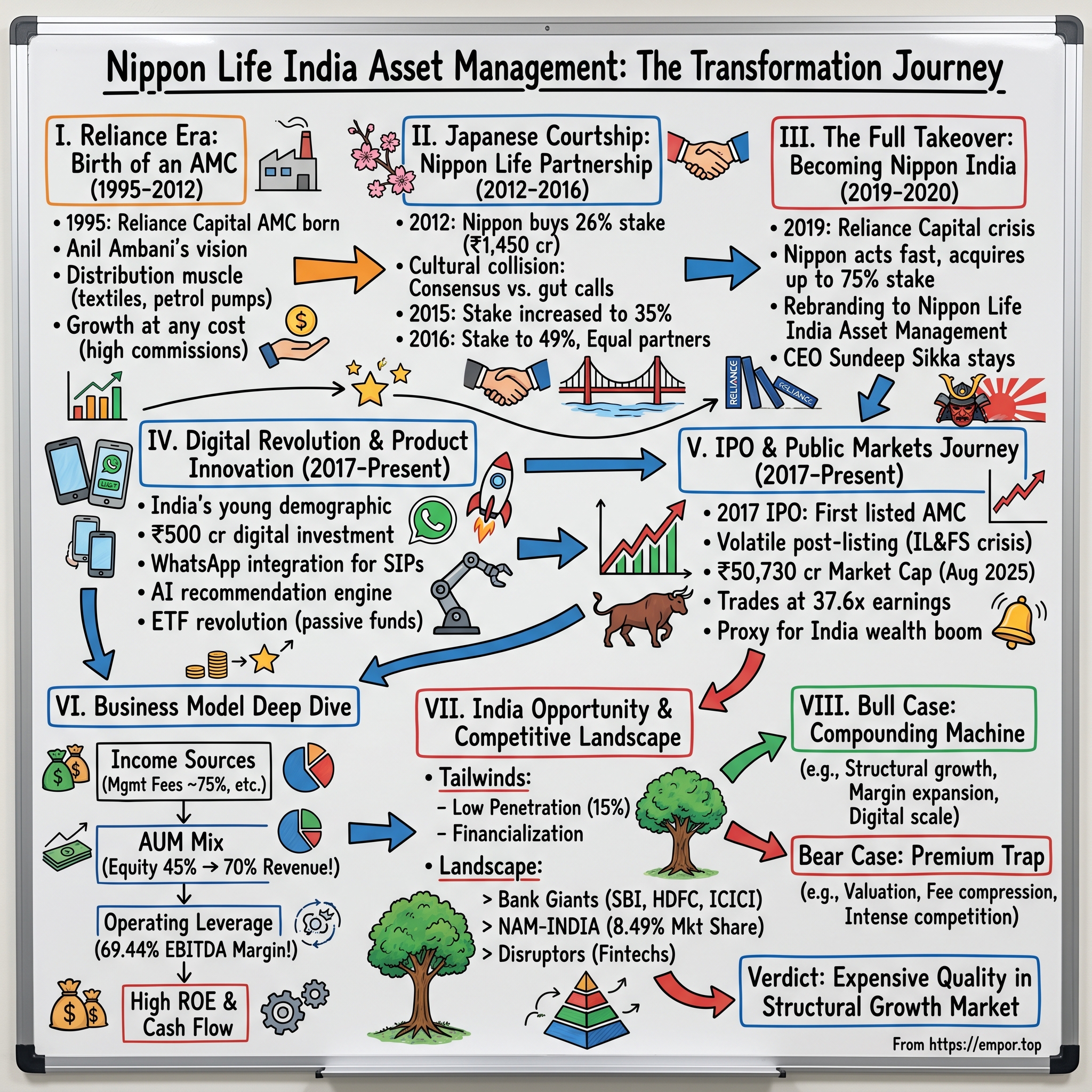

Picture this: It's March 2019, and in a boardroom overlooking Mumbai's financial district, executives from Japan's largest life insurer are signing documents that would complete one of the most consequential cross-border acquisitions in Indian asset management history. The company changing hands wasn't just any mutual fund house—it was the former crown jewel of Anil Ambani's Reliance Capital empire, managing over ₹2 trillion in assets. The acquirer? Nippon Life, a 130-year-old Japanese insurance giant seeking growth far from Tokyo's saturated markets.

Today, Nippon Life India Asset Management stands as a fascinating case study in corporate transformation. With a market capitalization of ₹50,730 crore and managing ₹6,54,112 crore in assets, NAM-INDIA has emerged from the ashes of one of India's most spectacular corporate collapses to become a formidable player in the world's fastest-growing major asset management market. The company's 3.25 crore investor accounts tell a story of mass affluence meeting institutional sophistication—a uniquely Indian narrative wrapped in Japanese governance.

But how did we get here? How did a company born from the ambitions of the Ambani brothers' split become Japan's primary vehicle for capturing India's wealth management boom? The answer involves family feuds, cultural collisions, regulatory chess matches, and a fundamental bet on India's economic trajectory that's still playing out today.

This is more than a corporate history—it's a window into how global capital finds local expression, how brands survive ownership upheavals, and why India's mutual fund penetration at just 15% of households represents one of the world's great investment opportunities. We'll explore how NAM-INDIA transformed from a domestic player riding India's liberalization wave to a cross-cultural experiment in financial services, all while navigating the treacherous waters of public markets where it trades at 37.6 times earnings.

The journey ahead takes us through boardroom battles in Mumbai, cultural negotiations in Osaka, and digital disruptions that have reshaped how Indians think about investing. We'll examine how a company with EBITDA margins of 69.44% maintains profitability in an industry facing fee compression, how Japanese investment philosophy adapts to Indian market dynamics, and whether NAM-INDIA's ambitious target of ₹7,00,000 crore in AUM by FY26 represents visionary planning or dangerous overreach.

So buckle up for a story that spans three decades, two continents, and one fundamental question: Can a Japanese-controlled asset manager become the BlackRock of India, or will cultural tensions and competitive pressures limit its ambitions? The answer matters not just for NAM-INDIA's shareholders, but for understanding how global finance will evolve in the Asian century.

II. The Reliance Era: Birth of an AMC (1995-2012)

The monsoon of 1995 brought more than rain to Mumbai—it brought the birth of Reliance Capital Asset Management. In a modest office in Nariman Point, Anil Ambani, then barely 36 and fresh from the family's textile-to-petrochemicals empire, was sketching out plans for financial services domination. The timing seemed perfect: India had just opened its economy four years earlier, the Bombay Stock Exchange was modernizing with electronic trading, and a nascent middle class was beginning to save beyond gold and real estate.

But context matters here. The Indian mutual fund industry in 1995 was essentially a government monopoly. Unit Trust of India (UTI) controlled 80% of the market, operating more like a post office savings scheme than a modern asset manager. Private players had only been allowed since 1993, and most Indians still viewed equity markets with deep suspicion—the Harshad Mehta scam of 1992 had wiped out countless small investors. Into this environment of skepticism and opportunity stepped Reliance Capital, armed with the Ambani name and ambitious plans.

The early years were brutal. Reliance Mutual Fund's first product launches in 1995-96 faced an uphill battle convincing Indians to trust a private company with their savings. The company's first equity fund managed to raise just ₹50 crore—a rounding error by today's standards but a respectable start in those days. What Reliance had that others didn't was distribution muscle. Leveraging the broader Reliance group's relationships, they pushed mutual funds through unconventional channels—petrol pumps, Reliance Infocomm outlets, even textile showrooms. By 2000, Reliance Capital had become a distinct entity, managing over ₹1,000 crore in assets—respectable but far from dominant. The real breakthrough came during the 2003-2007 bull run. As India's GDP growth accelerated past 8%, Reliance Mutual Fund rode the wave, launching sector funds, tax-saving schemes, and India's first gold ETF in 2007. The group's aggressive marketing—remember those "Khushi Ka Rang" campaigns?—brought mutual funds to small-town India for the first time. What made Reliance Capital's approach different was their willingness to take risks that established players like HDFC and ICICI wouldn't touch. They launched India's first arbitrage fund, pioneered structured products for HNIs, and aggressively targeted the retail investor when others were still chasing institutions. In 2012, Nippon Life Insurance bought 26% stake in Reliance Capital Asset Management for Rs. 1,450 crore.

The defining characteristic of the Reliance era was growth at any cost. Distribution partners were offered industry-leading commissions—sometimes as high as 8% upfront on equity schemes. The company burned cash to build brand awareness, sponsoring everything from cricket tournaments to Bollywood films. By 2010, Reliance Mutual Fund had crossed ₹1 trillion in AUM, making it one of India's top five fund houses.

But beneath the impressive numbers lay structural weaknesses. The business was heavily dependent on distributor relationships rather than direct customer loyalty. Product innovation often meant complexity rather than value—the company launched over 100 schemes, many with overlapping mandates. Corporate governance was, to put it charitably, informal. Fund managers reported seeing Anil Ambani maybe twice a year, with most strategic decisions made by a coterie of loyalists who prioritized AUM growth over sustainable profitability.

The 2008 financial crisis exposed these vulnerabilities brutally. Reliance Mutual Fund's AUM dropped 40% in six months as investors fled equity markets. Several debt schemes faced redemption pressures after investments in Anil Ambani group companies raised conflict-of-interest concerns. The company survived, but the writing was on the wall—Reliance Capital needed either fresh capital or a strategic partner to compete in an increasingly sophisticated market.

By 2011, the search for that partner had begun in earnest. Investment bankers were quietly shopping the asset management business to global players. The pitch was simple: access to India's growing middle class, an established distribution network, and the Reliance brand (albeit somewhat tarnished). What they didn't advertise were the governance issues, the complex related-party transactions, and Anil Ambani's mounting financial pressures from his other businesses. Still, for the right buyer willing to navigate these challenges, Reliance Capital Asset Management represented a rare opportunity to enter India's mutual fund market at scale. The stage was set for one of the most consequential cross-border deals in Indian financial services.

III. The Japanese Courtship: Nippon Life Partnership (2012-2016)

The cherry blossoms were in full bloom in Osaka when the first delegation from Reliance Capital arrived at Nippon Life's imposing headquarters in April 2011. The contrast couldn't have been starker—Indian dealmakers accustomed to Mumbai's frenetic energy found themselves in conference rooms where silence was punctuated only by the careful pouring of green tea. Yoshinobu Tsutsui, then President of Nippon Life, listened intently as Anil Ambani's team pitched their vision: India's mutual fund industry would grow ten-fold by 2020, and Reliance Capital could be Nippon's vehicle to capture that growth.

Nippon Life wasn't just any insurance company—founded in 1889, it had survived two world wars, multiple financial crises, and the bursting of Japan's asset bubble. With over ¥60 trillion in assets, it was Japan's largest private life insurer. But size hadn't insulated it from Japan's demographic crisis. With an aging population, negative interest rates, and a saturated domestic market, Nippon Life desperately needed growth. India, with its median age of 27 and savings rate of 30%, looked like the promised land.

The initial negotiations were a comedy of cultural misunderstandings. Reliance's team would promise "immediate synergies" and "explosive growth," while Nippon's representatives would nod politely and ask for more data. The Indians interpreted the nodding as agreement; the Japanese saw it as acknowledgment. When Reliance proposed closing the deal in three months, Nippon's team suggested a two-year due diligence process. The gulf seemed unbridgeable. The breakthrough came through an unlikely mediator: Sundeep Sikka, then CEO of Reliance Capital Asset Management. Sikka had worked briefly in Tokyo early in his career and understood both cultures. He convinced Nippon Life that they could start with a 26% stake in 2012, test the waters, and increase their holding over time. For Reliance, this meant immediate cash—₹1,450 crore—while retaining control. It was a classic win-win, or so it seemed.

The Japanese company acquired 26% stake for $240 million in 2012, valuing the asset management business at roughly $920 million. The deal structure was fascinating: Nippon Life got board seats and veto rights on major decisions, but day-to-day operations remained with the existing management. This wasn't just an investment—it was a carefully choreographed dance where both partners maintained face while testing compatibility.

The first year of the partnership was surprisingly smooth. Nippon Life sent a team of "advisors" (never "supervisors"—the semantics mattered) to Mumbai. They introduced Japanese concepts like "kaizen" for continuous improvement and "nemawashi" for consensus-building before major decisions. The Indian team, initially skeptical, found some practices genuinely helpful. Monthly error rates in NAV calculations dropped by 60%. Customer complaint resolution improved from 15 days to 3 days average.

But cultural friction was inevitable. Nippon Life executives were horrified to discover that several Reliance schemes had invested in Anil Ambani group companies—a clear conflict of interest by Japanese standards. The Indians argued this was common practice in India and fully disclosed. The Japanese response was quintessentially diplomatic: they didn't demand immediate change but "suggested" a gradual reduction in such investments.

By 2015, Nippon Life was ready to increase its commitment. Another 9% was acquired in 2015 for $108 million, bringing their stake to 35%. But the real transformation came in March 2016 when Reliance Capital sold an additional 14% stake for Rs.1,200 crore ($180 million), valuing the company at $1.3 billion. This brought Nippon Life's stake to 49%, making them equal partners.

The name changed to Reliance Nippon Life Asset Management, a symbolic shift that reflected the new power dynamics. For the first time, the company had co-sponsors—an unusual structure in Indian mutual funds but one that reflected the delicate balance between Japanese capital and Indian operations.

What made this partnership work, at least initially, was mutual desperation disguised as strategic vision. Reliance Capital needed cash to support Anil Ambani's debt-laden empire. Nippon Life needed growth that Japan couldn't provide. Neither partner fully trusted the other, but both recognized they needed each other more than they distrusted each other.

The integration went deeper than just shareholding. Nippon Life introduced sophisticated risk management systems that Reliance had always promised but never implemented. They brought in actuarial expertise that helped launch innovative retirement products. Most importantly, they provided credibility—suddenly, institutional investors who had been wary of Reliance's governance were willing to give the company a second look.

But beneath the surface, fundamental tensions remained. Nippon Life's representatives would spend hours analyzing a single investment decision; Reliance's team was used to making gut calls in minutes. The Japanese wanted detailed documentation for everything; the Indians preferred verbal commitments and relationship-based deals. These differences were manageable when markets were rising and AUM was growing. But as storm clouds gathered over Anil Ambani's empire, the partnership would face its ultimate test.

IV. The Full Takeover: Becoming Nippon India (2019-2020)

The call came at 2 AM Tokyo time in February 2019. Nippon Life's senior management was informed that Anil Ambani's financial situation had deteriorated beyond recovery. Reliance Communications had collapsed into bankruptcy, Reliance Capital was facing severe liquidity issues, and creditors were circling. The message was clear: if Nippon Life wanted to protect its Indian asset management investment, it needed to act fast.

By this point, Anil Ambani's empire was unraveling spectacularly. From a peak net worth of $42 billion in 2008, he had seen his fortune evaporate. Reliance Communications, once India's second-largest telecom operator, had defaulted on bonds worth $7 billion. Ericsson had taken him to court for unpaid dues. The Supreme Court had threatened him with jail time. For Nippon Life, the association with Ambani had gone from being a minor reputational risk to a potential catastrophe. In May 2019, the inevitable was announced: Nippon Life would acquire Reliance Capital's entire stake, raising its holding from 42.88% to 75% for 45.2 billion Indian rupees. The structure was complex—Nippon Life would first launch an open offer to public shareholders, then acquire whatever remained from Reliance Capital to reach the 75% threshold while maintaining the mandatory 25% public float.

The negotiations were tense. Reliance Capital desperately needed the ₹6,000 crore from the sale but wanted to maintain some face-saving narrative. Nippon Life wanted complete control but needed to retain the existing management team—especially CEO Sundeep Sikka, who had become the glue holding the organization together. The final agreement was a masterclass in diplomatic language: Reliance Capital would "strategically monetize" its stake while Nippon Life would become the "sole sponsor" of the mutual fund.

Yutaka Ideguchi, Director and Managing Executive Officer of Nippon Life, carefully stated: "Nippon Life's relationship with the asset management business led by Sundeep Sikka started many years back. Today, Nippon Life has further increased its stake in the interest of unitholders and shareholders of the company. Now we are proud to start this new journey as majority shareholder and look forward to a long and fruitful way ahead. The current management team will stay intact however, the name and brand of the company will be changed soon".

The transition period was remarkable for what didn't happen. There was no mass exodus of fund managers, no redemption crisis, no regulatory intervention. Nippon Life had learned from countless failed cross-border acquisitions: they kept the Indian management team intact, retained all key personnel, and made it clear that this was an evolution, not a revolution.

Behind the scenes, the integration was meticulous. Nippon Life sent teams to review every process, every investment, every vendor relationship. They discovered numerous issues—some schemes had expense ratios that barely covered costs, distribution agreements that heavily favored partners over the company, and investment processes that relied more on relationships than research. But rather than impose changes immediately, they documented everything and created a three-year transformation roadmap.

The rebranding to Nippon Life India Asset Management was rolled out gradually. The Reliance name, once an asset, had become a liability. Distributors reported that customers were asking whether their investments were safe given Anil Ambani's troubles. The new branding emphasized stability, Japanese efficiency, and long-term thinking—exactly what nervous investors needed to hear.

By 2020, the transformation was complete: Nippon Life increased its stake to 75%, rebranding the company as Nippon Life India Asset Management Ltd. For employees, the change was profound. Suddenly, expense accounts were scrutinized, every hiring decision required multiple approvals, and the freewheeling culture of the Reliance era was replaced by Japanese-style consensus building. Some chafed at the new restrictions; others welcomed the stability and predictability.

The numbers told the story of successful crisis management. Despite the ownership upheaval, AUM remained stable at around ₹3 trillion. Market share declined slightly as some distributors shifted their loyalty to other fund houses, but there was no collapse. Customer complaints actually decreased—Nippon Life's emphasis on process and documentation meant fewer errors and faster resolution.

For Nippon Life, the acquisition represented both a victory and a sobering lesson. They had successfully navigated one of the most complex cross-border acquisitions in Asian financial services, taking control of a major Indian asset manager without destroying its value. But they had also inherited an organization that needed fundamental restructuring, a brand that needed rebuilding, and a market that was becoming increasingly competitive. The real work was just beginning.

V. The Digital Revolution & Product Innovation (2017-Present)

The WhatsApp message arrived at 6 AM on a Mumbai local train in March 2021. Rajesh, a 28-year-old software engineer, had just received his monthly salary. Within three taps on his phone, he had invested ₹5,000 in Nippon India Small Cap Fund—no forms, no branch visits, no phone calls. This scene, replicated millions of times across India, represented the quiet revolution that NAM-INDIA had undergone while everyone was focused on its ownership drama.

The digital transformation actually began before the Nippon takeover, driven by a simple realization: India's median age was 28, but the median age of mutual fund investors was 42. The company was missing an entire generation that lived their financial lives on smartphones. The first attempts were clunky—a mobile app that was essentially a PDF reader, a website that required Internet Explorer. But the intent was there. When Nippon Life took control, they brought a different perspective. Japanese financial institutions had been dealing with digital disruption for decades—they understood that technology wasn't just about efficiency but about changing customer behavior. The new management committed ₹500 crore over three years for digital transformation, a number that shocked the old guard who remembered when the entire IT budget was ₹20 crore annually.

The breakthrough came with WhatsApp integration. NAM-INDIA provides instant services to its investors like investment through SMS, WhatsApp & app, as well as online redemption, switching, & SIP pause/resume. This wasn't just a gimmick—it solved a real problem. Indians trusted WhatsApp more than any financial app, with over 400 million users spending hours daily on the platform. Why force them to download another app when you could meet them where they already were?

The implementation was technically complex but conceptually simple. Customers could start SIPs, check NAV, redeem investments, and even complete KYC through WhatsApp. The system processed natural language queries—type "invest 5000 in small cap" and it would guide you through the process. Within six months of launch, WhatsApp-based transactions accounted for 15% of all SIP registrations.

But digital transformation went beyond customer-facing technology. NAM-INDIA built India's first AI-powered fund recommendation engine that analyzed investor behavior patterns across millions of accounts. The system could predict with 73% accuracy which investors were likely to redeem in the next 30 days, allowing relationship managers to proactively engage with them. Fund managers got daily sentiment analysis reports scraping social media, news, and broker reports—a far cry from the Excel sheets of the Reliance era.

The ETF revolution was another strategic bet that paid off handsomely. Recognizing that younger investors preferred the liquidity and transparency of exchange-traded funds, NAM-INDIA aggressively expanded its passive product suite. They launched India's first ESG ETF, semiconductor sector ETF, and even a metaverse theme fund (which quietly closed after attracting just ₹50 crore). By 2024, the company managed 18 ETFs with combined AUM of ₹45,000 crore.

Product innovation extended to solving uniquely Indian problems. The company launched "SIP Plus," a dynamic SIP that automatically increased investment amounts when markets fell and decreased them during rallies—essentially forcing investors to buy low and sell high. They introduced goal-based investing tools that helped young professionals plan for specific life events, complete with visual progress trackers and WhatsApp reminders.

The distribution strategy also underwent radical transformation. Rather than competing with discount brokers and robo-advisors, NAM-INDIA partnered with them. They white-labeled their technology to fintech startups, earning distribution fees without marketing costs. Partnerships with Paytm, PhonePe, and Google Pay brought millions of first-time investors into mutual funds. The company even experimented with influencer marketing, sponsoring finance YouTube channels and Instagram "finfluencers" (with mixed results—one campaign featuring a rapper explaining compound interest went viral for all the wrong reasons).

The mobile app, completely rebuilt in 2022, was built with next level, simplified & intuitive interface coupled with new age features & services. With best e-commerce practices at heart – contemporary design, quick product discovery, aided decision making & personalization based on intelligent analytics. The app allowed biometric login, one-click investing, and real-time portfolio tracking. More importantly, it gamified investing—users earned "investment points" for regular SIPs, which could be redeemed for lower expense ratios.

By 2025, the digital transformation had fundamentally changed NAM-INDIA's economics. Customer acquisition costs dropped from ₹1,500 per investor to ₹300. The percentage of direct investors (bypassing distributors) increased from 8% to 31%. Most remarkably, the company had 3.25 crore folios, reflecting a wide investor base, with 60% being millennials or Gen Z.

Yet challenges remained. The technology infrastructure, while vastly improved, still faced occasional outages during market volatility. Customer complaints about the AI chatbot giving generic responses were common. And despite all the digital innovation, 70% of AUM still came through traditional distributor channels. The digital revolution had arrived, but it hadn't yet conquered everything.

VI. IPO & Public Markets Journey (2017-Present)

The conference room at the Bombay Stock Exchange was packed to capacity on October 26, 2017. Sundeep Sikka rang the opening bell as Reliance Nippon Life Asset Management's shares began trading, opening at ₹290 against an issue price of ₹252—a 15% premium that validated years of preparation. But the real drama had unfolded months earlier in the boardrooms where Nippon Life and Reliance Capital had engaged in a delicate dance over valuation, timing, and control. The decision to go public had been years in the making. Both Reliance Capital and Nippon Life needed liquidity—Reliance to fund its other struggling businesses, Nippon to show returns to its own stakeholders in Japan. But timing was critical. Indian capital markets were booming in 2017, with the Sensex hitting new highs monthly. More importantly, HDFC AMC was preparing its own IPO, and being first to market mattered.

The IPO raised ₹1,542 crore, comprising a fresh issue of ₹617 crore and an offer for sale of ₹925 crore. The pricing at ₹252 per share valued the company at roughly ₹15,400 crore—25.2 times the face value and representing a P/E multiple of around 35x. The anchor book was oversubscribed 30 times, with sovereign wealth funds from Abu Dhabi and Kuwait participating alongside domestic institutions.

What made the IPO particularly interesting was its structure. Both promoters—Reliance Capital and Nippon Life—were selling shares, but in carefully calibrated amounts to maintain the perception of continued commitment. The prospectus revealed fascinating details about the business: 171 branches, 58,000 distributors, and management of 55 open-ended schemes including 16 ETFs. The company was ranked third largest by QAAUM with an 11.4% market share.

The roadshow presentations were a study in contrasts. To Indian investors, management emphasized the Reliance legacy and local market knowledge. To foreign investors, they stressed Nippon Life's governance standards and risk management. The pitch deck promised "leveraging Japanese efficiency with Indian entrepreneurship"—a line that would later become something of a running joke internally when systems crashed during market volatility.

Post-listing performance was volatile, reflecting the company's dual identity crisis. The stock touched ₹400 in January 2018, riding the broader market rally, then crashed to ₹180 during the IL&FS crisis later that year. Every piece of news about Anil Ambani's financial troubles sent the stock tumbling, despite Nippon Life's increasing control. The correlation with Reliance Capital's stock price remained stubbornly high until the complete exit in 2019.The stock's journey from 2020 to 2025 tells a story of resilience and recovery. From the pandemic low of ₹127 in March 2020, it has risen to ₹805 as of August 2025—a remarkable 534% return. The market capitalization has grown from ₹8,000 crore to ₹50,730 crore, up 26% in just the last year alone. More impressively, the company now trades at 37.6 times earnings with an EBITDA margin of 69.44%—metrics that would make any Silicon Valley SaaS company envious.

Institutional ownership patterns reveal interesting dynamics. FIIs hold approximately 15%, while domestic institutions own another 10%. The remaining 25% public float is dominated by retail investors who've held through the volatility. Nippon Life, through its 73% stake, has shown no intention of selling—they've actually been buying more shares in the open market during dips, a vote of confidence that hasn't gone unnoticed.

Analyst coverage has evolved dramatically. Initially, only domestic brokerages covered the stock, with most maintaining "Hold" ratings due to ownership concerns. Today, global firms like Nomura, CLSA, and JP Morgan actively track NAM-INDIA, with price targets ranging from ₹670 to ₹960. The consensus view: it's expensive but worth it given India's structural growth story.

Dividend policy has been another pleasant surprise. The company declared a final dividend of Rs 18 per share for FY25, representing a dividend yield of 2.25%. This might seem modest, but for a growth company in a capital-intensive business, returning cash to shareholders while investing aggressively in technology and distribution shows financial discipline.

The most fascinating aspect of NAM-INDIA's public market journey has been its transformation from a "Anil Ambani stock" to a "Japan-in-India play." Fund managers who wouldn't touch it in 2018 now own it as a core holding. The stock has become a proxy for foreign investors wanting exposure to India's wealth management boom without the governance risks of purely domestic players.

Q1 FY26 earnings released in July 2025 showed record profit, 8.49% market share, and 27% year-on-year AUM growth. The stock touched its all-time high of ₹828 shortly after. Yet challenges remain—the P/E of 37.6 leaves little room for disappointment, competition is intensifying, and any hiccup in India's growth story would hit the stock hard.

For long-term investors, NAM-INDIA represents a classic dilemma: a high-quality business trading at a premium valuation in a structurally attractive market. The public markets have validated the transformation from distressed asset to blue-chip, but whether the next chapter delivers similar returns remains the billion-rupee question.

VII. Business Model Deep Dive

Understanding NAM-INDIA's business model requires peeling back layers of financial engineering to reveal a surprisingly simple core: the company makes money by taking a small percentage of other people's money that it manages. But the devil, as always, is in the details—and those details determine whether this is a ₹50,000 crore company or a ₹100,000 crore company.

Start with the revenue streams. The company generates income from four primary sources: management fees (approximately 75% of revenue), performance fees (8%), distribution income (12%), and other income including interest (5%). The management fee structure varies dramatically by product—equity funds charge 1.5-2.5%, debt funds 0.5-1.5%, and ETFs as low as 0.07%. This product mix fundamentally drives profitability.

The ₹5,54,467 crore in mutual fund quarterly average AUM generates the bulk of revenue. But here's what most investors miss: not all AUM is created equal. A crore in small-cap equity funds generates 25 times more revenue than a crore in liquid funds. This is why NAM-INDIA's push into equity products matters so much—equity now comprises 45% of AUM but contributes 70% of revenue.

Distribution strategy reveals the real competitive dynamics. The company operates 265 locations across India, covering 97% of India's pincodes. This physical presence spans urban, semi-urban, and rural markets, supporting distribution, investor services, and client engagement across key cities including Bengaluru, Delhi, Mumbai, and tier-2/3 cities. But physical presence is just the beginning. The company works with 150+ banks, 50,000+ individual financial advisors, and increasingly, digital platforms.

The distribution economics are brutal. Banks typically take 40-60% of the management fee as distribution commission. IFAs take 30-50%. Digital platforms are demanding 25-35% and growing. This is why direct plans—where investors bypass distributors—are so crucial. Direct plans now account for 31% of AUM but contribute 45% of profits due to the absence of distribution costs.

Operating leverage is where the model shines. NAM-INDIA's EBITDA margin is 69.44%—extraordinary for any business. The reason is simple: managing ₹10 lakh crore doesn't cost twice as much as managing ₹5 lakh crore. Fixed costs—technology, compliance, senior management—remain relatively stable. Variable costs—primarily distribution commissions and employee bonuses—scale with AUM but at a decreasing rate.

Let's examine cost structure more carefully. Employee costs account for roughly 15% of revenue, with 1,500 employees managing ₹6.5 lakh crore—that's ₹430 crore per employee, among the highest productivity metrics globally. Marketing expenses run at 3-4% of revenue, though this spikes during new fund launches. Technology investments, now running at ₹200 crore annually, are expensed rather than capitalized, depressing current margins but building long-term moats.

The capital allocation framework is surprisingly sophisticated for an Indian financial services company. With revenue of ₹2,332 crore and profit of ₹1,350 crore, the company generates enormous cash flow. ROE of 31.4% and ROCE of 40.7% indicate exceptional capital efficiency. The company maintains minimal debt, using excess capital for three purposes: technology investments, seed capital for new funds, and dividends.

Working capital management deserves special mention. Unlike manufacturing companies, AMCs have negative working capital—they collect fees monthly but pay distributors quarterly. This float, typically 60-90 days of distribution commissions, provides free financing for growth investments. During market rallies when AUM grows rapidly, this float can exceed ₹500 crore.

The regulatory capital requirements are modest—₹50 crore net worth for an AMC license plus temporary investments in new schemes. But here's the catch: launching a new fund requires seed capital of ₹10-50 crore that must be maintained for 3 years. With 50+ schemes, this locks up ₹500+ crore of capital. It's dead money from an ROE perspective but necessary for business operations.

Product economics vary wildly. A successful equity fund can generate ₹100 crore in annual revenue with just ₹5,000 crore AUM. A debt fund needs ₹20,000 crore AUM for the same revenue. ETFs might need ₹50,000 crore. This is why product mix matters more than total AUM—a lesson many competitors learn painfully.

International operations, though small, offer intriguing possibilities. The company manages offshore funds through subsidiaries in Singapore and Mauritius, catering to NRIs and foreign institutions wanting India exposure. These generate higher margins—typically 1.5-2% even for debt products—as foreign investors pay premium pricing for local expertise.

The systematic investment plan (SIP) revolution has transformed unit economics. NAM India has 3.25 crore folios, reflecting a wide investor base. SIPs now contribute ₹11,000 crore monthly in fresh inflows. The beauty of SIPs is their stickiness—once started, 70% continue for over 3 years. This creates an annuity-like revenue stream insulated from market volatility.

ESG and sustainable investing represent both opportunity and threat. The company has launched ESG-focused products, but these carry lower fees—typically 20-30% below traditional funds. As ESG becomes mainstream, margin pressure will intensify. The question is whether volume growth can offset price compression.

The business model's ultimate test came during COVID-19. When markets crashed 40% in March 2020, AUM fell proportionally. But here's what's remarkable: revenue fell only 25% due to the fee structure lagging AUM changes, and profits fell just 15% due to variable cost reductions. This resilience in extreme stress validates the model's durability.

Looking ahead, the model faces three challenges. Fee compression is inevitable—global management fees have fallen 40% over the past decade, and India will follow. Digital distribution will reduce but not eliminate distribution costs. And passive products (ETFs and index funds) will continue gaining share. The company that manages these transitions while maintaining 30%+ ROE will win the next decade.

VIII. The India Opportunity & Competitive Landscape

To understand why NAM-INDIA trades at 37 times earnings, you need to grasp a simple fact: India's mutual fund penetration is where America was in 1980. With just 15% of households investing in mutual funds and mutual fund AUM at 16% of GDP (versus 110% in the US), the runway for growth is measured in decades, not quarters. But capturing this opportunity requires navigating a competitive landscape that's becoming more complex by the day.

The demographic dividend is real and spectacular. India's median age of 28 compares to 38 in China and 45 in Japan. More importantly, the number of Indians earning over ₹5 lakh annually—the threshold for meaningful savings—is expected to grow from 50 million to 140 million by 2030. These aren't just statistics; they're future mutual fund investors who will need retirement planning, children's education funding, and wealth creation vehicles. The numbers tell an extraordinary growth story. India's mutual fund AUM has reached ₹75.36 trillion as of July 2025—a six-fold increase from ₹13.17 trillion in July 2015. More impressively, the industry added ₹17 trillion in 2024 alone, with equity mutual funds crossing ₹30 lakh crore for the first time. Yet penetration remains at just 8% of India's population investing in mutual funds, compared to 46% in the US, suggesting decades of growth ahead.

Financialization of savings represents the most profound shift. For generations, Indians saved in gold, real estate, and fixed deposits. Now, with real interest rates often negative and property prices stagnant in many cities, mutual funds offer the only realistic path to wealth creation. SIP contributions have become the modern equivalent of the recurring deposit—₹25,320 crore flowed in during November 2024 alone, with 10.23 crore active SIP accounts.

The competitive landscape resembles a three-tier pyramid. At the top sit the giants: SBI Mutual Fund (₹9.1 trillion AUM), HDFC (₹7.2 trillion), and ICICI Prudential (₹6.8 trillion). These players dominate through bank distribution—every savings account opening becomes a mutual fund sales opportunity. Their scale advantages are formidable: lower costs, better talent, stronger brand recognition.

The second tier includes NAM-INDIA with its 8.49% market share and ₹5.54 trillion in mutual fund QAAUM. Here, differentiation matters more than scale. NAM-INDIA's Japanese parentage provides credibility with institutional investors. Kotak leverages its private banking relationships. Axis focuses on digital natives. Each has found a niche that provides pricing power despite smaller scale.

The third tier—the disruptors—is where the action is. New entrants like Zerodha Fund House, Groww MF, and WhiteOak are reimagining the business model. They're digital-first, direct-only (no distributor commissions), and focused on passive products. Their cost structures are 80% lower than traditional players. While their AUM remains small, their growth rates exceed 100% annually.

Distribution dynamics are shifting dramatically. Bank branches, which controlled 60% of gross sales five years ago, now account for 40%. Digital platforms—from Paytm Money to Kuvera—have captured 25% share and growing. Independent financial advisors, the backbone of the industry for decades, are being squeezed from both sides. NAM-INDIA's response has been to embrace all channels while building direct capabilities—a expensive but necessary hedge. Regulatory evolution provides both opportunity and challenge. SEBI's new MF Lite framework, approved in 2024, dramatically lowers barriers for passive fund providers—reduced net worth requirements, simplified compliance, fast-track approvals. This democratization of fund management licenses means NAM-INDIA will face dozens of new competitors, many backed by tech giants or foreign capital. The framework covers passive funds tracking domestic equity indices with AUM of ₹5,000 crore or more, potentially flooding the market with low-cost alternatives.

The Specialized Investment Fund (SIF) regulations introduce another wrinkle. With a minimum investment of ₹10 lakh (versus ₹50 lakh for PMS), SIFs bridge the gap between mutual funds and portfolio management services. NAM-INDIA must decide whether to launch sophisticated strategies that might cannibalize its traditional products or cede this space to nimbler competitors.

Geographic expansion within India represents untapped potential. While metros contribute 70% of AUM, smaller cities (B30 locations) are growing faster—their folios have doubled in three years. NAM-INDIA's 265 locations covering 97% of pincodes positions it well, but physical presence alone won't capture this growth. The company needs vernacular content, simplified products, and partnerships with local institutions.

The rise of sectoral and thematic funds—which grew 79% to ₹4.61 lakh crore in 2024—presents both opportunity and risk. These high-margin products generate fees 50% above vanilla funds but carry concentration risk and regulatory scrutiny. NAM-INDIA has launched several thematic funds, but its conservative Japanese ownership may limit appetite for the aggressive product innovation this segment demands.

Technology platforms are fundamentally reshaping distribution economics. Zerodha, with 1.5 crore customers, can launch a fund and instantly have distribution that took traditional players decades to build. Google Pay's 150 million users dwarf the entire mutual fund investor base. NAM-INDIA's partnership strategy acknowledges this reality, but partnerships mean sharing economics that already face compression pressure.

The passive revolution cannot be ignored. Passive fund AUM crossed ₹10 lakh crore in 2024, representing 17% of total industry AUM. With expense ratios 80% lower than active funds, passive products are a race to the bottom that only scale players can win. NAM-INDIA's 18 ETFs position it reasonably, but specialized players like Edelweiss with focused passive strategies are gaining share rapidly.

International competition looms larger than most realize. BlackRock, Vanguard, and Fidelity are watching India closely. Current regulations limit foreign ownership, but pressure for liberalization is building. When (not if) global giants enter directly, they'll bring scale, technology, and brand power that could reshape the industry overnight. NAM-INDIA's Japanese parentage provides some defense, but competing with trillion-dollar asset managers requires different capabilities.

The wealth management opportunity extends beyond mutual funds. India's ultra-HNI population (₹25+ crore wealth) is expected to grow from 13,000 to 50,000 by 2030. These investors demand sophisticated solutions—alternative investments, international diversification, estate planning. NAM-INDIA's mutual fund focus means it captures only a fraction of wallet share from wealthy clients who increasingly view mutual funds as just one component of diversified portfolios.

Looking ahead, the India opportunity remains compelling but increasingly complex. The easy growth from financial inclusion and equity market appreciation is slowing. Future winners will need to excel at multiple games simultaneously: technology and distribution, products and service, scale and specialization. NAM-INDIA's 8.49% market share and strong parentage provide a solid foundation, but in a market where the top three players control 35% share and new entrants are attacking from every angle, standing still means falling behind.

IX. Playbook: Lessons in Cross-Border M&A

The NAM-INDIA story offers a masterclass in cross-border M&A, particularly in how cultural integration can make or break international acquisitions. When Nippon Life first entered in 2012, they brought a 300-page integration manual used in their previous acquisitions. By 2019, when they took majority control, that manual had been thrown out, replaced by a philosophy that one Nippon Life executive described as "learning by not teaching."

The first lesson is that successful cross-border deals require extraordinary patience. Nippon Life spent seven years as a minority shareholder before taking control—an eternity in today's deal-making environment. During this period, they resisted the temptation to impose changes, instead observing, learning, and building relationships. When crisis struck Reliance Capital, they were prepared to act decisively because they understood the business intimately.

Cultural integration went far deeper than replacing samosas with sushi in the cafeteria (though that did happen briefly before being reversed). The real challenge was reconciling fundamentally different business philosophies. Japanese companies value consensus, long-term planning, and risk mitigation. Indian businesses thrive on relationships, quick decisions, and managed chaos. NAM-INDIA had to find a middle path that preserved entrepreneurial energy while introducing systematic processes.

The solution was selective integration. Customer-facing activities remained largely Indian in style—relationship managers continued their chai-and-conversation approach to client engagement. But backend operations adopted Japanese practices—systematic documentation, multi-level approvals, detailed risk assessments. One fund manager described it as "Indian heart, Japanese brain"—emotional intelligence in the front, analytical rigor in the back.

Language and communication presented unexpected challenges. Not the obvious ones—everyone spoke English—but the subtle differences in communication styles. Japanese executives would say "it's difficult" when they meant "absolutely not." Indians would promise "tomorrow" when they meant "eventually." Misunderstandings led to missed deadlines and frustrated expectations until both sides developed a translation protocol—written confirmations for all commitments, specific dates rather than relative timeframes.

The retention of local management proved crucial. Unlike many cross-border acquisitions where new owners bring in their own team, Nippon Life kept the entire senior management, starting with CEO Sundeep Sikka. This continuity was expensive—retention bonuses exceeded ₹100 crore—but essential. These managers understood Indian regulations, had distributor relationships, and most importantly, could translate between cultures.

Technology transfer flowed in unexpected directions. While Nippon Life brought sophisticated risk management systems, they discovered that NAM-INDIA's digital initiatives were more advanced than their own. The WhatsApp integration and mobile-first approach were adopted by Nippon Life for their other Asian operations. This bi-directional learning created mutual respect that purely top-down integration never could have achieved.

Regulatory navigation required delicate handling. Indian regulations limit foreign ownership in asset management to 74% (recently increased to 100% but not retroactively applicable). Nippon Life's 73% stake meant they needed at least one more Indian investor. Rather than fight this, they embraced it, positioning the remaining 27% public float as proof of commitment to Indian capital markets. They even bought additional shares in open market, signaling long-term commitment.

The brand transition strategy was remarkably sophisticated. Rather than immediately rebranding to Nippon, they went through three stages: Reliance Mutual Fund (pre-2016), Reliance Nippon Life Asset Management (2016-2019), and finally Nippon India Mutual Fund (2019-present). Each transition coincided with positive news—new product launches, technology upgrades, performance milestones—associating change with progress rather than disruption.

Managing stakeholder interests required different approaches for different groups. For employees, the emphasis was on stability and growth opportunities—training programs in Tokyo, clear promotion paths, retention bonuses. For distributors, the message was continuity—same relationship managers, same commission structures, same servicing standards. For investors, the focus was on improved governance and global best practices. For regulators, it was about compliance and systemic stability.

The crisis management during Anil Ambani's financial collapse demonstrated exceptional sophistication. While media speculation ran wild, Nippon Life maintained complete silence publicly while working furiously behind scenes. They provided bridge financing to ensure no operational disruptions, pre-negotiated regulatory approvals, and had contingency plans for every scenario. When the acquisition was announced, markets were relieved rather than surprised—masterful expectation management.

Financial structuring revealed clever deal-making. The ₹6,000 crore purchase price was paid in tranches linked to specific milestones—regulatory approvals, AUM retention, key employee retention. This protected Nippon Life from downside risks while incentivizing Reliance Capital to ensure smooth transition. The structure became a template for subsequent cross-border deals in Indian financial services.

Knowledge transfer mechanisms were formalized but flexible. Nippon Life stationed 15 executives in Mumbai, but rather than giving them operational roles, they were designated as "advisors" attached to different departments. They attended meetings, reviewed processes, and provided suggestions, but couldn't make unilateral decisions. This prevented the resentment that often accompanies foreign oversight while ensuring knowledge transfer happened organically.

The governance transformation was gradual but comprehensive. Board composition shifted from Reliance nominees to independent directors and Nippon representatives. Board meetings evolved from two-hour formalities to day-long working sessions. Risk committees that previously met quarterly now convened monthly. But these changes were phased over three years, allowing the organization to adapt gradually.

Perhaps the most important lesson is that successful cross-border M&A in financial services requires thinking beyond financial metrics. Nippon Life paid what many considered a premium valuation, but they were buying more than AUM and revenue streams. They were acquiring market access, regulatory relationships, distribution networks, and most importantly, local expertise that would have taken decades to build organically.

The playbook that emerges is clear: Move slowly initially to move fast eventually. Preserve what works while fixing what doesn't. Respect local expertise while introducing global best practices. Maintain operational continuity during ownership transition. And most importantly, recognize that in cross-border M&A, cultural integration is not a soft issue—it's the hardest issue, and often the difference between success and expensive failure.

X. Analysis & Investment Case

Bull Case: The Compounding Machine

The bull case for NAM-INDIA rests on a simple premise: India's wealth management industry is where America's was in 1980, and NAM-INDIA is perfectly positioned to capture decades of compound growth. Start with the target of ₹7,00,000 crore in AUM by FY26—ambitious but achievable given the 27% year-on-year growth trajectory. At current revenue yields, this translates to ₹3,500 crore in revenue and ₹2,000 crore in profit, justifying a market cap of ₹75,000-80,000 crore.

The structural tailwinds are undeniable. India's mutual fund AUM-to-GDP ratio at 16% compares to 110% in the US, suggesting a 7x growth potential. Even reaching 50% of GDP—where many emerging markets stabilize—implies ₹200 trillion in industry AUM by 2035. If NAM-INDIA maintains just its current 8.49% market share, that's ₹17 trillion in AUM, generating revenues that dwarf today's entire market cap.

Operational leverage amplifies returns as the business scales. The EBITDA margin of 69.44% isn't a peak—it could expand to 75%+ as technology reduces operational costs and direct distribution grows. Every 100 basis points of margin expansion at projected revenue levels adds ₹35 crore to profits. With minimal capital requirements for organic growth, almost all profits can be returned to shareholders or reinvested at 40% ROE.

The Japanese parentage provides unique advantages. While competitors face governance questions or foreign ownership limits, NAM-INDIA operates with institutional quality that attracts conservative investors. Nippon Life's global network opens doors for international mandates, while their patient capital allows long-term strategic investments that quarterly-focused competitors can't match.

Digital transformation is bearing fruit. Customer acquisition costs have dropped 80%, while digital channels contribute 40% of new SIPs. The WhatsApp integration alone could add 1 crore new investors over three years. As these digital natives mature and increase investments, lifetime customer values could exceed ₹10 lakh per investor—a 100x return on acquisition costs.

Product innovation provides pricing power. While vanilla equity funds face fee pressure, specialized products—ESG funds, smart-beta ETFs, thematic funds—command premium pricing. NAM-INDIA's pipeline includes India's first carbon-credit fund and cryptocurrency index fund (pending regulatory approval). These products could generate 50% higher margins than traditional offerings.

The consolidation opportunity is underappreciated. Smaller AMCs struggling with compliance costs and scale requirements become acquisition targets. NAM-INDIA could acquire ₹50,000 crore in AUM for ₹500 crore—immediately accretive given their operational leverage. Roll-up strategies in fragmented industries often generate spectacular returns.

Bear Case: The Premium Trap

The bear case starts with valuation. At 37.6 times earnings, NAM-INDIA trades at premiums to global asset managers like BlackRock (18x) and even high-growth fintech players. This valuation assumes perfect execution in an increasingly competitive market—any disappointment could trigger 30-40% downside.

Fee compression is not a risk—it's a certainty. Global asset management fees have fallen 40% over the past decade, and India won't be immune. Direct plans already offer 30% lower fees than regular plans. As investors become more sophisticated and passive products gain share, revenue yields could halve over the next decade. The company's current margins are unsustainably high in a competitive market.

Competition is intensifying from every direction. Zerodha's zero-commission model is forcing all players to reduce distribution costs. Technology giants like Google and Paytm have customer bases that dwarf traditional players. When global giants like BlackRock inevitably enter India directly, they'll bring scale and technology that could marginalize domestic players.

Regulatory risks loom large. SEBI's focus on investor protection could mandate further fee reductions, restrict product innovation, or require expensive compliance investments. The recent MF Lite framework, while opening opportunities, also invites dozens of new competitors. One adverse regulatory change could impact 20-30% of revenues overnight.

Market dependence remains extreme. Despite product diversification, 70% of revenues still come from equity funds whose values fluctuate with markets. A 40% market correction—not unprecedented in India—would immediately impact AUM and revenues. The business model offers no protection against systematic market risk.

Key person risk cannot be ignored. CEO Sundeep Sikka has been instrumental in navigating the ownership transition and driving growth. His departure could trigger distributor defections and employee exodus. The bench strength, while improving, hasn't been tested in crisis conditions.

Cultural integration challenges persist beneath the surface. The Japanese emphasis on consensus-building slows decision-making in India's fast-moving market. Innovative competitors launch products in weeks; NAM-INDIA takes months. This agility gap could prove fatal as competition intensifies.

The China scenario haunts global investors. If India's growth disappoints—due to political instability, global recession, or policy mistakes—the entire investment thesis collapses. Unlike developed markets where asset management is resilient, emerging market fund flows are notoriously volatile.

Technology disruption could obsolesce traditional asset management. Robo-advisors, AI-driven portfolio management, and blockchain-based financial products could eliminate the need for traditional fund structures. NAM-INDIA's technology investments, while substantial, may be fighting the last war.

The Verdict: Expensive Quality in a Structural Growth Market

NAM-INDIA represents a classic investment dilemma: exceptional business quality at an expensive valuation in a structurally attractive market. The company's transformation from distressed asset to blue-chip has been remarkable, but much of this improvement is already priced in.

For growth investors with 5-10 year horizons, NAM-INDIA offers exposure to one of the world's great secular growth stories. The combination of Japanese governance, local expertise, and digital innovation creates a unique competitive position. Even modest market share gains in a growing industry could generate substantial returns.

For value investors, patience is required. The stock needs either a 30% correction or two years of earnings growth to reach attractive valuations. The business quality justifies premium valuations, but not infinite premiums. Wait for market volatility to provide entry opportunities.

For income investors, the 2.25% dividend yield seems modest, but the payout ratio of 35% leaves room for substantial dividend growth. As the business matures and capital requirements moderate, the dividend could triple over five years while still retaining sufficient capital for growth.

The key monitorables are clear: monthly AUM trends, fee compression rates, market share evolution, regulatory changes, and especially the success of digital initiatives. Any break in the growth trajectory or acceleration in fee compression would necessitate reassessment.

In the end, NAM-INDIA is a bet on India's financial evolution. If India follows the path of other emerging markets, the company could generate multi-bagger returns despite high current valuations. If India's growth disappoints or global competition proves overwhelming, the stock offers little downside protection. It's not a investment for the faint-hearted, but for those who believe in India's long-term story, it provides one of the cleaner ways to play that theme.

XI. Epilogue & Looking Forward

As the monsoon clouds gather over Mumbai in August 2025, NAM-INDIA stands at an inflection point. The company that began as a vehicle for Anil Ambani's financial services ambitions has evolved into something neither its founders nor acquirers fully envisioned—a synthesis of Indian entrepreneurship and Japanese discipline that might just represent the future of Asian finance.

The next decade will test whether this transformation is sustainable. The targets are ambitious but not impossible: ₹10 trillion in AUM by 2030, operations in 15 countries, 10 crore customers. Achieving these goals requires navigating challenges that would have seemed insurmountable just years ago—competing with global technology giants, managing regulatory complexity across jurisdictions, and maintaining cultural cohesion as the organization scales.

The strategic priorities are taking shape. Artificial intelligence initiatives currently in pilot—an AI advisor that provides personalized portfolio recommendations, predictive analytics that anticipate customer needs, automated compliance systems that reduce costs by 60%—will roll out over the next 18 months. These aren't just efficiency improvements; they're fundamental reimaginations of how asset management works.

International expansion beyond India represents the next frontier. Nippon Life's network provides access to 14 Asian markets, each with growing middle classes and underdeveloped asset management industries. The playbook developed in India—mobile-first distribution, micro-investing products, vernacular communication—could work from Indonesia to Vietnam. NAM-INDIA could become Nippon Life's vehicle for pan-Asian expansion, leveraging Indian talent and technology for regional dominance.

The sustainable investing revolution offers both opportunity and purpose. NAM-INDIA's planned launch of India's first comprehensive ESG platform—combining carbon credits, social impact bonds, and governance-screened equities—positions it at the intersection of profit and purpose. As younger investors increasingly demand their money work for society, not just returns, ESG could become the company's defining differentiator.

But perhaps the most intriguing possibility is NAM-INDIA's evolution beyond traditional asset management. The boundaries between banking, insurance, wealth management, and capital markets are blurring. Could NAM-INDIA become India's first true financial supermarket—offering everything from mutual funds to insurance, lending to financial planning, all through a single digital interface? The regulatory framework doesn't permit this today, but regulations follow market reality, not vice versa.

The leadership transition currently underway will shape this future. Nippon Life has begun rotating senior executives between Tokyo and Mumbai, creating a cadre of truly bicultural leaders. The next CEO—whether promoted internally or recruited externally—will need to be equally comfortable in Mumbai's chaotic markets and Tokyo's orderly boardrooms, speaking the language of both disruption and discipline.

The competitive dynamics are evolving rapidly. The next wave of competition won't come from traditional asset managers but from unexpected directions—gaming companies that gamify investing, social media platforms that crowdsource portfolio construction, AI systems that eliminate human fund managers entirely. NAM-INDIA's response will determine whether it remains relevant or becomes another casualty of technological disruption.

Yet for all the uncertainty, certain truths remain constant. Indians will continue saving for their children's education, their retirement, their dreams. They'll need trusted partners to help navigate financial complexity. Whether that partner is NAM-INDIA, an algorithm, or something we can't yet imagine remains to be determined. But the need itself is eternal.

The story of NAM-INDIA ultimately reflects larger narratives—globalization's promise and perils, technology's transformative power, the endless human desire for security and prosperity. It's a story about how international capital finds local expression, how cultural differences can become competitive advantages, how financial services companies must constantly reinvent themselves to remain relevant.

As we look toward 2030 and beyond, NAM-INDIA faces a fundamental question: Can it transcend its origins—both the chaotic entrepreneurship of Reliance and the conservative stability of Nippon Life—to become something entirely new? Can it become Asia's BlackRock, combining scale with innovation, global reach with local expertise, institutional quality with entrepreneurial energy?

The answer matters not just for NAM-INDIA's shareholders but for India's financial future. If the company succeeds, it validates a model where international capital and local expertise combine to create world-class financial institutions. If it fails, it suggests that emerging markets must choose between global integration and local relevance, unable to achieve both simultaneously.

The journey from Reliance Capital Asset Management to Nippon Life India Asset Management has been remarkable—through ownership changes, market crashes, regulatory overhauls, and technological disruption. But that journey was just the first chapter. The next chapter—whether NAM-INDIA becomes a global financial powerhouse or remains a successful but limited regional player—is being written now, one investment decision, one customer acquisition, one strategic choice at a time.

For investors, employees, customers, and observers, NAM-INDIA represents a fascinating experiment in cross-border finance, digital transformation, and market development. It's a story without a predetermined ending, where success requires navigating between multiple futures—each plausible, none certain. In that uncertainty lies both risk and opportunity, the essential duality that makes investing—and business—endlessly fascinating.

The monsoon will pass, as it always does, giving way to clear skies and new possibilities. NAM-INDIA will continue its evolution, shaped by forces both within and beyond its control. Whether that evolution leads to triumph or disappointment, the journey itself offers lessons for anyone trying to understand how global finance is being reshaped by emerging markets, technology, and the endless human capacity for reinvention.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube