Mazagon Dock Shipbuilders Limited: The Sovereign Compounder

I. Introduction & The $10 Billion Sovereign Compounder (00:00 – 15:00)

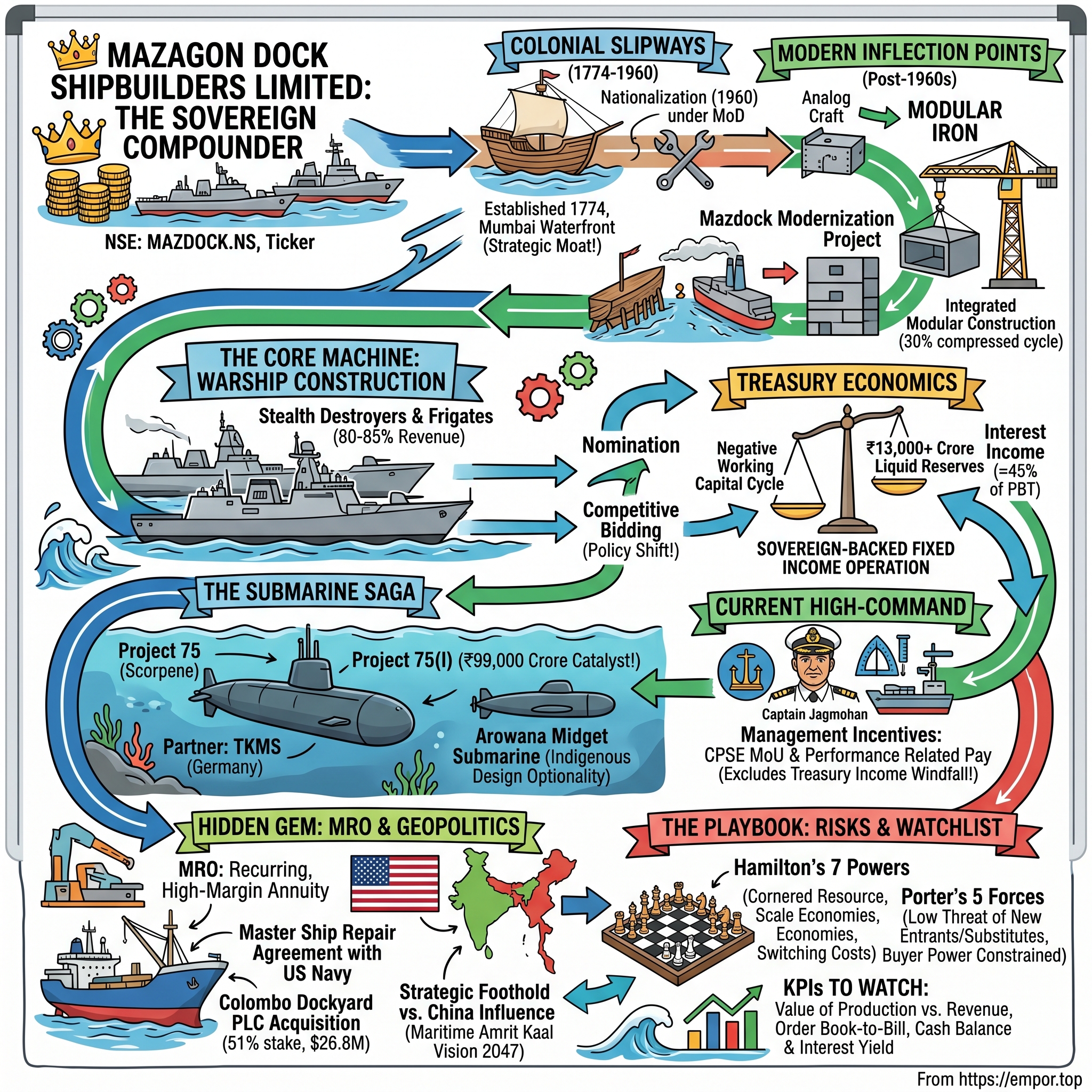

Picture the Mumbai waterfront at dawn. The Arabian Sea is the color of gunmetal, the air is thick with monsoon salt, and along a sliver of impossibly expensive real estate in the south of the city—land that today would fetch a king's ransom per square foot—sits a sprawling industrial complex that looks more like a working steel mill than a stock-market darling. Gantry cranes loom over half-finished hulls. Sparks rain down from welders perched on scaffolding. And somewhere in a climate-controlled shed, a 300-tonne crane is lowering a pre-outfitted block of a stealth destroyer onto a waiting keel with the precision of a surgeon. This is Mazagon Dock. It has been building things that float in this exact spot since before the United States declared independence.

Here is the puzzle that makes this story irresistible. How does a colonial-era repair yard—established in 1774 in what was then a sleepy cluster of fishing villages on the western coast of India—transform, two and a half centuries later, into one of the most spectacular wealth-creation engines in the entire Indian public market? Because that is precisely what happened. Following its 2020 listing on the National Stock Exchange, Mazagon Dock Shipbuilders Limited (NSE: MAZDOCK.NS)4 became a textbook "multibagger," the kind of stock that turns a modest stake into a generational return and gets whispered about at every dinner party in Mumbai. It is a crown jewel of India's defense establishment, a Defence Public Sector Undertaking that builds the warships and submarines patrolling the Indian Ocean—and, almost incidentally, one of the most fascinating financial machines you will ever encounter.

And that brings us to the central paradox of this episode, the thing that should make any fundamental investor sit up straight. Walk into a boardroom of a Western defense contractor—a Lockheed, a BAE, a Huntington Ingalls—and you will find a familiar shape: capital-intensive, frequently debt-laden, wrestling with pension liabilities and the brutal working-capital demands of building things that take years to deliver. Now look at Mazagon Dock. It carries virtually no debt. It runs a negative cash-conversion cycle, meaning its customers fund the business before a single sheet of steel is cut. And it sits on a treasury hoard of more than ₹13,000 crore—well over $1.5 billion—in liquid reserves.2

Let that sink in. The single most remarkable fact about this shipbuilder has almost nothing to do with ships. In recent years, nearly 45% of the company's pre-tax profit has come not from the painstaking work of welding warships together, but from the interest earned on the enormous advance payments the Indian Navy hands over before construction even begins.2 Mazagon Dock is, in the most literal sense, a treasury operation wearing a shipyard's overalls. It builds destroyers with one hand and runs what amounts to a sovereign-backed fixed-income desk with the other.

So what are we really analyzing here—a defense manufacturer, or a financial institution that happens to own dry docks? That tension runs through everything that follows.

Over the next three hours, we will trace the full arc. We will start with the transition from analog craft—men hammering iron plates by eye—to modular steel construction that looks like industrial Lego. We will dissect the mechanics of being the favored supplier to a monopsony, a market with exactly one buyer, and why that relationship is both a moat and a leash. We will go deep into the high-stakes submarine programs that tied this Mumbai yard to the naval engineering houses of France and Germany. We will examine the audacious 2026 acquisition of Sri Lanka's Colombo Dockyard, a chess move on the geopolitical board of the Indian Ocean. And finally, we will run the whole enterprise through Hamilton Helmer's 7 Powers and Porter's Five Forces to understand what, exactly, protects this state-controlled monopoly—and what could break it.

Let's begin where every great compounding story begins: not with the numbers, but with the dirt under its feet.

II. Colonial Slipways to Strategic Command: Succinct Origins (15:00 – 30:00)

Every empire that ever ruled the seas needed somewhere to fix its ships. In 1774, the British East India Company—then the most powerful corporation the world had ever seen, a private firm with its own army and its own navy—needed a place on India's west coast to careen, caulk, and repair the wooden merchant vessels that carried the fortunes of empire back to London. They found it in Mazagon, a fishing settlement on what was then one of the seven islands of Bombay. A modest dry dock went in. Ships came, were patched, and sailed away. For the better part of a century and a half, that was the whole business: a colonial repair shop, indispensable to the men who ran it, invisible to history.

We are going to move through this old-world chapter quickly, because the truth is that almost nothing about Mazagon Dock's pre-1960 existence explains the company you can buy on the exchange today. But two threads from the colonial era reach all the way into the present, and they are worth pulling. The yard was formally incorporated as a company in 1934, under the joint ownership of two British shipping titans—the Peninsular and Oriental Steam Navigation Company, the legendary P&O, and the British India Steam Navigation Company. It was, in other words, born as a piece of British corporate infrastructure, an asset of the very shipping lines whose vessels it serviced.1

Then came the pivot that changed everything. India won its independence in 1947, and within a little over a decade the new republic confronted a hard strategic truth: a nation with a 7,500-kilometer coastline and ambitions of sovereignty could not depend on foreign-owned yards to keep its navy afloat. In 1960, the Government of India acquired the yard outright and placed it under the Ministry of Defence as a Defence Public Sector Undertaking.1 This was nationalization as the ultimate pivot—the moment a colonial repair shop was conscripted into the project of building maritime sovereignty for an independent nation. The customer changed from British merchantmen to the Indian Navy, and the mission changed from patching to creating.

Now, here is why that two-hundred-fifty-year-old dirt matters to a fundamental investor in 2026, and it is the single most underappreciated asset on the balance sheet. The physical footprint of Mazagon Dock sits in the middle of south Mumbai's premium waterfront—land that is now surrounded by one of the densest, most expensive urban cores on the planet. You could not build a heavy shipyard there today. The permits, the displacement, the sheer cost of acquiring deep-water frontage in central Mumbai make it flatly impossible. The geography that the British happened to claim in 1774 has become, through nothing but the passage of time and the growth of a megacity around it, a non-replicable moat. In Helmer's language, this is a textbook Cornered Resource, handed down not by genius but by colonial accident. No private competitor can simply decide to compete by pouring concrete next door. There is no "next door" left.

The transformation from repair shop to builder reached its first true milestone in 1972, with the delivery of INS Nilgiri, India's first major indigenously built frigate—a Leander-class warship constructed under British license.1 To a casual observer it was one ship. To the Indian Navy it was a coming-of-age. Until that point, India had been what naval strategists call a "Buyer's Navy," shopping the world's shipyards for finished hulls. With Nilgiri, it began the structural transition to a "Builder's Navy"—a nation that designs and constructs its own instruments of sea power. That distinction is the entire thesis of the company. Everything that makes Mazagon Dock valuable today—the institutional knowledge, the workforce, the favored relationship with the Navy—was seeded in that decision to build rather than buy.

The yard would spend the next four decades building frigates and destroyers, slowly accumulating expertise. But it was still, fundamentally, an old-world operation: ships rose keel-up, one at a time, on open slipways, the way they had for generations. To understand how Mazagon Dock became a compounding machine, we have to watch it tear up that century-old method and reinvent how a warship gets born.

III. Modern Inflection Points: From Craftsmanship to Modular Iron (30:00 – 55:00)

For most of its history, building a warship at Mazagon Dock looked a lot like building a cathedral. You started at the bottom—the keel, the spine of the ship—and you worked upward, sequentially, on a fixed slipway exposed to the Mumbai sky. Steel was cut, bent, and welded in place, layer upon painstaking layer. A single slipway could hold a single hull, and that hull monopolized the slot for years. If the monsoon rolled in, work slowed. If one section fell behind, everything above it waited. It was craftsmanship in the oldest sense—and it was a chokehold on capacity. You simply could not build many complex warships at once when each one squatted on a slipway for half a decade.

The turning point—and this is the single most important technological inflection in the company's modern history—was the Mazdock Modernization Project, the great capital overhaul that came to fruition around 2014. Think of it as the moment Mazagon Dock stopped building cathedrals and started building with industrial Lego. The company poured serious capital into transforming the physical plant: a massive new Wet Basin where multiple ships could be fitted out simultaneously, a state-of-the-art Submarine Section Assembly Shop, and the crown of the whole enterprise—a towering 300-tonne Goliath crane straddling the construction dock.1

Here is what that hardware actually unlocked, in plain terms. Instead of building a ship bottom-to-top in the open air, Mazagon Dock shifted to Integrated Modular Construction. Engineers fabricate large, pre-outfitted blocks of the warship—complete with piping, cabling, and equipment already installed—inside climate-controlled workshops, sheltered from weather and working at ground level where access is easy. Then the Goliath crane lifts each finished block, swings it over the dock, and sets it down to be welded to its neighbors. It is the difference between assembling a piece of furniture flat-pack-style, with each module built on a comfortable workbench, versus contorting yourself to build it in the cramped corner where it will finally stand.

The payoff was enormous. Modular construction compressed shipbuilding cycle times by more than 30%, and—crucially—it freed the slipway from being the bottleneck.1 Suddenly the yard could have multiple stealth destroyers and stealth frigates progressing in parallel, blocks maturing in the sheds while the dock handled final integration. This is not a cosmetic upgrade; it is the operational foundation of every revenue figure we will discuss later. Without modular construction, the order book the company carries today would be physically impossible to execute. The MMP turned a capacity-constrained craft shop into a genuine industrial platform.

But industrial capability is only half a transformation. The other half came on the capital-markets side, and it arrived in October 2020.

For most of its life, Mazagon Dock had been an opaque arm of the government—a department, really, whose accounts disappeared into the vast ledgers of the Ministry of Defence. The 2020 IPO blew the doors open. The offering was a sensation: it was oversubscribed roughly 157 times, one of the most heavily bid public issues the Indian market had seen.4 That number tells you something visceral about the moment. Investors who had spent years searching for a clean, listed way to play India's defense-indigenization wave suddenly had one, and they trampled each other to get in.

The listing did something more important than create a tradeable ticker, though. It imposed discipline. A government department answers to a ministry on the ministry's timetable. A listed company answers to the market every ninety days. Mazagon Dock now had to disclose its order book, report its milestone progress, and explain its margins to analysts who could do arithmetic. And as the public markets did that arithmetic, they began to grasp the sheer scale of the domestic defense pipeline sitting behind this company—the destroyers, the frigates, the submarines, the decades of visibility. The stock re-rated dramatically. What had been a sleepy state asset became a market favorite, and the transparency forced by listing arguably made the company run better than it ever had under purely ministerial oversight.

The third inflection was as much symbolic as it was structural, and it landed in 2024, the company's 250th anniversary year. The Government of India conferred "Navratna" status on Mazagon Dock—an elevation announced through the Press Information Bureau in June of that year.5 "Navratna," literally "nine gems," is a designation reserved for the most capable and financially sound of India's central public-sector enterprises, and it is far more than a ceremonial ribbon. It granted the board the autonomous power to commit capital expenditure of up to ₹1,000 crore on a single project without running back to the Ministry for prior approval.5

Why does an investor care about a bureaucratic delegation of authority? Because speed is strategy. In the world of state enterprises, the ability to deploy capital without waiting months for ministerial sign-off is the difference between catching an opportunity and watching it sail past. As we will see, this newfound autonomy is precisely what made the company's first-ever international acquisition possible—a deal that would have been unthinkable when every rupee of capex required a trip up the chain of command. Navratna status was the key that unlocked the door to global ambition.

With the plant modernized, the company public and disciplined, and the board freshly empowered, we can finally open the hood and look at the machine itself—how Mazagon Dock actually makes money, and why its economics are so strange and so beautiful.

IV. The Core Machine: Warship Construction & Treasury Economics (55:00 – 85:00)

Stand on the dock and look at what generates the cash, and the answer is unambiguous: warships. Big, gray, bristling steel warships. Surface combatants—stealth guided-missile destroyers and stealth frigates—have historically accounted for somewhere between 80% and 85% of Mazagon Dock's total revenue.2 Everything else, however glamorous, is a minority of the top line. If you want to understand whether this company is healthy in any given year, you start by asking how many destroyers and frigates moved through physical milestones. This is, first and foremost, a builder of heavy combatants.

To appreciate where Mazagon Dock sits, you need the lay of the competitive land—and Indian defense shipbuilding is a peculiar, almost clubby landscape. It is dominated by four state-owned yards, each with its own niche carved out by decades of nomination and specialization, plus a rising private challenger. Think of it less as a free-for-all and more as a guild, where each master craftsman owns a corner of the trade.

At one end is Cochin Shipyard (COCHINSHIP.NS), the yard that built India's first indigenous aircraft carrier and specializes in massive flat-deck vessels and commercial repair, running annual revenue in the neighborhood of ₹4,000 crore.3 At another sits Garden Reach Shipbuilders & Engineers (GRSE.NS) in Kolkata, the specialist in smaller platforms—frigates, corvettes, fast patrol and survey vessels—turning over roughly ₹3,500 crore a year.[^4] Goa Shipyard rounds out the quartet of public yards with patrol craft and smaller hulls. And then there is the private interloper: Larsen & Toubro, whose Kattupalli yard near Chennai represents the most credible private-sector threat to the state monopoly, a genuinely capable builder unencumbered by PSU bureaucracy.

Mazagon Dock sits at the very peak of the complexity curve. Its signature products are the Project 15B Visakhapatnam-class stealth destroyers and the Project 17A Nilgiri-class stealth frigates—the most sophisticated surface combatants India builds, dense with weapons, sensors, and the kind of systems integration that takes generations of accumulated know-how. That positioning, building the hardest things in the catalog, is why Mazagon Dock's annual revenue has run well ahead of its peers, in the broad range of ₹9,500 crore to ₹11,000 crore in recent years.2 It is the heavyweight in a division of welterweights.

Now, how does the money actually flow into these yards? For most of its history, through a mechanism called nomination. The Ministry of Defence would simply designate Mazagon Dock to build a given class of hyper-complex warship—no auction, no competitive tender—on a cost-plus basis. The yard recovered its actual costs and earned a guaranteed margin on top, typically in the range of 7.5% to 10%.2 If you are an investor steeped in competitive markets, your instinct is to recoil: cost-plus contracting is the classic recipe for fat, lazy, gold-plated suppliers with no incentive to control costs. And historically, that critique has real force in defense procurement worldwide.

But here the story has a twist, and a policy shift worth watching closely. India has been moving, deliberately, toward competitive bidding even for complex platforms—pitting yards against one another and against L&T rather than handing out work by fiat. On paper, that threatens Mazagon Dock's cozy margins. In practice, the modular-construction efficiency we discussed earlier, combined with the company's unmatched institutional knowledge of building these specific classes of ship, makes it genuinely hard for any domestic rival to underbid Mazagon Dock on large destroyers. The moat here is not the nomination policy itself—that may erode—but the deep, hard-won cost advantage that decades of building the hardest hulls have produced. The policy could change tomorrow; the experience cannot be cloned.

And now we arrive at the heart of the entire investment case—the part that makes seasoned investors do a double-take. It is the negative working-capital engine, and it is the closest thing to financial alchemy you will find in heavy industry.

Here is the mechanism. When the Indian Navy places a multi-billion-rupee order for a warship, it does not pay on delivery. It pays in large milestone-linked advances, front-loaded and generous, because the Navy has every interest in keeping its sole heavy-destroyer builder liquid and healthy. A destroyer, remember, takes six to eight years to build. So Mazagon Dock receives enormous sums of cash years before it has to spend the bulk of it—and in the meantime, it parks that money in fixed and call deposits with banks, earning interest the entire time.2

The scale of this is staggering. As of 2026, the company's liquid cash and bank balances stand at more than ₹13,000 crore.2 That is not retained earnings slowly accumulated; it is overwhelmingly customer money held in trust against future construction. And that float throws off a torrent of interest income. In recent fiscal years, the line item the company calls "Other Income"—which is almost entirely interest on these deposits—has hovered around ₹1,100 crore annually, an amount that has represented roughly 45% of total Profit Before Tax.2

Stop and absorb what that means. Nearly half of this shipbuilder's pre-tax profit comes from interest on cash it is holding for its customer. The core operating business is effectively self-funding; the company barely needs its own capital to build ships, which is precisely why it carries almost no debt and runs a negative working-capital cycle of around minus-118 days.2 A negative cycle means the company is, on net, financed by its customer—the opposite of the cash-hungry capital trap that defines most heavy manufacturing.

This is the dual identity we flagged at the very start, now made concrete. Mazagon Dock is simultaneously a defense manufacturer earning a thin, regulated margin on welding steel, and a sovereign-backed treasury operation earning a fat, near-riskless return on a multi-billion-dollar float. For a fundamental investor, the implications cut both ways. On the bull side, it is a structurally over-capitalized, self-funding compounder with a floor under its earnings. On the bear side—and we will return to this—an enormous chunk of profitability depends not on building better ships but on the Navy's willingness to keep paying generous advances and on interest rates staying elevated. Strip out the treasury income and the underlying manufacturing business is a far more modest, single-digit-margin affair.

That tension—steel versus treasury—is the lens through which to view everything else. And nowhere is the steel side more technically dazzling, or more strategically consequential, than in the part of the yard where they build machines designed to disappear beneath the sea.

V. The Submarine Saga: From Scorpene to the ₹99,000 Crore Project 75(I) (85:00 – 110:00)

If warship construction is Mazagon Dock's bread and butter, submarines are its caviar. The Submarine and Heavy Engineering segment has typically represented 15% to 20% of revenue—a minority of the top line, but the crown jewel by every other measure.2 This is where the technological barriers are highest, where the margins on know-how are richest, and where the company's claim to being genuinely irreplaceable rests on its firmest ground. Building a submarine is, without exaggeration, one of the hardest things human beings manufacture.

Consider what is actually required. A conventional submarine is a steel tube that must dive hundreds of meters, where the water pressure would crush an ordinary hull like a soda can, and it must do so silently—because in the undersea world, the submarine that makes the least noise wins, and the one that is heard first dies. That demands welding high-tensile steel to tolerances measured in fractions of a millimeter, aligning propulsion machinery so precisely that it does not betray the boat with vibration, and integrating sensitive weapons and sensor suites into a hull where every cubic centimeter is contested. There is no faking this. You either have a workforce that has done it, or you do not.

Mazagon Dock built that workforce through Project 75. Under a technical collaboration with France's Naval Group, the yard constructed six Scorpene-class submarines—known in Indian service as the Kalvari class—conventional diesel-electric stealth boats of formidable capability.1 The program stretched across more than a decade, and that long, grinding apprenticeship was the point. Each boat taught the yard something the previous one had not. By the end, Mazagon Dock possessed something no amount of capital can buy off the shelf: a living, breathing cadre of engineers and tradespeople who know, in their hands and not just their manuals, how to build a submarine that works.

Which sets up the mega-catalyst that hangs over the entire investment case today: Project 75(I).

This is the big one. Project 75(I) is a tender to build six advanced conventional submarines equipped with Air-Independent Propulsion, valued at a colossal ₹99,000 crore—on the order of $12 billion.[^10] To understand why AIP matters, here is the simple version. A conventional diesel-electric submarine has an Achilles' heel: it must periodically rise near the surface to run its diesel engines and recharge its batteries, and that act—called snorkeling—is when it is most vulnerable to detection. Air-Independent Propulsion lets the boat generate power without surfacing or snorkeling, allowing it to stay submerged and silent for far longer. In undersea warfare, that extended invisibility is the whole game. AIP boats are dramatically harder to find and kill.

The strategic maneuvering around this tender is a story in itself. Mazagon Dock chose its dance partner carefully, completing commercial negotiations in late 2025 and early 2026 to bid for the program in partnership with Germany's ThyssenKrupp Marine Systems, or TKMS—one of the world's premier submarine builders, whose interest in the India deal had been reported as far back as 2023.7 Pairing the German firm's design pedigree with Mazagon Dock's proven construction muscle and its existing submarine workforce created a formidable bid. The technology-transfer model—build the early boats with foreign expertise, indigenize the rest—is the same playbook that built the Scorpene capability, now run at a far larger scale.

The financial materiality is hard to overstate, and this is where investors should focus. If Mazagon Dock is formally awarded the contract—which, as of this writing, awaits final approval from the Cabinet Committee on Security—it would nearly quadruple the company's current order book of ₹20,535 crore.2 More than the headline number, it would lock in double-digit-year revenue visibility, securing the yard's heavy-engineering pipeline for the better part of fifteen years. A submarine order of this size does not just fill the book; it underwrites a decade and a half of high-barrier, high-value work. This single contract is, fairly, the central swing factor in the bull case—and its dependence on a government committee's decision is equally central to the bear case.

There is one more submarine thread worth pulling, smaller but strategically telling: the Arowana midget submarine, which Mazagon Dock launched as a prototype in 2024.1 In dollar terms it is a novelty—a small, speculative project that contributes nothing meaningful to today's revenue. But it represents something the analysts' spreadsheets tend to miss: optionality. The Arowana was designed 100% in-house. That is a quiet but profound signal. For its entire modern history, Mazagon Dock has been a "build-to-print" contractor—a superb manufacturer executing someone else's design under license, whether French or German. An indigenous design, however modest, hints at a transition toward becoming a proprietary defense-IP owner, a company that captures the high-margin value of design rather than just the labor of assembly. If that transition ever scales, it changes the long-run margin story entirely. For now, it is a seed worth watching.

Submarines, then, are where Mazagon Dock's technical credibility lives. But credibility is also a function of who is steering the enterprise—and in 2025 and 2026, the bridge of this company got a new commander with a very specific mandate.

VI. Current High-Command: Management, Incentives, & the PSU Contrast (110:00 – 125:00)

Let's talk about the people in charge—and let's do it the way a serious investor should, by ignoring the long parade of rotating civil servants who came before and focusing on the leadership that actually shapes the company you can analyze today. The figure who matters is Captain Jagmohan.

On April 21, 2025, Captain Jagmohan (Retd.) was appointed full-time Chairman and Managing Director of Mazagon Dock.1 His résumé reads like it was written for the job. He is a Naval Architect by training—someone who designs ships for a living—with more than 25 years of service in the Indian Navy. But what makes his appointment genuinely interesting is that he is not a generalist bureaucrat parachuted in from an unrelated ministry. He is an industry insider through and through, having previously served as Director of Corporate Planning and Business Development at Goa Shipyard and held senior roles at GRSE.1 In other words, the man now running India's premier warship yard has spent his career inside the very guild of state shipbuilders we mapped earlier. He knows where the bodies are buried, because he helped build the graveyard.

His mandate has been notably aggressive, and it has had a distinctly outward-facing cast. Under his leadership, Mazagon Dock has pushed hard for its first genuine international footprint—a strategic ambition that culminated in his appointment as Non-Executive Chairman of Colombo Dockyard PLC in Sri Lanka in April 2026, the capstone of the acquisition we will dissect in the next section.[^8] A CMD who personally takes the chair of a freshly acquired foreign subsidiary is sending a message: this is no longer a purely domestic enterprise content to build for one customer in one harbor. The ambition has gone regional.

But here is where the story takes a turn that will feel deeply foreign to anyone raised on Silicon Valley or Wall Street incentive structures—and it is essential to understanding how this company is actually governed. Captain Jagmohan and his board hold virtually zero shares of Mazagon Dock.1 None of the founder-equity, stock-option, get-rich-with-the-shareholders alignment that defines Western corporate leadership exists here. The Government of India retains an 81.22% controlling promoter stake, and management's personal net worth is essentially untethered from the stock price.4 If MAZDOCK.NS triples, the CMD does not become wealthy. If it halves, his bank account does not notice.

So how on earth do you motivate executives to run a tight, ambitious enterprise when you cannot dangle equity in front of them? This is one of the most fascinating governance questions in the entire Indian state-enterprise universe, and the answer is a system most public-market investors have never examined.

Compensation at Indian central public-sector enterprises is rigidly governed by guidelines from the Department of Public Enterprises.8 The central mechanism is an annual Memorandum of Understanding—a formal performance contract that management signs with the Ministry of Defence each year, laying out specific, measurable targets. Performance against that MoU is then graded, and the grade determines compensation through a system called Performance Related Pay. In FY24, Mazagon Dock scored an "Excellent" rating of 90.5 against its MoU targets, the top band, which unlocked 100% eligibility for Performance Related Pay for its management.2 The incentive, in other words, is not stock—it is the bonus tied to hitting concrete operational and financial goals negotiated with the owner.

And now comes the genuinely clever part, the detail that should reassure investors worried about the treasury-income distortion we discussed earlier. Regulations issued by the Department of Public Enterprises in late 2025 mandate that extraordinary items—explicitly including the interest earned on those idle cash deposits—must be excluded from the Profit Before Tax figure used to calculate management bonuses.8 Read that again, because it is subtle and important. Management cannot coast on treasury income. They cannot hit their bonus targets simply because interest rates happened to be high and the float happened to be large. Their pay is tied to operational deliverables: keels laid, ships physically delivered, modular efficiency improved, core operating EBITDA generated.

This is a remarkably well-designed incentive, and it directly addresses the central paradox of the business. The thing that makes Mazagon Dock financially beautiful—the treasury engine—is precisely the thing management is forbidden from taking credit for. They are paid to build ships well and on time. The interest income is, from an incentive standpoint, treated as what it really is: a windfall of the business model, not a measure of managerial skill. For an investor trying to assess whether leadership is actually creating operating value or merely surfing a float, this carve-out is an unusually honest piece of governance.

That outward-looking ambition under Captain Jagmohan, and the operational discipline that the incentive structure enforces, converged most dramatically in a single transaction—one that took Mazagon Dock across an international border for the first time in its 252-year history.

VII. The Hidden Gem: MRO, Colombo Dockyard, & Maritime Geopolitics (125:00 – 145:00)

There is a part of Mazagon Dock's business that rarely makes the headlines, gets buried beneath the multi-thousand-crore drama of newbuild warships, and yet may matter more to the company's future margins than almost anything else. It is the unglamorous, deeply lucrative world of Maintenance, Repair, and Overhaul—MRO, in the trade. And to understand why management has been quietly betting on it, you have to understand the fundamental problem with building warships for a living.

Warship construction is brutally cyclical. There are long, fallow gaps between the moment a design is approved and the moment steel is finally cut—periods when the order book is healthy on paper but the docks are not fully utilized. Revenue arrives in lumps tied to milestones, and a slip in one program can leave expensive assets and skilled workers underemployed for months. MRO is the antidote. Repairing and overhauling ships generates recurring, predictable, and—critically—significantly higher-margin cash flow than building them, and it does so while keeping those dry docks and that workforce productively busy in the gaps. It is the difference between a feast-or-famine project business and a steady annuity. For a yard trying to smooth its earnings and lift its blended margin, MRO is the obvious, high-return move.

The first major validation of Mazagon Dock's MRO ambitions came from an unexpected direction: the United States. In September 2023, the company signed a Master Ship Repair Agreement with the US Navy.6 On its face it is a technical procurement document. In substance it is an enormous quality endorsement. The US Navy does not sign repair agreements with yards it does not trust to touch its warships, and the MSRA positioned Mazagon Dock as a strategic hub for voyage repairs of American military vessels operating across the Indo-Pacific. For a yard whose entire customer base had historically been a single domestic navy, gaining a second customer—and the world's most demanding one at that—was a profound signal that its technical standards travel.

But the move that crystallized the whole strategy came in April 2026, and it was the boldest thing this company has done in its modern era: its first-ever international acquisition.

Mazagon Dock purchased a 51% controlling stake in Sri Lanka's Colombo Dockyard PLC for $26.8 million, buying the shares from Japan's Onomichi Dockyard, which had long held the controlling interest.[^8] The headline price is almost comically small for a deal of this strategic weight—less than thirty million dollars for control of a fully operational, established shipyard. So the first question any disciplined investor must ask is: did they overpay, or did they steal it?

The evidence points firmly to the latter. For that $26.8 million, Mazagon Dock did not buy a distressed shell. It bought a working yard sitting directly astride the world's busiest East-West shipping lanes—the maritime highway down which a staggering share of global trade flows. And the timing was exquisite. In late 2025, just months before the acquisition closed, Colombo Dockyard had signed a roughly $150 million contract with France's Orange Marine to build advanced cable-laying vessels, with keel-laying reported in early April 2026.[^13] Pause on that arithmetic. Mazagon Dock acquired control of a yard whose freshly signed order book was several times the entire purchase price of its controlling stake. This is not capital recklessness; it is capital discipline of a high order—buying an active, revenue-generating asset for a fraction of the value of the work already booked inside it. The Navratna autonomy that let the board move on a deal this size without grinding through ministerial approval, you will recall, was the enabling mechanism.

And yet the financial bargain, impressive as it is, is almost a footnote to the geopolitical logic—which is where this transaction becomes genuinely fascinating. The acquisition is a deliberate strategic counterweight, executed under the banner of India's Maritime Amrit Kaal Vision 2047, the long-range national plan to make India a dominant maritime power by the centenary of its independence.9 Here is the chessboard. China holds a 99-year lease on Sri Lanka's Hambantota Port, a deep-water facility on the island's southern coast that has become a symbol of Beijing's expanding influence in India's maritime backyard. For New Delhi, watching a strategic rival entrench itself on the doorstep of the Indian Ocean has been a persistent anxiety.

By securing control of the dockyard in the Port of Colombo—Sri Lanka's commercial heart, just up the coast from the Chinese-leased Hambantota—India plants its own strategic repair footprint on the island. It gives the Indian Navy and India's commercial and dredging fleets a friendly, India-controlled dock to route their repairs through, rather than depending on foreign-controlled facilities. It is a move on the great-power board dressed up as a commercial shipyard acquisition. For under thirty million dollars, India bought both an order book and a foothold in one of the most contested stretches of ocean on the planet. Whether that foothold ultimately pays off commercially or proves a strategic distraction is a real question—but the logic behind it is anything but careless.

Having walked the entire enterprise—the steel, the treasury, the submarines, the leadership, and now the geopolitics—we can finally do what we came to do: subject Mazagon Dock to the cold frameworks that separate durable advantage from temporary luck.

VIII. The Playbook: Hamilton's 7 Powers & Porter's 5 Forces Applied (145:00 – 160:00)

Strip away the romance of warships and the drama of geopolitics, and the question every long-term investor must answer is brutally simple: what protects this business, and for how long? Frameworks are the discipline that keeps us honest here. Let's run Mazagon Dock through Hamilton Helmer's 7 Powers, then pressure-test it against Porter's Five Forces.

Hamilton's 7 Powers Framework

Cornered Resource (High). We touched this in the origin story, but it deserves its formal place here because it is the most durable power Mazagon Dock holds. The company controls three irreplaceable assets that stack on top of one another: the physical real estate on the Mumbai waterfront that cannot legally or physically be replicated by any new entrant; the highly classified licenses and security clearances required to build submarines and combat platforms; and a specialized workforce of naval architects and submarine tradespeople whose skills were accumulated over decades of foreign-collaboration programs. You cannot buy any of these on a market. The land is gone, the clearances take a generation of trust to earn, and the workforce was forged in the crucible of the Scorpene program. This is the bedrock.

Scale Economies (High). The heavy capital sunk into the Mazdock Modernization Project—the 300-tonne Goliath crane, the climate-controlled submarine shops, the wet basin—created a fixed-cost base that Mazagon Dock now spreads across multiple multi-billion-rupee hulls built in parallel. The more complex ships it builds simultaneously, the lower its per-unit assembly cost falls. No other yard in South Asia can match that overhead-absorption at the top of the complexity curve. This is the power that, in practice, defends the company even as nomination gives way to competitive bidding: rivals must underbid a competitor whose fixed costs are already amortized across a fleet.

High Switching Costs (High). This one is structurally enormous and underappreciated. A warship or submarine has a service life of 30 to 40 years. Across those decades, the vessel needs periodic Medium Refits and Life Certifications—deep overhauls that are nearly impossible to perform without the original builder's proprietary blueprints, specialized steel specifications, and integrated combat-management systems. Once Mazagon Dock builds a ship, it has effectively locked in the refit and life-extension work for the next four decades. The Navy is not just a customer; it is a captive of the installed base. Every hull delivered is an annuity stretching out across a generation.

Counter-Positioning (Low). Here we are honest about what Mazagon Dock is not. Counter-positioning is the power of a newcomer adopting a business model that incumbents cannot copy without damaging themselves. Mazagon Dock is the ultimate incumbent—a state-backed monopoly that wins through institutional lock-in and national indigenization policy, not through some clever model that competitors fear to imitate. It has no need for counter-positioning, and claiming it would be analytical dishonesty. Its powers are those of the entrenched, not the insurgent.

Porter's 5 Forces Analysis

Threat of New Entrants (Virtually Zero). The barriers here are about as high as they get in any industry on earth. A would-be competitor would need to replicate physical deep-water infrastructure in a country where suitable sites are scarce, earn security clearances that take decades of demonstrated trust, obtain naval certifications, and assemble a workforce that does not exist on the open market. The capital bill runs to billions, and the time bill runs to decades. This is why the competitive set has remained a stable handful of yards for two generations.

Bargaining Power of Buyers (High but Protected). The Ministry of Defence is a monopsony—a single dominant buyer—and in most industries a single buyer would crush its supplier's economics. But national defense is a sovereign priority, and that flips the usual dynamic. The buyer has every incentive to keep its sole heavy-destroyer and submarine builder financially robust, which is exactly why it pays generous front-loaded advances and historically guaranteed cost-plus margins. The buyer's power is real—it sets prices and can shift toward competitive bidding—but it is constrained by its own strategic dependence on the seller's survival. It is a leash, but the buyer dares not pull it too tight.

Threat of Substitutes (Virtually Zero). There is simply no substitute for a blue-water destroyer or a stealth conventional submarine when the mission is securing the Indian Ocean theater against capable rivals. You cannot deter a hostile navy with anything other than a navy. As long as India needs sea power, it needs the platforms Mazagon Dock builds, and there is no technological end-run around that need on any relevant time horizon.

Run the whole analysis and a clear picture emerges: Mazagon Dock's competitive position is about as fortified as a business can be, anchored by a cornered resource that literally cannot be recreated and switching costs measured in decades. The forces that usually erode returns—new entrants, substitutes—are essentially absent. The one genuine pressure point is the buyer, and even that is softened by the buyer's own strategic self-interest. Which is exactly why the bull and bear cases for this stock both hinge on the same fulcrum: the behavior of a single, sovereign customer.

IX. The Investor's Dilemma: Bull vs. Bear Case & KPIs to Watch (160:00 – 175:00)

So we arrive at the reckoning every investor must make—weighing what could go gloriously right against what could go quietly wrong. Let's argue both sides honestly, because the truth of Mazagon Dock lives in the tension between them.

The Bull Case

The bull case rests on three pillars, and the first is the submarine super-cycle. The imminent signing of the ₹99,000 crore Project 75(I) contract, should it land, would multiply the order book and lock in fifteen years of high-barrier, high-margin submarine work—the kind of revenue visibility that almost no manufacturing business anywhere enjoys.[^10] For a company whose current order book sits at ₹20,535 crore, a single contract that quadruples it transforms the entire forward picture.2

The second pillar is the MRO re-rating. The structural shift from low-margin domestic warship building toward higher-margin global commercial repair—via the Colombo Dockyard platform—and US Navy voyage repairs offers a path to expand the company's blended corporate EBITDA margins beyond their historically modest 12-15% range.2 If MRO grows into the recurring, high-margin annuity that management is clearly betting on, the market may eventually re-rate the whole enterprise from a lumpy defense contractor to a steadier, higher-quality compounder.

The third pillar is the one we have circled all episode: the sovereign cash cow. Debt-free, sitting on a treasury hoard north of ₹13,000 crore earning near-riskless interest, Mazagon Dock has a structural floor under its earnings that almost no industrial company can claim.2 That float is a shock absorber, a war chest for acquisitions, and a profit engine all at once.

The Bear Case

Now the other side, and a serious investor must take it just as seriously. The first risk is execution—the curse of lumpy, milestone-driven revenue. Warships depend on a global supply chain of specialized components: gearboxes, propulsion engines, radar and sensor systems, much of it imported. A delay in a single critical import—say, a propulsion engine from a German supplier—can defer an entire milestone and, with it, the revenue recognition tied to that milestone. The result is the savage quarterly lumpiness that has long characterized this stock. A weak quarter often reflects a delayed gearbox, not a broken business, but the market does not always make that distinction in real time.

The second risk strikes at the very heart of the financial machine—call it the "treasury cap" risk. Recall that interest on customer advances supplies roughly 45% of Profit Before Tax. That dependence is a double-edged sword. If the Navy tightens its payment terms or reduces the percentage it pays in advance—a plausible move as procurement practices evolve—the float shrinks, and with it the high-margin Other Income that props up nearly half the company's pre-tax profit. Strip out the treasury and the underlying manufacturing margin is thin. An investor who buys Mazagon Dock is, whether they realize it or not, taking a position on the durability of the Navy's advance-payment generosity and on the level of interest rates. Both can change.

The third risk is the slow erosion of the nomination regime. If the Ministry of Defence aggressively forces all future destroyer and frigate programs into competitive multi-vendor bidding, a capable and hungry private player like L&T could squeeze Mazagon Dock's margins on the surface-combatant business that supplies the bulk of revenue. The scale and switching-cost moats we identified are real defenses, but competitive bidding is precisely the mechanism designed to compress the comfortable cost-plus margins of the past. This is a structural, policy-driven risk that no amount of operational excellence can fully neutralize.

Key KPIs to Track

For a company this idiosyncratic, the usual headline metrics mislead. A long-term investor should anchor on three signals and largely ignore the noise.

First, Value of Production versus Revenue from Operations. Because revenue is recognized against milestones, accounting revenue can drift away from actual physical progress on the docks. Value of Production is the company's measure of the real physical work completed in a period. When VoP tracks revenue closely, the business is converting steel into recognized sales cleanly. When they diverge, something—a supply delay, a milestone slip—is worth investigating. This is the single best lie-detector for the lumpiness problem.

Second, the Order Book-to-Bill ratio. Historically healthy in the 2x to 3x range, this ratio tells you whether the pipeline is renewing fast enough to sustain future revenue. Watch it especially around the Project 75(I) decision: a strong award sends it soaring, while a stalled book—orders being burned through faster than they are replenished—is the early warning that the multi-year growth runway is shortening.

Third, the treasury cash balance and the interest yield on it. This is the direct gauge of the Other Income profit engine that drives nearly half of pre-tax profit. A shrinking cash pile signals either tightening Navy advances or heavy capital deployment; a falling yield signals the interest-rate environment turning against the float. Either way, this is the number that tells you whether the financial half of this dual-identity company is firing.

Track those three, and you are watching the actual machine rather than the quarterly theatrics around it. Everything else—the headlines about launches and keel-layings—is color, not signal.

X. Epilogue & Outro (175:00 – 180:00)

So what, in the end, is Mazagon Dock Shipbuilders?

The easy answer is that it is a defense company—a builder of gray steel warships and silent submarines for the Indian Navy. But that answer misses the soul of the thing. What we have really been examining across these three hours is one of the most unusual financial organisms in any public market: a highly sophisticated cash-flow compounder masquerading as a shipyard. It sits at the precise intersection of three forces that rarely converge in one enterprise—geopolitical necessity, which guarantees its demand; financial engineering, which turns its customer's advances into a sovereign-backed treasury; and state-backed technology transfer, which let it climb from a build-to-print contractor toward an owner of proprietary defense IP.

Trace the arc and the improbability of it stands out. A dry dock dug to patch the wooden ships of the East India Company in 1774 became, through nationalization, modernization, and a 157-times-oversubscribed public listing, a company that builds the most complex machines its nation manufactures—and that earns nearly half its pre-tax profit from interest on a float its customer is happy to provide. The land it stands on cannot be replicated. The skills it holds cannot be bought. The buyer it serves cannot afford to let it fail. And in 2026, for less than the price of a single small warship, it planted its flag across the water in Sri Lanka, turning a balance-sheet treasury into an instrument of national maritime strategy.

There are real risks—the lumpiness, the dependence on advance payments and interest rates, the slow drift toward competitive bidding that could thin the margins of the past. A thoughtful investor holds those squarely in view alongside the moats. But the story itself is unambiguous. This is the shipbuilder that helped turn the Indian Ocean into a fortress, and that, almost as a side effect, turned its own balance sheet into a treasury vault. Mazagon Dock—the sovereign compounder—is what happens when colonial geography, naval ambition, and financial discipline all wash up on the same Mumbai shore.

References

-

Mazagon Dock Shipbuilders Annual Report FY 2023-24 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Press Information Bureau — Navratna Status Announcement, 2024-06-25 ↩↩

-

India's Mazagon Dock signs repair agreement with US government — Reuters, 2023-09-08 ↩

-

Germany, India near $7 billion deal to build submarines — Bloomberg, 2023-06-07 ↩

-

Department of Public Enterprises (DPE) Guidelines on CPSE Performance Related Pay ↩↩

-

India's Maritime Amrit Kaal Vision 2047 — Ministry of Ports, Shipping and Waterways ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube