MobiKwik: The Scrappy Survivor of India's Fintech Wars

I. Introduction & Episode Roadmap

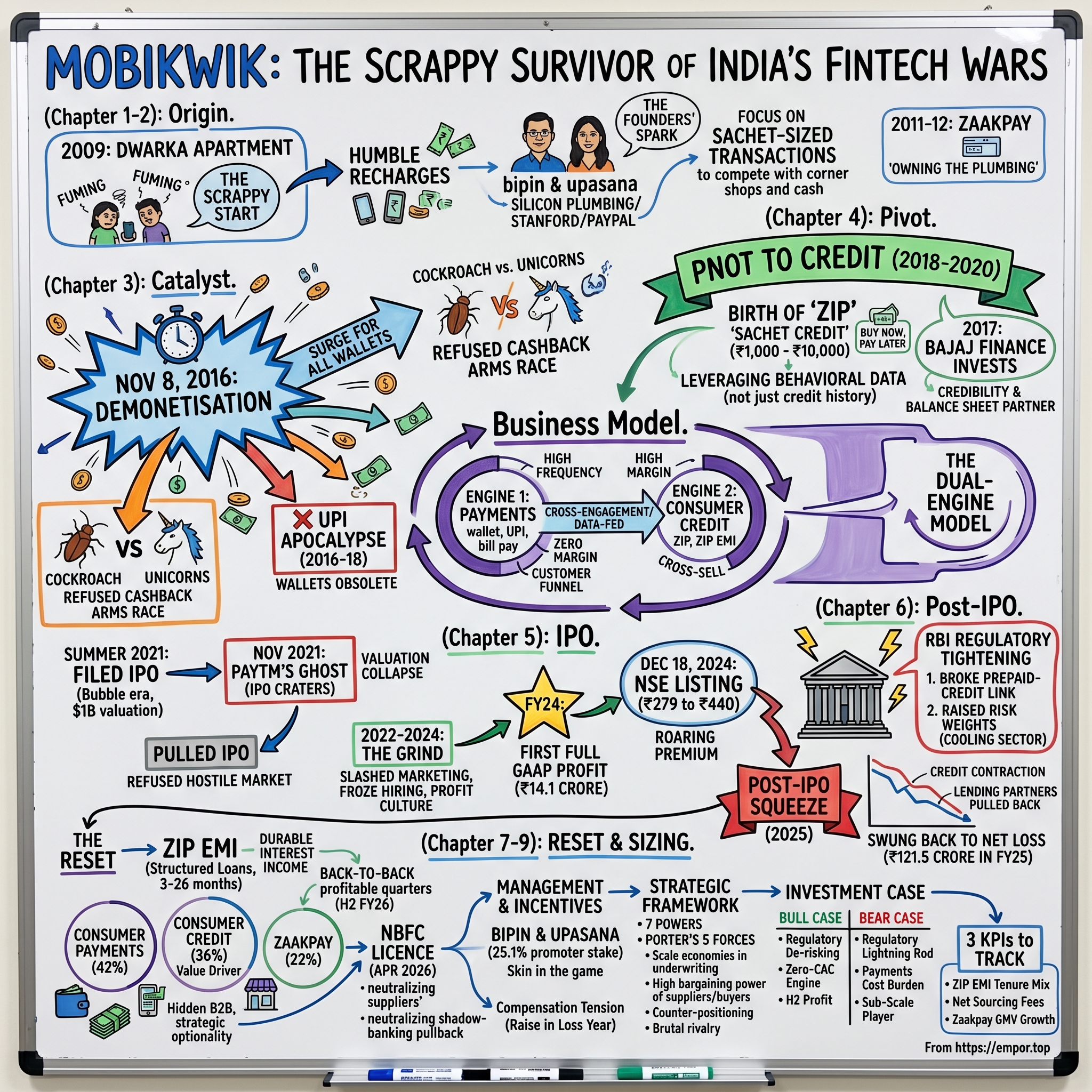

On the morning of December 18, 2024, a small crowd gathered at the National Stock Exchange in Mumbai to watch a fifteen-year-old startup finally cross a threshold it had been chasing, on and off, for the better part of a decade. When the bell rang for One MobiKwik Systems Limited, the screen did something nobody quite dared to predict. Against an issue price of ₹279, the stock opened at ₹440 — a 58% premium — and over the following sessions it kept climbing, brushing close to ₹700 before the euphoria cooled.[^3] For Bipin Preet Singh and Upasana Taku, the husband-and-wife duo who had started the company in a two-bedroom apartment, it was the validation of a survival strategy that had been mocked for years. The "cheap" wallet that refused to die had outlasted unicorns that burned ten times its capital.

And then, almost on cue, the story turned. By mid-2026, the same stock that had touched ₹700 was trading below ₹200 — a drawdown of more than 70% from its peak.4 The company that had finally tasted profit in FY24 swung back into the red. The regulator that had blessed India's fintech revolution had begun, methodically, to tighten the screws on exactly the business line that made MobiKwik money.

Here is the narrative paradox we are going to unpack. How does a company that raised only around $150 million across its entire private life — pocket change in a market where rivals raised billions — manage to outlast nearly all of them, reach GAAP profitability, list at a roaring premium, and then find itself caught in a regulatory storm that erased most of its market value? The answer is not a clean tale of triumph or failure. It is something more interesting: a study in capital efficiency as a competitive weapon, in the brutal economics of running a payments business that makes almost no money, and in what happens when a scrappy private company collides with the unglamorous realities of being public.

Our roadmap runs in four movements. First, the "cockroach" survival instinct of the founders — the discipline that let them refuse the cashback wars. Second, the external shocks that nearly killed and then remade the company: demonetisation, the rise of free UPI that vaporised the wallet's reason to exist, and the pivot to digital credit. Third, the post-IPO reality — squeezed by the Reserve Bank of India, dragged into a loss, and clawing back to profit in the back half of FY26. And fourth, the business playbook itself: how you run a dual-engine fintech when your primary customer-acquisition engine generates almost zero margin. Let's start where every good origin myth starts — with two people and an apartment.

II. The Founders' Spark & Early Digital Wallet Era

Picture Dwarka, on the western edge of New Delhi, in 2009. It is a neighbourhood of half-finished apartment blocks and dusty arterial roads, the kind of place where the metro has only just arrived. In a two-bedroom flat there, an IIT Delhi engineer named Bipin Preet Singh is fuming over something almost comically small: he cannot easily top up the prepaid balance on his mobile phone. To recharge, you found a corner shop, hoped they had your operator's vouchers, paid cash, scratched a card, and typed in a code. It was friction layered on friction, repeated hundreds of millions of times a day across India. Bipin, who had spent his career as a chip architect — first at Intel, then at NVIDIA, designing the silicon plumbing inside computers — looked at this everyday annoyance and saw an engineering problem begging for a solution.[^1]

That is the genesis of MobiKwik: not a grand vision of disrupting banking, but a man who wanted to recharge his phone without leaving his desk. The original product, launched in 2009, was about as humble as it gets — a web-and-SMS-based portal for mobile recharges. No app, because there was barely anything to put it on. This is the crucial context for understanding everything that follows: India in 2009 was a cash society with smartphone penetration in the low single digits. Most phones ran on 2G networks, mobile data was a luxury, and the banking system lived almost entirely offline, behind branch counters and stacks of paperwork. A digital wallet in that world was not competing with credit cards. It was competing with the corner shop and a fistful of rupee notes.

So MobiKwik did the only sensible thing: it went sachet-sized. Just as Indian consumer giants had learned to sell shampoo in one-rupee single-use sachets to reach customers who couldn't afford a full bottle, MobiKwik built itself around tiny, high-frequency utility payments — a ₹50 recharge here, an electricity bill there. Small transactions, enormous volume, and a product that solved a genuine pain point for people the formal financial system mostly ignored.

The second founder is where the story gains its emotional core. Upasana Taku had taken the more conventional glittering path — a master's degree from Stanford, then a coveted seat in Silicon Valley working on payments at PayPal, followed by a stint at HSBC.[^1] She had, by any measure, "made it" in the American sense. And she walked away from it to come back to India and build a payments company with the man she would marry. The decision says a great deal about both of them. This was not a pair of founders hedging their bets; it was a couple putting their professional reputations, their savings, and their shared future into the same fragile venture. That fusion of personal and professional stakes — the fact that a bad quarter was also a bad dinner-table conversation — is, more than any single product decision, the DNA of the company. It is why they would later prove almost pathologically unwilling to set fire to their own capital.

The early move that would echo for years came in 2011–2012, when the duo built Zaakpay, their own merchant-side payment gateway. This deserves a pause, because it is the kind of decision that looks unremarkable at the time and turns out to be foundational. Most startups in their position would have plugged into a third-party payment aggregator and gotten on with growth. MobiKwik instead built its own plumbing — the rails that let merchants accept digital payments — rather than renting someone else's. It was a capital-efficient, control-obsessed instinct: own the infrastructure, don't pay a middleman, and keep the option open to monetise the merchant side later. At the time it was a modest engineering project. A decade on, that early piece of in-house plumbing would become one of the company's most strategically interesting assets. But to get there, MobiKwik first had to survive a shock that turned the entire country's relationship with cash upside down.

III. The Great Catalysts: Demonetisation & The Wallet Wars

At 8:15 in the evening on November 8, 2016, Prime Minister Narendra Modi appeared on national television and detonated a bomb under India's cash economy. With a few minutes' notice, he declared that ₹500 and ₹1,000 notes — roughly 86% of all the currency circulating in the country — would cease to be legal tender at midnight. Overnight, the cash that lubricated nearly every transaction in India turned into worthless paper. Queues snaked around banks and ATMs for weeks. And in the middle of that chaos, mobile wallets stopped being a techie convenience and became, almost literally overnight, a survival utility.

For MobiKwik, the demand surge was the kind of growth no marketing budget could buy. Downloads exploded, transaction volumes spiked, and millions of Indians who had never typed a card number into a phone suddenly had a reason to learn. But — and this is the part that defines the chapter — the same windfall fell on every wallet in the country, and the wallet with the deepest pockets was not MobiKwik. It was Paytm.

Paytm, run by Vijay Shekhar Sharma, was bankrolled by two of the most aggressive capital allocators on earth: 軟銀 SoftBank, the vehicle of Masayoshi Son, and 螞蟻集團 Ant Group, the fintech arm of Jack Ma's Alibaba empire. With that backing, Paytm did what well-funded startups do — it flooded the zone. Full-page front-page newspaper advertisements (one famously featuring the Prime Minister's image, which drew political controversy), relentless cashback offers, subsidised everything. It was a textbook blitzscaling land-grab, and it worked to make Paytm the household name of Indian digital payments.

Here is where Bipin and Upasana made the decision that would define the company's character. They looked at the cashback arms race — where every rupee of "growth" was effectively a rupee handed to a customer who would vanish the moment the subsidy stopped — and they refused to play. They could not match SoftBank's chequebook even if they wanted to, but the deeper point is that they didn't try to fake it. Instead of carpet-bombing the market, they went granular: local merchant integrations, neighbourhood relationships, and offline "cash-loading" points where customers without easy bank access could put money into their wallets. They learned to operate on a fraction of the capital their rivals consumed, and in doing so earned a nickname that they came to wear with something like pride — the "cockroach" of Indian fintech. Not glamorous. Nearly impossible to kill.

The discipline mattered because what came next was not a competitor but an extinction event, and it came from the government's own innovation engine. Between 2016 and 2018, the Reserve Bank of India and the National Payments Corporation of India rolled out UPI — the Unified Payments Interface. To understand why this was apocalyptic for the wallet business, you have to understand what a wallet actually was. A digital wallet was a holding pen for money: you loaded rupees from your bank into the wallet (sometimes paying a small fee to do so), and then spent from the wallet. The business model leaned on that loading friction and on float. UPI obliterated the entire premise. It let any Indian send money instantly, directly from one bank account to another, using a phone — and it was free. No loading. No float. No wallet-to-wallet walls. Why would anyone keep money parked in a MobiKwik wallet when they could pay anyone, anywhere, straight from their bank for nothing?

The carnage was real. Freecharge, another wallet darling that Snapdeal had bought at a frothy valuation, collapsed in value and was fire-sold to Axis Bank. The standalone, fee-based wallet — the very product MobiKwik had been built on — was rendered fundamentally obsolete in the space of about two years. The cockroach had survived the cashback war only to face an asteroid. And so the founders did the only thing survivors do. They accepted that the original business was dying, and went looking for a new reason to exist.

IV. The Pivot to Credit: The Birth of ZIP & The Dual-Engine Model

The realisation that reshaped MobiKwik can be stated in a single uncomfortable sentence: payments are a wonderful way to get customers and a terrible way to make money. In India this is not a temporary condition; it is structural. The Merchant Discount Rate — the fee a merchant pays to accept a digital payment, the lifeblood of card networks in the West — has been compressed toward zero by regulation and competition. And on UPI, the government's explicit policy made person-to-merchant transactions free, meaning the rails that now carried the vast majority of India's digital payments generated essentially no revenue at all. MobiKwik had built a high-frequency engine that touched millions of lives daily and threw off almost nothing to the bottom line.

But buried inside that high-frequency engine was something genuinely valuable: data. Every recharge, every electricity bill, every wallet top-up was a breadcrumb of behaviour. Who pays on time. Who is stretched at month-end. Whose income is lumpy. For a country where the majority of adults had no formal credit history — no credit-card statement, no neat bureau score for a bank to underwrite against — that behavioural exhaust was a quiet goldmine. MobiKwik's most valuable asset, it turned out, was not its wallet balance. It was knowing how millions of underbanked Indians actually handled small sums of money.

So between roughly 2018 and 2020, the company built MobiKwik ZIP — sachet-sized credit. The idea mirrored the original recharge instinct: keep it small, keep it instant, keep it frictionless. ZIP offered tiny, instant credit lines, typically in the ₹1,000 to ₹10,000 range, extended right at the checkout. A young customer buying something online who didn't have a credit card — and most didn't — could tap ZIP and pay later. It was Buy Now, Pay Later, but tuned for the Indian mass market rather than aspirational shoppers buying sneakers in instalments. For millions, a ZIP line was the first formal credit they had ever been offered.

A crucial vote of confidence had arrived a little earlier, in 2017, when Bajaj Finance — one of India's most respected and conservatively run non-bank lenders — invested around ₹225 crore for a stake of roughly 13.4%.[^1] This was more than money. Bajaj Finance had spent decades mastering exactly the discipline MobiKwik lacked: underwriting consumer credit at scale without blowing up. Their willingness to put capital and credibility behind the company validated the credit thesis and gave MobiKwik a balance-sheet partner to help fund early lending. When a lender as careful as Bajaj decides your data is worth betting on, the market notices.

What emerged from all this was the architecture that still defines the company — the dual-engine model. Engine one is payments: wallet, UPI, bill pay. High frequency, low (often zero) margin, but a colossal, near-costless funnel that pulls in and re-engages users every single day. Engine two is credit: ZIP and its descendants, high-margin consumer lending cross-sold to that captive, already-acquired user base. The elegance is in the hand-off. The payments engine is a customer-acquisition machine that runs at almost no marginal cost, and the credit engine is where you finally turn all that attention into money. Payments are the loss-leading front door; credit is the room where the rent gets paid.

Not every move in this period aged well, and it is worth being honest about one that didn't. In October 2018, MobiKwik acquired Clearfunds, a small robo-advisory mutual-fund platform, and committed to a roughly $15 million investment to build out a wealth-management arm branded "MobiKwik Money."[^10] The logic was defensive and of its era — Paytm was loudly building Paytm Money, and the fear of being left out of the "super-app" wealth land-grab was real. But the bet never paid off the way the press release implied. Where Paytm Money scaled, MobiKwik's wealth effort stayed a minor footnote, and the broader category was steamrolled by purpose-built giants like Groww and Zerodha that out-executed everyone on focus and brokerage economics. In hindsight it was a reactive play that cost the company scarce capital and, more importantly, scarce management attention on a front it was never going to win. The lesson — that MobiKwik's edge lay in its own funnel, not in chasing competitors into adjacent arenas — would have to be re-learned the hard way. With the dual-engine model in place, the company turned toward the one milestone that had eluded it for years: the public markets.

V. The IPO Drama: Paytm's Ghost, The Grind, and the 2024 Listing

By the summer of 2021, the entire technology world was levitating on a cushion of free money, and India's startup scene was no exception. In July 2021, MobiKwik filed its first Draft Red Herring Prospectus, reaching for a valuation around $1 billion and a raise of roughly ₹1,900 crore.[^11] It was the height of the bubble, the moment when unprofitable growth stories could command unicorn prices simply by promising scale. MobiKwik, freshly leaning into credit and riding the post-pandemic digital wave, lined up to join the party.

Then the party ended, violently, in the most public way imaginable. In November 2021, Paytm staged what was at the time the largest IPO in Indian history — and the stock immediately cratered, shedding a quarter of its value on the very first day and continuing to bleed for months afterward. For investors, Paytm became the cautionary tale that poisoned the well for every unprofitable Indian fintech behind it. The message from the public market was blunt: we no longer pay unicorn multiples for losses and a story. MobiKwik's institutional order book, contingent on exactly that appetite, evaporated. And here Bipin and Upasana made another of those quietly defining decisions. Rather than force a listing into a hostile market and risk their own Paytm-style debacle, they pulled the IPO. Painful, embarrassing in the moment, and absolutely correct.

What followed was the least glamorous and most important chapter in the company's history: the grind. From roughly 2022 through 2024, with no IPO windfall coming and the funding environment frozen, the founders did what cockroaches do. They slashed marketing spend, froze hiring, and turned the engineering culture inward — onto the unglamorous work of making the credit underwriting actually profitable. Every basis point of delinquency mattered. Every rupee of customer acquisition had to justify itself. It was a period of forced discipline, and it produced the number that changed the whole trajectory.

In FY24, MobiKwik posted its first full year of GAAP profitability — a net profit of ₹14.1 crore on revenue of ₹875 crore.[^7] In the context of Indian fintech, where giants were still reporting losses measured in thousands of crores, a small but real profit was almost subversive. It was not a large number. But it was the number, because it transformed the equity story from "trust us, scale will eventually mean profit" into "we already make money, now fund our growth." Profit changed the conversation entirely.

And so MobiKwik came back to the market in 2024 a humbler, smaller, and far more credible company. The refiled IPO was a fresh issue of just ₹572 crore — a fraction of the 2021 ambition — pricing the company at a conservative valuation around $250 million.[^2] Read that against the roughly $1 billion the founders had chased three years earlier and you see a markdown of about 70% from the private-market peak. Most founders' egos cannot survive that kind of haircut. Bipin and Upasana priced for a clean listing rather than for vanity, and the market rewarded the restraint. When the stock listed on December 18, 2024, it closed its first day at a 48% premium and kept running in the weeks after, briefly carrying a market value near ₹4,000 crore — roughly $500 million.[^3] The company that had walked away from the bubble had, in the end, listed twice the valuation it humbly asked for. The celebration, however, would prove almost cruelly brief.

VI. Post-IPO Turbulence: The Regulatory Squeeze & The Reset

If you want a lesson in how quickly a victory lap can turn into a sprint for survival, study what happened to MobiKwik in the months after that triumphant listing. The champagne had barely gone flat before the Reserve Bank of India turned the full weight of its attention onto the exact business line that made MobiKwik's profitability possible: unsecured, small-ticket consumer credit. The central bank had grown deeply uneasy about the explosion of sachet-sized digital loans — millions of tiny, instant credit lines extended to young, thin-file borrowers, the systemic equivalent of a thousand small fires that could, in aggregate, become a blaze. And the RBI, institutionally, would always rather smother a fire early than fight it late.

The squeeze came in two distinct moves, and it helps to separate them. The first was structural plumbing. Through a sequence of rulings on prepaid instruments and a tightening set of Digital Lending Guidelines, the regulator made it impermissible to load a wallet directly from a credit line — effectively breaking the neat trick of pouring borrowed money into the spending instrument. ZIP had to be re-plumbed from a "load your wallet with credit" product into a checkout-only mechanism, where the credit is applied at the point of a specific purchase rather than handed to the user as general-purpose spending power. Cleaner from a regulatory standpoint, but a meaningful drag on usage and convenience.

The second move was about capital, and it was blunter. In November 2023, the RBI raised the risk weights on unsecured consumer loans from 100% to 125%.[^12] In plain terms: a risk weight determines how much expensive capital a lender must hold against a given loan. Raise the weight, and every rupee of unsecured lending suddenly consumes more capital and earns a lower return. The point of the move was deliberately to make this kind of lending less attractive and to cool the sector down. It worked. The banks and non-bank lenders that actually funded MobiKwik's ZIP book — partners such as IDFC First Bank and the platform Lendbox — saw their own cost of capital climb, and they responded exactly as you would expect: by tightening limits and pulling back on lending channelled through fintech platforms. MobiKwik did not control the spigot. Its funding partners did, and the regulator had just made them nervous.

The financial toll showed up fast and it was ugly. The high-margin credit segment — the engine that produced essentially all of the company's profit — contracted by about 28%, falling from roughly ₹557.9 crore in FY24 to ₹402.8 crore in FY25.2 As credit shrank, the revenue mix tilted back toward the low-margin payments business, where gross transaction value surged but contribution to actual profit stayed thin. Payments revenue jumped to around ₹767.4 crore in FY25, which sounds like growth until you remember those rupees barely carry margin.2 The arithmetic was unforgiving: a more valuable engine shrinking while a less valuable one grew. MobiKwik swung from its hard-won ₹14.1 crore profit in FY24 straight back to a net loss of ₹121.5 crore in FY25.2 The market, which had been pricing the company as a freshly profitable grower, repriced it as a regulated lender with vanishing margins, and the stock duly collapsed below ₹200.4

What kept this from becoming an obituary was the founders' response, which was characteristically pragmatic. If the regulator hated tiny, instant, general-purpose BNPL, then MobiKwik would shift the credit book toward something the regulator viewed more kindly: longer-dated, instalment-based lending. The company pivoted its ZIP credit away from sachet BNPL and toward ZIP EMI — structured loans running anywhere from 3 to 26 months, the kind of disclosed, tenured credit that fits comfortably inside the new guidelines and produces more durable interest income per customer. The reset began to show in the FY26 numbers. Annual revenue stabilised at roughly ₹1,119.2 crore, and the net loss was cut nearly in half, to about ₹62.1 crore.2 Most importantly, the back half of the year turned positive: the company reported a net profit of ₹4.04 crore in the third quarter and ₹4.38 crore in the fourth quarter of FY26.2 Two profitable quarters do not erase a loss-making year, but they signalled that the bottom had been found and that the new credit mix could carry the company back into the black. To understand whether that recovery is durable, we have to look under the hood at how the business actually breaks down.

VII. Segment Proportionality & Sizing the Optionality

Strip away the drama and MobiKwik is really three businesses bolted onto one user base, and the only way to understand the company is to weigh each engine honestly — not by the revenue it reports, but by the value it actually creates. Revenue, as the FY25 whiplash demonstrated, can be deeply misleading when one rupee of credit income is worth several rupees of payments income.

Start with consumer credit, the financial-services segment, which contributed roughly 36% of FY26 revenue. Despite the regulatory mauling it took, this remains the value driver — the beating heart of the unit economics and, bluntly, the only reason MobiKwik can post a net profit at all. The payments funnel can grow to the moon, but it is the credit engine that converts attention into earnings. When investors ask whether MobiKwik is a "real" business, this is the segment they are really asking about, and its health is the single best proxy for whether the equity story works.

Next, consumer payments — the wallet, UPI, and bill-pay machine — which made up about 42% of FY26 revenue and is the high-volume funnel that gives the company its reach. This is where the headline user numbers live: a registered base of 186.6 million users, re-engaged daily by products like Pocket UPI, a feature that lets users pay via UPI directly from the app and which grew around 170% year-on-year in the fourth quarter of FY26.2 But here the warning from earlier sections must be kept firmly in mind: this is the biggest revenue line and one of the smallest value lines. Payment-gateway and processing costs eat most of the economics, so for all its scale, the segment's contribution to net value remains thin. It is the front door, not the cash register.

The third engine is the one most observers miss, and it is the most strategically interesting: Zaakpay, the merchant-facing payment gateway the founders quietly built back in 2011–2012. In FY26 it contributed roughly 22% of revenue, having generated around ₹297 crore in FY25 — a hidden B2B business growing inside the consumer story.2 What makes it matter now is regulatory: securing the full Payment Aggregator licence from the RBI — a process that ran through the 2023–2026 window and which the regulator had approved in principle for Zaakpay back in October 2023 — lets MobiKwik scale a genuine merchant-acquiring business rather than operating on sufferance.3

Why does a merchant gateway matter to a consumer-credit company? Because it closes the loop. Zaakpay is targeting roughly a 10x expansion in gross merchandise value by FY28, and the strategic prize is not gateway fees in isolation.2 It is that owning the checkout on thousands of merchant websites lets MobiKwik embed its own ZIP credit directly at the point of sale — bypassing expensive third-party gateways and capturing more of the credit margin for itself. The plumbing the founders built fourteen years ago to save a middleman's fee turns out to be the rails on which the highest-margin product can ride. That is the optionality hiding in plain sight. And it is the people steering all of this whom we should now meet on their own terms.

VIII. Current Management, Ownership & Incentives

There is a clarifying simplicity to MobiKwik's leadership question. You do not need an org chart or a history of revolving-door executives, because the company has always been, and remains, the project of two people. We will set aside the historical and non-founder management entirely, because the ultimate decision-makers have never changed: Bipin Preet Singh and Upasana Taku. The same pair from the Dwarka apartment still run the company they listed on the NSE.

What gives that continuity weight is skin in the game, and theirs is substantial. After the IPO, Bipin Preet Singh — Managing Director and CEO — held roughly 14.5% of the company's equity, while Upasana Taku — Chairperson, Whole-Time Director, and CFO — held about 10.1%.[^2] Together the promoter stake settled around 25.1%, a level high enough to ensure their personal fortunes rise and fall with the public shareholders'.[^2] In a market littered with founders who diluted themselves to near-irrelevance chasing growth, a quarter of the company still in the founders' hands at listing is a meaningful signal of both conviction and capital discipline. They did not sell the company out from under themselves to fund the burn, because they never burned that way.

Compensation is where the public-market transition gets uncomfortable, and it is worth being candid. As the company went public, both founders' pay packages were structured at ₹4 crore per annum each — split into roughly ₹2.5 crore fixed and ₹1.5 crore of performance-linked variable pay, a reasonable design that ties a chunk of the reward to results. For FY25, however, their remuneration was raised by about 40%, to roughly ₹6.2 crore each, working out to a pay ratio of about 21.8 times the median employee salary. Here lies a genuine governance tension: FY25 was the year the company swung to a ₹121.5 crore loss, and a 40% raise into a loss-making year is exactly the kind of thing that draws shareholder scrutiny and proxy-adviser frowns. The structure is designed to align founders with performance metrics, but the optics of rising founder pay against falling profits is a fair flag for any long-term owner to keep watching.

The most telling ownership event came in April 2026, and it cuts both ways. Peak XV Partners — the firm formerly known as Sequoia Capital India, and a MobiKwik backer for more than a decade — fully exited its remaining 7.7% stake for ₹130 crore in a secondary block deal, at an average price around ₹214 per share.[^4]1 Pointedly, the exit came right after the RBI granted MobiKwik its own NBFC licence, a milestone we will return to.[^6] How you read this depends on your temperament. The bearish reading: a sophisticated, decade-long insider chose to ring the register and walk away entirely, even after the licence that was supposed to de-risk the business. The bullish reading: a venture fund nearing the end of its fund life returning capital to its limited partners is doing exactly what venture funds do, and the clean removal of a long-standing overhang — a known seller finally gone — can be healthy for the stock. Both readings are legitimate, and a careful investor holds them simultaneously. What is not in doubt is that the founders, unlike their earliest backer, are still all-in. With the people and incentives mapped, we can step back and ask the strategic question: what, if anything, actually protects this business?

IX. Playbook & Strategic Frameworks

To pressure-test MobiKwik's durability rather than its story, it helps to run the business through two well-worn lenses — Hamilton Helmer's 7 Powers, which asks what sustainable advantage a company truly possesses, and Porter's Five Forces, which asks how brutal its industry really is. Used together they cut through the optimism of an IPO deck and the pessimism of a drawdown.

Hamilton Helmer's 7 Powers Applied to MobiKwik

The clearest Power MobiKwik holds is a Cornered Resource, and it is the zero-cost acquisition funnel we have been circling all episode. The company's 186.6 million registered users and 4.79 million merchants are not just a vanity metric; they are a captive distribution asset that competitors cannot easily replicate.2 Consider the contrast that makes this real: a standalone digital lender in India must spend somewhere between ₹1,500 and ₹3,000 in marketing to acquire a single borrower. MobiKwik's incremental cost to offer credit to a user already paying their electricity bill in the app is close to nothing. When your customer acquisition cost for the high-margin product rounds to zero because the low-margin product already paid for it, you have a structural edge that money alone cannot buy.

The second Power is Counter-Positioning, and it explains why MobiKwik exists at all. Traditional banks are built, almost philosophically, to underwrite prime, well-documented, relatively affluent customers — the credit-card applicant with salary slips and a bureau history. Their entire cost structure and risk appetite is wired for that customer, and they cannot easily reach down-market without cannibalising their own model and economics. MobiKwik counter-positions by serving precisely the customer the banks structurally can't: the young, thin-file, underbanked Indian who would never clear a credit-card desk but can be offered an instant, sachet-sized ZIP limit underwritten on behavioural data. The incumbent sees the segment as too small and too risky to bother re-engineering for — which is exactly the gap a counter-positioned challenger lives in.

The third Power, Scale Economies in underwriting, is more aspirational but real in direction. Every repayment and default feeds the credit models more data, and in lending, data compounds: more repayment history means sharper risk pricing, lower delinquency, and better selection than a smaller, newer competitor can manage. The more MobiKwik lends well, the better it should get at lending — provided it lends well, which the FY25 stumble reminds us is not guaranteed.

The fourth, Network Effects, is where we should be honest about the limits. The dominant UPI network effects belong to PhonePe and Google Pay, not MobiKwik. What MobiKwik has is a narrower, niche network effect: users keep the app because specific merchants, utility billers, and local QR integrations live there, and those merchants stay because the users do. It is a real but bounded moat — a defensible neighbourhood, not the whole city.

Porter's Five Forces Analysis of the Indian Fintech Industry

Run the industry through Porter and the picture is bracing. The threat of new entrants is high, and not from scrappy startups but from titans: 信實 Reliance's Jio Financial Services and Tata's Tata Neu are wading into fintech with balance sheets and customer bases that dwarf MobiKwik's, escalating the fight for consumer attention. The bargaining power of suppliers is high — and this is the force that drew blood in FY25. Because MobiKwik historically relied on third-party banks and NBFCs to fund its lending book, those capital suppliers held real leverage, and when the RBI raised risk weights, they used it, tightening the taps. The single most important strategic event of 2026 is precisely MobiKwik's move to neutralise this force: securing its own NBFC licence in April 2026, which lets it lend directly from its own book and bypass the supplier chokehold that nearly strangled the credit engine.[^6]

The bargaining power of buyers is high on the payments side, where switching costs are effectively zero — a user can hop between Google Pay, PhonePe, and MobiKwik in seconds, and loyalty is thin. It is only moderate on the credit side, where a borrower has some incentive to preserve a hard-won ZIP limit and relationship. The threat of substitutes is high: UPI Lite, traditional credit cards making a downmarket push, and instant overdraft products from banks all crowd the space. And the competitive rivalry is simply brutal — PhonePe commands roughly 48% of UPI volume, Google Pay around 38%, a wounded-but-massive Paytm fights on, and credit-focused challengers like Slice and KreditBee press on the lending flank. This is not a comfortable industry. It is a knife fight in a growing room, which is exactly why the bull and bear cases on MobiKwik are both so easy to argue.

X. The Investment Case: Bull vs. Bear

Every contested stock is really an argument between two coherent stories told over the same set of facts, and MobiKwik below ₹200 is one of the more evenly matched arguments in Indian fintech. Let's give each side its strongest case rather than a straw man.

The Bull Case

The bull starts with regulatory de-risking, and it is a genuinely strong opening. The thesis is that the worst is behind the company because MobiKwik has now collected the two licences that change its structural position: its own NBFC licence, granted in April 2026, and the full Payment Aggregator licence for Zaakpay.[^6]3 The NBFC licence is the more important of the two. It means MobiKwik can lend from its own balance sheet rather than at the mercy of skittish third-party partners — capturing the full net interest margin instead of a sliver of sourcing fees, and insulating itself from exactly the "shadow-banking" partner-pullback that detonated FY25. The bull argues the company has effectively bought its way out of the supplier-power problem Porter flagged.

The second pillar is the zero-CAC engine we have examined at length — a 186.6 million-user, 4.79 million-merchant funnel into which credit and insurance can be cross-sold for years without meaningful incremental marketing spend.2 If even a modestly larger fraction of that base takes a ZIP EMI loan from MobiKwik's own book, the operating leverage is considerable. And the third pillar is proof, not promise: the back-to-back profitable quarters in H2 FY26 demonstrate that the pivot from sachet BNPL to tenured ZIP EMI actually works in practice, with losses narrowing sharply across the year.2 The bull's summary: a cheaper, de-risked, structurally profitable version of the company is emerging, and the market is still pricing the trauma of FY25.

The Bear Case

The bear's first and most powerful point is that MobiKwik is a regulatory lightning rod by its very nature. Unsecured digital consumer credit is the single most politically and prudentially sensitive corner of Indian finance, and the RBI has shown — twice now — that it will reach in and change the rules with little warning. A licence does not immunise the company from the next policy shift; it arguably makes MobiKwik more visible and more directly accountable to the regulator. Business predictability in this segment is structurally low, and that deserves a permanently higher discount rate, not a victory lap.

The second bear point is the payments cost burden, which is not a one-time problem but a permanent gravitational drag. As long as the largest revenue line is a near-zero-margin payments business whose processing costs keep climbing, the company's return on equity is hostage to the credit engine scaling fast enough to carry the dead weight. If credit volumes stall — because the regulator tightens again, or because the lending sours — the payments business doesn't cushion the fall; it deepens it. The third point is simply valuation and skepticism: the stock trades well below its listing price for a reason, and the market remains unconvinced that a sub-scale player can out-grow far larger, far better-capitalised rivals in the brutal arena Porter described. The bear's summary: a small, perennially regulated lender wrapped around a structurally unprofitable payments business is not obviously a bargain just because it fell 70%.

The Three KPIs to Track

Cut through both narratives and there are really only three things a long-term owner needs to watch. The first is credit disbursal volume and the ZIP EMI tenure mix — because the size and shape of the high-margin credit book is the master variable for the entire profit story; watch whether disbursals are growing and whether they are skewing toward the longer, regulator-friendly EMI tenures. The second is net sourcing fees and net interest margin — now that the NBFC licence lets MobiKwik lend on its own book, NIM becomes the single cleanest gauge of whether owning the lending actually translates into the richer economics the bull case promises. The third is Zaakpay's gateway GMV growth — the execution proof-point for the 10x merchant expansion that would let the company embed its own credit at checkout and finally fuse its three engines into one.2 Three numbers. Track those, and you are tracking the thesis.

XI. Outro & Historical Lessons

The enduring lesson of the MobiKwik story is almost subversively old-fashioned: capital efficiency is itself a durable competitive advantage. In a market where the loudest competitors raised and incinerated billions of dollars to rent market share with cashbacks, two engineers from a Dwarka apartment chose to survive on a fraction of the money — and that choice, more than any product or pivot, is why they were standing on the NSE floor in December 2024 while flashier rivals had been fire-sold, folded, or humbled. The cockroach strategy was never glamorous. It was simply, repeatedly, the thing that kept them alive long enough to reach the next chapter.

But the second lesson is the harder one, and it is still being written. Surviving as a private unicorn and thriving as a public company are different disciplines entirely. The private game rewarded scrappiness and the refusal to burn. The public game demands something the founders are still learning to navigate: living quarter to quarter at the mercy of a regulator that can rewrite your economics overnight, and a market that prices your stock on the shifting tides of macro and policy rather than the quality of your survival instinct. MobiKwik proved it could outlast the competition. Whether it can master the public-market version of the game — turning two profitable quarters into a durable franchise under a regulator's permanent gaze — is the question that will define its next decade.

References

-

Peak XV Partners fully exits Mobikwik in block deal worth ₹130 crore — Business Standard, 2026-04-28 ↩

-

MobiKwik swings back to H2 profitability in FY26 as losses narrow to Rs 62 Crore — Business Standard, 2026-05-28 ↩↩↩↩↩↩↩↩↩↩↩↩

-

RBI approves MobiKwik's Zaakpay for Payment Aggregator License — Moneycontrol, 2023-10-23 ↩↩

-

One MobiKwik Systems Limited — Market Watch & Performance History, National Stock Exchange of India ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube