Manorama Industries: From Forest Floor to Fortune 500 Tables

I. Introduction & Episode Setup

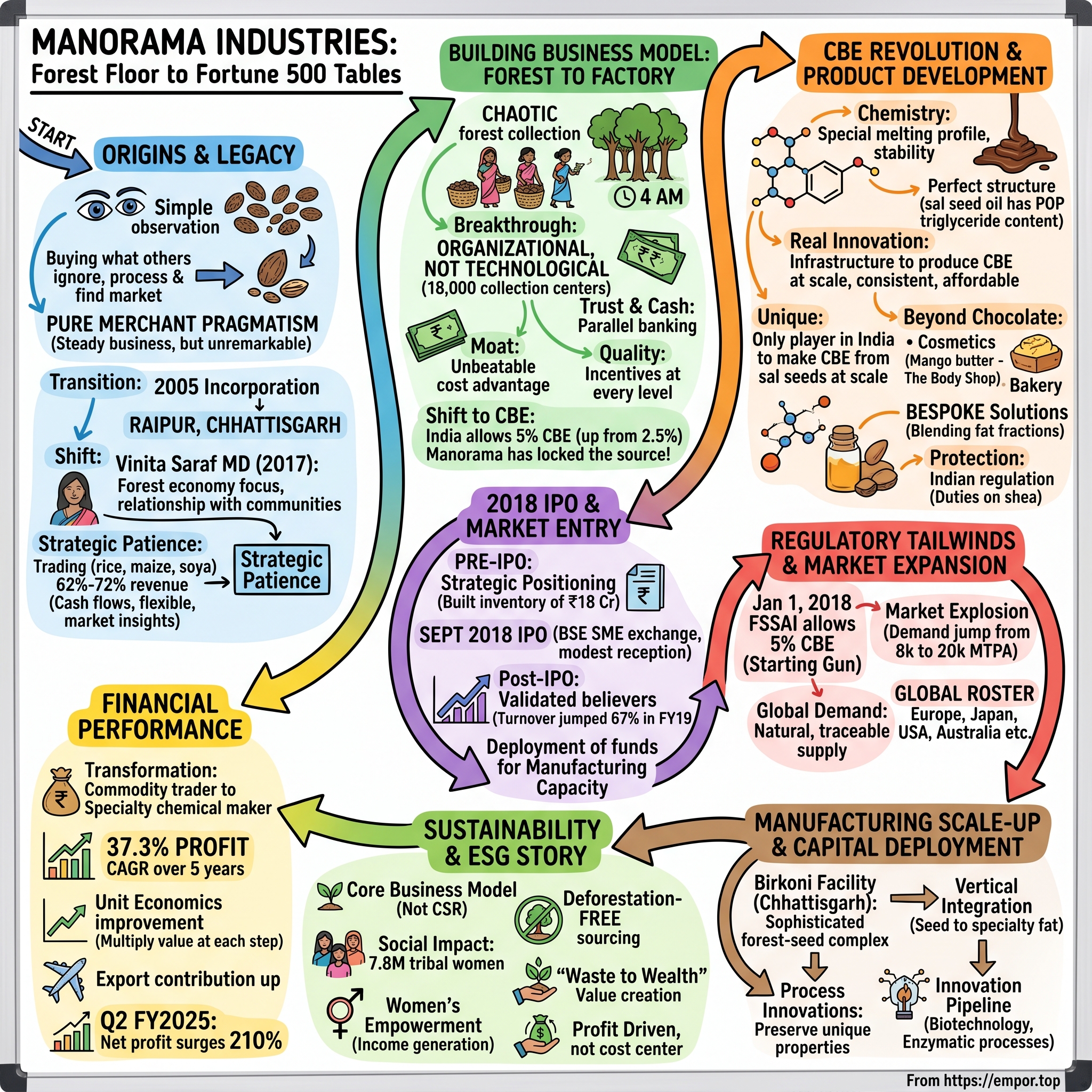

Picture this: Deep in the forests of Chhattisgarh, as dawn breaks through the sal trees, a tribal woman bends down to collect seeds that have fallen overnight. These seeds—dismissed as forest waste for generations—will travel thousands of miles to end up in a Swiss chocolate bar or a luxury cosmetic product in Paris. This is the unlikely story of Manorama Industries, a company that built an ₹8,252 crore empire by seeing value where others saw debris.

"We source from the poor and sell to the rich," the Saraf family likes to say, and the numbers back it up. Their network spans 7.8 million tribal women across India's heartland, collecting what was once considered worthless—sal seeds, mango kernels, kokum butter—and transforming them into specialty fats that command premium prices in global markets. The company's stock has surged 80.4% in the past year alone, but the real story isn't in the price charts. It's in how a small Indian company managed to corner the global market for cocoa butter equivalents (CBE), creating a business model so unique that even multinational giants struggle to replicate it.

The central question driving this episode: How did Manorama Industries build an unassailable moat in what should be a commoditized market? The answer lies at the intersection of forest economics, food chemistry, and perhaps most importantly, the ability to organize one of the world's most dispersed supply chains.

Think about the audacity of the business model for a moment. You're telling investors that your competitive advantage comes from coordinating millions of individual collectors in remote forests, with no formal contracts, no technology infrastructure initially, just trust and cash transactions. You're competing against companies like AAK Kamani and Wilmar International—giants with sophisticated supply chains and deep pockets. And yet, Manorama has become the only Indian company capable of manufacturing CBE from sal seeds at scale.

What makes this story particularly fascinating is the timing. Just as global consumers began demanding sustainable, ethically-sourced ingredients, just as India relaxed regulations on CBE usage in chocolates, just as cosmetic companies started prioritizing natural butters over synthetic alternatives—Manorama was perfectly positioned with a supply chain that had taken decades to build.

This isn't just another commodity trading story dressed up as innovation. It's about recognizing that in India's forest economy, the real goldmine wasn't in the trees themselves but in what fell from them. It's about understanding that "waste to wealth" isn't just a CSR tagline—it's a fundamentally different way of thinking about value creation.

Over the next several hours, we'll trace this journey from forest collection networks to Fortune 500 contracts, from a small Raipur operation to a global specialty fats powerhouse. We'll examine how regulatory changes became catalysts for transformation, how sustainability became a profit driver rather than a cost center, and how a company with roots in traditional trading pivoted to become a technology-driven manufacturer.

But let's start where all great business stories begin—with an origin that seems almost too humble to spawn an empire.

II. Origins & The Manorama Group Legacy

The conference rooms of today's Manorama Industries, with their gleaming presentations about specialty fats and global supply chains, feel worlds away from the company's origins in 1960s India. The Manorama Group began over six decades ago with a simple observation: across the forests of central India, valuable oil-bearing seeds were rotting on the ground while the country imported edible oils.

The group's initial foray into extracting oil from sal seeds and mango kernels wasn't driven by some grand vision of becoming a global CBE supplier—that market didn't even exist then. It was pure merchant pragmatism: buy what others ignore, process it, find a market. For decades, this remained a steady but unremarkable business, the kind of operation that provided good returns but rarely made headlines.

The transformation began in 2005 when Manorama Industries Private Limited was incorporated in Raipur, Chhattisgarh. But the real catalyst for change came in the form of Vinita Saraf, who would later become the face of the company's metamorphosis. At 47, with a Bachelor of Commerce from Bangalore University, Saraf brought something different to what had been a traditional trading operation. When she was designated Managing Director in April 2017, she had already spent over a decade understanding the intricate dynamics of India's forest economy.

What Saraf recognized was that Manorama wasn't really in the oil extraction business—it was in the business of organizing India's informal forest economy. The tribal communities collecting these seeds weren't just suppliers; they were the company's greatest asset. While competitors focused on improving extraction technology or finding cheaper raw materials, Saraf doubled down on deepening relationships with forest communities.

The numbers tell a story of patient empire-building. By the time of its conversion to a public limited company in March 2018, Manorama had quietly assembled one of India's most extensive rural collection networks. But here's what's remarkable: during this entire buildup phase, most of the company's revenue didn't even come from specialty fats. In fiscal years 2016, 2017, and 2018, trading activities—rice, maize, soya doc—generated 62%, 61%, and 72% of business respectively.

To outside observers, this might have looked like a lack of focus. Why was a company supposedly specialized in forest-based oils doing commodity trading? But this was strategic patience at work. The trading business generated the cash flows needed to build the collection infrastructure, establish processing capabilities, and most importantly, maintain relationships with tribal collectors even during lean seasons.

Understanding India's forest economy requires appreciating its unique characteristics. Unlike plantation-based supply chains where you can predict yields and control quality, forest collection is inherently chaotic. Seeds fall when they want to fall. Quality varies by microclimate. Collectors work when they need money, not on corporate schedules. Building a reliable supply chain in this environment isn't about imposing order—it's about embracing and managing chaos.

The vision of converting "waste to wealth" sounds almost clichéd in today's sustainability-obsessed corporate world, but for Manorama, it was operational reality long before it became fashionable. Every sal seed collected represented multiple value transfers: income for a tribal family, raw material for the company, and eventually, a premium ingredient for global brands. The elegance lay in aligning everyone's incentives without formal contracts or legal frameworks.

This foundation—built over decades of patient relationship cultivation, strategic diversification through trading, and deep understanding of forest economics—would prove crucial when the opportunity to dominate the CBE market emerged. But first, the company had to solve one of the most complex operational challenges in Indian business: building a reliable supply chain from millions of independent collectors spread across some of the country's most remote regions.

III. Building the Business Model: Forest to Factory

The logistics nightmare begins at 4 AM. Across the forests of Jharkhand, Odisha, Chhattisgarh, and Madhya Pradesh, millions of women set out with woven baskets, walking miles before the heat becomes unbearable. They're looking for sal seeds—small, oily kernels that look unremarkable but contain the molecular structure that makes them perfect substitutes for cocoa butter. By noon, they'll have collected perhaps 5-10 kilograms, worth maybe ₹100-200. Multiply this scene by 7.8 million collectors, and you begin to understand both the scale and complexity of Manorama's operation.

Building this network didn't happen through some Silicon Valley-style blitzscaling. It took decades of patient expansion, village by village, establishing 18,000 collection centers across India's forest belt. Each center represents a delicate balance of trust, logistics, and economics. Too far apart, and collectors won't make the journey. Too close together, and they cannibalize each other's supply. Pay too little, and collectors sell to competitors. Pay too much, and margins evaporate.

The company's breakthrough wasn't technological—it was organizational. While competitors tried to bypass tribal collectors through mechanization or plantation models, Manorama recognized that the distributed collection model, despite its complexity, created an unbeatable cost advantage. A plantation requires land acquisition, cultivation costs, and years before production. The forest provides free raw material; you just need to organize its collection.

Quality control in this environment seems impossible. How do you ensure consistent quality when your suppliers are millions of individual collectors with no formal training? Manorama's solution was elegant: create quality incentives at every level. Collection centers compete on quality metrics. Supervisors receive bonuses for low rejection rates. Most importantly, the company pays premium prices for better quality, creating a direct incentive for collectors to avoid mixing old seeds with fresh ones or adulterating their baskets with stones for extra weight.

The trust equation is particularly fascinating. These transactions happen entirely in cash, often in areas with limited banking infrastructure. A collection center might handle lakhs of rupees daily during peak season, all in small denominations. The company had to become, in effect, a parallel banking system, moving cash into remote areas and products out. One delayed payment, one bounced promise, and years of relationship-building could unravel.

But here's where the story takes an unexpected turn. In fiscal years 2016 through 2018, while building this elaborate collection infrastructure, the majority of Manorama's revenue came from trading rice, maize, and soya doc—62%, 61%, and 72% respectively. Why would a company investing heavily in forest-based supply chains generate most of its revenue from agricultural commodity trading?

The answer reveals strategic sophistication often missed by casual observers. The trading business served three critical functions. First, it generated steady cash flows to fund the build-out of the forest collection network. Second, it provided operational flexibility—when forest seed availability was low, trading revenues kept the company stable. Third, and perhaps most importantly, it gave Manorama deep insights into commodity markets, pricing dynamics, and global supply chains that would prove invaluable when pivoting to specialty fats.

The pivot from trading to manufacturing specialty fats wasn't sudden—it was methodical. By 2018, the company had assembled all the pieces: a reliable supply chain, processing expertise, and market intelligence. When India announced it would allow 5% CBE in chocolates (up from 2.5%), Manorama was ready. While competitors scrambled to secure supply, Manorama had already locked up the source.

The complexity of managing tribal collection networks extends beyond logistics. It's about understanding seasonal patterns—when sal seeds fall, when collectors need money most, when alternative employment is available. It's about managing political dynamics—working with state forest departments, navigating tribal area regulations, ensuring local political support. It's about social dynamics—respecting traditional collection rights, ensuring equitable distribution of income, managing conflicts between villages.

Initial challenges were numerous and sometimes unexpected. Collectors would sometimes hold back supply hoping for price increases, creating artificial shortages. Middlemen would try to insert themselves into the value chain, adding costs without value. Competing buyers would show up offering marginally higher prices, trying to disrupt established relationships. Each challenge required a nuanced response that balanced immediate business needs with long-term relationship preservation.

The transformation from a trading company with a collection network to a manufacturer of specialty fats represented more than a business model shift—it was a bet that organizing India's informal forest economy could create a sustainable competitive advantage in global markets. That bet was about to pay off in ways even the Saraf family couldn't have fully anticipated.

IV. The CBE Revolution & Product Development

The chemistry lesson that changed everything happened in a food science lab, but its implications would ripple through boardrooms from Hershey to Nestlé. Cocoa butter equivalent isn't just a substitute—it's an improvement. When you blend stearin (70-80%) with palm mid fraction (20-30%), you get a fat with the exact same melting profile as cocoa butter, but with better stability and consistency. For chocolate manufacturers dealing with volatile cocoa prices and inconsistent quality, CBE wasn't just an alternative—it was a solution to decades-old problems.

Understanding the technical breakthrough requires appreciating what makes cocoa butter special. It melts at precisely human body temperature—that's why chocolate has that distinctive melt-in-your-mouth sensation. It crystallizes in specific forms that give chocolate its snap and shine. Replicating these properties isn't just about finding similar fats; it's about understanding triglyceride structures, polymorphic behavior, and crystallization dynamics. Manorama didn't just stumble onto sal seed oil—they recognized that its unique POP (palmitic-oleic-palmitic) triglyceride content made it molecularly perfect for CBE production.

The real innovation wasn't discovering that sal seeds could make CBE—food scientists had known this for years. The breakthrough was building the infrastructure to do it at scale, with consistency, at price points that made economic sense. Global players like AAK might have superior technology, but they couldn't match Manorama's raw material costs. Indian competitors might have processing capabilities, but they lacked the collection network. Manorama sat at the sweet spot where supply chain advantage met technical capability.

Here's what makes Manorama's position nearly unassailable: they're the only player in India with the ability to manufacture CBE from sal seeds at scale, thanks to their procurement strength. A competitor trying to replicate this would need to build relationships with millions of tribal collectors—a process that took Manorama decades. Even if a global giant wanted to enter this market, they'd find themselves bidding against Manorama for the same sal seeds, driving up prices for everyone.

The product applications extend far beyond chocolate bars. In cosmetics, mango butter from Manorama provides superior moisturizing properties compared to synthetic alternatives. The company's supply agreement with The Body Shop—a brand that built its reputation on ethical sourcing and natural ingredients—validates both the quality and sustainability story. In bakery applications, these specialty fats provide better shelf stability and texture. Each application requires different formulations, different quality parameters, different customer education.

The customization capability deserves special attention. CBEs aren't one-size-fits-all. A chocolate manufacturer in Belgium has different requirements than a bakery in Japan. Some prioritize melting point, others crystallization speed, still others focus on oxidative stability. Manorama's ability to blend different fat fractions—sal with mango, kokum with palm—allows them to create bespoke solutions. This isn't commodity trading; it's specialized chemical formulation.

The regulatory environment provided crucial protection. Indian regulations specify that CBE manufacturing is permitted only from Indian sal, mango, and kokum, with high import duties for shea-based fats. This wasn't protectionism—it was recognition that India's forest-based fats had unique properties worth preserving. For Manorama, it created a regulatory moat around their business model.

The technical capabilities required significant investment. Fractionation technology to separate different fat components. Interesterification plants to modify triglyceride structures. Quality control labs that could measure polymorphic forms and predict shelf stability. This wasn't village-level oil extraction anymore—it was sophisticated chemical processing requiring serious capital investment and technical expertise.

But technology alone doesn't explain Manorama's success. The company understood that selling CBE to global food companies required more than good products—it required trust. Food safety certifications, traceability systems, quality assurance protocols—all the boring but essential infrastructure that transforms a commodity supplier into a strategic partner. When a Fortune 500 company puts Manorama's CBE in their products, they're betting their brand reputation on consistent quality.

The knowledge transfer aspect is particularly interesting. Manorama didn't just sell CBE; they educated customers on its applications. They worked with R&D teams to reformulate products. They provided technical support for production challenges. They became consultants as much as suppliers, embedding themselves in customers' product development processes.

The transformation from forest seed collector to specialty chemical manufacturer represents one of the most dramatic value-addition stories in Indian industry. A sal seed worth ₹20 per kilogram becomes CBE worth hundreds of dollars per ton in international markets. But this value creation required mastering every step of a complex chain—from forest floor to laboratory to factory to customer's production line.

As 2018 approached, all these capabilities—supply chain, technology, customer relationships—were about to be tested in the public markets.

V. The 2018 IPO & Market Entry

The numbers seemed almost too good to be true. Just before the IPO in fiscal 2018, Manorama's expense-to-revenue ratio suddenly dropped to 92%, delivering profits that made investors do double-takes. The company had mysteriously accumulated ₹18 crore in inventory. For skeptics, this looked like financial engineering. For insiders, it was strategic positioning for a regulatory windfall they saw coming.

When Manorama Industries opened for IPO bidding on September 21, 2018, it wasn't seeking to join the mainboard giants. This was an SME IPO—34,04,400 equity shares at ₹188 each, raising ₹64 crores. The venue was BSE SME, not the main exchange. For a company claiming to revolutionize specialty fats, the modest ambitions seemed incongruous. Why not go bigger? Why not price higher? The answer lay in the Saraf family's patient approach to value creation—better to under-promise in the IPO than over-hype and disappoint.

The pre-IPO preparation tells its own story. That inventory buildup of ₹18 crore? It was a calculated bet on India opening up CBE usage from 2.5% to 5% in chocolates starting January 2018. While others were waiting for official confirmation, Manorama was stockpiling raw materials. When the regulation changed, they were the only ones with ready inventory to meet sudden demand surge. What looked like speculation was actually informed positioning.

The market's initial reception was lukewarm. This was October 2018—the IL&FS crisis had just exploded, markets were jittery, and an SME IPO from a Chhattisgarh-based company processing forest seeds didn't exactly scream "hot investment." The stock listed on October 4, 2018, to modest volumes and limited analyst attention. The financial press barely noticed. The company that would later command a ₹8,000+ crore market cap began its public journey in relative obscurity.

Pre-IPO performance questions centered on the sudden profitability improvement. How does a company primarily doing commodity trading suddenly become highly profitable? The answer lay in the business mix shift that was already underway but not yet visible in reported numbers. The trading business—rice, maize, soya—was being systematically wound down while specialty fats ramped up. The margin differential was staggering: 3-5% on commodity trading versus 15-20% on specialty fats.

The skepticism was understandable. Manorama's story required believing several things simultaneously: that tribal women could be organized into a reliable supply chain, that forest seeds could compete with plantation crops, that Indian companies could meet global food safety standards, that specialty fats were actually special enough to command premium prices. For investors used to software companies or consumer brands, this forest-to-factory narrative seemed almost fantastical.

But post-IPO transformation validated the believers. Manufacturing turnover jumped 67% to ₹102.87 crore in FY2018-19 from ₹61.33 crore the previous year. More importantly, the revenue mix shifted decisively toward higher-margin specialty fats. The company wasn't just growing—it was transforming its economic model in real-time.

The IPO proceeds deployment revealed strategic priorities. Rather than distribution or marketing, money went into manufacturing capacity—solvent extraction, refining, fractionation. This wasn't about buying growth through sales spending. It was about building technical capabilities that would be hard to replicate. Every rupee spent on manufacturing infrastructure increased the barriers to entry for competitors.

The governance improvements post-IPO were equally important but less visible. Public listing brought scrutiny, which brought discipline. Financial reporting became more transparent. Related party transactions were curtailed. Professional managers were hired. The family-run operation was evolving into an institution, though the Saraf family retained firm control through their shareholding.

What made the IPO particularly interesting in hindsight was its timing. The company went public just as several trends converged: regulatory liberalization of CBE usage, global shift toward sustainable sourcing, rising demand for cocoa butter alternatives due to price volatility, and increasing focus on ESG metrics by institutional investors. Manorama didn't create these trends, but they positioned themselves perfectly to benefit from all of them.

The SME exchange listing served another strategic purpose—it allowed the company to access capital markets while maintaining some flexibility in disclosures and compliance requirements. As the business scaled and matured, migration to the main board would become possible, but starting on SME exchange reduced initial compliance costs and scrutiny pressure.

The validation would come not from stock price movements but from customer acquisitions. Post-IPO, Manorama's client list began reading like a who's who of global FMCG: companies that wouldn't risk their supply chains on an unreliable partner. The public listing provided the credibility boost needed to crack these accounts. The transformation from SME IPO to multi-thousand crore market cap was about to begin, powered by a regulatory change that Manorama had been preparing for all along.

VI. Regulatory Tailwinds & Market Expansion

January 1, 2018, marked a watershed moment disguised as a bureaucratic update. The Food Safety and Standards Authority of India (FSSAI) quietly amended regulations to allow 5% CBE in chocolates, up from the previous 2.5% limit. For most companies, this was a footnote in regulatory filings. For Manorama, it was the starting gun for a transformation they'd been preparing for years.

The numbers tell the story of an industry transformation: CBE consumption in India was projected to leap from 8,000 metric tons per annum in 2018 to over 20,000 MTPA by 2022. That's not growth—that's a market explosion. Every percentage point increase in allowable CBE usage meant chocolate manufacturers could reduce costs by 15-20% without compromising quality. In a price-sensitive market like India, where a five-rupee difference determines purchase decisions, this was revolutionary.

But here's the strategic masterstroke hidden in regulatory fine print: Indian regulations specified that CBE manufacturing must use only Indian sal, mango, and kokum, with prohibitive import duties on shea-based alternatives. While global giants like AAK relied on African shea butter, Manorama had spent decades cornering the Indian forest seed supply. The regulation wasn't just enabling market growth—it was building a wall around Manorama's garden.

The domestic demand surge caught even optimists off guard. Mondelez, Nestlé, Ferrero—every major chocolate brand operating in India suddenly needed reliable CBE supply. They couldn't import it economically due to duties. They couldn't source raw materials without competing against Manorama's established network. The choice became simple: partner with Manorama or figure out how to build a parallel supply chain from scratch.

The global expansion strategy revealed sophisticated market understanding. Rather than trying to compete in African shea-dominated markets, Manorama targeted countries where their Indian forest-based CBE offered differentiation. Japan valued the sustainability story. European buyers appreciated the traceability. American companies liked the supply chain diversification away from West African sources.

The customer roster reads like a diplomatic achievement: Japan, Italy, France, Russia, Malaysia, Indonesia, Singapore, Netherlands, Germany, Sweden, Denmark, UK, USA, Australia. Each market required different certifications, different quality specifications, different relationship-building approaches. The company that started in Chhattisgarh's forests was now navigating international food safety regulations, customs procedures, and currency hedging.

What's particularly clever about the regulatory arbitrage is how it compounds over time. Any new player entering the market faces a 3-4 year waiting period for customer and regulatory approvals. By the time they're approved, Manorama has locked up more supply, expanded capacity, and deepened customer relationships. The first-mover advantage in a regulated market becomes nearly insurmountable.

The sustainability angle added another layer of competitive advantage. As European Union regulations on deforestation-free supply chains tightened, Manorama's model of collecting naturally fallen seeds—requiring zero deforestation—became increasingly valuable. They weren't cutting trees; they were collecting what trees dropped naturally. In an era of supply chain scrutiny, this was marketing gold.

The company's response to regulatory tailwinds showed operational sophistication. Rather than just riding the demand wave, they invested aggressively in quality certifications—ISO, HACCP, SEDEX, RSPO. Each certification opened new markets and customer segments. The tribal women collecting seeds might not know what SEDEX meant, but their livelihoods depended on Manorama maintaining these standards.

The pricing power that emerged from regulatory protection was remarkable. CBE prices moved from commodity-like volatility to specialty chemical stability. Customers couldn't easily switch suppliers, creating sticky relationships. Contract terms improved—longer commitments, better payment terms, volume guarantees. The regulatory framework had transformed a commodity business into a specialty franchise.

International expansion brought unexpected challenges. Different countries had different definitions of CBE, different labeling requirements, different quality parameters. Manorama had to become experts not just in Indian food law but in the regulatory frameworks of dozens of countries. They hired food lawyers, regulatory consultants, certification specialists—building capabilities that would be impossible for smaller competitors to replicate.

The strategic positioning for global markets went beyond just meeting regulations. Manorama began participating in international food ingredient exhibitions, joining global sustainability initiatives, publishing research on forest-based fats. They were transforming from an Indian supplier into a global thought leader on sustainable specialty fats.

By 2020, the regulatory tailwinds had transformed into sustained competitive advantage. The combination of Indian regulatory protection, international sustainability requirements, and growing CBE acceptance had created a perfect storm of opportunity. But capturing this opportunity required massive scaling of manufacturing capabilities—the next chapter in Manorama's evolution.

VII. Manufacturing Scale-Up & Capital Deployment

The Birkoni facility in Chhattisgarh doesn't look like much from the outside—industrial sheds surrounded by rural landscapes. But inside, ₹400 crores of capital investment has created one of the world's most sophisticated forest-seed processing complexes. When it became fully operational in March 2020, just as COVID was shutting down the global economy, Manorama was counter-cyclically expanding capacity while competitors retreated.

The 2022 installations marked a step-change in ambition: a solvent extraction plant with 90,000 MTPA capacity, refinery capacity enhanced from 15,000 to 40,000 MTPA. These aren't just bigger machines—they represent a fundamental shift in process technology. Solvent extraction achieves 95%+ oil recovery versus 60-70% for traditional expelling. That efficiency gain, multiplied across millions of kilograms of seeds, translates directly to competitive advantage.

The May 2023 commissioning revealed even grander ambitions: a new 30,000-tonne refinery accompanied by a 15,000-tonne interesterification plant. Interesterification is where commodity oil becomes specialty fat—rearranging molecular structures to achieve specific melting points, crystallization behaviors, and stability profiles. This technology, typically found in European or American facilities, was now operating in rural Chhattisgarh.

The state-of-the-art fractionation facility, bringing total input capacity to 40,000 tonnes annually, completed the integrated manufacturing puzzle. Fractionation separates fats into components with different melting points—stearin for structure, olein for flow, mid-fractions for specific applications. It's like having a refinery that can produce custom fuels for different engines, except these fuels go into chocolate bars and cosmetics.

The integrated manufacturing approach created multiple competitive moats. Vertical integration from seed to specialty fat meant capturing value at every step. Competitors buying processed oil missed the margins from extraction. Those without fractionation couldn't offer customized products. Those lacking interesterification couldn't match Manorama's product specifications. Each capability multiplied the value of others.

Technology investments went beyond just capacity. Automation reduced labor costs and improved consistency. Quality control labs with gas chromatography and differential scanning calorimetry ensured products met international standards. Enterprise resource planning systems tracked materials from forest collection through final shipment. This wasn't your grandfather's oil mill—it was a 21st-century chemical processing facility.

The process innovations deserve special attention. Manorama developed proprietary techniques for preserving the unique properties of forest-based fats during processing. Traditional refining strips away minor components that provide oxidative stability and nutritional benefits. Manorama's modified processes retained these while still meeting food safety requirements. The result: products that commanded premium prices for both functional and marketing reasons.

Building competitive moats through vertical integration had financial implications beyond just margin capture. It reduced working capital requirements—no need to finance raw material purchases from third parties. It improved supply chain resilience—less dependence on external processors. It enhanced customer confidence—full control from source to delivery.

The capital efficiency metrics reveal sophisticated financial management. Despite massive capacity expansion, asset turns improved. How? By synchronizing capacity additions with confirmed demand, minimizing idle capacity. By locating facilities near raw material sources, reducing transportation costs. By designing flexible plants that could process multiple feedstocks, improving utilization rates.

The timing of capacity additions showed market insight. The 2020 expansion coincided with regulatory liberalization. The 2022 scale-up anticipated post-COVID demand recovery. The 2023 additions positioned for the next growth phase. Each expansion was timed to capture market opportunity without creating excess capacity that would pressure margins.

Human capital investments paralleled physical infrastructure. Chemical engineers from IITs. Food technologists from international programs. Quality specialists with pharmaceutical experience. The company that started with traditional oil extraction knowledge was now building R&D capabilities rivaling multinational competitors.

The innovation pipeline emerging from these facilities extends beyond current products. Research into new forest-based feedstocks. Development of higher-value derivatives. Applications in pharmaceuticals and nutraceuticals. The manufacturing infrastructure wasn't just about meeting today's demand—it was about creating tomorrow's products.

Environmental investments embedded in the manufacturing scale-up paid both regulatory and marketing dividends. Zero liquid discharge systems. Solar power integration. Biomass boilers using agricultural waste. These weren't CSR additions—they reduced operating costs while strengthening the sustainability narrative that premium customers valued.

The return on invested capital from this manufacturing scale-up validated the strategy. While the absolute numbers grew impressively, the efficiency metrics improved even more dramatically. Higher yields, lower processing costs, better product quality, faster time-to-market—each percentage point improvement multiplied across growing volumes to create expanding margins.

By 2024, Manorama's manufacturing footprint had transformed from a single traditional facility to an integrated complex capable of competing globally. But technology and capacity were just enablers. The real competitive advantage lay in how these capabilities supported a larger narrative—one about sustainability, social impact, and the transformation of waste into wealth.

VIII. Sustainability & ESG Story

The United Nations Global Compact signature sits prominently in Manorama's corporate presentations, but the real sustainability story predates any formal ESG framework by decades. When 7.8 million tribal women collect forest seeds for Manorama, they're not participating in a corporate social responsibility program—they're the core business model. This isn't sustainability as marketing veneer; it's sustainability as competitive advantage.

The social impact metrics stagger in their scope. Each collector earns ₹3,000-5,000 during the collection season—supplementary income that funds children's education, medical emergencies, and household improvements. Multiply that by 7.8 million participants, and you're looking at one of India's largest informal employment programs. No government scheme reaches this deep into forest communities with this consistency.

The "Waste to Wealth" model creates value loops that traditional supply chains can't match. Seeds that would decompose on forest floors become industrial inputs. Tribal communities gain income without depleting forest resources. Chocolate manufacturers get sustainable ingredients without deforestation. Consumers get products with authentic sustainability stories. Everyone wins because the incentives align naturally, not through forced compliance.

The environmental benefits compound at scale. Zero deforestation—seeds are collected, not cultivated. Carbon sequestration continues in standing forests. Biodiversity preservation through economic value creation for forest communities. Water conservation compared to plantation agriculture. These aren't offset programs or carbon credits—they're inherent to the business model.

Global Fortune 500 companies don't partner with suppliers for charity. When Unilever, Nestlé, or The Body Shop sign long-term contracts with Manorama, they're buying supply chain security, regulatory compliance, and brand protection. Consumer preference for sustainable products isn't sentiment—it's purchasing power. Brands that can't demonstrate sustainable sourcing lose market share to those that can.

The transparency requirements from global customers forced operational improvements that became competitive advantages. Traceability systems that track seeds from specific forest areas to final products. Fair trade certifications that ensure equitable value distribution. Gender impact assessments showing women's economic empowerment. What started as customer requirements became differentiators that competitors couldn't match.

The tribal empowerment angle deserves deeper examination. These aren't employees with contracts and benefits. They're micro-entrepreneurs who choose when and how much to collect. This flexibility is crucial for communities with seasonal agricultural obligations, cultural festivals, and family responsibilities. Manorama's model works because it adapts to tribal life patterns rather than forcing communities to adapt to corporate schedules.

Building trust with global brands through sustainability required more than certifications. It meant hosting customer visits to collection centers, facilitating direct interaction between brand representatives and tribal collectors, documenting impact through third-party assessments. When a European cosmetics executive sees tribal women explaining how seed collection funded their daughters' college education, that story becomes part of the brand narrative.

The ESG metrics that institutional investors now scrutinize were baked into Manorama's model from inception. Environmental scores excel through zero-deforestation sourcing. Social scores benefit from massive employment generation. Governance scores improve through transparent supply chain management. The company didn't pivot to ESG—ESG frameworks finally caught up to what Manorama was already doing.

The United Nations Sustainable Development Goals alignment isn't forced—it's natural. SDG 1 (No Poverty) through income generation. SDG 5 (Gender Equality) through women's economic empowerment. SDG 8 (Decent Work) through ethical sourcing. SDG 12 (Responsible Consumption) through waste utilization. SDG 15 (Life on Land) through forest preservation. Academic case studies could be written on each alignment.

Consumer awareness evolution transformed sustainability from cost to revenue driver. Premium pricing for sustainable ingredients more than offset certification costs. Customer loyalty increased with sustainability storytelling. New market segments opened for natural and ethical products. The same consumers driving demand for organic food and electric vehicles valued forest-based ingredients over synthetic alternatives.

The risk mitigation aspect of sustainability often goes unappreciated. Climate change threatens agricultural supply chains, but forest ecosystems are more resilient. Regulatory scrutiny on labor practices intensifies, but Manorama's model empowers rather than exploits. Consumer activism targets unsustainable practices, but Manorama's story invites celebration rather than criticism.

The institutional investor interest sparked by strong ESG credentials translated into valuation premiums. ESG funds that couldn't invest in traditional commodity processors could invest in Manorama. Impact investors seeking measurable social returns found a perfect fit. The sustainability story didn't just help operations—it expanded the investor base and reduced capital costs.

By making sustainability profitable rather than sacrificial, Manorama solved the fundamental tension in corporate ESG initiatives. They proved that environmental protection and social development could drive financial returns rather than diminish them. This wasn't about choosing between profit and purpose—it was about recognizing that in certain business models, they're the same thing.

IX. Financial Performance & Unit Economics

The transformation from commodity trader to specialty chemical manufacturer shows up starkly in the numbers. That 67% manufacturing turnover jump to ₹102.87 crore in FY2018-19 was just the opening act. By fiscal 2024, revenues had reached ₹927 crore with profits of ₹149 crore—a 37.3% profit CAGR over five years that would make software companies envious.

But raw growth numbers don't tell the real story. The margin expansion through value addition transformed the unit economics entirely. Consider the journey of a kilogram of sal seeds: purchased from tribal collectors at ₹20-30, processed into crude oil worth ₹80-100, refined into specialty fat worth ₹150-200, formulated into CBE worth ₹300-400. Each processing step doesn't just add cost—it multiplies value.

The working capital dynamics reveal operational sophistication beneath the growth headlines. In commodity trading, working capital turns maybe 4-5 times annually. In specialty fats, despite longer processing times, Manorama achieves 6-7 turns through careful synchronization of collection, processing, and delivery cycles. They've essentially created a just-in-time supply chain from millions of forest collectors—a feat that shouldn't be possible.

The projected revenues of ₹675-700 crore for fiscal 2025 seemed conservative when announced, but they reflect management's preference for under-promising rather than hockey-stick projections. What's more interesting is the revenue mix evolution—specialty fats now dominate, export contribution has increased, and customer concentration has actually decreased despite adding Fortune 500 clients. The recent Q2 FY2025 results validate the trajectory: revenue jumped 65.99% year-over-year to ₹198.90 crore, while net profit surged 210.22% to ₹26.71 crore. Even more impressive, net profit margins expanded to 13.43%—in a business that started as commodity trading with 3-5% margins.

The cash flow dynamics reveal both opportunity and challenge. The massive inventory buildup before regulatory changes, while strategically brilliant, stressed working capital. Debtor days increased from 36.8 to 48.2 days, reflecting the shift toward larger corporate customers with longer payment terms. But this is the price of moving upmarket—Fortune 500 companies pay slowly but surely.

The capital allocation strategy shows discipline. Rather than chasing growth through acquisitions or unrelated diversification, management focused on deepening competitive moats. Every rupee of retained earnings went toward capacity expansion, technology upgrades, or working capital to support organic growth. No vanity projects, no conglomerate ambitions—just relentless focus on specialty fats.

The unit economics improvement comes from multiple vectors. Raw material costs benefit from direct sourcing. Processing costs decline with scale. Product mix shifts toward higher-value formulations. Customer acquisition costs amortize over longer relationships. Each improvement might be small—1-2% here, 2-3% there—but compounded over years, they transform the business model.

What's particularly noteworthy is margin stability despite raw material volatility. Sal seed prices fluctuate with weather patterns and collection dynamics. Palm oil prices swing with global commodity cycles. Yet Manorama maintains relatively stable margins through formula-based pricing contracts, inventory management, and product mix optimization.

The return ratios tell the story of capital efficiency. ROE and ROCE stood at 21.3% and 28.9% respectively as of September 2024—numbers that would be respectable for an asset-light business, remarkable for a manufacturing company with significant fixed assets. This isn't financial engineering—it's operational excellence translating to superior returns.

Looking ahead, management targets revenue of INR 1,050 crores for FY26, implying continued strong growth but at a more sustainable pace. The focus seems to be shifting from pure growth to profitable growth—expanding margins while scaling revenues, improving capital efficiency while building capacity.

The stock market has noticed. Trading at 54.2 times earnings and 17.9 times book value, Manorama commands valuation multiples typically reserved for technology companies or consumer brands. Whether these multiples are justified depends on one's view of the sustainability of growth, the durability of competitive advantages, and the scalability of the business model.

The financial transformation from commodity trader to specialty chemical manufacturer is complete. What started as a traditional business with commodity economics now displays the financial characteristics of a differentiated industrial franchise. The question for investors isn't whether this transformation is real—the numbers confirm it is. The question is whether it can continue.

X. Competitive Landscape & Market Dynamics

The global specialty fats market reads like a David and Goliath story, except David is winning. The CBE market, valued at USD 1450.46 million in 2020 and projected to reach USD 1805.62 million by 2028, is dominated by giants like AAK Kamani, Wilmar International, and Fuji Oil. Yet Manorama, with its forest-based supply chain, has carved out a position these behemoths struggle to attack.

AAK Kamani brings Swedish efficiency and global scale, but their shea-based supply chain from West Africa faces increasing scrutiny over labor practices and deforestation. Wilmar International leverages massive palm oil operations across Southeast Asia, but palm's environmental baggage limits premium market access. Fuji Oil's technological sophistication leads in certain applications, but their cost structure can't match Manorama's forest-collection economics.

The competitive dynamics reveal an interesting paradox. The specialty fats and butter market is expected to reach $142.1 billion by 2026, with APAC alone contributing $36.8 billion. In a market this large, you'd expect intense competition and commoditization. Instead, we see increasing differentiation based on source, sustainability, and specialization. Manorama's forest-based fats occupy a unique position—natural, sustainable, traceable—that synthetic alternatives or plantation-based products can't replicate.

The barriers to entry compound over time. Any new player entering the market faces a 3-4 year waiting period for obtaining customer and regulatory approvals. But approvals are just the beginning. Building collection networks takes decades. Establishing customer trust requires consistent quality over years. Developing application expertise needs repeated iteration with client R&D teams. By the time a new entrant is ready to compete, established players have moved further ahead.

India's unique positioning in the global CBE market stems from regulatory protection and natural advantages. The country's vast forest reserves, large tribal population, and specific tree species create natural moats. Unlike palm oil or cocoa, which can be planted anywhere tropical, sal trees grow only in specific Indian forests. You can't relocate this supply chain to Vietnam or Africa for cheaper labor—the trees won't grow there.

The customer dynamics further reinforce competitive positions. Large food manufacturers won't risk supply chain disruption by frequently switching suppliers. Qualifying a new CBE supplier requires extensive testing—shelf life studies, production trials, consumer panels. Once a supplier is integrated into product formulations and production processes, switching costs become prohibitive unless there are quality issues or supply failures.

Technology disruption seems limited in this sector. While synthetic biology might eventually produce CBE-like compounds, consumer preference trends toward natural ingredients. Precision fermentation could theoretically produce specific fat molecules, but the economics don't work at commodity prices. The most likely disruption would come from alternative chocolate formulations that don't require CBE at all—but chocolate has remained remarkably consistent for centuries.

The competitive landscape varies significantly by geography. In India, Manorama dominates due to regulatory advantages and supply chain control. In Southeast Asia, they compete with palm-based alternatives but win on sustainability credentials. In Europe and America, the competition centers on specialty applications where customization and service matter more than price. Each market requires different competitive strategies.

Pricing dynamics in specialty fats differ from true commodities. While base prices track raw material costs, premiums for specific formulations, certifications, and service levels create differentiation. Manorama's ability to customize CBE for specific chocolate types or cosmetic applications allows premium pricing that commodity suppliers can't achieve. It's the difference between selling crude oil and selling specialized lubricants.

The consolidation trends in the industry favor established players. Smaller specialty fat producers struggle with the capital requirements for modern processing facilities and the relationship investments needed for global customers. Larger players seek acquisitions for technology or market access rather than capacity. Manorama sits in the sweet spot—large enough to compete globally, focused enough to maintain competitive advantages.

Substitution threats exist but remain manageable. Cocoa butter itself competes with CBE, but price volatility makes it unreliable for mass-market products. Other vegetable fats could theoretically substitute, but they lack the specific properties that make CBE valuable. The real substitution threat would come from changing consumer preferences—if chocolate consumption declined or consumers rejected any cocoa alternatives—but these trends show no signs of materializing.

The competitive intensity varies by product segment. In commodity CBE for mass-market chocolates, price matters most. In specialty formulations for premium chocolates, quality and consistency dominate. In cosmetic applications, sustainability and marketing story drive decisions. Manorama's portfolio spans all segments, but their competitive advantages are strongest in specialty and sustainable applications.

XI. Growth Strategy & Future Roadmap

The ambition is clear but calculated: become a leading player in the CBE and specialty fats market globally. But unlike the grand pronouncements typical of corporate vision statements, Manorama's growth strategy builds methodically on existing advantages rather than chasing new horizons. The roadmap reveals a company that understands the difference between growth and sustainable growth.

The B2C entry plans represent the most significant strategic pivot since the IPO. Management plans to enter the Indian B2C segment and is currently developing a range of new products. This isn't about competing with Amul or Britannia in mass-market products. It's about leveraging the sustainability story and forest-sourced credentials to create premium positioned products for increasingly conscious consumers. Imagine artisanal chocolates highlighting sal seed content, or cosmetics featuring "forest-to-face" mango butter.

Geographic expansion follows a targeted approach rather than spray-and-pray internationalization. During FY2024-25, Manorama incorporated six new subsidiaries—five in Africa and one in UAE. The African subsidiaries will strengthen sourcing of shea seeds, while Manorama Mena Trading LLC aims to tap customers from the MENA region. Each expansion addresses specific strategic needs: Africa for raw material diversification, Middle East for market access to premium confectionery manufacturers.

The product portfolio diversification extends beyond current categories. The worldwide cosmetics market, valued at USD 380.2 billion in 2019 and expected to reach USD 463.5 billion by 2027, offers massive expansion potential. But rather than trying to compete across all cosmetic ingredients, Manorama focuses on applications where forest-based butters provide genuine differentiation—anti-aging creams, natural moisturizers, sustainable sun care products.

The vertical integration strategy continues deepening. Beyond just processing seeds into oils, the company explores higher-value derivatives. Fractionation creates specialized components. Interesterification produces designer fats. The next frontier involves biotechnology—using enzymatic processes to create novel fat structures that command pharmaceutical-grade prices. Each step up the value chain multiplies margins while leveraging the same raw material base.

Technology investments focus on differentiation rather than just efficiency. While automation reduces costs, the real investments go toward capabilities competitors can't easily replicate. Analytical laboratories that can characterize fat structures at molecular levels. Pilot plants that can rapidly prototype customer-specific formulations. Application development centers that work directly with customer R&D teams. These investments create switching costs and deepen customer relationships.

The sustainability leadership positioning becomes increasingly valuable as regulations tighten globally. The European Union's deforestation-free supply chain requirements, set to be fully implemented by 2025, turn Manorama's forest collection model from nice-to-have to must-have for European customers. Similar regulations in development in the US and other markets will further advantage sustainable suppliers over the next decade.

Market development initiatives extend beyond just selling products. Manorama invests in educating markets about forest-based fats—sponsoring research, participating in industry conferences, publishing white papers. They're not just suppliers but thought leaders in sustainable specialty fats. This positions them to shape industry standards and customer specifications in ways that advantage their unique supply chain.

The partnership strategy reveals sophisticated thinking about growth. Rather than competing with everyone, Manorama seeks complementary partnerships. Technology partnerships for processing innovations. Distribution partnerships for new geographic markets. Application partnerships for product development. Even potential partnerships with competitors where Manorama's forest-based fats could complement plantation-based products in blended formulations.

Risk management becomes more crucial as the company scales. Geographic diversification reduces dependence on Indian forests. Product diversification reduces exposure to any single application. Customer diversification prevents concentration risk. But the core risk—dependence on forest ecosystems and tribal collectors—remains deliberately unhedged because it's also the core competitive advantage.

The capacity expansion plans align with anticipated demand rather than speculative growth. Each new facility or production line ties to specific customer commitments or market developments. This disciplined approach prevents the excess capacity that plagued many Indian manufacturers who expanded aggressively during boom periods only to face utilization challenges during downturns.

The innovation pipeline suggests sustained growth potential beyond current products. Research into new forest-based feedstocks could unlock entirely new product categories. Development of sustainable alternatives to other industrial fats could expand addressable markets. Applications in emerging categories like plant-based foods or sustainable packaging could create new growth vectors.

The financial targets remain achievable rather than aspirational. Revenue goals tie to capacity additions and confirmed customer pipelines. Margin targets reflect realistic efficiency improvements rather than heroic assumptions. The management team that transformed a trading business into a specialty manufacturer has credibility, but they maintain the conservatism that got them here.

XII. Investment Thesis & Risk Analysis

The bull case for Manorama rests on multiple reinforcing pillars that create a compelling investment narrative. The regulatory moats run deeper than simple government protection—they reflect genuine competitive advantages that regulations merely recognize. India's requirement that CBE use only domestic forest seeds isn't arbitrary protectionism; it acknowledges that sal seed CBE has unique properties that shea or palm-based alternatives can't match. As global food regulations increasingly demand traceability and sustainability, Manorama's forest-to-factory model becomes a compliance advantage, not burden.

The procurement advantages compound over time rather than erode. While technology typically democratizes supply chains, Manorama's model does the opposite. Building relationships with 7.8 million tribal collectors can't be digitized or accelerated with venture capital. A competitor with unlimited funding would still need decades to replicate the trust networks, collection infrastructure, and logistics capabilities. This isn't a software platform where network effects can be rapidly scaled—it's a physical network built through patient, grassroots relationship cultivation.

Growing global demand for sustainable alternatives isn't just ESG theater—it's consumer-driven and regulation-enforced reality. The European chocolate market increasingly demands deforestation-free ingredients. American cosmetic brands seek natural alternatives to synthetic ingredients. Asian confectioners want stable alternatives to volatile cocoa prices. Manorama sits at the intersection of all these trends, offering products that satisfy sustainability mandates while delivering functional benefits.

The customer relationships with Fortune 500 companies provide both validation and stickiness. When Unilever or Nestlé qualifies a supplier, they're not just checking boxes—they're embedding that supplier into complex global supply chains. Product reformulations, quality specifications, audit protocols—all create switching costs that protect incumbent suppliers. These aren't transactional relationships but strategic partnerships that deepen over time.

Margin expansion through value addition has multiple innings left to play. The evolution from commodity trading (3-5% margins) to specialty fats (15-20% margins) to custom formulations (25-30% margins) shows a clear trajectory. Future opportunities in pharmaceutical-grade fats, nutraceutical applications, or proprietary formulations could push margins even higher. Each step requires more technology and expertise, creating higher barriers to competition.

But the bear case deserves equal consideration. The dependence on forest collection creates existential climate risk. Changing rainfall patterns affect seed production. Rising temperatures shift forest ecosystems. Extreme weather events disrupt collection activities. While forest ecosystems show more resilience than monoculture plantations, they're not immune to climate change. A multi-year drought or unseasonable weather pattern could severely impact raw material availability.

Single geography concentration in India, despite recent international expansion, remains concerning. Over 80% of operations depend on Indian forests, Indian regulations, and Indian tribal communities. Political instability, regulatory changes, or social unrest in tribal areas could disrupt operations. The company's international subsidiaries provide some diversification, but core operations remain India-centric.

Competition from synthetic alternatives poses a long-term threat. While current consumer preferences favor natural ingredients, technology advances could produce synthetic fats indistinguishable from natural ones at lower costs. Precision fermentation, cellular agriculture, or other emerging technologies could eventually disrupt plant-based specialty fats. The timeline remains uncertain, but the threat is real.

Raw material price volatility can squeeze margins despite formula-based pricing. Sal seed prices depend on forest production, which varies with natural cycles. Competition for collection from other uses (traditional medicines, local consumption) can spike prices. While Manorama has pricing power with customers, sudden raw material cost increases can create temporary margin pressure before price adjustments flow through.

The valuation at 54.2 times earnings and 17.9 times book value prices in perfect execution. Any operational hiccup, customer loss, or margin compression could trigger significant multiple compression. The stock has already captured much of the transformation story—future returns require continued exceptional performance rather than just improvement from a low base.

Regulatory changes could eliminate competitive advantages. If India liberalized CBE imports or allowed synthetic alternatives, Manorama's moat would narrow significantly. While current political economy suggests continued protection for forest-based industries that support tribal employment, policies can change with governments.

The key person risk around the Saraf family management remains material. While professional managers have been added, strategic decisions still center on family leadership. Succession planning, while presumably in place, hasn't been tested. The transformation from trading to manufacturing succeeded under current leadership—whether next-generation leadership can navigate future challenges remains unknown.

Working capital intensity could pressure cash flows during growth phases. Debtor days have already increased from 36.8 to 48.2 days as corporate customers replaced traders. Further growth, especially in international markets with longer payment terms, could strain working capital. While profitable growth eventually generates cash, the intermediate period requires careful financial management.

Technology disruption in end markets poses indirect risks. If chocolate consumption declined due to health concerns, or if cosmetics shifted away from butter-based formulations, demand for CBE could shrink. While these seem unlikely near-term, consumer preferences can shift rapidly, as seen in other food categories.

XIII. Lessons & Takeaways

The Manorama story offers profound lessons about building sustainable competitive advantages in seemingly commoditized markets. The first insight challenges conventional strategy wisdom: sometimes the most powerful moat isn't technology or capital but patient relationship-building in complex, informal ecosystems. While competitors focused on plantation efficiency or processing technology, Manorama recognized that organizing India's forest economy—messy, informal, and chaotic as it was—created an unreplicable advantage.

The power of community-based supply chains extends beyond cost advantages. When 7.8 million tribal women depend on your business for supplementary income, you've created a constituency that transcends supplier relationships. Politicians protect you because you provide employment. NGOs support you because you empower marginalized communities. Customers embrace you because your story resonates with consumers. This social capital, built over decades, proves more durable than technological advantages that can be disrupted or regulatory protections that can be withdrawn.

Converting ESG from cost center to profit driver requires authentic integration, not retrofitted initiatives. Manorama didn't adopt sustainability because consultants recommended it or investors demanded it—their entire business model depends on forest preservation and tribal welfare. When sustainability is operational necessity rather than marketing veneer, it creates genuine differentiation that competitors can't replicate through certifications or offset programs.

Timing regulatory changes for business transformation separates winners from also-rans. Manorama's pre-positioning for the 5% CBE allowance—building inventory, expanding capacity, qualifying customers—turned a regulatory update into a catapult for growth. They understood that regulations don't just happen; they emerge from years of industry lobbying, technical committees, and pilot programs. Companies that engage in this process can anticipate and prepare for changes rather than react to them.

The importance of patient capital in deep-tech food innovation cannot be overstated. Manorama's transformation from trader to specialty chemical manufacturer took over a decade. The technology investments, customer qualifications, and supply chain development required sustained investment with uncertain returns. Quarterly earnings pressure would have killed this transformation. The family ownership structure, while creating other risks, provided the patient capital necessary for fundamental business model change.

Creating global brands from emerging markets requires solving the trust equation. Indian companies often struggle to break into global supply chains, dismissed as low-cost but low-quality suppliers. Manorama overcame this through relentless focus on certifications, quality systems, and customer service. They didn't try to be cheaper than competitors—they aimed to be better in specific dimensions that mattered to premium customers.

The value of vertical integration depends on industry structure and competitive dynamics. In fragmented industries with volatile supply chains and differentiated products, vertical integration creates competitive advantages. Manorama's control from forest collection through final formulation allows margin capture, quality control, and supply security that non-integrated competitors can't match.

Building defensible positions in commodity markets requires finding non-commoditizable elements. While fats might seem like ultimate commodities, Manorama identified multiple differentiation points: source (forest vs. plantation), sustainability (natural collection vs. cultivation), story (tribal empowerment vs. industrial agriculture), and customization (formulation capabilities vs. standard products). The lesson: even in commodity markets, creative positioning can create premium segments.

The importance of indigenous knowledge and local expertise in global competition deserves recognition. Manorama's understanding of forest ecosystems, tribal collection patterns, and traditional processing methods—knowledge accumulated over generations—proved more valuable than imported technology or international consultants. Global competitiveness doesn't always require global best practices; sometimes local expertise provides unique advantages.

Scaling informal economies requires different management approaches than scaling formal businesses. You can't manage millions of tribal collectors like factory employees. Manorama succeeded by adapting to existing social structures rather than imposing corporate hierarchies. They worked with traditional collection rights, seasonal patterns, and social networks. The lesson: when scaling informal economies, flexibility and adaptation beat standardization and control.

The role of business in development extends beyond CSR to fundamental business model design. Manorama demonstrates that profitable businesses can be built on empowering marginalized communities. This isn't about charity or development projects—it's about recognizing that underserved populations represent not just moral obligations but business opportunities if approached with respect and patience.

Finally, the Manorama story illustrates that transformation is possible even for traditional businesses in seemingly stagnant industries. A company that spent decades as an unremarkable commodity trader transformed into a global specialty chemical player. The key wasn't revolutionary technology or massive capital but clear vision, patient execution, and the wisdom to build on existing strengths rather than abandon them for fashionable new strategies.

These lessons extend beyond Manorama or even the specialty fats industry. They apply to any business trying to build sustainable competitive advantages in an increasingly complex, regulated, and sustainability-conscious global economy. The path from forest floor to Fortune 500 tables wasn't just about processing seeds into specialty fats—it was about recognizing value where others saw waste, building trust where others saw transaction costs, and creating shared prosperity where others saw zero-sum competition.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube