Lloyds Metals and Energy Limited: Unlocking India's Stranded Treasure

I. Introduction & Episode Roadmap

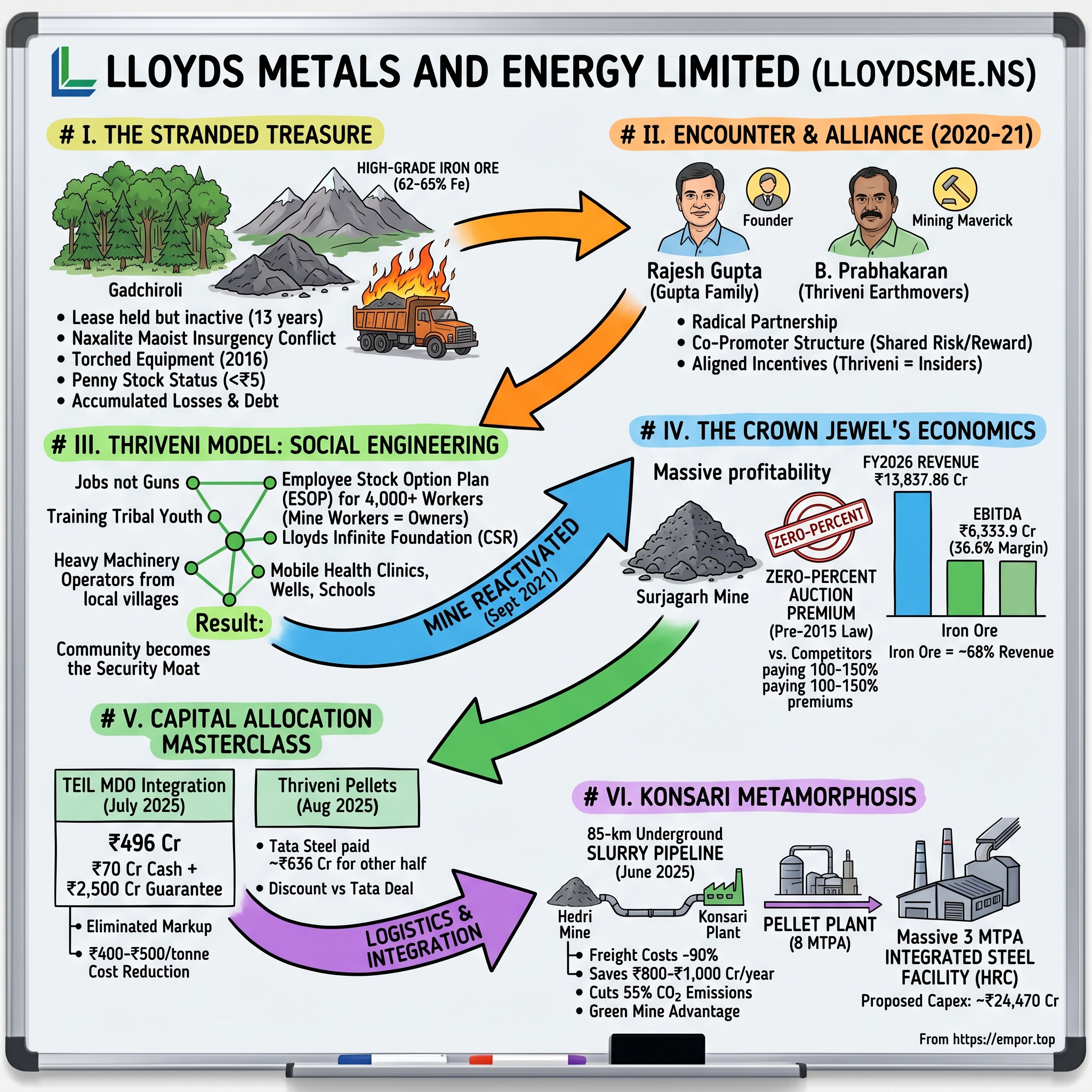

Picture a mining lease that exists on paper but not in reality. For roughly thirteen years, somewhere in the dense, monsoon-soaked forests of Gadchiroli in eastern Maharashtra, sat a geological lottery ticket nobody could cash. Beneath the tree canopy lay one of the highest-grade iron ore deposits in India—hematite running 62 to 65 percent iron content, the kind of ore that steelmakers around the world fight wars in boardrooms to secure. And on top of it sat a company that legally owned the right to dig it out, watching helplessly as its own bulldozers were torched, its executives killed, and its share price collapse to the price of a cup of chai.

That company was Lloyds Metals and Energy Limited, ticker LLOYDSME.NS on India's National Stock Exchange. In 2018, if you had described it to a portfolio manager, you would have used words like "distressed," "penny stock," and "stranded asset." It was a low-margin merchant of sponge iron—the industrial equivalent of a corner shop selling a commodity nobody loved—drowning in accumulated losses and debt, sitting on a treasure it could not touch because the treasure was buried in the bleeding heart of India's Left-Wing Extremism conflict, the decades-old Naxalite Maoist insurgency.

Now fast-forward to the financial year ending March 2026. That same company reported revenue of ₹13,837.86 crore and EBITDA of ₹6,333.9 crore—an operating margin of 36.6 percent that puts it not just at the top of the Indian steel value chain but among the most profitable mining operations anywhere on Earth.[^4] Penny stock to powerhouse. Stranded asset to crown jewel.

So here's the central question of this episode: How does a bankrupt, debt-ridden industrial company take a world-class deposit trapped inside an active war zone and turn it into one of the lowest-cost, highest-margin mining operations on the planet? This is not a story about a clever app or a viral product. This is a story about geology, regulation, capital allocation, and—most remarkably—about social engineering. About disarming an insurgency not with guns, but with payroll.

The cast is small but extraordinary. There is Rajesh Gupta, the founding-family promoter who spent twenty-seven years refusing to let a dormant mining lease die, holding onto a piece of paper that everyone else considered worthless. And there is B. Prabhakaran, the self-made mining operator from Tamil Nadu, the man behind Thriveni Earthmovers, who walked into a forest where global multinationals would not dare set foot and pacified a rebellion by making the rebels' own children co-owners of the mine.

Over the next several sections we'll trace the whole arc: the early years of the Indian sponge iron grind; the thirteen-year paralysis of the Surjagarh lease under Maoist blockade; the strategic masterstroke of the Thriveni alliance in 2020–21; the almost unfair, grandfathered economics of India's pre-2015 mining laws that give Lloyds a cost advantage competitors literally cannot buy; the surgical 2025 acquisition of the mine operator itself; the engineering marvel of an 85-kilometre underground slurry pipeline; and the company's audacious leap downstream into a fully integrated, ultra-low-cost steel giant rising at Konsari. Let's begin where every great industrial story begins—with a founder, a furnace, and a problem.

II. The Gupta Origins & The Ghugus Sponge Iron Era

In the early 1990s, India was a different country. The economy had just been cracked open by the 1991 liberalization reforms, license-raj walls were crumbling, and a generation of mid-sized industrial entrepreneurs sensed that the moment to build had finally arrived. Among them was the Gupta family, who set up Lloyds Metals to do something deeply unglamorous but genuinely useful: make sponge iron in Ghugus, a dusty industrial town in the Chandrapur district of Maharashtra.

To understand the whole saga, you have to understand what sponge iron actually is, because it sits at the very bottom of the steelmaking food chain. Sponge iron—the industry calls it Direct Reduced Iron, or DRI—is what you get when you take iron ore and strip the oxygen out of it using coal or natural gas, without ever melting it. The result is a porous, spongy lump of metallic iron that steel mills then feed into their furnaces. Think of it as a halfway product: more refined than raw ore, but a long way from a finished steel beam or a car body panel. It is the hamburger meat of the steel world—essential, ubiquitous, and almost impossible to make a fortune selling on its own.

Why is standalone sponge iron such a brutal business? Because you are squeezed from both ends. On one side, your raw material costs—iron ore and coal—are volatile and largely outside your control. On the other side, the price you can sell your sponge iron for is dictated by the swings of the broader steel market. You are a sandwich filling with no pricing power, no brand, and no moat. When ore prices spike or steel prices crater, your margins evaporate. Run a single DRI kiln with no captive raw material and no downstream integration, and you are essentially running a leveraged bet on commodity spreads you cannot influence. Good years are tolerable. Bad years are existential.

Rajesh Gupta and the early team understood this brutal arithmetic from the inside. They knew that the only way a sponge iron maker survives the cycle is to own its raw material—to mine its own ore rather than buying it at the mercy of merchant traders. Captive sourcing was the holy grail. It would turn a margin-squeezed converter into something far more durable.

So in 1993, the company went looking for ore. And they found it in a place that would define their destiny for the next three decades: a 348.09-hectare block at the Surjagarh Iron Ore Mine in the Etapalli tehsil of Gadchiroli district. On paper, it was a dream. The deposit held world-class hematite, the premium ore grading 62 to 65 percent iron—dramatically richer than the low-grade material many Indian steelmakers were forced to work with. Geologically, it was a once-in-a-generation prize.

Geographically, it was a nightmare. Gadchiroli is one of the most isolated and heavily forested districts in India, a sea of green hills near the borders of Chhattisgarh and Telangana. And it was, and remains, the historic sanctuary of the Naxalite Maoist insurgency—armed revolutionary groups who for decades have controlled vast tracts of these forests, opposing the Indian state and any sign of industrial development on tribal land. The very remoteness that left the ore undisturbed for millennia was the same remoteness that made it a fortress for an insurgency.

The lease application crawled through the Indian bureaucracy at geological speed. Fourteen years passed. Fourteen years of clearances, objections, forest regulations, and file-pushing between Mumbai and New Delhi. Finally, in May 2007, the twenty-year mining lease was formally executed—valid, with later extensions, all the way out to 2057. Champagne, presumably, was opened. The family had finally secured the captive ore that would transform Lloyds.

Except they had it exactly backwards. Getting the lease, it turned out, was the easy part. Holding the lease and actually operating it would drag the company to the very edge of total ruin. Because the moment Lloyds tried to put a shovel in the ground at Surjagarh, the forest answered.

III. The Forest of Shadows: 13 Years of Paralysis and LWE Conflict

The Maoists had a simple message for any company that arrived in Gadchiroli with earthmoving equipment: leave, or die. To the insurgents, a mine was not development—it was "capitalist exploitation" of tribal land, an outside corporation extracting wealth from the forest while the indigenous Adivasi communities remained poor. Industrialization, in their telling, was theft. And they enforced that ideology with a strict, brutal ban on mining, backed by the gun.

For Lloyds, the lease that had taken fourteen years to win became thirteen years of terror and paralysis. The forest swallowed the project whole. Every attempt to build infrastructure, every camp, every fleet of trucks became a target.

The violence was not abstract. In 2013, Naxalite cadres struck the mining camp directly, killing senior company personnel and workers in an attack designed to send an unmistakable message: this land would not be mined.[^9] For a company already stretched thin, the human cost was devastating and the operational message was clear—Surjagarh was off-limits.

Then came the firestorm. On a single night in December 2016, a coordinated Maoist force descended on the Surjagarh site and torched the operation to the ground. Roughly eighty vehicles—heavy mining trucks, earthmovers, dumpers, and supporting infrastructure—were set ablaze in one of the most spectacular acts of industrial sabotage in modern Indian history.[^9] Imagine an entire mining fleet, tens of crores of capital equipment, reduced to charred steel skeletons in the forest by morning. It was not just an attack on machinery; it was a statement that the insurgency could erase any industrial ambition at will.

Operationally, Surjagarh went dark. The mine that held a multi-billion-rupee deposit of premium ore became the textbook definition of a stranded asset—a resource of immense theoretical value that could not be touched, could not be financed against, could not generate a single rupee of cash flow. On the balance sheet it was an asset. In reality it was a money pit guarded by an army that did not answer to the company or, in much of the district, even to the state.

And here's where the second-order damage compounded. Remember why Lloyds wanted Surjagarh in the first place: to feed captive ore into the Ghugus sponge iron plant. With the mine paralyzed, that entire strategic rationale collapsed. The Ghugus kiln was forced to keep buying ore on the open market from third-party merchant miners at full retail prices—the exact high-cost dependency the company had spent fourteen years trying to escape. The sponge iron squeeze tightened into a vise. Buying expensive ore, selling cheap sponge iron into a cyclical market, with no captive cushion—the margins simply bled out.

The financial consequences were predictable and grim. Accumulated losses piled up. Debt mounted. And the stock, that ultimate scoreboard of market faith, collapsed into penny-stock territory, at points trading below ₹5 a share. For a sense of how far it had fallen: this was a company whose equity the market valued at roughly the cost of a bus ticket per share, a company that owned a world-class ore body it could not mine, a company that most investors had simply written off as a value trap with a tragic backstory.

By the late 2010s, leadership was, by any honest assessment, paralyzed. The conventional toolkit had been exhausted. You could not out-spend the insurgency on security—armed guards and razor wire only deepened local resentment and made the company a bigger target. You could not wait it out, because waiting bled cash. And you could not abandon the lease, because the lease was the only thing of real value the company had left. Lloyds was trapped in a strategic dead end of its own geology.

What it needed was not another security contract or another bank loan. It needed someone who understood that the problem in Gadchiroli was never really about engineering or capital. It was about people. And that someone was about to arrive from a thousand kilometres south, from a very different mining culture, carrying a very different idea about what "security" actually means.

IV. Enter the Mining Maverick: The Bold Alliance with B. Prabhakaran

To understand the turnaround, you have to understand the man who engineered it—and B. Prabhakaran is not your typical Indian industrialist. There's no inherited business empire here, no elite pedigree. Prabhakaran is a self-made mining entrepreneur from Tamil Nadu who built Thriveni Earthmovers from the ground up into India's premier Mine Developer and Operator, the kind of firm that does the actual dirty, dangerous, capital-intensive work of running a mine on behalf of the lease-holder.

His reputation was forged in the iron ore belts of Odisha, particularly the Keonjhar region, where Thriveni earned a name for doing something rare: operationalizing complex, high-friction mining projects in places where the conventional playbook failed. Where global multinationals studied a difficult mine, calculated the risk, and walked away, Prabhakaran's teams walked in. He built an operational culture obsessed with three things—throughput, cost discipline, and, crucially, managing the human and political environment around a mine rather than just the rock inside it. In an industry full of engineers who think in tonnes and grades, Prabhakaran thought in tonnes, grades, and trust.

By 2020, Lloyds Metals was a company out of options and out of road. And it's here that Rajesh Gupta made the decision that defines this entire story—a decision that, in hindsight, separates the founders who merely own assets from the founders who know how to unlock them. Most distressed promoters, cornered like this, would have done one of two things: sold the lease for scrap value to a larger player, or hired Thriveni as a hired-gun contractor on a fixed fee and prayed.

Gupta did neither. Instead of treating Thriveni as a vendor, he invited Prabhakaran inside the tent—as a co-promoter and genuine strategic partner.5 This was radical. It meant diluting the founding family's control. It meant sharing the upside of any future success with an outsider. It meant betting that Prabhakaran's operational genius was worth more than the equity it would cost. For a family that had clung to this lease for twenty-seven years through fire and death, handing a co-promoter seat to a Tamil Nadu earthmover was an act of either desperation or profound clarity. It turned out to be the latter.

The alliance was structured with surgical precision to align everyone's interests. First, Thriveni Earthmovers was appointed the exclusive Mine Developer and Operator for Surjagarh—the operational engine. Second, and far more importantly, Prabhakaran and Thriveni were formally inducted into the promoter group of Lloyds Metals, becoming insiders with skin in the game rather than contractors with an invoice. Third, Prabhakaran himself stepped into the role of Managing Director of the listed company, bringing his entire operational team with him to run the show, while Rajesh Gupta shifted his focus to architecting the downstream expansion—the steel and pellet ambitions that would come later.

The genius was in the incentive design. In a normal MDO contract, the operator wants to maximize its fee and the company wants to minimize it—their interests point in opposite directions, and every tonne mined is a negotiation. By making Prabhakaran a major equity holder, Gupta flipped that dynamic entirely. Now Prabhakaran's personal wealth was tied not to how big a contracting fee he could extract, but to how high Lloyds' stock could climb and how much ore the mine could produce. The operator and the owner were finally rowing in the same direction. The restructured combined promoter holding settled at a robust 61.64 percent, putting a controlling block of equity firmly in the hands of the very people responsible for the company's day-to-day success—and aligning them tightly with the minority shareholders along for the ride.5

It was a beautiful piece of corporate architecture. But architecture alone doesn't move ore out of a forest controlled by an armed insurgency. The real test was still ahead, in the villages of Surjagarh and Hedri, where Prabhakaran was about to deploy a security doctrine that no mining textbook had ever taught.

V. The Thriveni Model: How "Social Engineering" Disarmed a Rebellion

Here is the most counterintuitive idea in this entire story, and it's worth sitting with: the way you secure a mine in an insurgency is not by adding more guns. It's by removing the reason anyone wants to attack it.

Every company before Lloyds had reached for the same toolkit when facing the Naxalite threat—more state police, more private armed guards, more razor wire, more checkpoints. And every time, the result was the same. The fortifications became symbols of the very "outside occupation" the insurgents railed against. Each armed guard was a recruiting poster for the Maoists. Each checkpoint deepened the local tribal community's sense that the mine was a hostile foreign presence extracting their wealth at gunpoint. The harder companies tried to secure the asset by force, the more they fueled the resentment that made the asset un-securable.

Prabhakaran's philosophy inverted the whole equation. His thesis, in essence: development is the ultimate shield against militancy. If the surrounding villages were poor and excluded, the insurgency would always have a recruiting pool and a sympathetic population to hide among. But if those same villages became economically dependent on the mine—if the mine became the source of their prosperity rather than the symbol of their dispossession—then the community itself would become the security perimeter. You don't guard the mine from the people. You make the mine belong to the people.

The execution started with jobs, and not menial ones. Rather than importing skilled machine operators from outside the district—the standard practice, which would have meant the economic benefits flowed straight out of Gadchiroli—Thriveni built training academies inside the forests themselves. They recruited local tribal youth, including, remarkably, many young men who had grown up sympathetic to or entangled with the insurgent movement. And then they taught them to operate multi-crore heavy machinery: the excavators, the high-capacity dumpers, the earthmovers that are the beating heart of a modern mine.

Think about what that does to a young man's life. Yesterday he was an unemployed tribal youth in one of India's poorest districts, with the insurgency as one of the few organizations offering him purpose and a wage. Today he is a trained heavy-equipment operator earning a stable, high salary with full benefits—a salary that doesn't just support him but makes him the primary economic engine of his entire village. The mine didn't take something from his community. It made him the richest, most employable person his family had ever produced. Multiply that across thousands of households, and the social calculus of the entire region shifts.

Around the jobs, the company wrapped a comprehensive community program through the Lloyds Infinite Foundation, its CSR vehicle. This was not box-ticking philanthropy. They deployed mobile health clinics into villages that had never seen a doctor, drilled clean drinking-water wells, built schools, and set up self-help groups and tailoring units that gave tribal women their own independent incomes in Surjagarh and Hedri. Piece by piece, the mine stitched itself into the fabric of daily life across the region—healthcare, water, education, women's livelihoods. The company stopped being an extractor and started being infrastructure.

And then came the masterstroke, the move that genuinely had no precedent in Indian mining. In 2025, Lloyds implemented an Employee Stock Option Plan that extended ownership not just to managers and engineers in air-conditioned offices, but to over 4,000 employees—crucially including roughly 1,800 ground-level mine workers and drivers.[^11] Let that land. The tribal youth operating the dumpers, the drivers hauling ore through the forest—these were now literal co-owners of a publicly listed company. Lloyds became the first private Indian mining player to put equity into the hands of its frontline tribal workforce. The man driving the truck now had a stake in the share price.

This is where the social engineering became self-reinforcing. The local community now had a direct, personal, financial stake in the mine running safely and continuously. Every day of operations was a day their salaries arrived, their ESOPs accrued value, their village prospered. So when insurgent groups tried to threaten or disrupt mining, they ran into something no amount of armed guards could ever provide: the villagers themselves, standing up to protect their own livelihoods. The community had become the moat. The insurgency's old recruiting pool had been converted into the mine's own defenders.

The proof was in the production. Mining at Surjagarh recommenced at full throttle in September 2021—the asset that had been stranded for over a decade finally, irreversibly, came alive.[^9] Thirteen years of paralysis ended not with a military victory but with a payroll. And once the ore started moving, the world got to see just how extraordinary the underlying economics of this mine really were.

VI. The Crown Jewel's Economics: Iron Ore, Royalty Moats, and Competitor Benchmarking

Let's clear up a common misconception right at the top. People hear "Lloyds Metals" and "integrated steel plant" and assume this is a steel company. It is not—not yet, and not primarily. Strip away the narrative and look at where the money actually comes from, and one segment dominates everything: iron ore mining accounts for 67.89 percent of FY2026 revenue, roughly ₹9,394 crore, and over 80 percent of net profit.[^4] Everything else—pellets, sponge iron, the coming steel plant—is built on top of this one spectacular cash machine. To understand Lloyds, you have to understand why this mine prints money. And the answer is one part geology, one part a quirk of Indian law so favorable it almost feels unfair.

Start with the law, because it's the deepest part of the moat. In 2015, India fundamentally rewrote the rules of mining with an amendment to the Mines and Minerals (Development and Regulation) Act, the MMDR. Before 2015, the government granted mining leases through an administrative process—you applied, you waited, you got the lease, and you paid a standard royalty. After 2015, that world ended. Every new mining lease now had to be won through competitive auction. And here's the brutal part: bidders compete by offering the government a percentage of their ore's value—the "auction premium"—on top of all the normal royalties and costs.

This auction premium is the single most punishing line item in modern Indian mining, and it's where Lloyds' moat lives. Because Surjagarh's lease was executed back in 2007, it was grandfathered in. It sits entirely outside the auction regime. Lloyds pays a zero-percent auction premium, and it gets to keep that privileged status all the way out to 2057.3 In a single stroke of timing—a lease signed eight years before the law changed—Lloyds holds a cost structure that no competitor can ever replicate, because the door to zero-premium leases is permanently, legally shut.

Now let's make the math visceral, because this is the whole ballgame. Imagine a modern steel major—a JSW Steel, an ArcelorMittal Nippon Steel—bidding today for a fresh iron ore mine in Odisha or Karnataka. To win the auction, they routinely commit to auction premiums of 100 to 150 percent or more of the ore's value. So picture ore worth roughly ₹4,000 a tonne. The winning bidder might have to hand the government ₹4,000 to ₹6,000 per tonne in auction premium alone—before they've spent a single rupee actually digging the ore out of the ground. They are paying more than the ore is worth just for the right to mine it.

Lloyds pays none of that. Zero. Their obligations are the standard government royalty—around 15 percent of the Indian Bureau of Mines average sale price—plus minor statutory contributions to the District Mineral Foundation and the National Mineral Exploration Trust. That's it. So set the two cost structures side by side: a competitor handing over 100-plus percent of the ore's value before mining costs, versus Lloyds handing over roughly 15 percent. The gap isn't a rounding error; it's the difference between a thin-margin grind and one of the lowest cash costs of any iron ore producer in the world.

The strategic implication of that gap is what makes this asset so resilient. Consider a deep global steel downturn where iron ore prices fall by half. The competitor who paid a 130 percent auction premium is now selling ore for less than their premium-laden cost base—they bleed cash with every tonne, and they keep bleeding until prices recover or they shut the mine. Lloyds, sitting on a cash cost that's a fraction of the market price, stays comfortably profitable straight through the trough. This is what a true cornered resource buys you: not just fat margins in good times, but survival and profitability in the brutal times that bankrupt everyone else. It's a margin moat that holds when the tide goes out.

To appreciate just how unusual Lloyds' position is, walk through the competitive landscape. At the top sits NMDC, the National Mineral Development Corporation—the state-owned giant producing around 40 million tonnes a year with revenue north of ₹20,000 crore. NMDC is genuinely profitable and operates at enormous scale, but it's a merchant miner hemmed in by public-sector constraints, bureaucratic decision-making, and a notable lack of rapid downstream integration. It sells ore; it doesn't nimbly transform itself.

Then there are the respected integrated mid-caps in neighboring Chhattisgarh—Godawari Power & Ispat and Sarda Energy & Minerals. These are well-run, disciplined companies that investors rightly admire. But look at the scale: Godawari operates at a mining capacity of roughly 3 million tonnes a year against revenue around ₹5,400 crore, and Sarda runs at roughly 1.5 million tonnes. They are excellent small operators playing a fundamentally smaller game.

And this is where Lloyds' trajectory becomes almost vertiginous. They scaled Surjagarh production from 3 million tonnes a year to 10 million tonnes. And then, in June 2025, they secured Environmental Clearance to expand the mine to a colossal 55 million tonnes per annum.3 Read that again in context: a single mine cleared to produce more than the entire output of NMDC, the state-owned national champion. If Lloyds executes anywhere close to that clearance, they don't just join the front rank of Indian iron ore—they have a credible path to becoming the country's single largest iron ore powerhouse, from a lease that sat dead in the forest a decade ago.

There was, however, one leak in this beautiful machine—a place where some of that spectacular mining margin was quietly draining out of the listed company and into a private operator's pocket. Fixing it would require some of the most disciplined M&A India's mid-cap world has seen.

VII. Masterclass in Capital Allocation: The MDO Integration & Pellets Deals

Every great economic engine has a friction point, and for Lloyds it was hiding in plain sight in the very alliance that had saved the company. Thriveni Earthmovers ran the Surjagarh mine as the contracted MDO—and for that service, Lloyds paid Thriveni a fee on every tonne mined. That fee was the company's salvation. It was also a slow margin leak. Every rupee of operator markup paid to Thriveni was a rupee of mining EBITDA captured by a private entity rather than by the listed company's shareholders. And because Prabhakaran sat on both sides—co-promoter of Lloyds and owner of Thriveni—institutional investors had legitimate Related-Party Transaction concerns. Was the MDO fee fair? Was value flowing to the right place? It was the kind of governance overhang that caps a stock's multiple no matter how good the underlying business.

The fix arrived in July 2025, and it was a piece of capital allocation worth studying. Lloyds acquired a 79.82 percent equity stake in Thriveni Earthmovers and Infra Private Limited—the demerged MDO business that held the Surjagarh operating rights—for a cash consideration of just ₹70 crore.61 Seventy crore. For context, that's a fraction of what this business throws off in a single quarter. On the face of it, the headline price looks almost too small to be real.

Did Lloyds steal it? On the raw numbers, yes—₹70 crore for a business that operates a mine sitting on an order book worth around ₹70,000 crore over a 15-to-18-year horizon is, by any conventional valuation lens, a giveaway.1 But the headline price never tells the whole story in a deal like this, and the real consideration was more complex. As part of the transaction, Lloyds also had to step in behind TEIL's existing external lenders, issuing a ₹2,500 crore financial guarantee to backstop the operator's debt.6 So the "₹70 crore acquisition" really meant taking ₹70 crore of cash off the table plus assuming a multi-thousand-crore contingent liability. That's the catch the headline misses, and it's why disciplined investors read past the press release.

Even with the guarantee, though, the financial logic was overwhelming. By bringing the MDO business inside the listed entity, Lloyds eliminated the contractor markup entirely—the margin that used to leak out to Thriveni now stayed with Lloyds' own shareholders. Management has guided that this consolidation reduces iron ore mining costs by ₹400 to ₹500 per tonne.6 On a mine moving tens of millions of tonnes a year, that per-tonne saving compounds into enormous, recurring profit, captured permanently inside the listed company. And as a bonus, it dissolved the Related-Party overhang in one move: there's no related-party fee to scrutinize when the operator and the owner are the same legal entity. Better margins and better governance, bought for a song. That is what world-class capital allocation looks like.

A month later, Lloyds ran the same playbook on the next link in the chain. In August 2025, the company acquired a 49.99 percent stake in Thriveni Pellets Private Limited, the pelletizing business, for ₹495.71 crore—structured as ₹200 crore in cash plus a ₹285.89 crore stock swap.[^7] Pellets are the next step up the value ladder from raw ore: you take iron ore fines, bind them into uniform marble-sized balls, and produce a premium, furnace-ready feedstock that commands better pricing and is exactly what modern steel plants want. Owning the pellet business meant Lloyds captured yet another margin layer that would otherwise have sat outside the company.

But here's the detail that reveals just how shrewd Lloyds' negotiators were—and it comes from an almost perfect natural experiment. In December 2025, Tata Steel, one of the most respected blue-chip steelmakers in the world, approved the purchase of the remaining 50.01 percent stake in that very same Thriveni Pellets business—for ₹636 crore.[^7] So we have two buyers acquiring almost identical halves of the same company within months of each other. Tata, the blue-chip, paid ₹636 crore for its half. Lloyds paid ₹495.71 crore for its near-identical half. Lloyds secured a discount of more than ₹140 crore versus what one of the savviest buyers in Indian industry was willing to pay for the same asset. When a mid-cap negotiates a better entry price than Tata Steel on the identical deal, that's not luck—that's discipline, and it's exactly the kind of signal long-term investors should weigh when judging a management team's stewardship of shareholder capital.

So Lloyds had now consolidated the mine and the pellet plant under one roof, capturing margin at every stage from rock to furnace-ready feedstock. But there remained a physical problem that no clever acquisition could solve—a problem of distance, diesel, and forest roads. And solving it would require burying an engineering marvel 85 kilometres long.

VIII. Logistics and Integration: The Slurry Pipeline and the Konsari Metamorphosis

Here's a logistics puzzle that would keep any operations executive up at night. You're mining millions of tonnes of iron ore deep inside a remote forest. Now you have to get all of that ore out—every single tonne—to a processing plant kilometres away. Your only option, historically, is trucks. Thousands upon thousands of heavy diesel trucks, grinding day and night along narrow, winding forest roads that were never built for this kind of traffic.

The costs of that approach pile up in every dimension. Financially, road freight on millions of tonnes is staggeringly expensive. Socially, a relentless convoy of heavy trucks tearing through tribal villages generates exactly the kind of local friction Lloyds had worked so hard to dissolve—noise, dust, accidents, road damage. Environmentally, all that diesel means a mountain of carbon emissions. And operationally, a fleet strung out along forest roads is vulnerable—the very kind of soft, dispersed target that an insurgency had exploited before. Trucks were a bottleneck, a cost center, and a risk all at once.

So in June 2025, under Prabhakaran's direction, Lloyds commissioned one of the most impressive pieces of infrastructure in Indian mining: a 10-million-tonne-per-annum, 85-kilometre underground slurry pipeline connecting the Hedri mine to the Konsari processing plant.2 If you've never encountered slurry transport, the concept is elegantly simple. You crush the iron ore into fine particles, mix it with water until it forms a thick, flowing slurry—imagine a dense, metallic mud—and then pump that slurry at high velocity through a sealed pipe buried underground, straight from the mine to the plant. No trucks. No drivers. No forest roads. Just ore flowing silently beneath the earth like water through a pipe, twenty-four hours a day.

The economics are transformative, and they're worth dwelling on because they reshape the entire cost structure. The pipeline slashed freight costs by ₹800 to ₹1,000 per tonne—making ore transport roughly 90 percent cheaper than moving it by road.2 Run that across 10 million tonnes of annual transport, and this single buried asset saves the company somewhere in the neighborhood of ₹800 to ₹1,000 crore every year. That's not a marginal efficiency gain; that's a structural reset of the delivered cost of ore, dropping straight to the bottom line year after year, and it stacks directly on top of the ₹400-to-₹500-per-tonne saving from the MDO consolidation. The two cost reductions compound. Lloyds isn't just low-cost because of a lucky lease—it has aggressively engineered every rupee out of the chain between rock and plant.

And there's a "green mine" dividend that doubles as a strategic moat. By bypassing road transit entirely, the pipeline cuts truck traffic off the forest roads, reduces transportation-related carbon emissions by roughly 55 percent, and eliminates the daily friction with local villages.2 In an era when global steel buyers and lenders increasingly scrutinize the carbon footprint of their supply chains, having a demonstrably greener, lower-emission ore supply isn't just good citizenship—it's a commercial advantage that's hard for truck-dependent competitors to match. The pipeline simultaneously made the operation cheaper, cleaner, safer, and more socially acceptable. Rarely does one asset deliver on every axis at once.

The pipeline feeds the next stage of integration at Konsari: pelletization. Pellets now represent 19.26 percent of FY2026 revenue, roughly ₹2,665 crore—the crucial midstream layer that bridges raw ore and finished steel.[^4] Lloyds moved aggressively here too, commissioning the first phase of its Konsari pellet capacity in June 2025 and doubling capacity to 8 million tonnes a year with Phase 2 in May 2026, with stated plans to scale further toward 12 million tonnes.[^4] Each tonne of pellets is ore that Lloyds has upgraded into a premium product inside its own four walls, capturing the value-add rather than selling cheap fines to someone else who does.

But pellets are not the destination. They are the launchpad for Lloyds' most audacious bet—and the one that will define the next decade of this story. To finally escape the merchant ore cycle altogether, Lloyds is building a massive integrated steel facility at Konsari. The project centers on a 3-million-tonne-per-annum Hot Rolled Coils flat steel plant paired with a 483-megawatt captive power plant, carrying a proposed capital expenditure of around ₹24,470 crore.4 Hot Rolled Coils—flat sheets of steel rolled at high temperature—are the workhorse product that goes into everything from cars to construction to appliances, and they sit far higher up the value chain than ore or pellets.

The strategic logic is the culmination of everything we've discussed. By feeding its own ultra-low-cost captive ore and pellets directly into its own steel furnaces, Lloyds aims to produce Hot Rolled Coils at a cash cost among the lowest anywhere in the world. A normal steelmaker buys ore at market prices and lives or dies by the spread between volatile raw material costs and volatile steel prices—the same brutal squeeze that defined the old Ghugus sponge iron days, just at a larger scale. Lloyds is engineering that squeeze out of existence. When your ore is grandfathered at zero auction premium, transported at 90 percent below road cost, and converted in your own plant, your steelmaking margin becomes extraordinarily resilient through the cycle. That's the prize: not just a steel company, but the lowest-cost integrated steel company in the country. The question for investors is whether that thesis holds up under a rigorous strategic framework—so let's war-game it.

IX. Playbook: Strategic Powers and Framework Analysis

Strip away the dramatic narrative—the insurgency, the burning trucks, the tribal ESOPs—and ask the cold analytical question every long-term investor must ask: where does Lloyds' competitive advantage actually come from, and is it durable? Two classic frameworks help us pressure-test the answer.

Start with Hamilton Helmer's 7 Powers, the gold standard for identifying genuine, persistent competitive advantage. Lloyds exhibits three of them, in descending order of strength.

The primary power, and it's a textbook example, is the Cornered Resource. The Surjagarh lease—valid to 2057, carrying a zero-percent auction premium, sitting on world-class 62-to-65-percent hematite—is the single most important fact about this company. A cornered resource is preferential access to a coveted asset that competitors cannot replicate at any price, and that's precisely what the pre-2015 grandfathered lease represents. No amount of capital lets a rival buy an equivalent. The auction regime that governs every new lease guarantees that any competitor must pay 100-plus percent premiums for inferior access. The state granted Lloyds a monopoly on a specific geological prize and then, by changing the law in 2015, slammed the door so no one else can ever get the same terms. This is the bedrock of the entire investment case.

The secondary power is Scale Economies. As Lloyds ramps mining toward 26 and ultimately 55 million tonnes a year, runs an 85-kilometre slurry pipeline, and operates 8-million-tonne pellet plants, its enormous fixed-infrastructure costs spread across ever-larger volumes. The pipeline costs roughly the same whether it carries 8 or 10 million tonnes; the per-tonne fixed cost falls as throughput rises. This drives unit costs toward rock-bottom levels and creates a virtuous cycle—lower costs fund more expansion, which lowers costs further. Scale here isn't just bigness; it's a self-reinforcing cost advantage.

The third power is the subtlest and, in some ways, the most interesting: Process Power, embodied in what we might call the Thriveni social engineering model. The organizational capability to operate mines, manage tribal community relationships, and maintain security through local development in a Left-Wing Extremism zone is not a thing you can buy off a shelf or replicate with a consulting deck. It was built painfully, over years, through trust earned village by village, job by job, ESOP grant by ESOP grant. A traditional corporate competitor parachuting into Gadchiroli could not reproduce it quickly, if at all—they'd reach for guards and razor wire and fail exactly as everyone before Lloyds failed. This process power is what made the cornered resource accessible in the first place; geology gave Lloyds the prize, but process power is what let them actually pick it up.

Now run it through Porter's Five Forces, the classic industry-structure lens, and the picture is just as favorable.

Threat of new entrants: very low. Mining leases are finite, government-granted, and now auction-gated. Any new entrant must win a lease at a competitive premium that structurally destroys their margin relative to Lloyds. The barrier isn't capital or technology—it's that the regulatory door to favorable economics is permanently closed.

Bargaining power of suppliers: very low. After the July 2025 MDO acquisition, Lloyds owns its own upstream—the mine operator, the heavy machinery fleet, the slurry logistics network. There's no powerful external contractor to extract rent. The company is, increasingly, its own supplier.

Bargaining power of buyers: low to moderate. High-grade iron ore and pellets are in structural shortage in India, precisely because steel majors like JSW, Tata, and ArcelorMittal Nippon Steel are adding enormous downstream capacity that all needs feeding. When demand structurally outstrips supply of quality feedstock, the seller holds the cards. As Lloyds integrates into steel itself, it increasingly becomes its own buyer, neutralizing this force further.

Threat of substitutes: very low. There is simply no economic substitute for iron ore in primary steelmaking. Steel runs the modern world, and iron ore makes the steel. This is about as substitute-proof as an industrial input gets.

Intensity of competitive rivalry: low. And here's the elegant conclusion the whole framework points to: because Lloyds sits in the lowest-cost quartile of the global cost curve, it doesn't really compete on price at all. It's a price-taker that remains robustly profitable even when prices fall to levels that wipe out higher-cost rivals. You don't fight a price war when you can simply outlast everyone in the trench. Low-cost position converts brutal industry cyclicality from a threat into a competitive weapon.

Put both frameworks together and the structural picture is unusually strong—a cornered resource protected by regulation, amplified by scale, made accessible by a unique process, and operating in an industry whose forces all tilt in the incumbent's favor. But "structurally strong" is not the same as "without risk." So let's turn to the other side of the ledger.

X. The Investment Case: Bull vs. Bear, Key KPIs, and Risks

If you're going to track this company as a long-term owner, you don't need to monitor fifty metrics. You need to watch three things—the three KPIs that, between them, capture nearly the entire thesis. The reader keeps the scorecard; here's what belongs on it.

The first is mining dispatch and volume growth, measured in million tonnes per annum. This is the engine. The entire bull case rests on Lloyds ramping Surjagarh from its current 10 million tonnes toward the cleared 26 million and ultimately 55 million tonne levels.3 Volume is where the cornered resource and scale economies convert into actual cash flow. If dispatches stall—whether from clearances, infrastructure, or security—the growth story stalls with them. Watch the tonnes.

The second is delivered raw material cash cost per tonne. This is the moat made measurable. It captures whether the structural advantages—the zero-premium lease, the ₹800-to-₹1,000 per tonne pipeline saving, the ₹400-to-₹500 per tonne MDO consolidation benefit—are actually showing up in the numbers and holding through the cycle.26 A rising delivered cash cost would be the earliest warning that the magic is fading. A falling one confirms the machine is working as designed.

The third is Konsari steel capex execution. The ₹24,470 crore integrated steel project is the company's biggest bet and its biggest risk simultaneously.4 Track the construction milestones, the timeline discipline, and crucially the debt-versus-equity funding mix. Execution here determines whether Lloyds successfully transforms from a brilliant miner into a brilliant integrated steelmaker—or whether the ambition outruns the balance sheet.

Now the bear case, because no honest analysis skips it, and the risks here are real and specific.

The first and most viscerally obvious is security and Left-Wing Extremism risk. Yes, the Thriveni model has been a remarkable success, and yes, the community has become the mine's defender. But Gadchiroli remains a historically volatile zone, and the social peace, however well-engineered, is not guaranteed to be permanent. A major resurgence of insurgent activity, a shift in regional politics, or a coordinated act of sabotage—particularly against the 85-kilometre slurry pipeline, which is a long, fixed, hard-to-guard target buried across forest terrain—could disrupt or halt operations. The very asset that makes Lloyds efficient also concentrates risk into a single physical artery. This is the tail risk that never fully goes away.

The second is regulatory and windfall-tax risk, and it's the dark mirror of the company's greatest strength. Lloyds is spectacularly profitable precisely because of its grandfathered zero-premium lease. But spectacular profitability earned from a state-granted advantage makes a company a natural political target. A cash-strapped state government looking at Lloyds' margins could impose a new mineral cess, a windfall tax, or push for retrospective changes to royalty structures. India has a history of exactly this kind of intervention when commodity profits become conspicuous. The same regulatory quirk that built the moat could, with a stroke of a legislative pen, narrow it. Investors should watch state-level mining policy closely.

The third is capex overrun and balance-sheet strain. Pouring more than ₹24,000 crore into the Konsari integrated steel project is a bet of enormous magnitude. If steel prices enter a multi-year downturn while the plant is mid-construction—or if the project runs over budget and behind schedule, as megaprojects so often do—the debt taken on to fund it could strain a balance sheet that has only recently emerged from a distressed past. The financial guarantee structures around the Thriveni acquisitions add contingent liabilities on top. Diversifying downstream is strategically sound, but execution risk on a project this large is non-trivial, and leverage amplifies mistakes.

And yet, weigh all of that against the bull case, and you understand why the market re-rated this company so dramatically. Lloyds possesses what may be the single most profitable upstream steel asset in India: a grandfathered, zero-premium lease on a world-class ore body, made dramatically cheaper still by an 85-kilometre slurry pipeline and full ownership of its own mining operation. That combination puts Lloyds among the lowest-cost producers of iron ore and pellets in the world—a position that generates cash through the deepest downturns. As the company integrates downstream into flat steel, it stands to capture the entire value chain from rock in the Gadchiroli forest to Hot Rolled Coil rolling off the line at Konsari. If the execution holds, this is a business engineered to throw off massive free cash flow for decades, with a cost structure competitors cannot legally replicate. The bull case isn't that Lloyds got lucky. It's that Lloyds turned luck—a lease signed in 2007—into a fortress through relentless operational and capital-allocation discipline.

XI. Epilogue & Outro

Step back from the spreadsheets and the strategic frameworks, and the deepest lesson of the Lloyds Metals story is almost philosophical. The most valuable corporate assets in the world are not always stranded by the obvious things—by missing technology, by superior competitors, by a lack of capital. Sometimes the world's richest treasure sits in plain sight, fully owned and legally secured, rendered worthless by something far harder to solve than any engineering problem: social friction and political conflict. For thirteen years, Lloyds owned a multi-billion-rupee deposit it could not touch, not because the ore was hard to find, but because the people around it had every reason to burn its trucks.

What unlocked it was not a better drill or a bigger security budget. It was an idea—that you don't conquer a community, you align with it. By weaving together the incentives of local tribal workers, a strategic operating partner, and the founding promoters into a single shared stake in success, Lloyds converted its greatest liability into its strongest defense. The young men who might once have been recruited to attack the mine became the heavy-equipment operators, the co-owners, and ultimately the protectors of it. A security crisis was transformed into an economic fortress, and a stranded asset became, by FY2026, one of the most profitable mining operations on Earth.

That is the real takeaway, and it travels far beyond one iron ore mine in Maharashtra. Operational excellence in the hardest places on Earth is rarely just a matter of engineering. It is a matter of social integration—of understanding that beneath every stranded asset there is usually not a geological problem, but a human one. Solve the human problem, and the treasure unlocks itself.

References

-

Thriveni Earthmovers and Infra Stake Acquisition Disclosure — EquityBulls, 2025-01-08 ↩↩

-

Lloyds Metals commissions 85-km underground iron ore slurry pipeline — Business Standard, 2025-06-18 ↩↩↩↩

-

Environmental Clearance for Surjagarh Mining Expansion to 55 MTPA — Ministry of Environment, Forest and Climate Change, Govt of India, 2025-06-22 ↩↩↩

-

Lloyds Metals plans massive Rs 25,000 crore integrated steel plant expansion in Gadchiroli — ET Infra, 2025-03-12 ↩↩

-

Promoter Shareholding Pattern and Corporate Disclosures — National Stock Exchange of India (NSE) ↩↩

-

Acquisition of 79.8% stake in Thriveni Earthmovers and Infra Completed — HDFC Sky Research, 2025-07-01 ↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube