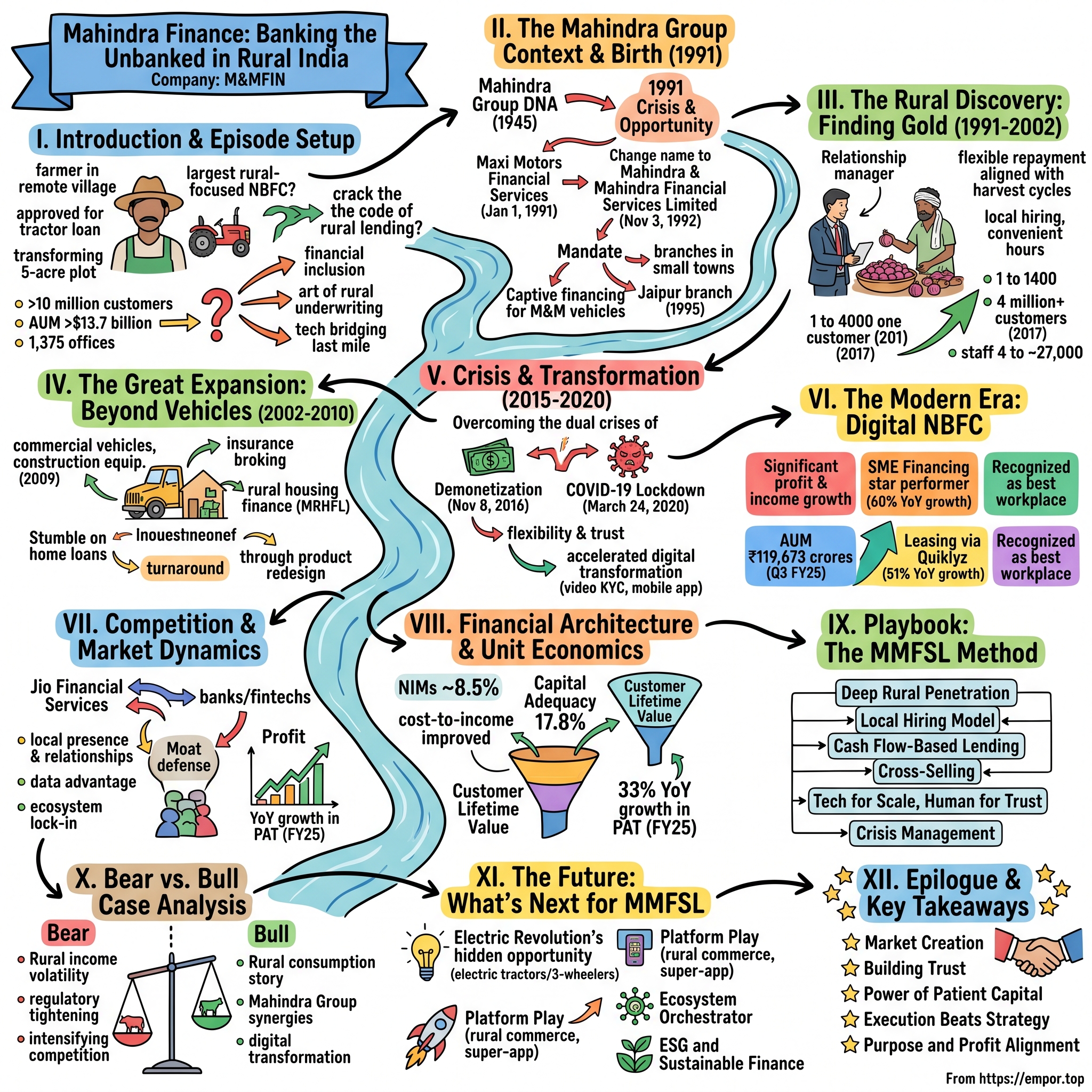

Mahindra Finance: Banking the Unbanked in Rural India

I. Introduction & Episode Setup

Picture this: A farmer in a remote village in Maharashtra, 200 kilometers from the nearest bank branch, walks into a small office with mud-splattered boots and calloused hands. He's carrying a bundle of papers—land records, harvest receipts, a letter from the local sarpanch. Within hours, he's approved for a tractor loan that will transform his 5-acre plot from subsistence to surplus. This scene plays out 50,000 times a month across India, powered by a financial services company that most urban investors have never fully understood.

Mahindra & Mahindra Financial Services—M&MFIN to the markets—has quietly built one of India's most remarkable financial franchises. With over 10 million customers and an AUM exceeding $13.7 billion, it's become the financial backbone for rural India. Yet this wasn't the plan when it started as a captive finance arm in 1991, meant simply to help sell Mahindra trucks and tractors.

The paradox is striking: How did a division created to boost vehicle sales become India's largest rural-focused NBFC? How did a company that banks wouldn't touch—operating in markets they deemed "unbankable"—build a network of 1,375 offices reaching 480,000 villages? And perhaps most intriguingly, how did they crack the code of lending to customers with no credit history, irregular income, and minimal documentation?

This is a story of transformation—from captive financier to rural banking pioneer. It's about finding opportunity where others saw only risk, building trust in communities forgotten by formal finance, and creating a business model that survived demonetization, COVID-19, and countless monsoon failures. It's also a masterclass in patient capital, strategic pivots, and the power of understanding your customer better than they understand themselves.

The key themes we'll explore: financial inclusion as competitive advantage, the art of rural underwriting, strategic diversification beyond the parent company, and how technology is finally bridging the last mile. But at its core, this is about a fundamental bet—that rural India's informal economy could be formalized, that seasonal cash flows could be understood and underwritten, and that serving the underserved could be both profitable and transformative.

What makes this particularly relevant now? As India's economy modernizes and digitizes, the battle for rural financial services is intensifying. Giants like Jio Financial Services are entering, banks are finally venturing beyond cities, and fintechs promise to disrupt traditional models. Yet Mahindra Finance maintains its moat, suggesting there's something deeper at play than just first-mover advantage.

II. The Mahindra Group Context & Birth of MMFSL

To understand Mahindra Finance, you first need to understand the DNA of its parent—a conglomerate born from post-independence optimism and industrial ambition. The Mahindra Group, founded in 1945 as Mahindra & Mohammed, embodied the Nehruvian dream of self-reliant industrialization. By the 1980s, it had become synonymous with utility vehicles, tractors, and the rugged reliability rural India demanded.

But 1991 changed everything. As India's economy opened up, foreign competition loomed. Mahindra's leadership faced a stark reality: international auto giants would soon flood the market with better financing options. The old model of cash sales and informal credit wouldn't survive liberalization. On January 1, 1991—months before the actual economic reforms—Mahindra launched Maxi Motors Financial Services Limited, a prescient move that would prove transformative. The timing was no accident. Mahindra Finance started on 1 January 1991, as Maxi Motors Financial Services Limited—six months before Finance Minister Manmohan Singh would present his historic budget liberalizing India's economy. The Mahindra leadership, particularly Vice Chairman Keshub Mahindra, had sensed the winds of change. They understood that the liberalisation process was prompted by a balance of payments crisis and that the old protectionist walls would soon crumble.

The initial mandate was straightforward: captive financing for Mahindra vehicles. Help farmers buy tractors, help small businesses buy pick-up trucks. Nothing revolutionary. Yet within this narrow remit lay the seeds of something transformative. The company received its certificate of commencement of business on 19 February 1991, and by 3 November 1992, Mahindra Finance changed their name to Mahindra & Mahindra Financial Services Limited—a signal that this was no longer just about Maxi trucks.

The early strategy debates within Mahindra's boardrooms were fierce. Conservative voices argued for staying within the safety of captive financing—why venture beyond when you have guaranteed business from the parent? But a younger cohort, influenced by global examples of GE Capital and Ford Credit, saw opportunity in independence. They argued that financing could become a profit center, not just a sales enabler.

What tipped the balance was a simple observation: Mahindra's vehicles were going to places banks wouldn't touch. The company's dealers in small towns complained that customers had cash for down payments but couldn't get loans. Banks demanded salary slips, IT returns, formal documentation—papers that a farmer with seasonal income simply didn't have. This wasn't just a financing gap; it was a chasm.

The liberalization context added urgency. As India opened up, global auto majors would enter with sophisticated financing arms. If Mahindra didn't build financial services capability now, it would lose not just financing income but vehicle sales too. The decision was made: expand beyond captive, but stay close to what you know—rural India, commercial vehicles, the informal economy.

By 1993 it commenced financing M&M utility vehicles and in 1995 started its first branch outside Mumbai, in Jaipur. That Jaipur branch—a modest office with three employees—would become the template for 1,375 branches. But that expansion, and the discovery of rural India's true potential, is where our story really begins.

III. The Rural Discovery: Finding Gold in the Villages (1991-2002)

The epiphany came in 1994, in a dusty village outside Nashik. A Mahindra Finance relationship manager, visiting to collect a delayed EMI, found the defaulting farmer not at home but at the local mandi, selling onions. The harvest had been spectacular—the farmer had cash, lots of it, but hadn't thought to pay his tractor loan first. He wasn't evading; he simply operated in a different financial universe where obligations were seasonal, not monthly.

This moment crystallized what would become Mahindra Finance's core insight: rural India didn't lack money, it lacked financial products that understood rural money. Cash flows were lumpy, tied to harvests, festivals, and agricultural cycles. A rigid monthly EMI structure designed for salaried employees made no sense for someone whose entire annual income might arrive in two harvests. Ramesh Iyer, who would become Vice Chairman and Managing Director, recounts: "We started as a captive finance company initially to finance the Mahindra range of vehicles. At that time, we did not envisage tractor finance at all but only financing of the Mahindra utility vehicles, which were predominantly sold in the rural markets of India. So, by design, we had to go out to the rural market and start understanding the opportunities and challenges."

The solution was radical for its time: flexible repayment schedules aligned with harvest cycles. Instead of 12 equal monthly installments, Mahindra Finance pioneered structures where a farmer might pay 70% of the annual obligation post-kharif and rabi harvests, with minimal payments during sowing seasons. As Professor Vijay Mahajan noted: "Companies that plan to tap rural markets should understand that farmers do not have a weekly or monthly pay cheque. They generate income only when they sell their crops. And their income is heavily dependent on the weather. Businesses need to factor in this seasonality."

Building the branch network required a complete reimagination of financial services delivery. Banks operated from 10 to 4, Monday to Friday—useless hours for a farmer who worked dawn to dusk. Mahindra Finance branches opened at 8 AM, stayed open till 7 PM, and worked Saturdays. More importantly, they hired locally—the branch manager wasn't a transferred city executive but someone who spoke the local dialect, understood local crops, knew which villages had irrigation and which depended on rain.

From one branch and a couple of customers in 1995 to 1400 branches and 4 million plus customers by 2017 was the transformation narrative. "It has been a phenomenal journey for us through these 22 years," says Ramesh Iyer, who converted the organization from just four people in the staff to some 27,000 people.

The underwriting model they developed was revolutionary. Traditional banking looked at income proof, tax returns, bank statements—documents that 80% of rural India didn't have. Mahindra Finance looked at landholding size, crop patterns, local rainfall data, and most importantly, social standing. A defaulter in rural India doesn't just lose access to credit; he loses face in his community. This social collateral often proved stronger than physical assets.

One thing they knew was that in rural India there were two sources of finance possible—the banking system and informal moneylenders. Banks were bureaucratic and distant; moneylenders were accessible but predatory, charging 36-60% annual interest. Mahindra Finance positioned itself in between—more accessible than banks, more affordable than moneylenders.

Competition was virtually non-existent, but not by accident. Other NBFCs looked at rural markets and saw only problems: no credit bureaus, no reliable income documentation, high collection costs, weather-dependent repayment capacity. Mahindra Finance saw these same challenges and recognized them as moats. Every difficulty that deterred competitors became a competency they developed.

By tracking their customers, they could spot them in 330,000 villages in the country, which is one in two villages. "That is the reach we have built," says Iyer. This wasn't just geographic expansion; it was deep market penetration, building relationships village by village, customer by customer.

The big breakthrough came in 2002 when the company began financing non-M&M vehicles. This was the moment Mahindra Finance transformed from captive financier to independent NBFC. It was also validation that their model worked—they could underwrite rural credit risk better than anyone, regardless of the vehicle brand.

IV. The Great Expansion: Beyond Vehicles (2002-2010)

The boardroom was tense in late 2008. Lehman Brothers had just collapsed, global credit markets were frozen, and India's growth story seemed suddenly fragile. Yet Mahindra Finance's leadership was discussing expansion—into commercial vehicles, construction equipment, even SME lending. "Everyone thinks we're crazy," one director reportedly said. "That's exactly why it's the right time," came the response. The company got into the business of financing commercial vehicles and construction equipment in 2009. This timing—entering new segments during global turmoil—revealed something fundamental about Mahindra Finance's strategy. While others retreated, they saw opportunity in disruption.

From 2006 to 2015 the company achieved a top line compounded annual growth rate of 26% by systematically creating new markets through new business verticals – vehicle finance, insurance, home loans and SME finance. Each expansion followed a pattern: identify an underserved segment within their existing geography, adapt the rural lending model, and scale gradually.

The insurance broking subsidiary launch represented a natural extension of the ecosystem approach. Rural customers buying vehicles needed insurance but didn't understand policies, couldn't evaluate options, and often got exploited by agents. The company offers insurance to retail customers as well as corporations through its subsidiary Mahindra Insurance Brokers Limited. By bundling insurance with loans, Mahindra Finance simplified the customer journey while earning fee income.

But the most ambitious expansion was into rural housing finance through MRHFL (Mahindra Rural Housing Finance Limited). Traditional home loans required salary slips, IT returns, and formal property titles—documents that barely existed in rural India. A farmer might own land passed down through generations with no clear title, earn seasonal income with no documentation, and want to build incrementally as cash became available.

Case A describes the growth trajectory of Mahindra Finance until 2009 when it stumbles with its new product – home loans for the rural market. The initial approach—simply copying urban home loan products with rural distribution—failed spectacularly. Default rates spiked, disbursements slowed, and critics questioned whether Mahindra Finance had overreached.

The turnaround came through radical product redesign. Instead of funding completed homes, they financed construction in stages—foundation, walls, roof—with disbursements tied to progress. "Mahindra Rural Housing Finance has developed a mortgage plan for rural areas with adaptations for this cycle. Because farmers often lack the income documentation and credit history that banks require, Mahindra came up with other criteria." They accepted alternative documentation: panchayat certificates instead of property titles, crop receipts instead of salary slips.

By incorporating specific changes to the business model in terms of the product, interest rates, repayment schedules and customer acquisition channels, the home loans segment turned around in 2010. In 2012, Mahindra Finance went on to launch yet another product – finance for small and medium enterprises – with success.

The SME financing launch leveraged everything they'd learned. Small businesses in tier-3 towns needed working capital but couldn't access bank credit. A kirana store owner might turn inventory 20 times a year but have no books to prove it. A small workshop might have steady orders but no formal contracts. Mahindra Finance developed cash flow assessment models based on observation rather than documentation—counting customer footfalls, tracking inventory movement, verifying supplier relationships.

Technology deployment during this period was deliberately low-tech but high-impact. While banks rolled out internet banking for urban customers, Mahindra Finance gave rural branches basic tablets for customer data collection. While fintechs built sophisticated apps, they focused on SMS-based payment reminders in local languages. The philosophy was consistent: technology should reduce friction, not create it.

The ecosystem approach began showing network effects. A customer who took a tractor loan might later need a pick-up truck loan for transportation, then a home loan for his expanding family, then SME financing for a small agri-processing unit. Cross-selling wasn't pushed through aggressive sales but emerged naturally as customers' needs evolved and trust deepened.

By 2010, the transformation was complete. Mahindra Finance was no longer a vehicle financier that happened to operate in rural areas. It had become rural India's financial partner, present at every milestone of economic progress. The numbers reflected this: from financing only Mahindra vehicles in 2002 to becoming among the biggest financiers of Maruti cars in rural areas, from single-product tractor loans to comprehensive financial services.

What's remarkable is how this expansion maintained the core DNA. Whether financing a tractor or a home, a Mahindra vehicle or a competitor's, the principles remained: understand cash flows not documents, build relationships not transactions, and align repayment with income patterns not calendar months. The great expansion wasn't just about adding products; it was about proving that rural finance, done right, could be both inclusive and profitable.

V. Crisis & Transformation: The Asset Quality Journey (2015-2020)

The SMS arrived at 8:47 PM on November 8, 2016: "Rs 500 and Rs 1000 notes will cease to be legal tender from midnight tonight." Within hours, 86% of India's currency by value had become worthless paper. For Mahindra Finance, with millions of rural customers who operated entirely in cash, demonetization wasn't just a disruption—it was an existential test.

Rural India ran on cash. A farmer sold his harvest for cash, paid for inputs in cash, and most importantly for Mahindra Finance, paid his EMIs in cash at branch counters. Overnight, this entire ecosystem froze. Customers had money but couldn't access it. New ₹2000 notes were scarce in villages. Digital payments, the government's intended alternative, required infrastructure that simply didn't exist—no smartphones, no internet, often no electricity.

Collection efficiency, typically above 95%, crashed to 60% within weeks. The stock market reacted brutally—shares fell 30% as analysts questioned whether the rural lending model itself was broken. "Maybe formal finance and rural India are simply incompatible," one foreign brokerage noted, downgrading the stock to sell.

But the real crisis was human. Branch managers reported heart-wrenching scenes: customers walking 20 kilometers with old notes, pleading to pay but being unable to. Others sold assets at distress prices just to get valid currency for EMI payments. The irony was crushing—a financial inclusion success story being undone by a financial inclusion policy.

Leadership's response revealed character. Instead of aggressive collection, they announced flexibility. EMI holidays were offered, penalty waivers extended. Branch staff were redeployed from collection to customer support—helping exchange notes, facilitating bank account openings, teaching digital payments. It was expensive, with provisions spiking and profits crashing, but it preserved something more valuable: trust. The recovery was slow but revelatory. There was a large immediate negative impact of demonetisation on employment, though studies showed that the impact was short lived and the economy picked up soon after. For Mahindra Finance, the crisis forced innovation. Field officers started carrying point-of-sale machines to collect digital payments. WhatsApp groups connected branch managers to share collection strategies. Most importantly, the company discovered that customers who couldn't pay during demonetization made extraordinary efforts to catch up once cash returned—social collateral remained strong.

But demonetization was just the beginning. By 2017-18, a perfect storm was brewing. Farm loan waivers announced by state governments created moral hazard—why pay if a waiver might be coming? Unseasonal rains destroyed crops. Competition intensified as banks, flush with post-demonetization deposits, aggressively entered rural lending.

Asset quality deteriorated sharply. In the quarter ended December 31, 2021, the company's net NPA (stage 3 assets), stood at 5.63 per cent under IND-AS accounting norms, while under RBI's IRACP norms, its net NPA was at around 11 per cent. The market lost faith—the stock fell 40% from its 2018 peak. Analysts questioned whether rural lending could ever be consistently profitable.

The leadership transition in 2021 marked a turning point. Raul Rebello, who joined as Chief Operating Officer in September 2021, brought fresh perspective from his experience in rural banking at Axis Bank. The strategy wasn't to abandon rural but to reimagine it through technology and data. Then came COVID-19. When India announced the world's strictest lockdown on March 24, 2020, rural India faced an unprecedented crisis. Migrant workers fled cities, local markets shut, and cash flows evaporated overnight. For Mahindra Finance, with its entire business model built on understanding rural cash flows, this was uncharted territory.

The RBI announced a moratorium—customers could defer EMIs from March 1, 2020 to May 31, 2020, later extended to August 31, 2020. A moratorium of three months on payment of all instalments including principal and/or interest components, bullet repayments, and equated monthly installments, falling due between March 1, 2020 and May 31, 2020 was permitted. For Mahindra Finance, this meant zero collections from millions of customers while interest continued to accrue.

The response revealed organizational maturity. Instead of viewing moratorium as a crisis, they treated it as an opportunity to deepen customer relationships. All eligible customers were contacted by Mahindra Finance by way of text message (SMS) on their registered mobile number. Loans approved till 31st March, 2020 with due dates falling in the moratorium period were eligible. Branch staff became counselors, helping customers understand that moratorium wasn't waiver—interest would accumulate and extend tenure.

Digital transformation, delayed for years, happened in months. Video KYC replaced physical verification. WhatsApp became a collection tool. The Mahindra Finance app, previously an afterthought, became central to customer engagement. Rural customers, forced to adopt digital payments during lockdown, suddenly became comfortable with technology.

The restructuring that followed was massive. Over three years of restructuring efforts have been pivotal in strengthening its business model. The company tightened underwriting, exited marginal geographies, and focused on quality over growth. The application of technology and data analytics has played a crucial role in transforming Mahindra Finance's risk profile.

By 2021, the transformation was evident. Collections improved, NPAs started declining, and the business model emerged stronger. The crisis had forced Mahindra Finance to evolve from a relationship-based lender to a technology-enabled financial services company that maintained its rural soul. The asset quality journey—from crisis to transformation—proved that rural lending could survive even black swan events, provided you never lost sight of your customer.

VI. The Modern Era: Digital NBFC & Market Leadership (2020-Present)

The earnings call for Q3 FY25 was electric. Analysts who had written off Mahindra Finance during COVID were scrambling to understand the transformation. Recent results show significant profit and income growth. AUM had expanded by 19% year-on-year, reaching ₹119,673 crores. But the real story wasn't the numbers—it was the complete reimagination of what a rural NBFC could be. The transformation began with a fundamental restructuring. During the quarter, the company stabilized the operating model changes brought about in the previous quarter across the Centralized processing center (CPC), and the new retail branch structure. These changes will drive improvements on efficiency, standardization, controls, customer service, and cross-sell in the future.

The numbers tell a compelling story. Mahindra Finance continues to be a leader in the tractor-financing segment, and remains the top five NBFCs for financing three-wheelers, passenger vehicles (PVs), Used passenger vehicles, light commercial vehicles (LCVs), and small commercial vehicles (SCVs). But the real growth story was in diversification. The non-vehicle finance portfolio grew by 27% over the past year.

SME financing emerged as the star performer. During the quarter, this segment delivered a Disbursement growth of 60% YoY (9MFY25 YoY growth: 60%), which drove asset book expansion by 20% on a YoY basis and was at ₹ 5,464 crore as of December 31, 2024. The secret? Moving from unsecured to secured lending. The growth is driven through its secured product offering, Loan against property (LAP) which now accounts for 42% of the overall SME assets.

The leasing business under the Quiklyz brand represented a bold bet on India's evolving consumption patterns. Instead of owning vehicles, urban millennials preferred subscriptions—monthly payments covering insurance, maintenance, everything. Leasing disbursement grew 51% YoY in Q3FY25 & 36% YoY in FY25 YTD. Rural customers, surprisingly, adopted the model for commercial vehicles, treating it as operational expense rather than capital investment.

Strategic partnerships transformed distribution. Tie-ups with SBI, Bank of Baroda, and India Post gave Mahindra Finance access to millions of customers without branch expansion costs. The India Post partnership was particularly clever—leveraging postal savings accounts in 150,000 post offices to originate loans in villages too small for bank branches.

Technology adoption accelerated beyond recognition. The company deployed AI models for credit scoring that analyzed 200+ variables—from rainfall patterns to mobile usage. Automated underwriting reduced turnaround time from days to hours. Digital collections through UPI reached 40% of total collections, unthinkable just three years ago.

But perhaps the most significant achievement was asset quality improvement. Asset quality: GS2+GS3 @ 10.2%. Stage-3 @3.9%. Credit Cost: 0.0% v/s 1.2% (Q3FY24) Capital Adequacy healthy at 17.8%, Tier-1 Capital @ 15.1%. The dramatic improvement in credit costs—from 1.2% to zero—reflected not just better underwriting but complete transformation of risk management.

In a strategic move to expand its footprint, the NBFC division of Mahindra & Mahindra continues to prioritize asset quality, as stated by Group CEO Anish Shah. Insights from recent financial results showcase Mahindra Finance's focus on diversifying and enhancing controls, marking its ambition to lead in the banking sector. Shah emphasized that the company's approach began with establishing quality benchmarks. Over three years of restructuring efforts have been pivotal in strengthening its business model and ensuring robust asset management. The application of technology and data analytics has played a crucial role in transforming Mahindra Finance's risk profile.

Recognition followed performance. Mahindra Finance received multiple recognitions during the quarter. The company was named among the best workplaces in the categories of 'Top Rated Large Company' and 'Top Rated Financial Services Company' at the AmbitionBox Employee Choice Awards 2024. It also won the 'Best Learning & Development Program of the Year - NBFC/HFC/MFI' for its Transformational Leadership Development Program at the ETBFSI Exceller Awards 2024. Additionally, it was awarded 'Best NBFC in Talent & Workforce' at the Business Today Banking and Economy Summit 2025.

The modern Mahindra Finance operates at multiple speeds. In metros, it's a digital-first subscription platform competing with startups. In tier-2 cities, it's an SME financier leveraging data analytics. In villages, it remains the trusted partner, but now armed with technology. This multi-speed model—maintaining rural roots while embracing digital transformation—positions it uniquely for India's heterogeneous growth story.

The company continues to expand into new categories beyond vehicle financing through a focus on SME lending, leasing (Quiklyz), insurance, payments, and mortgages. Each new business leverages the core competency—understanding India beyond metros—while adding new capabilities. The result is not just growth but resilience, not just scale but sustainability.

VII. Competition & Market Dynamics

The announcement sent shockwaves through the financial services industry: Jio Financial Services, backed by Mukesh Ambani's war chest and Reliance's distribution muscle, was entering rural lending. If Jio could disrupt telecom, could it do the same to rural finance? For Mahindra Finance, this wasn't just another competitor—it was an existential question about the durability of their moat.

Despite fierce competition, especially from major corporates like Jio Financial Services, Mahindra Finance maintains its leadership in rural and semi-urban domains. But why? The answer reveals something fundamental about financial services—that in lending, unlike telecom or retail, distribution is just the beginning. The real competitive advantage lies in underwriting, collections, and relationships built over decades.

Traditional banks had been trying to crack rural markets for years with mixed results. SBI, with its massive branch network, seemed best positioned. Yet they struggled with the economics—urban branches cross-subsidized rural operations, staff rotated too frequently to build relationships, and standardized products didn't fit rural needs. HDFC Bank made selective forays, cherry-picking profitable segments but avoiding deep rural penetration.

The fintech invasion brought different challenges. Companies like IndiaLends and PaySense promised instant loans through apps. Their algorithms analyzed digital footprints—social media activity, e-commerce purchases, smartphone usage. But rural India's digital footprint remained thin. A farmer might own land worth crores but have no online presence. Fintechs excelled at small-ticket personal loans but struggled with asset-backed lending that formed Mahindra Finance's core. Mahindra Finance's response to competition was counterintuitive: go deeper, not wider. While others fought for market share in tier-2 cities, Mahindra pushed into tier-4 towns and villages. Focused on financing for the agricultural sector, this NBFC benefits from its deep rural penetration and association with the Mahindra brand. Its emphasis on digital transformation is expected to drive future growth.

The moat had multiple layers. First, the distribution network—1,375 branches staffed by locals who understood crop cycles, knew which villages had good water tables, which castes dominated local politics. This granular knowledge couldn't be replicated quickly. When a competitor opened a branch, Mahindra's manager already knew every creditworthy customer by name.

Second, the data advantage. Three decades of lending had created proprietary datasets—which PIN codes defaulted during droughts, which vehicle models had better resale value in specific districts, which crops provided stable cash flows. This data, mostly unstructured and embedded in field officers' experience, powered underwriting models competitors couldn't match.

Third, the ecosystem lock-in. A customer might have a tractor loan, insurance through MIBL, a home loan through MRHFL, and fixed deposits—switching costs weren't just financial but emotional. The Mahindra Finance manager who helped during demonetization, who understood the farmer's seasonal income, who spoke the local dialect—that relationship had value beyond interest rates.

Regulatory changes added complexity. The RBI tightened NBFC regulations post-IL&FS crisis—higher capital requirements, stricter asset classification norms, enhanced disclosure requirements. These regulations, while necessary for financial stability, increased compliance costs and favored larger, well-capitalized players like Mahindra Finance over smaller NBFCs.

The competitive dynamics vary by product. In tractor financing, Mahindra Finance remains dominant, leveraging parent company synergies and deep rural presence. In personal loans, fintechs compete aggressively on speed and convenience. In SME lending, banks have the cost of funds advantage but lack the agility and local knowledge.

What's emerging is segment specialization. Bajaj Finance dominates urban consumer finance with slick technology and instant approvals. Shriram Finance owns commercial vehicle financing with specialized recovery capabilities. Mahindra Finance's specialty—rural and semi-urban asset-backed lending—remains defensible because it requires capabilities difficult to build: local presence, relationship banking, and patient capital.

The Jio Financial Services threat, while real, faces execution challenges. Building a rural lending franchise requires more than capital and technology. It needs thousands of trained staff who understand agriculture, vehicles modified for rural roads, collection infrastructure for cash payments, and most critically, trust built over decades. Jio might disrupt payments and deposits, but lending—especially secured lending in rural markets—has different dynamics.

Mahindra Finance, a part of Mahindra & Mahindra Limited, is a leading NBFC established in January, 1991. While its primary area was financing Mahindra vehicles, it has now expanded to financing rural households and small businesses as well, making it one of the key players in rural finance. This evolution—from captive financier to rural finance leader—created competitive advantages that new entrants, however well-funded, find difficult to replicate.

The future competitive landscape will likely see convergence—banks becoming more like NBFCs in product innovation, NBFCs becoming more like banks in digital capabilities, and fintechs partnering with traditional lenders for distribution. In this evolving landscape, Mahindra Finance's hybrid model—combining the reach of a bank, the agility of an NBFC, and increasingly, the technology of a fintech—positions it uniquely. The moat isn't just about being first; it's about being irreplaceable in the lives of 10 million customers who see Mahindra Finance not as a lender but as a partner in their economic journey.

VIII. Financial Architecture & Unit Economics

The numbers tell a story of transformation, but understanding Mahindra Finance's financial architecture requires looking beyond headline metrics to the underlying unit economics that drive sustainable returns. At ₹119,673 crores in AUM as of FY25, the company has built scale, but scale alone doesn't guarantee profitability in lending—the details matter.

The evolution of AUM from captive financing to a diversified portfolio reveals strategic discipline. In FY2010, 90% of assets were vehicle loans to Mahindra customers. Today, vehicle financing represents 73% of AUM, but within that, non-Mahindra vehicles account for over half. This diversification happened gradually, maintaining asset quality while expanding the addressable market.

Asset quality metrics reveal the transformation's success. Stage-3 assets at 3.9% seem high compared to private banks but are remarkable for rural lending. Credit Cost at 0.0% versus 1.2% in Q3FY24 represents not just cyclical improvement but structural changes in underwriting and collection. The dramatic improvement reflects three factors: better customer selection through data analytics, proactive restructuring before accounts turn bad, and the economic recovery in rural India post-COVID.

NIMs management showcases the balance between growth and profitability. At approximately 8.5%, NIMs are healthy but not excessive. The company consciously trades off some margin for volume and asset quality. In rural lending, trying to maximize NIMs often means adverse selection—the customers willing to pay the highest rates are often the riskiest.

The cost structure reveals operational leverage emerging. Cost-to-income ratio has improved from 45% to under 40% over five years. Branch productivity increased 30% through technology deployment. The centralized processing center handles routine operations, freeing branch staff for customer acquisition and relationship management. Digital collections reduced collection costs by 20%, though human touch remains essential for complex cases.

Capital allocation strategy balances growth, returns, and resilience. Capital Adequacy at 17.8% with Tier-1 at 15.1% provides a buffer for growth and potential stress. The company maintains higher capital than regulatory requirements, understanding that rural lending can be volatile. This conservative approach proved valuable during demonetization and COVID.

The funding mix demonstrates improving market confidence. Initially dependent on banks for funding, Mahindra Finance now accesses diverse sources—NCDs, commercial paper, external commercial borrowings, and recently, retail deposits. Cost of funds improved 150 basis points over three years as credit rating upgrades reduced borrowing costs.

ROE journey reflects the cycle. From 20%+ during boom years to single digits during crisis, now stabilizing at 15-17%. The target isn't maximizing ROE but optimizing risk-adjusted returns. The company explicitly chose lower ROE during 2018-2020 to clean up the book rather than evergreening loans to show optical profitability. The unit economics at branch level reveal the model's strength. A typical rural branch with 5-6 employees manages ₹30-40 crores in assets, generates ₹3-4 crores in revenue, and breaks even within 18 months. The low-cost structure—minimal real estate, local staff, basic infrastructure—enables profitability even in small towns. Digital adoption improved these metrics further, with cost per transaction falling 40% over three years.

Customer lifetime value calculations justify the patient approach. A customer starting with a ₹3 lakh tractor loan might generate ₹50,000 in lifetime profits through multiple products over 15 years. The upfront acquisition cost of ₹5,000 seems high, but the payback comes through relationship longevity. Rural customers, once acquired, show remarkable loyalty—churn rates below 5% annually versus 15-20% in urban markets.

The provision coverage philosophy reflects conservatism. Provision coverage on Stage 3 loans prudent at 51.2%. While this depresses near-term profitability, it provides cushion during downturns. Management explicitly states they'd rather over-provide during good times than face surprises during stress. This approach, criticized by some analysts as too conservative, proved prescient during COVID.

Cross-sell economics are increasingly important. The cost of acquiring a new customer for SME loans is ₹8,000, but cross-selling to existing vehicle loan customers costs just ₹2,000. As the customer base matures, cross-sell ratios improve—30% of customers now have multiple products, up from 10% five years ago. Each additional product improves customer ROE by 3-5 percentage points.

The technology investments, while dilutive short-term, show promising returns. Digital origination reduces processing costs by 60%. Automated underwriting improves approval rates while maintaining asset quality. AI-based collection models prioritize efforts, improving field productivity 25%. The payback period for technology investments has shortened from 5 years to 2 years.

Comparison with peers highlights the model's efficiency. While Bajaj Finance generates higher ROEs through urban consumer lending, it faces higher customer acquisition costs and competitive intensity. Shriram Finance, focused on used commercial vehicles, has better NIMs but higher credit costs. Mahindra Finance's balanced approach—moderate NIMs, controlled credit costs, steady growth—delivers consistent through-cycle returns.

The return on equity (ROE) ratio for the company stood at 9.7% during FY24. MMFSL reported a 33% year-on-year growth in Profit After Tax (PAT) for FY25. The parent company has delivered an ROE of 18% in FY25. The improvement trajectory is clear, with the company targeting 15%+ ROE by FY27 through operating leverage and normalized credit costs.

Investor returns reflect this transformation. From the 2020 lows, the stock has delivered 150%+ returns, outperforming the Nifty Financial Services index. More importantly, the volatility has reduced—beta falling from 1.5 to 1.1—as the business model stabilized. The dividend payout increased—the Board has proposed a final dividend of Rs. 6.50 per fully paid equity share, 325% of face value—signaling confidence in sustainable cash generation.

The financial architecture ultimately reflects strategic choices. By accepting lower NIMs for better asset quality, maintaining higher capital buffers, and investing in technology despite near-term dilution, Mahindra Finance has built a resilient model. The unit economics work not because of aggressive pricing or leverage but through deep customer relationships, operational efficiency, and disciplined risk management. In rural lending, as management often says, "It's not about how fast you grow, but how long you survive."

IX. Playbook: The MMFSL Method

If you had to distill Mahindra Finance's success into reproducible principles, what would emerge isn't a technology platform or a financial innovation—it's a philosophy about how to serve markets others ignore. The MMFSL method, refined over three decades, offers lessons beyond finance, applicable to any business targeting India's next billion consumers.

Deep Rural Penetration: Being First Isn't Enough

Mahindra Finance wasn't just first to rural markets; they went deeper than anyone thought profitable. While competitors stopped at district headquarters, Mahindra pushed to block levels. Today, they're present in 480,000+ villages—not through branches in each, but through a hub-and-spoke model where field officers travel daily to remote areas. The insight: in rural markets, physical presence matters more than digital presence. A customer who's never had a bank account won't trust an app, but they'll trust the person who visits their village monthly.

Local Hiring Model: Building Social Capital

The company's 27,000+ employees aren't MBAs from metros but locals who understand the nuances of their regions. The branch manager in Vidarbha knows cotton cycles, speaks Marathi with the right accent, understands which villages have water disputes. This local hiring creates natural advantages—lower attrition (employees don't want transfers), better collections (social pressure works when the collector is from the community), and superior risk assessment (knowing whose land has clear titles, whose family has a history of honoring debts).

Cash Flow-Based Lending: Seeing Money Where Others See Risk

Traditional lending looks at assets and documentation. Mahindra Finance developed models to assess cash generation capacity. A vegetable vendor with no assets might get a loan based on daily footfall at their stall. A farmer with no salary slip gets credit based on landholding, irrigation access, and crop patterns. The innovation wasn't in complex algorithms but in training field officers to observe and document informal economic activity. They turned qualitative assessment into quantitative scores.

Cross-Selling as Relationship Deepening

Unlike aggressive cross-selling in retail banking, Mahindra Finance's approach is organic. They don't push products; they wait for life events. When a tractor loan customer's daughter reaches college age, they offer education loans. When his son starts a transport business, they provide commercial vehicle finance. When the family wants to upgrade their house, home loans appear. Products follow life cycles, not sales targets.

Technology Adoption: Digital for Scale, Human for Trust

The technology strategy is deliberately hybrid. Customer acquisition and relationship management remain human-intensive. Document collection, processing, and disbursement are increasingly digital. Collections blend both—automated reminders and UPI for regular payers, field visits for delinquencies. The principle: digitize what improves efficiency without compromising trust.

Crisis Management: Turning Disasters into Moats

Every crisis—from the 2008 financial meltdown to demonetization to COVID—followed a pattern. First, immediate customer support without waiting for regulatory direction. Second, using the crisis to deepen relationships—helping customers beyond just loan deferrals. Third, improving processes based on crisis learnings. The 2016 demonetization crisis led to digital payment adoption. COVID accelerated video KYC implementation. Crises became catalysts for innovation.

The collection methodology deserves special attention. While urban lenders rely on credit bureaus and legal recovery, rural collections work differently. Field officers don't just collect EMIs; they become financial advisors. They know when harvests happen, when government subsidies arrive, when family functions require cash. They'll accept partial payments during tough months, knowing the customer will compensate during good times. This flexibility, which would seem risky in urban lending, actually reduces defaults—customers prioritize lenders who showed flexibility during distress.

The training system embeds organizational DNA. New hires spend months in villages, not classrooms. They learn to assess a farmer's credibility by looking at his cattle's health, his children's education, his standing in the panchayat. They understand that a customer missing EMIs during his daughter's wedding will resume payment afterward, but someone gambling needs immediate intervention. This tacit knowledge, impossible to codify in manuals, gets transmitted through apprenticeship.

Risk management philosophy differs fundamentally from conventional approaches. Instead of avoiding risk, they price and manage it. Lending to rainfall-dependent farmers seems risky, but spreading exposure across different crops, geographies, and seasons creates portfolio resilience. They'll take concentrated exposure in a good village rather than scattered exposure across unknown territories. Local knowledge trumps diversification theory.

The partnership approach extends beyond business. Mahindra Finance doesn't just work with dealers; they train them in financial literacy, help them manage inventory, even assist with their children's education. These dealers become evangelists, steering customers to Mahindra Finance even when competitors offer lower rates. The relationship transcends commercial transaction.

Perhaps the most important element is patience. The MMFSL method assumes relationships measured in decades, not quarters. They'll stay in an unprofitable geography for years, knowing that rural development is inevitable. They'll maintain staff in branches that barely break even, understanding that presence itself has value. They'll keep lending through agricultural crises, knowing that farmers remember who stood by them.

This playbook isn't easily replicable because it requires capabilities that take years to build and cultural commitments that markets don't always reward. But for those willing to invest the time, serve the underserved, and build trust over transactions, the MMFSL method offers a blueprint for creating value in markets where conventional business models fail.

X. Bear vs. Bull Case Analysis

The investment case for Mahindra Finance presents a fascinating study in contrasts—compelling structural tailwinds meeting cyclical headwinds, proven execution facing evolving risks. Understanding both perspectives requires examining not just the company but the broader canvas of rural India's economic transformation.

Bull Case: The Rural Consumption Story

India's rural economy, home to 65% of the population but contributing only 46% of GDP, represents one of the world's last great convergence opportunities. Per capita income in rural areas is still just 40% of urban levels. As this gap narrows—through better infrastructure, digital connectivity, and government support—the addressable market for rural finance expands exponentially.

The numbers are staggering. Tractor penetration in India is 22 per 1000 hectares versus 271 in the US. Commercial vehicle ownership in rural areas is a fraction of urban levels. Housing finance penetration in rural India is below 5% compared to 30%+ in cities. Even modest convergence implies decades of growth. Mahindra Finance, with its established presence and trust, is positioned to capture disproportionate share.

Our legacy is deeply rooted in promoting financial inclusion and making a positive impact in the lives of people across rural and semi-urban India. This isn't just corporate rhetoric—it's competitive advantage. While others talk about financial inclusion, Mahindra Finance has spent 30 years building the infrastructure to deliver it.

The Mahindra Group synergies remain underappreciated. As the parent expands—electric tractors, new vehicle models, rural infrastructure—Mahindra Finance benefits. The upcoming launch of electric three-wheelers and small electric tractors opens new financing opportunities. The group's 'Farming as a Service' initiative could transform agricultural economics, with Mahindra Finance enabling the transition.

Digital transformation is bearing fruit. The application of technology and data analytics has played a crucial role in transforming Mahindra Finance's risk profile. Cost ratios are improving, asset quality is stabilizing, and new products are scaling faster. The company that was written off as a legacy rural lender is emerging as a tech-enabled financial services platform.

Diversification reduces concentration risk. The non-vehicle finance portfolio grew by 27% over the past year. SME lending, growing at 60% annually, could become as large as vehicle finance within five years. Each new product line reduces dependence on rural vehicle cycles while leveraging existing customer relationships.

Bear Case: The Structural Challenges

Rural income volatility remains the fundamental challenge. Climate change is making monsoons more erratic. Minimum support prices for crops face fiscal constraints. Rural employment programs may not sustain as fiscal priorities shift. A single drought year can spike NPAs, as history repeatedly shows.

Under the Reserve Bank of India's Prudential Norms on Income Recognition, Asset Classification and Provisioning pertaining to Advances (IRACP), released in November last year, its net NPA was at around 11 per cent in the third quarter of the current fiscal. While asset quality has improved since, the structural vulnerability to rural stress remains.

Regulatory tightening poses ongoing challenges. The RBI's increasing focus on NBFCs post-IL&FS crisis means higher compliance costs, stricter lending norms, and reduced flexibility. The regulatory arbitrage that NBFCs enjoyed over banks is narrowing. Future regulations could mandate priority sector-like obligations without corresponding benefits.

Competition is intensifying from multiple directions. Despite fierce competition, especially from major corporates like Jio Financial Services, Mahindra Finance maintains its leadership in rural and semi-urban domains. But maintaining leadership requires constant investment in technology, people, and products—pressuring margins.

Technology disruption risk is real. While Mahindra Finance is digitizing, digital-native players move faster. A fintech leveraging India Stack—Aadhaar, UPI, Account Aggregator—could theoretically offer instant, paperless loans at lower costs. The relationship moat might erode if technology enables trust-less lending at scale.

The parent company dependence, while beneficial, creates vulnerability. Any strategic shift at Mahindra Group level—focus changes, capital allocation priorities, management transitions—impacts the finance arm. The recent focus on SUVs and electric vehicles might reduce emphasis on rural products where Mahindra Finance has maximum penetration.

Execution risks multiply with diversification. Moving from vehicle finance to SME lending to housing finance requires different capabilities. Each new product increases operational complexity. The company's historical strength—focused expertise in rural vehicle finance—gets diluted with expansion.

The Balanced View

The truth likely lies between extremes. Rural India will grow, but unevenly. Technology will disrupt, but not eliminate relationship banking. Competition will intensify, but create market expansion too. Mahindra Finance will capture opportunity, but at lower returns than history.

The key variables to watch: rural income growth rates, regulatory evolution, technology adoption in target segments, and execution on diversification. The company's track record suggests capability to navigate challenges, but past performance in a protected market doesn't guarantee future success in a competitive one.

For investors, the decision hinges on time horizon and risk appetite. Short-term investors might find the cyclical headwinds concerning—rural stress, regulatory uncertainty, competitive intensity. Long-term investors might see structural opportunity—financial inclusion, rural formalization, consumption growth—worth temporary volatility.

The investment case ultimately reflects a bet on India's rural transformation and Mahindra Finance's ability to remain relevant through that transformation. Neither is certain, but both seem probable. In that probability lies both the opportunity and the risk.

XI. The Future: What's Next for MMFSL

Standing at the threshold of 2025, Mahindra Finance faces its most intriguing chapter yet. The rural NBFC that survived demonetization and COVID must now navigate an even more complex transition—from lending to mobility, from products to platforms, from rural to rural-plus. The next decade won't be about survival but transformation.

The Electric Revolution's Hidden Opportunity

While everyone focuses on urban EV adoption, the real disruption might come from rural electrification. Electric tractors, with lower operating costs and government subsidies, could transform agricultural economics. Electric three-wheelers are already disrupting last-mile transport. Mahindra Finance's challenge: financing assets with uncertain resale values and evolving technology. The opportunity: becoming the primary enabler of rural India's electric transition.

The company continues to expand into new categories beyond vehicle financing through a focus on SME lending, leasing (Quiklyz), insurance and mortgages. But the real innovation might come from convergence. Imagine financing a farmer's electric tractor through a subscription model, bundling insurance and maintenance, with payments linked to crop yields. This isn't traditional lending—it's Farming-as-a-Service enabled by financial innovation.

The Platform Play Nobody Sees Coming

Mahindra Finance sits on a goldmine—transaction data from 10 million rural customers, relationships with 480,000 villages, trust built over decades. This positions them uniquely for platform opportunities. Not competing with Paytm or PhonePe in payments, but enabling rural commerce in ways others can't.

Consider agricultural input financing—seeds, fertilizers, pesticides constitute a ₹2 trillion market with minimal formal credit. Mahindra Finance could create a platform connecting input suppliers, farmers, and output buyers, with embedded finance throughout the value chain. They understand farming cycles, have collection infrastructure, and enjoy farmer trust—advantages no fintech can replicate quickly.

The rural fintech platform ambitions go beyond lending. The company's app could become rural India's financial super-app—not just loans but insurance, investments, government schemes, commodity prices, weather information. The constraint isn't technology but execution—can a traditional NBFC transform into a platform company?

Partnership Evolution: From Vendor to Ecosystem Orchestrator

The strategic partnerships with SBI, Bank of Baroda, and India Post were just the beginning. Future partnerships might be more transformative. Imagine exclusive financing partnerships with agricultural equipment manufacturers moving to subscription models. Or white-label lending products for rural e-commerce platforms. Or co-lending arrangements where Mahindra Finance provides origination and servicing while banks provide capital.

The India Post partnership hints at possibilities. With 150,000 post offices reaching every village, this could become the world's largest rural financial distribution network. Mahindra Finance provides products and underwriting; India Post provides distribution and trust. Together, they could reach customers no traditional financial institution can serve profitably.

ESG and Sustainable Finance: The Unexpected Growth Driver

Climate change makes sustainable finance critical for rural India. Farmers need credit for drought-resistant seeds, micro-irrigation systems, solar pumps. Small businesses need working capital for green transitions. Rural households need financing for rooftop solar, biogas plants, energy-efficient equipment.

Mahindra Finance could pioneer rural green finance. They understand agricultural risks, have relationships with farmers, and can assess sustainable farming practices' credit impact. International climate funds seeking rural deployment channels could provide low-cost capital. The company could transform from rural lender to sustainable development enabler.

The Banking License Question That Won't Go Away

Should Mahindra Finance become a bank? The advantages are clear—lower funding costs, ability to accept deposits, payments infrastructure. But banking licenses come with obligations—priority sector lending, statutory requirements, regulatory restrictions—that might constrain the agility that defines Mahindra Finance.

The answer might be selective banking. Small Finance Bank licenses allow focused operations. Payments Bank licenses enable transaction services. Or the company might remain an NBFC but deepen banking partnerships. The strategic choice will define the next decade.

Technology Architecture for the Next Billion

The technology strategy must balance sophistication with simplicity. Rural customers need intuitive interfaces, vernacular support, offline functionality. But backend systems need AI for underwriting, blockchain for supply chain finance, cloud for scalability.

Mahindra Finance is building this hybrid architecture. Customer-facing applications prioritize simplicity—WhatsApp for queries, voice-based interfaces for illiterate users, visual tools for documentation. Backend systems leverage cutting-edge technology—machine learning for risk assessment, satellite imagery for crop monitoring, alternative data for credit scoring.

The Demographic Dividend's Second Wave

India's demographic story has a rural chapter often overlooked. Rural youth, better educated than their parents but unwilling to depend solely on agriculture, are starting small businesses—mobile repair shops, coaching centers, logistics services. They need credit but don't fit traditional lending models.

Mahindra Finance could own this segment. They understand rural dynamics, have local presence, and can assess informal businesses. Products designed for rural entrepreneurs—working capital lines based on digital transaction history, equipment finance for service businesses, education loans for skill development—could drive the next growth phase.

Risk Management in an Uncertain World

Climate change, technological disruption, regulatory evolution—future risks differ from historical ones. Traditional risk models based on historical data might not capture emerging risks. Mahindra Finance needs predictive capabilities—scenario planning for climate events, stress testing for technology disruptions, regulatory impact assessments.

The company is building these capabilities, but the challenge is cultural. Risk management in uncertain environments requires comfort with ambiguity, rapid experimentation, and acceptance of intelligent failures. Can an organization built on conservative rural lending embrace calculated risk-taking?

The 2030 Vision

By 2030, Mahindra Finance might look very different. Still rooted in rural India but serving evolved needs. Not just lending but enabling—commerce, sustainability, development. Not just an NBFC but a platform connecting rural India to opportunities.

The AUM might reach ₹300,000 crores, but composition will change—30% traditional vehicle finance, 30% SME and supply chain finance, 20% rural housing, 20% new products like subscription models and embedded finance. ROE might stabilize at 18-20%, reflecting mature market dynamics but superior execution.

Most importantly, impact metrics might matter as much as financial metrics. Farmers enabled to double income, rural women becoming entrepreneurs, villages achieving energy independence—these outcomes, not just loan disbursements, might define success.

The future isn't predetermined. It depends on execution choices made today, bets placed on emerging opportunities, and most critically, the ability to remain relevant to rural India's evolving needs. Mahindra Finance has proven resilience through crisis. The next test is transformation through opportunity.

XII. Epilogue & Key Takeaways

As we conclude this deep dive into Mahindra Finance, it's worth stepping back to appreciate what this company represents in the broader narrative of Indian business and development. This isn't just a story about a financial services company that found success in rural markets—it's a case study in patient capital, market creation, and the power of serving the underserved.

MMFSL as a Case Study in Market Creation

When Mahindra Finance started operations in 1991, rural financial services wasn't a market—it was a problem. Banks saw risk, not opportunity. The government saw obligation, not business. Mahindra Finance saw differently. They didn't just enter an existing market; they created one.

From being a captive finance company, it has matured to become India's largest non-banking finance company in the semi-urban and rural areas, perhaps larger than some of the private sector banks in the country. This transformation required reimagining fundamental assumptions about lending—from documentation to assessment, from collection to relationship management.

The market creation playbook has lessons beyond finance. First, underserved doesn't mean unprofitable—it means un-understood. Second, creating markets requires patient capital and long-term thinking. Third, trust, once earned in underserved segments, becomes a powerful moat. Fourth, solving real problems creates sustainable value—Mahindra Finance didn't just provide loans; they enabled economic mobility.

Lessons on Building Trust in Underserved Markets

Trust in rural India isn't built through advertising or technology—it's earned through presence and consistency. For us, success is measured by impact—helping a farmer invest in their field, empowering an auto-rickshaw driver to own their vehicle, or supporting a small shop owner expand their business. These individuals are the foundation of our nation's progress, and we're honoured to play a role in their journey.

The trust-building methodology has universal application. Show up consistently, especially during difficulties. Speak the customer's language, literally and figuratively. Hire from the community you serve. Align your success with customer success. Be flexible in approach but consistent in presence. These principles work whether you're serving farmers in Maharashtra or small businesses in Michigan.

The Power of Patient Capital and Long-Term Thinking

In an era of quarterly earnings calls and instant gratification, Mahindra Finance's journey reminds us that some opportunities require decades to mature. They stayed in unprofitable geographies for years. They invested in relationships that took seasons to generate returns. They built capabilities that had no immediate payoff.

Mahindra Finance (MMFSL) has been making steady progress in its strategy, witnessing 40% increase in Market Cap since F21. The company's focus on asset quality has paid dividends. In F24, Mahindra Finance achieved steady improvement in its Gross Stage 3 assets achieving a record low 3.4% by year end even as it crossed 1 lakh Crore Assets Under Management.

This patient approach enabled compound advantages. Early presence created data advantages. Long relationships enabled cross-selling. Decades of trust facilitated crisis management. Patient capital, deployed intelligently, creates exponential returns—not just financial but strategic.

Why Execution Beats Strategy in Emerging Markets

Emerging markets reward execution over strategy. Everyone knew rural India needed financial services. Many tried. Few succeeded. The difference wasn't strategic insight but execution capability—the ability to hire and train thousands of field officers, to assess credit without documentation, to collect payments without legal infrastructure.

Mahindra Finance's execution excellence came from focus. Instead of trying everything, they mastered rural vehicle finance first, then carefully expanded. Instead of copying global best practices, they developed India-specific solutions. Instead of optimizing for efficiency, they optimized for effectiveness.

The execution lessons apply broadly. In emerging markets, the constraint isn't opportunity but capability. Success comes from doing simple things consistently well rather than complex things occasionally right. Building execution capability—people, processes, culture—matters more than strategic brilliance.

Final Verdict: Financial Inclusion as a Business Model

The Mahindra Finance story ultimately validates financial inclusion as a sustainable business model. Serving the underserved isn't charity—it's opportunity. The key is approaching it as business, not development—with discipline on returns, focus on sustainability, and commitment to scale.

Focused on the rural and semi-urban sector, the Company has over 10 million customers and has an AUM of over USD 13.7 Billion. The Company is a leading vehicle and tractor financier, provides loans to SMEs and also offers fixed deposits. These numbers prove that financial inclusion, done right, creates value for all stakeholders—shareholders, customers, society.

But financial inclusion as business requires different metrics. Success isn't just ROE but lives impacted. Growth isn't just AUM but geographic penetration. Quality isn't just NPAs but customer resilience built. When these metrics align—as they have for Mahindra Finance—sustainable value creation follows.

The Broader Implications

Mahindra Finance's journey has implications beyond business. It demonstrates that India's rural transformation is investible. That patient capital can generate returns while creating social impact. That business model innovation matters as much as technological innovation. That serving the underserved profitably is possible—it just requires different approaches.

For investors, the lesson is clear: look beyond metros for growth, beyond traditional metrics for value, beyond quarterly results for sustainability. For entrepreneurs: underserved markets offer opportunity if you're willing to invest time understanding them. For policymakers: enabling businesses like Mahindra Finance might achieve financial inclusion faster than direct intervention.

The Road Ahead

As India aspires to become a $7 trillion economy, rural development isn't optional—it's essential. Financial services will enable this transformation, and companies like Mahindra Finance will be central to it. The next decade will test whether they can maintain relevance while markets evolve, preserve culture while scaling operations, and balance profit with purpose.

The challenges are real—climate change affecting rural incomes, technology disrupting traditional models, competition intensifying from all directions. But so are the opportunities—a billion people entering formal finance, rural consumption converging with urban, sustainability becoming business imperative.

Mahindra Finance's story isn't finished—it's entering its most interesting chapter. From a captive finance arm to rural NBFC to whatever it becomes next, the journey reflects India's own transformation. And in that reflection lies both its relevance and its opportunity.

For three decades, Mahindra Finance has been banking the unbanked, not as charity but as business, not as obligation but as opportunity. In doing so, they've proven that serving the underserved isn't just morally right—it's economically smart. That's perhaps the most important lesson of all: that purpose and profit, when aligned correctly, create value that transcends both.

The story of Mahindra Finance is ultimately the story of trust—earned slowly, tested repeatedly, rewarded eventually. In a world of instant everything, there's something profound about a business built on showing up, season after season, monsoon after drought, crisis after recovery, until presence itself becomes promise. That's the Mahindra Finance way. That's the opportunity in serving the underserved. And that's why, despite all challenges, the future belongs to those who see possibility where others see problems.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube