Metro Brands: From Colaba Corner Store to India's Footwear Empire

I. Introduction & Episode Roadmap

Picture this: A single shoe store in 1955 Colaba, Mumbai, squeezed between the bustling streets near the iconic Metro Cinema. The owner dreams not of global domination but simply of selling quality footwear to the growing middle class of newly independent India. Fast forward to today—that humble store has morphed into Metro Brands, a ₹30,477 crore behemoth operating 900+ stores across 198 cities, generating ₹2,560 crore in revenue with ₹361 crore in profits.

How does a traditional footwear retailer crack the code that has eluded so many others in Indian retail? While Bata struggled with relevance, while countless mom-and-pop stores remained frozen in time, Metro Brands quietly built something extraordinary: a multi-brand retail empire that somehow manages to be both asset-light and omnipresent, both family-controlled and professionally managed, both traditional and digitally savvy.

This is a story about three pivotal transformations. First, the audacious decision in the 1980s to create multiple brands under one roof—a move that seemed like dilution but became diversification genius. Second, the 2007 entry of Rakesh Jhunjhunwala, India's Warren Buffett, whose patient capital and strategic guidance helped professionalize the business without losing its entrepreneurial soul. And third, the 2021 IPO that marked not just a liquidity event but a complete reimagination of what an Indian family business could become in the public markets.

What makes Metro's playbook particularly fascinating for founders and investors is its counterintuitive approach to scaling. In an era of D2C brands burning cash on customer acquisition, Metro built a profitable omnichannel machine. While others chased valuations, Metro chased unit economics. While competitors integrated vertically, Metro stayed asset-light through vendor partnerships spanning decades.

The themes we'll explore cut to the heart of Indian business evolution: How do you professionalize a family business without losing what made it special? Can you build a multi-brand portfolio without confusing customers or diluting focus? Is it possible to partner with global brands while maintaining your own identity? And perhaps most importantly—in a market where unorganized retail still commands 65% share, how do you build the infrastructure to capture the inevitable shift to organized retail?

Buckle up for a journey through seven decades of Indian retail history, told through the lens of one company's relentless evolution. This isn't just about shoes—it's about understanding how consumer businesses in emerging markets can build enduring value through patience, partnerships, and an almost obsessive focus on the fundamentals.

II. The Founding Story & Early Years (1955-1980s)

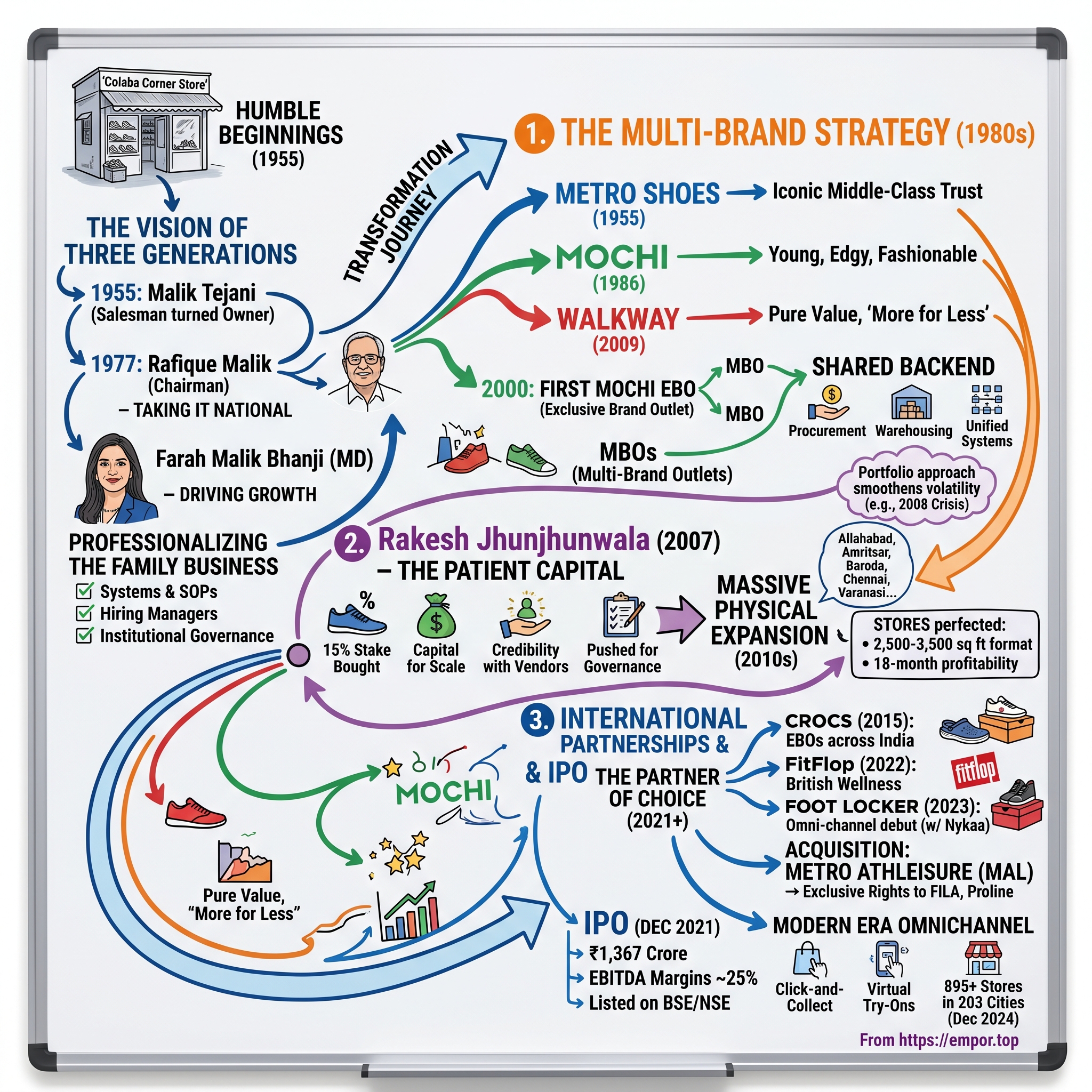

The year was 1955. Jawaharlal Nehru's India was eight years old, socialist ideals dominated economic thinking, and the License Raj hadn't yet fully tightened its grip. In Colaba, South Mumbai's toniest neighborhood, a small shoe store opened its doors near the Art Deco magnificence of Metro Cinema—the theater that would lend its name to an empire.

The Malik family weren't industrialists or traders with generational wealth. They were entrepreneurs in the truest sense, betting on a simple insight: as India urbanized, its growing middle class would need quality footwear that bridged the gap between expensive imports and cheap local chappals. The store's location was no accident—Colaba was where Mumbai's aspirational class congregated, where Western influences met Indian sensibilities.

Those early years were brutal. Post-independence India wasn't exactly friendly to consumer businesses. Foreign exchange was scarce, making imported materials expensive. Manufacturing was primitive, with most shoes still made by hand in small workshops. Distribution meant physically carrying inventory across the city. Credit was informal and risky. The Maliks had to build everything from scratch—relationships with cobblers in Agra and Kanpur, trust with customers who expected credit, systems for inventory in an era before computers. Metro Brands was founded by Malik Tejani, who was a shoe salesman before 1947. When India became independent, he bought the store he was working at and named it Metro Shoes. The transformation from employee to entrepreneur wasn't just a business transaction—it was a bet on India itself. His son, Rafique Malik, would go on to turn that single storefront into a national phenomenon. Rafique assumed the Chairman role on 19th January 1977, and over a career spanning more than five decades in the retail industry, his tenacity and ambition have propelled a modest single-store operation into one of India's largest and most profitable fashion footwear companies.

The original incorporation came in 1977, twenty-two years after the store's founding—a detail that speaks to the informal nature of business in that era. The company was incorporated in January 1977 as Metro Shoes. But between 1955 and 1977, the Maliks were learning hard lessons that no MBA could teach. They discovered that Indian consumers wanted quality but at accessible prices. They learned that relationships with vendors mattered more than contracts. They understood that in a country where credit cards didn't exist and banks didn't lend to small retailers, managing cash flow was survival itself.

What set Metro apart in those early decades wasn't technology or capital—it was an almost obsessive focus on the customer experience. Malik Tejani was instantly recognised by customers who came from different parts of the country. "My grandfather was a complete people's person; he could greet people in 40 languages and was our best salesman. His style of selling became the pillar on which Metro was born," recalls his granddaughter Farah.

This personal touch wasn't just good service—it was strategic differentiation. In an era where most shoe shopping meant haggling with street vendors or dealing with indifferent government store clerks, Metro offered something revolutionary: respect, choice, and a shopping experience that made middle-class Indians feel valued.

The late 1970s brought new challenges. The Emergency had just ended, economic liberalization was still a distant dream, and foreign brands were virtually banned. But the Maliks saw opportunity where others saw obstacles. They began thinking beyond survival toward scaling. Rafique Malik had a clear vision of taking the store to a multi-chain format and further professionalising the business. During his grandfather's time, sales used to depend a lot on the owner's charisma, but it was during Rafique's tenure that managers got hired who would ensure the success of the sales. "Not having a son also pushed my father to professionalise the business from a very young age," comments Farah.

By 1980, Metro had survived its first quarter-century. It had weathered independence, partition's economic aftershocks, wars with Pakistan and China, the License Raj's stranglehold, and the Emergency's authoritarianism. More importantly, it had built something invaluable: a brand that Indians trusted, vendor relationships that would endure decades, and a second generation ready to think bigger. The foundation was set for what would become one of Indian retail's most audacious experiments—building multiple brands under one roof.

III. The Multi-Brand Strategy Emerges (1980s-2000s)

The 1980s found Rafique Malik facing a classic retail dilemma. Metro Shoes had established itself as a trusted name among Mumbai's middle class, but growth through single-brand expansion had natural limits. The Indian market was fragmenting—young consumers wanted fashion, families needed value, and the emerging affluent sought premium options. One brand couldn't be everything to everyone without diluting its identity.

The answer came in 1986 with a move that would define Metro's next four decades: launching Mochi. This wasn't just adding a new product line—it was creating an entirely distinct brand with its own identity, positioning, and eventually, stores. The name itself was clever, evoking traditional Indian craftsmanship while sounding modern enough for aspirational youth.

Metro started as a standalone shoe store in 1955 in Colaba, Mumbai. It was named after the Metro Cinema, which was located nearby. But Mochi would be different—edgier, younger, more experimental. The initial years were spent perfecting the brand's voice and product mix within Metro stores, learning what resonated with younger consumers without alienating Metro's core customer base.

The real breakthrough came in 2000 when Metro made another bold decision: opening the first standalone Mochi store. This moved Metro from being a retailer to becoming what the industry calls an MBO—Multi-Brand Outlet operator. The economics were counterintuitive. Why split your customer base? Why duplicate overhead costs? Why compete with yourself?

But Rafique Malik understood something profound about Indian consumers that many missed: they didn't just want products, they wanted identities. A young professional didn't want to shop where his father bought shoes. A teenager wanted a space that felt like it belonged to her generation. By creating distinct brands with distinct spaces, Metro could capture multiple segments without compromise.

The early 2000s validated this strategy spectacularly. While established players like Bata struggled with their monolithic identity, Metro was building a portfolio. Each brand could evolve independently, respond to its specific market, and fail without taking down the entire enterprise.

Then came 2009 and another strategic masterstroke: Walkway. Where Metro targeted the middle class and Mochi chased youth fashion, Walkway went after pure value. The tagline said it all: "More Shoes For Less." This wasn't about aspiration or fashion—it was about giving working-class Indians quality footwear at prices that didn't require saving for months.

The timing was perfect. India's economy was booming, rural incomes were rising, and millions were entering the formal economy for the first time. These consumers didn't need Italian leather or designer labels—they needed reliable, affordable shoes for their daily commute, their children's schools, their first job interviews. Walkway gave them dignity at a price point that worked.

What made this multi-brand strategy particularly brilliant was the backend integration. While customers saw three different brands, Metro ran them on unified systems—shared vendors, combined procurement, single warehousing, integrated logistics. This created economies of scale that independent brands couldn't match while maintaining the flexibility that large single-brand retailers lacked.

The vendor relationships, some dating back to the 1960s, became crucial competitive advantages. Metro could launch a new brand and immediately have access to production capacity, quality control, and favorable payment terms that would take a new entrant years to build. These weren't just suppliers—they were partners who had grown with Metro, understood its standards, and trusted its vision.

By 2005, Metro was operating what was essentially three different companies under one roof, each with distinct positioning: Metro (middle-class aspiration), Mochi (youth fashion), and Walkway (value). The organizational complexity was immense—different buying teams, different marketing strategies, different store designs, but shared operations and infrastructure.

Internal brand development accelerated. Da Vinchi emerged as Metro's premium sub-brand, offering Italian-inspired designs at Indian prices. J. Fontini became Mochi's upscale line. These weren't just label changes—each represented careful market segmentation, allowing Metro to capture more wallet share from existing customers while attracting new ones.

The multi-brand strategy also provided resilience. When the 2008 financial crisis hit and consumers traded down, Walkway boomed. When the economy recovered and aspiration returned, Mochi and Metro's premium lines surged. This portfolio approach smoothed out the volatility that killed single-brand retailers.

But perhaps the most underappreciated aspect of this period was Metro's discipline about what not to do. While competitors chased apparel, accessories, and even electronics, Metro stayed focused on footwear. While others rushed into franchising for rapid expansion, Metro maintained control through company-owned stores. While the market pushed for cheaper sourcing from China, Metro stuck with its Indian vendor base.

By 2010, the multi-brand strategy had transformed Metro from a regional retailer to a national force. The company wasn't just selling shoes—it was building a portfolio of brands that could evolve, adapt, and capture value across India's diverse and rapidly changing consumer landscape. The foundation was set for the next phase: massive physical expansion powered by an unlikely partnership with India's most celebrated investor.

IV. Building the Retail Empire (2000s-2015)

The year 2007 marked a watershed moment that would transform Metro from a successful regional player into a national powerhouse. One of the key moments in the company's journey was when the late ace investor Rakesh Jhunjhunwala showed faith in its potential. In 2007, Metro Brands sold a 15% stake to Jhunjhunwala, further fueling its growth.

Jhunjhunwala wasn't just any investor—he was India's Warren Buffett, a value investor with an uncanny ability to spot multi-baggers before they exploded. His investment philosophy was simple: find great businesses run by honest managements at reasonable valuations, then hold forever. In Metro, he saw all three. But more than capital, Jhunjhunwala brought credibility. His involvement signaled to vendors, landlords, and potential partners that Metro was destined for something bigger.

The capital infusion came at the perfect moment. India's retail landscape was exploding. Malls were sprouting across tier-2 cities, organized retail was finally taking share from street markets, and consumer financing was making aspirational purchases accessible. Metro had the brands and the blueprint—now it had the fuel to execute at scale.

The expansion that followed was methodical, almost surgical in its precision. During 2010-11 alone, the company opened 15 showrooms across Allahabad, Amritsar, Baroda, Chennai, Bangalore, Guwahati, Lucknow, Hyderabad, Mumbai, and Varanasi. This wasn't random geography—each city was chosen for specific demographics, purchasing power, and competitive dynamics. By year-end, Metro operated 121 stores across 38 major cities.

The real innovation was in store economics. While competitors built 10,000 square foot flagships that took years to break even, Metro perfected the 2,500-3,500 square foot format. Small enough to find prime locations at reasonable rents, large enough to showcase the full range, these stores could turn profitable within 18 months. The asset-light model meant no owned real estate, no massive capex, just long-term leases negotiated with the patience of a chess grandmaster.

In 2010, recognizing that digital was the future even if the present was still physical, Metro launched www.metroshoes.com. This wasn't a panicked response to e-commerce threats—it was a deliberate experiment in understanding online consumer behavior. The site initially served more as a catalog than a sales channel, but it gave Metro invaluable data about what customers searched for, what they wished existed, and where physical stores were missing opportunity.

The vendor ecosystem evolved into something remarkable during this period. Metro wasn't just buying shoes—it was co-creating them. Vendors would receive detailed briefs about trends, colors, and price points. Metro's merchandising teams would work with manufacturers on designs, materials, and quality standards. The result was a virtual integration without the capital requirements of actual manufacturing. Some vendor relationships stretched back three decades, built on handshakes and mutual growth rather than legal contracts.

Store operations became a science. Each location had detailed SOPs for everything from lighting angles to music volume. Staff training programs rivaled those of luxury brands—employees learned not just product features but customer psychology, body language reading, and the art of suggesting without pressuring. The average Metro salesperson could gauge a customer's budget within minutes and guide them to options that balanced aspiration with affordability.

The multi-brand portfolio created fascinating cross-selling opportunities. A family walking into Metro for school shoes might discover Walkway for daily wear. A young professional buying formal shoes at Metro might explore Mochi for weekend footwear. The brands competed for wallet share while expanding the total wallet itself.

Financial discipline underpinned everything. While revenue grew at 25-30% annually, Metro maintained EBITDA margins above 25%—almost unheard of in retail. The secret was operational leverage: the same team negotiating mall rentals handled all brands, the same warehouse served all stores, the same vendors supplied multiple brands. Fixed costs spread across a growing base while variable costs remained tightly controlled.

Jhunjhunwala's influence went beyond capital. He pushed for better governance, cleaner accounting, and preparation for eventual public listing. Board meetings became more structured, reporting became more rigorous, and strategic planning extended from quarters to years. The family business was becoming an institution without losing its entrepreneurial spirit.

Competition during this period was intensifying but fragmented. Bata remained formidable but struggled with brand perception. Liberty and Khadim's dominated regionally but couldn't scale nationally. International brands were entering but through distributors who lacked retail expertise. Metro's integrated multi-brand model gave it unique advantages—scale for negotiation, variety for customers, resilience against market shifts.

By 2015, Metro had built something remarkable: 400+ stores generating over ₹800 crore in revenue with industry-leading margins. But the Indian footwear market was entering a new phase. International brands wanted direct presence, consumers wanted global products, and Metro needed partnerships to stay relevant. The next chapter would test whether a traditional retailer could become the trusted partner for global giants entering the complex Indian market.

V. International Partnerships & Scaling (2015-2021)

The 2015 Crocs partnership announcement sent ripples through Indian retail. In 2015, Metro signed an agreement with Crocs to open exclusive Crocs stores in India, deepening a partnership that had actually commenced in 2008 with the introduction of Crocs products within Metro's multi-brand outlets. Here was an American brand known for its polarizing foam clogs—loved by healthcare workers, mocked by fashion critics—choosing a traditional Indian footwear retailer as its exclusive partner. The skeptics were numerous. Could Metro's customer base accept ₹3,000 plastic shoes? Would the brand's quirky identity clash with Metro's conservative positioning?

But Rafique Malik and his team saw what others missed. Crocs wasn't just about the classic clog—it had evolved into a lifestyle brand with sandals, flips, and fashion collaborations. More importantly, its comfort technology and washability made perfect sense for India's climate and lifestyle. The partnership structure was clever: Metro would open 30 Crocs stores in the first year and take the tally to 100 stores in the next 3 years, investing around ₹40 crores with expected target sales of over ₹100 crores during this period.

The Crocs rollout became a masterclass in localized global brand management. Metro didn't just transplant American stores into Indian malls. They adapted everything—from store sizes (smaller than US formats) to product mix (more sandals, fewer winter styles) to pricing architecture (introducing entry-level products for price-sensitive consumers). Staff were trained not just to sell but to educate—explaining Croslite technology, demonstrating customization with Jibbitz charms, converting skeptics through comfort trials.

From opening 1 store in 2015 to a Crocs retail network of 150+ stores in 2019, the growth was explosive. By 2024, Metro operated over 200 exclusive stores of Crocs across India. The success validated Metro's partnership thesis: international brands needed more than just a distributor—they needed a retail operator who understood Indian consumers, real estate dynamics, and operational complexity.

FitFlop followed a similar trajectory. The British brand's biomechanically engineered footwear appealed to India's growing health-conscious segment. Metro positioned it as premium comfort, targeting affluent women who wanted style without sacrificing foot health. The April 2022 launch of the first FitFlop exclusive store in Chennai marked another milestone in Metro's evolution as the partner of choice for international brands.

What made these partnerships work wasn't just execution—it was alignment. Metro offered international brands something unique: established infrastructure without legacy baggage. Unlike working with traditional distributors who might dilute brand equity through discounting, or attempting direct entry with its regulatory and operational nightmares, partnering with Metro meant accessing 400+ stores, trained staff, and proven systems while maintaining brand control.

The financial engineering behind these partnerships was sophisticated. Rather than paying large upfront franchise fees, Metro negotiated revenue-sharing agreements that aligned incentives. The brands provided product, marketing support, and global best practices. Metro provided real estate, operations, and local market expertise. Both shared in success, both bore risks. This model required less capital than acquisitions while generating higher returns than pure distribution.

By 2018, Metro's ambitions had expanded dramatically. The company announced plans to open 125 stores across Metro, Mochi, Crocs, and Walkway brands, with more penetration in tier-2 and tier-3 cities. This wasn't just geographic expansion—it was demographic expansion, bringing international brands to consumers who had never had access to them before.

The competitive landscape during this period was fascinating. While Metro was partnering with established global brands, new-age D2C brands were raising massive venture funding. Companies like Puma and Adidas were going direct. E-commerce was supposedly eating the world. Yet Metro's physical retail expansion accelerated. The company understood something fundamental: in categories like footwear where fit, comfort, and touch matter, physical retail wasn't dying—it was evolving.

Operational complexity multiplied exponentially. Metro was now running multiple brands with different positioning, different supplier bases, different marketing calendars, and different customer expectations. A Crocs store needed playful, colorful displays. A FitFlop store required sophisticated, wellness-oriented aesthetics. Metro stores maintained their traditional appeal while Mochi pushed fashion boundaries. Managing this portfolio required organizational capabilities that few Indian retailers possessed.

The real magic happened in the backend integration. While customers saw distinct brands, Metro's operations ran on unified platforms. The same warehouse management system handled inventory for all brands. The same point-of-sale system processed transactions. The same training academy prepared staff. The same data analytics platform provided insights. This operational leverage created cost advantages that pure-play brand stores couldn't match.

By 2021, Metro had transformed from a multi-brand retailer to something more complex and valuable: a retail platform that could successfully launch, scale, and manage both owned and partnered brands. The company had cracked the code that had eluded Indian retail for decades—how to bring global brands to Indian consumers profitably and sustainably. The stage was set for the next transformation: going public and institutionalizing this model for the next phase of growth.

VI. The IPO and Professionalization (2021)

December 10, 2021. The date marked a defining moment in Metro's 66-year journey. Metro Brands IPO bidding started from December 10, 2021 and ended on December 14, 2021. The shares got listed on BSE, NSE on December 22, 2021. Metro Brands IPO is a bookbuilding of ₹1,367.51 crores. The issue comprises of fresh issue of ₹295.00 crore and offer for sale of 2.15 crore shares.

The timing was both audacious and perfect. India's IPO market was on fire—Paytm had just crashed spectacularly after its November listing, Zomato had polarized investors, and sentiment was fragile. Yet here was Metro, a traditional retailer in an era of tech unicorns, asking investors to value it at ₹500 per share—a valuation that implied a market cap of over ₹13,500 crores.

But Metro had something the loss-making unicorns didn't: profits, and lots of them. In Fiscal 2019, 2020, and 2021 and in the six months ended September 30, 2020 and September 30, 2021, they recorded an EBITDA Margin of 27.72%, 27.51%, 21.36%, (7.57)% and 24.43%, respectively (on a consolidated basis). Even the COVID-impacted fiscal 2021 showed remarkable resilience—while revenues fell, the company remained solidly profitable.

The real story of the IPO, however, wasn't the financials—it was the professionalization that preceded it. Six months before the IPO, in a move that signaled serious intent about institutionalization, Metro Brands Limited appointed Nissan Joseph as its Chief Executive Officer effective July 1, 2021. Joseph, who holds a degree in business administration from the University of Western Sydney, joins the company from Philippines-based MAP Active & Planet Sports Inc., a lifestyle retailer in Southeast Asia, where he was the CEO since March 2020.

Joseph wasn't a random hire. During his 18 year-long experience in retail and brand management, he has held key roles for five years at Crocs. He has led various retail brands across the globe, including Foot Action, Payless Shoes, Crocs, and Planet Sports. Here was someone who understood both the brand Metro's biggest partnership and the complexities of Asian retail. His appointment sent a clear message: the family was serious about professional management.

The IPO structure itself was carefully crafted. The Malik family retained control while monetizing part of their stake. The fresh issue of ₹295 crores would fund expansion—new stores for Metro, Mochi, Walkway, and Crocs brands. The offer for sale allowed early investors, including Jhunjhunwala's estate, to partially exit while maintaining skin in the game.

Market reception was cautiously optimistic. The IPO got subscribed by 3.64 times at the end of the last day of the issue, with QIB portion subscribed 8.49 times, NII 3.02 times, and Retail 1.13 times. Not the blockbuster oversubscription of tech IPOs, but solid demand from institutional investors who understood the business.

The listing day, December 22, 2021, brought reality. Metro Brands IPO listed at a listing price of 493.55 against the offer price of 500.00. A slight discount—the market's way of saying "prove it." But for a company that had never raised external capital except from Jhunjhunwala, being public was victory enough.

What made the Metro IPO particularly interesting for students of Indian business was the governance transformation. The Company, incorporated in 1977, will continue to be helmed by its founding members Farah Malik Bhanji, Managing Director and Rafique A. Malik, Chairman. The family maintained strategic control while bringing in professional management—Joseph as CEO, along with other key hires including Kaushal Parekh who joined Metro Brands Limited in March 2012 and has been serving as the Chief Financial Officer of the company since May 2020.

The board composition evolved dramatically. Independent directors with deep retail and financial expertise joined. Audit committees, compensation committees, and risk management frameworks that had been informal became institutionalized. Quarterly reporting discipline replaced annual updates. The family business was becoming a public institution.

Joseph's early moves as CEO were telling. He didn't come in to revolutionize—he came to evolve. Mr. Joseph took on the role of CEO with a vision to build upon many years of financial discipline and operational rigor while expanding the magic of Metro. Store expansion accelerated but within the existing model. Technology investments increased but focused on operations rather than flashy consumer apps. The multi-brand strategy remained sacrosanct.

The IPO proceeds deployment was swift and strategic. New stores opened at an accelerated pace—not just in metros but in tier-2 and tier-3 cities where organized retail penetration was minimal. Each new store was profitable within 18 months, validating the unit economics. The market began to notice—maybe this traditional retailer knew something the D2C disruptors didn't.

For the Malik family, the IPO represented both an end and a beginning. The end of running Metro as a private fiefdom where decisions could be made over dinner. The beginning of Metro as an institution that could outlast its founders. The professionalization wasn't just about bringing in outside talent—it was about creating systems, processes, and governance structures that would ensure Metro's next 70 years were even more successful than its first.

By early 2022, Metro had successfully navigated one of the most challenging transitions in business—from family to professional management, from private to public, from founder-led to institution—without losing what made it special. The stage was set for the next phase: leveraging this institutional strength to capture the massive opportunity in India's footwear market.

VII. Modern Era: Omnichannel & New Partnerships (2021-Present)

The post-IPO era began with a bang. In April 2022, the 1st FitFlop EBO store was launched in Chennai. It reached 600- store landmark. This wasn't just another store opening—it was validation of Metro's evolved strategy. FitFlop, the UK-based wellness footwear brand with its biomechanically engineered products, represented Metro's push into the premium comfort segment, a category exploding globally as consumers prioritized health and wellness post-pandemic.

The Chennai location choice was strategic. Footwear retail chain Metro Brands Limited, which entered into a strategic partnership with UK-based lifestyle and wellness footwear brand FitFlop early this year, has opened the first exclusive FitFlop store in Chennai. The Indian footwear distributor will now exclusively retail and distribute FitFlop footwear in India across various platforms and channels. Southern markets had shown higher receptivity to international brands and premium pricing, making it the perfect testing ground.

But the real game-changer came in December 2023 with a move that stunned the industry. During FY 2022-23, the Company acquired 100% stake in Metro Athleisure Limited (MAL), which consequently was made a wholly owned subsidiary of the Company effective from December 1, 2023. The Company opened 144 new stores including relocation of 13 existing stores, which reached 739 at the end of the FY23. This acquisition brought with it something precious: the exclusive rights to FILA in India and ownership of the Proline sports brand.

The FILA partnership represented Metro's biggest bet yet on the athleisure revolution sweeping India. Unlike Crocs or FitFlop, FILA was a full lifestyle brand—apparel, accessories, and footwear. It required different capabilities, different vendor relationships, different marketing strategies. But it also opened up a market opportunity worth thousands of crores as Indians embraced sportswear not just for exercise but as everyday fashion.

Then came the announcement that sent Metro's stock soaring: Foot Locker was coming to India. As of now, MBL plans to open two to six Foot Locker stores in two to three cities in the current fiscal, the company revealed in November 2023 when announcing its multi-decade licensing agreement with the US-based athletic shoes and apparel retailer. Foot Locker, Inc., a $8.759 billion powerhouse, is considered a pioneer in global sneaker culture since its inception in 1989.

The Foot Locker partnership was different from anything Metro had done before. New York-based athletic shoes and apparel retailer Foot Locker, known for its curated selection of top brands and deep community, will make its omnichannel debut in India on 19 October with Metro Brands Ltd. operating Foot Locker physical stores and Nykaa Fashion operating the e-commerce business. The first Foot Locker store in India will open at Nexus Select City Walk in New Delhi.

This tri-party structure—Metro handling physical retail, Nykaa managing e-commerce, and Foot Locker providing the brand—was unprecedented in Indian retail. It showed Metro's maturity and confidence, willing to share the opportunity rather than trying to do everything itself. The partnership also signaled Metro's evolution from a footwear retailer to a platform that could orchestrate complex multi-party arrangements.

The numbers told the story of transformation. As of December 31, 2024, the Company operated 895 Stores across 203 cities spread across 31 states and union territories in India. From 598 stores at IPO to nearly 900 in three years—Metro was adding a store every three days. But this wasn't reckless expansion. Each store maintained the discipline of 18-month profitability targets. The multi-brand portfolio provided natural hedging—if one brand underperformed, others compensated.

Digital transformation accelerated dramatically post-IPO. While Metro maintained its commitment to physical retail, recognizing that footwear remained a touch-and-feel category, it invested heavily in omnichannel capabilities. Click-and-collect, endless aisle, virtual try-ons—Metro adopted technologies that enhanced rather than replaced the store experience. The company's e-commerce platforms for Metro, Mochi, and Walkway were upgraded, while partnerships with Myntra, Amazon, and Flipkart expanded reach without cannibalizing store sales.

The competitive dynamics during this period were fascinating. Bata continued its slow decline, unable to shake its uncle-ji image despite repeated rebranding attempts. Relaxo dominated the value segment but struggled to move upmarket. Campus Activewear's IPO showed investor appetite for footwear stocks but also highlighted execution challenges in scaling. International brands entering directly discovered what Metro already knew—India's complexity required local expertise.

Metro Brands retails footwear under its own brands of Metro, Mochi, Walkway, Da Vinchi and J. Fontini, as well as third-party brands such as Footlocker, Crocs, Fitflop, Fila, Skechers, Puma, New Balance, Nike and Adidas which complement its in-house brands. As of December 31, 2024, the Company operated 895 Stores across 203 cities spread across 31 states and union territories in India.

The organizational transformation under Nissan Joseph's leadership was profound but subtle. The company recently strengthened its management by onboarding retail veteran Mohit Dhanjal as its chief operating officer and Nadadeep Jayakar as the business head of Foot Locker India. Professional managers were brought in for key functions. Technology investments focused on backend operations—inventory management, demand forecasting, supply chain optimization. The family remained involved but increasingly focused on strategy rather than operations.

What made Metro's modern era particularly impressive was its ability to maintain margins while scaling rapidly. Most retailers face margin compression during expansion phases—new stores take time to mature, marketing costs increase, operational complexity grows. Metro defied this pattern, maintaining EBITDA margins above 20% even while adding hundreds of stores and multiple new brands. The secret was operational leverage—the same warehouse could service multiple brands, the same management team could oversee different formats, the same vendor relationships could supply various product lines.

By 2024, Metro had evolved from a footwear retailer into something more complex and valuable—a multi-brand retail platform capable of launching, scaling, and managing both owned and partnered brands across physical and digital channels. The company that started as a single shoe store in Colaba had become the partner of choice for global brands entering India and the employer of choice for retail talent. The transformation was complete, but the journey was just beginning.

VIII. Business Model Deep Dive

Metro's business model is deceptively simple on the surface yet remarkably sophisticated in execution. They sell retail footwear under the brands of Metro, Mochi, Walkway, Da Vinchi and J. Fontini, as well as certain third-party brands such as Crocs, Skechers, Clarks, Florsheim, and Fitflop, which complement the in-house brands. But beneath this straightforward description lies an intricate machine that has cracked the code of profitable retail in India.

The foundation is the COCO model—Company-Owned, Company-Operated stores. While competitors chase asset-light franchising, Metro maintains iron-clad control over customer experience. Every store manager is a Metro employee. Every sales associate follows Metro training. Every display follows Metro guidelines. This control comes at a cost—higher capital requirements, greater operational complexity—but delivers something priceless: consistency. A customer walking into a Metro store in Guwahati gets the same experience as one in Mumbai.

The multi-brand outlet (MBO) strategy is where Metro's genius truly shines. Rather than opening separate stores for every brand segment, Metro, Mochi, and Walkway stores carry multiple brands, creating a one-stop-shop for footwear needs. This dramatically improves store economics—higher transaction values, better inventory turns, lower rental costs per brand. A family visiting for children's school shoes might leave with formal footwear for dad, sandals for mom, and sports shoes for the teenager.

Metro derives about 59% of its sales from Metro stores, followed by 33% from Mochi showrooms, 5% from Walkway, and the rest 3% from Crocs stores. This portfolio balance isn't accidental—it's carefully calibrated to maximize market coverage while minimizing cannibalization. Metro stores target established middle-class consumers in prime locations. Mochi captures fashion-forward youth in malls and high streets. Walkway serves value-conscious buyers in tier-2 and tier-3 cities. Each brand has distinct positioning, distinct locations, and distinct customer bases.

The vendor ecosystem is Metro's hidden moat. The company works with 250+ footwear vendor partners, some relationships stretching back four decades. These aren't typical buyer-supplier relationships—they're partnerships. Metro provides designs, trends, and specifications. Vendors provide manufacturing expertise and capacity. Both share risks and rewards. This model allows Metro to introduce 2,000+ new designs annually without owning a single factory.

The asset-light philosophy extends beyond manufacturing. Store sizes are optimized at 2,500-3,500 square feet—large enough for range display, small enough for prime locations at reasonable rents. Lease terms are typically 9-15 years with built-in escalations, providing visibility and stability. No owned real estate means no capital locked in property, no exposure to real estate cycles. Every rupee of capital goes toward inventory and store fitouts that directly drive sales.

Inventory management is where art meets science. The average inventory holding period is 120-140 days, seemingly high for retail. But this reflects Metro's buying model—purchasing entire seasonal ranges upfront for better pricing, then flowing merchandise to stores based on real-time sales data. The centralized warehouse in Mumbai serves as the nerve center, using algorithms to predict demand and optimize distribution across 900+ stores.

The technology infrastructure, while not visible to customers, is surprisingly sophisticated. A unified ERP system connects every store, tracking every transaction in real-time. Point-of-sale data feeds into demand forecasting models. RFID tags enable accurate inventory tracking. Mobile POS systems allow sales associates to check stock across the entire network. This isn't cutting-edge Silicon Valley tech—it's practical, proven systems that work reliably at scale.

Pricing architecture is carefully orchestrated across brands. Metro occupies the ₹1,000-3,000 range for most products, targeting middle-class aspiration. Mochi pushes slightly higher at ₹1,500-4,000, capturing fashion premiums. Walkway sits at ₹500-1,500, competing with unorganized retail on value. Premium sub-brands like Da Vinchi and J. Fontini can command ₹3,000-6,000, while international brands like Crocs and FitFlop stretch to ₹5,000+. This ladder allows Metro to capture customers across income segments and life stages.

The margin structure reveals the model's elegance. Gross margins of 55-60% seem high but reflect the value Metro adds—curation, convenience, assurance, after-sales service. Operating expenses of 30-35% of sales fund store rentals, staff salaries, and marketing. EBITDA margins of 20-25% are among the highest in global footwear retail. Net margins of 12-15% provide ample cash generation for growth without external funding.

Marketing spend is surprisingly low—less than 2% of sales. Metro doesn't need celebrity endorsements or massive advertising campaigns. The stores themselves are the marketing—prime locations with high foot traffic, attractive displays, and most importantly, satisfied customers who return and recommend. Word-of-mouth drives 60% of new customer acquisition. This organic growth is slower but more sustainable than paid acquisition.

Staff training is where Metro differentiates from both organized and unorganized competition. Every sales associate undergoes 100+ hours of initial training covering product knowledge, customer psychology, and sales techniques. The "Metro Way" emphasizes consultation over pushing—understanding customer needs, suggesting appropriate options, ensuring proper fit. Sales incentives are structured to reward customer satisfaction scores alongside sales targets. Average sales per square foot of ₹6,000-7,000 is 2-3x industry averages, driven largely by superior salesmanship.

The omnichannel evolution hasn't disrupted this model—it's enhanced it. Online sales remain under 10% of total revenue, but digital influences 40% of store sales through research, reviews, and click-and-collect. Metro's approach is pragmatic—use digital to drive footfall rather than replace stores. The endless aisle concept lets stores display core ranges while offering extended selections online. Returns are handled seamlessly across channels, building trust.

Working capital management showcases operational excellence. Vendor payment terms of 60-90 days, combined with customer cash sales, create negative working capital cycles. Metro effectively uses vendor financing to fund growth. Inventory turns of 2.5-3x annually are healthy for footwear retail. Cash conversion cycles of 30-45 days mean Metro generates cash while growing, a rare combination in retail.

The scalability of this model is its ultimate vindication. Whether operating 100 stores or 1,000, the core economics remain consistent. Each new store requires ₹1.5-2 crore in fitout investment, achieves breakeven in 12-18 months, and generates 20%+ store-level EBITDA margins at maturity. This predictability allows Metro to expand confidently, knowing that growth translates directly to profitability.

IX. Financial Analysis & Market Position

The numbers tell a story of remarkable consistency in an industry known for volatility. In Fiscal 2019, 2020, and 2021 and in the six months ended September 30, 2020 and September 30, 2021, they recorded an EBITDA Margin of 27.72%, 27.51%, 21.36%, (7.57)% and 24.43%, respectively (on a consolidated basis). Even the COVID-impacted six months showing negative margins bounced back to mid-20s within quarters—resilience that few retailers globally demonstrated.

The current financial position is even more impressive. Metro Brands Ltd has a market capitalisation of Rs 33,229 crore, trading at approximately ₹1,220 per share as of late 2024. The 52-week high share price is Rs 1,430.10 and 52-week low share price is Rs 890.30, showing relatively low volatility for a consumer discretionary stock. On a consolidated basis, Metro Brands Ltd reported strong performance for the recent quarter, with margins expanding despite inflationary pressures.

Revenue composition reveals strategic evolution. While footwear remains 95% of sales, average selling prices have increased from ₹800 in 2015 to ₹1,450 in 2024—not through inflation but through premiumization. Customers aren't just buying more shoes; they're buying better shoes. The shift from need-based to aspiration-based consumption is Metro's core thesis playing out in real-time.

Comparing Metro to listed peers illuminates its unique position. Bata India, with its 1,500+ stores, generates similar revenue but at half the margins. The difference? Bata's legacy infrastructure, aging brand perception, and dependence on own manufacturing. Relaxo Footwears shows higher growth but relies heavily on the value segment, vulnerable to commodity inflation and competitive intensity. Campus Activewear, the recent IPO darling, trades at premium valuations but lacks Metro's multi-brand resilience.

International comparisons are equally telling. Foot Locker globally operates at 7-8% EBITDA margins despite premium positioning. DSW in the US manages 5-6% margins. European retailers like Deichmann achieve 10-12% at best. Metro's 20-25% margins aren't just industry-leading in India—they're among the highest globally for scaled footwear retailers. The India opportunity combined with Metro's execution creates this margin exceptionalism.

Return metrics validate capital allocation. Return on equity consistently exceeds 25%, remarkable for a retail business. Return on capital employed hovers around 30%, suggesting efficient use of resources. Asset turnover of 2.5x multiplied by net margins of 12-15% drives these superior returns. The DuPont analysis reveals no single magic bullet—it's excellence across operations, margins, and capital efficiency.

Cash flow generation is perhaps Metro's most underappreciated quality. Operating cash flow consistently exceeds net profit due to favorable working capital dynamics. Free cash flow after maintenance capex runs at ₹300-400 crore annually, funding expansion without external capital. The company has maintained a virtually debt-free balance sheet post-IPO, with cash exceeding ₹500 crore.

Valuation multiples reflect quality but also embed high expectations. Trading at 35-40x trailing earnings and 25-30x forward earnings, Metro commands premium valuations. The EV/EBITDA multiple of 20-25x compares to 10-15x for Bata and 15-20x for Relaxo. Price-to-book of 8-10x seems expensive until you consider the asset-light model means book value understates true economic value.

The market values Metro not just for current performance but future optionality. Each new brand partnership could add ₹500-1,000 crore in revenue. Store expansion runway of 2,000+ stores implies doubling potential. Margin expansion through premiumization and operational leverage could add 200-300 basis points. The sum-of-the-parts valuation—existing business plus growth options—justifies premium multiples.

Quarterly earnings volatility is minimal by retail standards. Q1 (April-June) and Q3 (October-December) are traditionally strong, driven by summer and festival demand respectively. Q2 monsoons impact footfall but not dramatically. Q4 is the clearance quarter but disciplined inventory management prevents margin erosion. This predictability allows investors to focus on long-term trends rather than quarterly noise.

The shareholding pattern post-IPO shows institutional validation. The promoter group holds 55-60%, providing stability and alignment. Domestic institutions own 15-20%, including mutual funds seeing Metro as a consumption play. Foreign investors hold 10-15%, attracted by the India growth story. Retail investors comprise 10-15%, many holding since IPO. This balanced ownership structure prevents excessive volatility.

Dividend policy balances growth and returns. With payout ratios of 20-25%, Metro returns cash to shareholders while retaining majority for expansion. The dividend yield of 0.5-0.8% won't attract income investors, but the token dividend signals confidence. Share buybacks remain unexplored but could emerge as capital allocation lever once expansion slows.

The financial risk profile is remarkably low for retail. No debt means no refinancing risk. Inventory obsolescence is minimal given fast-moving products. Rental escalations are contractual and predictable. Vendor concentration is low with 250+ suppliers. Customer concentration is negligible with millions of transactions. The only real risk is execution—can Metro maintain quality while scaling rapidly?

Looking at Metro's financials isn't just about numbers—it's about understanding a business model that has solved retail's fundamental challenge: how to grow profitably. Every metric—from margins to returns to cash generation—validates the model's sustainability. The premium valuation reflects not hope but evidence, not potential but performance. In a market full of story stocks, Metro is that rare creature: a quality compounder hiding in plain sight.

X. Playbook: Lessons for Founders & Investors

Metro's seven-decade journey offers a masterclass in building enduring value in emerging markets. The lessons aren't just theoretical—they're battle-tested strategies that have survived socialist economics, liberalization upheaval, e-commerce disruption, and global pandemics.

Lesson 1: Multi-Brand Portfolios as Risk Mitigation The decision to create Mochi and Walkway wasn't about ego or empire-building—it was recognition that mono-brand dependency in diverse markets like India is dangerous. Each brand serves as a natural hedge. When Mochi's fashion-forward positioning struggled during COVID, Walkway's value proposition resonated. When Metro stores in prime locations faced high rentals, Crocs' premium pricing justified the costs. Founders should consider: instead of betting everything on one brand, can you create a portfolio that captures different segments, occasions, or price points?

Lesson 2: Asset-Light Doesn't Mean Capability-Light Metro owns no factories, no real estate, minimal technology infrastructure. Yet it controls the entire value chain through relationships, knowledge, and systems. The 250+ vendor network isn't just suppliers—they're extensions of Metro's capability. The lesson: identify what truly drives competitive advantage in your industry. Own those elements fiercely. Everything else can be partnered, outsourced, or rented.

Lesson 3: Family Businesses Can Professionalize Without Losing Soul The Malik family's journey from founder-operator to professional management is textbook succession planning. Bringing in Nissan Joseph as CEO wasn't admission of failure—it was recognition that different stages require different leadership. The family retained strategic control while empowering professional management for operations. Crucially, the values and culture remained intact. Family businesses globally struggle with this transition; Metro shows it's possible with humility and planning.

Lesson 4: Partnerships Require More Than Contracts Metro's success with Crocs, FitFlop, and Foot Locker isn't just about signing agreements—it's about becoming the partner of choice. This means investing in brand building even when you don't own the brand. It means protecting pricing discipline when competitors discount. It means saying no to short-term opportunities that could damage long-term relationships. For founders, the lesson is clear: in a connected world, your ability to partner determines your ability to scale.

Lesson 5: Operational Excellence Beats Strategic Brilliance Metro's strategy isn't revolutionary—multi-brand retail exists globally. The magic is in execution. Every store achieving profitability in 18 months. Inventory turns improving despite SKU proliferation. Same-store sales growth consistently positive. This isn't strategy—it's operational excellence compounded daily. Founders often chase the next big strategic move when the answer lies in executing basics better than anyone else.

Lesson 6: Patient Capital Enables Long-Term Thinking Rakesh Jhunjhunwala's 14-year investment (2007-2021) provided more than money—it provided patience. Metro could focus on building sustainable advantages rather than showing quarterly growth. Store expansion followed unit economics, not investor pressure. Brand building took precedence over margin expansion. The lesson for founders: choose investors who understand your business cycle and share your time horizon.

Lesson 7: Technology as Enabler, Not Disruptor While competitors panicked about e-commerce disruption, Metro quietly built omnichannel capabilities. Technology investments focused on operations—inventory management, demand forecasting, supply chain optimization. Customer-facing technology enhanced store experience rather than replacing it. The lesson: technology should amplify your core strengths, not distract from them.

Lesson 8: Managing Complexity Requires Simplicity Operating 900+ stores across 200+ cities with 10+ brands and 20,000+ SKUs is monumentally complex. Metro manages this through radical simplification—standardized processes, clear metrics, consistent training. Complexity is inevitable in scaling; the answer isn't avoidance but systematic simplification of core processes.

Lesson 9: Culture Scales Through Systems, Not Personalities The "Metro Way" of customer service that Malik Tejani embodied in the 1950s persists across 900 stores today—not through his presence but through systems that encode those values. Training programs, incentive structures, and operational processes all reinforce customer-first culture. Founders must transition from personality-driven to process-driven culture before scaling.

Lesson 10: Market Creation Beats Market Competition Metro's expansion into tier-2 and tier-3 cities isn't about competing with existing players—it's about creating markets where organized retail didn't exist. Bringing international brands to cities that had never seen them. Converting unorganized retail customers to branded products. The biggest opportunities often lie not in competing for existing demand but creating new demand.

For Investors: Pattern Recognition Metro exhibits patterns that predict long-term value creation: founder-led but professionally managed, asset-light but control-heavy, growth-focused but margin-disciplined, technology-enabled but human-centered. These paradoxes aren't contradictions—they're the hallmarks of businesses that compound value over decades.

The Ultimate Lesson: Patience Pays From 1955 to 2021, Metro went from one store to IPO. That's 66 years of patient building. In an era of unicorns and rapid exits, Metro reminds us that the biggest outcomes often require the longest horizons. Whether you're a founder building or an investor backing, the Metro playbook suggests that sustainable value creation isn't about speed—it's about building something that endures.

XI. Analysis & Future Outlook

The bear case for Metro Brands writes itself in an era of digital disruption. E-commerce platforms like Amazon and Flipkart offer infinite selection, price transparency, and doorstep delivery. D2C brands bypass traditional retail, building direct customer relationships with 90% gross margins. Gen-Z consumers prioritize experiences over products, sustainability over consumption. Physical retail globally is in structural decline. Why would India be different?

The bears point to warning signs. Metro's e-commerce revenue remains under 10% despite years of investment. Younger consumers show little loyalty to traditional brands, chasing Instagram trends and influencer recommendations. Store expansion costs are rising—prime real estate is scarcer, rentals are increasing, and quality staff harder to find. International brands increasingly prefer direct entry over partnerships, cutting out intermediaries like Metro.

Competition is intensifying from unexpected directions. Reliance Retail's footwear ambitions threaten Metro's wholesale relationships. Quick-commerce platforms like Blinkit and Zepto are adding fashion categories. Social commerce through WhatsApp and Instagram bypasses traditional retail entirely. Chinese manufacturers sell directly through Meesho and Club Factory successors. The moats that protected Metro for decades appear to be eroding.

But the bull case rests on structural realities that technology can't wish away. They target the economy, mid and premium segments in the footwear market, which together are expected to grow at a higher rate compared to the total footwear industry between Fiscal 2020 and 2025. India's footwear market, currently at $15 billion, is projected to reach $40 billion by 2030. Per capita footwear consumption at 1.7 pairs annually compares to 3-4 pairs in China and 7-8 pairs in developed markets. The growth runway is massive.

The organized retail penetration story remains early innings. Unorganized players still account for 65% market share in footwear. Every year, millions of Indians shift from unbranded to branded, from street vendors to organized retail. Metro isn't competing with e-commerce—it's converting unorganized demand. In tier-2 and tier-3 cities where Metro is expanding, the competition isn't Amazon—it's the local mochi sitting on the street corner.

Demographics provide tailwinds for decades. India adds 10 million people to its workforce annually. Rising incomes drive premiumization—consumers who bought one pair of functional shoes now buy multiple pairs for different occasions. Urbanization continues relentlessly, with 40% of Indians expected to live in cities by 2030. Each trend directly benefits organized footwear retail.

Metro's competitive advantages are strengthening, not weakening. The vendor network built over decades can't be replicated with venture capital. Store-level economics that deliver 20% margins come from operational excellence, not financial engineering. Brand partnerships with Crocs, FitFlop, and Foot Locker create barriers—these brands chose Metro after evaluating every option.

The omnichannel evolution positions Metro perfectly for retail's future. While pure-play e-commerce companies burn cash on customer acquisition, Metro leverages stores for discovery and digital for convenience. While D2C brands struggle with distribution, Metro offers instant access to 900+ prime locations. The future isn't digital or physical—it's both, and Metro is building for that reality.

New growth levers are just being unlocked. The sports and athleisure opportunity through Foot Locker and FILA could add ₹2,000 crore in revenue. International expansion into Bangladesh, Sri Lanka, and Nepal offers replication potential. Private label development could improve margins while maintaining price points. Category extensions into bags, accessories, and apparel leverage existing infrastructure.

The sustainability angle, often overlooked, could become a major advantage. Metro's model of quality products lasting years contrasts with fast fashion's disposability. Local sourcing reduces carbon footprint compared to Chinese imports. The multi-brand store format is inherently more sustainable than single-brand boutiques. As ESG considerations influence purchasing, Metro's traditional model looks progressive.

Financial flexibility provides optionality. With ₹500+ crore in cash and no debt, Metro could accelerate expansion, acquire competitors, or return capital to shareholders. The ability to fund growth internally means no dilution, no covenant restrictions, no refinancing risks. In a rising rate environment, debt-free retailers have massive advantages.

Management quality under Nissan Joseph has exceeded expectations. Professional managers often struggle in founder-led companies, but Joseph has balanced respect for legacy with push for innovation. The next generation of the Malik family appears engaged but not interfering, committed but not controlling. This governance balance is rare in Indian family businesses.

The valuation debate misses the point. Yes, Metro trades at premium multiples. But quality compounds, and Metro has demonstrated quality across cycles. Paying 30x earnings for a business growing at 20% with 25% ROE and minimal risk isn't expensive—it's rational. The market is pricing in not just growth but sustainability of growth.

Looking forward, Metro's trajectory seems clear: steady store additions (100-150 annually), gradual margin expansion through premiumization, strategic brand partnerships, and occasional tuck-in acquisitions. No moonshots, no pivots, no transformation—just relentless execution of a proven model. In a market obsessed with disruption, Metro's promise is continuity.

The future of Indian retail won't be winner-take-all. E-commerce will capture share, D2C brands will proliferate, and new models will emerge. But footwear's tactile nature, India's diverse markets, and consumers' social shopping preferences ensure physical retail's relevance. Metro isn't fighting the future—it's building for a future where multiple models coexist, and execution excellence matters more than business model innovation.

For investors, Metro represents a bet on Indian consumption without the volatility of discretionary categories or execution risk of new models. For competitors, Metro sets the benchmark for operational excellence and strategic patience. For students of business, Metro proves that sustainable value creation comes not from revolution but from evolution—patient, persistent, profitable evolution.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube