MSTC Limited: From Scrap Trader to India's E-Commerce Infrastructure Pioneer

I. Introduction & Episode Roadmap

Picture a 61-year-old government company that started life importing scrap metal for India's socialist steel mills. Today, that same company runs the digital infrastructure behind India's most consequential government transactions—5G spectrum auctions worth billions of dollars, coal mine allocations reshaping the energy sector, and transparent e-procurement systems processing tens of thousands of events annually.

MSTC Limited is a listed, Schedule-B, Mini Ratna Category-1 Central Public Sector Enterprise under the administrative control of Ministry of Steel, Government of India, primarily engaged in providing e-commerce related services across diversified sectors. But this clinical description masks a remarkable transformation story—one of reinvention, strategic pivots, and the quiet building of digital moats in an economy rapidly modernizing its public sector operations.

The central question this article explores: How did a 1960s-era scrap metal importer transform into the digital auctioning backbone for India's largest government transactions? And more importantly for investors today—is this a hidden platform business camouflaged by commodity trading volatility, or a PSU struggling with structural constraints?

Presently, the Government of India holds 64.75% shareholding in the company. The remaining 35% trades publicly, but often with puzzling disconnects between the company's growing e-commerce capabilities and market perception. The shares listed on BSE and NSE on March 29, 2019, at INR115 per share, down 4.17% from the IPO price of INR120. The lukewarm reception reflected market skepticism about PSU profitability and uncertainty about the company's true value proposition.

Today, MSTC operates two distinct businesses under one roof. The legacy trading division sources bulk industrial raw materials—heavy melting scrap, metallurgical coke, crude oil, coal—acting as facilitator and charging markup percentages. This is the old MSTC, born of the license raj, thriving in the shadows of monopoly, now competing in open markets.

But the crown jewel is the e-commerce vertical. In 2002, MSTC developed and launched an e-Auction platform and ventured into the B2B e-Commerce sector, subsequently establishing itself as one of the leading e-commerce service providers in the country. This platform business conducts electronic auctions primarily on behalf of the government and state-owned companies—a service where trust, transparency, and technical capability create formidable competitive advantages.

This article traces MSTC's journey across six decades, identifying the key inflection points that fundamentally altered its trajectory. We'll examine its Cold War origins, the 1991 liberalization shock that forced reinvention, the pivotal 2002 e-commerce gambit, marquee wins in spectrum and coal auctions, recent strategic moves like the FSNL divestment, and what lies ahead. For investors seeking to understand whether MSTC deserves a platform business valuation or commodity trader multiples, the story begins in post-independence India's planned economy.

II. The Cold War Era Origins: Building the Socialist Industrial Complex (1964–1991)

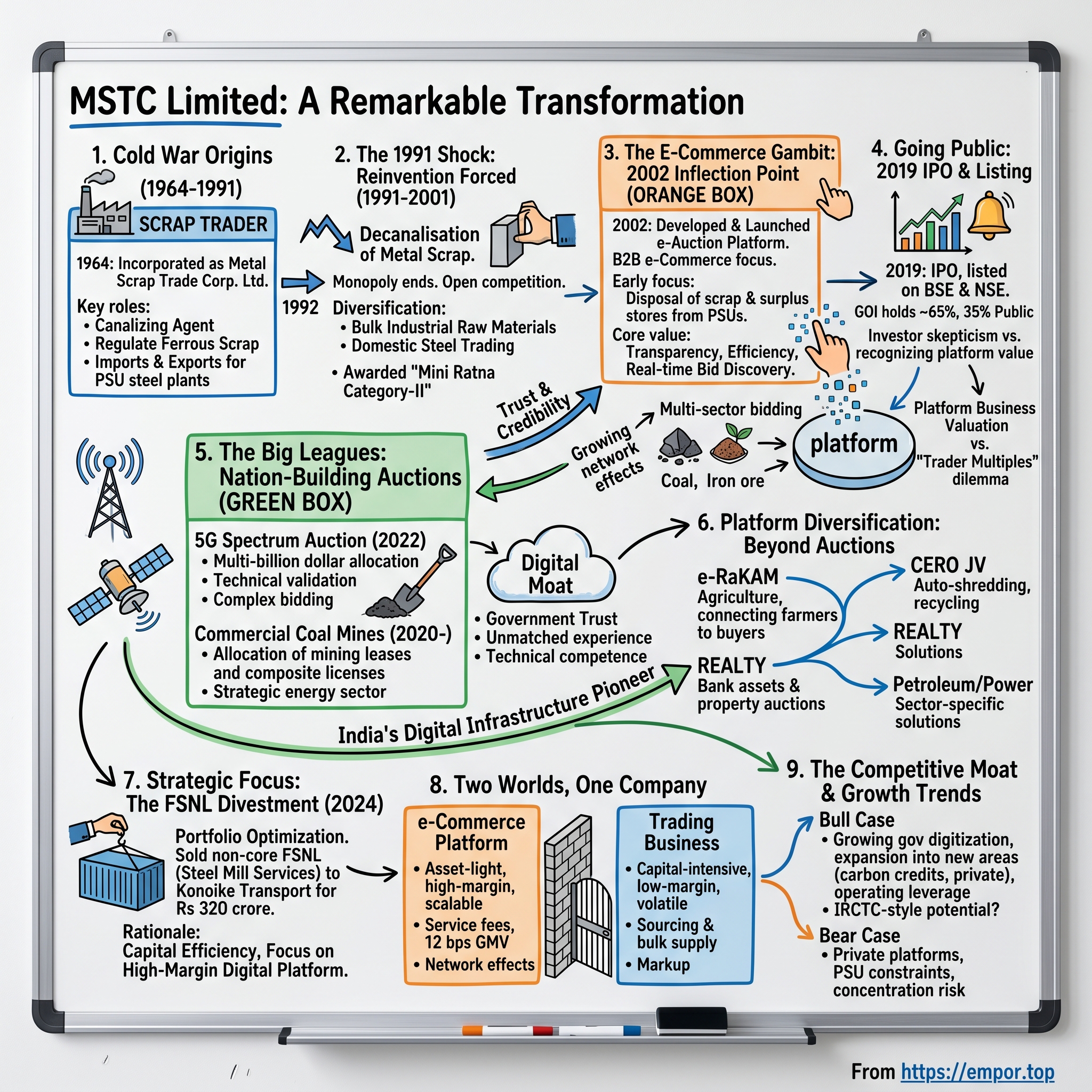

The year was 1964. India, less than two decades post-independence, embraced Nehruvian socialism with fervor. The Second Five-Year Plan prioritized heavy industries—steel, coal, power—as foundations for self-reliance. Yet building a steel industry required not just iron ore and coal, but also scrap metal for secondary steel production. India needed institutional mechanisms to channel this critical input.

The company was incorporated as Metal Scrap Trade Corporation Limited under the Companies Act, 1956, on September 9, 1964, in Kolkata. Its original mandate was straightforward: regulate ferrous scrap exports and, soon after, manage imports as a government canalizing agency. Initially incorporated to engage in the export of ferrous scrap, the company became a subsidiary of SAIL in 1974, and a canalizing agent for the Government of India for importing metal scrap.

In those days, "canalizing agency" meant government monopoly. Private players couldn't import metal scrap, rerollable scrap, sponge iron, or ships for breaking without going through MSTC. The logic was quintessentially socialist: centralized control ensured strategic industries received inputs at regulated prices, preventing speculative hoarding and profiteering. MSTC sat at a chokepoint in India's industrial supply chain.

The company became a subsidiary of SAIL on August 22, 1973 to act as a canalizing agent of the Government of India for the import of metal scrap, and since its incorporation until the decanalisation of metal scrap by the GoI in 1992, the company was mainly engaged in import of metal scrap. For nearly three decades, MSTC operated in a comfortable monopoly. Demand was predictable—SAIL's steel plants, secondary steel producers, petrochemical industries all needed scrap. Supply was controlled. Margins were steady. Risk was minimal.

This was MSTC's first life: a cog in India's license raj machinery, essential yet unremarkable. Employees enjoyed public sector job security. Management faced little competitive pressure. Performance metrics centered on volumes handled, not innovation or efficiency. The company served its purpose within the planned economy's architecture.

But beneath the surface, vulnerabilities accumulated. MSTC developed no distinctive capabilities beyond government relationships and import logistics. It built no proprietary technology, no unique market insights, no competitive moat beyond regulatory protection. When the Berlin Wall fell and India's own economic crisis loomed, MSTC's comfortable monopoly era was about to collide with reality.

III. The 1991 Shock: Liberalization Forces Reinvention (1991–2001)

July 1991 brought India to the brink. Foreign exchange reserves covered barely three weeks of imports. The IMF demanded structural reforms. Finance Minister Manmohan Singh and Prime Minister P.V. Narasimha Rao dismantled the license raj—slashing import tariffs, abolishing industrial licensing, devaluing the rupee, and critically for MSTC, ending canalizing monopolies.

The government decanalised metal scrap in 1992. Overnight, MSTC's monopoly evaporated. Private traders could now import scrap directly. Foreign suppliers gained multiple Indian buyers. Competition emerged on price, service, relationships, logistics—dimensions where a bureaucratic PSU held no inherent advantages.

The existential crisis was immediate. How does a government monopoly survive in a competitive market? Many PSUs didn't—either withering into irrelevance, requiring perpetual government bailouts, or becoming privatization candidates. MSTC faced the same fork in the road.

After the decanalisation, the company decided to diversify its business and emerge as a multi-product and a multi-functional organization. This decision—prosaic in retrospect—represented MSTC's first major inflection point post-independence. Rather than resist change or accept decline, management chose adaptation.

The diversification took several forms. After decanalization, the company established itself as a major player in importing bulk raw material for various industries, and in 2001, the company was accorded Mini Ratna Category-II status. MSTC positioned itself not as a regulator but as a facilitator—helping steel producers, oil companies, and power utilities source raw materials globally. Instead of exercising monopoly power, it leveraged decades of supplier relationships, logistics knowledge, and government entity trust.

The company also entered domestic steel trading. In 2001, as part of diversification, MSTC entered the marketing of finished steel and Pig Iron in domestic markets. This brought MSTC closer to end users, diversifying revenue beyond pure import facilitation.

Yet throughout the 1990s, a more fundamental question emerged: What is MSTC's sustainable competitive advantage in a liberalized economy? It couldn't compete on capital—private traders had deeper pockets. It couldn't compete on agility—PSU bureaucracy constrained decision-making. Size alone offered no protection.

What MSTC did possess, however, was something intangible yet powerful: trust. Decades of handling government transactions, maintaining neutrality between buyers and sellers, and operating with transparency (even within a controlled economy) built credibility. Public sector undertakings and government departments knew MSTC as a reliable intermediary. This trust—fragile, hard to quantify, easily squandered—would prove critical for MSTC's next transformation.

By the late 1990s, another technology revolution was brewing. The internet promised to digitize commerce, disintermediate traditional middlemen, and create transparent marketplaces. For MSTC, this technological shift presented both threat and opportunity. The question was whether the company could leverage its trust advantage in a digital age.

IV. The E-Commerce Gambit: The 2002 Inflection Point

The turn of the millennium brought India's IT services boom, dot-com frenzy, and slowly, government digitization initiatives. In Delhi's corridors of power, conversations turned to transparency, efficiency, and eliminating corruption in public procurement. Manual tender processes—opaque, paper-heavy, prone to collusion—cried out for technological disruption.

In 2002, MSTC developed and launched an e-Auction platform and ventured into the B2B e-Commerce sector. This decision—MSTC's second major inflection point—would ultimately define the company's future far more than any commodity trading business could.

Why did e-auctions matter? Consider the status quo in 2002. When government departments or PSUs wanted to dispose of scrap, surplus stores, old machinery, or auction minerals, they published notices in newspapers, invited sealed bids, held physical auctions in obscure locations, and often faced questions about price discovery and favoritism. Transparency was difficult to verify. Participation was limited to those physically present or connected to intermediaries. Small bidders faced barriers.

MSTC Limited launched its e-auction portal in 2002 and since then it has emerged as the leading e-auction service provider in the country, developing the most diversified e-commerce portfolios with vast experience of many years in the area of e-auction.

The platform started small. The journey started in 2002 on a very small scale for disposal of scrap and surplus stores. Early auctions focused on what MSTC knew best—scrap metal disposal from PSUs. But the digital format offered immediate advantages: broader reach (bidders could participate from anywhere with internet access), time-stamped transparency (every bid recorded electronically), automatic floor price enforcement (no manual intervention), and data trails that deterred manipulation.

Since 2002, MSTC has been an e-auction service provider to a large number of government departments and PSUs. Government organizations began noticing something crucial: e-auctions generated higher realized prices than manual tenders. When more bidders participate and can see competitive bids in real-time, price discovery improves. Sellers captured more value. Buyers gained confidence in fair process.

Network effects began compounding. As more government departments used MSTC's platform, more bidders registered to access those auctions. More registered bidders made MSTC's platform more attractive to new government sellers. The platform became self-reinforcing.

Critically, MSTC occupied a unique position. Unlike private e-commerce platforms, MSTC carried government pedigree and six decades of PSU trust. Unlike other government entities, MSTC possessed e-commerce technical capabilities and commodity expertise. This intersection of government credibility, technical competence, and domain knowledge created a defensible market position.

The business model proved capital-light and high-margin. MSTC didn't buy or sell goods—it provided technology infrastructure and auction services. In this segment of business, the company acts as service provider for e-auction/s-sale, e-procurement and development of customized software/solutions. Revenue came from service charges—typically a small percentage of transaction value or fixed fees per auction event. With relatively fixed technology costs, incremental auctions generated strong margins.

By 2004, diversification accelerated. The company commenced e-auctioning of coal in 2004, e-auction of tea in 2010, e-auction of human hair in 2011, e-auction of iron ore in Karnataka in 2012, chrome ore and chrome concentrate for Odisha Mining Corporation in 2012, iron ore in Goa and red sanders in Andhra Pradesh in 2014. Each new vertical validated the platform's flexibility and deepened MSTC's government relationships.

The jewel in MSTC's crown wasn't any single auction—it was the platform itself. MSTC's auction services eliminate manual inefficiencies and foster trust through unbiased processes, providing transparency. In a country where corruption in public procurement remained endemic, MSTC offered something invaluable: a neutral, auditable, technology-enabled marketplace.

Yet in 2002, few could predict that this e-auction platform would eventually handle spectrum auctions worth hundreds of billions of rupees or become critical infrastructure for India's energy sector. That transformation required winning marquee mandates that would elevate MSTC from a PSU e-auction provider to a strategic national asset.

V. Going Public: The 2019 IPO and Listing

By the late 2010s, the Modi government accelerated PSU disinvestment, seeking to unlock value and meet fiscal targets. MSTC, with growing e-commerce revenues and established profitability, became a disinvestment candidate. For investors, the IPO offered rare access to a government e-commerce platform play—albeit one wrapped inside commodity trading operations.

MSTC IPO was a main-board IPO of 1,76,70,400 equity shares of face value of ₹10 aggregating up to ₹211.04 Crores, priced at ₹120 per share, opening on March 13, 2019, and closing on March 20, 2019. The offering was an Offer for Sale—the government selling down its stake rather than MSTC raising fresh capital.

The IPO structure revealed government priorities but also market realities. Retail investors received only 10% allocation, reflecting either cautious positioning or acknowledgment that PSU IPOs often underperform. The price band was set at ₹120 per share, with a lot size of 90 shares.

Market reception was tepid. The listing price on NSE was INR115 per share, down 4.17% from the IPO price of INR120, with closing price of INR113.8 per share, down 5.04% from IPO price. The discount on Day 1 signaled investor skepticism—perhaps about PSU governance, perhaps about commodity trading volatility, perhaps about business model complexity.

Investor commentary at the time captured the ambivalence: One noted MSTC's inconsistent profits as a reason for small investor allocation, but added that things would improve as MSTC operates in the growing e-commerce field, and the car shredding joint venture with Mahindra is also in a sunrise industry.

The structural challenge was clear: how do you value a company with two disparate businesses? The trading division—high revenue, low margin, volatile, capital-intensive—resembled a commodity distributor. The e-commerce division—lower revenue, high margin, recurring, capital-light—resembled a SaaS platform. Traditional metrics like P/E ratios or revenue multiples struggled to capture this duality.

Yet the IPO marked MSTC's third major inflection point. Public listing brought scrutiny, quarterly reporting pressures, investor expectations, and most importantly, market discipline. The government retained 64.75% shareholding post-IPO, ensuring continued control but allowing 35% of equity to trade freely. For the first time, MSTC faced public market judgment.

Post-listing, MSTC's challenge became clearer: demonstrate that the e-commerce platform could sustain growth independent of trading volatility, and convince markets that platform economics—not commodity distribution—defined the company's intrinsic value. Over the last 3 years from IPO, MSTC share price moved up by 94.28% on BSE, suggesting some investors eventually recognized the hidden value.

The IPO also occurred just as MSTC secured its most prestigious mandates—spectrum and coal auctions—that would validate the platform's capabilities at national scale.

VI. The Big Leagues: Spectrum, Coal, and Nation-Building Auctions (2010s–2020)

If MSTC's 2002 e-commerce launch proved the concept, and the 2019 IPO brought market visibility, winning marquee government auction mandates cemented its status as critical digital infrastructure. These weren't routine scrap disposal auctions—they were multi-billion dollar allocations of national resources where failure meant embarrassment at the highest political levels.

The 5G Spectrum Triumph

India's telecom sector transformation required periodic spectrum auctions—complex, high-stakes events where telecom operators bid for airwave rights. The amounts involved staggered: billions of dollars, shaping India's digital future. The Department of Telecommunications needed an auctioneer capable of handling sophisticated bidding mechanisms, managing intense scrutiny, and ensuring absolute fairness.

In February 2022, the DoT selected MSTC as the auctioneer for the upcoming 5G spectrum auction. This selection—over private competitors—validated MSTC's technical capabilities and government trust. The stakes were enormous.

The auction of 5G spectrum for providing services in twenty-two Licensed Service Areas started on July 26, 2022, and concluded on August 1, 2022, using SMRA (Simultaneous Multiple Rounds Ascending) e-auction methodology, conducted by MSTC.

The results were spectacular. India's 5G auction generated massive government revenues, and MSTC's platform performed flawlessly across 40 bidding rounds spanning multiple days. The company provides e-solutions for the allocation of telecom 4G/5G spectrum. The complexity was extraordinary—managing simultaneous bidding across multiple spectrum bands, different geographic circles, varying technical parameters, and intense competitive dynamics among telecom giants.

For MSTC, the 5G mandate represented validation at the highest level. This wasn't a PSU disposing of scrap—this was allocating scarce national resources that would shape India's digital economy for years. The platform's transparency, technical robustness, and audit trails proved critical. No bidder could credibly claim unfairness. No government official faced corruption allegations. The process stood as a model for transparent resource allocation.

Coal Block Auctions: Powering India's Energy Transition

If spectrum built MSTC's reputation in telecom, coal auctions demonstrated dominance in natural resources. India's coal sector history included notorious scandals—the "coalgate" controversy of 2012 involved arbitrary allocations worth billions, eventually cancelled by the Supreme Court. When the government reopened coal mining to private sector through transparent auctions, the stakes were equally high.

The sector was opened up for commercial coal mining by private players in 2020, and the first ever successful auction of commercial mining was launched by the Hon'ble Prime Minister on June 18, 2020, concluding with allocation of 19 coal mines. MSTC developed the e-bidding platform for these pioneering auctions.

The scale proved massive. MSTC provides bidding solutions for allocation of mining leases, composite licenses, critical mineral allocations, exploration licenses, royalty collection, and mine development contracts for major mineral blocks. Multiple tranches followed the first—each expanding private participation in India's coal sector.

In the 1st tranche of commercial auction, 38 mines were put on offer and 19 mines were successfully auctioned, helping create nearly 69,000 jobs and investment of over Rs 7,650 crore for the states. Subsequent rounds continued: By November 2022, the Ministry of Coal launched the 6th tranche and second attempt of the 5th tranche, offering 141 mines total.

For MSTC, coal auctions became a recurring revenue stream with strategic importance. Each successful tranche reinforced the government's confidence in MSTC's platform. The technical requirements were demanding—two-stage bidding processes, complex eligibility criteria, integration with government clearance systems, and regional variations across states.

By FY 2024-25, 18 Coal Mine blocks had been allotted for commercial mining, 77 major mineral blocks allocated for various states through auctions, and the first stage bid submission of the 11th tranche of Coal Block auction for commercial mining had been completed.

Beyond Spectrum and Coal: Platform Diversification

MSTC didn't rest on spectrum and coal laurels. The platform expanded across sectors:

Petroleum and Energy: The company developed the EXIM Portal for Petroleum Industry—the online bidding platform for Export & Import of petroleum products for Indian Oil Corporation. Oil companies needed transparent platforms for product trading and bidding.

Power Sector: MSTC facilitates power procurement, transmission contracts, and equipment purchases. State electricity boards used MSTC for tariff-based competitive bidding.

Aviation: MSTC designed an e-bidding platform to facilitate implementation of the scheme to promote air connectivity between smaller cities and bigger cities. The UDAN regional connectivity scheme leveraged MSTC's infrastructure.

Critical Minerals: MSTC developed the bidding portal for auction for leasing Critical Mineral Blocks, with 6 blocks of critical minerals auctioned in FY 2024. As India sought self-reliance in strategic minerals, MSTC provided auction infrastructure.

Minor Minerals: The company provides auction services for allocation of minor mineral and sand blocks with integrated payment and billing solutions. State governments outsourced sand mining lease auctions to MSTC.

The pattern became clear: wherever government needed to allocate scarce resources transparently, MSTC's platform emerged as default choice. The company accumulated unmatched experience. By recent counts, the company had conducted over 190,000 auctions serving more than 110,000 users.

Each new vertical created learning effects. Auction methodologies refined through coal auctions informed spectrum bidding. Payment gateway integrations developed for minerals carried over to petroleum. The platform became more robust with each deployment.

For investors, these marquee wins validated MSTC's moat. The company wasn't simply a PSU benefiting from government favoritism—it delivered complex, high-stakes projects successfully. Spectrum and coal auctions proved MSTC's technical excellence and operational reliability under pressure. These weren't commoditized services easily replicated by competitors. They were specialized capabilities built over two decades of iterative platform development.

VII. Platform Diversification: Beyond Auctions (2020–2024)

While spectrum and coal dominated headlines, MSTC quietly expanded its digital platform footprint across less glamorous but equally important sectors. This diversification wasn't about chasing revenue—it was about embedding MSTC's infrastructure deeper into India's economic fabric, creating switching costs and demonstrating platform versatility.

Agriculture: The e-RaKAM Initiative

In 2017, the government launched a new platform for selling agricultural produce named e-RaKAM (e-Rashtriya Kisan Agri Mandi), a joint initiative of MSTC and Central Warehousing Corporation.

The agricultural marketing problem in India was well-understood: fragmented mandis, middleman exploitation, opaque price discovery, and farmers lacking direct market access. E-RaKAM leveraged technology to connect farmers of the smallest villages to the biggest markets of the world through internet and e-RaKAM centres, developed by MSTC Limited and supported by marketing & logistics partner CRWC Limited.

E-RaKAM is a digital initiative bringing together farmers, FPOs, PSUs, civil supplies and buyers on a single platform to ease the selling and buying process of agricultural products, with e-RaKAM centres being developed in a phased manner throughout the country.

At launch, ambitions were substantial. The Food Minister stated the effort should be to auction 20 lakh tonnes of pulses in the first phase, noting that 20 lakh tonnes of pulses were lying idle at warehouses with no buyers, and e-RaKAM would help farmers hugely.

For MSTC, e-RaKAM represented strategic expansion beyond industrial commodities into agriculture—a sector affecting hundreds of millions of Indians. While adoption faced challenges (farmer digital literacy, logistics infrastructure, mandi resistance), the platform demonstrated MSTC's ability to customize solutions for different sectors. The same core auction technology that allocated spectrum could help farmers sell pulses.

Recycling and Sustainability: The CERO Joint Venture

CERO is a joint venture of MSTC Ltd and Mahindra Accelo, establishing the first auto shredding plant in India for recycling end-of-life vehicles and other white goods by converting these into shredded scrap, located in Greater Noida.

The recycling business addressed India's growing environmental challenges. End-of-life vehicles, electronic waste, and industrial byproducts needed organized recycling infrastructure. MSTC entered the recycling sector in 2017 through its subsidiary MMRPL, setting up an auto shredding plant for recycling end-of-life vehicles into shredded scrap, a vital raw material for steel plants.

MMRPL set up one of the organized state-of-the-art auto dismantling plants in India at Greater Noida, and established 6 Registered Vehicle Scrapping Facilities (RVSFs) in Noida, Chennai, Indore, Ahmedabad, Guwahati, and Bengaluru, plus 34 collection centers throughout India.

This vertical integration made strategic sense. MSTC's traditional scrap trading business evolved toward organized recycling, aligning with government's vehicle scrapping policy and circular economy goals. The recycling joint venture created new revenue streams while leveraging MSTC's existing scrap market knowledge.

MSTC launched an ELV (End-of-Life Vehicle) auction portal for disposal of end-of-life vehicles for Central and State Governments in compliance with the MoRTH's notified Motor Vehicles Rules, 2021, extending services for individual ELV owners also.

Real Estate and Banking Assets

As non-performing assets became a focus for Indian banking sector cleanup, banks needed transparent mechanisms to auction seized properties and stressed assets. MSTC's platform found another use case.

MSTC launched MSTC REALTY Auction Portal on January 15, 2025 for property auctions. Banks and financial institutions could list foreclosed properties, reaching broad bidder bases while ensuring process transparency.

The property auction vertical demonstrated MSTC's platform adaptability—the same technology stack supporting coal mine auctions could facilitate residential property sales. For MSTC, each new vertical added incremental revenue with minimal additional infrastructure investment.

Recent Wins: Coal India Contract

In March 2025, MSTC secured a significant mandate reinforcing its coal sector dominance. MSTC announced it had been awarded a work order from Coal India Limited to serve as the exclusive e-auction service provider for coal and coal products spanning 2 years, enabling digital auctioning of coal across CIL and its subsidiaries.

The contract covers 40% of the estimated work value and includes 166 auction events during the contract period, awarded by a domestic entity for provision of e-auction services for coal products in the Indian market.

This Coal India contract validated two critical points: First, MSTC's platform remained the preferred choice for India's largest coal producer. Second, multi-year contracts provided revenue visibility and recurring business—moving MSTC closer to predictable, subscription-like revenue streams that platform businesses enjoy.

The platform diversification strategy revealed MSTC's long-term vision: becoming the default digital infrastructure for transparent allocation and trading of goods across India's economy. Each new sector—agriculture, recycling, real estate, petroleum—added nodes to a growing network. As more stakeholders used MSTC's platform for more transactions, the switching costs increased and the competitive moat deepened.

VIII. Portfolio Optimization: The FSNL Divestment (2024)

While MSTC expanded its e-commerce platform, management simultaneously executed a strategic divestment that signaled clear priorities: exit non-core assets, focus capital on high-margin digital businesses, and streamline the portfolio.

The journey towards Ferro Scrap Nigam Limited's (FSNL) divestment began with the CCEA's 'in-principle' approval in October 2016, gaining momentum in March 2022 with the issuance of a Preliminary Information Memorandum inviting Expressions of Interest from potential bidders.

FSNL, a wholly-owned MSTC subsidiary, provided steel mill services—recovering and processing scrap from slag generated during iron and steel making. FSNL was incorporated on March 28, 1979, specializing in the recovery and processing of scrap from slag generated during iron and steel making across different steel plants.

On its face, FSNL seemed aligned with MSTC's historical scrap business. But the strategic calculus had shifted. FSNL was asset-heavy, required ongoing capital expenditure, operated in competitive steel services, and offered limited synergy with MSTC's platform e-commerce focus.

After due diligence and bidding, the highest bid submitted by Konoike Transport Co. Ltd amounted to ₹320 crore, surpassing the independently fixed reserve price of ₹262 crore, securing the acquisition with a bid of ₹320 crore.

Japan-based Konoike Transport Co. Ltd was the highest bidder for acquiring FSNL at Rs 320 crore, and after completing a two-stage open competitive bidding process, would hold 100% stake in FSNL with full management control.

The transaction closed by early 2025. DIPAM successfully completed the strategic disinvestment of Ferro Scrap Nigam Ltd at Rs 320 crore in late 2024/early 2025, transferring 100% equity and management control. Ferro Scrap Nigam Limited, a 100% owned subsidiary of the Company, was fully transferred to the new Management on January 21, 2025.

The Strategic Rationale

Why divest a profitable subsidiary? In 2023-24, MSTC posted consolidated revenue of Rs 750 crore and profits after tax of Rs 204 crore, while FSNL's revenue stood at Rs 467.72 crore with PAT of Rs 64.92 crore. FSNL contributed meaningfully to consolidated results.

Yet from a portfolio management perspective, the divestment made sense:

Capital Efficiency: FSNL required ongoing capex for steel mill equipment and operations. The Rs 320 crore proceeds freed capital for e-commerce platform development or returns to shareholders.

Strategic Focus: MSTC's competitive advantage lay in government relationships and digital platform capabilities—not steel mill services. FSNL diverted management attention from core e-commerce growth.

Valuation Arbitrage: If markets valued MSTC primarily as commodity trader rather than platform business, shedding asset-heavy operations clarified the remaining business profile. The Rs 320 crore from Konoike went to MSTC, not the government directly, given that 35% of MSTC's shares are publicly held.

Buyer Quality: Konoike Transport is an established Japanese firm with investments from global FIIs like Vanguard and BlackRock, providing credibility to the transaction.

Some controversy surrounded the valuation. Critics noted FSNL's valuation, given its assets, profitability and ability to diversify into sectors set for rapid growth, seemed low. The question was raised: how much will MSTC, which got a third of its revenues from FSNL, lose after the divestment?

Yet for investors focused on MSTC's platform business, the FSNL divestment was clarifying. It removed revenue volatility from steel sector cyclicality, simplified the business model, and signaled management's commitment to becoming a pure-play e-commerce infrastructure company. The proceeds could fund dividend returns—MSTC gave ₹45.50 dividend for the full year in recent periods—or reinvestment in platform development.

The FSNL exit marked MSTC's fourth major inflection point: strategic portfolio rationalization in service of a focused, asset-light, high-ROIC business model.

IX. The Business Model Deep Dive: Two Worlds, One Company

Understanding MSTC requires dissecting its dual personality—legacy trading and modern platform—businesses that couldn't be more different yet coexist under one corporate umbrella.

Segment 1: The E-Commerce Platform (~63% of recent revenue)

MSTC undertakes trading activities, e-commerce, and disposal of ferrous and non-ferrous scrap, surplus stores, minerals, agri and forest produce, mostly from PSUs, leading private sector entities and government departments, with core activity divided into two Operational Divisions: e-Commerce and Trading.

The e-commerce business model is elegant in its simplicity:

Revenue Model: MSTC charges service fees—typically around 12 basis points (0.12%) of Gross Merchandise Value (GMV) transacted. On a Rs 1,000 crore auction, MSTC earns approximately Rs 12 crore. Additional revenue comes from registration fees, EMD processing, software customization, and value-added services.

Cost Structure: Technology infrastructure (servers, software, security), personnel (platform development, customer support, legal compliance), and marketing. Critically, MSTC doesn't hold inventory, doesn't take commodity price risk, doesn't finance transactions. It's a pure intermediary.

Operating Leverage: Once the platform exists, incremental auctions cost little. Adding a new coal auction or property sale uses existing infrastructure. Gross margins in e-commerce segment likely exceed 70-80%, though MSTC doesn't disclose segment-level margins.

Capital Intensity: Near zero. MSTC reported revenue of 319 Cr and profit of 425 Cr recently, though earnings include other income of Rs 354 Cr. The business requires minimal working capital—bidders deposit EMDs, payments flow through the system, and MSTC remits proceeds to sellers after taking its fee.

Network Effects: Every new buyer registered makes the platform more attractive to sellers (larger bidder pool drives better price discovery). Every new seller brings more auction opportunities, attracting more buyers. This two-sided marketplace dynamic creates defensibility.

Customer Stickiness: Government departments using MSTC for auctions face high switching costs. New platforms require retraining staff, migrating bidder databases, and risking process disruptions. For high-stakes auctions (spectrum, coal), trust in tested platforms exceeds cost considerations.

Scalability: The platform can theoretically handle unlimited GMV without proportional cost increases. A Rs 1 lakh crore auction year generates 10x the fee revenue of a Rs 10,000 crore year, but doesn't require 10x the technology spending.

The platform exhibits classic digital marketplace characteristics: low marginal costs, high gross margins, network effects, and scalability. This is the business investors should value using platform multiples—not commodity distributor multiples.

Segment 2: Trading/Marketing Business (~37% of revenue)

The trading division handles import/export and domestic trade of mainly bulk industrial raw material, looking after sourcing, purchase and sales of industrial raw materials like Heavy Melting Scrap, Low Ash Metallurgical Coke, HR Coil, Crude Oil, Naptha, Coking Coal, Steam Coal etc for supply to Indian industries.

This business operates fundamentally differently:

Revenue Model: MSTC acts as facilitator/trader, buying or arranging purchase of commodities and selling to industrial customers, earning markup percentage on transaction value.

Cost Structure: Working capital (financing inventory or arranging letters of credit), logistics (freight, insurance), credit risk (customer defaults), commodity price risk (prices changing between purchase and sale).

Operating Leverage: Limited. Each transaction requires similar working capital and logistics effort. Volumes scale linearly with capital deployed.

Capital Intensity: High. Commodity trading ties up cash in inventory and receivables. Steel, coal, and petroleum transactions involve large ticket sizes and payment cycles.

Margins: Thin. Competitive commodity markets limit pricing power. Gross margins likely in single digits, net margins even thinner.

Volatility: Extreme. Commodity prices swing with global markets, demand fluctuations, currency movements. Quarterly revenue varies dramatically based on deal timing and volumes.

Differentiation: Minimal. MSTC competes with numerous commodity traders. Relationships and reliability matter, but offer limited moat.

For investors, the trading business is the anchor—high revenue visibility but low margins, capital-intensive, cyclical, and ultimately a distraction from the platform business gem.

The Valuation Puzzle

Recent reporting showed MSTC with Mkt Cap of 3,755 Crore, revenue of 319 Cr, and profit of 425 Cr, with earnings including other income of Rs 354 Cr.

The financial statement mixing creates confusion. High trading revenue inflates top line but contributes marginally to profit. E-commerce revenue appears smaller but generates most profit. "Other income" (likely including treasury income, FSNL dividends before divestment, and one-time gains) further clouds operating performance.

For the year ended 2025, MSTC posted a profit of Rs 407.07 crore on total income of Rs 310.96 crore. Profit exceeding revenue suggests significant other income, not operating performance.

Isolating e-commerce segment performance requires forensic analysis:

- Auction event counts growing (200,000+ cumulative events conducted)

- GMV expanding as marquee auctions (spectrum, coal) repeat and new verticals launch

- Operating leverage improving as fixed platform costs spread across growing transaction volumes

For fundamental investors, the critical task is looking through accounting complexity to understand the underlying platform business economics, which management's capital allocation (divesting FSNL, focusing on e-commerce expansion) increasingly clarifies.

X. The Competitive Moat: Why MSTC Wins

In business, sustainable competitive advantages determine long-term value creation. MSTC's moat—while not impenetrable—combines several reinforcing elements that create meaningful barriers to competition.

Trust and Government Relationships: The Intangible Foundation

MSTC is a Mini Ratna Category-1 CPSE under the Ministry of Steel, with Government of India holding 64.75% shareholding. This ownership structure isn't just financial—it signals credibility. For government departments considering e-auction providers for sensitive transactions (natural resource allocation, strategic asset sales), a government-owned entity carries presumptive trustworthiness that private competitors must overcome.

Six decades of operating history matter. MSTC's institutional memory, bureaucratic navigation skills, and understanding of government procurement norms create soft barriers. Private competitors may offer slicker technology, but they lack relationship depth built over generations.

MSTC's auction services eliminate manual inefficiencies and foster trust through unbiased processes, with transparency eliminating manual inefficiencies and fostering trust.

Technical Capabilities: Proven at Scale

MSTC conducted the 5G spectrum auction using SMRA (Simultaneous Multiple Rounds Ascending) e-auction methodology. Successfully executing spectrum auctions—with multiple simultaneous bidding rounds, real-time bid processing, complex eligibility rules, and zero tolerance for technical failures—demonstrates capabilities few competitors can match.

These aren't simple English auctions. Spectrum and coal block bidding involve sophisticated mechanisms: activity rules preventing strategic withdrawal, clock rounds with price increments, package bidding with combinatorial constraints. MSTC developed and deployed software handling this complexity reliably.

The company conducted over 190,000 auctions serving more than 110,000 users. This scale creates learning effects—each auction generates data improving algorithms, user interfaces, and exception handling. Competitors starting today face significant experience gaps.

First-Mover Advantages and Network Effects

MSTC launched its e-auction portal in 2002, emerging as the leading e-auction service provider in the country. Being first in government e-auctions created lasting advantages:

Bidder Database: Over 110,000 registered users represent valuable network effects. Buyers register once to access multiple auctions across sectors. This installed base makes MSTC's platform default choice—bidders check MSTC first for opportunities.

Seller Familiarity: Government procurement officers trained on MSTC's platform prefer familiar systems. Switching costs include retraining, process documentation updates, and risking delays. Inertia favors incumbents.

Data and Insights: Two decades of auction data—bid patterns, price outcomes, participation trends—inform platform improvements and client guidance that new entrants lack.

Regulatory Positioning: Coexistence with GeM

MSTC provides bidding solutions for allocation of mining leases, composite licenses, critical mineral allocations, and auction services for minor mineral and sand blocks with integrated payment and billing solutions.

India's Government e-Marketplace (GeM) handles procurement—buying goods and services. MSTC handles sales—disposing government assets and allocating scarce resources. This division of labor reduces direct competition with GeM while creating complementary positioning. For investors, the existence of GeM validates government e-commerce platforms generally and confirms MSTC's niche in the selling/allocation space.

Pan-India Presence

MSTC has offices at 21 locations across India with four regional offices at Kolkata, Mumbai, Chennai and New Delhi, plus 13 branch offices across Ranchi, Guwahati, Bhubaneswar, Lucknow, Chandigarh, Bhopal, Raipur, Jaipur, Vadodara, Bangalore, Trivandrum, Vizag and Hyderabad.

Physical presence matters for government clients preferring face-to-face interactions, local language support, and regional relationship management. While technology enables remote operations, bureaucratic comfort with local presence persists. Competitors replicating 21-office national footprints face significant fixed costs.

Moat Limitations and Vulnerabilities

Honest assessment requires acknowledging moat weaknesses:

Technology Disruption: Better-funded tech companies could build superior platforms. Cloud infrastructure democratizes technology development, reducing barriers to entry.

Competition Emerging: Private e-auction platforms are proliferating. MSTC faces growing competition from well-capitalized players in specific verticals.

Government Ownership: PSU structure limits agility. Decision-making bureaucracy, hiring constraints, and political considerations slow innovation relative to private competitors.

Concentration Risk: Revenue heavily dependent on government clients. Policy changes, budget constraints, or privatization could disrupt business model.

The moat exists but isn't unassailable. MSTC's advantages are substantial but require continuous reinforcement through platform improvement, client service, and strategic positioning. For investors, the key question is whether MSTC can sustain advantages long enough to justify platform business valuations.

XI. Financial Performance & Market Perception

MSTC's financial story reflects its dual business complexity—impressive profitability occasionally overshadowed by revenue volatility, strong recent results clouded by accounting nuances, and market valuation disconnected from underlying business quality.

Recent Financial Highlights

MSTC reported a massive 506.04% year-on-year jump in net profit reaching ₹250.9 crore for Q3 ended December 31, 2024, compared to ₹41.4 crore in Q3FY24, attributed to exceptional gain of ₹275.5 crore in Q3FY25 versus loss of ₹1.9 crore in Q3FY24.

The 500%+ profit jump grabbed attention but required context—exceptional items drove the surge, not operating improvements alone. For the year ended 2025, MSTC posted profit of Rs 407.07 crore on total income of Rs 310.96 crore. Profit exceeding revenue confirms substantial other income.

In Q1 FY 2025-2026, MSTC's revenue jumped 8.89% year-over-year to ₹93.66Cr, though showing -16.4% fall quarterly, while net profit jumped 7.85% YoY to ₹42.34Cr but fell -43.93% quarterly.

The quarterly volatility reflects trading business lumpiness—large commodity transactions timing affects quarterly comparisons. E-commerce revenue tends toward stability, but gets masked by trading swings.

Profitability and Returns

MSTC's net profit margin stood at 45.21% in Q1 2025-2026. Margins exceeding 40% signal the e-commerce segment's profitability contribution. Traditional trading generates single-digit margins—the blended 45% suggests e-commerce dominance in profit pools.

Return ratios impress: Reports indicate ROE above 50% and minimal debt. The company maintained a low Debt-Equity Ratio of 0.15 times, indicating reduction in borrowing relative to equity capital. Asset-light e-commerce generates high returns on capital—precisely what platform businesses should deliver.

Balance Sheet Strength

MSTC carries minimal debt and substantial cash. The company is essentially debt-free, with strong liquidity supporting operations. Following FSNL divestment, cash position strengthened further with Rs 320 crore proceeds.

MSTC has issued bonus shares multiple times—1:1 in 1992-93, 3:1 in 2011-2012, 1:1 in 2015-16, 1:1 in 2016-17, and 1:1 in 2018-19, with current paid-up capital of Rs 70.40 Crores, and is a regular dividend paying company.

Dividend Story

In the quarter ending December 2024, MSTC declared dividend of ₹4.50 translating to dividend yield of 8.73%, having declared dividend worth ₹40.50 in the last year, with latest dividend declared on March 26, 2025.

High dividend yields reflect strong cash generation and shareholder-friendly management. The dividend policy balances rewarding investors with retaining capital for platform investment.

Stock Performance: A Tale of Volatility

Over the last 3 years, MSTC share price moved up 94.28% on BSE. Long-term holders enjoyed substantial appreciation from post-IPO levels.

Yet volatility dominated: Recent 52-week low was Rs 411.1 and 52-week high was Rs 809.75, with 6-month returns showing 2.21% increase but 1-year decline of 28.42%. The stock saw -28.75% returns over last 6 months and -43.67% over last year.

The wide trading range reflects market confusion—is MSTC a trading company (deserving low multiples) or platform business (justifying premium valuations)? Quarterly result swings driven by trading volatility and other income create momentum trading rather than fundamental accumulation.

Valuation Disconnect

Promoter holding stands at 64.8%. With 35% free float and market cap around Rs 3,750 crore recently, MSTC trades at relatively modest valuations compared to private e-commerce platforms.

The valuation puzzle persists: Comparable platform businesses (digital marketplaces, transaction processors, SaaS companies) trade at 10-20x revenue multiples based on growth and margins. MSTC's e-commerce segment—if valued independently—arguably deserves similar multiples. Yet consolidated trading obscures this value.

For sophisticated investors, MSTC presents a sum-of-the-parts opportunity: Assign low multiples to declining trading business, platform multiples to growing e-commerce business, and unlock the "hidden value" as FSNL divestment and operational focus clarify the story.

XII. Challenges & Headwinds

No investment thesis is complete without clear-eyed assessment of risks and challenges. MSTC faces structural and cyclical headwinds that could impair future performance.

Trading Business Decline

The company delivered poor sales growth of -24.1% over past five years. This decline primarily reflects trading business challenges—commodity markets are competitive, margins compressed, and MSTC's differentiation limited.

As trading revenue shrinks, consolidated top-line growth appears weak even if e-commerce thrives. Markets focused on revenue growth may miss the business mix improvement occurring beneath surface declines.

Competitive Pressures Intensifying

Private e-commerce platforms are proliferating across India. Well-funded startups bring superior technology, aggressive pricing, and entrepreneurial speed. While MSTC enjoys government relationships, private competitors target corporate clients and specific verticals where incumbency advantages matter less.

Technology giants (Google, Amazon, Microsoft) could theoretically enter government e-commerce with platform capabilities and capital dwarfing MSTC. While government preference for domestic PSUs provides near-term protection, long-term competitive dynamics are uncertain.

Government Ownership Constraints

PSU structure creates drag on agility:

Hiring Limitations: Government recruitment procedures and pay scales make attracting top technology talent difficult. Private competitors offer stock options, faster career progression, and startup culture that MSTC cannot match.

Decision-Making Bureaucracy: Major decisions require government approvals, slowing strategic pivots. Private competitors iterate faster.

Political Considerations: Government ownership means political pressures—employment protection, regional expansion mandates, pricing constraints—that may conflict with shareholder value maximization.

Privatization Risk: While current government privatizes PSUs, MSTC's strategic importance (running spectrum auctions) might protect it. Yet policy uncertainty creates overhang.

Revenue Concentration Risk

Heavy dependence on government clients creates vulnerability. Government budget constraints, policy changes favoring other platforms (GeM expansion into MSTC's territory), or privatization of major clients (Coal India, oil PSUs) could disrupt revenues.

Large marquee auctions (spectrum, coal) recur irregularly—creating lumpiness. A year without major spectrum auction significantly impacts results. Diversification across many smaller verticals helps but doesn't eliminate concentration.

Technology Debt and Innovation Pace

Platform businesses require continuous technology investment. MSTC's systems, developed over two decades, may carry technical debt—legacy code, outdated architecture, security vulnerabilities. Modernizing infrastructure while maintaining operational continuity challenges any organization, especially PSUs with procurement constraints.

The pace of innovation—mobile-first experiences, AI-powered bidding, blockchain for transparency, advanced analytics—may exceed MSTC's capability to deliver given resource and talent constraints. Falling behind technologically could erode competitive position.

Regulatory and Legal Risks

Government auctions involve high stakes and aggrieved parties. Spectrum losers, unsuccessful coal bidders, and others may legally challenge auction processes. While MSTC's transparent platforms minimize legal exposure, any successful challenge questioning auction integrity could damage reputation catastrophically.

Evolving data privacy regulations, cybersecurity requirements, and procurement norms create compliance burdens. A significant data breach or security incident affecting a major auction would severely harm credibility.

Macroeconomic Sensitivity

Mining auctions depend on commodity demand—if coal, minerals, or petroleum markets collapse, government auction activity slows. Infrastructure spending, government budgets, and industrial activity all correlate with MSTC's business volumes.

Economic slowdowns particularly hurt trading business, which amplifies consolidated revenue volatility and diverts management attention from e-commerce growth.

XIII. The Bull Case: India's Digital Infrastructure Play

Despite challenges, the bull case for MSTC rests on powerful secular trends, strategic positioning, and underappreciated platform economics.

India's Digital Transformation: Tailwinds for Decades

India's government digitization remains early innings. The Digital India mission aims to make government services digitally accessible, transparent, and efficient. Every ministry, department, PSU, and state government becomes potential MSTC client.

Current e-auction penetration in government sales/procurement likely below 30-40% economy-wide. As digitization mandates expand, MSTC's addressable market expands proportionally. The shift from manual to digital processes isn't cyclical—it's structural and irreversible.

Growing Government Auction Activity

India's development requires allocating scarce resources—spectrum for connectivity, coal for energy, minerals for manufacturing, land for infrastructure. Each allocation increasingly occurs through transparent auctions rather than administrative allocation (which invites corruption).

The coal sector opened for commercial mining by private players in 2020, with first successful auction launched June 18, 2020, concluding with 19 mine allocations. This privatization trend creates recurring auction opportunities as government opens sectors.

Spectrum auctions recur every few years as technology evolves (5G, eventually 6G) and licenses expire. Government may launch 5G at Indian Mobile Congress, with India joining the elite club of seventy countries offering 5G services, with services expected in thirteen cities in first phase by end of 2022. Each spectrum auction generates significant MSTC revenues.

Critical minerals, renewable energy projects, stressed asset sales, privatizations—all create auction opportunities where MSTC's platform advantages matter.

Platform Economics: Operating Leverage Kicking In

The beautiful aspect of platform businesses: as GMV grows, incremental margins expand. MSTC's technology infrastructure handles Rs 10,000 crore or Rs 1 lakh crore GMV with similar fixed costs. Every incremental auction drops disproportionate profit to bottom line.

Experience from conducting more than 190,000 events has given MSTC confidence to develop any customized auction platform to suit client requirements. This accumulated expertise means new verticals launch faster and cheaper than initial platform development.

Asset-Light, High-ROIC Business Model

Following FSNL divestment, MSTC increasingly resembles a pure-play platform business. Minimal capital requirements, high cash generation, strong returns on equity—characteristics typically rewarded with premium valuations.

The company can return capital through dividends or buybacks while simultaneously investing in platform growth. Unlike capital-intensive businesses requiring earnings retention, MSTC can do both.

International Expansion Potential

While currently India-focused, MSTC's platform capabilities could address similar needs in other developing economies. Government transparency challenges aren't unique to India. MSTC could export technology and expertise to South Asia, Africa, or Southeast Asia—markets where government credibility and transparent resource allocation remain works in progress.

Undervalued Relative to Comparables

If MSTC's e-commerce business were valued at even 5-10x revenues (conservative for platform businesses showing 40%+ margins), it would justify market caps significantly above current levels. The market appears to value MSTC as trading company plus modest e-commerce, rather than recognizing the platform business potentially worth multiples of current valuation.

As management clarifies the story (FSNL exit, e-commerce focus), trading segment revenue declines, and platform business metrics (GMV, auction counts, unique users) receive disclosure emphasis, rerating potential exists.

Government Digital India Push

Political will behind digitization creates institutional support for MSTC's business model. Government actively seeks to showcase transparent auction successes (spectrum, coal) as governance achievements. This high-level support translates to departmental budgets for e-auction adoption and mandates favoring electronic processes.

XIV. The Bear Case: What Could Go Wrong

Intellectual honesty requires presenting the strongest counterarguments to bullish narratives.

Technological Disruption from Superior Platforms

A well-funded private competitor—or technology giant—could build markedly superior platform with better user experience, faster performance, advanced analytics, and aggressive pricing. If government clients prioritize technology excellence over incumbency, MSTC could lose marquee mandates.

Private companies iterate faster, attract better talent, and deploy capital more efficiently. MSTC's PSU constraints may prove fatal in technology arms race.

Government Policy Shifts

Political winds change. A future government prioritizing privatization might sell MSTC to private buyers or shift auction mandates to GeM (the government procurement platform) as it expands. Policy changes favoring international auction houses or decentralized blockchain-based allocation could disrupt MSTC's business model.

Budget pressures might force government departments to minimize auction costs, compressing MSTC's fees. Mandates requiring lowest-cost bidding could undermine quality-based selection favoring MSTC.

Trading Business: Value Trap

The trading business decline might accelerate, overwhelming e-commerce growth. If commodity trading losses mount and drag consolidated profitability, investor patience could evaporate before platform value realizes.

Markets might permanently assign "PSU trader" multiple to MSTC, regardless of underlying business mix improvement. Value trap risk—where cheapness persists indefinitely without catalyst for rerating—is real.

Execution Missteps

Platform businesses live or die on technology execution. A major system failure during high-profile auction (spectrum, coal)—causing delays, bid processing errors, or security breaches—could irreparably damage MSTC's reputation.

Government clients have low tolerance for operational failure in high-stakes events. One catastrophic incident could undo two decades of credibility building.

Limited TAM (Total Addressable Market)

Perhaps government sales/auctions simply aren't large enough market to support major valuation. If most government transactions occur through GeM (procurement) rather than MSTC (sales), and if auction frequency and volumes remain modest, the business might be "good but small"—profitable niche rather than transformative platform.

PSU Discount Persists

Markets may forever discount PSU equities due to governance concerns, political interference, and bureaucratic inefficiency—regardless of business quality. Even if MSTC executes perfectly, the stock might trade at persistent discount to private comparables, limiting wealth creation for public shareholders.

Competition Already Intensifying

It's possible private competitors have already caught up or surpassed MSTC in technology, and MSTC's market position erodes from here. Network effects might be weaker than bulls believe, and clients might switch more easily than anticipated.

The bear case fundamentally questions whether MSTC's competitive advantages are durable and whether platform economics will drive valuation rerating or remain hidden indefinitely under trading volatility and PSU structure.

XV. Comparison: IRCTC & The PSU E-Commerce Playbook

MSTC's valuation and growth trajectory naturally invite comparison with Indian Railway Catering and Tourism Corporation (IRCTC)—another government-owned monopoly-turned-platform that captured investor imagination.

Structural Similarities

Both started as government service providers with monopolistic characteristics. MSTC is a Mini Ratna Category-1 CPSE under Ministry of Steel. IRCTC similarly operates under Ministry of Railways. Both serve critical government functions—MSTC facilitating transparent auctions, IRCTC enabling railway ticketing.

Both are B2B or B2G (business-to-government) primarily, though IRCTC has significant B2C (catering, tourism). Both transformed from manual processes to digital platforms. Both enjoy government relationships as competitive advantage.

Business Model Differences

Volume vs. Value: IRCTC handles massive transaction volumes—millions of daily railway tickets—at low per-transaction value. MSTC handles lower volume (thousands of auctions annually) at massive per-transaction value (spectrum auctions worth billions).

Customer Base: IRCTC is predominantly B2C—millions of retail consumers booking train tickets. MSTC is B2B/B2G—government departments and corporate bidders. This distinction affects growth potential, customer acquisition costs, and business volatility.

Revenue Model: IRCTC charges convenience fees per ticket plus catering margins and tourism commissions. MSTC charges auction service fees as percentage of GMV or fixed event fees. Both are transaction-based, but MSTC's revenue correlates more with commodity prices and auction activity than IRCTC's volume-driven model.

Market Perception and Valuation

IRCTC captured investor imagination, achieving market cap peaks exceeding Rs 80,000 crore despite relatively modest revenues. The market recognized monopolistic railway ticketing platform with growing ancillary revenues as high-quality franchise deserving premium valuation.

MSTC, with market cap around Rs 3,750 crore, trades at fraction of IRCTC's peak despite arguably stronger economics (B2B typically more defensible than consumer, auction GMV potentially unlimited). The valuation gap partly reflects:

Brand Recognition: Every Indian knows IRCTC from booking train tickets. Few consumers know MSTC—it's B2B, operating behind scenes.

Growth Narrative: IRCTC told clear story of digitizing Indian Railways, expanding into tourism and payments. MSTC's story—buried under commodity trading—lacked clarity until recently.

Liquidity: IRCTC had higher free float and trading volumes, attracting institutional investors and momentum traders. MSTC with 64.75% government holding has smaller free float limiting liquidity.

Can MSTC Achieve IRCTC-Style Rerating?

The question for investors: Does MSTC have potential for IRCTC-like valuation transformation?

Bulls argue: Once markets understand MSTC's platform economics—especially post-FSNL divestment clarifying business mix—rerating is inevitable. The e-commerce vertical alone could justify multiples of current market cap if valued as platform business.

Bears counter: IRCTC had unique monopoly on essential consumer service touching 20+ million daily passengers. MSTC's government auction niche, while valuable, lacks comparable scale and isn't irreplaceable—government could theoretically move auctions in-house or to private providers.

The realistic middle ground: MSTC may achieve partial rerating as e-commerce story clarifies, but expecting IRCTC-level valuations seems aggressive given structural differences. More probable is MSTC trading at premium to commodity traders but discount to pure-play digital platforms—reflecting hybrid characteristics.

Other PSU Digital Comparables

GeM (Government e-Marketplace): Unlisted, handles government procurement (buying vs. MSTC's selling). Both demonstrate government e-commerce viability but serve complementary functions.

MSTC vs. GeM: GeM addresses larger TAM (all government procurement vs. MSTC's sales/auctions), but procurement involves more complex supplier onboarding, quality control, and logistics—potentially lower margins than MSTC's transaction facilitation.

The broader lesson: PSU digital platforms with defensible positions and platform economics can achieve premium valuations once markets recognize business quality beneath government ownership structure. MSTC's challenge is telling that story convincingly.

XVI. The Future: What's Next for MSTC

MSTC's trajectory over next 3-5 years will likely determine whether the company remains niche PSU or transforms into recognized digital infrastructure provider deserving premium valuations.

Strategic Priorities: E-Commerce Uber Alles

Post-FSNL divestment signals management priorities: grow e-commerce platform, divest non-core assets, and clarify value proposition. Expect continued focus on:

Vertical Expansion: Launching platforms for new sectors—stressed assets, environmental credits, carbon markets, infrastructure projects, privatization auctions. Each vertical adds incremental high-margin revenue.

Technology Upgrades: Platform modernization—mobile-first interfaces, AI/ML for fraud detection, blockchain for audit trails, advanced analytics for clients. Staying technically competitive requires sustained investment.

Geographic Expansion: Deeper penetration of state governments and PSUs not yet using MSTC. Currently concentrated in central government and major PSUs—state-level adoption could double addressable market.

New Verticals: High-Growth Opportunities

Environmental Credits: MSTC developed bidding portal for critical mineral blocks with 6 blocks auctioned in FY 2024, and launched comprehensive Steel Import Management System SIMS 2.0 for Ministry of Steel in FY25. As India implements carbon trading, renewable energy certificate markets, and EPR (Extended Producer Responsibility) mechanisms, MSTC could provide auction infrastructure.

The tender committee of Central Pollution Control Board recommended MSTC for development and operation of Electronic Trading Platform for EPR Certificates—potentially large new vertical.

Privatization Auctions: As government privatizes PSUs, transparent auction mechanisms will facilitate stake sales to strategic buyers. MSTC could become preferred platform for government disinvestments.

International Markets: MSTC's platform capabilities address universal needs—transparent resource allocation, government auction infrastructure, procurement digitization. Exporting technology and expertise to neighboring markets could open greenfield growth.

Financial Outlook

Base case assumes: - E-commerce GMV growing 15-20% annually as existing verticals (coal, minerals) expand and new verticals launch - Commission rates stable around 10-15 basis points, though may compress with scale - Trading business declining 5-10% annually as MSTC de-emphasizes commodity distribution - Consolidated revenue flat to modest growth, but profit growing 10-15% as high-margin e-commerce increases contribution

Bull case adds: - Major new verticals (environmental credits, privatizations) launching successfully - International expansion bearing fruit - Platform technology licensing to other countries/entities - 20%+ profit CAGRs as operating leverage kicks in

Bear case involves: - Competition eroding market share in coal/minerals - Marquee auction mandates lost to private competitors - Trading business losses offsetting e-commerce gains - Flat to declining profitability

Shareholder Returns: Dividend vs. Reinvestment

MSTC's cash generation and minimal capex requirements enable generous dividends. Recent dividend yields approached 8-9%, attractive for income-focused investors.

Yet platform businesses thrive on reinvesting for growth—technology development, market expansion, talent acquisition. The tension between returning cash to shareholders (including 65% government owner wanting dividend income) and reinvesting for growth will define capital allocation.

Optimal strategy likely balances both: maintain healthy dividend yields (4-6%) while retaining sufficient capital for platform investment. Share buybacks could return capital while supporting stock price.

Potential Catalysts for Rerating

What might trigger market revaluation recognizing platform business quality?

Clean Financial Reporting: Separate segment disclosure clarifying e-commerce economics—GMV, commission rates, segment margins, operating leverage. Currently, consolidated reporting obscures platform performance.

Strategic Communication: Management articulating vision—"We are digital infrastructure provider for government resource allocation"—rather than identity confusion between trader and platform.

Marquee Wins: Securing major new mandates (privatization auctions, carbon markets, international contracts) validating growth potential.

Further Divestments: Exiting remaining trading operations entirely, becoming pure-play e-commerce platform.

Analyst Coverage: Attracting research coverage from analysts who understand platform businesses, educating institutional investors.

Inclusion in Indices: Qualifying for key indices increasing passive fund ownership and liquidity.

The 2030 Vision

Optimistically, MSTC in 2030 could be: - India's largest government e-commerce platform by GMV - Handling 90%+ of major government resource allocation auctions - Expanded into 5-10 new verticals (environmental, privatization, international) - Technology platform licensed to other countries - Market cap multiple of today's levels as platform economics recognized - Potentially privatized or majority stake divested to strategic partner

Pessimistically, MSTC could remain: - Niche PSU handling certain auctions - Facing intensifying private competition - Constrained by bureaucratic structure - Valued as commodity trader with e-commerce side business - Limited growth and modest shareholder returns

The most probable outcome lies between extremes: MSTC solidifies position as leading government e-auction provider, grows steadily, improves margins, returns decent shareholder value, but never becomes transformative compounder that bulls envision.

For investors today, MSTC represents classic "special situation"—company undergoing transformation, hidden value beneath complex financials, optionality from multiple growth vectors, but execution risk and valuation uncertainty. Those who study carefully, buy patiently, and hold through volatility may be rewarded as the platform business story clarifies. Those seeking certainty and liquidity should look elsewhere.

Conclusion: A Story Still Being Written

MSTC's journey from 1964 scrap metal regulator to 2025 digital infrastructure provider spans six decades of adaptation. The company survived liberalization's existential threat, reinvented itself through e-commerce, won marquee mandates validating capabilities, and now stands at another inflection point.

The fundamental investment question persists: Is MSTC a declining commodity trader with digital side business, or a platform company with legacy trading operations obscuring value? Management's actions—divesting FSNL, expanding e-commerce verticals, focusing on high-margin businesses—suggest the latter. Market valuation suggests the former.

This disconnect creates opportunity for patient, analytical investors willing to look beyond accounting complexity and PSU skepticism to recognize underlying platform economics. MSTC won't achieve IRCTC-level valuations, but rerating from "PSU trader" to "government e-commerce platform" multiples could generate substantial returns.

The story is still being written. Whether MSTC's next chapter involves transformative growth, steady compounding, or disappointing stagnation depends on execution, competition, government support, and market recognition. For those following the narrative closely, MSTC offers a fascinating case study in business transformation, strategic positioning, and the challenge of uncovering hidden value in complex organizations.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube