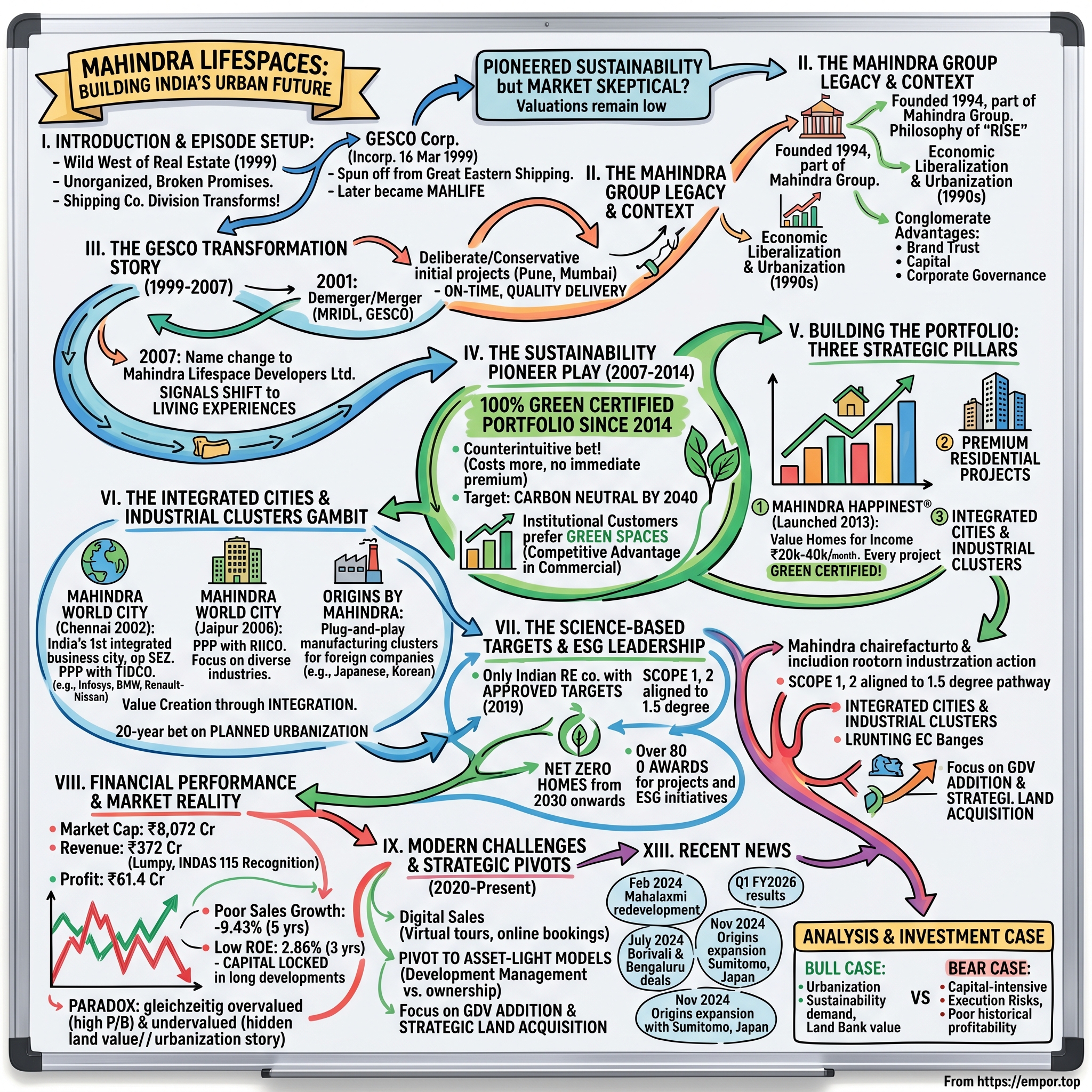

Mahindra Lifespaces: Building India's Urban Future

I. Introduction & Episode Setup

Picture this: It's 1999, and the Indian real estate sector is a wild west of unorganized players, black money, and broken promises. Against this backdrop, a shipping company's property division is about to transform into something unprecedented—a real estate developer that would pioneer sustainable urbanization in India before "ESG" became a boardroom buzzword.

GESCO Corporation Limited was incorporated as a Private Limited Company on 16 March 1999 which was converted to a Public Limited Company on 18 August 1999. GESCO was originally the real estate division of Great Eastern Shipping and was spun off into an independent company in April 1999. What started as a strategic spinoff would evolve into Mahindra Lifespace Developers Limited (MAHLIFE), one of India's most intriguing real estate stories—a company that would bet its entire future on green buildings when nobody cared, achieve a 100% sustainable portfolio, yet struggle to convince the market of its worth.

The central question isn't just how a division of a shipping company became one of India's pioneering sustainable real estate developers. It's deeper: How does a company become the first real estate company in India to have committed to the global Science Based Targets initiative (SBTi), with a 100% Green portfolio since 2014, working towards carbon neutrality by 2040, win over 90 awards for its projects and ESG initiatives, yet trade at valuations that suggest the market remains unconvinced?

This is the story of Mahindra Lifespaces—a tale of ambitious vision meeting harsh market realities, of building entire cities from scratch, and of betting that India's urbanization would reward those who thought in decades, not quarters. It's about a company that chose the hardest path in Indian real estate: transparency, sustainability, and long-term thinking in an industry notorious for the opposite.

II. The Mahindra Group Legacy & Context

The Mumbai monsoon of 1994 was particularly brutal, flooding streets and bringing the city to its knees. But inside the Mahindra towers, executives were planning something audacious—entering the real estate business at a time when organized players were virtually non-existent. The company was founded in 1994 and is part of the Mahindra Group, bringing the Mahindra Group's philosophy of 'Rise' to India's real estate and infrastructure industry.

To understand why Mahindra entered real estate, you need to understand India in the 1990s. The License Raj was crumbling, liberalization was unleashing entrepreneurial energy, and urbanization was accelerating. Yet the real estate sector remained trapped in the past—dominated by local strongmen, characterized by delayed projects, poor quality construction, and a complete absence of corporate governance. For most conglomerates, this was a sector to avoid. For Mahindra, it was an opportunity to apply manufacturing discipline to an unorganized industry.

The Mahindra Group itself was no stranger to transformation. Founded in 1945 as a steel trading company, it had evolved into one of India's most respected conglomerates, with leadership positions in automobiles, tractors, and information technology. The group's philosophy of "Rise"—enabling people to rise through technology and innovation—would find a new expression in real estate.

But why real estate? The answer lay in Mahindra's reading of India's future. With economic liberalization, millions would migrate to cities seeking opportunity. These cities would need homes, offices, and infrastructure—but more importantly, they would need planned, sustainable development. The group saw an opportunity to bring corporate credibility to a trust-deficit industry, to apply automotive manufacturing principles to construction, and to create value through patient, long-term development.

The strategic logic was compelling: real estate would benefit from Mahindra's brand trust, access to capital, corporate governance, and most importantly, its ability to think in decades—a luxury most real estate developers couldn't afford. What the group perhaps didn't fully anticipate was just how patient they would need to be.

III. The GESCO Transformation Story (1999-2007)

The story takes a dramatic turn in 1999. Great Eastern Shipping Company, one of India's largest private shipping companies, decided to focus on its core business. Its real estate division—GESCO—needed a new home. Enter Mahindra.

In 2001, GESCO Corporation and Mahindra Realty & Infrastructure Developers Ltd (MRIDL) demerged the realty and infrastructure divisions of MRIDL and merged it into GESCO. Mahindra Lifespace Developers Limited (MLDL), a Wholly Owned Subsidiary of Mahindra & Mahindra Ltd came into existence with the Demerger of the Property Development Division of Great Eastern Shipping.

The early years were about survival and credibility-building. Imagine trying to sell apartments in 2001 when the company's heritage was in shipping, its parent was known for jeeps and tractors, and customers had been burned by countless failed projects from other developers. Every sale was a battle for trust.

The company's first moves were deliberate and conservative. Small residential projects in Pune and Mumbai—markets where the Mahindra brand had recognition. Each project became a statement: delivered on time, built to quality, promises kept. In an industry where delays were the norm and quality was optional, this was revolutionary.

In 2007, the Company name was changed from Mahindra GESCO Developers Limited to Mahindra Lifespace Developers Ltd. (MLDL). This wasn't just a rebranding—it was a declaration of intent. "Lifespace" signaled a shift from building structures to creating living experiences. The company was ready to think bigger.

During these formative years, MLDL made crucial strategic decisions that would define its future. First, it decided to focus on both residential and commercial development, but with a twist—integrated developments that combined living, working, and leisure. Second, it committed to transparency and corporate governance in a sector notorious for opacity. Third, and most importantly, it began exploring sustainable development practices, though the term "green building" was still alien to most Indians.

The transformation wasn't without challenges. The company had to build an entirely new team, transitioning from shipping industry veterans to real estate professionals. It had to develop new competencies in land acquisition, project management, and customer service. Most challenging of all, it had to convince stakeholders—from investors to customers—that a Mahindra real estate company made sense.

IV. The Sustainability Pioneer Play (2007-2014)

In 2007, as India's real estate market was heating up with easy credit and soaring prices, Mahindra Lifespaces made a counterintuitive decision that would define its next decade: it would become India's green building pioneer.

The decision seemed absurd at the time. Green buildings cost 5-10% more to develop. Indian homebuyers, stretched by high property prices, showed zero willingness to pay premiums for sustainability. Even within Mahindra, there were skeptics. Why add cost when the market didn't demand it?

The answer came from an unlikely source: the automotive industry. Mahindra's automotive division had learned that global trends eventually hit India, just with a lag. Environmental consciousness, energy efficiency, regulatory requirements—all were coming. The question wasn't if, but when. By moving early, Mahindra Lifespaces could build expertise, establish supplier relationships, and most importantly, create differentiation in a commoditized market.

India's only real estate company developing 100% green certified projects since 2014. Mahindra Lifespaces has paved a unique path as a real estate developer with a 100% green-certified portfolio since 2014, working towards carbon neutrality by 2040. This wasn't a gradual transition—it was a cliff jump. Every single project, regardless of segment or geography, would be green certified.

The economics initially didn't work. Green features—solar panels, rainwater harvesting, energy-efficient fixtures—added costs that couldn't be fully passed to customers. The company absorbed these costs, betting that volumes and operational efficiencies would eventually compensate. It was a classic Mahindra move: sacrifice short-term margins for long-term positioning.

But something interesting happened. While individual homebuyers remained price-sensitive, institutional customers—particularly multinational corporations setting up offices—began showing preference for green-certified spaces. They had global sustainability commitments and needed partners who could help meet them. Suddenly, Mahindra Lifespaces' green portfolio became a competitive advantage in the commercial segment.

The Mahindra Teri Centre of Excellence was developed to reduce the footprint of the real estate industry and to influence the real estate industry and its value chain to move towards innovative and sustainable development. This culminated into strategic partnership with 'The Energy and Resources Institute (TERI)' and launch of 'Mahindra-TERI Centre of Excellence (MTCoE)'. This wasn't just about building green—it was about creating an ecosystem for sustainable development in India.

The residential market took longer to respond, but when it did, the response was unexpected. It wasn't environmental consciousness that drove customers—it was economics. Green buildings meant lower electricity bills, better water availability, and reduced maintenance costs. In cities like Bengaluru and Pune, where utility costs were rising and water was scarce, these benefits resonated. Mahindra Lifespaces had stumbled upon a truth: in India, sustainability sells when it saves money.

V. Building the Portfolio: Three Strategic Pillars

By 2010, Mahindra Lifespaces had crystallized its strategy around three distinct but complementary pillars, each targeting different aspects of India's urbanization story.

The first pillar emerged from a stark reality: India's housing shortage wasn't at the top of the pyramid—it was at the bottom. Mahindra Lifespace Developers Limited (MLDL) launched its new business vertical focused on making quality housing at affordable prices accessible to a wider cross-section of people. Happinest is aimed at families having a current, combined monthly income of Rs.20,000/- to Rs.40,000/- per month. The Happinest brand, launched in 2013, wasn't charity—it was a business model innovation.

The insight was simple but powerful: millions of Indians earning ₹20,000-40,000 monthly could afford EMIs of ₹8,000-15,000, but they couldn't accumulate the down payment. By partnering with microfinance institutions and creating innovative payment plans, Happinest made homeownership possible for auto drivers, small shopkeepers, and factory workers. The projects were smaller (400-600 sq ft), locations were peripheral, but the quality was uncompromised. Every Happinest project was green certified—probably making these the world's most sustainable affordable homes.

Mahindra Lifespaces' development portfolio comprises premium residential projects; value homes under the 'Mahindra Happinest®' brand; and integrated cities and industrial clusters under the 'Mahindra World City' and 'Origins by Mahindra' brands respectively.

The second pillar—integrated cities under the Mahindra World City brand—was the most audacious. This wasn't just real estate development; it was city-building. The model combined industrial zones, residential areas, commercial spaces, and social infrastructure into self-contained ecosystems. If Happinest was about solving India's housing shortage, World Cities were about reimagining urbanization itself.

The third pillar—Origins by Mahindra—targeted India's manufacturing ambitions. These industrial clusters provided plug-and-play infrastructure for factories, particularly targeting Japanese and Korean companies entering India. The value proposition was compelling: instead of navigating India's bureaucratic maze, companies could set up operations in pre-approved, infrastructure-ready facilities.

Each pillar reinforced the others. Industrial clusters created jobs, driving demand for affordable housing. Integrated cities attracted companies seeking comprehensive solutions for their workforce. Premium residential projects built brand credibility that helped sell affordable homes. It was ecosystem thinking applied to real estate.

VI. The Integrated Cities & Industrial Clusters Gambit

The conference room in Chennai was tense. It was 2002, and Mahindra executives were presenting their vision to Tamil Nadu government officials. They weren't proposing another residential complex or office park. They were proposing to build an entire city.

Mahindra World City is a public–private partnership promoted by the Mahindra Group and TIDCO. Mahindra World City was inaugurated on 21 September 2002 by the then Chief Minister of Tamil Nadu J. Jayalalithaa. Established in 2002, Mahindra World City Chennai is India's first integrated business city and corporate India's first operational SEZ.

The Chennai project would become the template for Mahindra's most ambitious bet. Spread across 1,500 acres, it combined three SEZs (Special Economic Zones) for IT, auto ancillaries, and apparel, along with residential zones, schools, hospitals, and hotels. This wasn't development—it was nation-building at corporate scale.

The economics were daunting. Land acquisition costs were massive. Infrastructure—roads, power, water, sewage—required upfront investment of hundreds of crores with returns expected over decades. The company essentially had to function as a municipal corporation, providing services typically handled by government. Why take on such complexity?

The answer lay in value creation through integration. A standalone factory plot might sell for ₹1,000 per sq ft. But a factory plot in an integrated city—with worker housing, schools for employees' children, hospitals, entertainment options—could command ₹1,500-2,000. Companies would pay premiums for ecosystems, not just land.

Mahindra World City is now a mature business district with leading companies such as Infosys, BMW, Braun, TTK Group, Capgemini, Renault-Nissan, Tech Mahindra, Wabco, Lincoln Electric, Wipro, Timken, and TVS Group having set up within its premises. More than 25,000 employees have found employment in this zone.

The Jaipur project, launched in 2006, took the model further. MWC Jaipur is a joint venture between Mahindra Lifespace Developers Ltd (MLDL) and Rajasthan State Industrial Development and Investment Corporation (RIICO). This 3,000-acre development targeted different industries—gems and jewelry, engineering, handicrafts—aligned with Rajasthan's strengths.

But integrated cities weren't just about economics—they were about solving India's urbanization crisis. Indian cities were growing chaotically, with infrastructure perpetually playing catch-up to growth. Mahindra's integrated cities offered an alternative: planned, sustainable, self-contained urban centers that could absorb growth without chaos.

The Company's development footprint spans 35.06 million sq. ft. of completed, ongoing and forthcoming residential projects across seven Indian cities; and over 5000 acres of ongoing and forthcoming projects under development / management at its integrated developments / industrial clusters across four locations.

The execution challenges were immense. Each city required negotiations with multiple government agencies, management of thousands of construction workers, coordination with dozens of contractors, and most challenging of all—creating social infrastructure that would make these developments livable, not just workable. It was a 20-year bet that India's manufacturing sector would grow, that companies would value integrated solutions, and that planned urbanization would win over organic chaos.

VII. The Science-Based Targets & ESG Leadership

The year 2019 marked a watershed moment. While most Indian real estate companies were focused on surviving the liquidity crisis triggered by IL&FS and demonetization, Mahindra Lifespaces made an announcement that puzzled the market: it was committing to science-based emission reduction targets.

Mahindra Lifespaces, Mahindra world City Developer(Chennai) Ltd and Mahindra World City(Jaipur) Ltd lead the way to in climate action in India. The only companies in real estate sector in India to get Science Based Targets approved by SBTi in 2019. Our Scope 1 and 2 targets are aligned to 1.5 degree pathway. SBTi approved targets are a means for reaching carbon neutrality.

This wasn't greenwashing or corporate PR. The Science Based Targets initiative (SBTi) requires companies to reduce emissions in line with climate science—what's actually needed to limit global warming to 1.5°C. For a real estate company, this meant fundamental changes to how buildings were designed, constructed, and operated.

The commitment went further. As a pioneer in Net Zero homes in India, Mahindra Lifespaces is committed to building only Net Zero homes from 2030 onwards. Another significant milestone in MLDL's journey is its commitment to construct only Net Zero buildings beginning in 2030. In an industry where most companies couldn't predict next quarter's sales, Mahindra was making decade-long commitments to carbon neutrality.

The market's reaction was tepid. Sustainability reports don't move stock prices in India. But Mahindra Lifespaces was playing a different game. It had noticed that multinational corporations were increasingly requiring their suppliers and partners to meet sustainability criteria. Indian companies wanting to be part of global supply chains would need green-certified facilities. By positioning itself as India's most sustainable developer, Mahindra was betting on becoming the default choice for ESG-conscious corporations.

Mahindra Lifespaces® is the recipient of over 80 awards for its projects and ESG initiatives. Mahindra Lifespaces® is the only Indian company to secure a place on CDP's annual 'A' list and has been awarded the 'Leadership' status. Only Indian company to receive a Double A rating by CDP for Climate Change and Water Security (2023). Conferred Global Sector Leader in Development Benchmark category by GRESB. Received the Green Champion Award by Indian Green Building Council.

The awards were nice, but the real validation came from customers. BMW chose Mahindra World City Chennai for its manufacturing facility partly due to sustainability credentials. Japanese companies, facing pressure from Tokyo to reduce supply chain emissions, preferred Origins by Mahindra industrial parks. Premium homebuyers in Bengaluru and Pune began asking about green certifications. The market was finally catching up to Mahindra's vision.

But ESG leadership came with costs. Net-zero buildings required expensive technology—solar panels, advanced HVAC systems, water recycling plants. The company had to invest in training contractors on sustainable construction practices. It had to source materials locally to reduce transportation emissions, even when imports were cheaper. Every decision had to be evaluated not just on financial metrics but on environmental impact.

The sustainability focus also created internal transformation. Employees began carpooling and segregating waste not because of mandates but because it became part of the culture. Contractors who initially resisted green requirements became evangelists after seeing reduced accidents and improved worker health at sustainable construction sites. Sustainability wasn't just a business strategy—it had become organizational DNA.

VIII. Financial Performance & Market Reality

The numbers tell a sobering story. Market Cap: ₹8,072 Crore, Revenue: ₹372 Cr, Profit: ₹61.4 Cr. Stock is trading at 4.28 times its book value. The company has delivered a poor sales growth of -9.43% over past five years. Promoter Holding: 52.4%.

For a company with such ambitious projects and sustainability leadership, these numbers raise uncomfortable questions. Why is revenue so low relative to market cap? Why has growth been negative? Why does the market value it at 4.28 times book value despite poor recent performance?

The answer lies in understanding Mahindra Lifespaces' business model. Unlike typical developers who focus on rapid turnover of projects, Mahindra's integrated cities and industrial clusters are 20-30 year developments. In accordance with INDAS 115, Company recognises its revenues on completion of contract method. This means revenues are lumpy—a project might generate no revenue for years during development, then suddenly contribute hundreds of crores upon completion.

Company has a low return on equity of 2.86% over last 3 years. This is particularly painful for investors expecting real estate companies to generate 15-20% ROEs. But again, the integrated city model explains this. Huge capital is locked in land banks and infrastructure development, generating returns over decades, not quarters.

The COVID-19 pandemic brutally exposed the model's weaknesses. Operating income during the year fell 65.0% on a year-on-year (YoY) basis. The company's operating profit decreased by 88.9% YoY during the fiscal. Operating profit margins witnessed a fall and stood at 4.0% in FY24 as against 12.5% in FY23. When economic activity stopped, industrial leasing froze. When white-collar workers went remote, commercial real estate demand evaporated. When migrant workers returned to villages, affordable housing projects stalled.

Yet there are green shoots. Mahindra Lifespace Developers Limited announced its financial results for the quarter ended 31st March 2024. Achieved pre-sales of ₹1086 Crore. We closed FY24 with our highest ever annual sales driven by successful launches throughout the year. The company is pivoting toward asset-light models, focusing on development management rather than ownership.

The financial paradox of Mahindra Lifespaces is that it's simultaneously overvalued and undervalued. Overvalued if you look at current earnings and ROE. Undervalued if you believe in India's urbanization story and the eventual monetization of its massive land banks. The market's confusion is reflected in the stock's volatility—it's been as high as ₹647 and as low as ₹255 in the past 52 weeks.

IX. Modern Challenges & Strategic Pivots (2020-Present)

The pandemic changed everything. In March 2020, construction sites shut down, sales offices closed, and migrant workers fled cities. For a capital-intensive, long-gestation business like Mahindra Lifespaces, this was an existential crisis.

But crisis forced innovation. The company pivoted to digital sales—virtual tours, online bookings, digital documentation. Happinest Kalyan leveraged a 'digital-first' approach during launch, where all bookings were accepted only online and nearly 80% of booking payments were made online. What seemed like a temporary adjustment became permanent transformation.

The affordable housing segment, surprisingly, recovered fastest. Mahindra Happinest has sold 1000 apartments amounting to 80% of the total inventory in its project 'Happinest Kalyan'. The government's push for "Housing for All," combined with stamp duty cuts and low interest rates, drove demand. Working-class families, having experienced the vulnerability of rental housing during lockdowns, prioritized homeownership.

Competition intensified from unexpected quarters. New-age proptech startups began offering end-to-end digital home buying experiences. Co-living startups targeted the same young professionals Mahindra was courting. International funds, attracted by India's urbanization potential, partnered with local developers, bringing capital and expertise.

Mahindra's response has been selective modernization. It hasn't tried to out-tech the proptechs or out-capital the funds. Instead, it's leveraged its unique strengths—the Mahindra brand trust, sustainability leadership, and integrated development expertise. The company is focusing on strategic land acquisitions in micro-markets with specific competitive advantages.

The recent strategic pivots reveal a company learning from its mistakes. The focus is shifting from ownership to development management—earning fees for managing projects rather than locking capital in land. The company is partnering with funds for capital-intensive projects, reducing balance sheet strain. Most significantly, it's accelerating project launches to improve capital turnover.

We closed the year with over ₹4400 Crore of GDV in our business development and are optimistic for the coming year given our strong pipeline of deals. The pipeline suggests renewed aggression, but with a difference. These aren't mega-cities requiring decades of development, but focused projects in established micro-markets with clear exit timelines.

X. Playbook: Lessons in Real Estate Development

The Mahindra Lifespaces story offers unique lessons for real estate development, particularly in emerging markets.

The Conglomerate Advantage: Being part of the Mahindra Group provided patient capital, brand trust, and corporate governance—critical advantages in a trust-deficit industry. But it also brought bureaucracy, conservative decision-making, and the constant need to justify real estate investments to stakeholders more familiar with manufacturing. The lesson: conglomerate backing is powerful but comes with strings.

Long-term Thinking in a Short-term Market: Mahindra's 20-30 year development horizons for integrated cities seemed visionary but proved challenging in a market obsessed with quarterly results. The company absorbed years of poor returns while building tomorrow's cities. The lesson: long-term thinking requires not just patient capital but patient investors—a rare commodity in public markets.

Building Trust in a Trust-Deficit Industry: Every on-time delivery, every green certification, every sustainability report was a deposit in the trust bank. In an industry where delays are normal and quality compromises routine, reliability became Mahindra's moat. The lesson: in industries with trust deficits, consistency and transparency are competitive advantages.

The Sustainability Premium Paradox: Mahindra discovered that Indian customers wouldn't pay premiums for environmental benefits but would pay for economic benefits that happened to be green. Lower electricity bills sold better than carbon reduction. Water security sold better than rainwater harvesting. The lesson: in price-sensitive markets, sustainability must make economic sense.

Capital Allocation in Cyclical Markets: Real estate's cyclicality brutally punished Mahindra's capital-intensive model. When markets turned, the company couldn't quickly reduce exposure. The lesson: in cyclical industries, asset-light models provide flexibility that asset-heavy models can't match.

Managing Stakeholder Complexity: Each project involved multiple stakeholders—government agencies for approvals, financial institutions for funding, contractors for execution, customers for sales. Integrated cities multiplied this complexity exponentially. The lesson: real estate isn't just about building—it's about orchestrating ecosystems.

XI. Analysis & Investment Case

The bull case for Mahindra Lifespaces rests on three pillars. First, India's urbanization is inevitable and massive—400 million people will move to cities by 2050. Second, sustainability will transition from nice-to-have to must-have, driven by regulation and corporate commitments. Third, the company's land banks and ongoing projects represent hidden value that will eventually be monetized.

The bear case is equally compelling. The company's capital-intensive model generates poor returns in a capital-scarce country. The long development cycles create massive execution risks—a project started today might complete in a very different economic environment. Most concerning, the company hasn't demonstrated it can consistently generate profits despite two decades of operations.

Against competitors, Mahindra Lifespaces occupies an unusual position. It lacks DLF's scale, Godrej Properties' execution track record, or Oberoi Realty's luxury focus. But it has something others don't—a unique positioning at the intersection of sustainability, integrated development, and affordable housing. Whether this differentiation translates to superior returns remains unproven.

The valuation puzzle persists. At 4.28 times book value, the market is pricing in significant future value creation. But with ROE at 2.86%, the company is destroying value at current operations. This disconnect suggests the market is betting on transformation—that Mahindra will eventually unlock its land banks, monetize its integrated cities, and benefit from India's urbanization.

The investment case ultimately depends on time horizon and belief. For traders and short-term investors, Mahindra Lifespaces offers little—volatile stock, unpredictable earnings, no clear catalysts. For long-term investors who believe in India's urbanization story and sustainability mega-trend, it represents an option on the future—expensive today but potentially valuable tomorrow.

XII. Future Scenarios & Strategic Options

Three scenarios could play out over the next decade, each with dramatically different implications for Mahindra Lifespaces.

Scenario 1: The Sustainability Premium Materializes

By 2030, India implements stringent building codes requiring net-zero emissions. Corporate occupiers demand green-certified spaces. Homebuyers, facing water scarcity and extreme heat, prioritize sustainable buildings. Mahindra's decade-long sustainability investments suddenly become a massive competitive advantage. The company's pipeline of net-zero projects commands premium pricing. Stock re-rates as markets recognize the value of its green portfolio. This is the dream scenario—validation of the long bet on sustainability.

Scenario 2: The Asset-Light Pivot Succeeds

Mahindra successfully transitions from developer to development manager. It partners with global funds seeking Indian exposure, earning fees for project management without capital investment. The integrated cities mature, generating steady cash flows from leasing. ROE improves dramatically as capital efficiency increases. The company becomes a play on India's real estate growth without the capital intensity. This is the pragmatic scenario—accepting market realities and adapting the business model.

Scenario 3: The Disruption Scenario

Technology disrupts traditional real estate development. Modular construction reduces development time from years to months. Digital platforms disintermediate developers, connecting land owners directly with buyers. Co-living and co-working models reduce demand for traditional real estate. Mahindra's capital-intensive, long-gestation model becomes obsolete. The company struggles to adapt, eventually breaking up into pieces—land assets sold to nimbler developers, brand licensed to others. This is the nightmare scenario—disruption making the traditional model irrelevant.

The strategic options are clear but difficult. Mahindra could double down on sustainability, betting that regulations and climate change make green buildings mandatory. It could accelerate the asset-light transition, becoming primarily a service company. It could focus on one segment—perhaps affordable housing where it has clear competitive advantages. Or it could exit real estate entirely, returning capital to shareholders.

International expansion remains tantalizingly possible but fraught with risk. Mahindra's integrated city model could work in other emerging markets—Bangladesh, Vietnam, Africa. But real estate is inherently local, and Mahindra's advantages in India might not translate abroad.

What success looks like in 2035 depends on which path Mahindra chooses. It could be India's largest sustainable developer, with a portfolio of net-zero buildings generating premium returns. It could be a real estate services powerhouse, managing developments across Asia. Or it could be a cautionary tale of ambition exceeding execution in one of the world's most challenging industries.

The next decade will determine whether Mahindra Lifespaces' patient, sustainable approach to real estate development was visionary or quixotic. The company has built the foundation—green portfolio, integrated cities, brand trust. Whether it can build a profitable business on this foundation remains the ultimate test. For investors, employees, and stakeholders, the wait continues. In Indian real estate, perhaps more than any other industry, time will tell.

XIII. Recent News

The recent months have brought significant developments that signal both continuity and change in Mahindra Lifespaces' strategy.

In February 2024, Mahindra Lifespace Developers Limited partnered with Livingstone Infra Private Limited for a cluster redevelopment project in Mahalaxmi, with a Gross Development Value of ₹1650 Crore. This marks a strategic pivot—entering South Mumbai's premium market through redevelopment rather than greenfield projects. "This development marks Mahindra Lifespaces' strategic expansion into South Mumbai's premium real estate market by creating residences that contribute to Mumbai's urban renewal", noted CEO Amit Kumar Sinha.

The momentum continued in July 2024. The company announced the closure of two deals aggregating to ₹2050 Crore in Gross Development Value, including securing a third redevelopment project in Mumbai and acquiring a prime land parcel in Bengaluru. Mahindra Lifespaces was chosen as the preferred partner for the redevelopment of seven residential societies in prestigious Borivali West, while acquiring 2.37 acres of land in Singasandra, South Bengaluru, with a developable potential of approximately 0.25 million square feet and a Gross Development Value of around ₹250 Crore.

The industrial segment saw major expansion through international partnerships. In November 2024, Mahindra World City Developers Limited announced the second phase of their Industrial Parks project in Tamil Nadu under the brand "Origins by Mahindra," in partnership with Sumitomo Corporation, Japan. This expansion marks a significant step in enhancing industrial growth in the region. The partnership's success was further validated when Mahindra Industrial Park and Sumitomo Corporation signed a Strategic Cooperation Agreement with Osaka Government to Support Japanese Businesses Entering India.

Residential launches showed strong market response. In December 2024, Mahindra announced the launch of Phase 2 of its project in Kharadi Annex, Mahindra IvyLush, strategically located in the vibrant suburb of upscale East Pune. Earlier in May 2024, Mahindra announced the launch of the final phase of Mahindra Happinest Tathawade in Pune, with most of the inventory in Phases 1, 2, and 3 nearly sold out, making it one of the fastest-selling developments in the micro-market of PCMC.

The financial performance showed mixed signals. For Q1 FY2026, the company reported total income of Rs. 40.61 crores during the period ended June 30, 2025, compared to Rs. 55.44 crores in the previous quarter, with net profit of Rs. 51.24 crores versus Rs. 85.08 crores for the period ended March 31, 2025. The sequential decline reflects the lumpy nature of real estate revenue recognition.

Most recently, in August 2025, Mahindra World City Developers leased 22.71 acres at Paranur to Ashiana Housing, and launched 166 premium residences at Lakewoods, Mahindra World City Chennai, demonstrating continued momentum in both industrial leasing and residential development.

XIV. Links & Resources

For deeper exploration of Mahindra Lifespaces' journey and current position, several resources provide valuable context:

Company Resources: - Annual Reports and Investor Presentations: Available at www.mahindralifespaces.com/investor-center/ - Sustainability Reports: Detailing the company's journey toward carbon neutrality - Project Portfolio: Comprehensive details of residential, commercial, and industrial developments

Industry Analysis: - CREDAI Reports: Indian real estate market trends and forecasts - JLL India Research: Premium insights on commercial and residential markets - Knight Frank India Reports: Detailed analysis of regional real estate dynamics - ANAROCK Property Consultants: Affordable housing market studies

Regulatory Framework: - RERA (Real Estate Regulatory Authority) Guidelines - Ministry of Housing and Urban Affairs Publications - Science Based Targets initiative (SBTi) documentation - Indian Green Building Council Standards

Academic and Research Papers: - "Sustainable Urban Development in India: Challenges and Opportunities" - various academic journals - "The Evolution of Integrated Townships in India" - urban planning studies - "Green Building Economics in Emerging Markets" - sustainability research

Books on Indian Real Estate: - "The Indian Real Estate Story" by various industry veterans - "Urban Planning and Development in India" - academic texts - Mahindra Group biographies detailing the conglomerate's evolution

Video and Media: - Management interviews on business news channels - Project walkthroughs and customer testimonials - Sustainability initiatives documentaries - Earnings call transcripts and webcasts

Competitive Intelligence: - DLF, Godrej Properties, Oberoi Realty annual reports - Industry conferences and summit presentations - Rating agency reports on Indian real estate sector

Final Thoughts: The Long Game in Indian Real Estate

The Mahindra Lifespaces story ultimately asks a fundamental question: Can patient capital and sustainable practices succeed in an industry driven by short-term cycles and quick returns?

After two decades, the answer remains frustratingly ambiguous. The company has undoubtedly built something unique—a real estate developer with impeccable sustainability credentials, a portfolio of integrated cities that represent the future of Indian urbanization, and a brand that stands for trust in a trust-deficit industry. With a Gross Development Value Addition of ₹18,100 Crore in FY25, a 4.1x year-on-year increase, the company is finally showing signs of accelerated growth.

Yet the market remains skeptical. The stock's valuation multiples suggest investors see value in the land banks and brand but question the ability to generate consistent returns. The company's transformation from asset-heavy to asset-light, from ownership to management, represents an acknowledgment that the original model, however visionary, needs adaptation to market realities.

The sustainability bet appears increasingly prescient. As Indian cities grapple with water scarcity, extreme heat, and pollution, Mahindra's green portfolio positions it well for regulatory changes and evolving customer preferences. The net-zero commitment by 2030, once seen as expensive idealism, might become a competitive necessity sooner than expected.

For investors, Mahindra Lifespaces represents a complex calculus. It's a play on India's inevitable urbanization, the growing importance of ESG criteria, and the eventual monetization of massive land banks. But it's also a bet on management's ability to execute complex projects, navigate regulatory mazes, and generate returns in a capital-intensive business.

The next decade will likely determine whether Mahindra Lifespaces becomes a case study in visionary leadership or a cautionary tale about the limits of patient capital in impatient markets. The company has built the foundation—sustainable practices, integrated developments, brand trust. Whether it can build a profitable business on this foundation while maintaining its values will define not just Mahindra's future, but potentially offer a template for sustainable development in emerging markets.

In the end, Mahindra Lifespaces embodies the tension at the heart of modern capitalism: the struggle between long-term value creation and short-term performance pressure, between doing good and doing well, between building for tomorrow and delivering today. How this tension resolves will shape not just one company's destiny, but perhaps the future of sustainable urban development in India.

The story continues, the cities keep rising, and time—as always in real estate—will tell.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube