MAS Financial Services Limited: The Compounder of Ahmedabad

I. Introduction & Episode Roadmap

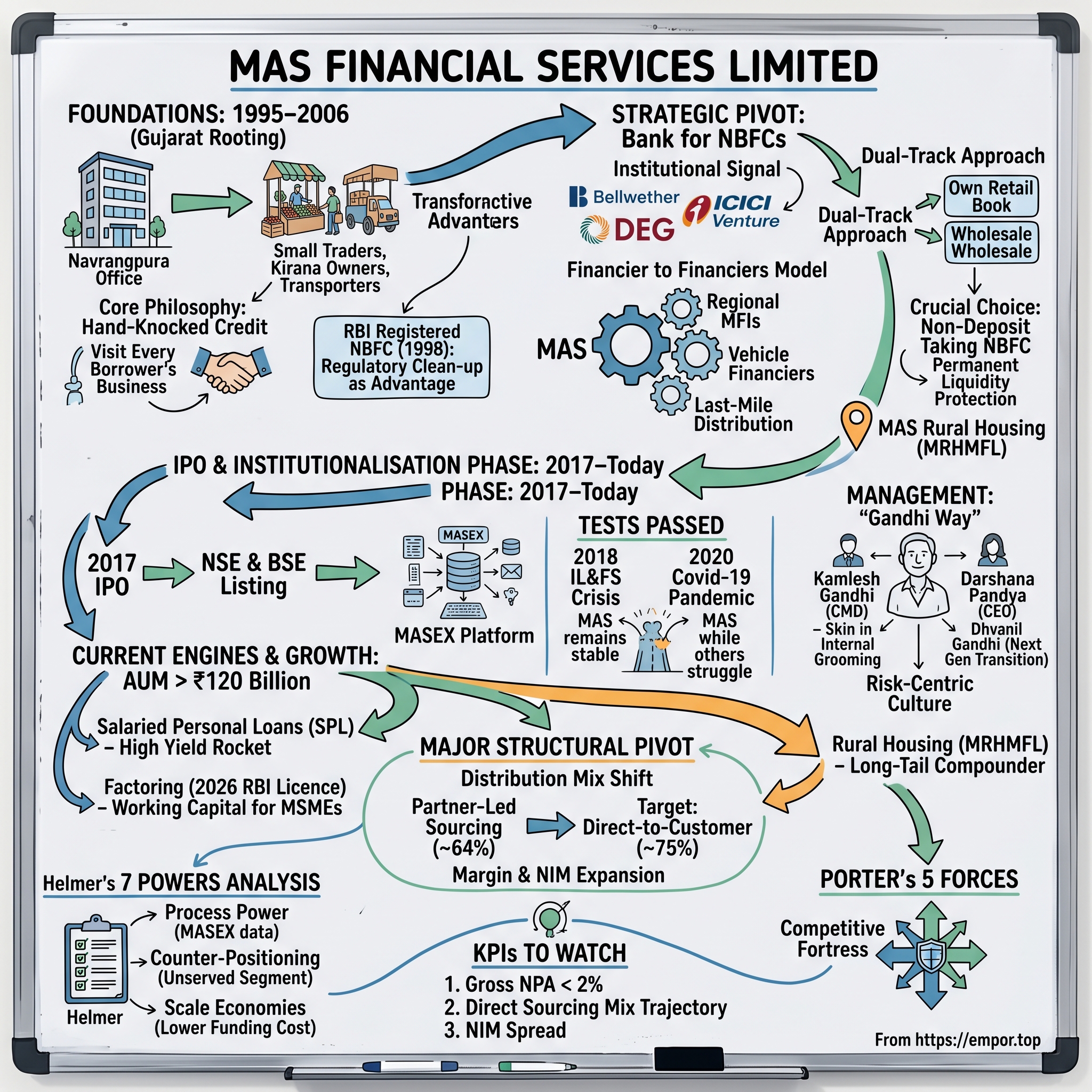

There is a quiet street in the Navrangpura neighbourhood of અમદાવાદ Ahmedabad where, on most weekday mornings, a procession of two-wheelers and dust-caked Maruti sedans arrive at an unremarkable six-storey office building. The men and women who step inside are not investment bankers from मुंबई Mumbai or fintech evangelists from Bengaluru. They are shopkeepers, vegetable wholesalers, kirana owners, transporters, the proprietors of two-bay tyre-puncture garages. Some of them have ledgers under their arms wrapped in red cloth. Many have never set foot inside a commercial bank's branch in their lives.

This is the head office of માસ ફાઇનાન્સિયલ સર્વિસીસ લિમિટેડ MAS Financial Services Limited — a thirty-year-old गैर-बैंकिंग वित्तीय कंपनी Non-Banking Financial Company (NBFC) that has, with very little fanfare, built one of the most disciplined small-ticket lending franchises in the country.[^1] If you have heard of HDFC Bank, Bajaj Finance, or Shriram Finance, you have heard of the giants of Indian retail credit. MAS is not a giant. It is, depending on how you count, somewhere between a mid-cap and a small-cap, with an Assets Under Management book that crossed roughly ₹120 billion in early 2026.1 But what MAS has done — and what makes it irresistible as a case study — is hold a Gross Non-Performing Asset ratio below two percent for more than two consecutive decades, across a demonetisation shock, a sector-wide NBFC liquidity crisis, and a pandemic that gutted the customers it serves.[^3]

Today's episode is, in a sense, a study in restraint. It is the story of a Gujarati family-run NBFC that watched the entire Indian credit industry chase scale, glamour, fintech valuations, and unsecured-loan IRRs — and instead built a business by lending to the people the big banks would not look at, then lending to the smaller NBFCs the big banks were too frightened to touch. Three themes will recur. The first is the so-called "Financier to Financiers" model — MAS as the wholesale credit pipe for the very bottom of India's pyramid. The second is the discipline of credit underwriting at scale, including a proprietary platform the company calls MASEX. And the third is the very Indian, very Ahmedabadi question of how a family promoter, with around two-thirds of the equity in hand, professionalises a business while keeping its DNA intact.[^4]

If Bajaj Finance is the Ferrari of Indian retail credit, MAS is closer to a Toyota Hilux — unglamorous, durable, and the thing the locals know will actually start when it rains. With that, let us go back to where it began.

II. The Gujarat Foundations: 1995–2006

Picture Ahmedabad in 1995. India had been "liberalised" for four years, but for the average small trader, that word still meant very little. The state-owned banks were polite enough but distant. A two-wheeler loan required a salary slip, a guarantor with property, and a manager in the mood to say yes. For a young dairy-equipment retailer in Naroda or a saree wholesaler in Dhalgarwad who needed ₹40,000 to buy stock for दिवाली Diwali, the options were ugly: a moneylender at thirty-six percent annual interest, a चिट फंड chit fund of dubious legality, or a hand extended to a cousin.

Into this gap stepped two cousins-by-marriage from middle-class Gujarati trading families. કમલેશ ગાંધી Kamlesh Gandhi and his partner Mukesh Gandhi were both chartered accountants by training, and both had spent enough time inside the existing financial-services ecosystem to know two things. First, there was an enormous appetite for credit among the small self-employed. Second, almost nobody was willing to do the granular underwriting work required to lend to them safely. So in May 1995 they incorporated MAS Financial Services with a small equity cheque and a profoundly unfashionable plan: lend two-wheeler loans, micro-enterprise loans, and a handful of used-commercial-vehicle loans, ticket sizes from ₹15,000 to ₹2,00,000, and visit every single borrower's place of business before disbursal.2

The early years were not a story of momentum. They were a story of door-knocking. In one anecdote that Kamlesh Gandhi has retold across investor calls over the years, the founding team would spend their mornings tracing the supply chains of small Ahmedabad markets — who supplied wheat to whom, which transporter ran which route to સુરત Surat, which kirana owner was actually solvent versus merely well-dressed. This was relationship lending in its rawest form: the credit decision was made by people who personally knew the customer's customer.

The first inflection point was regulatory. In 1998 the Reserve Bank of India formally registered MAS as a public deposit-taking NBFC under the new framework that had emerged after the post-CRB-Capital-Markets scare of the mid-1990s.2 If you remember nothing else about the NBFC sector pre-2000, remember this: the entire industry had just been through a near-death experience. Hundreds of deposit-taking NBFCs had collapsed; retail depositors had lost money; the RBI had responded with capital adequacy requirements, prudential norms, and the beginnings of what would become a strict supervisory regime. Most ambitious entrepreneurs in 1998 wanted nothing to do with this corner of finance. The Gandhis ran towards it.

Why? Because the founders understood something subtle. The regulatory cleanup did not destroy demand — it destroyed supply. The moneylender's market did not vanish; it simply lost its formal-sector competitor. Whoever could survive the new RBI rules would inherit a market with structurally less competition. That insight — that the painful, paperwork-heavy, slow-growth path through formal regulation was an advantage, not a tax — became the founding piece of the MAS DNA.

By the early 2000s MAS had quietly built a book of a few hundred crores, mostly in two-wheeler and micro-enterprise loans, almost entirely in Gujarat. The team was small. The funding was a mix of bank lines, retail public deposits, and reinvested profits. It was, by any reasonable definition, a regional finance company with no obvious right to become anything larger. The pivot that turned it into something different came next.

III. The Strategic Pivot: The "Bank for NBFCs"

If you want to understand the moment MAS Financial Services stopped being a Gujarat regional lender and started becoming a national wholesale credit machine, you have to understand a small piece of philanthropic capital called Bellwether Microfinance Trust. In 2006, Bellwether — an early Indian microfinance-focused vehicle backed by भारतीय लघु उद्योग विकास बैंक SIDBI — wrote a cheque into MAS that, in retrospect, was less about the money and more about a signal.3 Here was an institutional, mission-driven investor saying, on the record, that a small Ahmedabad NBFC with a clean book and a self-employed customer base was an interesting platform.

That signal changed two things. The first was the cost of funds. Suddenly larger commercial banks, who could now point to a credible institutional shareholder, began offering MAS term loans at meaningfully tighter spreads. The second was strategic permission. The Gandhis no longer had to act like a captive Gujarat operation. They could think bigger. And bigger, in their case, did not mean opening branches across India. It meant a counter-intuitive insight that would define the company for the next twenty years.

Here is the insight in one sentence: most of India was being served by NBFCs even smaller and more local than MAS, and those smaller NBFCs themselves needed credit. A microfinance institution in ओडिशा Odisha that wanted to lend to women's self-help groups had to borrow the rupees from somewhere. A two-wheeler financier in केरल Kerala that knew its district intimately could not get sensible terms from a दिल्ली Delhi bank head office. MAS, sitting in Ahmedabad with its own clean book of underwriting data, could lend to those smaller NBFCs as a wholesale lender and let them do the last-mile distribution. The Gandhis called it the "Financier to Financiers" model.[^8]

This is the conceptual heart of MAS. To use a non-finance analogy: most fashion retailers either own factories or sell at retail. MAS chose to be the textile mill that sells fabric to the smaller boutiques — a layer up the value chain, where capital is the product. But MAS did not abandon its own retail loan book. It ran both in parallel. Retail loans gave it ground-level data on actual borrower behaviour. Wholesale lending to smaller NBFCs gave it geographic reach without the cost of branches. Each side informed the other.

Around the same time, the company made an unglamorous but structurally critical regulatory choice. It moved from being a public-deposit-taking NBFC to a गैर-जमा स्वीकार करने वाली non-public-deposit-taking Category B NBFC.2 In plain English: it gave up the right to take money from the public, and committed to funding itself entirely from banks, financial institutions, and shareholders. For most NBFCs, this would have been a constraint. For MAS, it was a feature. Public deposits are sticky in good times and a death trap in bad times, because once a rumour spreads in a town like राजकोट Rajkot or वडोदरા Vadodara, the deposits run faster than the lending book can shrink. By stepping off that platform early, MAS bought itself permanent protection from a particular type of liquidity crisis — the same type that would later destroy several of its eventual competitors.

The second half of the 2000s and the early 2010s brought the institutional capital that turned the model into a machine. In 2008 the German development-finance institution DEG took a stake, bringing the dollar-cost balance-sheet hygiene of a European DFI into the boardroom. In 2012 ICICI Venture followed, adding domestic credibility and PE-grade governance.[^4] The Gandhis used these inflows not to grow recklessly but to benchmark themselves against the giants of Indian non-bank lending — चोलामंडलम Cholamandalam Investment and Finance Company and महिंद्रा फાइनेंस Mahindra & Mahindra Financial Services in particular — on the only metric that mattered to them: cost of funds versus credit cost.[^9]

The other initiative of this period, easy to overlook because it is buried inside today's group structure, was the launch of માસ રૂરલ હાઉસિંગ MAS Rural Housing & Mortgage Finance Limited (MRHMFL) — a housing-finance subsidiary aimed squarely at the semi-urban and rural informal worker. While the rest of Indian housing finance was busy building mortgages for IT engineers in गुड़गांव Gurugram, MRHMFL went after the carpenter, the auto-rickshaw owner, the small dairy farmer whose income was real but undocumented. It would not be visible to the broader equity market for another decade, but it was being seeded here.

By the mid-2010s, the company had stopped being a curiosity. It had become a credible, regulated, institutionally-backed wholesale-and-retail hybrid NBFC. What it needed next was permanent capital. That meant the public markets.

IV. IPO & The Institutionalisation Phase: 2017–Today

October 2017 was, for the Indian primary market, a euphoric month. The Sensex had crossed thirty-three thousand for the first time, and a parade of mid-cap financials and consumer companies were lining up to list. Into that crowded calendar came an IPO that drew almost no consumer interest but enormous institutional curiosity — a mid-sized Ahmedabad NBFC offering shares in a price band that valued the company at a few thousand crore. The MAS Financial Services initial public offering opened in early October and listed on both the National Stock Exchange and the Bombay Stock Exchange.4 The issue was oversubscribed many times over on the institutional side. Quiet money — long-only mutual funds, insurance treasuries, a handful of foreign portfolio investors — recognised what the retail crowd had missed: this was a clean compounder being put up at a sensible price.

What changed after the listing was the speed of institutionalisation. A privately held NBFC can run on the founder's instincts and a few trusted lieutenants. A listed NBFC must produce quarterly numbers, manage analyst expectations, and operate at a level of process maturity that survives a transition out of founder-era. The Gandhis took this seriously. The signature initiative of the post-IPO years was an internal tech platform the company calls MASEX — a proprietary loan-origination, credit-decisioning, and monitoring system that captures, at the borrower level, the granular data that traditional NBFCs leave on paper or in branch managers' heads.[^1] If you imagine a Bajaj Finance-style consumer credit engine but specialised for the self-employed and the small NBFC counterparty, you are not far off.

By the time the company had crossed ₹30 billion in AUM in the late 2010s, MAS was visibly different from its peers in three ways. It had a lower cost-to-income ratio than most regional NBFCs because of MASEX-driven productivity. It had a higher proportion of partner-led sourcing — meaning a meaningful share of its retail disbursements came through arrangements with smaller NBFCs and originator partners. And it had a return on assets that consistently sat in the high single digits, with a return on equity in the mid-to-high teens. This is the boring beauty: not the highest growth in the sector, not the flashiest brand, but the most consistent unit economics, year after year.

Then came the test. In September 2018, IL&FS — Infrastructure Leasing & Financial Services, one of the country's largest shadow-banking giants — defaulted on commercial-paper obligations. The shock blew a hole in the short-term funding market for every Indian NBFC. Mutual funds stopped rolling over commercial paper. Banks tightened sanctioned limits. Several large, well-known NBFCs found themselves staring at an asset-liability mismatch they could not close. Stock prices halved across the sector. For a moment, the entire NBFC business model in India looked like it might be permanently impaired.[^11]

MAS sailed through. The reason was the structural choice the Gandhis had made years earlier, when they refused to fund themselves with public deposits or rely heavily on short-tenor commercial paper. The company's Asset-Liability Management book — the matching of how long the loans last against how long the funding lasts — sat in surplus, not deficit. While peers were scrambling for liquidity, MAS was disbursing loans. To borrow a phrase from Charlie Munger, the company had spent a decade being prepared for a crisis it could not specifically predict. When it came, the preparation paid.

The Covid-19 pandemic of 2020 was, in some ways, an even harsher test. MAS's customer is, almost by definition, the bottom of the pyramid — the self-employed informal worker whose income evaporates during a national lockdown. Many bears predicted that the company's gross NPA, which had spent two decades below two percent, would finally crack. It did not. The book held. Restructured assets stayed manageable. Collection efficiency, after the initial lockdown shock, returned to pre-pandemic levels within several quarters. Management later attributed this to two factors: the granularity of the book (no single borrower of meaningful size), and the relationship intensity with originator partners who functioned as on-the-ground collection agents.1

By 2026 MAS sat at an AUM north of ₹120 billion, with a Gross NPA still inside the historical band, a credit rating of CARE A+ with a positive outlook, and a fresh strategic initiative the rest of this episode will dwell on.[^12] But to understand how the company got here, we need to spend time with the people who built it.

V. Management: The "Gandhi Way" and the Next Generation

Inside the MAS office in Ahmedabad there is a corner office that does not look like the corner office of a chairman of a publicly listed financial-services company with a book of several hundred million dollars. It is functional. The desk is not large. The chairs are not leather. The chairman, Kamlesh Gandhi, has a habit, by multiple accounts of analysts who have visited over the years, of walking into mid-level credit-committee meetings unannounced, pulling up a chair, and asking very specific questions about individual delinquent accounts. This is not theatre. This is the texture of how he has run the business for thirty years.

Kamlesh Gandhi is the Chairman and Managing Director, and together with the founding promoter group, the family holds approximately sixty-six-and-a-half percent of the company's equity.5 That is an enormous concentration by the standards of professionally managed Indian listed companies, where promoter holdings of forty to fifty percent are more typical, and global precedent says you should be nervous about this. In MAS's case, the data argues the other way. Skin in the game has functioned as a discipline, not a temptation. The Gandhis have not engaged in the kind of related-party adventurism that has plagued other promoter-led Indian NBFCs. Acquisitions have been few. Subsidiary structures have stayed clean. The dividend policy has been moderate. Capital has been raised primarily to fund the lending book, not adventurous diversifications.

The second person to know is Darshana Pandya, the Chief Executive Officer. Pandya's story is, in itself, the cleanest single piece of evidence about how the company is run. She joined MAS in the 1990s — not as a senior hire, but as a junior trainee in the credit function — and built her career inside the firm over more than two decades.[^14] She knows where the bodies are buried in the loan book because she has, at one point in her career, personally underwritten the kind of loans she now oversees in aggregate. In an industry where most large NBFCs eventually parachute in an external CEO from a private-sector bank, MAS deliberately did not. The grooming of an internal candidate signalled something cultural: the company values continuity of judgement over the appearance of a marquee hire.

The third person — and the one who will matter most over the next decade — is Dhvanil Gandhi, the next-generation entrant. The transition that the Gandhi family has begun to architect is what an Indian financial-services consultancy might politely call a "professionalised promoter-led" structure. The promoter family retains strategic and cultural stewardship; day-to-day operating leadership sits with a professional CEO; the next-gen heir enters at a meaningful but not dominant role, with the explicit understanding that promotion to senior leadership has to be earned, not inherited. It is more सूरत हीरा बाजार Surat-diamond-merchant than Silicon Valley unicorn, but for a credit business that depends on multi-decadal continuity of judgement, this is a feature.

What you do not see on the org chart is just as interesting as what you do. There is no Chief Strategy Officer. There is no Chief Innovation Officer. There is no aggressive M&A team. There is, however, an unusually large credit-and-risk function relative to peer NBFCs. The company's senior bonus pool is structured around return on assets and asset quality, not headline AUM growth.[^14] If a managing director of branches grew his book thirty percent in a year but the credit cost on that book ran above plan, his variable pay would shrink, not expand. That sounds obvious. In the Indian NBFC industry of the last decade, it has been spectacularly uncommon.

A final note on culture. The MAS office in Ahmedabad uses Gujarati as freely as it uses English. Internal meetings switch between the two languages. Customer interactions in tier-3 and tier-4 towns happen in the regional vernacular. This is not romantic — it is operational. Credit underwriting at the bottom of the pyramid is an exercise in reading body language, hearing nuance, and catching the tonal shift when a borrower says, in Gujarati or Marathi or Hindi, "yes I will pay" in a way that means "I am not sure I can pay." Indian credit, at this segment, is a language business. MAS has organised itself around that fact.

With management understood, the question becomes: what is actually inside the AUM today? Because the headline number obscures a much more interesting mix.

VI. Hidden Engines: SPL, Factoring, and Housing

If you opened the most recent investor presentation in 2024 and 2025 and looked only at the AUM headline, you would see steady high-teens growth — perfectly respectable, perfectly unexciting. If you opened the segment breakdown, however, you would see something more interesting: the mix is shifting fast, and the highest-yielding pieces are growing at rates that, in any other context, would attract a fintech valuation.[^15]

The first hidden engine is Salaried Personal Loans, or SPL. For most of MAS's history, the company's borrower has been the self-employed micro-entrepreneur. Yields on that book are healthy but the underwriting is heavy. SPL flips the model. The customer is a salaried worker — often at a small or mid-tier company, sometimes a contractual or gig employee — borrowing a small unsecured personal loan against verifiable monthly salary inflow. The product is higher-yield than the self-employed book, the underwriting is more data-driven and digital, and the segment was growing at year-over-year rates in the high seventies in the most recent reported periods.[^15] To be clear: that is growth from a small base. But it is the kind of growth that, sustained for three to five years, can move from "interesting line item" to "structurally important contributor to net interest margin." Management is treating it as the latter.

The second is the factoring business. In early 2026 MAS received approval from the Reserve Bank of India to operate as a registered factoring company.[^16] To translate the jargon: factoring is the business of buying a small or medium-sized enterprise's unpaid invoices at a discount, immediately giving the seller cash, and then collecting the full amount from the buyer when it falls due. It is one of the oldest forms of finance in the world — Italian merchants did it in the thirteenth century — and it solves a very specific Indian problem. A small auto-component supplier in पुणे Pune who has sold ₹50 lakh of goods to a large OEM, on ninety-day credit, is, on paper, solvent. In practice, he is starving for working capital while he waits for the OEM to pay. Factoring turns his receivable into cash on day three instead of day ninety-three. MAS's existing relationships with small businesses, and its underwriting infrastructure for them, make this a natural extension. The factoring licence is, in effect, the company saying "we already know who these MSME customers are, we already know who is paying them, and now we can finance the invoice cleanly under an RBI-regulated wrapper."

The third is the existing core book, which itself contains several segments worth distinguishing. Micro-Enterprise Loans (MEL) remains the heritage product — the stable, granular, slow-growing core that anchors yield and asset quality. Commercial Vehicle financing is a higher-velocity segment growing in the low thirties percent on a year-over-year basis, riding both the post-pandemic recovery in goods movement and a structural premiumisation of small fleet operators.[^15] The two-wheeler book, which was once the company's signature product, has matured into a smaller share of the mix but still plays a role in customer acquisition.

And then there is housing — MRHMFL, the subsidiary that has been quietly compounding inside the group for over a decade. The housing book targets the same informal-worker borrower that the parent has always served, but with a secured-mortgage product against the borrower's primary dwelling. Yields are lower than micro-enterprise loans but tenures are longer and credit losses are structurally lower because the borrower is, quite literally, lending against the roof over his head. MAS has been progressively investing in this subsidiary — including a ₹24.99 crore rights issue subscription in recent years — and management has guided towards thirty-plus percent growth in this vertical.[^4] If MEL is the heritage product and SPL is the high-yield rocket, MRHMFL is the long-tail compounder.

The single most important strategic shift across all of these segments, however, is the move in distribution mix. Historically, a significant share of MAS's retail sourcing came through originator partners — smaller NBFCs and aggregators who brought customers and earned a share of the spread. As of the most recent disclosures, partner-led sourcing was around sixty-four percent of disbursals; management has set a target of moving direct-to-customer sourcing to roughly seventy-five percent over the medium term.6 This is not a minor tactical adjustment. It is a structural margin pivot. Every basis point of distribution cost that MAS removes from a partner and keeps in-house is a basis point of net interest margin on a multi-billion-rupee book. Compounded over five years, this is the difference between a 2.5 percent return on assets and something materially higher.

The risk, of course, is that direct sourcing requires real-world feet on the street. You cannot grow a direct-distribution book by buying Google leads; the customer is, by definition, not on Google. So the company has been hiring sales officers, opening lean satellite branches in tier-3 and tier-4 towns, and investing in MASEX to support a more digital application flow. The bet is that the per-loan acquisition cost of direct sourcing, at scale, will be lower than the partner commission it replaces — and that the credit cost on directly underwritten loans will be no worse, and possibly better, than partner-sourced ones. This is the central operating wager of the next three years.

Which brings us to the bigger structural question: why has MAS been able to do all of this without being out-competed by a thousand fintechs and a dozen private banks?

VII. Playbook: The 7 Powers and 5 Forces Analysis

If you handed an analyst Hamilton Helmer's framework of the Seven Powers and asked her to apply it to MAS Financial Services, three of the seven would light up immediately. The first is Process Power. MAS has been underwriting loans to the self-employed informal economy of western and central India for thirty years, capturing structured data on borrower behaviour, business cycle volatility, and repayment patterns across multiple credit cycles. That dataset is not on a public credit bureau, because much of it predates the modern bureau era. It is not in a fintech competitor's hands, because no fintech was lending to this customer in 1998. It sits inside MASEX, inside the company's risk models, and inside the institutional memory of the credit team. A new entrant cannot replicate it by raising a $200 million Series C. It is a literal black box that competitors cannot reverse-engineer, and Process Power, in Helmer's framing, is precisely this: a know-how advantage that builds slowly, persists, and is held by an organisation rather than an individual.

The second is Counter-Positioning. Look at what MAS did between 2006 and 2018. It built a wholesale-credit business lending to the very NBFCs that India's largest private and public banks would not touch directly. The banks would not lend a few crore to a small Andhra Pradesh microfinance institution because the deal size was uneconomic for them and the risk model was illegible. MAS could, because its entire underwriting infrastructure was already designed for that level of granularity. The banks ceded the segment. By the time direct lending to those underlying borrowers became attractive — that is, once the market had been "warmed up" by years of credit history and bureau formalisation — MAS could pivot to direct lending without abandoning the wholesale piece. A bank trying to enter the same segment today would have to build a parallel infrastructure that would cannibalise its existing corporate-and-retail model. That is counter-positioning in its textbook form: the incumbent cannot copy you without hurting itself.

The third is Scale Economies, and this one becomes more important the larger MAS gets. As of early 2026 the company's AUM was approaching ₹120 billion.1 At that scale, the marginal cost of an additional rupee borrowed from a bank consortium is materially lower than what a ₹2,000 crore regional NBFC pays for the same wholesale funding. That funding-cost advantage flows directly through to net interest margin, and from there to return on assets, and from there to internal capital generation. The smaller competitor cannot match the loan pricing without surrendering profitability. The larger competitor — say a Bajaj Finance — does not bother with the segment because the unit economics, while attractive in percentage terms, are uninteresting in absolute terms relative to its core book.

What about the other four powers — Switching Costs, Network Economies, Cornered Resource, and Branding? Switching costs are modest at the borrower level (a self-employed borrower can refinance) but meaningful at the partner-NBFC level (a smaller NBFC that relies on MAS for term loans cannot easily replace that funding line). Network economies are not really present here; this is not a marketplace. Cornered Resource is partial — the institutional memory of the senior team is a kind of cornered resource, but it is fragile to succession. Branding is weak; MAS is not a consumer brand and never will be. So we have three of the seven, which is more than most NBFCs in the country can credibly claim.

Now layer in Michael Porter's Five Forces. Start with the Bargaining Power of Suppliers — and in finance the "supplier" is the lender of funds. MAS has progressively earned its way into a preferred-borrower category with major banks including बैंक ऑफ महाराष्ट्र Bank of Maharashtra, State Bank of India, and a clutch of others, alongside development-finance institutions and bond-market lenders.[^4] The cost of those term loans is competitive because MAS's credit history, asset quality, and disclosure standards make it an unusually easy underwriting decision for a bank's credit committee. Supplier power is moderated.

Bargaining Power of Buyers — the borrowers — is structurally low. A small kirana shop owner in tier-3 India is not negotiating against a sophisticated menu of alternatives. The choice set is MAS, two or three other NBFCs, a bank that may or may not respond, and a moneylender. Price-sensitivity exists but it is bounded by the realistic alternatives.

Threat of New Entrants is the most interesting force. On paper, the Indian NBFC sector saw a flood of fintech entrants in the 2018-to-2022 window — digital lenders, BNPL platforms, embedded-finance models. Most of them targeted the urban salaried consumer, not the self-employed informal worker MAS serves. Of those that did target the bottom of the pyramid, several have either pivoted, scaled back, or are operating at credit costs MAS would consider unacceptable. The barrier to entry, it turns out, is not technology. It is the willingness to do thirty years of patient underwriting work to build the data set.

Rivalry within the industry deserves a specific comparison. The natural peers are श्रीराम फाइनेंस Shriram Finance (commercial vehicle and small business lending heritage), मुथूट Muthoot Finance (gold-loan dominant), Cholamandalam, and Mahindra Finance. MAS does not win on absolute scale against any of them. It wins, consistently, on credit cost as a percentage of average loan assets, and on the stability of that credit cost across cycles.[^9] This is a quieter form of winning. It does not get you on the front page of the Economic Times. It does get you compounding equity per share at rates that, over a decade, look extraordinary.

Threat of Substitutes is real but evolving. The traditional substitute — the unregulated moneylender — has been steadily losing ground for fifteen years. The newer substitute — fintech instant-credit apps — competes only at the surface of the market, where customers can be acquired digitally. The deep segment that MAS serves is, for now, structurally hard to digitise away.

So MAS sits with three of seven Helmer powers, low buyer power, moderated supplier power, high barriers to entry through patient know-how, and a competitive set it can outlast on the metric that matters most to a lender — credit cost. That is a fortress. The question for any investor in 2026 is what could break it.

VIII. Analysis, Bear vs Bull, and KPIs to Watch

The bull case for MAS Financial Services in 2026 is, in one sentence, that India's MSME credit gap is vast, MAS is one of the few institutions structurally positioned to fill it profitably, and the company has earned the right to compound. According to multiple Indian regulator and multilateral studies, the formal credit gap for Indian MSMEs runs into many lakhs of crores — that is, hundreds of billions of dollars of unmet demand that the existing banking system has not been able to serve at acceptable risk-adjusted returns. MAS is not going to close that gap on its own. But its share of the gap, even on extremely modest assumptions, supports several years of high-teens to low-twenties AUM growth at stable credit costs.

Layered on top of that is the margin pivot. The shift from sixty-four percent partner sourcing toward seventy-five percent direct sourcing is, if executed cleanly, a multi-hundred-basis-point opportunity on net interest margin compounded over the medium term.6 The SPL business is a high-yield engine that scales the blended portfolio yield without (so far) breaking asset quality. The new factoring licence opens a regulated wrapper for the company to monetise relationships with MSMEs it already knows. MRHMFL is the long-tail compounder. And the fortress balance sheet — clean ALM, granular book, low single-borrower concentration, no unhedged FX, no public deposits — has been stress-tested through demonetisation, the IL&FS crisis, and Covid. Bulls argue that when the next sectoral shock comes, MAS will once again disburse loans while peers are scrambling for liquidity. That is the optionality argument: a clean balance sheet is most valuable precisely when other balance sheets are dirty.

The bear case has three pillars and they are not trivial. The first is regulatory. The Reserve Bank of India has, over the last several years, progressively tightened its supervisory grip on NBFCs through the Scale Based Regulation framework, in which entities above certain asset thresholds face progressively more bank-like prudential rules around capital, governance, listing, and disclosure.7 For an NBFC at MAS's scale, this is manageable today but not free. A tighter capital regime translates directly into lower achievable return on equity for the same return on assets. A future RBI tightening on unsecured lending — a perpetual possibility in the personal-loan segment — could specifically slow the SPL growth engine that bulls are excited about.

The second pillar is geographic concentration. The company's lending book has historically been concentrated in Gujarat and Maharashtra, with growing but still secondary positions in other Indian states. Concentration of this kind is a credit risk that does not show up in good times. A state-specific economic shock — say, a textile-industry downturn in Surat, or a real-estate cycle in पुणे Pune that ripples into small-business cash flows — could test the book in ways the historical track record does not predict. Management has been deliberately diversifying geographically but the pace is gradual.

The third is the fintech and platform threat, and it is more nuanced than the lazy version of the argument. The naive bear case is that some app will eat MAS's lunch. That is unlikely at the bottom-of-pyramid self-employed segment. The more sophisticated bear case is that an account-aggregator-enabled, ULI-platform-driven, digitally underwritten model, sponsored by a large bank, could over the next five years compress the cost-of-acquisition and cost-of-underwriting in segments adjacent to MAS — and in doing so, force MAS to absorb pricing pressure on the easier slices of its book. The company would then be left with a stickier but more difficult residual portfolio. This is not an existential threat. It is a margin-compression risk.

A myth worth fact-checking. The consensus view of MAS in some retail-investor commentary is that it is essentially a microfinance company that got lucky. That is wrong. The company's exposure to pure-microfinance loans is, by design, limited; the dominant exposures are micro-enterprise loans secured against business cash flows, two-wheeler and commercial-vehicle financing, salaried personal loans, and housing. Microfinance — the joint-liability-group, women's-self-help-group product — is something MAS has historically participated in through its wholesale lending to MFIs, not directly at scale. The distinction matters because the regulatory regime and the credit-cost behaviour of true microfinance is materially different from the small-business and salaried segments that dominate MAS's book. Confusing the two will lead an investor to mis-price both the risk and the opportunity.

Another common claim to test: that MAS has overpaid in its capital deployment into the housing subsidiary. The ₹24.99 crore rights issue subscription in MRHMFL has been cited by some sceptics as inefficient capital allocation given affordable-housing-finance valuations in the listed peer set.[^4] The counter-argument is that MAS is not buying a stake at a listed-market multiple; it is funding organic balance-sheet growth in a wholly-owned platform whose marginal return on equity, at scale, is likely competitive with what the public market is paying for affordable-housing-finance pure-plays. The capital allocation is unusual only if you assume the subsidiary's growth is finite. If you assume it is durable, the math reverses.

So how should an investor actually monitor MAS over the next several years? Three KPIs matter more than the rest. The first is Gross Non-Performing Assets as a percentage of AUM. This is the single number that the entire MAS thesis rests on. The company has held it below two percent for more than two decades. A sustained breach above that threshold — say, two consecutive quarters at 2.5 percent or higher — would not be the end of the world, but it would be the first meaningful signal that the underwriting machine is fraying.

The second is the direct-sourcing mix as a percentage of disbursements. Management has targeted moving from approximately sixty-four percent partner-led to roughly seventy-five percent direct over the medium term.6 This is the operating wager. Watch the trajectory quarter by quarter. If it moves quickly without breaking credit cost, the margin pivot is real. If it stalls below seventy percent, expectations of margin expansion may need to come down.

The third is the spread between cost of funds and yield on advances — the net interest margin, in plain English. As a lender, MAS lives or dies on this number. If it expands as the direct mix grows, the bull thesis is being delivered. If it compresses despite the mix shift, the competitive landscape is meaningfully tougher than the bulls assume.

Three numbers. Reported quarterly. Anyone who tracks these well will be ahead of ninety percent of investors who watch only the headline AUM growth.

IX. Epilogue

Is MAS the "HDFC Bank" of the Indian MSME world? Probably not, and probably it should not aspire to be. HDFC Bank's genius was scale, breadth, and a relentless focus on the formal-economy customer; MAS's genius has been depth, granularity, and a relentless focus on the informal-economy customer that HDFC Bank cannot easily serve. They are not the same business. The more useful analogy is probably this: MAS is to small-ticket Indian credit what Costco is to suburban American retail — unglamorous, low-frills, structurally low-cost, and operated by people who treat capital with respect. Both businesses bore people who want excitement and make a great deal of money for people who want compounding.

The deeper lesson, for founders watching from outside the financial-services industry, is that "boring is beautiful" is not a marketing slogan. In credit, it is the entire game. The best NBFCs in India over the next ten years will not be the ones with the loudest brand, the slickest app, or the most aggressive growth target. They will be the ones whose senior management knows the names of their largest delinquent borrowers, whose credit committees meet weekly without fail, whose Chairman walks into mid-level meetings unannounced, and whose CEO joined as a trainee and stayed thirty years. There are not very many companies in India that fit that description. MAS Financial Services, for now, fits it. The next decade will reveal whether the institutional architecture the Gandhis have built can outlast the founders who built it. On the evidence of the last thirty years, the bet is reasonable. On the evidence of every other family-led Indian financial-services succession in history, the bet is not free. That tension — between the proven discipline of the past and the unknown of the next generation — is the central dramatic question hanging over MAS as it enters its fourth decade.

For now, the office in Navrangpura opens its doors every weekday morning, and the shopkeepers and transporters and small dairy owners walk in with their red-wrapped ledgers, and a credit officer sits across the table from them and asks the same patient questions that have been asked there since 1995. The compounding continues.

References

References

-

MAS Financial Services Q4 Results — Moneycontrol, 2024-05-15 ↩↩↩

-

MAS Financial Services IPO Prospectus (RHP) — SEBI/NSE, 2017 ↩↩↩

-

MAS Financial Services IPO Prospectus (RHP) — SEBI/NSE, 2017 ↩

-

MAS Financial Services IPO Listing Notice — NSE India, 2017 ↩

-

MAS Financial's Shift to Direct Distribution: A Margin Play — Mint/Moneycontrol, 2024-05-15 ↩↩↩

-

RBI Master Direction - Non-Banking Financial Company – Scale Based Regulation (SBR) — RBI.org.in ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube