L&T Finance: The Transformation of India's Infrastructure Lender into a Retail Powerhouse

I. Introduction & Episode Roadmap

Picture this: It's 2021, and the boardroom at L&T Finance's Mumbai headquarters is electric with tension. The company, a stalwart of India's infrastructure financing landscape for nearly three decades, is about to announce something unthinkable—a complete pivot away from its bread-and-butter wholesale lending business. CEO Dinanath Dubhashi stands before the board, proposing what seems like corporate suicide: exit the very business that built the company, and bet everything on retail lending in a market already crowded with banks, NBFCs, and aggressive fintech startups.

The numbers on the table are staggering. L&T Finance, with its ₹49,592 crore market capitalization and AAA rating from four agencies, is proposing to transform from a wholesale-heavy lender to achieving 80% retailization by 2026. The target? A retail return on assets of 2.8-3% and a compound annual growth rate above 25%. In a room full of seasoned financiers who've weathered multiple economic cycles, more than a few eyebrows are raised.

This is the story of how a subsidiary born from India's engineering giant Larsen & Toubro—a company more associated with building airports and power plants than personal loans—transformed itself into one of India's fastest-growing retail finance companies. It's a tale that spans nearly three decades, from the heady days of India's 1990s economic liberalization to today's digital finance revolution.

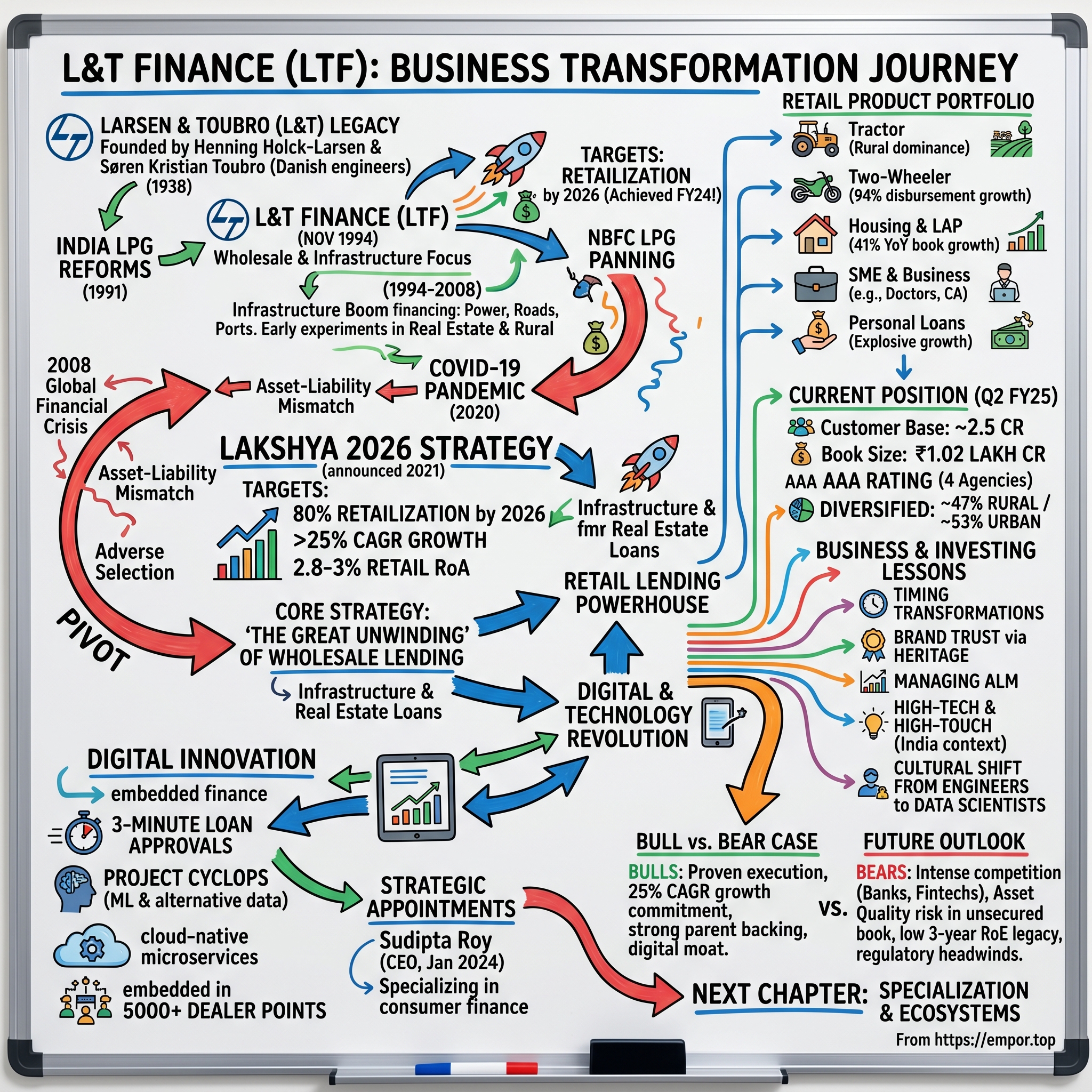

Founded in November 1994, L&T Finance began life as the financial services arm of the Larsen & Toubro conglomerate, initially focused on what it knew best: financing the infrastructure that its parent company built. Today, it's a radically different beast—disbursing two-wheeler loans in minutes through mobile apps, financing tractors for farmers across rural India, and competing head-to-head with both traditional banks and venture-backed fintechs.

The question that drives this narrative isn't just how this transformation happened, but why it succeeded where so many others have failed. How does a traditional NBFC, carrying the DNA of a 1930s engineering firm, reinvent itself for the smartphone age? What made L&T Finance believe it could compete in retail lending when giants like HDFC Bank and Bajaj Finance already dominated the space?

Over the next several hours, we'll unpack this remarkable pivot through the lens of strategic decisions, market timing, and sheer execution prowess. We'll explore how the company's Lakshya 2026 strategy—announced with much fanfare but initially met with skepticism—not only met its targets but achieved them two years ahead of schedule. We'll dig into the technology revolution that reduced loan approval times from days to minutes, the delicate dance of maintaining wholesale relationships while exiting the business, and the cultural transformation required to turn infrastructure financiers into retail lending experts.

This isn't just another corporate transformation story. It's a masterclass in reading market signals, leveraging conglomerate advantages while avoiding their typical pitfalls, and most importantly, having the courage to abandon what you're good at for what the market actually needs. As we'll see, sometimes the biggest risk isn't changing—it's staying the same.

The Larsen & Toubro Legacy & Founding Context

In 1938, in a cramped office in Mumbai so small that only one person could work at a time, two Danish engineers launched what would become the industrial backbone of modern India. Henning Holck-Larsen and Søren Kristian Toubro established Larsen & Toubro in 1938, armed with little more than engineering degrees, a modest retainer from Danish dairy equipment manufacturers, and an almost foolhardy optimism about India's industrial future.

The timing seemed absurd. India was still under British colonial rule, industrial infrastructure was virtually non-existent, and most European businessmen saw the subcontinent as a market for finished goods, not a place to build manufacturing capacity. Yet these two Danes saw something different. Toubro had read a report quoting Gandhi saying he wasn't "leading a movement to rid India of its white colonial masters in order to substitute them with brown ones," and felt such an India would "offer great opportunities to anyone with modern technological and management skills."

Both men had originally come to India as employees of F.L. Smidth & Co. of Copenhagen—Toubro arriving in 1934 to erect cement factory equipment, Larsen following in 1937 as a chemical engineer. Their job was essentially to be advance scouts for Danish industrial exports, setting up cement plants so that Danish machinery could be imported. But something about India captured their imagination. The idea of L&T was conceived during a holiday in Matheran, a hill station near Mumbai.

The contrast between the two founders shaped the company's DNA from the start. Holck-Larsen was a risk-taker while Toubro was more conservative. This balance—aggressive expansion tempered by prudent financial management—would become a defining characteristic of L&T's culture for decades to come. Their initial business model was deceptively simple: represent Danish dairy equipment manufacturers in India. But World War II changed everything. When Germany invaded Denmark in 1940, imports ground to a halt. Rather than fold, L&T pivoted to manufacturing dairy equipment indigenously—a move that would define its approach to crisis management for decades to come. They saw opportunities where others saw obstacles: ship repair during wartime, taking over construction projects when German engineers were interned, and gradually building capabilities that would make them indispensable to independent India's infrastructure ambitions.

The idea of L&T was conceived during a holiday in Matheran, a hill station near Mumbai. The first office of L&T, located in Mumbai, was so small that only one of them could use it at a time. This scrappy beginning became part of company lore—a reminder that even the mightiest industrial conglomerates start somewhere humble.

The post-independence era saw L&T transform from a trading company into an engineering powerhouse. In 1944, Larsen and Toubro established Engineering Construction & Contracts (ECC). By the 1960s and 1970s, L&T had become synonymous with India's infrastructure development—building everything from airports to nuclear reactors. The company that once imported dairy equipment was now fabricating pressure vessels for fertilizer plants and constructing power plants across the subcontinent.

Fast forward to the 1990s. India was undergoing its most dramatic economic transformation since independence. The License Raj was dismantled, foreign investment was welcomed, and the economy was opening up to global competition. It was in this heady atmosphere of liberalization that L&T made a decision that would seem prescient in hindsight: they needed a financial services arm. Larsen & Toubro established a financial services subsidiary called L&T Finance in November 1994. The timing was perfect. The crisis in 1991 forced the government to initiate a comprehensive reform agenda, including Liberalisation, Privatisation and Globalisation, referred to as LPG reforms. Commercial banks were given the freedom to determine interest rates. Previously, the Reserve Bank of India used to decide this. The financial sector was opening up, foreign banks were entering, and there was a massive need for capital to fund India's infrastructure ambitions.

R. Shankar Raman joined L&T Group in November 1994 to set up L&T Finance Limited. For L&T, having a captive finance arm made strategic sense—they could finance the very infrastructure projects they were building, creating a virtuous cycle of construction and credit. The synergy was obvious: who better to assess the creditworthiness of an infrastructure project than the company actually building it?

But here's where the story takes an interesting turn. What started as a support function for the parent company's infrastructure business would, over the next three decades, undergo multiple transformations, ultimately emerging as something its founders could never have imagined—a retail-focused, digitally-driven financial services company that would compete not with project financiers but with consumer lenders, fintechs, and banks.

The question that makes this transformation so compelling isn't just what happened, but why it worked when so many similar pivots by industrial conglomerates have failed. The answer, as we'll see, lies in a combination of market timing, strategic courage, and perhaps most importantly, the willingness to kill your own golden goose before someone else does it for you.

III. Early Years: Infrastructure Finance Focus (1994–2008)

The Mumbai office of L&T Finance in 1995 looked nothing like a typical financial institution. Engineers outnumbered MBAs, technical drawings cluttered desks alongside loan documents, and discussions about debt-service coverage ratios were punctuated by debates about soil bearing capacity and concrete strength. This wasn't a traditional lender—it was an infrastructure company that happened to have a banking license.

In those early days, L&T Finance operated almost like an internal treasury function with external clients. The team's first major deals weren't with strangers but with contractors and suppliers already working with the parent company. They knew these businesses intimately—their cash flows, their capabilities, their management teams. This insider knowledge gave them an edge that pure financial institutions couldn't match.

The infrastructure boom of the late 1990s and early 2000s provided the perfect growth environment. India was building everything—power plants, roads, ports, airports. The Golden Quadrilateral highway project alone required financing of unprecedented scale. L&T Finance positioned itself as the lender that understood these projects not just as financial assets but as engineering challenges. When they underwrote a power plant, they weren't just looking at projected cash flows—they understood turbine efficiency, fuel supply agreements, and grid stability. In 2008, L&T Finance received its NBFC (Non-Banking Financial Company) license from the Reserve Bank of India, allowing it to expand its portfolio significantly. This wasn't just a regulatory milestone—it was a strategic inflection point. The NBFC license transformed L&T Finance from a project finance specialist into a legitimate financial institution with the freedom to lend across sectors.

But freedom brought complexity. The team that had spent years perfecting the art of infrastructure finance suddenly found itself evaluating real estate developers, small businesses, and even rural lending opportunities. The cultural clash was immediate and visceral. Infrastructure financiers were used to multi-year project cycles, detailed technical evaluations, and large ticket sizes. Now they were being asked to consider loans to farmers buying tractors or small businesses needing working capital.

The early forays outside infrastructure were mixed at best. A push into real estate financing in 2006-2007 seemed brilliant—until the global financial crisis hit. Suddenly, half-built apartment complexes and stalled commercial projects littered the portfolio. The team learned a painful lesson: expertise in one type of lending doesn't automatically translate to another.

Yet there were bright spots. Rural finance, which initially seemed like a regulatory obligation more than a business opportunity, revealed surprising potential. L&T's engineering DNA actually helped here—they understood farm equipment, irrigation systems, and rural infrastructure in ways that pure financial players didn't. When they financed a tractor, they knew exactly what that machine could do, how long it would last, and what maintenance it would need.

By 2008, L&T Finance had grown to over ₹5,000 crores in assets under management, with infrastructure still comprising about 70% of the book. They had established relationships with most major infrastructure developers in India and had participated in financing landmark projects from the Delhi Metro to major power plants. The business was profitable, growing, and seemingly on the right track.

But beneath this success, fundamental questions were emerging. The infrastructure financing space was becoming increasingly competitive. Banks, armed with cheaper deposits, were muscling into deals that L&T Finance once dominated. International banks brought sophisticated structured finance capabilities. New infrastructure-focused NBFCs were emerging with aggressive pricing strategies. The moat that came from technical expertise was eroding as the market matured.

More troubling was the asset-liability mismatch inherent in infrastructure financing. L&T Finance was funding 15-20 year projects with 3-5 year borrowings, constantly rolling over debt in what amounted to a high-stakes game of financial musical chairs. One liquidity crisis, one credit freeze, and the entire model could unravel.

The global financial crisis of 2008 would prove to be the crucible that tested these vulnerabilities. As credit markets froze worldwide, L&T Finance found itself in an uncomfortable position—committed to long-term projects but struggling to raise short-term funding. They survived, thanks partly to the parent company's support and India's relatively insulated financial system, but the experience left scars.

In boardroom discussions post-crisis, a new realization emerged: infrastructure finance, despite being their core competency, might not be their future. The best infrastructure projects were increasingly being cherry-picked by banks with their cost-of-funds advantage. The riskier projects that banks wouldn't touch came with hair-raising complexity and political risk. It was a classic case of adverse selection—L&T Finance was getting the deals nobody else wanted.

The stage was set for transformation, though nobody quite knew what form it would take. As 2008 drew to a close, L&T Finance stood at a crossroads, successful by any measure but increasingly aware that past success might be the enemy of future survival.

IV. The Growth Years & Portfolio Expansion (2008–2020)

The conference room on the 14th floor of L&T House in Mumbai had seen many heated debates, but the one in early 2009 was different. The global financial crisis had just demonstrated the fragility of wholesale lending, and the leadership team was grappling with an uncomfortable truth: their traditional business model was under siege. "We're becoming the lender of last resort for infrastructure projects," one executive said bluntly. "Banks take the cream, we get what's left."

The company's major segments now include retail finance, wholesale finance, and financial inclusion. But this neat categorization masks the messy, often painful evolution that occurred over the next decade. The expansion wasn't a carefully orchestrated strategy—it was more like a series of experiments, some brilliant, others costly.

The first major diversification came through rural finance, driven partly by regulatory requirements but increasingly by genuine opportunity. India's rural economy was transforming. Tractors were replacing bullocks, smartphones were reaching villages, and rural incomes were rising. L&T Finance's approach was different from traditional rural lenders. They didn't just lend against land or gold—they financed productive assets. A tractor wasn't just collateral; it was a productivity tool that would generate the cash flows to repay the loan.

The numbers told a compelling story. A tractor loan of ₹5 lakhs would typically increase a farmer's income by ₹2-3 lakhs annually through custom hiring and improved productivity. The default rates, surprisingly, were lower than many urban loans. Rural borrowers, it turned out, valued their creditworthiness highly—default meant social stigma in tight-knit communities.

By 2012, L&T Finance had become one of India's largest tractor financiers, funding over 50,000 tractors annually. But this wasn't just about tractors. They were building a rural ecosystem—financing farm equipment dealers, providing working capital to rural entrepreneurs, and even venturing into micro-finance through joint ventures.

The urban expansion followed a different trajectory. Two-wheeler financing started almost by accident—a manufacturer relationship that needed a financing partner. But the team quickly realized this was a massive market with attractive economics. Unlike infrastructure loans that took months to process, a two-wheeler loan could be approved in hours, disbursed in a day, and fully repaid in two years. The ticket sizes were small—₹50,000 to ₹1 lakh—but the volumes were enormous.

The housing finance entry was more strategic. By 2015, India's real estate market had recovered from its post-crisis lows, and affordable housing was the new buzzword. L&T Finance positioned itself in the ₹10-30 lakh segment—too small for most banks to bother with, too large for microfinance. They targeted salaried employees in tier-2 and tier-3 cities, leveraging their parent company's construction expertise to assess property quality.

But the real innovation was in SME lending. Rather than competing with banks for established businesses, L&T Finance focused on the "missing middle"—businesses too large for microfinance but too small for banks. They developed specialized products for specific professions. Loans for doctors to buy medical equipment, with repayment tied to insurance claim cycles. Working capital for small manufacturers, with payments linked to their invoice settlements. Each product required deep understanding of that particular business ecosystem.

The wholesale business, meanwhile, was undergoing its own transformation. Pure infrastructure finance was giving way to structured finance, real estate, and renewable energy. The team learned to structure complex transactions—part debt, part equity, with various triggers and covenants. They became experts at financial engineering, turning risky projects into investable propositions. The numbers from this period tell a story of explosive growth masking underlying tensions. By 2019, CRISIL, ICRA, India Ratings, and CARE assigned/reaffirmed AAA rating of L&T Finance Holdings and its subsidiaries, despite multiple downgrades across the sector. But the poor 5-year sales growth of 2.46% that would later haunt the company was already taking shape. The return on equity of 7.09% over the last 3 years was respectable but not spectacular—a reflection of the challenging mix of high-growth retail and struggling wholesale portfolios.

The pre-Covid years also saw critical organizational changes. The company was building capabilities it had never needed before—retail branch networks, digital platforms, collection infrastructure. They hired thousands of employees, many from banks and consumer finance companies. The culture clash was palpable. Old-timers talked about basis points and project IRRs; newcomers focused on customer acquisition costs and digital adoption rates.

One particularly telling episode occurred in 2018 when the company launched its digital lending platform for personal loans. The technology team, staffed with engineers from fintech startups, wanted to approve loans in under 10 minutes using alternative data sources. The risk team, veterans of infrastructure finance, insisted on traditional documentation and multi-day verification processes. The compromise—a 30-minute process with selective documentation—satisfied nobody but somehow worked.

The rural business was evolving beyond recognition. What started as tractor financing had expanded into a complex ecosystem play. L&T Finance was now financing entire value chains—from seeds and fertilizers to warehouses and cold storage. They had become deeply embedded in rural India, with over 1,000 touch points across the country.

But success bred complexity. By 2020, L&T Finance was essentially running multiple businesses under one roof—each with different economics, risk profiles, and operational requirements. The infrastructure team barely spoke to the two-wheeler team. Rural finance operated like a separate company. Housing finance had its own systems and processes. The company was less a unified financial institution and more a holding company for various lending businesses.

The wholesale book, meanwhile, was becoming increasingly problematic. Real estate exposure, built up during the boom years, was turning sour as developers struggled with unsold inventory. Infrastructure projects were getting delayed due to land acquisition issues and regulatory clearances. The asset quality was deteriorating, and provisions were eating into profitability.

Then came COVID-19.

The pandemic hit in March 2020 like a sledgehammer. Collections stopped overnight. Customers who had never missed a payment suddenly couldn't pay. Rural areas were locked down, preventing field staff from reaching borrowers. The wholesale book faced moratorium requests from virtually every borrower. It was the perfect storm that the company had never planned for.

But crisis has a way of clarifying strategy. As the leadership team held emergency video conferences from their homes during the lockdown, a consensus emerged: the old model was broken. The future wasn't in wholesale lending where they competed with banks on price. It wasn't in complex infrastructure deals that tied up capital for decades. The future was retail—digital, scalable, and focused on India's growing consumer class.

The stage was set for the most dramatic transformation in the company's history. Pre-Covid, L&T Finance was largely a wholesale plus rural NBFC, carrying the DNA of its infrastructure heritage. Post-Covid, it would emerge as something entirely different. The only question was whether they had the courage to kill the business that had defined them for 26 years.

V. The Lakshya 2026 Transformation: Bold Pivot to Retail (2021–Present)

The virtual board meeting on April 15, 2021, started with an unusual request from CEO Dinanath Dubhashi: "I want everyone to forget everything we know about our business and imagine we're starting L&T Finance today. What would we build?"

The silence that followed wasn't just pandemic-induced video lag. The question cut to the heart of a brutal reality—their traditional business model was dying. Wholesale lending margins had compressed to unsustainable levels. Banks with their 4% cost of funds were undercutting them on every deal. The infrastructure financing space where they'd built their reputation was now commoditized. Meanwhile, nimble fintechs were capturing the retail lending opportunity with digital-first models that made traditional NBFCs look prehistoric.

What emerged from that meeting and dozens that followed was Lakshya 2026: The Group's 5-year strategic plan for value-accretive growth with focus on ESG and Sustainability. But this wasn't just another corporate strategy document. It was a declaration of war on their own past.

The targets were audacious: Post Covid, around 2022, started getting out of wholesale lending and fully focused on retail with target CAGR above 25%. The company aimed for 80% retailisation and retail RoA of 2.8-3% by FY26. To put this in perspective, they were proposing to flip their entire business model—from 70% wholesale to 80% retail—in just five years.

The execution began with what insiders called "the great unwinding." Starting in late 2021, L&T Finance began systematically exiting wholesale lending. This wasn't a fire sale—it was a carefully orchestrated retreat. Long-term infrastructure loans were sold to banks eager for stable assets. Real estate exposures were either recovered or provisioned aggressively. The team that had spent decades building relationships with corporate borrowers was now tasked with ending them.

The human cost was significant. Entire departments that had defined the company's identity were being disbanded. Senior executives who'd spent careers structuring complex project finances found themselves redundant. One veteran recalled, "It felt like we were demolishing our own house to build something we didn't fully understand. "But parallel to the unwinding was an equally dramatic buildup. The Board of Directors of L&T Finance approved the appointment of Sudipta Roy as their new Managing Director and Chief Executive Officer with effect from January 24, 2024. Mr. Roy has a deep understanding of consumer finance, cards and retail loans, lending and payments technology systems and associated risk management practices and has worked extensively in India, China and Canada in the consumer lending and payments business, having built green-field lending and cards businesses in all three countries. He was voted as one of the Top 50 Digital Finance Influencers in the country in 2024 as well as the top 30 Fintech Influencers in India in the year 2021 and is a speaker at various forums on Retail Lending and Credit, History of Payments, Risk and Fraud Control and Future of Payments business. Mr. Roy has also been a part of several Government and Reserve Bank of India committees in areas of transit payment systems, banking security and retail payments.

The new CEO's vision was radically different from his predecessors. Where they saw infrastructure finance as the core and retail as adjacency, Roy saw retail as the only sustainable future. His mantra—"Fintech@Scale"—became the rallying cry for transformation. The idea was audacious: combine the trust and balance sheet of a traditional NBFC with the speed and customer experience of a fintech.

The transformation wasn't just about changing what they lent but how they lent. The company embarked on building tech infrastructure for scale with five key pillars: Customer acquisition, credit underwriting, digital architecture, brand visibility, capability building. Each pillar required fundamental reimagination of existing processes.

Take customer acquisition. The old model involved relationship managers courting corporate clients over months. The new model needed to acquire thousands of retail customers daily through digital channels. They built a platform that could process loan applications from social media ads, e-commerce checkouts, and dealer points simultaneously. The system could ingest data from multiple sources—bank statements, GST returns, utility bills—and make credit decisions in real-time.

Credit underwriting underwent a complete overhaul. Infrastructure lending relied on detailed project reports and cash flow models. Retail lending needed instant decisioning based on alternative data. They partnered with fintech companies to access digital footprints, built machine learning models to predict default probability, and created automated rule engines that could approve loans without human intervention.

The results were staggering. The early achievement of targets outlined in the strategy roadmap Lakshya'26 under Dubhashi's leadership demonstrates L&T Finance's transformation, which has positioned it as a top-tier digitally enabled and customer-focused retail financier. What was supposed to take five years was largely achieved in three.Q2 FY25: PAT of ₹696 crore (up 17% YoY), retail book at ₹88,975 crore (28% YoY growth). The numbers validated the strategy, but more importantly, they represented a complete reimagination of what an NBFC could be.

The company's distribution network reaching around 2 lakh villages through more than 1,900 rural meeting centers and over 160 urban branches, supported by over 13,200 distribution points developed over the last decade. It serves a substantial customer base of approximately 2.5 crore individuals. The scale achieved in just three years of focused retail transformation was unprecedented in Indian NBFC history.

But perhaps the most remarkable achievement was cultural. A company that had defined itself by the complexity of its deals—multi-billion rupee infrastructure projects with hundreds of pages of documentation—was now celebrating two-wheeler loans approved in minutes through a mobile app. Engineers who once debated turbine specifications were now obsessing over user experience metrics. The transformation wasn't just strategic; it was existential.

Looking back, Achieved Lakshya 2026 strategy well in advance in FY24—two years ahead of schedule. The company that entered 2021 as a wholesale lender with retail operations had emerged as a retail powerhouse that happened to have some legacy wholesale exposure. It was one of the most dramatic business model pivots in Indian corporate history, executed not through acquisition or merger, but through sheer operational transformation.

The question now wasn't whether the transformation had succeeded—it clearly had. The question was whether this new avatar of L&T Finance could sustain its momentum in an increasingly competitive retail lending market where everyone from banks to Big Tech wanted a piece of the action.

VI. The Digital & Technology Revolution

The moment of truth came at 2:47 PM on a Tuesday afternoon in March 2023. A customer in Coimbatore applied for a two-wheeler loan through a dealer's tablet. By 2:50 PM—exactly three minutes later—the loan was approved, documents were e-signed, and the money was on its way to the dealer's account. The customer rode away on his new motorcycle before his coffee got cold. For a company that once took three months to close infrastructure deals, this represented nothing short of a revolution.

The entire loan journey completely transparent, paperless and end-to-end digital with turn-around time for loan sanction of just 2-3 minutes, disbursements within an hour. But achieving this wasn't simply about buying technology—it was about reimagining every assumption about how lending worked.

The transformation began with a fundamental question: why does lending take time? The traditional answer involved credit assessment, documentation, verification, and approvals. But when the team decomposed each step, they realized most delays weren't about risk management—they were about process inefficiency. A credit bureau check that took hours could be done in seconds through APIs. Document verification that required physical inspection could be automated through OCR and AI. Approval hierarchies that added days could be replaced by rule engines that operated in milliseconds.

Building tech infrastructure for scale became the company's obsession. The Five key pillars: Customer acquisition, credit underwriting, digital architecture, brand visibility, capability building weren't just buzzwords—each represented a massive engineering challenge.

Customer acquisition was revolutionized through what they called "embedded finance." Instead of waiting for customers to come to them, L&T Finance embedded itself into customer purchase journeys. When someone browsed for motorcycles online, L&T Finance's loan calculator appeared alongside. When they visited a dealership, the salesperson could initiate a loan application on the spot. The company integrated with over 5,000 dealer points, each equipped with tablets running their proprietary loan origination system.

Credit underwriting—the heart of any lending business—underwent the most dramatic transformation. The old model relied on financial statements, salary slips, and bank statements. The new model pulled data from everywhere. Social media profiles revealed stability (people who frequently changed jobs were higher risk). Shopping patterns indicated financial stress (sudden shifts from branded to generic products preceded defaults). Mobile phone usage patterns predicted repayment behavior (customers who recharged regularly were more likely to pay EMIs on time).

The company built Project Cyclops, a three-dimensional credit underwriting engine that combined traditional bureau data with alternative data sources and behavioral analytics. The system could process thousands of data points in real-time, generating not just a yes/no decision but a customized loan offer—amount, tenure, interest rate—optimized for both risk and conversion.

But technology without adoption is worthless. The company faced massive resistance, particularly from field staff who saw digital processes as threats to their jobs. The breakthrough came when they reframed digitization not as replacement but as augmentation. Field officers were given tablets that made them more productive—instead of collecting documents, they became relationship managers. Instead of chasing payments, they focused on customer service. The same technology that could have eliminated jobs ended up making existing employees more valuable.

The digital architecture itself was a marvel of modern engineering. Built on cloud-native microservices, the platform could scale elastically—handling 100 applications or 100,000 without missing a beat. Each component was designed for failure, with automatic failovers and redundancy built in. The entire system was API-first, allowing third-party integrations in days rather than months.

But perhaps the most innovative aspect was the approach to data. Every interaction, every click, every pause was captured and analyzed. The system learned continuously—if customers from a particular pin code had higher default rates during certain months (perhaps due to seasonal employment), interest rates would automatically adjust. If applications from certain IP addresses showed suspicious patterns, additional verification would trigger automatically.

The results spoke for themselves. Customer acquisition costs dropped by 60%. Loan processing time went from days to minutes. Most remarkably, despite the speed of approvals, NPAs in digitally originated loans were lower than traditionally sourced ones. The machine, it turned out, was better at assessing risk than humans—not because it was smarter, but because it was consistent, processing every application with the same rigor without fatigue or bias.

The fintech challenge: Competing with startups while leveraging legacy strengths became L&T Finance's strategic advantage. While fintech startups had agility, they lacked the balance sheet to scale. While banks had capital, they lacked the risk appetite for innovation. L&T Finance positioned itself perfectly in the middle—the stability of an established institution with the innovation mindset of a startup.

The company also made strategic partnerships with technology giants. A collaboration with Amazon Pay launched in Q3 FY25 to develop cutting-edge credit solutions. Rather than seeing Big Tech as competition, L&T Finance saw them as distribution channels. They would handle customer acquisition and user experience; L&T Finance would provide the credit assessment and capital.

By 2024, L&T Finance wasn't just using technology—it was becoming a technology company that happened to be in lending. They open-sourced some of their tools, hosted hackathons for developers, and even launched an accelerator for fintech startups. The message was clear: the future of finance was digital, and L&T Finance intended to help write that future.

Yet for all the technological sophistication, the company never forgot a crucial truth: lending is ultimately about trust. The best algorithm in the world can't replace the confidence that comes from a recognized brand. So while the loan might be approved by an AI, it still carried the L&T name—a name that had built India's infrastructure and now was financing its dreams, one small loan at a time.

VII. Product Portfolio & Market Position Today

In a small town outside Salem, Tamil Nadu, a 23-year-old software engineer named Priya walks into a Honda dealership. She's been saving for months, and today she's finally buying her first motorcycle—a modest 110cc commuter that will replace her unreliable bus commute. The salesperson, barely looking up from his tablet, says, "Ma'am, you qualify for 100% financing. Would you like to complete the loan process now?" Five minutes later, Priya owns a motorcycle. She doesn't know it, but she's just become part of L&T Finance's ₹12,669 crore two-wheeler portfolio.

Meanwhile, 400 kilometers away in rural Karnataka, a farmer named Raju is at a tractor dealership. The monsoon was good this year, and he's upgrading from his 10-year-old machine. L&T Finance has already pre-approved him based on his land records, crop patterns, and payment history from his previous loan. The entire process takes less than an hour. He's one of over 1 lakh new tractors financed by L&T Finance in FY23, part of their dominant position in rural lending.

These stories, multiplied millions of times across India, represent the new L&T Finance. The company's product portfolio today reads like a catalogue of middle India's aspirations: Housing loans, personal loans, two-wheeler loans, business loans (SME, doctor, CA), rural loans, farmer loans including tractor financing. Each product carefully calibrated to serve a specific need, each with its own risk model, distribution strategy, and growth trajectory.

As of Q2FY25, its customer portfolio is evenly split, with 47% in rural areas and 53% in urban settings. This unique positioning—47% rural, 53% urban book—gives L&T Finance a diversification that few competitors can match. When urban markets slow, rural compensates. When monsoons fail, urban cushions the impact. It's portfolio theory applied to Indian demographics.

Urban Finance, comprising 56% of AUM, has become the growth engine. Within this, two-wheeler finance has emerged as a standout performer. ₹9,285 Cr disbursed in FY25 represents not just numbers but a deep understanding of urban mobility needs. The company realized that for millions of Indians, a two-wheeler isn't just transportation—it's economic liberation, enabling everything from gig economy participation to small business operations.

Personal loans showed explosive growth—disbursements surged 94% YoY to Rs 1,642 crore in Q3 FY25. But this wasn't indiscriminate lending. Each loan was underwritten using sophisticated models that considered everything from employment stability to social media behavior. The average ticket size of ₹2-3 lakhs targeted the sweet spot—large enough to be profitable, small enough to be manageable for middle-class borrowers.

The housing finance business represented perhaps the most dramatic transformation. In Q3 FY25, housing loans & loans against property (LAP) disbursement surged 24% to Rs 2,475 crore as compared with Rs 1,998 crore in Q3 FY24. The book size increased 41% YoY to Rs 23,461 crore during the quarter. This growth came from focusing on the ₹15-40 lakh segment in tier-2 and tier-3 cities—customers whom banks found too small and microfinance found too large.

SME lending showed remarkable momentum. SME Finance disbursement jumped 29% to Rs 1,249 crore during the quarter as compared with Rs 965 crore in Q3 FY24. The book size surged 89% to Rs 5,817 crore in Q3 FY25 as compared with Rs 3,078 crore in the same quarter last year. The company had cracked the code on small business lending by focusing on specific professions—doctors, chartered accountants, small manufacturers—and building products tailored to their cash flow patterns.

The rural business remained a cornerstone, though growth was moderating. Farmer finance, particularly tractor loans, maintained its leadership position. The company financed more than 1 lakh new tractors in FY23, leveraging deep relationships with manufacturers and dealers built over decades. But this wasn't just about selling loans—L&T Finance had become embedded in the rural ecosystem, understanding cropping patterns, weather risks, and commodity cycles better than many agricultural companies.

Geographic expansion followed a hub-and-spoke model. Major cities served as hubs for technology and training, while smaller branches and partnership points provided last-mile connectivity. The branch network strategy wasn't about physical presence—each location was chosen based on data analytics, positioned to maximize catchment area while minimizing overlap.

The Competition landscape had evolved dramatically. Banks like HDFC and ICICI were moving downstream into retail lending. Fintechs like Paytm and PhonePe were leveraging their payment platforms to offer credit. NBFCs like Bajaj Finance and Shriram Finance were expanding aggressively. International players were eyeing India's massive credit opportunity.

L&T Finance's response was strategic positioning rather than head-to-head competition. Against banks, they offered speed and convenience. Against fintechs, they provided trust and stability. Against other NBFCs, they leveraged their unique rural-urban mix and parent company backing. It wasn't about being the biggest—it was about being the best in chosen segments.

The product strategy also reflected a sophisticated understanding of customer lifecycle value. A two-wheeler loan customer today could become a personal loan customer tomorrow and a home loan customer eventually. The company built systems to track customer journeys, offering progressively larger credit products as relationships matured and credit histories built.

Risk management evolved to match the portfolio complexity. Each product had its own risk framework, early warning systems, and collection strategies. Two-wheeler loans were managed through dealer relationships and technology-enabled collections. Rural loans leveraged community relationships and seasonal cash flows. Housing loans combined physical collateral with careful underwriting.

By 2024, L&T Finance had achieved something remarkable: a diversified retail portfolio that was both fast-growing and relatively stable. The company wasn't just participating in India's consumption story—it was enabling it, one small loan at a time. The transformation from infrastructure financier to retail lending powerhouse was complete. The question now was how to sustain this momentum in an increasingly competitive and regulated market.

VIII. Financial Performance & Market Dynamics

The PowerPoint slide on the screen during the Q2 FY25 earnings call told a story of remarkable transformation, but CEO Sudipta Roy's tone was notably cautious. "Looking ahead, we expect that the sectoral challenges may persist for the next two quarters, and, in response, we may dynamically recalibrate our business objectives in the coming quarters, prioritising positive credit outcomes over assets under management growth," he said. It was a sobering reminder that even successful transformations face headwinds.

The Board of LTF, a prominent Non-Banking Financial Company (NBFC) in India, announced its financial results for the second quarter ending September 30, 2024. The Company has established a strong pan-India retail franchise, with a distribution network reaching around 2 lakh villages through more than 1,900 rural meeting centers and over 160 urban branches, supported by over 13,200 distribution points developed over the last decade. It serves a substantial customer base of approximately 2.5 crore individuals, employing effective cross-selling and up-selling strategies to enhance customer engagement and deliver tailored financial solutions. As of Q2FY25, its customer portfolio is evenly split, with 47% in rural areas and 53% in urban settings.

The consolidated book size of ₹1,02,314 crore represented massive scale, but beneath the headline numbers lay a more complex reality. The poor 5-year sales growth of 2.46% and low 3-year RoE of 7.09% were reminders of the wholesale legacy that still weighed on overall performance. The company was essentially running two businesses—a fast-growing retail operation and a slowly unwinding wholesale book—with dramatically different economics.

GS3 at 3.31%, NS3 at 0.99% in Q1 FY26 appeared manageable, but the trend was concerning. Reflecting signs of building stress, its credit costs rose to 2.59 per cent in Q2FY25 from 2.58 per cent a year ago. Sequentially, they rose by 22 basis points from 2.37 per cent in Q1FY25. The microfinance crisis affecting the broader industry was starting to impact rural portfolios. Urban segments faced their own challenges with rising competition and regulatory scrutiny on unsecured lending.

RoE at 10.86%, RoA at 2.37% in Q1 FY25 showed improvement but remained below management's aspirations. The challenge was structural—retail lending, while profitable, required significant investment in technology and distribution. The payback period for these investments meant current profitability understated the true economic value being created.

Promoter holding: 66.2% provided stability in volatile markets. L&T's continued backing sent a strong signal to the market about long-term commitment. But it also raised questions about minority shareholder interests and the company's ability to attract institutional investors who preferred more diverse shareholding patterns.

Stock performance told its own story. The shares had moved up substantially from pandemic lows but remained volatile, reflecting market uncertainty about the sustainability of the retail transformation. The stock was caught between two narratives—bulls who saw a successful transformation story, bears who worried about asset quality in a rapidly grown retail book.

The regulatory environment added another layer of complexity. The Reserve Bank of India had been tightening norms for NBFCs, particularly around unsecured lending. Capital requirements were increasing, leverage limits were being enforced more strictly, and there was constant speculation about further regulatory changes. L&T Finance's AAA rating from 4 agencies provided some buffer, but regulatory risk remained a constant overhang.

The interest coverage ratio concerns flagged by analysts reflected the fundamental challenge of the NBFC model. Unlike banks with access to low-cost deposits, NBFCs relied on wholesale borrowings. L&T Finance's cost of funds, while competitive for an NBFC, was still significantly higher than banks. This structural disadvantage meant they had to be better at risk assessment and more efficient in operations just to match bank returns.

Market dynamics were shifting rapidly. The post-pandemic credit boom was moderating. Interest rates had risen sharply, impacting both borrowing costs and customer affordability. Competition was intensifying as everyone from banks to Big Tech wanted a piece of the retail lending pie. Customer acquisition costs were rising as the easy-to-reach segments got saturated.

The company's response was nuanced. Rather than chasing growth at any cost, management emphasized quality. "We may dynamically recalibrate our business objectives in the coming quarters, prioritising positive credit outcomes over assets under management growth," became the new mantra. It was a mature response, choosing profitability over growth, but markets accustomed to high growth stories weren't entirely convinced.

International comparisons provided context. Globally, successful NBFCs had either specialized in niche segments or scaled massively to compete with banks. L&T Finance was attempting both—maintaining specialized positions in segments like tractor financing while scaling retail operations to gain economies of scale. Few had succeeded at this dual strategy.

The financial metrics also revealed operational improvements. Cost-to-income ratios had improved as digital adoption increased. Customer acquisition costs had dropped even as volumes increased. The efficiency gains from technology investments were starting to show, though the full impact would take years to materialize.

Analyst opinions remained divided. Some saw L&T Finance as successfully navigating a difficult transformation, building a sustainable retail franchise while managing legacy issues. Others worried about asset quality in a rapidly grown book, especially in segments like personal loans and microfinance where industry stress was evident. The truth, as often, lay somewhere in between.

The company's guidance reflected this balanced reality. Growth targets were being moderated, profitability was being prioritized over expansion, and investment in technology and risk management continued. It was the strategy of a management team that had learned from both success and stress, understanding that sustainable growth mattered more than headline numbers.

IX. Playbook: Business & Investing Lessons

The conference room in L&T House has seen many strategy sessions, but the one in late 2023 was different. The leadership team wasn't discussing next quarter's targets or new product launches. They were documenting lessons learned—creating a playbook from their transformation that others might follow. Or avoid.

The conglomerate advantage: L&T backing and synergies turned out to be more nuanced than simple parent company support. Yes, the L&T brand opened doors, provided credibility, and offered financial backing during tough times. But it also came with baggage—bureaucratic processes, conservative risk appetite, and a culture that initially resisted the entrepreneurial agility needed in retail finance. The real advantage wasn't the parentage itself but the ability to selectively leverage strengths while maintaining operational independence.

The first lesson was about timing transformations: Why the retail pivot worked. L&T Finance didn't move first—companies like Bajaj Finance had already proven retail NBFC models. They didn't move last—avoiding the late-mover disadvantage that plagued banks entering retail lending. They moved at exactly the right time: when technology had matured enough to enable scale, when India's consumption story was accelerating, but before the market got oversaturated. Timing, they learned, mattered more than being first or having the best technology.

Building trust in financial services through industrial heritage proved to be a masterclass in brand leverage. When a farmer in Punjab or a small business owner in Tamil Nadu saw the L&T name, they saw the company that built India's infrastructure. This wasn't some fly-by-night fintech—this was institutional credibility earned over eight decades. The lesson: heritage brands can compete with digital natives if they modernize operations while maintaining trust.

AAA rating from 4 agencies, top ESG ratings weren't just badges of honor—they were competitive weapons. The ratings allowed cheaper borrowing, which in a spread business like lending, directly translated to competitive advantage. More subtly, they provided comfort to regulators, partners, and customers. The lesson: in financial services, reputation is quantifiable and directly impacts economics.

The retailization playbook for NBFCs that emerged had several counterintuitive insights. First, don't try to be a bank. Banks have structural advantages in cost of funds that NBFCs can't match. Instead, focus on segments where speed, flexibility, and specialization matter more than price. Second, technology isn't just about efficiency—it's about creating new business models. The ability to approve loans in minutes didn't just reduce costs; it enabled point-of-sale financing that banks couldn't match.

Digital transformation without losing the human touch became a critical balance. Pure digital players struggled with trust, especially in rural markets. Traditional players couldn't match digital efficiency. L&T Finance's hybrid model—digital processes with human interfaces where needed—proved optimal. A farmer might apply for a tractor loan through a tablet, but there was still a person explaining terms in the local language. The lesson: in India, high-tech needs high-touch.

Managing asset-liability mismatches in transition revealed sophisticated financial engineering. As the company shifted from long-term infrastructure loans to short-term retail loans, the liability side had to transform too. They diversified funding sources, reduced dependence on any single channel, and built buffers for liquidity stress. The lesson: balance sheet transformation is as important as business model transformation.

The playbook also documented failures. Early attempts at unsecured personal loans without proper risk models led to losses. Rapid expansion into new geographies without understanding local dynamics created NPAs. Over-reliance on dealer channels in some products created concentration risks. Each failure was expensive but educational.

Cultural transformation emerged as perhaps the most difficult challenge. Converting infrastructure financiers into retail lenders wasn't just about training—it required fundamental mindset shifts. The company learned to hire for attitude and train for skills, bringing in fresh talent while retaining institutional knowledge. The lesson: in transformation, culture eats strategy for breakfast.

The approach to competition was particularly instructive. Rather than competing head-to-head with established players, L&T Finance found white spaces—segments too small for banks, too complex for fintechs, too risky for traditional NBFCs. They didn't try to be the best at everything; they tried to be the only one doing certain things.

Risk management evolution provided crucial insights. Traditional risk models based on historical data didn't work for new products. The company learned to combine quantitative models with qualitative judgment, automated decisioning with human oversight, portfolio-level risk management with individual underwriting. The lesson: in retail lending, risk management is about probability, not certainty.

The partnership strategy demonstrated ecosystem thinking. Rather than building everything in-house, L&T Finance partnered strategically—with technology companies for digital capabilities, with manufacturers for distribution, with e-commerce platforms for customer acquisition. The lesson: in modern financial services, competition is between ecosystems, not individual companies.

Perhaps the most important lesson was about courage. Exiting wholesale lending—the business that defined the company for decades—required enormous organizational courage. Leaders had to tell longtime clients they were no longer in that business. Entire teams had to be redeployed or let go. The safe path would have been gradual evolution; L&T Finance chose revolution.

The playbook concluded with a sobering reminder: transformation is never complete. Markets evolve, regulations change, technology advances, customer needs shift. The capability to transform—not any specific transformation—was the real competitive advantage. L&T Finance hadn't just changed its business model; it had built the organizational muscle to change again when needed.

X. Analysis & Bear vs. Bull Case

The investment committee meeting at a major mutual fund in Mumbai is getting heated. The analyst presenting L&T Finance is bullish: "They've achieved Lakshya 2026 targets two years early. Retail book growing at 25%+. Digital capabilities rival any fintech." But the risk manager pushes back: "Five-year sales growth of 2.46%. RoE of 7% over three years. These aren't numbers that inspire confidence." Both are right. That's what makes L&T Finance such a fascinating—and divisive—investment case.

The Bull Case starts with transformation momentum. Committed to 25% CAGR growth till FY26 isn't just a target—it's a trajectory already being achieved. The retail book growing at 28% annually while maintaining reasonable asset quality suggests the transformation isn't just working—it's accelerating. Bulls argue this isn't a turnaround story anymore; it's a growth story with the hard part already done.

Strong parent backing and brand value provide a moat that's hard to replicate. The L&T parentage means never having to worry about capital during stress, guaranteed access to funding even during liquidity crunches, and a brand that resonates across India. When farmers in Bihar trust you with tractor loans and software engineers in Bangalore trust you with personal loans, you've achieved something special.

Successful retailization ahead of schedule changes the entire narrative. What was supposed to be a five-year journey was largely completed in three. This execution capability—the ability to not just plan transformation but deliver it—is rare in Indian corporates. Bulls see a management team that under-promises and over-delivers.

Digital capabilities with physical presence create a unique competitive position. Pure digital players struggle with trust and complex products. Traditional players struggle with efficiency and customer experience. L&T Finance has seemingly cracked the code—digital where it adds value, human where it matters. The 2.5 crore customer base acquired through this hybrid model validates the approach.

The diversified product portfolio provides resilience. When microfinance faces stress, housing compensates. When urban slows, rural picks up. When two-wheeler sales decline, tractor financing grows. This isn't a single product bet—it's a portfolio approach to retail lending that smooths out cycles and reduces concentration risk.

The Bear Case is equally compelling. Poor 5-year sales growth of 2.46%, low 3-year RoE of 7.09% are backward-looking but still concerning. Yes, these numbers reflect the wholesale legacy, but they also raise questions about whether the retail transformation can overcome historical drags quickly enough to matter for investors.

Low interest coverage ratio concerns reflect structural challenges. NBFCs fundamentally borrow wholesale to lend retail—a model that works in good times but can quickly unravel during stress. Rising interest rates directly impact profitability. Unlike banks that can reprice deposits slowly, NBFCs face immediate margin pressure when rates rise.

Intense competition from banks and fintechs is only intensifying. Every major bank is pushing into retail lending. Every fintech with a payment app is offering credit. Big Tech giants are entering financial services. The competitive intensity means customer acquisition costs will rise, margins will compress, and growth will become increasingly expensive.

Asset quality risks in retail expansion are yet to fully play out. The retail book has grown from almost nothing to ₹90,000 crores in just a few years. History suggests that such rapid growth often comes with hidden asset quality issues that only emerge during economic stress. The next downturn will be the real test of underwriting quality.

Regulatory changes impact looms large. The RBI has been progressively tightening NBFC regulations—higher capital requirements, stricter NPA recognition, limits on leverage. There's constant speculation about further restrictions on unsecured lending. Each regulatory change disproportionately impacts NBFCs compared to banks.

The Nuanced Reality lies between these extremes. L&T Finance has successfully transformed its business model—that's indisputable. But whether this transformation creates sustainable competitive advantage remains uncertain. The company operates in structurally challenging segments where margins are thin, competition is intense, and regulatory oversight is increasing.

The valuation reflects this uncertainty. Trading at modest multiples compared to successful retail NBFCs like Bajaj Finance but premium to traditional wholesale NBFCs, the market hasn't fully decided what L&T Finance is worth. Is it a successful transformation story deserving premium valuations? Or a challenged NBFC trying to find its place in an increasingly difficult market?

The macro environment adds complexity. India's long-term consumption story remains intact—rising incomes, increasing formalization, growing credit penetration. But near-term challenges are mounting—inflation impacting affordability, rising rates increasing borrowing costs, global uncertainty affecting sentiment. L&T Finance is leveraged to both the opportunity and the risk.

The technology investment thesis is particularly interesting. Bulls see the digital capabilities as a differentiator that will drive efficiency and growth. Bears worry about the capital intensity of constantly upgrading technology and the risk of disruption from new players. The truth is that technology in financial services is now table stakes—necessary but not sufficient for success.

Risk-reward ultimately depends on time horizon and belief in execution. For long-term investors who believe in India's consumption story and management's execution capability, L&T Finance offers exposure to retail credit growth with the safety net of strong parentage. For skeptics worried about structural challenges and competitive intensity, better opportunities exist elsewhere.

The investment case for L&T Finance isn't about choosing between bull and bear—it's about weighing transformation success against structural challenges, execution capability against competitive intensity, growth potential against regulatory risk. It's a complex story requiring nuanced analysis, which perhaps explains why opinions remain so divided.

XI. Epilogue & Future Outlook

As 2025 dawns, Sudipta Roy stands where his predecessor once did, looking out from the 14th floor of L&T House at the Mumbai skyline. But the view has changed. The infrastructure projects that once dominated the horizon—metro lines, flyovers, commercial complexes—are no longer L&T Finance's primary concern. Instead, Roy sees millions of retail customers—each with their own dreams, needs, and financial journeys.

Post-Lakshya 2026: What's next? The company achieved its five-year targets in three years, but success brings its own challenges. The easy growth from retailization is behind them. Now comes the harder task of sustainable, profitable growth in an increasingly competitive market. The next strategic plan, still being formulated, will likely focus on deepening rather than broadening—higher wallet share from existing customers, better risk-adjusted returns, and operational excellence.

The Original bank ambitions vs. current path as diversified NBFC remains an intriguing subplot. L&T Finance had once harbored dreams of becoming a bank, even applying for a license during the 2014 round. That dream has been shelved, perhaps permanently. The realization: being a world-class NBFC might be better than being an average bank. The focus now is on leveraging NBFC advantages—flexibility, specialization, innovation—rather than chasing banking status.

The India credit story: Demographics and opportunity remains compelling despite near-term challenges. India's credit-to-GDP ratio at around 55% significantly lags global averages. Retail credit penetration is even lower. The opportunity isn't just large—it's generational. Millions of Indians will access formal credit for the first time in the coming decade. The question isn't whether the opportunity exists but who will capture it.

Technology disruption and embedded finance represent both opportunity and threat. The next wave of financial services won't be about standalone loans but credit embedded in purchase journeys. Buy now, pay later at checkout. Invoice financing at point of sale. Insurance bundled with loans. L&T Finance is positioning itself as the credit engine behind these experiences, partnering with platforms rather than competing with them.

Climate finance and ESG opportunities are emerging as unexpected growth drivers. The company's infrastructure heritage provides unique advantages in green financing—solar projects, electric vehicle loans, energy-efficient housing. The parent company's engineering expertise helps assess technical risks that pure financial players can't understand. It's a return to roots but in a completely different context.

The organizational evolution continues. The company that started with engineers has hired data scientists. The firm that once prized relationship managers now celebrates product managers. The culture that valued stability now rewards innovation. It's not just business model transformation—it's organizational metamorphosis.

Competition will intensify but also evolve. The next battle won't be between banks and NBFCs or traditional players and fintechs. It will be between ecosystems—integrated platforms offering complete financial solutions versus specialized providers offering best-in-class products. L&T Finance is betting on specialization with integration—excellent at what they do while partnering for what they don't.

Regulatory evolution remains a wildcard. The RBI's approach to NBFCs continues to tighten, but there's also recognition of their crucial role in financial inclusion. The regulatory framework is moving toward activity-based rather than entity-based regulation—same activity, same risk, same regulation. This could level the playing field between banks and NBFCs, or it could eliminate NBFC advantages entirely.

The human story underlying the financial narrative is worth noting. Thousands of employees who joined an infrastructure finance company found themselves in a retail lending firm. Many adapted, some thrived, others left. New talent joined—technologists, data scientists, digital marketers. The organization today would be unrecognizable to someone from 2010, yet the core values—engineering excellence, customer focus, ethical practices—remain unchanged.

Customer evolution will drive strategy. The farmer who took a tractor loan now wants a smartphone loan for his daughter. The young professional who started with a two-wheeler loan now needs a home loan. The small business that began with working capital now seeks expansion funding. L&T Finance's ability to grow with customers, serving evolving needs throughout their lifecycle, will determine long-term success.

Global perspectives provide sobering context. Worldwide, traditional financial services are being unbundled and rebundled in unexpected ways. Payment companies offer loans. E-commerce platforms provide insurance. Social media giants enable money transfers. The boundaries between financial and non-financial services are blurring. L&T Finance must navigate this convergence while maintaining its core lending expertise.

Final Reflections on the Transformation Journey

The story of L&T Finance's transformation from infrastructure lender to retail powerhouse is ultimately a story about adaptation. It's about recognizing when your core business is becoming obsolete and having the courage to change. It's about leveraging heritage while embracing innovation. It's about serving India's aspirations—from building its infrastructure to financing its dreams.

The transformation isn't complete—transformations never are. Markets evolve, customers change, technology advances, regulations shift. The capability to continuously transform, to remain relevant in changing times, is perhaps the most valuable asset L&T Finance has built.

As we close this narrative, L&T Finance stands at an inflection point. The first transformation—from wholesale to retail—is largely complete. The next transformation—from traditional retail lender to digital-age financial services provider—is just beginning. Whether they succeed will depend not on their ability to execute a plan but their capacity to adapt to an uncertain future.

The company that once financed India's infrastructure is now financing its consumption. The firm that built roads and power plants now enables motorcycle purchases and home ownership. It's a profound shift that reflects India's own evolution from an infrastructure-deficit nation to a consumption-driven economy.

In the end, L&T Finance's story is a microcosm of India's financial evolution—from project finance to retail credit, from relationship banking to digital lending, from serving corporations to empowering individuals. The next chapter of this story is being written now, loan by loan, customer by customer, dream by dream.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube