Laxmi Organic: The Alchemy of Acetyls

I. Introduction & The "Invisibles"

Pick up the strip of paracetamol tablets sitting in the kitchen drawer. Run a finger along the glossy ink on the foil. Now open the medicine, swallow it with water, and trace the chain backwards. The white powder pressed into that tablet probably began its life as a clear, pungent liquid called ketene, dimerised into something called डाइकीटीन diketene, and then converted, through a series of catalytic dances, into a pharmaceutical intermediate that smells faintly of vinegar. There is a reasonable chance — perhaps better than one in three for India's domestic supply — that the molecule passed through a single, sprawling industrial site in महाड़ Mahad, a humid, monsoon-lashed industrial belt about 170 kilometres south of Mumbai.[^1]

That site belongs to लक्ष्मी ऑर्गेनिक Laxmi Organic Industries Limited, a company most retail investors had never heard of until its initial public offering on the National Stock Exchange in March 2021.[^1] Even today, despite a market capitalisation that has crossed the ten-thousand-crore mark multiple times since listing, Laxmi is what the Acquired hosts would call a "hidden compounder" — a company whose products you have touched, eaten, swallowed, and worn, almost certainly within the last twenty-four hours, without ever knowing the name on the back of the drum.

Consider the inventory of invisibility. The acetate solvent in the printing ink on a cereal box. The ester that gives a perfume its top note of pear or pineapple. The intermediate in a cough syrup, an anti-malarial, a beta-blocker. The fluorinated building block in a next-generation crop protection molecule. The electrolyte additive that one day might keep an electric vehicle battery from catching fire. Laxmi makes the things that go into the things that you use. It is, in a very literal sense, the chemistry behind the consumer.

Two numbers anchor the story. The first is roughly thirty percent — Laxmi's estimated share of the Indian Ethyl Acetate (EtAc) market, making it the country's largest producer and largest exporter of a solvent that pours, by the tanker, into pharma, packaging, paint, and adhesives plants across South Asia, Europe, and the Middle East.[^1]1 The second is approximately fifty-five percent — the share Laxmi commands in domestic Diketene derivatives, a notoriously dangerous and technically demanding chemistry that almost no one else in India has bothered to master.[^1][^5] One number describes scale. The other describes a moat.

The story of how a small distillery in coastal Maharashtra, founded in 1989 to crack ethanol into solvents, became the keystone supplier to half of India's pharmaceutical formulations and a critical node in the global agrochemical supply chain, is not a story of luck or of timing alone. It is a story of three deliberate pivots — into Diketene, into Fluorochemicals, into Specialty Intermediates — each engineered by a chairman who treats process chemistry the way Warren Buffett treats compounding interest: patiently, ruthlessly, and with an obsessive eye on the next decade.

This is the story of how रवि गोयनका Ravi Goenka and his team turned a commodity chemicals business into a specialty chemicals business — and why investors who looked past the boring acetyl label found themselves holding a front-row seat to what McKinsey has called India's "next decade" in fine and specialty chemicals.5 It is also the story of the inevitable price one pays for climbing a ladder whose bottom rungs are made of cyclical, dollar-denominated petrochemicals, and whose top rungs require billions of rupees of capital expenditure to even reach.

The hook is simple. Every two-hour Acquired episode answers one question: how did this company come to be? For Laxmi Organic, the answer reduces, after a great deal of distillation, to a single sentence — they learned the chemistry no one else wanted to learn, and then they did it again, and again.

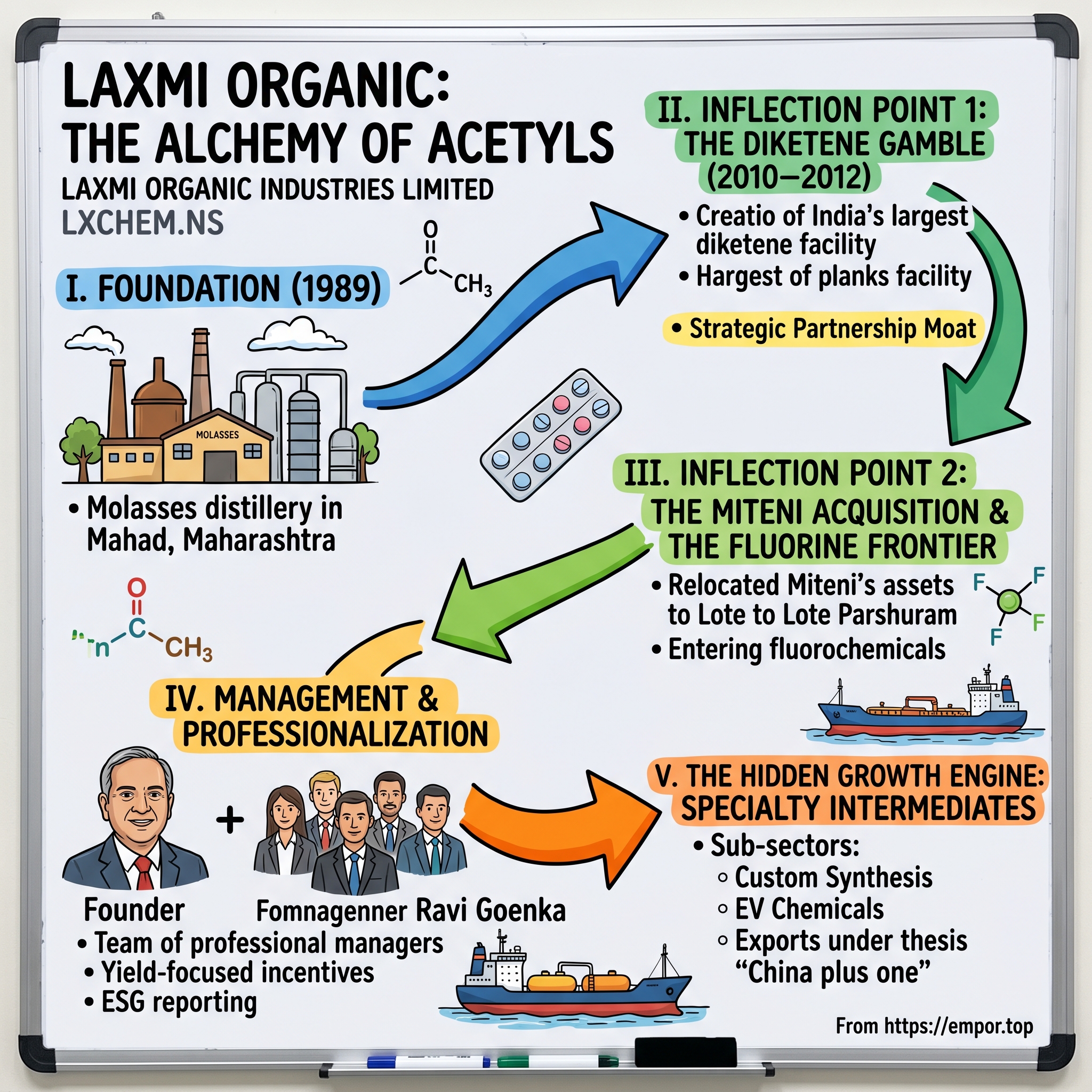

II. Foundation: The Goenka Vision

The Konkan coast in 1989 was a strange place to start a chemicals company. The Bombay High oil discoveries were two decades old, the petrochemical clusters at Vadodara and Hazira were maturing northward, and the country's solvent demand was still small enough that most ethyl acetate was either imported or made captively by alcohol distilleries on the margins of the sugar industry. Into this awkward gap stepped a fledgling outfit called Laxmi Organic Industries, set up to make acetaldehyde and ethyl acetate from molasses-based alcohol in a stretch of industrial land near Mahad, in the कोंकण Konkan belt of Maharashtra.[^1]

The name itself carried weight. Laxmi — the Hindu goddess of wealth and prosperity, traditionally invoked at the inauguration of any new family enterprise — was less a brand than a benediction. The company belonged to the Goenka family, members of the Marwari trading community that has, for over a century, supplied a disproportionate share of Indian industrial founders. The Marwari template is well documented in business school case studies: arbitrage first, manufacture second, professionalise third. Laxmi's first decade fit the pattern almost exactly. The early plants distilled ethanol, cracked it to acetaldehyde, esterified the acetaldehyde with acetic acid, and sold the resulting ethyl acetate to anyone who would write a cheque — paint companies, ink companies, the first wave of Indian generics, the early packaging converters.

It was a commodity business. Margins were thin. Working capital ate cash. And for most of the 1990s, the company was barely distinguishable from the dozens of small acetate makers dotting the Indian map. The defining shift came not from a product but from a person: the gradual, then total, ascent of रवि गोयनका Ravi Goenka into the chairman and managing director role of what was still, at heart, a family-managed enterprise.[^1]

Ravi Goenka is the kind of operator who reads a French chemical patent on a Saturday afternoon for pleasure. He trained in chemical engineering, spent time studying global specialty chemicals players, and developed what his closest collaborators describe as a near-religious belief that India's chemical industry was about to repeat what the textile industry had done a generation earlier: ride the wave of Western de-industrialisation, environmental regulation, and labour arbitrage into a structural cost advantage that could compound for thirty years.[^14] His thesis was not subtle. China had built scale through state subsidy and ecological externalisation. India would build scale through patience, process know-how, and the willingness to do the technically hard things that the Chinese capacity binge had ignored.

This sounds obvious in 2026. It was a heretical bet in the early 2000s, when Indian chemical equity multiples sat in the single digits and the consensus view was that the country could never compete on either feedstock cost or scale. Goenka's response was to refuse to compete on either. He would compete on chemistry. The first concrete expression of that thesis was the decision, around 2004, to begin moving Laxmi up the acetate value chain — from ethyl acetate, which any competent distillery could make, into ethyl-acetate derivatives and esters where formulation chemistry, food-grade purity, and pharma-grade certification could command real premiums.

By 2010, that climb had reached a plateau. Laxmi had become, by domestic standards, a serious acetate player, with multiple plants at Mahad, a growing exports book, and a balance sheet that — while not exactly investment-grade — was respectable enough to begin contemplating something bolder. The textile metaphor was still in Goenka's head, but the model was now visibly shifting. India's pharmaceutical sector was racing toward USFDA approvals and Drug Master File filings. The agrochemical formulators were beginning to invest in active ingredient capacity. The packaging industry was discovering flexography. Every single one of those end markets demanded more than ethyl acetate. They demanded clean, traceable, specialised intermediates. The opportunity, in other words, was visible. The question was whether Laxmi had the nerve to grab it.

The setting for that decision — a humid afternoon in a Mahad boardroom around the start of the 2010s — would not have looked like a turning point to a casual visitor. But the gamble that emerged from it would, within a decade, transform Laxmi from a regional acetate maker into one of the most strategically positioned mid-cap chemical companies in India, and would frame every capital allocation choice that followed.

III. Inflection Point 1: The Diketene Gamble (2010–2012)

To appreciate what Laxmi did with डाइकीटीन diketene, one first has to appreciate why almost nobody else wanted to. Diketene is what chemists politely call a "challenging molecule." Translated from the polite version, it means: it self-polymerises with enthusiasm at room temperature, it reacts with water to give acetic acid and heat (which then accelerates further decomposition), it has a vapour pressure that punishes any sloppy gasket, and it is sufficiently unstable that the international shipping community simply gave up — almost all diketene consumed globally is consumed within sight of the plant that made it, because moving it any meaningful distance involves continuous refrigeration, nitrogen blanketing, and a class of risk that most logistics companies will not underwrite at any price.

This is, paradoxically, the source of its commercial beauty. Because diketene cannot be shipped, the global market is structurally short. Pharmaceutical and agrochemical companies who need diketene-derived intermediates — acetoacetates, acetoacetamides, dehydroacetic acid, certain pigments — must either build their own diketene plant (costly, dangerous, and well outside the core competence of a pharma manufacturer) or buy from one of a small handful of specialised producers globally. In Europe, that meant Lonza and a German chemicals maker. In Japan, Daicel. In the United States, the supply was thinning by the year as Western chemical companies retreated from anything that combined high hazard with low headline glamour.9

India, in 2010, had essentially no domestic diketene capacity worth speaking of. Indian generic pharma was importing every kilogram of diketene derivative it needed. This was the gap that Laxmi spotted, and the gap into which Ravi Goenka decided to push perhaps thirty to forty percent of the company's then-available capital, with the technological partnership and licensing support that allowed the firm to commission a commercial diketene unit at Mahad in the early 2010s.[^1][^5]

The internal debate, by all accounts, was not a small one. Diketene is a chemistry that punishes complacency. A single runaway reaction can destroy a plant, kill workers, and trigger regulatory shutdowns that can cripple a mid-cap balance sheet. The case studies on diketene incidents in Europe were neither short nor cheerful. Going into this chemistry meant building not just a reactor but an entire safety culture: continuous instrumentation, redundant cooling, hazard-and-operability studies repeated on every shift change, training programmes that took new operators months rather than weeks. The capital expense was significant. The operating expense, particularly the cost of qualified manpower, was even more significant. And the time-to-payback assumed that customers — Indian pharma majors who had been comfortably importing from Europe for two decades — would actually switch.

They switched. The switch took longer than the boardroom presentations had promised, as switches always do, but by the middle of the 2010s Laxmi had become not just a domestic diketene player but, quietly, one of the larger diketene-derivatives producers in the world outside of Europe and Japan.[^5]9 More importantly, the company had crossed a threshold that the financial statements could not fully capture: it had moved from being a vendor to being a strategic partner. Pharmaceutical Drug Master Files, the regulatory documents that pin a specific manufacturer to a specific molecule in a specific finished dosage, began to list Laxmi as the source of the diketene-derived intermediate. Once a DMF is filed and an ANDA approved, changing supplier is not a procurement decision. It is a regulatory project, with months of stability data, multiple regulatory filings, and the kind of incumbency premium that academic economists call switching costs.

The Diketene gamble accomplished something more subtle than a margin uplift, though the margin uplift was real. It rewired Laxmi's customer base. The conversation with a buyer at a contract development and manufacturing organisation went from "what is your price per tonne" to "can your team co-develop a custom acetoacetamide for our discovery pipeline?" Volumes might rise more slowly, but stickiness rose dramatically. The pricing was no longer pegged to the daily ethanol benchmark on a commodity exchange but to a project-specific negotiation rooted in technical capability.

By 2018, Laxmi was being described in the trade press as the "Diketene King of India," a label that was equal parts marketing and accurate.[^5] It had done what Ravi Goenka had argued for a decade earlier: it had refused to compete on feedstock and chosen to compete on process. It would not be the last time. The company was about to make a much larger bet, on a chemistry that was even more strategic, even more difficult, and crucially, available at a deep discount from a bankrupt European seller.

IV. Inflection Point 2: The Miteni Acquisition & The Fluorine Frontier

Spinetta Marengo is a village in the Piedmont region of northern Italy, near Alessandria, where for the better part of a century the चालकोजेन chalcogen and fluorine processing site originally owned by Marzotto and later operated as Miteni made fluorinated intermediates for the European chemical industry. The plant was technically sophisticated. It was also, by the late 2010s, mired in an environmental scandal so severe that the parent company filed for bankruptcy in late 2018, leaving behind decades of perfluorinated compound (PFAS) groundwater contamination, a tangle of Italian regulatory proceedings, and a piece of physical infrastructure — reactors, distillation columns, fluorination know-how — that was, on paper, essentially worthless.

This is the kind of situation that traditional acquirers run from. The legacy environmental liability alone would deter most strategic buyers. The reputational risk of being associated with a PFAS contamination case would deter most public companies. And the practical question of what to do with a plant in northern Italy that local communities desperately wanted closed would deter almost everyone else. Laxmi Organic, with the kind of contrarian instinct that defines successful distressed-asset investors, looked at this picture and saw something different. The reactors were good. The fluorine handling expertise embedded in the engineering drawings was world-class. The supplier qualifications, the process recipes, the operating data — all of this was knowledge that would take fifteen years to recreate from scratch.

In July 2019, Laxmi Organic announced that it had agreed to acquire selected assets of Miteni, with the explicit intention of dismantling the equipment, shipping it to India, and re-erecting it at Laxmi's planned fluorochemicals site on the west coast of Maharashtra.4 The reported consideration was modest by global M&A standards — the assets, not the legal entity, were being purchased, with the Italian environmental liabilities firmly ring-fenced and left behind in the bankruptcy estate.4 In the press releases this was described as a strategic entry into fluorochemicals. In the boardroom, it was something more audacious: buying twenty years of European fluorine R&D at the price of scrap-and-shipping.

The site for the relocation was लोटे परशुराम Lote Parshuram, a chemical industrial estate further down the Konkan coast from Mahad.[^12] The choice was deliberate. Lote Parshuram is one of the few Indian industrial clusters with the combination of port access, water availability, and existing chemical infrastructure to host a hazardous fluorine plant without triggering the kind of community resistance that has stalled greenfield chemicals projects across the country. Laxmi began the painstaking work of containerising European reactors, shipping them to India, and reassembling them — a process that several industry observers described as more akin to archaeological reconstruction than industrial commissioning.[^12]

To understand why Laxmi was willing to wear this complexity, one has to understand what fluorine chemistry means for a specialty chemicals company. Fluorinated intermediates are the active building blocks for some of the most valuable molecules in modern pharma and agrochemistry. Roughly a third of newly approved small-molecule drugs contain at least one fluorine atom, and a similar proportion of next-generation crop protection chemistries depend on fluorinated cores. The reason is simple: introducing a fluorine atom into a molecule tends to increase metabolic stability, lipophilicity, and bioavailability, which is to say it makes the drug or the herbicide work better, last longer, and cost less per dose. The chemistry to introduce fluorine in a controlled, selective, scalable way is notoriously hard. The list of companies that have mastered it globally is short — Solvay, Honeywell, Daikin, AGC in the developed world, and in India, a handful of specialist players like SRF Limited, Navin Fluorine, and Gujarat Fluorochemicals.

By acquiring the Miteni assets, Laxmi was buying its way into that club. The question, naturally, was whether it had overpaid — not in the headline price, which was a fraction of a comparable greenfield build — but in the hidden cost of execution risk. A relocated plant is not the same as a new plant. Aging equipment requires recertification. Process recipes optimised for European feedstock may need to be reformulated for Indian raw materials. Operating teams trained in Mahad on acetate chemistry have to be retrained on something fundamentally more dangerous. And the regulatory environment for handling fluorinated compounds, while less stringent in India than in Italy, is tightening every year.

The comparison to SRF Limited and Navin Fluorine is instructive. Both companies built their fluorine positions over decades, with patient organic investment and a slow ladder up from refrigerant gases into specialty intermediates. Their capital deployed per kilogram of fluorine capacity is high but their execution risk is low — the equipment is new, the teams trained from day one. Laxmi chose the opposite trade-off: dramatically lower capital cost per kilogram of capacity, but a multi-year ramp during which the inherited equipment had to be reconditioned, reactor by reactor, and the workforce trained in a chemistry the company had no prior history with.

The Lote Parshuram site updates through 2023 and into 2024 suggested that the ramp was proceeding, though not without delays.[^12] The fluorochemicals contribution to revenue remained modest in early reporting periods, with management consistently framing the Fluoro Specialty (FCS) business as a multi-year build-out rather than a quarterly story.23 But the strategic logic was clear. Laxmi had moved from being a one-trick acetate company into a two-trick acetate-and-diketene company, and was now wagering its next decade on becoming a three-trick acetate-diketene-fluorine company. Each step took it further from commodity chemistry and closer to the high-margin, high-switching-cost specialty business that has made companies like SRF a benchmark of Indian industrial value creation.

Whether the Miteni gamble pays off in the way the diketene gamble did will be the defining commercial question for Laxmi over the next five years. The man making that bet, however, was no longer betting alone.

V. Management Analysis & The "Professionalized" Founder

There is a particular kind of Indian founder-chairman who runs a company the way an oil tanker captain runs a ship: hands on the wheel, eyes on the horizon, and a deep, instinctive distrust of the navigation officers, the engineers, and frankly anyone else who might be tempted to steer in their absence. The first generation Marwari industrialist archetype was built on this template. It produced extraordinary entrepreneurial energy and, equally often, the governance problems that have haunted Indian mid-cap public markets for thirty years: opaque related-party transactions, board composition padded with family members and friendly chartered accountants, capital allocation driven by ego rather than return on invested capital.

रवि गोयनका Ravi Goenka, by the testimony of investors who have sat across from him in dozens of analyst meetings, is recognisably from this tradition and recognisably trying to evolve beyond it.[^14] The Laxmi promoter group, anchored by the Goenka family, holds approximately seventy-two percent of the company's equity, a stake that places the company firmly in the "owner-operator" bucket that long-term Indian equity investors generally prefer.67 At the time of listing, this concentration was both the company's strength and the principal corporate governance question that prospective public-market investors had to weigh. A seventy-two percent promoter holding means alignment with minority shareholders is, in theory, near-perfect. It also means that if something goes wrong, minority shareholders have very limited recourse.

What Ravi Goenka chose to do in the years leading up to and following the 2021 IPO suggests he understood this tension acutely. The board was reconstituted to include independent directors with pedigree in global chemicals, finance, and audit.[^1] The senior management team was deliberately professionalised — the chief financial officer role, the head of operations, the head of strategy, the head of the fluorochemicals business — all increasingly drawn from outside the founding family, and increasingly remunerated in ways that aligned them with long-term value creation rather than short-term volume.[^1] In one of the more telling indicators, executive incentives were progressively re-anchored around what management itself describes as "yield per kilogram" rather than "volume per quarter."2 In a commodity-adjacent chemicals business, this is not a cosmetic distinction. It is the difference between chasing tonnage to fill capacity and chasing margin to fill the bank account.

Goenka's own style, by the accounts of those who have watched him present, is detail-obsessed in a way that occasionally exasperates equity analysts looking for tidy guidance. He treats the conversation about, say, Acetic Acid pricing curves the way a particle physicist treats discussions about quantum chromodynamics: with technical depth, with a certain pride in the technical depth, and with very little patience for shortcuts. The flip side is that the company's quarterly disclosures and earnings calls, particularly post-IPO, have been notably granular by Indian mid-cap chemicals standards.2 Segment-level revenue, raw material cost movements, capacity utilisation by plant, capital expenditure phasing — the kind of detail that allows fundamental investors to actually build a model rather than guess at one — has been broadly available.

The other striking feature of the management evolution is the explicit emphasis on environmental, social, and governance reporting. Laxmi published its first formal ESG report in the early 2020s and has subsequently expanded its disclosures around water consumption, hazardous waste, and process safety incidents.10 For a company in a sector where the global narrative has been dominated by PFAS contamination, hazardous waste exports, and the carbon footprint of petrochemical-derived feedstocks, this is not just a public relations exercise. It is increasingly a precondition for being on the approved vendor list of European and Japanese pharmaceutical multinationals who have, in the last five years, become extraordinarily sensitive to upstream ESG risk.

There is one structural question that hangs over the Goenka-led era and that is, by definition, not resolvable from the outside: succession. Ravi Goenka is, as of mid-2026, very much in the saddle. The next generation of the family is involved in the business, though their visible exposure has been limited. The professionalised management layer is broad enough that the business is not, technically, a one-man show. But the strategic vision that took Laxmi into diketene in 2010 and into fluorine in 2019 has, by all available evidence, originated overwhelmingly from one person.[^14] Investors comfortable with founder-led companies will read this as a strength; investors who have lived through Indian succession transitions, with all their associated dramas, will read it as the principal long-tail risk.

What is not in dispute is the cultural posture. Laxmi has positioned itself as a company that thinks in decades rather than quarters, that treats process know-how as the durable competitive asset, and that allocates capital with the kind of patience that one normally associates with private companies rather than listed mid-caps. The most concrete expression of that posture is hidden, perhaps appropriately, inside the segment that the headline numbers do not always make obvious.

VI. The "Hidden" Growth Engine: Specialty Intermediates

Walk through a Laxmi presentation in 2021, in 2023, and again in 2025, and a quiet but unmistakable rebalancing emerges. The slides dedicated to the legacy Acetyl Intermediates (AI) business — the ethyl acetate, the ethyl-acetate derivatives, the basic acetates that pay the salaries — gradually shrink. The slides dedicated to Specialty Intermediates (SI) — diketene derivatives, ketene-based custom intermediates, and increasingly the fluorochemicals book — quietly expand.3 By the most recent investor presentations, Specialty Intermediates was contributing on the order of a third of group revenue, with margins meaningfully above the company-wide blended average.23

This is the segment that does not show up in the headline narrative. AI is the cash cow. SI is the growth engine. The mathematics is straightforward and brutal at the same time. A kilogram of standard Ethyl Acetate sold into the paint and coatings industry might trade for something around the cost of an extra packet of imported coffee. A kilogram of a custom diketene-derived intermediate sold into a regulated pharmaceutical supply chain might trade for an order of magnitude more, with significantly less price sensitivity and significantly more customer lock-in. The transition from AI to SI is, in essence, a transition from selling commodities by the tanker to selling differentiated intermediates by the drum. Volumes go down. Realisations go up. Working capital intensity, somewhat counterintuitively, often falls — because specialty buyers are pharma majors with cleaner credit profiles than commodity solvent distributors.

The Specialty Intermediates story splits, on closer inspection, into three sub-stories. The first is the Diketene franchise itself, the original specialty leg, where Laxmi has continued to extend its product portfolio from basic acetoacetates into more complex acetoacetamide derivatives, dehydroacetic acid for cosmetics, and increasingly customised molecules designed in collaboration with specific pharma and agrochemical customers.[^5] The second is the Ketene-based custom synthesis business, where Laxmi acts as a contract development partner for innovator molecules — a service business with sticky multi-year contracts rather than a product business.3

The third sub-story is the youngest and, potentially, the most strategically important: what Laxmi has begun describing as Essentials & EV Chemicals. This is a deliberately broad umbrella that captures, among other things, the company's growing exposure to lithium battery electrolyte additives and to specialty solvents used in lithium-ion cell manufacturing.3 The strategic logic mirrors the diketene logic of a decade earlier. Battery electrolyte chemistry is technically demanding, the global supply is concentrated in a handful of Chinese, Japanese, and Korean producers, and the Indian electric vehicle and stationary storage ecosystem is rapidly building local cell manufacturing capacity that will need a domestic specialty solvent supply chain. If Laxmi can credibly position itself as the Indian supplier of battery-grade specialty intermediates in the way it positioned itself as the Indian supplier of diketene derivatives, the long-tail revenue stream could be transformational.

This is, to be clear, not yet a meaningful revenue contributor. Management has been careful to frame the EV Chemicals exposure as a strategic adjacency rather than a near-term earnings driver.2 The capital expenditure is being deployed in measured steps. The customer qualifications, particularly with the cell manufacturers themselves, are multi-year affairs. But the optionality is real. If domestic Indian cell manufacturing achieves anything close to the scale that government policy and private capital are currently pursuing, the specialty solvent and electrolyte additive market in India will be, in a decade, an order of magnitude larger than it is today. Whoever has the first qualifications in will inherit the structural position.

The other quiet growth lever inside Specialty Intermediates is geographic. Laxmi has been steadily building its export book, particularly into Europe and Southeast Asia, where its combination of cost competitive Indian manufacturing and regulated-market product qualifications represents a relatively rare combination.[^1]1 The strategic implication is that the Specialty Intermediates segment is no longer a purely domestic story leveraged to Indian pharma. It is, increasingly, a global story leveraged to the diversification of supply chains away from concentrated Chinese sources — the so-called "China plus one" thesis that has dominated specialty chemicals investment discourse since 2020.

If the Acetyl Intermediates business is the company's heart, providing the steady cash flow that funds everything else, the Specialty Intermediates business is the company's brain. It is where the long-term margin trajectory lives, where the customer relationships are built rather than bought, and where the chemistry that the rest of the industry finds inconvenient becomes a source of structural pricing power. To understand whether that pricing power is durable, however, one has to step back and look at the company through a more formal strategic lens.

VII. Playbook: Porter's 5 Forces & Hamilton's 7 Powers

Hamilton Helmer's 7 Powers framework, which has become something of a unofficial scripture for the Acquired audience, divides durable competitive advantage into seven distinct sources. Applied to Laxmi Organic, three of those seven powers show up unmistakably, two show up in early form, and two are essentially absent. Mapping each onto the company's actual operations clarifies a great deal about where the moat is real and where it is rhetorical.

The first and most obvious power is Process Power. Helmer defines process power as embedded company organisation and activity sets that enable lower costs and/or superior products that can only be matched by a long commitment. The handling of diketene is a textbook example. The chemistry is in textbooks, the equipment can theoretically be bought, but the actual operating capability — the layered safety culture, the trained workforce, the catalyst recipes refined over a decade of incidents and near-incidents — is genuinely tacit knowledge. A new entrant cannot replicate it by writing a cheque. The same logic, in early form, applies to the relocated fluorine chemistry at Lote Parshuram, where the embedded Italian process know-how represents a head start that competitors would need years to close.[^5]4

The second power, Scale Economies, applies in a more constrained way. In Ethyl Acetate, Laxmi's roughly thirty percent share of the Indian market gives it real advantages in raw material procurement, logistics, and fixed-cost absorption.[^1]1 These advantages are not absolute — global Ethyl Acetate pricing is set on the international commodity benchmark and a single Chinese capacity addition can erase years of margin advantage — but they are tangible enough to keep Laxmi as the default domestic supplier across multiple end markets. Outside of EtAc, the scale economics are less pronounced; in Diketene derivatives, scale matters less than process know-how, and in Fluorochemicals, Laxmi is still building toward genuine scale.

The third power, Switching Costs, is where the Specialty Intermediates story really pays off. Once Laxmi is listed as the source of a specific intermediate in a customer's regulatory filings — a Drug Master File with the USFDA, an Active Substance Master File with the European Medicines Agency, a comparable filing with one of the agrochemical regulators — changing supplier is no longer a procurement decision. It is a regulatory project, with months of stability testing, fresh impurity profiles, and the risk of triggering a regulatory review of the finished product itself. The economic value of this lock-in is substantial. It is also, importantly, asymmetric — the longer the relationship runs, the deeper the lock-in becomes, which is why customer cohort revenue at specialty chemicals companies tends to grow even when overall industry pricing is weak.

The remaining four powers are weaker but worth noting. Branded Power does not really apply at the molecular level — pharma buyers do not buy on the strength of a brand but on the strength of a regulatory filing. Network Economies are essentially absent in B2B intermediates. Counter-Positioning — the inability of incumbents to copy without harming their existing business — is a power Laxmi could, in theory, claim in the relocation of European fluorine assets to Indian cost structures, since established European fluorine players cannot match Indian operating costs without dismantling their own businesses. Cornered Resource does not apply in the classical sense; ethanol, acetic acid, and the various petrochemical inputs are all globally traded commodities.

Now turn to Porter's classic five forces. The picture is more mixed and more interesting. Bargaining power of suppliers is the structural weakness of the business. Acetic acid is a globally traded petrochemical whose price moves with crude oil, the Chinese methanol-to-acetic-acid balance, and global natural gas dynamics.[^1]3 Ethanol pricing is anchored to Indian molasses and sugar policy, which moves on its own logic of monsoon outcomes and minimum support prices for sugarcane farmers. Neither feedstock can be hedged out cleanly, and both can compress margins materially in a bad quarter. Bargaining power of buyers is moderate; pharma and agrochemical majors have leverage, but the regulatory lock-in described above offsets some of that leverage on specialty molecules.

Threat of new entrants is the structurally favourable force. The combination of capital intensity, hazardous chemistry, environmental clearances, and regulatory qualifications creates entry barriers that are far higher than in most Indian manufacturing sectors. A new domestic diketene entrant would need not just capital but five to ten years of qualification work to displace incumbents. Threat of substitutes is low for most of Laxmi's product mix; the alternative to a specific diketene-derived intermediate is, generally, a different and worse synthetic route.

Industry rivalry is the most context-dependent force, varying dramatically across product lines. In Ethyl Acetate, rivalry is high and largely structural — Indian acetate producers fight a global commodity cycle that they do not control. In Diketene derivatives, rivalry is low and Laxmi enjoys an oligopoly-like position. In Fluorochemicals, rivalry is high but the market is growing fast enough that all credible players can grow simultaneously for some years to come. Industry observers have been quick to highlight the China plus one tailwind as a structural positive — major Western and Japanese specialty chemical buyers have been actively de-risking their Chinese exposure for half a decade, and Indian players with the right product portfolios are the natural beneficiaries.5

The strategic upshot is that Laxmi's moat is product-line specific. The deepest moats sit around Diketene chemistry and increasingly around Fluorine chemistry. The shallowest sit around legacy Ethyl Acetate. The implication for investors is straightforward: the mix shift away from AI and toward SI is, in 7 Powers terms, a mix shift from the shallow end of the company's moat to the deep end. Whether that mix shift continues, accelerates, or stalls is the central operational question.

VIII. Analysis: The Bear vs. Bull Case

Every fundamental equity story breaks down, eventually, into a competing pair of plausible futures. Laxmi Organic is no exception. The bull case and the bear case are not symmetrically weighted, but both are honestly arguable, and a thoughtful investor benefits from holding both in mind at the same time.

The bull case begins, naturally, with the FCS ramp. If the relocated and recommissioned fluorochemicals platform at Lote Parshuram reaches its planned capacity utilisation and begins generating the kind of realisations associated with global specialty fluorine players — broadly speaking, the difference between a kilogram of commodity acetate at perhaps two dollars and a kilogram of specialty fluorinated intermediate at twenty dollars and upward — the segment-level contribution to group EBITDA could become, over a multi-year horizon, comparable to or larger than the legacy Acetyl Intermediates business.3[^8] This is the transformation that Motilal Oswal's coverage and other sell-side initiations have generally placed at the heart of the multi-year thesis on the stock.[^8] The bull does not need everything to go right; the bull needs the FCS business to mature into something resembling SRF's mid-cycle specialty chemicals economics, and for the existing Diketene franchise to continue compounding at mid-teens revenue growth with margin expansion.

The China plus one tailwind reinforces the bull case. Global pharmaceutical and agrochemical supply chain diversification away from concentrated Chinese sourcing has, since the COVID-19 disruption of 2020, become not a slogan but an active procurement priority at most multinational buyers.5 Indian specialty chemicals players with regulatory qualifications, environmental compliance, and demonstrated execution capability are the structural beneficiaries. Laxmi's Diketene and emerging Fluorine positions both sit squarely in the categories where European and American buyers most actively seek non-Chinese sources. The bull thesis treats this not as a quarterly tailwind but as a decade-long structural mix shift.

The optionality on EV Chemicals — battery electrolyte additives, specialty solvents for cell manufacturing, intermediates for cathode and anode chemistries — is, in the bull case, a free option layered on top of the core thesis.3 If Indian cell manufacturing capacity reaches the scales currently being publicly discussed by government and private investors, Laxmi's early positioning could compound into a third major specialty leg. If it does not, the company has not bet the farm on the outcome.

The bear case begins with the cyclicality of the legacy business. Acetic Acid is a global petrochemical whose price can move thirty or forty percent in a quarter, and Ethyl Acetate margins follow with painful predictability.[^1] For all the strategic narrative around Specialty Intermediates, the AI business still contributes the majority of group revenue and a meaningful share of group EBITDA. A sustained downturn in global acetate spreads can compress group margins faster than the specialty business can scale to compensate. This is not a hypothetical risk; it is the lived experience of Indian acetate producers across multiple historical cycles.

The execution risk at Lote Parshuram is the second leg of the bear case. Relocating a European fluorine plant to India is, in practical terms, a multi-year engineering project layered on top of a multi-year operating learning curve, layered on top of a multi-year customer qualification cycle.[^12] Each of those layers has historically taken longer than initial guidance suggested at companies pursuing comparable transitions. A delay of one or two years in the FCS ramp does not destroy the thesis, but it does materially compress the present value of the cash flows the bull case relies on.

The third bear consideration is competitive. Laxmi is not the only Indian specialty chemicals player chasing the China plus one opportunity. Jubilant Ingrevia, born from the demerger of Jubilant Life Sciences, has its own large acetyl-and-specialty platform and competes directly in several of Laxmi's adjacencies. गोदावरी बायोरिफाइनरीज Godavari Biorefineries plays in the alcohol-and-acetate value chain with a different feedstock strategy. The fluorochemicals space is occupied by SRF Limited, Navin Fluorine International, and Gujarat Fluorochemicals, each of which has years of head start on Laxmi's relocated Italian assets. The market is large enough for multiple winners, but the competitive pressure on capital allocation and pricing is real.

Benchmarked against these peers, Laxmi's position is best characterised as the lowest-cost optionality play in the specialty chemicals universe. It does not have SRF's scale in fluorine. It does not have Navin Fluorine's pure-play purity. It does not have Jubilant Ingrevia's integrated nutrition and life sciences breadth. But it bought into its high-margin chemistries at a fraction of the capital cost that any of those peers paid for theirs, and it sits on a Diketene franchise that none of them can easily replicate. The bull would describe this as the most asymmetric risk-reward in the Indian specialty chemicals mid-cap universe. The bear would point out that asymmetric risk-reward is, by definition, a polite way of saying high variance.

The myth versus reality angle is worth pausing on. The consensus narrative around Laxmi, particularly post-IPO, was that this was a fluorochemicals story with optionality on EV chemicals — a high-multiple specialty platform that just happened to have a legacy acetate business attached. The reality is closer to the inverse: a profitable, cyclical acetate platform that is incrementally building a specialty engine on top of itself, with the specialty engine growing fast enough that the mix shift becomes financially meaningful only on a multi-year view. Investors who expected fluorine to dominate the P&L within a year or two of listing have, predictably, been disappointed. Investors who expected the patient compounding that the management consistently described have been less so.

For the long-term fundamental investor, the bear-and-bull stack reduces to a relatively narrow set of variables to track. Watching the right ones is more important than parsing every quarterly headline.

IX. Epilogue & Closing Thoughts

There is a certain poetry in the trajectory. A small distillery on the Konkan coast, founded the year India's economic liberalisation was still two years away, started by cracking molasses-based ethanol into a few thousand tonnes of low-margin acetaldehyde and ethyl acetate, finds itself, three and a half decades later, dismantling a European fluorochemicals plant and reassembling it on the same stretch of coastline to make twenty-dollar-per-kilogram intermediates for global pharma. The compounding here is not financial in any abstract sense. It is chemical, geographic, and human. Each pivot built on the last. Each piece of process knowledge bought time and option value for the next piece. Each customer qualification opened the door to ten more.

The Indian chemical renaissance — the broader story within which Laxmi sits — is real, and it is also unevenly distributed. The McKinsey work that has framed much of the institutional thesis on the sector projects a multi-fold expansion of Indian specialty chemicals revenue over the next decade, driven by China plus one, by domestic pharma growth, and by the structural advantages of Indian labour, engineering talent, and increasingly serious environmental compliance.5 But that aggregate growth will not lift every Indian chemicals company evenly. The winners will be those that have done the patient, unglamorous work of building genuine process moats, qualifying with regulated customers, and reinvesting cash flow into capabilities that compound. Laxmi has done the first two more clearly than most of its peer group. The third is the question of the next five years.

The most useful frame for tracking the company going forward reduces, by this writing, to perhaps two or three operational metrics that genuinely matter and that the financial statements actually disclose. The first is the revenue mix between Acetyl Intermediates and Specialty Intermediates — the trajectory of that ratio, more than any single quarterly margin print, captures whether the strategic transformation is on track. The second is the realised gross margin on the specialty business specifically, particularly the Fluorochemicals contribution as Lote Parshuram ramps. The third, somewhat less obvious, is capital expenditure intensity relative to incremental revenue generated — a metric that will tell investors whether the patient capital allocation philosophy the company has espoused is actually being practised, or whether the inevitable temptation toward larger and showier projects is starting to dilute returns. Two to three KPIs, no more. The rest is noise.

The deeper lesson, the one that the Acquired hosts return to in almost every episode of their long-running show, is that durable businesses are built by people who think in decades and execute in quarters. लक्ष्मी ऑर्गेनिक Laxmi Organic, through the patient idiosyncratic vision of रवि गोयनका Ravi Goenka and a small group of professionalised executives around him, has spent the better part of two decades climbing a value chain that almost no one else wanted to climb. The reward has been a company that, at any given moment, looks superficially like a boring acetate maker and, on closer inspection, turns out to be something rather more interesting: a quiet, technically competent compounding machine, hidden in plain sight inside the chemistry of every Indian medicine, every printed package, and every bottle of nail polish remover one might happen to come across.

The next chapter — the one where Fluorochemicals either delivers on its promise or does not, where EV Chemicals either becomes the next Diketene or does not, where the next generation of Goenka management either inherits the patient process culture or does not — has not yet been written. The previous chapters, however, suggest that whatever does come next, the company writing it has earned the right to be taken seriously. That, for a humble distillery from coastal Maharashtra, is the alchemy. The real philosopher's stone, it turns out, was always the slow, careful, unglamorous mastery of chemistry that no one else wanted to do.

References

References

-

Laxmi Organic Investor Relations — Annual Reports & Filings ↩↩↩

-

Q3 FY24 Earnings Call Transcript — Laxmi Organic Industries, February 2024 ↩↩↩↩↩

-

Investor Presentation — Laxmi Organic Industries, May 2024 ↩↩↩↩↩↩↩↩

-

Laxmi Organic to Acquire Miteni Assets in Italy — Reuters, 2019-07-22 ↩↩↩

-

Specialty Chemicals: The India Opportunity — McKinsey & Company ↩↩↩↩

-

Corporate Governance and Board Composition — National Stock Exchange of India ↩

-

The Global Diketene Market Outlook — Fortune Business Insights ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube