Minda Corporation: The Evolution of India's Auto Component Champion

I. Introduction & Cold Open

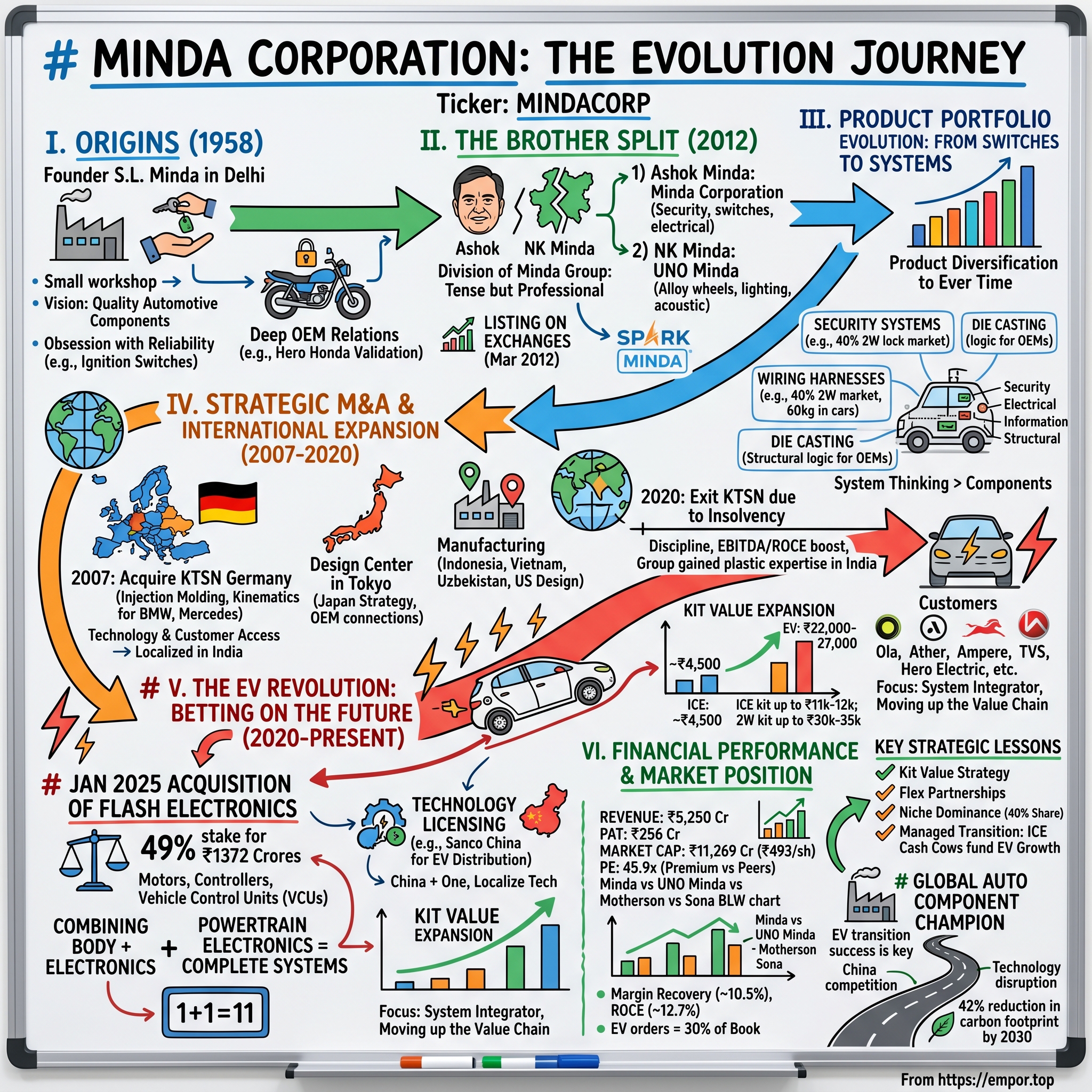

The year is 2012. In a conference room in Delhi, two brothers sit across from each other, lawyers flanking both sides. On the table between them lies the blueprint for dividing an empire—the Minda Group, built over five decades from a small workshop into one of India's most formidable automotive component manufacturers. Ashok Minda and NK Minda, sons of the late S.L. Minda who founded the company in 1958, are about to split the business their father built with borrowed capital and boundless ambition.

This moment—tense, consequential, deeply personal—would reshape India's auto component landscape. From this division would emerge two separate public companies, each charting its own course through the turbulent waters of India's automotive revolution. Ashok would take Minda Corporation, the flagship entity focused on switches and security systems. NK would build Minda Industries, specializing in alloy wheels and lighting. Both brothers would prove the skeptics wrong, building businesses that today command market capitalizations exceeding ₹10,000 crores each.

But here's the real story: How did a small ignition switch manufacturer, operating from a modest Delhi workshop in the License Raj era, transform into a ₹11,000+ crore automotive powerhouse? How did Minda Corporation navigate family dynamics, technological disruptions, and the seismic shift from combustion engines to electric vehicles while maintaining its grip on 40% of India's two-wheeler lock market?

This is a story about more than corporate strategy—it's about the evolution of Indian manufacturing itself. From import substitution to global competitiveness, from mechanical locks to smart key systems, from supplying Hero Honda to partnering with Ola Electric. It's about how a traditional family business embraced professional management, international acquisitions, and technological partnerships to stay relevant across six decades of change.

The numbers tell part of the story: ₹5,250 crores in revenue, operations across 38 manufacturing plants, exports to over 25 countries, and an order book exceeding ₹8,000 crores. But the real narrative lies in the decisions made at critical junctures—the choice to acquire a German technology company in 2007, the bet on electric vehicles before the market was ready, the strategic pivot from component supplier to system integrator.

What makes Minda Corporation particularly fascinating is its position at the intersection of India's old economy and new. While Tesla captures headlines with its vertical integration strategy, Minda quietly supplies critical components to virtually every major two-wheeler manufacturer in India. While startups raise billions to build EV infrastructure, Minda leverages six decades of OEM relationships to capture the electrification opportunity.

As we dive into this story, we'll explore three critical themes that define not just Minda Corporation but the entire Indian auto component industry: First, how family businesses can successfully navigate generational transitions and corporate splits while creating value for all stakeholders. Second, how traditional manufacturers can reinvent themselves for technological disruptions without abandoning their core strengths. And third, how Indian companies can compete globally not through cost arbitrage alone but through strategic partnerships, technology acquisition, and market dominance in specific niches.

The road ahead promises even more transformation. With India's EV market projected to grow at 49% CAGR through 2030, and Minda targeting a 5x increase in kit value per vehicle—from ₹4,500 in traditional vehicles to ₹22,000-27,000 in EVs—the company stands at another inflection point. But to understand where Minda Corporation is heading, we must first understand where it came from, starting with a young entrepreneur in newly independent India who saw opportunity where others saw only chaos.

II. Origins: The Minda Legacy & Early Foundation

Delhi, 1958. The city still bore the scars and energy of Partition, just eleven years old. In the industrial areas of the capital, small workshops hummed with the sound of opportunity—India was building itself, literally from the ground up. Among these workshops, in a modest facility with borrowed capital and grand ambitions, Shadi Lal Minda founded what would become the Minda Group, steering it since 1958 to emerge as a leading player in the Indian automotive industry.

Picture the scene: a young entrepreneur with technical skills but limited resources, navigating the byzantine bureaucracy of the License Raj. Every piece of imported machinery required permits. Every expansion needed government approval. Foreign collaboration meant months of paperwork. Yet in this constrained environment, S.L. Minda saw what others missed—India's automotive industry was nascent but inevitable. The country would need vehicles, and vehicles would need components.

The timing was prescient. India's first Five Year Plan had just concluded, emphasizing industrialization. Premier Automobiles and Hindustan Motors were assembling cars, while Bajaj and Enfield were setting up two-wheeler production. But the component ecosystem? Virtually non-existent. Most parts were imported, expensive, and unreliable in supply. Minda's vision was simple yet revolutionary for its time: build quality automotive components locally, starting with the most basic yet critical part—the ignition switch.

Minda Corporation Limited's formal incarnation came much later. The Group was founded in 1958 by Late Sh. S. L. Minda in Delhi, but the flagship company was incorporated in March 1985 as Minda Huf Limited—the "HUF" standing for Hindu Undivided Family, a traditional business structure that would later prove limiting as the company sought institutional capital. The transformation to Minda Corporation Limited in March 2007 signaled a shift from family enterprise to corporate entity, though family control would remain paramount.

What distinguished S.L. Minda from countless other small manufacturers of that era was his understanding of a fundamental truth: in automotive manufacturing, reliability trumps everything. A vehicle might have thousands of components, but a single faulty ignition switch renders it useless. This obsession with quality—unusual for Indian manufacturers in an era of protected markets and guaranteed demand—would become the company's defining characteristic.

The early years were brutal. Working capital was perpetually short. Technology had to be reverse-engineered or developed from scratch. Skilled workers were rare. Yet Minda persevered, gradually expanding from ignition switches to a broader range of electrical components. Each new product meant months of development, testing with skeptical OEMs, and gradual trust-building. Hero Honda's decision to source switches from Minda in the early 1980s marked a turning point—validation from Japan's Honda that an Indian supplier could meet international standards.

The License Raj, paradoxically, provided both constraints and protection. While limiting growth and technology access, it also restricted competition. Foreign manufacturers couldn't easily enter India, and domestic competitors faced the same regulatory hurdles. Minda used this protected period wisely, building relationships with every major OEM, understanding their needs intimately, and creating switching costs that would endure long after liberalization.

By the late 1980s, Minda had established a unique position. The company wasn't the largest component manufacturer, nor the most technologically advanced. But in the specific niche of switches and electrical systems for two-wheelers—the fastest-growing segment of India's automotive market—they had become indispensable. Every Hero Honda, every Bajaj scooter, every TVS moped likely had Minda components. Market share in certain categories exceeded 40%, creating a moat that would prove remarkably durable.

S.L. Minda believed and worked through various ways for his single mission of "Social Change for Nation Building". This wasn't mere corporate rhetoric. The Minda Bal Gram, schools for underprivileged children, and various charitable trusts established by the founder created a culture of social responsibility that would permeate the organization. Employees weren't just workers but stakeholders in a larger mission of industrial development and social progress.

The stage was set for dramatic expansion. By the early 1990s, as India began liberalizing its economy, Minda Corporation had built three critical assets: deep OEM relationships, manufacturing expertise in electrical components, and a reputation for reliability. But the real test would come with the next generation. S.L. Minda's sons, Ashok and NK, had joined the business, each with their own vision for the future. Their collaboration would drive remarkable growth through the 1990s and 2000s. Their eventual split would reshape India's auto component landscape entirely.

III. The Brother Split & Corporate Restructuring (2012)

The mahogany conference table at the Taj Palace Hotel in Delhi had seen many corporate negotiations, but perhaps none as emotionally charged as this one in 2012. The company was formed after a split between the businesses of the Minda brothers in 2012. Across from each other sat Ashok Minda and Nirmal Kumar (NK) Minda, second-generation scions of the automotive empire their father had built from scratch. Between them lay spreadsheets detailing assets worth thousands of crores, customer relationships cultivated over decades, and the weight of a legacy that neither wanted to diminish.

The split wasn't sudden—it had been brewing for years. Brothers who had once worked side by side to modernize their father's business now had fundamentally different visions for the future. Ashok, the elder, believed in aggressive expansion through technology partnerships and international acquisitions. NK favored organic growth and deeper penetration in existing markets. Both approaches had merit; neither brother was willing to compromise. What started as strategic disagreements in board meetings had evolved into something more fundamental—a recognition that the Minda Group had grown too large for a single vision.

NK Minda owns and operates Minda Industries Ltd and Ashok Minda is the owner of Minda Corporation Ltd, with NK Minda getting control of Minda Industries and Ashok Minda receiving Minda Corporation. The division wasn't arbitrary—it reflected each brother's strengths and interests. Ashok retained the flagship Minda Corporation with its dominance in switches, locks, and wiring harnesses. NK took Minda Industries, focusing on alloy wheels, lighting, and acoustic systems. The name of Minda Industries was changed to UNO Minda recently to reflect its different identity from Minda Corporation.

The mechanics of the split were complex, involving months of valuation exercises, customer negotiations, and employee communications. Key OEM relationships had to be carefully divided—some customers preferred continuity and chose to work with both entities, while others aligned with one brother based on product dependencies. The Maruti Suzuki account, crown jewel of any component supplier, was particularly sensitive. Both companies ultimately retained Maruti as a customer, but for different product lines.

What's remarkable about the Minda split is what didn't happen. Unlike many family business separations that end in acrimony and litigation, this was relatively amicable. No court battles, no public mudslinging, no disruption to operations. Employees were given choices about which entity to join. Suppliers were assured of continuity. Most importantly, customers saw no interruption in quality or delivery—a testament to the professional management both brothers had instituted.

Both the companies are listed on the exchanges. Minda Corporation was listed on the stock exchanges in March 2012. The public listing added another dimension to the separation—now both brothers would be judged not just by each other but by the market. Share prices would become the ultimate scorecard, quarterly results the new battleground.

The immediate aftermath revealed interesting dynamics. Rather than competing destructively, both companies found their niches. Minda Corporation doubled down on its strength in two-wheeler components and security systems. UNO Minda expanded aggressively in four-wheeler segments and international markets. The market initially remained skeptical—investors worried about losing synergies, duplicated costs, and potential price wars. But within two years, both companies had proven the skeptics wrong.

Consider the numbers: By 2015, three years post-split, Minda Corporation had grown revenues by 40% while maintaining margins. UNO Minda had successfully launched new product lines and expanded internationally. Combined, the two entities were worth more than the unified group would have been—a validation of the decision to separate. The split had unlocked value by allowing each entity to pursue focused strategies without compromise.

The human element deserves attention. Spark Minda is owned by Mr.Ashok Minda and UNO Minda is owned by Mr.Nirmal Minda and interestingly both are brothers. In Indian business culture, where family unity is paramount and splitting the family silver is seen as failure, the Minda brothers had done something radical. They had prioritized business logic over emotional attachment, professional growth over family harmony. Yet paradoxically, by separating their business interests, they may have preserved their personal relationship.

Industry veterans offer an interesting perspective on the split. One senior auto executive, requesting anonymity, noted: "The Minda separation was probably inevitable. The Indian auto component industry was becoming too sophisticated for consensus-based family management. You needed quick decisions, focused strategies, and clear accountability. The split gave both brothers the freedom to execute their visions without compromise."

The strategic implications extended beyond the Minda family. For OEMs, the split meant more negotiating leverage—two suppliers instead of one, competitive tension that could drive innovation and cost reduction. For competitors, it meant facing two agile, focused entities instead of one large, potentially slower conglomerate. For investors, it offered two distinct investment theses—Minda Corporation's steady cash flows from market-leading positions versus UNO Minda's growth potential in passenger vehicles.

Looking back, the 2012 split represents a watershed moment not just for the Minda family but for Indian family businesses generally. It demonstrated that separation, done professionally, could create rather than destroy value. It showed that family businesses could evolve beyond traditional structures while maintaining their entrepreneurial spirit. Most importantly, it proved that sometimes the best way to honor a legacy is to divide it thoughtfully rather than preserve it forcefully.

The road ahead would test both brothers' strategic acumen as the Indian automotive industry faced its biggest transformation yet—the shift to electric vehicles.

IV. Product Portfolio Evolution: From Switches to Systems

The evolution of Minda Corporation's product portfolio reads like a technical manual of India's automotive history. Each new product category represents not just business expansion but a response to how Indians travel, what they value, and how technology reshapes mobility. From the humble ignition switch of 1958 to today's smart key systems and EV components, Minda's journey mirrors the sophistication of Indian consumers and the globalization of automotive standards.

Walk into Minda's Pune technical center today and you'll find engineers reverse-engineering a European smart key system, designers creating dashboard clusters for electric scooters, and quality teams testing wiring harnesses that must survive 15 years of Indian road conditions. The company commands a market share of ~40% in 2W lock sets, and wiring harness for 2W, 3W, tractors, and CVs. This dominance wasn't built overnight—it's the result of six decades of incremental innovation, strategic bets, and deep understanding of what Indian OEMs actually need versus what global suppliers think they need.

The security systems business exemplifies Minda's approach to product evolution. In the 1980s, a lock was purely mechanical—tumblers, springs, and precision machining. By the 1990s, electronic immobilizers were being integrated. The 2000s brought transponder keys. Today, Minda manufactures keyless entry systems that communicate with smartphones, backed by military-grade encryption. Each generation built on the previous one's expertise while adding new capabilities. The company didn't abandon mechanical locks—they still generate substantial revenue—but layered electronic intelligence on top.

Consider the product range today: mechatronic products including ignition switch cum steering locks, smart key systems, mechatronics handles and immobiliser systems; die casting components for structural applications; starter motors and alternators for electrical systems; information and connected systems spanning wiring harnesses, connectors, terminals, and components; plus instrument clusters, dashboards, and a comprehensive range of sensors for speed, temperature, position, pressure, and exhaust gas monitoring. This isn't random diversification—it's systematic expansion into adjacent categories where existing capabilities provide competitive advantage.

The wiring harness business deserves special attention. To outsiders, a wiring harness seems commodity-like—copper wires, plastic connectors, basic assembly. But in reality, it's one of the most complex components in a vehicle. A modern car contains over 5,000 individual wires, weighing up to 60 kilograms, connecting hundreds of components. The harness must be customized for each vehicle model, survive temperature extremes from -40°C to +125°C, resist vibration, moisture, and chemical exposure, all while maintaining perfect electrical conductivity for 15+ years. Minda's 40% market share in two-wheeler and three-wheeler harnesses reflects mastery of this complexity at Indian cost points.

The sensor portfolio reveals another dimension of evolution. Starting with basic mechanical speedometer cables, Minda now produces sophisticated electronic sensors measuring everything from exhaust gas composition to tire pressure. Each sensor type required different expertise—mechanical, electrical, chemical, software. The company didn't develop all capabilities internally; strategic partnerships filled gaps. But Minda retained system integration expertise, understanding how sensors interact with other vehicle systems—a capability many pure-play sensor manufacturers lack.

Die casting represents a fascinating strategic pivot. Aluminum high-pressure die casting, and compressor housing might seem disconnected from electrical components, but the logic becomes clear when examining customer needs. As vehicles became lighter for fuel efficiency, aluminum replaced steel in many structural applications. OEMs wanted suppliers who could provide complete sub-assemblies—not just electrical components but also the housings, brackets, and structural elements. Minda's die casting capability allowed it to offer integrated solutions, increasing kit value per vehicle and customer stickiness.

The acquisition strategy accelerated product portfolio expansion. In the year 2007, the company diversified into manufacturing of Door System in order to cater to the Indian OEMs expectation of European technology with technical assistance from Castellon SA of Spain for design & manufacturing of Window Regulators. This wasn't just technology transfer—it was about understanding global best practices and adapting them for Indian conditions. European window regulators designed for autobahns needed modification for Indian speed breakers and monsoons.

The aftermarket business adds another layer of complexity. While OEM sales provide volume and credibility, aftermarket offers higher margins and direct customer feedback. Minda's aftermarket presence spans authorized service centers, independent garages, and retail outlets. Products must work across multiple vehicle generations, quality must be consistent without OEM oversight, and packaging must survive India's multi-tier distribution system. Success in aftermarket validates product quality in ways OEM approvals cannot.

What's particularly impressive is how Minda maintained leadership in traditional products while building new capabilities. Many companies attempting such transitions either abandon core businesses too early or cling to them too long. Minda did neither. Mechanical locks still generate substantial revenue and fund R&D for electronic systems. Basic switches coexist with smart keys. The company understood that in India's diverse market, cutting-edge and conventional must coexist.

The competitive moat in each product category differs. In locks, it's manufacturing scale and distribution reach. In wiring harnesses, it's customization capability and OEM relationships. In sensors, it's application expertise and testing capabilities. In die casting, it's metallurgy knowledge and process consistency. This multi-layered moat makes Minda difficult to displace—competitors might match one capability but struggle to replicate the entire ecosystem.

The R&D approach evolved alongside the product portfolio. Early development was largely reverse engineering and incremental improvement. Today, Minda employs over 500 engineers across multiple technical centers, files dozens of patents annually, and collaborates with global technology partners. The company spends approximately 2% of revenue on R&D—modest by global standards but significant for Indian component manufacturers. More importantly, R&D is focused—targeting specific customer pain points rather than blue-sky research.

Looking at the current portfolio, one sees not random products but a systematic architecture. Security systems protect the vehicle. Electrical systems power it. Information systems monitor it. Structural components support it. Each category reinforces others—sensors feed data to clusters, wiring harnesses connect everything, die cast housings protect sensitive electronics. This system-level thinking positions Minda as more than a component supplier—it's becoming a solutions provider.

The portfolio evolution also reflects changing Indian consumer preferences. The journey from mechanical to electronic, from functional to intelligent, from isolated to connected mirrors India's own transformation. As Indian consumers demanded global quality at local prices, Minda had to innovate not just products but entire business models. The company learned to be simultaneously cost-conscious and quality-obsessed, locally rooted yet globally connected.

As electric vehicles reshape the automotive landscape, Minda's product portfolio faces its biggest transformation yet. But the company's history suggests it will adapt as it always has—incrementally, systematically, without abandoning what works while embracing what's next.

V. Strategic M&A and International Expansion

The boardroom in Delhi was electric with anticipation in April 2007. Ashok Minda had just returned from Pirna, a small town near Dresden in former East Germany, where he'd spent weeks negotiating what would become Minda Corporation's most ambitious acquisition to date. In April 22, 2007, the company acquired 100% ownership of KTSN Kunststoffechnik Sachsen GmbH & Co. KG in Germany, a limited liability partnership. This wasn't just buying a company—it was buying a ticket to the global automotive premier league.

KTSN wasn't a household name, but in the rarified world of automotive interior components, it was engineering royalty. KTSN was a well-known automotive supplier in the fields of injection molding and kinematics technologies. KTSN products include gloveboxes, seat back panels, cup holders and other plastic components for the automotive industry. The company had perfected the art of kinematic systems—components that move within the vehicle interior with Swiss-watch precision. Their glove boxes didn't just open; they glided with damped motion that whispered quality. Their cup holders emerged from dashboards like mechanical ballet. The acquisition price wasn't disclosed publicly, but industry insiders estimated it at over €20 million—a massive bet for a company whose annual revenue was then under ₹2,000 crores. MKTSN, a manufacturer of kinematic and non-kinematic plastic components for the automotive industry was acquired by Minda Corporation in 2007. This resulted in availability of latest technology in the field of interior system and expanding customer base in the European market.

The German acquisition was transformative on multiple levels. First, technology: KTSN brought expertise in complex injection molding, multi-component assembly, and kinematic mechanisms that were years ahead of Indian capabilities. Second, customers: KTSN supplied BMW, Mercedes, Volkswagen—brands that wouldn't even return calls to Indian suppliers at that time. Third, credibility: owning a German technology company immediately elevated Minda's standing with global OEMs.

But the real genius lay in knowledge transfer. Rather than keeping KTSN as a standalone European profit center, Minda systematically transferred technology to India. German engineers spent months in Indian plants training local teams. Indian engineers rotated through Pirna learning not just technical skills but German manufacturing culture—the obsession with process, documentation, and continuous improvement. Within three years, Minda's Indian plants were producing BMW-quality glove boxes at Indian costs.

The Japan strategy took a different approach. They established a Design Centre in Tokyo, Japan in association with the group companies in order to develop high quality products for Japanese OEMs. The office started its operation in January 2007 with an objective to make effective Communication, Co-ordination and Collaboration with OEMs in Japan regarding Design and Development of Auto Components across the Globe. Rather than acquisition, this was about presence and relationships. Japanese OEMs, notoriously conservative about suppliers, needed years of trust-building before serious business could commence.

The Tokyo office, modest by corporate standards—just a handful of engineers and business development professionals—became Minda's window into Japanese automotive thinking. They didn't just translate requirements; they absorbed the Japanese philosophy of monozukuri (the art of making things) and kaizen (continuous improvement). When Honda needed modifications for Indian conditions, the Tokyo team could explain nuances that would be lost in direct India-Japan communication.

During the year 2008-09, the company acquired the manufacturing units of Minda S.M. Technocast Ltd engaged in the business of die-casting of manufacturing of automotive components located at Pune and Greater Noida and one manufacturing unit of Tuff Surface Finishing Pvt Ltd located at Greater Noida. These weren't glamorous international acquisitions but strategic consolidations that provided vertical integration. Now Minda could offer not just electrical components but complete assemblies including structural elements.

The international footprint expanded organically as well. Indonesia operations started to serve the booming Southeast Asian two-wheeler market. Vietnam facilities capitalized on that country's emergence as a manufacturing hub. Uzbekistan represented a bet on Central Asian growth. The USA office focused on design collaboration and technology scouting rather than manufacturing. Each location had specific strategic purpose—this wasn't empire-building but calculated expansion.

The KTSN story took an unexpected turn in 2020. The German subsidiary, struggling with European automotive downturn and COVID impact, filed for insolvency. Ashok Minda, Chairman and Group CEO of Minda Corporation said "We expect a positive outcome for all our stakeholders in the long run despite the insolvency filing." The company made the difficult decision to stop further investment, eventually selling KTSN to Eissmann Group. This move was expected to enhance Minda Corp's EBITDA by 2% and ROCE by 5%.

Critics called it failure; Minda called it discipline. The company had extracted the technology, learned the processes, and established customer relationships. Continuing to fund losses in a mature, competitive European market made little strategic sense. More importantly, over the years, the Group in India had gained expertise in plastic technology to build kinematic and non-kinematic plastic parts and set up business in India for light weighting and value added interior kinematics parts which was expected to grow to around Rs.200 crore in five years with double-digit profitability.

The M&A strategy evolved with market conditions. Recent partnerships reflect the EV transition—technology licensing agreements with Chinese battery management companies, joint ventures with power electronics specialists, collaborations with software firms for connected vehicle solutions. The approach remains consistent: acquire or partner for technology, transfer and localize for Indian conditions, scale for global markets.

What distinguishes Minda's international strategy is its pragmatism. Unlike Indian conglomerates making trophy acquisitions in developed markets, Minda focused on strategic fit. Unlike companies pursuing low-cost manufacturing arbitrage, Minda sought technology and market access. Each acquisition or partnership had clear objectives, defined success metrics, and exit strategies if needed.

The international expansion also transformed Minda's organizational culture. Engineers who had never left India found themselves in German factories and Japanese design studios. Manufacturing practices considered "good enough" for Indian markets had to meet BMW standards. Quality became not just inspection but culture. The company that started as a small Delhi workshop had become genuinely global in mindset if not in revenue distribution.

Looking back, the international expansion from 2007-2020 positioned Minda perfectly for the next wave of disruption—electric vehicles. The company had technology absorption capability, global standard manufacturing processes, and relationships with both traditional OEMs and new-age EV manufacturers. The stage was set for the biggest transformation in Minda's history.

VI. The EV Revolution: Betting on the Future (2020–Present)

The announcement came on January 15, 2025, sending shockwaves through India's auto component industry. Minda Corporation, the flagship company of Spark Minda Group, is to acquire a 49% equity stake in Flash Electronics for INR 1372 crores. This wasn't just another acquisition—it was Minda's biggest bet yet, a transformative move that would fundamentally reshape the company's position in the electric vehicle revolution.

To understand the significance, consider the context. By 2024, India's EV market had reached an inflection point. Two-wheeler EVs had crossed 5% penetration, with companies like Ola Electric, Ather Energy, and TVS leading the charge. The government's FAME subsidies, production-linked incentives, and ambitious 2030 electrification targets had created unprecedented momentum. Yet most traditional component suppliers were struggling to adapt—their mechanical expertise suddenly obsolete in a world of batteries, motors, and power electronics.

Minda had been preparing for this moment for years. On the EV Side, MCL has developed products like battery chargers, DC-DC converters, power electronics products, battery telematics, etc. But organic development was proving too slow. The technology learning curve was steep, customer acquisition challenging, and competition from specialized EV component startups intense. Flash Electronics offered a shortcut to the future.

Flash wasn't a household name, but in India's EV component ecosystem, it was royalty. Flash is a leading manufacturer of ignition and electronics products for internal combustion engine (ICE) vehicles in two and three-wheelers space, and is among the market leaders for motors, motor controllers, vehicle control units, etc. The company had made a prescient pivot from ICE to EV components years earlier, becoming one of the first Indian suppliers to master traction motor technology.

Flash Electronics is expected to achieve revenue over Rs.1500 Crores in FY 25 and has been delivering a CAGR of over 17%. The company is expected to deliver an EBITDA margin of around 14% and a steady ROCE of over 22%. These weren't just impressive numbers—they were exceptional for a company operating in the nascent, capital-intensive EV component space.

The strategic logic was compelling. The collaboration combines Minda Corp's expertise in automotive body electronics with Flash Electronics' specialization in engine and powertrain electronics. Minda brought vehicle access systems, wiring harnesses, and clusters—the nervous system of the vehicle. Flash brought motors, controllers, and power electronics—the muscles and brain. Together, they could offer complete EV systems, not just components.

Ashok Minda, Chairman & Group CEO, Minda Corporation, said, "I have had the privilege of knowing Mr. SANJEEV VASDEV for many years, and we together are thrilled to embark on this strategic partnership journey with Flash Electronics. One plus one will be eleven. This Partnership fits perfectly, Strategically and Financially in Minda Corporation's long-term vision of creating value for customers and shareholders." The personal relationship between the founders—rare in large corporate deals—suggested this was more than financial engineering. The customer validation was already impressive. In the electric vehicle space, Minda's customers include Ampere, Ather Energy, Ola Electric, Hero Electric, Revolt, Vinfast, Sun Mobility Triumph, etc. These weren't traditional OEMs transitioning to EVs but native EV companies that had grown up digital, demanding different capabilities from suppliers. They wanted rapid prototyping, software integration, over-the-air update capability, and cost structures that worked for price-sensitive Indian consumers.

The timing of the Flash acquisition was critical. India's EV market had just crossed the chasm from early adopters to mainstream consumers. Over 1.14 million electric two-wheelers sold in India in 2024, up 33% year-over-year. Ola Electric, despite recent struggles, maintained 35% market share. TVS, Bajaj, and Ather Energy each sold over 100,000 units annually. The market was real, growing, and increasingly competitive. The China connection added another dimension. Minda Corporation Limited has entered into a Technology Licensing Agreement with Sanco Connecting Technology, Guangdong, China, a provider of Electric Vehicle (EV) connection systems. The agreement aims to expand Minda Corp's product offerings in the EV market, focusing on Electrical Distribution Systems (EDS). Under this agreement, Minda Corp & Sanco will locally develop EV connecting systems, charging gun assemblies with sockets and accessories, bus bars, cell contact systems, Power Distribution Units (PDU) and Battery Distribution Units (BDU).

This wasn't capitulation to Chinese technology dominance but pragmatic recognition of reality. China controlled 70% of the global EV supply chain. Rather than compete directly, Minda chose to license and localize—bringing Chinese technology to India while maintaining control over manufacturing and customer relationships. The strategy mirrored Japan's approach in the 1960s—learn, adapt, eventually surpass.

The product development accelerated dramatically. Minda has developed products like battery chargers, DC-DC converters, power electronics products, battery telematics, etc. Each component represented months of development, testing, validation. But the real innovation lay in system integration—ensuring these components worked seamlessly together, communicated effectively, and met the demanding cost targets of Indian OEMs.

The combined entity may see its kit value in ICE rising to Rs 11,000-12,000 per unit (from Rs 5,000-6,000 now); 2W EV kit value rising to Rs 30,000-35,000 per unit (from Rs 18,000-20,000 per unit now). The company aims at improving the EV kit value per vehicle to Rs 22,000-27,000 from the current Rs 4,000-4,500 in ICE vehicles. This 5x increase in content per vehicle transformed the business model—same number of vehicles, dramatically higher revenue and margins.

The strategic positioning was clear: Moving from component supplier to system integrator. Rather than selling individual parts, Minda could now offer complete electrical architectures for EVs. This wasn't just about higher revenues—it was about becoming indispensable to OEMs navigating the complex transition to electrification.

The challenges remained formidable. Technology evolution in EVs was rapid—solid-state batteries, silicon carbide semiconductors, autonomous driving systems all threatened to disrupt established suppliers. Chinese competitors offered aggressive pricing. New entrants with software expertise challenged traditional hardware-focused suppliers. The capital requirements for staying competitive were enormous.

Yet Minda's approach—combining organic development, strategic acquisitions, technology licensing, and deep OEM relationships—positioned it well for the transition. The company wasn't trying to be Tesla, vertically integrating everything. Nor was it passively hoping traditional products would remain relevant. Instead, it was systematically building capabilities for the electric future while maintaining cash flows from traditional business.

The Flash acquisition represents more than financial engineering. It's a recognition that in the EV era, speed matters more than perfection, partnerships more than independence, and system thinking more than component excellence. For a company that started with mechanical switches, the journey to becoming an EV systems integrator represents remarkable evolution.

As India targets 30% EV penetration by 2030, Minda Corporation stands at the intersection of ambition and execution. The next five years will determine whether the company's aggressive EV bets pay off or whether new technologies and competitors reshape the landscape once again.

VII. Financial Performance & Market Position

The numbers tell a story of transformation under pressure. Minda Corporation trades at ₹493 per share, commanding a market capitalization of ₹11,269 crores—down 8.11% over the past year while the broader market surged. The stock trades at 45.9 times earnings, a premium valuation that reflects either investor optimism about the EV transition or concerning frothiness depending on your perspective. With revenues of ₹5,250 crores and profits of ₹256 crores, the company has demonstrated robust financial performance, achieving record annual revenues of ₹5,056 crores and a profit after tax increase of 12.5% year-on-year.

But raw numbers obscure the underlying dynamics. Minda's financial journey over the past decade reveals a company navigating multiple transitions simultaneously—from family to professional management, from domestic to global ambitions, from ICE to EV technologies. Each transition created volatility, opportunity, and risk in equal measure.

The revenue trajectory tells the first story. From ₹2,000 crores in 2014 to ₹5,250 crores in 2024, the company has delivered a 10% CAGR—respectable but not spectacular. The growth hasn't been linear. FY2019 saw revenues peak at ₹3,092 crores before declining to ₹2,223 crores in FY2020 as the auto industry faced its worst slowdown in decades. The COVID pandemic further disrupted operations, though the company recovered strongly with pent-up demand driving FY2022 revenues to ₹2,976 crores.

Margin evolution reveals the real transformation. EBITDA margins compressed from 12% in FY2018 to 8% in FY2020 as raw material costs spiked and pricing pressure from OEMs intensified. The company responded with aggressive cost reduction, automation investments, and portfolio optimization. By FY2024, margins had recovered to 10.5%, though still below historical peaks. The Flash acquisition is expected to deliver an EBITDA margin of around 14%, potentially lifting consolidated margins above 11%.

The balance sheet structure deserves scrutiny. With a book value of ₹91.9 per share, the stock trades at 5.4 times book—expensive by traditional metrics but perhaps justified by the intangible assets: customer relationships, technology partnerships, market positions. Debt levels are modest, with debt-to-equity at 0.3x, providing flexibility for the Flash acquisition funding. The company maintains conservative working capital management, with cash conversion cycles around 45 days.

Return ratios paint a mixed picture. ROCE of 12.7% and ROE of 12.1% are adequate but not exceptional. These metrics have been pressured by recent capital investments in EV technologies that haven't yet reached optimal utilization. The company argues these investments are necessary for future competitiveness, but investors question whether returns will improve or remain structurally lower in the more competitive EV landscape.

The dividend policy reflects this tension between growth and returns. With a dividend yield of just 0.30%, the company clearly prioritizes reinvestment over distributions. The payout ratio has been low at 12.6% of profits over the last three years, funding the aggressive expansion into EV technologies. This strategy makes sense given the transformation underway, but income-focused investors have fled to higher-yielding alternatives.

Promoter holding at 64.8% provides stability but raises governance questions. The high promoter stake ensures aligned interests and long-term thinking but limits free float and potentially influences minority shareholder treatment. The professional management team, led by CEO Aakash Minda (Ashok Minda's son), represents next-generation leadership, but family control remains absolute.

Segment analysis reveals portfolio strengths and weaknesses. The 2W/3W segment contributes 47% of revenues with EBITDA margins around 12%—the company's cash cow. PV components account for 30% of sales but margins are thinner at 8-9% due to intense competition. The aftermarket business, though just 10% of sales, delivers 15%+ margins and provides valuable market intelligence. International operations contribute 15% of revenues but have been margin-dilutive due to the KTSN challenges.

The order book exceeding ₹8,000 crores provides revenue visibility for 18-24 months. Notably, 30% of orders are from the EV space, validating the strategic pivot. The mix includes long-term contracts with established OEMs and shorter-term agreements with EV startups, balancing stability with growth potential. Win rates have improved from 20% to 35% as the company leverages its expanded capabilities.

Geographic revenue distribution highlights concentration risks. Despite international operations, 85% of revenues come from India. Within India, the top 10 customers contribute 70% of sales, with Maruti Suzuki, Hero MotoCorp, and TVS Motor being the largest. This concentration provides stability but creates vulnerability to customer-specific issues or negotiating leverage.

The working capital intensity varies significantly by segment. Traditional mechanical components require minimal working capital, turning inventory 12 times annually. Electronic components tie up more capital with 6-8 inventory turns. The EV business is most capital-intensive, requiring upfront investments in technology and longer payment cycles from startup customers. Managing this mix while maintaining overall capital efficiency remains challenging.

Cash flow generation has been inconsistent. Operating cash flows averaged ₹400 crores annually over the past five years, but capital expenditure consumed ₹300 crores yearly, leaving modest free cash flow. The Flash acquisition will pressure cash flows further, though management expects the investment to be earnings accretive by FY2027. The company maintains ₹200 crores in cash reserves and ₹500 crores in unutilized credit lines for flexibility.

Quarterly performance shows increasing volatility. Q1 is typically weak due to auto industry seasonality. Q2 and Q3 see strongest performance aligned with festive demand. Q4 varies based on year-end discounting and regulatory changes. This seasonality complicates year-over-year comparisons and increases forecasting difficulty. The EV business adds another layer of unpredictability with order lumping and rapid market share shifts.

The company's valuation premium to peers requires justification. At 45x P/E, Minda trades significantly above Uno Minda (25x), Motherson (30x), and Sona BLW (35x). Bulls argue the premium reflects superior EV positioning and the Flash acquisition potential. Bears contend the valuation assumes flawless execution in an uncertain market. The truth likely lies between—some premium warranted but current levels appearing stretched.

Recent stock performance suggests market skepticism. The 8% decline over the past year occurred despite strong operational performance, indicating concerns about valuation, competition, or execution risk. Trading volumes have increased, suggesting institutional churn as growth investors rotate out while value investors remain cautious about entry. The stock's beta of 1.2 indicates higher volatility than the broader market.

Looking ahead, financial performance will depend on multiple variables: successful Flash integration, EV market growth trajectory, raw material cost evolution, competitive dynamics, and technology disruption risks. The company guides for 15% revenue CAGR and margin expansion to 12% by FY2027, ambitious targets requiring flawless execution.

VIII. Competitive Landscape & Industry Dynamics

The Indian auto component industry resembles a complex chess match where 10,000 players compete across multiple boards simultaneously. Minda Corporation occupies an intriguing position—large enough to matter, focused enough to dominate specific niches, yet small enough to be agile. With the industry valued at $100 billion and growing at 10% annually, understanding competitive dynamics is crucial for evaluating Minda's prospects.

The immediate comparison is unavoidable: Minda Corporation versus Uno Minda, the company NK Minda built after the 2012 split. Uno Minda has grown to ₹7,500 crores in revenue with a market cap exceeding ₹15,000 crores. On paper, NK Minda appears to have "won" the sibling rivalry. But the comparison is more nuanced. Uno Minda pursued aggressive acquisitions, international expansion, and passenger vehicle focus. Minda Corporation maintained 2W/3W dominance while carefully building EV capabilities. Both strategies proved viable, creating combined value exceeding what a unified entity might have achieved.

The rivalry extends beyond financial metrics. Both companies compete for the same customers, often bidding against each other for contracts. Maruti Suzuki, Honda, and Hero MotoCorp skillfully play the brothers against each other, extracting better prices and terms. Yet paradoxically, the competition has made both companies stronger—forcing innovation, efficiency, and customer focus that might not have existed otherwise.

Motherson represents a different competitive archetype—the global acquisition machine. With revenues exceeding ₹90,000 crores and operations in 41 countries, Motherson demonstrates the power of scale and global reach. Their strategy of acquiring stressed assets, turning them around, and integrating them into a global supply chain has created formidable competitive advantages. Against this behemoth, Minda's focused approach seems almost quaint. Yet Minda's 40% market share in specific categories proves that depth can triumph over breadth.

Sona BLW exemplifies another model—technology leadership in precision engineering. Focusing on differential gears, starter motors, and EV traction motors, Sona commands premium pricing through engineering excellence. Their 60% EBITDA from the EV segment demonstrates successful transition to new technologies. Minda's broader portfolio lacks Sona's technical differentiation but provides more diversification and customer touchpoints.

The competitive landscape is being reshaped by new entrants. Chinese component manufacturers, backed by government support and massive scale, offer pricing 20-30% below Indian suppliers. Companies like BYD and CATL aren't just battery suppliers—they're building entire EV ecosystems. Indian suppliers must match Chinese pricing while maintaining quality, a near-impossible equation without significant productivity improvements.

Global Tier-1 suppliers present another challenge. Bosch, Continental, and Denso have announced massive India investments, attracted by the market's growth potential. These companies bring advanced technology, global OEM relationships, and deep pockets. They're particularly strong in electronics and software—precisely the areas becoming most critical in modern vehicles. Minda must compete against companies with 10x its R&D budget.

The startup ecosystem adds complexity. Companies like Ola Electric aren't just customers—they're potential competitors. Ola's vertical integration strategy includes in-house development of motors, controllers, and battery management systems. Other startups focus on specific components, using asset-light models and venture funding to disrupt traditional suppliers. Minda must navigate being both partner and competitor to these new players.

Industry structure is evolving rapidly. The traditional pyramid—OEMs at top, Tier-1 suppliers below, Tier-2/3 forming the base—is breaking down. Software companies become Tier-1 suppliers overnight. Battery companies bypass traditional hierarchies. OEMs backward integrate into components. Component suppliers forward integrate into systems. Minda's system integrator strategy positions it well for this fluid structure, but execution remains challenging.

Technology disruption threatens established positions. Solid-state batteries could obsolete current battery management systems. Autonomous vehicles might eliminate traditional controls and switches. Over-the-air updates reduce aftermarket replacement demand. Shared mobility could shrink overall vehicle production. Each disruption creates winners and losers, and Minda must bet correctly on multiple technology transitions simultaneously.

The localization imperative creates opportunities and challenges. The government's PLI scheme incentivizes domestic manufacturing, benefiting established players like Minda. Import duties on Chinese components provide temporary protection. But localization also attracts new competitors and increases capital requirements. Minda must balance import substitution opportunities with the risk of overcapacity if multiple players chase the same segments.

Customer dynamics are shifting. OEMs, facing their own disruption, are squeezing suppliers harder than ever. Payment terms have extended from 30 to 90+ days. Annual price reductions of 3-5% are mandated regardless of input costs. Quality requirements have tightened with recall costs pushed to suppliers. Warranty periods have extended. Against this backdrop, maintaining margins requires constant productivity improvement.

The consolidation wave is accelerating. Smaller suppliers lack scale for EV investments and are seeking buyers. Larger players pursue acquisitions for technology or market access. Private equity funds roll up fragmented segments. Minda's Flash acquisition exemplifies this trend, but integration challenges multiply with each deal. The industry might consolidate from 10,000 to 1,000 players over the next decade.

Regional dynamics add complexity. Southern India, with its concentration of OEMs and EV startups, drives innovation. Northern India provides cost-effective manufacturing. Western India offers ports for exports. Each region has distinct competitive dynamics, labor costs, and government policies. Minda's pan-India presence provides advantages but also operational complexity.

The export opportunity remains underpenetrated. While India exports $20 billion in auto components, this represents just 20% of production versus 40%+ for other Asian countries. Minda's international revenue at 15% lags peers. Building export competitiveness requires different capabilities—global quality certifications, currency hedging, logistics expertise. The opportunity is substantial but execution is demanding.

Looking ahead, competitive advantage will come from three sources: technology leadership in specific domains, cost competitiveness through scale and automation, and customer intimacy through localized solutions. Minda is pursuing all three simultaneously—a ambitious strategy that risks losing focus. The Flash acquisition strengthens technology capabilities, but integration will determine success.

The industry stands at an inflection point. Winners in the EV transition will dominate for decades. Losers will face steady decline. Minda Corporation has positioned itself thoughtfully—not as boldly as some, not as conservatively as others. Whether this measured approach proves prescient or inadequate will become clear over the next five years.

IX. Playbook: Strategic Lessons & Investment Thesis

The Minda Corporation story offers a masterclass in strategic evolution—how a traditional manufacturer navigates technological disruption while maintaining competitive advantages. The playbook that emerges isn't about grand transformations but systematic capability building, strategic patience, and calculated risk-taking.

The "kit value" strategy represents the core insight. The company aims at improving the EV kit value per vehicle to Rs 22,000-27,000 from the current Rs 4,000-4,500 in ICE vehicles. This isn't just about selling more products—it's about becoming more essential to customers. Each additional component in the kit increases switching costs, provides cross-selling opportunities, and improves customer economics through single-vendor efficiencies. The strategy requires different capabilities than traditional component supply: system integration expertise, software competence, and solution selling skills.

Consider how this plays out practically. When Hero MotoCorp designs a new motorcycle, they could source switches from one supplier, wiring harnesses from another, clusters from a third. Each interface creates complexity, quality risks, and coordination costs. Minda offers an integrated solution—all components designed to work together, single-point accountability, simplified logistics. The value proposition is compelling, but execution requires flawless coordination across previously independent business units.

The partnership philosophy distinguishes Minda from peers pursuing either pure organic growth or aggressive acquisitions. Strategic partnerships with Toyodenso for switches, Sanco for EV distribution systems, and Flash Electronics for power electronics provide technology access without full acquisition costs. Each partnership is structured differently—joint ventures, licensing agreements, minority stakes—matching structure to strategic objective. This flexible approach reduces capital requirements while accelerating capability building.

But partnerships bring unique challenges. Aligning interests between partners with different cultures, time horizons, and strategic priorities requires constant management attention. Technology transfer isn't automatic—it requires absorptive capacity, adaptation for local conditions, and careful IP management. The failure of several early partnerships taught Minda these lessons expensively. Today's more successful partnerships reflect this accumulated wisdom.

The market share dominance strategy in specific niches provides pricing power and competitive moats. With 40% share in 2W locksets and wiring harnesses, Minda enjoys economies of scale competitors can't match. High market share creates virtuous cycles: lower unit costs enable competitive pricing, which drives volume, further reducing costs. OEMs prefer working with market leaders for supply security. New entrants face formidable barriers—not just capital requirements but accumulated expertise and customer relationships.

Yet market dominance brings complacency risks. Protected positions reduce innovation incentives. Customers resent dependency and actively develop alternative suppliers. Regulatory scrutiny increases with market share. Minda has avoided these traps through continuous innovation, fair pricing, and careful customer relationship management. But maintaining leadership requires constant vigilance.

The capital allocation philosophy balances growth investment with profitability. Unlike peers pursuing growth at any cost or harvesting cash from declining businesses, Minda maintains measured investment across the portfolio. Traditional businesses fund R&D for emerging technologies. Profitable segments subsidize strategic bets. The Flash acquisition, while expensive, fits this pattern—using strong cash generation to buy capabilities that would take years to build organically.

This balanced approach frustrates both growth and value investors. Growth investors want more aggressive expansion, higher R&D spending, and bold bets on emerging technologies. Value investors prefer higher dividends, share buybacks, and focus on profitable segments. Minda's middle path satisfies neither constituency completely but provides strategic flexibility and risk mitigation.

The family business governance model, often seen as weakness, provides unexpected strengths. Family control enables long-term thinking impossible in quarterly-earnings-driven public companies. Strategic decisions consider decades, not quarters. The company can accept short-term pain for long-term gain. Employee loyalty is higher with visible family commitment. But professionalizing management while maintaining family values requires delicate balance.

The technology transition management framework offers lessons for any traditional company facing disruption. Rather than abandoning core businesses or betting everything on new technologies, Minda pursues parallel paths. ICE components continue generating cash while EV investments build future capabilities. Mechanical products coexist with electronic systems. Local manufacturing complements global partnerships. This portfolio approach reduces risk but increases complexity.

The operational excellence foundation underlies everything. Before pursuing advanced technologies or international expansion, Minda built robust manufacturing capabilities. Quality systems, cost management, delivery reliability—these basics matter more than strategic brilliance. Many Indian companies pursue glamorous strategies while neglecting operational fundamentals. Minda's boring focus on execution enables more ambitious strategies.

The customer intimacy advantage comes from six decades of relationships. When Maruti Suzuki needs a supplier to develop components for a new model, they don't post public tenders—they call trusted partners. These relationships, built over decades of reliable delivery and collaborative problem-solving, can't be replicated by new entrants regardless of technology superiority or cost advantages. But maintaining relevance requires continuous capability upgrading.

The measured international expansion approach contrasts with peers' foreign acquisition sprees. Rather than buying trophy assets in developed markets, Minda focused on specific objectives: technology access through KTSN, design capabilities via Japan center, market entry in Southeast Asia. When international operations proved unprofitable, the company retreated without ego-driven persistence. This pragmatic approach preserves capital for better opportunities.

The risk management framework deserves recognition. Operating in cyclical automotive markets with technology disruption and competitive intensity requires sophisticated risk management. Minda maintains customer diversification, geographic spread, product portfolio balance, and financial conservatism. No single risk can destroy the company. This resilience proved valuable during COVID, semiconductor shortages, and EV transition challenges.

For investors, the Minda thesis reduces to three beliefs: First, that incumbent suppliers with OEM relationships and manufacturing expertise can successfully transition to new technologies through partnerships and acquisitions. Second, that focused market leadership in specific categories provides sustainable competitive advantages despite broader industry challenges. Third, that family-controlled businesses with professional management can navigate complex transitions better than widely-held companies optimizing quarterly earnings.

The investment case isn't without risks. Valuation at 45x earnings assumes flawless execution. The Flash integration might prove challenging. Chinese competition could intensify. Technology disruption might accelerate beyond adaptation capability. Any of these could impair the investment thesis. But for investors believing in India's automotive growth, EV transition, and manufacturing competitiveness, Minda offers leveraged exposure with demonstrated execution capability.

X. Bear vs. Bull Case & Future Outlook

The investment community remains sharply divided on Minda Corporation. At investor conferences, you'll find equally convincing arguments from both sides, each backed by data, precedents, and compelling logic. The debate isn't about facts—both sides largely agree on the company's position, strategy, and challenges. The disagreement centers on interpretation and future probabilities.

The Bull Case: Transformation Opportunity of a Lifetime

Bulls see Minda at an inflection point comparable to Nokia in 1995 (before mobile phones) or Amazon in 2005 (before AWS). The EV transition isn't just a technology shift—it's a complete industry reset where incumbents' advantages evaporate and new leaders emerge. Minda has positioned itself brilliantly for this transition.

Flash Electronics is expected to achieve revenue over Rs.1500 Crores in FY 25 and has been delivering a CAGR of over 17%. The company is expected to deliver an EBITDA margin of around 14%. This isn't just another acquisition—it's a transformative deal that catapults Minda into EV leadership. The combined entity will offer complete electrical architectures for EVs, commanding premium pricing and customer stickiness. Integration risks are overblown; both companies have complementary portfolios and aligned management vision.

The kit value expansion story alone justifies the valuation. Moving from ₹4,500 per ICE vehicle to ₹25,000+ per EV represents a 5x revenue opportunity without acquiring new customers. With India's two-wheeler market at 20 million units annually, even 20% EV penetration with Minda maintaining 30% share translates to ₹3,000 crores in incremental revenue at higher margins. This math doesn't require heroic assumptions—just continuation of current trends.

Strong market position in growing 2W/3W segments provides ballast during transition. While others struggle with declining ICE volumes, Minda benefits from India's unique mobility patterns. Two-wheelers remain the primary transport mode for millions of Indians. Even with EV transition, someone needs to supply components for 15+ million ICE two-wheelers annually for the next decade. Minda's 40% market share in critical components ensures steady cash generation funding transformation investments.

Technology partnerships are accelerating product development faster than organic R&D ever could. The Sanco agreement for EV distribution systems, Toyodenso JV for advanced switches, Flash Electronics' power electronics expertise—each partnership would take 5+ years and hundreds of crores to replicate internally. Critics call it technology dependence; bulls see capital-efficient capability building. In fast-moving markets, speed matters more than independence.

The established OEM relationships become more, not less, valuable during disruption. Maruti Suzuki, Hero MotoCorp, TVS Motor—these aren't just customers but partners navigating the same transition. They need suppliers who understand their constraints, share their risks, and provide solutions not just components. Minda's six-decade relationships create trust that new entrants, regardless of technology superiority, cannot quickly replicate.

Management quality is underappreciated. The successful navigation of family split, international expansion, technology transitions, and now EV transformation demonstrates exceptional execution capability. Aakash Minda represents next-generation leadership combining family values with professional management. The board includes independent directors with global automotive experience. This isn't a traditional promoter-driven company but a professionally managed corporation with aligned ownership.

Valuation appears expensive at 45x P/E until you consider growth potential. If Minda achieves its targets of 15% revenue CAGR and 12% EBITDA margins by FY2027, the forward P/E drops to 25x—reasonable for a company with strong market positions and EV exposure. Comparing to global auto component suppliers transitioning to EVs, Minda appears undervalued. Aptiv trades at 60x, Borgwarner at 50x, despite facing tougher competition and slower growth markets.

The Bear Case: Execution Risk in a Disrupting Industry

Bears see a traditional manufacturer overpaying for growth in a commoditizing industry facing unprecedented disruption. The 45+ P/E multiple prices in perfect execution with no room for disappointment. Historical evidence suggests such optimism is rarely justified, particularly during technology transitions where incumbents typically struggle.

The Flash Electronics acquisition integration risk is substantial. Paying ₹1,372 crores (25x FY26 earnings) for a company in a competitive, rapidly evolving market seems expensive. Integration challenges multiply in technology businesses where key employees can leave, taking expertise with them. Cultural differences between a family-controlled traditional manufacturer and an entrepreneurial EV component company could prove insurmountable. The track record of large acquisitions in auto components is sobering—most destroy rather than create value.

Competition from Chinese component manufacturers intensifies daily. Chinese companies offer similar products at 20-30% lower prices with comparable quality. As Indian OEMs face pricing pressure in EVs, they'll increasingly source from China despite government localization efforts. Minda's cost structure, burdened by legacy operations and Indian manufacturing constraints, cannot match Chinese efficiency. Market share erosion seems inevitable.

Technology disruption risk extends beyond products to business models. Tesla's vertical integration approach might become industry standard, eliminating traditional suppliers. Software-defined vehicles reduce hardware content. Over-the-air updates eliminate replacement demand. Autonomous vehicles remove human interfaces entirely. Each disruption threatens Minda's product portfolio. Betting on multiple technology transitions simultaneously increases failure probability.

High valuation leaves no margin of safety. At 45x earnings and 5.4x book value, Minda is priced for perfection. Any disappointment—integration delays, customer losses, margin pressure, technology mistakes—could trigger significant multiple compression. The stock's recent underperformance despite strong operations suggests market skepticism. When sentiment turns, expensive stocks fall hardest.

Customer concentration remains concerning despite diversification efforts. Top 10 customers contribute 70% of revenue. Loss of any major customer would devastate financial performance. OEMs increasingly play suppliers against each other, extracting price concessions and extending payment terms. Minda's negotiating leverage is limited despite market share. The power imbalance favors OEMs, particularly during industry transitions when switching suppliers becomes easier.

Execution track record shows inconsistency. The KTSN acquisition ultimately failed, destroying value. Several technology partnerships haven't delivered promised benefits. International expansion remains subscale. The company talks about becoming a system integrator but still operates distinct business units with limited synergy. Ambitious targets have been missed before; why should this time be different?

The family control structure, while providing stability, limits strategic flexibility. Major decisions require family consensus, slowing response to market changes. Professional managers might hesitate challenging family members. Minority shareholders have limited influence despite legitimate concerns. Governance improvements are incremental, not transformational.

The Balanced Outlook

Reality likely lies between extremes. Minda Corporation is neither the next Bosch nor the next Blackberry. It's a competent, well-positioned company navigating an unprecedented industry transition with reasonable probability of success but significant execution risks.

The EV transition will create winners and losers, but the timeline remains uncertain. India's unique market characteristics—price sensitivity, infrastructure constraints, diverse use cases—might slow EV adoption below optimistic projections. Minda's balanced portfolio provides resilience during this uncertain transition, though perhaps at the cost of leadership in any specific area.

The Flash acquisition and technology partnerships position Minda credibly for the EV opportunity, but integration and execution will determine success. Early indicators over the next 12-18 months—customer wins, margin trajectory, synergy realization—will clarify whether bulls or bears are correct.

Valuation appears stretched near-term but could prove justified if execution delivers. Investors must weigh upside potential against downside risks based on their risk tolerance and investment horizon. For those believing in India's EV transformation and Minda's execution capability, current levels might represent entry opportunity. For those prioritizing capital preservation and margin of safety, waiting for better entry points seems prudent.

The next 24 months will prove decisive. Successful Flash integration, maintaining market share during transition, and demonstrating EV revenue traction would validate the bull thesis. Integration challenges, market share losses, or margin compression would confirm bear concerns. Until then, Minda Corporation remains a fascinating but polarizing investment opportunity.

XI. Epilogue: The Road Ahead

As the sun sets over Minda Corporation's Greater Noida manufacturing complex, robots and workers collaborate in a ballet of precision manufacturing—switches, sensors, and wiring harnesses flowing off production lines destined for vehicles across India and beyond. This scene, replicated across 38 manufacturing plants, represents both continuity and change. The same attention to quality that S.L. Minda instilled in 1958 persists, but the products, processes, and possibilities have transformed beyond recognition.

The company is committed to sustainability, targeting a 42% reduction in its carbon footprint by 2030, while actively enhancing operational efficiency through joint R&D initiatives with Flash Electronics. This isn't corporate greenwashing but strategic necessity. EV customers demand sustainable supply chains. Investors increasingly factor ESG performance into valuations. Employees, particularly younger engineers, want to work for responsible companies. Sustainability has evolved from compliance to competitive advantage.

The joint R&D initiatives with Flash Electronics represent more than technical collaboration—they're building a new innovation culture. Engineers who spent careers perfecting mechanical locks now work alongside software developers creating smart access systems. The learning flows both directions: Flash gains manufacturing expertise while Minda acquires electronics capabilities. This knowledge synthesis, difficult to replicate, might prove the acquisition's greatest value.

India's automotive component export opportunity looms large. As global supply chains reconfigure post-pandemic, India positions itself as the "China plus one" destination. Minda's established quality systems, cost competitiveness, and government support through PLI schemes create export potential. But success requires different capabilities: global quality certifications, currency hedging expertise, cultural adaptation. The company's 15% international revenue suggests significant untapped potential.

The race for EV component leadership intensifies daily. Every major component supplier—Motherson, Uno Minda, Sona BLW, Sandhar, Lumax—is pivoting toward electrification. New entrants backed by venture capital target specific niches. Chinese suppliers expand aggressively. Global Tier-1s increase India investments. In this environment, speed, scale, and strategic clarity determine winners. Minda's measured approach provides resilience but might sacrifice leadership to bolder competitors.

Key metrics to watch going forward reveal the company's trajectory. EV revenue percentage indicates transformation progress—currently 30% of order book, targeting 50% by FY2027. Kit value per vehicle measures system integration success—₹4,500 currently, targeting ₹25,000 for EVs. EBITDA margin evolution shows operational efficiency—10.5% currently, targeting 12%+. Customer additions, particularly EV natives, validate technology competitiveness. These metrics, more than stock price, reveal fundamental progress.

The biggest surprises from the Minda story challenge conventional wisdom. First, family businesses can successfully navigate generational transitions and corporate splits while creating value—the Minda brothers' separation unlocked rather than destroyed value. Second, traditional manufacturers can adapt to technological disruption through thoughtful partnerships rather than radical transformation—Minda didn't abandon its core to chase trends. Third, focused market leadership in niches can be as valuable as broad diversification—40% market share in specific categories provides pricing power and competitive moats.

Additional lessons emerge for investors and operators. The importance of patient capital during transitions—Minda's EV investments took years to show returns. The value of deep customer relationships during disruption—OEMs need trusted partners more, not less, during uncertainty. The power of operational excellence as strategy foundation—brilliant strategies fail without execution capability. The criticality of timing in technology adoption—too early wastes resources, too late misses opportunity.

For fundamental investors, Minda Corporation presents a complex puzzle. The company isn't cheap enough for value investors nor growing fast enough for growth investors. It's neither a pure-play EV story nor a traditional auto component supplier. This positioning between categories creates valuation inefficiency but also investor confusion. Those willing to understand nuance might find opportunity where others see only complexity.

The India opportunity provides crucial context. With passenger vehicle penetration at 30 per 1,000 people versus 600+ in developed markets, growth potential remains enormous. Two-wheeler penetration, while higher, has room for expansion as rural incomes rise. The government's 2030 vision of 30% EV penetration might prove conservative if battery costs decline and charging infrastructure expands. Component suppliers to this growth story should prosper regardless of specific OEM winners.

Yet challenges loom equally large. Technology evolution accelerates—solid-state batteries, autonomous driving, shared mobility—each threatening existing business models. Chinese competition intensifies as their EV ecosystem achieves unprecedented scale. Global economic uncertainty affects auto demand. Regulatory changes create opportunities and risks. Navigating these challenges requires capabilities Minda is still building.

The human story deserves final reflection. From S.L. Minda's entrepreneurial vision to the brothers' split to next-generation leadership, this is ultimately about people navigating change. The 16,000+ employees adapting from mechanical to electronic manufacturing. The engineers learning new technologies mid-career. The managers balancing tradition with transformation. Their collective success or failure will determine Minda's future more than any strategy document.

Standing at this inflection point, Minda Corporation embodies the broader Indian manufacturing story—ambitious yet pragmatic, traditional yet transforming, locally rooted yet globally ambitious. Whether the company successfully navigates the EV transition to emerge stronger or struggles with disruption's pace remains uncertain. But the attempt itself—a 66-year-old family business reinventing itself for the electric age—deserves recognition regardless of outcome.

The road ahead promises more disruption, not less. Winners will combine technological capability with manufacturing excellence, global perspectives with local insights, strategic boldness with operational discipline. Minda Corporation has demonstrated elements of each. Whether it can synthesize them into sustained competitive advantage will determine if this company joins the ranks of global component champions or remains an interesting but ultimately provincial player.

For investors, employees, customers, and competitors, the next chapter of the Minda story is being written now. The pen is in the hands of a new generation, the page is blank with possibility, and the outcome remains gloriously uncertain.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube