LIC Housing Finance: The Story of India's Housing Finance Giant

I. Introduction & Episode Roadmap

The Mumbai skyline tells two stories. Glass towers pierce the monsoon clouds while below, millions navigate narrow lanes searching for that most fundamental human need—a home. In 1989, as India stood at the cusp of economic liberalization, a new player entered this vast housing market with an audacious promise: to democratize home ownership through the backing of the nation's insurance behemoth.

LIC Housing Finance Limited emerged not from Silicon Valley disruption or Wall Street financial engineering, but from the corridors of India's largest financial institution—Life Insurance Corporation of India. Today, with a loan portfolio exceeding ₹2,87,000 crore and serving millions of Indian families, LICHSGFIN stands as the country's largest housing finance company. Yet its journey from government subsidiary to market leader reveals deeper truths about India's financial evolution, the perils of sector-wide crises, and the delicate balance between public purpose and private profit.

How did a subsidiary of India's insurance giant navigate economic liberalization, survive the IL&FS liquidity crisis that decimated NBFCs, and emerge as the housing finance leader in the world's most populous nation? The answer lies not just in government backing—many state-owned enterprises have faltered—but in a series of strategic pivots, crisis management decisions, and an unlikely digital transformation that would make even fintech startups take notice.

This is the story of LIC Housing Finance: a tale of bureaucratic vision meeting market reality, of surviving when peers collapsed, and of serving both shareholders and society in one of the world's most complex housing markets. As we'll discover, the company's evolution mirrors India's own economic journey—from socialist ideals to market capitalism, from paper forms to digital apps, from serving the elite to financing the dreams of middle India.

II. Origins & Parent Company Context - The Birth of LIC India

Picture September 1956. In the newly independent India's Parliament, lawmakers debated a radical proposition: nationalize the entire life insurance industry. The architect of this transformation wasn't a Wall Street banker or a business tycoon, but Finance Minister C.D. Deshmukh, who saw insurance not as a commercial enterprise but as a sacred trust. When the Life Insurance of India Act passed that year, 245 insurance companies and provident societies—some British, some Indian, many struggling—were merged into a single entity: Life Insurance Corporation of India.

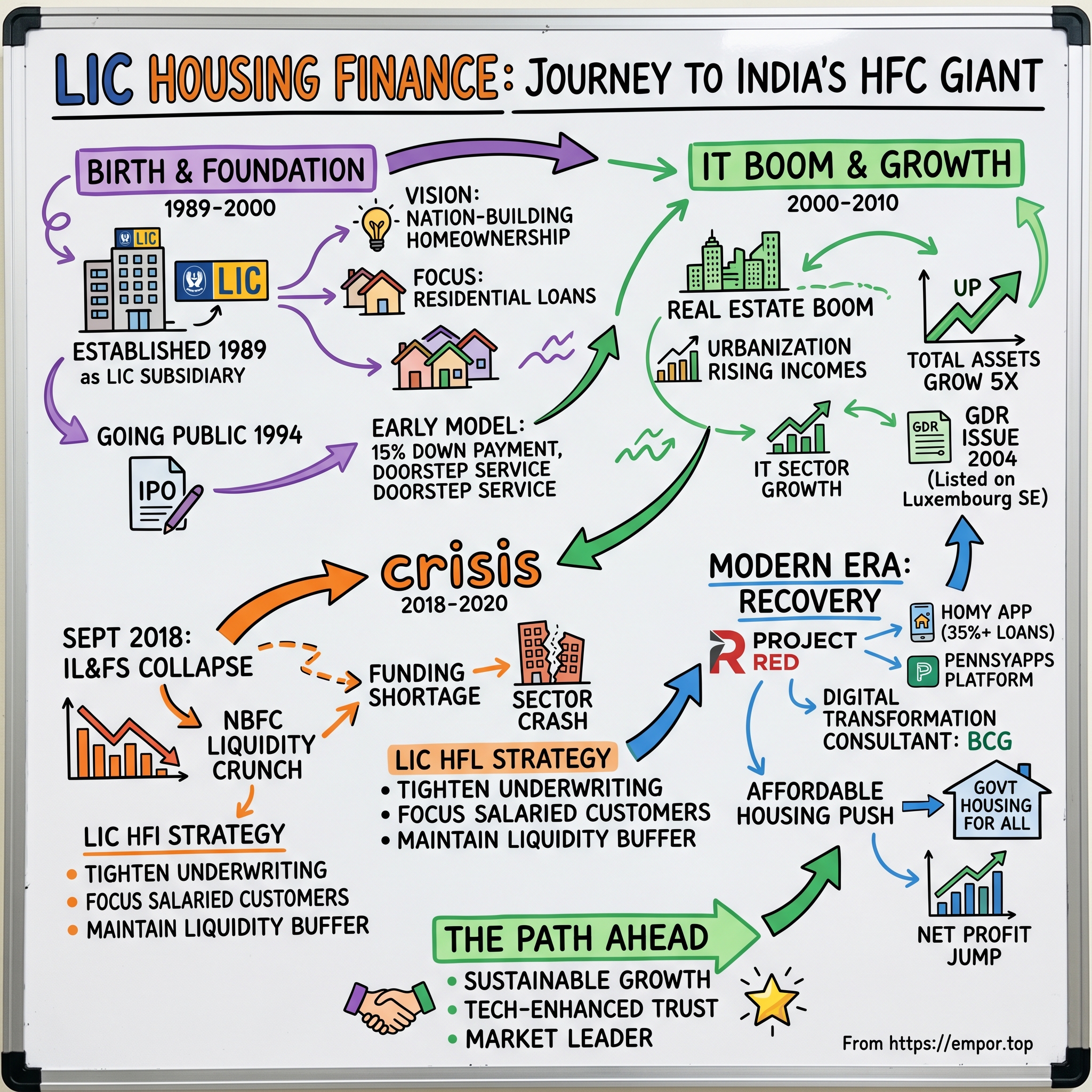

Three decades later, on June 19, 1989, this insurance colossus would birth its most ambitious subsidiary: LIC Housing Finance Limited, established as a wholly-owned subsidiary of LIC. The timing was no accident. India stood at the precipice of economic transformation—the socialist economy was creaking, foreign exchange reserves were dwindling, and within two years, the nation would embrace liberalization. But in 1989, the government still believed in strategic interventions, and housing was deemed too important to leave entirely to market forces.

LIC itself had grown into something extraordinary by then. From those 245 merged entities, it had become India's financial bedrock—the place where millions of Indians parked their savings, bought their first insurance policies, and trusted their financial futures. By the time it created LIC Housing Finance, the parent company was already managing assets that dwarfed most financial institutions in Asia. Today, LIC manages assets worth ₹54.52 lakh crore (US$640 billion), making it not just India's largest insurance company but its largest institutional investor.

The strategic rationale for LIC's entry into housing finance revealed the government's sophisticated understanding of financial ecosystems. Insurance companies generate massive float—premiums collected today for claims paid years later. This patient capital, perfectly matched to long-term mortgages, could solve India's housing crisis while generating stable returns for policyholders. The company was formed to cater to the housing finance needs of individuals and developers in India, filling a gap that banks were reluctant to address.

Consider the landscape LIC Housing Finance entered: In 1989, getting a home loan in India was like extracting water from stone. Banks viewed mortgages as risky, paperwork-intensive, and unprofitable. Interest rates hovered around 18%. Documentation requirements were Byzantine. The middle class—teachers, clerks, small business owners—had virtually no access to formal housing finance. They relied on informal lenders, sold ancestral jewelry, or simply accepted that homeownership was a multi-generational project.

LIC Housing Finance would change this equation fundamentally. With the backing of its parent's reputation ("LIC" carried almost governmental trust), deep pockets, and a mandate to serve rather than merely profit, it could take risks others wouldn't. Incorporated on 19th June, 1989 under the Companies Act, 1956, the Company was promoted by LIC of India with a vision that went beyond commercial success—it was about nation-building through homeownership.

The company's DNA carried both the strengths and contradictions of its parentage. From LIC, it inherited patient capital, governmental trust, and access to a vast agency network. But it also inherited bureaucratic decision-making, political interference, and the burden of serving social objectives alongside commercial ones. This duality—part public servant, part profit-seeking enterprise—would define its journey through India's economic transformation.

III. Early Years & Foundation (1989–2000)

The first LIC Housing Finance office opened in Mumbai's Bandra-Kurla Complex with just 47 employees, most poached from LIC's own ranks. The CEO's corner office overlooked construction sites that would, years later, become India's financial district. But in 1989, it was mostly marshland and optimism. The company's first advertisement, published in The Times of India, didn't promise lowest rates or fastest approvals. It simply said: "Your own home is now possible."

In its early years, LIC HFL primarily focused on providing loans for the purchase of residential properties. By 1995, it had expanded its offerings to include loans for construction, home improvement, and land purchase. This expansion wasn't driven by market research or McKinsey consultants—it came from loan officers hearing the same request repeatedly: "Can you also finance the construction?" "What about buying the plot first?" "My house needs repairs, can you help?"

The company's early business model was deceptively simple yet revolutionary for its time. While banks demanded 40% down payments and charged floating rates that could spike unpredictably, LIC Housing Finance introduced products that seemed radical: 15% down payments, fixed rates for initial years, and most importantly, doorstep service through agents who spoke local languages and understood local customs.

Consider the story of R.K. Sharma, one of the company's first thousand customers in 1990. A government schoolteacher in Pune, he had saved for fifteen years to buy a small flat. Banks had rejected his application three times—his salary was deemed too low, his employment "unstable" (despite being a permanent government employee). LIC Housing Finance approved his loan in three weeks. The loan officer, himself a former teacher, understood that government salaries, while modest, were rock-solid. This wasn't just underwriting; it was understanding India.

The Company possesses one of the industry's most extensive marketing network in India: Registered and Corporate Office at Mumbai, 9 Regional Offices, 16 Back Offices and 282 marketing units across India. But these numbers, achieved after years of expansion, don't capture the ground-level innovation. In Tamil Nadu, agents set up desks at temple festivals. In Punjab, they partnered with grain merchants who knew every farmer's creditworthiness. In Kerala, they worked through Gulf emigrant associations, understanding that remittance income was more stable than local salaries.

The target market wasn't the wealthy—they had options. It was the vast Indian middle class: the railway employee dreaming of moving from quarters to his own flat, the small shopkeeper wanting to build a second floor, the retired soldier returning to his village with his pension and plans. These weren't subprime borrowers; they were un-served prime borrowers, and LIC Housing Finance was the first to recognize the distinction.

By 1994, just five years after inception, the company made a bold move: went public in the year 1994. The IPO was oversubscribed 7.5 times, with applications from over 400,000 retail investors. The offering price of ₹10 per share seems quaint now, but it represented something larger—public participation in India's housing finance revolution. LIC reduced its stake but remained the dominant shareholder, a structure that would provide both stability and flexibility.

The competitive landscape of the 1990s was sparse but evolving. HDFC, established in 1977, was the pioneer and market leader, focusing on urban markets and salaried employees. A few smaller players like Dewan Housing and PNB Housing operated regionally. Banks largely avoided the sector, viewing it as operationally intensive and risky. This created a sweet spot for LIC Housing Finance—less premium than HDFC, more trustworthy than smaller players, and backed by the LIC brand that resonated in tier-2 and tier-3 cities.

The company's expansion strategy during this period reflected deep market understanding. Instead of competing head-on with HDFC in Mumbai and Delhi's premium markets, it focused on emerging cities: Nashik, Coimbatore, Vishakhapatnam, Lucknow. These cities were experiencing rapid growth but had virtually no organized housing finance. A branch manager in Indore later recalled: "HDFC would finance the doctor's clinic. We would finance the doctor's home, the nurse's flat, and the ward boy's plot purchase."

Technology adoption was minimal—this was pre-internet India—but process innovation was constant. The company introduced the concept of "pre-approved" loans, where customers could know their eligibility before selecting a property. It pioneered the "construction-linked disbursement" for under-construction properties, protecting both borrower and lender. These seem obvious now; in 1995, they were revolutionary.

By 2000, LIC Housing Finance had disbursed over ₹10,000 crore in cumulative loans and built a network spanning 100 cities. The company's total assets rose from approximately ₹10,000 crore in 2000, setting the stage for explosive growth. More importantly, it had proven that housing finance could be both profitable and socially impactful—a duality that would define its next phase of evolution.

IV. The Growth Years (2000-2010): India's Real Estate Boom

The millennium dawn broke over India with Y2K fears dissipating and IT fortunes rising. In boardrooms across Bangalore, Hyderabad, and Gurgaon, young engineers counted stock options while real estate developers sensed opportunity. The early 2000s marked a significant real estate boom in India. Rapid urbanization, an emerging middle class, and easier access to financing led to soaring property prices. For LIC Housing Finance, this wasn't just another business cycle—it was transformation on steroids.

Between 2000 and 2010, the company's metamorphosis was staggering. Between 2000 and 2010, LIC HFL witnessed significant growth in its operations. The company's total assets rose from approximately ₹10,000 crore in 2000 to around ₹50,000 crore by 2010. This expansion was fueled by increasing demand for housing finance in India, driven by urbanization and rising incomes. These weren't just numbers on a balance sheet—they represented millions of Indians moving from rented quarters to owned homes, from joint families to nuclear households, from saving for decades to borrowing for today.

Since India had a large English speaking, technologically advanced working population, a huge chunk of the Information Technology (IT) and Information Technology Enabled Services (ITeS) found its way into the Indian markets. The average unemployed Indian youth suddenly had a swanky job with a decent paying salary. However, more importantly, American jobs also brought American culture to the real estate markets. More and more of the newly wealthy Indians abandoned conservative values and borrowed to buy their homes. Mortgages, which were the exception at one time suddenly, became the norm. This created a bubble of unseen proportions in the Indian market. Firstly, millions of buyers which were not there in the market suddenly had the purchasing power.

The company's strategic positioning during this period was masterful. While competitors chased the cream—software engineers in Electronic City, investment bankers in BKC—LIC Housing Finance played a different game. They financed the accountant who audited the software company, the teacher who educated the banker's children, the shopkeeper who fed them all. This wasn't just market segmentation; it was understanding that India's growth story had multiple protagonists.

In 2004, the company took another leap into global markets: The company launched its maiden GDR issue in 2004, with The GDR's listed on the Luxembourg Stock Exchange. This wasn't merely capital raising—it was a statement that an Indian housing finance company could attract European institutional money. The proceeds weren't just used for lending; they funded technology upgrades, branch expansion, and crucially, talent acquisition from private banks.

Product innovation accelerated dramatically. The company introduced flexi-fixed schemes offering fixed rates for the first five years and variable thereafter—a product that balanced borrower certainty with lender flexibility. They launched "Griha Laxmi" loans against financial securities, allowing customers to unlock value from their fixed deposits and insurance policies. For senior citizens, they created "Griha Jestha," recognizing that retirees with lump-sum retirement benefits were an underserved segment.

The distribution strategy evolved from mere expansion to intelligent penetration. By 2010, the company had established one of the industry's most extensive marketing networks in India with regional offices, back offices and marketing units across India. But the real innovation was the army of over 12,000 intermediaries—not just agents, but trusted local advisors who understood community dynamics, family structures, and informal credit histories that no algorithm could capture.

Consider the Pune market in 2007. While banks focused on IT parks in Hinjewadi, LIC Housing Finance quietly dominated the financing of row houses in Kothrud, apartments in Nigdi, and plots in Wakad. They understood that for every software professional buying a 3BHK, there were ten middle-class families upgrading from 1BHK to 2BHK, from rental to ownership, from aspiration to achievement.

The competitive landscape during this boom period intensified but remained fragmented. HDFC maintained its premium positioning, ICICI Bank entered aggressively with teaser rates, and State Bank of India finally woke up to the mortgage opportunity. Yet LIC Housing Finance carved its niche—more flexible than SBI, more trustworthy than aggressive private players, more accessible than HDFC. They occupied the sweet spot of Indian financial services: government trust with private sector efficiency.

The mid-2000s marked the rise of the Indian IT and ITES sectors, driving demand for commercial spaces in cities like Bangalore, Hyderabad, Pune, and Chennai. This period also saw the emergence of integrated townships and luxury housing projects catering to an expanding middle class and NRIs. Real estate investment gained momentum as financial institutions introduced home loans with more accessible terms. However, the 2008 global financial crisis temporarily slowed growth, highlighting the need for better regulation and risk management.

The 2008 global financial crisis tested the company's risk management. While American mortgage lenders collapsed and Indian real estate developers defaulted, LIC Housing Finance weathered the storm relatively unscathed. Their conservative underwriting—much mocked during the boom as leaving money on the table—suddenly looked prescient. They had avoided the temptation of 95% loan-to-value ratios, teaser rates, and subprime segments that decimated others.

Post-crisis, as competitors retreated, LIC Housing Finance advanced. They gained market share not through aggressive lending but through consistent presence. When ICICI Bank pulled back from developer finance, when foreign banks exited mortgage markets, when real estate prices corrected 20-30%, LIC Housing Finance kept lending—more cautiously, but consistently. This counter-cyclical approach would define their strategy for the decade ahead.

By 2010, the company had transformed from a government subsidiary fulfilling a social mandate into a formidable financial institution. The numbers told only part of the story—the real transformation was cultural. They had learned to balance growth with prudence, social objectives with commercial returns, traditional values with modern processes. As India entered a new decade, LIC Housing Finance stood ready for its next evolution, unaware that the biggest crisis in NBFC history lurked just eight years away.

Business Model Evolution & Digital Transformation

October 2020. The pandemic had shuttered offices, frozen real estate markets, and forced even the most traditional institutions online. In LIC Housing Finance's Mumbai headquarters, CEO Siddhartha Mohanty unveiled something that would have seemed impossible just years earlier: Project RED (Re-imagining Excellence through Digital Transformation). For a company whose loan officers once carried physical ledgers to villages, this wasn't evolution—it was revolution.

The housing finance company appointed Boston Consulting Group (BCG) as its consultant for the project, a move that raised eyebrows. Government-backed financial institutions rarely hired top-tier consultants for transformation projects. But Mohanty understood something fundamental: competing with fintech-powered banks and digital-native NBFCs required more than incremental change. It demanded reimagination.

The numbers tell a stunning transformation story. Currently, 35-40 per cent of the loan applications of the company are being processed digitally and the percentage will improve to 90-95 per cent post completion of this project, Mohanty announced in 2020. By FY23, the results exceeded even these ambitious targets. Using its "HOMY App," more than 35% of all loan disbursements have occurred since FY23, up from only 3% in FY21. The app wasn't just a digital channel—it became the company's growth engine.

But let's rewind to understand the pre-digital LIC Housing Finance. The company offers public and corporate deposits; home loans to residents and non-residents, as well as to pensioners; plot loans, home improvement and construction loans, home extension, and top up loans; refinance; construction finance and term loans for builders and developers; and loans for staff quarters and other lines of credit for corporates. It also provides loans against properties for companies and individuals; loans against securities; loans under rental securitization; and loans to professionals. This vast product portfolio, built over three decades, operated through paper forms, manual underwriting, and relationship-based decisions.

The traditional distribution model was both the company's strength and weakness. The Company possesses one of the industry's most extensive marketing network in India: Registered and Corporate Office at Mumbai, 9 Regional Offices, 16 Back Offices and 282 marketing units across India. In addition the company has appointed over 12000 Intermediaries to extend its marketing reach. This network gave unparalleled reach but created operational nightmares—loan files traveled physically between offices, approvals took weeks, and customer data lived in silos.

Launched on February 14, 2020, the LIC HFL Home Loans (HomY) App was envisioned under the digital transformation plan of on-boarding customers and sanctions through mobile. Within a year, the results were remarkable: It said the app has facilitated 14,155 customer home loan applications since its launch on February 14, 2020. More than 7,300 of these customers have had their home loans sanctioned. Of these, loans were disbursed to 6,884 customers amounting to Rs 1,331 crore so far.

The technology transformation went beyond customer-facing apps. In February 2023, LIC Housing Finance deployed Pennant Technologies' state-of-the-art lending platform – pennApps Lending Factory – to modernise and transform its mortgage operations with a focus on improving operational efficiencies and delivering enhanced customer experience. This wasn't just digitizing existing processes—it was reimagining the entire lending lifecycle.

In 2017, before the digital push, the company made another strategic pivot. In 2017, LIC HFL made a strategic shift by entering the affordable housing finance segment. It introduced various products aimed at low and middle-income customers, which helped it strengthen its market position. The company's focus on affordable housing aligned with the Indian government's "Housing for All" initiative launched in 2015. This wasn't corporate social responsibility masquerading as strategy—it was recognizing that India's next billion consumers wouldn't come from premium segments.

The affordable housing push revealed the company's evolving understanding of risk and opportunity. Traditional lenders viewed low-ticket loans as unprofitable—high operational costs, thin margins, perceived credit risk. LIC Housing Finance flipped this logic. They understood that a ₹10 lakh loan to a government employee in Tier-3 city carried lower risk than a ₹1 crore loan to a businessman in Mumbai. Technology made this insight actionable—digital processes slashed operational costs, making small-ticket loans viable.

Consider the transformation in customer experience. Pre-2020, applying for a home loan meant multiple branch visits, stacks of photocopies, weeks of waiting. Post-Project RED, customers could apply via app, upload documents digitally, receive instant eligibility, and track applications real-time. The same company that once required guarantors' physical signatures now offered video KYC. The contrast was jarring, deliberate, and necessary.

The distribution strategy also evolved radically. Going ahead, the housing financier will expand to newer geographies but that will be more through the digital mode than having a physical office. This wasn't abandoning physical presence but augmenting it intelligently. High-touch remained for complex cases and relationship building; high-tech handled routine transactions and scale.

The digital transformation also addressed a critical vulnerability: data. For decades, customer information lived in branch files, Excel sheets, and relationship managers' memories. Project RED centralized this treasure trove, enabling analytics, risk modeling, and personalized offerings. A company that once knew customers through local agents now understood them through algorithms—without losing the human touch that defined its culture.

But transformation created tensions. Veteran employees who built careers on relationship banking suddenly needed to master apps and analytics. The 12,000 intermediaries who generated business through personal networks feared digital channels would make them redundant. Management's challenge wasn't just implementing technology but managing change—preserving institutional knowledge while embracing digital natives' energy.

The results validated the strategy. By 2023, digital channels contributed not just to efficiency but to growth. Turnaround times dropped from weeks to days. Customer acquisition costs plummeted. Most importantly, the company could now serve segments previously deemed unviable—young professionals wanting instant approvals, NRIs seeking remote processing, small-town entrepreneurs needing quick disbursements.

Yet the business model's core remained unchanged: patient capital funding long-term mortgages for India's aspiring middle class. Technology amplified this mission rather than replacing it. The company still valued relationships over transactions, prudence over aggression, inclusion over exclusivity. Digital transformation didn't change who they were—it enhanced what they could do.

As competitors struggled with fintech disruption and regulatory pressures, LIC Housing Finance's digital evolution positioned it uniquely. Unlike digital-only players, it had trust and distribution. Unlike traditional players, it now had technology and agility. This hybrid model—government backing with private sector efficiency, traditional values with modern execution—would prove invaluable when the next crisis struck.

VI. The IL&FS Crisis & NBFC Liquidity Crunch (2018-2020)

September 21, 2018. The Bombay Stock Exchange opened to carnage. Within minutes of trading, Dewan Housing Finance Limited (DHFL) crashed 60%. Indiabulls Housing plummeted 20%. Even blue-chip names weren't spared—HDFC dropped 8%, Bajaj Finance fell 13%. The trigger? A series of announcements revealing that IL&FS, the infrastructure financing giant with ₹91,000 crore in debt, had defaulted on multiple obligations. India's shadow banking sector wasn't just facing a crisis—it was staring into the abyss.

It all began in September 2018, when financing behemoth Infrastructure Leasing & Financial Services (IL&FS) collapsed. Here's a timeline of what went wrong for India's NBFCs: June 2018: IL&FS defaults for the first time on repayment of commercial paper (short-term borrowing) and inter-corporate deposit (unsecured borrowing) worth Rs450 crore ($60 million). This alarms credit rating agencies, which start downgrading the company and its subsidiaries. CNBC-TV18 reports that the IL&FS group is saddled with a debt of Rs91,091 crore and is facing losses to the tune of Rs1,887 crore in the financial year 2018.

Mumbai-based DSP Mutual Funds dumps Rs300 crore worth of commercial papers of another NBFC, Dewan Housing Finance Limited (DHFL), at a discounted rate in September, sparking speculation that the company is staring at a rating downgrade. The contagion spread with frightening speed. DHFL which is considered to a blue chip NBFC stock suddenly saw its stock price decline by 60% in one day!

For LIC Housing Finance, this wasn't just another market correction—it was an existential moment. The company is the largest housing finance company in India with a total loan portfolio of Rs. ~2,87,000 Cr in FY24 vs Rs. ~2,10,000 Cr in FY20. But size offered no immunity. The crisis questioned the viability of the entire NBFC model: borrowing short-term from mutual funds and banks to lend long-term for housing and infrastructure.

Upon further discussion, it was identified that the fund house had IL&FS debt and IL&FS was roiled by a lot of defaults in commercial papers, which led to a shortage of INR 1000 billion in the system. Exposure to IL&FS formed the base of all the rumours and it spoiled DHFL's valuation, and the same thing happened for other NBFCs as well.

The market's reaction was brutal but logical. The aggregate borrowings of IL&FS Group accounts for almost 2% of outstanding Commercial Papers in the money market, around 1% of Non-Convertible Debentures (NCDs) and roughly 0.7% of the entire banking system loans. Hence, any significant financial distress to IL&FS Group naturally poses a major systemic risk to the overall banking and financial system in India.

These developments make investors nervous and the market cap of NBFCs is decimated. Between Sept. 21 and 24, large NBFCs like Housing Development and Finance Corporation (HDFC) and Bajaj Finance's market cap erodes by around Rs18,600 crore and Rs13,800 crore, respectively. Yet in this maelstrom, something interesting happened: Investors flock to strong private NBFCs such as HDFC and quasi-sovereign financing companies like Rural Electrification Corporation, Power Finance Corp, National Bank for Agriculture and Rural Development, National Housing Bank, and LIC Housing Finance.

The "quasi-sovereign" label became LIC Housing Finance's lifeline. While pure-play private NBFCs saw funding dry up overnight, government-backed entities retained access to capital markets. This wasn't just about credit ratings—it was about perception. In a crisis, investors fled to safety, and nothing seemed safer than an entity backed by Life Insurance Corporation of India, itself backed by the government.

A severe funding shortage following the crisis in 2018 led to NBFCs experiencing a liquidity crisis. Following the crisis, NBFCs struggled mainly due to Infrastructure Leasing and Financial Services demise (IL&FS). As a result, investors withdrew substantial sums from significant NBFCs, especially housing lending institutions.

The company's management, led by then-CEO Vinay Sah, faced a delicate balancing act. They needed to maintain lending to preserve market share and customer relationships, but couldn't appear reckless when peers were collapsing. The strategy they adopted was nuanced: tighten underwriting standards, focus on salaried customers with stable income, reduce developer finance exposure, and most importantly, maintain liquidity buffers even at the cost of profitability.

Consider the operational challenges. Pre-crisis, LIC Housing Finance could raise funds through commercial paper at 7-8% and lend at 9-10%, a comfortable 200 basis point spread. Post-crisis, commercial paper markets froze. Bank funding, when available, came at 9-10%. The company's net interest margins compressed dramatically, but survival trumped profitability.

The Reserve Bank of India (RBI) has taken some steps to prevent the conversion of this Non-Banking Financial Companies (NBFCs) crisis into a full-fledged financial crisis. The RBI has changed its rules in order to make it easier for Non-Banking Financial Companies (NBFCs) to obtain capital. Banks were earlier restricted in the number of loans they could make to NBFCs. Banks were earlier allowed to lend a maximum of 10% of their loans to NBFCs. This limit has been temporarily raised to 15% for a few months. The immediate effect of this step has been to release close to $10 billion worth of liquidity to the cash-starved NBFC sector.

Government intervention proved crucial but controversial. On 2 November 2018, RBI announced Partial Credit Enhancement (PEC) to bonds, the period of occupancy of which should not be less than three years. These were issued by systemically important non-deposit takings of NBFCs amid the liquidity crisis. To reduce the stress of NBFCs, RBI relaxed its rules to sell or securitise the loan books. Therefore, NBFCs can securitise loans of more than five-year maturity after holding those for six months.

For LIC Housing Finance, these measures provided breathing room. Unlike peers who desperately sold loan portfolios at discounts, the company could afford patience. Their parent's deep pockets meant they didn't need fire sales. But this advantage came with scrutiny—every loan written off, every quarter of weak results faced questions about whether government backing encouraged complacency.

The human cost was significant. Thousands of homebuyers who'd taken loans from smaller NBFCs faced uncertainty as lenders collapsed or stopped disbursements mid-construction. LIC Housing Finance quietly stepped in for many such "orphaned" customers, taking over loans from failed competitors. This wasn't charity—these were good customers caught in bad circumstances—but it reinforced the company's reputation as a stable, reliable lender when stability itself had become rare.

Now how did liquidity squeeze manifest itself? It manifested itself in the lack of purchase of cars and autos, purchase of real estate and construction by real estate companies. Around 95% of vehicles may have been financed by the NBFCs or by agents. Hence, most of the financing was done by the NBFCs which they stopped. Due to this consumer car loans came down and car purchases also fell subsequently.

The real estate sector, already reeling from demonetization and RERA implementation, faced a triple whammy. Thirdly, the real estate companies were getting money largely from the NBFCs because they were not getting any lending from the banks. With NBFC funding frozen, construction halted, buyers panicked, and prices stagnated. LIC Housing Finance's exposure to developer finance—always a smaller part of their portfolio than retail—suddenly looked prescient rather than conservative.

By early 2020, as the sector showed signs of stabilization, COVID-19 struck. For NBFCs already weakened by the IL&FS crisis, the pandemic threatened to be the final blow. In a recent report, Moody's said the inability of borrowers to repay loans amid the Covid-19 crisis, coupled with a six-month moratorium on repayment allowed by India's central bank, will lead to a disruption of inflow for NBFCs, even as outflow will have to continue. "Most NBFCs do not have substantial on-balance sheet liquidity because they primarily manage liquidity by matching cash inflows from loan repayments by customers with cash outflows to repay their own liabilities," the ratings agency said in a report on May 18.

Yet LIC Housing Finance not only survived but thrived. The moratorium period, while disrupting cash flows, also demonstrated the quality of their underwriting—most customers resumed payments once the moratorium lifted. The company's technology investments, initially planned for efficiency, proved invaluable for remote operations during lockdowns. Most importantly, the crisis validated their conservative approach: slow and steady had won the race while fast and aggressive had crashed and burned.

The IL&FS crisis fundamentally altered India's financial landscape. Mutual funds became wary of NBFC exposure. Banks tightened lending standards. Regulators increased oversight. For LIC Housing Finance, it marked a transition from being seen as a stodgy government company to being valued as a stable, well-managed institution. Sometimes, the best strategy in a crisis isn't to be the smartest or fastest—it's simply to survive when others don't.

VII. Recovery & Modern Era (2020–Present)

January 31, 2025. As LIC Housing Finance announced its Q3 FY25 results, the numbers told a story of remarkable resilience. LIC Housing Finance Ltd's net profit jumped 22.75% since last year same period to ₹1,434.84Cr in the Q3 2024-2025. For a company that had weathered the IL&FS storm, survived a pandemic, and undergone digital transformation, these weren't just numbers—they were validation of a strategy forged in crisis and refined in recovery.

The post-crisis recovery began even before COVID ended. While competitors licked their wounds from the NBFC liquidity crunch, LIC Housing Finance quietly strengthened its foundation. Net Profit After Tax for the year ended March 31, 2025, was Rs 5,429.02 crore, as against Rs 4,765.41 crore, during the same period in the previous year, up by 14%. This wasn't explosive growth—it was deliberate, measured expansion that prioritized sustainability over spectacle.

Speaking on the performance, Tribhuwan Adhikari, Managing Director & Chief Executive Officer of LIC Housing Finance said, "The housing finance sector has been witnessing strong credit growth with tier-2 and tier-3 cities as main drivers. This has provided a momentum to our efforts towards deeper penetration and improving financial inclusion across the country. Our constant focus towards customer service, effective cost management and improvement in asset quality have contributed to stable margins and improved profitability.

The transformation under Adhikari's leadership marked a distinct shift from the company's traditional approach. Where previous management focused on maintaining the status quo, the new leadership embraced calculated risk-taking. The affordable housing segment, once considered too operationally intensive, became a growth driver. Technology, once viewed skeptically, became central to strategy.

Consider the asset quality turnaround. Its stage 3 assets, or loans that are overdue for more than 90 days, declined to 2.75% for the quarter from 4.26% a year earlier. This improvement didn't happen through write-offs or restructuring gymnastics—it came from better underwriting, proactive recovery, and most importantly, choosing the right customers in the first place.

The digital lending expansion, initiated during Project RED, now showed tangible results. The HOMY app, launched in February 2020 just before the pandemic, had evolved from a crisis response tool to a competitive advantage. Customers who once spent weeks visiting branches could now get approvals in days. The company that once epitomized bureaucratic slowness now competed on speed and convenience.

Yet challenges persisted. We are slightly concerned about the margin we are getting on our products; our backbook has been under pressure, impacting our margins to some extent. Incrementally, there is a lot of competition in the market as well as from banks. Markets are slightly compressed. The admission was refreshingly honest—in a market where banks aggressively entered housing finance and fintech players offered instant approvals, maintaining margins while growing required constant recalibration.

The company's response was strategic rather than reactive. We realise the need to move into high-margin segments. Last month, we launched an affordable segment product. This wasn't abandoning their core middle-class customer base but expanding at both ends—affordable housing for volume, premium segments for margins.

The Individual Home Loan portfolio stood at Rs 2,62,411 crore as on June 30, 2025, as against Rs 2,46,275 crore as on June 30, 2024, up by 7%. The Project loan portfolio stood at Rs 8,950 crore as on June 30, 2025, as against Rs 8,099 crore as on June 30, 2024, up by 10%. The total outstanding portfolio grew by 7% to Rs 3,09,587 crore from Rs 2,88,665 crore in the earlier year.

The growth numbers, while modest by some standards, reflected conscious choices. Unlike the pre-crisis era when NBFCs grew at 20-30% annually by taking excessive risks, LIC Housing Finance targeted sustainable 7-10% growth with superior asset quality. The tortoise and hare fable found new relevance in Indian finance.

The competitive landscape had fundamentally altered post-crisis. Banks, flush with liquidity and under pressure to deploy funds, aggressively entered housing finance. Digital-first players like Home First Finance and Aavas Financiers targeted specific niches with technology-enabled models. Traditional HFCs consolidated—HDFC merged with HDFC Bank, creating a behemoth. In this environment, LIC Housing Finance's positioning as the stable, government-backed alternative became both advantage and limitation.

The current year has started off strongly as we reduced the lending rates during this quarter in view of RBI rate cut. Additionally, we also introduced zero processing fee, in order to ease access to housing credit. These moves signaled a more aggressive stance—competing on price when necessary while maintaining underwriting discipline.

The company's geographic expansion strategy evolved significantly. Instead of opening physical branches in every town, they leveraged digital channels for origination while maintaining physical presence for collections and relationship management. This hybrid model—digital where possible, physical where necessary—optimized costs while maintaining the human touch crucial in Indian markets.

Risk management, always conservative, became even more sophisticated. The company implemented artificial intelligence for fraud detection, machine learning for credit scoring, and predictive analytics for early warning signals. Yet these tools supplemented rather than replaced human judgment—the final credit decision still required experienced underwriters' approval.

The transformation extended beyond operations to culture. The organization that once moved at government pace now celebrated quick decisions. Employees who once prioritized compliance over growth now balanced both. The company that once viewed private sector practices suspiciously now actively recruited from banks and fintechs.

The affordable housing focus proved particularly prescient. With government incentives, growing urbanization, and increasing financial inclusion, this segment offered volume growth with acceptable risks. The company's understanding of this market—built over decades of serving lower-middle-class customers—provided competitive advantage that technology-first players couldn't easily replicate.

LIC Housing Finance Ltd's revenue jumped 3.91% since last year same period to ₹7,070.51Cr in the Q3 2024-2025. On a quarterly growth basis, LIC Housing Finance Ltd has generated 1.89% jump in its revenue since last 3-months. The steady revenue growth, while not spectacular, demonstrated the model's resilience.

Looking ahead, the company faced both opportunities and threats. India's housing shortage—estimated at 30 million units—provided decades of growth potential. Rising incomes, government support, and demographic trends favored housing finance. Yet regulatory changes, interest rate volatility, and technological disruption posed constant challenges.

The recovery wasn't just about returning to pre-crisis levels—it was about emerging stronger, more agile, and better positioned for the future. LIC Housing Finance had transformed from a sleepy government subsidiary into a modern financial institution, from a bureaucratic lender into a customer-focused organization, from a crisis survivor into a market leader. The journey from 2020 to present proved that sometimes, the greatest transformations come not from disruption but from evolution—deliberate, sustained, and purposeful.

VIII. Financial Analysis & Market Position

The numbers paint a picture of paradox. Market Cap ₹ 31,565 Cr. Current Price ₹ 574; High / Low ₹ 736 / 484; Stock P/E 5.75; Book Value ₹ 661; Dividend Yield 1.73 % ROCE 8.93 % ROE 16.0 %. For a company that survived the IL&FS crisis and emerged stronger, the market's valuation seems almost punitive. Trading at just 5.75 times earnings when private banks command multiples of 15-20, LIC Housing Finance exemplifies the classic value trap—or opportunity, depending on perspective.

LIC HOUSING FINANCE LTD EBITDA is 73.83 B INR, and current EBITDA margin is 25.82%. These are healthy numbers by any standard, yet the stock has underperformed dramatically. Mkt Cap: 31,527 Crore (down -10.7% in 1 year). While the broader market celebrated new highs, LIC Housing Finance shareholders watched their wealth erode, questioning whether government ownership was blessing or curse.

The valuation disconnect becomes starker when compared to peers. HDFC Bank, post-merger with HDFC Ltd, trades at a P/E of approximately 18. Can Fin Homes, a much smaller player, commands a P/E of 12. PNB Housing Finance, with similar parentage issues, trades at 7. Even adjusting for government ownership discount, LIC Housing Finance appears deeply undervalued—unless the market knows something the numbers don't reveal.

Company has low interest coverage ratio. The company has delivered a poor sales growth of 7.33% over past five years. These warnings from screening services highlight the bear case succinctly. In a sector where growth drives valuations, 7% annual expansion barely keeps pace with inflation. The interest coverage concern, while manageable, raises questions about leverage in a rising rate environment.

The capital structure tells its own story. With promoter holding at 45.2% (primarily LIC), the company operates in a peculiar zone—neither fully government-controlled nor truly independent. Institutional holdings are notably high at 42.46%, reflecting confidence from larger investors who typically possess greater analytical resources. Yet retail participation remains muted, suggesting individual investors remain skeptical.

Profitability metrics reveal operational efficiency despite growth challenges. ROE at 16% surpasses many private banks, demonstrating effective capital deployment. The net interest margin, while compressed from historical highs, remains healthy at 2.73% for FY25. These aren't the numbers of a struggling institution but of a profitable, well-managed company trapped by perception.

The funding mix showcases both strength and vulnerability. Unlike pure-play NBFCs dependent on wholesale funding, LIC Housing Finance maintains diversified sources—bank loans, bond markets, retail deposits, and parent support. This diversification proved crucial during the liquidity crisis. Yet it also increases complexity and cost, contributing to margin pressure.

Asset quality metrics have improved dramatically post-crisis. Stage 3 assets declining to 2.75% from 4.26% a year earlier represents genuine improvement, not accounting manipulation. The provision coverage ratio at 48% might seem conservative, but it reflects management's caution after witnessing peer failures. Better to over-provide and surprise positively than under-provide and face credibility questions.

The comparison with peers reveals strategic choices and their consequences. While PNB Housing pursued aggressive growth and faced asset quality issues, LIC Housing Finance chose stability. While Can Fin Homes focused on niche southern markets, LIC Housing Finance maintained national presence. While new-age players like Aavas Financiers targeted specific segments with technology, LIC Housing Finance served everyone, everywhere, everything—jack of all trades, master of none?

The efficiency ratios tell a mixed story. Cost-to-income ratio has improved post-digitalization but remains higher than nimble competitors. The company maintains 282 marketing offices across India—impressive reach but expensive overhead. Digital initiatives reduce marginal costs but the fixed cost base remains substantial. It's like running a modern software company with a manufacturing company's cost structure.

Geographic concentration, or lack thereof, impacts returns. Unlike regional players who dominate specific markets, LIC Housing Finance spreads resources nationally. This diversification reduces risk but also dilutes returns. In Tier-1 cities, they compete with banks offering lower rates. In Tier-3 cities, operational costs erode margins. The sweet spot—Tier-2 cities—faces increasing competition from focused players.

The product mix evolution reflects market realities. Individual home loans dominate at ₹2,62,411 crore, providing stable, predictable returns. Project loans at ₹8,950 crore remain modest, reflecting post-crisis conservatism. The company hasn't aggressively entered high-margin segments like loan against property or lease rental discounting, prioritizing safety over returns—admirable but frustrating for growth-seeking investors.

Technology investments, while improving efficiency, haven't translated to premium valuations. The market values digital natives like Bajaj Finance differently than digital immigrants like LIC Housing Finance. Fair or not, perception matters in valuation, and the company still carries the imagery of government clerks processing papers, not algorithms approving loans.

The dividend policy reveals management priorities. With dividend yield at 1.73%, the company returns modest cash to shareholders while retaining capital for growth and regulatory buffers. This conservative approach satisfies regulators and rating agencies but disappoints income-seeking investors who might prefer higher payouts given limited growth opportunities.

Market positioning remains the fundamental challenge. Too big to be nimble, too small to dominate. Too government to be entrepreneurial, too commercial to be social. Too traditional for tech valuations, too modern for value investing. LIC Housing Finance occupies an uncomfortable middle ground where excellence in execution isn't enough—the market demands a compelling narrative, and "steady and stable" doesn't excite anyone.

The recent adjustment in evaluation reflects the company's current market position and financial metrics. The PEG ratio stands at 0.4, suggesting a potentially favorable valuation in relation to growth. For patient investors, this combination of low valuation, improving operations, and sector tailwinds presents opportunity. For growth seekers, the structural challenges and competitive dynamics suggest continued underperformance.

The ultimate question isn't whether LIC Housing Finance is cheap—it demonstrably is. The question is whether cheap can become fair, whether fair can become premium. History suggests government-linked financial institutions trade at permanent discounts. Yet history also shows that structural changes—privatization, strategic sales, management buyouts—can unlock value dramatically. Until then, LIC Housing Finance remains a classic value stock: financially sound, operationally solid, and perpetually undervalued.

IX. Playbook: Business & Investing Lessons

The LIC Housing Finance saga offers a masterclass in navigating the intersection of public purpose and private profit. Each crisis survived, each transformation attempted, each strategic choice made reveals deeper truths about building and investing in financial institutions, particularly in emerging markets where government influence and market forces constantly collide.

The Power and Perils of Government Backing

The LIC parentage provided LIC Housing Finance with advantages most competitors could only dream of: patient capital during crises, instant credibility with customers, and implicit government support during systemic shocks. When IL&FS collapsed and private NBFCs faced funding freezes, investors fled to quasi-sovereign safety. This "flight to quality" phenomenon saved LIC Housing Finance while peers perished.

Yet government backing extracts its price. Decision-making slows as bureaucratic approvals multiply. Innovation suffers when failure carries political consequences. Talent acquisition becomes challenging when private sector pays multiples of government-influenced salaries. Most perniciously, the market applies a permanent "PSU discount," assuming inefficiency even when evidence suggests otherwise. The lesson: government backing is a double-edged sword—invaluable during crises, constraining during growth phases.

Asset-Liability Management in Housing Finance

The IL&FS crisis exposed a fundamental truth: in financial services, asset-liability mismatch isn't just a risk—it's an eventual death sentence. NBFCs borrowing short-term to lend long-term works until it doesn't. When it stops working, the unraveling is swift and merciless. LIC Housing Finance's survival stemmed from conservative ALM practices that seemed outdated during the boom but proved prescient during the bust.

The company's approach—matching 15-year mortgage assets with long-term bonds and deposits rather than commercial paper—reduced profits but ensured survival. They left money on the table by not playing the yield curve aggressively, but they remained at the table when others were carried out. For investors, this highlights a crucial insight: in leveraged financial institutions, risk management matters more than growth. The best returns come not from the fastest growers but from the survivors.

Surviving Sector-Wide Liquidity Crises

The 2018-2020 period offered a real-time lesson in crisis navigation. While competitors panicked, sold assets at distressed prices, or simply froze, LIC Housing Finance followed a measured playbook: conserve liquidity even at the cost of growth, maintain lending to preserve franchise value, communicate constantly with stakeholders, and use the crisis to gain market share from weakened competitors.

The strategy required nerves of steel. When everyone retreats, standing still looks like advance. When competitors offer desperate rates to attract deposits, matching them seems reckless. When the market demands immediate action, patience appears like paralysis. Yet LIC Housing Finance's measured approach proved optimal—they emerged stronger while aggressive players disappeared and overly conservative ones became irrelevant.

Digital Transformation in Traditional Finance

Project RED demonstrated that even 30-year-old government-linked institutions could reinvent themselves technologically. But the transformation revealed important nuances. Digital transformation in traditional finance isn't about becoming a fintech—it's about selectively adopting technology while preserving relationship-based strengths.

The company didn't try to out-tech the fintechs. Instead, they digitized the routine (application processing, document collection) while preserving the human touch for complex decisions (credit assessment, collection). They understood that in India, technology enables but trust closes. The HomY app succeeded not because it was cutting-edge but because it combined digital convenience with LIC brand trust.

Building Moats in Commoditized Lending

Housing finance is ultimately commoditized—one loan looks much like another. Yet LIC Housing Finance built sustainable advantages through distribution network density, brand trust from government association, customer data accumulated over decades, and operational knowledge of India's diverse markets. These moats aren't spectacular but they're real.

The lesson for investors: in commoditized industries, competitive advantages come from accumulation rather than innovation. The company that has processed a million loans knows things the company processing its first thousand cannot know. The brand that survived multiple crises carries trust that marketing budgets cannot buy. These advantages compound slowly but durably.

Risk Management Through Cycles

LIC Housing Finance's history spans multiple cycles: the pre-liberalization scarcity, the 2000s boom, the 2008 global crisis, the IL&FS collapse, and the COVID pandemic. Each cycle taught different lessons but the meta-lesson was consistent: in financial services, surviving the down cycle matters more than maximizing the up cycle.

The company's approach—conservative during booms, aggressive during busts—seems obvious in hindsight but requires extraordinary discipline in practice. When competitors grow 30% annually, growing 10% feels like failure. When everyone leverages up, maintaining conservative ratios seems foolish. When the market rewards risk-taking, prudence appears cowardly. Yet over full cycles, the tortoise beats the hare with remarkable consistency.

The Importance of Parent Company Support

The relationship between LIC and LIC Housing Finance offers lessons in subsidiary management. Unlike some conglomerates that milk subsidiaries for dividends or abandon them during crises, LIC provided consistent support—capital during stress, brand endorsement throughout, and strategic patience always. This parent-subsidiary dynamic created value for both entities.

For investors, this highlights an underappreciated factor: quality of parent matters as much as quality of business. A mediocre business with a committed parent often outperforms an excellent business with an extractive parent. In emerging markets where institutional voids exist, parent company support can substitute for missing market infrastructure.

Balancing Stakeholders in Quasi-Government Entities

LIC Housing Finance constantly balanced competing demands: shareholders wanting returns, government wanting financial inclusion, customers wanting low rates, employees wanting job security, and regulators wanting safety. This stakeholder juggling act, while complex, created unexpected stability. No single stakeholder could push the company toward excessive risk.

The investment lesson is counterintuitive: entities with multiple stakeholders often prove more resilient than those with single-minded focus. The need to balance competing interests creates natural risk management. The inability to maximize any single metric prevents fatal optimization. In complex systems, satisficing beats maximizing.

The Regulatory Arbitrage Reality

Throughout its history, LIC Housing Finance benefited from regulatory gaps. As an NBFC, it faced lighter regulation than banks. As a government-linked entity, it received favorable treatment during crises. As a housing financier, it enjoyed priority sector benefits. These regulatory advantages, while never decisive individually, cumulatively created significant value.

For investors, understanding regulatory positioning matters as much as understanding business positioning. Companies operating in regulatory sweet spots—enough regulation to create barriers, not enough to stifle operations—often generate superior returns. The key is identifying when regulatory arbitrage is sustainable versus when it invites adverse regulatory response.

Timing Transformation

The decision to launch Project RED in 2020, amid pandemic uncertainty, seemed risky but proved inspired. Crisis created burning platform for change, reduced resistance to transformation, and provided cover for investments that might otherwise face scrutiny. The lesson: the best time for transformation is during crisis when change is essential, not optional.

The Value of Boring Businesses

In an era celebrating disruption, LIC Housing Finance represents the power of boring. Housing finance isn't exciting. Government ownership isn't sexy. Conservative growth isn't headline-worthy. Yet boring businesses often generate superior long-term returns through predictability, sustainability, and survivability.

For investors, the lesson is to distinguish between boring businesses (predictable, stable) and bad businesses (declining, disrupted). The market often conflates the two, creating opportunities. LIC Housing Finance, trading at 5.75 times earnings while growing steadily and improving operationally, exemplifies this opportunity.

The playbook that emerges from LIC Housing Finance's journey isn't about brilliant strategies or breakthrough innovations. It's about consistency, conservatism, and competence—boring virtues that compound into extraordinary outcomes over time. In finance, as in life, survival is the ultimate performance metric.

X. Bear vs. Bull Case

The investment case for LIC Housing Finance presents a fascinating study in contrasts. Bulls see a deeply undervalued franchise trading at distressed multiples despite operational improvement. Bears see structural challenges that justify the discount. Both sides marshal compelling evidence, and the truth likely incorporates elements of each perspective.

Bull Case: The Undervaluation Opportunity

The arithmetic seems compelling. Market Cap ₹ 31,565 Cr for India's largest housing finance company, with a total loan portfolio of Rs. ~2,87,000 Cr in FY24 vs Rs. ~2,10,000 Cr in FY20. Trading at just 5.75 times earnings while generating 16% ROE, the valuation appears to price in catastrophe that isn't materializing. This isn't a distressed asset—it's a profitable, growing company wearing a distressed valuation.

The government backing through LIC parentage provides a safety net most financial institutions lack. During the IL&FS crisis, this quasi-sovereign status proved invaluable. September 2018: IL&FS defaults on repayment of a Rs1,000 crore short-term loan from Small Industries Development Bank of India. This alarms credit rating agencies, which start downgrading the company and its subsidiaries. CNBC-TV18 reports that the IL&FS group is saddled with a debt of Rs91,091 crore and is facing losses to the tune of Rs1,887 crore in the financial year 2018. News reports also say IL&FS has been funding long-term projects via short-term borrowing. As the cost of borrowing rises due to an increase in debt, short-term liquidity dries up and projects get delayed, and IL&FS finds it difficult to make repayments. While peers collapsed, LIC Housing Finance not only survived but gained market share. In future crises—and they will come—this backing provides unmatched resilience.

The digital transformation showing tangible results cannot be ignored. Currently, 35-40 per cent of the loan applications of the company are being processed digitally and the percentage will improve to 90-95 per cent post completion of this project. From the beginning of the third year, 90-95 per cent of loan applications are processed digitally. This isn't cosmetic digitization but fundamental transformation, reducing costs while improving customer experience. The company that once epitomized bureaucratic slowness now competes on digital efficiency.

The housing finance sector has been witnessing strong credit growth with tier-2 and tier-3 cities as main drivers. This geographic shift plays to LIC Housing Finance's strengths—extensive distribution in smaller cities where brand trust matters more than app features. While fintech players struggle to penetrate beyond metros, LIC Housing Finance already owns these markets.

The affordable housing segment opportunity remains massive. Government initiatives like "Housing for All" create tailwinds that could persist for decades. With India's housing shortage estimated at 30 million units, primarily in affordable segments, LIC Housing Finance's positioning seems prescient. Their experience serving lower-middle-class customers provides competitive advantages that neither banks nor fintechs can easily replicate.

Asset quality improvements suggest operational excellence rather than mere cycle benefits. Its stage 3 assets, or loans that are overdue for more than 90 days, declined to 2.75% for the quarter from 4.26% a year earlier. This improvement during a period of economic uncertainty demonstrates robust risk management. The company hasn't just survived—it's thriving.

Low valuations create asymmetric risk-reward. At P/E of 5.75, the market prices in significant deterioration. Even modest multiple expansion to 8-10 times earnings would generate 40-75% returns. The downside seems limited—how much cheaper can a profitable, growing financial institution trade? The risk-reward skews positively for patient investors.

The capital allocation optionality remains underappreciated. With strong capital adequacy and improving profitability, management could increase dividends, buy back shares, or pursue acquisitions. Any shareholder-friendly action could catalyze rerating. The company has options—markets eventually recognize optionality value.

Bear Case: Structural Challenges Persist

The company has delivered a poor sales growth of 7.33% over past five years. In financial services, growth drives valuations, and 7% barely exceeds inflation. While management talks about acceleration, evidence remains limited. Without growth, multiple expansion seems unlikely regardless of operational improvements.

Interest rate sensitivity poses increasing risks. Housing finance companies are essentially spread businesses—borrowing at one rate, lending at another. Rising rates compress spreads, especially for companies with large legacy books at lower rates. Net Interest Margin (NIM) for FY25 stood at 2.73% as against 3.08% for the previous year. The margin compression trend could accelerate if rates rise further.

Competition from banks intensifies daily. Post-HDFC merger with HDFC Bank, banks realize housing finance's attractiveness. With lower funding costs, stronger brands, and existing customer relationships, banks can underprice NBFCs structurally. LIC Housing Finance's cost of funds disadvantage is permanent, not temporary.

Technology disruption accelerates beyond catch-up capability. While Project RED improved operations, competing with digital-native players requires more than technology adoption—it requires technological innovation. Companies designed digitally from inception possess advantages that digital immigrants cannot match. LIC Housing Finance digitized existing processes; disruptors reimagine processes entirely.

Government ownership creates permanent constraints. Political interference, bureaucratic decision-making, and social obligations limit strategic flexibility. While private competitors can exit unprofitable segments, pivot strategies quickly, or take calculated risks, LIC Housing Finance operates within government-influenced parameters. This "PSU discount" reflects real limitations, not market prejudice.

Asset quality concerns lurk beneath improving metrics. Real estate sector stress, particularly in commercial segments, could materialize suddenly. The company's developer finance exposure, while modest, could prove problematic if property markets correct. India's real estate sector's opacity makes risk assessment difficult—problems emerge suddenly and severely.

The regulatory environment grows increasingly challenging. Recent RBI guidelines on interest rate reset, foreclosure charges, and customer protection reduce profitability. Housing finance companies face bank-like regulations without bank-like advantages. Regulatory arbitrage that benefited NBFCs historically disappears steadily.

Demographic shifts might not favor traditional housing finance. Younger Indians increasingly prefer renting in cities over owning in suburbs. Work-from-home reduces location importance. Shared economy concepts challenge ownership models. These secular trends could reduce housing finance demand structurally, not cyclically.

ESG concerns increasingly matter to institutional investors. Government ownership, while providing stability, raises governance questions. Board independence, executive compensation, and strategic autonomy face scrutiny. ESG-focused funds might avoid regardless of valuation attractiveness. As ESG investing mainstreams, this could perpetuate undervaluation.

The talent challenge compounds over time. Attracting and retaining quality professionals becomes harder when private sector competitors offer superior compensation. Stock options, the currency of talent acquisition, lack appeal when shares underperform perpetually. Without talent, competing in increasingly sophisticated markets becomes impossible.

The Balanced Perspective

Reality likely lies between extremes. LIC Housing Finance isn't the distressed asset its valuation implies, nor the hidden gem bulls proclaim. It's a solid, stable financial institution facing structural headwinds while navigating sectoral transformation. The company will likely survive and even prosper modestly, but explosive growth seems improbable.

For value investors with patience, the risk-reward appears favorable. The company trades below book value despite generating mid-teens ROE. Even modest improvement could generate acceptable returns. The dividend yield provides some compensation for waiting. Downside seems limited given current valuations.

For growth investors, better opportunities exist elsewhere. Structural constraints limit upside regardless of operational improvements. The 7% historical growth rate might represent ceiling, not floor. In a market offering dynamic growth stories, why accept static stability?

For income investors, the proposition seems mixed. Current dividend yield of 1.73% underwhelms, but potential for increased payouts exists. The stability and government backing provide safety, but inflation protection seems minimal.

The investment decision ultimately depends on time horizon and risk tolerance. Short-term traders should probably avoid—catalysts seem limited. Long-term investors might find value, particularly if willing to wait for strategic changes like privatization or stake sales. The bear-bull debate will likely persist until structural changes provide definitive resolution.

XI. Epilogue & "If We Were CEOs"

Standing at the helm of LIC Housing Finance in 2025 would feel like captaining a battleship in the age of speedboats. The vessel is sturdy, well-armed, and battle-tested, but maneuverability in rapidly changing waters presents constant challenges. If we were CEOs, the strategic priorities would balance respect for institutional heritage with urgency for transformation.

Strategic Priority 1: Redefine the Competitive Arena

Rather than competing head-to-head with banks in prime segments or fintechs in digital innovation, we would identify and dominate underserved niches. India's 30 million housing shortage isn't monolithic—it comprises dozens of micro-segments, each with distinct needs. Self-employed professionals in Tier-2 cities. Women borrowers seeking independent property ownership. Senior citizens monetizing property wealth. Green housing pioneers seeking sustainable financing. Each niche offers opportunity for specialization and premium pricing.

The strategy would involve creating specialized verticals with dedicated teams, customized products, and targeted marketing. Instead of being everything to everyone, become everything to someone. The government backing provides unique credibility in segments others fear to enter.

Strategic Priority 2: Technology as Enabler, Not Strategy

The temptation to become a "digital-first" company should be resisted. Technology should enhance strengths, not define identity. The focus would shift from digitizing everything to digitizing intelligently. Use AI for risk assessment but maintain human underwriters for complex decisions. Deploy chatbots for routine queries but preserve relationship managers for high-value customers. Automate back-office processes but maintain physical presence where trust requires proximity.

The technology investments would prioritize APIs enabling ecosystem partnerships over standalone app features. Partner with PropTech players rather than competing. Integrate with government databases for instant verification. Create white-label solutions for smaller institutions. Become the infrastructure others build upon, not another app in an overcrowded marketplace.

Strategic Priority 3: Balance Sheet Optimization

With capital adequacy comfortable but ROE suboptimal, aggressive balance sheet management becomes imperative. This means securitizing seasoned portfolios to free capital for fresh lending, using co-lending arrangements with banks to leverage their low-cost funds, developing fee-based products that generate income without consuming capital, and optimizing geographic and segment allocation based on risk-adjusted returns.

The goal isn't growth for growth's sake but intelligent capital deployment. Every rupee should work harder, generating maximum return within acceptable risk parameters. This might mean shrinking in some segments while expanding in others—strategic retreat can enable strategic advance.

Strategic Priority 4: Cultural Revolution Within Evolution

Transforming a 35-year-old institution requires delicate cultural navigation. Rather than imposing Silicon Valley culture on government DNA, we would create hybrid models. Establish innovation labs staffed by young talent but overseen by experienced hands. Create fast-track promotion paths for digital natives while respecting tenure-based progression for others. Implement variable compensation for new hires while maintaining stability for existing employees.

The cultural change would emphasize outcomes over activities, customer satisfaction over compliance checkboxes, and innovation within boundaries over disruption without direction. Change the how without losing the why.

Strategic Priority 5: The Affordable Housing Moonshot

India's affordable housing represents a generational opportunity requiring boldness. We would launch a "10 Million Homes Initiative"—ambitious, measurable, and aligned with national priorities. This would involve partnering with state governments for land and approvals, collaborating with developers for construction finance, working with employers for salary-deduction loans, and leveraging technology for standardized, rapid approvals.

The initiative would position LIC Housing Finance as the affordable housing champion, creating social impact while generating sustainable returns. Government support would likely follow, potentially including interest subsidies, guarantee programs, or priority sector benefits.

Strategic Priority 6: Product Innovation Within Regulatory Boundaries

Innovation doesn't require regulatory arbitrage. We would develop products addressing real customer pain points: graduated payment mortgages for young professionals expecting income growth, reverse mortgages for senior citizens seeking liquidity, green mortgages with rate benefits for sustainable construction, Islamic finance-compliant products for underserved communities, and rental yield-based underwriting for investment properties.

Each product would undergo rigorous testing before scaling. Innovation would be disciplined, not chaotic. The failures of IL&FS and DHFL remind us that financial innovation without risk management is destruction, not creation.

Strategic Priority 7: Geographic Expansion Through Partnerships

Physical expansion is expensive and slow. Instead, we would create a partnership ecosystem. Regional rural banks for last-mile connectivity. Fintech platforms for origination. Local developers for project finance. State governments for employee housing schemes. The strategy transforms fixed costs into variable costs while maintaining quality control through technology and training.

Strategic Priority 8: The Talent Transformation

Attracting talent to a government-linked institution requires creativity. We would establish a subsidiary with startup culture and compensation. Create an ESOP program linked to performance metrics. Partner with premier institutions for management trainees. Implement reverse mentoring where young employees teach digital skills to senior management. The goal is making LIC Housing Finance an employer of choice for specific talent pools, not competing broadly for all talent.

Strategic Priority 9: Investor Communication Revolution

The undervaluation partially stems from poor market communication. We would implement quarterly investor days with transparent metrics, regular thematic presentations on strategic initiatives, proactive engagement with research analysts, and social media presence humanizing the institution. The story needs telling—profitable growth, digital transformation, social impact, and undervaluation. Markets respond to narratives backed by numbers.

Strategic Priority 10: The Exit Strategy Options

While building for perpetuity, we would create optionality for strategic changes. This might involve preparing for potential privatization through operational improvements, exploring strategic partnerships with global housing finance players, considering merger opportunities with complementary institutions, or evaluating subsidiary spin-offs for value unlocking. Options have value—creating them enhances shareholder returns regardless of execution.

The Next Decade Vision

Looking ahead, LIC Housing Finance could evolve from India's largest housing finance company to India's most trusted home ownership enabler. This requires moving beyond lending to encompassing the entire home-buying journey—property search, legal verification, construction monitoring, and post-purchase services.

The company could leverage its data treasure trove—decades of customer information, payment histories, and property valuations—to create new business models. Credit scoring services. Property valuation platforms. Mortgage insurance products. Each leverages existing strengths while creating new revenue streams.

The affordable housing focus could catalyze broader financial inclusion. Today's affordable housing borrower becomes tomorrow's prime customer. Children educated in owned homes achieve more than those in rented accommodations. Communities with high homeownership demonstrate greater stability. The social impact multiplies the financial returns.

Technology adoption could accelerate from digitization to innovation. Blockchain for property titles. AI for fraud detection. IoT for property monitoring. VR for remote property tours. The company that once processed applications on paper could pioneer PropTech innovation.

The regulatory relationship could evolve from compliance to collaboration. Work with regulators on sandbox initiatives. Pioneer self-regulation in emerging areas. Share data for policy formulation. Become the bridge between government intent and market reality.

Final Reflections

India's housing finance evolution mirrors its economic transformation—from scarcity to abundance, from government control to market forces, from physical to digital. LIC Housing Finance, present at each inflection point, shaped and was shaped by these transitions.

The company's journey from 1989 to present demonstrates that sustainable success comes not from brilliant strategies or charismatic leaders but from consistent execution, conservative risk management, and patient capital allocation. In finance, boring is beautiful. Survival is success. Stability is strength.

The challenges ahead—technological disruption, regulatory evolution, competitive intensity—are real but manageable. The opportunities—housing shortage, financial inclusion, digital transformation—are massive and achievable. The company that survived demonetization, RERA, IL&FS, and COVID can navigate future uncertainties.

For investors, employees, and stakeholders, LIC Housing Finance represents a bet on India's housing story. As millions move from villages to cities, from joint families to nuclear households, from renting to owning, demand for housing finance will grow inevitably. The question isn't whether the opportunity exists but who captures it.

If we were CEOs, the north star would be simple: enable 10 million Indian families to own homes profitably and sustainably. Everything else—technology, products, partnerships—serves this mission. The company that achieves this won't just generate returns; it will transform lives, communities, and ultimately, the nation.