MARICO: The Story of India's Coconut Oil to Consumer Giant

I. Introduction & Episode Roadmap

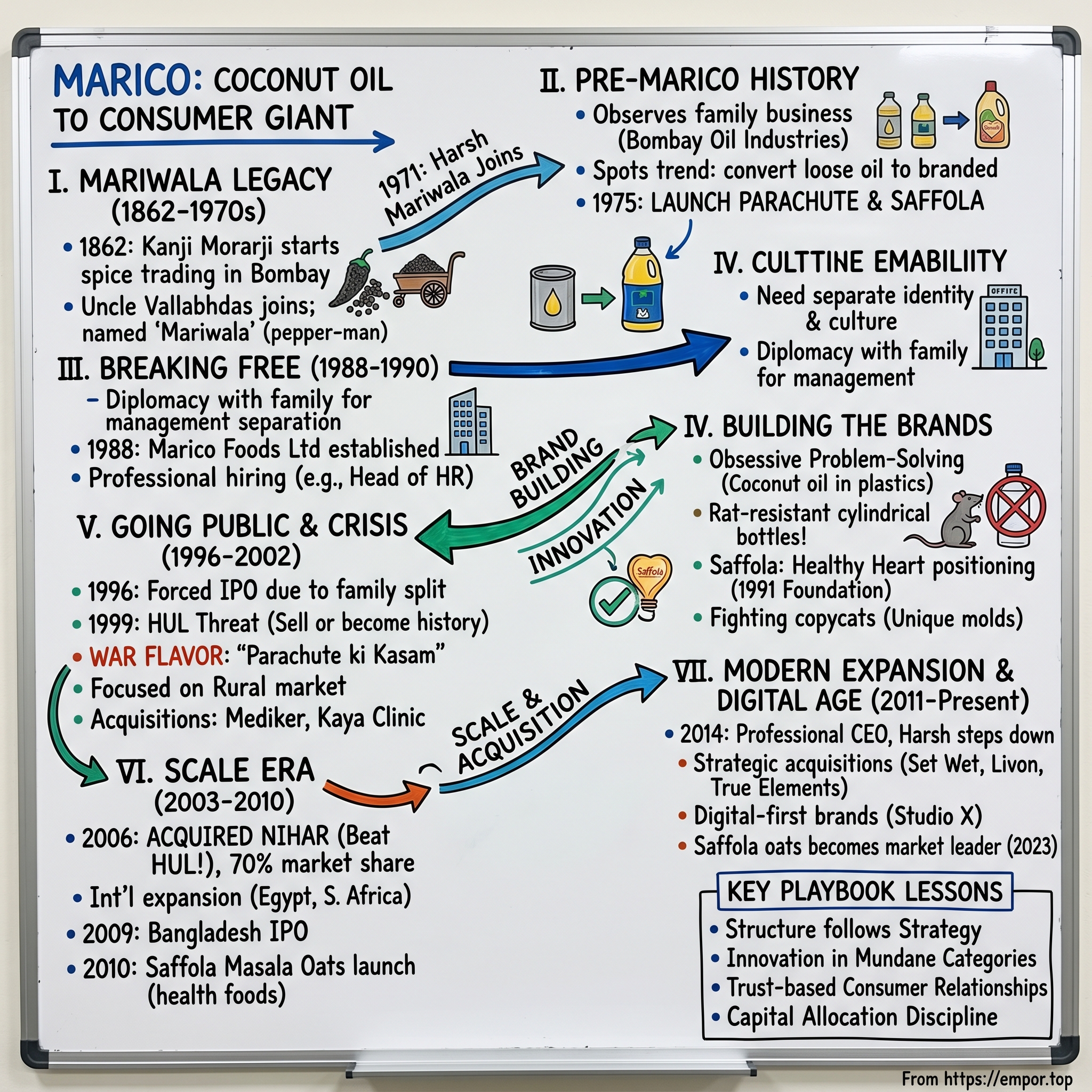

Picture this: It's 1862 in the bustling port city of Bombay. A young trader named Kanji Morarji has just arrived from the arid lands of Kutch in Gujarat, his cart loaded with pepper from the spice gardens of Kerala. Within years, his nephew Vallabhdas Vasanji would join him, and together they'd earn a new name—"Mariwala," literally "pepper-man" in Gujarati. They couldn't have imagined that more than a century later, their descendant would transform this spice-trading legacy into one of India's leading FMCG companies.

Today, Marico Limited stands as a ₹91,360 crore market cap colossus, present in over 25 countries across Asia and Africa. But here's the fascinating question: How does a traditional commodity trader, operating from the crowded lanes of Masjid Bunder in Mumbai, build a consumer empire that touches the lives of one in every three Indians through its flagship brands including Parachute, Saffola, Nihar Naturals, Parachute Advansed, Hair & Care, Livon and Set Wet?

This is not just a story about coconut oil and healthy edibles. It's a masterclass in family business transformation, building brands during India's License Raj era, and the art of defeating multinational giants at their own game. We'll explore how Harsh Mariwala, who joined the family business at just 20 years old, navigated family politics, took on Hindustan Unilever in an epic David-versus-Goliath battle, and built trust with millions of Indian consumers through relentless innovation.

Over the next few hours, we'll unpack the three major transformations that defined Marico: the shift from commodity to consumer brands in the 1970s, the brave spinoff from the family business in 1988-90, and the international expansion that followed. We'll examine the playbook that turned a traditional trading house into a modern FMCG powerhouse—and what it means for investors looking at the company today.

II. The Mariwala Legacy & Pre-MARICO History

Kanchi Morarji, hailing from Kutch in Gujarat, started this business in 1862. Later, he included his nephew Vallabhdas as a partner. The commission agency of Morarji and Vallabhdas first hit Kerala as it was then the paradise of spices. What started as a simple trading operation would evolve into something extraordinary. Together, they navigated the intricate trade routes, exporting prized commodities like pepper and ginger to the far corners of Europe.

The Mariwala name itself tells a story. 'Mari' means pepper in Gujarat. Soon, this word was added to 'Vallabhdas' name by traders as a token of appreciation for his efforts in boosting the spice trade. It wasn't just a nickname—it was a badge of credibility in an era when your word was your bond and your name was your brand.

Fast forward to 1948. India had just gained independence, and Bombay Oil Industries, which traded in spice extracts, edible oils and chemicals, which his father had established in 1948. This wasn't your typical post-independence business story. While others were chasing industrial licenses and government contracts, the Mariwalas were quietly building expertise in a decidedly unglamorous sector: edible oils and chemicals.

Then came 1971—a pivotal year. After graduating from Sydenham College in Mumbai in 1971, Mariwala joined Bombay Oil Industries. Harsh was just 20 years old, the first of the third generation to join the business. But what he found wasn't quite what he expected. As I said, we were in Masjid Bandar, difficult to attract talent, completely family managed. My father being the eldest, three of his brothers, and then I joined, and by the time I started the business, 3 – 4 of my cousins joined the business. So there are 7, 8 same surname, individuals in the organization.

The young Harsh spent his first years observing, learning, traveling. "We had a chemicals business, a spice extracts business, and we also had an edible oil business. During my exploration for one year, I visited all the factories and markets, and I realised that if I can convert the business of loose unbranded edible oils to a branded business, it will be far more sustainable and far more profitable. That is how I began the journey of distribution, network expansion, and brand building."

In 1975, at age 24, Harsh made his first major move. Mariwala took the family company into branded consumer products, a departure from the former business to business model, and launched the Parachute coconut oil and Saffola refined oil brands. This wasn't just a product launch—it was a philosophical shift. While the rest of the family saw commodities and bulk trading, Harsh saw brands and consumer relationships.

The transformation wasn't immediate or easy. Operating in the License Raj era meant navigating a maze of regulations, permits, and government controls. Distribution was a nightmare—there were no modern highways, no cold chains, no organized retail. Yet Harsh persisted, driven by a simple observation: Indian consumers were ready for branded, packaged goods that offered consistency and trust.

So what for investors? The pre-Marico era reveals a crucial pattern: the ability to spot consumer trends years before they become obvious. The shift from B2B commodities to B2C brands in 1975—fifteen years before India's economic liberalization—shows the kind of long-term thinking that characterizes enduring businesses.

III. Breaking Free: The MARICO Formation Story (1988–1990)

By the late 1980s, Harsh Mariwala faced an entrepreneur's nightmare wrapped in a family drama. At Bombay Oil Mills, Mariwala had limited autonomy as management responsibilities were shared amongst the family members. Moreover, he saw the firm as a business to business venture more than the business to consumer venture he envisaged. Imagine trying to build a consumer products company when your cousins control different pieces of the business and every decision requires family consensus.

The negotiation to separate the consumer business from Bombay Oil Industries wasn't a boardroom battle—it was a three-year family diplomacy exercise. "In the early 90s, he convinced his parents that consumer product business needs a separate kind of up culture and identity, and requested them to take the business as a different company." This wasn't about money or ownership—Starting up Marico was not a financial separation from his family business, but a management separation. "It was just a management separation, where the company got divided into three to four different subsidiaries, and each of my cousins took over one part of the business. But in terms of ownership, it is all together, owning the same percentage i.e., 25 percent, which considering the fact that my father had three brothers so totally four brothers. So, I also had a 25 percent shareholding."

The talent challenge was equally daunting. Mariwala initially found it difficult to recruit talented employees given that their office was then located in the crowded market area of Masjid Bunder, hence he held interviews at the Royal Willingdon Sports Club and later moved the Marico office to a more accessible area, Bandra. Picture this: You're trying to hire India's best marketing talent, but your office is in a wholesale market where trucks block the roads and the smell of spices permeates everything. Harsh's solution? Conduct interviews at an upscale sports club, sell the vision, and promise a move to modern offices.

Marico Limited was established on 13 October 1988 under the name of Marico Foods Limited. Later, in 1989 the name of the company was changed from Marico Foods Limited to Marico Industries Limited. The official spinoff in 1990 marked more than just a corporate restructuring—it was a declaration of independence.

Building a professional culture from scratch meant challenging every assumption of the traditional family business. The first hire was telling—a Head of HR from Asian Paints, not a sales manager or operations head. Harsh recruited 40 senior professionals to manage 200 employees inherited from the family business. The message was clear: meritocracy would trump family connections.

So what for investors? The 1988-1990 period demonstrates management's willingness to make hard structural changes for long-term gain. The separation from the family business, while maintaining family shareholding, created the governance structure necessary for institutional growth—a critical factor in Marico's later ability to attract public market investors.

IV. Building the Brands: Parachute & Saffola (1970s–1990s)

The plastic bottle revolution of the 1980s reads like a business school case study in obsessive problem-solving. About 10 years before us, someone else had come in with coconut oil in plastics and they had packed them into square-shaped bottles. They didn't do a good job in terms of packaging so the oil would ooze out. Then the rats would attack the coconut oil in plastics because they love the plastics and coconut oil combination, and the whole retailer shop would get spoilt.

Harsh didn't give up. Harsh, the quintessential problem solver, identified the plastic can's square shape as the vulnerable point and envisioned a solution – round bottles made of superior rodent resistant plastic that would thwart the rodents' attempts. A meticulous team, led by RV Bindumadhavan, then crafted Parachute's iconic cylindrical bottle design, rendering it resistant to rat attacks.

But how do you convince skeptical retailers who've been burned before? To alleviate concerns, a fascinating experiment ensued: rats were confined with the newly designed bottles, and their interactions were recorded. The footage was later used to convince vendors of the bottle's resilience against these intrepid creatures. Also, the container was designed in such a way that rats could not smell the oil. Marico then experimented by putting the container in a cage full of rats and took photographs to demonstrate the solution worked.

The results were staggering. That pioneering moment from tin to plastic gave us a huge increase in market share. Virtually from 0% market share we became market leaders. Within five years, market share jumped from 10-15% to 50%. The iconic blue bottle became synonymous with pure coconut oil across India.

The Saffola story followed a different trajectory. While Parachute targeted the mass market, Saffola positioned itself as the healthy choice for India's emerging middle class. The 1991 launch of the Saffola Healthy Heart Foundation wasn't just marketing—it was a long-term investment in consumer education about heart health, complete with health camps and a nutritionist hotline. By 1995, Saffola had diversified into health foods, anticipating the wellness trend by decades.

Competition was fierce. Shalimar from Kolkata, Postman, Tata's own brands, and looming largest, Hindustan Unilever. Each required different strategies—price competition with local players, quality differentiation against established brands, and innovation to stay ahead of copycats. At one stage, we had 100 copycats of Parachute and were losing about 20% of our sales to them. So, we designed a certain mold with a foreign mold maker at a very high cost, and the copycats were not able to copy it.

So what for investors? The brand-building era reveals Marico's core competitive advantage: the ability to create and defend category leadership through innovation in mundane products. The shift from commodity to brand increased margins, created pricing power, and built the moat that exists today.

V. Going Public & Professional Management (1996–2002)

Harsh Mariwala took Marico public with an initial public offering in 1996. But this wasn't a triumphant IPO story—it was forced by circumstances. I was forced to go public. There was a split in the family in terms of financials. And as I mentioned earlier, my father, three brothers, I bought over two of my uncles and their children. So, two 50% of the business I bought over and Marico was the largest part of the family, total business. So as a part of that deal, I had entered into an agreement and put my shares in escrow. And the final step was valuation of Marico. Now the valuation was Marico was much higher than what I thought it would be.

The IPO transformed more than Marico's capital structure—it forced professional governance. The company that went public in 1996 was radically different from the family firm of the early 1990s. Professional managers ran key functions, independent directors joined the board, and quarterly reporting imposed discipline.

Then came the existential threat. In the late 1990s, Hindustan Unilever, India's FMCG giant, decided it wanted to dominate the hair oil market. In 1999, Harsh Mariwala, the Chairman of Marico received a call from Keki Dadiseth, the then Chairman of HLL (Hindustan Lever, now Hindustan Unilever or HUL). The conversation was chilling in its directness: "Mr. Kaki told him that if he sold Parachute to HUL he will be given enough resources to take care of himself and all of his future generations."

When Harsh refused, Dadiseth's response was a declaration of war: "One fine day, Dadiseth picked up the phone and rang Harsh Mariwala, confidently declaring that if Harsh didn't agree to a sale to HUL, then Marico would become history."

This wasn't an idle threat. HUL had just successfully dethroned Colgate in oral care. They had deep pockets, unmatched distribution, and a track record of crushing competition. Lever started increasing their discounts to retailers, they offered a 35% discount to them against just 10% which Marico was providing. They began spending money on advertising Nihar like never before.

Harsh sought advice from unlikely sources. Karsanbhai Patel of Nirma and consultant Ram Charan both told him the same thing: protect your resource-generating engine at all costs. Marico's response was total war. Mr. Mariwala and other senior leaders at Marico gave it a war flavour. They called the operation "Parachute ki Kasam". He launched a huge advertising campaign of his own, focusing on the sacred relevance of coconuts in religion and traditions, which struck an emotional chord with viewers. Marico also strengthened its focus on the rural market, hiring 250 personnel for direct-to-consumer sales.

The battle raged for six years. By 2002, Marico had not only survived but started pushing into new categories. The acquisition of Mediker in 2001 and entry into dermatology-led clinics in 2002 signaled that Marico was thinking beyond defense—it was planning for the future.

So what for investors? The HUL battle proved Marico's resilience and revealed its true competitive advantages: deep consumer understanding, nimble decision-making, and the ability to mobilize resources quickly. Companies that survive existential threats often emerge stronger—Marico was no exception.

VI. Scale & Acquisition Era (2003–2010)

2003 marked a strategic inflection point. Marico Innovation Foundation, responsible for executing the Corporate Social Responsibility of Marico was formed. In the same year Marico set up copra collection centres to procure directly from farmers increasing their margins. This wasn't corporate charity—it was vertical integration disguised as social responsibility.

In 2003, Mariwala spotted an opportunity in the skin care clinics space and founded Kaya Clinic as a subsidiary of Marico. In 2013, when Kaya was demerged from Marico and listed on stock exchanges as a separate entity it had 107 skincare clinics out of which 82 were located in India and had a range of 54 skin care products in its portfolio. Kaya represented Marico's ambition to move beyond traditional FMCG into services—a bold bet that skincare would premiumize.

But the real coup came in 2006. After years of bitter competition, HUL got tired of competing with Marico and finally gave up. It decided to sell its brand Nihar. As poetic justice would have it, Nihar was acquired by none other than Marico. The acquisition price of ₹216 crore gave Marico over 70% market share in coconut oil—an unassailable position.

International expansion accelerated. 2006-7 – Marico acquired Fiancée and Hair Code in Egypt and Caivil, Black Chic and Hercules in South Africa. These weren't random acquisitions—each gave Marico local brands and distribution in markets with similar hair care needs to India.

The 2009 Bangladesh IPO was particularly clever. Marico made a public offering of equity in Bangladesh; a first for one of its overseas subsidiaries. By listing locally, Marico signaled long-term commitment to the market and gained local shareholders as ambassadors.

The 2010 launch of Saffola Masala Oats seems obvious in retrospect, but it was prescient at the time. India's breakfast habits were changing, health consciousness was rising, and Marico was ready with a product that fit perfectly. Marico launched Saffola breakfast, Masala Oats in India.

So what for investors? The 2003-2010 period demonstrated Marico's ability to execute complex M&A, integrate acquisitions, and expand internationally while maintaining domestic momentum. The portfolio approach—from value (Nihar) to premium (Kaya)—showed sophisticated market segmentation.

VII. Modern Expansion & Digital Age (2011–Present)

The transition to professional management came in 2014. In 2014, Mariwala decided to step down as Managing Director whilst continuing to serve as Chairman. Mariwala brought in professional leadership to replace him in the company and his focus since has been on strategic direction and board management at Marico. This wasn't a retirement—it was an evolution. Harsh moved from operator to strategist, focusing on long-term vision while professional management handled execution.

The 2016 acquisition from Reckitt Benckiser was transformative. Marico bought personal care brands Set Wet, Livon and Zatak from Reckitt Benckiser in 2016. These weren't distressed assets—they were underleverage brands that Reckitt couldn't prioritize. In Marico's focused portfolio, they could flourish.

Digital transformation accelerated post-2018. 2018 – Marico invested in Revolutionary Fitness (Revofit); launched a new brand – True Roots that delays hair greying and launched its first digital exclusive brand – Studio X; launched Saffola Fittify. Studio X particularly represented a new model—digital-first brand creation targeting millennials.

The Vietnam expansion in 2022 showed Marico's continued international ambitions. Acquiring Pure de Provence and Oliv gave Marico premium positioning in a fast-growing market. The True Elements nutraceuticals acquisition the same year positioned Marico in the high-margin health supplements space.

By 2023, a quiet victory: Saffola oats became market leader, validation of the 2010 bet on healthy breakfast foods. This wasn't just market share—it was proof that Marico could enter established categories and win through better execution and brand building.

Recent performance has been solid if not spectacular. In 2024, the total revenue of Marico Limited amounted to about 71 billion Indian rupees. The company continues to balance growth investments with profitability, expansion with focus.

So what for investors? The modern era shows a company successfully navigating generational transition, digital disruption, and portfolio expansion while maintaining its core strengths. The ability to acquire and integrate brands suggests continued consolidation opportunities.

VIII. International Strategy & Emerging Markets Playbook

Marico has a significant presence in Bangladesh, South East Asia, Middle East, Egypt and South Africa. But the international story began with an accident. NRI in the Middle East had been smuggling Parachute oil with them for their daily use when export of the oil was restricted prior to the 1991 economic liberalisation. Marico decided to try to sell products in that market after liberalisation, but found out that the Arab customers did not like the scent of coconut, wanted a less sticky hair product, and needed a product to counteract the high level of chlorination in their water.

This insight—that international expansion required localization, not just export—shaped Marico's entire international strategy. In the international market, Marico is represented by brands like Parachute, HairCode, Fiancée, Caivil, Hercules, Black Chic, Code 10, Ingwe, X-Men and Thuan Phat. Each brand serves specific local needs while leveraging Marico's manufacturing and distribution expertise.

The Bangladesh story deserves special attention. In Bangladesh, Marico operates through Marico Bangladesh Limited, a wholly owned subsidiary. Its manufacturing facility is located at Shirirchala, in Dhaka Division. Marico didn't just export to Bangladesh—it became a Bangladeshi company, with local manufacturing, local employees, and eventually, local shareholders through the 2009 IPO.

Manufacturing footprint reveals strategic thinking. Marico has 8 factories in India located at Puducherry, Perundurai, Kanjikode, Jalgaon, Paldhi, Dehradun, Baddi and Paonta Sahib. Notice the locations—each chosen for proximity to raw materials (coconut growing regions) or tax advantages (Himachal Pradesh, Uttarakhand).

Today, international operations contribute 25% of company revenue—not just exports, but truly international business with local operations in multiple countries. The model works because Marico picks markets with similar consumption patterns to India—tropical countries where coconut oil is traditional, emerging markets where branded goods are aspirational.

So what for investors? International expansion provides both growth runway and risk diversification. The focus on similar markets (tropical, emerging, with Indian diaspora) reduces execution risk while providing exposure to faster-growing economies.

IX. Business Model & Financial Performance

Let's talk numbers. Over the past 5 years, the revenue of MARICO has grown at a CAGR of 7.2%. Over the past 5 years, MARICO net profit has grown at a CAGR of 9.5%. This isn't explosive growth, but it's consistent, profitable growth—the kind that compounds wealth over decades.

The portfolio composition tells the strategy story. Personal care drives ~59% of revenue, foods and other ~41%. Within this, Hair Care dominates at ~43% of revenue, followed by Edible Oils at ~29%. This concentration could be weakness or strength—Marico sees it as focus.

Market positions matter more than market sizes. Parachute commands ~43% market share in coconut oil, while Saffola holds ~21% in refined edible oils. These aren't just leading positions—they're dominant positions that provide pricing power and distribution leverage.

Distribution remains the moat. Marico reaches over 5 million outlets (the company reported 7 million in 2023). In India, distribution is destiny, and Marico has spent decades building direct reach into rural markets where 65% of Indians live.

The net profit of MARICO stood at Rs 15,020 m in FY24, which was up 13.6% compared to Rs 13,220 m reported in FY23. Net profit for the year grew by 13.6% YoY. Net profit margins during the year grew from 13.5% in FY23 to 15.6% in FY24. Expanding margins while growing revenue is the holy grail of FMCG—Marico is achieving it through premiumization and cost management.

Looking forward, the company expects 16% earnings growth for FY23-25E, driven by premium segments and rural recovery. The math is simple: volume growth of 8-10%, price increases of 3-4%, and margin expansion through mix improvement.

So what for investors? Marico offers a classic FMCG investment proposition: steady growth, expanding margins, and strong cash generation. The question isn't whether Marico will grow, but whether the market's valuation (often at 50+ PE) prices in too much of that growth.

X. Playbook: Business & Investing Lessons

The family business transformation offers the first lesson: structure follows strategy. Harsh Mariwala spent three years negotiating the separation from Bombay Oil Industries—not because he wanted control, but because he understood that consumer businesses require different capabilities than commodity trading. The lesson for investors: look for companies willing to make hard structural changes for strategic clarity.

The Mariwala management philosophy is refreshingly practical. Despite having no MBA, Harsh built a culture of learning. His approach—hire people smarter than yourself, maintain a flat organization, encourage bottom-up innovation—created an environment where professional managers thrived alongside family members. Along with focus on innovation and investing in brand building, Mariwala focused on establishing a company culture to empower employees and values such as trust to establish it as a force to reckon with.

Innovation in mundane categories provides the second lesson. Plastic bottles for coconut oil? Wider mouths for winter? These aren't revolutionary innovations, but they solved real consumer problems. The lesson: sustainable competitive advantages often come from accumulation of small innovations, not breakthrough inventions.

Capital allocation discipline shines through Marico's history. The company avoided the conglomerate temptation that destroyed many Indian family businesses. Even when diversifying, Marico stayed within adjacent categories where its capabilities provided advantage. The Nihar acquisition at ₹216 crore looks expensive at 2x sales, but gaining 20% market share in your core category? Priceless.

Trust-based customer relationships represent long-term thinking. The Saffola Healthy Heart Foundation (1991) invested in consumer education decades before it became fashionable. Today, Saffola is a $143 million brand because consumers trust its health claims. The lesson: brand building is a multi-decade investment that requires patience capital markets often lack.

The social impact integration through Marico Innovation Foundation (2003), Mariwala Health Initiative (2014), and ASCENT Foundation (2012) isn't CSR checkbox-ticking. As of 2024, ASCENT has over 1000 member entrepreneurs. The annual revenue of ASCENT members crosses Rs.1,00,000 crore. By nurturing entrepreneurship, Marico strengthens the ecosystem it operates in.

So what for investors? The Marico playbook—focus, innovation in mundane categories, patient brand building, strategic M&A—is replicable but requires discipline most companies lack. Look for companies following similar strategies in other categories.

XI. Analysis & Bear vs. Bull Case

Bull Case:

The bulls see Marico as an inevitable beneficiary of India's consumption story. One in three Indians uses Marico products—that's reach money can't buy. The company's strong market positions in growing categories (hair care, health foods) provide runway for decades.

The premiumization journey has just begun. As Indians get richer, they upgrade from loose oil to packaged, from coconut oil to value-added hair care. Marico is positioned at every price point to capture this upgrade cycle. The successful premium extensions (Parachute Advansed, Saffola Gold) prove execution capability.

International diversification is understated. 25% of revenue from international markets provides both growth and stability. These aren't mature markets—Bangladesh, Vietnam, Middle East are growing faster than India. As these markets formalize, Marico's first-mover advantage compounds.

Management quality remains exceptional. The successful transition from founder to professional management, continued innovation pipeline, and strategic discipline suggest the culture will endure beyond individuals.

Bear Case:

The bears point to uncomfortable numbers. 5-year sales CAGR of just 8.17% in a supposedly fast-growing market raises questions. Is Marico losing relevance with younger consumers?

Competition intensifies from every direction. Hindustan Unilever remains formidable with 10x Marico's resources. Dabur and Emami compete directly in hair care. New-age D2C brands like WOW, Mamaearth attack with digital-first strategies. Can Marico defend all fronts?

Commodity price volatility creates earnings uncertainty. Copra (dried coconut) prices can swing 50% in a year. While Marico hedges, sustained input inflation squeezes margins or requires price increases that hurt volume.

Digital disruption is real. Young consumers discover brands on Instagram, not TV. They trust influencers, not celebrity endorsements. Marico's traditional brand-building playbook may be obsoleting.

The valuation at 50+ PE prices in perfection. Any disappointment—a failed launch, margin pressure, competitive loss—could trigger significant correction.

Competitive Dynamics:

Versus Hindustan Unilever, it's still David and Goliath. HUL has the portfolio breadth, but Marico has focus. The Nihar battle proved Marico can win through superior execution in chosen categories.

Against Dabur and Emami, it's a knife fight among equals. Similar heritage, similar categories, similar strategies. Differentiation comes from execution and innovation speed—Marico's professional management provides edge.

The D2C threat is existential but manageable. These brands grab share in premium segments but struggle with distribution and scale. Marico's response—acquiring brands like Beardo, launching digital-first brands—shows adaptability.

So what for investors? Marico is a quality company at a premium valuation. The bull case requires continued execution excellence and market share gains. The bear case sees structural challenges to the traditional FMCG model. The truth likely lies between—steady but unspectacular returns for patient investors.

XII. Epilogue & Looking Forward

The FY30 target is ambitious: double turnover to ₹20,000 crore. The math requires 12-15% annual growth—achievable but demanding. The strategy hinges on foods becoming a second growth engine alongside personal care.

The strategic shift from low-margin edible oils to premium foods and personal care continues. Each new launch—quinoa, chia seeds, premium hair serums—moves the portfolio upmarket. This isn't diversification for growth—it's margin expansion through mix improvement.

The next generation question looms. Rishabh Mariwala is a second-generation entrepreneur and investor, currently at the helm Sharrp Ventures, the Mariwala Investment Office. He is also an Independent Director on the Board of ASK Investment Managers Limited. The family remains involved but not operational—a balance that few Indian companies achieve.

Three critical questions will determine Marico's future:

First, can innovation continue at scale? As Marico grows, maintaining the entrepreneurial spirit becomes harder. The launch success rate, time to market, and innovation pipeline will be key metrics.

Second, can international expansion accelerate? 25% international revenue could become 40% with successful execution. But each market requires localization, investment, and patience.

Third, can Marico navigate the digital transition? Building digital-first brands, engaging young consumers, competing with D2C players—all require capabilities different from traditional FMCG.

The Harsh Mariwala legacy is secure. From a crowded office in Masjid Bunder to a ₹91,000 crore company touching billions of consumers—it's an extraordinary journey. But as Harsh would say, borrowing from his entrepreneurial philosophy: "Entrepreneurs cannot take no for an answer. There are always alternatives to some limitations you have and you have to find ways to overcome those limitations."

For long-term investors, Marico represents a bet on Indian consumption, professional management, and steady compounding. It won't be the highest returning stock in your portfolio, but it might be the most dependable. In a world of uncertainty, that's worth something.

The story that began with pepper trading in 1862 continues. The products change—from pepper to coconut oil to health foods. The challenges evolve—from License Raj to liberalization to digitalization. But the core remains: understanding Indian consumers, building trust through quality, and relentless innovation in everyday products.

As we look forward, remember that Marico's greatest victories came during its greatest challenges. The HUL battle strengthened distribution. The commodity price volatility drove premiumization. The digital disruption sparked innovation.

Perhaps that's the real lesson: in business, as in life, it's not the absence of challenges but the response to them that defines winners. And if history is any guide, Marico will keep finding ways to win.

So what for investors? Marico at 50+ PE requires faith in India's consumption story and management execution. It's not a value play or a growth rocket—it's a quality compounder for patient capital. The next decade will test whether traditional FMCG moats—distribution, brand, and scale—remain defensible in a digital age. Betting on Marico is betting they will.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube