Muthoot Finance: The Golden Empire of India

I. Introduction & Episode Setup

In the bustling streets of India, where ancient traditions meet modern finance, stands a remarkable institution that holds more gold than most central banks of smaller nations. Muthoot Finance Limited, with 202 tonnes of gold jewelry in its vaults, serves over 250,000 customers daily across 4,800+ branches, commanding a market capitalization of ₹1,06,024 crores. This is not just another financial services company—it's a testament to how understanding cultural nuances can build billion-dollar empires.

The story of Muthoot Finance poses a fascinating question: How did a grain trader's descendants transform a small-town trading business into India's largest gold loan NBFC, holding more gold than the reserves of countries like Singapore or Sweden? The answer lies in a unique combination of cultural insight, operational excellence, and an unwavering focus on serving India's underbanked population.

This deep dive explores the 137-year journey from a modest trading post in Kerala to a financial powerhouse that has fundamentally changed how Indians leverage their most precious asset—gold. We'll examine how three generations of the Muthoot family built an empire by recognizing that in India, gold isn't just jewelry; it's savings, security, and social capital rolled into one. The company's evolution mirrors India's own economic transformation, from colonial commerce through socialist planning to liberalized markets and digital disruption.

What makes this story particularly compelling is how Muthoot Finance solved a uniquely Indian problem. In a country where households collectively hold over 25,000 tonnes of gold—roughly 11% of the world's entire gold stock—most of this wealth remained unproductive, locked away in safes and lockers. Muthoot pioneered the transformation of this dead asset into working capital, creating a bridge between India's informal economy and formal financial system.

The implications extend far beyond finance. This is a story about financial inclusion, about bringing banking to the unbanked, about understanding that sometimes the best innovations aren't technological but cultural. It's about recognizing that in emerging markets, the path to scale often runs through trust, not technology; through branches, not apps; through understanding local needs, not imposing global solutions.

As we unpack this narrative, we'll discover how a company built on the simple premise of lending against gold became instrumental in India's economic development, financing everything from children's education to small business expansions, from medical emergencies to agricultural investments. This is the story of how gold, India's traditional store of value, became the key to unlocking modern financial services for millions.

II. The Muthoot Origins: Three Generations of Foundation (1887–1939)

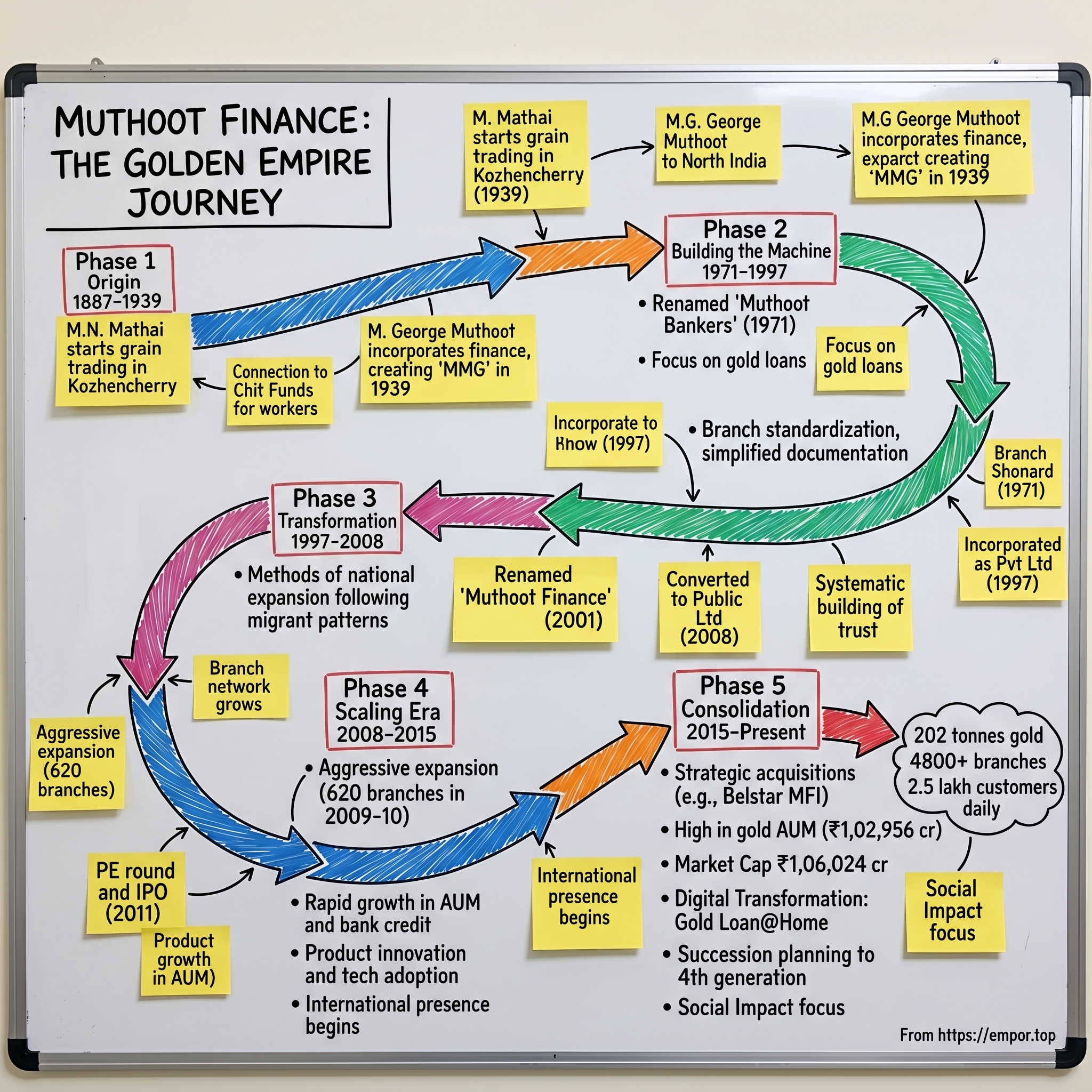

The story of Muthoot Finance begins not in boardrooms or banks, but in the dusty grain markets of colonial Kerala in 1887. M.N. Mathai, known as N. Mathai Muthoot, established a trading business in 1887 at Kozhencherry, a small town in Kerala. This was an era when Kerala was part of the Travancore princely state, a time of British colonial rule, emerging cash economies, and traditional communities navigating modern commerce.

The family traces its roots to Thevervelil Family in the small town of Kozhencherry in Central Travancore. The Muthoots belonged to Kerala's Syrian Christian community, one of the oldest Christian communities in the world, claiming apostolic origins from St. Thomas's arrival in 52 AD. This community had developed a unique position in Kerala's social hierarchy—neither part of the Hindu caste system nor aligned with colonial powers, they occupied a distinctive entrepreneurial space, engaging in trade, agriculture, and money lending.

The wholesale goods were supplied to the large Estates owned by British Companies. This connection to British estates proved crucial. The plantation economy—rubber, tea, coffee, and spices—created new cash flows and credit needs. Workers needed advances against wages, planters required working capital, and traders needed inventory financing. Traditional banking barely existed outside major cities, creating vast unmet financial needs.

Understanding the unmet saving needs of the estates' workers, Mr. Ninan Mathai, started the Chit Funds business with an aim to provide philanthropic services and give the workers an avenue for saving. Chit funds—rotating savings and credit associations—were perfectly suited to Kerala's social fabric. They combined collective saving with credit access, operating on trust and social capital rather than formal collateral.

The Orthodox Christian faith shaped the family's business philosophy profoundly. Unlike the Protestant work ethic that Max Weber famously analyzed, Orthodox Christianity in Kerala emphasized community welfare, charitable obligations, and viewing wealth as stewardship rather than personal achievement. This worldview would later manifest in Muthoot's approach to financial inclusion—seeing money lending not as exploitation but as social service.

The business was later taken over by his son M George Muthoot, who incorporated the finance division of the group, which was until then primarily involved in wholesale of grains and timber. This transition from pure trading to finance represented a crucial evolution. M. George Muthoot recognized that in an economy transitioning from barter to cash, from agricultural to mixed, the real opportunity lay not in moving goods but in moving money.

In 1939, M. George Muthoot created a partnership firm under the name of Muthoot M. George & Brothers (MMG). MMG was a chit fund based out of Kozhencherry. The timing was significant—1939 marked the beginning of World War II, which would bring unprecedented economic changes to India. War financing, commodity shortages, and inflation created both challenges and opportunities for financial intermediaries.

The choice of gold as collateral wasn't accidental but deeply rooted in Indian culture and Kerala's specific context. Kerala had the highest per capita gold ownership in India, driven by several factors. The matrilineal inheritance systems of certain communities meant women controlled significant wealth, traditionally held in gold. The Gulf migration boom, which would accelerate in later decades, had already begun, with overseas workers sending gold instead of cash remittances. Gold served multiple functions—savings account, insurance policy, status symbol, and religious offering.

Unlike land, which was difficult to value and transfer, or agricultural produce, which was perishable, gold offered unique advantages as collateral. It was easily valued, highly liquid, emotionally significant (ensuring borrowers would redeem it), and resistant to depreciation. Most importantly, it was owned by those excluded from formal banking—women, farmers, small traders—making it the perfect bridge to financial inclusion.

The family structure itself became a business asset. The Syrian Christian joint family system, where multiple generations lived and worked together, provided built-in succession planning, capital accumulation through pooled resources, and trust networks extending across communities. Business wasn't separate from family; it was family expression through commerce.

By 1939, the foundations were set: a trading heritage providing commercial acumen, a finance division understanding credit and risk, community trust built over two generations, and recognition of gold's unique role in Indian society. The Muthoots weren't trying to import Western banking models; they were creating something uniquely Indian, building on existing social and cultural infrastructure.

What distinguished the Muthoots from countless other trader-lenders of the era was their vision of scale and systematization. While others saw money lending as a local, relationship-based activity, the Muthoots began imagining it as an organized, replicable business model. They understood that India's financial exclusion wasn't a bug but a feature of the formal system, creating massive opportunity for those willing to serve the excluded.

The Orthodox Christian emphasis on documentation and record-keeping, inherited from centuries of maintaining church records and property deeds, gave them administrative capabilities rare in informal finance. They maintained meticulous accounts, creating trust through transparency in an industry notorious for opacity.

As World War II reshaped India's economy, the Muthoots positioned themselves at the intersection of traditional society and modern finance. They weren't abandoning tradition for modernity or resisting change for tradition's sake. Instead, they were creating a hybrid—modern financial services delivered through traditional social channels, formal documentation supporting informal relationships, and global economic forces channeled through local community networks.

This period established patterns that would define Muthoot Finance for decades: patient capital accumulation over generations, viewing financial services as social service, building on cultural insights rather than fighting them, creating formal structures for informal practices, and maintaining family control while professionalizing operations.

The transformation from grain trader to gold lender wasn't just a business pivot; it was recognition that in India's complex social economy, trust was the ultimate currency, and gold was its physical manifestation. By anchoring their business in gold, the Muthoots weren't just choosing collateral; they were aligning with five thousand years of Indian civilization that had always known gold's true value lay not in its price but in its meaning.

III. The Formal Beginning: Building the Gold Loan Machine (1971–1997)

The year 1971 marked a watershed moment in Muthoot's evolution. In 1971, the firm was renamed as Muthoot Bankers, and started to finance loans using gold jewellery as collateral. This wasn't just a name change but a fundamental business model transformation. India in 1971 was experiencing seismic shifts—the Bangladesh Liberation War, nationalization of banks, and Indira Gandhi's socialist policies that would culminate in the Emergency. In this environment of economic uncertainty and political upheaval, gold became even more precious, and access to credit even more critical.

The Indian economic context of the 1970s-1990s period created both challenges and opportunities. The License Raj—India's byzantine system of permits, regulations, and controls—made formal business expansion difficult but also created massive inefficiencies that nimble players could exploit. Banking was heavily regulated, with priority sector lending requirements, controlled interest rates, and limited rural penetration. Banks focused on large corporate clients and government securities, leaving vast swathes of the population underserved.

Into this void stepped Mathai George George Muthoot (2 November 1949 – 5 March 2021), whose first job was as an office assistant in the family's bank. In 1979, he became managing director of the bank. He was appointed chairman of Muthoot Group in February 1993. This third-generation scion brought a unique combination of traditional values and modern ambitions.

M.G. George Muthoot's background was distinctive. A graduate in Mechanical Engineering from Manipal Institute of Technology, attended various Executive Management Courses at the Harvard Business School. Working as an office assistant despite his engineering degree wasn't humiliation but education—understanding the business from the ground up, earning credibility with employees, and learning the nuances that textbooks couldn't teach.

At the time he took over the operations at Muthoot, the Group had 31 branches in four states, namely Kerala, Delhi, Chandigarh, and Haryana. This geographic spread was strategic—Kerala provided the home base and trust foundation, Delhi offered access to North Indian markets and regulatory corridors, while Chandigarh and Haryana represented affluent agricultural regions with significant gold holdings.

The company's formal incorporation came later. Company incorporated as private limited company on 14 March 1997 with name "The Muthoot Finance Private Limited"—a move that reflected the growing sophistication and scale of operations. This formalization wasn't abandoning tradition but institutionalizing it, creating structures that could outlast individuals while maintaining family control.

Building trust in gold lending required solving multiple challenges simultaneously. Security was paramount—branches needed vault-grade safes, armed guards, and insurance, all expensive investments that traditional pawnbrokers couldn't afford. Valuation expertise was critical—accurately assessing gold purity and weight required trained staff and testing equipment. Speed was essential—customers choosing gold loans over banks wanted immediate liquidity, not lengthy processing.

The Muthoot solution was elegant: standardize everything that could be standardized while personalizing everything that mattered to customers. Loan documentation was simplified to single-page agreements in local languages. Gold testing procedures were codified but performed in front of customers for transparency. Interest calculations were straightforward—no hidden charges or complex formulas. Repayment was flexible—pay interest monthly, quarterly, or at maturity.

The branch expansion strategy during this period followed a hub-and-spoke model. Major branches in district headquarters served as hubs, with smaller branches in surrounding towns as spokes. This allowed centralized gold storage and administration while maintaining local presence. Each branch was designed to feel both secure and welcoming—strong rooms visible to build confidence, but comfortable seating areas to reduce intimidation.

Technology adoption, though limited by the era's constraints, focused on practical improvements. Computerized accounting replaced manual ledgers, reducing errors and improving audit trails. Communication systems linked branches for fund transfers and rate updates. Training programs standardized procedures across locations. These weren't cutting-edge innovations but pragmatic improvements that enhanced reliability and scale.

The competitive landscape was fragmented and informal. Local pawnbrokers dominated most markets, operating on personal relationships and informal agreements. They offered convenience and discretion but also charged usurious rates and employed aggressive collection practices. Banks occasionally offered gold loans but treated them as secured personal loans with lengthy processing and extensive documentation. Other NBFCs existed but focused on vehicle or consumer finance, viewing gold loans as too operationally complex.

Muthoot's differentiation strategy centered on trust and transparency. Interest rates were clearly displayed, not negotiated in back rooms. Gold was weighed and tested in customer presence, not taken to back offices. Loan amounts were standardized by gold weight and purity, not adjusted by customer desperation. Default procedures were regulated and respectful, not arbitrary and aggressive. This approach attracted customers tired of exploitation but wary of formal banking.

The regulatory environment evolved significantly during this period. The Reserve Bank of India gradually recognized NBFCs as legitimate financial intermediaries, establishing prudential norms and capital requirements. This regulation, rather than constraining Muthoot, actually benefited them by creating entry barriers for informal operators and building customer confidence in regulated entities.

Cultural factors profoundly influenced business development. In India, gold isn't just an asset but an emotional repository—wedding gifts from parents, ancestral jewelry passed through generations, religious offerings accumulated over years. Pledging gold was psychologically different from selling it—temporary transfer versus permanent loss. Muthoot understood this psychology, marketing loans as "unlocking gold's value" rather than "pawning jewelry."

The agricultural cycle drove seasonal demand patterns. Farmers needed credit for sowing but had gold from previous harvests. Small traders required working capital for festival seasons. Families faced education expenses when academic years began. Medical emergencies arose unpredictably. Each scenario required different loan products, repayment schedules, and service approaches.

Risk management evolved through experience rather than models. Gold price volatility was managed through conservative loan-to-value ratios—typically 60-75% of gold value, providing cushion against price declines. Customer default risk was minimized through social pressure—defaulting on gold loans meant losing family jewelry, a powerful deterrent. Operational risk was controlled through standardized procedures and regular audits.

The family governance structure balanced continuity with competence. While leadership remained within the family, professional managers were recruited for specialized functions. Decision-making combined patriarchal authority with collective consultation. Succession planning began early, with next-generation members rotating through different functions before assuming leadership roles.

By 1997, when the company formally incorporated, Muthoot had established the foundational elements of its business model: trust-based brand recognition in core markets, operational procedures balancing efficiency with empathy, risk management through conservative practices rather than complex models, expansion capacity through proven replication strategies, and regulatory compliance as competitive advantage. The gold loan machine wasn't just built; it was refined, tested, and ready for massive scale.

The transformation from Muthoot Bankers to Muthoot Finance Private Limited represented more than corporate evolution—it marked the transition from family business to institution, from regional player to national ambition, from traditional practice to modern enterprise. Yet throughout this transformation, the core insight remained unchanged: in India, gold was more than metal, and lending against it was more than finance—it was facilitating dreams, enabling aspirations, and providing dignity in distress.

IV. The Transformation Years: From Regional to National Player (1997–2008)

The decade from 1997 to 2008 witnessed India's economic transformation and Muthoot Finance's parallel evolution from regional lender to national player. Post-liberalization India was experiencing unprecedented changes—GDP growth accelerating, middle class expanding, consumption patterns shifting, and financial needs multiplying. The IT boom created new wealth, telecom revolution connected markets, and retail explosion changed aspirations. In this dynamic environment, Muthoot recognized that their traditional model, while solid, needed scaling to capture emerging opportunities.

In 2001, the company was renamed to Muthoot Finance, dropping "Bankers" to reflect its identity as a specialized NBFC rather than a traditional banking institution. This rebranding wasn't cosmetic but strategic—positioning the company as a modern financial services provider while retaining its core gold loan expertise. The name change also coincided with systematic efforts to professionalize operations, standardize procedures, and prepare for exponential growth.

The competitive landscape was evolving rapidly. Local jewelers and pawnbrokers still dominated unorganized markets, but organized players were emerging. Manappuram Finance, founded in 1992, was expanding aggressively in South India. Banks like State Bank of India and Indian Bank began offering gold loans, leveraging their branch networks and deposit bases. New NBFCs entered the space, attracted by high margins and growing demand. The market was transitioning from fragmented to competitive, from relationship-based to service-differentiated.

Muthoot's expansion strategy during this period was methodical and market-tested. Rather than rushing nationwide, they followed migrant patterns and economic corridors. Kerala migrants in Gujarat became entry points to that market. Tamil Nadu's cultural similarity to Kerala eased expansion there. Karnataka's IT boom created new customer segments. Each new market was entered through careful study of local gold ownership patterns, competitive dynamics, and regulatory requirements.

Technology adoption accelerated significantly. While not at the cutting edge, Muthoot invested in practical systems that enhanced operational efficiency. Branch connectivity improved from dial-up to broadband, enabling real-time transaction updates. Centralized accounting systems replaced branch-level bookkeeping. SMS alerts kept customers informed about payment dates. These weren't innovations that made headlines but improvements that made differences.

In November 18, 2008, the company was converted into public limited company and the name was changed to Muthoot Finance Ltd. This conversion marked a crucial transition in corporate governance and growth ambitions. Becoming a public limited company meant enhanced disclosure requirements, professional board composition, and institutional scrutiny—disciplines that would prove invaluable for future capital raising and expansion.

The systematic building of trust extended beyond customer relationships to regulatory compliance. Muthoot Finance falls under the category of systematically important non-banking financial company(NBFC) of the RBI guidelines, a designation that brought both increased oversight and enhanced credibility. Meeting RBI's capital adequacy norms, maintaining asset quality standards, and ensuring transparent reporting became competitive advantages in a market where many operators remained informal.

Product innovation during this period focused on addressing specific customer pain points. Traditional gold loans required full interest payment upfront or monthly installments—challenging for customers with irregular income. Muthoot introduced flexible payment options: pay interest quarterly, accumulate it till loan closure, or choose partial payments. Loan tenures expanded from the traditional 3-6 months to 12 months, accommodating longer-term needs. Top-up loans allowed customers to borrow additional amounts against the same gold when prices appreciated.

The branch design philosophy evolved to balance security with accessibility. Strong rooms with transparent viewing panels showed gold was safely stored. CCTV systems provided surveillance while building customer confidence. Air-conditioned waiting areas made branches comfortable, not intimidating. Local language signage and documentation reduced literacy barriers. Female staff members made women customers—often the gold owners—feel secure. These design choices reflected deep understanding of customer psychology and cultural sensitivities.

Marketing strategies shifted from pure advertising to trust-building exercises. Sponsorships of local festivals and religious events built community connections. Financial literacy camps educated rural populations about formal credit. Transparent interest rate displays at branches eliminated negotiation anxiety. Customer testimonials in local newspapers provided social proof. The message was consistent: Muthoot was not just another lender but a community partner.

Risk management systems matured through experience and scale. Gold purity testing equipment upgraded from traditional touchstone methods to electronic karat meters. Valuation training ensured consistent assessment across branches. Vault management procedures standardized gold storage and retrieval. Audit systems caught discrepancies before they became problems. Insurance coverage protected against theft, fire, and natural disasters. These systems weren't glamorous but were fundamental to sustainable growth.

The human resource strategy recognized that in a high-touch service business, people were the ultimate differentiator. Recruitment focused on local hiring—branch staff who understood local languages, customs, and concerns. Training programs covered not just technical skills but soft skills—how to handle distressed customers, respect cultural sensitivities, and build relationships. Career progression paths retained talent and built institutional knowledge. Incentive structures balanced growth with quality, volume with compliance.

Geographic expansion accelerated but remained strategic. During the year 2008-09, the company opened 278 new branches across various states. Each new branch opening followed a careful process: market study identifying gold ownership patterns and competition, location selection prioritizing accessibility and visibility, staff recruitment emphasizing local knowledge and relationships, and soft launch periods testing operations before full-scale marketing.

The funding strategy diversified beyond traditional bank loans. Fixed deposits from retail investors provided stable, lower-cost funds. Commercial paper tapped money markets for short-term liquidity. Inter-corporate deposits leveraged corporate relationships. Bank consortiums spread risk and increased limits. This diversification reduced dependence on any single funding source while optimizing costs.

Partnership strategies extended reach without proportional investment. Tie-ups with post offices in rural areas provided collection points. Arrangements with cooperative banks offered referral channels. Associations with gold jewelers created customer acquisition pipelines. These partnerships leveraged existing infrastructure and relationships, accelerating market penetration while controlling costs.

The operational excellence achieved during this period created a replicable model. New branches could be profitable within 6-12 months. Customer acquisition costs remained low due to word-of-mouth marketing. Operating expenses as a percentage of assets under management declined with scale. Asset quality remained strong despite rapid growth. These metrics demonstrated that Muthoot had cracked the code for profitable, scalable growth.

By 2008, as global financial crisis erupted, Muthoot Finance was perfectly positioned. While traditional lenders retreated, gold loans became more attractive—countercyclical demand during economic uncertainty. While credit markets froze, gold provided instant liquidity. While asset values collapsed, gold retained worth. The very factors causing crisis elsewhere created opportunity for Muthoot.

The transformation from regional to national player wasn't just geographic expansion but fundamental evolution. Systems replaced relationships as the foundation for scale. Processes standardized what could be standardized while preserving personal touch where it mattered. Technology enhanced rather than replaced human interaction. Compliance became competitive advantage rather than regulatory burden. Brand building complemented branch building. The company that entered 1997 as a Kerala-centric traditional lender emerged in 2008 as a national financial services company ready for explosive growth.

This period established patterns that would define Muthoot's future: patient market entry followed by aggressive expansion, operational standardization enabling rapid replication, technology adoption focused on practical benefits, regulatory compliance as strategic differentiator, and cultural understanding as competitive moat. The foundation was set for the next phase—accessing institutional capital and going public.

V. The Scaling Era: Private Equity, IPO, and Explosive Growth (2008–2015)

The period from 2008 to 2015 marked Muthoot Finance's transformation from a large regional player to India's undisputed gold loan leader. This era began against the backdrop of the global financial crisis, which paradoxically created perfect conditions for gold loan expansion. As traditional credit dried up and economic uncertainty peaked, gold prices soared from $800 per ounce in 2008 to over $1,900 in 2011, making gold loans both more valuable and more necessary.

During the year 2009–10, the company added 620 new branches. This aggressive expansion—nearly two branches per day—represented one of the fastest retail financial services rollouts in Indian history. Each branch opening was a calculated bet that local demand would justify investment, and the bet consistently paid off. The branch network became Muthoot's primary competitive moat, creating density that competitors couldn't match and customer convenience that digital platforms couldn't replicate.

The institutional capital infusion marked a turning point. In 2010, Muthoot Finance sold 4% of its shares in a private equity round to Barings Bank and Matrix Partners, raising ₹157 crore. This wasn't just about money—it was validation from sophisticated global investors that the gold loan model was scalable and sustainable. The PE investors brought governance improvements, strategic insights, and credibility that would prove invaluable for the upcoming IPO.

Muthoot Finance IPO opens on April 18, 2011, and closes on April 21, 2011. Muthoot Finance IPO is a main-board IPO of 5,15,00,000 equity shares of the face value of ₹10 aggregating up to ₹901.25 Crores. The issue is priced at ₹175 per share. The IPO timing was perfect—gold prices were near historic highs, the Indian economy was recovering strongly from the global crisis, and investor appetite for financial services stocks was robust.

Muthoot Finance IPO was subscribed 24.55 times. This overwhelming response validated the market's confidence in the gold loan model and Muthoot's execution capabilities. The shares got listed on BSE, NSE on May 6, 2011. The successful listing provided not just capital but also liquidity for early investors, currency for acquisitions, and enhanced brand visibility.

The post-IPO period witnessed explosive growth across all metrics. In 2011, the company's retail loan portfolio crossed Rs 15800 crore, retail debenture portfolio crossed Rs 3900 crore, net owned funds crossed Rs 1300 crore, gross annual income crossed Rs 2300 crore, bank credit limit crossed Rs 6000 crore and branch network crossed 2,700 branches. These numbers represented not just scale but market dominance—Muthoot was becoming synonymous with gold loans in India.

The competitive landscape intensified dramatically during this period. Banks, seeing Muthoot's success, aggressively entered gold loans. State Bank of India launched dedicated gold loan counters. HDFC Bank and ICICI Bank offered competitive rates. Regional players like Manappuram Finance went public and expanded nationally. New entrants like Sapna Corporation and Shriram City Union Finance entered the market. The gold loan industry transformed from Muthoot's near-monopoly to intense competition.

Muthoot's response to competition was multifaceted. Rather than engage in rate wars, they focused on service differentiation. Loan disbursement time reduced from hours to minutes. Documentation simplified to single-page agreements. Customer service emphasized respect and empathy—crucial when dealing with distressed borrowers. Branch staff trained to handle emotional situations with sensitivity. The message was clear: Muthoot offered not just loans but dignity.

Marketing innovation during this period broke traditional financial services advertising molds. The partnership with Delhi Daredevils IPL team from 2011-2013 brought unprecedented visibility. TV commercials featuring Bollywood celebrities normalized gold loans, removing stigma. Regional language advertising connected with local audiences. The tagline "Muthoot Finance—the name you can trust" emphasized reliability over rates.

Product innovation accelerated to serve diverse customer needs. Online gold loans allowed digital-savvy customers to apply remotely. Gold loan ATM cards enabled withdrawal flexibility. Overdraft facilities against gold provided revolving credit. Business loans against gold served SME needs. Each product addressed specific pain points while maintaining operational simplicity.

Technology transformation, while not visible to customers, revolutionized backend operations. Core banking systems integrated all branches. Risk management systems monitored portfolio quality real-time. Treasury management optimized funding costs. Audit systems ensured compliance across thousands of branches. Mobile apps enabled field staff to originate loans remotely. These investments created scalability that manual processes couldn't achieve.

The regulatory environment evolved significantly during this period. RBI introduced specific regulations for gold loan NBFCs, including LTV ratio caps, standardized valuation procedures, and enhanced disclosure requirements. Rather than viewing these as constraints, Muthoot embraced regulation as competitive advantage. Compliance became a differentiator from unorganized players and smaller NBFCs struggling with regulatory requirements.

Risk management sophistication increased with scale. As of 2009, it was the largest non-banking financial company issuing gold-backed loans. Portfolio diversification across geographies reduced concentration risk. Dynamic LTV adjustments responded to gold price volatility. Auction management systems optimized recovery from defaults. Insurance coverage protected against operational risks. Stress testing prepared for adverse scenarios.

The funding strategy evolved from bank-dependent to market-diversified. During the year, the company raised Rs 693 crore through Non-convertible Debenture Public Issue- Series I and Rs 459 crore through Non-convertible Debenture Public Issue - Series II. Public NCDs tapped retail savings. Commercial paper accessed money markets. External commercial borrowings leveraged international rate differentials. This diversification reduced cost of funds while ensuring liquidity.

Geographic expansion followed economic opportunity. During the year 2008-09, the company opened 278 new branches across various states. Urban branches captured salaried class needs. Rural branches served agricultural communities. Semi-urban branches bridged both segments. Each geography required different approaches—urban branches emphasized speed and privacy, rural branches focused on trust and relationships.

Human capital became increasingly critical with scale. Employee count grew from hundreds to tens of thousands. Training infrastructure expanded to handle continuous recruitment. Career development programs retained talent. Performance management systems aligned incentives with company goals. Cultural integration ensured Muthoot values permeated despite rapid growth.

The customer base evolution reflected India's changing economy. The target market of Muthoot Finance includes small businesses, vendors, farmers, traders, SME business owners, and salaried individuals. Small business owners used gold loans for working capital. Farmers bridged crop cycles with gold financing. Salaried individuals managed emergencies without disturbing investments. Students funded education without education loans' complexity. Each segment valued different aspects—farmers wanted flexibility, businesses needed speed, salaried sought privacy.

Operational metrics during this period demonstrated exceptional execution. Customer acquisition cost remained below industry average despite intense competition. Operating expense ratios declined with scale. Asset quality stayed robust despite rapid growth. Branch productivity improved despite increasing branch count. These metrics proved that Muthoot's model wasn't just growing but improving with scale.

The international expansion began during this period. Outside India, Muthoot Finance is established in the UK, the US, and the United Arab Emirates. These weren't random choices but strategic entries into NRI concentrations. UK operations served the large Kerala diaspora. UAE presence captured Gulf remittance flows. US operations targeted high-net-worth Indian immigrants. Each market offered learning that enhanced domestic operations.

Strategic partnerships extended capabilities without capital investment. Money transfer tie-ups with Western Union leveraged branch network. Insurance distribution through branches monetized customer relationships. Forex services captured international transaction needs. Gold coin sales utilized branch infrastructure. Each partnership created value from existing assets.

By 2015, Muthoot Finance had transformed from a traditional NBFC to a financial services powerhouse. In 2012, Muthoot Finance's retail Loan portfolio crossed Rs 24600 crore, retail debenture portfolio crossed Rs 6600 crore, net owned funds crossed Rs 2900 crore, gross annual income crossed Rs 4500 crore, bank credit limit crossed Rs 9200 crore and branch network crossed 3,600 branches. The company that had started the period with hundreds of branches now operated thousands. The family business had become a professionally managed public company. The regional player had achieved national dominance.

This period established Muthoot's position as India's gold loan leader—a position it would maintain despite intense competition. The combination of first-mover advantage, execution excellence, and strategic capital access created a competitive moat that proved remarkably durable. The foundation was set for the next phase of growth—consolidation, digital transformation, and category leadership.

VI. Modern Muthoot: Consolidation and Dominance (2015–Present)

The period from 2015 to present represents Muthoot Finance's evolution from market leader to dominant institution, a transformation marked by operational excellence, strategic acquisitions, and digital innovation while maintaining the core gold loan focus that built the empire. It operates 4,800+ branches across 29 States and Union territories. It holds 202 tons of gold jewelry as security and services 2+ lakh customers daily.

The scale achieved is staggering by any measure. Market capitalization stands at ₹1,05,771 Crore, with revenue jumping 35.89% year-over-year to ₹5,221.69Cr in Q3 2024-2025. Net profit jumped 25.89% year-over-year to ₹1,389.18Cr in the same period, demonstrating not just growth but profitable expansion.

The modern era began with strategic acquisitions that expanded capabilities beyond organic growth. In 2014, Muthoot Finance acquired a majority stake in Asia Asset Finance plc, a Sri Lankan publicly listed financial services company, marking international expansion through acquisition rather than greenfield operations. In July 2016, Muthoot Finance acquired 46.83% of the capital of Belstar Investment and Finance Private Limited (BIFPL), entering the microfinance segment. In May 2018, Muthoot Finance acquired Muthoot Money, a Non Deposit taking Non-Banking Financial Company, strengthening vehicle finance capabilities.

The operational metrics reveal extraordinary efficiency at scale. The company reached an all-time high in its gold loan AUM, which hit ₹1,02,956 crore, reflecting a 41% increase compared to the previous year. The rise in AUM is primarily driven by robust gold loan growth, which continues to be the backbone of Muthoot Finance's business. This growth isn't just about more branches or customers but deeper penetration and higher ticket sizes.

Digital transformation, long overdue in the gold loan industry, accelerated dramatically. The company launched online gold loan platforms enabling customers to apply remotely, receive doorstep service, and manage loans through mobile apps. The Gold Loan@Home service, introduced during COVID-19, revolutionized service delivery—customers could get loans without visiting branches, with gold valuation and documentation completed at their doorstep. This wasn't just convenience but a fundamental reimagination of the gold loan process.

The pandemic period of 2020-2021 proved transformative rather than disruptive. While other lenders struggled with lockdowns and moratoriums, gold loans proved resilient. Customers needed emergency liquidity, gold prices soared providing collateral cushion, and Muthoot's branch network provided essential service status. The company emerged from the pandemic stronger, with market share gains and enhanced digital capabilities.

Leadership transition following M.G. George Muthoot's passing in March 2021 tested institutional resilience. The smooth succession to fourth-generation leadership demonstrated that Muthoot had evolved beyond founder dependence. Professional management structures, institutionalized processes, and distributed decision-making ensured continuity. The family maintained strategic control while empowering professional management for operational execution.

Geographic consolidation accompanied expansion. Rather than pure branch addition, the focus shifted to network optimization—closing underperforming locations, upgrading successful branches, and deepening presence in high-potential markets. Urban branches evolved into relationship centers offering multiple products. Rural branches maintained transaction focus with simplified operations. Semi-urban locations bridged both models.

Product diversification accelerated while maintaining gold loan centrality. The Company offers a range of other products and services including foreign inward money transfer services, domestic money transfer services, instant money transfer services, microfinance, non-convertible debentures, home loans, personal loans, corporate loans, foreign exchange services and insurance services. Each product leveraged existing customer relationships and branch infrastructure, creating revenue synergies without operational complexity.

The competitive landscape evolved significantly with new challenges and opportunities. Banks intensified gold loan focus with competitive pricing. Fintech startups offered digital-first gold loans. Regional players consolidated through mergers. Yet Muthoot maintained leadership through brand strength, network density, and operational excellence. The moat wasn't just first-mover advantage but continuous innovation and execution superiority.

Risk management sophistication increased with regulatory evolution. RBI's guidelines on gold loan NBFCs became more stringent—LTV ratio caps, auction procedures, and capital requirements. Muthoot's proactive compliance and conservative practices meant regulatory changes often validated existing practices rather than forcing changes. The company's AA rating from CRISIL and ICRA reflected this prudent approach.

Technology infrastructure underwent complete transformation. Core banking systems upgraded to handle millions of daily transactions. Data analytics identified customer patterns and credit risks. Artificial intelligence enhanced gold valuation accuracy. Blockchain experiments explored gold loan securitization. Cloud infrastructure ensured scalability and resilience. These weren't headline-grabbing innovations but fundamental capability enhancements.

Customer service evolution reflected changing expectations. Muthoot Finance disbursed ₹21,888 crore in gold loans to nearly 18 lakh new customers during FY25, marking another record high for the company. The growth in both loan disbursements and new customers is a testament to the company's strong market presence. Multilingual call centers provided 24/7 support. WhatsApp banking enabled account management. Video KYC reduced documentation requirements. Instant loan renewals eliminated branch visits. Each innovation addressed specific friction points in the customer journey.

Financial performance reached new heights consistently. For the full financial year 2024-25 (FY25), Muthoot Finance reported a 20% increase in its consolidated PAT, reaching ₹5,352 crore, compared to ₹4,468 crore in FY24. The standalone PAT for the year was ₹5,201 crore, marking a 28% YoY growth from ₹4,050 crore in FY24. These weren't just good numbers but industry-leading metrics demonstrating sustainable competitive advantages.

The brand evolution from functional to emotional resonance marked maturation. Most Trusted Financial Services Brand, according to the Brand Trust Report 2019, 2018, 2017 & 2016 consecutively. Marketing moved beyond product features to life moments—funding dreams, enabling aspirations, providing dignity in distress. Celebrity endorsements gave way to customer stories. National campaigns complemented local engagement.

International operations expanded strategically rather than opportunistically. UK operations served the diaspora with culturally relevant services. UAE presence captured remittance flows and NRI investments. US operations targeted high-net-worth immigrants. Each market provided learning—regulatory compliance, customer preferences, operational practices—that enhanced domestic capabilities.

The social impact dimension gained prominence. All philanthropic activities are conducted through the Muthoot M George Foundation, which conducts tree plantation drives and offers scholarships. The company is involved in various philanthropic initiatives focusing on education, environment, health, financial assistance and eco-friendliness. Financial inclusion wasn't just business but mission—serving customers banks wouldn't, providing credit where none existed, enabling economic participation for the marginalized.

Capital market recognition validated the business model. Muthoot Finance has crossed the ₹1 lakh crore market capitalization milestone, becoming the first listed company from Kerala to do so. ICICI Securities projected a target price of ₹2,670. Institutional investors increased stakes. Index inclusions brought passive flows. Rating upgrades reduced funding costs. Each validation reinforced market leadership.

Regulatory challenges emerged as the sector matured. Muthoot Finance's stock price fell 5% amid concerns about the Reserve Bank of India's draft loan-to-value guidelines. The new draft guidelines could potentially restrict the maximum loan amount that can be disbursed against gold. Yet these challenges also created opportunities—weaker players exited, compliance costs created entry barriers, and regulatory clarity attracted institutional capital.

Operational excellence metrics demonstrated world-class execution. Average loan processing time reduced to 30 minutes. Customer acquisition costs remained industry-lowest. Branch productivity increased despite rising branch count. Employee productivity improved through training and technology. Asset quality remained robust despite rapid growth. These operational advantages created sustainable competitive moats.

The dividend policy reflected confidence and shareholder focus. Muthoot Finance declared its highest-ever dividend of ₹26 per equity share, representing 260% on the face value of ₹10 per share. This is a significant reward for the company's shareholders, reflecting strong earnings and cash flow. Consistent dividend payments, even during challenging periods, built investor trust and attracted long-term capital.

Future readiness initiatives positioned for next-generation growth. Digital gold loans targeted millennials comfortable with online transactions. Paperless branches reduced environmental impact and operational costs. API partnerships enabled embedded finance opportunities. Data analytics identified cross-selling opportunities. Innovation labs explored blockchain and AI applications. Each initiative balanced current performance with future preparation.

Strategic priorities crystallized around sustainable leadership. Market share protection through service excellence rather than price competition. Geographic deepening in existing markets rather than new market entry. Product expansion leveraging existing capabilities rather than unrelated diversification. Digital enhancement complementing rather than replacing physical presence. Regulatory compliance as competitive advantage rather than cost burden.

The transformation from 2015 to present established Muthoot Finance as more than a gold loan company—it became a financial institution integral to India's economic fabric. The company that began as a family business in rural Kerala now stands as a systematically important financial institution, a transformation achieved through vision, execution, and unwavering focus on customer needs. The foundation is set for the next phase—navigating digital disruption, regulatory evolution, and competitive intensification while maintaining the trust and service excellence that built the empire.

VII. The Gold Loan Business Model Deep Dive

The gold loan business model represents one of the most elegant solutions to financial inclusion ever developed, combining ancient cultural practices with modern financial engineering. At its core, the model is deceptively simple: customers pledge gold jewelry as collateral, receive instant cash, pay interest, and reclaim their gold upon repayment. Yet beneath this simplicity lies sophisticated operations, nuanced risk management, and deep cultural understanding that separates successful operators from failures.

The mechanics begin with valuation, the critical first step that determines everything else. When a customer walks into a Muthoot branch with gold jewelry, trained assessors examine the gold using multiple methods. Traditional touchstone testing provides initial assessment, while electronic karat meters confirm purity. Weight measurement uses precision scales accurate to 0.01 grams. The entire process happens in front of customers, building trust through transparency. Valuation typically takes 10-15 minutes, with assessors checking for stones, calculating net gold weight, and determining current market value.

Loan-to-value (LTV) ratios represent the primary risk management tool. RBI regulations cap LTV at 75%, meaning customers can borrow maximum 75% of their gold's market value. Muthoot typically operates at 60-70% LTV, providing cushion against price volatility. This conservative approach means that even if gold prices fall 25-30%, the loan remains fully secured. The LTV ratio balances customer needs—maximizing loan amount—with lender security—ensuring adequate collateral coverage.

Interest rate structures reflect market dynamics and customer segments. Rates typically range from 12-24% annually, varying by loan amount, tenure, and customer profile. Smaller loans carry higher rates due to fixed processing costs. Longer tenures command higher rates reflecting increased risk. Regular customers receive preferential pricing. Agricultural loans, backed by government schemes, offer subsidized rates. The pricing matrix balances profitability with affordability, recognizing that customers choose gold loans for convenience, not necessarily lowest cost.

The customer journey demonstrates operational excellence. A typical customer—let's call her Lakshmi, a small shopkeeper needing working capital—enters a branch with her wedding jewelry. After brief documentation (ID proof and address proof), her gold is assessed. Within 15 minutes, she knows the exact loan amount available. If she agrees, the gold is sealed in tamper-proof packets with detailed description, weighed again, and stored in strong rooms. Cash is disbursed immediately or transferred to her bank account. The entire process, from entry to exit, takes 30-45 minutes—faster than ATM visits to many banks.

Customer segments reveal gold loans' versatility. Farmers constitute 30-35% of customers, using gold loans to bridge crop cycles—borrowing for sowing, repaying after harvest. Small businesses represent 25-30%, managing working capital needs—inventory purchase, payment delays, seasonal fluctuations. Salaried individuals form 20-25%, handling emergencies—medical expenses, education fees, family obligations. Self-employed professionals comprise 15-20%, managing cash flow—project delays, client payments, business investments. Each segment values different aspects: farmers want flexibility, businesses need speed, salaried seek privacy, self-employed require higher amounts.

The trust equation transcends mere transaction. Customers aren't just pledging gold; they're entrusting family heritage, emotional memories, and social status. Wedding jewelry carries blessings from parents. Ancestral ornaments connect generations. Festival gifts embody relationships. This emotional weight means customers will do everything possible to redeem their gold, making default rates remarkably low—typically 1-2% versus 3-5% for other secured loans and 5-10% for unsecured loans.

Operational excellence differentiates leaders from laggards. Branch location strategies prioritize accessibility—ground floor locations, parking availability, proximity to markets. Staff training emphasizes soft skills—empathy for distressed customers, respect for elderly clients, patience with first-time borrowers. Security measures balance protection with convenience—visible strong rooms build confidence, but excessive security intimidates customers. Technology adoption enhances rather than replaces human interaction—tablets speed documentation, but staff explain every step.

Risk management in gold loans differs fundamentally from other lending. Credit risk is minimal due to collateral coverage, but operational risks are significant. Physical security requires sophisticated systems—vaults, alarms, guards, insurance. Gold purity assessment needs expertise—fake gold detection, stone weight calculation, making charges evaluation. Price risk management uses dynamic LTV adjustments—reducing ratios when prices spike, increasing when stable. Fraud prevention requires multiple checks—customer identity verification, gold ownership confirmation, duplicate loan prevention.

The unit economics reveal why gold loans are highly profitable. Customer acquisition costs are minimal—walk-in customers, word-of-mouth marketing, repeat business. Processing costs are low—simplified documentation, quick turnaround, standardized procedures. Default losses are negligible—full collateral coverage, customer motivation to redeem, easy liquidation. Funding costs are competitive—secured lending status, high asset quality, regulatory comfort. Operating leverage improves with scale—fixed branch costs, technology investments, training infrastructure.

Regulatory evolution shaped industry development. Initial years saw minimal regulation, allowing rapid growth but also excesses. RBI's 2012 interventions—LTV caps, auction procedures, capital requirements—created a level playing field. Subsequent refinements—priority sector classification, interest rate guidelines, fair practice codes—balanced growth with consumer protection. Current regulations—digital lending norms, data protection requirements, grievance redressal mechanisms—modernize while maintaining stability.

The auction process for unredeemed gold demonstrates operational complexity. After loan tenure expires, lenders provide notice periods—typically 3-6 months—for redemption. If unclaimed, gold enters auction process—public notices, reserve price determination, bidder registration. Auctions must be transparent—multiple bidders, price discovery, documentation. Surplus amounts (auction price minus loan outstanding) must be returned to customers. The entire process requires careful management—regulatory compliance, customer communication, reputation protection.

Competitive dynamics evolved from local to national. Traditional pawnbrokers operate on relationships—knowing customers personally, flexible terms, informal processes—but charge usurious rates and employ aggressive collection. Banks offer lower rates and regulatory safety but involve lengthy processes, extensive documentation, and limited flexibility. Other NBFCs provide comparable service but lack Muthoot's network density and brand trust. Fintech players promise convenience but struggle with physical gold handling and rural penetration.

Innovation opportunities exist despite model maturity. Digital gold loans eliminate branch visits—doorstep collection, online valuation, instant disbursement. Gold loan cards provide ATM access—withdraw within limits, pay interest only on utilized amount. Micro gold loans serve bottom-of-pyramid—loans against 1-2 grams, daily interest options. Gold accumulation products combine saving with borrowing—systematic gold purchase, loan eligibility creation. Each innovation expands addressable market while maintaining core model integrity.

Cultural factors profoundly influence business dynamics. Regional variations affect gold ownership—South India has highest per capita gold, cultural acceptance of pledging. Religious considerations impact operations—auspicious days see higher redemptions, festival seasons drive demand. Gender dynamics shape service delivery—women own most gold but men often negotiate loans, requiring sensitive handling. Generational differences emerge—older customers prefer physical branches, younger seek digital options. Understanding these nuances separates successful operators from failures.

The multiplier effects extend beyond direct lending. Gold loans enable economic activity—small businesses maintain operations, farmers continue cultivation, families avoid distress sales. Financial inclusion advances—unbanked populations access formal credit, credit histories get created, financial literacy improves. Gold becomes productive—idle assets generate returns, wealth gets unlocked without sale, economic circulation increases. Social impacts manifest—dignity in financial distress, avoiding predatory lending, maintaining social status.

Technology transformation enhances rather than disrupts the model. Blockchain could enable gold tokenization—fractional ownership, easier transfer, transparent records. Artificial intelligence improves risk assessment—pattern recognition, fraud detection, price prediction. IoT sensors enhance security—real-time monitoring, automated alerts, tamper detection. Mobile apps democratize access—loan applications, payment reminders, account management. Yet technology supplements rather than supplants human elements—trust, empathy, and cultural understanding.

Future evolution will balance tradition with innovation. The fundamental model—lending against gold—remains robust because it solves real problems with elegant simplicity. Cultural attachment to gold ensures continued relevance. Regulatory framework provides stability. Operational excellence creates competitive advantages. Brand trust builds customer loyalty. Network effects strengthen with scale. The gold loan business model, perfected over decades, stands as testament to the power of understanding local needs, respecting cultural values, and executing with excellence.

VIII. Financial Inclusion & Social Impact

Muthoot Finance Ltd (MFL): The company is India's largest gold financing company in terms of loan portfolio, but its true significance extends far beyond market leadership into fundamental transformation of India's financial landscape. The company has served as a bridge between India's vast informal economy and formal financial system, bringing banking to the unbanked and credit to the creditless.

The scale of financial exclusion Muthoot addresses is staggering. Despite India's economic growth, nearly 190 million adults remain unbanked, with millions more underbanked—having accounts but no access to credit. Traditional banks find serving these populations unprofitable due to small ticket sizes, documentation challenges, and operational costs. Into this gap stepped Muthoot, recognizing that the poor aren't unbankable; they're just differently bankable.

The gold holdings among Indian households represent one of the world's largest private reserves. The total gold holdings among individuals is estimated to be more than 20,000 tonnes, worth approximately $1.5 trillion at current prices. Most of this gold sits idle in lockers and safes, representing dead capital in economic terms. Muthoot's innovation wasn't creating new wealth but unlocking existing wealth, transforming static assets into dynamic capital.

Rural penetration demonstrates commitment to inclusive growth. It operates 4,800+ branches across 29 States and Union territories, with 60% located in Tier III to Tier VI cities and rural areas. These aren't token presences but full-service branches offering the same products as urban locations. Each rural branch represents significant investment—infrastructure, staff, security—in markets where returns are lower but social impact higher.

The customer profile reveals the depth of inclusion achieved. It holds 202 tons of gold jewelry as security and services 2+ lakh customers daily. Agricultural workers use gold loans for crop inputs, avoiding middleman exploitation. Micro-entrepreneurs access working capital without collateral requirements. Daily wage earners manage income volatility through credit access. Students fund education without complex education loans. Each transaction represents not just financial service but economic empowerment.

Women's financial inclusion deserves special attention. In Indian households, women traditionally own and control gold jewelry—received during marriage, inherited from mothers, accumulated during festivals. Yet they often lack independent income or formal credit access. Gold loans provide agency—accessing credit without husband's permission, managing household finances independently, starting small businesses. Muthoot's branches report 35-40% women customers, significantly higher than traditional banking.

The speed of service transforms emergency management for vulnerable populations. Medical emergencies don't wait for loan processing. School fees have deadline pressures. Business opportunities require immediate capital. Traditional loans taking weeks force distress decisions—selling assets below value, borrowing from moneylenders at usurious rates, missing opportunities. Muthoot's 30-minute disbursement isn't just convenience but crisis prevention.

Interest rate rationalization brought transparency to opaque markets. Before organized gold loans, local pawnbrokers charged 36-60% annually, often with hidden charges and arbitrary terms. Muthoot's transparent pricing—clearly displayed rates, no hidden fees, standardized terms—forced market discipline. Even those who don't borrow from Muthoot benefit from competitive pressure on informal lenders.

The agricultural impact merits detailed examination. Indian farmers face unique challenges—seasonal income, weather dependence, price volatility. Traditional crop loans require land documentation, often unavailable for tenant farmers. Gold loans provide alternative—using wife's jewelry for seeds, repaying after harvest. This flexibility prevented countless farmer suicides, enabling continuation during crisis periods.

Small business facilitation drives economic multiplication. A vegetable vendor borrowing ₹10,000 against gold maintains inventory, earning ₹500 daily profit. A tailor accessing ₹25,000 purchases sewing machine, doubling income. A tea shop owner managing ₹50,000 working capital employs two helpers. Each loan enables economic activity far exceeding the principal amount, creating employment and value chains.

Educational access expansion changes generational trajectories. Engineering admission requires immediate payment, but education loans take weeks. Medical seat donations demand lump sums. Coaching class fees need upfront payment. Gold loans bridge these gaps, enabling education access that transforms family futures. Muthoot branches near educational institutions report 20-25% loans for education purposes during admission seasons.

The microfinance complementarity deserves recognition. Muthoot's microfinance operations through acquired subsidiaries serve different needs—group lending for income generation, individual loans for consumption smoothing. Combined with gold loans, this creates comprehensive financial inclusion—multiple products for different needs, graduated credit access, and financial literacy development.

Healthcare financing represents critical social service. Medical emergencies are leading causes of poverty—pushing families into debt traps. Insurance coverage remains limited. Government schemes have gaps. Gold loans provide immediate liquidity for treatment, preventing delayed care that worsens outcomes. Branches near major hospitals process dozens of medical emergency loans daily.

CSR initiatives extend impact beyond lending. All philanthropic activities are conducted through the Muthoot M George Foundation, which conducts tree plantation drives and offers scholarships. The company is involved in various philanthropic initiatives focusing on education, environment, health, financial assistance and eco-friendliness. Free medical camps serve thousands annually. Scholarship programs enable higher education. Skill development initiatives create employment. Environmental programs promote sustainability.

The dignified lending approach transforms borrower experience. Traditional money lending involved humiliation—public negotiations, aggressive collection, social shaming. Bank lending required multiple visits, complex documentation, and often bribes. Muthoot's professional service—respectful treatment, private transactions, transparent processes—provides dignity in distress, crucial for psychological well-being beyond financial relief.

Economic formalization benefits extend beyond direct impact. Gold loan customers create formal credit histories, enabling future bank access. GST registration for business loans brings enterprises into tax net. Digital payments for disbursements promote cashless transactions. KYC documentation creates identity verification. Each element contributes to broader economic formalization.

Crisis response capability proved invaluable during disruptions. During demonetization, gold loans provided liquidity when cash vanished. During COVID-19 lockdowns, doorstep service maintained credit access. During floods and cyclones, quick disbursements enabled recovery. This resilience makes Muthoot critical infrastructure for vulnerable populations facing shocks.

The behavioral impact influences financial habits. Regular repayment builds financial discipline. Interest payment requirements encourage income planning. Gold's emotional value prevents reckless borrowing. Formal sector exposure reduces informal dependence. These behavioral changes create long-term benefits beyond immediate credit access.

Regional development contributions matter significantly. Branches in backward districts provide formal employment—managers, assessors, security staff. Local procurement supports small businesses—stationery, maintenance, services. Tax payments fund government services. Property rentals generate income. Each branch becomes economic nucleus, catalyzing local development.

Innovation in inclusion continues evolving. Vernacular language interfaces reduce literacy barriers. Video KYC enables remote onboarding. WhatsApp banking provides accessible channels. Voice-based authentication serves illiterate customers. Biometric systems prevent identity fraud. Each innovation expands inclusion boundaries.

The competitive effects benefit entire markets. Muthoot's success attracted competitors, expanding access. Service standards forced improvements across the industry. Regulatory attention enhanced consumer protection. Media coverage reduced stigma. Market development benefited all participants, including customers.

Partnership models amplify impact. Collaborations with post offices extend rural reach. Bank correspondents provide last-mile connectivity. NGO partnerships identify vulnerable beneficiaries. Government schemes provide subsidized credit. Technology partners enable digital access. Each partnership multiplies inclusion effectiveness.

Gender impact deserves special recognition. Women entrepreneurs access startup capital. Female farmers manage agricultural operations independently. Mothers fund children's education without dependence. Daughters support parental medical needs. Wives manage household finances autonomously. Gold loans provide financial agency previously denied.

The trust building in formal systems has generational implications. Positive experiences with Muthoot encourage formal sector engagement. Children observe parents using banking services. Communities share success stories. Trust spreads through social networks. This cultural shift toward formal finance transforms economic participation.

Future inclusion initiatives show continued commitment. Financial literacy programs educate on credit management. Entrepreneur development schemes build business skills. Digital literacy initiatives bridge technology gaps. Health insurance products provide risk protection. Pension schemes enable retirement planning. Each initiative deepens inclusion beyond basic credit.

The measurement of social impact reveals impressive achievements. Over 70 crore customers served (including repeat customers) represents massive reach. Average ticket size of ₹30,000-50,000 indicates bottom-of-pyramid focus. Repeat customer rates exceeding 60% demonstrate value creation. Low default rates under 2% indicate responsible lending. These metrics quantify but don't fully capture transformation achieved.

Muthoot Finance's role in financial inclusion represents more than business success—it's social transformation at scale. By recognizing that the poor need credit not charity, that gold represents opportunity not just ornament, and that dignity matters as much as money, Muthoot created a model that serves shareholders while transforming society. This alignment of profit with purpose, scale with service, represents the highest achievement in social enterprise.

IX. Playbook: Key Business Lessons

The Muthoot Finance story offers a masterclass in building enduring businesses in emerging markets, providing lessons that transcend industries and geographies. These aren't theoretical frameworks but battle-tested strategies proven over 137 years and validated through multiple economic cycles, regulatory changes, and competitive challenges.

Building Trust in Financial Services: The Muthoot Approach

Trust in financial services isn't built through advertising but through consistent execution over generations. Muthoot understood that in markets where formal institutions had failed communities repeatedly, trust required patient cultivation. Every transaction became trust-building opportunity—transparent gold valuation, immediate cash disbursement, respectful treatment during distress, and fair auction processes. The company invested in physical infrastructure (strong rooms visible to customers) and human infrastructure (local staff speaking local languages) that signaled permanence and commitment. Trust compounds like interest—slowly initially, then exponentially.

Network Effects in Physical Retail: Branch Density Advantages

While digital platforms celebrate network effects, Muthoot demonstrated physical network effects through branch density. Each new branch in a district enhanced existing branches' value—customers could borrow at one branch and repay at another, word-of-mouth marketing intensified with visibility, and operational costs per branch declined with regional scale. The company achieved critical mass district by district rather than spreading thin nationally, creating local monopolies that competitors couldn't challenge economically. This density strategy created switching costs—customers stayed with Muthoot not just for service but for convenience of accessing any nearby branch.

Regulatory Navigation: Working with RBI, Managing Compliance

Muthoot's regulatory strategy transformed potential constraints into competitive advantages. Rather than resisting regulation, the company actively engaged with RBI, often implementing best practices before mandation. When RBI introduced gold loan NBFC regulations, Muthoot's existing practices largely exceeded requirements, while competitors scrambled to comply. The company maintained dedicated compliance teams, invested in systems before deadlines, and built reputation as responsible operator. This proactive approach earned regulatory goodwill, enabling favorable treatment during crisis periods and influence in policy formation.

Family Business Governance: Managing Succession, Professionalizing Operations

The transition from family business to professional organization while maintaining family control represents delicate balance. Muthoot achieved this through structured evolution—family members gained external education and experience before joining, professional managers handled operational functions while family retained strategic control, and independent directors provided governance oversight. Succession planning began decades before transition, with next-generation members rotating through functions, earning credibility through performance, and understanding business from ground up. The family's commitment to institution over individual prevented destructive succession battles that destroyed many Indian family businesses.

Cultural Arbitrage: Understanding Indian Gold Psychology

Muthoot's deepest insight was recognizing that gold in India isn't commodity but culture. The company understood emotional attachments—gold represents mother's love, family heritage, and social status. This cultural intelligence informed every decision: branches designed like jewelry stores not banks, marketing emphasizing preservation not sale, and products structured around cultural events (wedding seasons, festivals, harvests). While competitors saw gold as collateral, Muthoot saw it as relationship anchor. This cultural arbitrage—profiting from deep cultural understanding—created competitive advantages no amount of capital could replicate.

Speed as Competitive Advantage: Quick Disbursals vs Traditional Banking

In financial services, speed isn't just convenience but competitive moat. Muthoot weaponized speed—reducing loan processing from days to minutes, documentation from files to pages, and decisions from committees to individuals. This speed required operational excellence: standardized processes eliminating variations, delegated authority preventing bottlenecks, technology infrastructure enabling instant verification, and trained staff making rapid assessments. Speed became brand promise—customers chose Muthoot not for lowest rates but fastest service. Traditional banks couldn't match this speed without fundamental restructuring, creating sustainable differentiation.

Brand Building in Commoditized Markets: Trust and Service Differentiation

Gold loans are ultimately commoditized—gold is gold, money is money. Yet Muthoot built powerful brand in this commodity business through service differentiation. The brand didn't promise lowest rates but best experience—dignified treatment during distress, transparent processes eliminating surprises, convenient locations reducing travel, and flexible products accommodating needs. Brand building required consistency—every branch delivering same experience, every customer receiving same respect. Marketing reinforced rather than created brand—communicating existing strengths rather than manufacturing new positioning.

Physical Infrastructure as Moat: Branch Networks in Digital Age

While fintech celebrates asset-light models, Muthoot proved physical infrastructure remains powerful moat. Branches aren't just transaction points but trust anchors—customers see their gold stored safely, meet staff who become familiar faces, and access services beyond loans. The branch network created barriers competitors couldn't overcome—replicating 4,800 branches requires billions in capital, years of execution, and regulatory approvals. Even as digital adoption accelerates, physical presence provides competitive advantages—immediate cash disbursement, gold storage security, and human interaction during emotional transactions.

Operational Excellence Through Standardization

Muthoot scaled from dozens to thousands of branches through relentless standardization. Every process—from gold testing to documentation—followed standard operating procedures. Branch layouts standardized for efficiency and security. Training programs ensured consistent service delivery. IT systems enforced process compliance. This standardization enabled rapid replication—new branches operational within weeks, new staff productive within months. Yet standardization didn't mean rigidity—local customization within frameworks, continuous improvement through feedback, and innovation through controlled experimentation.

Capital Allocation Discipline

Despite abundant growth opportunities, Muthoot maintained capital allocation discipline. Expansion followed proven markets rather than speculation. Acquisitions filled capability gaps rather than pursuing unrelated diversification. Technology investments enhanced core operations rather than chasing trends. Dividend payments balanced growth reinvestment with shareholder returns. This discipline prevented value-destroying adventures that plagued many successful companies. Every capital decision answered simple question: does this strengthen our core gold loan business?

Risk Management Through Conservatism

Muthoot's risk management philosophy emphasized conservatism over sophistication. LTV ratios stayed below regulatory limits. Geographic expansion followed migrant networks rather than market studies. Product innovations tested extensively before scaling. Funding diversified across sources. This conservatism appeared costly during boom periods but proved invaluable during crises. The company never faced existential threats despite operating in volatile markets with regulatory uncertainties.

Human Capital Development

In service businesses, people are the product. Muthoot invested heavily in human capital—recruiting locally for cultural fit, training extensively for technical skills, and promoting internally for institutional knowledge. Career paths extended from branch staff to senior management. Performance systems balanced individual achievement with team collaboration. Cultural values emphasized service over sales. This human capital investment created competitive advantages—lower attrition, higher productivity, and better customer satisfaction.

Partnership Strategy: Leveraging Ecosystems