Markolines Pavement Technologies: The Road Preservation Engine

I. Introduction & Episode Roadmap

Between roughly 2014 and 2024, India built highways at a pace that reshaped the map. National highway length expanded by more than half, expressways multiplied, and the country's Tier-1 developers — Larsen & Toubro, GR Infraprojects, Dilip Buildcon — became household names in the infrastructure trade, celebrated for the sheer tonnage of earth they moved and the kilometres they laid. The headlines belonged to construction. But construction is a one-time event. Maintenance is forever.

Every road, once built, begins to die. Water seeps into cracks, heavy trucks fatigue the pavement, the sun oxidises the bitumen, and the surface that was pristine on opening day degrades on a predictable clock. Somebody has to arrest that decay — patrol it, patch it, and every five to seven years tear up and rebuild the top layers in what the industry calls Major Maintenance & Repairs. That "somebody" operates in a market almost nobody covers, because it lacks the ribbon-cutting drama of a new expressway. It is the silent, recurring, multi-decade half of the infrastructure economy.

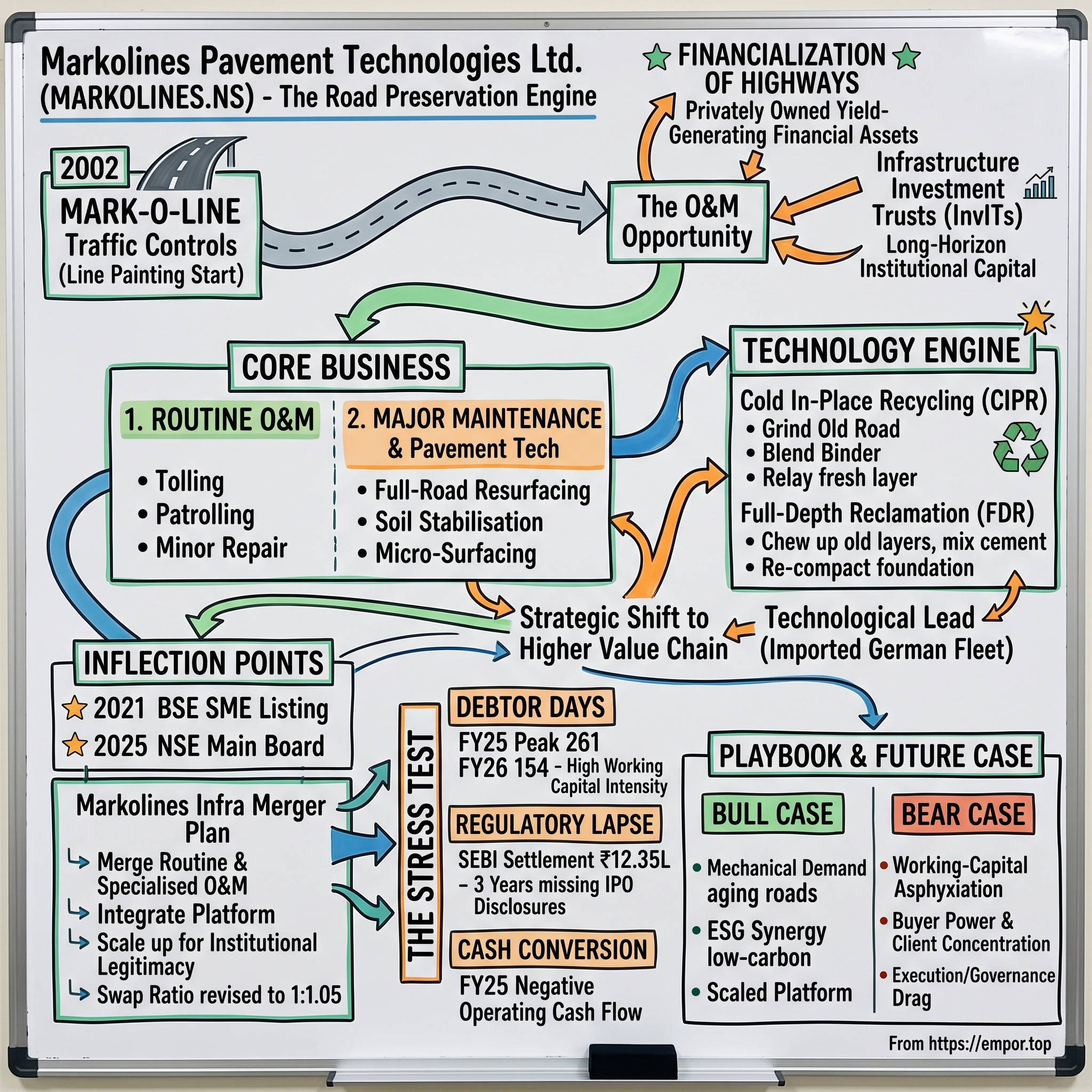

Markolines Pavement Technologies Ltd., which trades on the NSE and BSE under the ticker MARKOLINES, has spent two decades positioning itself in exactly that space.1 It is a small company — a market capitalisation in the few-hundred-crore range and FY26 revenue of ₹348.49 crore on a consolidated basis[^2] — that pitches itself as a technology-led specialist in highway pavement recycling, rehabilitation, and long-term asset operations and maintenance. The pitch is that as India's enormous road build-out ages into its mandatory repair cycles, the demand for what Markolines does is structurally locked in, and that its particular technical toolkit lets it win work that the giants find too small and the local players find too hard.

That is the bull thesis in one sentence. This article exists to test it, not to sell it. Four themes run through the story, and each carries its own tension.

The first is the financialization of highways — the quiet transformation of Indian roads from public engineering works into privately owned, yield-generating financial assets. A road that used to belong to a government agency is now increasingly owned by an infrastructure investment trust backed by global pension and sovereign money. That shift changed who buys maintenance and why, and it is the demand engine underneath everything Markolines does.

The second is the green road revolution — a set of cold-recycling technologies with acronyms like CIPR and FDR that let a contractor reuse essentially all of an old road's material on-site, cutting both carbon and cost. This is Markolines' claimed technical edge. We will unpack how it actually works, and ask how durable an edge it really is.

The third is the governance dilemma. In April 2026 Markolines paid a settlement to India's securities regulator over three years of missing disclosures tied to its own IPO proceeds.2 Its balance sheet carries the receivables burden characteristic of its industry, with debtor days that at one point stretched past 260.3 These are not fatal facts, but they are exactly the facts a skeptical investor should sit with.

The fourth is the consolidation playbook — a 2026 plan to merge an unlisted, promoter-held sister company into the listed entity, a move that could double the platform's scale and reach for main-board respectability, or could hand the promoters a favourable deal at minority shareholders' expense. The share-swap terms have already been revised once. We will read that carefully.

So the roadmap is set. Begin with the market that created the opportunity, then the founders who bet on it, then the machinery that is supposed to defend it, and finally the money — the merger, the receivables, the regulator, and the case for and against. Start where the money now sits: not with the builders, but with the owners.

II. The Indian Highway Gold Rush: From Bidding to Maintaining

To understand why a company like Markolines can exist, rewind three decades and watch how India decided to pay for its roads. The evolution of that financing model is the whole plot, because each iteration created a new kind of road owner, and each new owner had a different relationship with the maintenance problem.

In the 1990s and early 2000s, the model was mostly Engineering, Procurement and Construction — EPC — and early Build-Operate-Transfer concessions. Under EPC, the government paid a contractor to build a road and then owned and maintained it. Under BOT, a private developer built the road with its own capital and earned it back by collecting tolls for a fixed concession period, bearing the traffic risk itself. BOT was elegant in theory and brutal in practice: developers who guessed traffic wrong, or who over-leveraged, ended up with stranded assets, and by the mid-2010s the model had largely stalled under the weight of stressed balance sheets.

The government's answer, rolled out in the 2010s, was the Hybrid Annuity Model — HAM — a deliberate de-risking of the private developer. Under HAM the state funds a large share of construction cost directly and pays the balance to the developer as inflation-linked annuities over the concession, while the developer takes no toll risk. HAM did what it was designed to do: it unclogged the pipeline and pulled private capital back into road construction at scale. But notice what all three models share. Every one of them is optimised around the act of building. The developer's core competence is heavy civil engineering — moving earth, pouring concrete, deploying enormous capital and enormous machines against a construction deadline.

There is a fourth model that closes the loop, and it is the one that turned roads into pure financial instruments: the Toll-Operate-Transfer structure and the InvIT. Under Toll-Operate-Transfer, the highway authority auctions the right to collect tolls on a bundle of already-built, already-operating national highways for a long lease in exchange for a large upfront payment, keeping ownership but monetising the future cash flow immediately. The National Highways Authority of India used it to raise capital against roads it had already constructed, and in doing so it created a clean, de-risked, income-producing asset that was tailor-made for one kind of buyer: long-horizon institutional capital that wants yield without construction risk. The InvIT was the wrapper that let that capital in at scale, pooling operating roads into a listed trust that passes toll income through to unit-holders. NHAI launched its own InvIT to do exactly this, and a wave of private sponsors followed. The consequence for our story is precise: a road that was once a public works project became, in the space of a single decade, a security on a fund manager's screen — and securities have to be maintained to standard, or they are marked down.

Here is the post-construction hangover. Once the asphalt dries, the same road that demanded a battalion of earthmovers now demands something entirely different: patient, dispersed, unglamorous upkeep for twenty or thirty years. Patrolling for accidents. Sealing hairline cracks before water gets in. Trimming vegetation. Repainting lines. And, on a slower clock, ripping up and rebuilding worn pavement layers. For a company built to construct, running maintenance is a low-margin distraction from the next big bid — operationally fiddly, geographically scattered, and a poor use of a balance sheet geared for greenfield megaprojects.

Then the ownership of Indian roads changed hands again, and this is the pivot that matters most. Global yield-seekers arrived. Infrastructure funds, sovereign wealth vehicles and development-finance institutions — the kind of capital that manages pensions in Toronto and reserves in Abu Dhabi — began acquiring operating Indian highways through Infrastructure Investment Trusts, the InvIT structure that packages toll-earning roads into a listed, income-distributing security. The most visible of these buyers, Cube Highways, assembled one of the country's largest portfolios of operating road assets, and Markolines names it among its long-standing customers.4 To these owners a highway is not a construction project at all. It is a bond-like cash flow, and their entire job is to protect the yield.

Why did this capital arrive when it did? Because the arithmetic became irresistible. A mature Indian toll road throws off relatively predictable, inflation-linked cash for decades, and in a world where developed-market bond yields spent years near zero, a de-risked asset yielding well above that — in a large, fast-growing economy — was exactly what pension funds, insurers, and sovereign wealth managers were hunting for. The InvIT structure gave them a governed, liquid, tax-efficient way in without having to operate anything themselves. So sovereign and pension money from the Gulf, North America, and beyond flowed into Indian roads, sponsored through vehicles run by the likes of global infrastructure managers, and the ownership of the country's highways quietly internationalised. That detail matters to Markolines specifically, because it means the ultimate paymasters standing behind its clients are foreign institutions operating under formal environmental and governance mandates — a fact that will become central when we get to why a low-carbon paving method is not just an engineering nicety but a commercial door-opener.

That protective mandate is not optional. Under the concession agreements these owners inherit, the road must be kept to defined quality standards — riding surface, pothole response times, safety furniture — or the owner faces penalties that bite directly into toll revenue. A financial owner obsessed with predictable yield cannot afford a stretch of failing pavement, both because it triggers penalties and because it destroys the asset's value. But that same financial owner has no desire whatsoever to buy recycling trains, hire paving crews, and run field operations. They want a corporate-scale, technically credible contractor to hand the whole problem to.

And there is the vacancy. The O&M opportunity is the recurring, contractual need of sophisticated asset owners to outsource both routine upkeep and the periodic heavy resurfacing — the Major Maintenance & Repairs cycle that recurs roughly every five to seven years — to someone who can be trusted not to get them penalised. It is a demand pool created not by construction spending but by the aging of what was already built, and it grows mechanically as the network ages. That is the market Markolines set out to own. The question is who was in the room in 2002 when the bet was placed.

III. Markolines' Genesis: Finding the Riches in the Ditches

The company was born on 8 November 2002, in Pune, under a name that told you exactly how small the ambition was: Mark-O-Line Traffic Controls Private Limited.5 It painted lines on roads. Its first project was road-marking work on the Ahmedabad–Vadodara corridor, and its founding idea was a modest one — bring better extrusion technology to the humdrum business of thermoplastic lane markings and traffic signage.5 There is no monsoon epiphany here, no visionary sketching a revolution on a napkin. There is a mechanical engineer named Sanjay Bhanudas Patil, then in his mid-thirties, who understood that India was about to build a great many roads and that every one of them would need white lines.

Patil is the central human figure in this story, and worth pausing on. A diploma holder in mechanical engineering, he took the director's chair at incorporation and became managing director at the end of 2003, and he has run the company ever since.5 The company's own materials describe him with the generous gloss of three decades in the business; the more sober record in its 2021 prospectus credited him with "20+ years" across trading in industrial goods, construction, and O&M services.5 Both can be true. What matters is that Markolines has been, from the beginning, a founder-operator's company — an engineer's shop, not a financier's — and that texture explains a great deal about both its strengths on the ground and its weaknesses in the back office, which we will come to.

What kind of operator is Patil? The public record is thin on personal colour — he is not a founder who courts the press — but the shape of the company tells you a good deal about how he thinks. This is a man who spent two decades methodically converting a commodity line-painting shop into a technical pavement specialist, one adjacency at a time, and who chose to sink scarce capital into owning a fleet of imported German machines rather than take the asset-light path of subcontracting. That is the profile of an engineer who believes control of the physical means of execution is the thing worth owning — a builder's instinct, not a financier's. It is a coherent philosophy and it has clearly worked on the ground. Its blind spot is equally legible in the record: a company built by someone who cares intensely about machines and pavements, and rather less about the administrative machinery of being a listed entity, which is precisely the gap the regulator would later find. The founder's greatest strength and the company's central governance weakness are, uncomfortably, the same trait viewed from two sides.

Around Patil formed a promoter group rather than a neat founding trio. Vijay Ratanchand Oswal, a chemical engineer from the University of Poona, is the company's chief financial officer and part of the promoter family that holds a large equity block; the company describes him as a co-founder, though the formal record frames him as CFO and promoter-group member.5 Karan Atul Bora, a much younger civil-and-environmental engineer trained at Cardiff University in Wales, was named alongside Patil as an individual promoter and served as an executive director — though he stepped off the executive board at the start of 2025, a reminder that the founding cast has already begun to change.5 The point is less the roster than the DNA: field engineers with skin in the game, controlling a majority of the stock.

The strategic pivot — the moment the company stopped being a line-painter — came from a simple, unsentimental realisation. Painting white lines is a commodity. Anyone with an extrusion machine and a labour crew can do it, margins are thin, and there is no defensible position. So through the 2000s and 2010s the company pushed steadily up the value chain, from markings into toll operations and routine highway upkeep, and then into the technically demanding heart of the business: heavy pavement rehabilitation. By its own account it has executed more than ninety highway O&M projects since inception,5 and by the time it went public its revenue was dominated by major maintenance work rather than the signage it started with.

Consider what that pivot actually demanded of a small, unglamorous line-marking outfit. Moving from signage into toll operations meant learning to run cash-handling plazas around the clock and manage hundreds of low-wage workers across scattered sites. Moving from there into major maintenance meant becoming a civil contractor capable of passing the technical pre-qualification screens that serious clients impose. Each step required new capital, new skills, and a tolerance for the receivables drag that defines infrastructure work — the very drag that would later become the company's defining financial weakness. The founders were, in effect, repeatedly betting the company's modest balance sheet on climbing one more rung, and the fact that they got from white lines to German recycling trains at all is the genuinely impressive part of the origin story, whatever one thinks of the finances that resulted.

The most consequential decision in that climb was technological. As India's roads matured, they would need not just patching but wholesale rebuilding of worn pavement — and the default way to do that, hot-mix asphalt overlay, is expensive, slow, and carbon-heavy, because it means quarrying fresh aggregate, trucking it in, and heating bitumen to searing temperatures. Markolines chose to skip ahead to the cold-recycling technologies that the developed world's road agencies were adopting, importing specialised German machinery to grind up and reuse the existing road in place rather than haul it to a landfill and start over. That is the "riches in the ditches" insight — that the deteriorated road under your wheels is not waste to be removed but raw material to be reprocessed — and it became the company's identity. We will dissect the engineering in its own section, because the durability of Markolines' edge lives or dies there.

The financial coming-of-age arrived in September 2021, when the company — by then renamed Markolines Traffic Controls Limited and soon to become Markolines Pavement Technologies — listed on the BSE's SME platform.6 The IPO priced at ₹78 a share and raised roughly ₹40 crore, with the stated purposes including repaying about ₹3.8 crore of long-term debt and funding working capital.56 The listing itself was not a triumph. The stock opened at ₹62.20, more than twenty percent below the issue price — a cold reception that says something about how the market first regarded a tiny, working-capital-hungry road contractor.6 But the listing did what listings do: it gave the company a currency, a public balance sheet, and the credibility to sit across the table from institutional asset owners as a legitimate corporate counterparty rather than a local subcontractor. That credibility is the thing it would spend the next several years trying to convert into scale — and, as we will see, the thing its own disclosure lapses would later put under scrutiny. First, though, what exactly does the company sell?

IV. The Core Business: Demystifying Major Maintenance & Pavement Tech

Picture two very different working days at Markolines. On the first, a crew in high-visibility vests works a night shift at a toll plaza, managing lane closures, logging an overturned truck, patrolling a fifty-kilometre stretch for debris, and sealing a few cracks before dawn. On the second, a convoy of heavy machines a hundred metres long crawls down a closed carriageway, chewing up the old road surface at the front and laying a rebuilt one at the back in a single continuous pass. Both are Markolines. The gap between them is the key to the business model.

The company runs on two engines. The first is routine operations and maintenance — tolling, route patrolling, incident management, minor crack sealing, landscaping. This work is high-frequency and highly predictable: the contracts run for years, the revenue is stable, and the counterparties are the asset owners who need someone reliable on the ground every single day. But it is also labour-intensive and structurally lower-margin, because much of what it involves — standing at a toll booth, cutting grass on a median — is not technically differentiated. Anyone can be trained to do it.

The second engine is major maintenance and specialised construction — the execute-on-demand contracts for full-road resurfacing, soil stabilisation, and micro-surfacing. This is where the margins live, because this is where the technical barrier lives. Rebuilding a pavement correctly is genuinely hard; get it wrong and the road fails structurally within a year, the owner incurs penalties, and everyone gets sued. It requires specialised, capital-heavy machinery and the engineering judgment to run it. Markolines' pitch is that it sits at the intersection of these two engines, using the sticky, always-on routine contracts to stay embedded with an asset owner, and then winning the lucrative periodic resurfacing work from inside that relationship.

Why does that intersection stay open to a company this size? Because of a structural squeeze that keeps both bigger and smaller players out. The Tier-1 developers — the GR Infraprojects and Dilip Buildcons of the world — have cost structures engineered for billion-rupee greenfield expressways. Mobilising their machinery and overhead for a localised, ₹50-crore resurfacing job is uneconomic; they would lose money bidding at a price a specialist can live on. At the other end, the unorganised local contractors who might love that ₹50-crore job usually cannot get it: they lack the capital to own recycling trains, the balance sheet to carry the receivables, and — crucially — the technical pre-qualification credentials that institutional owners demand before letting anyone touch their asset. Markolines' claim is that it lives in the vacant middle, too specialised for the giants to bother with and too capitalised for the locals to challenge. That is a coherent competitive story. Whether it is a durable one depends on how hard the middle is to enter, which is the question the technology section will press on.

The customer roster reflects the financialization theme from earlier. Markolines' long-standing, repeat clients are institutional asset owners and their operating companies — Cube Highways, Highway Concession One, and a set of infrastructure-fund vehicles including Macquarie's asset-management arm among the group's named counterparties.4 These are exactly the yield-focused owners with the statutory pressure to keep their roads immaculate, and exactly the sort of relationship that, once established, tends to recur across an owner's portfolio of assets. The strength of that roster is quality; the weakness, which we will treat honestly in the bear case, is concentration. At the time of its IPO the company disclosed that its top five customers accounted for roughly 87 percent of sales and its top ten for about 96 percent — an eye-watering dependence on a handful of names.5

It is worth naming the specialised techniques, because they define the technical end of the portfolio and recur throughout the company's marketing. Beyond the two flagship recycling processes, Markolines does micro-surfacing — laying a thin, engineered slurry of polymer-modified emulsion, fine aggregate, and additives over an aging but structurally sound road to renew the wearing surface and seal it against water, a preventive treatment that buys years of extra life at a fraction of the cost of a rebuild. It does soil stabilisation, chemically or mechanically treating weak subgrade soils so they can bear traffic loads, and rigid pavement (concrete) maintenance for the stretches built in cement rather than asphalt. The through-line is that every one of these is a preservation technology — a way to extend or restore an existing asset rather than construct a new one — which is exactly what an owner protecting a yield wants to buy. That framing, "pavement preservation" rather than "road construction," is the identity the company chose when it renamed itself Markolines Pavement Technologies, and it is a deliberate signal to the market about which half of the infrastructure economy it intends to live in.

Lately the company has been reaching for new growth vectors that leverage the same paving-and-civil skill base. It has talked up a move into tunnelling and rigid-pavement (concrete) work, and in April 2026 it won ₹29.38 crore of sports-infrastructure contracts from the Sports Authority of Andhra Pradesh — stadium and indoor-hall construction to be completed inside nine months.7 Then, in July 2026, it announced a strategic entry into marine infrastructure: jetty construction and repair, and fire-protection systems for marine facilities, with no order value attached yet.8 Read these charitably and they are logical extensions of a civil-engineering platform hunting for higher-margin niches. Read them skeptically and they are a small company wandering into a widening set of unrelated end-markets — sports halls, jetties — a pattern experienced investors have learned to watch warily, because diversification and diworsification look identical until the results come in. The company's own identity, though, still rests on one technical claim above all others, and it is time to open the machine and see whether the claim holds.

V. The Technology Engine: Deep Dive into Cold In-Place Recycling (CIPR) & FDR

Stand at the edge of a road being rebuilt the old way, and the first thing you notice is the heat and the trucks. Hot-mix asphalt is exactly what it sounds like: aggregate and bitumen heated to around 150 degrees Celsius in a plant, trucked to site while still hot, and laid before it cools. To rebuild a worn road this way you first mill off and cart away the old surface — waste — then quarry, crush, heat, and haul in an entirely new one. It works, and it has paved the world, but it is energy-hungry, materials-hungry, and slow, and every one of those trucks is a cost and a carbon emission.

Now watch the cold way, and you understand Markolines' whole pitch. In Cold In-Place Recycling — CIPR — a continuous train of machines does the rebuild in a single moving pass without heat and without hauling. The lead machine grinds off the deteriorated top layer of asphalt and pulverises it on the spot. That reclaimed material is immediately blended, right there in the machine, with a binder — foamed bitumen or a chemical emulsion — and relaid and compacted as a fresh structural layer. The old road becomes the new road. Think of it as resurfacing a wooden table by planing and re-pressing the same wood in place, rather than throwing the table away and buying new lumber.

Full-Depth Reclamation — FDR — is the heavier-duty cousin. Instead of just reworking the top layer, FDR pulverises the entire asphalt thickness and blends it down into the underlying base course, stabilising the whole mixture with cement or lime to create a completely new, structurally superior foundation from the material that was already there. Where CIPR renews the surface, FDR rebuilds the bones. Both share the defining trait: the deteriorated road is treated as feedstock, not garbage.

The value proposition to an institutional client stacks up on three axes, and it is worth being precise about each because this is the core of the "why win" case. First, cost: reusing essentially all of the existing road material eliminates most of the quarrying, the fresh aggregate, and the trucking, which the industry associates with material savings on the order of twenty to thirty percent on the relevant scope. For an InvIT running dozens of assets, that compounds into real money. Second, speed: a single-pass cold train can rebuild pavement far faster than the mill-away-and-relay hot-mix sequence, which matters enormously to a toll-road owner because every day a lane is closed is a day of forgone toll revenue and, potentially, contractual penalty. Faster rebuilds protect the owner's yield directly. Third, carbon: because cold processes skip the energy-intensive heating of hot-mix asphalt, they carry a substantially lower emissions footprint — the kind of reduction that matters to the European and North American pension and sovereign funds standing behind Indian InvITs, many of whom operate under hard ESG investment mandates. Markolines' technology, in other words, is not just cheaper and faster; it is reportable in a sustainability disclosure, and that is a genuine commercial hook with this particular customer base.

It helps to make the FDR idea concrete with an everyday analogy. Imagine a gravel driveway that has rutted and weakened over years. The expensive way to fix it is to dig out and cart away the whole thing, buy fresh stone, truck it in, and rebuild — new material, lots of hauling, lots of waste. The FDR way is to run a machine that chews up the old rutted layer together with the soft ground beneath it, mixes in a little cement to bind the blend, and re-compacts the whole thing into a foundation stronger than the original — using almost entirely what was already lying there. Now scale that from a driveway to a national highway carrying thousands of trucks a day, and you have both the appeal and the difficulty: the appeal is that you barely buy or move any material, and the difficulty is that getting the mix design, the binder dosage, and the compaction exactly right on a road that must not fail under load is genuine engineering. Do it well and you have a superior road for far less money and carbon; do it badly and you have a very expensive failure that gets you fired by a penalty-conscious owner. That asymmetry — high skill required, high cost of getting it wrong — is itself part of the barrier that protects a competent operator.

A necessary word of analytical caution: figures like "20–30% cheaper" and "up to 50% lower emissions" are the standard framing of the cold-recycling industry and of the company's own marketing. They are directionally well-established in pavement engineering literature, but the exact saving on any given job depends on haul distances, material condition, and design life, and an investor should treat them as an order-of-magnitude case rather than a guaranteed number on every contract. The mechanism is real; the precise percentages are a sales range.

There is a second-order commercial point buried in the speed argument that deserves surfacing, because it explains why this technology sells itself to precisely the right buyer. A toll road only earns when traffic flows over it, and a lane under repair earns nothing while it is closed — worse, prolonged closures can trip contractual availability penalties written into the concession. So when a cold-recycling train rebuilds a carriageway in a fraction of the time a conventional mill-and-relay would take, it is not merely cheaper to the contractor; it directly protects the owner's revenue by minimising the window during which the asset is offline. The vendor's efficiency and the client's yield are aligned. For a financial owner whose entire investment thesis is "predictable toll cash flow," a maintenance method that shortens the one thing that interrupts that cash flow is worth paying attention to on its own, before a single rupee of material saving is counted. This is why the pitch lands with InvITs specifically, and less so with a government department that does not think in terms of revenue days lost.

Which brings us to the actual moat, if there is one: the fleet. These recycling trains are not off-the-shelf equipment. The specialised cold-recycling machinery is dominated globally by Germany's Wirtgen Group, and buying, importing, and operating a fleet of it requires serious capital and serious operator skill.5 Markolines' strategic choice to own its heavy machinery rather than rent it from subcontractors is what it points to as its barrier to entry — you cannot casually enter this business, the argument goes, because you would first have to sink crores into a fleet of German machines and then learn to run them without wrecking a client's road. There is truth in this. But an honest skeptic notes the limits: machinery that Markolines can buy, a determined competitor with capital can also buy, because it is a purchasable good from a willing global vendor, not a proprietary secret. The barrier is capital intensity and accumulated operating know-how, not exclusivity. That is a real but contestable moat — high enough to keep out the local line-painters, not high enough to keep out a well-funded new entrant who decides the market is worth attacking. Holding that thought, turn to the corporate manoeuvre the company hopes will widen the barrier: the merger.

VI. The Corporate Reorganization: The Markolines Infra Merger

Here the story shifts from asphalt to financial engineering, and the tone sharpens, because this is where the interests of the promoters and the interests of minority shareholders can quietly diverge. In March 2026 the board of Markolines Pavement Technologies approved a plan to absorb Markolines Infra Limited, an unlisted, promoter-held sister company, into the listed entity.9

The two halves fit the two-engine model precisely. Markolines Infra, incorporated in 2005 and promoted by the same Patil–Oswal–Bora group, is the routine side of the house — tolling, route patrolling, incident management, day-to-day O&M — and it is the entity through which many of the marquee institutional client relationships, Cube Highways and Highway Concession One among them, actually run.4 The listed company, MPTL, is the specialised technical side — the recycling, the major maintenance, the pavement rehabilitation. On paper, bolting them together turns two partial businesses into one end-to-end platform.

The mechanism is a share swap, and the detail here is where a careful reader should slow down. When the deal was first announced, the exchange ratio was stated as 1:1.15 — Markolines Infra holders would receive 1.15 MPTL shares for each Infra share. Weeks later the company corrected that number to 1:1.05, attributing the change to a clerical error, and in the same breath clarified that a different merchant banker was providing the fairness opinion than originally named.9 A clerical error on the single most important number in a related-party merger — the ratio that determines how much of the combined company the promoters walk away with — is not a trivial slip. It may be exactly what the company says it is, an administrative correction. It is also precisely the kind of detail an activist would circle in red, because the difference between 1.15 and 1.05 is a direct transfer of value between the promoter-held unlisted entity and the public shareholders of the listed one. That the draft scheme had also been returned once by the exchange for technical issues does not inspire confidence in the process discipline around this transaction.9

Set the governance question aside for a moment and take the strategic rationale on its own terms, because it is genuinely coherent. Combining routine and specialised work lets the merged company bid for comprehensive, long-dated O&M mandates — ten-to-fifteen-year contracts that bundle everyday upkeep with periodic heavy maintenance under a single counterparty. Those are the contracts InvIT owners increasingly prefer, because one integrated vendor is simpler and lower-risk than stitching together a tolling contractor and a separate resurfacing specialist. The merger also promises the ordinary synergies — stripping out duplicate corporate overhead, cleaning up the tangle of related-party transactions between the two entities, and pooling working-capital facilities, which for a company this receivables-heavy is not nothing.

There is also a subtler operational logic that the strategic framing tends to gloss. The two entities were already deeply entangled — sharing promoters, chasing overlapping clients, and transacting with each other — which means the pre-merger structure carried an inherent web of related-party dealings between a listed company and an unlisted one controlled by the same family. That is an arrangement institutional investors instinctively distrust, because it is exactly where value can leak from public shareholders to private ones without ever being visible on the listed company's face. Folding Markolines Infra into MPTL, if done at a genuinely fair ratio, actually cleans up that structure: the related-party transactions between the two collapse into a single set of accounts, and the promoters' incentives are pulled into a single listed vehicle where minority holders can see everything. Read that way, the merger is not just a growth move but a governance simplification — which makes the corrected share ratio doubly important, because the entire benefit of the clean-up depends on the terms of the swap being defensible. A fair-ratio merger tidies the house; an unfair one simply relabels the leakage as a one-time transfer.

And there is a scale prize. Management frames the combined platform as a step-change: the merged entity would carry substantially larger revenue — the group has spoken of combined revenue well above ₹500 crore, with Markolines Infra contributing something on the order of 45 percent of the listed company's revenue base — and marches toward an aspirational ₹1,000-crore revenue target.[^2] Scale of that order is the ticket to institutional legitimacy: bigger revenue and free float attract mutual funds, improve liquidity, and let the company bid for larger individual projects. The company had already been climbing that ladder in the market's plumbing — migrating from the BSE SME platform to the BSE main board in mid-2025, then listing on the NSE main board in October 2025 — and the merger is the logical capstone to that graduation.10

But hold the two skeptic's questions the outline rightly flags, because they are the crux. First: did the promoters consolidate an unlisted asset they control on terms favourable to themselves and adverse to minority holders? The revised ratio, the returned draft scheme, and the inherent conflict of a promoter selling to a company the same promoters run all mean this deserves scrutiny rather than applause; the fairness opinion and the eventual NCLT process are the safeguards, and their quality is what an investor should watch. Second: does absorbing a lower-margin, labour-intensive tolling business dilute the high-margin technology narrative that is the whole reason to find Markolines interesting? Almost certainly it changes the blend — routine O&M simply does not carry the margin of specialised recycling — and the market will have to decide whether it is buying a technology story or an infrastructure-services conglomerate. That tension between the shiny narrative and the cash-generating reality runs straight into the least flattering part of this company's file.

VII. The Skeptical Investor Stress Test: Working Capital, Debtor Days, and SEBI

Every good business story has a chapter the management would rather skip. For Markolines there are two, and they are related: a back office that could not keep up with the obligations of being public, and a balance sheet that struggles to turn accounting profit into actual cash. Take them in turn, because together they define the "why not" case.

Start with the regulatory lapse. When a company raises money in an IPO, the rules require it to tell the market, every six months, whether it actually spent the proceeds the way it promised in the prospectus — the statement of deviation or variation mandated by Regulation 32 of India's listing regulations. It is a basic accountability mechanism: you told investors you would repay debt and fund working capital, now prove it. From its September 2021 listing all the way through September 2024 — three full years — Markolines simply did not file these statements.2 The regulator issued a show-cause notice in May 2025, and rather than fight, the company settled: it belatedly filed the missing disclosures and, in April 2026, paid ₹12.35 lakh to close the matter under SEBI's settlement framework, neither admitting nor denying the findings.211

The settlement route itself is worth understanding, because it colours how to read the episode. Settling "without admitting or denying" guilt is a standard, entirely legal mechanism that lets a company close a regulatory matter quickly and cheaply without a finding of wrongdoing on the record. It is not an admission of fraud, and nothing in the case suggests the IPO money went anywhere improper — the stated uses were the mundane repayment of a few crore of debt and working capital. But settlement is also the path of least resistance, and choosing it means the underlying question — why did a listed company go three years without telling its owners how it spent their money — never gets a fuller airing. For an investor, the takeaway is not the ₹12 lakh, which is trivial, but what the lapse reveals about the maturity of the control environment, and whether the same under-resourced back office is the one now tasked with executing a complex merger and reporting cleanly to a newly institutional shareholder base.

The fine is small; the signal is not. A ₹12 lakh payment is a rounding error for even a micro-cap. But three years of silence on how a company spent its IPO money is a textbook governance flag, and it fits the founder-engineer pattern we identified earlier a little too neatly. This is a company whose leadership is demonstrably competent in the field — running machines, executing pavements, keeping asset owners happy — and demonstrably less disciplined in the compliance functions that a public company is obligated to staff and honour. The lapse is not evidence of fraud; the objects of the IPO were mundane, and the money was modest. It is evidence of a structural back-office deficit, an administrative capability that lagged the company's ambitions. As Markolines scales — into a merger, onto a bigger board, toward institutional investors who conduct real diligence — that deficit is exactly the kind of thing that has to be fixed and monitored, and the burden is on management to show it has been.

Now the harder problem, the one that governance discipline alone will not cure: working capital. This is an industry that pays its bills long before it collects its dues. Markolines buys the fuel, the bitumen, the machine time, and the labour up front to execute a resurfacing job, then invoices an infrastructure owner or a government entity that pays on its own unhurried schedule. The result is a receivables balance that swells relentlessly, and the single number that captures it is debtor days — roughly, how many days of sales are sitting uncollected as trade receivables at any moment.

The figures tell an uncomfortable story. Markolines' debtor days have chronically run high — around 150 at various points — but in FY25 they blew out to roughly 261 days, meaning the company was waiting the better part of a year to collect on work it had already done and booked.3 By March 2026 they had come back toward 154 days, an improvement, but still an enormous chunk of the year's sales locked up in receivables.12 Behind that spike sat the industry's habit of skewed, end-of-quarter billing and the slow-paying nature of infrastructure and government counterparties.

Here is why that matters more than the healthy-looking income statement suggests. On the surface FY26 looks good: consolidated revenue of ₹348.49 crore, net profit of ₹26.23 crore, and an EBITDA margin around fourteen percent.[^2] Those are respectable numbers for a small contractor. But profit is an opinion; cash is a fact. Because so much of each year's revenue converts into receivables and unbilled work rather than money in the bank, Markolines' operating cash flow has repeatedly failed to follow its profits. In FY25 — the year debtor days exploded — the company generated negative cash from operations of roughly ₹33 crore even as it reported a rising profit.12 Read that sentence again: the company earned more accounting profit and simultaneously drained cash from its operations, because the working-capital hole swallowed everything and more. FY26 saw operating cash flow swing back to modestly positive, around ₹11 crore, which is genuine progress, but the multi-year pattern is unmistakable — this is a business whose reported earnings and its cash generation live in different worlds.12

There is a tell in the shareholding register that corroborates the strain. Promoter ownership, which stood above 72 percent in 2023, fell to roughly 55 percent by 2025 and has held there — a decline of some seventeen percentage points in about three years.12 The bulk of that drop came in a single stretch around late 2024, coinciding with the preferential issue of equity and convertible warrants. In plain terms, the company kept raising fresh equity to fund a business that its own operations were not funding, and each raise diluted the founders' stake. A falling promoter holding is not automatically sinister — it can reflect legitimate capital-raising rather than founders cashing out — but the pattern here, repeated equity top-ups by a profitable company, is itself the diagnosis: profits that do not become cash have to be replaced with someone else's cash, and that someone is the equity market.

To bridge that gap while it waits to be paid, Markolines leans on external funding. Total borrowings climbed from about ₹31 crore in FY23 to roughly ₹86 crore by FY26, and the company has repeatedly turned to the equity market to shore up liquidity — a preferential issue and a tranche of convertible warrants at ₹165 a share in 2024, and the earlier rights issue.1213 Its credit is rated in the investment-grade-but-modest territory, at IND BBB- with the rating placed on watch pending the merger's regulatory approvals, and the rating agency has been explicit that the working-capital intensity and stretched receivables are central to its assessment.3 This funding dependence is the mechanism that turns a receivables problem into an existential one: as long as banks extend working-capital limits and equity investors keep topping up, the machine runs; if credit tightens or debtor days lurch out again, the company is forced into more expensive financing, and margins and equity value both suffer. That single vulnerability is the hinge on which the entire investment case swings — which is why it deserves a proper framework, not just a narrative.

VIII. Playbook: Strategic Moats & Hamilton Helmer's 7 Powers

Strip away the story and ask the cold structural question: does Markolines actually have a durable competitive advantage, or just a decent position in a growing market? Hamilton Helmer's 7 Powers framework is a useful scalpel here, because it forces you to distinguish a real, persistent edge from a temporary one. Run Markolines through the powers that plausibly apply and the picture is honestly mixed — some real edges, none of them overwhelming.

The first candidate is a cornered resource, and here Markolines has a moderate claim. Its owned fleet of specialised Wirtgen recycling trains and its accumulated operating expertise — the know-how to run FDR and CIPR without failing a client's pavement — are genuine assets that a local competitor cannot conjure overnight.5 But as we established in the technology section, this is a bought resource, not a cornered one. The machines are available to anyone with capital and a purchase order to Germany. The "corner," such as it is, lies in the combination of capital already sunk and skill already built, which buys a lead but not exclusivity. Call it a head start with a fence around it, not a monopoly.

The second, and strongest, is switching costs, which we can fairly rate high. For an InvIT like Cube Highways, changing the O&M partner in the middle of a concession is genuinely dangerous. A botched major-maintenance job does not just cost money; it can cause structural pavement failure, trigger penalties from the highway authority, and impair the value of the underlying asset. An owner who has watched a contractor execute cleanly across several cycles has every reason not to gamble on an unproven replacement to save a few percent. That reluctance is real switching-cost power, and it is the most defensible thing Markolines owns — an incumbency advantage measured in trust and track record rather than technology. The vulnerability, of course, is the flip side of concentration: switching costs protect you with the clients you have, and do nothing about your dependence on so few of them.

The third is scale economies, and here the rating is emerging rather than established. The whole logic of the Markolines Infra merger is to spread the heavy fixed cost of a machinery fleet across a larger cluster of contracts, so that the company can bid aggressively on localised jobs while still covering its equipment costs. If it works, scale lets Markolines underprice both the giants (whose overhead is too heavy) and the locals (who have no fleet to spread) — a real economy. But it is prospective. The company is not yet large enough for scale to be a decisive weapon, and a merger that also loads on lower-margin routine work may blunt the effect as much as sharpen it. This power is a bet, not a fact.

Now widen the lens to Porter's Five Forces, which captures the industry structure Markolines is trapped inside regardless of its own cleverness. The most punishing force by far is the bargaining power of buyers, which is very high. The pool of institutional highway owners — the InvITs and large developers who control private concessions — is small, sophisticated, and price-disciplined. When a handful of buyers account for the overwhelming majority of a vendor's revenue, as they do here, they hold the whip on pricing and payment terms. This is not a hypothetical: it is the direct cause of the debtor-days problem, because powerful buyers pay slowly and the small vendor absorbs it. Buyer power is the force that most limits how good this business can ever be.

The mirror image of buyer power is supplier power, and it is more benign but not negligible. The critical input on the technology side is the specialised recycling machinery, and that market is concentrated around a small number of global manufacturers led by Wirtgen. A contractor that has standardised on one manufacturer's fleet is, to a degree, captive to that manufacturer for parts, service, and future units — a dependency that runs the other way from the road owners but is real. On the routine side, the main inputs are bitumen, aggregate, fuel, and labour, all of which are competitively supplied but expose the company to input-cost inflation that it cannot always pass straight through to fixed-price contracts. Neither supplier dynamic is threatening on its own; together they are a reminder that a contractor is squeezed from both ends of its value chain.

The threat of new entrants is more comforting, rating low-to-medium. The capital required for a cold-recycling fleet and the technical pre-qualification hurdles that institutional owners impose do keep the low-end contractors out of the major-maintenance market — the very barriers Markolines relies on. But "low-to-medium," not "low," because those barriers stop the small fry, not a serious, well-capitalised entrant who decides the aging-highway maintenance market is large enough to attack. The intensity of rivalry splits cleanly along the two-engine line: in high-end CIPR and FDR the field of credible competitors is thin, so rivalry is muted and margins hold; in routine tolling and upkeep the work is commoditised, competitors are plentiful, and rivalry is fierce. That split is precisely why the merger's blending of high- and low-margin work cuts both ways.

Put it together and the verdict is neither dismissive nor triumphant. Markolines has one strong power (switching costs), one moderate (its fleet and know-how), and one still unproven (scale), operating inside an industry defined by punishing buyer power. That is a defensible niche, not a fortress — an edge worth having, but one that has to be continuously re-earned rather than banked. Whether that is enough to reward an investor is the final question.

IX. The Future Investment Case: Bull vs. Bear

Lay the two cases side by side without a thumb on the scale, because Markolines is genuinely a company where thoughtful investors can disagree.

The bull case — the "why win" — rests first on a structural tailwind that is close to mechanical. The enormous highway network India built over the last decade is now aging into its mandatory five-to-seven-year major-maintenance cycles. That demand does not depend on GDP growth, interest rates, or sentiment; a road built in 2016 needs heavy maintenance around 2022–2024 and again after that whether the economy is booming or not. The work is, in a real sense, locked in by physics and by concession contracts, and Markolines sits in the specialised niche positioned to capture it. Second, the ESG-mandate synergy is a genuine commercial edge with the specific buyers who dominate this market: global funds under decarbonisation pressure are increasingly obliged to favour lower-carbon methods, and cold recycling is a ready answer, giving Markolines a first-mover commercial hook rather than just an engineering preference. Third, the consolidated platform brings scale and visibility — an unexecuted order book north of ₹600 crore providing twelve-to-eighteen months of revenue cover, a bid pipeline the company puts above ₹2,000 crore, and the size to court institutional equity.[^2]14 Management's stated ambition is aggressive: standalone revenue growth of at least thirty percent in FY27 and a march toward roughly triple the current revenue over time, articulated by Sanjay Patil on the back of that pipeline.[^2] If even part of that materialises with disciplined execution, the operating leverage on a fixed machinery base could be meaningful.

The bear case — the "why not" — begins with the vulnerability we have already diagnosed and simply refuses to go away: working-capital asphyxiation. This is not a soft risk; it is the mechanism most likely to actually break the company. A tightening of credit, or a fresh blowout in debtor days back toward or beyond the 261 seen in FY25, would force Markolines into expensive short-term borrowing at exactly the moment its cash is most trapped, eroding margins and, in a bad scenario, threatening solvency. A company that grows revenue while burning operating cash is running up a down escalator; it can do it for a while, but the faster it grows, the more working capital it must fund, and the growth story and the cash story can pull against each other. Second is client concentration in its most acute form — a top-heavy revenue base skewed to a few marquee names.5 If a Cube Highways decided to internalise its O&M, or simply used its buyer power to force down rates at renewal, the impact on Markolines' order book and margins would be severe and largely outside the company's control. Third is the execution-and-governance drag: the SEBI settlement already on the record, the merger ratio that had to be corrected, the draft scheme returned by the exchange, and the sheer integration risk of absorbing a sister company. Any repeat of that administrative friction would damage the promoter credibility that a company graduating toward institutional ownership can least afford to lose.

A word on management credibility belongs here, because with a founder-run micro-cap the quality of the people setting these targets is part of the analysis. The record is genuinely mixed. On one hand, the operating track record is real: the company has grown revenue from roughly ₹73 crore in FY19 to ₹348 crore in FY26, and it has kept winning and executing work for demanding institutional clients across multiple maintenance cycles.[^2]12 On the other, the targets management now sets are ambitious — thirty-percent-plus growth, a tripling of revenue, a ₹1,000-crore aspiration — and they are being made by the same team whose back office missed three years of mandatory disclosures and whose flagship merger required a corrected share-swap ratio. An investor should also read the headline growth with care: even in the strong FY26, the fourth quarter's revenue was actually down year-on-year, with the full-year "growth" carried by the earlier quarters, and the margin recovery in that quarter flattered a softer top line.14 That is not damning, but it is the kind of texture that separates a durable growth story from a lumpy, execution-dependent one. The right posture is to weigh the promises against the delivery over the next several quarters, and to treat the aspirational revenue figures as a direction of travel management is selling, not a base case to underwrite.

The honest synthesis is that the bull and bear cases are not really in tension about the facts — they agree on the facts. They differ on which fact dominates. The bull weights the structural demand and the defensible niche; the bear weights the cash conversion and the concentration. And the reason cash conversion probably deserves the heavier weight is the one Porter force we could not soften: buyer power. As long as a few slow-paying, price-disciplined giants sit across the table, the receivables problem is not a management failing to be fixed so much as a structural feature to be survived. That reframing is the whole point of the closing chapter.

X. Epilogue & Outro

There is an old line among infrastructure investors that belongs on the wall of every contractor's office: scale is vanity, profit is sanity, but cash is reality. Markolines Pavement Technologies is close to a textbook illustration of it. The company has a real technological niche, a defensible incumbency with high-quality clients, and a structural tailwind that few of its peers can claim — the near-certainty that India's vast, aging road network will need exactly what it sells, for decades. And it has, hanging over all of that, a cash-conversion cycle that turns its own success into a financing problem, and a governance record that is competent in the field and shaky in the back office.

Neither half of that picture cancels the other. This is not a company to be dismissed as a mere contractor, nor one to be embraced as a clean compounding machine. It is a small-cap sitting precisely on the fault line between an attractive market position and a challenging financial model, and the next two years — through the merger's completion, the integration, and the test of whether scale actually improves cash generation — will reveal which side of that line it settles on.

It is worth stepping back to appreciate how much of Markolines' fate is not in Markolines' hands. The demand tailwind is a gift of the highway build-out of the 2010s and the ownership shift that followed — the company created neither. The receivables burden is imposed by the buyer power of a concentrated, slow-paying clientele — a structural feature of the industry, not a management error to be coached away. Even the technology edge rests on machines built in Germany and on ESG mandates written in Toronto and Abu Dhabi. What management genuinely controls is narrower but decisive: execution quality that keeps the marquee clients renewing, capital discipline that stops the working-capital hole from swallowing the equity, and the integrity of a merger that could either clean up the corporate structure or entrench a conflict. That is the real scorecard, and it is why the metrics that matter most are the ones that measure conversion and control rather than the ones that measure growth.

What should a genuinely engaged investor watch? Not the revenue headlines, which management will happily supply, but the cash. Does the consolidated platform, once merged, finally begin throwing off positive operating cash flow, or does the routine O&M business consume capital as fast as the specialised business earns it? Can management use its enlarged scale as leverage to compress debtor days from the 150-plus range toward the 90-to-100 days that would signal a genuinely healthier business, or do the slow-paying giants simply keep dictating terms? And does the amalgamation clear its regulatory path through FY27 cleanly, or does the administrative friction that has already surfaced compound into something worse?

If you strip the entire story down to what actually matters for tracking this company from here, three numbers carry the weight. The first is the ratio of cash flow from operations to EBITDA — the single clearest test of whether reported profit is becoming real cash, and the metric that would confirm or demolish the bull case faster than any other. The second is debtor days, the receivables gauge whose every movement telegraphs the working-capital risk that defines the downside. The third is the consolidated EBITDA margin, which will reveal whether the merger's blending of high-margin technology and low-margin routine work strengthens or dilutes the economics that make Markolines interesting in the first place. Watch those three, and the story tells itself — because in the end, on the roads Markolines maintains and on the balance sheet it runs, the surface can look perfectly smooth right up until the moment the foundation gives way.

References

-

Markolines Pavement Technologies Pays ₹12.35 Lakh To Settle SEBI Case over IPO Disclosure Lapses — Moneylife, 2026 ↩↩↩

-

India Ratings and Research — Markolines Pavement Technologies Credit Rating & Liquidity Press Release ↩↩↩

-

Infomerics Ratings — Markolines Infra Limited Rating Rationale, 2025-11-19 ↩↩↩

-

Markolines Traffic Controls Limited — Draft Prospectus, 2021-08-29 ↩↩↩↩↩↩↩↩↩↩↩↩

-

Markolines Traffic Controls IPO — Date, Price, Listing Details, Chittorgarh ↩↩↩

-

Markolines Pavement Technologies Wins ₹29.38 Crore Andhra Pradesh Sports Infra Orders — Whalesbook, 2026 ↩

-

Markolines Pavement Technologies enters marine infrastructure segment — ScanX, 2026 ↩

-

Markolines Pavement Fixes Merger Ratio to 1:1.05 After Clerical Error — Whalesbook, 2026 ↩↩↩

-

Markolines Pavement Technologies Lists on NSE Mainboard, Reports Strong Q1 FY26 Performance — ScanX, 2025 ↩

-

SEBI — Settlement Order in the matter of Markolines Pavement Technologies Limited, 2026-04 ↩

-

Markolines Pavement Technologies Ltd — Financials & Key Insights, Screener.in ↩↩↩↩↩↩

-

Markolines Pavement Technologies Converts Warrants into Equity Shares at ₹165 Each — ScanX, 2026 ↩

-

Markolines Reports Strong Q4 and FY26 Performance — Construction World, 2026 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube