Lux Industries: From Kolkata Hosiery to India's Innerwear Empire

I. Introduction & Episode Roadmap

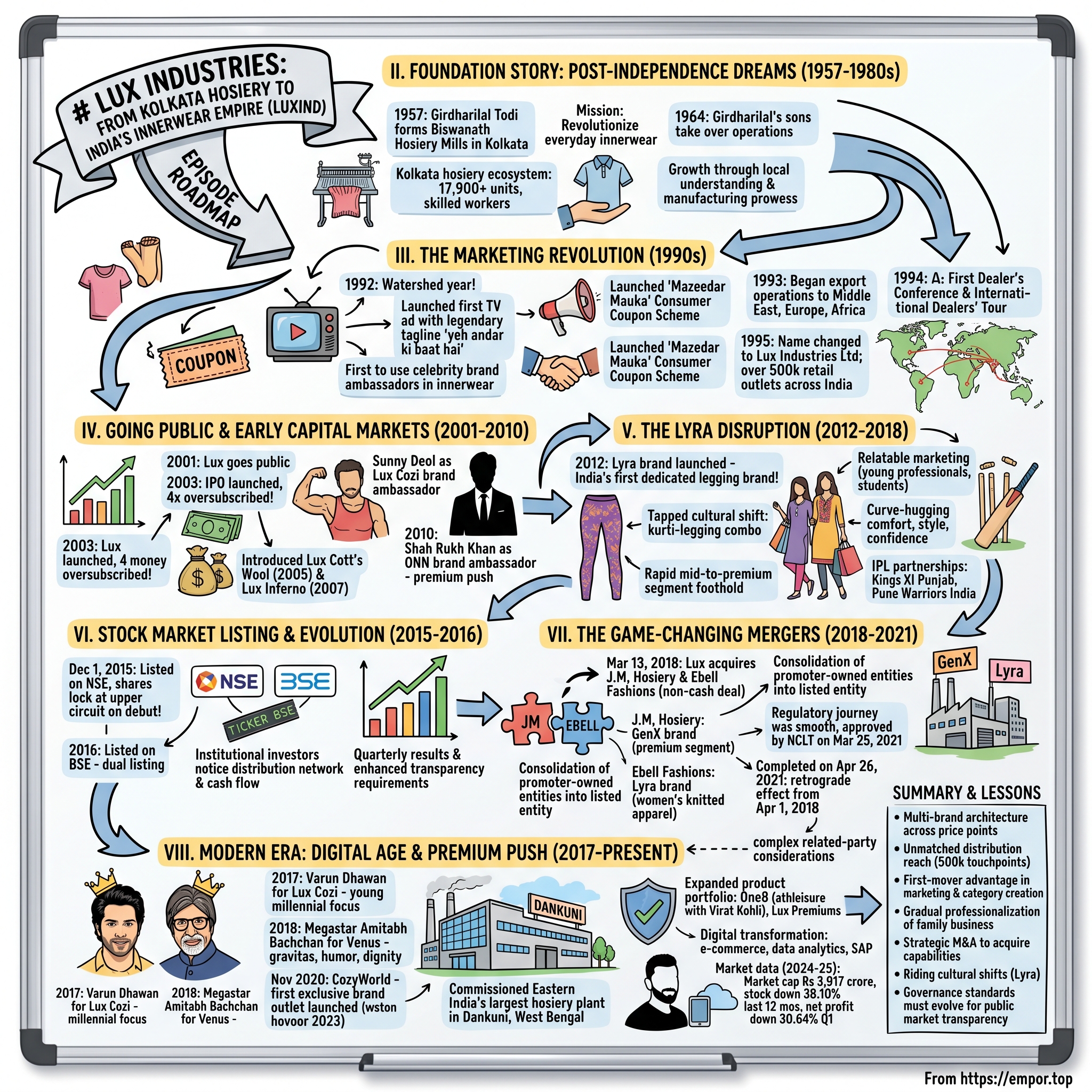

Picture this: A modest hosiery mill in the bustling lanes of 1950s Kolkata, where the rhythmic clatter of knitting machines mingles with the dreams of post-independence India. In 1957, Girdharilal Todi embarked on a mission to revolutionize everyday innerwear comfort for Indians by establishing Biswanath Hosiery Mills. What started as one man's vision to provide dignity and comfort to the common Indian has transformed into an innerwear empire spanning 500,000 retail touchpoints across the subcontinent.

Today, Lux Industries stands with a market capitalization of Rs 3,917 crore, commanding approximately 15% of India's organized innerwear market. With seven manufacturing facilities churning out products, 1,150+ dealers spreading the brand's reach, and exports to over 46 countries, the company has become synonymous with "comfort" in Indian households. Yet behind this success lies a fascinating saga of marketing innovation, family dynamics, strategic mergers, and the occasional governance controversy.

This is the story of how a family from Kolkata's traditional Marwari business community transformed a commodity product—the humble vest and underwear—into aspirational brands that have clothed three generations of Indians. It's a tale of being first: first to use celebrity endorsements in innerwear, first to launch consumer coupon schemes, first to create a dedicated women's leggings brand. But it's also a cautionary tale about navigating family business transitions, related-party transactions, and the challenges of maintaining governance standards in a public company.

From the sons taking over from their father in 1964 to the third generation now steering the ship, from that game-changing "yeh andar ki baat hai" tagline to Amitabh Bachchan's recent endorsements, from a small Kolkata mill to Eastern India's largest hosiery plant—this is the Acquired-style deep dive into Lux Industries, where marketing genius meets manufacturing scale, and where the most intimate of garments became the foundation of a business empire.

II. Foundation Story: Post-Independence Manufacturing Dreams (1957-1980s)

The year was 1957. Jawaharlal Nehru's vision of a self-reliant India echoed through the industrial corridors of Kolkata, then the commercial capital of newly independent India. The birthplace of the Indian Hosiery Industry and of Bengal Hosiery Industry was incidentally the same – the city of Kolkata, where pioneers had established the first hosiery factory as early as 1893. Into this ecosystem stepped Girdharilal Todi, a man with modest means but immodest ambitions.

The timing couldn't have been more challenging—or more opportune. Import restrictions imposed by the newly-formed government of India had changed the game, as hosiery products had been imported from Hong Kong and Japan in large quantities in the pre-Independence era, which continued till as late as 1955 under the open license policy. These restrictions created a vacuum in the market, one that domestic manufacturers rushed to fill.

Girdharilal didn't just see a business opportunity; he saw a chance to clothe the common man with dignity. The hosiery industry in Bengal had already weathered tremendous storms. The industry had to sail through turbulent waters during the two world wars, tensions and anxieties of foreign competition in the twenties, great depression of thirties, birth pangs of independence and holocaust of partition. Yet it had survived, even thrived. After World War II, the hosiery industry in the region expanded exponentially, but in an unplanned way.

In 1964, Girdharilal's sons took over the operating responsibilities, marking the beginning of a crucial transition. The second generation—Kishan Kumar Todi, Ashok Kumar Todi, and Pradip Kumar Todi—brought fresh energy and ambition to the enterprise. They weren't content with just running a mill; they wanted to build a brand.

The next two decades witnessed extraordinary growth through sheer manufacturing prowess and local market understanding. The next 20 years saw the company growing 100 times in size through a series of marketing and manufacturing innovations. This wasn't just organic growth—it was explosive expansion driven by an understanding that innerwear, despite being hidden from view, could be marketed as aspirationally as any visible garment.

The Kolkata textile ecosystem provided unique advantages. Kolkata and its surroundings had around 17,900 hosiery units, which included major brands such as Amul, Lux, Rupa. This hosiery sector employed a workforce of more than 1 lakh, and produced around 180 million kg of hosiery goods. The density of skilled workers, the proximity to cotton supplies from eastern India, and the entrepreneurial spirit of the Bengali business community created a perfect storm for growth.

But success in the License Raj era required more than just manufacturing capability. It demanded an ability to navigate complex regulations, manage scarce foreign exchange for importing machinery, and build relationships with distributors who controlled access to retail markets. The Todi family excelled at this delicate dance, slowly building a network that would become one of their most valuable assets.

By the late 1980s, Biswanath Hosiery Mills had established itself as a reliable player in the regional market. The foundation was set, the manufacturing capabilities were proven, and the second generation had demonstrated their ability to scale the business. What came next would transform not just the company, but the entire Indian innerwear industry.

III. The Marketing Revolution: Building a Consumer Brand (1990s)

The year 1992 marked a watershed moment—not just for Lux Industries, but for the entire Indian innerwear industry. While economic liberalization was opening India's doors to the world, the Todi family was orchestrating a marketing revolution that would forever change how Indians thought about their undergarments.

The company launched the Consumer Coupon Scheme in 1992, branded as "Mazedar Mauka," and in the same year became the first company in the industry to employ celebrity brand ambassadors. Think about the audacity of this move: in a country where innerwear was purchased discreetly, often by women for their entire families, wrapped in newspaper to hide the embarrassment, here was a company putting it on television for the entire nation to see.

The masterstroke came with their first television commercial. In 1992, Lux launched their first television commercial with the famous "yeh andar ki baat hai" tagline. Those four words became cultural shorthand, a phrase that transcended its commercial origins to enter everyday parlance. The genius lay not in what it said, but in what it didn't say—it acknowledged the taboo while simultaneously breaking it, creating a shared secret between the brand and millions of Indian consumers.

The "Mazedar Mauka" consumer coupon scheme was equally revolutionary. In an era before loyalty programs and cashbacks, Lux created a direct relationship with end consumers, bypassing the traditional wholesaler-retailer stranglehold. Customers could collect coupons from product purchases and redeem them for gifts—a simple idea that created massive brand stickiness and repeat purchases.

The following year, 1993, saw the company launch their export operations, quickly establishing offices in the Middle East, Europe, and Africa. This wasn't just about finding new markets; it was about learning global quality standards and bringing that expertise back to India. The export push forced the company to upgrade its manufacturing processes, improve quality control, and think beyond the traditional Indian consumer.

In 1994, Lux organised the first Dealer's Conference in the Indian hosiery industry and also established the industry's first International Dealers' Tour. While competitors were still treating dealers as necessary evils, Lux was treating them as partners, investing in relationships that would pay dividends for decades. These conferences became legendary in the trade, with dealers from small towns getting their first international trips, creating emotional bonds that no competitor could easily break.

The culmination of this transformative period came in 1995. The company changed its name to Lux Industries Limited, signaling its evolution from a manufacturing unit to a consumer brand. This was followed by the establishment of over 500,000 retail outlets across India, with offices in Kolkata, Delhi, Agra, Indore, Mumbai, Ludhiana, Jaipur, and Roorkee.

The distribution achievement deserves special attention. In a pre-digital era, without modern logistics infrastructure, Lux created a network that reached from metropolitan cities to rural villages. They understood that innerwear purchasing in India happened everywhere—from air-conditioned malls to roadside stalls—and they needed to be present at every touchpoint. This wasn't just distribution; it was democratization of access to quality innerwear.

By the end of the 1990s, Lux had accomplished something remarkable. They had taken a product category that nobody talked about and made it a topic of conversation. They had transformed a commodity into a brand. Most importantly, they had laid the groundwork for what would become one of India's most successful IPOs in the consumer goods sector.

IV. Going Public & Early Capital Markets Journey (2001-2010)

The dawn of the new millennium brought with it a critical decision for the Todi family: should they remain a closely-held family business or tap into the capital markets for growth? In 2001, Lux went public and for the first time, ownership of the company was available outside of the Todi family. This wasn't just a financial transaction—it was a fundamental shift in how the company would operate, bringing with it new responsibilities, scrutiny, and opportunities.

The Lux Industries IPO was launched in 2003, garnering significant attention from investors. The overwhelming response led to an oversubscription of four times, highlighting the trust and confidence the market had in the brand's potential for growth. In an era when most IPOs struggled to get fully subscribed, Lux's offering was a testament to the brand equity built over the previous decade.

The IPO's success wasn't accidental. By 2003, Lux had already established itself as a household name. The celebrity endorsement strategy was in full swing, with Sunny Deol engaged as Lux Cozi's brand ambassador. The choice of Sunny Deol—the embodiment of masculine strength in Bollywood—was strategic. It positioned Lux Cozi not just as comfortable innerwear but as the choice of strong, confident men.

The capital raised from the IPO fueled ambitious expansion plans. New manufacturing facilities were established, technology was upgraded, and the product portfolio expanded beyond basic vests and briefs. The company introduced Lux Cott's Wool in 2005 and Lux Inferno in 2007, targeting the growing thermal wear segment. Each product launch was backed by substantial marketing investment, reinforcing the brand's premium positioning.

A pivotal moment came in 2010 when Shah Rukh Khan was engaged as brand ambassador for ONN. The signing of Bollywood's biggest star signaled Lux's ambitions to move beyond the mass market into premium segments. ONN was positioned as the choice of the modern, urbane Indian man—a significant departure from the traditional, value-focused positioning of the core Lux brand.

With consistent consumer satisfaction, Lux Industries witnessed a positive growth of over 100% in just 20 years. This wasn't just numerical growth; it was a transformation in scale, scope, and ambition. The company had successfully navigated the transition from family-owned to professionally-managed, from regional to national, from manufacturer to brand.

The period also saw important organizational changes. Professional managers were brought in to complement family members in key positions. Systems and processes were strengthened to meet the compliance requirements of a listed company. The board was expanded to include independent directors, bringing fresh perspectives and governance oversight.

Yet beneath the surface of this success story, tensions were emerging. The challenge of balancing family control with public ownership, of maintaining entrepreneurial agility while ensuring corporate governance, would become increasingly apparent in the years ahead. But for now, Lux Industries stood at the threshold of its next big leap—one that would take it from being a men's innerwear company to a complete wardrobe solutions provider.

V. The Lyra Disruption: Creating a Women's Wear Revolution (2012-2018)

Lyra was launched as a women's wear brand of Lux Industries Ltd. in the year 2012. But calling it just another brand launch would be missing the revolution it represented. Lyra was the first legging brand in the country—not just from Lux, but the first dedicated leggings brand in India, period.

The timing was impeccable. India was experiencing a cultural shift. The traditional salwar-kameez was giving way to the kurti-legging combination as the everyday wear of choice for millions of young Indian women. Western wear was becoming acceptable in offices, colleges were seeing more women students, and the workforce participation of women was rising. Into this transformation, Lux dropped Lyra like a perfectly timed beat in a song.

Lux Industries transformed the women's bottom wear segment, with Lyra becoming one of the company's remarkable success stories. In a very short span of time, Lyra successfully established its foothold in the mid to premium segment. The brand didn't just fill a gap in the market; it created a category that didn't exist before in organized retail.

The Lyra story is really about understanding consumer behavior at a granular level. The Todi family recognized that while men might be brand-agnostic about innerwear (often having their purchases decided by women in the family), women were intensely brand-conscious about their clothing choices. They also understood that leggings weren't just functional garments—they were fashion statements, comfort wear, and confidence boosters rolled into one.

The distribution strategy for Lyra was markedly different from the core Lux brands. While Lux Cozi was sold everywhere from roadside stalls to supermarkets, Lyra targeted modern retail formats, exclusive brand outlets, and increasingly, e-commerce platforms. The brand was positioned not as innerwear but as fashion wear, competing not with other innerwear brands but with ready-to-wear fashion labels.

Marketing for Lyra broke new ground too. Instead of celebrity endorsements, the brand focused on relatable imagery—young professionals, college students, homemakers who juggled multiple roles. The messaging wasn't about durability or value (traditional innerwear selling points) but about style, comfort, and confidence. "Curve-hugging comfort" became more than a product feature; it became a promise of body positivity.

The IPL partnerships during this period—with Kings XI Punjab and Pune Warriors India—weren't random sponsorship deals. Lux became the comfort partner of two popular IPL teams, understanding that cricket viewership included a significant female audience, especially for the glamorous T20 format. The Lyra brand benefited from this halo effect, associating itself with modernity and excitement.

By 2018, what had started as an experiment had become a crucial growth driver. The women's wear segment, virtually non-existent in Lux's portfolio a decade earlier, was now contributing significantly to both revenues and margins. The success of Lyra proved that Lux could innovate beyond its traditional strengths, that it could create new categories rather than just compete in existing ones.

This period also set the stage for one of the most significant corporate actions in the company's history—the merger with Ebell Fashions, which owned the Lyra brand, bringing it fully into the listed entity. But that's a story that deserves its own chapter.

VI. Stock Market Listing & Capital Markets Evolution (2015-2016)

December 1, 2015, marked a new chapter in Lux Industries' capital markets journey. The company officially listed their shares on the prestigious National Stock Exchange (NSE), over a decade after its initial public offering. The stock opened at Rs 3,342.05 and immediately locked at the upper circuit at Rs 3,509.15—a dream debut that reflected investor confidence in the company's growth story.

The following year, 2016, marked another milestone as Lux Industries Limited listed their shares on the Bombay Stock Exchange (BSE). This dual listing wasn't just about prestige; it was about liquidity, visibility, and access to a broader investor base. The company was signaling its readiness to play in the big leagues of Indian capital markets.

The timing of these listings was strategic. By 2015, Lux had successfully diversified beyond men's innerwear, Lyra was gaining traction, and the company's financial metrics were robust. The organized innerwear market in India was growing at double digits, driven by increasing disposable incomes, brand consciousness, and the gradual shift from unorganized to organized retail.

Institutional investors began taking notice. The company's strong distribution network, established brand equity, and consistent cash generation made it an attractive play on India's consumption story. Fund managers saw in Lux what they looked for in consumer companies—high return on capital employed, strong free cash flow generation, and significant barriers to entry in the form of distribution reach and brand recognition.

The NSE and BSE listings also brought enhanced transparency and governance requirements. Quarterly results became events watched by analysts, conference calls with management became regular features, and the company's strategic decisions faced public scrutiny. This visibility pushed the company to professionalize further, bringing in experienced independent directors and strengthening internal controls.

Yet the public market listing also brought challenges. The stock's performance became a report card updated every trading day. Promoter shareholding patterns were scrutinized, related party transactions questioned, and every management decision analyzed for its impact on minority shareholders. The family-run business culture had to adapt to the demands of quarterly capitalism.

The market's initial enthusiasm was justified by the numbers. Between 2015 and 2017, the company delivered consistent growth in revenues and profits, expanded its retail footprint, and successfully integrated new product categories. The stock price reflected this performance, creating wealth for investors who had believed in the Lux story.

But beneath this success, structural changes were brewing. The company's growth ambitions required bringing its various group entities under one umbrella. Premium brands like GenX and the rapidly growing Lyra were housed in separate unlisted entities owned by the promoters. The market wanted these assets in the listed company, and the management was preparing to deliver exactly that.

VII. The Game-Changing Mergers: JM Hosiery & Ebell Fashions (2018-2021)

On March 13, 2018, Lux Industries Limited agreed to acquire J.M.Hosiery & Co. Limited and Ebell Fashions Private Limited. This wasn't just another corporate transaction—it was the culmination of a strategic vision to consolidate the family's various business interests under one listed entity. The non-cash deal at a combined valuation of Rs. 861 crore was termed as 'EPS accretive' for the company.

Understanding why these mergers mattered requires understanding what these companies brought to the table. JM operates in the premium segment under the brand "GenX" while Ebell is into rapidly growing women's knitted apparels, primarily the Lyra brand. Both companies were owned by the promoter group, making this essentially a consolidation of family assets into the listed entity—a move that would benefit minority shareholders by giving them exposure to high-growth brands.

As on March 31, 2017, J.M.Hosiery & Co. Limited reported turnover of INR 2.5 billion while Ebell Fashions Private Limited reported turnover of INR 1.65 billion. Combined, these entities were adding over Rs 400 crore in revenues to Lux Industries, representing a significant scale-up of operations. More importantly, they brought premium positioning and higher margins to the predominantly mass-market focused listed entity.

The merger structure revealed careful financial engineering. For every 100 equity shares held in JM, shareholders would receive 29 equity shares of Lux. For every 100 equity shares held in Ebell, shareholders would receive 1142 equity shares of Lux. The differential swap ratios reflected the relative valuations and growth potential of each entity, with Ebell (owner of Lyra) commanding a significant premium.

The regulatory journey wasn't smooth. As on February 13, 2020, regulatory approval was still pending. As on March 25, 2021, National Company Law Tribunal finally sanctioned this scheme. The acquisition was finally completed on April 26, 2021—more than three years after the initial announcement.

Why did it take so long? The merger involved complex related-party considerations. JM & Ebell belonged to the promoter group with entire share capital held by promoters except for 1.32% of JM held by Lux. Post-transaction, promoters' stake would increase beyond the maximum limit, requiring them to bring their holding down to ~75% in compliance with SEBI listing norms.

The appointed date of the merger was April 1, 2018, which means the full impact would reflect from 2018-19 onwards. This retroactive effect meant that the benefits of the consolidation would be captured even during the long regulatory approval process, protecting shareholder interests.

The strategic implications were transformative. Lux Industries was no longer just a men's innerwear company with some women's products. It was now a complete wardrobe solutions provider with strong positions across price points and categories. GenX gave it credibility in the youth segment, while Lyra's success in women's wear opened up an entirely new growth avenue.

Market reaction was initially positive, recognizing the value unlocking potential. However, the extended timeline for completion and the complexity of the transaction raised some governance concerns. The fact that these were promoter-owned entities being merged at valuations determined by the promoters themselves required careful scrutiny, even if independent valuers and committees were involved.

By the time the merger was completed in 2021, the Indian innerwear market had evolved significantly. E-commerce had exploded during COVID-19, D2C brands were challenging traditional players, and consumer preferences had shifted toward comfort and functionality. The consolidated Lux Industries was better positioned to face these challenges, with a portfolio spanning from value to premium, from men's basics to women's fashion.

VIII. Modern Era: Digital Age & Premium Push (2017-Present)

The modern chapter of Lux Industries reads like a playbook on navigating digital disruption while leveraging traditional strengths. In 2017, the company signed Varun Dhawan as brand ambassador for Lux Cozi, marking a generational shift in its marketing approach. The young Bollywood star represented the millennial consumer—digitally native, brand conscious, and willing to pay for quality.

But the masterstroke came in 2018. Lux Industries achieved another first in the hosiery industry as they launched megastar Amitabh Bachchan as brand ambassador for its Venus brand. The campaign was brilliant in its simplicity—Big B, the embodiment of Indian gravitas, talking about innerwear with humor and dignity. The creative agency conceptualized a campaign featuring Bachchan in a witty character, focusing on him telling the audience what it takes to make it big in life, in an intriguing and entertaining manner.

November 2020 saw another significant development: the launch of CozyWorld, Lux's first exclusive brand outlet. This wasn't just about retail presence; it was about controlling the brand narrative, creating experiential touchpoints, and gathering direct consumer insights. In an era where D2C brands were disrupting traditional retail, Lux was adapting its model while maintaining its wholesale strength.

The product portfolio expansion during this period was remarkable. The company commissioned Eastern India's largest hosiery product manufacturing plant in Dankuni, West Bengal. This wasn't just capacity addition; it was a statement of intent. The facility incorporated modern manufacturing techniques, automated quality control, and flexibility to produce across categories—from basic innerwear to fashion-forward leggings.

Then came the governance storm. On January 24, 2022, SEBI barred 14 entities for indulging in insider trading, including executive director Udit Todi, and ordered impounding ill-gotten gains of Rs 2.94 crore. The investigation centered around suspicious trading patterns before the announcement of strong financial results in May 2021. The ban was revoked by SEBI in November 2023 and the insider trading charges were dropped, but the reputational damage lingered.

The insider trading episode highlighted the challenges of managing a family-run business in the public market spotlight. While the charges were eventually dropped, the incident raised questions about governance standards, information firewalls, and the company's commitment to minority shareholder interests.

Despite these challenges, business momentum continued. The company expanded into new categories, launched premium sub-brands, and strengthened its e-commerce presence. The One8 brand, launched in collaboration with Virat Kohli, targeted the athleisure segment. Premium lines under Lux Premiums aimed at metro consumers willing to pay more for superior quality and design.

Digital transformation wasn't just about e-commerce sales. The company invested in data analytics to understand consumer preferences, implemented SAP for better supply chain management, and used social media for direct consumer engagement. The traditional distributor-retailer model was augmented with modern trade partnerships and online marketplace presence.

Lux became one of the primary sponsors of Kolkata Knight Riders, maintaining its cricket connection but with a more premium association. The sponsorship strategy evolved from mass visibility to targeted engagement, reflecting the changing media consumption patterns of Indian consumers.

The recent financial performance tells a mixed story. As of 2024-25, the company has a market cap of Rs 3,917 crore, with the stock down 38.10% in the last 12 months. Net profit fell 30.64% year-on-year in Q1 2025-26, reflecting challenging market conditions and increased competition.

Yet the fundamental strengths remain. The distribution network of 500,000+ retail points, the brand equity built over decades, and the manufacturing scale provide moats that new-age competitors find hard to breach. The question for investors is whether these traditional advantages are enough in an increasingly digital, brand-fluid marketplace.

IX. Business Model & Competitive Moats

At its core, Lux Industries' business model is deceptively simple: manufacture quality innerwear, build strong brands, and distribute them widely. But the execution of this simple model has created formidable competitive advantages that new entrants find nearly impossible to replicate.

The multi-brand portfolio strategy stands as the first pillar of strength. The company operates through three distinct verticals: Vertical A comprises Lux Cozi, ONN, Lux Cotts wool, Lux Mozze, and One8; Vertical B includes Lux Venus, Lyra, Lux Inferno, and Lux Nitro; and Vertical C includes GenX, Lux Classic, Lux Karishma, and Lux Amore. This isn't just product proliferation; it's strategic market segmentation allowing the company to capture value across price points without brand dilution.

Distribution density remains perhaps the strongest moat. Those 500,000+ retail touchpoints weren't built overnight—they represent decades of relationship building, credit management, and market understanding. In India's fragmented retail landscape, where 90% of innerwear is still sold through traditional trade, this network is gold. A new D2C brand might capture urban millennials, but reaching the buyer in Bhagalpur or Bareilly requires the kind of distribution Lux has perfected.

Manufacturing scale provides cost advantages that are hard to match. Lux Industries stands as one of India's largest hosiery manufacturers, producing 1.2 million garments daily across nine advanced facilities. This scale allows for backward integration, bulk raw material procurement, and the ability to serve large orders while maintaining quality standards. The facilities strategically located across West Bengal, Tamil Nadu, Punjab, and Uttar Pradesh ensure proximity to both raw materials and markets.

The celebrity endorsement strategy, pioneered by Lux in the innerwear category, created a different kind of moat—mind space. From Sunny Deol to Shah Rukh Khan, from Varun Dhawan to Amitabh Bachchan, the company has consistently associated itself with aspirational figures. In a category where product differentiation is minimal, this brand equity becomes the differentiator.

Export operations to 46 countries provide not just revenue diversification but also learning opportunities. International markets demand higher quality standards, better packaging, and consistent delivery—capabilities that strengthen domestic operations. The export exposure also provides natural hedging against domestic market volatility.

The financial moat is equally important. Despite delivering poor sales growth of 9.14% over the past five years and a low return on equity of 9.60% over the last 3 years, the company maintains a strong balance sheet with minimal debt. This financial strength allows for countercyclical investments, aggressive marketing during downturns, and the ability to extend credit to dealers—crucial in the Indian market context.

Raw material management showcases operational sophistication. Cotton price volatility can destroy margins in the textile industry, but Lux's scale allows for strategic procurement, inventory management, and some pricing power with suppliers. The company's long-standing relationships with yarn suppliers ensure consistent quality and supply even during disruptions.

The intellectual property moat, while less visible, is significant. The company holds numerous trademarks, has developed proprietary fabric blends, and owns design patents. The "yeh andar ki baat hai" tagline itself has become a cultural artifact, impossible to replicate or appropriate.

Technology adoption, while not cutting-edge, is pragmatic. The company uses SAP for operations, has invested in automated cutting and stitching machines, and employs data analytics for demand forecasting. This isn't about being a tech company; it's about using technology to enhance traditional strengths.

Yet these moats face erosion threats. E-commerce reduces the value of physical distribution, D2C brands challenge the celebrity endorsement model with influencer marketing, and global players like Jockey and Calvin Klein attack the premium segment with superior brand equity. The question isn't whether these moats will hold forever, but whether Lux can build new ones while defending the old.

X. Playbook: Building Brands in Traditional Industries

The Lux Industries story offers a masterclass in brand building within seemingly commoditized categories. Their playbook, refined over six decades, provides lessons that transcend the innerwear industry.

Lesson 1: First-Mover Advantage in Marketing Innovation

Being first matters, but being first in marketing matters more. Lux didn't invent innerwear, but they invented innerwear advertising in India. The 1992 television commercial wasn't just an ad; it was a cultural moment that gave them a two-decade head start over competitors. The lesson: in traditional industries, marketing innovation can be more powerful than product innovation.

Lesson 2: Celebrity Endorsement as Category Creation

The genius of using Sunny Deol, then Shah Rukh Khan, and later Amitabh Bachchan wasn't just about borrowing star power. It was about elevating the category itself. By associating innerwear with mainstream celebrities, Lux transformed it from a hidden necessity to a lifestyle choice. The playbook: use premium associations to lift the entire category, then capture the value created.

Lesson 3: Distribution Density as Competitive Advantage

In India, distribution still wins wars. Lux's 500,000+ touchpoints aren't just sales channels; they're information networks, credit systems, and brand ambassadors rolled into one. The playbook: build distribution like you're building a nation-wide infrastructure project, because in many ways, you are.

Lesson 4: Multi-Brand Architecture for Market Coverage

Rather than stretching one brand across all segments, Lux created distinct brands for different consumer cohorts. Lux Cozi for mass market, GenX for youth, Lyra for women, ONN for premium—each with its own identity but leveraging common backend infrastructure. The lesson: in diverse markets, portfolio strategies beat monolithic approaches.

Lesson 5: Managing Family Business Transitions

The successful transition from first to second to third generation, while maintaining entrepreneurial energy, offers lessons in family business management. Professionalization happened gradually—outsiders were brought in for specific functions while family retained strategic control. The balance between family wisdom and professional management became a competitive advantage.

Lesson 6: Strategic M&A for Capability Building

The JM Hosiery and Ebell Fashions mergers weren't just financial engineering. They were about bringing complementary capabilities—premium positioning, women's wear expertise—into the mother ship. The playbook: use M&A not just for scale but for capability acquisition, especially when organic development would take too long.

Lesson 7: Riding Cultural Shifts

Lux's timing with Lyra coincided perfectly with the cultural shift in women's clothing preferences. The company didn't create the trend of women wearing leggings; they recognized it early and built a brand around it. The lesson: in traditional industries, watch for cultural shifts that create new consumption patterns.

Lesson 8: Premium Migration Strategy

The journey from Lux Cozi to ONN to One8 shows how to migrate upmarket without abandoning your base. Each premium launch used the credibility earned at lower price points while maintaining distinct positioning. The playbook: use your mass market strength as a launching pad, not an anchor.

Lesson 9: Technology as Enhancement, Not Disruption

Unlike tech startups trying to disrupt traditional industries, Lux used technology to enhance its traditional model. E-commerce complemented physical retail, data analytics enhanced dealer relationships, and manufacturing automation improved quality while maintaining employment. The lesson: in traditional industries, evolution beats revolution.

Lesson 10: Governance Challenges in Public Markets

The insider trading controversy, even though charges were eventually dropped, highlights the challenges family businesses face in public markets. The playbook learning here is cautionary: governance standards must evolve faster than business growth, and perception management is as important as performance management.

XI. Analysis & Investment Thesis

The Bull Case: Structural Tailwinds and Execution Capability

The optimistic view on Lux Industries rests on several pillars. India's innerwear market, growing at 10-12% annually, remains significantly underpenetrated compared to global standards. The shift from unbranded to branded, accelerated by GST implementation and COVID-19's hygiene focus, provides a multi-decade growth runway.

The distribution moat remains formidable. Those 500,000+ retail points, built over decades, cannot be replicated quickly. In India's fragmented retail landscape, where 90% of purchases still happen offline, this network provides unmatched reach. Digital-first competitors may capture urban markets, but the vast Bharat market remains Lux's stronghold.

During 2021-22, two major group companies were merged, with the Scheme of Amalgamation of J.M. Hosiery & Co Limited and Ebell Fashions Private Limited becoming effective. The merger synergies are still playing out, with opportunities for cross-selling, operational efficiencies, and margin expansion as integration deepens.

The women's segment, particularly through Lyra, offers significant growth potential. Women's innerwear in India is where men's innerwear was two decades ago—ripe for organization, branding, and premiumization. Lyra's first-mover advantage in leggings could translate to leadership in the broader women's innerwear market.

Manufacturing excellence provides cost advantages. With nine facilities producing 1.2 million garments daily, Lux enjoys economies of scale that new entrants cannot match. The recent capacity additions position the company well for the next phase of growth.

The Bear Case: Structural Challenges and Governance Concerns

The pessimistic view points to several red flags. The stock is down 38.10% in the last 12 months, reflecting market concerns about growth sustainability and governance standards. The stock is down 44.04% from its 52-week high, suggesting fundamental challenges beyond market volatility.

Competition is intensifying from multiple directions. Global brands like Jockey and Calvin Klein are expanding aggressively in India. D2C brands are using digital marketing to build strong connections with young consumers. Even traditional competitors like Page Industries (Jockey licensee) are executing better, with superior margins and growth rates.

The governance concerns linger. While SEBI dropped the insider trading charges, the episode raised questions about information management and related-party transactions. With promoter holding at 74.2%, minority shareholders have limited influence on key decisions.

Financial performance has been disappointing. Net profit fell 30.64% year-on-year in Q1 2025-26, and the company has delivered poor sales growth of 9.14% over the past five years. These numbers suggest execution challenges or market share losses to competitors.

The traditional retail model faces disruption. E-commerce platforms are reducing the importance of physical distribution, direct-to-consumer brands are bypassing traditional retail entirely, and quick commerce is changing purchase patterns in urban areas. Lux's greatest strength—its distribution network—might become less relevant over time.

Valuation Considerations

At Rs 3,917 crore market cap, Lux trades at a significant discount to peers like Page Industries. The market cap of Rs 3,911 crore compares to a peer median of Rs 1,568 crore, suggesting relative size advantage but also possibly reflecting governance discounts.

The company's return metrics are concerning. With return on equity at 9.60% over the last 3 years, Lux significantly underperforms peers like Page Industries (40%+ ROE). This suggests either operational inefficiencies or capital allocation issues.

XII. Epilogue & Lessons

As October 2025 draws to a close, Lux Industries stands at a crossroads that mirrors the broader challenges facing India's traditional businesses. The company that pioneered celebrity endorsements in innerwear, that built one of India's widest distribution networks, that successfully created categories where none existed, now faces questions about its next chapter.

The journey from Biswanath Hosiery Mills to Lux Industries Limited offers enduring lessons about building brands in unglamorous categories. The Todi family proved that with the right marketing, even the most commoditized products could command premium valuations. They demonstrated that in India's diverse market, distribution density could be a more powerful moat than technology or innovation.

The power of being a first-mover in marketing innovation cannot be overstated. That 1992 television commercial didn't just sell vests; it changed how Indians thought about innerwear. "Yeh andar ki baat hai" became more than a tagline—it became part of the cultural lexicon, a feat no competitor has matched in three decades.

Managing multi-generational family businesses presents unique challenges. The Todis successfully navigated the transition from founder to second to third generation, professionalizing operations while maintaining entrepreneurial spirit. Yet the insider trading controversy, even though resolved, highlighted the governance challenges inherent in family-controlled public companies.

The complexity of related-party transactions remains a critical lesson. The three-year journey to merge JM Hosiery and Ebell Fashions, while ultimately successful, raised questions about valuation fairness and process transparency. For investors, it reinforced the importance of scrutinizing transactions between listed companies and promoter-owned entities.

Looking ahead, Lux Industries faces a dramatically different landscape than the one Girdharilal Todi encountered in 1957. The next decade will test whether traditional competitive advantages—distribution reach, manufacturing scale, brand equity—can withstand the assault of digitization, changing consumer preferences, and global competition.

The company's response will determine whether Lux remains a case study in successful brand building or becomes a cautionary tale about the limits of traditional business models in a digital age. For now, millions of Indians still reach for Lux products every morning, a testament to six decades of trust building. Whether that trust translates to sustainable shareholder value remains, quite literally, an inside matter—yeh andar ki baat hai.

The story of Lux Industries ultimately reflects the story of Indian business itself—the journey from post-independence manufacturing dreams to global ambitions, from family enterprises to professional corporations, from protected markets to fierce competition. It's a story still being written, one vest, one brief, one legging at a time.

As investors evaluate Lux Industries today, they're not just analyzing a company; they're making a bet on the future of traditional Indian business models, on the continued relevance of physical distribution, on the ability of established brands to fend off digital-native challengers. The outcome of that bet will reveal much about where Indian consumer markets are headed in the decades to come.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube