Maharashtra Seamless: The Steel Pipe Dynasty of India

I. Introduction & Episode Setup

The year is 1987. India's oil and gas sector is booming, refineries are expanding, and power plants are mushrooming across the subcontinent. Yet there's a problem nobody talks about at industry conferences: nearly every high-grade seamless pipe—the critical arteries carrying oil, gas, and steam under extreme pressure—is imported. Ships from Japan, Germany, and Italy dock at Mumbai and Chennai ports, offloading millions of dollars worth of steel tubes that Indian industry desperately needs but cannot produce. Into this gap steps D.P. Jindal, a man who built his fortune making welded pipes and now sees an opportunity that others dismiss as too technically complex, too capital-intensive, too risky.

Maharashtra Seamless Limited today stands as India's largest manufacturer of seamless and ERW pipes, commanding a market capitalization of ₹8,758 crore with annual revenues touching ₹5,263 crore. The company produces pipes ranging from 1 inch to a staggering 20 inches in diameter—a feat no other Indian manufacturer has achieved. With promoters holding 68.9% stake and the company maintaining an almost debt-free status in a notoriously capital-intensive industry, this is a story that defies conventional wisdom about commodity businesses.

The central question that drives this narrative: How did a company that entered the seamless pipe business in the late 1980s—decades after global giants had established dominance—become India's only manufacturer of large-diameter seamless pipes? And perhaps more intriguingly, how did they build this empire while maintaining financial discipline that would make even software companies envious?

This is not just a story about steel and industrial machinery. It's about timing market transitions, the patient accumulation of technical capabilities, and the peculiar dynamics of Indian family capitalism. It's about how import substitution—that much-maligned economic policy of the License Raj era—created pockets of opportunity for those bold enough to seize them. And it's about how a company in the unglamorous business of making pipes built competitive moats that have lasted three decades.

As we trace Maharashtra Seamless's journey from a greenfield project in Nagothane to a pan-India manufacturing powerhouse with operations spanning renewable energy and offshore drilling, we'll uncover lessons about capital allocation, technology transfer, and the art of competing in cyclical industries. The D.P. Jindal Group's approach—methodical, technically focused, financially conservative—offers a masterclass in building industrial enterprises in emerging markets. Let's begin where all great business stories begin: with the founder's vision.

II. The D.P. Jindal Legacy & Group Origins

The morning sun catches the gleam of freshly rolled steel pipes at the Howrah factory in 1952. Bhavi Chand Jindal, having arrived from rural Haryana just years earlier with his brothers, watches as India's first indigenously manufactured steel pipes emerge from the production line. The Jindal family embarked into business activity in 1952, with their first venture, Jindal India Ltd., set up in Howrah, becoming the first and foremost manufacturers of steel pipes and tubes in India. This wasn't just another industrial venture—it was a declaration that India could build its own industrial infrastructure without depending on colonial-era suppliers.

But our story centers on a different branch of this industrial family tree. While B.C. Jindal and O.P. Jindal would go on to build their separate empires (the confusion between the various Jindal groups remains a favorite topic at Mumbai business dinners), it was D.P. Jindal who would forge a distinctly different path—one focused on technical excellence and patient capital deployment rather than rapid diversification.

D.P. Jindal is presently the Chairman of Jindal Pipes Limited, Maharashtra Seamless Limited and Jindal Drilling & Industries Limited, with varied and vast experience in all the Group companies. His leadership style earned him a peculiar moniker: "Always on the move" industrialist—though those who worked with him knew this meant methodical progression rather than restless expansion.

The D.P. Jindal Group's evolution tells a story of calculated vertical integration. After establishing lead and consolidating their position in steel pipes/tubes, they diversified into tea plantation in 1980, casing pipes in 1987, offshore oil drilling in 1989 and seamless pipes in 1992. Each move wasn't random—tea plantations provided stable cash flows during steel downturns, casing pipes leveraged existing customer relationships, offshore drilling created captive demand for their pipes, and seamless pipes represented the technical pinnacle of their manufacturing ambitions.

D.P. Jindal's achievements include indigenous development of tube welder (200 kW capacity) and establishing first state-of-art seamless manufacturing facility in India, also responsible for having generated largest tube manufacturing capacity in the country. This technical focus wasn't accidental. While competitors chased market share through acquisitions, D.P. Jindal obsessed over manufacturing processes, spending hours on factory floors discussing welding temperatures and steel metallurgy with engineers.

The group's philosophy crystallized around four principles that would guide every major decision: perseverance and hard work resulting in a job universally recognised as having been well done, with ingenuity and innovation as parameters of progress, enhancing customers' satisfaction through products of superior quality with endearing service. These weren't just corporate platitudes—they became operational doctrine.

Family dynamics played a crucial role in shaping the group's trajectory. D.P. Jindal brought his sons Saket and Raghav into the business early, but unlike the public succession battles that plagued other Indian business houses, the transition was methodical. Saket focused on operations and technology, while Raghav handled finance and strategy. The division wasn't rigid—both brothers regularly crossed into each other's domains—but it created accountability without rivalry.

The group's social compact extended beyond family. Philanthropic activities include running a free-medical aid dispensary, an English medium higher secondary school, and generous donations for betterment of society, with Jindal always eager to provide further development in the life style and career development of his people. This wasn't mere corporate social responsibility—it was recognition that industrial success in India required community buy-in, especially when setting up capital-intensive projects in rural Maharashtra.

By the mid-1980s, the D.P. Jindal Group had established itself as a reliable, technically competent player in the welded pipes segment. But D.P. Jindal saw a larger opportunity emerging. India's ambitious oil and gas exploration programs, coupled with massive power plant construction, created demand for seamless pipes—products that could withstand pressures and temperatures that would destroy ordinary welded pipes. The technology to make these pipes existed in only a handful of companies worldwide, primarily in Germany, Japan, and Italy. The capital requirements were staggering, the technical complexity daunting, and the market risk substantial given that established importers had locked up most major customers.

Yet D.P. Jindal saw what others missed: India's foreign exchange crisis of the late 1980s would eventually force the government to support import substitution in critical industries. The question wasn't whether India would need domestic seamless pipe manufacturing—it was who would have the technical capability and financial staying power to capture this market when it emerged. The stage was set for Maharashtra Seamless's birth.

III. Birth of Maharashtra Seamless (1988-1992)

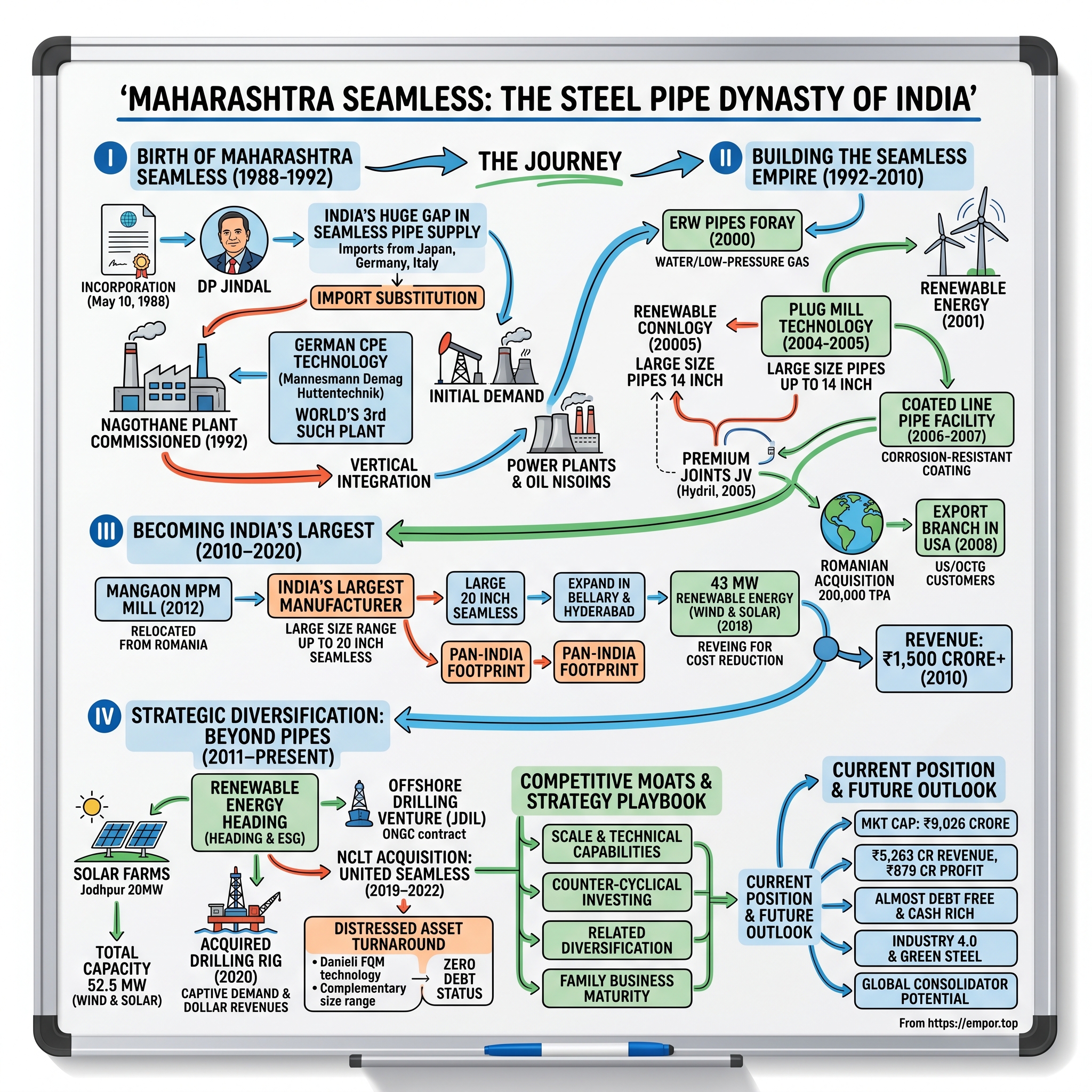

May 10, 1988. The boardroom at the Jindal Group's Mumbai office overlooks the Arabian Sea, where container ships drift lazily toward the port. D.P. Jindal signs the incorporation documents for Maharashtra Seamless Limited, but his mind isn't on the paperwork—it's on a conversation he had six months earlier with a German engineer at a steel conference in Düsseldorf. Maharashtra Seamless Ltd (MSL) was incorporated on May 10, 1988. The engineer, from Mannesmann Demag Huttentechnik, had mentioned something intriguing: their CPE (Cross Roll Piercing and Elongation) technology could produce seamless pipes with quality matching Japanese standards but at lower capital costs.

The company was conceived after noticing huge demand and supply gap in the seamless pipe market, which was met mostly through imports. The numbers were staggering—India imported over 200,000 tonnes of seamless pipes annually, draining precious foreign exchange at a time when the country's reserves could barely cover three weeks of imports. Every refinery expansion, every power plant commission, every oil drilling project sent procurement managers scrambling to European and Japanese suppliers who dictated prices and delivery schedules.

The technical collaboration with Mannesmann Demag Huttentechnik (MDH) wasn't just another licensing agreement. This import substitute project was set up in 1991 at Nagothane (near Mumbai), Distt. Raigad (Maharashtra), to manufacture seamless pipes & tubes with the finest quality and wide product range using the world renowned CPE technology acquired through technical collaboration with Mannesmann Demag Huttentechnik Gmbh (MDH), Germany at a capital cost of Rs 69 crore. MDH represented the pinnacle of German engineering—Mannesmann Demag is a world leader in steel and seamless pipe industry. The Mannesmann Group itself had invented the process for rolling seamless steel pipes back in 1886, fundamentally transforming how high-pressure pipes were manufactured globally.

What made this collaboration extraordinary was its exclusivity and sophistication. Our state of the art plant is only the third of its kind in the world. Think about that—in 1992, only two other plants globally operated with this specific configuration of CPE technology. This wasn't about buying off-the-shelf machinery; it was about transplanting cutting-edge metallurgical knowledge from the Rhine Valley to the Konkan coast.

The location choice—Nagothane in Raigad district, about 100 kilometers from Mumbai—was strategic. Close enough to Mumbai's port for importing raw materials and exporting finished products, yet far enough to secure large land parcels at reasonable prices. The site had access to the Mumbai-Goa highway and proximity to JNPT port, India's largest container port. But more importantly, it was near the industrial corridors feeding Mumbai and Pune, where many potential customers operated.

The project was appraised and financed by ICICI in participation with IDBI & IFCI and other banks. Getting India's premier financial institutions on board wasn't easy. The loan officers were skeptical—seamless pipe manufacturing was notoriously capital-intensive with long gestation periods. D.P. Jindal spent months educating bankers about the technology, taking them to Germany to see MDH's reference plants, showing them import data, and most crucially, securing letters of intent from Indian oil companies desperate for reliable domestic suppliers.

The plant was commissioned in February 1992. The main plant and machinery was imported from USA based on MDH design. The commissioning phase revealed the complexity of technology transfer. German engineers lived in Nagothane for months, training Indian operators on the nuances of temperature control, roll pressure adjustment, and quality testing. The CPE process wasn't forgiving—a few degrees of temperature variation or slightly incorrect roll alignment could ruin entire batches.

MSL's state-of-the-art plant uses world renowned CPE Technology acquired through technical know-how from German giant MANNESMANN DEMAG HUTTENTECHNIK Gmbh. The CPE (Cross Roll Piercing and Elongation) process begins with the piercing of a hot billet on the piercer, followed by crimping and then elongation on the push-bench and finally the dimensions are controlled within specified variation on the Stretch Reducing Mill (SRM). This process minimises longitudinal and transverse defects in pipes and tubes. It also ensures better control over wall thickness variation as compared to other manufacturing processes.

The technical superiority of the CPE process was immediately apparent. Unlike the older Mannesmann plug mill process used by competitors, CPE offered better dimensional accuracy and surface finish. The wall thickness variation—a critical parameter for high-pressure applications—was kept within ±10%, compared to ±12.5% for conventional processes. For customers in the oil and gas sector, this meant safer operations and longer pipe life.

The initial production runs in 1992 were nerve-wracking. The first batch of pipes failed pressure tests—the wall thickness was uneven. German engineers flew in urgently, spending sleepless nights recalibrating the stretch reducing mill. The second batch passed, but surface defects appeared. More adjustments, more learning. By the fourth month, the plant was producing pipes that matched German quality standards. When samples were sent to Indian Oil Corporation for testing, the procurement manager reportedly said, "If you hadn't told me these were made in India, I would have assumed they were German imports."

The financial structure revealed D.P. Jindal's conservative approach. At Rs 69 crore, the project cost was substantial but not reckless. Compare this to Essar Steel's integrated steel plant being set up simultaneously at a cost of Rs 2,400 crore. Jindal chose focused excellence over diversified mediocrity. The debt-equity ratio was kept at 2:1, ensuring the company wouldn't be crushed by interest payments if commissioning was delayed.

By late 1992, Maharashtra Seamless had proved something important: India could manufacture world-class seamless pipes. The first year's production was modest—just 15,000 tonnes against a capacity of 75,000 tonnes. But every pipe that left Nagothane carried a message to the market: the era of import dependence was ending. Orders started flowing from refineries tired of waiting months for European deliveries. The foundation was laid, but the real challenge—scaling up while maintaining quality and fighting entrenched import lobbies—was just beginning.

IV. Building the Seamless Empire (1992-2010)

The mid-1990s found Maharashtra Seamless at a crossroads. The initial euphoria of successful commissioning had given way to harsh market realities. Capacity utilization hovered around 40%, import lobbies spread rumors about quality issues, and the Asian financial crisis loomed. Yet D.P. Jindal saw opportunity where others saw obstacles. "Markets don't stay depressed forever," he told his management team during a particularly difficult quarter in 1997. "We build for the next upturn."

The strategic decision to enter ERW pipes transformed the company's trajectory. MSL made a foray in the ERW pipe category in the year 2000. It has put up a plant at Raigad, Maharashtra, capable of producing ERW pipes having OD range between 168.3 mm to 530 mm OD and wall thickness of 3.2 mm to 12.7 mm with present installed capacity of 200000 TPA, making India's first par excellence largest outer diameter pipe manufacturer using ERW technology. This wasn't just capacity addition—it was strategic positioning. ERW pipes served different applications than seamless pipes, particularly in water transmission and low-pressure gas pipelines. By offering both technologies, Maharashtra Seamless could now bid for entire project requirements rather than just specialized segments.

The ERW plant setup revealed the company's evolving technical sophistication. Unlike the seamless plant where technology was transferred wholesale from Germany, the ERW facility involved selective technology adoption. The forming mills came from Mannesmann, the welding technology from Thermatool USA, and the testing equipment from various European suppliers. MSL's engineers had learned enough from running the seamless plant to integrate best-in-class components rather than accepting turnkey solutions.

The quality is unsurpassed and the product well accepted & appreciated in the market. This plant is catering for requirement of large diameter ERW pipes for applications in the field of natural gas, crude oil, refineries and other core sector industry like fertilizers etc. The market response validated the strategy. GAIL's massive natural gas pipeline projects, connecting India's eastern gas fields to western markets, became early anchor customers. Unlike seamless pipes which competed directly with imports, large-diameter ERW pipes had limited import competition due to transportation economics—shipping a 20-inch diameter pipe from Europe wasn't economically viable for most projects.

December 2001 marked another pivotal moment. A Wind Power Project having 7 MW capacity was successfully commissioned in the month of December 2001 at district Satara, Maharashtra with a total cost of Rs. 36 crores (approx.) The entire project cost has been financed by the company with its internal resources only. This wasn't mere diversification—it was strategic hedging. Power costs constituted nearly 15% of pipe manufacturing expenses. By generating their own renewable power, Maharashtra Seamless not only reduced operational costs but also positioned itself as an environmentally conscious manufacturer—increasingly important for international customers.

The 2004-2005 period brought technological breakthroughs that would define the company's next decade. In same year of 2004-2005 the company expanded its production facilities, using plug mill technology supported by world class revelers, to manufacture for the first time in India, large size seamless pipes of diameter up to 14 inches and wall thickness up to 40 mm. The plug mill technology represented a quantum leap. While CPE technology excelled at smaller diameters with superior surface finish, plug mill technology enabled production of larger, thicker pipes essential for deepwater drilling and high-pressure applications.

The joint venture with Hydril LP in 2005 deserves special attention. During the year 2004-2005, the company entered into joint venture with Hydril LP to manufacture premium joint connections to facilitate company consolidation in both domestic and international markets of seamless pipes by going to new export avenues. Premium connections—the threaded joints that connect pipes in oil wells—were the highest margin segment of the OCTG market. Without premium connections, Maharashtra Seamless was essentially selling commodities. With them, they could offer complete solutions competing directly with international majors.

During the financial year 2006-07 the company has successfully commissioned coated line pipe facility by using the latest technology for FBE and 3 layer PE/PP coating near to the existing facility at Nagothane. The coating facility represented another layer of value addition. Pipes for cross-country pipelines required specialized anti-corrosion coatings. Previously, Indian pipe manufacturers shipped uncoated pipes to coating facilities in Gujarat or imported pre-coated pipes. By integrating coating capabilities, Maharashtra Seamless captured additional margins while offering faster delivery times.

The Romanian acquisition in 2007-2008 was the company's boldest move yet. Maharashtra Seamless (MSL) - a flagship company of the Rs 3,000 crore turnover DP Jindal Group - announced that the parent company is acquiring Romania-based seamless plant with a capacity of 2,00,000 TPA. The timing seemed counterintuitive—global financial markets were showing stress signals, commodity prices were volatile, and credit was tightening. But D.P. Jindal understood something others missed: distressed assets in Eastern Europe, struggling with EU environmental regulations and aging ownership, could be acquired at fraction of replacement cost.

As on 4th January 2008, the company acquired seamless plant in Romania with an installed capacity of 200,000 TPA. The Romanian plant, originally built in the 1970s to supply the Soviet bloc, had good bones—solid infrastructure, skilled workforce, strategic location for European markets. What it lacked was capital for modernization and market access. Maharashtra Seamless provided both, planning to eventually relocate the most valuable equipment to India while maintaining a European manufacturing presence.

The international expansion continued with strategic market development. In the same year, the company opened its export branch in USA to facilitate better services and customer support to its large base of Oil Country Tubular Goods (OCTG) and Line pipe customers in USA, Canada and Latin America. In June of the same year 2008, MSL had bagged export orders worth USD 45 million from USA. The US office wasn't just a sales outpost—it was a learning laboratory. American customers, particularly in the shale gas sector, had the world's most demanding specifications. Meeting their requirements forced Maharashtra Seamless to continuously upgrade quality systems.

By 2010, Maharashtra Seamless had transformed from a single-product, single-location manufacturer to a diversified, international steel pipe company. Revenue had grown from Rs 105 crores in 1994-95 to over Rs 1,500 crores. The company could now produce pipes from 10mm to 14 inches in seamless and up to 21 inches in ERW—a range few global manufacturers could match. More importantly, they had built capabilities across the value chain: from basic pipes to premium connections, from uncoated to sophisticated multi-layer coatings, from domestic focus to global presence.

The foundation was set for the next phase: becoming India's undisputed leader in large-diameter seamless pipes. But first, they would have to navigate the global financial crisis and its aftermath—a test that would separate the truly resilient from the merely ambitious.

V. The Expansion Years: Becoming India's Largest (2010-2020)

March 2012, Mangaon, Maharashtra. The monsoon hadn't arrived yet, and dust clouds rose from the construction site where German-designed equipment from Romania was being reassembled piece by piece. D.P. Jindal stood watching as the massive MPM (Mandrel Pipe Mill) took shape—machinery that had crossed continents to find its new home. In 2012, MSL extended its seamless pipes to range up to 20" at Nagothane. In the same year, another state-of-the-art MPM Mill was started in Mangaon, Maharashtra to increase the capacity of seamless pipe manufacturing. This wasn't just expansion; it was a statement of intent to dominate every segment of the Indian pipe market.

The significance of achieving 20-inch diameter seamless pipes cannot be overstated. MSL is also the only manufacturer in India to offer the maximum size range upto 20" catering to customers across all sectors. Consider the technical challenge: as pipe diameter increases, maintaining uniform wall thickness becomes exponentially harder. The forces involved in piercing and elongating a 20-inch billet are enormous. Temperature gradients can cause catastrophic failures. Yet Maharashtra Seamless had cracked the code, becoming the sole Indian company capable of producing seamless pipes across the entire spectrum from half-inch to 20 inches.

The Romanian plant relocation to Mangaon revealed strategic brilliance masked as operational necessity. The plant has been completely dismantled and relocated to India at Mangaon, Vile Bhagad, Maharashtra near the existing plant. Plant was commissioned on March 2012. Rather than maintaining an expensive European operation with declining competitiveness, Maharashtra Seamless transported the best equipment to India where labor costs were lower, raw material supply was closer, and growing domestic demand justified the investment. The Government of Maharashtra has conferred the status of "Mega Project" to company's' aforesaid project, enabling various incentives that improved project economics.

The MPM technology at Mangaon represented a technological leap. MPM (Mandrel Pipe Mill) process is suitable for small diameter thick wall carbon-high alloy grade pipes & tubes and has a range of 6". Elongation through six stand continuous rolling mill with high precision mandrel in this mill ensures smooth surface and close tolerances. While the Nagothane plant's CPE technology excelled at thin-wall pipes and the plug mill handled large diameters, MPM filled the crucial gap for thick-wall, smaller diameter pipes used in high-pressure applications.

We have the finest technology available in the world for manufacturing seamless pipes, i.e., CPE, MPM & Plug Mill, the company's leadership could now claim. This trinity of technologies—each optimal for different product segments—gave Maharashtra Seamless unmatched flexibility. A refinery needing thin-wall heat exchanger tubes, an offshore platform requiring thick-wall high-pressure pipes, and a power plant seeking large-diameter steam pipes could all be served from the same company.

Geographic expansion followed technological diversification. Furthermore, we have also expanded our ERW business by setting up a plant in Bellary, Karnataka and Hyderabad, Andhra Pradesh. The Bellary plant, located in India's iron ore belt, enjoyed proximity to raw materials. The Hyderabad facility tapped into South India's industrial corridor. This pan-India manufacturing footprint—We have established a pan-India presence with manufacturing facilities in Uttar Pradesh, Maharashtra, Karnataka, and Telangana—reduced logistics costs and improved customer service while spreading operational risk.

The product portfolio evolution during this period reflected changing market dynamics. Our product portfolio caters to each and every sector and application like oil & gas, refineries, petrochemicals, chemicals, fertilizers, power, railways, boiler, automotive, bearing, gas cylinders, infrastructure, mechanical, and structural applications. This wasn't scatter-shot diversification but careful market segmentation. Each application had specific requirements—API certification for oil and gas, IBR approval for boilers, precise tolerances for bearings—and Maharashtra Seamless methodically built capabilities to serve each segment.

Quality systems evolved in parallel with capacity expansion. Also, our modern laboratories have been NABL-approved. We have NACE laboratories for supplying seamless pipes for service. Besides, we are equipped with all the testing facilities like NDT, UT, EMI, Eddy-current, MPM, Hydro Tester, Impact testing, Hardness Tester, etc. These weren't just compliance checkboxes. American shale gas producers, burned by pipe failures in horizontal drilling applications, demanded metallurgical testing that pushed Maharashtra Seamless's labs to international standards.

The export breakthrough during this period deserves special attention. From the early years MSL has been exporting its products to the oil-fields of the US. Now MSL exports more than one-third of its volume to the markets of the US, Canada, Latin America, Europe, Africa & Asia. Breaking into the US market—the world's most sophisticated and demanding pipe market—required more than just competitive pricing. It meant meeting API specifications consistently, maintaining inventory in Houston, providing technical support in West Texas oil fields, and building relationships with conservative American purchasing managers who had bought from European suppliers for decades.

Financial performance during 2010-2020 validated the expansion strategy. The turnover of the company for the year ended 31.03.2013 is approx. Rs. 1710 crores, growing from around Rs 1,500 crores in 2010. But more importantly, the company maintained profitability through commodity cycles that crushed weaker competitors. When oil prices collapsed in 2014-2015, sending global pipe demand plummeting, Maharashtra Seamless's diversified portfolio—spanning oil and gas to railways to renewable energy—provided resilience.

The integration of renewable energy operations provided an unexpected competitive advantage. With 7 MW wind power already operational since 2001, the company added solar capacity throughout the decade. By 2018, the company achieved a total capacity of 43 MW of Renewable Energy. This wasn't greenwashing—energy costs represent 15-20% of pipe manufacturing expenses. By generating their own power, Maharashtra Seamless insulated itself from grid tariff volatility while earning carbon credits that international customers increasingly valued.

Now with this new expansion the total installed capacity of Seamless plant is 350000 TPA, making Maharashtra Seamless indisputably India's largest seamless pipe manufacturer. The transformation from a single-plant operation producing 75,000 tonnes in 1992 to a multi-location conglomerate with 550,000 tonnes capacity represented one of Indian manufacturing's quieter success stories. Unlike software companies that captured headlines, Maharashtra Seamless built its empire pipe by pipe, customer by customer, certification by certification.

By 2020, the company stood at another inflection point. The next acquisition would test whether Maharashtra Seamless could absorb distressed assets and turn them profitable—a skill that would prove crucial as India's infrastructure boom accelerated amid global economic uncertainty.

VI. Strategic Diversification: Beyond Pipes (2011–Present)

The boardroom discussion in early 2011 was heated. Oil prices had crossed $100 per barrel, seamless pipe demand was booming, and competitors were scrambling to add capacity. Yet D.P. Jindal was proposing something counterintuitive: invest heavily in solar power generation in Rajasthan's desert. "Are we a pipe company or a power company?" asked a board member. Jindal's response was characteristically measured: "We are an energy infrastructure company. The synergies will become clear in time."

The renewable energy pivot wasn't random diversification—it was strategic hedging with multiple layers of logic. The Company successfully commissioned and started generation from 20 MW Solar Power Plant at Khetusar, District Jodhpur, Rajasthan. The location in Jodhpur wasn't accidental. Rajasthan's strong solar irradiance provides year-round energy generation, with some of the highest solar radiation levels in India. But more importantly, generating power in Rajasthan allowed Maharashtra Seamless to wheel electricity to its manufacturing plants in Maharashtra under open access regulations, effectively arbitraging interstate power price differentials.

By 2018, With this Company has achieved a total capacity of 43 MW of Renewable Energy. The economics were compelling: solar power generation costs had fallen to Rs 2.50 per unit while industrial grid tariffs in Maharashtra exceeded Rs 8 per unit. Every megawatt of renewable capacity translated directly to bottom-line savings. But the strategic value went beyond cost reduction. International customers, particularly European buyers facing stringent carbon regulations, increasingly demanded suppliers with renewable energy credentials. Maharashtra Seamless could now claim that a significant portion of its manufacturing was powered by clean energy—a differentiator in commodity markets.

The offshore drilling venture represented a different kind of synergy. Jindal Drilling & Industries Limited (JDIL) part of the D.P. Jindal Group Drilling Division, is a leading company amongst Indian private sector companies in offshore drilling in India's Oil & Gas sector with operation since 1989. The drilling business wasn't just about diversification—it created a captive customer for high-specification seamless pipes while providing market intelligence about upcoming exploration projects. When ONGC planned new drilling campaigns, Maharashtra Seamless knew months in advance, allowing better production planning.

The 2020 acquisition revealed this strategy's maturity. Maharashtra Seamless has acquired an Offshore Jack Up Drilling Rig from Star Drilling, Singapore, an associate of the company for $100 million, consequent upon receipt of requisite approval from the Seller. The said Rig is currently operating under contract with Oil and Natural Gas Corporation (ONGC). Acquiring a rig already under contract with ONGC wasn't speculation—it was buying cash flow. The $100 million investment generated predictable returns while deepening relationships with India's largest oil company.

JDIL has achieved nearly a 100% efficiency standard across all its rigs, with significantly higher commercial speed than its competitors and other operator owned rigs. This operational excellence wasn't coincidental. The same engineering rigor that made Maharashtra Seamless a leader in pipe manufacturing—attention to specifications, preventive maintenance, systematic training—translated directly to rig operations. A drilling rig, after all, is essentially a complex assembly of high-pressure pipes and hydraulic systems.

The Brazilian iron ore investment told a different story—one of ambition meeting market reality. During the year 2014, a subsidiary of the Company has acquired 20 percent stake in an Iron ore mine in Amapa, Brazil with estimated reserves of more than 250 million tons. The logic seemed compelling: secure raw material supply for future steel-making ambitions while riding the commodity supercycle. Brazilian ore could be shipped to India or sold in international markets, providing another revenue stream.

Not only into the Pipes and Tubes, MSL has diversified its business portfolio in varied strategic areas such as Renewable Power generation and acquisition of a stake in an iron ore mine in Amapa, Brazil. But timing proved unfortunate. Iron ore prices collapsed from $180 per tonne in 2011 to below $40 by 2015. The Company had made investments in a mining asset through its foreign subsidiaries. The subsidiary, holding the mining investments partially impaired the said investments. Accordingly the Company impaired its exposures, partially for Rs. 145.98 Crore during the year 2019.

The iron ore misadventure offered valuable lessons. Unlike renewable energy (which provided immediate operational benefits) or drilling rigs (which leveraged existing capabilities), the Brazilian mine was a pure commodity play in an unfamiliar geography. Maharashtra Seamless learned that related diversification—where operational synergies exist—works better than unrelated ventures, regardless of how attractive commodity prices appear.

The solar expansion continued more successfully. Maharashtra Seamless, a manufacturer of electric resistance welded and seamless pipes and tubes, announced that it has commissioned a 20 MW solar project in Khetusar village, Jodhpur, Rajasthan. The company also commissioned 1 MW rooftop solar power plant at Nagothane and 10 MW captive power plants at Beed Maharashtra. The rooftop installations at manufacturing facilities served dual purposes: generating power while reducing factory heat load, improving worker comfort and productivity.

The strategic diversification transformed Maharashtra Seamless's financial profile. Revenue streams became more predictable—renewable energy provided steady cash flows independent of steel cycles, drilling rigs generated dollar revenues hedging rupee depreciation, and the core pipe business benefited from lower costs and enhanced reputation. The company's debt-to-equity ratio remained below 0.5 even after these investments, testament to careful capital allocation.

By 2020, Maharashtra Seamless had evolved from a pure-play pipe manufacturer to an integrated energy infrastructure company. The diversification wasn't about abandoning core competencies but enhancing them. Solar arrays powered pipe plants, drilling rigs consumed specialized pipes, and operational excellence in manufacturing translated to superior drilling performance. Each business supported the others, creating a resilient ecosystem rather than a disconnected conglomerate.

Yet the biggest test of this diversified model was about to come. The NCLT acquisition opportunity would require Maharashtra Seamless to integrate a distressed competitor while navigating post-pandemic market volatility—a challenge that would test every capability the company had built over three decades.

VII. The NCLT Acquisition & Consolidation (2019-2022)

January 21, 2019, Hyderabad. The National Company Law Tribunal's courtroom was packed with lawyers, bankers, and industry observers. After eighteen months of insolvency proceedings, the fate of United Seamless Tubulaar Private Limited—once a crown jewel of the Kamineni Group's industrial ambitions—would finally be decided. When the judge announced approval for Maharashtra Seamless's resolution plan, D.P. Jindal's team knew they had just acquired not just a plant, but a strategic foothold in South India's industrial heartland.

Hyderabad Bench of National Company Law Tribunal on 21 January 2019 has approved the Resolution Plan submitted by the Company (resolution applicant) for acquisition of United Seamless Tabulaar (USTPL) under the Corporate Insolvency Resolution Process (CIRP) initiated against USTPL under the Insolvency and Bankruptcy Code 2016. The acquisition wasn't opportunistic—it was the culmination of months of due diligence, negotiations with creditors, and strategic planning.

United Seamless Tubulaar Private, a joint venture between the Kamineni Group and UMW Group of Malaysia, is involved manufacturing of seamless pipes and tubes. The company's pedigree was impressive—Ours is one of the most advanced plants built using Danieli Centro Tube FQM-Fine Quality Mill 3-roll retained mandrel mill technology. Danieli's FQM technology is the best available technology today for the manufacturing of seamless pipes and Danieli ranks among the three largest suppliers. This wasn't a distressed asset in the traditional sense—it was a technologically sophisticated facility that had fallen victim to overleveraging and market timing.

The numbers told a compelling story. The bid of Maharashtra Seamless Ltd, of Rs 477 crore was backed by majority lenders (87 per cent), who had approved the bid. Breaking down the payment structure revealed Maharashtra Seamless's financial discipline: Payment of Rs. 477 crore to towards settlement of financial creditors, corporate insolvency resolution process cost, admitted operational creditors, workmen and employee dues, etc. Rather than aggressive bidding, they offered what the asset was worth to them—no more, no less.

In 2020, we also acquired another seamless manufacturing unit called United Seamless Tubulaar Pvt. Ltd. (USTPL) at Narketpally, Telangana, through NCLT. It is a 100 percent subsidiary of MSL and the merger process with MSL is on. The Narketpally location offered strategic advantages: proximity to Hyderabad's engineering ecosystem, access to skilled workforce from the region's technical institutes, and a gateway to South Indian markets previously difficult to serve from Maharashtra.

The Seamless Pipe Mill capacity is based on Rotary Hearth Furnace capacity of 110 MT / hour and the size range. Our Product range covers Seamless Pipes in the size range 5" OD to 14" OD (Scalable to 16" OD), in all API and special grades. The complementary size range was crucial—while Maharashtra Seamless's Nagothane plant excelled at smaller diameters and the Mangaon facility handled large-diameter pipes, USTPL filled the middle range perfectly. The combined entity could now offer customers a true one-stop solution.

The integration challenges were substantial. USTPL had been in insolvency for over eighteen months, during which maintenance had been deferred, key personnel had left, and customer relationships had atrophied. Maharashtra Seamless deployed a 50-person team to Narketpally immediately after NCLT approval, focusing on three priorities: technical assessment, workforce retention, and customer reconnection.

The technical assessment revealed both problems and opportunities. While the Danieli equipment was world-class, software systems were outdated, quality control processes needed overhaul, and the furnace required significant refurbishment. Maharashtra Seamless invested an additional Rs 100 crore in the first year alone, modernizing control systems and implementing their proven quality protocols. The investment paid off—within six months, the plant was producing pipes that met Maharashtra Seamless's stringent quality standards.

Workforce integration proved surprisingly smooth. workmen and employee dues were settled immediately, building goodwill. Maharashtra Seamless retained most of USTPL's 800 employees, recognizing that their knowledge of the Danieli equipment was invaluable. Cross-training programs brought Narketpally workers to Maharashtra plants, while experienced managers from Nagothane mentored their Telangana counterparts. The cultural integration wasn't forced—both organizations shared an engineering-first mindset that transcended regional differences.

Customer win-back required delicate handling. Many of USTPL's former customers had switched to competitors or imports during the insolvency period. Maharashtra Seamless leveraged its reputation and financial strength to offer extended credit terms, quality guarantees, and most importantly, supply reliability that USTPL couldn't provide in its final years. Within eighteen months, capacity utilization at Narketpally reached 70%, exceeding pre-insolvency levels.

The financial engineering behind the acquisition deserves attention. The company has prepaid its long-term loans for the Telangana plant and rig acquisitions in October 2022 and June 2023, achieving a zero-debt status. This wasn't just financial conservatism—it was strategic positioning. By maintaining a debt-free status, Maharashtra Seamless could move quickly on future opportunities without lengthy bank approvals or covenant restrictions.

The merger with MSL & USTPL would pave the way for achieving the envisioned goals. The merger process, initiated immediately after acquisition, aimed to create operational synergies: unified procurement reducing raw material costs by 5%, shared technical services eliminating redundancy, and integrated sales teams offering comprehensive solutions to large customers.

The capital allocation strategy post-acquisition reflected long-term thinking. capital expenditures of approximately Rs. 852 Cr funded through internal accruals, allocated as follows: Narketpally (USTPL) at Rs. 264 Cr, Mangaon (MSL) at Rs. 195 Cr, and Nagothane (MSL) at Rs. 393 Cr. Rather than milk the acquired asset, Maharashtra Seamless committed to upgrading all facilities simultaneously, ensuring no plant became a bottleneck.

The market response validated the strategy. The share price hit an intraday high of 449 on BSE and 448.9 on NSE. Earlier during the day's trade, stock touched an intra-day high of Rs 449 after opening at Rs 444.80, against previous closing price of Rs 432.90. Investors recognized that Maharashtra Seamless hadn't just bought capacity—they had consolidated the Indian seamless pipe industry, achieving market share that would be difficult for competitors to challenge.

By 2022, the USTPL integration was complete. The Narketpally plant operated at full capacity, contributing over Rs 500 crore in annual revenue. More importantly, the successful turnaround demonstrated Maharashtra Seamless's ability to acquire and integrate distressed assets—a capability that would prove valuable as India's infrastructure boom accelerated and weaker players struggled with volatility. The company now operated a truly pan-India manufacturing network, with strategic presence in every major industrial corridor.

VIII. Financial Performance & Market Position

The numbers tell a story of patient capital deployment finally bearing fruit. Mkt Cap: 9,026 Crore (up 17.0% in 1 year) · Revenue: 5,263 Cr · Profit: 879 Cr. These headline figures mask a more nuanced narrative—a company that transformed from a single-product manufacturer to a diversified industrial conglomerate while maintaining the financial discipline of a family-run enterprise.

The journey to becoming debt-free deserves special scrutiny. Company is almost debt free. The company is debt free and has a strong balance sheet enabling it to report stable earnings growth across business cycles. In an industry where competitors routinely operate with debt-to-equity ratios exceeding 1.5, Maharashtra Seamless's zero-debt status is almost unprecedented. This wasn't achieved through conservatism alone but through aggressive cash generation and disciplined capital allocation.

Consider the capital efficiency metrics. With a market capitalization of Rs 9,026 crore generating Rs 879 crore in profit, the company trades at a PE ratio of approximately 10.3—remarkably cheap for a market leader with 55% market share in seamless pipes. The valuation discount reflects market skepticism about commodity businesses, but Maharashtra Seamless has proven it's not a typical commodity player.

Financial performance through cycles reveals the company's resilience. For FY25, the company has registered a consolidated net profit of Rs 777.46 crore (down 18.3% YoY) and net sales of Rs 5,268.67 crore (down 2.5% YoY). The decline wasn't operational failure but strategic choice—the company prioritized margins over volume during a period of input cost volatility, choosing to cede low-margin business rather than chase revenue growth.

The quarter-by-quarter performance tells an interesting story. Maharashtra Seamless Ltd's net profit jumped 10.84% since last year same period to ₹242.04Cr in the Q4 2024-2025. This recovery wasn't accidental—it reflected the company's ability to pass through cost increases with a lag, a pricing power that only market leaders possess. EBIDTA margin declined by 300 basis points YoY to 20% in Q4 FY25, but maintaining 20% EBITDA margins in a commodity downcycle is itself an achievement.

Capital allocation priorities reveal management thinking. The board of Maharashtra Seamless has recommended a dividend of Rs 10 per equity for the financial year 2024-25. With Dividend payout has been low at 13.4% of profits over last 3 years, the company clearly prioritizes reinvestment over distributions. This makes sense—with returns on capital employed consistently exceeding 20%, every rupee retained generates superior returns compared to what shareholders could achieve independently.

The balance sheet strength enables strategic flexibility. We are now completely debt-free, boasting liquid investments of nearly INR 1,300 crores. This war chest isn't idle cash—it's optionality. When the next distressed asset becomes available through NCLT, when a technology partnership requires upfront investment, or when a customer needs extended credit terms to win a large contract, Maharashtra Seamless can move without board approvals or bank negotiations.

Working capital management deserves attention. In a business where customers routinely demand 90-day payment terms while raw material suppliers expect payment within 30 days, managing working capital becomes crucial. Maharashtra Seamless's negative working capital cycle—where customer advances and supplier credit exceed inventory and receivables—generates free cash flow that funds growth without external capital.

The dividend policy reflects confidence without complacency. In the quarter ending March 2024, Maharashtra Seamless Ltd has declared dividend of ₹10 - translating a dividend yield of 2.23%. For a company growing at double digits with multiple expansion opportunities, this 2%+ yield signals management's confidence in sustained cash generation while retaining flexibility for growth investments.

Peer comparison reveals competitive advantages. While competitors struggle with debt servicing costs that consume 15-20% of EBITDA, Maharashtra Seamless's debt-free status translates directly to bottom-line advantage. When steel prices spike and banks tighten working capital limits, Maharashtra Seamless can extend customer credit while competitors scramble for liquidity. This financial flexibility becomes market share during downturns.

The segment performance breakdown is revealing. our seamless pipes segment remains the largest contributor to overall EBITDA, contributing 87% of the total EBITDA. While diversification into renewable energy and drilling provides stability, the core pipe business remains the profit engine. This focus—rather than empire building through unrelated diversification—has served shareholders well.

The company's inclusion in indices validates institutional recognition. its inclusion in the Morgan Stanley Capital Invest India Domestic Small Cap Index led to a significant bump in foreign investment. Index inclusion creates a virtuous cycle—passive fund flows reduce volatility, lower volatility attracts active managers, institutional ownership improves governance perception, and better governance drives valuation re-rating.

Institutional shareholding patterns tell their own story. These investors have better resources and capabilities to analyze the fundamentals of companies, making their stake of 15.91% in the company a positive sign. The gradual increase in institutional ownership—from under 5% a decade ago—reflects growing comfort with management quality, disclosure standards, and business predictability.

The promoter holding of 68.9% might concern governance purists, but it ensures alignment. The Jindal family's wealth is tied to Maharashtra Seamless's performance. They can't exit easily, forcing long-term thinking. This patient capital approach—building capabilities over quarters, relationships over years, and reputation over decades—has created value that quarterly capitalism often destroys.

Looking at valuation metrics, Pre-tax margin of 23% is great, ROE of 16% is good. These aren't software-like margins, but for a manufacturing business requiring significant fixed assets, generating 16% ROE while maintaining zero debt is exceptional. It implies the business generates returns well above its cost of capital, creating economic value with every rupee invested.

The cash flow generation capability deserves emphasis. From negative free cash flow during the expansion years of 2010-2015, Maharashtra Seamless now generates Rs 500+ crore in annual free cash flow even after growth capex. This transformation from cash consumer to cash generator marks the transition from growth company to mature compounder.

By 2024, Maharashtra Seamless's financial position is enviable: debt-free, cash-rich, market leader, and generating predictable cash flows. The company stands ready for the next phase of growth, whether through organic expansion, acquisitions, or technology investments. The financial fortress built over three decades provides the foundation for whatever opportunities or challenges lie ahead.

IX. Playbook: Business & Strategic Lessons

The conference room at the Jindal Group's Mumbai office has witnessed decades of strategic discussions, but the presentation on this particular afternoon in 2023 was different. Saket Jindal, now Managing Director, was explaining to a group of IIM students why Maharashtra Seamless succeeded where others failed. "Everyone sees our success today," he began, "but few understand the playbook we followed."

Import Substitution as Opportunity Identification

The first lesson seems obvious in hindsight but required courage in execution: identify products where India's technical capabilities lag global standards, then systematically bridge that gap. Maharashtra Seamless didn't invent seamless pipes or discover their applications. They recognized that India's annual import bill for seamless pipes exceeded $500 million in the late 1980s—a structural inefficiency waiting to be exploited.

But import substitution alone doesn't guarantee success. The graveyard of Indian industry is littered with companies that tried to replicate foreign products with inferior quality. Maharashtra Seamless understood that import substitution only works when you match or exceed import quality. This meant accepting higher initial costs, longer gestation periods, and the humility to learn from global leaders rather than attempting indigenous innovation prematurely.

Technology Partnerships and Knowledge Transfer

The collaboration with Mannesmann Demag Huttentechnik reveals sophisticated understanding of technology transfer. Maharashtra Seamless didn't just buy machinery; they bought knowledge. The agreement included training programs, ongoing technical support, and crucially, the right to adapt technology for Indian conditions. This wasn't technology dependence but technology absorption—a critical distinction.

The company's approach to technology partnerships evolved over time. The initial Mannesmann relationship was teacher-student. By the time of the Hydril joint venture for premium connections, it was more equal. And when acquiring the Romanian plant, Maharashtra Seamless was the technology upgrader, not receiver. This progression from technology importer to technology adapter to technology enhancer represents a maturation arc few Indian companies achieve.

Vertical Integration and Diversification Timing

Maharashtra Seamless's diversification strategy offers a masterclass in timing and sequencing. They didn't diversify from day one—they first established dominance in seamless pipes. Only after achieving 40%+ market share did they add ERW pipes. Renewable energy came after stable cash flows were established. Drilling rigs were added when the core business could fund acquisitions without leverage.

Each diversification built on existing capabilities. ERW pipes leveraged customer relationships from seamless pipes. Solar power reduced manufacturing costs while providing ESG credentials. Drilling rigs created captive demand for specialized pipes. The failed Brazilian iron ore venture taught them that unrelated diversification, regardless of commodity attractiveness, destroys value. The lesson: diversify into adjacencies where operational synergies exist, not financial synergies alone.

Family Business Management and Succession

The Jindal family's management approach defies both traditionalists who insist families should stay and modernists who demand professional management. They found a middle path: family provides vision and values while professionals handle operations. D.P. Jindal remains Chairman, providing continuity and relationships. Saket Jindal as Managing Director bridges family and management. Professional presidents run day-to-day operations.

This structure避免了many pitfalls of family businesses. There's no public succession drama that destroys value. Brothers have defined roles preventing turf wars. The 68.9% promoter holding ensures control while public listing enforces discipline. The family's willingness to dilute from 90%+ to below 70% shows they prioritize growth over control—a maturity rare in Indian family businesses.

Capital Allocation in Cyclical Industries

Maharashtra Seamless's capital allocation framework offers lessons for any cyclical business. During upturns, they don't chase growth at any cost. Instead, they strengthen balance sheets, paying down debt and accumulating cash. During downturns, when competitors are distressed, they acquire assets at attractive valuations—the USTPL acquisition being a prime example.

The company maintains counter-cyclical investment discipline. Major capex programs often begin during downturns when equipment costs are lower and execution capacity is available. By the time upturns arrive, new capacity is operational, capturing maximum value. This requires resisting pressure to invest at cycle peaks when investors demand growth and avoiding panic during troughs when they demand conservation.

Building Moats Through Scale and Technical Capabilities

Maharashtra Seamless's competitive moats aren't immediately obvious. Steel pipes seem like commodities—standardized products where price alone determines purchase decisions. Yet the company maintains 55% market share and 20%+ EBITDA margins. The moat lies in the combination of scale and technical capabilities that's expensive and time-consuming to replicate.

Consider what a competitor needs to challenge Maharashtra Seamless: Rs 1,000+ crore for a modern plant, 3-5 years for construction and commissioning, technical partnerships with global leaders who may have exclusivity agreements, certifications from API, IBR, and other bodies requiring 2+ years of testing, relationships with conservative procurement managers at oil companies, and working capital to offer competitive payment terms. The totality of these requirements, not any single factor, creates the moat.

Managing Through Cycles

The company's approach to cyclical downturns offers valuable lessons. They don't cut maintenance capex or quality control to preserve margins—short-term moves that destroy long-term value. They don't chase market share through price cuts that trigger industry-wide margin destruction. Instead, they focus on operational efficiency, customer relationships, and strategic positioning for the upturn.

During the 2014-2015 oil price collapse, when pipe demand plummeted, Maharashtra Seamless accelerated training programs, upgraded IT systems, and strengthened supplier relationships. When demand recovered, they emerged stronger while competitors struggled with deferred maintenance and departed talent. This patient approach requires financial strength and psychological fortitude—both abundant at Maharashtra Seamless.

The Premium Strategy in Commodities

Maharashtra Seamless proves you can pursue a premium strategy even in commodities. They don't compete on price alone but on total cost of ownership. Their pipes might cost 5% more, but superior metallurgy means longer life. Better dimensional consistency reduces installation problems. Reliable delivery avoids project delays. Local inventory eliminates emergency import premiums. When these factors are considered, Maharashtra Seamless often provides the lowest total cost despite higher unit prices.

This premium positioning requires continuous capability building. Every API certification, every successful project reference, every on-time delivery builds reputation. Over decades, these accumulate into a brand that commands premium pricing. It's a slow process—there are no shortcuts—but once established, it's extremely difficult for competitors to replicate.

Risk Management Philosophy

The company's risk management approach balances entrepreneurial aggression with financial conservatism. They take operational risks—new technologies, new markets, new products—but avoid financial risks. Zero debt means no refinancing risk. Multiple revenue streams mean no customer concentration. Pan-India manufacturing means no geographic concentration.

This risk management extends to stakeholder relationships. They maintain conservative accounting, avoiding aggressive revenue recognition that backfires eventually. They under-promise and over-deliver to customers, building trust. They treat suppliers as partners, paying on time even during downturns. They provide consistent communication to investors, avoiding surprises. This 360-degree risk management creates resilience that purely financial metrics don't capture.

The Learning Organization

Perhaps the most underappreciated aspect of Maharashtra Seamless's playbook is their commitment to continuous learning. Engineers regularly attend international conferences. Operators are sent to customer sites to understand applications. Managers rotate across functions building cross-functional understanding. The company maintains relationships with technical universities, sponsoring research and recruiting talent.

This learning orientation enabled successful technology absorption. When German engineers left after commissioning the first plant, Indian teams could operate and improve processes. When customers demanded new specifications, R&D teams could develop solutions. When markets shifted, management could adapt strategies. In industries where technology evolves slowly, continuous learning provides cumulative advantage.

The strategic playbook that built Maharashtra Seamless wasn't revolutionary—it was evolutionary. Each capability built on previous ones. Each success enabled the next challenge. Each crisis strengthened resilience. Over three decades, these accumulated into a formidable competitive position. The playbook's beauty lies not in any single brilliant move but in the consistent execution of sound principles over time.

X. Analysis & Investment Thesis

Standing at the intersection of India's infrastructure ambitions and energy transition, Maharashtra Seamless presents a fascinating investment paradox: a commodity business with differentiated economics, a cyclical company with structural growth drivers, and a traditional manufacturer embracing modern sustainability. The investment case isn't immediately obvious—which perhaps explains why the stock trades at just 10 times earnings despite market leadership—but careful analysis reveals a compelling opportunity.

Bull Case: The Convergence of Favorable Factors

India's infrastructure spending is not just large—it's accelerating. The government's Rs 11 lakh crore infrastructure budget for 2024-25 represents a 35% increase over previous years. Every kilometer of gas pipeline, every refinery expansion, every power plant upgrade requires specialized pipes. Maharashtra Seamless, as the only Indian manufacturer with size range up to 20", captures a disproportionate share of high-value, large-diameter pipe demand that cannot be served by smaller competitors.

The oil and gas capex cycle has turned decisively positive. After years of underinvestment during the 2014-2020 downturn, global energy companies are committing to massive spending programs. India's state-owned oil companies alone plan to invest Rs 82,000 crore over the next three years. Private sector players like Reliance and Adani are building new refineries and petrochemical complexes. Each project requires millions of tons of specialized pipes where quality, certification, and delivery reliability matter more than price.

Strong balance sheet with minimal debt provides strategic flexibility that competitors lack. When ONGC floats a tender requiring 180-day payment terms, Maharashtra Seamless can bid while leveraged competitors hesitate. When a distressed asset becomes available, they can acquire without lengthy bank negotiations. When raw material prices spike, they can build inventory while others scramble for working capital. This financial strength becomes market share during volatile periods.

Diversified revenue streams (pipes, renewable energy, drilling) reduce cyclical risk. The 52.5 MW of renewable energy capacity generates Rs 50+ crore of steady EBITDA regardless of steel cycles. The drilling rig on contract with ONGC provides dollar-denominated cash flows for three years. These non-pipe revenues now contribute 13% of EBITDA, providing stability that pure-play pipe manufacturers lack.

The 68.9% promoter holding showing confidence deserves attention. The Jindal family has consistently increased their stake over the past seven years, buying shares in open market whenever prices weaken. This isn't forced buying to maintain control—they already have that. It's voluntary capital allocation by insiders with the best information about business prospects. When promoters buy with their own money, it's the strongest endorsement possible.

The technical capabilities moat continues widening. Maharashtra Seamless now operates three different seamless technologies (CPE, MPM, Plug Mill), manufactures the widest size range in India (½" to 20"), holds certifications from every major international standard, and maintains NABL-accredited testing laboratories that few competitors can match. Replicating these capabilities would require Rs 2,000+ crore and 5+ years—assuming technology partners were even available.

Bear Case: The Structural Challenges

Commodity business with cyclical demand remains the fundamental challenge. Steel pipes are ultimately commodities where customers can switch suppliers, technology differences are modest, and price remains the primary purchase criterion. When oil prices collapse—as they did in 2014 and 2020—pipe demand can disappear almost overnight. No amount of operational excellence fully insulates against commodity cycles.

Competition from imports and domestic players is intensifying. Chinese manufacturers, despite anti-dumping duties, continue finding ways to access Indian markets through third countries. Domestic competitors like Jindal SAW and Welspun are expanding capacity. New technologies like composite pipes threaten steel pipes in certain applications. The 55% market share Maharashtra Seamless enjoys today may prove difficult to maintain as competition intensifies.

Capital intensive with high fixed costs creates operational leverage that cuts both ways. The company requires Rs 500+ crore in annual maintenance capex just to maintain current capacity. Fixed costs—salaries, power, maintenance—continue regardless of capacity utilization. When demand drops, margins compress rapidly as fixed costs are spread over lower volumes. This operational leverage amplifies cyclical volatility.

Regulatory and environmental challenges are mounting. Steel manufacturing faces increasing environmental scrutiny with carbon taxes and emission norms tightening globally. The European Carbon Border Adjustment Mechanism could impact exports. Domestic environmental regulations are becoming stricter, requiring expensive pollution control investments. These regulatory costs could erode the 20%+ EBITDA margins that Maharashtra Seamless currently enjoys.

Dependence on oil & gas sector health creates concentration risk. Despite diversification efforts, 60%+ of revenues still come from oil and gas customers. The global energy transition toward renewables threatens long-term demand for oil and gas infrastructure. Electric vehicles reducing oil demand, renewable energy replacing gas-fired power plants, and hydrogen potentially replacing natural gas in industrial applications all pose long-term risks to pipe demand.

The Balanced View: Probabilistic Thinking

The truth, as often, lies between extremes. Maharashtra Seamless is neither a secular growth story immune to cycles nor a melting ice cube facing structural decline. It's a well-managed company in a mature industry with both opportunities and challenges.

The next 3-5 years look favorable. India's infrastructure spending is committed and funded. Oil and gas capex is recovering from decade-low levels. The company's competitive position is strong and strengthening. These factors suggest earnings could grow 15%+ annually through 2027, justifying a valuation re-rating from current levels.

The longer-term picture is more nuanced. Energy transition is real but slow—oil and gas will remain crucial for decades. India's manufacturing ambitions require massive industrial infrastructure where steel pipes are essential. Maharashtra Seamless's financial strength allows adaptation to changing market dynamics. The company will likely remain relevant, though growth rates may moderate.

Valuation Considerations

At current prices, Maharashtra Seamless trades at compelling valuations: PE ratio of 10.3 versus 5-year average of 14, EV/EBITDA of 6.5 versus industry average of 8+, and Price/Book of 1.4 despite 16% ROE. The market is pricing in significant challenges that may not materialize or may be more than offset by opportunities.

The dividend yield of 2.23% provides some downside protection. With Rs 1,300 crore in liquid investments and zero debt, the company could theoretically pay Rs 40+ per share as a special dividend while maintaining operational capacity. This balance sheet strength provides a margin of safety often absent in cyclical companies.

Risk-Reward Analysis

The asymmetry appears favorable. Downside seems limited given: asset value exceeds market capitalization, the company generates positive free cash flow even at cycle troughs, and promoters provide support through open market purchases. Meanwhile, upside potential is substantial if infrastructure spending continues, energy capex accelerates, or valuations normalize to historical averages.

The key risks to monitor include oil price collapse triggering demand destruction, Chinese dumping overwhelming anti-dumping duties, new technology making steel pipes obsolete, and execution failures in capacity expansion or M&A.

The Investment Decision

Maharashtra Seamless suits investors who can accept commodity volatility for market leadership, prefer balance sheet strength over growth promises, and have 3–5-year investment horizons rather than quarterly focus. It's not for those seeking explosive growth stories, predictable quarterly earnings, or pure-play sectoral exposure.

The current risk-reward appears favorable for patient investors. The company combines strategic positioning in essential infrastructure, financial strength to weather downturns and seize opportunities, proven management with aligned interests, and valuation providing margin of safety. While not without risks, Maharashtra Seamless offers a compelling opportunity to invest in India's infrastructure story through a financially strong, technically capable market leader trading at reasonable valuations.

XI. Epilogue & Future Outlook

The morning mist rises over the Nagothane plant as the first shift arrives. These workers—some here since the 1992 commissioning—have witnessed Maharashtra Seamless transform from a single-product startup to India's undisputed seamless pipe champion. As furnaces roar to life and steel billets begin their journey through German-designed machinery, one can't help but wonder: what comes next for this industrial titan?

Industry 4.0 and Digital Transformation

The fourth industrial revolution isn't just buzzword bingo at Maharashtra Seamless—it's operational reality taking shape. Sensors now monitor vibration patterns in the stretch reducing mills, predicting maintenance needs before breakdowns occur. Artificial intelligence algorithms optimize furnace temperatures, reducing energy consumption by 3% while improving metallurgical properties. Digital twins of critical equipment allow engineers to simulate process changes before implementation, eliminating costly trial-and-error.

But the real transformation lies ahead. The company is piloting blockchain-based quality certification, where every pipe's manufacturing parameters—temperature profiles, pressure tests, chemical composition—are immutably recorded. Customers in Houston can verify that pipes delivered to their West Texas drilling sites meet exact specifications, were manufactured on claimed dates, and underwent required testing. This transparency transforms commodity pipes into trusted products, justifying premium pricing.

Predictive analytics are revolutionizing inventory management. By analyzing historical demand patterns, weather data affecting construction schedules, and even satellite imagery of customer project sites, Maharashtra Seamless can anticipate orders before customers place them. This proactive approach reduces working capital while improving service levels—a combination that seemed impossible in traditional manufacturing.

Green Steel and Sustainability Initiatives

The global steel industry contributes 7% of worldwide CO₂ emissions—a fact that keeps forward-thinking executives awake at night. Maharashtra Seamless recognizes that sustainability isn't corporate virtue signaling but existential necessity. European customers already demand carbon footprint documentation. Indian regulations will inevitably follow. The company that masters green steel manufacturing will dominate the next decade.

The pathway to green steel is complex but clear. The company's 52.5 MW renewable energy capacity already reduces carbon intensity. Plans for additional 100 MW solar capacity could make manufacturing operations carbon neutral for electricity consumption. But the real challenge lies in the steel-making process itself, where coal-based reduction must eventually give way to hydrogen-based processes.

Maharashtra Seamless is exploring partnerships with green hydrogen producers, recognizing that first-movers will capture premium markets. The economics don't work today—green hydrogen costs 5x more than coal-based reduction. But costs are falling 15% annually. By 2030, green steel might achieve cost parity. Companies starting pilot projects now will have mastered the technology when economics turn favorable.

Water management represents another sustainability frontier. The Nagothane plant already recycles 80% of process water, but zero liquid discharge is the goal. Rainwater harvesting, improved cooling tower efficiency, and membrane-based treatment systems could eliminate freshwater dependence—crucial as water scarcity intensifies across India.

Export Potential and Global Opportunities

Maharashtra Seamless's export success—over one-third of production sold internationally—hints at greater potential. The global seamless pipe market exceeds $50 billion annually. India's share is barely 2%. As Chinese manufacturers face increasing trade barriers and environmental restrictions, opportunities emerge for Indian companies with proven quality and competitive costs.

The Middle East represents immediate opportunity. Saudi Arabia's Vision 2030 includes $500 billion in infrastructure investment. The UAE is expanding refining capacity. Iraq requires complete oil infrastructure rebuilding. Maharashtra Seamless's geographic proximity, cultural familiarity, and cost competitiveness position it perfectly for these markets. The company is establishing warehouses in Dubai and exploring joint ventures with local partners.

Africa offers longer-term potential. The continent's oil and gas discoveries—from Mozambique's offshore fields to Uganda's inland deposits—require massive pipe infrastructure. Chinese companies currently dominate through government-backed financing, but quality issues and payment delays are creating openings for Indian alternatives. Maharashtra Seamless is building relationships today that could yield major contracts tomorrow.

The real prize might be becoming a global consolidator. As energy transition pressures mount, subscale pipe manufacturers worldwide face existential challenges. Maharashtra Seamless's strong balance sheet and operational expertise could enable acquiring distressed assets in Europe or Americas, creating a truly global seamless pipe company—an Indian multinational competing with European and Japanese giants.

Next Generation Leadership

The transition from founder to next generation often destroys family businesses. Maharashtra Seamless appears to be navigating this passage successfully. Saket Jindal, the Managing Director, brings modern management approaches while respecting institutional knowledge. His focus on technology and sustainability resonates with younger employees while his respect for relationships maintains old-guard support.

The next generation faces different challenges than their parents. D.P. Jindal built the business through relationships and technical excellence. Saket must navigate digital disruption, sustainability mandates, and globalization. The skills required—data analytics, carbon accounting, cross-cultural management—differ from traditional manufacturing expertise.

Encouraging signs emerge. The company is recruiting from IITs and IIMs, bringing fresh perspectives. Young engineers are encouraged to challenge existing processes. A reverse mentoring program pairs senior executives with junior employees to understand digital trends. This cultural evolution—from hierarchical to collaborative—positions Maharashtra Seamless for future challenges.

Key Metrics and Inflection Points

Investors should monitor specific indicators for Maharashtra Seamless's trajectory. Capacity utilization above 75% signals strong demand. EBITDA margins sustaining above 20% indicates pricing power. Order book exceeding Rs 2,000 crore provides revenue visibility. Export percentage rising above 40% demonstrates global competitiveness. Renewable energy capacity reaching 100 MW shows sustainability commitment.

Critical inflection points loom. The 2025 completion of capacity expansion could add Rs 1,000 crore in revenue. Successful commissioning of the USTPL integration might improve margins by 200 basis points. A major export contract could validate global ambitions. Conversely, oil prices below $40 or China dumping despite duties could pressure near-term performance.

The biggest inflection might be valuation re-rating. If Maharashtra Seamless successfully positions itself as an infrastructure play rather than commodity company, PE multiples could expand from 10 to 15. If sustainability initiatives attract ESG investors, institutional ownership could double. If digital transformation improves returns on capital, the market might recognize this as a quality compounder rather than cyclical value trap.

The Next Chapter

As 2025 dawns, Maharashtra Seamless stands at an inflection point. The foundations—technical capabilities, financial strength, market position—are solid. The opportunities—infrastructure growth, energy expansion, global markets—are substantial. The challenges—competition, technology disruption, energy transition—are real but manageable.

The company that started with a vision of import substitution has evolved into something more significant: a demonstration that Indian manufacturing can compete globally not through labor arbitrage but through technical excellence, operational efficiency, and strategic thinking. The seamless pipes flowing from Nagothane, Mangaon, and Narketpally don't just carry oil and gas—they carry the ambitions of industrial India.

The story of Maharashtra Seamless is far from over. The next decade will determine whether it remains a successful Indian company or evolves into a global industrial champion. The pieces are in place, the strategy is clear, and the leadership is committed. What remains is execution—the patient, persistent, purposeful execution that has defined Maharashtra Seamless from the beginning.