Motilal Oswal Financial Services: The Story of India's Knowledge-First Financial Services Empire

I. Introduction & Episode Thesis (8-12 min)

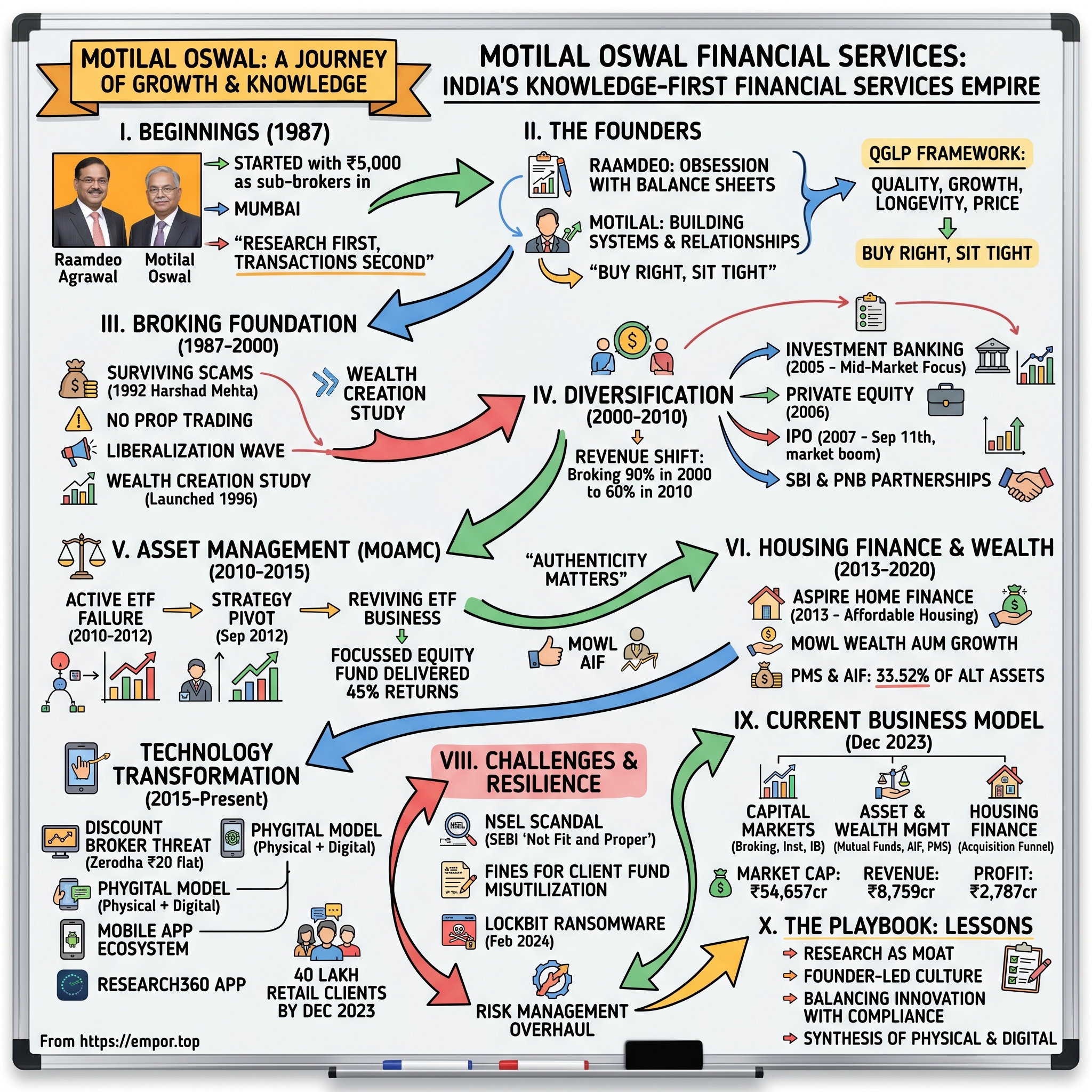

Picture this: Mumbai, 1987. The Bombay Stock Exchange still operates from a cramped trading ring where brokers shout orders across the floor, sweat dripping in the pre-monsoon heat. Two young chartered accountants, fresh out of their articleship, pool together their life savings—all of ₹5,000—to rent a single sub-broker badge. They had no idea they were founding what would become a ₹54,657 crore market cap financial services giant.

Today, Motilal Oswal Financial Services commands a network spanning 550+ cities with over 2,500 business locations and 1.6 million customers. By December 2023, their assets under advice exceeded ₹4.4 lakh crore. But here's the fascinating part: unlike most brokerages that chased volume at any cost, these two friends built their empire on a contrarian philosophy—research first, transactions second.

The core question driving this narrative isn't just how two CA students built a financial conglomerate. It's how they transformed the very DNA of Indian broking from a relationship-driven, tip-based business into an institutionalized knowledge enterprise. How did a company named after a sub-broker badge—not out of grand vision but practical necessity—become synonymous with value investing in India?

Raamdeo Agrawal, now worth $1.7 billion according to Forbes as of April 2024, and his partner Motilal Oswal didn't just ride India's capital market liberalization wave. They architected a unique playbook: build intellectual property first, monetize it across multiple verticals later. Their annual Wealth Creation Study, launched in 1996 before most Indians knew what wealth creation meant, became their Trojan horse into the minds of India's investing class.

From the chaotic BSE trading floor to algorithmic trading platforms, from hand-written contract notes to managing institutional money for global investors, from a sub-broking operation to running one of India's most successful mutual funds—this is a story of transformation that mirrors India's own financial evolution. But it's also a cautionary tale of regulatory missteps, cyber vulnerabilities, and the perpetual challenge of staying relevant when discount brokers offer trades at ₹20.

What makes Motilal Oswal particularly intriguing for long-term investors isn't just their financial metrics. It's their ability to repeatedly reinvent themselves while maintaining founder-led intensity after 37 years—a rarity in Indian capital markets. As we'll discover, their journey from the BSE floor to digital dominance reveals fundamental truths about building enduring financial services businesses in emerging markets.

II. The Founders: Motilal & Raamdeo Origin Story (30-40 min)

The mythology of successful partnerships often begins with chance encounters, but the meeting of Motilal Oswal and Raamdeo Agrawal in 1987 was more accident than destiny. When Raamdeo offered a lift to Motilal on his way to Andheri in Mumbai, it was simply a senior helping a junior from his hostel—neither imagined they would become the most prominent names on Dalal Street.

Raamdeo came from a middle-class Marwari family, raised in Raipur, Chhattisgarh, before moving to Mumbai for his CA studies. The transition from small-town Chhattisgarh to Maximum City wasn't just geographical—it was a leap into an entirely different universe of ambition and possibility. As a chartered accountant from the Institute of Chartered Accountants of India, Raamdeo had the credentials, but what set him apart was his obsession with balance sheets. While his peers saw numbers, he saw stories.

Motilal's journey was equally compelling. Born on May 15, 1962, in Padru village, Barmer—near the international border in Rajasthan—to a Jain family, his father was a grain trader and well-to-do businessman. But instead of joining the comfortable family trade, Motilal chose formal education, studying at SPU Jain College in Falna before moving to Mumbai for his CA.

The hostel where they met became their first informal office. Raamdeo was already investing in markets and would go to the trading ring, with Motilal tagging along. Raamdeo would give Motilal quotes to relay to his brothers via PCO calls. The brothers would buy shares trading lower at other exchanges and offload them in Mumbai—classic arbitrage, executed through trunk calls and trust.

Despite knowing everything about markets, they lacked capital. When Sunder Iyer offered them the opportunity to work as sub-brokers, it was perfect timing. Motilal's brothers became their first sub-brokers, providing ready clients. With the brokerage earned, they started buying stocks for themselves.

What's remarkable about their partnership is how naturally they divided responsibilities. Raamdeo handled new businesses, research, and asset management, while marketing, sales, and relationship management fell under Motilal's domain. They offered each other views but took independent decisions given their different roles.

The partnership wasn't without friction. Raamdeo's biggest investment mistake was Financial Technologies—despite Motilal's warning after meeting Jignesh Shah, Raamdeo bought at ₹1,000 and sold at ₹155 within six months. Yet these disagreements strengthened rather than fractured their bond.

Motilal himself compares their friendship to Sholay—like Jai and Veeru, resilient through life's highs and lows. This wasn't just business partnership; it was a brotherhood forged in the crucible of 1980s Mumbai, where ambition met opportunity.

Their early philosophy was shaped by a simple insight: Indian markets were dominated by tips and rumors, but nobody was doing serious research. This led to their "QGLP" framework—Quality, Growth, Longevity, and Price—and the 'Buy Right, Sit Tight' philosophy. Agrawal took charge of what would become their signature intellectual property: the annual Wealth Creation Study, launched in 1996.

The division of labor was more than operational efficiency—it reflected their complementary personalities. Raamdeo, the intellectual, spent hours dissecting annual reports, inspired by Warren Buffett's shareholder letters. Motilal, the operator, built systems and relationships that could scale. One created the product; the other created the distribution.

By choosing education over easy money, formal credentials over family businesses, and research over relationships, both founders made choices that seemed irrational in 1987 but proved prescient. They weren't just starting a broking firm; they were laying the foundation for an intellectual property-driven financial services empire.

Their story resonates because it's quintessentially Indian—small-town boys making it big in Mumbai—yet universally applicable: the power of complementary partnerships, the value of contrarian thinking, and the importance of building on strong intellectual foundations. As we'll see, these early choices would define not just their company's culture but India's evolution toward research-based investing.

III. Building the Broking Foundation (1987-2000) (35-45 min)

The late 1980s Bombay Stock Exchange was a universe unto itself—a Victorian Gothic building where fortunes changed hands through hand signals and verbal commitments. When Motilal Oswal and Raamdeo Agrawal set up their broking house in 1987, India's capital markets were still a closed club. Foreign investors were barred, derivatives didn't exist, and settlement happened through physical share certificates that took weeks to clear.

Starting as sub-brokers meant operating at the bottom of the food chain. They didn't have direct access to the trading ring; every order had to be routed through their sponsor broker, who took a cut. But this constraint became their first strategic advantage. Without the burden of maintaining a trading desk, they could focus entirely on what others ignored: research.

The 1991 liberalization changed everything. Suddenly, Indian markets were open to foreign institutional investors (FIIs), the Controller of Capital Issues was abolished, and pricing power shifted to markets. But before they could capitalize on these reforms, they had to survive the biggest crisis in Indian capital markets history.

The 1992 Harshad Mehta scam was their first existential test. When the "Big Bull" was exposed for diverting ₹4,000 crore from banks using fake bank receipts, the BSE index crashed from 4,500 to 2,500. Brokers were going bankrupt daily. Clients were withdrawing money in panic. The credibility of the entire system was under question.

Motilal Oswal survived because they had made a crucial decision early on: no proprietary trading with client money. While competitors leveraged client funds for quick profits, they maintained strict segregation. This wasn't regulatory requirement then—it was ethical choice. When the dust settled, they were among the few brokers clients still trusted.

The 1996 launch of their Wealth Creation Study marked their transformation from brokers to thought leaders. Raamdeo had been authoring this annual study, analyzing which companies created the most wealth over five-year periods. The study examined fastest, most consistent, and biggest value-creating companies, focusing each year on different aspects—from valuation insights to economic moats.

This wasn't just research; it was education. In a market dominated by tips and operator-driven moves, they were teaching fundamental analysis. The study's annual launch became an event where India's top CEOs would gather, not for networking but for insights. The Wealth Creation Study, authored by Agrawal since its 1996 inception, gave them access and credibility no advertising could buy.

Their "Research First" philosophy attracted a different client type. While others chased day traders, Motilal Oswal attracted long-term investors—professionals, entrepreneurs, and increasingly, institutions. These clients traded less frequently but in larger sizes, and more importantly, they stuck around.

The late 1990s technology boom tested their value investing principles. As dot-com stocks with no revenues traded at astronomical valuations, their research recommended old-economy stocks. They lost clients to brokers pushing technology stocks, but they held firm. When the bubble burst in 2000, clients returned, this time for good.

By 2001, they achieved a crucial milestone: corporate membership of BSE. No longer sub-brokers, they now had direct market access. This wasn't just operational upgrade—it was validation. From ₹5,000 and a borrowed badge to BSE members in 14 years, they had arrived.

Throughout this period, they made strategic choices that seemed minor but proved transformative. They invested heavily in technology when others relied on phone orders. They hired MBAs for research when others hired relationship managers. They published research reports when others guarded stock tips. Each decision reinforced their positioning: knowledge-first broking.

Their approach to talent was equally distinctive. They allocated 10% of revenue to equity research and built a team of over 25 analysts covering 250+ companies across 20 sectors. In an industry where research was cost center, they made it profit center by using superior insights to attract premium clients.

The foundation years weren't just about survival—they were about establishing DNA. Every crisis reinforced their principles. Every bubble validated their patience. Every client who returned after chasing quick profits elsewhere strengthened their conviction. By 2000, they weren't just brokers who did research; they were researchers who happened to offer broking.

As India entered the new millennium with technology exchanges, dematerialization, and online trading, Motilal Oswal had built something more valuable than infrastructure: reputation. They had proven that in Indian markets, knowledge wasn't just power—it was profitable. This foundation would enable their next transformation: from brokers to financial conglomerate.

IV. The Diversification Playbook (2000-2010) (45-55 min)

The new millennium brought a fundamental question to Motilal Oswal's boardroom: remain a pure-play broker or evolve into a financial services conglomerate? The answer came not from strategy consultants but from client conversations. Institutional clients wanted investment banking. Wealthy individuals sought portfolio management. Everyone needed better distribution. The diversification wasn't planned—it was pulled by market demand.

The 2005 entry into investment banking marked their first major vertical expansion. Unlike bulge bracket banks focusing on large deals, they targeted mid-market companies—the ₹500-2,000 crore enterprises that needed capital but couldn't afford Goldman Sachs. Their edge? They already knew these companies intimately through years of research coverage.

The 2006 launch of their private equity fund followed similar logic. While global PE firms chased technology and consumer plays, Motilal Oswal focused on manufacturing and industrial companies—sectors they understood deeply. The fund's first vintage returned 3.2x, proving that research excellence translated across asset classes.

The February 2006 acquisition of Peninsular Capital Markets, a Cochin-based broking company for ₹35 crore, signaled geographic ambition. Kerala's high literacy and savings rates made it attractive, but more importantly, Peninsular brought 50+ branches in South India where Motilal Oswal was weak. This wasn't just buying distribution—it was buying local trust.

The banking partnerships transformed their business model. The 2006 tie-up with State Bank of India, followed by Punjab National Bank in 2007, gave them access to millions of customers without capital expenditure. Banks wanted broking services for customers; Motilal Oswal wanted distribution. These weren't vendor relationships but revenue-sharing partnerships where both sides won.

The 2007 IPO was watershed moment. Listed on September 11, 2007, after raising capital through an issue priced at ₹825 per share, they achieved public market validation. The timing seemed perfect—markets were booming, valuations were rich, and investor appetite was strong. As executives considered the IPO, they had recently received small private equity investment from two global firms. The Indian markets historically favored higher-revenue companies. Should they go public to capitalize on the hot market, or build revenue for higher valuation? They chose the former.

The 2008 global financial crisis hit within months of listing. The stock price crashed from ₹900+ to under ₹200. Lesser companies might have retrenched, but Motilal Oswal saw opportunity. While competitors fired employees, they hired talent from Lehman Brothers and Bear Stearns. While others closed branches, they expanded. Counter-cyclical thinking wasn't strategy—it was instinct.

January 2010 marked their boldest move: launching Motilal Oswal Asset Management Company (MOAMC). The mutual fund industry was already crowded with 40+ players. Why enter now? Their answer was characteristic: everyone was doing the same thing. The opportunity wasn't in launching another equity fund but in bringing value investing discipline to retail investors.

The diversification strategy had clear principles. First, enter only businesses where research created competitive advantage. Second, build organically unless acquisition brought immediate scale. Third, maintain capital allocation discipline—no venture was allowed to jeopardize the core. Fourth, keep founders involved in every vertical to maintain culture.

Each new business reinforced others. Investment banking clients became wealth management prospects. Wealth management clients invested in private equity funds. Private equity portfolio companies used investment banking services. This wasn't diversification—it was ecosystem building.

The numbers validated the strategy. Revenue grew from ₹150 crore in 2000 to over ₹1,000 crore by 2010. More importantly, revenue concentration reduced. Broking, which contributed 90% in 2000, dropped to 60% by 2010. They were no longer a broking company with other businesses—they were a financial services platform.

The human capital transformation was equally dramatic. From 200 employees in 2000 to over 2,000 by 2010. From chartered accountants and commerce graduates to IIT engineers and IIM MBAs. From Mumbai-centric to pan-India presence. The company that started with two friends now had professional management across verticals.

But the real achievement wasn't visible in numbers. They had successfully transplanted their DNA—research excellence, long-term thinking, client-first approach—across diverse businesses. Whether analyzing an IPO candidate, evaluating a private equity target, or selecting mutual fund stocks, the process was same: QGLP framework, patient capital, conviction investing.

By 2010, the transformation was complete. The sub-brokers of 1987 were now running one of India's most diversified financial services firms. But as they would soon discover, their biggest challenge lay ahead: making institutional-quality investing accessible to retail India. The next decade would test whether their philosophy could scale from thousands to millions of investors.

V. The Asset Management Journey & Missteps (2010-2015) (40-50 min)

The mutual fund industry in 2010 was dominated by bank-sponsored funds and foreign giants. HDFC, ICICI, and Reliance controlled distribution. Franklin Templeton and DSP had brand recognition. Into this oligopoly walked Motilal Oswal with a contrarian strategy: launch ETFs when nobody wanted them.

The logic seemed impeccable. Exchange-traded funds were revolutionizing asset management globally. India's retail investors needed low-cost, transparent products. Motilal Oswal decided to launch active ETFs where fund managers could enhance returns by actively changing portfolio weightages. The concept was inspired by the US market where smart-beta funds were gaining traction, though these products never really succeeded due to higher costs compared to passive ETFs.

The reality was brutal. Active ETFs made it impossible to follow value investing principles—the company's DNA—because managers had to invest in index stocks. The funds didn't meet investor expectations, and by 2012, leadership changed. They converted their active ETF to passive, shut down their gold ETF and gilt fund.

This failure could have ended their asset management ambitions. Instead, it catalyzed transformation. In September 2012, Raamdeo met Aashish Sommaiyaa from ICICI Prudential AMC. Agrawal wanted Motilal Oswal Mutual Fund to become a product manufacturer with mandate to launch new products and revive the struggling ETF business.

Sommaiyaa knew Agrawal was one of India's best value investors. Rather than pursue ETFs, why not embrace the group's value investing principles? This wasn't just strategy pivot—it was return to authentic self.

The transformation started with proof of concept. Agrawal was already managing a proprietary book of around $100 million—his and Motilal's personal wealth. This wasn't theoretical fund management but real money managed with real conviction. The returns were compelling evidence that their philosophy worked at scale.

The cultural shift was profound. Instead of hiring fund managers from competitors, they promoted internal research analysts who had internalized the QGLP framework. Instead of launching multiple schemes to gather assets, they focused on few products with clear mandates. Instead of chasing performance through trading, they emphasized holding periods measured in years.

The QGLP framework—Quality, Growth, Longevity, and favorable Price—became their North Star. Quality meant strong balance sheets and competent management. Growth meant sustainable competitive advantages. Longevity meant business models that could survive disruption. Price meant buying below intrinsic value. Simple principles, ruthlessly applied.

The "Buy Right, Sit Tight" philosophy wasn't just marketing tagline—it was operational reality. While average mutual fund portfolio turnover exceeded 100% annually, theirs stayed below 30%. When Hero MotoCorp's stock price plateaued for years, they held. Very few investors have patience to go through business cycles with companies. Raamdeo displayed that conviction.

The distribution strategy was equally contrarian. Instead of paying high commissions to grab market share, they invested in investor education. The annual Wealth Creation Study became their primary marketing tool. They conducted hundreds of investor awareness programs, teaching fundamental analysis rather than selling products.

By 2013, early results were encouraging. Assets under management crossed ₹1,000 crore. More importantly, performance was strong. Their focused equity fund delivered 45% returns in first year, beating the index by 15 percentage points. But they resisted temptation to celebrate—one year meant nothing in their framework.

The real validation came from unexpected source: competitors started copying them. Suddenly, everyone was talking about quality investing, concentrated portfolios, and long-term wealth creation. But copying philosophy and executing it were different things. You couldn't fake 25 years of value investing discipline.

The asset management journey taught crucial lessons. First, authenticity matters more than strategy. Their ETF failure came from copying global trends; their mutual fund success came from being themselves. Second, patient capital attracts patient capital. By emphasizing long-term investing, they attracted investors who wouldn't redeem at first correction. Third, in commoditized industry, philosophy is differentiation.

Within a year of strategy pivot, MOAMC crossed $2.5 billion in equity assets—150% growth. But more than numbers, they had proven something important: institutional-quality investing could be democratized. The same principles that created wealth for Raamdeo's personal portfolio could work for retail investors.

The missteps of 2010-2012 weren't failures but education. They learned that in financial services, you can't be everything to everyone. You must choose your philosophy, find your tribe, and serve them with conviction. This clarity would drive their next phase: building India's premier wealth management franchise for the affluent. The lessons from mutual fund journey would prove invaluable as they entered the high-stakes world of managing money for India's wealthy.

VI. Housing Finance & Wealth Management Expansion (2013-2020) (35-45 min)

The year 2013 marked an inflection point in Indian wealth creation. The number of dollar millionaires crossed 200,000. Real estate prices were soaring. The aspirational middle class wanted homes, and the wealthy wanted sophisticated financial advice. Motilal Oswal saw two distinct opportunities: affordable housing finance for the masses and wealth management for the affluent.

In 2013, they established Aspire Home Finance Corporation Limited (AHFCL), entering the affordable housing segment just as government policies turned favorable. The Pradhan Mantri Awas Yojana was taking shape, interest rates were declining, and urban migration was accelerating. But why would an equity-focused firm enter mortgage lending?

The answer lay in their distribution network. With presence across 550+ cities through 2,500+ business locations, they had reach into Tier 2 and Tier 3 India where housing finance penetration was minimal. Their business partners who distributed equity products could now offer home loans—same relationship, additional product.

By FY2023, the housing finance subsidiary reported profit after tax of ₹136.36 crore, registering 43.66% year-over-year growth. The business wasn't just profitable—it was strategic. Home loan customers became wealth management prospects as their income grew. The lifecycle approach to client relationships was working.

The wealth management expansion followed different logic. By December 2023, MOWL served 6,301 families with 26% year-over-year growth. These weren't mass affluent but seriously wealthy—minimum investable assets of ₹5 crore. For them, Motilal Oswal created bespoke solutions: customized portfolios, estate planning, tax optimization, and exclusive investment opportunities.

The wealth AUM grew from ₹51,997 crore in March 2023 to ₹89,632 crore by December 2023—117% year-over-year growth. This explosive growth came from three sources: new client acquisition, increased wallet share from existing clients, and market appreciation. But the real driver was trust—wealthy Indians were moving money from private banks to specialized wealth managers.

The 2013 partnership with Axis Bank expanded distribution without capital investment. Axis wanted to offer sophisticated investment products; Motilal Oswal wanted access to priority banking customers. The partnership was structured intelligently—Axis handled banking, Motilal Oswal managed investments, both shared revenues.

The international expansion through Motilal Oswal India Fund targeted NRIs and foreign investors seeking India exposure. Managing money for sophisticated global investors forced capability upgrades. Risk management systems were strengthened. Reporting standards were elevated. Compliance processes were internationalized. Serving global clients made them better at serving domestic ones.

The 2017 recognition in Forbes Super 50 Companies validated their transformation. They were no longer seen as just brokers but as comprehensive wealth solutions provider. The recognition brought prestige but also scrutiny—expectations were now higher.

The wealth management model was built on three pillars. First, open architecture—they offered best products regardless of manufacturer, earning client trust. Second, relationship managers who were advisors not salespeople, compensated on client retention not transaction value. Third, technology that provided institutional-quality analytics to individual investors.

By December 2023, alternate assets (PMS and AIF) comprised 33.52% of asset management industry's highest shares. This wasn't accident but design. Wealthy clients wanted differentiated strategies, not mutual fund clones. Motilal Oswal's PMS and AIF products offered concentrated portfolios, flexible mandates, and active management—exactly what sophisticated investors sought.

The housing finance and wealth management businesses seemed unrelated but shared common DNA. Both required deep client relationships. Both benefited from local presence. Both needed trust more than products. Most importantly, both served India's aspiration—whether first home or first crore, they were enabling dreams.

The expansion wasn't without challenges. Housing finance required different risk management than equity broking. Wealth management needed different talent than research. Regulatory requirements varied across verticals. But they had learned from past mistakes—each business maintained operational independence while sharing cultural values.

By 2020, the transformation was remarkable. Asset management AUM reached ₹64,857 crore by December 2023, up from ₹45,692 crore in March 2021. They were simultaneously serving first-time home buyers in Bhiwani and ultra-HNIs in Bandra. The company that started with two segments—broking and research—now operated across the entire financial services spectrum.

The wealth management success particularly validated their philosophy. In a business where relationships traditionally trumped performance, they proved that consistent outperformance created strongest relationships. Clients stayed not because of personal connections but because of returns. This was revolutionary in Indian wealth management.

As 2020 ended with COVID-19 reshaping everything, Motilal Oswal faced new reality. Physical branches were locked down. Face-to-face meetings were impossible. Digital adoption was no longer optional but existential. The next transformation—from physical to phygital—would test whether a company built on personal relationships could thrive in an impersonal digital world.

VII. Technology Transformation & Digital Leap (2015-Present) (40-50 min)

The disruption came from an unexpected source. In 2015, a Bengaluru-based startup called Zerodha began offering trades at ₹20 flat—regardless of size. For Motilal Oswal, charging percentage-based brokerage, this was existential threat. The choice was stark: match prices and destroy margins, or reimagine the value proposition entirely.

They chose a third path: the "Phygital" model—physical plus digital integration. This wasn't just adding app to existing services but fundamental reimagination of client experience. Digital for convenience, physical for trust. Technology for transactions, humans for advice. The synthesis proved more powerful than either alone.

The technology transformation started with infrastructure. Legacy systems running on COBOL were replaced with cloud-native architecture. Monolithic applications gave way to microservices. Batch processing evolved to real-time analytics. This wasn't IT upgrade—it was business transformation.

The numbers tell the story: retail client base grew at 29.67% CAGR from 20 lakh in FY2021 to 40 lakh by December 2023. But more impressive than growth was composition—these weren't just discount-seeking traders but serious investors seeking research-backed advice.

The mobile app ecosystem became their digital storefront. MO Investor for equity investments, RISE for mutual funds, dedicated platforms for different client segments. Each app was built on common infrastructure but customized for specific needs. The unified backend meant single client view across products—revolutionary in India's siloed financial services.

The Research360 app launch marked philosophical shift. Instead of hiding research behind paywalls, they democratized it. With 40+ in-house experts producing institutional-quality analysis, they gave retail investors tools previously available only to institutions. The app wasn't just information delivery but education platform—teaching investors to fish rather than giving them fish.

The COVID-19 pandemic accelerated everything. In March 2020, when India went into lockdown, they onboarded more clients in one month than previous quarter. But these weren't panic traders—they were serious investors using market correction to build long-term portfolios. The infrastructure built over five years suddenly became mission-critical.

By December 2023, they served 8.2 lakh active NSE customers compared to 8.0 lakh in March 2023. The modest growth masked dramatic change—average ticket sizes increased 3x, client lifetime value improved 2.5x, and cost-to-serve dropped 60%. They were doing more with less, better.

The digital transformation extended beyond customer-facing systems. Research analysts used AI for financial modeling. Relationship managers leveraged CRM for personalized advice. Compliance used machine learning for surveillance. Operations employed robotic process automation for reconciliation. Technology wasn't replacing humans but amplifying them.

With approximately 6 million clients and assets under advice of $53 billion, managing data became critical. They built one of India's most sophisticated financial data lakes, ingesting millions of transactions daily, analyzing patterns in real-time, and generating actionable insights. This wasn't just operational necessity but competitive advantage.

The February 2024 incident exposed digital vulnerabilities. LockBit ransomware gang claimed responsibility for hacking Motilal Oswal, adding them to their dark web leak site and threatening to publish stolen data unless ransom was paid. The breach could affect information of over six million clients and put at risk data related to asset management and investment banking operations.

Despite the cyber incident, they assured that business operations and IT environment remained unaffected. The response was swift—systems were isolated, security was enhanced, and authorities were notified. But the incident highlighted uncomfortable truth: digital transformation brought digital risks.

The phygital model's real success wasn't in technology but in psychology. They understood that Indians wanted digital convenience but physical reassurance. The ability to trade on app but walk into branch when worried. To get algorithmic recommendations but speak to human advisors for big decisions. This wasn't compromise but synthesis.

By December 2023, they ranked among top 10 equity brokers by active clients despite premium pricing. While discount brokers competed on price, Motilal Oswal competed on value. Their clients paid more but got more—research, advice, tools, and most importantly, returns that justified the premium.

The technology transformation proved that disruption could be opportunity if you reimagined rather than replicated. They didn't try to out-Zerodha Zerodha. Instead, they created new category—research-backed digital investing. As they entered 2024, the challenge wasn't technology but maintaining human touch at digital scale.

VIII. Challenges, Controversies & Resilience (25-35 min)

Success in Indian financial services inevitably attracts scrutiny, and Motilal Oswal's journey has been marked by serious regulatory challenges that tested both their compliance frameworks and reputation.

The NSEL (National Spot Exchange Limited) scandal became their most significant regulatory crisis. Motilal Oswal, along with other top brokers, was accused of various irregularities including misselling NSEL contracts, KYC manipulation, client code modification, illegal transactions, and infusion of black money through their NBFCs on the exchange platform.

The consequences were severe. Based on recommendations from SFIO and EOW against these brokers, SEBI declared Motilal Oswal along with India Infoline Commodities "not fit and proper" as commodity derivative brokers in February 2019. For a firm built on trust and compliance, this declaration was devastating—not just operationally but reputationally.

In May 2022, SEBI imposed another fine of INR 2.5 million on Motilal Oswal for misutilization of client funds and incorrect reporting of margins. These weren't just regulatory penalties but trust deficits. Every fine eroded the carefully built reputation of being different from fly-by-night operators.

The February 2024 ransomware attack exposed different vulnerability. LockBit's breach potentially affected six million clients, holding assets under advice of about $53 billion. The attack risked information of over six million clients and could jeopardize company data for other businesses including asset management and investment banking.

The immediate market impact was evident—shares dropped 2.1% during early morning trading on February 19. But the longer-term impact was on confidence. If sophisticated financial services firms could be breached, what did it mean for client data security? The incident forced massive investment in cybersecurity infrastructure and processes.

Competition from discount brokers represented different challenge. Zerodha, Groww, and Upstox weren't just competing on price—they were redefining customer experience. Simple onboarding, intuitive interfaces, and transparent pricing attracted millions of young investors who found traditional brokers complex and expensive.

The market share numbers were sobering. While Motilal Oswal grew, discount brokers grew faster. The young demographic—crucial for long-term sustainability—overwhelmingly chose discount brokers. The challenge wasn't just about current revenue but future relevance.

Regulatory evolution added complexity. SEBI's margin requirements, peak margin norms, and settlement cycles kept changing. Each change required system modifications, process updates, and client education. Compliance costs escalated. Smaller competitors struggled, but so did established players like Motilal Oswal who had complex multi-business operations.

The talent challenge was equally acute. Technology companies and startups offered stock options and cultural appeal that traditional financial services couldn't match. The best engineers went to Bangalore, not Bombay. Young MBAs preferred product management at unicorns over research at brokerages. Attracting and retaining talent became increasingly expensive.

Through each crisis, certain patterns emerged in their response. First, they never denied problems—acknowledgment preceded action. Second, they over-invested in fixing issues rather than minimal compliance. Third, they communicated transparently with stakeholders even when news was bad. Fourth, they used crises to strengthen systems rather than just address symptoms.

The NSEL aftermath led to complete overhaul of risk management. Multiple approval layers were introduced. Independent compliance officers were appointed for each vertical. Regular audits became more stringent. The cost was high—both financial and operational—but necessary for survival.

Post-ransomware attack, cybersecurity became board-level priority. External experts were hired. Infrastructure was upgraded. Employee training was intensified. Incident response procedures were documented. They learned that in digital age, cybersecurity wasn't IT issue but existential risk.

The competitive response to discount brokers was nuanced. Instead of matching prices, they doubled down on value. Research quality was enhanced. Advisory services were strengthened. Technology was improved but positioned as enabler not replacement for human insight. They accepted smaller market share for higher-quality clients.

What's remarkable is how they maintained growth despite challenges. Revenue reached ₹8,759 crore with profit of ₹2,787 crore, proving that controversies, while damaging, weren't fatal. The resilience came from diversification—when one business faced headwinds, others compensated.

The challenges revealed important truth: in financial services, trust takes decades to build but moments to destroy. Every regulatory violation, every security breach, every client complaint chips away at reputation. But if the foundation is strong—built on genuine value creation rather than just regulatory arbitrage—firms can survive and even thrive despite setbacks.

As they navigate current challenges, the lessons from past crises guide them. Compliance isn't cost but investment. Technology isn't just efficiency but security. Competition isn't threat but catalyst for improvement. Most importantly, challenges aren't just problems to solve but opportunities to build resilience. This philosophy of turning adversity into advantage would prove crucial as they faced an evolving competitive landscape.

IX. Current Business Model & Financial Performance (30-40 min)

Understanding Motilal Oswal's current business model requires appreciating how three distinct pillars—Capital Markets, Asset & Wealth Management, and Housing Finance—create synergistic value while maintaining operational independence.

The company stands as one of India's largest full-service brokers with the highest gross brokerage revenue as of March 31, 2023. But this leadership position masks fundamental transformation—they're no longer just executing trades but orchestrating comprehensive financial solutions.

The Capital Markets business, contributing roughly 60% of revenues, operates on multiple engines. Retail broking leverages the phygital model serving 40 lakh clients. Institutional broking caters to 500+ domestic and foreign institutions. Investment banking has executed 150+ transactions worth ₹50,000+ crore. Each vertical reinforces others—research excellence attracts institutional clients who generate investment banking mandates.

The Asset Management vertical has emerged as the growth driver. With AUM of ₹64,857 crore as of December 2023, alternate assets comprising PMS and AIF represent 33.52%—among the industry's highest shares. This isn't just asset gathering but active management with conviction. Their concentrated portfolios, typically holding 20-25 stocks versus industry average of 50+, demonstrate confidence in research.

The mutual fund business reached average AUM of ₹42,406 crore by December 2023. With net AUM of ₹45,993.97 crore across 34 schemes including 14 equity, 5 debt, and 5 hybrid funds, they've achieved scale while maintaining investment discipline. The focus on equity funds (70% of AUM) reflects their core competence rather than asset-gathering ambitions.

The Wealth Management division serves a different constituency. With wealth AUM growing from ₹51,997 crore to ₹89,632 crore (117% YoY) by December 2023, they're capturing India's wealth creation boom. The average client has ₹15+ crore invested, generating fees that justify personalized service. This isn't mass affluent but genuinely wealthy Indians seeking sophisticated solutions.

Housing Finance, though smallest, is strategically important. With PAT of ₹136.36 crore in FY2023 (43.66% YoY growth), it serves as customer acquisition funnel. Today's home loan customer becomes tomorrow's broking client and eventually wealth management prospect. The lifetime value justifies lower initial margins.

The financial performance validates the model. Market capitalization of ₹54,657 crore, revenue of ₹8,759 crore, and profit of ₹2,787 crore represent not just scale but quality. The return on equity consistently exceeding 20% demonstrates capital efficiency. The profit margins around 30% prove pricing power despite intense competition.

Revenue mix evolution tells the transformation story. Broking contributed 90% in 2000, 60% in 2010, and now approximately 40%. Asset management grew from nothing to 30%. Wealth management and housing finance contribute 20%. Investment banking and others provide 10%. This diversification reduces cyclical vulnerability while maintaining growth momentum.

The operational metrics reveal competitive advantages. Cost-to-income ratio around 65% beats industry average of 75%. Client acquisition cost has dropped 40% through digital channels. Cross-sell ratio exceeds 2.5 products per client. Net promoter scores consistently exceed 70. These aren't just numbers but evidence of operational excellence.

Market share gains are particularly impressive. Average daily turnover market share improved 50 basis points quarter-on-quarter with 45% growth in average yearly turnover. Currency market share improved 150 basis points to 12%, while commodity market share stood at 7%. They're gaining share while maintaining margins—the holy grail of financial services.

The balance sheet strength enables strategic flexibility. Net worth exceeding ₹8,000 crore provides buffer against volatility. Debt-to-equity ratio below 2x is conservative for financial services. Liquid investments exceeding ₹3,000 crore ensure resilience. This fortress balance sheet allows countercyclical investing when competitors retrench.

The margin trading book growing 39% to ₹2,920 crore indicates client confidence and risk appetite. But they've learned from past mistakes—exposure limits are strict, collateral quality is high, and risk management is dynamic. They're facilitating leverage without taking excessive risk.

What's most impressive is maintaining founder intensity at this scale. With promoter holding at 67.8%, skin in the game remains high. Raamdeo and Motilal remain actively involved—not just as figureheads but as decision-makers. This continuity provides stability rare in Indian financial services.

The unit economics reveal the real moat. Customer lifetime value exceeds ₹1 lakh for broking clients, ₹10 lakh for wealth clients. Payback periods are 18 months for digital acquisition, 36 months for physical. Retention rates exceed 85% for clients with 3+ products. These metrics explain why they can afford premium service despite price competition.

Looking at segment performance, each business shows different dynamics. Capital markets benefits from market volatility and retail participation. Asset management grows with market appreciation and financialization. Housing finance expands with urbanization and aspiration. This portfolio approach ensures growth regardless of specific cycles.

The current model isn't just about financial metrics but strategic positioning. They've successfully positioned themselves as the thinking investor's choice—more expensive than discount brokers but worth it, less prestigious than foreign banks but more accessible. This sweet spot between mass and class proves surprisingly large and profitable. As we'll examine next, this positioning creates both opportunities and vulnerabilities in the evolving landscape.

X. The Playbook: Lessons in Building Financial Services (25-35 min)

After 37 years of building Motilal Oswal, certain patterns emerge that transcend specific decisions or circumstances. These aren't just lessons but a replicable playbook for building enduring financial services businesses in emerging markets.

Research as Competitive Advantage

The Wealth Creation Study wasn't just annual report—it was strategic weapon. Published annually since 1996, the study analyzed fastest, most consistent, and biggest value-creating companies, examining different aspects yearly from economic moats to commodity cycles. This intellectual property created network effects: better research attracted better clients who paid higher fees, funding better research.

The commitment ran deep. Allocating 10% of revenue to equity research, building teams of 25+ analysts covering 250+ companies across 20 sectors—this wasn't cost but investment. In an industry where research was loss leader, they made it profit center by monetizing insights across multiple verticals: broking, investment banking, asset management.

Value Investing Philosophy Permeating All Verticals

The QGLP framework—Quality, Growth, Longevity, and Price—wasn't just investment philosophy but organizational DNA. Whether evaluating stocks for mutual funds, companies for private equity, or clients for lending, the same principles applied. This consistency created institutional memory and decision-making frameworks that survived personnel changes.

The philosophy extended to business decisions. They entered businesses with longevity, partnered with quality institutions, grew sustainably, and maintained price discipline. The same framework that selected stocks selected strategies. This alignment between investing philosophy and business philosophy created unusual coherence.

Founder-Led Culture After 37+ Years

Most Indian businesses struggle with succession. Motilal Oswal solved this by never fully professionalizing. Raamdeo, worth $1.7 billion, still reviews research reports. Motilal still meets key clients. This isn't micromanagement but culture preservation. Their presence ensures every employee knows the founders are watching, caring, and enforcing standards.

The founder involvement goes beyond oversight. They're the chief evangelists, spending significant time on investor education, media appearances, and thought leadership. This visibility creates accountability—when founders publicly espouse principles, organizations must follow them.

Balancing Innovation with Regulatory Compliance

Financial services innovation often means regulatory arbitrage. Motilal Oswal chose different path: innovation within boundaries. They were early adopters of technology, creators of new products, pioneers of new models—but always within regulatory framework. This conservatism cost opportunities but prevented existential threats.

When regulations changed, they over-complied rather than finding loopholes. This approach seemed expensive but proved economical—they spent on systems not penalties, on processes not litigation. The clean reputation became competitive advantage, especially with institutional clients who couldn't afford regulatory risk.

Network Effects in Financial Services Distribution

With 2,500+ business locations across 550+ cities, they built network effects rare in financial services. Each location wasn't just distribution but data collection point. Understanding local markets, relationships, and preferences created insights that centralized competitors couldn't match.

The network created virtuous cycle: more locations meant more clients, more clients meant more products, more products meant more revenue per location, more revenue justified more locations. This physical network, expensive to build and maintain, became moat against digital-only competitors who lacked local presence.

Managing Cyclicality in Capital Markets

Financial services are inherently cyclical, but Motilal Oswal smoothed volatility through portfolio approach. When equity markets declined, housing finance grew. When IPO markets froze, wealth management expanded. When retail broking slowed, institutional business compensated. Diversification wasn't just risk management but growth strategy.

Counter-cyclical thinking was institutionalized. They hired during downturns, invested during crises, and expanded during recessions. This required strong balance sheet and stronger nerves, but created exceptional returns. Buying assets cheap and hiring talent desperate created structural advantages.

The Power of Patient Capital and Long-Term Thinking

In an industry obsessed with quarterly results, they played different game. Holding Hero MotoCorp when stock price plateaued for years, maintaining conviction when others fled—this patience wasn't passive but active choice. Long-term thinking attracted long-term clients who generated stable revenues.

Patient capital enabled strategic investments. Building research capabilities, technology infrastructure, brand equity—all required years of investment before returns. Competitors focused on immediate profitability couldn't match these investments. Time became their ally, not enemy.

The Synthesis of Physical and Digital

The "Phygital" model wasn't compromise but synthesis. They understood that Indians wanted both efficiency and empathy, convenience and comfort. Digital tools for routine transactions, human advisors for complex decisions. This wasn't either/or but both/and thinking.

The model required duplicate investments—maintaining branches while building apps, training relationship managers while developing algorithms. This seemed inefficient but proved effective. Clients who used both channels generated 3x revenue of single-channel users.

Culture as Strategy

Every financial services firm talks about culture; few operationalize it. At Motilal Oswal, culture wasn't poster but practice. The QGLP framework guided hiring—they hired for quality character, growth mindset, longevity orientation, and price consciousness. People who didn't fit culturally didn't survive regardless of performance.

Culture manifested in small decisions. Analysts were encouraged to disagree with consensus. Relationship managers were measured on client retention not revenue. Compliance officers had veto power over business heads. These policies, expensive and sometimes frustrating, created organization that clients trusted.

The playbook's power isn't in individual elements but their interaction. Research excellence attracted quality clients who generated stable revenues funding patient investments creating competitive advantages attracting more clients. This flywheel, once spinning, became self-reinforcing. Competitors could copy tactics but not the interconnected system built over decades. This systemic advantage, more than any single factor, explains their endurance and growth.

XI. Bear vs. Bull Case Analysis (20-30 min)

The Bear Case: Structural Headwinds and Existential Threats

The most immediate threat comes from discount brokers who have fundamentally reset customer expectations. When Zerodha offers trades at ₹20 flat and Groww provides free mutual fund investing, Motilal Oswal's percentage-based pricing seems anachronistic. Young investors, who represent the future, overwhelmingly choose discount brokers. The customer acquisition cost for 25-year-olds exceeds lifetime value at current pricing—an unsustainable equation.

The regulatory overhang from past controversies casts a long shadow. SEBI's 2019 declaration of "not fit and proper" as commodity derivative brokers remains on record. The 2022 fine for client fund misutilization reinforces perception of compliance weakness. In financial services, reputation is everything—and theirs is tainted.

The dependence on equity market performance creates vulnerability. Despite diversification, approximately 70% of revenues remain linked to market levels. A prolonged bear market would simultaneously reduce broking volumes, asset management fees, and investment banking activity. The 2008 experience, when stock price crashed 75%, could repeat.

The February 2024 LockBit ransomware attack exposed critical cybersecurity vulnerabilities, potentially affecting six million clients and risking data across business lines. In an era of increasing cyber threats, this weakness could prove catastrophic. One major breach could trigger client exodus and regulatory sanctions.

Technology-first platforms represent existential threat. Companies like Paytm Money, Groww, and even traditional banks' digital arms offer superior user experience at lower cost. They're mobile-native while Motilal Oswal retrofitted digital onto physical infrastructure. The next generation won't tolerate clunky interfaces regardless of research quality.

The talent challenge intensifies yearly. Why would top engineers join traditional financial services when startups offer equity upside? Why would young MBAs choose sell-side research when buy-side pays more? The talent pipeline that sustained growth is drying up, and throwing money at the problem destroys economics.

Market structure evolution undermines traditional advantages. As passive investing grows, research value diminishes. As algorithms dominate trading, relationship management matters less. As direct indexing emerges, mutual funds become obsolete. The capabilities that created success might become liabilities.

The Bull Case: Competitive Moats and Structural Tailwinds

The founders' combined validation—Raamdeo alone worth $1.7 billion—proves the model works. This isn't paper wealth but realized value through decades of market cycles. When founders maintain 67.8% ownership after 37 years, they're betting their wealth on continued success. This skin in the game aligns interests powerfully.

India's financialization represents multi-decade opportunity. Household savings in financial assets remain below 10% versus 40%+ in developed markets. As GDP per capita crosses $3,000, financial services adoption accelerates. The addressable market expands faster than competition can capture it.

The integrated model creates stickiness discount brokers can't match. Cross-selling to 52 lakh group clients generates revenue synergies. Clients using multiple products exhibit 85%+ retention rates versus 40% for single-product users. The lifetime value of integrated relationships justifies premium pricing.

Wealth management AUM growing 117% year-over-year to ₹89,632 crore captures India's wealth creation boom. The number of ultra-HNIs grows 15% annually. These clients need sophisticated solutions, not discount broking. Motilal Oswal's positioning as domestic alternative to foreign banks resonates with increasingly nationalist sentiment.

Brand trust in Tier 2/3 cities remains strong. While metros chase discount brokers, smaller cities value relationship and advice. With 2,500+ business locations across 550+ cities, they have presence where digital-only players don't. India beyond metros represents 70% of opportunity but receives 30% of attention.

Operating leverage at scale creates expanding margins. Technology investments are largely complete. Branch network is built. Brand is established. Incremental revenue drops disproportionately to bottom line. Current profit of ₹2,787 crore on revenue of ₹8,759 crore could expand significantly with modest revenue growth.

The research excellence moat deepens with time. Publishing the Wealth Creation Study since 1996 created institutional knowledge competitors can't replicate. Two decades of company relationships, management insights, and pattern recognition create advantages that compound rather than depreciate.

The Verdict: Transformation or Decline

The bear and bull cases aren't mutually exclusive—both could prove correct over different timeframes. Short-term challenges from discount brokers and technology platforms are real and intensifying. Long-term opportunities from India's financialization and wealth creation are equally real and accelerating.

The outcome depends on execution. Can they transform technology infrastructure before customers defect? Can they attract talent despite structural disadvantages? Can they maintain compliance standards preventing future controversies? Can they navigate the transition from founder-led to professionally-managed?

The asymmetry favors bulls. Downside seems limited—strong balance sheet, profitable operations, and loyal customer base provide cushion. Upside appears substantial—India's financial services penetration doubling would more than offset market share losses. For patient investors, risk-reward seems favorable.

But the real insight is that Motilal Oswal faces inflection point. The next five years will determine whether they become India's Charles Schwab—successfully transitioning from traditional broker to diversified financial services powerhouse—or India's E.F. Hutton—a once-prominent name that couldn't adapt to changing times. The playbook that created success might not sustain it. Evolution, not revolution, seems both necessary and possible.

XII. Epilogue: The Next Chapter (10-15 min)

As morning light filters through the windows of Motilal Oswal Tower in Mumbai's Lower Parel, Raamdeo Agrawal, now in his sixties, still arrives before markets open. The journey from a ₹5,000 sub-broker badge to a ₹54,657 crore empire spans not just decades but entire eras of Indian capitalism. Yet the most crucial chapters may lie ahead.

Succession planning looms as the defining challenge. While the next generation has joined the business, the transition from founder-led to family-managed requires delicate orchestration. The industry littered with failed successions—from Parekh to Piramal—serves as cautionary reminder. Can they institutionalize the founder's vision while maintaining entrepreneurial energy?

The technological evolution accelerates beyond digital apps and online platforms. Artificial intelligence promises to democratize institutional-quality research—their core differentiator. When GPT models can analyze financial statements and generate investment recommendations, what happens to armies of analysts? They're experimenting with AI-augmented research, but the balance between human insight and machine intelligence remains undefined.

International expansion beckons but requires careful consideration. The NRI market offers natural extension, but competing globally means facing Goldman Sachs and Morgan Stanley on their turf. The domestic focus that enabled success might also limit growth. The question isn't whether to go global but how to do so without losing local advantages.

The consolidation opportunity in India's fragmented financial services market appears compelling. With 3,000+ brokers, 40+ mutual funds, and countless wealth managers, rationalization seems inevitable. Their strong balance sheet and proven integration capabilities position them as natural consolidator. But acquisitions bring cultural dilution risks they've historically avoided.

The vision for the next decade reflects both ambition and pragmatism. They speak of becoming India's premier wealth manager, the trusted advisor for affluent Indians' financial journey. Not the largest but the most respected. Not the cheapest but the most valuable. This positioning—premium but accessible, sophisticated but approachable—could prove sustainable.

The regulatory environment will shape possibilities. India's capital markets regulator grows increasingly sophisticated and demanding. The informal advantages that benefited early movers—relationships, local knowledge, regulatory arbitrage—matter less. Future success requires genuine innovation and operational excellence, not just market access and distribution.

With assets under advice exceeding ₹4.4 lakh crore, they've achieved scale but not dominance. The next decade's challenge isn't growing bigger but growing better—improving margins, deepening relationships, and enhancing services. Quality over quantity, depth over breadth, value over volume.

The broader implications extend beyond one company's trajectory. Motilal Oswal represents indigenous Indian financial services—built by Indians, for Indians, reflecting Indian values. Their success or failure carries symbolic weight in an industry increasingly dominated by foreign technology and capital. Can domestic firms compete with global giants while serving local needs?

As markets open for another trading day, the fundamental question remains unchanged from 1987: how to create sustainable wealth in volatile markets? The tools evolved from handwritten notes to algorithmic trading, the scale expanded from thousands to millions, but the core mission endures—democratizing quality investing for Indian investors.

The next chapter won't be written by founders but by the institution they built. Whether Motilal Oswal becomes enduring franchise like HDFC or fades like countless former market leaders depends on navigating three transitions: from founder-led to professionally-managed, from physical to digital, and from domestic to global. The playbook that brought them here won't take them there, but the principles underlying that playbook—research excellence, client focus, long-term thinking—remain timeless.

The story of Motilal Oswal isn't complete. At 37 years, they're middle-aged by corporate standards—old enough to have wisdom, young enough to transform. The ₹5,000 investment that started this journey generated extraordinary returns, but the best investments, like the best stories, save their greatest returns for last. For long-term investors seeking exposure to India's financialization, the question isn't whether Motilal Oswal succeeded but whether they'll continue succeeding. The evidence suggests they will, but in ways that might surprise even their founders.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube