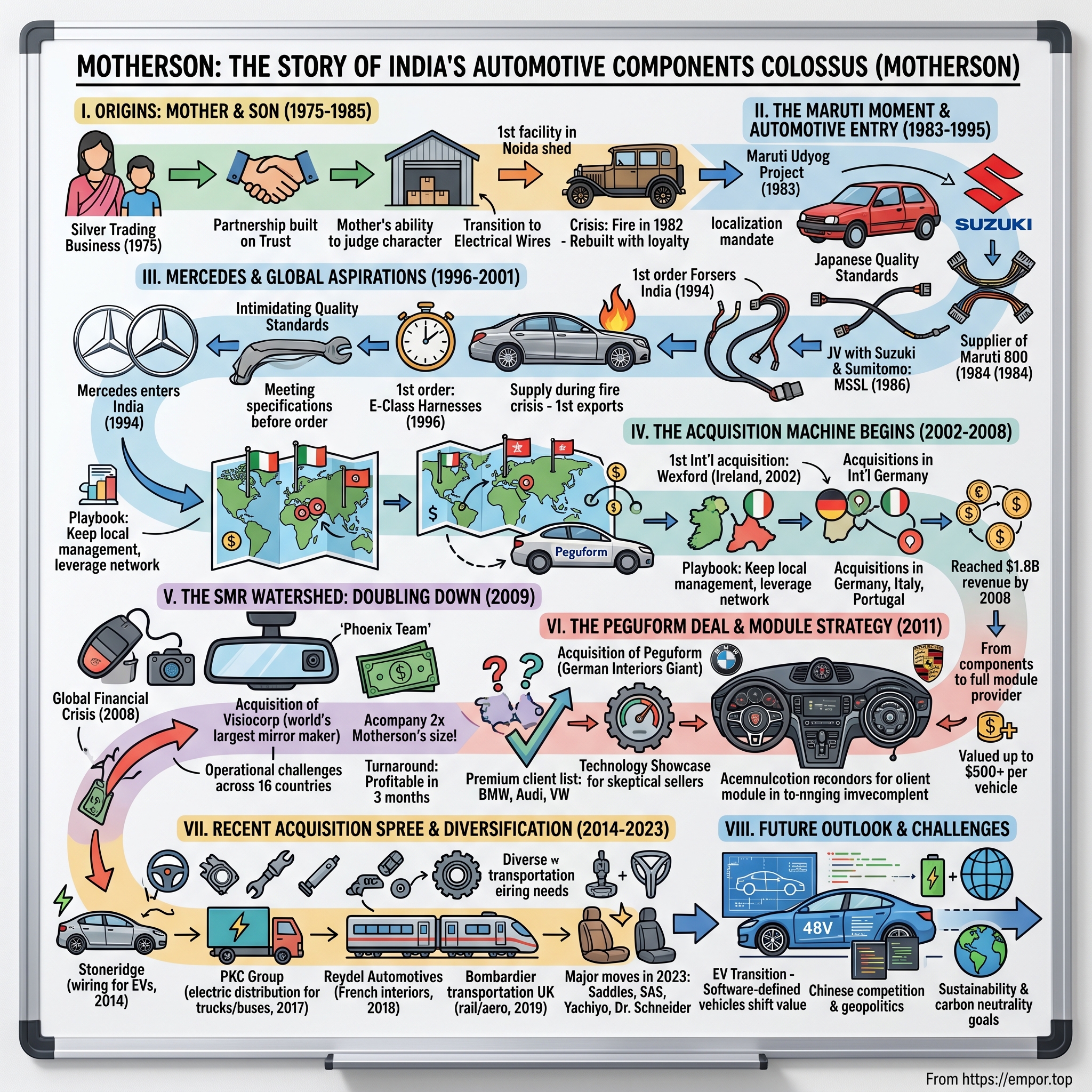

Motherson: The Story of India's Automotive Components Colossus

I. Introduction & Episode Setup

In the sprawling industrial corridors outside Delhi, where the dust from construction sites mingles with the exhaust of countless trucks ferrying auto parts, stands a nondescript building that serves as the nerve center for one of the most remarkable business transformations in modern corporate history. From this headquarters, Samvardhana Motherson International orchestrates a global empire spanning 350 facilities across 41 countries, employing over 180,000 people, and generating revenues of ₹1,13,663 crore—roughly $13.7 billion.

The numbers alone command attention: a market capitalization of ₹96,520 crore places Motherson among India's corporate elite. But what makes this story truly extraordinary isn't just the scale—it's the journey. How does a mother-son silver trading operation, started with modest capital in 1975, transform into one of the world's largest automotive component suppliers, counting Mercedes-Benz, BMW, Volkswagen, and virtually every major automaker as customers?

This is a story about trust—a word that Vivek Chaand Sehgal, the company's founder and chairman, invokes with almost religious fervor. It's about perfectly timed bets on India's automotive revolution, starting with the Maruti 800. It's about an acquisition machine that has averaged one deal per year since 2002, often buying companies twice its own size. And perhaps most remarkably, it's about maintaining a 40% return on capital employed target for over two decades while expanding at breakneck speed.

The Motherson playbook defies conventional wisdom. While most Indian companies of its generation either remained domestic players or struggled with international expansion, Motherson became genuinely global—with less than 10% revenue from any single customer and operations spread across five continents. They didn't just supply parts; they became indispensable partners to the world's most demanding automakers.

Today, when you sit in a Mercedes S-Class and adjust your rearview mirror, when you grip the steering wheel of a BMW, or when you notice the seamlessly integrated dashboard of an Audi, you're likely touching something made by Motherson. The company has become so deeply embedded in the global automotive supply chain that it's virtually impossible to find a car without its components.

But this isn't just another corporate success story. It's a masterclass in strategic patience, disciplined capital allocation, and the art of cultural integration across borders. It's about how an Indian company cracked the code of becoming a trusted tier-one supplier to the world's most prestigious brands—at a time when "Made in India" was more liability than asset in global markets.

As we unpack this journey, we'll explore how Motherson navigated India's pre-liberalization maze, seized the Maruti moment, earned Mercedes' trust, and then embarked on an acquisition spree that would make even the most aggressive private equity firms blush. We'll examine their unique Five-Year Plan culture, their obsession with customer diversification, and how they're positioning themselves for the electric vehicle revolution that threatens to upend their entire industry.

This is the story of Motherson—a company that proves emerging market champions don't need to follow Western playbooks to succeed globally. Sometimes, a mother's blessing and a son's ambition, combined with relentless execution and an almost naive belief in trust-based business, can build something extraordinary.

II. Origins: Mother & Son (1975-1985)

The year was 1975. India was in the grip of Indira Gandhi's Emergency, a period of suspended civil liberties and press censorship that would become one of the darkest chapters in the country's democratic history. The economy was strangled by the License Raj—a byzantine system of permits and quotas that made starting any business an exercise in bureaucratic navigation. Foreign exchange was so tightly controlled that importing a simple machine part required government approval. In this suffocating environment, where entrepreneurship was viewed with suspicion and private enterprise faced endless restrictions, Vivek Chaand Sehgal made a decision that would seem either brave or foolish: he would start a business with his mother.

Sehgal was not your typical entrepreneur. Educated and soft-spoken, he came from a middle-class family that valued stability over risk-taking. His mother, a traditional Indian woman who had never worked outside the home, seemed an even more unlikely business partner. But they had noticed something others had missed: in the chaos of India's controlled economy, silver trading offered a unique opportunity. The metal was needed for various industrial applications, religious ceremonies, and jewelry, yet the market was highly fragmented and inefficient.

"My mother had this incredible ability to judge character," Sehgal would later recall in a rare interview. "She could meet someone once and tell you whether they were trustworthy. In the silver trading business, where deals were often made on handshakes and promises, this was invaluable." The partnership was unconventional—a son handling operations and negotiations while his mother provided the moral compass and, surprisingly, the strategic vision.

The naming of the company revealed everything about their approach. Sehgal's father, watching this unlikely partnership take shape, suggested "Motherson"—a portmanteau that captured both the literal partnership and something deeper. "I loved it immediately," Sehgal explains. "In Indian culture, the mother-son bond represents unconditional trust and sacrifice. It signified that this company would be built on relationships, not just transactions."

The silver trading business was profitable but limiting. By 1978, as they watched their working capital tied up in commodity cycles and their growth constrained by market volatility, the mother-son duo made their first strategic pivot. They noticed that India's nascent electrical infrastructure boom—driven by rural electrification programs and urban construction—was creating demand for basic electrical components. Specifically, electrical wiring for homes was being imported at high costs or produced locally with poor quality.

The transition from trading to manufacturing wasn't smooth. Their first facility, a small shed in Noida, could barely be called a factory. They had two second-hand wire-drawing machines purchased from a closing textile mill, a handful of workers, and a quality control process that consisted of Sehgal personally testing every batch. The pre-liberalization economy meant that getting raw materials required navigating a maze of government allocations. Copper, the primary input, was controlled by the state, and private companies received quotas based on mysterious calculations that seemed to change monthly.

What set Motherson apart in these early years wasn't technology or scale—they had neither. It was their approach to business relationships. In an era where suppliers routinely delivered substandard goods and payment delays were endemic, Motherson built a reputation for two things: consistent quality and paying on time. "We would rather lose money on an order than deliver something substandard," became Sehgal's mantra, one that seemed quaint in the rough-and-tumble world of Indian manufacturing.

By 1980, Motherson had graduated from household wiring to industrial cables. They won their first significant contract with Delhi Transport Corporation, supplying wiring for public buses. The order was small by global standards—worth less than ₹10 lakhs—but it represented a crucial validation. A government entity had chosen them over established players, based purely on quality and reliability.

The early 1980s brought an unexpected challenge that would forge Motherson's character. A fire destroyed their Noida facility in 1982, wiping out inventory and equipment worth everything they had earned in seven years. Insurance in those days was minimal and claims took years to process. Most observers expected them to fold. Instead, Sehgal convinced his workers to help rebuild—many worked without pay for three months, sustained by daily meals that his mother personally cooked and served at the site.

This crisis revealed something crucial about Motherson's DNA: loyalty flowed both ways. Every worker who stayed through the crisis became a shareholder when the company later incorporated. Many of their children still work at Motherson today, four decades later. This approach to human capital—treating workers as family rather than resources—would become instrumental when Motherson later acquired Western companies with strong union cultures.

By 1983, Motherson had rebuilt stronger than before. They were now producing specialized cables for industrial applications, with annual revenues touching ₹1 crore. They had also begun experimenting with polymer compounds, sensing that plastics would revolutionize electrical insulation. But the real transformation was about to come from an unexpected source: a small Japanese car that most Indians couldn't yet afford to dream about.

As 1983 drew to a close, rumors swirled through Delhi's business circles about a joint venture between the government and Japan's Suzuki Motor Corporation. The project, to be called Maruti Udyog, aimed to produce an affordable car for middle-class Indians. For Motherson, quietly making cables in Noida, this news would change everything. The age of Indian automotive was about to dawn, and with it, the opportunity that would transform a small cable manufacturer into a global automotive giant.

III. The Maruti Moment & Automotive Entry (1983-1995)

The press conference at Delhi's Ashok Hotel on December 14, 1983, was packed beyond capacity. Journalists crammed into doorways as R.C. Bhargava, the newly appointed managing director of Maruti Udyog, unveiled a small red hatchback that looked almost toy-like next to the hulking Ambassador and Premier Padmini cars that dominated Indian roads. The Maruti 800, priced at ₹48,000, promised something revolutionary: a car that a middle-class family could actually afford, that would actually start in the morning, and that wouldn't guzzle petrol like its predecessors.

Vivek Sehgal was in that audience, but not as a journalist or curious onlooker. He had managed to secure an invitation through a government contact, and he sat transfixed as Bhargava explained the localization requirements. The Indian government had mandated that within five years, 95% of the car's components must be made locally. Japanese quality standards would be non-negotiable. Most Indian manufacturers in the room mentally calculated their chances and quietly slipped out. The technical requirements were unlike anything Indian industry had seen.

"I stayed until the very end," Sehgal would later recount. "After everyone left, I approached the Suzuki team. I didn't pitch our company or talk about our capabilities. I simply asked: 'What is the most critical component you're worried about localizing?' The Japanese executive looked at me with surprise and said, 'Wiring harnesses. They're the nervous system of the car. One faulty connection and the entire vehicle fails.'"

Sehgal had never made an automotive wiring harness. In fact, he had to look up what exactly it entailed—bundles of wires and connectors that carry power and information throughout the vehicle, requiring precision that household wiring never demanded. But he saw opportunity where others saw impossibility. The next morning, he was on a flight to Japan, having maxed out Motherson's credit to buy the ticket.

What happened in Japan became Motherson lore. Sehgal spent three weeks sleeping in capsule hotels and visiting Suzuki suppliers, not to pitch business but to understand. He studied how harnesses were made, tested, and integrated. He learned about Japanese quality philosophy—concepts like Kaizen and Zero Defect that seemed almost mystical to Indian manufacturers accustomed to "acceptable" defect rates of 5-10%.

Upon returning, Sehgal made a decision that his board—now expanded to include external investors—thought was insane. He would build a facility specifically for Maruti before securing a single order. Using borrowed money at 18% interest rates, Motherson constructed a 10,000-square-foot facility in Noida that replicated Japanese clean room standards. Workers would remove shoes, wear uniforms, and follow protocols that seemed excessive for an industrial product.

The gamble paid off spectacularly. When Maruti's procurement team visited in March 1984, they found something unprecedented in India: a facility that looked like it belonged in Hamamatsu rather than Noida. But the real test came with the samples. Motherson's harnesses had to undergo 200 hours of vibration testing, temperature cycling from -40°C to +85°C, and salt spray exposure that simulated years of corrosion. They passed every test.

On October 1, 1984, when the first Maruti 800 rolled off the assembly line with Prime Minister Indira Gandhi handing over keys to the first customer, Motherson's wiring harnesses were inside. It was a small component in value terms—worth perhaps ₹800 per car—but symbolically enormous. An Indian company had met Japanese quality standards in one of the most critical safety components.

The Maruti plant in Gurgaon became Motherson's university. Suzuki engineers, initially skeptical of Indian suppliers, began working closely with Motherson to improve processes. They introduced Statistical Process Control, Total Quality Management, and Just-In-Time delivery—concepts that would revolutionize Indian manufacturing. Motherson absorbed these lessons with remarkable speed, often surprising their Japanese mentors.

By 1986, the relationship had evolved beyond supplier-customer. Suzuki proposed something unprecedented: a joint venture to create a dedicated automotive components company. The company was established in 1986 as a joint venture with the Sumitomo Group of Japan, specifically Sumitomo Wiring Systems, marking a pivotal transformation from domestic supplier to international standards bearer.

The joint venture, christened Motherson Sumi Systems Limited (MSSL), brought together Motherson's local market knowledge and Sumitomo's technical expertise in a structure that was unusual for its time. Unlike typical joint ventures where the foreign partner dominated, this was structured as an equal partnership with clearly defined roles: Sumitomo would provide technology and quality systems, while Motherson would handle local operations and customer relationships.

The cultural integration proved fascinating. Japanese executives arrived in Noida expecting chaos; instead, they found workers who had already internalized quality principles through the Maruti experience. One Sumitomo engineer reportedly said, "We came to teach, but we also learned. The Indian approach to jugaad—creative problem-solving—complemented our systematic methods in unexpected ways."

The timing couldn't have been better. Maruti's sales exploded from 5,759 units in 1984 to over 100,000 by 1990. Every car needed a wiring harness, and Motherson Sumi was supplying the majority. But Sehgal understood that depending on one customer, even one as successful as Maruti, was dangerous. He began courting other manufacturers entering India—Daewoo, Hyundai, Honda—each requiring localization but demanding global quality.

The real test came in 1991 when India's economic crisis forced the government to liberalize the economy. Suddenly, import duties dropped, foreign competitors could enter, and Indian companies faced global competition. Many local auto component makers, protected for decades, crumbled. Motherson Sumi thrived. Their joint venture structure had already forced them to meet international standards, and liberalization simply leveled a playing field where they were already competitive.

By 1993, Motherson Sumi took another bold step: listing on the Bombay Stock Exchange. The IPO was modest—raising just ₹15 crores—but it signaled ambition beyond being a vendor. They were building an institution. The prospectus made interesting reading, promising not just growth but a commitment to maintaining 40% return on capital employed, a metric that would become Motherson's North Star.

The mid-1990s brought an unexpected opportunity that would reshape Motherson's destiny. Mercedes-Benz, the epitome of automotive luxury, announced plans to enter India. For a company that had built its reputation on small car wiring harnesses, the chance to supply the three-pointed star seemed almost fantastical. But Sehgal saw it differently: this was the moment to prove that an Indian company could meet the standards of the world's most demanding automaker.

IV. Mercedes & Global Aspirations (1996-2001)

The Mercedes-Benz executives who landed in Delhi in January 1994 carried with them a 400-page manual titled "Supplier Quality Standards for Mercedes-Benz Worldwide Operations." The document, translated into English but retaining its German precision, specified everything from the thread count in worker uniforms to the acceptable variance in crimp pressure for wire terminals—measured in hundredths of a Newton. Most Indian suppliers who received the manual returned it unopened, intimidated by requirements that seemed designed for a different planet.

Vivek Sehgal spent three nights reading every page, making notes in the margins. On page 247, discussing supplier facility requirements, he found his opportunity: "Suppliers must demonstrate capability to establish dedicated production lines within 60 days of order confirmation." Most established suppliers needed six months. Sehgal called his team together with a simple question: "Can we do it in 30?"

Mercedes was the first luxury car brand to enter the Indian market in 1994, choosing to assemble the E-Class at a new facility in Pune rather than simply import completely built units. This decision, driven by India's steep import duties, meant they needed local suppliers who could meet their exacting standards. The head of Mercedes procurement, Wolfgang Renschler, was skeptical. In his previous role in Brazil, he had spent two years developing local suppliers with mixed results.

The Motherson Sumi presentation to Mercedes was unlike anything Renschler had seen from an Indian company. Instead of promises and relationship-building—the typical Indian business approach—Sehgal's team presented data: defect rates per million opportunities, statistical process control charts, real-time quality metrics from their Maruti supplies. But what caught Renschler's attention was something else: Motherson Sumi was already implementing Mercedes' quality standards without having received a single order.

"We visited their facility expecting to make a list of required improvements," Renschler would later recount at a supplier conference. "Instead, we found they had anticipated our requirements. They had created a clean room that exceeded our specifications, trained workers in German quality methods using materials they had translated themselves, and even installed testing equipment typically found only in our German suppliers' facilities."

The order came through in February 1996: wiring harnesses for 500 E-Class vehicles annually, with potential expansion to dashboard assemblies if quality targets were met. The volumes were tiny compared to Maruti—Mercedes sold in a year what Maruti sold in a week—but the symbolic value was enormous. The per-unit price Mercedes paid was three times what Maruti paid for similar complexity harnesses.

Then came the moment that would become Motherson legend. The first batch of production was scheduled for April 1996, giving them 60 days to set up. On March 7, 1996, a fire broke out at Mercedes' primary harness supplier in Germany, disrupting European production. Mercedes desperately needed alternative supply. Sehgal received a call at 2 AM: Could Motherson Sumi supply harnesses not just for Indian assembly but for export to Germany?

In 39 days—not the promised 60—Motherson Sumi had a fully operational Mercedes production line. But more remarkably, they shipped their first export batch to Stuttgart before supplying the Pune facility. When those harnesses arrived in Germany and passed quality inspection without a single defect, it sent shockwaves through Mercedes' global procurement team. An Indian supplier had met German quality standards on the first attempt, something many established European suppliers struggled with.

The Mercedes relationship opened doors that had been firmly shut. BMW, Volkswagen, and Audi—all planning Indian entries—began approaching Motherson Sumi. But Sehgal was thinking bigger. If they could meet Mercedes standards in India, why not supply Mercedes globally? This audacious thought led to the company's first Five-Year Plan, launched in 2000.

The plan, presented to shareholders in a packed auditorium in Delhi, set targets that seemed delusional: achieve ₹1 billion turnover by 2005 (they were at ₹200 million), maintain 40% ROCE despite rapid expansion, and most ambitiously, ensure no single customer contributed more than 15% of revenue. An analyst from HDFC Securities stood up and asked, "Mr. Sehgal, these targets imply 40% annual growth for five years. No automotive supplier globally has achieved this. Why should we believe you can?"

Sehgal's response became part of company folklore: "Because we're not trying to be a global automotive supplier. We're trying to be our customers' most trusted partner. The growth is a byproduct of trust, not the goal itself."

The Five-Year Plan introduced another crucial element: a formal acquisition strategy. Sehgal recognized that organic growth alone wouldn't achieve their targets. They needed technology, market access, and capabilities that would take decades to build internally. The plan allocated 30% of projected cash flows to acquisitions, with specific criteria: targets must bring either technology, customer relationships, or geographic presence that Motherson Sumi lacked.

By 2001, as the plan's first year concluded, revenues had grown 47% to ₹294 million. Mercedes had expanded orders to include dashboard assemblies, making Motherson Sumi their first integrated module supplier outside Germany. BMW had begun sourcing, and Volkswagen was in advanced trials. The company had also made its first international investment, a small technical center in Frankfurt to support European customers.

But the real transformation was internal. The Mercedes experience had fundamentally changed how Motherson Sumi thought about itself. They were no longer an Indian company trying to meet international standards; they were a global supplier that happened to be headquartered in India. This shift in mindset would prove crucial for what came next: an acquisition spree that would transform them from a billion-rupee company to a billion-dollar corporation.

V. The Acquisition Machine Begins (2002-2008)

The conference room at Dublin's Shelbourne Hotel on a grey March morning in 2002 was filled with skeptical faces. Executives from Wexford Electronics, an Irish company specializing in electronic control units, had agreed to meet this Indian buyer more out of curiosity than serious intent. Wexford was bleeding money—losses of €2 million on revenues of €8 million—but they were still a European company with sophisticated technology. What could an Indian wiring harness maker possibly offer?

Vivek Sehgal didn't talk about synergies or cost savings. Instead, he pulled out a map of Europe and began placing small red dots. "These are Mercedes factories. These are BMW facilities. Here's Volkswagen." Then he added blue dots. "These are where Wexford's technologies are needed but you're not present." The room went quiet. Sehgal continued, "We don't want to buy Wexford to strip its costs. We want to buy it to multiply its opportunities."

The Wexford acquisition, completed for €3.5 million in September 2002, was tiny by global standards but transformative for Motherson Sumi. It wasn't just their first international acquisition; it was the prototype for a playbook they would refine over the next two decades. The approach was counterintuitive: instead of replacing management or cutting costs, Motherson Sumi invested €1 million in new equipment and retained every employee, including the CEO who had presided over the losses.

Within eighteen months, Wexford was profitable. The transformation wasn't through Indian-style cost management but through Motherson's customer relationships. Orders from Mercedes and BMW, previously unimaginable for small Wexford, began flowing. The Irish engineers, initially wary of their Indian owners, became evangelists for the Motherson way. The CEO, Patrick O'Brien, would later say, "We expected colonial masters. We got partners who understood our potential better than we did."

The Wexford success established three principles that would guide every subsequent acquisition. First, never acquire for cost arbitrage alone—buy for capability, customer access, or technology. Second, retain and empower local management, integrating culture slowly rather than imposing change. Third, leverage the entire Motherson network to multiply the acquired company's opportunities.

Between 2002 and 2007, Motherson Sumi executed six acquisitions, five in Europe. Each followed the Wexford template but added new dimensions. The 2004 purchase of a small German engineering firm brought design capabilities. The 2005 acquisition of an Italian plastics component maker added polymer processing expertise. A Portuguese operation in 2006 provided entry into Iberian markets. None exceeded €20 million in price, but collectively they transformed Motherson from an Indian supplier with international customers to a genuinely global operation.

The acquisition strategy was funded through a combination of internal accruals and creative financing. Motherson pioneered the use of Foreign Currency Convertible Bonds (FCCBs) for Indian companies, raising $100 million in 2005 at rates that seemed impossible for an emerging market manufacturer. The bond prospectus made fascinating reading—instead of emphasizing cost advantages, it highlighted Motherson's customer concentration metrics (no customer over 15%) and ROCE consistency (over 40% for five consecutive years).

But the real genius was in integration. Unlike Western acquirers who typically imposed standardized systems immediately, Motherson Sumi took what they called the "2-3-5 approach." For two years, observe and understand. In year three, begin selective integration. By year five, achieve full cultural and operational harmony. This patience seemed inefficient to Western observers but proved remarkably effective.

The approach was tested severely with the 2007 acquisition of a British foam technology company supplying Jaguar Land Rover. The company's union was militant, having fought off three previous acquisition attempts. The union leader, Tommy Morrison, prepared for battle when the Indians arrived. Instead, he found Sehgal sitting in the factory canteen, eating the same food as workers, asking about their families, their concerns, their ideas for improvement.

"Other buyers came with PowerPoints about synergies," Morrison recalled. "Sehgal came with questions about our children's education and our pension concerns. He promised no involuntary redundancies for five years—and put it in writing. We'd never seen anything like it. "The company's approach to cultural integration was revolutionary in Indian M&A practice. Motherson Sumi Systems went on to acquire several companies, the first being in 2002 when it acquired the assets of the bankrupt Irish company Wexford Electronics, a manufacturer of wiring harnesses for material handling and earthmoving equipment. Each acquisition became a laboratory for refining their integration model.

By 2008, the acquisition machine had transformed Motherson's scale and scope. From a $200 million company in 2002, they had grown to $1.8 billion, with operations in ten countries. The second Five-Year Plan (2005-2010) target of becoming a billion-dollar company had been achieved three years early. More importantly, customer concentration had reduced dramatically—no single customer contributed more than 12% of revenue, and they supplied 14 of the world's top 20 automakers.

The financial crisis of 2008, which devastated the global automotive industry, presented Motherson with its most audacious opportunity yet. As competitors retreated and valuations collapsed, Sehgal prepared to execute a deal that would double the company's size overnight. The target was Visiocorp, the world's largest manufacturer of automotive mirrors—a company twice Motherson's size and bleeding cash as auto production plummeted worldwide. What happened next would either establish Motherson as a global automotive giant or destroy everything they had built.

VI. The SMR Watershed: Doubling Down (2009)

The emergency board meeting convened at 3 AM Delhi time on February 28, 2009, via video conference connecting directors across three continents. Vivek Sehgal, calling from Frankfurt where he had been camping for three weeks, looked exhausted but determined. On the screen behind him was a single slide: "Visiocorp Acquisition—Risk or Opportunity?" The numbers were staggering—Visiocorp, with revenues of €660 million, was larger than Motherson Sumi. It was also in administration (bankruptcy), bleeding €2 million per week, with 8,500 employees across 16 countries who hadn't been paid in two months.

The global financial crisis had devastated the automotive industry. General Motors and Chrysler were heading toward bankruptcy. Global vehicle production had plummeted 20%. Every automotive supplier was slashing costs and conserving cash. In this environment, Sehgal was proposing that Motherson Sumi acquire a company twice its size, in an unfamiliar product category, with operations in countries where they had no presence. The board thought he had lost his mind.

"Let me tell you what I see," Sehgal began, his voice steady despite the fatigue. "Visiocorp makes 30% of the world's automotive mirrors. Every Mercedes, BMW, Audi—they all need mirrors. Cars can go electric, autonomous, shared—but they'll always need mirrors. The technology is irreplaceable for safety. This isn't a company in crisis; it's a monopoly in distress."

The acquisition structure was as creative as it was bold. The acquisition from Visiocorp plc (in administration) comprises only assets in the form of shares of the operating companies and no debt is being acquired from Visiocorp plc (in administration). The acquired subsidiaries also have minimal debt. SMVSL is 95% owned by Samvardhana Motherson Global Holdings Limited (SMGHL), a joint venture between MSSL and Samvardhana Motherson Finance Limited (SMFL) in the ratio of 51:49. Motherson would pay just €25 million in cash for assets that had been valued at €800 million eighteen months earlier.

But the real challenge wasn't financial—it was operational. Visiocorp's facilities were shutting down. The plant in Hungary hadn't paid electricity bills for three months and was operating on diesel generators. The Mexican facility had armed guards preventing equipment removal by unpaid suppliers. The Chinese operations were days away from being seized by local authorities. If Motherson couldn't restart operations within weeks, every major automaker would resource their mirror supplies, potentially taking years to win back.

Sehgal had assembled what he called the "Phoenix Team"—50 managers from across Motherson's global operations, each chosen for specific expertise. The team was divided into five-person units, each assigned to a distressed Visiocorp facility. Their mission: restart operations within 14 days. The preparation was military in precision. Each team carried cash—actual physical currency—to pay workers and suppliers. They had satellite phones, portable generators, even food supplies.

On March 7, 2009, the acquisition closed. In 2009, it acquired the global rearview mirror business of the world's largest rearview mirror maker Visiocorp (now renamed as Samvardhana Motherson Reflectec). Within hours, Phoenix Teams were airborne. The Hungarian team leader, Rajesh Dongre, later recalled landing in Budapest: "The Visiocorp facility looked like a war zone. Workers were burning furniture for heat. The parking lot was empty—everyone had stopped coming. But when we announced that Motherson had arrived with three months of back pay, grown men cried."

The turnaround was extraordinary. Within ten days, every Visiocorp facility was operational. Within a month, they were meeting delivery schedules that had been disrupted for six months. The secret wasn't just the cash injection—it was Motherson's approach. Instead of laying off workers as everyone expected, they retained all 8,500 employees. Instead of closing marginal facilities, they invested in upgrades. Instead of renegotiating supplier contracts, they paid all outstanding dues.

The business logic was counterintuitive but brilliant. Visiocorp's mirror technology was sophisticated—electrochromic mirrors that automatically dimmed, integrated turn signals, blind spot detection systems. This wasn't commodity manufacturing but high-tech production requiring specialized knowledge. The 8,500 employees represented decades of accumulated expertise. Losing them would mean losing the technology.

By June 2009, just three months after acquisition, the renamed Samvardhana Motherson Reflectec (SMR) was profitable. The speed stunned the industry. Volkswagen, which had been weeks away from resourcing mirrors to a Chinese supplier, instead increased orders to SMR. BMW signed a new five-year contract. Mercedes expanded SMR's content per vehicle from mirrors to complete vision systems.

But our international expansion really took off with the acquisition of mirror maker SMR — a company that was twice our size at the time. The SMR acquisition transformed Motherson's position in the global automotive hierarchy. They were no longer just a wiring harness supplier but a vision systems leader. The combined entity had revenues exceeding $3 billion, operated in 25 countries, and supplied every major global automaker.

The integration process revealed Motherson's evolved acquisition philosophy. Unlike Western acquirers who typically imposed standardized systems immediately, Motherson took a nuanced approach. They identified SMR's strengths—product technology, customer relationships, engineering capabilities—and preserved them completely. They identified weaknesses—financial controls, operational efficiency, supplier management—and gradually introduced Motherson systems.

The cultural integration was particularly fascinating. SMR's German engineers, initially skeptical of Indian ownership, discovered that Motherson's quality standards often exceeded their own. The company's ROCE focus—maintaining 40% returns even during integration—forced a discipline that German managers admired. Within a year, SMR's German operations director was advocating for Motherson methods to be implemented across European facilities.

The financial performance validated the strategy. SMR's EBITDA margins improved from negative to 12% within eighteen months. Return on capital employed reached 35%. Customer concentration decreased as SMR's technology was cross-sold to Motherson's existing customers. The acquisition, which observers had labeled reckless, was generating returns that made it look prescient.

But the SMR deal's greatest impact was psychological. Motherson had successfully acquired and integrated a company twice its size during the worst financial crisis in decades. They had proven that an Indian company could rescue and revitalize Western operations. The global automotive industry, previously skeptical of emerging market acquirers, now saw Motherson as a serious player.

The success attracted attention beyond automotive. Private equity firms began approaching Sehgal with partnership proposals. Investment banks pitched larger acquisitions. But Sehgal remained focused on a specific vision: becoming a full systems supplier, providing not just components but complete modules. The path to this vision would lead to the next transformative acquisition—one that would double Motherson's size yet again.

VII. The Peguform Deal & Module Strategy (2011)

The Porsche Cayenne that pulled up to Motherson's Noida headquarters in March 2011 was an unusual sight. The car itself wasn't remarkable—wealthy industrialists often visited. What made this arrival significant was the cargo in the trunk: a complete dashboard module, removed from a BMW 7 Series, with a note in German that translated to "Can you make this?" The module had been sent by Peguform Group, a German automotive interiors giant that was simultaneously Motherson's next acquisition target and its most skeptical potential seller.

Peguform was automotive royalty. Founded in 1959, the company had pioneered polymer-based car interiors, transforming dashboards from metal shells to sophisticated integrated modules combining electronics, safety systems, and aesthetics. Their client list read like a who's who of premium automakers—BMW, Audi, Volkswagen, Porsche. Their technology was so advanced that competitors often reverse-engineered Peguform products just to understand how they were made.

The company was also in deep trouble. The 2008 financial crisis had crushed premium car sales. Peguform's revenues had dropped 30%, and debt servicing was consuming cash flows. The company's private equity owners, who had loaded it with debt during the leveraged buyout boom, were desperate to exit. They had already rejected three potential buyers—two Chinese companies and one American firm—deeming them incapable of maintaining Peguform's technological edge.

Sehgal's approach to Peguform was different from previous acquisitions. Instead of focusing on financial metrics or synergies, he organized what he called a "Technology Showcase." For three days in Noida, Motherson's engineers demonstrated their capabilities—not in presentations but in actual production. They recreated a Peguform dashboard assembly process using equipment jury-rigged from their existing lines, achieving quality levels that matched German specifications.

The Peguform executives were stunned. "We expected to see low-cost manufacturing," recalled Thomas Müller, Peguform's Chief Technology Officer. "Instead, we saw innovation. They had developed assembly techniques we hadn't considered, using methods adapted from their wiring harness experience. It was humbling and exciting."

The negotiation took six months and nearly collapsed multiple times. The sticking point wasn't price—Motherson agreed to pay €465 million, a fair valuation. The issue was control. Peguform's German works council, representing 3,000 employees, demanded guarantees that no German facilities would close and that R&D would remain in Germany. The German government, sensitive about foreign acquisitions of industrial assets, required assurances about technology transfer and employment.

Sehgal's masterstroke was proposing a "Centers of Excellence" structure. Instead of integrating Peguform into Motherson, they would maintain it as an autonomous technology center. German facilities would lead global R&D. Indian operations would focus on cost optimization. Chinese plants would drive volume production. Each geography would leverage its strengths while sharing knowledge globally. The works council, initially hostile, became advocates for the deal.

In 2011, it acquired the German interior and exterior polymer modules maker Peguform (now named Samvardhana Motherson Peguform). The acquisition closed in December 2011, but the real work began immediately after. That was followed by SMP, a major producer of polymer modules, which doubled the size of the Motherson Group. Motherson faced a massive integration challenge: combining a German engineering culture with Indian operational efficiency, Mexican manufacturing pragmatism, and Chinese scale ambitions.

The integration revealed unexpected synergies. Peguform's polymer expertise combined with SMR's mirror technology enabled new products—integrated overhead consoles with built-in cameras and displays. Motherson's wiring harness capabilities allowed Peguform to offer fully integrated electronic modules rather than just plastic components. The company could now provide complete cockpits—dashboard, center console, door panels, and all electronics—as a single, pre-assembled unit.

The financial impact was immediate and dramatic. The combined entity's revenues jumped to $5.5 billion, achieving the third Five-Year Plan target of becoming a $5 billion company ahead of schedule. More importantly, Motherson had transformed from a component supplier to a full module provider. The value per vehicle increased from $50 for standalone components to $500+ for integrated modules.

The Peguform acquisition also brought unexpected strategic benefits. The company's facilities in Eastern Europe provided low-cost manufacturing close to German customers. The Mexican operations offered entry into the North American market just as automotive production was shifting from Detroit to Mexico. The Chinese joint ventures provided access to local automakers that Motherson had struggled to penetrate.

But perhaps the most significant outcome was credibility. By successfully acquiring and integrating a German technology leader, Motherson had proven it could handle complexity at scale. The company was no longer seen as an emerging market player punching above its weight but as a legitimate global tier-one supplier. This perception shift would prove crucial for future acquisitions.

The module strategy fundamentally changed Motherson's competitive position. Instead of competing on individual components where Chinese manufacturers had cost advantages, they competed on integrated systems where their cross-functional expertise created differentiation. A Chinese company could make cheaper mirrors or wiring harnesses, but only Motherson could deliver a complete vision system integrating mirrors, cameras, displays, and wiring in a single module.

Customer relationships deepened significantly. Automakers increasingly preferred dealing with fewer suppliers who could provide complete solutions. Motherson's ability to deliver everything from a simple mirror to a complete vehicle interior made them indispensable. BMW increased Motherson's content per vehicle from €200 to €1,200. Volkswagen designated them a strategic supplier, involving them in vehicle development from concept stage.

The success triggered a virtuous cycle. Higher content per vehicle meant better economies of scale. Better economies enabled competitive pricing. Competitive pricing won more business. More business justified further investments in technology and acquisitions. By 2013, Motherson was generating enough cash flow to fund one major acquisition annually without diluting shareholders or increasing debt beyond comfortable levels.

The transformation was remarkable. In just two years, through two massive acquisitions, Motherson had quintupled its size, expanded from components to modules, and established itself as one of the world's top 20 automotive suppliers. But Sehgal wasn't satisfied. The automotive industry was on the cusp of fundamental disruption—electrification, autonomous driving, shared mobility. Motherson needed to position itself not just for the current automotive paradigm but for whatever came next.

VIII. Recent Acquisition Spree & Diversification (2014-2023)

The Tesla Model S that Vivek Sehgal test-drove in Palo Alto in early 2014 changed everything. As the car accelerated silently from 0 to 60 mph in 4.2 seconds, Sehgal wasn't thinking about the electric powertrain or the autopilot features. He was calculating what this meant for Motherson. "A traditional luxury car has about 5 kilometers of wiring," he told his team later. "This Tesla has less than 2 kilometers but three times the data cables. The entire architecture of automobiles is about to change."

That realization triggered Motherson's most aggressive acquisition phase yet. In 2014, it bought the wiring harness business of Stoneridge Inc for $65.7 million. The Stoneridge acquisition wasn't about scale—it was about capability. Stoneridge's expertise in high-voltage wiring systems for commercial vehicles provided critical knowledge for the electrification transition. Their engineers understood how to handle the 800-volt systems that would power next-generation electric vehicles.

But the real prize came in 2017. This was followed by the acquisition of Finnish electrical distribution systems manufacturer PKC Group in 2017 for $619 million. PKC Group, a Finnish company specializing in electrical distribution systems for commercial vehicles, represented Motherson's entry into the rapidly growing electric bus and truck market. The timing was perfect—cities worldwide were mandating electric public transport, and PKC had the technology to capitalize on this shift.

The PKC integration demonstrated Motherson's evolved acquisition approach. Instead of centralizing operations, they created what they called a "Federation Model." PKC's Finnish engineers continued leading cold-weather testing—critical for electric vehicles operating in Nordic conditions. The Brazilian operations focused on biofuel-compatible systems. Chinese facilities developed solutions for mega-cities with extreme pollution. Each unit maintained autonomy while sharing innovations globally.

French interior components maker Reydel Automotives in 2018 for $201 million. The Reydel acquisition brought something different—access to French automotive elegance. Reydel had been the preferred supplier for Renault and PSA Group's premium interiors. Their soft-touch plastics and ambient lighting systems represented the aesthetic future of automotive interiors, particularly important as autonomous vehicles would transform cars into living spaces.

The pace accelerated dramatically in 2019. Bombardier Transportation's UK electrical component and systems business in 2019. This acquisition marked Motherson's first serious move beyond automotive into aerospace and rail transport, industries with similar component needs but different certification requirements and longer product lifecycles.

Then came 2023, a year that would see Motherson execute four major acquisitions in twelve months, each targeting a specific strategic gap. Samvardhana Motherson's notable acquisitions in 2023 include 51% stake in Saddles International, an Indian automotive upholstery company, for ₹207 crore (US$24 million); 100% of SAS Autosystemtechnik, a German automotive cockpit manufacturer, from Faurecia at an enterprise value of €540 million; 81% stake in the four-wheeler business of Yachiyo Industry, a Honda Group company, for ¥22.9 billion (US$208.66 million); and the insolvent German automotive supplier Dr. Schneider Group for €118.3 million.

Each 2023 acquisition told a different story. Saddles International brought leather and fabric expertise as automakers moved toward sustainable interiors. SAS Autosystemtechnik, purchased from Faurecia, added complete cockpit assembly capabilities for premium German brands. The Yachiyo acquisition from Honda provided deep access to Japanese automakers, historically difficult for non-Japanese suppliers to penetrate. Dr. Schneider, acquired from insolvency, brought specialized instrument cluster and display technologies crucial for digital cockpits.

The Dr. Schneider acquisition was particularly instructive of Motherson's approach to distressed assets. The company had developed cutting-edge head-up display technology but collapsed under debt from overexpansion. Motherson retained the entire R&D team, paid severance to laid-off workers, and honored warranty commitments to customers. Within six months, Dr. Schneider was profitable, with its technology being integrated across Motherson's global operations.

Since our first acquisition in 2002, we've welcomed 21 more companies into the Motherson family. By 2023, the cumulative impact of these acquisitions had fundamentally transformed Motherson's business model. The company was no longer just an automotive supplier but a mobility solutions provider. Their products were in cars, certainly, but also in trains, planes, trucks, buses, and even electric scooters.

The diversification strategy extended beyond transportation. Motherson began applying automotive technologies to adjacent industries. Their precision plastics found applications in medical devices. Wiring harness expertise translated to data center cable management. Vision systems technology adapted to security and surveillance. By 2023, non-automotive revenue reached 15% of total sales, providing cushion against automotive cyclicality.

The acquisition strategy also drove geographic expansion. Through acquired companies, Motherson entered markets that would have taken decades to penetrate organically. The PKC acquisition brought strong positions in Brazil and Russia. Reydel provided access to North Africa. Dr. Schneider had facilities in Eastern Europe. By 2023, Motherson operated in 41 countries, with no single country contributing more than 20% of revenue.

Financial discipline remained paramount throughout this expansion. Despite averaging more than one acquisition per year, Motherson maintained its 40% ROCE target. The secret was selective integration—keeping what worked, changing what didn't, and always focusing on cash generation. Acquired companies typically saw EBITDA margins improve by 300-500 basis points within two years of acquisition.

The human dimension of these acquisitions was remarkable. Motherson had absorbed over 50,000 employees through acquisitions, each bringing different cultures, languages, and work styles. The company's "Proud to be Part of" philosophy—emphasized in every integration—created surprising unity. Employee satisfaction scores in acquired companies often exceeded those in Motherson's organic operations.

But the most impressive achievement was customer retention. Across all acquisitions, Motherson retained over 95% of existing customers while adding new ones. This wasn't luck—it was systematic. Every acquisition included a "Customer Confidence Plan" with guaranteed supply continuity, quality improvements, and price stability for at least two years. Customers learned that Motherson acquisitions meant better service, not disruption.

The acquisition machine had transformed Motherson from a billion-dollar Indian company to a $13 billion global giant. But as Sehgal looked ahead to 2024 and beyond, he saw new challenges. The automotive industry faced its greatest disruption since the invention of the assembly line. Electric vehicles, autonomous driving, shared mobility, and software-defined vehicles threatened to obsolete traditional suppliers. Motherson's next phase wouldn't be about acquiring companies but about acquiring capabilities for an uncertain future.

IX. Product Portfolio & Technical Capabilities

Inside Motherson's Technical Center in Frankfurt, a team of engineers huddles around what looks like a car stripped to its skeleton. But this isn't a typical vehicle—it's what they call the "Component Map," a physical demonstration where every single Motherson product is highlighted in fluorescent paint. The result is striking: nearly 40% of the vehicle glows, from the intricate wiring harness snaking through the chassis like a nervous system to the sleek rearview mirrors, from the soft-touch dashboard to the precision-molded air vents. A BMW engineer visiting the center once remarked, "We build cars, but Motherson builds everything that makes them work."

The breadth of Motherson's product portfolio defies simple categorization. The company manufactures products ranging from humble door seals that cost pennies to sophisticated camera-based driver assistance systems worth thousands of dollars. This isn't random diversification—it's a carefully orchestrated strategy to become indispensable to automakers by solving multiple problems with integrated solutions.

The wiring harness business remains Motherson's DNA, but it has evolved far beyond simple copper wires wrapped in plastic. Modern vehicles require different types of wiring systems: high-voltage cables for electric powertrains that can handle 800 volts without electromagnetic interference, ultra-thin data cables for infotainment systems that transmit terabytes of information, specialized heat-resistant wiring for engine compartments, and flexible flat cables for moving parts like seats and doors. Motherson produces all of these, often customizing solutions for specific vehicle architectures.

The vision systems division, built through the SMR acquisition and subsequent developments, represents Motherson's highest technology products. The humble rearview mirror has evolved into an intelligent device incorporating cameras, displays, ambient light sensors, and even biometric monitoring systems that can detect driver drowsiness. Motherson's latest electrochromic mirrors automatically dim based on following vehicle headlight intensity, while integrated cameras provide blind-spot monitoring and lane-departure warnings. They're developing mirrors that can display navigation information, vehicle diagnostics, and even video calls—transforming a safety device into an information hub.

The polymer products division showcases Motherson's materials science capabilities. They work with over 200 different polymer compounds, each engineered for specific applications. Soft-touch plastics for luxury car interiors require a precise balance of tactile feel and durability. Exterior plastics must withstand temperature variations from -40°C to +85°C while maintaining dimensional stability. Under-hood components need chemical resistance and heat tolerance. Motherson's materials laboratory in Germany develops custom compounds, sometimes spending years perfecting a single formulation for a specific customer requirement.

The complete modules business represents the pinnacle of Motherson's integration capabilities. A modern car dashboard isn't just a plastic shell—it's a complex assembly incorporating the instrument cluster, infotainment display, HVAC vents, airbag deployment systems, ambient lighting, touch controls, and dozens of sensors. Motherson delivers these as pre-assembled, pre-tested units that automakers can install in minutes rather than hours. This modular approach reduces assembly line complexity and improves quality by moving complex integration from the vehicle assembly line to specialized module facilities.

The technology story extends beyond traditional products. Motherson has quietly become a leader in automotive lightweighting—replacing metal components with advanced composites that maintain strength while reducing weight. Their carbon fiber reinforced plastics, developed for premium sports cars, reduce component weight by up to 60% compared to steel alternatives. As automakers chase efficiency gains, particularly in electric vehicles where every kilogram affects range, these lightweight solutions become increasingly valuable.

The company's innovation pipeline reveals where automotive technology is heading. They're developing "smart surfaces"—interior panels that look like wood or metal but incorporate hidden touch controls and displays that appear only when activated. Their bio-based plastics, derived from agricultural waste, address sustainability concerns while maintaining performance. Acoustic materials that actively cancel road noise are being integrated into door panels and floor systems.

The software dimension has become increasingly important. Modern vehicles contain over 100 million lines of code, and many Motherson products require embedded software. Their mirrors run facial recognition algorithms for driver identification. Lighting systems execute complex sequences synchronized with vehicle dynamics. Even seemingly simple components like window regulators incorporate software for anti-pinch detection and one-touch operation. Motherson employs over 2,000 software engineers, a number that would have seemed absurd for a components company a decade ago.

Testing and validation capabilities set Motherson apart from smaller competitors. Their test facilities can simulate decades of wear in weeks, subjecting components to extreme temperatures, humidity, vibration, and chemical exposure. The electromagnetic compatibility labs ensure that electronic components don't interfere with each other—critical as vehicles become rolling computers. Crash test facilities validate that interior components properly deploy airbags and don't create projectiles during impacts. This testing infrastructure, requiring hundreds of millions in investment, creates a significant barrier to entry.

The manufacturing technology is equally sophisticated. Motherson operates some of the world's largest injection molding machines, capable of producing entire dashboard structures in single shots. Their laser welding systems join plastics with precision measured in microns. Automated optical inspection systems check millions of solder joints daily. The level of automation varies by geography and product—highly automated in Germany for complex products, more manual in India for labor-intensive assemblies—optimizing cost and quality for each market.

Vertical integration provides strategic advantages. Motherson produces many of its own tools and dies, reducing dependence on external suppliers and protecting intellectual property. They compound their own plastics, ensuring consistent quality and supply security. They even manufacture some production equipment, customizing machines for specific products. This integration provides flexibility and speed—when a customer needs a design change, Motherson can modify tools, materials, and processes without coordinating multiple suppliers.

The quality philosophy permeates everything. Motherson doesn't just meet automotive quality standards—they often exceed them. Their defect rates, measured in parts per million, are among the industry's lowest. They've won quality awards from virtually every major automaker. But quality isn't just about statistics—it's about consistency. A Motherson product made in Mexico is indistinguishable from one made in Germany or China, a remarkable achievement given different workforces, suppliers, and environments.

Looking ahead, Motherson is positioning its product portfolio for the automotive industry's transformation. They're developing high-voltage distribution systems for electric vehicles, integrated sensor suites for autonomous driving, and modular interiors that can be reconfigured for shared mobility applications. The company that started with simple cables now produces some of the most sophisticated components in modern vehicles. As one customer remarked, "Motherson doesn't just supply parts—they supply solutions to problems we haven't even identified yet."

X. Culture, Strategy & Five-Year Plans

The scene at Motherson's global leadership summit in Dubai every five years resembles something between a United Nations assembly and a family reunion. In 2020, despite the pandemic, 500 leaders from 41 countries gathered—some physically, others virtually—for what the company calls its "Vision Setting Exercise." Unlike typical corporate planning sessions dominated by PowerPoints and consultants, this three-day event begins with an unusual ritual: each participant shares a personal story about trust, either given or received, that changed their life. Vivek Sehgal, now in his seventies, still goes first, setting a tone of vulnerability and authenticity that permeates the entire organization.

The Five-Year Plan culture, initiated in 2000, has become Motherson's defining management innovation. While most companies engage in annual planning cycles that encourage short-term thinking, Motherson's five-year horizons force a different perspective. "We don't ask what's possible next quarter," explains Laksh Vaaman Sehgal, Vivek's son and Vice Chairman. "We ask what's necessary five years hence and work backward."

The first Five-Year Plan (2000-2005) seemed almost naive in its ambition: achieve ₹1 billion revenue while maintaining 40% ROCE. The targets weren't picked from thin air—they represented what Motherson needed to become a credible global supplier. The 40% ROCE requirement, which many thought impossible to sustain during growth, forced a discipline that became cultural DNA. Every investment, every acquisition, every new facility had to clear this hurdle or it didn't happen.

What makes these plans remarkable isn't just their ambition but their success rate. The second plan targeted $1 billion revenue—achieved. The third aimed for $5 billion—surpassed. The fourth sought $18 billion—delayed by COVID but ultimately reached. Each plan included specific metrics beyond financials: customer diversification targets, geographic expansion goals, technology capabilities to acquire. The discipline of five-year thinking creates patience for long-term investments while maintaining urgency in execution.

The planning process itself is unique. Instead of top-down target setting, Motherson uses what they call "Collective Visioning." Each business unit develops its own five-year view, not in isolation but through intensive customer engagement. They ask key customers about their five-year plans, technology roadmaps, and sourcing strategies. These insights aggregate into a mosaic that reveals where the industry is heading and what capabilities Motherson needs to develop.

The 3CX10 philosophy—no customer, component, or country exceeding a specific percentage of revenue—emerged from the second Five-Year Plan and has become sacred. Initially targeting 15% maximum concentration (3CX15), the company has progressively reduced this to 10% as they've grown. This forced diversification might seem to limit growth opportunities, but it has created remarkable resilience. When any market, customer, or product line struggles, the impact on overall performance remains manageable.

The cultural values underpinning these plans go deeper than metrics. "Trust" isn't just a word at Motherson—it's measured, discussed, and reinforced constantly. Supplier payment terms are non-negotiable: 30 days maximum, often less. Customer commitments are tracked religiously: on-time delivery rates exceed 99.5% globally. Employee promises are sacred: no acquisition has resulted in involuntary layoffs during integration periods.

The "Proud to be Part of" philosophy sounds like corporate speak until you see it in action. In acquired companies, Motherson typically retains not just employees but traditions, celebrations, even company names when they carry local significance. The Peguform facility in Germany still celebrates its founding day sixty years later. PKC's Finnish operations maintain their traditional summer closure. These might seem like small gestures, but they create psychological ownership that transcends employment contracts.

The approach to failure is particularly instructive. When Motherson's first attempt to enter Russia failed in 2012—a joint venture collapsed amid regulatory challenges—the company didn't fire anyone or abandon the market. Instead, they treated it as learning, documenting lessons and maintaining relationships. Five years later, when PKC brought Russian operations, Motherson had institutional knowledge and local contacts that enabled rapid integration.

Compensation philosophy reinforces long-term thinking. Senior executives receive significant portions of compensation in stock options vesting over five years. Middle managers participate in "shadow equity" programs tied to five-year performance. Even factory workers receive bonuses based on multi-year customer satisfaction scores rather than quarterly production metrics. This alignment creates remarkable consistency—Motherson's senior leadership team has average tenures exceeding 15 years, unusual in the job-hopping automotive industry.

The innovation culture balances experimentation with discipline. Each business unit must allocate 3% of revenue to "future technologies"—projects with uncertain returns but strategic potential. These aren't random bets but systematic explorations guided by customer insights and technology roadmaps. Many fail, but successes like smart mirrors and integrated electronics have generated billions in revenue.

Communication systems reinforce cultural values. The company publishes a daily newsletter in 14 languages sharing stories from global operations. Monthly "Trust Talks" feature employees discussing ethical dilemmas and solutions. Annual "Innovation Days" showcase developments from every facility, with awards not for the biggest breakthroughs but for the most creative problem-solving. These mechanisms create shared identity across vast geographic and cultural distances.

The response to COVID-19 demonstrated cultural resilience. When the pandemic shut down automotive production globally, Motherson faced an existential crisis—90% revenue loss in some months. Instead of massive layoffs, the company implemented what they called "Shared Sacrifice." Leadership took 50% pay cuts, middle management 25%, workers faced temporary furloughs but retained health benefits. The company repurposed facilities to produce medical equipment, generating alternative revenue while serving community needs.

The most recent Five-Year Plan, Vision 2025, reveals evolved thinking. Revenue: 1,13,663 Cr Beyond financial targets, it emphasizes sustainability (carbon neutrality by 2040), digitalization (50% of products incorporating smart features), and diversification (25% non-automotive revenue). These aren't just goals but recognition that Motherson's next phase requires transformation, not just growth.

The succession planning embedded in the culture ensures continuity. Vivek Sehgal has gradually transitioned responsibilities to the next generation, not through dramatic announcements but through systematic capability building. His children work in the business but had to prove themselves in external companies first. Professional managers run most operations, with family providing strategic guidance rather than operational control.

Critics argue that Motherson's culture is too idealistic for the brutal automotive industry. The 40% ROCE target forces the company to pass on acquisitions that might provide strategic value. The diversification requirements prevent them from dominating specific segments. The trust-based approach seems naive in an industry famous for adversarial supplier relationships.

Yet the results speak for themselves. Employee turnover rates are half the industry average. Customer retention exceeds 95%. The company has never missed a Five-Year Plan target by more than 10%. In an industry where suppliers often struggle with 5% margins, Motherson consistently achieves double digits. The culture hasn't limited success—it has enabled it.

XI. Global Footprint & Current Scale

From the observation deck of Motherson's newest facility in Tuscaloosa, Alabama, you can watch a peculiar ballet unfold every six minutes. A truck arrives from the Mercedes-Benz plant three miles away, picks up a precisely sequenced set of pre-assembled cockpit modules, and departs. Another truck immediately takes its place. This choreography continues 24/7, 365 days a year, with Motherson shipping finished modules just hours before they're installed in vehicles. The facility doesn't even have a warehouse—everything produced is immediately shipped. This is modern automotive manufacturing: zero inventory, perfect synchronization, absolute reliability.

Motherson's global footprint reads like a strategic chess game played across continents. With 350 facilities across 41 countries, the company has achieved something remarkable: they're local everywhere while being global in scale. This resulted in expanding our footprint to 41 countries, diversifying our product portfolio, forging new partnerships and acquiring companies that have synergies with us. This isn't random expansion but careful positioning to serve customers wherever they manufacture while optimizing costs, capabilities, and risks.

The geographic strategy follows what Motherson calls the "Follow the Customer" principle. When Volkswagen opened a plant in Chattanooga, Tennessee, Motherson established facilities within 50 miles. When Mercedes expanded in India, Motherson was operational in Chennai before the first Mercedes rolled off the line. This proximity isn't just about logistics—it's about integration. Modern just-in-sequence manufacturing requires suppliers to be part of the assembly process, delivering components in the exact order vehicles move through production.

The scale achieved is staggering. Motherson employs over 180,000 people—more than many automotive manufacturers themselves. If Motherson were a city, it would be larger than Oxford, England. These employees speak 50 languages, hold passports from over 100 countries, and somehow collaborate seamlessly. The company processes over 50,000 tons of plastic annually, uses enough copper wire to circle Earth 20 times, and produces mirrors that, laid end to end, would stretch from London to Tokyo.

The customer portfolio reveals Motherson's true achievement in diversification. They supply 90% of global automotive manufacturers, from volume producers like Toyota and Volkswagen to ultra-luxury brands like Rolls-Royce and Bentley. 3CX15 meaning exposure to any country, component or customer should not be more than 15% of its total turnover. No single customer contributes more than 9% of revenue, a remarkable achievement given the automotive industry's consolidation. This wasn't luck but systematic effort—deliberately limiting exposure even to profitable customers to maintain independence.

The regional distribution tells different stories. Europe, contributing 35% of revenue, showcases technological leadership with advanced R&D centers and sophisticated manufacturing for premium vehicles. Asia, at 30%, balances high-volume production for emerging markets with cutting-edge facilities for Japanese quality standards. The Americas, at 25%, combines cost-efficient Mexican operations with high-tech U.S. facilities serving both traditional and electric vehicle manufacturers. The remaining 10% from Africa, Australia, and other markets might seem marginal but provides crucial diversification and growth potential.

China deserves special mention. With 25 facilities and 15,000 employees, Motherson has achieved what many Western suppliers struggle with: genuine localization. They don't just manufacture in China but develop products specifically for Chinese consumers—larger displays for rear passengers (where chauffeur-driving is common), air quality sensors for pollution-conscious buyers, and payment systems integrated into vehicles. Their joint ventures with Chinese companies provide market access while protecting intellectual property.

The India story has evolved remarkably. While headquarters remain in Noida, India now represents less than 15% of global revenue—not because Indian operations have shrunk but because international operations have exploded. Indian facilities have evolved from low-cost manufacturing to Centers of Excellence for frugal engineering, developing cost-effective solutions that find applications globally. The Chennai Technology Center, employing 2,000 engineers, develops products for worldwide deployment.

The operational complexity of managing this footprint would overwhelm most companies. On any given day, Motherson facilities produce 50,000 different part numbers, manage 10,000 active customer projects, coordinate 5,000 suppliers, and handle 1,000 engineering changes. They operate in dozens of currencies, navigate hundreds of regulatory regimes, and manage thousands of customer specifications. Yet delivery performance exceeds 99%, quality metrics lead the industry, and customer satisfaction scores consistently rank in the top quartile.

Technology enables this coordination. Motherson's digital backbone, developed over a decade, connects every facility in real-time. A design change in Germany immediately updates production systems in Mexico. Quality issues in China trigger alerts in India. Customer orders in Detroit automatically adjust production schedules in Thailand. This isn't just ERP implementation but a custom-built nervous system that provides real-time visibility and control across the global network.

The facility design philosophy balances standardization with localization. Core processes—quality systems, safety protocols, environmental standards—remain consistent globally. But implementation adapts to local contexts. German facilities emphasize automation and precision. Indian plants leverage skilled manual labor for complex assemblies. Mexican operations balance automation with flexibility for high-mix production. Each facility optimizes for its specific advantages while maintaining group standards.

Sustainability initiatives span the global footprint. Over 100 facilities have achieved zero-waste-to-landfill status. Solar installations across facilities generate 50 MW of renewable power. Water recycling systems, particularly in water-stressed regions like India and Mexico, achieve 90% reuse rates. These aren't just corporate responsibility initiatives but operational necessities—customers increasingly demand sustainable supply chains, and regulations worldwide tighten environmental standards.

The human dimension of this global scale remains remarkably personal. Despite employing 180,000 people, Motherson maintains practices that seem impossible at this size. Every employee receives a birthday greeting from senior management. Major festivals from every culture are celebrated at all facilities—Diwali in Detroit, Christmas in Chennai, Lunar New Year in Munich. The company maintains an emergency fund that has assisted thousands of employees facing personal crises, from medical emergencies to natural disasters.

Risk management across this footprint requires sophisticated approaches. Geographic diversification provides natural hedging—when one region struggles, others compensate. Multiple facilities can produce most products, providing backup for disruptions. Inventory strategies balance efficiency with resilience—critical components maintain strategic buffers while commodities operate just-in-time. The company survived the Fukushima tsunami, Thai floods, COVID lockdowns, and semiconductor shortages with minimal customer impact.

The Vision 2030 roadmap reveals ambitions that would transform Motherson into something unprecedented—a $50 billion revenue company maintaining the agility of a startup. Plans include 100 additional facilities, entry into 10 new countries, and employment exceeding 250,000. But growth isn't the only goal. The roadmap emphasizes capability building—artificial intelligence integration, sustainable materials development, and preparation for mobility paradigms that don't yet exist.

Looking at Motherson's global footprint today, it's hard to imagine this started with a single facility in Noida making simple cables. The company has achieved what few emerging market companies have managed—genuine global leadership without losing their entrepreneurial spirit. As one competitor admitted, "Motherson isn't just participating in the global automotive industry—they're shaping it."

XII. Playbook: The Motherson Way

In the boardroom of every Motherson acquisition target, the same question inevitably arises: "How do they make it work?" The numbers seem impossible—22 successful acquisitions without a single failure, 40% ROCE maintained through massive expansion, 95% customer retention across integrations. When pressed for the secret, Vivek Sehgal offers a cryptic smile and says, "There is no secret. We just do what we promise." But observing Motherson's playbook in action reveals a sophisticated methodology that combines strategic discipline, operational excellence, and cultural sensitivity in ways that business schools are only beginning to understand.

The three-fold growth strategy—organic, collaborative, and inorganic—sounds simple but operates with Swiss watch precision. Organic growth follows customer pull rather than market push. When BMW needs a new component, Motherson develops it, even if the initial volumes don't justify investment. This customer-led innovation has generated over 60% of revenue growth, with margins improving as volumes scale. The discipline is remarkable: Motherson has never developed a product without a confirmed customer order, avoiding the expensive mistakes that plague companies chasing hypothetical markets.

Collaborative growth through joint ventures reveals nuanced thinking about capability building. Unlike many companies that use JVs as market entry vehicles, Motherson structures partnerships for technology access and risk sharing. The Sumitomo partnership provided quality systems that would have taken decades to develop independently. Recent ventures with Chinese technology companies bring electric vehicle expertise while protecting core intellectual property. Each partnership has clear exit provisions—Motherson can buy out partners at pre-determined valuations, avoiding the acrimonious divorces that often plague joint ventures.

The inorganic growth playbook—the acquisition machine—operates with military precision. Target identification begins years before approach, with Motherson maintaining active files on over 200 potential acquisitions. They track financial performance, technology capabilities, customer relationships, and management quality. When opportunities arise—often during industry downturns—Motherson can move within weeks because homework is already complete.

The acquisition criteria are ruthlessly consistent. First, strategic fit—does the target bring technology, customers, or geography that Motherson lacks? Second, cultural compatibility—can the organization adapt to Motherson's trust-based approach? Third, financial discipline—can integration achieve 40% ROCE within three years? If any criterion fails, Motherson walks away, regardless of price attractiveness. They've passed on acquisitions that investment bankers insisted were "perfect fits" because cultural assessment revealed incompatibility.