Meesho: The Unlikely Conqueror of Bharat

I. Introduction: The "Anti-Amazon" of India

Picture a small, sun-bleached lane in Sitapur, a district town in Uttar Pradesh that most Indians cannot find on a map. Inside a two-room concrete house, a woman in her early thirties is hunched over a battered smartphone. She is not scrolling Instagram. She is running a business. On the screen are thumbnails of polyester kurtas, plastic kitchen organisers, and "imported-look" handbags, each tagged with a price ending in nine. She forwards the images to a WhatsApp group of fifty-odd women — neighbours, cousins, the wives of her husband's friends — and waits. By evening, she has sold eleven items. She has never met the suppliers in Surat who stitched the kurtas. She has never met the courier in Bhopal who will deliver them. She has, in fact, never used a credit card.

This is the customer that built मीशो Meesho.

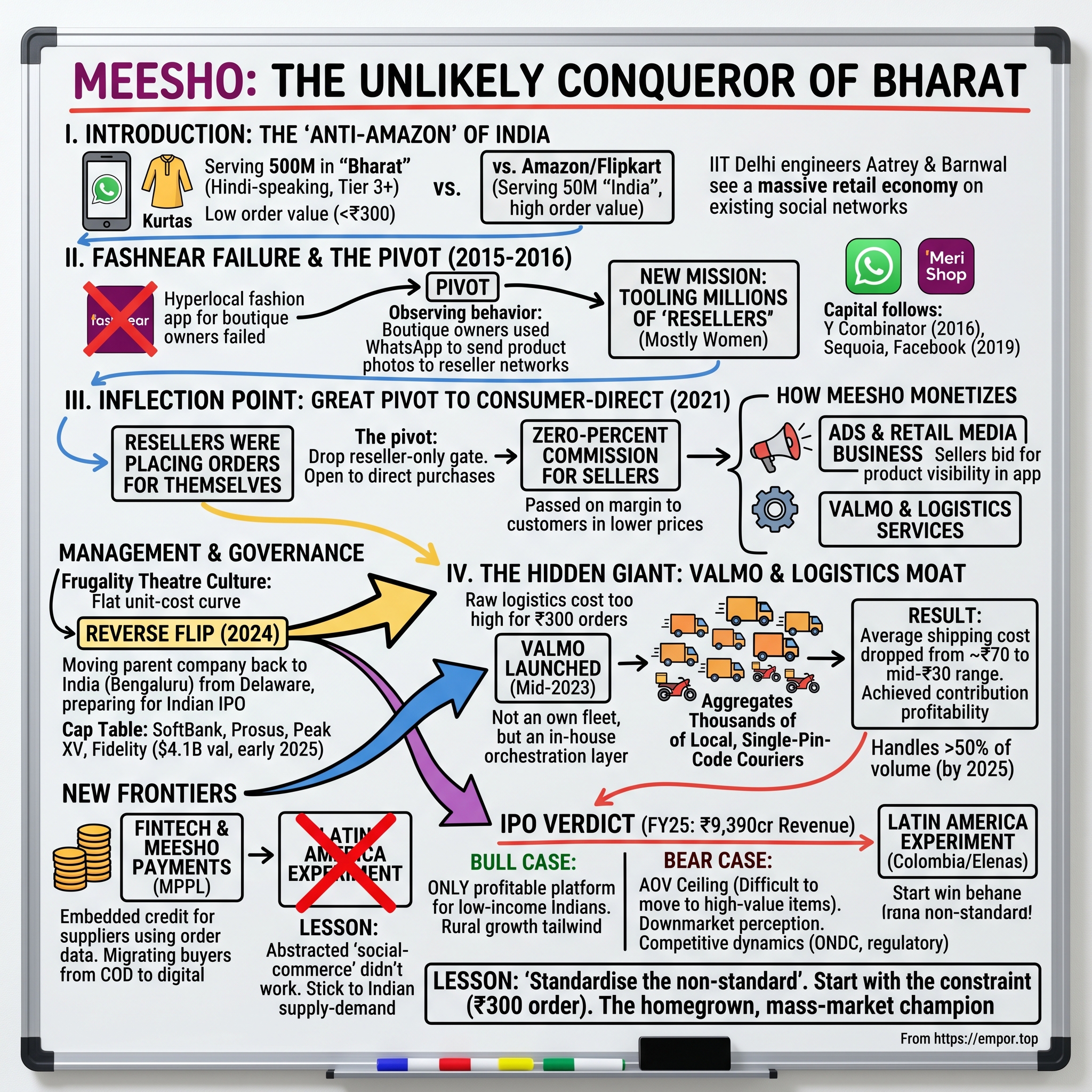

The mainstream India story of the last decade was supposed to belong to फ्लिपकार्ट Flipkart and Amazon India — two heavyweights that together absorbed more than thirty billion dollars of patient foreign capital chasing the country's top fifty million consumers.[^1] Both companies built warehouse empires modelled on Seattle and Bentonville, hired armies of MBAs, and discounted Apple iPhones and Samsung televisions into oblivion. They were, in the language of Indian marketers, fighting for इंडिया India — the English-speaking, card-carrying, metro-dwelling slice of the country that looked, from a balance sheet perspective, very much like the West.

Meanwhile, the next five hundred million Indians — भारत Bharat, the Hindi-speaking, cash-preferring, tier-three-and-below interior — were a footnote. Their average online order was under three hundred rupees. Their internet was a 2G connection wedged between dead spots. They did not trust card transactions. They returned thirty percent of what they ordered. To a Bentonville-trained merchandiser, they were not a market. They were a margin disaster.

Two engineers from IIT Delhi looked at the same picture and saw something different. Vidit Aatrey and Sanjeev Barnwal saw a half-billion-person retail economy that already worked — it just worked on WhatsApp groups, on Facebook reseller pages, on the back of the second-hand smartphone that one daughter shared with her mother and aunt. The trick, they decided, was not to drag this economy into a Western-style marketplace. The trick was to build a Western-style marketplace that bent, in every conceivable way, around what the existing economy already did.

The result, as of 2026, is a company that has been variously described as the most downloaded shopping app in the world,1 the only Indian e-commerce platform to operate at a zero-percent commission, and — depending on which set of cap-table investors one trusts — somewhere between a four-billion-dollar and a ten-billion-dollar enterprise on its way to a public listing.[^3] Backed by SoftBank, Prosus, Meta, Fidelity, and a long bench of venture firms, Meesho has executed what may be the most successful counter-positioning play in Indian internet history.

This is the story of how a failed hyperlocal fashion app became the operating system of small-town India, how a "hidden" logistics subsidiary called वालमो Valmo quietly rewired the unit economics of low-ticket commerce, and how a "reverse flip" from Delaware back to Bengaluru positioned Meesho for what may become the most-watched Indian tech IPO of the decade. It is also, in a less flattering frame, a cautionary tale about the limits of a model built on three-hundred-rupee orders. We will cover both. As Ben and David like to say on Acquired — let's get into it.

II. The FashNear Failure and the Pivot to Social Commerce

The founding myth of Meesho does not begin in a garage. It begins in a Powai apartment, in late 2015, with two twenty-six-year-olds who had quit jobs that their parents in Bihar and Uttar Pradesh did not entirely understand. Vidit Aatrey, an IIT Delhi mechanical engineering graduate, had spent two years at InMobi before resigning to start something.2 Sanjeev Barnwal, a fellow IITian who had been at Sony in Tokyo, joined him on the bet. Their idea — christened FashNear — was a hyperlocal fashion discovery app. Open it, geo-fence yourself to a three-kilometre radius, browse the inventory of the boutiques in your neighbourhood, and either pick up your purchase or have it delivered.

It was, in the polite phrasing of the venture community, a "thesis-first" product. The thesis sounded reasonable on a whiteboard. Indian fashion was hyperlocal, suppliers were small, discovery was broken. What FashNear quickly discovered, however, was that the boutiques the founders had built the app for were not, in any meaningful sense, online merchants. They did not photograph inventory. They did not track stock. They certainly did not respond to push notifications from a venture-backed startup that wanted them to upload SKUs at midnight. After roughly six months of paddling, Aatrey and Barnwal had a few hundred users, a high churn rate, and a slowly tightening seed runway.

The pivot moment is the part of the story that has been retold in every Indian founder interview since. While doing customer development calls — actually visiting the boutique owners and asking them where their orders came from — the two founders noticed that the boutique owners were not, in fact, using FashNear. They were using WhatsApp. A boutique in Jaipur would forward a photograph of a लहंगा lehenga to a network of housewives in Delhi NCR; the housewife, in turn, would forward it to her own WhatsApp group, mark up the price by thirty to a hundred rupees, and pocket the difference. There was no app, no marketplace, no payment gateway, no logistics. There was only social trust and the world's most ubiquitous messaging service.

That, the founders decided, was the real business. Not building demand for boutiques — but tooling the millions of "resellers," most of them women, most of them with no formal employment, who were already doing the demand-generation themselves. In late 2016 and early 2017, FashNear was wound down. The new product was a thin app that let any reseller browse a catalogue of supplier-listed inventory, share product images directly to WhatsApp with their own markup baked in, and let the platform handle the boring bits — payments, fulfilment, returns. The new name was Meesho, a contraction of "Meri Shop" — "my shop" in Hindi.3

The model resonated immediately with two constituencies that almost no other Indian internet company was serving. The first was the supplier side — small manufacturers in Surat, Tiruppur, Ludhiana, and Jaipur, who had spent years getting squeezed by middlemen and had no real route onto Flipkart or Amazon, whose listing fees and brand norms were built for a different kind of seller. The second was the demand side — the resellers, who could now run a side income without inventory risk, without learning a website, and without leaving the WhatsApp interface they already lived in.

Capital followed. Meesho was admitted into Y Combinator's summer 2016 batch, becoming one of the first Indian companies to make it into the program with an explicitly Bharat-focused thesis. Sequoia (now Peak XV), SAIF Partners, and Venture Highway came in. And in 2019, the company made global headlines as the first Indian startup to receive a direct equity investment from Facebook — a roughly twenty-five-million-dollar cheque that, even more than the money itself, validated the social-commerce thesis to the broader market.4 At that point Meesho was processing tens of millions of orders annually through hundreds of thousands of resellers and was beginning to think about the problem that would define the next phase of the company: what to do when your own users stop wanting middlemen.

III. Inflection Point: The Great Pivot to Consumer-Direct

By 2020, the social-commerce thesis was working — and quietly breaking. Working, because Meesho had become genuinely large; the reseller network had crossed several million participants, and the company was processing orders from corners of the country that Amazon's logistics partner had never heard of. Breaking, because the founders had begun to notice an awkward pattern in their own analytics. Resellers were placing orders for themselves. Or for one specific aunt. Or for a single neighbour who had asked them to source a pressure cooker. The platform had been built on the assumption of a one-to-many fan-out — one reseller shipping to her network of fifty. The actual data looked more like one-to-one.

This was the inflection that almost no outside observer saw coming. In 2021, Meesho made what would later be called inside the company "the great pivot": it dropped the reseller-only gate and opened the platform up to direct consumer purchases. Anyone with a phone number could now download the app, browse the catalogue, and check out — no reseller required.[^7] On the surface, this looked like a sharp left turn that abandoned the very thesis that had defined the company. In practice, it was a recognition that the reseller was no longer a sales channel; she was a customer acquisition mechanism. The app had spent five years training small-town India to associate Meesho with affordability. Now it was time to let the demand walk in through the front door.

The pivot was paired with a decision that, in hindsight, looks like the strategic masterstroke of the entire company history. Meesho went to zero-percent commission. Sellers — overwhelmingly small manufacturers and traders without the resources to fight platforms on take-rate — would list their inventory on Meesho and pay nothing on transaction value.5 The platform would make money on advertising, on fulfilment, on payment-gateway services, and on logistics. But it would not, under any circumstance, dip into the gross merchandise value of the trade itself.

To understand why this move was so brutal to incumbents, it helps to think about how Indian e-commerce platforms had historically priced their take. Flipkart, Amazon India, and the smaller verticals charged anywhere from five percent on staples to twenty-five percent on apparel and accessories, plus payment-gateway and shipping mark-ups. For a low-AOV business — say, a three-hundred-rupee polyester kurta — a fifteen-percent commission meant the platform was extracting forty-five rupees from a sale where the supplier's gross margin might be sixty. Meesho's zero-commission posture meant that the same supplier could list the same kurta and keep, on a transaction basis, the entire spread. The supplier could then either pocket the extra margin, or — far more powerfully from a flywheel perspective — pass it on to the customer in the form of a price that no commission-bearing platform could match.

This is the Hamilton Helmer concept of counter-positioning at its purest. The threat to Amazon and Flipkart was not that Meesho would steal their customers; the threat was that the incumbents could not respond without imploding their own business model. A platform that has built its entire P&L around twenty-percent take-rates cannot drop to zero without writing off billions of dollars of expected commission revenue and breaking its unit economics with sellers it has trained for a decade. Meesho, having never depended on commission, had nothing to lose. The competitor's strength — commission revenue — had quietly become a constraint.

The monetization question, of course, did not go away; it merely got displaced. If you do not earn on commission, you must earn somewhere else. Meesho's answer was to convert the platform into what looks much more like a media business than a retail one. Sellers compete for promoted-listing real estate inside the app. Every search, every category browse, every "you may also like" rail is, at its root, an auction. The genius of this design is that ad revenue scales with seller competition, not with the platform's willingness to squeeze the customer. As the catalogue density on Meesho grew — and by 2024 it was the largest seller-supply marketplace in the country by listed SKU count1 — the ad take naturally inflated, with no commission ever needing to enter the conversation.

This new architecture set up the third leg of the business, which is where the story gets genuinely interesting — because it turns out that the most defensible asset Meesho was building was not the app at all.

IV. Management and Governance: The Vidit and Sanjeev Era

The founders' offices in HSR Layout, Bengaluru, do not particularly look like the headquarters of an internet company about to file one of the largest tech IPOs in Indian history. There is no atrium. The conference rooms are named after Indian cities the founders have personally walked through doing customer research — Indore, Bhopal, Jodhpur — and the company canteen has, for years, served the same subsidised vegetarian thali. Visitors who arrive expecting a Silicon-Valley-style campus tend to leave slightly disoriented.

That sense of unglamorous discipline is, by every account, deliberate. Vidit Aatrey, the CEO, is in his mid-thirties, soft-spoken in the way that Indian engineering-school products tend to be, and is far more comfortable on a customer call than on a stage. His public commentary leans relentlessly operational: cost-per-order, return rates, ad-yield. Sanjeev Barnwal, the CTO and co-founder, is the more reclusive of the pair, and is generally credited inside the company with two things — the original platform architecture that scaled from a few hundred to a few billion API calls, and the obsessive focus on inference cost that has made Meesho's AI-driven discovery layer (internally called PRISM) one of the more efficient at its scale in Indian tech.

The defining cultural artefact of the company is what employees call, half-jokingly, "frugality theatre." Management reviews are reportedly punctuated with questions like: why are we running this model on a GPU when a CPU shaves cost by ninety-five percent? Why are we using a third-party CDN when we can negotiate two more percentage points off direct contracts? Why is travel for the Mumbai customer-research trip not by bus? The aggregate of these decisions has produced an unusually flat unit-cost curve. Public reporting in the run-up to the IPO suggested that in FY25 — the year ending March 2025 — Meesho's server and cloud spend grew in the low single digits even as revenue grew at well over twenty percent year over year.[^9] At an industry where most internet platforms see infrastructure scale roughly in line with usage, the divergence is not a rounding error. It is a strategic outcome.

Equity ownership tells the same story in a different register. The two founders collectively retain a shareholding in the mid-teens of percentage points, with the precise split disclosed in the company's draft red herring prospectus.[^3] The remainder of the cap table is dominated by SoftBank's Vision Fund, Prosus, Peak XV (formerly Sequoia India), Elevation Capital, Meta, Facebook (separately on Meta's balance sheet), and Fidelity — the last of whom marked up the company's valuation to approximately 4.1 billion dollars in early 2025 in its mutual-fund holdings, providing one of the more credible third-party reference prices ahead of the IPO.6 Employee share ownership has expanded sharply in the lead-up to the listing, with a notable ESOP pool expansion in 2024 designed to align senior operators across the run-up.[^11]

The governance event that pre-IPO institutional investors have probably spent the most time on is the so-called "reverse flip." For most of its history, Meesho's parent company sat in Delaware, a structure that was standard for Indian-founded startups that raised early dollars from US venture capital and that wanted optionality on a US listing. By 2023, however, the calculus had shifted. The Indian capital market had matured to the point that domestic IPOs were both possible and, in many cases, better priced. Zomato, Nykaa, Policybazaar, and Mamaearth had all listed on Indian exchanges. The Reserve Bank of India and SEBI had, over multiple years, signalled openness to bringing parent entities back onshore, even when the tax bill for the transition was significant.

In 2024, Meesho executed the flip. The Delaware parent was wound down and the Indian operating subsidiary was repositioned as the listed parent, a process that crystallised an estimated tax liability of several hundred crores of rupees in long-term capital gains.[^12] The company swallowed the bill, on the theory that the unlock value of a domestic listing — accessing Indian retail and mutual-fund pools that cannot easily buy a foreign-listed Indian company — would dwarf the one-time cost. It was the kind of decision that becomes obvious only in retrospect; at the time, paying a multi-hundred-crore tax voluntarily so you can list locally took the kind of pre-IPO conviction that most founders are not willing to expend. With the corporate structure in place, attention turned to the asset inside it that almost nobody outside the company had been talking about.

V. The Hidden Giant: Valmo and the Logistics Moat

For most of Meesho's life, the largest operational expense on the company's P&L was not engineering, not marketing, not even payment-gateway fees — it was shipping. A three-hundred-rupee polyester kurta sold to a customer in a tier-three town in Madhya Pradesh, fulfilled out of a supplier warehouse in Surat, will not move by truck for less than thirty or forty rupees of raw logistics cost. Add the surcharges that traditional third-party couriers — Delhivery, Ecom Express, Shadowfax, Xpressbees — extracted for low-density rural pin codes, and the per-shipment cost could easily push past seventy rupees. On a kurta where the supplier had a sixty-rupee margin and the customer was already squeezed on price sensitivity, the math simply did not work. Either the supplier raised prices, the platform absorbed the gap, or one of the parties walked.

For years, Meesho absorbed the gap. The bet was that the rest of the business would compound fast enough to make logistics a fixable problem later. By 2022, "later" had arrived. The third-party courier rate card was the single largest variable cost item on every order, and any further growth into deeper rural geographies — exactly the customer Meesho most wanted — was making the cost-per-order curve worse, not better. The strategic question that Aatrey and the operating team confronted in late 2022 was the one Indian e-commerce had been confronting for fifteen years: should Meesho build its own fleet, the way Flipkart had built Ekart and Amazon had built ATS?

The answer was no — and the way they said no is the most interesting strategic decision the company has ever made. In mid-2023, Meesho quietly launched वालमो Valmo, an in-house "logistics orchestration platform" with no trucks, no aircraft, no last-mile riders of its own. Instead, Valmo built a software layer that aggregated thousands of small, regional courier companies and local entrepreneurs across the country — the kind of single-pin-code logistics operators that the big four couriers either ignored or treated as low-margin extensions of their main fleets.7

The Valmo bet rests on a very specific reading of Indian logistics. The big-four players are optimised for density. Their cost curves work when a courier can deliver thirty packages per day off a single van within a fifteen-kilometre radius. In tier-three and tier-four India, density is not the default — a courier might cover a hundred kilometres for ten packages. The legacy fleets either priced for that reality (which made the rate card unaffordable for a three-hundred-rupee order) or did not service the pin codes at all. Meanwhile, in the same geographies, there were thousands of local logistics outfits — sometimes one or two trucks, sometimes a single courier on a motorcycle — who already knew every lane and shopkeeper in their territory. They lacked tech, scale, and a steady demand pipeline. Valmo provided all three.

The unit economics shift this produced was the kind that quietly remakes a company. Public reporting and industry estimates put Meesho's average per-order shipping cost in the mid-thirty-rupee range under Valmo, down from a pre-Valmo level that was nearly double.7 By 2025, Valmo was reportedly handling well over half of Meesho's order volume across the country.[^14] On a platform that ships well over a billion orders a year, a thirty-rupee reduction in per-shipment cost is not a line item — it is the difference between contribution-margin-negative and contribution-margin-positive. It is, in concrete terms, why Meesho was able to claim in the run-up to its IPO that the consolidated business had reached contribution profitability without raising commission, without compressing seller take, and without giving up on the three-hundred-rupee order.

The deeper question Valmo poses is whether it stays captive. By 2026, multiple reports had suggested that Meesho was exploring opening the Valmo network to non-Meesho merchants — effectively turning a captive logistics arm into a third-party logistics service in the mould of अमेज़न Amazon's AWS or Shopify's Shop Promise.[^14] The strategic logic is compelling: a network that has been built and tuned on the hardest, lowest-density, smallest-AOV e-commerce flow in the world is, by definition, capable of handling almost any easier flow on top of it. The strategic risk is equally real: every external order that Valmo accepts is one that arms a competitor with the same logistics cost curve that has been Meesho's distinctive advantage. How management resolves that tension will be one of the most-watched capital-allocation calls of the next five years.

VI. New Frontiers: Ads, Fintech, and Segment Reality

If Valmo is the iceberg below the waterline, the part above the surface — the part that institutional investors will actually price in the run-up to the IPO — is the advertising business. The fastest-growing and arguably highest-margin segment inside Meesho is its seller-funded advertising auction, which in industry parlance is sometimes called retail media. Every time a customer searches the app for "kurta under 300" or scrolls a category page, the order in which products appear is, in effect, an auction outcome. Sellers bid, in real time, for placement against keywords, categories, and audience cohorts. The platform keeps the spread.

The economics of this business are, in a word, beautiful. Unlike a marketplace commission — which is bounded by what suppliers can absorb without raising prices — the ad-auction take is bounded by what sellers think incremental visibility is worth, which on a high-density marketplace with hundreds of competing sellers per SKU is almost always more than what the customer pays. Public reporting in the run-up to the IPO suggested ad revenue was the single fastest-growing line on Meesho's income statement, and that ad take-rate as a percentage of GMV had begun to climb into the mid-single-digit range.[^9] By the standards of Amazon's own retail media business — which is widely understood to be the most profitable segment of the entire Amazon empire — Meesho is still early. Even a partial closing of that gap implies a meaningful tailwind to consolidated margins over the next several years.

The second adjacency is financial services. In January 2026, Meesho announced an infusion of one hundred crore rupees into Meesho Payments Private Limited (MPPL), its wholly-owned fintech subsidiary, to deepen credit, payments, and lending services across the platform.8 The strategic logic is well-trodden in the playbook of Asian super-apps. Meesho already knows, with a granularity that no traditional Indian bank can match, the order flow, repeat behaviour, return rate, and seller history of more than a million small merchants. Most of those merchants — operating out of small workshops in Surat, Tiruppur, Jaipur — do not have the credit history that a public-sector bank requires for working capital. They do, however, have a daily order ledger on Meesho that can be underwritten almost in real time. Embedded credit, fulfilled via partner non-banking financial companies and over time via Meesho's own balance sheet, becomes both a tool to lock sellers into the platform and a high-yield product in its own right.

There is also a buyer-side fintech story, though it is less mature. Cash-on-delivery remains the dominant payment mode for the kind of low-AOV, low-trust customer who shops on Meesho. The platform has been progressively migrating customers onto UPI (Unified Payments Interface) and prepaid digital flows, both because they reduce the operational cost of cash handling and because they create the engagement data that future buy-now-pay-later and lending products can be built on. Whether Meesho ever issues a co-branded credit card or launches a full neo-bank wrapper is a question for the post-IPO chapter; the optionality is, at minimum, real.

The third strand of the new-frontiers story is, ironically, the one that did not work. In 2021, Meesho experimented with an international footprint in Latin America via a small partnership with Elenas, a Colombian social-commerce platform. The thesis was that the reseller-driven social-commerce model would travel; Latin American demographics, smartphone penetration, and the cultural prevalence of catalogue-based selling looked, on paper, similar enough to India that a port should have been feasible. In practice, it was not. The unit economics of cross-border platform scaling, the absence of an India-style cheap-supply manufacturing base in Colombia, and the operational distraction of running a second geography during a fundraising and pivot cycle led the company to quietly fold the international ambition.[^16] The lesson, as Aatrey has hinted at in subsequent interviews, was that Meesho's advantage was not the social-commerce abstraction; it was the specific combination of Indian supply, Indian logistics, and Indian price-conscious demand. Try to abstract that and the magic disappears.

The capital-allocation discipline implied by the Elenas wind-down — recognise the failure quickly, take the write-down, and concentrate the firepower on India — is the kind of behaviour that tends to age well in capital markets. With the international ambition shelved, the third leg of the stool was clear: ads to fund the platform, Valmo to fix the unit economics, fintech to deepen the seller relationship — all converging on the same Indian buyer the company had been building for since the FashNear days.

VII. The Playbook: 7 Powers and Strategic Chess

A useful exercise, when analysing any consumer internet company at this stage of maturity, is to walk through Hamilton Helmer's 7 Powers framework and ask, with as little marketing affection as possible, which of the seven the business actually demonstrates. For Meesho, three of the seven look genuinely defensible, two look partial, and two look absent. Investors who confuse the partial and the genuine will misprice the asset in both directions.

The clearest source of power is counter-positioning. The zero-commission model is not just a marketing posture; it is a structural feature that the largest incumbents in the market — अमेज़न Amazon India and फ्लिपकार्ट Flipkart — cannot replicate without writing off billions of dollars of expected commission revenue and breaking faith with sellers who have built their pricing around commission-bearing platforms. The longer Meesho operates at zero commission, the more deeply the seller base is anchored to that pricing reality, and the more painful any incumbent move to match becomes. This is counter-positioning in its textbook form: a strategy that the incumbent can see, can analyse, and still cannot copy.

The second clear power is the network effect, though it is a more interesting variant than the standard "more users brings more sellers" story. Meesho's network effect is best understood as a data flywheel. With more than a billion orders a year flowing through the platform — and the average order coming from a customer with thin or no formal credit history — Meesho has accumulated a deeply granular view of small-town Indian taste, pricing elasticity, return propensity, and seasonal demand swings. That data is the substrate on which the PRISM AI engine runs personalised discovery, dynamic pricing recommendations to sellers, and routing decisions across the Valmo network. Every additional order makes every subsequent decision marginally better, which is, in Helmer's vocabulary, exactly what a moat looks like.

The third clear power is what Helmer calls cornered resource — and in Meesho's case, the cornered resource is the Valmo logistics network. The thirteen-thousand-plus local courier partners that Valmo has aggregated were not signed by anyone else for the simple reason that no other platform had the order density in tier-three and tier-four India to make those partners a viable counterparty. Once Valmo is in place and pumping orders through a given pin code, the local operator's economics are tied to Meesho. The cost for a competitor to replicate that web is not measured in dollars; it is measured in the number of years of customer development you would need to do, town by town, before the same logistics partners would even take your call.

The two partial powers are scale economies and switching costs. Scale economies are real on the ads side, where ad-yield rises faster than the cost of running the auction, but only modest on the marketplace side itself, since most of the input costs (supplier inventory, courier rates) do not deflate dramatically with volume in the way that, say, AWS compute does. Switching costs are real for sellers, who have spent years tuning their listings, ad spend, and inventory to Meesho's algorithm, but weak for buyers, who can — and frequently do — also shop on Flipkart and Amazon when the order value goes up.

The two largely absent powers are branding and process power. Meesho's brand strength among its core customer is high, but it is, candidly, a brand built on cheapness; it has none of the premium signalling that allows Apple or Nike to extract pricing power across categories. Process power — the kind of accumulated organisational know-how that lets Toyota or TSMC manufacture at a quality level competitors cannot match — is also limited; Meesho's operational excellence is impressive, but it is replicable by a similarly disciplined competitor with enough time and capital.

Looking at the same business through Porter's पोर्टर Five Forces sharpens the picture further. Threat of new entrants is moderate: building a marketplace is technically straightforward, but rebuilding the Valmo equivalent is a multi-year capital project. Bargaining power of buyers is high, since switching costs are low and price sensitivity is the defining trait of the customer. Bargaining power of suppliers is paradoxically low, despite their numerical strength — small suppliers individually have little leverage against a platform that controls demand aggregation in their core market. Threat of substitutes is real: WhatsApp commerce, ONDC (the government-backed Open Network for Digital Commerce), and rising D2C brands all compete for the same wallet share. Industry rivalry is high but, critically, structurally different from Flipkart and Amazon — Meesho competes more directly with regional resellers, unorganised retail, and emerging social-commerce challengers than with the marketplace incumbents themselves.

The strategic synthesis, then, is that Meesho is not in the same business as Amazon India. It is, instead, in a business that Amazon India structurally cannot enter, that has its own logistics moat, that monetises through media rather than retail, and that — for better or worse — rises and falls with the consumption power of the bottom seven hundred million Indians. That framing matters enormously for the bull and bear case.

VIII. Bear vs. Bull and the IPO Verdict

Walking into a public listing, every company has a bull narrative and a bear narrative. For most, those two stories are mirror images of the same set of facts. For Meesho, they are slightly stranger — the bull and the bear are looking at the same balance sheet and disagreeing not on the numbers but on the durability of the model that produced them.

The bull case begins with profitability. In its FY25 results, Meesho disclosed revenue from operations of approximately 9,390 crore rupees, a year-on-year growth rate in the mid-twenties percentage range, alongside meaningful narrowing of consolidated losses.[^9] More importantly, the company has begun framing itself as having reached contribution-margin profitability — a metric that excludes corporate overhead but captures the question of whether each incremental order pays for itself. For a business that for years subsidised three-hundred-rupee orders out of venture capital, that is a structurally different operating posture. The bull continues: Meesho is the only Indian e-commerce platform that can profitably serve the bottom seven hundred million of the population. Every other player has either explicitly given up on that customer or is doing so implicitly by raising AOV and chasing premium SKUs. As भारत Bharat consumption rises — and it has been rising, on the back of UPI penetration, rural electrification, smartphone affordability, and improving last-mile infrastructure — Meesho is the listed vehicle that is most cleanly geared to that wave.

The bear case is at least as serious. The first concern is the AOV ceiling. A platform that has trained an entire customer base to expect three-hundred-rupee polyester kurtas may find it structurally difficult to move that customer into eight-thousand-rupee smartphones or fifty-thousand-rupee laptops — and those higher-AOV categories are where the dollar GMV in Indian e-commerce ultimately lives. The bear scenario is that Meesho has built an exquisitely engineered machine for a category of demand that, in aggregate value terms, is a small slice of the total pie. The second concern is brand perception. Meesho's reputation among urban and tier-one customers is decidedly downmarket; whether that perception will follow the company up the AOV curve, or actively prevent the move, is an empirical question that the next five years will answer.

The third bear concern is competitive dynamics. The Indian government's Open Network for Digital Commerce (ONDC) is, in design, an attempt to commoditise exactly the platform layer that Meesho has spent a decade building. If ONDC works as intended — and that "if" has done a lot of heavy lifting in Indian e-commerce conversations for three years — then the platform power of any individual marketplace, including Meesho, could erode. The fourth is regulatory: the FDI rules on Indian e-commerce platforms have been periodically tightened, the GST regime on small sellers is in flux, and the policy environment is, at minimum, an active overhang.

Then there is the capital-allocation comparison that institutional investors will inevitably make. Meesho has raised slightly over one billion dollars across its lifetime, and the most recent third-party reference point — Fidelity's markup to approximately 4.1 billion dollars in early 20256 — implies a capital efficiency that is in a fundamentally different class from फ्लिपकार्ट Flipkart, which has reportedly absorbed more than ten billion dollars to reach its current scale. The IPO range that has been discussed in trade press is in the high single-digit-billion dollars, an outcome that would imply roughly seven-to-eight times return on every dollar raised — a multiple that would, in the Indian internet context, stand out.[^17]

The myth-versus-reality lens is useful here. The first popular myth is that Meesho is a "social-commerce" company. The reality is that social commerce, in the original reseller sense, is now a minority of platform GMV; Meesho is, in 2026, a full-spectrum marketplace whose competitive edge derives from logistics and pricing, not from WhatsApp-based fan-outs. The second myth is that zero-commission is unsustainable and the company will have to "eventually" raise take-rates. The reality is the opposite: zero-commission is the strategic moat that disciplines incumbents; raising it would be the move that destroys the model. The third myth is that Valmo is a sideshow. The reality, as Section V argued, is that Valmo is the asset that makes the entire P&L work.

For investors trying to monitor this company over the years ahead, the noise-to-signal ratio in Indian internet quarterly disclosures is famously high. Three KPIs are likely to do most of the explanatory work. The first is contribution margin per order — whether Meesho can sustain and modestly expand the unit-level profitability that it has only recently achieved, especially as it grows into deeper rural geographies where logistics density is structurally lower. The second is ad take-rate as a percentage of GMV — the closer this number creeps toward what Amazon's retail-media business has demonstrated globally, the more the company's terminal margin profile improves. The third is Valmo's share of total order volume and, in due course, the share of Valmo's revenue coming from non-Meesho merchants — the latter being the leading indicator of whether the logistics arm becomes a standalone platform business in its own right.

The light second-layer diligence checklist is short but real: watch for any material adverse change in the FDI compliance regime applicable to Indian marketplaces, monitor the Karnataka labour-and-payment disputes that periodically surface around the gig-courier base, track the post-listing lockup expiries of SoftBank and Prosus (both of whom hold positions large enough to move the float), and watch for any further valuation marks from Fidelity, T. Rowe Price, or other US mutual-fund holders whose quarterly NAVs will provide an ongoing third-party reference price even after the company lists.6

IX. Outro: Lessons for Founders

There is a phrase that, by 2026, has become something of a corporate proverb inside Meesho: "standardise the non-standard." It is a deceptively simple sentence that captures the entire intellectual posture of the company. India's interior is non-standard. The pin codes are non-standard. The sellers are non-standard. The customers are non-standard. The payment behaviour, the return rate, the device, the language, the trust model — all non-standard. The instinct of most Western-trained operators is to standardise the standard and ignore the rest. The Meesho instinct, formed over a decade of customer development in towns most of the company's investors will never visit, is to standardise the chaos itself: build a tech layer that absorbs the variance, rather than a tech layer that excludes anyone who fails to fit a clean schema.

The second proverb is one Aatrey has articulated in multiple interviews over the years: start with the constraint. The defining constraint of Meesho's customer was the three-hundred-rupee order. That single number — the average value of what an aspirational housewife in Sitapur was willing to spend on a polyester kurta — was the gravitational centre around which every subsequent decision orbited. Could the platform charge a fifteen-percent commission on a three-hundred-rupee order? No. So the commission had to be zero, and ads had to fund the company. Could third-party couriers ship a three-hundred-rupee item profitably to a rural pin code? No. So Valmo had to be built. Could traditional banks underwrite a supplier whose biggest sale was a three-hundred-rupee kurta? No. So Meesho Payments had to extend embedded credit. The entire architecture of the business is a logical consequence of refusing to walk away from the constraint of the small order.

There is a third lesson, less articulated but worth dwelling on, and that is the discipline of saying no. The Elenas wind-down. The deferral of categories like consumer electronics where the AOV gravity pulls in the wrong direction. The refusal, despite immense pressure during the 2021 funding cycle, to abandon zero-commission. Each of those decisions cost the company something — either in optionality or in short-term growth narrative. Each of them, in hindsight, is a decision that compounds.

The final reflection is the one that institutional capital markets will be watching most closely as the company prepares for its listing. The bet inside Meesho is that the next leg of Indian consumption growth — slower than the headline GDP numbers, but deeper in its penetration of the population — will be disproportionately captured by the platform that has spent the longest time learning the unsexy mechanics of the small-town shopper. If the bet is right, Meesho will, in the second half of the 2020s, occupy a position in Indian consumer internet roughly analogous to what पतंजलि Patanjali once threatened to occupy in Indian FMCG — the homegrown, frugal, mass-market champion that the foreign multinationals could neither buy nor outspend. If the bet is wrong, the company will discover that the three-hundred-rupee customer was a smaller market than the bull case required, and the next decade will be a grind of trying to graduate that customer into higher-value categories where its brand was never built to play.

Either way, the story already merits a permanent place in the small canon of Indian internet companies that built something durable from a thesis the rest of the market refused to take seriously. It is the kind of story that, on a Tuesday morning in Sitapur, ends with a woman closing her WhatsApp group, opening her Meesho app, and placing the eleventh order of the day.

References

References

-

Meesho Statistics and Business Model — Business of Apps, 2024-05-20 ↩↩

-

SoftBank's Vision for Meesho: From Social Commerce to Marketplace — Reuters, 2021-04-05 ↩

-

SoftBank's Vision for Meesho: From Social Commerce to Marketplace — Reuters, 2021-04-05 ↩

-

Meesho Statistics and Business Model — Business of Apps, 2024-05-20 ↩

-

Fidelity Marks Up Meesho's Valuation to $4.1 Billion — Bloomberg, 2025-01-15 ↩↩↩

-

How Valmo Logistics became Meesho's secret weapon — YourStory, 2024-02-06 ↩↩

-

Meesho infuses Rs 100 crore into payments subsidiary — Financial Express, 2026-01-20 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube