Max Healthcare Institute: Building India's Healthcare Powerhouse

I. Introduction & Episode Setup

The numbers tell a compelling story: India's second-largest hospital chain in terms of hospital revenue, EBITDA, and market capitalization, commanding a market value of over ₹1.2 trillion. This is Max Healthcare Institute—a company that has transformed from a fragmented regional operator into one of the most formidable healthcare platforms in emerging markets through a masterclass in private equity-led consolidation and operational excellence.

The central question we're exploring today isn't just how a hospital chain grew—it's how a combination of entrepreneurial vision, private equity sophistication, and operational expertise created extraordinary value in one of the world's most complex healthcare markets. This is a story about timing, transformation, and the art of building institutional healthcare in India.

We'll trace Max Healthcare's journey from its origins in post-liberalization India through multiple ownership transitions, examining how the company navigated the challenges of capital-intensive healthcare delivery while maintaining clinical excellence. The narrative arc takes us through organic expansion, international partnerships, the game-changing KKR-Radiant acquisition, pandemic-era public listing, and aggressive M&A-driven growth—all while generating exceptional returns for stakeholders.

Three key themes will guide our exploration: First, how healthcare consolidation creates value in fragmented emerging markets. Second, the mechanics of private equity value creation through operational transformation rather than financial engineering. And third, the delicate balance between commercialization and care delivery in building sustainable healthcare institutions.

This isn't just a business story—it's about solving one of humanity's most fundamental challenges: providing quality healthcare at scale in a developing nation. The Max Healthcare journey offers crucial lessons for entrepreneurs, investors, and policymakers grappling with similar challenges worldwide. From the boardrooms of global PE firms to the operating theaters of Delhi hospitals, this is the definitive account of how modern Indian healthcare was built, one acquisition at a time.

II. The Foundation Story: Healthcare in Post-Liberalization India

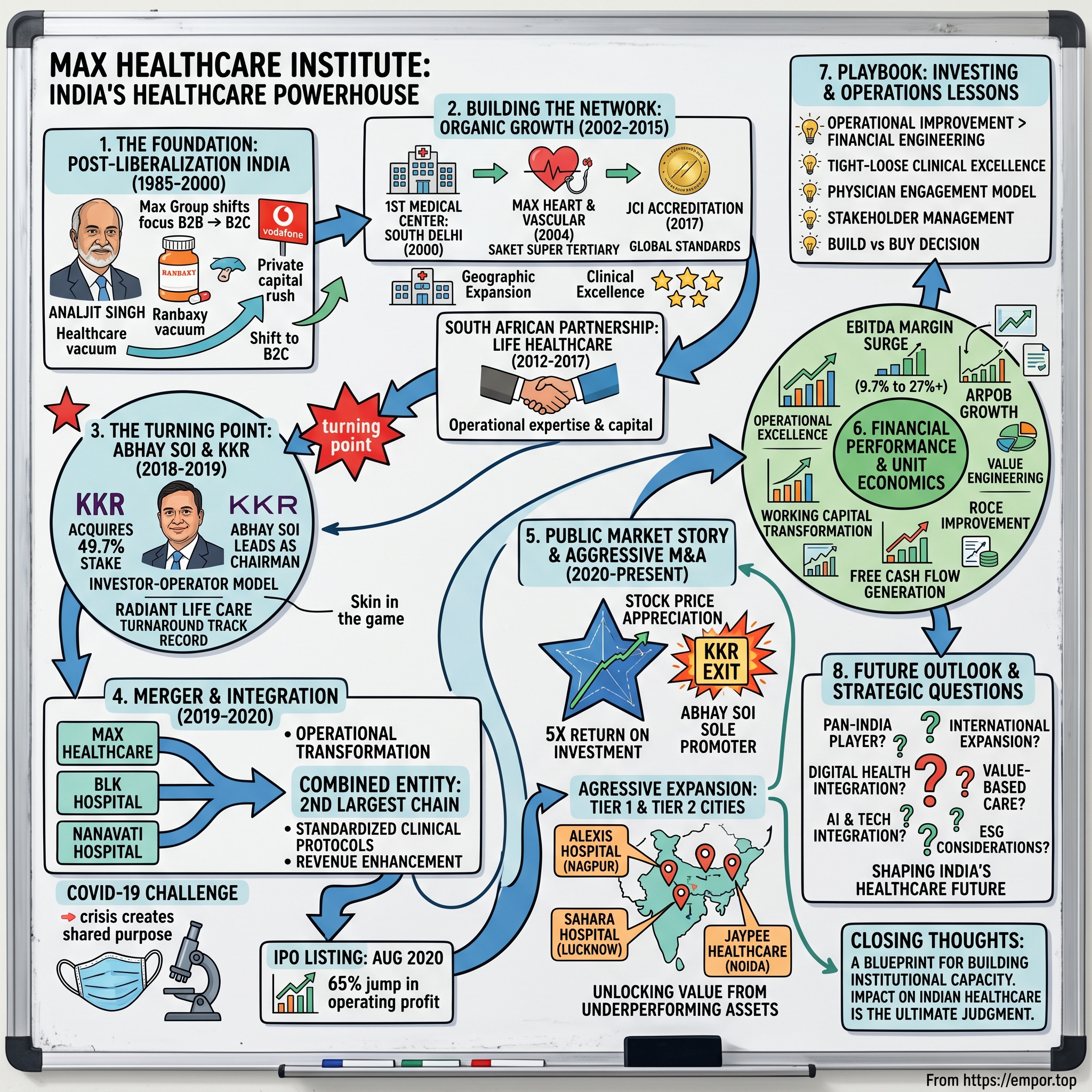

Max Healthcare's story begins with the Max Group, founded in 1985 by Analjit Singh following the death of his father Bhai Mohan Singh, founder of pharmaceutical company Ranbaxy Laboratories. But the healthcare venture itself would emerge much later, as Singh first built his business empire in other sectors. The company initially started life as a manufacturer of an active drug compound for penicillin, operating from an FDA-approved facility in Okhla, Delhi.

The India that Analjit Singh inherited in 1985 was fundamentally different from the one that would birth Max Healthcare. The 1991 economic liberalization marked a watershed moment for Indian business, and Singh was quick to recognize the opportunities. In 1993, the group ventured into telecommunications by forming a joint venture with Hutchison Asia Telecom Group, called Max Telecom, which was later sold to Vodafone and became Vodafone India. This early success in identifying and capitalizing on liberalization-era opportunities would prove crucial in shaping Singh's approach to healthcare.

The healthcare landscape of 1990s India presented both massive challenges and unprecedented opportunities. When India became independent of British rule in 1947, the private health sector provided only 5-10% of total patient care. By the time Max entered healthcare, it accounted for 82% of outpatient visits, 58% of inpatient expenditure, and 40% of births in institutions. This dramatic shift wasn't accidental—it was the direct result of deliberate policy choices and systemic underinvestment in public healthcare.

India's public spending on health care at 0.9% of gross domestic product was among the lowest in the world, ahead of only five countries—Burundi, Myanmar, Pakistan, Sudan, and Cambodia. This proportion had fallen from an already low 1.3% of GDP in 1991 when the neoliberal economic reforms began. The withdrawal of the state created a vacuum that private capital rushed to fill.

The Max Group shifted its focus from being a B2B to B2C company in 2000, by foraying into the fields of healthcare and life insurance. This wasn't just a business pivot—it was a recognition that India's growing middle class needed and could afford quality healthcare services. Max Healthcare opened its first medical center in South Delhi's Panchsheel Park in 2000, strategically choosing an affluent neighborhood where the demand for premium healthcare was evident.

The early 2000s saw rapid expansion. The company opened two other secondary care centers in Pitampura in North West Delhi and Noida in 2002. Each location was carefully chosen—Pitampura to serve North Delhi's emerging middle class, and Noida to tap into the burgeoning IT corridor's young professionals. Max Hospital, Pitampura became the first hospital to be ISO certified and first high-end secondary care centre in North Delhi, signaling the company's early commitment to quality standards that would differentiate it from competition.

The regulatory environment of this period was both enabling and challenging. The reduction in public health investments coupled with increase in user-fees in the public sector helped the private sector to fill the space and exploit the market opportunity. Private sector accounted for nearly four-fifth of the outpatient care services and almost half of inpatient care in India, happening in line with the emphasis given in health system reforms to increase involvement of voluntary, private players.

Building trust in private healthcare required more than just modern facilities. The Indian patient, historically dependent on government hospitals despite their shortcomings, needed convincing that private healthcare justified its premium pricing. Max's strategy was clear: offer international-standard care with Indian sensibilities. This meant investing heavily in medical technology while maintaining cultural sensitivity in patient care—a balance that many international entrants failed to achieve.

In a recent survey carried out by Transparency International, 30% of patients in government hospitals claimed that they had had to pay bribes or use influence to jump queues for treatment and for outpatient appointments with senior doctors, and to get clean bed sheets and better food in hospital. Against this backdrop, Max's promise of transparent, ethical healthcare delivery resonated strongly with patients who could afford to pay for dignity and quality.

The financing model for this expansion was crucial. Unlike the charitable trusts and religious foundations that had traditionally run private hospitals, Max represented a new breed of corporate healthcare—professionally managed, investor-backed, and growth-oriented. Large corporations and wealthy individuals—often from the Indian diaspora—had started providing health care to make money. They now dominated the upper end of the market, with five star hospitals manned by foreign trained doctors who provided services at prices that only foreigners and the richest Indians could afford.

Singh's vision went beyond just building hospitals. He understood that sustainable healthcare delivery required an ecosystem approach. This included developing standardized clinical protocols, investing in medical education and training, creating systems for quality assurance, and building a brand that stood for clinical excellence. Each element reinforced the others, creating a virtuous cycle that would prove difficult for competitors to replicate.

III. Building the Network: The Organic Growth Phase (2002-2015)

The period from 2002 to 2015 marked Max Healthcare's transformation from a collection of medical centers into a formidable hospital network. This wasn't just expansion—it was the methodical construction of North India's premier healthcare platform, built hospital by hospital, specialty by specialty, accreditation by accreditation.

In 2004, Max Heart & Vascular Institute opened in Saket as the first Super Tertiary Care Facility with Advanced Cardiac Life Support Ambulances and Air Evacuation Service. This wasn't merely another hospital opening—it represented Max's ambition to compete at the highest levels of clinical complexity. The Saket facility would become the flagship, the proving ground for Max's clinical capabilities and the training center for its next generation of medical leaders.

The strategic importance of cardiac care cannot be overstated. India was experiencing an epidemic of cardiovascular disease, driven by changing lifestyles, dietary patterns, and genetic predisposition. By establishing excellence in cardiac sciences early, Max positioned itself at the center of one of India's most pressing health challenges and lucrative medical specialties. The air evacuation service wasn't just a medical capability—it was a statement of intent, signaling that Max could handle the most critical cases from across the region.

Geographic expansion followed a clear logic. By 2005, Max Hospital in Patparganj emerged as the first multispecialty tertiary care centre in East Delhi. Each new facility filled a specific gap in Delhi-NCR's healthcare map, creating a network effect where patients could be referred within the Max system for specialized care. This internal referral network would prove crucial for both clinical outcomes and financial performance.

The pursuit of international accreditation became central to Max's differentiation strategy. Joint Commission International (JCI) accreditation, the gold standard for hospital quality globally, required fundamental changes in how Indian hospitals operated. It meant standardizing processes, implementing rigorous infection control protocols, establishing medication safety systems, and creating a culture of continuous quality improvement. In 2017, Max Super Speciality Hospital in Saket received prestigious Joint Commission International (JCI) accreditation, setting them up for international healthcare standards.

Beyond organic growth, Max recognized the importance of strategic partnerships. The most significant came from an unexpected source: South Africa. Life Healthcare, one of South Africa's largest private hospital operators, saw in Max an opportunity to enter the attractive Indian market. This wasn't just a financial investment—it brought operational expertise, international best practices, and credibility that money alone couldn't buy.

The partnership with Life Healthcare, which began with a 26% stake in 2012 and expanded to 49.7% by 2017, provided Max with more than capital. It offered access to Life Healthcare's experience in managing large hospital networks, insights into dealing with different payer models, and exposure to international clinical protocols. The South African healthcare system, having undergone its own transformation post-apartheid, offered valuable lessons for operating in a diverse, economically stratified market.

Talent acquisition and retention emerged as perhaps the greatest challenge during this expansion phase. India produces thousands of medical graduates annually, but the best often leave for opportunities abroad. Max needed to create an environment that could attract and retain top clinical talent. This meant competitive compensation, certainly, but also investment in continuous medical education, research opportunities, and a merit-based culture unusual in Indian healthcare's traditionally hierarchical environment.

The company's approach to medical specialization deserves particular attention. Rather than trying to be everything to everyone, Max chose to build centers of excellence in specific areas. Oncology, organ transplantation, neurosciences, and orthopedics became flagship programs, each with dedicated infrastructure, specialized teams, and focused marketing. This specialization strategy allowed Max to command premium pricing while achieving better clinical outcomes through volume and expertise.

Infrastructure development during this period was capital-intensive and complex. Building a modern hospital in urban India requires navigating byzantine regulations, managing construction in dense neighborhoods, and dealing with infrastructure challenges like power supply and water availability. Max learned to manage these challenges through a combination of political savvy, operational excellence, and strategic partnerships with local authorities.

The digital transformation of healthcare was just beginning during this period, and Max was an early adopter. Electronic medical records, picture archiving and communication systems (PACS) for radiology, and laboratory information systems were implemented across the network. While these required significant investment and caused temporary disruptions, they laid the foundation for operational efficiencies that would become crucial in later years.

Max Hospital in Noida focused on mother and child care alongside various specialities, recognizing the importance of obstetrics and pediatrics not just as medical specialties but as gateway services that introduced families to the Max ecosystem. A positive birthing experience often translated into lifetime loyalty, with families returning for pediatric care, vaccinations, and eventually, adult healthcare needs.

Quality metrics became an obsession. Infection rates, medication errors, patient satisfaction scores, clinical outcomes—everything was measured, benchmarked, and improved. Monthly quality reviews became forums for identifying best practices and addressing deficiencies. This data-driven approach to quality improvement, unusual in Indian healthcare at the time, would prove instrumental in Max's later ability to integrate acquisitions and maintain standards across a growing network.

The financial model evolved significantly during this period. Initial facilities were largely out-of-pocket focused, catering to affluent patients who could afford to pay. But as the network grew, Max began engaging more seriously with insurance companies and corporate clients. This required developing capabilities in insurance billing, corporate relationship management, and package pricing—competencies that would prove crucial as Indian healthcare financing evolved.

Regulatory challenges were constant companions. Healthcare in India is primarily a state subject, meaning regulations vary significantly across regions. Even within Delhi-NCR, different municipalities had different rules regarding hospital licensing, waste disposal, fire safety, and employment. Max developed a sophisticated regulatory affairs function, maintaining relationships with authorities while ensuring compliance across its growing network.

By 2015, Max Healthcare had established itself as North India's premium healthcare brand. The network included multiple hospitals, employed thousands of healthcare professionals, and served hundreds of thousands of patients annually. But success brought new challenges. The organic growth model was reaching its limits—prime urban land was increasingly scarce and expensive, competition was intensifying, and the capital requirements for continued expansion were enormous. The stage was set for a transformation that would redefine not just Max, but Indian healthcare itself.

IV. The Turning Point: Enter Abhay Soi and KKR (2018-2019)

The year 2018 marked a pivotal moment in Max Healthcare's history. The company, despite its strong brand and clinical reputation, faced significant challenges. Margins were under pressure, operational inefficiencies had crept in, and the capital structure needed optimization. The transformation that followed would become a case study in private equity value creation and operational turnaround.

Radiant Life Care Private Limited, a leading Indian hospital management company promoted by Abhay Soi and backed by KKR, completed the acquisition of a 49.7% stake in Max Healthcare Institute Limited from South Africa-based hospital operator Life Healthcare. Abhay Soi would now lead Max Healthcare as Chairman of its Board and Executive Council.

Understanding Abhay Soi's track record is crucial to appreciating what followed. This wasn't his first healthcare turnaround. Radiant forayed into healthcare in 2010 with the re-development and commissioning of BLK, a 650-bed hospital, one of the largest private sector hospitals in Delhi and NCR. Besides this flagship hospital, Radiant collaborated with the Nanavati Hospital Trust in 2014 to take over the operations of Nanavati, a 350-bed multi-specialty hospital in Mumbai.

The BLK turnaround was particularly instructive. When Soi took over, BLK was a struggling hospital with outdated infrastructure and poor financial performance. Through a combination of infrastructure investment, clinical program development, and operational improvements, he transformed it into one of Delhi's premier hospitals. The Nanavati experience added another dimension—managing a trust hospital with its unique stakeholder dynamics while implementing corporate management practices.

KKR's involvement brought more than just capital. Radiant funded this acquisition with an investment from KKR's Asian Fund III. The global private equity firm had been studying Indian healthcare for years, recognizing the sector's potential but waiting for the right opportunity and partner. In Soi, they found an operator who understood both healthcare delivery and financial value creation.

The transaction structure itself was complex and innovative. The acquisition was undertaken through a series of transactions, including Radiant's purchase of a 49.7% stake in Max Healthcare from Life Healthcare in an all cash deal, followed by demerger of Radiant's healthcare assets into Max Healthcare. Further, Max India would reverse merge into Max Healthcare creating a newly listed entity.

This wasn't just financial engineering—each element served a strategic purpose. The demerger of Radiant's assets (BLK and Nanavati hospitals) into Max created immediate scale and geographic diversification. The reverse merger with Max India provided a listing platform, offering liquidity to existing shareholders while maintaining operational control. Based on the share exchange ratio, the resultant shareholding of the Combined Entity would be 51.9%, 23.2% and 7.0% held by KKR, Abhay Soi and Max Promoters respectively.

The "investor-operator" model employed deserves special attention. Max Healthcare was entrusted to Abhay Soi, who played a pivotal role in operating the business and driving its value. Soi received a 23.1% stake to align his interests with KKR's, forming an investor-operator partnership. This wasn't a passive investment where PE firms simply provide capital and advice. Soi had skin in the game, with his personal wealth tied directly to Max's performance.

The operational transformation began immediately. At the time of KKR's investment, Max Healthcare was grappling with cost inefficiencies and low profit margins. Abhay Soi embarked on a journey to revamp the business. He employed several strategies including cost cutting and supply chain efficiencies by optimizing the supply chain, combining various functions to achieve economies of scale and renegotiating supplier contracts.

Supply chain optimization went beyond simple cost-cutting. Max had been operating as a collection of hospitals rather than an integrated network. Each facility negotiated its own contracts for medical supplies, pharmaceuticals, and equipment. By centralizing procurement, Max could leverage its scale to negotiate better prices while standardizing quality across the network. This alone generated millions in savings.

The clinical restructuring was equally important. Underperforming departments were either shut down or restructured. Clinical protocols were standardized across the network, reducing variability in care delivery while improving outcomes. High-margin specialties like oncology and cardiac sciences received additional investment, while low-margin services were optimized or outsourced.

Revenue enhancement initiatives complemented cost optimization. The average revenue per occupied bed (ARPOB) became a key metric, with systematic efforts to improve case mix, reduce discounting, and optimize bed utilization. The international patient program, historically underutilized, received renewed focus with dedicated teams and infrastructure.

Technology adoption accelerated under the new management. While Max had already invested in basic hospital information systems, the focus now shifted to analytics and decision support. Real-time dashboards tracked everything from bed occupancy to operating room utilization, enabling rapid intervention when metrics deviated from targets.

The transformation wasn't without challenges. Healthcare is inherently a people business, and rapid changes risked alienating doctors and staff. Soi managed this through a combination of communication, incentive alignment, and selective talent upgrades. Key clinicians were made stakeholders in the transformation through performance-linked incentives. Underperformers were counseled and, if necessary, replaced.

The merged entity would become the largest hospital network in North India and amongst the top three hospital networks by revenue—over 3,200 beds in 16 hospitals across India. The network would be supported by strong local brands such as BLK Hospital, Max Saket Hospital, Max Smart Hospital, Max Patparganj Hospital, Nanavati Hospital. The combined business was expected to drive significant growth and compelling business synergies.

The timing of this transformation, just before the COVID-19 pandemic, would prove fortuitous. The operational improvements and financial strengthening positioned Max to not just survive but thrive during the crisis. The integrated network could share resources, the improved financial position provided cushion during lockdowns, and the operational discipline enabled rapid adaptation to pandemic protocols.

Cultural integration posed unique challenges. Max had built its culture over two decades—formal, process-oriented, and hierarchical. BLK and Nanavati brought different cultures—more entrepreneurial but less structured. Creating a unified culture that preserved the best of each organization while eliminating inefficiencies required careful change management.

V. The Merger & Integration Playbook (2019-2020)

The period from 2019 to 2020 would test every aspect of the KKR-Radiant-Max combination. This was when strategy met execution, when PowerPoint projections confronted hospital floor realities, and when the COVID-19 pandemic added an unprecedented variable to an already complex equation.

In 2020, Max Healthcare merged with Radiant Lifecare, which operated BLK Hospital in Central Delhi and the Nanavati Hospital in Mumbai, to become the second-largest healthcare company in India by revenue. The company listed on the stock exchanges in August 2020. But these simple sentences obscure the enormous complexity of what actually transpired.

Integration began with the basics: creating unified systems and processes. Three different hospital groups meant three different ways of admitting patients, billing insurance companies, managing inventory, and scheduling doctors. The integration team, comprising members from all three organizations plus external consultants, worked through hundreds of standard operating procedures, deciding which to keep, which to modify, and which to discard.

The technology integration alone was a massive undertaking. Different hospital information systems, laboratory systems, and radiology systems needed to communicate with each other. Patient records needed to be accessible across the network while maintaining privacy and security. The decision was made to standardize on a single platform over time, but immediate interoperability was achieved through interfaces and data exchanges.

Clinical integration presented both opportunities and challenges. Each hospital had its strengths—Max in cardiac sciences and oncology, BLK in critical care and organ transplants, Nanavati in minimal access surgery. The challenge was to preserve these centers of excellence while creating network-wide standards. Clinical councils were established for each specialty, bringing together department heads to develop common protocols and share best practices.

The physician engagement model required particular attention. Doctors in Indian private hospitals often work on a fee-for-service model, with significant autonomy in their practice. Standardizing clinical protocols and implementing quality measures risked alienating these key stakeholders. The solution involved a combination of data-driven persuasion—showing how protocols improved outcomes—and financial incentives aligned with quality metrics.

Supply chain integration delivered immediate wins. Max Healthcare's EBITDA margin surged from 9.7% in FY2019 to an impressive 27.2% year-to-date in FY2022. This dramatic improvement wasn't magic—it was the result of systematic optimization. Vendor contracts were renegotiated using the combined entity's scale. Inventory management was centralized, reducing working capital requirements while ensuring availability. Generic substitution programs were implemented where clinically appropriate.

Then came COVID-19. The merger came into effect from June 01, 2020, right in the middle of India's first wave. What could have been a disaster became an opportunity to demonstrate the value of integration. The network's scale allowed for resource sharing—ventilators, oxygen supplies, and medical staff could be deployed where needed most. Centralized procurement proved invaluable in securing scarce supplies like PPE and medications.

The pandemic response showcased the operational discipline instilled by the new management. Protocols for COVID treatment were rapidly developed and deployed across the network. Dedicated COVID facilities were established, with clear separation from non-COVID areas. Telemedicine capabilities, previously nascent, were rapidly scaled to maintain continuity of care for non-COVID patients.

Financial management during this period was crucial. While COVID initially led to a sharp drop in elective procedures, the government's insurance schemes and the surge in COVID cases requiring hospitalization provided revenue cushion. The management's focus on cash conservation—deferring non-essential capital expenditure, optimizing working capital, and maintaining strict cost control—ensured financial stability.

The IPO preparation added another layer of complexity. This listing was the final outcome of the amalgamation of erstwhile Max India into Max Healthcare and demerger of healthcare businesses of Radiant Life into Max Healthcare pursuant to the Composite Scheme of Amalgamation and Arrangement as approved by the National Company Law Tribunal. Preparing for public listing while managing a pandemic and completing integration required extraordinary coordination.

The IPO timing seemed counterintuitive—listing during a pandemic when markets were volatile and investor sentiment uncertain. But the management recognized a unique window. Healthcare had moved from a niche sector to mainstream consciousness. The pandemic had demonstrated the critical importance of quality healthcare infrastructure. Moreover, Indian markets were flush with liquidity as global central banks pumped money into the system.

Max Healthcare recorded robust financial performance in FY 20, with net revenue of INR 4,026 Cr, with average occupancy of 72.5% over bed capacity of 3,391 beds. The company had operating margin of 14.6% with average revenue per operating bed of INR 51,000. The company out-performed peers on several operational metrics. The turnaround led to Max Healthcare posting 65% jump in operating profit in FY 20.

The cultural transformation during this period was remarkable. The crisis created a shared purpose that transcended organizational boundaries. Healthcare workers from Max, BLK, and Nanavati fought COVID together, creating bonds that no team-building exercise could have achieved. The hierarchy flattened as everyone from senior doctors to junior nurses worked together in crisis mode.

Quality metrics, surprisingly, improved during the pandemic. Infection control, always important, became existential. Hand hygiene compliance reached near 100%. Antimicrobial stewardship programs, designed to prevent resistance, were strengthened. These improvements, driven by COVID, created lasting changes in clinical practice.

The integration of back-office functions proceeded in parallel with clinical operations. Finance, human resources, marketing, and other support functions were consolidated. Shared service centers were established for transactional activities like payroll processing and accounts payable. This not only reduced costs but also improved service levels through standardization and automation.

Brand architecture required careful consideration. Max was the strongest brand in North India, but BLK and Nanavati had strong local recognition. The decision was made to maintain individual hospital brands while creating an overarching Max Healthcare corporate brand. This allowed preservation of local brand equity while leveraging network effects.

By late 2020, the integration was largely complete. Three organizations had become one, systems and processes were unified, and the network was operating as an integrated entity. The pandemic, rather than derailing integration, had accelerated it. Crisis had forced rapid decision-making and implementation that might have taken years in normal circumstances.

VI. Public Market Story & Expansion Strategy (2020-Present)

Going public during a pandemic might seem like madness, but for Max Healthcare, it proved to be masterful timing. The company listed on the stock exchanges in August 2020, entering public markets at a moment when healthcare's essential value had never been clearer and when abundant liquidity was searching for quality assets.

The public listing fundamentally changed Max Healthcare's trajectory. Access to capital markets provided the fuel for aggressive expansion, while public scrutiny enforced discipline in execution. The transparency requirements of a listed company—quarterly earnings calls, detailed disclosures, analyst coverage—created accountability that complemented the operational discipline already instilled.

The post-IPO performance validated the transformation story. The stock price appreciation reflected not just market exuberance but fundamental operational improvements. The company reported consolidated net PAT of INR 252 crores in quarter ending December 31, 2021. Over the past three years, the company achieved remarkable 32% compound annual growth rate in sales. Today, Max Healthcare stands as India's second-largest hospital chain in terms of revenue and market capitalization, boasting over 3,400 beds across 17 facilities.

Then came the surprising exit. Between 2021 and 2022, co-promoter KKR & Co. Inc. sold its entire stake in Max Healthcare. As a result, Abhay Soi became the sole promoter of the company with over 23% stake. This wasn't a distressed exit or a vote of no confidence—quite the opposite. KKR successfully exited Max Healthcare by selling its remaining 27.5% stake for INR 9,185 crores. This transaction marked a fivefold return on investment in just four years, as KKR had initially acquired the stake at INR 80 per share in 2018 and sold it at INR 353 per share in 2022.

The KKR exit, achieving a CAGR of approximately 63.75%, became legendary in Indian private equity circles. It demonstrated that healthcare, despite its complexity and capital intensity, could generate technology-like returns with the right operational approach. The exit also validated the investor-operator model, showing that aligned incentives and operational expertise could create extraordinary value.

With KKR's exit complete and Soi as sole promoter, Max Healthcare entered a new phase—aggressive expansion through acquisition. The company had proven its ability to integrate and improve hospitals; now it would do so at scale. The acquisition strategy was clear: focus on Tier 1 and Tier 2 cities with established healthcare ecosystems, acquire hospitals with good infrastructure but suboptimal operations, and integrate them into the Max network to realize synergies.

In Q4 FY24, Max Healthcare consummated two significant M&A transactions, adding approximately 750 beds to its capacity. The acquisitions included the 200-bed Alexis Hospital in Nagpur, effective February 9, 2024, and the 550-bed Sahara Hospital in Lucknow, effective March 7, 2024.

The Lucknow acquisition exemplified the strategy. Max Healthcare's acquisition of Sahara Hospital in Lucknow, involving total investment of ₹940 crore, marked Max Healthcare's first foray into the rapidly developing city. Starlit Medical Centre had previously agreed to acquire healthcare operations of Sahara Hospital from Sahara India Medical Institute Ltd through Business Transfer Agreement, facilitating the deal on slump sale basis.

Sahara Hospital represented exactly the type of opportunity Max sought. The prominent 550-bed healthcare facility located in 17-storey building offered wide range of medical services including gastroenterology, neurology, surgery, cardiology, and pulmonology. The facility, which included nursing college, currently operated with approximate capacity of 250 beds. It was reputed for its centre for neurosciences and catered to around two lakh patients each year.

The infrastructure was excellent—a modern building in a prime location. But operational performance lagged potential. Max Healthcare anticipated that the hospital would generate revenue of about ₹200 crore in fiscal year 2024, implying significant room for improvement given the 550-bed capacity. Max's playbook—operational improvement, clinical program enhancement, and network integration—could unlock substantial value.

The Nagpur acquisition followed similar logic. Max Healthcare announced acquisition of 100 per cent stake in 200-bed Nagpur-based Alexis Multi-Speciality Hospital Private Limited for enterprise value of Rs 412 crore. Max Healthcare added that bed capacity can be expanded to 340 beds in view of availability of floor area ratio for given land and strength of existing structure. The 200-bed hospital is recognised by Joint Commission International (JCI).

The Alexis acquisition strengthened Max's presence in Maharashtra, complementing the flagship Nanavati Hospital in Mumbai. This would be Max Healthcare's second hospital in Maharashtra after the 350-bed Nanavati Max Hospital situated in Mumbai, strengthening it in Western region, where healthcare company had seen weaker tailwinds.

Geographic expansion beyond the traditional North India stronghold was strategic. While Max dominated Delhi-NCR, growth opportunities there were becoming limited. Tier 1 and Tier 2 cities in other regions offered attractive demographics—growing middle class, increasing insurance penetration, and undersupply of quality healthcare. The challenge was selecting markets where Max's premium positioning would resonate.

The integration of acquired hospitals followed a proven playbook but with continuous refinement. Each acquisition taught lessons that improved the next integration. The Sahara integration, for instance, benefited from experiences with BLK and Nanavati. Standard operating procedures were ready, integration teams were experienced, and timelines were aggressive but realistic.

Financial performance during this expansion phase remained strong. The network operating EBITDA for FY24 stood at Rs 1,907 crore, marking 17% growth. Operating margin for FY24 was 27.8%, slightly higher than 27.7% recorded in FY23. These figures reflect company's strong operational efficiency and ability to generate substantial revenue growth.

The ability to maintain margins while expanding rapidly demonstrated operational excellence. Typically, acquisitions dilute margins as lower-performing assets are integrated. Max managed to buck this trend through rapid operational improvement and synergy realization. The acquisitions contributed Rs 42 crore to gross revenue and Rs 3 crore to operating EBITDA for the quarter, net of deal expenses. Integration of these hospitals into Max Healthcare's network expected to further bolster revenue and profitability.

Technology continued to play a crucial role in the expansion strategy. New acquisitions were quickly integrated into Max's technology backbone, enabling immediate operational visibility and control. Digital health initiatives, accelerated by COVID, became standard across the network. Telemedicine, remote monitoring, and digital engagement platforms extended Max's reach beyond physical hospitals.

The medical value travel (medical tourism) opportunity received renewed focus. With convenient flight connectivity to various countries, Max Healthcare aims to tap into burgeoning medical value travel segment by attracting patients from neighboring countries and Middle East to Max Super Speciality Hospital, Lucknow. India's cost advantage, combined with Max's quality credentials, positioned it well to capture this high-margin segment.

Capital allocation remained disciplined despite abundant opportunities. Not every available hospital was pursued—only those fitting strategic criteria and available at reasonable valuations. The company maintained a strong balance sheet, funding acquisitions through a combination of internal accruals and modest debt, avoiding the overleveraging that had troubled other aggressive acquirers.

The company reported free cash from operations of Rs 412 crore for Q4 FY24, and its net cash position stood at Rs 22 crore as of March 31, 2024. This cash generation capability, even while investing heavily in expansion, demonstrated the underlying strength of the business model.

Looking at the broader strategic picture, Max Healthcare's expansion wasn't just about adding beds. Each acquisition strengthened the network effect—more locations meant more patient referrals, better negotiating power with payors, greater attraction for clinical talent, and improved economies of scale. The company was building a platform that would become increasingly difficult for competitors to challenge.

VII. Financial Performance & Unit Economics Deep Dive

Understanding Max Healthcare's financial transformation requires diving deep into the unit economics that drive hospital profitability. The remarkable improvement in financial metrics from 2018 to 2024 tells a story of operational excellence, strategic focus, and disciplined execution that transformed Max from an underperforming asset into one of India's most profitable hospital chains.

For the fiscal year ended March 31, 2024, Max Healthcare reported gross revenue of Rs 7,215 crore, a 16% increase over the previous fiscal year. The network operating EBITDA for FY24 stood at Rs 1,907 crore, marking 17% growth. But these headline numbers only scratch the surface of the underlying transformation.

The EBITDA margin evolution tells the real story. Max Healthcare's EBITDA margin surged from 9.7% in FY2019 to impressive 27.2% year-to-date in FY2022. This 1,750 basis point improvement didn't happen by accident—it was the result of systematic improvements across every aspect of the business. For context, most Indian hospitals operate at EBITDA margins between 15-20%, making Max's performance exceptional.

The Average Revenue Per Occupied Bed (ARPOB) serves as the north star metric for hospital operations. ARPOB captures both pricing power and case mix complexity—higher ARPOB indicates either premium pricing, more complex procedures, or ideally both. The company had operating margin of 14.6% with average revenue per operating bed of INR 51,000 in FY20, which grew substantially in subsequent years.

Breaking down ARPOB growth reveals multiple drivers. First, the payor mix improved significantly. Insurance and corporate patients, who typically pay higher rates than walk-in patients, increased as a percentage of total revenue. International patients, paying premium rates, became a meaningful contributor. The government's insurance schemes, while lower-margin, provided volume that improved asset utilization.

Case mix optimization played a crucial role. The focus shifted toward complex, high-margin procedures—cardiac surgery, organ transplants, complex oncology, neurosurgery. These procedures not only commanded higher prices but also demonstrated Max's clinical capabilities, attracting more referrals and strengthening the brand. Simple, low-margin procedures weren't abandoned but were made more efficient through standardization and protocol-driven care.

Occupancy rates, the other key driver of hospital economics, showed consistent improvement. Hospital beds are perishable inventory—an empty bed today can never be sold tomorrow. Improving occupancy from 60% to 75% dramatically improves profitability since most costs are fixed. Max achieved this through better bed management, reduced average length of stay without compromising quality, and improved patient flow.

The working capital transformation deserves special attention. Hospitals typically struggle with working capital—insurance claims take months to settle, patients default on payments, and inventory of expensive medications and consumables ties up cash. Max systematically addressed each issue. Insurance claim processing was streamlined and automated, reducing settlement times. Credit policies were tightened without affecting patient access. Inventory management was centralized and optimized using predictive analytics.

Operating EBITDA stood at Rs 632 crore, reflecting 26 percent growth. The network's EBITDA margin stood at 27.2 percent, compared to 28 percent in Q4FY24. The slight margin compression reflected the integration of newly acquired hospitals, which initially operated at lower margins before improvement initiatives took effect.

Cost structure optimization went beyond simple cost-cutting. The focus was on value engineering—maintaining or improving quality while reducing costs. Generic substitution programs were implemented where clinically appropriate. Consumables were standardized, reducing SKUs and improving procurement leverage. Energy efficiency initiatives reduced utility costs. Outsourcing of non-core activities like housekeeping and security improved service while reducing costs.

The capital efficiency metrics showed dramatic improvement. Return on Capital Employed (ROCE), which measures how efficiently a company uses its capital, improved from single digits to mid-teens. This improvement came from both higher margins and better asset utilization. The company learned to do more with less—generating higher revenues from existing infrastructure before adding new capacity.

Free cash flow generation became a hallmark of the transformed Max. Cash from operations for the network during year ended Mar'25 was Rs 1,447 crore. This cash generation funded expansion without excessive leverage, maintained dividend payments to shareholders, and provided buffer for opportunistic acquisitions.

The international patient program emerged as a high-margin growth driver. It saw 28 per cent year-on-year increase in international patient revenue to Rs 202 crore in Q4 FY25, comprising nearly 9 per cent of hospital's revenue. International patients typically paid 2-3x Indian rates, stayed in premium rooms, and required minimal marketing spend due to word-of-mouth referrals.

Comparing Max's financial performance with peers highlighted its outperformance. Apollo Hospitals, India's largest chain, operated at EBITDA margins around 20-22%. Fortis Healthcare, despite its larger network, generated lower margins due to operational challenges. Regional players typically operated at even lower margins due to lack of scale. Max's combination of scale, operational excellence, and premium positioning created a unique competitive position.

The financial discipline extended to capital allocation. Growth capital expenditure was carefully evaluated using rigorous return metrics. Maintenance capital expenditure was optimized without compromising safety or quality. The company learned to phase investments, starting with high-return investments like medical equipment before moving to amenity improvements.

Revenue cycle management, often overlooked in hospital operations, received significant attention. The entire patient journey from admission to discharge and payment collection was mapped and optimized. Pre-authorization processes were streamlined to reduce insurance denials. Discharge processes were improved to reduce delays and improve patient satisfaction while ensuring complete billing.

The impact of technology on financial performance cannot be overstated. Analytics platforms provided real-time visibility into financial metrics, enabling rapid intervention when performance deviated from targets. Predictive models forecast patient volumes, helping optimize staffing and inventory. Automated billing systems reduced errors and improved collection rates.

Revenue from operations increased 30.01 percent to Rs 7028.46 crore in FY25, against Rs 5406.02 crore in FY24. Network operating EBITDA grew by 22 percent over year ended Mar'24, and stood at Rs 2,319 crore. Operating margin for FY25 was 26.8 percent, including new units, against 27.8 percent in last year.

The slight margin compression in FY25 reflected the J-curve effect of new acquisitions—margins initially dip as integration costs are incurred and operational improvements take time to implement. Historical experience showed that acquired hospitals typically reached network-average margins within 18-24 months of acquisition.

Looking at return metrics, the transformation was even more impressive. Return on Equity (ROE) improved from single digits to mid-teens, creating substantial shareholder value. The improvement came from both higher profitability and modest financial leverage. Unlike some peers who leveraged aggressively to grow, Max maintained conservative debt levels, providing financial flexibility and reducing risk.

The sustainability of these financial improvements was constantly tested. Were the margin improvements one-time gains from cost-cutting, or were they structural improvements that could be sustained and built upon? The consistent performance over multiple years, through COVID disruption and rapid expansion, suggested the latter. The company had fundamentally transformed its operating model, not just optimized the existing one.

VIII. Playbook: Healthcare Investing & Operations Lessons

The Max Healthcare story offers a masterclass in healthcare investing and operations, with lessons that extend far beyond hospitals to any capital-intensive, operationally complex business. The playbook developed through this journey—refined through multiple acquisitions, integration challenges, and market cycles—provides a template for value creation in emerging market healthcare.

The PE consolidation playbook in fragmented industries starts with a fundamental insight: operational improvement, not financial engineering, drives sustainable value creation. KKR's approach with Max exemplified this. Rather than leveraging the company aggressively or pursuing risky strategies, they focused on fundamental operational improvements. The investor-operator model, with Abhay Soi holding significant equity, aligned incentives perfectly. This wasn't a case of PE firms extracting value through dividends or fees—value was created and shared.

Building clinical excellence while scaling operations presents a fundamental tension in healthcare. Scale typically requires standardization, while clinical excellence often demands customization and physician autonomy. Max resolved this tension through a "tight-loose" model—tight on core processes like infection control and medication safety, loose on clinical decision-making within evidence-based protocols. This preserved physician autonomy while ensuring consistent quality.

The approach to physician engagement proved crucial. Indian healthcare traditionally operates on a fee-for-service model where doctors are independent practitioners using hospital infrastructure. Max gradually shifted toward an employed physician model in key specialties, offering competitive salaries plus performance incentives. This provided better control over quality and patient experience while aligning physician incentives with hospital objectives.

Managing diverse stakeholders—doctors, nurses, patients, regulators, investors—required sophisticated stakeholder management. Each group had different priorities and concerns. Doctors wanted clinical autonomy and fair compensation. Nurses wanted respect and career development. Patients wanted quality care at reasonable prices. Regulators wanted compliance and public health objectives met. Investors wanted returns. Balancing these sometimes conflicting demands required clear communication, transparent policies, and occasionally, difficult trade-offs.

Technology adoption in emerging market healthcare faces unique challenges. Unlike developed markets where healthcare IT is mature, Indian hospitals often leapfrog generations of technology. Max avoided the trap of over-investing in technology for its own sake. Instead, technology investments were evaluated based on clear ROI metrics—either revenue enhancement through improved patient experience or cost reduction through operational efficiency.

The brand building journey in trust-based businesses like healthcare requires patience and consistency. Trust, once lost, is nearly impossible to regain. Max invested heavily in clinical quality, knowing that outcomes ultimately drive reputation. Marketing focused on clinical capabilities rather than amenities. Patient testimonials and clinical outcome data became more powerful than any advertising campaign.

Capital allocation in healthcare requires balancing multiple time horizons. Some investments, like medical equipment, generate immediate returns. Others, like brand building or physician training, take years to pay off. Max developed a portfolio approach—quick wins funded long-term investments. The discipline to maintain this balance, even under pressure for quarterly earnings, proved crucial.

The build versus buy decision framework evolved through experience. Initially, organic expansion seemed attractive—complete control over quality, culture, and operations. But the reality of finding land, obtaining permissions, and construction timelines made organic growth slow and expensive. Acquisitions offered immediate capacity but came with integration challenges. The optimal strategy proved to be a combination—acquiring platforms in new markets, then expanding organically within those markets.

Price discipline in acquisitions remained paramount despite abundant capital. The temptation during bull markets is to overpay, justifying high prices through aggressive synergy assumptions. Max maintained valuation discipline, walking away from overpriced assets. This patience proved valuable—sellers eventually became more realistic, and better opportunities emerged.

Integration playbook refinement through repetition became a competitive advantage. Each acquisition taught lessons that improved the next integration. Standard operating procedures were documented. Integration teams became experienced. Timelines compressed from 18-24 months to 12-15 months. This integration capability became a moat—competitors couldn't replicate years of learning quickly.

The importance of patient mix and payer diversification became evident during COVID. Hospitals dependent on international patients or elective procedures suffered severely. Max's diversified payer mix—insurance, corporate, government schemes, and self-pay—provided resilience. No single payer dominated, reducing negotiating leverage and concentration risk.

Cultural transformation in traditional industries requires patience and persistence. Healthcare in India has deep-rooted traditions and hierarchies. Changing culture—from physician-centric to patient-centric, from department silos to integrated care, from individual excellence to team-based care—took years. Success required consistent messaging, aligned incentives, and visible leadership commitment.

The regulatory navigation strategy balanced compliance with advocacy. Rather than viewing regulation as a constraint, Max engaged constructively with regulators, often exceeding minimum requirements. This proactive approach built regulatory goodwill, valuable during crisis situations or when seeking approvals for expansion.

Talent development and retention in skill-short markets like healthcare required innovative approaches. Max established training programs, partnered with medical colleges, and created career pathways for nurses and technicians. The investment in talent development paid dividends through lower attrition, better clinical outcomes, and enhanced reputation among medical professionals.

The operational excellence journey never ends. Even after achieving industry-leading margins, continuous improvement remained embedded in the culture. Monthly performance reviews, benchmarking against global best practices, and systematic problem-solving ensured that complacency never set in. The Japanese concept of kaizen—continuous incremental improvement—became part of Max's DNA.

Risk management in healthcare extends beyond financial risk to clinical, regulatory, and reputational risk. Max developed sophisticated risk management systems—clinical quality committees, regulatory compliance teams, and crisis management protocols. The ability to identify and mitigate risks before they materialized prevented costly crises.

The network effects in healthcare proved powerful but took time to materialize. Initially, each hospital operated independently. Over time, physician referrals within the network increased. Centers of excellence in one hospital attracted patients to the entire network. Shared services reduced costs. Brand strength in one market facilitated entry into adjacent markets. These network effects created competitive advantages that standalone hospitals couldn't match.

Partnership strategies evolved from transactional to strategic. Early partnerships focused on immediate needs—equipment suppliers, insurance companies. Over time, partnerships became more strategic—clinical collaborations with international hospitals, research partnerships with pharmaceutical companies, training partnerships with medical colleges. These partnerships provided capabilities that would have been expensive or impossible to develop internally.

The importance of timing in healthcare investing cannot be overstated. KKR's entry in 2018 preceded COVID by two years—enough time to implement operational improvements but before the pandemic accelerated healthcare sector growth. The exit in 2021-22 captured peak valuations as healthcare commanded premium multiples. This timing wasn't luck—it reflected deep sector understanding and patient capital.

IX. Bear vs. Bull Case Analysis

Every investment thesis faces both tailwinds and headwinds, and Max Healthcare is no exception. Understanding both the bull and bear cases is essential for evaluating the company's future trajectory and the sustainability of its remarkable transformation.

The Bull Case: Structural Growth and Operational Excellence

The massive under-penetration of quality healthcare in India provides the foundation for the bull case. India spends only about 3.5% of GDP on healthcare versus 10-17% in developed countries. With rising incomes, increasing insurance penetration, and growing health awareness, healthcare spending is poised for multi-decade growth. Max, as a premium provider with proven operational capabilities, is ideally positioned to capture disproportionate value from this growth.

The demographic dividend strongly favors healthcare providers. India's population is aging, with the 60+ cohort growing faster than overall population. This age group consumes healthcare at 3-4x the rate of younger cohorts. Additionally, the epidemiological transition from infectious to lifestyle diseases—diabetes, cardiovascular disease, cancer—favors sophisticated tertiary care providers like Max over basic primary care facilities.

In September 2024, Max Healthcare acquired 64% stake in Jaypee Healthcare at enterprise value of ₹1,660 crore, gaining control of three hospitals in Noida, Bulandshahr and Anupshahr. This demonstrates the continuing M&A opportunity. India has thousands of subscale, underperforming hospitals that could benefit from Max's operational expertise. The proven integration playbook and strong balance sheet position Max to consolidate the fragmented market.

The medical tourism opportunity remains largely untapped. India offers procedures at 10-20% of Western costs with comparable quality. Max's JCI accreditations, clinical outcomes, and premium positioning make it attractive for international patients. As global healthcare costs rise and waiting times increase in developed countries, medical tourism to India could explode.

Operating leverage as occupancy improves provides significant earnings upside. Hospitals have high fixed costs—staff, equipment, infrastructure. Incremental occupancy drops almost directly to the bottom line. With new acquisitions operating below optimal occupancy, improvement to network averages could drive substantial margin expansion.

The insurance penetration story is still early. Health insurance coverage in India remains below 40%, compared to near-universal coverage in developed markets. Government schemes like Ayushman Bharat are expanding coverage. Private insurance is growing at 15-20% annually. As insurance penetration increases, hospital volumes and pricing power should improve.

Digital health integration could unlock new revenue streams. Telemedicine, remote monitoring, and digital therapeutics extend Max's reach beyond physical hospitals. These asset-light models could generate high-margin revenues while strengthening patient relationships. Max's brand and clinical credibility provide advantages in digital health that pure-play startups lack.

The Bear Case: Risks and Challenges

Regulatory risks and price controls pose the most immediate threat. Healthcare is politically sensitive in India. The government could impose price caps on procedures, mandate free or subsidized care, or change regulations adversely. The National Medical Commission's moves toward standardizing medical education and practice could reduce physician availability or increase costs.

Competition from new-age healthcare models challenges traditional hospitals. Retail health chains offering basic services at lower costs are proliferating. Single-specialty chains in areas like ophthalmology and dentistry offer focused services more efficiently. Digital health platforms provide convenience that physical hospitals can't match. These models could cherry-pick profitable services, leaving hospitals with complex, lower-margin cases.

Concentration risk in North India remains significant despite expansion. Delhi-NCR still accounts for the majority of revenues and profits. Economic slowdown, pollution-related health issues, or competitive intensity in this region would disproportionately impact Max. Geographic diversification is happening but slowly.

The high valuation multiples leave little room for error. The P/E ratio of Max Healthcare Institute is 112.26 times, a 118% premium to its peers' median range of 51.45 times. These valuations embed high growth expectations. Any disappointment in growth or margins could trigger significant multiple compression.

Execution risk on rapid expansion is real. Integrating multiple acquisitions simultaneously stretches management bandwidth. Each new market has unique dynamics—competitive landscape, payer mix, regulatory environment. The playbook that worked in Delhi might not work in Chennai or Kolkata. Cultural differences across regions could complicate integration.

Healthcare cost inflation could pressure margins. Medical equipment, pharmaceuticals, and talent costs are rising faster than general inflation. Salary inflation for doctors and nurses, driven by supply-demand imbalances, is particularly acute. If Max can't pass these costs to patients due to competitive or regulatory pressures, margins could compress.

Technological disruption could challenge traditional hospital models. AI-powered diagnostics could reduce the need for specialist consultations. Robot-assisted surgery could be performed remotely, reducing the advantage of physical presence. Gene therapy and precision medicine could shift treatment from hospitals to specialized centers. Max must continuously invest to stay relevant.

Economic sensitivity of healthcare spending is often underestimated. While healthcare is considered essential, discretionary procedures—cosmetic surgery, joint replacements, fertility treatments—are postponable. Economic downturns could reduce volumes and pressure pricing. The COVID experience showed that even essential procedures could be deferred.

Talent availability and retention challenges could constrain growth. India produces many doctors, but quality specialists are scarce. The best often emigrate for better opportunities. Nurses face even more acute shortages. As Max expands, attracting and retaining quality clinical talent becomes increasingly challenging and expensive.

Balancing the Cases

The weight of evidence suggests the bull case currently dominates, but bear case risks require constant monitoring. The structural growth drivers—demographics, disease burden, under-penetration—are powerful and persistent. Max's operational capabilities and financial strength position it well to capitalize on these trends.

However, the bear case risks are real and could materialize suddenly. Regulatory changes could happen overnight. Competition is intensifying. Valuations provide little cushion for disappointment. Successful navigation requires continuous innovation, operational excellence, and strategic flexibility.

The most likely scenario is neither pure bull nor bear but a complex evolution. Max will likely continue growing and generating value, but at moderating rates as the company scales. Margins might compress from current peaks but remain healthy. Valuation multiples could normalize but remain premium to the broader market. The company that emerges might look quite different from today—perhaps more digital, more specialized, more international—but still creating substantial value.

X. Future Outlook & Strategic Questions

As Max Healthcare stands at this inflection point—having successfully transformed operations, completed multiple acquisitions, and established market leadership—fundamental strategic questions will determine its trajectory over the next decade. These aren't just business decisions but choices that will shape Indian healthcare's evolution.

Can Max become a pan-India player versus maintaining regional dominance?

The ambition to become truly pan-Indian faces both opportunities and obstacles. India isn't one healthcare market but dozens of regional markets with distinct characteristics. Tamil Nadu's healthcare landscape, dominated by regional chains like Apollo and Kauvery, differs vastly from Bihar's underserved markets. Max must decide whether to pursue presence across all major markets or double down on markets where it has competitive advantages.

The pan-India expansion would require massive capital, potentially diluting returns. Each new region means understanding local regulations, building relationships with physicians, and establishing brand recognition. The alternative—deepening presence in existing markets through capacity addition and capability enhancement—might generate better risk-adjusted returns.

The answer likely lies in selective expansion. Focus on metros and Tier 1 cities where Max's premium positioning resonates. Enter new geographies through acquisitions of established platforms rather than greenfield developments. Build centers of excellence that attract patients nationally rather than trying to be everything everywhere.

International expansion possibilities

The success of Indian IT services companies in going global provides a template, but healthcare is fundamentally different. Healthcare delivery is local, regulated, and culture-specific. Yet opportunities exist. The Middle East, with its large Indian diaspora and underdeveloped healthcare infrastructure, presents obvious potential. Africa, with rapidly growing economies and minimal healthcare infrastructure, offers longer-term opportunity.

International expansion could take multiple forms. Management contracts to operate hospitals without capital investment. Joint ventures with local partners who understand regulatory and cultural nuances. Acquisition of distressed assets in markets experiencing healthcare sector disruption. Each model has different risk-return profiles and capability requirements.

The key question is whether international expansion would distract from massive domestic opportunities or provide valuable diversification and learning. The answer depends on Max's organizational capacity and strategic patience.

Digital health integration strategy

Digital health isn't just about telemedicine—it's about reimagining healthcare delivery. Chronic disease management through remote monitoring. AI-powered diagnostics reducing the need for specialist consultations. Digital therapeutics replacing or augmenting traditional treatments. Max must decide how aggressively to pursue digital transformation.

The challenge is that digital health often cannibalizes traditional hospital revenues. A successful diabetes management app might reduce hospital admissions. Effective telemedicine might decrease outpatient visits. Yet not pursuing digital transformation risks disruption by new entrants. The solution requires careful portfolio management—investing in digital while protecting the core business.

The opportunity lies in using digital to extend reach and strengthen relationships. Digital touchpoints between hospital visits improve outcomes and loyalty. Data from connected devices enables predictive interventions. The hospital becomes the hub of a broader health management ecosystem rather than just a site for episodic care.

Insurance penetration impact on business model

Rising insurance penetration is generally positive for hospitals, but the details matter enormously. Government insurance schemes provide volume but at low prices. Private insurance offers better margins but involves complex approval processes and payment delays. The evolution of the payer mix will fundamentally impact Max's business model.

The key strategic question is whether to optimize for the current cash-heavy model or prepare for an insurance-dominated future. This affects everything from service design to pricing strategy to working capital management. The U.S. experience, where hospitals became overly dependent on insurance and lost pricing power, provides a cautionary tale.

The optimal strategy likely involves maintaining payer diversity while building capabilities for insurance-based care. This means investing in revenue cycle management, developing standardized treatment protocols that insurers accept, and perhaps creating proprietary insurance products that align incentives.

Next generation of healthcare delivery models

Healthcare delivery is evolving globally from volume-based to value-based care. Instead of being paid for procedures, providers are paid for outcomes. This fundamental shift requires different capabilities—population health management, care coordination, risk bearing. Max must decide whether and how quickly to embrace value-based care.

The Indian market isn't yet ready for pure value-based models, but hybrid models are emerging. Corporate wellness programs that combine preventive care with acute treatment. Bundled payments for specific procedures like joint replacements. Disease management programs for chronic conditions. Each represents a step toward value-based care.

The strategic imperative is building capabilities while the core business remains fee-for-service. This means investing in data analytics to understand population health patterns. Developing care coordination capabilities across the continuum. Building partnerships with primary care providers, diagnostic chains, and pharmacies. The transition will take years, but preparation must begin now.

Potential for value-based care transition

The shift to value-based care isn't just a payment model change—it's a fundamental reimagining of healthcare delivery. Success requires different metrics (outcomes versus volume), different capabilities (prevention versus treatment), and different partnerships (collaboration versus competition). Max's hospital-centric model would need substantial evolution.

The opportunity is significant. Value-based care aligns provider and patient incentives, potentially improving outcomes while reducing costs. Early movers could capture disproportionate value as the market shifts. Max's operational excellence and data capabilities provide advantages in managing population health.

The challenges are equally substantial. Value-based care requires bearing insurance risk, a completely different business from healthcare delivery. It requires coordinating care across multiple providers, challenging in India's fragmented healthcare system. It requires patient engagement and behavior change, difficult in any market.

Technology and AI integration

Artificial intelligence promises to transform healthcare, from diagnostic accuracy to treatment planning to operational efficiency. Max must decide how aggressively to invest in AI and where to focus—clinical applications, operational optimization, or patient engagement.

The clinical applications are most promising but also most complex. AI-powered diagnostic tools could improve accuracy and reduce costs. Predictive models could identify high-risk patients for early intervention. Treatment planning algorithms could optimize outcomes while minimizing costs. But each application requires extensive validation, regulatory approval, and physician acceptance.

Operational applications might provide quicker wins. AI can optimize scheduling, reduce wait times, and improve asset utilization. Predictive maintenance can prevent equipment failures. Natural language processing can automate documentation. These applications face fewer regulatory hurdles and can generate immediate ROI.

Sustainability and ESG considerations

Environmental, social, and governance factors increasingly influence investment decisions and corporate reputation. Healthcare, as a major employer and resource consumer, faces particular scrutiny. Max must balance growth ambitions with sustainability commitments.

The environmental challenges are significant. Hospitals consume enormous energy and water, generate hazardous waste, and contribute to antimicrobial resistance. Addressing these requires investment in green buildings, waste management systems, and antimicrobial stewardship programs. The payoff comes through reduced operating costs and enhanced reputation.

Social responsibilities extend beyond patient care to employee welfare and community health. This means fair wages for support staff, career development for nurses, and community health programs. The challenge is balancing these investments with shareholder returns. The opportunity is building a sustainable competitive advantage through stakeholder loyalty.

XI. Closing Thoughts

The Max Healthcare journey from a single medical center in Panchsheel Park to India's second-largest hospital chain is more than a business success story—it's a blueprint for building institutional capacity in emerging markets. The transformation orchestrated by KKR and Abhay Soi, generating a CAGR of approximately 63.75% in just four years, demonstrates that operational excellence, not financial engineering, creates sustainable value.

The key takeaways for healthcare consolidation in emerging markets are clear. First, fragmentation creates opportunity—but only for operators with the capability to integrate and improve acquisitions. Second, alignment between capital and operations through the investor-operator model generates superior outcomes. Third, patience and discipline in execution matter more than aggressive growth targets.

For founders and investors, the Max story offers crucial lessons about building in capital-intensive sectors. Success requires patient capital willing to invest through cycles. It demands operational expertise that goes beyond financial analysis. Most importantly, it needs alignment between stakeholders—investors, operators, employees, and communities—to create sustainable value.

The role of patient capital in building healthcare infrastructure cannot be overstated. Healthcare isn't a quick flip—it requires years of investment before generating returns. KKR's willingness to invest substantial capital and wait four years for returns, while supporting operational transformation, exemplifies the patient capital needed to build critical infrastructure in emerging markets.

The broader implications extend beyond healthcare to any industry undergoing consolidation and institutionalization. The playbook—identify fragmented markets with structural growth, partner with exceptional operators, focus on operational improvement, execute disciplined M&A, and exit at optimal valuations—applies across sectors and geographies.

Looking ahead, Max Healthcare faces both enormous opportunities and significant challenges. The structural growth drivers remain intact—aging populations, rising disease burden, increasing insurance penetration. The company's operational capabilities and financial strength position it well to capitalize. But success isn't guaranteed. Regulatory changes, competitive dynamics, and technological disruption could challenge the current model.

The ultimate judgment of Max Healthcare's journey won't be just financial returns but its impact on Indian healthcare. Has it improved access to quality care? Has it raised standards across the industry? Has it created sustainable models that others can replicate? These questions will determine whether Max Healthcare is remembered as a financial success or a transformational force in Indian healthcare.

For India, the Max Healthcare story represents both achievement and challenge. The achievement is building world-class healthcare infrastructure through private enterprise. The challenge is ensuring such quality remains accessible to broader populations. The tension between commercial success and social responsibility will continue shaping healthcare policy and business models.

The lessons for other emerging markets are particularly relevant. Countries across Asia, Africa, and Latin America face similar challenges—fragmented healthcare delivery, underinvestment in infrastructure, rising disease burden. The Max model—private capital, operational excellence, and gradual consolidation—offers one path forward. But each market requires adaptation based on local conditions, regulations, and culture.

For the global healthcare industry, Max Healthcare demonstrates that emerging markets aren't just sources of cost arbitrage but can be centers of innovation. The frugal innovation required to deliver quality care at Indian price points creates models applicable globally. The operational excellence developed in resource-constrained environments provides lessons for developed market providers facing cost pressures.

The human element shouldn't be forgotten in this business narrative. Behind the financial metrics and strategic moves are thousands of healthcare workers delivering care, millions of patients seeking treatment, and communities depending on accessible healthcare. Max Healthcare's success ultimately depends on continuing to serve these stakeholders while generating returns for shareholders.

As we conclude this deep dive into Max Healthcare's journey, it's worth reflecting on what this means for the future of healthcare delivery. The traditional model of standalone hospitals competing independently is giving way to integrated networks leveraging scale and technology. The focus is shifting from treating disease to managing health. The boundaries between physical and digital, primary and tertiary, prevention and treatment are blurring.

Max Healthcare stands at the forefront of these transitions, with the capabilities and capital to shape India's healthcare future. Whether it fulfills this potential depends on strategic choices made today, operational excellence maintained tomorrow, and the ability to adapt to an uncertain future. The story is far from over—in many ways, it's just beginning.

The Max Healthcare narrative ultimately demonstrates that building transformational businesses in emerging markets requires more than capital and strategy—it demands patience, persistence, and purpose. For entrepreneurs attempting to build the next Max Healthcare, for investors seeking similar returns, and for policymakers shaping healthcare's future, the lessons are clear: think long-term, focus on operations, align incentives, and never lose sight of the ultimate purpose—improving human health and well-being.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube