Metropolis Healthcare: The Diagnostic Empire That Changed Indian Healthcare

I. Introduction & Episode Roadmap

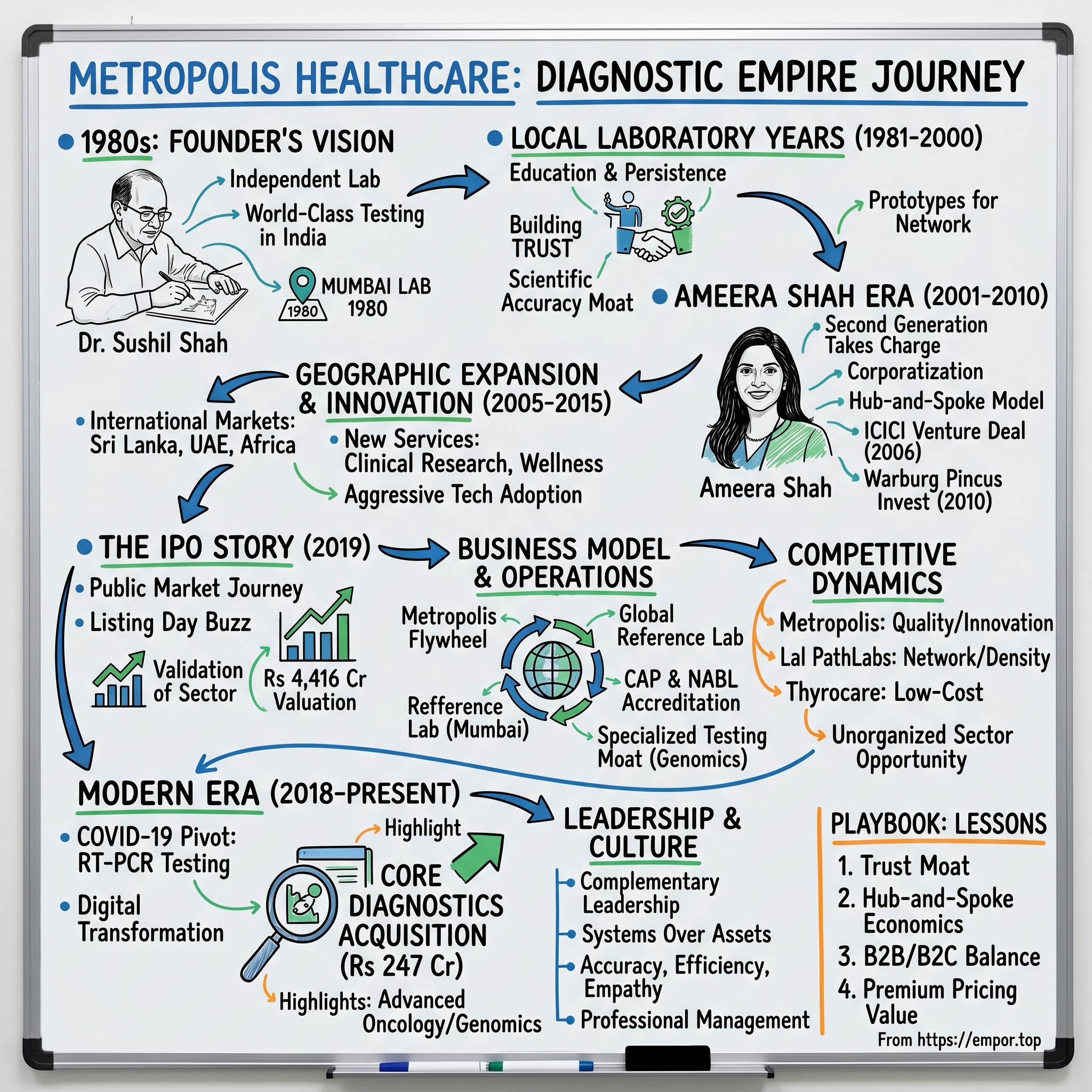

Picture this: It's 1980 in Mumbai, and while most pathologists are content running small labs attached to hospitals, Dr. Sushil Shah is sketching out something audacious—a professional diagnostic laboratory that would operate independently, serve multiple hospitals, and bring world-class testing to India. In an era when most blood tests required days of waiting and questionable accuracy, he imagined something that seemed almost fantastical: same-day results with international quality standards.

Fast forward to today, and that single Mumbai laboratory has transformed into Metropolis Healthcare—a Rs 10,356 crore diagnostic empire that processes over 30 million tests annually across 4,000+ centers. It's the second-largest diagnostic company in India and dominates Western and Southern markets with a presence that extends from Sri Lanka to Ghana. The company that started with one pathologist's vision now employs over 200 pathologists and 2,000 technicians, operating in a market that's grown from virtually nothing to Rs 596 billion.

But here's what makes this story particularly fascinating for investors and operators alike: Metropolis didn't just grow—it fundamentally transformed how Indians think about diagnostic testing. Before companies like Metropolis, getting a blood test meant navigating hospital bureaucracies, waiting in endless queues, and accepting whatever quality you got. The Shah family didn't just build a business; they professionalized an entire industry that was stuck in the dark ages of Indian healthcare.

This is a story of two generations—a father who brought scientific rigor to Indian diagnostics when nobody believed it was needed, and a daughter who transformed that scientific foundation into a corporate powerhouse. It's about building trust in an industry where trust is everything, scaling quality in a market that didn't value it, and creating a moat in what appears to be a commoditized business.

The narrative arc is almost Shakespearean in its scope: the scientist-entrepreneur who pioneers new techniques, the Harvard-educated daughter who takes over at 21 and transforms a doctor's practice into a corporate entity, the private equity players who bet big on Indian healthcare, and ultimately, the public markets that valued this diagnostic chain at over Rs 12,000 crores at its peak. Along the way, we'll explore how a company navigates the treacherous waters of Indian healthcare—from dealing with thousands of referring doctors to managing a hub-and-spoke model across diverse geographies, from fighting unorganized competitors who operate without quality standards to convincing insurance companies that preventive testing matters.

What we're about to unpack isn't just a business story—it's a masterclass in market creation, succession planning, and building defensibility in what many consider an undifferentiated service business. We'll examine how Metropolis built competitive advantages through trust and quality in a market where price seemed to be the only differentiator, how they managed the delicate transition from founder-led to professional management while keeping the family's vision intact, and what their journey tells us about the future of Indian healthcare.

The themes we'll explore transcend diagnostics: How do you professionalize a fragmented industry? Can quality be a sustainable moat in emerging markets? What happens when scientific excellence meets Indian jugaad? And perhaps most intriguingly—in a country where healthcare spending is just 3.5% of GDP compared to 17% in the US, what does Metropolis's journey tell us about the next decade of Indian healthcare?

We'll trace this journey from a single pathologist's lab in 1980s Mumbai through the competitive battles of the 2000s, the private equity boom of the 2010s, to the public markets debut in 2019 and beyond. We'll dissect the business model that generates 14.7% ROCE despite being asset-heavy, understand why the stock trades at 68x P/E despite single-digit revenue growth, and explore whether the recent Rs 247 crore acquisition of Core Diagnostics signals a new chapter or desperation for growth.

II. The Founder's Journey & Early Vision (1970s-1980)

The story begins not in a boardroom or venture capital pitch, but in the corridors of Grant Medical College in 1972, where a young Sushil Shah was completing his M.B.B.S. While his batchmates were eyeing lucrative clinical practices, Shah was drawn to something most considered a backwater specialty—pathology. By 1975, he had his M.D. in Pathology and Bacteriology, but what set him apart wasn't just his degrees—it was his obsession with bringing cutting-edge diagnostic techniques to India.

In 1978, Shah made a decision that would define his career trajectory. He secured a Research Fellowship at Cornell Medical Centre in New York, specializing in Endocrine Pathology. This wasn't just about adding another credential; Shah was studying Radio Immunoassay (RIA) techniques that were revolutionizing hormone testing globally but were virtually unknown in India. While Indian labs were still using basic chemical tests with accuracy rates that would make modern practitioners cringe, Shah was learning techniques that could detect hormone levels with unprecedented precision. Returning to Mumbai, Shah didn't immediately start his own lab. Instead, he strategically positioned himself at the intersection of clinical practice and pathology research. He secured department head positions at Mumbai's most prestigious hospitals—Breach Candy Hospital, Sir H.N. Hospital, Saifee Hospital, and Cumballa Hill Hospital. These weren't just job titles; they were laboratories for understanding what Indian healthcare needed but wasn't getting.

At Breach Candy Hospital in 1979, Shah witnessed a scene that would shape his entrepreneurial vision. A wealthy industrialist's wife needed hormone level testing for suspected thyroid issues. The blood sample had to be sent to a lab in Germany, results would take three weeks, and the cost was astronomical. Meanwhile, Shah knew he could perform the same test using RIA techniques that were "extremely sensitive to minute quantities" and deliver results in hours, not weeks. The disconnect between capability and availability was glaring.

Shah became India's pioneer in multiple diagnostic frontiers. He was the first to introduce Radio Immunoassay technique for hormone testing—a technology that could detect hormone levels with precision that traditional chemical tests couldn't match. When the HIV epidemic emerged in the 1980s, Shah was among the first in India to establish reliable HIV testing protocols. He also pioneered In-Vitro Fertilisation diagnostics, critical for the emerging IVF industry in India. These weren't just technical achievements; they were statements about what Indian diagnostics could become.

The decision to start Metropolis in 1980 (some sources cite 1981) wasn't driven by immediate commercial opportunity—the market barely existed. India's diagnostic industry in the early 1980s was a patchwork of hospital labs run by technicians with minimal quality control, small doctor-owned setups that served their own patients, and a handful of standalone labs with questionable standards. Most importantly, there was no concept of a "diagnostic brand"—patients went where their doctors sent them, no questions asked.

Shah's vision was radically different. He imagined independent diagnostic centers that would serve multiple hospitals and doctors, maintain international quality standards, and most crucially, build trust through scientific accuracy rather than personal relationships. In a market where a doctor's recommendation was everything, Shah was betting that quality could become its own recommendation.

The early Metropolis lab in Mumbai was less a business and more a mission. Shah insisted on protocols that seemed excessive for the Indian market—stringent quality controls, regular calibration of equipment, detailed documentation of every test. When competitors were delivering results on handwritten slips, Metropolis was producing typed reports with reference ranges and quality markers. The additional cost was significant, but Shah believed that credibility, once established, would be invaluable.

What's particularly interesting about Shah's approach was his dual focus on both ends of the diagnostic spectrum. While he was introducing cutting-edge techniques like RIA for specialized tests, he was simultaneously working to improve the accuracy of basic tests like complete blood counts and blood sugar levels—the bread and butter of diagnostic labs. This wasn't about choosing between premium and mass market; it was about elevating the entire industry's standards.

The entrepreneur-scientist duality defined Shah's early years. While building Metropolis, he maintained roles as Director at Dr. Reddy's Laboratories and Span Diagnostics, positions that gave him insights into the pharmaceutical industry's evolution and the medical devices market. These parallel tracks weren't distractions—they were intelligence-gathering operations that informed Metropolis's strategy. From Dr. Reddy's, he learned how Indian companies could match international quality standards. From Span Diagnostics, he understood the importance of technology in scaling healthcare delivery.

By 1985, five years into Metropolis's journey, the company had established something unprecedented in Indian diagnostics—a reputation that preceded doctor recommendations. Patients began asking their doctors to send samples to Metropolis, reversing the traditional power dynamic. The company wasn't just processing tests; it was setting standards that others would eventually have to match. But Shah knew that building a single excellent lab was just the beginning. The real challenge would be scaling quality across a geography as vast and diverse as India—a challenge that would require a different kind of leader.

III. Building the Foundation: The Local Laboratory Years (1981-2000)

The 1980s in Mumbai were a study in contrasts—gleaming skyscrapers rising next to sprawling slums, imported cars navigating streets filled with hand-pulled carts. In this environment, Dr. Sushil Shah's Metropolis occupied a peculiar position: a world-class diagnostic facility operating in a market that didn't yet understand why it needed world-class diagnostics. The real story of these two decades isn't about growth—it's about education, persistence, and laying foundations that wouldn't pay off for years.

Consider the typical patient journey in 1982 Mumbai. You'd visit your family doctor, who would scribble a prescription and maybe suggest a blood test. The test would happen at the hospital where you'd wait in line for hours, a technician would draw blood with questionable hygiene standards, and results would arrive days later—if at all. Accuracy? Nobody asked. Quality control? What was that? Into this ecosystem, Shah was trying to insert a professional diagnostic service that charged premium prices for something people didn't know they were missing: reliability.

The early challenges were almost comical in their fundamentality. Doctors needed to be convinced to refer patients to an external lab rather than their in-house facilities where they earned margins. "Why should I send my patient to you?" was the perpetual question. Shah's answer was simple but revolutionary for its time: "Because we'll make you look good." When Metropolis correctly diagnosed conditions that hospital labs missed, the referring doctor's reputation improved. It was a slow process, converting one doctor at a time, but each conversion was permanent.

The science-first approach manifested in ways that seemed obsessive to outsiders. While competitors stored blood samples in regular refrigerators, Shah invested in specialized cold storage with temperature monitoring. When others eyeballed chemical reagent quantities, Metropolis used precise measurement tools. The lab's standard operating procedures manual—a rarity in Indian diagnostics then—ran to hundreds of pages. Every deviation was documented, every error analyzed. This wasn't just quality control; it was building a culture where accuracy was non-negotiable.

A pivotal moment came in 1986 when a prominent Bollywood actor's mysterious illness stumped multiple hospitals. The family, desperate, brought blood samples to Metropolis. Shah's team identified a rare hormonal disorder that others had missed, enabling targeted treatment. The actor recovered, and word spread through Mumbai's elite circles. Suddenly, Metropolis wasn't just another lab—it was the lab that solved cases others couldn't. The brand was beginning to form, built not on advertising but on outcomes.

The competitive landscape of the late 1980s was peculiarly Indian. There were the hospital labs, which had captive customers but little incentive to improve quality. There were doctor-owned labs, which survived on personal relationships rather than technical excellence. And there were the "commercial labs"—often run by businessmen with no medical background, competing purely on price and turnaround time. Metropolis occupied a category of one: the scientific lab that operated like a business.

Shah's parallel roles during this period provided crucial strategic advantages. As Director at Dr. Reddy's Laboratories (one of India's pharmaceutical pioneers), he witnessed firsthand how Indian companies could match international standards in drug manufacturing. The key lesson: process discipline and documentation weren't Western luxuries but universal necessities. His position at Span Diagnostics exposed him to the latest diagnostic equipment and global trends in medical technology. While competitors were importing second-hand equipment, Shah knew exactly which cutting-edge machines would provide maximum advantage.

The 1990s brought India's economic liberalization, and with it, new challenges and opportunities. Suddenly, international diagnostic chains were eyeing the Indian market. Global equipment manufacturers were setting up offices. The comfortable, relationship-driven diagnostic industry was about to face its first real disruption. Shah's response was counterintuitive—instead of rapid expansion to grab market share, he focused on deepening capabilities in Mumbai.

Between 1991 and 1995, Metropolis introduced more new tests than in its entire first decade. Genetic testing, tumor markers, sophisticated hormone panels—capabilities that put it on par with leading international labs. The investment was massive relative to revenues, but Shah understood something his competitors didn't: in diagnostics, capability creates demand. Doctors who learned about new tests would find reasons to prescribe them. Patients who knew better testing existed would demand it.

The human capital strategy during these foundation years deserves special attention. While competitors hired lab technicians, Shah recruited pathologists. While others offered jobs, he offered careers. Young doctors joining Metropolis in the 1990s weren't just employees—they were apprentices learning from one of India's diagnostic pioneers. Many would later become department heads, others would start their own labs, but all carried forward the Metropolis emphasis on quality over quantity.

By 1995, Metropolis had achieved something remarkable yet invisible to casual observers. It had created a replicable model for high-quality diagnostics in India. The processes were documented, the training systems established, the quality benchmarks defined. What looked like a successful single lab was actually a prototype for a diagnostic network. But Shah, now in his 50s, recognized that scaling this prototype would require different skills—the ability to manage complexity, navigate corporate partnerships, and think in systems rather than procedures.

The late 1990s marked a subtle but crucial transition. Ameera Shah, Dr. Shah's daughter, began spending time at the lab during her college breaks. Harvard-bound and ambitious, she represented a generational shift in thinking. Where her father saw a medical service that happened to be a business, she saw a business that happened to be in medical services. The difference would prove transformational.

The foundation years ended with Metropolis at an inflection point. It had proven that Indians would pay for quality diagnostics—if they understood the value. It had demonstrated that scientific excellence could be profitable—if managed efficiently. Most importantly, it had created a brand in an industry that didn't believe in brands. The local laboratory had outgrown its local ambitions. What came next would require not just scaling the model but reimagining what an Indian diagnostic company could become.

IV. The Second Generation Takes Charge: Ameera Shah Era (2001-2010)

The scene was almost cinematic in its symbolism: In 2001, a 21-year-old Ameera Shah, fresh from her MBA at Harvard, stood in her father's Mumbai laboratory watching technicians process blood samples. She had just made one of the most consequential decisions of her life—turning down consulting offers from McKinsey and investment banking positions at Goldman Sachs to take over a diagnostic laboratory that most of her Harvard classmates had never heard of. Her professors thought she was crazy. Her classmates were politely puzzled. But Ameera saw something they didn't: the opportunity to transform not just a business, but an entire industry.

The generational handover wasn't just about age—it was about worldview. Dr. Sushil Shah had built Metropolis as a temple to diagnostic excellence, where quality was worship and accuracy was scripture. Ameera respected the temple but wanted to build a corporation. Her father thought in terms of tests and patients; she thought in terms of markets and scalability. Where he saw medical professionals who needed education about quality, she saw a fragmented industry ripe for consolidation. The transformation began immediately when she took over her father's pathology business in 2001. While she had been working at investment bank Goldman Sachs, the opportunity didn't leave her fully satisfied, which eventually led her to join her father's pathology business. She transformed a single diagnostic lab which had revenue of about $1.5 million and 40 employees into something far more ambitious.

Her first insight was brutal in its clarity: the pathology industry needed to transform "from being a doctor-led practice to a professional corporate group in an extremely unregulated, competitive, and fragmented market". This wasn't just about improving operations—it was about changing the fundamental nature of the business. Where doctors saw diagnostics as an extension of medical practice, Ameera saw it as a consumer service that happened to involve medical testing.

The strategy shift was immediate and multifaceted. Instead of competing head-to-head with thousands of small labs, Ameera pioneered a partnership model. Local and regional diagnostic chains that couldn't match Metropolis's testing capabilities became partners rather than competitors. They would collect samples and send them to Metropolis for advanced testing, sharing revenues while maintaining their local relationships. It was a masterstroke that turned potential enemies into allies.

The hub-and-spoke model that Ameera championed wasn't just logistics—it was economics. A central processing lab in Mumbai could handle sophisticated tests requiring expensive equipment and specialized expertise. Satellite collection centers needed minimal investment—just a phlebotomist, a refrigerator, and Metropolis branding. This capital-light expansion model allowed rapid scaling without the massive investments that opening full laboratories would require.

She began her journey at Metropolis in the early 2000s starting at the bottom, in customer servicing roles. According to Ameera Shah, this experience helped her understand ground-level issues of the business. When she was about 11–12 years old, she used to go to her dad's lab during summer holidays, working from eight in the morning to eight in the evening. One of her jobs was to give lab tours to guests, during which she once mistakenly referred to the serum collection room as the "semen collection room," much to everyone's amusement. These early experiences, both serious and humorous, gave her an intimate understanding of the business from the ground up.

By 2005, Ameera was ready for her boldest move yet—professional capital. The diagnostic industry in India had been largely self-funded or dependent on traditional bank financing. Private equity was virtually unknown. But Ameera understood that to compete at scale, Metropolis needed not just capital but strategic partners who could provide governance structures and growth expertise.

The 2006 ICICI Venture deal was transformative in ways beyond the Rs 35 crore injection. Due to its unique growth model and competitive advantage, Metropolis attracted three rounds of investment by reputed private equity investors. ICICI brought discipline—monthly board meetings, quarterly reviews, detailed financial reporting. For a company transitioning from family-run to professionally managed, this external pressure was invaluable. It forced Metropolis to articulate strategy, measure performance, and think in terms of return on capital rather than just quality of service.

The numbers tell the story of transformation. Between 2001 and 2010, Metropolis grew from that single Mumbai lab to a network spanning multiple states. Revenue increased over 20-fold. But more importantly, the company's positioning changed fundamentally. It was no longer "Dr. Shah's excellent laboratory"—it was Metropolis, a brand that stood for reliability regardless of which doctor referred you or which collection center you visited.

The 2010 Warburg Pincus investment of $85 million marked the end of the foundation-building phase. ICICI Venture exited with stellar returns, validating the private equity model in Indian diagnostics. But for Ameera, this was just the beginning. She had proven that a diagnostic company could be run like a modern corporation. The next challenge would be proving it could expand like one too.

Ms Shah had been responsible for corporatizing Metropolis by setting protocols, hiring expert professionals for the management team and bringing together a fully actualized board. The organizational changes went deep. Where the company once relied on Dr. Shah's personal reputation, it now had systems, processes, and governance structures that could outlive any individual. Department heads were hired from multinationals, bringing expertise in areas like supply chain management and IT that traditional diagnostic companies ignored.

The technology transformation deserves special mention. Ameera realized that Metropolis needed to up its game with respect to technology and innovation. "Not having that solid bedrock of technology and not investing in the right people early on truly came back to bite us. Technology keeps changing and is the hardest thing to undo and redo," she reflected. This early recognition of technology's importance would prove prescient as the industry digitized.

The culture clash between old and new was real but manageable. Senior pathologists who had worked with Dr. Shah sometimes struggled with Ameera's MBA-style management. But she navigated this carefully, respecting scientific expertise while insisting on professional discipline. It helped that results were undeniable—the company was growing faster and more profitably than ever.

By the end of 2010, Metropolis had been fundamentally transformed. Within 3–4 years of her entry, they had all the basics in place, completed a few acquisitions and Metropolis was ready for the next leap of expansion. What started as a scientist's quest for diagnostic excellence had become a corporate success story. But the biggest challenges—geographic expansion, public markets, and competing with global players—still lay ahead.

V. Geographic Expansion & Service Innovation (2005-2015)

The scene could have been from a corporate thriller: In 2005, Ameera Shah stood in a cramped government office in Colombo, Sri Lanka, negotiating Metropolis's first international expansion. The local health ministry officials were skeptical—why would an Indian diagnostic company succeed where local players struggled? Her answer was simple but powerful: "We're not bringing Indian diagnostics to Sri Lanka. We're bringing world-class diagnostics that happens to come from India." That subtle reframing would define Metropolis's entire international strategy. The international journey began in 2005 with Sri Lanka being the first market, a natural choice given the geographic proximity and cultural similarities. But what made Sri Lanka truly strategic was its role as a proof of concept—could the Metropolis model work outside India's unique healthcare ecosystem?

The answer came quickly. Sri Lankan doctors, frustrated with local labs' inconsistency, embraced Metropolis's reliability. Within 18 months, the company was processing samples from across the island nation, often flown to Mumbai for specialized tests that no Sri Lankan lab could perform. The hub-and-spoke model that worked within India proved even more powerful internationally—local collection, centralized processing, global standards.

The UAE expansion in 2006 presented entirely different challenges. Dubai and Abu Dhabi already had sophisticated healthcare infrastructure and international hospital chains. Metropolis couldn't compete on basic testing—it had to offer something unique. The answer: serving the massive Indian expatriate population who trusted the Metropolis brand from back home, while simultaneously offering specialized tests for genetic conditions prevalent in Middle Eastern populations. It was a masterclass in market segmentation.

The parallel service innovation happening in India during this period was equally transformative. Metropolis Healthcare expanded into new service areas like Clinical Research, Hospital Lab Management and Wellness Solutions in the past decade. Each vertical addressed a different market failure. Clinical Research capitalized on India's growing importance in global drug trials. Hospital Lab Management offered smaller hospitals the benefits of Metropolis's systems without capital investment. Wellness Solutions tapped into the emerging preventive healthcare trend among India's affluent classes.

The wellness pivot deserves special attention. Traditional diagnostics was reactive—you got tested when sick. But by 2010, Metropolis noticed affluent Indians increasingly requesting comprehensive health checkups, not because they were ill, but because they wanted to stay healthy. The company launched packages targeting specific demographics: executive health checkups for stressed corporate workers, women's wellness panels for urban professionals, senior citizen packages for aging parents. These weren't just bundles of tests but curated experiences with counseling, trend analysis, and lifestyle recommendations.

Technology adoption during this period was aggressive but strategic. While competitors were still faxing reports, Metropolis launched online report delivery in 2008. By 2010, patients could track their historical test results, spot trends, and share reports with multiple doctors electronically. This wasn't just convenience—it was creating switching costs. Once patients had years of data on Metropolis's platform, moving to another lab meant losing that history.

The African expansion began with Kenya in 2013, followed by Mauritius and Ghana in 2014. Africa represented the ultimate test of Metropolis's model. These markets had minimal diagnostic infrastructure, low purchasing power, and challenging logistics. But they also had massive unmet need. Metropolis's approach was innovative: partner with local entrepreneurs who understood the market, provide technology and training, but maintain quality control from Mumbai. With a strong presence in Kenya for over 10 years, the company proved that quality diagnostics could be profitable even in developing markets.

The competitive dynamics during this expansion phase were fascinating. In India, Dr. Lal PathLabs remained the primary rival, but the competition was increasingly about network density rather than quality. Both companies had established reputations for accuracy; the battle was about convenience—who had a collection center closer to the customer. This led to a land-grab mentality, with both companies racing to establish presence in tier-2 and tier-3 cities.

But the real innovation was happening at the intersection of B2B and B2C strategies. Metropolis realized that while patients chose convenience, doctors chose capability. So the company adopted a dual strategy: dense collection networks for patient convenience, but sophisticated test menus to attract doctor referrals. A small-town doctor could offer his patients the same advanced tests available at Apollo or Fortis hospitals, enhancing his practice's prestige.

The 2015 funding event marked a crucial transition. Due to its unique growth model and competitive advantage, Metropolis attracted three rounds of investment by reputed private equity investors. KKR's Rs 5.6 billion investment wasn't just capital—it was validation that Metropolis had evolved from a diagnostic company to a healthcare platform. The funding was structured as promoter debt to Ameera Shah, allowing her to increase her stake while bringing in a global investor known for operational excellence.

The organizational capabilities built during this decade were as important as the geographic expansion. Metropolis developed a team of 200 senior pathologists and over 2000 technicians delivering diagnostic solutions across routine, semi-specialty, and super-specialty domains. This wasn't just headcount growth—it was building India's largest concentration of pathology expertise outside the government sector.

The innovation in test offerings was relentless. The company expanded to offer a comprehensive range of 4000+ clinical laboratory tests and profiles, used for prediction, early detection, diagnostic screening, confirmation, and monitoring of diseases. Each new test represented not just technical capability but market education—doctors had to be trained on when to prescribe it, patients had to understand its value.

By 2015, Metropolis had transformed from an Indian diagnostic company with international presence to a truly multinational healthcare services firm. With over 35 years of experience in delivering accurate reports, Metropolis had earned the reputation of being India's most respected and only multinational chain of diagnostic centres with presence in UAE, Sri Lanka, South Africa, Kenya, Mauritius and Ghana. The foundation was set for the next phase: convincing public markets that a diagnostic company could be a growth story worthy of premium valuations.

VI. The IPO Story & Public Market Journey (2019)

The Mumbai stock exchange on April 15, 2019, witnessed something unusual—a diagnostic company's IPO that was creating buzz typically reserved for tech startups or consumer brands. As Ameera Shah rang the opening bell, she wasn't just listing a company; she was validating an entire sector that public markets had largely ignored. The journey to this moment had been anything but straightforward. The decision to go public had been years in the making. By 2018, Metropolis had achieved scale—106 clinical laboratories, over 2,000 collection centers, processing approximately 16 million tests from 7.7 million patient visits annually. But scale alone doesn't justify an IPO. What made Metropolis IPO-ready was its financial profile: consistent profitability, asset-light expansion model, and most critically, a business that could be understood by public market investors.

The IPO structure was telling about the company's maturity. This was entirely an offer for sale—13,685,095 equity shares at Rs 880 per share aggregating Rs 1,204.29 Crores, with 6,272,335 shares from Dr. Sushil Shah and 7,412,760 shares from CA Lotus Investments (Warburg Pincus). No fresh capital was being raised. This wasn't about funding growth—it was about providing exits to early investors and partial liquidity to the founder family.

The roadshow revealed fascinating dynamics about how Indian capital markets viewed healthcare services. Institutional investors were initially skeptical. Diagnostics seemed commoditized—what was Metropolis's moat? The management's answer was nuanced: in a business where the product (test results) appears identical, the moat lies in trust, consistency, and network density. A mother choosing where to test her child's blood doesn't comparison shop; she goes where her doctor recommends or where she's gone before.

On Tuesday, Metropolis Healthcare raised Rs 530 crore by selling shares to anchor investors, a strong vote of confidence from institutional players. The anchor book included marqu

ee names—both global funds who understood healthcare services and domestic institutions betting on India's healthcare consumption story.

The Metropolis IPO was subscribed 5.8255 times by April 5, 2019, with particularly strong interest from qualified institutional buyers. The retail category subscribed 2.1502 times, showing decent but not overwhelming retail interest. This subscription pattern was typical for a specialized B2B2C business—institutions understood it better than retail investors.

The pricing at Rs 880 per share valued Metropolis at approximately Rs 4,416 crores, putting it at a significant premium to book value but reasonable compared to consumer healthcare companies. The valuation implied that markets were pricing Metropolis not as a diagnostic company but as a consumer healthcare brand—a crucial distinction that would define its market trajectory.

On listing day, April 15, 2019, the stock opened at Rs 958 on NSE, up 8.86% from the IPO price, and closed at Rs 959.85, up 9.07%. This wasn't a blockbuster listing like some tech IPOs, but it was solid—exactly what a healthcare services company should deliver. The measured listing gains suggested that the IPO was fairly priced, leaving room for long-term appreciation rather than immediate profit-taking.

The post-IPO challenges emerged quickly. As a public company, Metropolis faced quarterly scrutiny that private equity investors never imposed. Every metric was dissected—same-store sales growth, new center additions, average revenue per test. The market wanted growth, but profitable growth. The company had to balance aggressive expansion with margin maintenance, a tightrope walk that would define its public market journey.

What's particularly interesting about the IPO timing was the competitive context. Dr. Lal PathLabs had gone public in 2015 and had seen its stock price multiply, validating the diagnostic sector for public investors. Thyrocare had also listed in 2016. But each company told a different story—Lal PathLabs was the network play, Thyrocare the low-cost disruptor, and Metropolis positioned itself as the quality and innovation leader.

The Indian diagnostics market context was compelling—valued at Rs 596 billion in 2018, expected to grow to Rs 802 billion by 2020. But more important than size was the structure: the market remained highly fragmented with unorganized players controlling nearly half the market. This suggested massive consolidation opportunity for organized players with access to capital.

The employee reservation portion of 300,000 shares was oversubscribed, indicating strong internal confidence. For a company transitioning from promoter-driven to professionally managed, employee participation in ownership was crucial for alignment. Many of these employees had been with Metropolis for years, watching it grow from a regional player to a national champion.

The use of proceeds—or rather, the lack thereof since this was entirely an OFS—sent an important message. Metropolis didn't need capital for growth; it was generating enough cash internally. This distinguished it from many IPOs where companies raise money because they can, not because they need to. The company's confidence in self-funded growth would prove both a strength and a limitation in the coming years.

Media coverage of the IPO was extensive but mixed. Business press praised the company's track record and market position. Healthcare publications questioned whether diagnostics could maintain pricing power as technology democratized testing. Technology media wondered if Metropolis was prepared for digital disruption—what if consumers could test at home?

For Ameera Shah, the IPO represented validation of a two-decade journey transforming her father's laboratory into a corporate entity worthy of public investment. Today, Metropolis is valued at 1.25 billion dollars, up from a valuation of half a billion dollars at the time of the IPO in April 2019—though this statement from 2021 would later prove optimistic as valuations fluctuated with market conditions.

The governance changes post-IPO were significant. Independent directors with healthcare and financial expertise joined the board. Quarterly earnings calls became platforms for articulating strategy. The company had to balance transparency with competitive sensitivity—how much to reveal about expansion plans without alerting competitors?

As the IPO day ended and Metropolis shares settled into regular trading, the real journey was just beginning. The company had successfully convinced public markets that a diagnostic laboratory could be a growth story. Now it had to deliver on that promise, quarter after quarter, in a market that was becoming increasingly competitive and where technology threatened to disrupt traditional models. The IPO wasn't the destination—it was just another milestone in Metropolis's evolution from a Mumbai laboratory to a healthcare platform with national ambitions.

VII. Business Model & Operations Deep Dive

Inside Metropolis's central laboratory in Mumbai at 4 AM, the scene resembles a high-stakes logistics operation more than a medical facility. Samples collected from across Western India the previous evening are arriving in temperature-controlled boxes, each tagged with barcodes that track their journey from collection to result. By noon, most of these samples will be processed, analyzed, and reported—a daily miracle of operational efficiency that processes over 30 million tests annually. Understanding how this machine works reveals why diagnostics, despite appearing commoditized, can be a surprisingly defensible business. The hub-and-spoke architecture is elegant in its simplicity but complex in execution. Metropolis has implemented a hub and spoke model for quick and efficient delivery of services through their widespread laboratory and service network. Its laboratory network consists of 115 clinical laboratories, comprising a global reference laboratory (GRL) located in Mumbai, which is the main hub; 14 regional reference laboratories (RRLs), 56 satellite laboratories, and 44 express laboratories. Each tier serves a specific purpose in the diagnostic value chain.

The Global Reference Laboratory in Mumbai is the crown jewel—a 50,000 square foot facility that can run tests most Indian hospitals have never heard of. Here, sophisticated equipment worth crores processes everything from routine CBCs to complex genetic sequencing. The economics are compelling: a machine that costs Rs 5 crore and requires a PhD to operate can serve the entire Western India market from this single location.

Regional Reference Laboratories act as mini-hubs, capable of processing 80% of test requests locally. These aren't just processing centers; they're quality control checkpoints. Every unusual result gets verified, every complex case reviewed by senior pathologists. This distributed expertise model ensures that a patient in Nashik gets the same quality as one in South Mumbai—a claim few diagnostic chains can credibly make.

The collection network—those 2,000+ centers—represents the real innovation. Most are tiny, sometimes just a 200-square-foot space with a phlebotomist and a refrigerator. But each follows a rigorous 8-Stage MET Protocol that ensures the most comprehensive testing for accurate and reliable reports. The capital requirement is minimal—perhaps Rs 5-10 lakhs per center—but the network effect is massive. Dense coverage means convenience for patients and efficient sample collection routes.

Metropolis has a team of 200 senior pathologists and over 2000 technicians delivering diagnostic solutions in routine, semi specialty and super specialty domains. The company offers a comprehensive range of 4000+ clinical laboratory tests and profiles. This isn't just about quantity—it's about capability. When a doctor in a tier-2 city encounters a rare condition, Metropolis can run tests that previously required sending samples abroad.

The B2B versus B2C split reveals sophisticated market segmentation. B2B clients—hospitals, nursing homes, other labs—provide volume and predictable revenue. Metropolis caters to leading laboratories, Hospitals, Nursing homes and 2,00,000 doctors. These institutional clients don't switch easily; once integrated into their workflow, Metropolis becomes sticky. B2C clients—walk-in patients and doctor referrals—provide higher margins but require constant marketing and service excellence.

Technology infrastructure is where Metropolis's corporate evolution shows most clearly. The Laboratory Information Management System (LIMS) isn't just software—it's the nervous system of the entire operation. Every sample is barcoded at collection, tracked through processing, and reported digitally. This isn't just efficiency; it's quality control. When a sample takes longer than expected, the system flags it. When results fall outside normal ranges, it triggers verification protocols.

The home collection service, which seemed like a luxury pre-COVID, has become a differentiator. Medical technicians take samples at 7:00am and return at 9:30 after breakfast for fasting tests. Results are sent by email at 6pm. The whole experience is professional and well organised. This isn't just convenience—it's expanding the addressable market to include elderly patients, busy professionals, and those in areas without nearby collection centers.

Quality control systems deserve special attention. Metropolis is one of the few laboratories that has received CAP (College of American Pathologists) accreditation, the global gold standard. Most laboratories in India have received NABL Accreditation. The central laboratory also adheres to CLIA guidelines and follows GCP and GLP. These aren't just certificates on the wall—they represent systematic processes that ensure accuracy across millions of tests.

The franchise versus company-owned debate has been crucial to Metropolis's expansion strategy. Unlike some competitors who franchise aggressively, Metropolis maintains control over critical parts of the value chain. Collection centers might be franchised, but processing happens in company-controlled labs. This hybrid model balances rapid expansion with quality control—a delicate equilibrium that many have failed to achieve.

Pricing dynamics reveal the complexity of Indian healthcare economics. A basic CBC might cost Rs 300 at Metropolis versus Rs 150 at a local lab. But the Metropolis report comes with historical tracking, digital access, and the confidence of accuracy. For affluent Indians, this premium is negligible. For middle-class families, it's justified for important tests. For the poor, it's often unaffordable—a reality that limits market expansion.

The recent expansion strategy shows evolution in thinking. Metropolis Healthcare is expanding into Tier 2, 3, and 4 towns across Uttar Pradesh, Madhya Pradesh, Andhra Pradesh, Telangana, and Assam, targeting under-served markets characterized by limited high-quality diagnostic services and lower competition. This isn't just geographic expansion—it's market creation. In these towns, Metropolis isn't competing with established players; it's replacing unorganized providers.

Operational efficiency metrics tell the story of scale. A Mumbai collection center might process 100 samples daily; a tier-3 town center might do 20. But the Mumbai center's costs are 5x higher. The math works because processing is centralized—whether handling 100 or 1,000 samples, the lab's fixed costs remain similar. This operating leverage is what makes the hub-and-spoke model economically viable.

The specialized testing portfolio represents both opportunity and challenge. Metropolis is focusing on therapeutic areas such as neurology, oncology, transplants, nephrology, and gastroenterology, while investing in genomics and molecular diagnostics. These high-value tests have better margins but require educating doctors about when to prescribe them—a slow, expensive process.

The competitive response to Metropolis's model has been telling. Dr. Lal PathLabs has doubled down on North India dominance. Thyrocare has pursued aggressive pricing. Local players have formed consortiums to share resources. But none have successfully replicated Metropolis's combination of scale, quality, and brand—suggesting the moat is deeper than it appears.

Looking at the numbers, the company generates Rs 1,404 Cr in revenue with Rs 153 Cr in profit, modest figures for a company valued at over Rs 10,000 crores. But the market isn't valuing current earnings—it's pricing in the opportunity to consolidate a fragmented industry, expand into underserved markets, and capture the growing preventive healthcare trend.

The operational model's true genius lies not in any single element but in how they reinforce each other. Quality attracts doctor referrals, which drives volume, which justifies technology investment, which improves efficiency, which enables competitive pricing while maintaining margins, which funds expansion, which increases convenience, which attracts more patients. It's a flywheel that, once spinning, becomes increasingly difficult for competitors to stop.

VIII. Competitive Dynamics & Market Position

The war room at Metropolis's Mumbai headquarters has a massive screen displaying real-time metrics: tests processed, revenue per location, competitor pricing in key markets. Every morning, the leadership team reviews overnight reports from 18 states. In Pune, Dr. Lal PathLabs has opened three new collection centers. In Bangalore, a local chain has slashed prices by 30%. In Chennai, a hospital chain is bringing diagnostics in-house. This is the daily reality of competing in Indian diagnostics—a knife fight in a phone booth where victory is measured in basis points of market share.

Metropolis Healthcare Ltd is the second largest diagnostic company in India and the largest player in Western and Southern India. This positioning sounds dominant until you understand the market structure. Being "second largest" in Indian diagnostics is like being the second tallest building in a city of bungalows—impressive relative to others, but tiny relative to the opportunity.

The Rs 596 billion diagnostics market in 2018 was misleadingly large. Nearly 48% was controlled by unorganized players—small labs, hospital departments, doctor-owned facilities operating without standardization or scale. Another 30% belonged to hospital chains doing in-house testing. The organized diagnostic chains—Metropolis, Dr. Lal PathLabs, Thyrocare, and a few others—were fighting over roughly 22% of the market. The real competition wasn't with each other but with the status quo.

Dr. Lal PathLabs, the market leader, presented a fascinating contrast to Metropolis. Where Metropolis emphasized quality and innovation, Lal PathLabs focused on network density and operational efficiency. Their Northern India stronghold was nearly impenetrable—in Delhi-NCR, they had collection centers every few kilometers. Their strategy was simple: be everywhere, be consistent, be affordable. It worked. Their revenue was nearly 50% higher than Metropolis, and their market cap often exceeded Metropolis by 20-30%.

Thyrocare disrupted from a different angle entirely. Founded by A. Velumani, a former Bhabha Atomic Research Centre scientist, Thyrocare was the diagnostic industry's answer to Southwest Airlines—strip everything non-essential, focus on volume, compete on price. Their central processing lab in Mumbai was a marvel of automation, processing over 100,000 samples daily. They offered a thyroid panel for Rs 300 that others priced at Rs 1,000. For routine tests, they were unbeatable on price.

But Thyrocare's model had limitations that Metropolis exploited. When you're the cheapest, customers assume you're cutting corners somewhere. Doctors hesitated to refer complex cases. Patients questioned accuracy when results differed from previous tests. Metropolis positioned itself as the premium alternative—yes, we're more expensive, but when it matters, you want us.

The hospital labs represented a different competitive threat. Apollo, Fortis, Max—these chains had captive customers and deep pockets. They could afford to run diagnostics at break-even or even losses, viewing it as a service to attract patients for more profitable procedures. Metropolis couldn't compete with free, but it could offer something hospitals couldn't: independence. Doctors increasingly valued second opinions from labs not affiliated with treatment providers.

The unorganized sector was both competitor and opportunity. These small labs survived on relationships—the local doctor who sent all his patients to his cousin's lab, the neighborhood facility that had served families for generations. They couldn't match Metropolis on quality or test menu, but they had trust and convenience. Metropolis's strategy was gradual absorption—acquire the better ones, compete the weaker ones to death, convert the rest into collection centers.

Geographic positioning revealed strategic thinking. Metropolis has widespread presence across 220 cities in India with leadership position in West and South India. This wasn't accidental. Western India, anchored by Mumbai and Pune, had high purchasing power and healthcare awareness. Southern India, particularly Bangalore and Chennai, had a culture of preventive healthcare. These markets valued quality over price—Metropolis's sweet spot.

The competitive dynamics in tier-2 and tier-3 cities were entirely different. Here, the enemy wasn't Dr. Lal or Thyrocare—it was ignorance. Patients didn't know that accurate diagnostics mattered. Doctors prescribed tests based on kickbacks rather than clinical need. The challenge wasn't winning customers from competitors but creating customers who understood the value of quality diagnostics.

Technology emerged as a new battlefield around 2015. Healthians, 1mg, and other digital-first players offered home collection and app-based reports at aggressive prices. They raised venture capital, spent heavily on marketing, promised to "disrupt" traditional diagnostics. Metropolis's response was measured—improve digital capabilities but don't panic. These new players were burning cash to acquire customers who were price-sensitive and disloyal. Let them burn, then pick up the pieces.

The insurance and corporate segment presented unique dynamics. Insurance companies wanted the lowest prices and highest kickbacks. Corporate wellness programs wanted comprehensive packages and convenient execution. Metropolis struggled here initially—their premium pricing didn't align with insurance economics. But they found a niche in high-end corporate wellness, serving companies that valued employee satisfaction over cost minimization.

Differentiation strategies evolved continuously. If Lal PathLabs opened centers, Metropolis improved turnaround time. If Thyrocare cut prices, Metropolis added new tests. If hospitals integrated backwards, Metropolis integrated forward into wellness. The key was never to compete directly on competitors' strengths but to constantly shift the battlefield to areas where Metropolis had advantages.

The specialized testing moat proved durable. When a patient needed a rare genetic test or complex cancer marker, the options narrowed quickly. Most labs couldn't even process these tests—they'd quietly forward them to Metropolis or send them abroad. This high-end segment had 70%+ margins and created a halo effect—if Metropolis could handle the complex stuff, surely they were trustworthy for routine tests.

Pricing discipline was crucial but challenging. In a market where unorganized players offered CBCs for Rs 100, Metropolis charging Rs 300 seemed exploitative. But the company held firm—we're not selling tests, we're selling accuracy and reliability. When customers compared total healthcare costs, including misdiagnosis and repeat testing, Metropolis often proved economical. But this was a sophisticated argument that many consumers didn't grasp.

Brand building in diagnostics faced unique challenges. Unlike consumer products, you couldn't advertise "better blood tests" on television. Trust built slowly, through doctor recommendations and word-of-mouth. One misdiagnosis could destroy years of reputation-building. Metropolis invested in medical education, sponsoring conferences and training programs. When doctors understood quality, they recommended Metropolis.

The competitive landscape's fragmentation presented consolidation opportunities. With thousands of small labs struggling with compliance costs and technology requirements, roll-up potential was massive. But integration was complex—each acquisition brought different systems, cultures, and quality standards. Metropolis was selective, acquiring only labs that enhanced geographic presence or technical capabilities.

Market share data was frustratingly opaque. Unlike organized retail where scanner data provided real-time competitive intelligence, diagnostics relied on estimates and surveys. Metropolis claimed leadership in Western and Southern India, but what did that mean? 10% share? 15%? The fragmentation made precise measurement impossible, which made strategic planning challenging.

The company has delivered poor sales growth of 9.22% over past five years and has a low return on equity of 12.8% over last 3 years. These metrics suggested that despite its market position, Metropolis faced growth challenges. The easy expansion was done—metros and tier-1 cities were saturated. Future growth required entering markets where the economics were less favorable and competition more fragmented.

The ultimate competitive question wasn't about Dr. Lal or Thyrocare—it was about relevance. As home testing technology improved and AI-enabled diagnosis emerged, would centralized labs remain necessary? Metropolis's bet was that quality and trust would matter more as healthcare became more complex. But this was a bet, not a certainty, and the competitive dynamics would ultimately be shaped by forces beyond any single company's control.

IX. Modern Era & Strategic Initiatives (2018-Present)

The conference room in December 2024 buzzed with nervous energy as Metropolis's board approved its largest acquisition ever—Core Diagnostics for Rs 24,683 lakhs (Rs 247 crores). This wasn't just another lab purchase; it was a statement about where Metropolis saw healthcare heading. Core Diagnostics brought advanced oncology testing, genomics capabilities, and most crucially, relationships with India's leading cancer hospitals. In a single move, Metropolis was betting that specialized diagnostics would drive the next decade of growth. The Core Diagnostics acquisition revealed Metropolis's strategic evolution. Core specialized in advanced oncology testing, deriving 85% of revenue from specialty tests versus 37% for Metropolis. With average revenue per test of Rs 2,300—five times Metropolis's average—Core represented the future of diagnostics: specialized, high-value, technology-driven. The acquisition would increase oncology's contribution to Metropolis's revenue from 4% to 10%, positioning the company as India's leading cancer diagnostics provider.

But the modern era had begun years earlier with a different kind of partnership. In February 2018, Metropolis partnered with National AIDS Control Organisation (NACO) for a three-year project for diagnosis of HIV at 560 locations in India. This wasn't just a contract—it was validation that Metropolis could execute at government scale while maintaining quality. The partnership required collecting samples from remote ART centers, transporting them to processing labs, and delivering results within mandated timeframes. It was logistics as much as diagnostics.

COVID-19 changed everything. When the pandemic hit in March 2020, Metropolis faced an existential crisis. Routine testing collapsed as people avoided hospitals. Wellness packages became irrelevant. International operations were cut off. Revenue dropped 40% in April 2020. But within weeks, the company pivoted. RT-PCR testing for COVID-19 became the new revenue driver. Metropolis conducted over half a million RT-PCR tests, leveraging its existing infrastructure for a completely new challenge.

The pandemic accelerated digital transformation by years. Home collection, previously a premium service, became essential. The company had to rapidly scale from hundreds of home visits daily to thousands. Digital reporting moved from convenience to necessity. The entire customer journey—booking, collection, payment, results—went contactless. What might have taken five years of gradual change happened in five months.

Post-pandemic, the market dynamics shifted fundamentally. Preventive healthcare, long preached but rarely practiced, suddenly had converts. People who'd never had a health checkup were booking comprehensive packages. The company's wellness initiative TruHealth launched across 36 cities, targeting this new health-conscious consumer. It wasn't just about testing anymore—it was about ongoing health monitoring, trend analysis, and preventive interventions.

The competitive landscape post-COVID looked different. Several small labs had shut down, unable to survive the lockdowns. Others had merged or been acquired. But new players had emerged—digital-first platforms backed by pandemic-era venture capital. The diagnostics market was simultaneously consolidating and fragmenting, creating both opportunities and threats.

Geographic expansion continued but with different priorities. The firm aims to strengthen its presence in tier 2 and tier 3 cities, supported by an investment of approximately Rs 65 crore. The company plans to expand reach to 1,000 towns in 18 months. This wasn't just about planting flags—it was about creating sustainable business models in markets with different economics. A collection center in rural Madhya Pradesh couldn't operate like one in Mumbai. Pricing, service levels, and test menus had to be localized.

The technology investments during this period were substantial. Metropolis is currently undergoing complete digital transformation including changing backend architecture, redesigning the core, and building API-led architecture for more agility. This wasn't just modernization—it was preparation for a future where diagnostics would be embedded in digital health platforms, integrated with telemedicine, and connected to AI-driven diagnosis tools.

Specialty focus intensified. "We are committed to leading in therapeutic areas such as transplants, neurology, nephrology, gastroenterology, and oncology," CEO Surendran Chemmenkotil stated. Each specialty required different capabilities—equipment, expertise, partnerships. Neurology testing needed sophisticated imaging interpretation. Transplant diagnostics required HLA typing capabilities. Oncology demanded both tumor markers and genetic profiling. Building these capabilities wasn't just capital investment—it was years of expertise development.

The financial performance reflected both challenges and opportunities. Q4FY24 showed revenue from operations of Rs 313 crores, an 11% increase from Q4FY23's Rs 282 crores. Core business revenue rose 15% to Rs 308 crores. EBITDA margins improved to 26.4% from 25.7%. But growth remained modest—the days of easy 20%+ expansion were over. Future growth would come from market share gains and new service lines, not just market expansion.

Partnership strategies evolved. Instead of just serving hospitals and doctors, Metropolis began collaborating with insurance companies on preventive care programs, with corporations on employee wellness, with governments on public health initiatives. Each partnership required different capabilities—insurance needed cost control, corporations wanted convenience, governments demanded scale.

The regulatory environment was also changing. The government's push for universal health coverage, Ayushman Bharat, and other initiatives were reshaping healthcare delivery. While Metropolis wasn't directly part of most government programs due to its premium positioning, the broader push for organized healthcare benefited the entire sector.

International operations, disrupted by COVID, were being reconsidered. The African and Middle Eastern markets remained attractive, but the focus shifted from owned operations to partnerships and franchising. The capital-light model that worked in India could work globally, but execution required local partners who understood regulatory and cultural nuances.

By late 2024, Metropolis stood at another inflection point. The Core Diagnostics acquisition signaled ambition—to be not just a diagnostic company but a specialized healthcare services provider. The market opportunity was massive—cancer cases in India were projected to increase 50% by 2030. But execution would be complex, requiring integration of different cultures, systems, and service models.

The modern era's defining characteristic was complexity. No longer could Metropolis succeed just by being better at basic diagnostics. It needed to be a technology company, a logistics provider, a healthcare partner, and a consumer brand simultaneously. The Core acquisition wasn't just about cancer testing—it was about positioning for a future where diagnostics would be predictive, not just diagnostic; where AI would interpret results; where genomics would personalize treatment. In this future, companies that controlled specialized expertise and data would win. Metropolis was betting Rs 247 crores that it could be one of them.

X. Leadership & Corporate Culture

The award ceremony at Mumbai's Taj Hotel in 2021 had all the trappings of corporate celebration, but for Ameera Shah, receiving the Ernst & Young Entrepreneur of the Year Award in healthcare carried deeper meaning. She was one of only three women to ever receive this award in 20 years and the youngest woman ever to receive it. Standing at the podium, she didn't talk about financial metrics or market share. Instead, she spoke about her grandmother, who died from a misdiagnosed condition that simple blood tests could have caught. "Every report we generate," she said, "is someone's grandmother, father, child. We're not in the testing business. We're in the trust business. "This philosophy—technical excellence wrapped in human empathy—defined Metropolis's leadership culture. Dr. Sushil Shah, who had won the same EY award in 2011, set the foundation with his scientist's precision and doctor's compassion. But Ameera added layers: corporate sophistication, strategic thinking, and crucially, the ability to scale culture across thousands of employees.

The father-daughter dynamic was unique in Indian business. Unlike typical family businesses where the second generation either rebels against or blindly follows the first, the Shahs achieved something rare: complementary leadership. Dr. Shah remained the technical conscience, reviewing complex cases, maintaining relationships with senior pathologists, embodying scientific integrity. Ameera became the corporate face, managing investors, driving expansion, building systems. Neither tried to be the other.

Fortune India's "Most Powerful Women in Business" recognized Ameera annually from 2017 to 2021, but power at Metropolis was deliberately distributed. The leadership team wasn't just family and loyalists but professionals hired from multinationals. The CFO came from a Big Four firm, the operations head from a global logistics company, the technology chief from an IT services major. This wasn't just about capability—it was about bringing different perspectives to a traditionally insular industry.

Building culture at scale presented unique challenges. How do you maintain quality standards across 4,000+ locations? How do you ensure a phlebotomist in rural Assam follows the same protocols as one in Mumbai? The answer wasn't just training—it was creating systems that made doing the right thing easier than doing the wrong thing. Every process was documented, every deviation tracked, every error analyzed not for punishment but for learning.

The scientific culture manifested in unexpected ways. While competitors celebrated sales achievements, Metropolis celebrated diagnostic breakthroughs. The employee who identified a rare genetic condition got more recognition than the one who closed a big corporate account. This wasn't anti-commercial—it was understanding that in diagnostics, technical excellence drives commercial success, not vice versa.

The transformation from family business to professional management happened gradually but deliberately. Board meetings evolved from informal discussions to structured governance. Independent directors with healthcare and financial expertise provided oversight. Audit committees, risk committees, nomination committees—the full apparatus of corporate governance was installed not because regulations required it but because excellence demanded it.

Employee development reflected long-term thinking. Metropolis invested heavily in training pathologists, even knowing many would eventually leave to start their own labs or join competitors. The logic was counterintuitive but powerful: by becoming the academy for Indian diagnostics, Metropolis ensured that industry standards everywhere reflected its values. Alumni became ambassadors, referring complex cases back to their alma mater.

The gender dynamics at Metropolis were noteworthy. In an industry dominated by male doctors and entrepreneurs, having a female MD created different possibilities. Ameera actively promoted women in leadership—not through quotas but through mentorship and opportunity. The head of operations, several regional managers, and many lab directors were women. This wasn't corporate feminism—it was recognition that healthcare consumption decisions were often made by women, and having women in leadership provided crucial perspective.

Crisis management revealed leadership character. During COVID-19's first wave, when staff were terrified of infection, leadership made critical decisions. PPE was procured at any cost. Insurance coverage was enhanced. Families of employees who contracted COVID while working received full support. Most importantly, no COVID-related layoffs were announced early, providing security when everything else was uncertain. These decisions cost money but built loyalty that money couldn't buy.

The succession planning discussion that most family businesses avoid was happening openly at Metropolis. Ameera, still in her 40s, wasn't going anywhere soon, but structures were being built for professional management independent of family involvement. This wasn't about exit but about sustainability—ensuring Metropolis could outlive its founders.

Communication styles reflected generational differences. Dr. Shah communicated through actions and presence—visiting labs, reviewing cases, teaching. Ameera communicated through systems and stories—town halls, emails, social media. Neither style was superior; both were necessary. Together, they reached different audiences within the organization.

The corporate culture had interesting paradoxes. It was hierarchical—titles mattered, reporting lines were clear—yet also informal—junior employees could email the MD directly with suggestions. It was process-driven—everything had an SOP—yet also entrepreneurial—new ideas were encouraged and quickly tested. It was Indian in values—respect for seniority, emphasis on relationships—yet global in ambitions and standards.

Performance management balanced multiple metrics. Yes, financial targets mattered, but so did quality scores, customer satisfaction, employee development. A lab director who hit revenue targets but had quality issues wouldn't survive. This multi-dimensional evaluation was complex to administer but essential for maintaining culture.

The role of medical professionals in leadership was carefully balanced. Unlike pure corporate entities where MBAs dominated, or traditional diagnostic labs where doctors ruled, Metropolis maintained equilibrium. Medical decisions were made by medical professionals, business decisions by business professionals, but both groups were required to understand and respect the other's domain.

External recognition mattered but wasn't pursued for its own sake. Awards were celebrated not as validation but as responsibility—each recognition raised expectations. When Ameera was named to Forbes Asia's Power Businesswomen list, the internal message wasn't celebration but challenge: "This recognition belongs to all 4,500 of you. Now let's earn it again."

The corporate values—"Accuracy, Efficiency, Empathy"—weren't just poster slogans. They were embedded in processes. Accuracy was measured through quality scores. Efficiency through turnaround times. Empathy through customer feedback. What got measured got managed, and what got managed shaped culture.

Dealing with failure was perhaps the truest test of culture. When a wrong diagnosis occurred—rare but inevitable in millions of tests—the response was systematic. Not blame, but analysis. Not cover-up, but transparency. Not just correction, but prevention. This approach was expensive—settlements, process changes, retraining—but essential for learning.

The leadership philosophy could be summarized in Ameera's often-repeated phrase: "We're building an institution, not just a business." This long-term orientation influenced everything from capital allocation (investing in capabilities that would pay off in years, not quarters) to talent management (developing leaders for roles that didn't yet exist) to market strategy (entering geographies that wouldn't be profitable for years).

By 2024, Metropolis's leadership had successfully navigated one of business's hardest transitions—from founder-led to professionally managed while retaining founder values. The culture that emerged was unique: scientifically rigorous yet commercially savvy, process-driven yet people-centric, Indian in heart yet global in ambition. Whether this culture could survive continued scaling, competitive pressure, and eventual complete transition from family leadership remained to be seen. But what the Shahs had built was more than a diagnostic company—it was a template for how Indian family businesses could modernize without losing their soul.

XI. Playbook: Business & Investing Lessons

Standing in a WeWork conference room in Bangalore, a healthcare startup founder sketches out his diagnostic platform idea to potential investors. "We'll be the Uber of diagnostics," he promises, "asset-light, tech-enabled, disrupting incumbents like Metropolis." The VCs nod appreciatively until one asks: "If it's so easy to disrupt, why has Metropolis's market share grown despite a dozen funded competitors?" The founder's stumbling answer reveals a fundamental misunderstanding of what Metropolis actually built—not just a diagnostic network, but a trust architecture that took four decades to construct.

Lesson 1: Trust as a Moat in Healthcare The power of credibility and trust in healthcare services cannot be replicated with technology or capital alone. When Metropolis correctly diagnosed that Bollywood actor's rare condition in 1986, they weren't just solving a medical mystery—they were making a deposit in a trust bank that would compound for decades. Every accurate diagnosis added to this balance; every error depleted it. Unlike software where bugs can be patched, diagnostic errors can be fatal. This asymmetry makes trust incredibly valuable and incredibly fragile.

Consider the economics: A customer choosing between two labs for a critical cancer marker test isn't price shopping—they're trust shopping. Metropolis charges 30-50% premiums not because their tests are chemically different but because their brand promises reduce anxiety. In healthcare, you're not selling products; you're selling confidence. This trust moat explains why despite numerous new entrants with venture capital backing, the organized diagnostic market remains concentrated among players with 20+ year histories.

Lesson 2: Hub-and-Spoke as Economic Architecture The hub-and-spoke model isn't just logistics—it's economic engineering. A Rs 10 crore genetic sequencing machine in Mumbai can serve customers in 200 cities. A PhD molecular biologist can review cases from across India. This model transforms fixed costs into variable revenues, creating operating leverage that improves with scale.

But execution complexity is severe. Sample degradation during transport, maintaining cold chains across Indian summers, ensuring collection quality at remote centers—each failure point can destroy the model's economics. Metropolis spent two decades perfecting these processes. New entrants discover that hub-and-spoke sounds simple but requires orchestration capabilities that money can't quickly buy. The lesson: operational models that seem obvious often have hidden complexity that creates competitive advantage.

Lesson 3: The B2B/B2C Balance in Healthcare Managing the B2B/B2C balance requires different capabilities that few companies master. B2B (hospitals, doctors) provides volume and stickiness but demands price concessions and service guarantees. B2C (patients) offers higher margins but requires consumer marketing and convenience.

Metropolis's genius was recognizing these weren't separate businesses but synergistic ones. Doctors who refer patients for specialized tests also recommend the lab for routine tests. Patients who trust the brand for complex diagnostics return for basic checkups. This flywheel effect—where B2B validates B2C and vice versa—creates compounding advantages. Pure B2B players lack consumer trust; pure B2C players lack medical credibility. The lesson: in healthcare, serving multiple stakeholders isn't complexity—it's competitive advantage.

Lesson 4: Capital Efficiency in Service Businesses Metropolis generates 14.7% ROCE despite being in a seemingly capital-intensive business. How? By disaggregating capital deployment. Processing requires heavy investment—machines, labs, technology. Collection requires minimal investment—a small room, basic equipment. By centralizing the former and distributing the latter, Metropolis achieves scale without proportional capital.

This extends to human capital. One senior pathologist at a hub can supervise 50 collection centers. One quality manager can monitor 20 locations through systems. This leverage means that incremental expansion requires marginal capital, improving returns as the network grows. The lesson: in service businesses, architecture determines capital efficiency more than operational efficiency.

Lesson 5: Consolidating Fragmented Industries The challenge of consolidating fragmented industries isn't acquisition—it's integration. Metropolis could buy 100 small labs tomorrow, but integrating different systems, qualities, and cultures would destroy value. Their selective approach—acquiring only labs that enhance capabilities or strategic geography—preserves operational integrity.

The unorganized market's persistence (still 48% share) isn't a failure—it's strategic patience. These players serve segments Metropolis can't economically address today. As regulations tighten and customer expectations rise, these players will face existential choices: upgrade or exit. Metropolis waits, knowing that time and market evolution are their allies. The lesson: in fragmentation, patience and selectivity beat aggressive consolidation.

Lesson 6: Timing Market Entry Being early versus being right is healthcare's perpetual dilemma. Dr. Shah introduced Radio Immunoassay in 1980, years before Indian markets were ready. The technology was superior, but customers didn't understand or value the superiority. Metropolis spent a decade educating the market—an expensive investment with uncertain returns.

But this early investment created knowledge advantages. When hormone testing became mainstream in the 1990s, Metropolis had a decade of experience while competitors were just starting. They knew which tests doctors actually needed, how to price for different segments, how to explain results to patients. The lesson: in healthcare, being early creates learning advantages that become competitively decisive when markets mature.

Lesson 7: Managing Succession in Founder-Led Businesses The transition from Dr. Sushil Shah to Ameera Shah offers a masterclass in succession. Rather than abrupt handover, it was gradual integration. Ameera worked in the business for years before taking charge, understanding ground-level operations before making strategic decisions. Dr. Shah remained involved but in a defined role, providing continuity without interference.

Most critically, they recognized that succession isn't just about leadership—it's about capability transformation. A scientist-entrepreneur built the foundation; a business-trained leader built the corporation. Neither could have done the other's job at that life stage. The lesson: successful succession requires recognizing that different business stages need different leadership capabilities.

Lesson 8: The Premium Pricing Paradox Metropolis's premium pricing strategy seems counterintuitive in price-sensitive India. But it works because they changed the conversation from price to value. When a test costs Rs 300 versus Rs 150, the discussion isn't about the Rs 150 difference—it's about the cost of misdiagnosis, repeat testing, delayed treatment.