MPS Limited: The Platform Play for Global Knowledge

I. Introduction & The "Captive" Thesis

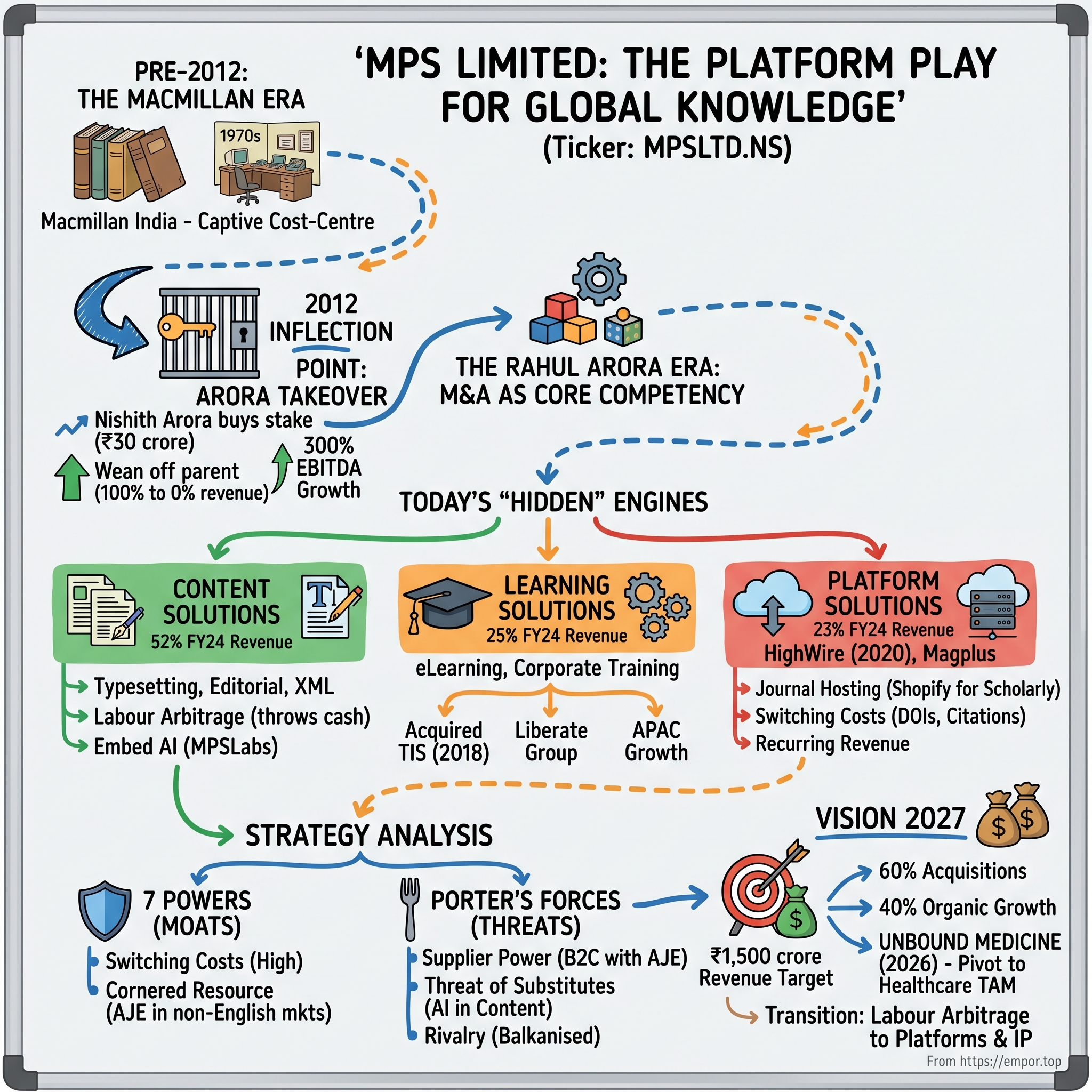

Picture a non-descript office block in central Bengaluru in the mid-1970s. The signage reads "Macmillan." Inside, rows of Indian typesetters bend over keyboards, encoding the manuscripts of professors at Cambridge, Oxford and the LSE so that — eight time zones away — a printing press in Basingstoke can spin up to feed the world's libraries. The office had been inaugurated in 1976 by former British Prime Minister Harold Macmillan himself, a member of the same Scottish-publishing family that founded the firm in 1843.1 To the people who worked there, this was a prestigious posting. To the parent company in London, it was something quieter and more useful: cheap, English-literate labour, plugged into the back end of a 170-year-old publishing empire.

Fast-forward fifty years, and the descendant of that captive back-office — एमपीएस लिमिटेड MPS Limited — is no longer in the typesetting business in any meaningful sense. It owns HighWire Press, the platform on which the British Medical Journal, the American Association for the Advancement of Science and hundreds of other scholarly societies host the entirety of their research output. It owns Research Square / American Journal Experts, the service that researchers in 中国 China and Brazil use to get their manuscripts into English before submitting to Springer Nature. It owns Tata Interactive Systems, an e-learning house that used to belong to the टाटा Tata Group. It owns Liberate Learning in Australia and, as of February 2026, Unbound Medicine in the United States — a clinical-decision-support business that puts MPS, of all people, into the AI-and-healthcare conversation.2 Market cap, depending on the day, hovers around the rupee equivalent of $400-500 million. EBITDA margins sit north of 25%.

How did a captive cost-centre in Bengaluru, with no external customers and no incentive to invent anything, end up as a buy-and-build platform compounder selling into Washington, Stockholm, Sydney and Beijing? That is the story of this episode. The short answer is that in October 2011, Macmillan sold the entire thing — its majority stake in what was then called Macmillan India / MPS — for somewhere in the region of ₹30 crore (roughly $6 million at the time) to a relatively low-profile Indian BPO entrepreneur named Nishith Arora, operating through a vehicle called ADI BPO Services.3 Within a year, the new owner had a single, slightly insane operating instruction: take Macmillan's share of revenue from 100% to zero. Build the company that the captive could never have become from inside the cage.

The long answer is more interesting, because what emerged from that decision was a rare specimen in Indian capital markets: a company that successfully moved from labour arbitrage (you pay us in dollars, we pay our staff in rupees, the spread is our gross margin) to platforms and IP (you pay us in dollars to host your content, and our marginal cost of serving you is close to zero). That transition — the one Indian IT services has been theoretically attempting for two decades — is the heart of what we're going to unpack. We'll meet two operators, father and son, who ran a textbook five-year succession; an M&A playbook that has now executed seven deals across three continents; and a thesis about what happens when scholarly publishing collides with generative AI. By the end, the question you should be asking is not whether MPS pulled off the transition — that part is largely done — but whether the next leg, into healthcare knowledge and AI, will re-rate the company or expose the limits of a roll-up. Let's start where the cage was built.

II. Pre-2012: The Macmillan Era

The opening scene of MPS's story is not glamorous. It is 1970, the Indian economy is socialist and inward-looking, foreign exchange is rationed, and the Indian government is more or less actively hostile to multinationals — five years away, in fact, from the FERA-driven exodus that would push Coca-Cola and IBM out of the country. Macmillan, the venerable British publisher, set up an Indian subsidiary essentially to handle the Indian market for its textbooks — schools, universities, the post-colonial appetite for English-language educational content.1 The Information Processing Division — the back-office typesetting business that would eventually become "MPS" in its own right — was bolted on in the mid-1970s, when Harold Macmillan himself flew out to inaugurate the Bangalore facility. The logic was unromantic and powerful: every page of every book Macmillan published, anywhere in the world, had to be typeset, copy-edited, indexed and formatted. India had cheap English-speaking graduates. Do the math.

For the next three decades, the Indian operation hummed along quietly as a back-office for the parent. Its job was to convert manuscripts into print-ready PDFs and, eventually, XML files. Its customer was Macmillan. Its margin was whatever Macmillan UK chose to give it under transfer-pricing — the textbook "cost-plus" arrangement that captive units the world over operate under. It was not loss-making. It was not particularly profitable either. It was, in the language of the venture business, a captive: it existed to serve a single internal user, and it would scale exactly as fast as that user needed it to.

The structure had two pernicious effects that took years to surface. First, it killed the sales DNA. A captive has no salespeople in any meaningful sense — there is nothing to sell, because the customer is in-house. Second, it killed pricing discipline. When your only customer is your parent, you don't price for value; you price for survival, with a thin spread above cost. Both of those deficiencies would, eventually, become MPS's biggest reconstruction projects in the post-2012 era. Through the late 1990s and 2000s, the Indian subsidiary did expand modestly — taking on overflow work from other Macmillan operating units, even doing some outside work for smaller publishers — but the cultural centre of gravity remained in London, and the operating cadence was set by a calendar made in Basingstoke.

The first crack came in 2009. Macmillan, by then part of the German Holtzbrinck publishing group, decided to split its Indian business in two: the textbook publishing arm (which would keep the Macmillan brand and serve the Indian schools market) and the technology services arm — the back-office typesetting, conversion and editorial production business — which would be renamed MPS Limited.1 To English readers, "MPS" stood for nothing dramatic; it was originally just "Macmillan Publishing Solutions." But the demerger did something important: it gave the back-office business its own legal identity, its own listing on the NSE and BSE, its own balance sheet — and, crucially, made it independently saleable.

Why would Macmillan want to sell it? Because by 2009, the math of being a captive owner had inverted. Scholarly publishing was consolidating fast — Elsevier, Springer, Wiley were the big three — and the production work, the actual typesetting and XML conversion, was becoming a commodity. Macmillan UK had no particular interest in owning a labour-arbitrage business in Bengaluru; it wanted to focus on owning content and brands (Nature, Palgrave, Macmillan Education) and to buy production capacity as a service from whoever was cheapest. The Indian subsidiary was, in other words, an asset on the wrong side of a strategic line. And once the demerger had separated it from the schools publishing business (which Macmillan did keep), the technology arm was simply a non-core orphan looking for a home.

So the captive — the safe, slow, single-customer cage — was put up for sale. The buyer, when he arrived, was not who anyone in Basingstoke had expected.

III. The 2012 Inflection Point: The Arora Takeover

The man who walked away with Macmillan's Indian back-office in October 2011 was Nishith Arora. He was not a publishing executive. He was not a global private-equity titan. He was the founder of a quiet, mid-sized BPO services firm called ADI BPO Services, and his particular interest was in something the publishing world had largely ignored: the same back-office labour arbitrage Macmillan was trying to offload, but run as a profit centre with multiple customers, not as a single-customer cost-centre. ADI had been in scholarly content services for years; what Arora saw on Macmillan's balance sheet was not a back-office, but an asset that — under different ownership — could be repositioned as a third-party vendor to all of Macmillan's competitors. The price he paid was roughly ₹30 crore for the controlling stake, and on December 7, 2011, he took his seat as an Additional Director on the board.3

The numbers that followed are worth pausing on, because they explain why this transaction — small by global M&A standards, almost invisible in the Indian press — is a kind of legendary trade in the back-channels of Indian capital allocation. Over the FY12-to-FY14 window, revenue grew roughly 23%, but EBITDA grew about 300% and PAT grew about 400%.4 Translated out of percentages: Macmillan had been running the operation with so much cost-plus slack and so little operating discipline that simply imposing third-party-vendor rigour on the cost base tripled the profit. This is the kind of statistic that, when private-equity people see it, makes their eyes go faintly glazed; it is the textbook captive-buyout setup.

Nishith Arora's playbook in those first three years was almost embarrassingly simple, but it required the will to do unpopular things. First: shift the centre of gravity out of Bengaluru, which had become an expensive labour market, into tier-II cities, principally Dehradun.4 The same English-literate workforce existed there at materially lower cost, with materially lower attrition. Second: replace the cost-plus transfer-pricing mentality with USD-priced third-party contracts. Third — and this was the existential one — wean the company off Macmillan as a customer. At takeover, essentially 100% of revenue came from the former parent. The target was to drive that toward zero. The mechanism: aggressively sell into the other big scholarly publishers — Elsevier, Wiley, Springer, Oxford University Press, Cambridge University Press, Taylor & Francis — most of whom had no particular emotional attachment to using Macmillan's old back-office, and were happy to do business with what was now effectively an independent vendor.

Then came Rahul Arora. Nishith's son joined the business in 2012 as Chief Marketing Officer — a deliberately customer-facing title for a company that had never really had customers in the commercial sense. Rahul's background was different from his father's: he had spent time outside India, his thinking was global, and his interest was not in defending the captive's margin but in flipping the entire business model. He was elevated to CEO in 2015, with Nishith stepping back to a Non-Executive Chairman role and beginning to map out a planned five-year succession.5 This is, by the way, an unusual artefact in Indian family business: a deliberate, calendared, publicly announced handover, rather than the more common "the patriarch dies in office and the children scramble." It speaks to a particular cast of operator: someone who treats the business as an institution to be transferred cleanly, rather than as a personal kingdom to be defended to the grave.

What Rahul Arora articulated, somewhere between 2015 and 2017, was what insiders would later call "MPS 2.0." The thesis went like this: the typesetting and content-services business was a commodity, with structurally limited margins. To break out of the BPO bracket — where Indian listed peers traded at single-digit EV/EBITDA multiples — MPS needed to own platforms, not just deliver services. It needed to move up the value chain from "we format your manuscript" to "we host your journal, we run the workflow that gets the manuscript to peer review, we provide the author services before the manuscript is even written." Each of those moves would change the unit economics: from per-page pricing (a treadmill) to subscription revenue (a moat).

The catch was capital allocation. MPS did not have the scale to build those platforms organically — building a journal-hosting platform from scratch in 2017 would have taken a decade, by which time the moats around the incumbent platforms would be insurmountable. The answer was to acquire. Which, in turn, required two things that Indian captives are not known for: a disciplined M&A muscle, and the cash flow to fund it. Nishith Arora had set up the second by squeezing the cost base. Rahul Arora was about to build the first.

IV. The Rahul Arora Era: M&A as a Core Competency

If you wanted to pick the single transaction that defined the new MPS, it would be the one announced on April 24, 2018: the agreement to acquire Tata Interactive Systems from Tata Industries Limited for ₹80 crore — roughly $12.3 million at the time.6 On paper this was a small deal. In strategic terms it was a tectonic event. Tata Interactive Systems — TIS — was an e-learning content business that the Tata Group had nurtured for two decades, with operations in India, Switzerland (TIS AG) and Germany (TIS GmbH). It served corporate-training customers globally. And it had been put up for sale because the Tatas, like Macmillan before them, had decided that owning a specialist e-learning house was no longer core to the group's strategy.

The price tag — ₹80 crore for the whole package, including the European subsidiaries that were closed in a second tranche in July 2018 — looked, to outside observers, ambitious. EdTech valuations globally were running hot; American comparables like Pluralsight (which would IPO in May 2018 at a $2 billion valuation) and the not-yet-public Coursera were trading at high multiples of revenue. By that yardstick, MPS was paying a sub-1x revenue multiple for a global e-learning business with two decades of corporate relationships, blue-chip clients and Swiss-German operating centres. The bear interpretation was that TIS had genuine problems — flat growth, legacy contracts, a service-heavy mix that looked nothing like Pluralsight's recurring-revenue model. The bull interpretation was that this was a classic Tata Group "non-core asset on the wrong side of the strategic line," exactly analogous to the Macmillan setup of 2011, and MPS was getting the asset at a price that reflected its current cash flow, not its repositioned potential.

What did MPS do with TIS? The first thing it did was rebrand it as MPS Interactive Systems and stop trying to be a pure e-learning content vendor. The second was to use TIS's customer base as an anchor for a much broader Learning Solutions push — eventually turning it into the eLearning segment that, by FY24, contributed roughly 25% of group revenue.7 The third — and this is the part that experienced acquirers will recognise — was to use TIS as a platform for tuck-in acquisitions, starting with E.I. Design Private Limited in May 2022, and then most consequentially with the Liberate Group in 2023. By the time you look at the segment in 2026, it bears very little resemblance to what TIS was in 2018. It's a global eLearning roll-up running on the back of an asset acquired from a willing seller at a friendly price.

The second defining transaction came on July 1, 2020 — the date MPS closed its acquisition of HighWire Press.8 HighWire's pedigree is unusual. It was founded in 1995 at Stanford University, as a Stanford Libraries initiative to put scholarly journals online in the very first wave of internet adoption — a year before the founding of Google, and arguably an even more contrarian bet on the academic world's willingness to go digital.9 By the 2010s, HighWire was hosting hundreds of scholarly journals; in 2014, Stanford handed the operating business over to the private-equity firm Accel-KKR, which spun it out as an independent commercial entity, retaining a minority stake.9 By 2020, HighWire — like many turn-of-the-millennium technology platforms — was the kind of asset that had genuine moats but no obvious next owner. Accel-KKR wanted out. MPS, which by then had been working with HighWire as a content supplier, stepped in.

The board-approved consideration was roughly $6.1 million for 100% of HighWire and its subsidiaries.10 That number is worth lingering on. Six million dollars for an asset that hosted the British Medical Journal, the journals of the American Association for the Advancement of Science, the journals of dozens of major scholarly societies. The reason the price could be so low was that HighWire, under prior ownership, had been a distressed asset: bleeding cash, technology stack creaking under the weight of two decades of accumulated complexity, customer relationships intact but eroding. MPS was, in effect, buying a turnaround. What it bought, in the long term, was switching costs: once a scholarly society's fifty years of journal archives are sitting on your platform, the cost — financial, technical, political — of moving them somewhere else is so high that most societies will pay the renewal fee and stay. This is the Hamilton Helmer textbook definition of a "Switching Cost" power, and HighWire's portfolio is full of them.

Five years and several restructurings later, HighWire is the cornerstone of the Platform Solutions segment that, by FY24, accounted for about 23% of group revenue and the highest gross margins in the company.7 That is the moment when the MPS thesis crystallised: a labour-arbitrage business funding the acquisition of recurring-revenue technology platforms, with the cash flow from the former financing the moat-building of the latter.

The 2023 transaction took MPS to Australia. On August 29, 2023, MPS announced the acquisition of a 65% stake in the Liberate Group — Liberate Learning, Liberate eLearning, App-eLearn (all Australian entities) and Liberate Learning Limited in New Zealand — with the remaining 35% to be acquired in tranches under an earnout structure.11 Liberate was a digital-learning provider with a blue-chip Australian and New Zealand customer base — government clients, large corporates, a particular strength in compliance and regulatory training. From MPS's perspective, this was a geographic move: the company had presence in the US (via HighWire), in Europe (via TIS AG/GmbH), and in India, but APAC outside India was an under-served whitespace. Liberate gave them a beachhead.

Then, in February 2024, came what is probably the most strategically interesting transaction of the lot. On February 29, 2024, MPS — via its U.S. subsidiary — closed the acquisition of Research Square Company / AJE LLC, including the Beijing-based American Journal Online subsidiary, for $8.4 million in cash.12 AJE — American Journal Experts — runs an author-services business: scientific editing, translation, manuscript-quality evaluation, and an AI writing assistant called Curie. Its customers are not publishers. Its customers are researchers, principally in China, Brazil, Japan, Korea — the non-native-English research economies. AJE edits a manuscript before the researcher submits it to a journal.13

This is what is meant in the original outline by "moving into the value chain before the content is even written." It is a defensive move against a structural trend: as Open Access (which we'll come to) shifts publishing economics from subscription-payer to author-payer, the person with the money in the system is no longer the librarian — it is the researcher writing the article. AJE puts MPS directly into that researcher's hand, with a B2C product (Curie) and a B2C revenue stream, for the first time in the company's history. It is a small business by revenue. It may turn out to be enormous in strategic value.

By the time the 2026 calendar opened, the M&A muscle had become a defining institutional competence. We'll come back to where it pointed next, but pause first on management's incentive structure: under Rahul Arora's tenure, executive compensation has been weighted toward USD-denominated revenue growth and EBITDA margin retention — both unusually disciplined KPIs for an Indian small-cap, and both consistent with the platform-over-services thesis. This is not a company being run for headline rupee revenue. It is being run for dollar earnings.

V. The "Hidden" Engines: Platforms & Learning

Here is the way to think about today's MPS, simplified to the point where it actually makes sense. The company has three businesses. The oldest — Content Solutions — is what was once Macmillan's back-office: typesetting, copy-editing, XML conversion, the production work that turns a manuscript into a journal article. As of FY24, this was still 52% of revenue.7 It is the labour-arbitrage business, and it remains profitable, but it is structurally a low-growth segment. It throws off cash. It does not, on its own, justify the company's multiple.

The two newer businesses are where the story is. The first — Platform Solutions, about 23% of FY24 revenue — is HighWire and a related platform called Magplus, the latter a Swedish-origin digital publishing engine that MPS acquired in 2016.1 These are SaaS-shaped assets: customers (scholarly societies, publishers, magazine groups) pay recurring fees to host their content on the platform, and the marginal cost of serving an additional reader is essentially zero. Gross margins are high. Revenue is sticky. And — this is the key part for a roll-up — the platforms can absorb additional content libraries without needing additional headcount in proportion.

The cleanest way to understand HighWire for a non-publishing-industry reader is by analogy: think of it as Shopify for scholarly journals. The journals themselves — the brands, the editorial boards, the prestige — belong to the societies. HighWire provides the technology layer underneath: the hosting, the subscription management, the article delivery, the analytics, the author submission workflow, the integration with the indexing services (PubMed, Web of Science, Crossref) that make a journal discoverable. The society pays HighWire a fee per year; HighWire's job is to be invisible. The moat is exactly the same as Shopify's moat: once you've migrated, migrating again is a nightmare. The difference is that scholarly journals' archives go back, in many cases, to the 19th century, and any migration has to preserve every DOI, every citation link, every metadata field, perfectly. The switching cost is not metaphorical. It is technically prohibitive.

The second growth engine — Learning Solutions, about 25% of FY24 revenue — is the eLearning roll-up: TIS (now MPS Interactive Systems), the European TIS operations, E.I. Design, and the Liberate Group in Australia and New Zealand. The customer base here is different — it's not academic publishers, it's corporates: financial-services firms, pharma, government, anyone with a regulatory or skills-training obligation. The product mix is content development plus increasingly platform-shaped services like learning experience platforms, immersive learning, brand museums and the like. This is the segment that grew fastest through FY22-FY25, and is the segment where the operating leverage of India-based delivery against Western-priced customer contracts is at its purest. If HighWire is the moat business, Learning Solutions is the growth business.

And then, in February 2026, the company opened a fourth front. On February 12, 2026, MPS — through its U.S. subsidiary MPS North America — announced the acquisition of Unbound Medicine, a U.S.-based clinical-decision-support and healthcare-education platform with roots going back more than 25 years.2 The deal value was not disclosed. The strategic logic, however, was. Unbound's products sit at the point of care: a clinician using a hospital workstation or mobile device pulls up Unbound's content (drug references, clinical guidelines, diagnostic checklists) and gets contextual, evidence-based answers. The platform layer beneath that — the AI that ranks the right answer for the right clinical context — is exactly the kind of asset that the platform engineering team at HighWire can scale.

It also extends a logic. Scholarly publishing's customer is the librarian. Healthcare knowledge management's customer is the hospital system, the medical school, the pharmacy. Both are paying for high-trust, professionally-curated, AI-mediated content delivery. The underlying engineering — content workflows, metadata pipelines, search relevance, subscription management — is much the same. Unbound gives MPS its first foothold in a vertical (healthcare) that is structurally much larger than scholarly publishing. In the bull case, it is the seed of a med-tech segment that ten years from now is larger than everything else MPS owns put together. In the bear case, it is a $X million experiment in a market MPS doesn't deeply understand. We'll come to which is more likely. But for the moment, the structural point is this: MPS has built the operational chassis — India-based platform engineering supporting Stockholm-based (Magplus), U.S.-based (HighWire, Unbound, AJE) and Australian/Kiwi (Liberate) front-end customer interfaces — that lets it absorb the next acquisition without bloating the cost base. The roll-up has its own internal flywheel.

The lesson of this section, for an investor, is that the segment mix today understates the structural shift underneath. Look at FY24's 52% content / 23% platform / 25% learning breakdown, and the company still looks like a content services house. Look at where incremental revenue and incremental margin are coming from, and a different company is emerging.

VI. Strategy Analysis: 7 Powers & Porter's Forces

Step back from the deal-by-deal narrative and ask the structural question: where, exactly, is the moat? This is the place to deploy Hamilton Helmer's 7 Powers framework, because MPS's portfolio is unusually clean as a worked example.

The dominant power, by a wide margin, is Switching Costs. We've already touched on HighWire, but the depth of the moat is worth dwelling on. A scholarly society — say, the American Physiological Society, or the British Medical Association — hosts its journal archive on HighWire. That archive may go back 80 or 100 years. Every article has a Digital Object Identifier (a DOI), every reference within every article is hyperlinked to its target citation, every author has an ORCID record linked back to their profile. The metadata is integrated into PubMed, Crossref, Web of Science, Scopus. Moving to a competing platform means rebuilding all of that, perfectly, while not breaking a single inbound citation anywhere on the indexed academic web. Most society publishers will not even contemplate the migration. The result is that HighWire renewals run at extremely high rates, and even modest annual price increases compound.

The second power is Cornered Resource, and it's subtler. MPS doesn't own scholarly societies — those are independent institutions. But the cumulative relationships, built over decades, between MPS (and its predecessor Macmillan business) and the editorial offices of the world's major scholarly societies are a cornered resource in the relevant sense: the network of contacts, the institutional credibility, the ability to walk into a society's annual meeting and not have to explain who you are. New entrants — a Google, a startup, a Chinese platform — would have to spend a decade building that trust. Plus, on the author services side, AJE has cornered a different resource: its concentration of relationships in Chinese, Brazilian, Korean and Japanese research universities, where the company is the default English-editing recommendation. This is structurally hard to replicate by a U.S. or European entrant, because the trust has been built over fifteen years of word-of-mouth in non-English research communities.

The third — minor, but real — is Process Power: the actual operational know-how of running an India-based content delivery operation at scale, with reliable quality control, on Western publisher production deadlines. This isn't dramatic, but it is genuinely hard to replicate, and it explains why the BPO peer group (Wipro, HCL, etc.) has never seriously moved into MPS's lane despite having the capacity.

Now flip to Porter's Five Forces. The most interesting one is Supplier Power, where MPS has done something genuinely defensive. In the traditional publishing economics, the "supplier" is the researcher who writes the article — and historically, the researcher was paid nothing and had little bargaining power. But Open Access (we'll come to this) has shifted the economics: the researcher (or the researcher's grant) now pays an Article Processing Charge to publish, and the researcher is the customer. Acquiring AJE was, in part, a hedge: it puts MPS in direct relationship with the researcher, not just the publisher. If the value capture in academic publishing migrates from publisher to author, MPS now has a foot in both camps.

The Threat of Substitutes is where the conversation gets uncomfortable, because the most plausible substitute is an LLM. Today's commodity layer of MPS's Content Solutions business — copy-editing, basic typesetting, indexing — is exactly the kind of work that GPT-class models, properly orchestrated, can do at materially lower cost per page. The bear case here is real: the floor under Content Solutions pricing is dropping. MPS's answer, branded MPSLabs, is to embed AI into its own workflows so that the company captures the productivity gain rather than passing it through to customers as price compression. Whether that holds is one of the open questions of the next three years.

Bargaining Power of Buyers is moderate. MPS's customer concentration in the top scholarly publishers is real — losing Elsevier or Springer Nature as a content services customer would hurt — but the platform business reduces this risk substantially, because platform customers (scholarly societies) are diffuse, not concentrated. Each individual society is too small to dictate terms.

Threat of New Entrants is structurally low for the platform business, given the switching costs, and structurally high for the commodity content services business, given Indian competitors and now Indian-AI competitors entering the lane. The mix shift over time — from content to platforms — is, among other things, a reduction of this competitive exposure.

Industry Rivalry, finally, is balkanised. There is no single global competitor that does what MPS does across all three segments. Codemantra, Aptara, SPi Global / Straive compete in pieces of Content Solutions. Atypon (owned by Wiley) and Silverchair compete with HighWire on the platform side. NIIT, Skillsoft, Cornerstone, and large content houses compete in Learning. None of them has the integrated stack. That fragmentation is, paradoxically, both an opportunity (more roll-up targets) and a constraint (MPS is not the obvious category-defining player in any single segment).

What does this analysis actually tell an investor? It tells you that the durable moat is in the Platform and the cornered-resource Cornered-Resource part of the relationship base, that the commodity content business is structurally exposed to AI compression, and that the learning business is a quality roll-up in a fragmented market — neither moat-rich nor moat-free, just well-executed. The strategic question is whether the share-of-revenue migration from segment one to segments two and three continues at pace.

VII. The Bear vs. Bull Case

Myth vs. Reality

A note before we run the cases. The consensus narrative on MPS, in the Indian small-cap commentary you find on Twitter and YouTube, tends to focus on dividend yield and on the company's history of generous payouts. That is a fact-true narrative — MPS has historically returned a meaningful share of free cash flow to shareholders — but it is the wrong frame. The interesting question about MPS is not whether it will keep paying dividends. It is whether it will keep deploying capital into acquisitions at the rate it has demonstrated since 2018, whether those acquisitions will continue to earn their cost of capital, and whether the segment mix continues to shift away from commodity content. Treat the dividend as the residual, not the story.

The Bear Case

The bear case has three distinct layers, and the most interesting one is not the most obvious.

The obvious one is AI. Large language models are demonstrably capable, today, of doing first-pass copy-editing, basic typesetting, indexing and even structured content conversion. The marginal cost is collapsing. If MPS's Content Solutions segment is half the business, and if pricing in that segment compresses by 20-30% over the next three to five years, that pulls the entire group's growth profile down and arguably forces a revaluation. The defence — MPSLabs, embedding AI into MPS's own workflows so that the productivity gain accrues to MPS — is real but not yet proven at scale.

The second is Open Access. The Plan S initiative in Europe — a coalition of major research funders committing to a 100% Open Access mandate — and broader U.S. and global movements toward author-pays publishing economics are restructuring the customer base of scholarly publishing. In the traditional model, libraries pay subscriptions; publishers pay vendors like MPS to produce the journal. In the OA model, authors (via their grants) pay Article Processing Charges; publishers run with thinner per-article margins. The vendors in the value chain — that's MPS — face direct pricing pressure from publishers seeking to defend margin. The AJE acquisition is a partial hedge here, but it doesn't fully insulate the group.

The third — and this is the underrated one — is customer concentration and key-person risk. MPS's Content Solutions revenue is meaningfully concentrated in the global top-five publishers. If any one of them in-sources its production work, or aggressively reprices it, the impact would be material. And on the management side, Rahul Arora is, by all accounts, the architect of the entire post-2018 strategy. The company is institutionalising — there's a board, there's a leadership bench, governance has been formalised — but the strategic clarity comes from one office.

The Bull Case

The bull case is also threefold, and it's a mirror-image structural argument.

First — the mix shift is real, and it is accelerating. Platform Solutions and Learning Solutions are growing faster than Content Solutions, and they are higher-margin and higher-multiple businesses than Content Solutions. Over a five-year window, even at modest organic growth rates, the segment mix could plausibly migrate from today's roughly 52/23/25 to something closer to 35/30/35 — at which point the company is no longer a content services house. It is a platform-and-learning house with a content services tail. That re-rating, on its own, is a meaningful re-equation of fair value.

Second — the M&A muscle compounds. The Vision 2027 target articulated by management is ₹1,500 crore in revenue at sustained margins, with roughly 60% of the scale-up coming from acquisitions and 40% from organic growth.14 Note that ₹1,500 crore implies roughly a tripling of FY24 revenue. The acquisition pipeline — distressed Western platforms with valuable IP but operational issues, exactly the HighWire template — is, by management's account, deep. Each successful tuck-in does two things: it adds revenue immediately, and it strengthens the operating leverage of the India delivery chassis. If MPS continues to acquire at sub-1x revenue multiples and re-rate the assets to its own multiple, the value creation per deal is significant.

Third — the Unbound Medicine pivot, if it works, opens a vertical of completely different scale. Scholarly publishing globally is a roughly $30 billion industry. Healthcare knowledge management — clinical decision support, medical reference, point-of-care information services — is several multiples of that, and is structurally growing as healthcare digitises and as AI moves into clinical workflow. If Unbound becomes the seed of a healthcare segment, the long-term TAM expansion is the single biggest re-rating lever in the story.

KPIs to Watch

For investors who actually want to track this, the noise can be filtered down to a small number of high-signal indicators. The most important are:

-

USD revenue growth in constant currency. This is the management's own preferred metric, and the right one. Rupee revenue can be flattered by INR depreciation; the underlying business runs in dollars. Look at YoY constant-currency USD revenue growth at the consolidated and segment level.

-

Group EBITDA margin retention. The implicit promise of the strategy is that margins stay above 25% even as the business scales and the mix shifts. Margins below that level mean either acquisitions are dragging, or content-services pricing is compressing faster than mix-shift can offset.

-

Segment mix as a percentage of revenue. Specifically: Platform Solutions plus Learning Solutions as a combined share of group revenue. The thesis is that this combined share climbs steadily. If it stalls, the strategy is stalling.

That's the trio. Watch those, and you'll know whether the company is executing.

VIII. Epilogue & Playbook Lessons

The lasting interest of MPS, beyond the specific business, is what it represents as a category of corporate transformation. It is the inverse, in many ways, of the Indian IT-services trajectory of the last decade: companies like TCS, Infosys, Wipro that built world-class labour-arbitrage businesses and have spent the last decade trying — with mixed success — to graft platform-and-product businesses on top. MPS started from the same place. It went the other way.

Three lessons, for any operator or capital allocator looking at similar setups.

The first is that the captive-to-independent transition is structurally a high-return trade, if the buyer can change the cost base and the customer base in parallel. Nishith Arora's three-year window after 2011 is a textbook of operational re-engineering: same workforce, different location, different customers, different pricing. The 300% EBITDA growth in that window is not an accounting artefact — it is what happens when you remove the cost-plus ceiling on a perfectly competent operating team.

The second is that inorganic-first growth strategies need a particular kind of cultural DNA, and that DNA is rare in Indian listed companies. Most Indian acquirers default to one of two failure modes: either they overpay because they see the trophy and not the cash flow, or they underintegrate and let the acquired business slowly decay inside a holding structure. MPS, so far, has avoided both. It has bought at low multiples (sub-1x revenue in most cases), and it has actually integrated the operations — same finance, same HR systems, same delivery chassis — without destroying the customer relationships of the acquired entities. That is hard to do, and harder to do repeatedly.

The third is that succession is a strategic act, not a family event. The Nishith-to-Rahul Arora handover, executed over five years, with public communication and clean role-definitions, is the kind of governance choreography that Indian small-caps almost never get right. It mattered because the strategic shift — from labour arbitrage to platforms — required a different CEO archetype than the one that had executed the captive turnaround. Recognising that, and acting on it, is a non-trivial managerial decision.

Where does the story go from here? The honest answer is that MPS is in the middle of executing a five-year plan whose end state has been articulated, but not yet earned. Vision 2027's ₹1,500 crore revenue target is, mathematically, a roughly threefold scale-up from FY24 in three to four years. That implies either a step-change in the M&A cadence — a deal a year, larger than the recent ones — or aggressive organic growth in Platform and Learning, or both. The Unbound Medicine acquisition signals that the buyer is willing to step outside the traditional scholarly-publishing perimeter, into healthcare and into AI-mediated workflows. Whether that signals a thoughtful expansion into adjacent moats or a riskier diversification away from the moats that originally justified the company's existence is the open question.

For now, what can be said with confidence is this: the company that Harold Macmillan inaugurated as a back-office in Bengaluru in 1976 no longer exists. The company that bears its DNA — listed on the NSE under the ticker MPSLTD, sitting at the intersection of scholarly content, e-learning, platform technology and now healthcare knowledge — is one of the more interesting case studies in Indian capital allocation of the last fifteen years. The story is not finished. The thesis is not fully proven. But the trajectory is one of the cleanest examples in the listed Indian universe of a captive turned platform, of a service house turned IP house, of an asset extracted from a global parent and built — patiently, deal by deal — into something its original owners would not recognise.

References

References

-

MPS Acquires Unbound Medicine, Expands into Healthcare Knowledge Management — MPS Limited press release, 2026-02-12 ↩↩

-

Exemption Order under Regulation 11 of SEBI (SAST) Regulations, 2011 in the matter of MPS Limited — SEBI / casemine.com ↩↩

-

MPS Re-Structuring — For Regulatory Purpose? — M&A Critique ↩↩

-

Rahul Arora confirmed Chairman and Chief Executive Officer of MPS Limited — MPS Limited, 2021 ↩

-

MPS Completes Acquisition of Tata Interactive Systems India — MPS Limited press release, 2018 ↩

-

MPS Quarterly Update Report Q2 FY25 — Keynote Capitals, 2024-11 ↩↩↩

-

MPS Completes Acquisition of HighWire Press to Accelerate Platform Business — MPS Limited press release, 2020-07-01 ↩

-

MPS Approves To Buy Highwire Press For $6.1 Mln — STM Publishing News, 2020 ↩

-

MPS Announced Strategic Investment in Liberate Learning — MPS Limited press release, 2023-08-29 ↩

-

MPS acquires AJE to scale AI capabilities and enter B2C market — MPS Limited press release, 2024-02-29 ↩

-

MPS Quarterly Update Report Q1 FY26 — Keynote Capitals, 2025-08 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube