MTAR Technologies: The Backbone of India's Deep-Tech Ambitions

I. Introduction & The "High-Stakes" Hook

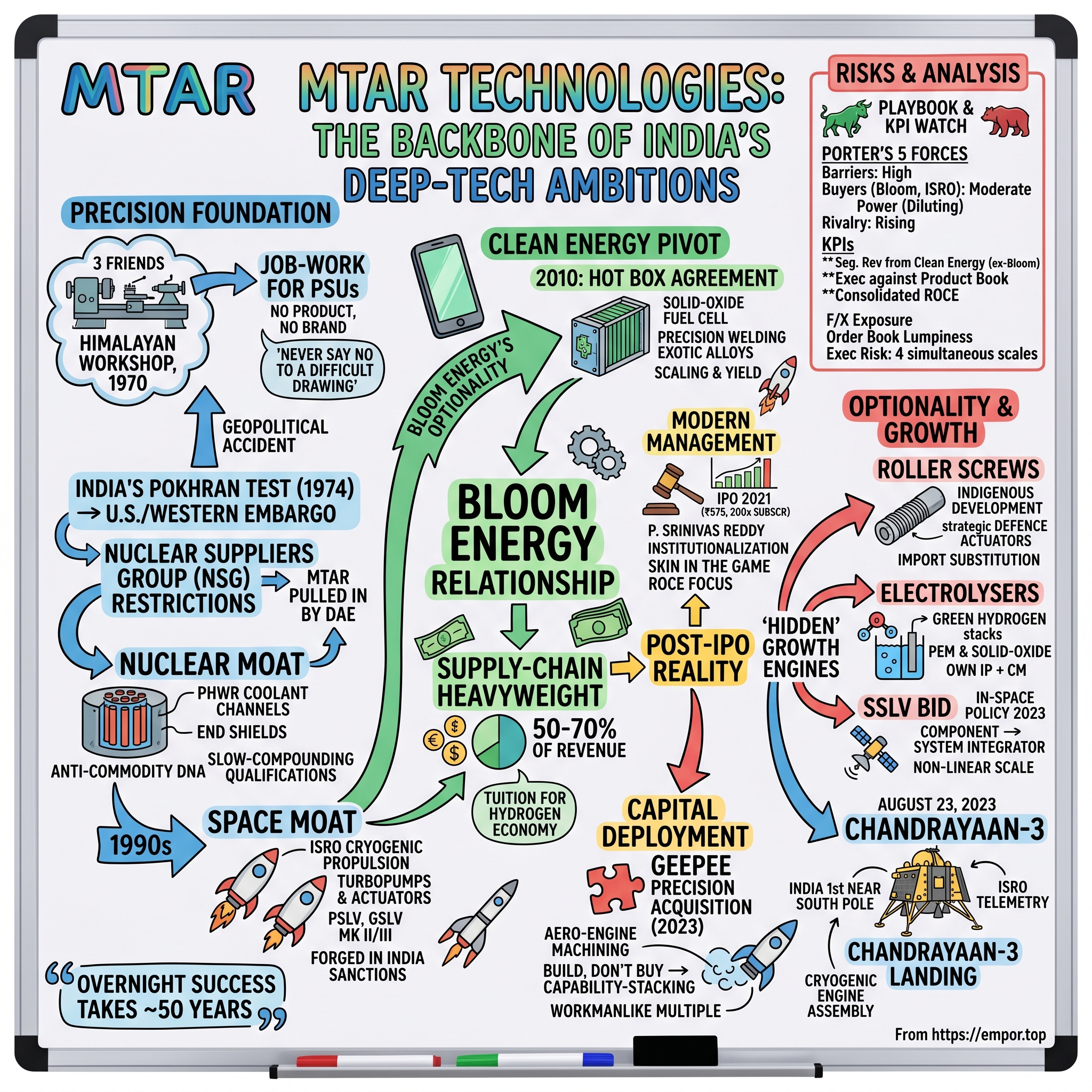

It is the afternoon of August 23, 2023. In the Mission Operations Complex at Bengaluru, the engineers of भारतीय अंतरिक्ष अनुसंधान संगठन Indian Space Research Organisation (ISRO) are watching a small screen. Telemetry is streaming in from a spacecraft 384,000 kilometres away. The Vikram lander, draped in golden multi-layer insulation, is descending toward the south polar region of the Moon, a place no other human mission has ever touched. For about twenty minutes the room barely breathes. And then, at 6:04 p.m. India Standard Time, Chandrayaan-3 lands. India becomes the fourth country in history to soft-land on the Moon and the first to land near the lunar south pole.[^7]

The world remembers ISRO. The world remembers Prime Minister Modi waving the tricolour over a video link from Johannesburg. What the world does not remember is the name of the unlisted-then-listed micro-cap company in Hyderabad that machined the cryogenic engine sub-assemblies, the actuators, and the structural components without which that lander would never have left the launchpad. That company is MTAR Technologies — eight hundred employees, two square kilometres of shop floor in the Balanagar industrial belt, and a customer list that reads like a fever dream of strategic-sector India: ISRO, the Nuclear Power Corporation of India न्यूक्लियर पावर कॉर्पोरेशन ऑफ इंडिया लिमिटेड (NPCIL), the Defence Research and Development Organisation (DRDO), the Indian Navy's submarine program, and across the Pacific, the American fuel-cell pioneer Bloom Energy.[^3]2

That single customer list is the thesis. MTAR is not really a machine shop, even though it owns one of the largest precision-engineering shop floors in southern India. It is a sub-tier strategic supplier — the kind of company that gets "designed in" to a nuclear reactor or a rocket engine, and then stays there for thirty years because the cost and regulatory friction of swapping it out is greater than the value of the part itself. For five decades it has climbed the complexity ladder, one impossible drawing at a time, from coolant channel rolling for pressurised heavy-water reactors in the 1980s, to liquid propulsion turbopumps for the GSLV in the 2000s, to hot-box components for solid-oxide fuel cells in the 2010s, to roller screws and electrolysers and small satellite launch vehicles in the 2020s.[^3][^4]

The roadmap for this episode follows that climb. Sections II and III walk through the two long arcs that built the modern MTAR — the nuclear-and-space backbone forged in the era of Indian sanctions, and the clean-energy pivot that quietly turned an obscure defence vendor into a fuel-cell supply-chain heavyweight. Sections IV and V examine the people running the company today, the governance arithmetic of the promoter family, and the tactical acquisition of Geepee Precision Engineering. Section VI walks the "hidden" growth lines — roller screws, electrolysers, the SSLV bid. Sections VII and VIII apply the frameworks Acquired listeners know well, Hamilton Helmer's 7 Powers and Porter's 5 Forces, and weigh the bull case against the bear case. The conclusion in Section IX returns to a question every founder eventually asks: how long does it take to become an overnight success? At MTAR, the answer is roughly fifty years.

II. Roots of Precision: The Hyderabad Nucleus

The story begins not in a boardroom but in a small workshop on the Balanagar industrial estate in Hyderabad, in 1970, with three friends, one second-hand machine, and a country that did not yet exist as an industrial power. India at that time was three years away from the Pokhran-I nuclear test, four years away from being placed under a near-total technology embargo by most of the Western world, and twenty years away from liberalising its economy. The state needed local companies who could read a complex engineering drawing and not flinch. Most could not.[^3]

MTAR was founded in 1970 by a group of engineer-entrepreneurs from undivided Andhra Pradesh, anchored by P. Jayaprakash Reddy and K. Satyanarayana Reddy, and built its first operations in Balanagar, the cluster that also housed Bharat Heavy Electricals and Bharat Dynamics.[^3] The founding story, as told inside the company, is not glamorous. The early years were "job-work" — taking blueprints from larger public-sector behemoths and turning them into metal. There was no product. There was no brand. There was only the question on every shop floor: can you actually hold this tolerance, or are you going to send us scrap?

What changed MTAR's trajectory was not a strategic plan; it was a geopolitical accident. The 1974 Pokhran test triggered the formation of the Nuclear Suppliers Group and a tightening export-control regime against India that would last for decades.[^3] Suddenly the Department of Atomic Energy could not buy critical reactor components from Westinghouse or Framatome. It had to make them at home, or with private partners at home who could be cleared and cultivated. MTAR, already working on the periphery of that ecosystem, was pulled inwards. By the late 1970s and through the 1980s, the company was machining components for India's pressurised heavy-water reactor (PHWR) program, including coolant channel assemblies and end shields — parts where a single dimensional error of a few microns can compromise the safety case of an entire reactor.[^3][^9]

This is where the "anti-commodity" DNA was forged. A normal Indian SME of that era survived by competing on price for simple parts. MTAR did the opposite. It chose the drawings nobody else would touch — the ones with material specifications nobody had welded before, with geometries that required five-axis CNC at a time when most Indian shop floors had three-axis, and with quality acceptance criteria written by atomic energy auditors. Internally the philosophy became a kind of slogan: never say no to a difficult drawing. That bias toward complexity is the single most underrated reason MTAR survives global competition today. The Koreans and the Japanese can build precision parts cheaper at scale; what they cannot easily do is take a one-off, never-before-made flight-critical assembly, build it twice, and certify it.

The 1990s opened the second front: space. As ISRO began its long march toward indigenous cryogenic propulsion — a capability the United States and Russia had explicitly tried to deny India in the Glavkosmos saga of 1992 — Liquid Propulsion Systems Centre (LPSC) needed Indian partners who could build the rotating machinery of a rocket engine. Turbopumps, gas turbines, injector assemblies, the kind of parts that spin at tens of thousands of RPM in cryogenic fluid. MTAR became one of the small handful of private firms cleared for that work, and over the following two decades supplied components for the PSLV, GSLV Mk II, and eventually the GSLV Mk III that would launch Chandrayaan-2 and Chandrayaan-3.[^3][^7]

So what does this fifty-year setup mean for an investor reading the company today? It means MTAR's competitive moat is not a patent and not a brand. It is a slow-compounding stock of qualifications — ISRO source approvals, NPCIL vendor codes, naval security clearances, ASME nuclear stamps — each of which took years to earn and would take competitors years to replicate. The next section is the story of how that strategic-sector machine was pointed, almost by accident, at the American hydrogen economy.

III. The Bloom Energy Inflection: The Pivot to Clean Energy

The most important phone call in MTAR's modern history was one that, by all accounts, almost did not happen. In the late 2000s, a young Silicon Valley fuel-cell company called Bloom Energy was getting ready to launch its first commercial product, the Bloom Energy Server — a refrigerator-sized solid-oxide fuel cell that converted natural gas or biogas directly into electricity at roughly twice the efficiency of grid combustion. Bloom needed a supplier for the most difficult part of the system: the "hot box," the high-temperature ceramic-and-metal core where the electrochemical magic actually happens. Hot-box fabrication demanded precision welding of exotic alloys, near-zero leak rates, and the ability to scale from prototype quantities to thousands of units per year without losing yield. Bloom looked at the usual American and European suppliers, did the math on cost, and started looking abroad.2

What happened next is the story of how MTAR became, almost without anyone noticing, one of the most strategically important Indian industrial exporters of the 2020s. Bloom approved MTAR as a hot-box supplier, and over the course of roughly fifteen years — the relationship dates from around 2009-2010 — turned it into a vertically integrated manufacturing partner.[^3]2 By the time MTAR filed its red herring prospectus with SEBI in early 2021, Bloom Energy alone accounted for more than half of the company's revenue, and the Clean Energy segment as a whole was the largest single contributor to the topline.[^3] In the years since, that share has bobbed between roughly 50% and 70% depending on the quarter and the order intake mix, but the structural reality has not changed: a Hyderabad nuclear-and-space supplier became, in financial terms, a clean-energy company.[^4]

Why did this work? Three reasons, all rooted in the previous section. First, the technical match. Hot boxes operate at around 800 degrees Celsius and demand the same metallurgical discipline as a nuclear pressure vessel. MTAR's nuclear-grade welding capability transferred almost directly. Second, the cost arbitrage was real but defensible — MTAR was not "cheap China" pricing; it was qualified Western-equivalent quality at Indian engineering cost, which is a much harder thing to replicate. Third, and most importantly, MTAR did something most Indian vendors fail to do with a global anchor customer. It invested ahead of the order book. It built a dedicated facility for Bloom, expanded capacity, in-housed sheet metal forming and complex sub-assembly, and let the relationship deepen into something more like a captive supplier than an arm's-length contractor.[^3][^4]

The financial profile changed accordingly. Pre-Bloom, MTAR was a steady but capacity-constrained business with lumpy, project-based nuclear and space revenue. With Bloom, it became a serial-production exporter, with the operating leverage and the dollar-denominated working capital cycle that come with it. The IPO documents describe a revenue base that grew from roughly ₹213 crore in FY2018 to ₹241 crore in FY2020, with margins that punched above the typical engineering services peer because of the strategic mix.[^3] By the mid-2020s, after a brief inventory correction at the customer end, the company guided to sustained mid-teens growth on a much larger base.[^4][^5]

And here is the second-order strategic gift of the Bloom relationship: it became MTAR's tuition payment for the broader hydrogen economy. The same hot-box knowledge that makes a solid-oxide fuel cell work also informs solid-oxide and PEM electrolysers — the equipment that splits water into hydrogen and oxygen using renewable electricity. By 2023-2024, MTAR was openly discussing electrolyser stack manufacturing as a future revenue line, including its own IP in addition to contract work for global OEMs.[^4][^5] That is not a coincidence. That is fifteen years of Bloom paying for the engineering muscle to enter what may be the largest industrial transition of the next quarter century.

The lesson here is the one Acquired listeners have heard before about Taiwan Semiconductor Manufacturing Company台積電 TSMC and its founding Texas Instruments relationship: a single anchor customer, properly handled, can be the trellis on which an entire industrial capability climbs. MTAR climbed. The next question, for both the company and its shareholders, was whether the climbers were the right people to take the company public.

IV. Modern Management & The New Guard

If the first thirty years of MTAR were a founder's story, the last fifteen have been a succession story. The transition is embodied by Parvat Srinivas Reddy, the Managing Director, who took the company from a privately held family-run precision-engineering firm to a publicly listed enterprise on the NSE and the BSE.[^3] Reddy is not a media presence in the mould of a Mukesh Ambani or a Vembu — he rarely gives extended interviews — and that reticence is itself a tell. The cultural code at MTAR is engineering-first, marketing-last. It is closer to the quiet, technocratic style of a German Mittelstand company than to the typical Indian listed mid-cap.

The pivotal moment of the modern era was the IPO. MTAR Technologies opened its initial public offering on March 3, 2021, and closed it three days later, with the price band set at ₹574-575 per share.[^3] The book was subscribed roughly 200 times over the issue size, making it one of the most heavily oversubscribed Indian IPOs of that calendar year. On listing day, March 15, 2021, the stock opened at a sharp premium to the issue price, validating the appetite the institutional book had shown. Whatever one thinks about market frothiness in early 2021, the demand signalled something real: institutional investors had identified MTAR as one of the cleanest publicly listed proxies for the simultaneous Indian themes of defence indigenisation, space privatisation, and the global energy transition.[^3]2

The promoter holding tells the governance story succinctly. Following the IPO and subsequent secondary transactions, the promoter group's stake settled in the high thirties as a percentage of the equity base — a level low enough to allow for serious institutional ownership and yet high enough to preserve clear founder-family stewardship.[^12] In the 2024-2025 disclosure cycle the promoter stake hovered around the 37% mark, with the balance distributed among domestic mutual funds, foreign portfolio investors, and a long retail tail.[^12] This is, in the Indian context, a comfortable arrangement: enough skin in the game to deter agency drift, but not so concentrated as to scare off public shareholders.

Where the new guard has visibly altered the company's behaviour is in three places. First, in capital allocation discipline. The post-IPO MTAR has stayed conservatively leveraged, has resisted the temptation to lever up for large M&A even when the share price would have made currency-funded deals attractive, and has explicitly framed return on capital employed (RoCE) as the governing metric rather than topline growth at any cost.[^4][^5] Second, in the institutionalisation of reporting. Investor decks, segment disclosures, and earnings calls now show segmental revenue splits across Clean Energy, Nuclear, Space and Defence, Product Engineering, and others — disclosure granularity that did not exist in the private era.[^4] Third, in the conscious cultivation of a multi-customer Clean Energy book. Management has spoken on calls about diversifying beyond Bloom into other global energy customers and into MTAR's own electrolyser IP, a tacit acknowledgement that single-customer concentration is the most cited bear concern.[^4][^5]

It would be misleading to paint this as a finished transition. MTAR's executive team is small, its bench beyond the top two or three names is thin compared to a Larsen & Toubro or a Bharat Forge, and the company is still adjusting to the rhythm of quarterly capital markets. The bumpy FY2024, in which Bloom-driven destocking and an extended order cycle compressed revenue and margins, was the first real test of how the team would communicate setbacks to public shareholders.[^5] The response — frank disclosure, lowered guidance, and a clear articulation of the longer-cycle thesis — was credible if uncomfortable. For long-term holders that is what professionalisation actually looks like.

The board's other notable move was strategic, and it set up the next section: the recognition that organic growth alone would not be enough to claim adjacent markets at the pace the next decade would demand.

V. M&A and Capital Deployment: The Geepee Move

For the first fifty years of its history, MTAR did not buy companies. It built capability the slow way — one drawing, one shop-floor cell, one machinist apprenticeship at a time. So when in August 2023 the company announced the acquisition of Geepee Precision Engineering, a Bengaluru-headquartered precision machining firm focused on small aero-engine and sub-assembly work, it was less a routine corporate development item and more a philosophical inflection.[^6]

The strategic logic of the deal was straightforward to anyone who had been listening to MTAR's investor calls over the previous eighteen months. The Indian and global aerospace primes — Pratt & Whitney, Safran, GE Aerospace, Honeywell, and their Tier 1 Indian licencees — were aggressively expanding their India supplier base under the combined logic of the Government of India's defence-indigenisation push and the global "China-plus-one" supply chain rebalancing.[^11] To plug into that wave, MTAR needed two things it did not yet have in sufficient depth: customer relationships with aero-engine OEMs, and qualified capacity in the smaller, higher-volume precision parts that fill an aero-engine bill of materials. Geepee offered both.[^6]

The deal economics, as disclosed, were modest in absolute terms — MTAR funded the acquisition out of internal accruals and balance-sheet cash, and the consideration was structured to align Geepee's existing management with continued performance.[^6] Was it expensive? Benchmarked against the listed Indian aerospace and defence engineering peers — names like Data Patterns, Paras Defence, Bharat Forge's aerospace vertical, and the unlisted aero-supply arms of larger groups — the multiples implied were in line with, rather than aggressive against, the public-market comparable set. Importantly, MTAR did not pay a strategic-control premium for a marquee asset; it paid a workmanlike multiple for a tuck-in that gave it a faster path into a specific end-market.

Two things make this transaction more interesting than the average mid-cap M&A note. The first is the philosophical shift it represents. MTAR's long-running internal preference for "build, don't buy" was rooted in a specific worry that acquisitions of precision-engineering shops too often deliver depreciated machinery and undertrained operators rather than real capability. Geepee was reportedly diligent-tested on exactly those questions — machine condition, customer qualification status, quality history — before the deal was signed.[^6] The second is the implicit declaration about the next decade. By formally moving beyond organic growth, MTAR signalled that the addressable opportunity in aerospace, defence, and clean energy was large enough that opportunistic capability-stacking would now be part of the toolkit.

The bigger question is what comes next. The Indian precision-engineering universe contains dozens of sub-scale, founder-aging, capability-rich shops that would be natural targets for a Tier 1 consolidator. MTAR has not articulated an explicit M&A program. But the Geepee playbook — small ticket, capability-additive, culture-compatible, internally funded — is a template that can plausibly be run again. And in capital allocation, as Acquired episodes have argued before, the first deal is usually the cheapest because the bar of credibility has not yet been set; once a company has executed two or three quietly, the option value of being known as a disciplined acquirer becomes its own moat.[^4]

What this section sets up is the realisation that MTAR's portfolio is now wider than its public reputation. The aerospace tuck-in is one of several growth seeds that have been planted but are not yet visible in the income statement. The next section walks the most important of those — roller screws, electrolysers, and the small satellite launch vehicle — because they are where the next ten years of optionality actually lives.

VI. "Hidden" Growth Engines: The Secret Projects

Inside MTAR's main facility in Hyderabad there is a project room whose contents would not have made sense to anyone outside the building five years ago. On one bench sits a roller screw assembly — a precision-machined steel cylinder threaded with helical grooves that mesh with rolling planetary elements, used to convert rotary motion into linear motion with vastly higher load capacity than a conventional ball screw. On another bench, a stack of metallic and ceramic plates joined into a solid-oxide electrolyser cell. On the wall, a poster of the Small Satellite Launch Vehicle, SSLV, ISRO's commercial-launch workhorse, with the names of vendors listed in the corner. Each of these three things is a different bet, but they share a common thesis: the next leg of MTAR's growth will come from products it owns the design of, not just parts it machines to someone else's drawing.[^4][^5][^10]3

Start with roller screws. To a non-engineer, a roller screw sounds banal. To a defence and aerospace engineer, it is one of the most strategically gated components in the modern actuator stack. Roller screws sit inside the linear actuators that move missile fin control surfaces, aircraft flight control systems, electric vertical-takeoff and landing (eVTOL) thrusters, and a wide range of industrial precision motion systems. For decades the global market has been an effective duopoly of Swiss and French manufacturers, with no Indian source. Indian defence programs that required roller screws had to import them, which created both a hard-currency cost and a strategic vulnerability — exactly the kind of friction that the government's आयात प्रतिस्थापन import substitution policy targets.[^10][^11] MTAR's announcement in 2023 that it had successfully indigenously developed roller screws was therefore not just a product launch. It was a category creation event. The medium-term revenue contribution will likely build slowly, because qualifying a precision motion component into a flight-critical system is a multi-year exercise. But the long-run optionality — across defence, aerospace, and industrial — is large enough to be a multi-year analyst question on its own.[^10]

Next, electrolysers. The global green hydrogen build-out, encouraged by U.S. Inflation Reduction Act tax credits, EU Green Deal subsidies, and India's own National Green Hydrogen Mission, will need millions of electrolyser stacks over the next two decades. MTAR's positioning here is unusual. Most entrants come from either the chemicals side (Reliance, L&T, Adani) or from the catalyst/electrolyser-OEM side (ITM Power, NEL ASA, Plug Power). MTAR comes from neither. It comes from the contract manufacturing side, with fifteen years of high-temperature stack experience in Bloom hot boxes. That gives it a credible claim to compete on solid-oxide electrolyser cells, where the supply chain is far less crowded than the PEM segment, and where the high efficiencies make sense for industrial offtakers like steel and ammonia.[^4][^5] The company has publicly discussed building both contract-manufacturing capacity and its own product family, though commercial revenue at meaningful scale is still ahead.

Third, the SSLV story. With the Indian Space Policy 2023, IN-SPACe was empowered to authorise private actors to design, build, and even operate small satellite launch vehicles based on ISRO-developed technology.3 For private precision-engineering players, this is the biggest single change in their addressable market since the cryogenic engine partnership of the 1990s. MTAR has historically been a component supplier to ISRO; in the new regime it can credibly bid alongside system integrators on full sub-assemblies and potentially on entire vehicle programs.3 This is the largest of the three optionality bets, because the financial scale of moving from component to system integrator is non-linear; an integrator captures more of the value chain per launch by a factor of five to ten, depending on the configuration.

Segment by segment, the picture that emerges from the most recent investor disclosures is of a company whose income statement is still dominated by clean energy (Bloom-anchored, with new customers being added), with nuclear contributing a smaller but utterly stable cash flow, defence and space contributing the highest-growth orders, and product engineering (where the three "hidden" projects live) still at the early-revenue stage.[^4][^5] For investors thinking in three- and five-year arcs, those product engineering bets are where the upside is being seeded. For investors thinking in twelve-month arcs, the variance in the Bloom order cycle will continue to dominate the quarterly print. Both can be true simultaneously, and the most common misreading of MTAR is to confuse the near-term volatility with the long-term option value.

That tension — short-cycle noise sitting on top of a long-cycle thesis — is exactly what makes the next section's frameworks useful.

VII. The Playbook: 7 Powers & Porter's 5 Forces

To understand why MTAR can survive in a world of much larger competitors, it helps to put the company through two frameworks long-time Acquired listeners will recognise: Hamilton Helmer's 7 Powers, and Michael Porter's classic 5 Forces.

Start with Helmer's framework. Of the seven powers — scale economies, network economies, counter-positioning, switching costs, branding, cornered resource, and process power — MTAR has clear claims on three, partial claims on two, and effectively none of the remaining two.

The clearest power MTAR holds is the cornered resource. Over five decades, the company has accumulated a workforce of more than nine hundred employees, including hundreds of highly specialised engineers, machinists, welders, and quality inspectors trained in defence-, nuclear-, and aerospace-grade processes.[^3][^4] It owns a fleet of large-format five-axis CNC machines, electron-beam welders, vacuum brazing furnaces, and inspection metrology that takes years to commission and longer to staff. None of these inputs is uniquely available to MTAR; what is uniquely available is the combination of them, in one place, with the cleared qualifications to run high-consequence parts. That bundle is genuinely difficult to replicate. A new entrant could buy the machines; it could not, in a reasonable timeframe, accumulate the source approvals.

The second power is switching costs. Once MTAR is qualified into a flight-critical assembly — a turbopump for an upper stage, a hot-box weldment for a fuel cell, a coolant channel assembly for a 700 MW reactor — the regulatory and commercial cost of replacing it is asymmetric. The customer has to re-qualify the new vendor against the same standards (ASME, IAEA, NADCAP, OEM-specific), re-run first-article inspections, and re-baseline its safety case. In a nuclear reactor or a launch vehicle, that may take years and may not be approved by the customer's own regulator. The result is that once MTAR is in, MTAR tends to stay in. The Bloom Energy relationship is the cleanest commercial example.2

The third partial power is process power. MTAR's culture of "never say no to a difficult drawing" is, in Helmer's terms, an internally accumulated practice that has not been articulated as a single transferable manual. It would not survive a leadership crisis intact, but it has survived multiple ones already.

What MTAR does not have, in any meaningful sense, are scale economies at the level of a global aerospace prime, network effects of any kind, or strong consumer-style branding. It does not need to. In the segments where it competes, the customer is sophisticated, the procurement is technocratic, and brand exists at the level of qualifications and approvals, not at the level of consumer mindshare.

Porter's 5 Forces gives a different, equally clarifying lens.

Barriers to entry in MTAR's segments are very high — high capital intensity, high regulatory friction, and a level of "trust capital" that takes a decade to build. A well-funded new entrant cannot simply "buy" its way into NPCIL's coolant channel program in three years.

Bargaining power of buyers has historically been the largest worry. With ISRO, NPCIL, and DRDO as the dominant Indian customers, MTAR sits across the table from monopsonist procurement authorities. With Bloom Energy as the dominant Clean Energy customer, the concentration is even sharper — for a stretch in the early 2020s, Bloom alone accounted for the majority of MTAR's topline.[^3] The strategic mitigant has been deliberate diversification: more global Clean Energy customers, more defence platforms, more aerospace OEMs through the Geepee channel, more product engineering revenue.[^4][^5][^6]

Bargaining power of suppliers is moderate. The exotic alloys (super-duplex stainless, Inconel, titanium aerospace grades) and specialised consumables (atomic-energy-cleared welding wire, qualified casting blanks) come from a small global supplier base. Material cost volatility flows through to gross margins in real time, which is why the company hedges where contractually feasible.

Threat of substitution is low at the component level. Nobody is going to substitute a rocket engine turbopump with software.

Industry rivalry is fragmented but rising. Domestically, peers include Godrej Aerospace (unlisted), Walchandnagar Industries, Larsen & Toubro's heavy engineering vertical, Hindustan Aeronautics' supply chain, and a long tail of mid-sized defence-engineering firms. Globally, the relevant peer set in clean energy includes the captive supply chains of large Korean and Japanese conglomerates such as 한화 에어로스페이스 Hanwha Aerospace.[^4] None of these are direct one-for-one comparables — they tend to overlap in two or three segments at most — but together they define the competitive boundary against which MTAR has to keep extending its qualifications.

The result of stacking these two frameworks is the anti-commodity strategy. MTAR has stated, both in its prospectus and in its investor presentations, that it deliberately does not compete on simple, high-volume parts.[^3][^4] It chooses the components with the highest complexity-to-revenue ratio, the highest regulatory friction, and the longest qualification lead times, because those are precisely the slots where its accumulated cornered resource and switching-cost moats actually count. It is, in short, the opposite playbook to a typical Indian engineering exporter.

VIII. Myth vs Reality, Bull, and Bear

Before moving to the bull and bear cases, it is worth pausing on the two most common consensus narratives about MTAR — the "myths" — and stress-testing them against the actual record.

Myth one: MTAR is a pure defence and space play. This is the way the company is most often described in popular financial media, and it is structurally wrong. Defence and space have always been the strategic anchor, but for most of the last five years the Clean Energy segment — overwhelmingly driven by Bloom Energy — has been the largest single revenue contributor.[^3][^4] The mental model for the company is closer to "strategic-sector precision platform with three roughly equal long-cycle legs" than to "defence stock."

Myth two: MTAR is a one-customer story. This was directionally true at the time of the 2021 IPO, when Bloom Energy contributed a large majority of Clean Energy revenue, and Clean Energy in turn was the largest segment.[^3] It is less true today. Through the FY2022–FY2025 cycle, management has added new Clean Energy customers, expanded the Defence and Aerospace order book, taken on the Geepee acquisition, and seeded product engineering programs in roller screws and electrolysers.[^4][^5][^6][^10] The customer concentration risk remains real, but it has been actively diluted, not ignored.

With the myths set aside, the bull case is straightforward to state. Three long-cycle tailwinds — Indian defence indigenisation under the Ministry of Defence's positive indigenisation lists and the broader Make in India framework; the privatisation of the Indian space sector under the Indian Space Policy 2023 and IN-SPACe; and the global energy transition toward fuel cells, electrolysers, and hydrogen-derived industrial fuels — all flow into precisely the segments MTAR has spent decades qualifying into.[^11]3 If India triples its annual orbital launches over the next decade, MTAR's component revenue per launch is structurally embedded. If the United States and Europe scale stationary fuel-cell deployment for data center backup and microgrids, Bloom's bill of materials is largely MTAR's revenue. If the Indian Navy moves forward with its next-generation submarine and aircraft carrier programs, MTAR is on the qualified vendor list.[^4][^5] Layer on top of that the optionality of roller screws, of solid-oxide electrolyser IP, and of an SSLV system-integrator bid, and the bull case is not a single trade but a portfolio of long-dated calls.[^10]3

The bear case is no less coherent. It rests on three pillars. The first is customer concentration: Bloom Energy is still, materially, MTAR's largest customer, and any disruption to Bloom's order cycle — whether due to natural-gas pricing, U.S. regulatory shifts, or a competing fuel-cell architecture — flows through to MTAR's revenue with little lag. The 2023-2024 destocking episode is a recent reminder of how that risk manifests.[^5] The second pillar is execution risk. MTAR is simultaneously scaling a clean-energy export business, integrating an acquisition, building three new product lines from a low base, and adjusting to the rhythm of public-market reporting. Any one of these is hard. Doing all four well at the same time is genuinely difficult, and the management bench, while improving, is not yet deep.[^4][^5] The third pillar is valuation sensitivity to a long-tailed thesis. MTAR's stock trades — and has traded since IPO — at multiples that imply meaningful realisation of the optionality embedded in roller screws, electrolysers, and the SSLV. If those programs take longer than the market expects, or if the Indian space and defence procurement cycles slow, the multiple is the first thing to compress.[^12]

Within the global peer set, the closest mental models are not exact comparables but indicative. Hanwha Aerospace 한화 에어로스페이스 in Korea has shown what scale economics in defence-grade precision engineering can look like inside a vertically integrated chaebol. Godrej Aerospace, unlisted, sits in roughly the same Indian addressable market as MTAR's space and defence vertical, with a different ownership structure. Bharat Forge's defence and aerospace verticals are larger but less specialised. None of these is a true read-across, but together they define the ceiling and floor of what an Indian precision-engineering platform can reasonably look like at scale.

For an investor doing the work, three KPIs deserve the most attention going forward. The first is segmental revenue from Clean Energy excluding the single largest customer — the cleanest measure of whether the customer concentration risk is genuinely abating. The second is execution against the product engineering order book — specifically, the pace at which roller screws, electrolyser stacks, and any disclosed system-integrator wins translate into revenue and contribute to RoCE.[^4][^5][^10] The third is return on capital employed (RoCE) at the consolidated level, because it is the single number that reveals whether the new growth is value-creating or value-diluting once capex for the new lines is fully reflected.[^4][^5] Holders do not need to recalculate these; the company discloses them. The discipline is to track them across cycles, not quarters.

The overlay risks to flag, briefly and without alarmism, are familiar to anyone following Indian mid-caps: one, the foreign exchange exposure inherent in a large dollar-revenue Clean Energy book is real and is managed but not eliminated; two, the order-book lumpiness inherent in strategic-sector procurement makes any single quarter a poor sample of underlying capability; three, the auditor and accounting hygiene of the company has thus far been clean, but as the segment count grows, so does the surface area for revenue recognition judgments — particularly in long-cycle, milestone-based contracts.[^2][^5] None of these is a thesis-breaker. All of them are worth re-checking annually.

IX. Conclusion: The Long Game

There is a particular kind of company that the Acquired team returns to again and again: the company that looks, on the surface, like an overnight success, but whose foundation took half a century to pour. Taiwan Semiconductor in the 1990s. Costco before Jim Sinegal. NVIDIA before the AI compute cycle of the 2020s. MTAR Technologies fits that pattern with unusual precision.

The Hyderabad workshop of 1970 did not set out to become a publicly listed clean-energy supplier with a 200x-oversubscribed IPO. It set out to make difficult parts that nobody else in India could make. For the first three decades, the reward for that bet was a steady drip of nuclear and space contracts, no public recognition, and the gradual accumulation of qualifications that, at the time, looked like overhead. For the next fifteen years, the reward was a Bloom Energy relationship that almost no one outside the company's small ecosystem noticed until the IPO documents made it impossible to ignore. And only in the last five years — since the listing in 2021, the Chandrayaan-3 success in 2023, the Geepee acquisition, and the public unveiling of the roller screw and electrolyser programs — has the cumulative scale of the bet become visible to the broader market.[^3][^7][^6][^10]

The takeaway for founders, the one Acquired episodes have circled back to in many other contexts, is simple to state and difficult to live: precision is a moat that scales, but only at the pace of trust. Each new customer qualification, each new safety case, each new regulatory clearance is a one-time investment that, properly stewarded, compounds for decades. There are very few categories in industrial India where this kind of compounding is still available; precision engineering for strategic and energy sectors is one of them.

The takeaway for long-term investors is a different formulation of the same idea. MTAR is not a stock that rewards a quarter-to-quarter mindset, and it has, with some regularity, punished the investors who have approached it that way. It is a company whose actual moat — the cornered resource of qualified workforce and approvals, the switching costs of being designed into mission-critical systems — operates on a five- to ten-year timescale.[^3][^4] The KPIs to watch are slow-moving by construction. The risks are real and concentrated, and they should be checked annually, not ignored. But the underlying question — whether India over the next twenty years will need a domestic precision-engineering champion that can supply ISRO, NPCIL, the Indian Navy, the global hydrogen economy, and the global aerospace supply chain simultaneously — is not really in dispute. The only question is whether MTAR will be that champion, or one of two or three that share the territory.

Fifty years of patient drawings suggest a reasonable working answer. The next fifty will deliver the verdict.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube