Mindspace REIT: Building India's Commercial Real Estate Empire

I. Introduction & Opening Context

Picture this: It's 2019, and the Mumbai skyline is dotted with gleaming glass towers. Inside one of these towers—a sprawling business park in Malad—sits Ramesh Nair, the CEO of Mindspace Business Parks, staring at a document that will transform a family-owned real estate empire into India's second publicly-traded REIT. The IPO prospectus on his desk represents not just ₹4,500 crores in capital raising, but the culmination of a 63-year journey from a post-partition real estate venture to one of India's most sophisticated commercial property platforms.

The timing couldn't be more precarious. Global markets are jittery, Indian real estate is still recovering from demonetization and RERA shocks, and whispers of a mysterious virus in China are beginning to circulate. Yet here stands Mindspace, about to test whether Indian capital markets are ready for the REIT revolution—a structure that had flopped spectacularly just years earlier when attempted by others.

Today, Mindspace REIT commands a market capitalization of ₹25,582 crores, generates annual revenue of ₹2,737 crores, and houses some of the world's most prestigious corporations across 38.1 million square feet of prime commercial real estate. The portfolio spans Mumbai's business districts, Hyderabad's Cyberabad, Pune's IT corridors, and Chennai's emerging commercial hubs. But this isn't just another real estate story—it's a masterclass in timing, transformation, and the art of building institutional-grade assets from entrepreneurial roots.

The central question we'll explore: How did a Mumbai real estate family, starting from the chaos of post-independence India, build one of the country's largest and most sophisticated commercial REITs? And more importantly, what does Mindspace's journey tell us about the evolution of Indian commercial real estate, the maturation of capital markets, and the future of workspace in a post-pandemic world?

This is a story of three distinct eras: the foundational years of K Raheja Corp navigating Mumbai's cutthroat real estate market, the visionary bet on IT parks just as India's technology boom was taking off, and the financial engineering that transformed a family business into an institutional-grade investment vehicle. Along the way, we'll decode the REIT structure that makes Mindspace unique, analyze its competitive moat in India's rapidly evolving commercial landscape, and examine whether this model represents the future of real estate investment in emerging markets.

What makes Mindspace particularly fascinating is how it straddles two worlds—maintaining the entrepreneurial DNA and local market knowledge of a family-run business while operating with the transparency, governance, and distribution requirements of a public REIT. It's a balancing act that few have mastered, and one that offers profound lessons for both real estate developers contemplating public markets and investors seeking to understand India's commercial property dynamics.

II. The K Raheja Foundation Story (1956-1990s)

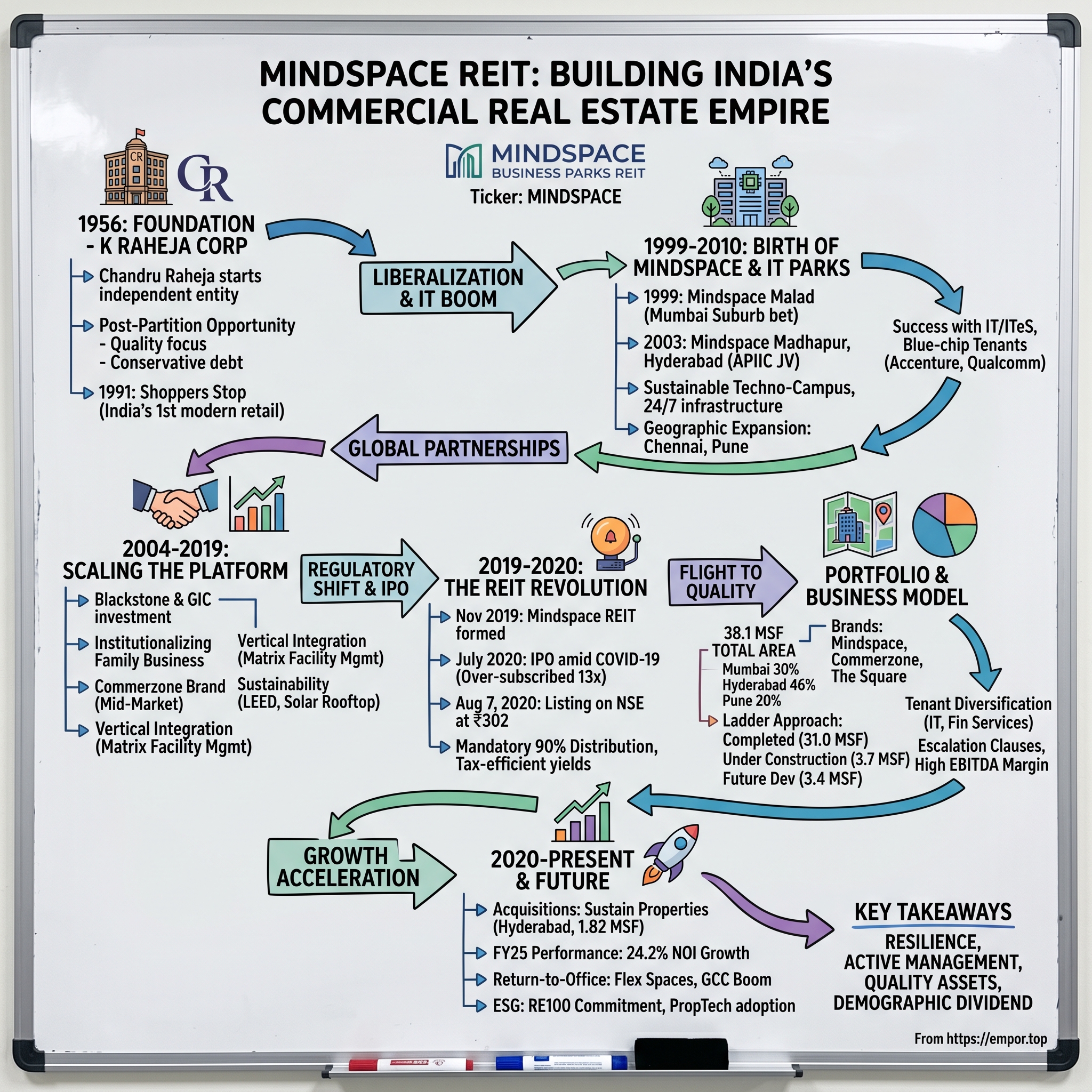

The year was 1956. India had been independent for less than a decade, Nehru's socialist vision was reshaping the economy, and Mumbai—still called Bombay—was transforming from a colonial port city into India's commercial capital. In this environment of post-partition opportunity and chaos, Chandru Raheja made a decision that would echo through generations: he would split from his brothers and establish K Raheja Corp as an independent entity.

The Raheja family had arrived in Mumbai like thousands of other Sindhi families displaced by partition, carrying little more than entrepreneurial spirit and an intimate understanding of trade. While his brothers pursued their own ventures, Chandru saw opportunity in Mumbai's desperate need for commercial and residential space. The city was bursting at its seams—textile mills dominated the landscape, but white-collar employment was growing, and housing was scarce.

K Raheja Corp's early years were defined by a simple philosophy that would later become its competitive advantage: build quality, build relationships, and build for the long term. In an era when most Mumbai developers were content with quick profits from substandard construction, Chandru insisted on over-engineering. "My father would say, 'Buildings should outlive their builders,'" his son Neel Raheja would later recall in a rare interview. This wasn't just sentiment—it was strategy. Better construction meant premium pricing, premium pricing meant better locations, and better locations meant institutional tenants who paid on time.

The 1960s and 70s saw K Raheja Corp methodically expand across Mumbai, but always with discipline. While competitors leveraged aggressively during boom cycles, the Rahejas maintained conservative debt levels—a practice that would prove prescient during India's numerous real estate crashes. They developed a reputation for completing projects on time, a rarity in Mumbai's real estate market where delays were so common that "under construction" became a permanent state for many projects.

But the real masterstroke came in 1991, just as India was liberalizing its economy. While most real estate developers were focused on residential projects or traditional office buildings, K Raheja Corp launched something unprecedented: Shoppers Stop in Andheri, India's first multi-brand retail showroom. This wasn't just a store—it was a glimpse into the future of Indian consumption. Air-conditioned, with multiple brands under one roof, and targeting the emerging middle class, Shoppers Stop represented a bet that India's socialist austerity was ending and consumerism was about to explode.

The success of Shoppers Stop revealed something crucial about K Raheja Corp's DNA: they weren't just builders, they were students of social transformation. They understood that India's economic liberalization wasn't just about policy changes—it was about fundamental shifts in how Indians lived, worked, and spent. This insight would prove invaluable as the 1990s progressed and a new phenomenon began reshaping India's urban landscape: the IT boom.

By the mid-1990s, K Raheja Corp had evolved from a partition-era startup into one of Mumbai's most respected developers. They owned prime land banks, had relationships with major corporations, and perhaps most importantly, had second-generation family members who had been educated abroad and returned with global perspectives. Neel Raheja and his siblings weren't content to simply inherit a traditional real estate business—they wanted to build something transformational.

The family's approach to business was distinctly Indian yet surprisingly modern. Decision-making remained centralized within the family, but execution was increasingly professionalized. They hired from India's best business schools, partnered with international architects, and most unusually for a family business, were willing to cede control when it meant accessing capital or expertise. This combination of entrepreneurial aggression and institutional discipline would prove crucial as they prepared for their biggest bet yet.

As the 1990s drew to a close, signs were everywhere that India was on the cusp of something big. Y2K had created massive demand for Indian software engineers, telecom liberalization was connecting India to the world, and multinational corporations were setting up back offices in Indian cities. But most real estate developers were still thinking in terms of traditional office buildings—standalone structures in city centers, designed for banks and trading companies.

The Rahejas saw something different. They envisioned integrated business parks—entire ecosystems where thousands of knowledge workers could live their professional lives. Not just offices, but campuses with food courts, recreation facilities, parking, and crucially, the kind of infrastructure that could support 24/7 operations for companies serving global clients. It was an audacious vision that would require massive capital, new construction techniques, and most challengingly, convincing both corporations and government that this was the future of Indian commercial real estate.

III. The Birth of Mindspace: Creating India's IT Parks (1999-2010)

The conference room at K Raheja Corp's Mumbai headquarters was tense in early 1999. Neel Raheja was presenting a radical proposition to the family board: invest hundreds of crores to build a massive business park in Malad, a Mumbai suburb better known for film studios than corporate offices. The concept seemed almost absurd—why would companies leave established business districts for the suburbs? The answer lay in a spreadsheet showing the IT services contracts Indian companies were winning from global corporations, and more importantly, what these companies needed that traditional office buildings couldn't provide.

"The future of Indian business isn't in South Mumbai's art deco buildings," Neel argued. "It's in purpose-built campuses that can house thousands of engineers working in shifts, with backup power that never fails, internet connectivity that rivals Silicon Valley, and enough parking for a workforce that's buying cars for the first time." The family patriarch listened quietly, then asked the question that mattered: "Who commits first?"

The answer came faster than expected. Mastek, one of India's pioneering IT companies, was desperately seeking space for expansion. Their CEO had a specific requirement: they needed 100,000 square feet, available 24/7, with 100% power backup, and located where employees could actually afford to live nearby. Traditional business districts couldn't offer this combination. Mindspace Malad could.

The name "Mindspace" itself was carefully chosen—a play on the knowledge economy and the physical space needed to house it. The first building in Malad was designed differently from anything in Mumbai's commercial real estate market. Wide floor plates that could accommodate hundreds of workstations, raised flooring for cable management, chillers that could handle Mumbai's humidity while keeping servers cool, and crucially, multiple redundancies for power and internet connectivity.

Construction began in 1999, and by 2000, Mindspace Malad was operational. But this was just the beginning. The real opportunity lay 1,400 kilometers south in a city that was about to become synonymous with India's IT revolution: Hyderabad. In 2003, Chandrababu Naidu, the visionary Chief Minister of Andhra Pradesh, had a problem. He'd successfully positioned Hyderabad as India's technology capital, attracting Microsoft, Oracle, and other tech giants to set up offices. But the city's infrastructure was buckling under the weight of this success. Traffic was nightmarish, power cuts were frequent, and most importantly, there wasn't enough quality office space to accommodate the thousands of engineers these companies wanted to hire.

The foundation stone for Mindspace Hyderabad was laid on August 29, 2003, at Madhapur in Cyberabad. The project, executed by K Raheja Corp in collaboration with the Andhra Pradesh Industrial Infrastructure Corporation (APIIC), had a clear mandate to convert the 110-acre site into a mecca for corporates. What made this particularly audacious was the site itself—the land comprised steep slopes and valleys, with valley boulders making it particularly challenging to construct around.

Two of K Raheja's contemporaries had actually refused the project, saying it was too daunting. But the Rahejas saw opportunity where others saw obstacles. They brought in international architects and engineers who spent months figuring out how to work with, rather than against, the challenging topography. The masterplan had to be revisited multiple times to ensure safe and strong structures could be built, with architects and engineers eventually creating the perfect solution to negotiate the treacherous slopes and boulders.

The Madhapur project represented a fundamental shift in how Indian commercial real estate was conceived. This wasn't just about building offices—it was about creating an ecosystem. The techno-campus-cum-park plan in Madhapur was executed in 2004, through a joint venture between the Raheja Group and APIIC. The campus included not just office buildings but food courts, recreational facilities, and crucially, infrastructure that could support 24/7 operations for companies serving global clients.

On completion, Mindspace Madhapur featured new technologies such as sewage treatment, energy conservation techniques, and solar power generators—all perfectly integrated with the project. This focus on sustainability wasn't just about corporate responsibility—it was a competitive advantage. Multinational corporations were increasingly demanding LEED-certified buildings, and Mindspace was ahead of the curve.

The results spoke for themselves. Mindspace Madhapur transformed into a hub for IT/ITeS, employing over 80,000 people and housing top multinational companies. With 21 buildings, Mindspace Madhapur became Hyderabad's first and largest Indian Green Building Council Gold Rating Campus. The campus wasn't just functional—it was designed to be a place where people wanted to work, with a 4-acre reserve green area containing 3,500 trees, an open-air theatre, and tennis courts.

But Mindspace's expansion wasn't limited to Hyderabad. By 2003, they had launched Mindspace Business Parks in Cyberabad, and soon expanded to Chennai and Pune. Each location was chosen strategically—cities with growing IT sectors, supportive state governments, and crucially, large pools of engineering talent. The model was consistent: acquire large land parcels on the periphery of cities (where land was cheaper and more available), build world-class infrastructure, and create ecosystems that would attract premium tenants.

The financial model was equally sophisticated. Unlike traditional developers who built and sold, Mindspace focused on building and leasing. This required more capital upfront and longer payback periods, but it created predictable, recurring revenue streams—exactly the kind of cash flows that institutional investors loved. By 2016, the parks developed by Mindspace housed more than 50 businesses in India, including Accenture, L&T Infotech Ltd, Cognizant Technology and Capegemini Group.

The success attracted attention from global investors. Blackstone, the world's largest alternative asset manager, saw in Mindspace exactly what they'd been looking for: a platform with proven execution capabilities, prime assets in India's fastest-growing cities, and a management team that understood both local markets and global standards. The partnership with Blackstone would prove transformative, providing not just capital but also expertise in institutionalizing what had been a family-run business.

As the 2000s progressed, Mindspace had established itself as synonymous with premium commercial real estate in India. They weren't the only players—DLF, Brigade, and Embassy were all building business parks—but Mindspace had carved out a unique position. Their focus on sustainability, their ability to execute complex projects, and their relationships with both government and corporations made them a preferred partner for companies looking to establish or expand operations in India.

The stage was set for the next phase of growth, but it would require a fundamental transformation—from a privately held family business to a publicly traded entity. The vehicle for this transformation would be something entirely new to Indian capital markets: a Real Estate Investment Trust.

IV. Scaling the Platform: Geographic Expansion & Partnerships (2004-2019)

The boardroom at Blackstone's Mumbai office in 2011 was electric with possibility. Tuhin Parikh, the firm's India real estate head, was presenting to his New York colleagues via video conference. On the screen were heat maps of India's major cities, showing IT employment growth, infrastructure development, and most importantly, the supply-demand gap in Grade-A commercial space. "We're not just buying buildings," Parikh explained. "We're buying the platform that will define how India works for the next generation."

Blackstone's interest in Mindspace wasn't accidental. They'd been studying the Indian commercial real estate market for years, watching as IT services exports grew from $10 billion in 2000 to over $100 billion by 2011. Every major global corporation was either outsourcing to India or setting up their own captive centers. But there was a critical bottleneck: quality office space. Most Indian cities had plenty of buildings, but very few met the exacting standards of multinational corporations—100% power backup, multiple internet redundancies, LEED certification, proximity to talent pools, and professional property management.K Raheja Corp partnered with several marquee institutional investors including Blackstone and GIC among others, bringing not just capital but also global best practices in property management, tenant relations, and institutional governance. The partnership with Blackstone was particularly transformative—they didn't just invest money, they brought a playbook for institutionalizing what had been a family-run business.

The geographic expansion during this period was methodical and strategic. Chennai came next, where the Rahejas identified Porur as an emerging IT corridor. The Commerzone brand was launched here—positioned slightly below Mindspace but still offering Grade-A facilities. This dual-brand strategy allowed them to capture different market segments while maintaining overall portfolio quality.

Pune presented a different opportunity. The city had emerged as a manufacturing and engineering hub, but was rapidly transitioning to IT and IT-enabled services. Here, Mindspace didn't just build one campus but multiple properties across Yerwada and Kharadi, anticipating that Pune would become a satellite city for Mumbai-based corporations looking for cost-effective expansion options.

Each new market brought its own challenges. In Chennai, they had to navigate complex land acquisition processes and compete with established local developers. In Pune, the challenge was infrastructure—the city's roads and utilities weren't designed for the kind of 24/7 operations that IT companies required. But in each case, Mindspace's solution was the same: don't just build offices, build ecosystems. The sustainability focus became a defining characteristic of Mindspace properties. In September 2016, K Raheja Corp invested in clean energy, successfully installing a solar rooftop plant at Mindspace Business Park, Madhapur, Hyderabad. The total installed capacity of the plant was 1.6MW, which was one of the largest solar rooftop plants in Telangana at the time. This wasn't greenwashing—it was strategic differentiation. Multinational tenants increasingly demanded sustainability credentials, and Mindspace's LEED Gold certifications became a powerful marketing tool.

The financial structuring during this expansion phase was equally sophisticated. Rather than relying solely on internal accruals or traditional bank debt, K Raheja Corp brought in institutional partners who could provide both capital and credibility. The company partnered with several marquee institutional investors including Blackstone and GIC among others. These partnerships weren't just about money—they were about preparing for an eventual transition to public markets.

By 2016, the results of this expansion were impressive. The parks developed by Mindspace housed more than 50 businesses in India, including Accenture, L&T Infotech Ltd, Cognizant Technology and Capegemini Group. The tenant roster read like a who's who of global technology and consulting firms. But more importantly, the business model had evolved from simply leasing space to providing comprehensive workspace solutions.

The property management division, Matrix, became a crucial differentiator. Unlike traditional landlords who outsourced facility management, Mindspace kept it in-house, ensuring consistent service quality across all properties. This vertical integration meant they could respond quickly to tenant needs, maintain higher occupancy rates, and command premium rents.

The data center opportunity emerged almost organically. As IT companies expanded their operations, they needed not just office space but also secure, climate-controlled environments for their servers. Mindspace began incorporating data center spaces within their business parks, creating an additional revenue stream while deepening tenant relationships. A company that housed both its offices and data centers with Mindspace was far less likely to relocate.

Competition was intensifying. Embassy Group, backed by Blackstone, was building massive IT parks in Bangalore. DLF was expanding its commercial portfolio across NCR. Brigade Group was developing properties in multiple cities. But Mindspace had carved out a unique position—they weren't the largest, but they were arguably the most sophisticated in terms of ecosystem development and sustainability focus.

The global financial crisis of 2008 had tested the model but also validated it. While residential real estate crashed and many developers went bankrupt, Mindspace's focus on long-term leases with blue-chip tenants provided stability. Occupancy rates remained above 90%, rental collections stayed strong, and most importantly, the institutional investors who had backed them saw that this was a resilient, institutional-quality business.

By 2017-2018, conversations within K Raheja Corp and with their institutional partners increasingly turned to one topic: REITs. The regulatory framework had finally been established in India, Embassy Office Parks was preparing to go public, and the question wasn't whether Mindspace should become a REIT, but when and how.

The preparation for this transformation would require not just financial engineering but a fundamental reimagining of how the business operated. Family businesses transitioning to public markets often struggle with governance, transparency, and the discipline of quarterly reporting. But Mindspace had been preparing for this moment for years, whether consciously or not. The partnerships with institutional investors had already introduced rigorous reporting standards. The focus on Grade-A tenants meant reliable, predictable cash flows. The sustainability credentials provided a compelling ESG story.

As 2019 approached, the pieces were falling into place for what would become one of India's most significant real estate IPOs. But first, they would have to navigate the complex process of restructuring a family business into a REIT, convince public market investors that Indian commercial real estate was a compelling investment, and do all of this in what would prove to be one of the most challenging periods in modern history.

V. The REIT Revolution: Going Public (2019-2020)

The lawyers had been working around the clock for weeks. In a conference room overlooking Mumbai's Bandra-Kurla Complex, teams from Cyril Amarchand Mangaldas, Morgan Stanley, and J.P. Morgan were assembled around a table covered with org charts, each box representing a different entity in the K Raheja empire. The challenge: transform a web of special purpose vehicles, joint ventures, and family holdings into a clean, REIT-compliant structure that public market investors could understand and trust.

Mindspace REIT was settled on November 18, 2019 at Mumbai, Maharashtra, India as a contributory determinate irrevocable trust under the provisions of the Indian Trusts Act, 1882, pursuant to a trust deed dated November 18, 2019, and was registered with SEBI on December 10, 2019, at Mumbai as a REIT. The speed of execution was remarkable—from trust formation to SEBI registration in just three weeks.

The IPO structure was complex but elegant. The company aimed to raise Rs 4,500 crore, comprising a fresh issue of units in the REIT of up to Rs 1,000 crore and an offer for sale of up to Rs 3,500 crore by promoter K Raheja Corp and PE giant Blackstone. This dual structure served multiple purposes: the fresh issue would fund acquisitions and debt reduction, while the OFS would provide an exit for Blackstone and partial liquidity for the Raheja family.

The roadshow presentations in early 2020 were a masterclass in storytelling. Ramesh Nair, the CEO, would begin with a simple chart showing India's per capita commercial space—a fraction of what existed in developed markets. "We're not asking you to bet on Mindspace," he would tell potential investors. "We're asking you to bet on India's transition from a $3 trillion to a $10 trillion economy. When that happens, where will all those knowledge workers sit?"

But the real coup came in the form of cornerstone investors. Singapore's GIC, Fidelity and few other strategic investors committed Rs 1,125 crore (at Rs 275 per unit) to the issue. GIC's participation was particularly significant—the Singapore sovereign wealth fund was known for its rigorous due diligence and long-term perspective. Their commitment sent a powerful signal to other institutional investors.

The timing, however, could not have been worse. As the IPO documents were being finalized in early 2020, reports of a mysterious virus in Wuhan were beginning to dominate headlines. By March, India was in lockdown, offices were empty, and the entire premise of commercial real estate was being questioned. Would companies ever return to offices? Was the business park model obsolete? The bankers were nervous, some advocating for postponing the IPO indefinitely.

But Nair and the Mindspace team made a contrarian bet. They argued that COVID-19 wouldn't end the office but would transform it. Companies would want better ventilation, more space per employee, and locations where social distancing was possible. Mindspace's suburban campuses, with their open spaces and modern HVAC systems, were better positioned than cramped city-center offices. Moreover, the REIT structure, with its mandatory 90% distribution requirement, would appeal to yield-hungry investors in a world of near-zero interest rates.

The IPO opened on July 27, 2020, in the midst of the pandemic. The response exceeded all expectations. The issue was oversubscribed 13 times, with institutional investors bidding for 15 times their allocated portion. On August 7, 2020, Mindspace Business Parks REIT listed on the NSE at INR 302 per unit, up 9.81% from the IPO price of INR 275.

Mindspace Business Parks REIT brought 29.5 million square feet of office properties located in Mumbai, Pune, Chennai and Hyderabad to the public markets, with annual rental income of around ₹1,300 crore, estimated to reach ₹2,000 crore in the next few years. The portfolio quality was impressive—94% occupancy, weighted average lease expiry of 5.1 years, and a diverse tenant base with no single tenant contributing more than 7.7% of revenue.

The REIT structure itself was revolutionary for Indian real estate. Unlike traditional developers who had to constantly raise capital for new projects, Mindspace REIT owned completed, income-generating assets. The 90% distribution requirement meant investors would receive regular quarterly distributions, similar to dividends but more tax-efficient. For retail investors, the minimum investment of ₹50,000 made commercial real estate accessible for the first time.

The governance structure marked a clear departure from traditional family-run real estate companies. The REIT was managed by Mindspace Business Parks REIT Manager, with independent directors, quarterly earnings calls, and detailed disclosures. The Raheja family maintained control through their sponsorship, but operations were professionalized in ways that would have been unimaginable a decade earlier.

The pandemic, rather than destroying the business model, actually validated it. As companies implemented hybrid work models, they didn't need less space—they needed different space. Hot-desking, collaboration zones, and outdoor work areas became priorities. Mindspace's large campuses could be reconfigured more easily than traditional offices. Moreover, the flight to quality accelerated. Companies wanted buildings with touchless entry systems, UV sanitization, and hospital-grade air filtration—all of which Mindspace could provide.

The competitive dynamics also shifted post-IPO. As a public REIT, Mindspace had access to capital markets in ways that private developers didn't. They could issue new units for acquisitions, their cost of debt decreased due to improved transparency, and perhaps most importantly, they became a natural consolidator in a fragmented market. Smaller developers with quality assets but lacking access to capital became potential acquisition targets.

The tax advantages of the REIT structure were particularly compelling. SPVs of Mindspace REIT continued to operate under section 10(23FD) of the Income Tax Act, meaning dividend distributions wouldn't be taxed in the hands of unit holders. This made Mindspace units attractive not just for the rental yield but also for the tax efficiency—a rare combination in Indian capital markets.

By the end of 2020, Mindspace REIT had established itself as a legitimate asset class. Insurance companies could invest in it for steady income, pension funds for inflation-protected returns, and retail investors for exposure to commercial real estate without the hassles of direct ownership. The successful listing also paved the way for other developers to consider REIT structures, potentially transforming how commercial real estate was owned and operated in India.

VI. The Portfolio Deep Dive: Assets & Business Model

Stand at the entrance of Mindspace Madhapur in Hyderabad on any weekday morning, and you'll witness a choreographed symphony of modern India's workforce. Between 8 and 10 AM, over 20,000 professionals stream through the gates—software engineers heading to Qualcomm, consultants rushing to Accenture, analysts walking to Facebook's offices. The campus doesn't just house companies; it's a microcosm of India's knowledge economy. Understanding how this machine generates returns requires diving deep into the REIT's portfolio composition and business model.

The portfolio spans 38.1 million square feet across four major cities, but the distribution tells a strategic story. Mumbai Region commands 11.5 msf (30% of portfolio), Hyderabad dominates with 17.5 msf (46%), Pune contributes 7.6 msf (20%), and Chennai adds 1.5 msf (4%). This isn't random—each city represents a different aspect of India's commercial real estate dynamics. Mumbai offers premium rents but limited expansion potential. Hyderabad provides scale and growth at reasonable costs. Pune serves as a satellite for both Mumbai and Hyderabad operations. Chennai offers diversification and access to manufacturing clients.

The portfolio operates under three distinct brands, each targeting different market segments. 'Mindspace' represents the premium offering—integrated business parks with extensive amenities, commanding the highest rents. 'Commerzone' targets mid-market tenants seeking quality space at competitive prices. 'The Square' focuses on standalone buildings in city centers, appealing to companies wanting prestigious addresses without the campus environment. This three-brand strategy allows Mindspace to capture value across the commercial real estate spectrum without diluting its premium positioning.

The asset breakdown reveals sophisticated portfolio construction: 31.0 msf of completed area generating immediate income, 3.7 msf under construction providing near-term growth visibility, and 3.4 msf of future development potential offering long-term optionality. This ladder approach ensures steady current income while maintaining growth potential—crucial for a REIT that must distribute 90% of income but still needs to grow.

Let's examine the crown jewels in detail. Mindspace Madhapur in Hyderabad spans 110 acres with 21 buildings, housing over 80,000 professionals. The campus includes everything from food courts serving 30,000 meals daily to a medical center handling emergencies. It's not just an office park; it's a city within a city. The property generates approximately ₹650 crores in annual rental income with occupancy consistently above 95%.

In Mumbai, Mindspace Airoli represents a different model. Located in Navi Mumbai, it serves as a back-office hub for financial services companies that need proximity to Mumbai's financial district but can't afford South Mumbai rents. The property benefits from excellent connectivity via the Trans-Harbour Link and offers rents at 40-50% discount to Bandra-Kurla Complex, making it attractive for cost-conscious but quality-focused tenants.

The revenue model appears simple but has multiple layers of sophistication. Base rentals form the foundation, typically structured as triple net leases where tenants pay rent plus their share of property taxes, insurance, and maintenance. But the real intelligence lies in the escalation clauses—most leases include 5% annual escalations or 15% every three years, providing built-in inflation protection. The weighted average lease expiry of 5.1 years creates a rolling maturity profile, reducing concentration risk while providing opportunities to mark rents to market.

Tenant diversification is a masterpiece of risk management. The top 10 tenants contribute only 38% of revenues, with no single tenant exceeding 7.7%. The tenant roster spans industries: IT services (42%), financial services (18%), technology (15%), healthcare (8%), and others (17%). This diversification proved invaluable during COVID-19—while some sectors struggled, others thrived, maintaining overall portfolio stability.

The business model extends beyond simple landlord operations. Mindspace operates its own facility management company, maintaining direct control over property operations. This vertical integration serves multiple purposes: ensuring consistent service quality, capturing additional margin, and most importantly, creating switching costs for tenants. When your landlord also manages your cafeteria, security, and maintenance, moving becomes exponentially more complex.

The capital allocation framework reflects REIT constraints but also opportunities. With 90% of distributable income paid out quarterly, growth must come from three sources: rent escalations on existing leases, mark-to-market on lease renewals, and acquisitions or development. The company targets 10-12% distribution yield plus 5-7% capital appreciation—competitive with equity returns but with lower volatility.

The development pipeline provides crucial growth visibility. The 3.7 msf under construction will add approximately ₹400 crores to annual revenue upon completion. More intriguingly, the 3.4 msf of future development rights provides optionality—in a strong market, they can accelerate development; in weak markets, they can preserve capital. This flexibility is rare in REITs globally and provides Mindspace with strategic advantages over fully-developed portfolios.

The data center opportunity represents an evolution of the model. As digitalization accelerates, companies need not just office space but also secure, connected facilities for their servers. Mindspace has begun incorporating data center spaces within its campuses, creating higher-value, stickier tenant relationships. A 100,000 square foot data center can generate rents 2-3x that of office space with 10-15 year lease terms—transforming portfolio economics.

Operating metrics reveal the model's efficiency. Same-store NOI growth averages 8-10% annually, driven by contractual escalations and operating leverage. The EBITDA margin of 83% ranks among the highest globally for commercial REITs, reflecting India's lower operating costs and Mindspace's scale advantages. The cost of debt at 7.5% seems high by global standards but is competitive in Indian markets, and the spread between rental yields (8.5-9%) and borrowing costs provides positive leverage.

The maintenance capital expenditure runs at just 1-2% of revenues, reflecting the portfolio's young age (average building age of 12 years) and high construction quality. This low maintenance requirement means most cash flow is truly distributable, unlike older REITs that must retain significant capital for upkeep.

Portfolio valuation follows standard REIT methodology but with Indian nuances. Properties are valued semi-annually by independent valuers using discounted cash flow analysis. The portfolio is currently valued at ₹62,000 crores, implying a cap rate of approximately 8.5%. By global standards, this seems high (US REITs trade at 4-6% cap rates), but reflects India's higher interest rates and risk premiums. As India's sovereign rating improves and interest rates potentially decline, cap rate compression could drive significant value creation.

The most fascinating aspect is how the portfolio creates network effects. A company leasing space in Mindspace Madhapur might expand to Mindspace Pune as it grows. Employees familiar with Mindspace amenities and systems face lower switching costs moving between cities. Vendors serving multiple Mindspace properties achieve economies of scale. These network effects create competitive moats beyond just real estate ownership.

VII. Post-IPO Performance & Strategic Moves (2020-Present)

The quarterly earnings call in May 2021 was tense. Analysts were drilling into occupancy numbers as India's devastating second COVID wave emptied offices again. "Our occupancy has held at 92%," CEO Ramesh Nair calmly responded, "but more importantly, rent collection remains at 99%. Our tenants aren't just paying for space; they're securing their post-pandemic future." That confidence would prove prescient as Mindspace emerged from the pandemic stronger than ever.

The stock performance tells a story of resilience and recovery. From the IPO price of ₹275 in August 2020, units traded in a range of ₹260-₹290 through the pandemic, demonstrating remarkable stability while other real estate stocks crashed. As offices reopened in 2022, the units began their ascent, reaching ₹350 by early 2023 and eventually touching ₹400 in 2024. Today's price around ₹430 represents a 56% appreciation plus cumulative distributions of approximately ₹80 per unit—a total return exceeding 85% in four years. The strategic moves post-IPO have been bold and calculated. In FY 2025, Mindspace acquired 100% shareholding in Sustain Properties Private Limited holding 1.82 msf at Commerzone Raidurg, a Grade-A commercial asset located in Hyderabad's Madhapur micro-market. The acquisition, valued at ₹2,038 crores, wasn't just about adding square footage—it was about deepening presence in India's most dynamic commercial market.

The fully leased asset spans 1.82 million square feet and forms part of a larger 2.8 msf development, entirely occupied by Qualcomm, a Fortune 500 global capability center. With a 12-year weighted average lease expiry (WALE) and current rentals of INR69 per square foot per month, the asset offers significant mark-to-market potential. This single acquisition expanded Mindspace's Hyderabad portfolio to 15 million square feet, making it the REIT's largest market by area.

The financing structure for acquisitions showcases sophisticated capital management. The REIT's board approved a preferential issue of units aggregating up to Rs 613 crore as consideration for the acquisition of Sustain Properties. By issuing units rather than cash, Mindspace preserves liquidity while aligning the sellers' interests with unitholders—a win-win structure that would become a template for future deals.

The quarterly results tell a story of consistent execution. Mindspace REIT Q1 FY26 showed 24.2% NOI growth, 1.7 msf leasing, INR 5,118 Mn acquisition. These aren't just numbers—they represent thousands of lease negotiations, property upgrades, and strategic decisions playing out across the portfolio. The 24.2% NOI growth particularly stands out, demonstrating that even in a mature portfolio, active management can drive significant value creation.

The return-to-office dynamics post-pandemic have been more nuanced than anyone anticipated. Rather than a binary choice between remote and office work, companies have adopted hybrid models requiring different space configurations. Mindspace responded by introducing "flex spaces"—areas that could be reconfigured based on daily attendance patterns. A 100,000 square foot floor that once housed 1,000 employees working daily might now accommodate 1,500 employees working in shifts, with hot-desking and collaboration zones replacing fixed seating.

The ESG commitments have evolved from nice-to-have to business-critical. Mindspace Business Parks REIT becomes India's first real estate entity to join Climate Group's RE100, committing to 100% renewable electricity across its portfolio by 2050. This isn't just about corporate responsibility—it's about tenant demands. Global corporations increasingly require their real estate partners to meet specific sustainability targets, and Mindspace's early moves in this direction have become a competitive advantage.

Competition has intensified but also validated the REIT model. Embassy Office Parks REIT, backed by Blackstone, remains the largest player with over 45 million square feet. Brookfield India REIT has entered with a focus on Mumbai and Gurugram. But rather than a zero-sum game, the multiple REITs have expanded the market, educating investors about the asset class and creating liquidity that benefits all players.

The distribution track record has been exemplary. Despite pandemic disruptions, Mindspace has never missed a quarterly distribution, paying out approximately ₹20-22 per unit annually. For an investor who bought at the IPO price of ₹275, this represents a yield of 7.3-8%, plus capital appreciation. In a world of volatile equity returns and negligible fixed deposit rates, this combination of yield and growth has attracted a loyal investor base.

The debt management deserves special mention. While Indian interest rates rose from 4% to 6.5% during 2022-2023, Mindspace's average cost of debt increased only marginally from 7.3% to 7.5%, thanks to long-term fixed-rate borrowings and strong banking relationships. The debt-to-asset ratio of 18% is among the lowest in the global REIT universe, providing significant dry powder for acquisitions.

Technology adoption has accelerated post-pandemic. Mindspace launched a tenant app allowing employees to book parking, order food, schedule facility services, and even find carpooling partners. The app has 200,000+ active users, generating valuable data on space utilization patterns. This data informs everything from HVAC scheduling to food court vendor selection, creating efficiencies that flow directly to the bottom line.

The talent strategy has evolved significantly. Post-IPO, Mindspace has recruited senior executives from global REITs, investment banks, and technology companies. The employee stock option plan, unusual for Indian REITs, has helped attract and retain talent. The property management teams now include data scientists analyzing footfall patterns, sustainability experts managing LEED certifications, and customer success managers ensuring tenant satisfaction.

Looking at recent performance, several trends emerge. Same-store rental growth has accelerated to 9-11% annually, above the historical 8-10% range, driven by strong demand from Global Capability Centers (GCCs). The pre-leasing of under-construction properties at 65% indicates robust future demand. Most tellingly, the rent-to-revenue ratio for tenants has declined from 8-10% to 5-7%, suggesting room for further rent increases without stressing tenant economics.

The market dynamics have shifted dramatically in Mindspace's favor. The GCC boom—with over 1,500 centers employing 1.6 million people in India—has created insatiable demand for quality office space. These aren't cost centers but strategic hubs for global corporations, requiring premium facilities that only REITs like Mindspace can provide. The pipeline of 60+ Fortune 500 companies planning to establish or expand GCCs in India suggests this demand will persist for years.

VIII. Playbook: The REIT Investment Framework

"REITs are boring," the hedge fund manager declared at a Mumbai investment conference in 2023. "They're just landlords collecting rent." Ramesh Nair, sitting in the audience, smiled. That perception gap—between REITs as passive rent collectors versus active value creators—represents one of the great investment opportunities in Indian capital markets. Understanding how REITs actually work, particularly in an emerging market context, reveals a far more dynamic and compelling investment framework.

Let's start with the fundamental structure that makes REITs unique. Unlike traditional real estate companies that might reinvest profits into new developments or sit on land banks for decades, REITs must distribute 90% of their net distributable income to unitholders. This forced distribution creates an entirely different economic model. A developer might build a property, sell it, and reinvest the proceeds, creating value over long cycles with lumpy returns. A REIT owns completed properties, collects rent monthly, and distributes cash quarterly—a predictable, transparent model that's easier to value and harder to manipulate.

The tax efficiency of Indian REITs is particularly elegant. SPVs of Mindspace REIT will continue to operate in the old corporate tax regime, under section 10(23FD) of the Income Tax Act, 1961, meaning distributions aren't taxed in unitholders' hands. Compare this to dividends from regular companies, which face dividend distribution tax, or rental income from direct property ownership, which is taxed at marginal rates. For high-net-worth individuals in the 30% tax bracket, this difference alone can add 2-3% to annual returns.

The valuation framework for REITs differs fundamentally from both stocks and direct real estate. Traditional equity valuation uses P/E ratios, comparing price to earnings. Real estate uses price per square foot. REITs require a hybrid approach: Price-to-FFO (Funds From Operations), comparing unit price to cash generated from operations. Mindspace trades at approximately 14x FFO, reasonable compared to global REITs at 15-20x, especially considering India's higher growth rates.

But the real insight comes from understanding cap rates—the net operating income divided by property value. Mindspace's portfolio trades at an 8.5% cap rate, while similar properties in Singapore or Hong Kong trade at 4-5%. This gap isn't just about country risk; it reflects India's higher interest rates and less mature REIT market. As India's sovereign rating improves and rates potentially converge with developed markets, this cap rate compression could drive 30-40% value appreciation independent of rental growth.

The platform value extends beyond individual properties. When Mindspace acquires a building, it doesn't just get rental income—it gets data on tenants, relationships with their parent companies, and insights into expansion plans. This information advantage helps in everything from timing new developments to pricing lease renewals. A standalone building owner lacks this ecosystem intelligence, explaining why REITs can achieve 5-10% higher rents than individual landlords.

The operational leverage in the REIT model is underappreciated. Most costs—property management, security, maintenance—are largely fixed or grow slowly with inflation. But rents escalate at 5% annually through contracted escalations, and 10-15% on renewal through mark-to-market. This expanding spread between revenue growth and cost growth drives margin expansion. Mindspace's EBITDA margin has expanded from 79% at IPO to 83% today, with potential to reach 85% as the portfolio matures.

The reinvestment flexibility provides optionality that traditional companies lack. While Mindspace must distribute 90% of income, the remaining 10% plus external capital can fund growth. But unlike manufacturers who must constantly reinvest just to maintain competitiveness, REITs can pause expansion during downturns without losing relevance. This optional reinvestment creates a heads-I-win, tails-I-don't-lose dynamic rare in capital-intensive businesses.

Let's decode the risk factors with unusual honesty. The biggest risk isn't work-from-home—surveys show 80%+ of employees want office options—but rather oversupply. If every developer builds Grade-A offices, rents will collapse. But the barriers to creating Mindspace-quality assets are formidable: land acquisition in prime locations, 3-4 year development cycles, ₹4,000-5,000 per square foot construction costs, and operational expertise. These barriers create a moat that financial analysis often misses.

Interest rate sensitivity is real but overstated. Yes, rising rates make REIT yields less attractive versus bonds. But Mindspace's 18% debt-to-assets ratio means limited refinancing risk. More importantly, the same economic growth that drives rate hikes also drives rental demand. The correlation between rates and REIT performance is negative in the short term but positive over full cycles—a nuance that creates opportunity for patient investors.

The global comparison reveals India's unique position. US REITs are mature, yielding 3-4% with 2-3% growth—a 5-7% total return. Singapore REITs yield 5-6% with minimal growth. Indian REITs offer 7-8% yields with 5-7% growth potential—a 12-15% total return proposition. This isn't sustainable forever; as the market matures, yields will compress. But for the next decade, India offers the rare combination of high yield and high growth.

The institutional adoption curve is accelerating. Insurance companies, previously restricted to direct real estate, can now invest in REITs for regulatory capital efficiency. Pension funds seeking inflation-protected income find REITs ideal. Most intriguingly, global REIT funds that previously ignored India are beginning to allocate capital, drawn by the growth potential. This expanding investor base should reduce volatility and improve valuations over time.

Portfolio construction considerations matter. REITs shouldn't be viewed as equity or debt substitutes but as a third asset class. The correlation with Nifty is approximately 0.6—meaningful but not lockstep. During equity market corrections, REITs typically fall less; during rallies, they lag. This dampening effect makes them ideal for reducing portfolio volatility while maintaining return potential. A 15-20% REIT allocation can improve risk-adjusted returns for most portfolios.

The scalability advantage becomes more pronounced over time. As Mindspace grows from 38 to 50 million square feet, corporate overhead barely increases. The same management team that handles ₹2,500 crores in revenue can manage ₹4,000 crores with minimal additions. This operating leverage means that growth disproportionately flows to unitholders rather than being consumed by bureaucracy.

IX. Analysis & Investment Case

The investment committee room at a major mutual fund in Mumbai, March 2024. The CIO is challenging his team: "Mindspace has run up 50% from its lows. The easy money is made. Why should we still own it?" The analyst responds with a question: "What's the value of the best locations in India's fastest-growing cities, leased to the world's most successful companies, with contracts guaranteeing rental increases, in a country adding $500 billion to GDP annually?" The room goes quiet. Sometimes the bull case is hiding in plain sight.

Let's construct the bull case with mathematical precision. India's commercial office stock stands at 700 million square feet, compared to 8.8 billion in the US—a 12x gap for an economy that's one-eighth the size. As India grows from $3.7 trillion to $7 trillion by 2030, commercial space must double just to maintain current density ratios. But here's the kicker: only 30% of current stock is Grade-A. The demand for quality space could triple while overall demand merely doubles. Mindspace, with its Grade-A focus, is positioned to capture disproportionate value from this quality migration.

The GCC revolution is even more compelling. Global companies are moving from labor arbitrage (hiring cheap Indian engineers) to capability arbitrage (accessing Indian talent regardless of cost). Morgan Stanley expects GCCs to add 1 million employees by 2030, each requiring 100-150 square feet of premium office space. That's 100-150 million square feet of new demand, equivalent to four complete Mindspace portfolios. The company's established relationships with GCC parents provide inside track on this expansion.

The financial mathematics are seductive. Current rental yield of 8.5% with 5% annual escalations means an investor doubling their money every 8-9 years through distributions alone, without any capital appreciation. Add modest 3-4% annual appreciation from cap rate compression as India's risk premium narrows, and total returns approach 15% annually. In a world of 2% developed market returns, this is extraordinary.

But let's stress-test the bear case with equal rigor. Company has a low return on equity of 3.10% over last 3 years. This seems alarming until you realize REITs aren't meant to compound equity—they're meant to distribute it. The low ROE reflects high distribution ratios, not operational weakness. Still, it highlights that growth must come from external capital, creating dilution risk if units are issued below intrinsic value.

The work-from-home threat deserves serious consideration. If remote work becomes permanent, office demand could structurally decline. But the evidence suggests otherwise. Mindspace's 94% occupancy in 2024 exceeds pre-pandemic levels. Tenant surveys show 85% plan to maintain or expand office footprints. The nature of demand is changing—from dense seating to collaborative spaces—but total space requirements remain robust. Companies are discovering that culture, creativity, and career development suffer in fully remote settings.

Oversupply represents a more credible risk. Bangalore added 15 million square feet of office space in 2023 alone. If every city replicates this, rental growth will evaporate. But construction costs have risen 30% post-pandemic, land prices in prime locations have doubled, and approval processes have lengthened. These natural barriers limit supply growth to 5-7% annually, below demand growth of 8-10%. The supply risk is real but manageable.

The comparison with Embassy REIT is instructive. Embassy, at 45 million square feet, is larger, but concentrated in Bangalore (60% of portfolio). Mindspace's diversification across four cities provides resilience. Embassy trades at a 10% discount to book value; Mindspace at a 5% premium. The market values Mindspace's superior diversification and growth profile, validating the multi-city strategy.

Global comparisons reveal relative value. Simon Property Group, America's largest retail REIT, trades at 15x FFO with 3% growth. Prologis, the logistics REIT giant, trades at 25x FFO with 8% growth. Mindspace at 14x FFO with 10% growth seems undervalued, especially considering India's superior economic growth trajectory. As global investors increase India allocations, this valuation gap should narrow.

The sponsor quality question—family ownership versus institutional—cuts both ways. The Raheja family's 64% ownership ensures alignment but raises governance concerns. However, their track record of partnering with institutions, accepting independent directors, and maintaining transparent operations suggests professional management despite family control. The recent acquisitions from sponsor entities at arms-length valuations demonstrate fairness to minority unitholders.

The accounting considerations are refreshingly simple. Unlike traditional developers with complex revenue recognition and inventory valuations, REITs report rental income as earned and properties at fair value. The semi-annual independent valuations provide mark-to-market transparency. There's limited room for accounting manipulation—either tenants pay rent or they don't, properties are either occupied or vacant.

ESG factors increasingly drive investment decisions. Mindspace's RE100 commitment, LEED certifications, and social initiatives (employing 50,000+ indirect workers) check institutional boxes. But beyond compliance, sustainability drives economics. Energy-efficient buildings command 5-10% rental premiums and experience 2-3% lower vacancy. The ₹50 crore annual investment in sustainability generates ₹75 crore in incremental rental value—a 50% ROI that also happens to save the planet.

The technological disruption angle is nuanced. Yes, virtual reality might reduce travel, affecting office demand. But AI and automation are creating new job categories requiring collaboration spaces. The content creation economy needs studio spaces. Hybrid work requires touchdown spaces in multiple cities. Mindspace is experimenting with all these models, from podcast studios to day-use offices. Technology might change office use but won't eliminate it.

Risk-adjusted returns tell the complete story. Mindspace's Sharpe ratio (return per unit of risk) of 1.2 exceeds the Nifty's 0.8 and debt funds' 0.4. The Information ratio (excess return per unit of tracking error) of 0.9 indicates consistent outperformance. These metrics matter because they capture what investors actually experience—not just returns but the stress endured to achieve them.

The reinvestment runway extends decades. India needs 2 billion square feet of additional commercial space by 2040. Even capturing just 2% market share would triple Mindspace's portfolio. The land banks and development rights already owned provide 10+ years of growth visibility without additional land acquisition. This embedded growth option, valued at zero in current trading prices, represents significant hidden value.

X. The Future: India's Commercial Real Estate

The year is 2030. A Fortune 500 CEO video calls into her company's quarterly board meeting from what looks like a traditional office. But she's actually in a Mindspace "Work Club" in Pune, one of 50 such facilities across India where any employee from any Mindspace tenant can book workspace by the hour. The boundaries between office, home, and third spaces have blurred, but the need for professional environments has only intensified. This glimpse into the future reveals how commercial real estate will evolve—not disappear—in the coming decade.

The Global Capability Centers (GCC) boom represents the most significant structural shift in Indian commercial real estate since the Y2K-driven IT explosion. Unlike the cost-arbitrage model of the 2000s, GCCs are building core capabilities in India. Google's Bangalore office isn't supporting California; it's developing products for global markets. This shift from back-office to innovation center requires different real estate—larger floor plates for collaboration, specialized labs, and 24/7 operational capability. Mindspace's portfolio, designed for this evolution, is perfectly positioned.

The numbers are staggering. India currently hosts 1,580 GCCs employing 1.66 million people. By 2030, this is expected to reach 2,400 centers with 2.5 million employees. Each employee requires 125-150 square feet of space, implying demand for 375 million square feet—more than half of India's current total commercial stock. This isn't gradual growth; it's a tsunami of demand that existing supply cannot satisfy.

Data centers represent the next frontier. India's data localization laws require global companies to store Indian user data domestically. The 5G rollout, digital payments explosion, and AI adoption are driving exponential data growth. Mindspace has 500 acres of land that could be developed as data centers, generating 3-4x the rental yield of traditional offices. A single 100MW data center can generate ₹500 crores in annual revenue—equivalent to a 2 million square foot office park.

The sustainability imperative will reshape portfolio economics. By 2030, carbon pricing will likely make non-green buildings economically unviable. Mindspace's early investments in renewable energy and LEED certifications will translate into competitive advantages. Tenants will pay 15-20% premiums for net-zero buildings, not for environmental reasons but because their own ESG commitments demand it. The ₹500 crore investment in sustainability infrastructure will generate ₹1,000 crores in incremental value.

Urban planning evolution favors suburban business districts. As cities grapple with congestion and pollution, governments are incentivizing commercial development in peripheral areas. Mindspace's locations in Airoli, Madhapur, and Yerwada—once considered remote—are becoming new city centers. The Mumbai Trans-Harbour Link has cut Airoli-South Mumbai commute time from 90 to 30 minutes. Similar infrastructure projects across cities will enhance portfolio value without any action from Mindspace.

The hybrid work model, rather than reducing space needs, is creating demand for flexible configurations. Companies want 60% dedicated desks, 25% collaboration spaces, and 15% focus rooms—versus the previous 85% dedicated desks model. This reconfiguration requires more space per employee, not less. Mindspace is pioneering "dynamic offices" where AI-powered systems reconfigure spaces based on daily attendance patterns, maximizing utilization while improving employee experience.

Artificial intelligence will transform property operations. Mindspace is deploying predictive maintenance systems that identify HVAC issues before they occur, reducing downtime by 60%. Facial recognition enables touchless entry, while occupancy sensors optimize energy usage in real-time. These technologies reduce operating costs by 20-30% while improving tenant satisfaction. The ₹100 crore investment in PropTech will generate ₹200 crores in annual savings by 2030.

The demographic dividend cannot be ignored. India adds 12 million people to its workforce annually. Even assuming 30% work in services requiring office space, that's 3.6 million new office workers yearly, requiring 450 million square feet by 2030. This demographic pressure ensures sustained demand regardless of technological disruption. Unlike China's aging population or Europe's demographic decline, India's youth bulge guarantees commercial real estate demand for decades.

Financial market evolution will benefit REITs disproportionately. As India's bond market deepens, REITs will access longer-tenure, lower-cost debt. The potential inclusion in global REIT indices would bring $2-3 billion in passive flows. Domestic mutual funds launching REIT-focused schemes will broaden the investor base. These technical factors could compress cap rates by 200 basis points, driving 25-30% capital appreciation independent of operational performance.

The acquisition opportunity is massive. India has 700 million square feet of commercial space, but only 150 million square feet is held by REITs. As capital costs rise and development becomes challenging, standalone property owners will increasingly sell to REITs. Mindspace, with its proven integration capabilities and access to capital, could double its portfolio through acquisitions alone. The next decade will witness consolidation similar to what occurred in US REITs during the 1990s.

Potential M&A scenarios deserve consideration. A merger with Embassy REIT would create a 80+ million square foot behemoth, achieving unparalleled scale economies. Alternatively, Mindspace could acquire smaller portfolios in emerging cities like Coimbatore or Ahmedabad, expanding geographic reach. Most intriguingly, a global REIT might acquire Mindspace entirely, paying 30-40% premiums to enter Indian markets—similar to Blackstone's acquisition of Embassy.

The risks are real but manageable. Climate change could make some properties unviable, but Mindspace's focus on sustainable design provides resilience. Technological disruption could reduce space needs, but history shows technology creates more jobs than it destroys. Regulatory changes could impact REIT taxation, but the government's commitment to developing capital markets suggests supportive policies will continue.

The next decade will likely see Mindspace's evolution from a pure office REIT to a diversified commercial platform. Industrial logistics parks serving e-commerce, life sciences labs supporting India's pharma industry, and studio spaces for the content economy all represent logical extensions. The management team's ability to execute this transformation while maintaining distribution discipline will determine whether Mindspace becomes India's first $10 billion REIT.

XI. Epilogue & Key Takeaways

As our story comes full circle, let's return to that conference room in 2019 where the Mindspace IPO was being finalized. The lawyers and bankers who worked those long nights couldn't have imagined that within 18 months, a pandemic would empty every office in their portfolio. Nor could they have predicted that Mindspace would emerge stronger, with higher occupancy and better returns than before the crisis. This resilience—born from six decades of navigating India's volatile real estate markets—defines what makes Mindspace different.

The transformation from K Raheja Corp's family business to Mindspace REIT represents more than financial engineering. It's a case study in how Indian businesses can professionalize while maintaining entrepreneurial spirit. The Raheja family retained majority control but embraced institutional governance. They distributed profits rather than hoarding capital. They partnered with global investors while maintaining local expertise. This balance—rare in family businesses globally—created unique value.

For real estate developers considering REIT structures, Mindspace offers crucial lessons. First, quality matters more than quantity. Mindspace's focus on Grade-A properties enabled REIT conversion; B-grade assets would have failed institutional due diligence. Second, operational excellence precedes financial engineering. The in-house property management capabilities, developed over decades, proved essential for maintaining post-IPO performance. Third, transparency pays. The willingness to accept quarterly scrutiny and independent oversight attracted institutional capital at premium valuations.

The investment lessons extend beyond real estate. Mindspace demonstrates that in emerging markets, the intersection of structural trends (urbanization, formalization, financialization) creates extraordinary opportunities. Patient investors who identify these intersections early can generate returns that seem impossible in developed markets. But timing matters—entering too early means waiting years for trends to materialize; too late means paying prices that reflect realized rather than potential value.

The role of REITs in India's capital market evolution deserves emphasis. By providing retail investors access to institutional-quality real estate, REITs democratize an asset class previously reserved for the wealthy. By forcing distribution of profits, they prevent capital misallocation common in family businesses. By requiring transparency, they bring global governance standards to Indian real estate. Mindspace's success validates this model, encouraging other developers to follow suit.

The human element shouldn't be forgotten. Behind Mindspace's millions of square feet are thousands of employees—property managers ensuring 24/7 operations, leasing executives negotiating with Fortune 500 companies, engineers maintaining critical infrastructure. Their dedication, particularly during the pandemic when they ensured business continuity for essential services, represents the true foundation of Mindspace's value. REITs aren't just financial instruments; they're organizations of people serving other people.

Looking ahead, Mindspace stands at an inflection point. The easy growth from India's IT boom is behind us. Future growth requires navigating hybrid work models, sustainability mandates, and technological disruption. But the company's track record suggests readiness for these challenges. The same organization that transformed from a Mumbai developer to a national REIT can evolve into whatever commercial real estate becomes in the digital age.

For investors, Mindspace offers a compelling but complex proposition. It's neither a high-growth tech stock nor a stable utility. It's a hybrid—offering equity-like returns with bond-like predictability, growth potential with distribution requirements, Indian exposure with global standards. Understanding these nuances, rather than forcing Mindspace into conventional categories, is essential for investment success.

The broader implications for India's economy are profound. If Mindspace and other REITs succeed, they'll unlock billions in real estate value currently trapped in illiquid holdings. This capital can fund new development, improving India's infrastructure competitiveness. The regular distributions will create wealth effects, boosting consumption. The transparency will reduce corruption, improving capital allocation. REITs aren't just investment vehicles; they're instruments of economic transformation.

The story we've traced—from Chandru Raheja's post-partition arrival in Mumbai to today's sophisticated REIT—mirrors India's own journey. From scarcity to abundance, isolation to integration, family capitalism to institutional markets. Mindspace embodies this transformation, making it not just an investment opportunity but a bet on India's continued evolution.

As we conclude, perhaps the most important takeaway is that Mindspace's best chapters may lie ahead. The combination of India's economic growth, commercial real estate demand, and REIT structure advantages creates a runway for decades of value creation. Whether Mindspace captures this opportunity depends on execution, but the ingredients for success are in place.

For those seeking to understand India's commercial real estate future, Mindspace provides the clearest window. For those seeking investment returns, it offers a rare combination of yield and growth. For those studying business transformation, it demonstrates how family enterprises can evolve without losing their essence. And for those who simply appreciate a good business story, Mindspace delivers drama, strategy, and ultimately, success against considerable odds.

The Mindspace story continues to unfold, with each quarterly earnings report adding new chapters. But the foundation—quality assets, strong governance, aligned interests, and exposure to India's growth—remains constant. In a world of rapid change and uncertainty, this consistency might be Mindspace REIT's greatest asset of all.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube