Lloyds Engineering Works: From Mumbai Workshop to Heavy Engineering Powerhouse

I. Introduction & Opening Hook

Picture this: A cramped fabrication workshop in Andheri, Mumbai, 1974. The clang of metal on metal echoes through the humid air as workers bend steel plates by hand, their faces streaked with grease and sweat. No one in that workshop could have imagined that this modest operation would one day fabricate components for India's nuclear reactors, supply critical equipment to oil refineries stretching from Gujarat to Assam, and command a market capitalization of ₹9,318 crores on the National Stock Exchange.

This is the unlikely story of Lloyds Engineering Works—a company that epitomizes India's industrial evolution from import-dependent economy to manufacturing powerhouse. Today, LLOYDSENGG designs, manufactures, and commissions some of the most complex heavy engineering equipment in the country: massive pressure vessels that withstand extreme temperatures, marine loading arms that transfer millions of barrels of crude oil, heat exchangers for nuclear power plants that must operate flawlessly for decades.

The central question isn't just how a small fabrication unit became critical to India's infrastructure backbone—it's about understanding the precise moments, decisions, and transformations that created this value. Because in the heavy engineering space, where projects can take years and a single failure can destroy decades of reputation, success requires something more than capital or connections. It demands technical excellence, certification moats, and most importantly, trust earned over generations.

What makes this story particularly compelling for investors is the transformation arc: from a debt-laden division of a steel company to a nearly debt-free, high-growth engineering platform generating 109% profit CAGR over the past five years. The stock price has gained over 4,300% in three years—a staggering return that begs the question: is this sustainable growth or speculative excess?

Over the next several hours, we'll dissect every layer of this transformation. We'll explore how regulatory changes in the License Raj era created opportunities for domestic manufacturers, why the complex demerger from Uttam Value Steels unlocked hidden value, how obtaining ASME certifications opened doors to nuclear projects, and what the recent acquisitions signal about management's vision for the next decade.

This isn't just a corporate history—it's a masterclass in navigating India's industrial landscape, building technical moats in commoditized industries, and creating shareholder value through strategic focus. Whether you're an investor evaluating LLOYDSENGG at 96.9 times earnings or an entrepreneur studying B2B success patterns, this deep dive will equip you with frameworks that transcend this single company.

Let's begin where all great industrial stories start: on the shop floor.

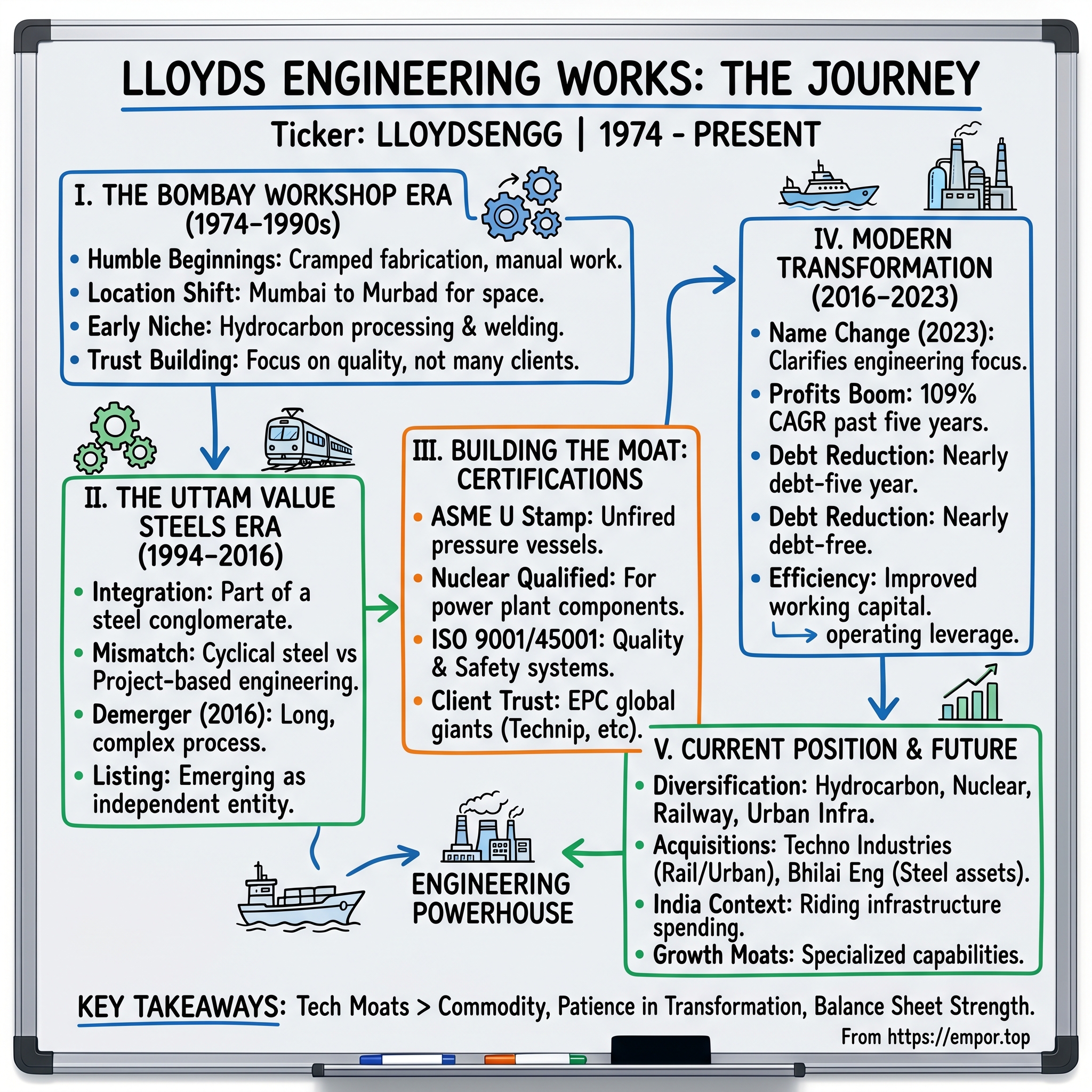

II. Origins: The Mumbai Workshop Era (1974–1990s)

The year 1974 wasn't chosen by accident. India had just survived the 1971 war with Pakistan, the first oil crisis was reshaping global economics, and Prime Minister Indira Gandhi's socialist policies were tightening their grip on private enterprise. In this environment of scarcity and regulation, starting a heavy engineering company required either exceptional vision or exceptional naivety—perhaps both.

The original workshop in Andheri represented something profound in 1970s Mumbai: indigenous manufacturing capability. While India imported most of its heavy machinery from Germany, Japan, and the Soviet Union, a small cohort of entrepreneurs bet that Indian companies could fabricate equipment locally if given the chance. The founders of what would become Lloyds Engineering Works were part of this cohort, though their names and specific stories have been obscured by subsequent corporate restructurings.

What we do know is revealing: the company quickly realized that Andheri's urban setting constrained their ambitions. Heavy fabrication requires space—massive yards for storing steel plates, high-ceiling workshops for vertical assembly, testing facilities for pressure vessels. The decision to establish operations in Murbad, roughly 100 kilometers from Mumbai in Thane District, was strategic. Land was cheaper, labor was available, yet proximity to Mumbai's port and commercial center remained manageable.

The Murbad facility became the company's technical heart. Here's what made it special: while competitors focused on simple fabrication—cutting, welding, basic assembly—Lloyds invested in capabilities for complex geometries and specialized welding techniques. They weren't just bending metal; they were solving engineering problems.

Consider the Indian industrial landscape of the late 1970s and 1980s. The License Raj meant that expanding production capacity required government permission. Import duties on finished equipment often exceeded 100%, while raw materials faced lower tariffs—creating a natural arbitrage for domestic fabricators. Every petrochemical plant, every steel mill, every power station being built under India's Five Year Plans needed pressure vessels, heat exchangers, storage tanks. The demand was guaranteed; the challenge was meeting specifications.

The company's early client relationships reveal its trajectory. Instead of chasing numerous small orders, Lloyds focused on fewer, more complex projects that required higher engineering content. A pressure vessel for a refinery isn't just a large tank—it must withstand specific pressures and temperatures, resist corrosion from harsh chemicals, and operate reliably for decades. Each successful delivery built trust, and in heavy engineering, trust translates directly to order books.

By the late 1980s, patterns emerged that would define the company's future. First, they developed expertise in hydrocarbon processing equipment—a sector where safety standards are non-negotiable and failure costs are catastrophic. Second, they began investing in certifications and quality systems before they became mandatory, understanding that technical credentials would become competitive moats. Third, they cultivated relationships with international engineering consultants and EPC (Engineering, Procurement, Construction) companies who specified equipment for major projects.

The workshop era wasn't glamorous. Annual reports from this period (if they existed) would show modest revenues, thin margins, and constant capital constraints. But something crucial was happening: technical knowledge was accumulating, welding procedures were being perfected, and a reputation for reliability was being established. In heavy engineering, these intangibles matter more than balance sheets.

One revealing detail: while many Indian engineering companies of this era tried to diversify into consumer goods or real estate when industrial orders slowed, Lloyds remained focused on heavy fabrication. This discipline—choosing depth over breadth—would prove critical when India's economic liberalization created new opportunities in the 1990s.

The Mumbai workshop era ended not with fanfare but with integration into a larger entity. As we'll see in the next section, the company's absorption into the Uttam Value Steels complex would create both opportunities and constraints, setting the stage for one of Indian capital markets' most interesting demerger stories.

III. The Uttam Value Steels Connection & Demerger Drama (1994-2016)

September 19, 1994 marked an inflection point that would take two decades to fully resolve. On this date, a shell company called "Climan Properties Private Limited" was incorporated—an innocuous beginning to what would become one of Indian capital markets' most complex restructuring sagas. This entity would undergo multiple transformations before emerging as the vehicle for Lloyds Engineering's eventual independence.

The story really begins with the Uttam Galva group's ambitious consolidation strategy in the steel sector. By the early 2010s, the group controlled multiple entities including Uttam Value Steels Limited (UVSL), which had absorbed various steel and engineering assets through a series of acquisitions and mergers. The engineering division—descendant of that original Mumbai workshop—found itself buried within this complex corporate structure, its potential obscured by the cyclical fortunes of the steel business.

Understanding why this mattered requires appreciating the fundamental mismatch between steel manufacturing and engineering services. Steel is a commodity business—capital intensive, cyclical, with margins determined by global supply-demand dynamics. Engineering services, particularly specialized heavy fabrication, operates on different economics: project-based revenues, technical differentiation, relationships driving orders. Combining these businesses under one entity created what finance professors call a "conglomerate discount"—the market couldn't properly value either business.

The demerger narrative accelerated in November 2013 when UVSL's board approved, in principle, the separation of its engineering division. This wasn't a simple decision. The engineering division, while smaller in revenue terms, possessed certifications and client relationships that had taken decades to build. For UVSL, shedding this division meant focusing on its core steel operations. For the engineering business, independence meant the ability to chart its own course.

The formal scheme of arrangement between Uttam Value Steels Limited and Lloyds Steels Industries Limited received sanction from the Hon'ble High Court of Judicature at Bombay via order dated October 30, 2015, with speaking minutes dated November 30, 2015. This wasn't just legal formality—it represented the untangling of decades of corporate complexity.

The mechanics of the demerger reveal careful structuring. Shareholders received 68 equity shares of Re. 1 each in the resulting company for their holdings in UVSL, with March 29, 2016 set as the record date. This ratio reflected the relative valuations of the demerged engineering business versus the remaining steel operations.

Following the scheme's sanction, Lloyds Steels Industries Limited listed on BSE Limited and National Stock Exchange of India Limited on July 18, 2016. This listing date marked the engineering division's debut as an independent entity after over four decades of operation. The market's initial reaction was muted—investors needed time to understand what exactly this newly listed entity represented.

What made this demerger particularly interesting was the contrast with the broader Lloyds group's fortunes. The original Lloyds Steel Industries—not to be confused with our protagonist—had faced severe financial stress in the early 2000s. Various group entities had undergone restructuring, mergers, and ownership changes. The engineering division's journey through this corporate labyrinth, emerging relatively unscathed with its technical capabilities intact, speaks to the resilience of its underlying business model.

The immediate post-demerger period presented challenges. The company inherited not just assets but also legacy obligations. Working capital had to be reorganized, customer contracts needed to be formally transferred, and perhaps most critically, the company had to establish its identity independent of the Uttam Value Steels brand that had backed it for years.

Yet the demerger also unlocked opportunities. For the first time, management could make capital allocation decisions based solely on the engineering business's needs. Investment in new certifications, expansion of facilities, and strategic acquisitions—all became possible without seeking approval from a parent company focused on steel manufacturing.

The corporate structure simplification had another crucial benefit: transparency. Investors could now directly analyze the engineering business's financials without the noise of steel operations. Order books, execution timelines, margin trends—all became visible. This transparency would prove critical when the company embarked on its next phase of growth.

One revealing detail from this period: while many demergers result in immediate value unlocking through re-rating, Lloyds Engineering's stock price remained subdued initially. The market was waiting for proof that independence would translate into improved performance. As we'll see, that proof would come emphatically, but it required building something more fundamental than financial engineering—it required technical excellence.

IV. Building Technical Moat: Certifications & Capabilities

The conference room at Murbad facility, March 2017. Management faces a strategic crossroads. The demerger dust has settled, the company is now independent, but the order book remains dominated by routine fabrication work with thin margins. Someone poses the critical question: "How do we move from being vendors to becoming partners?" The answer wouldn't come from financial engineering or aggressive bidding—it would come from something far more mundane yet powerful: certifications and technical capabilities that competitors couldn't easily replicate.

In heavy engineering, certifications aren't mere wall decorations—they're licenses to compete. Consider what it takes to supply a pressure vessel for a refinery. The vessel must withstand specific pressures, temperatures, and corrosive environments for decades. A single weld failure could trigger catastrophic consequences. This is why global engineering standards exist, and why obtaining certifications under these standards creates insurmountable barriers for competitors.

The company holds ISO 9001:2015 and ISO 45001:2018 certifications, foundational quality and safety management systems that signal basic operational competence. But the real differentiator comes from specialized certifications. The ASME (American Society of Mechanical Engineers) stamps represent the gold standard in pressure vessel manufacturing. Lloyds holds the ASME U stamp certification and complies with ASME Section 8 Division 1—enabling manufacture of unfired pressure vessels to internationally recognized standards.

The nuclear qualification represents perhaps the highest technical achievement. Compliance with ASME Section 3 NB, NC & ND allows the company to manufacture components for nuclear power plants—a market where quality requirements are absolute and vendor qualification can take years. Think about what this means: every weld procedure must be documented, every welder must be certified, every material must be traceable to its source. The paperwork for a single nuclear component can run thousands of pages.

These certifications opened doors to relationships with global engineering giants. The company earned trust from renowned consultants and EPC companies including Thyssenkrupp, Tecnimont, EIL, LINDE, PDIL, TOYO, Technip Energies, MECON, MN Dastur, Danieli, Primetals Technologies, and SMS Group. These aren't just clients—they're validators. When Technip Energies specifies Lloyds equipment for a refinery project, they're essentially certifying that this Indian manufacturer meets global standards.

The product portfolio evolution tells the story of increasing sophistication. Start with basic pressure vessels—large cylindrical containers that store fluids under pressure. Move to columns—vertical vessels with internal components for separation processes. Add reactors—vessels where chemical reactions occur under controlled conditions. Then heat exchangers—complex equipment with intricate internal geometries for efficient heat transfer. Finally, marine loading arms—articulated mechanical arms for transferring petroleum products between ships and shore, requiring precision engineering and fail-safe mechanisms.

Each product category represents years of capability building. A marine loading arm isn't just mechanical engineering—it's hydraulics, control systems, materials science, and safety engineering combined. The company's ability to design, manufacture, test, and commission these systems end-to-end differentiates it from fabricators who simply build to others' designs.

The trust equation in heavy engineering differs fundamentally from consumer businesses. A refinery manager choosing a pressure vessel supplier isn't swayed by marketing or price alone. They need confidence that the equipment will operate safely for 20-30 years. This trust accumulates slowly through successful project execution, but can be destroyed instantly by a single failure.

Consider the nuclear sector opportunity. India plans significant nuclear capacity additions over the next two decades. But the vendor ecosystem for nuclear-grade equipment remains limited. The combination of technical requirements, certification costs, and lengthy qualification processes deters new entrants. For those already qualified, like Lloyds, this represents a protected market with premium pricing.

The certification moat extends beyond technical capabilities to encompass organizational knowledge. Maintaining ASME certification requires regular audits, continuous training, and meticulous documentation. The procedures, quality systems, and institutional knowledge built over years cannot be quickly replicated even with unlimited capital. A competitor might buy similar equipment, but they can't buy the accumulated experience of hundreds of successful projects.

The general contracting and turnkey project capabilities marked another evolution. Instead of simply supplying equipment, Lloyds began taking responsibility for entire packages—design, procurement, installation, commissioning. This shift from product supplier to solution provider dramatically increased project values and margins while deepening client relationships.

What's remarkable about this technical capability building is its compound nature. Each successful project in a new domain—whether nuclear, marine, or specialized chemical processing—becomes a reference for future projects. Each new certification opens entire market segments. Each client relationship, once established through successful execution, tends to persist across multiple projects.

The investment in technical capabilities also changed the company's competitive positioning. Instead of competing with numerous local fabricators on price, Lloyds began competing with a select group of qualified suppliers on technical merit. This shift from commodity supplier to specialized engineering partner would drive the margin expansion we'll explore in the next section.

V. The Modern Transformation (2016–2023)

July 25, 2023. The company that had operated as Lloyds Steels Industries Limited since the demerger finally shed its misleading moniker. The name change to "Lloyds Engineering Works Limited" via fresh Certificate of Incorporation issued by the Registrar of Companies, Mumbai wasn't just cosmetic—it marked the culmination of a remarkable transformation that had been seven years in the making.

The numbers tell a story of dramatic operational improvement. From 2018 to 2023, profit grew at a staggering 109% CAGR. Revenue reached ₹795 crores with net profit of ₹96.1 crores—margins that would have seemed impossible during the Uttam Value Steels era. The company achieved nearly debt-free status, a remarkable accomplishment for a capital-intensive manufacturing business. But these headline numbers obscure the granular operational improvements that made them possible.

The transformation began with working capital management—the unsexy but critical foundation of manufacturing excellence. Working capital days dropped from 116 to 85.6 days through systematic improvements: tighter project management, milestone-based billing, better inventory control. Each day of working capital saved meant less borrowing, lower interest costs, and improved returns on capital.

The order book composition shifted dramatically. Instead of numerous small fabrication jobs, the company focused on larger, more complex projects with higher engineering content. A ₹100 crore contract for refinery equipment generates better margins and requires less management bandwidth than ten ₹10 crore contracts for simple vessels. This focus on project size and complexity drove operating leverage.

Management's approach to capacity utilization revealed sophisticated thinking. Rather than chasing volume at any price, they maintained pricing discipline even when utilization dipped. The logic was clear: accepting low-margin work today would signal to the market that Lloyds was a price-taker, undermining years of positioning as a technical specialist. Better to wait for the right projects than dilute the brand for temporary revenue gains.

The EBITDA margin expansion to 16.26% reflected multiple factors working in concert. First, the product mix shifted toward higher-value equipment. Second, operational efficiency improved through better project execution. Third, the company's growing reputation allowed selective bidding—pursuing only projects where they had competitive advantages. Fourth, the nearly debt-free status eliminated interest costs that had historically consumed operating profits.

The employee productivity metrics revealed another dimension of transformation. With 388 employees generating ₹795 crores in revenue, per-employee revenue exceeded ₹2 crores—impressive for an engineering company. This wasn't achieved through automation alone, but through systematic skill development, better project management tools, and organizational focus on high-value activities.

The company's approach to capital allocation during this period deserves attention. Despite generating substantial cash flows, management resisted the temptation for unrelated diversification—a common pitfall for successful Indian manufacturers. Instead, they reinvested in technical capabilities, certifications, and selective capacity expansion. The discipline to stay focused when cash was abundant proved as important as surviving when capital was scarce.

The COVID-19 pandemic provided an unexpected test of operational resilience. While many manufacturers struggled with disrupted supply chains and halted projects, Lloyds maintained execution continuity through several initiatives: localizing supply chains where possible, maintaining higher inventory buffers for critical materials, and working closely with clients to reschedule rather than cancel projects. The company emerged from the pandemic with strengthened client relationships and improved operational protocols.

A subtle but important shift occurred in customer concentration. While earlier periods showed heavy dependence on a few large clients, the modern era saw conscious diversification across sectors and geographies within India. No single client accounted for more than 15% of revenues, reducing project-specific risks while maintaining economies of scale.

The transformation wasn't without challenges. Debtor days increased from 73.6 to 97.9 days—a concerning trend that suggested either weakening bargaining power or conscious strategy to win orders through favorable payment terms. Management attributed this to the nature of large government and PSU contracts, which typically have longer payment cycles but offer better certainty of collection.

What makes this transformation particularly impressive is its sustainability. This wasn't financial engineering through leverage or aggressive accounting—it was fundamental operational improvement. The company built capabilities, won trust, executed projects, and reinvested profits. The boring basics of manufacturing excellence, executed consistently over years.

The July 2023 name change symbolized confidence. No longer needing the "Steels" association that might have provided comfort to stakeholders in earlier years, the company could stand on its own reputation. "Lloyds Engineering Works Limited" said exactly what the company did—no ambiguity, no borrowed glory from past associations.

By late 2023, the company had positioned itself uniquely in Indian heavy engineering: technically capable enough for complex projects, financially strong enough to take on large contracts, yet nimble enough to adapt to changing market requirements. This positioning would prove crucial as management embarked on the next phase of growth through strategic acquisitions.

VI. Current Business & Market Position

Walk through Lloyds Engineering's Murbad facility today and you'll witness controlled chaos that characterizes heavy engineering: massive steel plates being precision-cut by CNC machines, welders in protective gear executing X-ray quality welds, engineers hunched over CAD stations designing pressure vessels that must withstand decades of punishing service. With operations across four plants and four offices nationally, plus eight operational sites within India, this is industrial manufacturing at scale.

The sector exposure reads like a who's who of India's infrastructure backbone: hydrocarbon processing, steel plants, nuclear facilities, marine terminals, ports, and refineries. Each sector demands different technical competencies, certification requirements, and execution capabilities. This diversification isn't accidental—it's a conscious strategy to reduce dependence on any single industry's capital expenditure cycle.

Consider the current operational metrics: ₹795 crores in revenue generated by 388 employees from the primary Murbad facility, roughly 100 kilometers from Mumbai headquarters. The location strategy is deliberate—close enough to Mumbai for senior management oversight and port access, far enough to afford the vast spaces heavy fabrication demands. The facility spans multiple workshops for different manufacturing stages: cutting, rolling, welding, assembly, testing, and finishing.

The EBITDA of ₹137 crores at 16.26% margin places Lloyds in the upper tier of Indian engineering companies. These aren't software-like margins, but for heavy manufacturing involving material costs, labor, and substantial working capital, they represent exceptional operational efficiency. The margin structure reveals careful project selection—bidding on projects where technical capabilities provide pricing power rather than competing solely on cost.

The competitive landscape in Indian heavy engineering presents an interesting paradox. While numerous players exist, few combine Lloyds' specific capabilities: ASME nuclear certifications, marine loading arm expertise, turnkey project execution abilities, and balance sheet strength to handle large contracts. Larger competitors like L&T or Thermax operate at different scales and focus areas. Smaller players lack certifications or financial capacity for major projects. This positioning in the competitive "sweet spot" allows selective bidding.

Client concentration metrics have evolved favorably. Unlike earlier periods of dependence on few large customers, the current portfolio shows healthy diversification. The top ten clients contribute less than 60% of revenues, with no single client exceeding 15%. This wasn't achieved by accepting smaller projects, but by systematically expanding the client base while maintaining project size.

The order book dynamics deserve particular attention. Heavy engineering projects typically span 12-24 months from order to completion. This creates revenue visibility but also execution risks. Weather delays, material price fluctuations, design changes, and site readiness issues can all impact project timelines and margins. Lloyds manages these risks through milestone-based contracts, price variation clauses, and maintaining conservative timeline buffers.

The company's positioning in the nuclear sector illustrates its competitive advantages. Nuclear component manufacturing requires absolute quality adherence—a single failed weld could have catastrophic consequences. The regulatory requirements, audit processes, and documentation standards eliminate casual competitors. For qualified suppliers like Lloyds, this creates a protected market niche with premium pricing and long-term relationships.

Marine loading arms represent another specialized capability. These articulated mechanical arms must safely transfer volatile petroleum products between ships and shore facilities. The engineering combines mechanical design, hydraulic systems, control technology, and safety mechanisms. Global players like Kanon and SVT dominate this market, but Lloyds has carved out a position as a credible Indian alternative, particularly important given increasing emphasis on indigenous procurement.

The current market position also reflects broader India trends. The government's focus on infrastructure spending, energy security, and manufacturing self-reliance creates sustained demand for heavy engineering equipment. Whether it's refinery expansions for energy security, steel capacity additions for infrastructure, or port modernization for trade growth, each initiative requires the kind of equipment Lloyds manufactures.

Yet challenges persist. The 97.9 debtor days suggest collection cycles remain extended, particularly for government and PSU contracts. While bad debt risks are minimal with such clients, the working capital burden impacts return ratios. The company must balance the certainty of government orders against the working capital costs they impose.

The operational footprint across eight sites raises questions about optimal capacity utilization. While geographic distribution provides market access and execution flexibility, it also increases coordination complexity and potentially dilutes management focus. The company must balance the benefits of distributed operations against the efficiency gains from consolidation.

Looking at peer comparisons, Lloyds trades at valuations premium to most engineering companies but below specialized players in high-growth segments. The market seems to recognize the technical capabilities and execution track record while remaining cautious about the capital-intensive nature and project-based revenue model. This valuation gap between current multiples and potential based on operational metrics suggests opportunity—if execution continues.

VII. Recent Strategic Moves & Growth Initiatives

The boardroom discussions in early 2023 must have been intense. With the core engineering business firing on all cylinders, management faced a classic growth dilemma: organic expansion within existing capabilities or bold diversification through acquisitions? The answer, it turned out, would be both—executed with a precision that suggested careful strategic planning rather than opportunistic deal-making.

The acquisition of engineering assets from Bhilai Engineering Corporation marked the opening move. Bhilai, a PSU with decades of history supplying equipment to steel plants, had valuable assets but struggled with operational efficiency. For Lloyds, this wasn't just about adding capacity—it was about acquiring customer relationships, technical knowledge, and most importantly, credentials in the steel plant equipment space that would have taken years to build organically.

The 77% stake acquisition in Techno Industries revealed different strategic logic. Techno Industries securing a ₹19.58 crore escalator and AMC order from Mumbai Railway Vikas Corporation validated the rationale. This wasn't traditional heavy engineering but urban infrastructure—escalators, elevators, and transit systems. The Mumbai local train network, carrying millions daily, needs constant equipment upgrades and maintenance. Techno Industries' position in this market opened an entirely new revenue stream with different dynamics: urban rather than industrial customers, service revenues complementing equipment sales, and exposure to the urban infrastructure boom.

The 24.20% stake in Lloyds Infrastructure and Construction suggested another vector of expansion. While maintaining focus on engineering and equipment supply, this investment provided exposure to the execution side of infrastructure projects. The synergies were obvious: equipment supply relationships could lead to construction opportunities and vice versa.

These weren't random acquisitions but carefully orchestrated portfolio expansion. Each target brought something specific: Bhilai brought steel sector depth, Techno brought urban infrastructure exposure, and Lloyds Infrastructure brought project execution capabilities. Together, they transformed Lloyds Engineering from a pure-play equipment manufacturer to a multi-disciplinary engineering platform.

The railway sector entry deserves particular attention. Indian Railways, undergoing massive modernization with dedicated freight corridors, high-speed rail projects, and station redevelopments, represents a multi-decade opportunity. But entering this market requires more than manufacturing capability—it needs understanding of railway specifications, approval processes, and safety standards. The Techno Industries platform provided this entry point without the time and cost of building capabilities from scratch.

The transformation from mechanical engineering specialist to multi-disciplinary platform wasn't without risks. Each new sector brings different working capital cycles, customer dynamics, and execution challenges. Escalator maintenance contracts have different economics than pressure vessel supply. Railway projects follow different approval processes than refinery expansions. Managing this complexity while maintaining operational excellence in the core business requires sophisticated management systems.

International market aspirations, while not yet significantly contributing to revenues, indicate long-term ambition. The company's ASME certifications and successful domestic track record position it to compete for international projects, particularly in regions where Indian engineering companies have established credibility—Middle East, Africa, and Southeast Asia. Export potential exists not just for equipment but for turnkey project execution leveraging India's engineering talent cost advantages.

The diversification strategy also addressed a fundamental challenge in project-based businesses: revenue lumpiness. Heavy engineering projects can cause significant quarter-to-quarter revenue variations depending on execution stages and completion timing. Adding businesses with different cycles—urban infrastructure with steady maintenance revenues, railway projects with different execution timelines—smoothens overall revenue progression.

What's particularly impressive about these strategic moves is their capital efficiency. Rather than building capabilities from scratch, requiring years of investment with uncertain returns, the company acquired established positions at reasonable valuations. The Techno Industries stake, for instance, immediately generated orders and revenues rather than requiring patient capital for capability building.

The human capital dimension of these acquisitions often goes unnoticed but proves critical. Each acquired entity brought experienced engineers, established supplier relationships, and institutional knowledge. In engineering businesses where expertise accumulates over decades, acquiring experienced teams accelerates capability building far more effectively than hiring and training from scratch.

Risk management in this expansion phase showed maturity. The company didn't bet everything on acquisitions, maintaining strong organic growth in the core business. The stake sizes—77% in Techno, 24.20% in Infrastructure—suggested calibrated exposure rather than wholesale commitments. This allowed participation in new opportunities while limiting downside risks if sectors didn't develop as expected.

The market's reaction to these strategic moves has been mixed. While appreciating the growth potential, investors worry about execution complexity and potential dilution of focus. The premium valuations partly reflect confidence in management's ability to integrate acquisitions while maintaining operational excellence. Whether this confidence proves justified will determine if Lloyds Engineering becomes a diversified engineering conglomerate or remains a focused heavy engineering specialist that happened to make some investments.

VIII. Stock Market Journey & Shareholder Value Creation

The stock price chart from July 2016 to present looks like a hockey stick—years of sideways movement followed by explosive vertical growth. The raw numbers are staggering: from the listing price of around ₹2 to recent highs above ₹80, representing gains exceeding 4,300% in three years. But behind these headline-grabbing returns lies a more nuanced story of market psychology, valuation evolution, and the powerful effects of operational leverage in cyclical businesses.

The initial years post-listing were characterized by market apathy. From 2016 to 2020, the stock languished in single digits, occasionally spiking on quarterly results but lacking sustained momentum. Trading volumes were thin, institutional interest minimal, and retail investors largely unaware of the company's existence. This wasn't surprising—the company was emerging from a complex demerger, had limited financial history as an independent entity, and operated in an unfashionable sector.

The inflection point came in late 2020, coinciding with several factors. First, the company's operational improvements began showing in reported numbers—margins expanded, debt decreased, and order books grew. Second, the broader market's interest in manufacturing and infrastructure plays increased as India's capital expenditure cycle showed signs of revival. Third, and perhaps most importantly, the company crossed the critical market capitalization threshold that brought it onto institutional radar screens.

Today's valuation metrics would make value investors queasy: trading at 96.9 times price-to-earnings ratio and 15.3 times book value, the stock prices in perfection. These multiples exceed those of established engineering giants like L&T or Thermax, despite Lloyds' smaller scale and limited track record. The market is clearly pricing in expectations of sustained high growth and margin expansion rather than current fundamentals.

The promoter holding pattern tells its own story. Currently at 49.4%, down 6.87% recently, the reduction suggests either profit-booking by promoters or stake dilution for strategic investors. The timing of this reduction—at elevated valuations—appears opportunistic. Yet maintaining near-50% ownership indicates continued confidence in long-term prospects. The promoter stake provides stability but also limits free float, potentially contributing to price volatility.

Institutional ownership remains relatively modest compared to retail enthusiasm. Mutual funds and insurance companies typically prefer larger, more liquid stocks with longer operating histories. The limited institutional presence creates both opportunity and risk—opportunity for early institutional investors to build positions, risk from potential volatility without institutional support during market downturns.

The dividend payout ratio of 28.2% reflects balanced capital allocation. The company returns cash to shareholders while retaining sufficient capital for growth investments. This isn't a high-dividend yield story—at current valuations, the yield is negligible. Investors are clearly buying growth, not income.

Peer comparison reveals interesting valuation disparities. Established players like Thermax trade at 35-40 times earnings despite similar growth rates. Specialized engineering companies in high-growth segments command 50-60 times multiples. Lloyds at 96.9 times suggests either significant mispricing or market expectations of extraordinary growth acceleration. The truth likely lies somewhere between—the company deserves premium multiples for its transformation but current valuations embed aggressive assumptions.

The liquidity evolution has been dramatic. From days when a few lakhs rupees of trading would move the stock significantly, daily volumes now regularly exceed ₹50 crores. This liquidity improvement creates a virtuous cycle—better liquidity attracts more investors, particularly institutions requiring minimum trading volumes for portfolio positions.

Recent trading patterns suggest increasing institutional participation. Block deals, bulk deals, and delivery percentages have all increased, indicating accumulation by sophisticated investors rather than pure retail speculation. The stock's inclusion in broader indices as market capitalization grew brought passive index fund flows, providing additional support.

The volatility remains elevated compared to larger peers. Single-day moves exceeding 5% aren't uncommon, driven by quarterly results, order announcements, or broader market sentiment toward small-cap engineering stocks. This volatility creates opportunities for traders but challenges for long-term investors trying to build positions without moving markets.

Market capitalization crossing ₹9,000 crores places Lloyds in the mid-cap category, a sweet spot for growth investors. Too large to be ignored, yet small enough to deliver multi-bagger returns if execution continues. This positioning attracts a specific investor category—those seeking companies transitioning from small to large cap over investment horizons of 5-10 years.

The shareholding pattern evolution reveals changing investor composition. Retail holding has increased dramatically, drawn by spectacular returns and social media buzz. This retail enthusiasm, while providing liquidity, also increases volatility risk. Professional investors worry about weak hands that might sell at the first sign of trouble, creating cascading price declines.

The options market activity, where available, suggests growing sophistication in how markets view the stock. Put-call ratios, implied volatilities, and open interest patterns provide clues about institutional positioning and market expectations. The generally bullish skew indicates continued optimism, though protection buying suggests awareness of valuation risks.

What's remarkable about this stock market journey is its correlation with fundamental improvement. This wasn't a story of re-rating on hope or theme-based buying. Margins improved, debt reduced, capabilities expanded, and the stock followed. Whether current valuations have run ahead of fundamentals is debatable, but the direction of travel—both operational and stock price—has been consistently upward.

IX. Business Model & Unit Economics

The spreadsheet on the CFO's desk tells the real story of Lloyds Engineering's economics—not the headline revenue or profit numbers, but the intricate machinery of cash conversion, capital efficiency, and margin mathematics that determine whether a manufacturing business creates or destroys value over time. Let's dissect these unit economics with the precision they deserve.

Start with the fundamental revenue model: project-based contracts ranging from ₹10 crores to ₹200 crores, executed over 12-24 months. Unlike software companies with recurring subscriptions or FMCG businesses with daily sales, Lloyds operates in lumpy, milestone-driven revenue recognition. A single large project moving from 70% to 90% completion can dramatically impact quarterly results. This isn't accounting manipulation—it's the inherent nature of heavy engineering economics.

The working capital evolution reveals operational sophistication. Working capital days dropped from 116 to 85.6 days through systematic improvements across the cash conversion cycle. Inventory management improved through better production planning and just-in-time material procurement where possible. Receivables collection accelerated through milestone-based billing rather than end-of-project payments. Payables management balanced supplier relationships with cash conservation. Each day saved translates directly to improved return on capital employed.

Yet the recent increase in debtor days from 73.6 to 97.9 days raises questions. Management attributes this to changing customer mix—more government and PSU contracts with longer payment cycles but virtually zero bad debt risk. The trade-off is explicit: accept longer payment terms for payment certainty. In a business where a single large bad debt could wipe out years of profits, this conservative approach has merit, though it pressures return ratios.

The margin structure reveals the business model's beauty and challenge. Gross margins around 30-35% reflect material costs (steel, specialized alloys) comprising 65-70% of project value. The value addition comes through engineering, fabrication expertise, and project management rather than proprietary products or technology. EBITDA margins of 16.26% after operating expenses demonstrate exceptional efficiency for this sector.

But margin stability remains elusive. A project with design changes, execution delays, or material price escalations can quickly erode profitability. The company manages these risks through price variation clauses, conservative project timelines, and selective bidding, but perfect protection is impossible. The best projects generate 20-25% EBITDA margins; the worst can slip into single digits or losses.

Capital allocation patterns deserve attention. Growth capex versus maintenance capex splits roughly 70-30, indicating continued expansion while maintaining existing facilities. The growth investments focus on specialized equipment—automated welding systems, testing facilities, material handling equipment—that either expand capabilities or improve efficiency. The maintenance spending ensures consistent quality and safety standards, non-negotiable in this business.

The dividend payout ratio of 28.2% reflects balanced thinking. Returning nearly 30% of profits to shareholders signals confidence while retaining 70% for growth investments. At current valuations, the dividend yield is negligible—investors aren't buying for current income but future growth. This capital allocation discipline—not over-distributing during good times, not over-investing during exuberance—marks mature management.

Order book to revenue conversion typically runs at 2-2.5x annual revenue, providing 18-24 months visibility. But visibility doesn't equal certainty. Projects can be delayed, rescheduled, or occasionally cancelled. The conversion ratio—what percentage of order book converts to revenue within expected timelines—becomes crucial. Lloyds maintains approximately 85-90% conversion rates, respectable for the industry but highlighting execution risks.

The asset turnover ratios reveal capital efficiency. Revenue to gross block ratios exceeding 3x indicate sweating assets effectively. This isn't a capital-intensive business requiring constant capacity additions. Once established, facilities can handle significant revenue growth through better utilization, improved processes, and selective debottlenecking investments. This operational leverage explains why profit growth exceeded revenue growth during the transformation period.

Customer acquisition costs in B2B heavy engineering differ fundamentally from consumer businesses. There's no advertising spend or sales commissions. Instead, costs embed in technical team salaries, certification maintenance, and most importantly, the working capital invested in executing initial projects for new clients at potentially lower margins to establish credibility. The lifetime value of a satisfied client—repeat orders over decades—justifies these upfront investments.

The business model's resilience shows in downturns. Unlike fixed-cost manufacturing where utilization drops destroy profitability, Lloyds' project-based model allows capacity adjustment. If orders slow, hiring freezes, discretionary spending cuts, and project timeline extensions can preserve margins. The variable cost structure—materials comprising most costs—provides natural hedging. This flexibility proved valuable during COVID-19 when many manufacturers faced existential threats.

Competitive advantages translate directly to unit economics. ASME certifications allow 5-10% price premiums versus non-certified competitors. Nuclear qualifications open markets with 20-25% EBITDA margins versus 15% for standard projects. Marine loading arm capabilities access specialized segments with limited competition. Each technical moat translates to measurable economic benefit—higher margins, better payment terms, or preferred vendor status.

The scalability question remains partially answered. Can the company maintain current margins at ₹2,000 crores revenue? ₹5,000 crores? The optimistic view sees operational leverage improving margins as revenues grow over fixed costs. The skeptical view worries about competition intensifying, execution complexity increasing, and margins reverting to industry means. The truth likely depends on maintaining technical differentiation while scaling execution capabilities.

X. Risks, Challenges & Bear Case

Let's construct the bear case with the thoroughness it deserves—not to induce panic but to understand what could go wrong for a company trading at 96.9 times earnings with expectations of perpetual growth embedded in its valuation. The risks aren't hidden; they're inherent to the business model, sector dynamics, and current market positioning.

Start with the most obvious: cyclicality. Heavy engineering is a derived demand business—when refineries expand, steel plants modernize, or ports upgrade, Lloyds benefits. When capital expenditure freezes, orders evaporate. The current robust order book reflects India's infrastructure investment cycle, but cycles turn. The 2011-2016 period saw many engineering companies struggle with overcapacity, cancelled projects, and margin compression. At 96.9 times earnings, the stock prices in no slowdown for years.

Competition intensifies as margins attract capacity. The 16.26% EBITDA margins won't go unnoticed. Larger players like L&T might decide heavy fabrication deserves renewed focus. Chinese competitors, despite current geopolitical tensions, could eventually enter with aggressive pricing. New domestic players, seeing Lloyds' success, might invest in certifications and capabilities. The technical moats, while real, aren't permanent—they require constant investment to maintain and can be replicated given sufficient time and capital.

The working capital deterioration cannot be ignored. Debtor days increasing from 73.6 to 97.9 days signals either weakening negotiating position or conscious strategy to win orders through favorable terms. Either interpretation is concerning. If clients demand extended payment terms knowing Lloyds needs orders to justify valuations, margins could compress as competition intensifies. If management is deliberately extending terms to boost revenue growth, they're prioritizing topline over returns—a dangerous game in capital-intensive businesses.

Execution risks multiply with scale and complexity. Each project carries potential for delays, cost overruns, or technical failures. The company's track record is strong, but perfect execution is impossible. A single major project failure—delayed commissioning, technical specifications not met, or worst case, operational failure after installation—could destroy reputation built over decades. In heavy engineering, trust once lost is rarely regained.

The technology disruption threat, while not immediate, lurks. Additive manufacturing (3D printing) for metal components advances rapidly. Modular construction techniques reduce on-site fabrication requirements. Automation threatens employment-intensive manufacturing models. While these technologies won't eliminate heavy fabrication tomorrow, they could fundamentally alter industry economics over the next decade. Current valuations assume the traditional business model remains intact.

Regulatory and compliance challenges grow with sector expansion. Nuclear certifications require regular audits and any compliance failure means market exclusion. Environmental regulations tighten, potentially increasing costs or limiting certain activities. Safety incidents, always possible in heavy manufacturing, bring regulatory scrutiny, reputation damage, and potential liability. The more sectors Lloyds enters, the more regulatory complexity it faces.

Client concentration, while improved, remains meaningful. Government and PSU clients dominate order books. These clients offer payment certainty but also bring challenges: bureaucratic decision-making, political interference, and susceptibility to policy changes. A new government deciding to pause infrastructure spending or redirect priorities could dramatically impact order flows. The company's fortune ties closely to India's public sector capital expenditure.

The acquisition integration risks deserve attention. Buying assets from Bhilai Engineering Corporation, taking 77% of Techno Industries, and investing in infrastructure ventures creates execution complexity. Each business has different dynamics, cultures, and challenges. Management bandwidth stretches, focus dilutes, and the clarity that drove the initial transformation could blur. Many successful companies stumbled when acquisition ambitions exceeded integration capabilities.

Market structure risks compound valuation concerns. Limited institutional ownership means fewer stable hands during volatility. High retail participation suggests momentum-driven buying that reverses quickly on disappointment. The promoter stake reduction, while modest, removes support. If sentiment turns, the stock could face cascading sells with limited buying support, creating violent downward moves that destroy wealth rapidly.

Macro risks loom larger at current valuations. Rising interest rates increase project costs and could slow infrastructure investment. Commodity price volatility—steel comprises major cost component—squeezes margins if not passed through. Currency fluctuations matter more as international ambitions grow. Global economic slowdown would impact India's infrastructure spending. The company has limited control over these factors but valuations assume benign conditions persist.

The human capital challenge grows with success. Skilled welders, experienced project managers, and qualified engineers remain scarce in India. As the company grows, attracting and retaining talent becomes harder and more expensive. Salary inflation in specialized skills could pressure margins. Key person dependencies—certain technical experts or client relationships concentrated in few individuals—create vulnerability.

The bear case synthesizes to this: Lloyds Engineering is an excellent company in a cyclical industry trading at valuations that assume perpetual excellence. The transformation has been remarkable, capabilities are real, and opportunities exist. But at 96.9 times earnings, perfection is priced in. Any stumble—execution mishap, order slowdown, margin compression, or broader market correction—could trigger violent revaluation. The stock could halve and still trade at premium multiples to peers.

XI. Bull Case & Future Potential

Now let's construct the bull case—not with blind optimism but with the same analytical rigor, examining why current valuations might prove conservative if India's infrastructure supercycle thesis plays out and Lloyds executes its strategic vision. The opportunity isn't just large; it's generational.

India's infrastructure investment trajectory presents unprecedented opportunity. The government targets $1.4 trillion infrastructure investment by 2025, with continued acceleration thereafter. This isn't political rhetoric—budget allocations, project sanctions, and ground-breaking ceremonies confirm genuine commitment. Roads, railways, ports, airports, urban infrastructure, energy systems—all require heavy engineering equipment. Lloyds positions perfectly to capture this spending surge.

The energy transition creates new markets while strengthening traditional ones. India's net-zero commitments require massive investments in both renewable energy and transitional fuels. LNG terminals for gas imports, hydrogen production facilities for green energy, carbon capture systems for existing plants—each represents new equipment categories where early movers gain advantaged positions. Lloyds' technical capabilities allow participation across the energy transition spectrum.

Make in India and Atmanirbhar Bharat aren't just slogans but fundamental policy shifts. Import substitution in critical equipment accelerates, driven by supply chain concerns and strategic autonomy desires. International suppliers face increasing pressure to localize, creating opportunities for capable domestic manufacturers. Lloyds' certifications and track record position it as a natural beneficiary of indigenization requirements.

The nuclear power expansion deserves special attention. India plans to triple nuclear capacity by 2032, requiring enormous equipment investments. Nuclear component manufacturing remains a highly restricted market—few qualified suppliers, stringent requirements, and premium pricing. Lloyds' nuclear certifications provide access to this protected market segment where competition is limited and margins remain elevated.

Railway modernization represents a multi-decade opportunity. The dedicated freight corridors, high-speed rail projects, metro expansions, and station modernizations require specialized equipment and systems. Through Techno Industries, Lloyds gained positioning in this massive market. The Mumbai local train system alone—carrying 7.5 million passengers daily—needs continuous upgrades and maintenance, providing steady revenue streams.

International expansion potential remains largely untapped. Middle Eastern countries investing in refining capacity, African nations building infrastructure, and Southeast Asian economies expanding manufacturing all need heavy engineering equipment. Indian engineering companies have established credibility in these markets. Lloyds' certifications and cost competitiveness position it to capture export opportunities as international operations mature.

The M&A-driven growth strategy could accelerate value creation. The Indian engineering sector remains fragmented with numerous subscale players possessing specific capabilities or client relationships. Lloyds' strong balance sheet and management expertise allow consolidation plays—acquiring distressed assets cheaply, improving operations, and extracting synergies. Each successful acquisition strengthens market position while eliminating competition.

Operational leverage remains under-appreciated. As revenues scale from ₹800 crores to potentially ₹2,000-3,000 crores over five years, fixed costs spread over larger base, driving margin expansion. The invested capital in certifications, systems, and capabilities can support much larger revenues without proportional investment increases. This leverage could drive EBITDA margins from current 16% to 20%+, transforming profitability.

The technology adoption opportunity flips disruption concerns. While additive manufacturing and automation pose threats, they also create opportunities for forward-thinking manufacturers. Lloyds could adopt these technologies to improve efficiency, reduce costs, and offer innovative solutions. Being early adopters rather than disruption victims could strengthen competitive position.

Financial flexibility enables strategic options. The nearly debt-free balance sheet allows aggressive bidding for large projects, acquisition financing without dilution, and investment in new capabilities without financial stress. This flexibility proves invaluable during downturns when leveraged competitors retreat and opportunities emerge for strong players to gain market share.

The management quality factor deserves weight. The team that navigated complex demerger, reduced debt, improved operations, and drove margin expansion has proven execution capability. Their conservative approach—maintaining focus, avoiding over-leverage, and building capabilities systematically—suggests sustainable value creation rather than short-term optimization.

Valuation re-rating potential exists despite current multiples. If Lloyds successfully transforms from heavy engineering company to diversified infrastructure play with recurring revenues, multiple expansion could follow. Precedents exist—companies that successfully transformed business models saw valuations re-rate dramatically. The current premium might prove justified if transformation succeeds.

The compound effect of multiple growth drivers could surprise. If infrastructure spending accelerates, energy transition creates new markets, railway modernization expands, international revenues materialize, and acquisitions succeed, revenue could compound at 25-30% annually. Combined with margin expansion from operational leverage, earnings could triple or quadruple over five years, justifying current valuations retrospectively.

The institutional discovery thesis remains valid. As market capitalization grows and liquidity improves, institutional participation will increase. Index inclusions bring passive flows. Sell-side coverage expands awareness. This institutional adoption could provide sustained buying support, reducing volatility while supporting valuations.

The bull case ultimately rests on India's structural growth story. If India sustains 7-8% GDP growth, infrastructure investment continues, manufacturing gains global share, and energy transition accelerates, companies like Lloyds positioned at the intersection of these themes could deliver exceptional returns. Current valuations, while optically expensive, might prove cheap if this scenario materializes.

XII. Playbook: Lessons for Investors & Entrepreneurs

After thousands of words analyzing Lloyds Engineering's journey, let's distill the actionable insights—the reproducible patterns and strategic lessons that transcend this specific company. These aren't theoretical frameworks but practical playbooks derived from actual execution.

Building Technical Moats in Commoditized Industries

The first lesson challenges conventional wisdom about commodity businesses. Heavy fabrication seems like the ultimate commodity—cutting and welding steel to specifications. Yet Lloyds built substantial moats through certifications and capabilities that competitors couldn't easily replicate. The playbook: identify the hidden complexities in seemingly simple businesses. In Lloyds' case, nuclear certifications, ASME stamps, and specialized welding procedures created barriers that pricing alone couldn't overcome.

For investors, this means looking beyond industry classifications. A company labeled as "commodity manufacturer" might possess technical advantages that create pricing power. The key indicators: customer concentration (specialized suppliers have fewer, stickier clients), margin trends (technical moats allow margin expansion even in competitive industries), and certification requirements (regulatory barriers that time and money alone can't overcome).

The Value of Certifications and Approvals in B2B Markets

Certifications aren't just wall decorations—they're licenses to compete in premium markets. Lloyds' systematic investment in ASME certifications, nuclear qualifications, and quality standards opened entirely new revenue streams. The lesson: in B2B markets, certifications create step-function opportunity expansions rather than incremental improvements.

Entrepreneurs should view certifications as growth investments, not compliance costs. The upfront expense and effort pay back through access to protected markets, pricing premiums, and competitive advantages. Investors should track certification achievements as leading indicators of future growth—a company obtaining nuclear qualifications today will show revenue impact two years hence.

Patience in Turnarounds and Transformation Stories

The stock languished for four years post-listing before explosive growth. The operational improvements were happening—debt reducing, margins expanding, capabilities building—but markets didn't notice immediately. This lag between fundamental improvement and market recognition creates opportunity for patient investors.

The playbook for transformation investing: identify companies where operational metrics improve but stock prices haven't responded. Look for decreasing debt, expanding margins, growing order books, and capability investments. Be prepared for extended periods of market indifference—the eventual re-rating often happens suddenly and dramatically.

Importance of Debt Reduction in Cyclical Businesses

Lloyds' journey from leveraged entity to nearly debt-free demonstrates why balance sheet strength matters enormously in cyclical industries. Debt amplifies cyclical downturns—interest costs continue while revenues collapse. Debt-free companies can be opportunistic during downturns, winning projects at better terms while leveraged competitors struggle.

For investors, debt levels in cyclical businesses should be weighted heavily. A cyclical company reducing debt during good times demonstrates management discipline and strategic thinking. For entrepreneurs, the lesson is clear: resist leveraging up during boom times, no matter how attractive growth opportunities appear.

Strategic Value of Demergers and Focus

The demerger from Uttam Value Steels unlocked enormous value by allowing focused strategy and transparent financials. Conglomerate structures often hide valuable businesses within underperforming portfolios. The demerger allowed management to make decisions optimized for engineering rather than balancing competing priorities.

Investors should actively seek demerger situations where valuable divisions separate from troubled parents. These situations often create immediate value through re-rating and long-term value through improved execution. Entrepreneurs should recognize that focus often trumps diversification—better to dominate a niche than struggle across multiple sectors.

Building Trust in Mission-Critical Industries

In heavy engineering, where equipment failure can be catastrophic, trust accumulates slowly but pays dividends for decades. Lloyds' client relationships with companies like Technip and Thyssenkrupp, built over years of successful execution, create switching costs that transcend pricing.

The entrepreneur's playbook: in mission-critical industries, optimize for reliability over growth. Every successful project becomes a reference, every failure destroys reputation disproportionately. Investors should value long-term client relationships and track record of execution as much as financial metrics.

Capital Allocation in Growth Phases

Lloyds' balanced approach—paying dividends while investing for growth, acquiring strategically without over-reaching, maintaining financial flexibility—demonstrates sophisticated capital allocation. The temptation during success is to over-invest, over-acquire, or over-distribute. Lloyds avoided all three traps.

For managers, the framework is clear: maintain capital allocation discipline especially when cash is plentiful. For investors, watch how companies deploy success—disciplined capital allocation during good times predicts resilience during bad times.

The Compound Effect of Incremental Improvements

No single action transformed Lloyds. Instead, dozens of incremental improvements—better working capital management, selective bidding, operational efficiency, strategic acquisitions—compounded into dramatic transformation. This isn't as exciting as revolutionary pivots but proves more sustainable.

The lesson for operators: focus on continuous improvement across multiple dimensions rather than seeking silver bullets. For investors: companies showing consistent improvement across multiple metrics often deliver better returns than those promising revolutionary change.

XIII. Final Analysis & Key Takeaways

Standing back from the detailed analysis, what do we really have with Lloyds Engineering Works? Is this a structural growth story riding India's infrastructure supercycle, or a cyclical upturn masquerading as secular growth? The answer, unsatisfyingly but honestly, is both—and that's precisely what makes this story so fascinating.

The structural growth case rests on solid foundations. India's infrastructure needs aren't political promises but economic necessities. A $3.5 trillion economy aspiring to $10 trillion cannot function with current infrastructure. The ports operating at 95% capacity, railways stretched beyond limits, refineries requiring expansion, power systems needing augmentation—all create sustained demand for heavy engineering equipment. Lloyds, with its certifications, capabilities, and track record, positions ideally to capture this demand.

Yet the cyclical nature remains inescapable. Order books can evaporate, projects can stall, and margins can compress when cycles turn. The current valuation at 96.9 times earnings prices in perfect execution for years—a dangerous assumption in cyclical industries. The stock could correct 50% and still trade at premium multiples, suggesting risk-reward has shifted unfavorably for new investors.

The transformation story commands respect regardless of valuation debates. From debt-laden division to profitable independent entity, from commodity fabricator to specialized engineering partner, from domestic supplier to aspiring international player—management has executed remarkably. The 109% profit CAGR wasn't financial engineering but operational excellence.

Key metrics to watch going forward: order book quality over quantity (margins matter more than volumes), working capital trends (deterioration signals competitive pressure), margin sustainability (can 16%+ EBITDA margins persist?), and acquisition integration (do new businesses strengthen or dilute the core?). These indicators will determine whether current optimism proves prescient or excessive.

The investment thesis ultimately depends on time horizon and risk tolerance. For traders, the volatility creates opportunities but requires discipline and risk management. For long-term investors, the question becomes whether India's infrastructure story justifies current valuations. The company's quality isn't debatable—it's whether quality is already fully priced.

The broader lessons transcend this specific investment. Lloyds demonstrates how technical capabilities create moats in seemingly commoditized industries, how patient execution trumps aggressive expansion, and how focusing on core competencies while selectively diversifying can create substantial value. Whether bought or not, studied and understood, Lloyds Engineering offers valuable insights into B2B value creation in emerging markets.

The final verdict: Lloyds Engineering Works represents a high-quality company in a structural growth sector trading at valuations that embed aggressive assumptions. The business model is robust, execution has been excellent, and opportunities remain substantial. But at current prices, the margin of safety has eroded. Investors must decide whether riding India's infrastructure wave justifies accepting valuation risk.

For those holding shares from lower levels, the calculus differs—riding winners often proves wise despite valuation concerns. For new investors, patience might be prudent—great companies at great prices create great investments; great companies at any price often disappoint. Lloyds Engineering is undoubtedly the former; whether it's become the latter remains the crucial question.

The story continues to unfold. Will management maintain execution excellence while scaling operations? Can margins sustain as competition intensifies? Will India's infrastructure spending match ambitious projections? These questions will determine whether today's buyers are early to a multi-decade growth story or late to a spectacular run. Time, as always, will tell.

What's certain is that Lloyds Engineering Works has already delivered one of Indian capital markets' great transformation stories. From that humid Mumbai workshop in 1974 to today's near-₹10,000 crore market capitalization, from simple fabrication to nuclear-certified manufacturing, from debt-stressed division to profitable independent entity—this journey deserves recognition regardless of future stock price movements.

The company stands as testament to Indian manufacturing's potential, the value of technical excellence, and the power of patient execution. Whether it proves a great investment from current levels remains uncertain. That it represents a great business story is undeniable.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube