Vedant Fashions: The Emperor of Indian Celebration Wear

I. Introduction & The "Wedding Category" Thesis

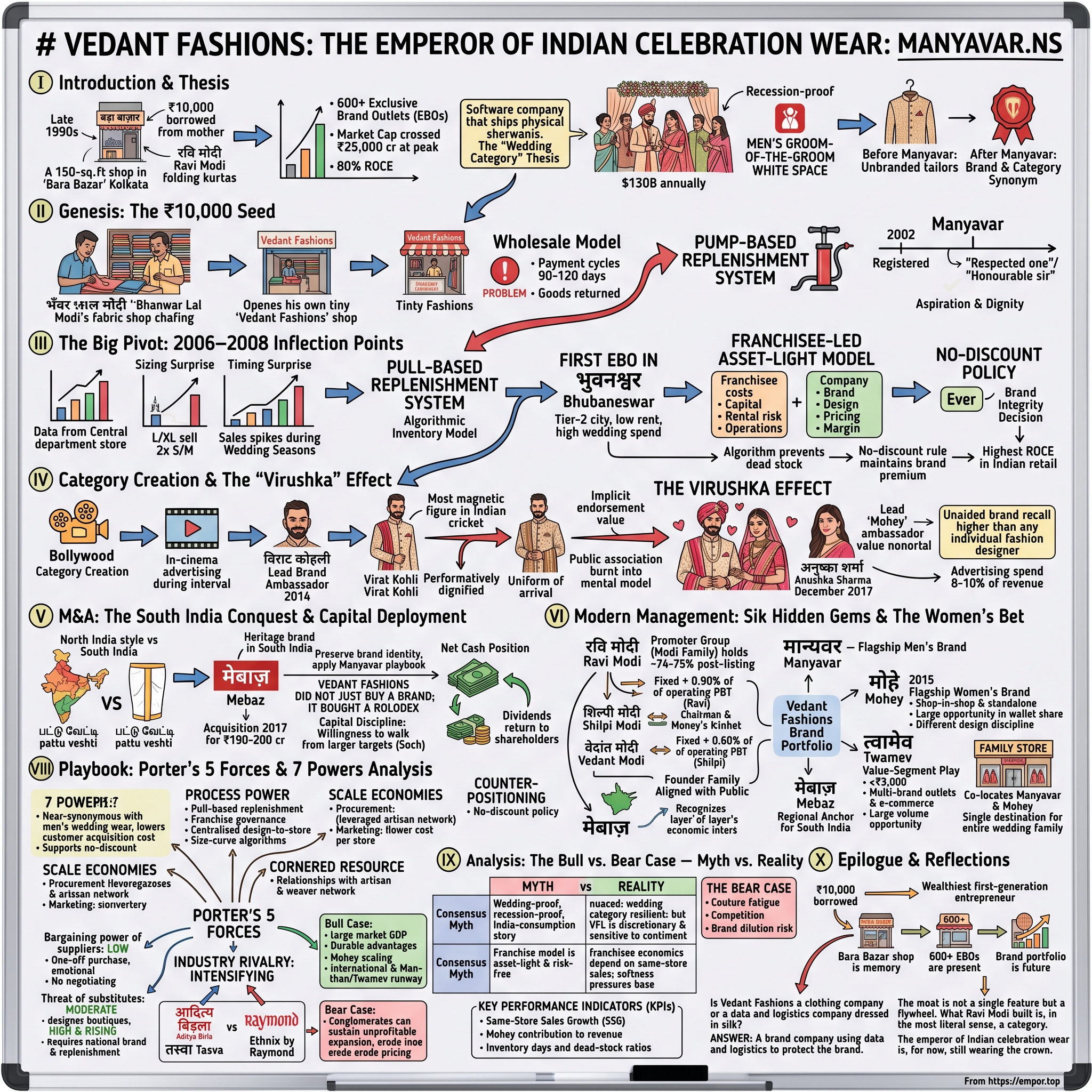

Picture a 150-square-foot rented shop in Kolkata's बड़ा बाज़ार Bara Bazar in the late 1990s. Bolts of polyester piled to the ceiling. A single ceiling fan stirring the humid Bengal air. A 22-year-old named रवि मोदी Ravi Modi is folding kurtas he has personally bought, designed, tagged, and priced. He has ₹10,000 in his pocket, borrowed from his mother because his father refused to seed the venture from the family's existing garment business.1 In the entire shop there is exactly one employee: himself.

Twenty-five years later, that shop has metastasised into वेदांत फैशंस Vedant Fashions Limited, a publicly listed business with a market capitalisation that has crossed ₹25,000 crore at peak, operating 600+ exclusive brand outlets across India and the global Indian diaspora, with return on capital employed that has hovered around the 80% range in normal years — a figure that puts it in the same statistical neighbourhood as Hermès and LVMH's best maisons.[^2]

That last number deserves a moment of reflection. When a clothing retailer earns 80 cents of operating profit per year for every dollar of capital employed in the business, you are no longer looking at a clothing retailer. You are looking at something closer to a software company that happens to ship physical sherwanis. And the question this episode is trying to answer is: how on earth did a man from a middle-class मारवाड़ी Marwari trading family in Kolkata, with no fashion training, no MBA, and no inherited capital, build a category-defining luxury franchise in the most fragmented apparel market on the planet?

The shorthand answer is that Ravi Modi did not set out to sell clothes. He set out to own a moment. Specifically, the Indian wedding. According to industry estimates the wedding industry is roughly $130 billion annually in India, second only to the United States, and uniquely it is essentially recession-proof because Indian households save for years — sometimes decades — for these single-week events, and they do not flinch on spend when the equity market wobbles.[^3] The genius of मान्यवर Manyavar was to recognise that in this market the male grooming-of-the-groom occasion was a vast white space — culturally heavy, financially significant, and yet served almost entirely by unbranded tailors and unorganised local shops.

Before Manyavar, asking an Indian man where he bought his sherwani was like asking him where he got his haircut: the answer was usually a name only he and his neighbourhood knew. After Manyavar, the answer became a brand. That semantic shift — from commodity to category synonym — is the entire investment story compressed into one sentence.

In this episode we are going to trace the arc from that 150-square-foot shop to the IPO that closed on February 8, 2022 and was subscribed roughly 2.57 times despite being priced as an entirely Offer-for-Sale, meaning not a single rupee of the ₹3,149-crore proceeds flowed into the company itself — every paisa went to existing shareholders cashing out.[^4]2 We will dwell on the 2008 pivot that abandoned the multi-brand wholesale model for owned-and-franchised exclusive brand outlets, the data discipline that made dead stock a non-issue, the विरुष्का Virushka brand marriage with विराट कोहली Virat Kohli and अनुष्का शर्मा Anushka Sharma, the मेबाज़ Mebaz acquisition that cracked South India, and the brand portfolio — मोहे Mohey, त्वामेव Twamev, मंथन Manthan — that quietly hedges the next decade.

And we will end where every Acquired episode ends: with the question of whether the moat is wide enough to survive the arrival of आदित्य बिड़ला Aditya Birla's तस्वा Tasva and Raymond's Ethnix — two of the deepest-pocketed industrial groups in India deciding, simultaneously, that they want to be in Ravi Modi's business. This is the story of how a one-man kurta shop became the emperor of Indian celebration wear, and why the next chapter is genuinely uncertain.

II. Genesis: The ₹10,000 Seed

Ravi Modi grew up in the back of a fabric shop. His father, भँवर लाल मोदी Bhanwar Lal Modi, ran a small textile trading business in Kolkata, and Ravi's earliest memories were of folded saris, the smell of starched cotton, and the staccato cadence of his father's haggling with wholesale buyers. After completing his B.Com, the expected path was clear: join the family business, learn the trade, marry within the community, repeat the cycle for another generation. Ravi did join. And almost immediately, he started chafing.[^6]

The friction was philosophical. His father sold what wholesalers wanted to buy. Ravi wanted to sell what consumers wanted to wear. He kept pushing his father to expand into men's ethnic wear — sherwanis, kurtas, indo-westerns — arguing that nobody was branding this category, and that there was an obvious gap between expensive bespoke tailoring and ill-fitting commodity wear. His father, who had survived decades of cycles in the unforgiving Kolkata cloth market by sticking to what he knew, refused. The disagreement escalated until Ravi did the unthinkable for an Indian son in 1999: he left.

He didn't leave with much. His mother, संगीता मोदी Sangeeta Modi, sympathised with her son and quietly handed him ₹10,000 — roughly $230 at the prevailing exchange rate, and not a transformational sum even by 1999 Kolkata standards.1 With that capital, Ravi rented a tiny shop, sourced his first batch of ethnic wear from suppliers he had cultivated during his father's business, and opened for business under a name that would later prove almost embarrassingly fitting: Vedant Fashions, after his future son.

The first three years were a study in survival economics. Ravi was the founder, the designer, the buyer, the cashier, and on slow days the cleaner. He sold to anyone who walked in, but the real money was supposed to come from wholesale: selling in bulk to multi-brand retailers across India who would then mark up his goods and sell them to consumers. The problem with this model was twofold. First, payment cycles in the Indian wholesale garment trade can stretch to 90 or 120 days, which is fatal for a thinly capitalised startup. Second, when retailers couldn't move stock, they returned it — and Ravi had no leverage to refuse.

There is a famous moment in the founding story, repeated in nearly every profile of him, where Ravi was so cash-strapped that he sold an entire seasonal collection to Vishal Mega Mart, the value-retail chain, at a loss simply to make payroll for his handful of employees that month.3 That moment, more than any boardroom epiphany, is what crystallised his strategic clarity: a wholesaler is a price-taker. A brand is a price-maker. If he was going to build a business that could pay wages reliably, he needed to control the relationship with the end consumer.

But that realisation took years to act on, because in the early 2000s Ravi did not yet have the data, the capital, or the conviction to leap directly into owned retail. So he did something cleverer: he started imposing structure on his wholesale book. He began curating which multi-brand outlets carried his goods, refusing to sell to retailers who discounted aggressively, and building credit terms that, while still painful, were less ruinous than the industry norm. He registered the brand "Manyavar" in 2002, a Sanskrit-derived honorific meaning roughly "respected one" or "honourable sir" — a name designed to signal aspiration without being foreign or affected.[^6]

The genius of the name choice, in hindsight, was that it solved a marketing problem most Indian apparel founders never even articulated. Indian men in the early 2000s wore ethnic clothing almost exclusively to celebratory occasions — weddings, festivals, religious functions — and they wanted, at those moments, to feel respected. They did not want to feel fashion-forward, edgy, or experimental. They wanted to feel dignified. The brand name itself delivered that promise before the customer even tried on the garment.

By 2005 Ravi had a recognisable brand circulating in roughly 100 wholesale outlets across eastern and northern India, a small but profitable operation, and a growing suspicion that the multi-brand model was a ceiling, not a runway.[^8] The next three years would prove that suspicion correct, and force the most consequential decision of his career.

III. The Big Pivot: 2006–2008 Inflection Points

The story of how Manyavar became Manyavar — the brand the entire industry now studies — really begins in 2006, on the second floor of a Central department store, almost certainly in either Hyderabad or Pune, where the company had taken its first shop-in-shop arrangement. For the first time, Ravi Modi could see in granular daily detail what was actually being bought, by whom, in what sizes, and at what price points. Before this, his data came from wholesale invoices, which told him what retailers ordered, not what consumers wanted. The difference, it turned out, was enormous.

The first surprise was sizing. Conventional Indian garment retail at the time stocked sizes in a roughly balanced curve — small, medium, large, extra-large in similar quantities — because that's what wholesalers reflexively ordered. Real-time Central data showed that large and extra-large were selling roughly twice as fast as small and medium, presumably because the customer base for celebration wear skewed older and more affluent than the average Indian male.3 If you were a wholesaler producing balanced size curves, your large-size stock-outs were costing you sales while your unsold small-size inventory was costing you working capital. Both ends of the curve were bleeding money.

The second surprise was timing. Sales did not move linearly across the year; they spiked violently around the Indian wedding seasons — roughly October through February in the north, with smaller bursts around regional festivals. A retailer that built inventory for a flat year was either drowning in dead stock in March or stocking out in November. Both outcomes were catastrophic.

What Ravi began to build out of this realisation, slowly between 2006 and 2010, was what the company today calls its "pull-based replenishment system" — an algorithmic inventory model that, instead of pushing seasonal collections into stores and praying, watches actual sell-through at each store in near-real-time and replenishes only what is moving. In the language of supply chain, he was attempting Zara's playbook on a vastly smaller capital base, in a country where the supply chain was almost entirely unorganised. It would take more than a decade to fully realise, but the discipline was already taking root.

The second pivot, layered on top of the data revelation, was the 2008 decision to open the first exclusive brand outlet, or EBO, in भुवनेश्वर Bhubaneswar.3 The choice of city is itself instructive. Bhubaneswar was not Bombay, not Delhi, not even Hyderabad. It was a Tier-2 city in eastern India where rents were low, competition was virtually nonexistent, and the wedding spend per household was, relative to local incomes, enormous. If the format worked there, it would scale anywhere in India. If it failed, the failure would be cheap enough to absorb.

The format worked. And once it did, Ravi made the second consequential decision: he would not own the stores himself. Vedant Fashions would scale through franchising, where local entrepreneurs put up the capital for the store, took on the rental risk, and ran day-to-day operations, while the company supplied the inventory on a consignment model, set every design and pricing decision centrally, and took a margin on every garment sold. This is the so-called asset-light franchise model that has become the textbook capital structure for high-ROCE retail in India.[^2]

The asset-light model deserves a longer pause, because it explains most of the financial magic that followed. In a conventional retail expansion model, every new store costs the company an upfront capital outlay — security deposit, fit-out, opening inventory, working capital — that can easily run to ₹50-100 lakh per store. To open 100 stores, you need ₹50-100 crore of capital, and the return on that capital depends on the new store actually generating traffic. In Vedant's model, the franchisee fronts almost all of that cost, while Vedant retains the brand, the design, the pricing power, and most of the gross margin. Stores that don't generate traffic are the franchisee's problem; stores that do generate traffic are everybody's reward.

The third pivot, and the one that most analysts undersell, was the no-discount policy. From the day the first EBO opened in Bhubaneswar, Manyavar set a firm rule: no end-of-season sales, no clearance discounts, no festival markdowns, no buy-one-get-one offers. Ever. This was nearly unheard of in Indian apparel retail, where discounting was the default lever for moving slow stock. The justification was simple: a brand selling celebration wear cannot afford to be associated with markdowns, because a man buying his wedding sherwani does not want his future wedding photographs to show a garment that might have been on a 50% rack a month later. The no-discount policy was not just a pricing decision; it was a brand integrity decision.

The no-discount policy was only sustainable because the pull-based replenishment system kept dead stock from accumulating in the first place. The two innovations are inseparable: the algorithm prevents the inventory pile-up that would force discounts, and the no-discount rule maintains the brand premium that justifies the franchisee economics. Take away either pillar and the whole model collapses. Together they form the operating engine that, by the mid-2010s, was producing the highest ROCE in Indian organised retail.

By 2015 Vedant Fashions operated roughly 300 exclusive brand outlets and had reached a scale where the question was no longer "will this model work" but "how big can it get."[^9] The answer to that question depended on one thing: whether Ravi Modi could convince a billion Indians that wearing a Manyavar sherwani was not a clothing decision but an identity decision. For that, he needed Bollywood.

IV. Category Creation & The "Virushka" Effect

Indian advertising in the 2010s was a particular kind of arms race. Television prime time was prohibitively expensive and increasingly fragmented across hundreds of cable channels. Print was dying. Digital was nascent and largely uninstrumented. For a category like men's ethnic wear, where the customer might make a single significant purchase decision every three-to-five years, the conventional advertising playbook — repeat exposure across mass channels — was both expensive and badly matched to the purchase cycle.

Ravi Modi's marketing intuition was that he needed to find the customer at the exact moment when they were thinking about celebration. That insight led to one of the more underappreciated branding decisions in modern Indian retail: Manyavar pioneered in-cinema advertising during the interval, when Bollywood audiences — disproportionately the same demographic preparing for upcoming weddings — were captive, in a celebratory mindset, and surrounded by family. The cost per impression was a fraction of TV prime time. The contextual fit was almost surgical.

But the masterstroke came in 2014 when Manyavar signed विराट कोहली Virat Kohli, then the most magnetic figure in Indian cricket, as its lead brand ambassador. Cricket endorsements in India were nothing new; what was new was how Manyavar used him. The campaigns did not show Virat playing cricket or being athletic; they showed him at weddings — his own family weddings, in some campaigns — looking deeply, almost performatively, dignified in a Manyavar sherwani. The message was unsubtle: the most popular man in India wears Manyavar at his most important moments. You should too.

The campaign reached its apotheosis in December 2017, when Virat Kohli married actress Anushka Sharma in a private ceremony in Tuscany, Italy. Anushka had been the lead female brand ambassador for Mohey, Vedant Fashions' women's ethnic-wear sub-brand, since shortly after its 2015 launch.[^10] When images of "Virushka" — the inevitable Indian celebrity-couple portmanteau — in their wedding attire began circulating, the implicit endorsement value was almost unfathomable. The country's biggest celebrity wedding became, in effect, a Vedant Fashions advertisement that the company could not have bought at any price.

Whether the couple's actual wedding attire was Manyavar and Mohey is a question on which the company has been characteristically circumspect. What matters for the brand is that the public association was made, reinforced through every subsequent festival campaign, and burnt into the Indian consumer's mental model. By 2019 unaided brand recall for Manyavar in the men's ethnic wear category was reportedly higher than for any individual fashion designer in India.[^11]

The deeper lesson here is about category creation, not celebrity marketing. Before Manyavar, "ethnic wear" was understood by Indian consumers as a duty — something you wore because tradition required it, often reluctantly, often uncomfortably, often regretting the lack of fit and finish. The Virat-Anushka campaigns, layered on top of a decade of brand-building, accomplished something subtler: they reframed ethnic wear as an aspirational choice. The sherwani stopped being a costume and started being a uniform — a uniform of arrival, of having made it, of being the kind of man (or woman) whose celebrations were worth investing in.

Once that perception shift was complete, the no-discount policy stopped looking like a pricing oddity and started looking like a luxury signal. Hermès does not have an end-of-season sale. Rolex does not have a Diwali offer. The fact that Manyavar refused to discount became, paradoxically, one of the strongest pieces of evidence that it belonged in the same category. The pricing strategy reinforced the brand strategy reinforced the celebrity strategy reinforced the pricing strategy. The flywheel was complete.

There is one additional piece of marketing infrastructure worth flagging, because it became visible to investors only after the IPO disclosed it: the brand spends roughly 8-10% of revenue on advertising and brand-building in normal years, a figure that is in line with global luxury houses and substantially above the spend ratios of typical Indian apparel retailers.[^12] The advertising spend is the operating cost that sustains the brand premium that supports the no-discount policy that protects the gross margin. It is a flywheel that only works if you commit to spending through cycles, which is precisely what a privately controlled company with a 75% promoter holding can do that a quarterly-managed conglomerate often cannot.

By 2017, with the brand machine running at full velocity and the cash flow predictable enough to fund acquisitions, Ravi Modi made the next strategic move. He went shopping.

V. M&A: The South India Conquest & Capital Deployment

There is a particular kind of geographic stubbornness in Indian consumer markets that anyone trying to build a national brand has to reckon with. The four South Indian states — तमिल नाडु Tamil Nadu, कर्नाटक Karnataka, केरल Kerala, and combined आंध्र प्रदेश Andhra Pradesh and तेलंगाना Telangana — together account for roughly a quarter of India's consumer spending, but they speak different languages, eat different food, and crucially for our story, dress differently at weddings. The North Indian sherwani-and-bandhgala tradition does not translate cleanly into a region where the groom's family expects பட்டு வேட்டி pattu veshti, silver-bordered cotton dhotis, and silk angavastrams.

By 2017 Manyavar had penetrated the South Indian market but its penetration was thinner than in the North, and the brand carried, fairly or not, the perception of being a Marwari-Bengali transplant in a market where heritage and lineage mattered enormously. Ravi Modi's diagnosis was that organic expansion would take a decade. Acquisition could compress that to a year.

The target was मेबाज़ Mebaz, a Hyderabad-based heritage brand founded in 1976 by the Boorugu family. Mebaz was deeply embedded in the Hyderabadi wedding economy, with a few flagship stores that locals had visited for generations and a brand voice that was unmistakably South Indian in its aesthetic vocabulary. In November 2017, Vedant Fashions announced its acquisition of Mebaz for a transaction value reported in the press at approximately ₹190-200 crore.[^13]

The deal economics, when reverse-engineered against the limited disclosed numbers, are instructive. Mebaz at the time of acquisition was generating roughly ₹140 crore of annual revenue and operating profitably though not extraordinarily so.[^13] An acquisition price in the ₹190-200 crore range implied a price-to-sales multiple of roughly 1.3-1.4x, which by Indian apparel acquisition standards in 2017 was a full but not unreasonable price. For context, the same year Vedant Fashions had reportedly walked away from a much larger potential acquisition of सोच Soch, the women's ethnic-wear brand, where the asking price reportedly approached ₹1,200 crore on a revenue base that did not justify the multiple. The Mebaz price was disciplined; the Soch price was not. Ravi Modi's willingness to walk from the bigger target tells you as much about his capital discipline as his willingness to sign the smaller one.

But the strategic logic was deeper than price. Mebaz was not just a regional brand; it was a relationship business. Hyderabadi wedding families had been visiting Mebaz stores for two generations, building familiarity with specific salesmen, returning for younger siblings' weddings. Vedant Fashions did not just buy a brand; it bought a Rolodex. Once the acquisition closed, the company moved deliberately to preserve the Mebaz brand identity — Mebaz stores continue to operate under the Mebaz name to this day, with their own design language — while quietly applying the Manyavar operating playbook underneath: the pull-based replenishment, the centralised pricing, the franchise expansion model.

This is the kind of acquisition that looks unimpressive on a deal-announcement headline and quietly creates enormous value over five years. The Mebaz business, post-integration, expanded its store count substantially and now contributes a meaningful, though not separately disclosed, fraction of Vedant Fashions' South Indian revenue. More importantly, it gave the company permission to operate in a regional market that had previously regarded it as an outsider.

The Mebaz deal also revealed something about Ravi Modi's M&A philosophy that bears emphasis. He is not a roll-up artist. He has not used Vedant Fashions' strong cash generation to acquire serially across categories or geographies. The Mebaz acquisition remains, as of mid-2026, the single significant acquisition the company has done in its 27-year history. Compare that to the typical Indian consumer roll-up of the past five years, where private-equity-backed platforms have stitched together a dozen brands of varying quality and called it a portfolio. Vedant Fashions has, with characteristic patience, made one bet, integrated it carefully, and kept the powder dry.

The reluctance to over-deploy capital is part of why the balance sheet looks the way it does. Even after the 2022 IPO, which raised no primary capital, the company has maintained a net cash position, returning excess cash to shareholders via dividends rather than chasing acquisition multiples that don't make sense. For a business throwing off the cash flow that this one does, the discipline is harder than it sounds. There is always a banker pitching the next consolidation deck. There is always a competitor reaching scale that could be acquired. The willingness to say no is itself a moat.

That capital discipline ties directly to how the founding family is incentivised, which is where this episode goes next.

VI. Modern Management: Skin in the Game

There is a particular Marwari business idiom that translates loosely as "the eye of the owner fattens the cattle," and few Indian listed companies illustrate it as starkly as Vedant Fashions. The promoter group — Ravi Modi and his family — held approximately 84.86% of the company at the time of the IPO and even after the Offer-for-Sale dilution continued to hold roughly 74-75% post-listing, a stake that ranks among the highest founder holdings in any listed Indian consumer business.[^4][^14]

To understand what this means in practice, consider the management structure. Ravi Modi serves as Chairman and Managing Director. His wife शिल्पी मोदी Shilpi Modi heads digital strategy and the Mohey women's business. Their son वेदांत मोदी Vedant Modi, after whom the company is named, joined as Chief Revenue Officer in the mid-2020s. This is a Marwari family business in the most literal sense of that phrase, and the company makes no apology for it. There is no professional CEO. There is no independent founder-handover plan. The compensation and incentive structure is built around aligning a founder family with the public shareholders who own the remaining quarter of the equity.

That alignment is engineered with unusual precision. Ravi Modi's compensation, as disclosed in the company's corporate governance filings, is structured as a fixed component plus 0.90% of operating profit before tax, while Shilpi Modi's compensation includes a variable component of 0.60% of operating PBT.[^14] In any year where operating profitability declines, their compensation declines roughly in lockstep with shareholder returns. In years of expansion, both rise together.

This is not the only way a founder family can be incentivised, but it is one of the cleanest. A pure salary structure can detach executive pay from corporate performance. An equity-grant structure can dilute existing shareholders and create perverse incentives around stock buybacks. A pure profit-share structure, particularly with promoters who already hold a dominant equity stake, simply tells the market: we eat what we kill, and what we kill is your dividend stream too.

The flip side of family control is the absence of conventional corporate independence. The board has independent directors, as Indian listing rules require, but the strategic direction of the company has unmistakably been a single-family project for its entire history. For long-only investors comfortable with concentrated promoter risk in exchange for long-term thinking, this is a feature. For investors who value managerial professionalisation and independent oversight, it is at minimum something to monitor.

Below the family layer, the management style has been deliberately lean. Vedant Fashions, as of its most recent annual reports, operated with a corporate headcount that for years sat in the few-hundreds range despite running an operation that generates several thousand crore of revenue and supports more than 600 stores.[^15] The leanness is a deliberate choice. Most of the operational complexity of the business — store management, customer service, local marketing — is pushed out to the franchise network. Most of the design and merchandising complexity is concentrated in a small Kolkata-based team. The headquarters runs the algorithm, the brand, and the cash; everything else is distributed.

To extend equity participation below the founding family, the company implemented Scheme Pratham, an ESOP plan for senior key managerial personnel, structured to give the small core of professional executives meaningful skin in the game without diluting the promoter holding materially.[^14] The scheme has been calibrated cautiously — Vedant Fashions has never been an aggressive equity-granter the way technology businesses are — but the existence of a structured ESOP at this scale matters more than the absolute quantum, because it telegraphs to the professional layer that the company recognises their economic interest.

The cultural texture that emerges from this structure is, by all accounts, demanding and intensely measurement-driven. Ravi Modi's reputation among industry peers is of an operator who reads weekly store-level sales reports personally, who walks the floor of flagship stores unannounced, and who is unsentimental about merchandise that fails to sell through. The same Marwari trading sensibility that drove his father's small shop now drives the working capital management of a multi-thousand-crore listed company. The tools have changed; the temperament has not.

What this all adds up to, from an investor perspective, is a company that behaves more like a privately held family business that happens to have a public listing than a typical listed corporate. Decisions are taken at family-board pace, capital is deployed with extreme caution, and the founding generation has every economic incentive to keep optimising for the next decade rather than the next quarter. Whether that is the right governance model is a normative question. That it has delivered the ROCE numbers it has delivered is empirical.

VII. Hidden Gems & The Women's Bet

Walk into any large Manyavar flagship today and you will notice something subtle: roughly half the floor space, in the more recent stores, is given over to a brand most casual observers couldn't name a decade ago. That brand is मोहे Mohey, Vedant Fashions' women's ethnic-wear vertical, launched in 2015, and it is the company's single most consequential strategic bet of the past decade.

The opportunity is straightforward in arithmetic terms and complicated in execution. The Indian women's ethnic-wear market is structurally several multiples larger than the men's market by addressable revenue. Where an Indian man might own one or two sherwanis for a wedding cycle, an Indian woman in the same family will typically need a sangeet outfit, a haldi outfit, a mehendi outfit, a reception lehenga, and so on — five-to-seven distinct ensembles for a single wedding event, each requiring matching jewellery, dupattas, and accessories. The wallet share per wedding family is dramatically tilted toward the women in the family, and Vedant Fashions for its first fifteen years had captured almost none of it.

Mohey was the move to fix that. The brand was launched in 2015, initially as a shop-in-shop concept inside existing Manyavar stores, and gradually rolled out as standalone exclusive brand outlets through the late 2010s and into the early 2020s. The strategic insight was that women shop for ethnic wear differently from men — they want more variation, more occasion-specific pieces, more frequent refresh — and the merchandising and design discipline needed to be different. But the operating playbook, mercifully, could be the same: pull-based replenishment, no-discount pricing, franchise expansion, central design control.

Mohey took longer to gain traction than the Manyavar bulls had hoped. Building a women's ethnic-wear brand against entrenched competitors like Sabyasachi, Anita Dongre, and a thousand local boutiques was a different fight from the relatively uncontested men's market. But by the early 2020s the brand was reportedly contributing a meaningful low-double-digit fraction of total revenue, with growth rates that outpaced the company average, and was a key reason the IPO was priced as confidently as it was.4

But Mohey is not the only secondary brand in the portfolio. त्वामेव Twamev — a Sanskrit word meaning roughly "you alone" or "thou only" — was launched as the accessible-luxury extension, targeting a price point reportedly around three times the average selling price of Manyavar, aimed at the customer who would otherwise go to a boutique designer for couture but who appreciates the Manyavar fit-and-finish and willingness to discount on neither.[^15] Twamev is the upmarket flank, and while its store count remains modest, it serves a strategic purpose: it gives the brand permission to play at the higher end of the wedding budget, where the absolute margins are largest.

At the other end of the portfolio sits मंथन Manthan, the value-segment play, distributed largely through multi-brand outlets and increasingly through e-commerce. Manthan exists because the Indian wedding-wear market is bifurcated: above ₹15,000, Manyavar and its peers dominate; below ₹5,000, an unorganised army of local tailors and small retailers captures the value-conscious customer. Manthan is the cannon aimed at that lower segment, designed to offer Vedant Fashions' design and brand credibility at price points that the core Manyavar customer would consider beneath their occasion needs but that, in aggregate, represent a much larger volume opportunity.

Add the heritage Mebaz brand to the mix, and the architecture starts to look deliberate: Manyavar as the flagship men's brand, Mohey as the flagship women's brand, Twamev as the premium extension, Manthan as the value extension, and Mebaz as the regional anchor for South India. Five brands, each occupying a distinct price-and-occasion niche, sharing the same back-end algorithm, the same supply chain of roughly 500-plus independent artisans and weavers, and the same central design discipline.[^15]

The synergy is most visible in what the company has begun to call "Family Stores" — large-format outlets in major cities that co-locate Manyavar and Mohey, sometimes with Twamev sections, designed to be the single destination a wedding family visits to outfit everyone from the groom and his father to the bride and her sisters. The lifetime value per family captured by a single Family Store is potentially multiples of what a standalone Manyavar store can generate. The operating economics of these larger formats are still being optimised, but the strategic logic is correct: in a category where the customer makes a single integrated purchase decision for an entire celebration, you want one storefront that captures the entire decision.

The hidden-gem framing here is important because the public market valuation of Vedant Fashions has, for most of its post-IPO life, been priced primarily on the strength of the core Manyavar brand. If Mohey scales to anywhere near Manyavar's penetration over the coming decade, the upside to revenue and earnings is non-trivial. If Twamev finds its footing in the urban affluent segment, it adds margin. If Manthan cracks the value tier through e-commerce, it adds volume. Each of these is an option that the market is not necessarily fully pricing into the headline multiple. Each is also an option that requires ongoing execution capital, brand spend, and management attention — which is why the bear case, when we get to it, focuses on whether the founder family can sustain that breadth of focus.

The competitive context for this brand portfolio is now sharpening, which is where the framework analysis takes us next.

VIII. Playbook: Porter's 5 Forces & 7 Powers Analysis

When हैमिल्टन हेलमर Hamilton Helmer's 7 Powers framework is applied to Vedant Fashions, the dominant powers visible are Branding, Process Power, and Scale Economies — with hints of Cornered Resource and Counter-Positioning at the edges. Let us take each in turn, because the diagnosis matters for whether the moat actually holds against the new entrants.

Branding is the most obvious power and is also the most quantifiable. The Manyavar name has, through twenty years of disciplined marketing and category-defining advertising, become near-synonymous with men's wedding wear in India. When a young Indian man's family begins planning a wedding, "let's go to Manyavar" is the default suggestion, in much the same way "let's Xerox it" became shorthand for photocopying in the 1980s. The economic value of that brand equity is enormous: it lowers customer acquisition cost, supports the no-discount pricing policy, and provides the franchise network with the inbound footfall that justifies their capital outlay. Brand erosion would be the single largest risk to the business, and the company's roughly 8-10% revenue spend on advertising is best understood as the rent the company pays to maintain that brand position.[^12]

Process Power is the less visible but arguably more durable power. The pull-based replenishment system, the franchise governance playbook, the centralised design-to-store cycle, the size-curve algorithms refined over a decade — these are not innovations a competitor can simply replicate by hiring a consultancy. They are accumulated organisational learnings that compound over time, embedded in proprietary IT systems and in the operational habits of a few hundred employees. When the company reports inventory turnover and dead-stock ratios that are dramatically better than industry comparables, that is process power talking.[^15]

Scale Economies operate at two levels. At the procurement level, Vedant Fashions sources from a network of roughly 500-plus independent artisans and small manufacturers, and its volume relative to any individual supplier gives it pricing leverage that no smaller brand can match.[^15] At the marketing level, a national television and cinema advertising campaign costs roughly the same whether you have 100 stores or 600, but the cost per store is dramatically lower at scale, which is why deep-pocketed conglomerate entrants like Aditya Birla and Raymond can match the marketing spend but smaller regional brands cannot. The scale moat protects the bottom of the competitive set; whether it protects against the top is the open question.

Counter-Positioning shows up most clearly in the no-discount policy. A legacy multi-brand retailer that has trained its customers to expect end-of-season sales cannot suddenly stop discounting without alienating its base; Vedant Fashions, having never discounted, is structurally positioned to maintain brand premium in a way incumbents cannot easily copy. Cornered Resource, finally, is harder to claim definitively, but the company's relationships with its artisan and weaver network — built over decades, often spanning multiple generations of the same families — constitute a soft form of supplier exclusivity that is difficult to displace.

Turning to पोर्टर Porter's Five Forces, the analysis is less uniformly favourable but still positive on balance.

Bargaining power of suppliers is low. With 500-plus independent suppliers, no single supplier can dictate terms. The artisanal supply base is so fragmented that the brand sets the price, not the maker.

Bargaining power of buyers is low. The end consumer is a wedding family making a one-off purchase decision; they have no repeat-purchase leverage, no negotiating posture, and they are buying on emotion at least as much as on price. The no-discount policy works precisely because buyers cannot effectively push back.

Threat of substitutes is moderate. The substitute is not another sherwani; it is a designer boutique, a custom tailor, or an online direct-to-consumer brand. None of these have yet aggregated to threaten Manyavar's positioning, but the long tail of substitutes is real, particularly at the upper and lower price ends.

Threat of new entrants is moderate to high — and rising. The barrier to opening a single sherwani store is low; the barrier to building a national brand with 600+ stores and pull-based replenishment is enormous. But the entrants that matter are not single-store operators; they are diversified conglomerates with the capital, the brand-building experience, and the patience to play a multi-year game.

That brings us to industry rivalry, which is intensifying. Aditya Birla Fashion and Retail's entry into the men's ethnic-wear category via तस्वा Tasva — a partnership with designer Tarun Tahiliani launched in 2021-2022 — was the first credible large-cap challenge to Manyavar's positioning.[^17] Tasva opened with a designer brand voice, premium pricing, and the full distribution muscle of the Aditya Birla retail network. Shortly thereafter, Raymond launched Ethnix by Raymond, leveraging its century-old men's wear brand equity into the celebration-wear category, with plans for hundreds of stores over the next several years.[^18]

The competitive question is whether the moat is wide enough to absorb these two simultaneous attacks. The bull case is that the wedding-wear category in India is large enough to support multiple winners, that Manyavar's brand and process advantages are durable, and that the new entrants will struggle to match Vedant's franchise-network depth and pull-based replenishment. The bear case is that conglomerate competitors with deep balance sheets can sustain unprofitable expansion for years, eroding Manyavar's pricing power and forcing a defensive response that hurts the high-ROCE economics. Both are reasonable views, and the next three to five years of same-store-sales data will determine which is closer to right.

That sets the stage for the explicit bull-versus-bear framing.

IX. Analysis: The Bull vs. Bear Case — Myth vs. Reality

Every long-form thesis on a category-defining business eventually has to grapple with the consensus narrative, and Vedant Fashions has accumulated its share of myths over the past five years. So let us start with what the consensus says, and where it might be wrong.

The consensus myth, repeated in nearly every sell-side initiation since the IPO, is that Vedant Fashions is a "wedding-proof, recession-proof, India-consumption story." The reality is more nuanced. The wedding category itself is genuinely resilient — Indian families do not postpone weddings during equity downturns, and wedding spend has historically grown faster than nominal GDP. But Vedant Fashions specifically is a discretionary, premium, branded play within that category, and it is more sensitive to consumer sentiment than the headline narrative suggests. The COVID disruption in fiscal 2021 and the subsequent normalisation provided a real-world stress test, and while the business recovered strongly, the volatility was not trivial.[^19]

The second consensus myth is that the franchise model is purely asset-light and risk-free for the company. The reality is that franchisee economics depend on continued strong same-store sales, and any prolonged softness in store-level traffic could pressure the franchise base and slow new store openings — which in turn slows the company's growth rate. The asset-light model insulates the balance sheet but not the income statement.

With those caveats, the bull case can be stated cleanly. India's nominal "wedding GDP" — the aggregate annual spend on weddings — is in the range of $130 billion and growing at roughly nominal GDP rates, structurally tilted upward by rising household incomes and the gradual organisation of what was an entirely unorganised category a decade ago.[^3] Vedant Fashions has the brand, the operating model, and the management discipline to capture an outsized share of that growth, particularly as the Mohey women's brand continues to scale.

Layer on the international expansion optionality — flagship stores in the United States, the United Arab Emirates, and other diaspora markets where Indian wedding spend per family is multiples of domestic spend — and the addressable market expands further.[^15] Layer on the Manthan value-segment expansion and the Twamev premium-segment expansion, and the brand architecture has runway across three distinct price tiers. None of this requires the company to do anything heroic; it requires the company to execute the playbook it has executed for fifteen years.

The bear case is the mirror image, and it has three distinct legs.

First, couture fatigue. Indian consumer tastes are shifting, slowly but visibly, away from the heavily embellished sherwani-and-lehenga aesthetic of the 2010s toward lighter, more minimalist, more occasion-flexible silhouettes. If that shift accelerates, the Manyavar brand voice — which is unapologetically maximalist — could find itself on the wrong side of fashion. The company has tried to hedge this with Twamev's more contemporary positioning, but the core brand remains anchored in a particular aesthetic moment.

Second, competition from deep-pocketed conglomerates. The simultaneous entry of Tasva and Ethnix is the most credible competitive threat the company has faced since the EBO model was conceived. Both backers can sustain years of unprofitable expansion, which is precisely the strategy that has historically broken category leaders in India. The Manyavar response so far has been to continue executing, accelerate Mohey, and trust the brand premium. Whether that response is sufficient will take three-to-five years to confirm.

Third, brand dilution risk. The portfolio strategy — extending into value (Manthan) and premium (Twamev) and women's (Mohey) — creates synergy opportunities but also creates the risk that the parent Manyavar brand gets pulled in too many directions. Luxury categories are punishing about this; once a brand is associated with the value segment, even tangentially, recovering the premium positioning is enormously difficult. Vedant Fashions has so far been careful to maintain clear separation between the brands, but the temptation to cross-leverage increases as the value brand scales.

The key performance indicators long-term investors should track are short and specific.

First and most important, same-store sales growth (SSG) — particularly in Tier 2 and Tier 3 cities, which is where the next decade of revenue growth has to come from. Sustained mid-to-high single-digit SSG indicates the brand is holding pricing and traffic; deceleration below that level is the early warning that the moat is narrowing.

Second, Mohey contribution to revenue. The market has priced in continued Mohey growth; if the women's brand stalls below 15-20% of revenue contribution, the long-term thesis weakens materially.

Third, inventory days and dead-stock ratios. These are the operating proxies for the pull-based replenishment system. Any deterioration is the early signal that the algorithm is breaking down, which would in turn pressure the no-discount policy.

That is the analytical frame. The story itself ends where it began.

X. Epilogue & Reflections

Twenty-seven years after Sangeeta Modi handed her son ₹10,000 to start a business his father refused to bless, Ravi Modi sits atop a publicly listed business that has made him, on paper, one of India's wealthiest first-generation entrepreneurs.5 The 150-square-foot shop in Bara Bazar is a memory. The 600-plus exclusive brand outlets are the present. The architecture of brands — Manyavar, Mohey, Twamev, Manthan, Mebaz — is the future-option-value the market is still figuring out how to price.

The question this episode opened with — is Vedant Fashions a clothing company or a data and logistics company dressed in silk? — has a more nuanced answer than the framing suggests. It is, at its core, a brand company that uses data and logistics as the operating substrate to protect the brand. Take away the algorithm and the dead stock returns; take away the no-discount policy and the brand premium evaporates; take away the brand premium and the franchisee economics collapse; take away the franchisees and the asset-light advantage disappears. Each layer of the moat reinforces the others, which is what every Acquired episode eventually concludes about every great business: the moat is not a single feature but a flywheel.

What Ravi Modi built is, in the most literal sense, a category. There was no organised men's ethnic-wear category in India in 1999. There is one now, and the dictionary entry for it is the name on the storefront. That alone is a rare entrepreneurial achievement, and it explains why the company has commanded the multiples it has commanded since its public listing.

What remains genuinely uncertain is the next chapter. The conglomerate competitors are real. The women's-wear scaling is still in progress. The international expansion is early. The next generation of Modi family management — Vedant, Shilpi — is still proving itself. Any one of these vectors could go well or badly. Most will go somewhere in between.

For the long-term fundamental investor, the question is not whether Vedant Fashions remains a great business — by every operational metric, it does. The question is whether the price you pay today reflects the optionality you are buying, and whether the moat is wide enough to absorb the next five years of competitive intensity. That is a question this article cannot answer for you. It is a question Ravi Modi has been answering, with a stubbornly consistent set of decisions, since the day he walked out of his father's shop with his mother's ₹10,000 and a registered brand name nobody had heard of.

The emperor of Indian celebration wear is, for now, still wearing the crown.

References

References

-

Ravi Modi: The man behind Manyavar's ₹3,120 crore IPO — Forbes India, 2022-02-04 ↩↩

-

Vedant Fashions: Mastering the Art of Celebration Wear — HDFC Securities Institutional Research ↩↩↩

-

Vedant Fashions: Mastering the Art of Celebration Wear — HDFC Securities Institutional Research ↩

-

Ravi Modi: The man behind Manyavar's ₹3,120 crore IPO — Forbes India, 2022-02-04 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube