Lenskart: The $6 Billion Vertical Integration Masterclass

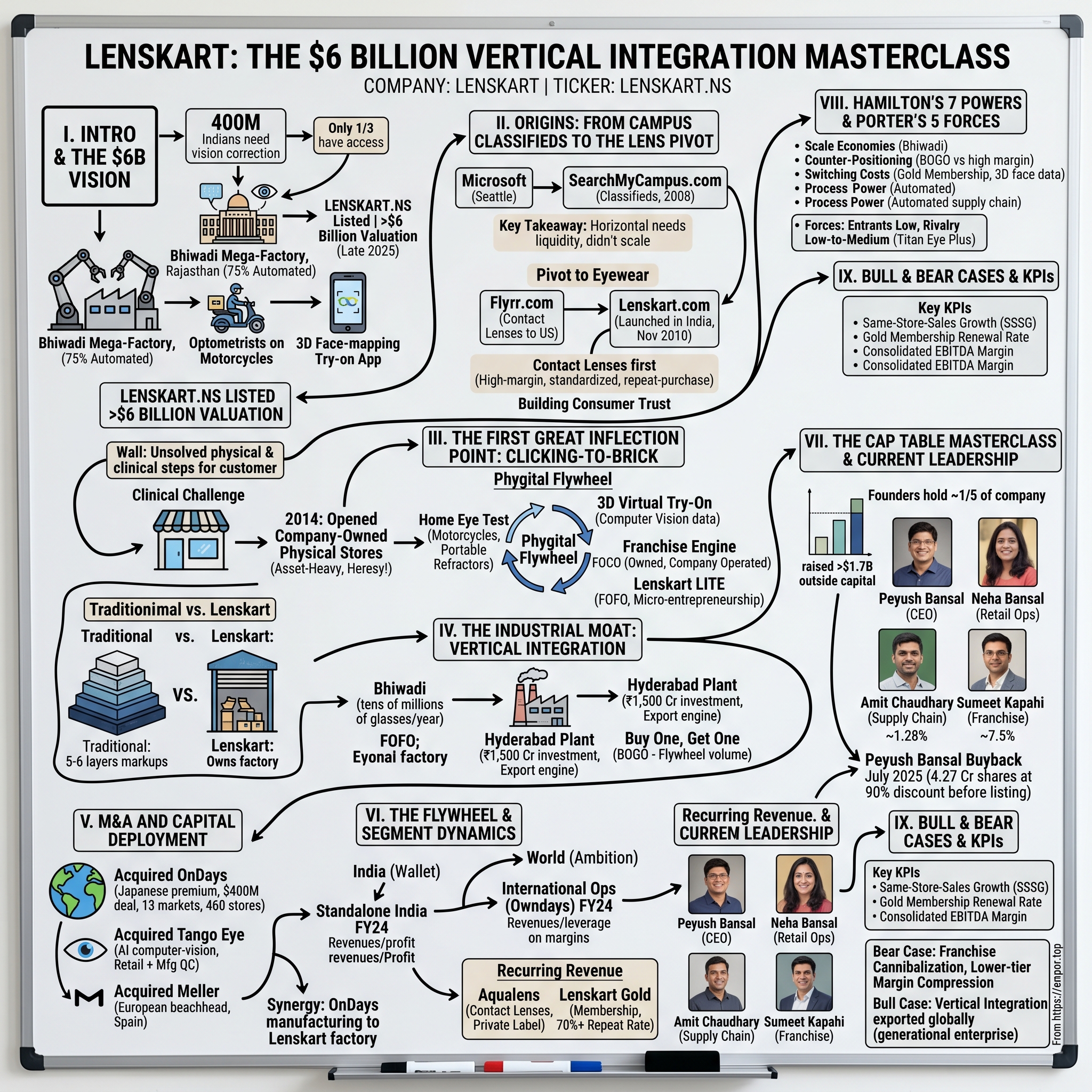

I. Introduction & The $6 Billion Vision

There is a number in India that almost nobody can picture, because it is too big to picture. Roughly 400 million Indians need some form of vision correction — more than the entire population of the United States, walking around with a refractive error they have never had measured. For most of independent India's history, perhaps a third of those people had any practical access to an accurate eye test and an affordable, well-made pair of glasses. The rest squinted. They bought ready-made readers off a cart, or a frame from a dusty glass cabinet in a shop where the price was whatever the owner decided your shirt could afford that morning. Vision, the most basic enabler of work and study and dignity, was rationed by geography and by trust.

Now hold that picture against another one. A glass-and-steel factory in the desert scrub of Rajasthan, where German robots cut and edge prescription lenses to sub-micron tolerances, churning out tens of millions of finished glasses a year, while a few hundred kilometres away a fleet of optometrists on motorcycles ride into residential colonies carrying portable refractors in their backpacks to give you a clinical eye exam in your own living room. Tie those two images together with software — a phone app that 3D-maps your face so you can "try on" a thousand frames before one is ever cut — and you have the rough shape of how a contact-lens website launched in 2010 became, by late 2025, a public company worth north of $6 billion, listed on the National Stock Exchange as LENSKART.NS.12

That is the puzzle this episode is about. Lenskart is routinely described, lazily, as "the Warby Parker of India" or a direct-to-consumer success story. Both descriptions miss the entire point. The thesis we want to argue today is that eyewear — real, prescription, medical-grade eyewear — is one of the most deceptively complex consumer products on earth. It is part fashion accessory, part precision optical instrument, part medical device, and part heavy-logistics nightmare. You cannot win it with a slick storefront and a clever ad campaign. You win it the way Luxottica won the West: by quietly owning the physical infrastructure — the factories, the lens labs, the stores, the supply chain, the prescription data — that sits between a customer's blurry eyesight and a finished pair of glasses on their nose.

Lenskart's founders figured this out the hard way, and the figuring-out is the story. They started online to look like a tech company and discovered they had to become a manufacturer. They copied the American playbook and then tore it up. They opened company-owned stores when every venture-capital orthodoxy screamed "stay asset-light." And then, having built the machine, they did something genuinely unusual for an Indian startup: they went shopping abroad, buying a Japanese premium eyewear giant, オンデーズ Owndays, in a $400 million cross-border deal, and folding its supply chain into their own robotic factories.3

Here is the roadmap. We'll go back to the campus-classifieds failure that came before the eyewear epiphany. We'll walk through the 2014 pivot from pure online into physical retail — the "clicking to brick" inflection that made the company. We'll stand inside the Bhiwadi mega-factory and explain why owning it changes the entire economics of the business and lets Lenskart hand you a second pair of glasses for free. We'll benchmark the Owndays deal, the tuck-in acquisition of an AI vision startup, and a European beachhead in Spain. We'll look at the recurring-revenue businesses hiding inside — the Aqualens contact-lens label and the Gold membership — and finally the cap-table choreography and pre-IPO manoeuvres that carried founder Peyush Bansal onto the public markets still holding a stake most founders only dream about. Let's start in a basement in Delhi.

II. Origins: From Campus Classifieds to the Lens Pivot

In the mid-2000s, Peyush Bansal was doing what a certain kind of ambitious Indian engineer was supposed to do: he was in the United States, employed by Microsoft in the Seattle area, on the comfortable escalator of a global tech career. He had the green-card trajectory, the salary, the résumé line that makes parents relax. And he was restless in the specific way of people who cannot stop noticing problems they think they could fix. The problem he kept circling was not a software problem. It was the gap he saw between the slick, organized retail and services he experienced in America and the chaotic, opaque, under-served version of the same things back home in India.

So he did the thing that looks insane on paper and obvious in hindsight. He left. He went back to Delhi, moved into his parents' house — the founding mythology, true enough in spirit, places the early work in the family basement — and in 2008 started a company called Valyoo Technologies. The first product was not eyewear at all. It was SearchMyCampus.com, an online classifieds portal aimed at students: a place to find flatmates, used textbooks, tutors, part-time gigs, the whole ecosystem of campus life. It was a sensible idea and it taught Bansal a hard lesson that would define everything after: horizontal marketplaces need enormous liquidity to work, and a cash-strapped startup trying to be everything to students everywhere couldn't generate it. SearchMyCampus didn't scale.4

But the team that gathered around the attempt was the real asset. Bansal assembled the co-founders who would still be running the company nearly two decades later: Amit Chaudhary and Sumeet Kapahi, with Neha Bansal joining the founding core. This is worth pausing on, because founder durability is one of the quietly predictive variables in business history. The Lenskart that listed in 2025 was still run by essentially the same people who couldn't make a student classifieds site work in 2009. They learned together, and they stayed.

The wedge into eyewear came, fittingly, from the United States and from a search for something — anything — with cleaner economics than classifieds. The team launched Flyrr.com, a site selling contact lenses to American customers. Contact lenses are a beautiful first product if you're a scrappy e-commerce operator: they're a standardized, regulated, repeat-purchase consumable with no fitting problem once the prescription is known. Flyrr worked well enough to prove the model — and, more importantly, to reveal the real prize. The American contact-lens market was already organized, competitive, and thin-margined. The Indian eyewear market, by contrast, was a wide-open frontier: over 80% of it unorganized, dominated by neighbourhood opticians with opaque pricing, limited selection, and wildly inconsistent quality. The opportunity wasn't in Seattle. It was at home.

In November 2010, Lenskart.com launched in India.4 And notice the careful, almost surgical choice of opening product. They did not lead with prescription eyeglasses, even though glasses were the obvious mass-market prize. Prescription eyewear in India sat behind real regulatory and trust hurdles — it is, after all, a medical product dispensed against a doctor's prescription — and selling it online to a population that had never bought medical-grade glass over the internet was a wall too high to climb on day one. So they started where Flyrr had taught them to start: contact lenses. High-margin, standardized, repeat-purchase, low regulatory friction. It got the cash register ringing and, crucially, it began the slow work of earning the one thing online medical commerce lives or dies on — consumer trust.

That early grind to convince Indians that it was safe and sensible to buy something that goes near your eyes from a website — that is the through-line to everything that follows. The trust deficit Lenskart fought in 2011 is exactly why, three years later, it would do the most counter-intuitive thing in its history and start pouring capital into physical stores. To understand that pivot, you have to understand that the company had hit a ceiling it didn't see coming.

III. The First Great Inflection Point: Clicking-to-Brick

By 2013, Lenskart looked, on the surface, like a textbook venture-backed e-commerce winner in the making. It had the website, the catalogue, the discounting, the digital-marketing flywheel, and a fashionable American comparison — Warby Parker — that investors loved to hear. And it was running into a wall that no amount of digital marketing could get through. The wall had a simple name: the Indian customer, standing in her own home, did not actually know what to buy.

Think about what buying prescription glasses online demands of a customer. First, you need a current, accurate prescription — and the overwhelming majority of Indians who needed glasses had never had a proper refraction test, or had one years ago. Second, you need to trust that a frame you've only seen on a screen will fit your face and look right. Third, and most subtly, you need to be comfortable putting a precision optical-medical product on your face that you bought, sight unseen, from the internet. American pure-play eyewear could lean on a population that mostly already had prescriptions and a high baseline of online-shopping trust. India had neither. The pure-play online D2C model, lifted straight from the U.S., hit a hard ceiling — not because Indians wouldn't shop online, but because the eyewear purchase had unsolved physical and clinical steps sitting right in the middle of it.

So in 2014, Lenskart did the thing that breaks the startup catechism. The entire religion of the 2010s venture world was "asset-light": don't own inventory, don't own real estate, let the internet be your storefront. Lenskart started opening company-owned physical stores. To a Sand Hill Road purist this looked like heresy — an internet company voluntarily taking on leases, fit-out costs, and store staff. To the founders it was the only way to actually solve the customer's problem. The store was where the prescription got taken, the frame got tried on, the trust got built. Online would still matter enormously — but as one channel in an integrated system, not the whole game.

What they built around that insight is the part worth dwelling on, because it's genuinely clever. Call it the phygital flywheel — physical plus digital, each feeding the other. Two innovations stand out.

The first was 3D virtual try-on. Using computer vision on the mobile app and web, Lenskart let a customer point a phone camera at their own face and map it in three dimensions, then "wear" any frame in the catalogue virtually. Over time the company generated tens of millions of these face scans.5 The genius here is not the gimmick of seeing yourself in glasses — it's the data. Every scan is a precise map of a human face: pupillary distance, frame fit, what suits which face shape. That dataset is both a conversion tool (people buy more confidently when they can see themselves) and a quietly accumulating competitive asset that a new entrant cannot replicate without first acquiring millions of customers.

The second was the home eye test — and this is the one that tells you how seriously the company took the Indian context. Lenskart put certified eye technicians on motorcycles, equipped with portable refraction kits and an iPad, and sent them into customers' homes. An optometrist would arrive at your living room, run the exam on the spot, and take the order on the tablet. For a customer who had never been to an optician, this collapsed three sources of friction — getting to a store, trusting the test, placing the order — into one home visit. It was logistically heavy, unglamorous, and exactly the kind of thing a pure software company would never build. It also worked.

The store-rollout problem was capital and control. Open everything company-owned and you grow slowly and chew through cash; franchise everything and you lose grip on the service quality and inventory that the whole trust thesis depends on. Lenskart's answer was a hybrid franchise engine with two distinct modes. The first, FOCO — Franchise Owned, Company Operated — lets a local partner put up the capital for the store fit-out and real estate, while Lenskart retains absolute control over staffing, service standards, and inventory.6 The partner brings money and local knowledge; Lenskart keeps the brand experience identical to a company-run store. The second mode, Lenskart LITE, is a lower-cost, micro-entrepreneurship FOFO model — Franchise Owned, Franchise Operated — built to push into Tier 3 and Tier 4 towns at a fraction of the setup cost of a flagship store.6 FOCO buys controlled growth in big markets; LITE buys deep, capillary reach into small-town India that company-owned economics could never justify.

This architecture — own the experience, share the capital, blanket the country — is what let Lenskart scale toward thousands of stores. But a retail network, however clever, is only as good as the product flowing through it. And the founders had realized that the real margin, the real moat, wasn't in the stores at all. It was in the factory they didn't yet own. So they went and built one.

IV. The Industrial Moat: Bhiwadi, Hyderabad, & Vertical Integration

To understand why Lenskart built a factory, you have to understand who normally stands between you and a finished pair of prescription glasses — and how many of them take a cut. In the traditional optical world, a frame is designed by a brand, licensed to a manufacturer, sold to a distributor, marked up to a wholesaler, sold to a retail optician, and then the lenses are ground and fitted by yet another specialist lab. Five or six layers, each adding margin and time. The reason a pair of branded glasses can cost what a smartphone costs has almost nothing to do with the few dollars of raw material and almost everything to do with that stack of intermediaries and brand-licensing fees. Luxottica built one of the great fortunes in consumer goods essentially by owning many of those layers at once.

Lenskart looked at that stack and decided to own the factory itself. The centrepiece is the mega-factory at Bhiwadi, in Rajasthan, an automated plant the company runs at roughly 75% automation, using imported robotic systems to cut, edge, and assemble lenses and frames at sub-micron accuracy and at a scale measured in tens of millions of finished glasses a year.[^7] Let's translate "sub-micron accuracy" out of the brochure. A micron is a thousandth of a millimetre; a human hair is about seventy of them across. The optical centre of a prescription lens has to sit in front of your pupil within a tolerance finer than that, or the prescription is subtly wrong and you get headaches and eye strain. Doing that by hand, reliably, lens after lens, is genuinely hard. Doing it with robots, identically, fifty million times a year, is a manufacturing achievement — and it's why an automated plant doesn't just cut cost, it raises and standardizes quality at the same time.

The strategic payoffs cascade. By manufacturing domestically rather than importing finished or semi-finished product from China and South Korea, Lenskart compresses its supply chain dramatically — inventory turnaround on a finished pair can run in the 24-to-48-hour range rather than the weeks an import cycle demands. That speed is itself a competitive weapon: a store that can refill a fast-selling frame in two days carries less dead inventory and stocks out less often than one waiting on an ocean container. Owning the plant also means Lenskart controls its own destiny on cost, quality, and design iteration in a way no asset-light competitor reselling third-party frames ever can.

And the company is not stopping at Bhiwadi. Lenskart has broken ground on a far larger facility near Hyderabad — a roughly ₹1,500 crore (about $180 million) investment on a 50-acre site in Telangana, backed by a memorandum of understanding with the state government, designed to be one of the largest eyewear plants in the world.78 The Hyderabad plant is explicitly an export engine: built to manufacture on the order of 200,000-plus glasses a day, end to end from frame and lens to finished product, serving not just India but the Middle East, Japan, and Southeast Asia.7 Read alongside the Owndays acquisition, the intent is unmistakable. Lenskart isn't building Indian manufacturing to serve Indian stores; it's building a global low-cost production base and then routing the world's eyewear demand through it.

Now we get to the punchline of the whole industrial strategy — the part that explains a sign you'll see in every Lenskart store. Buy One, Get One. BOGO. The legendary deal where a customer buys a pair of prescription glasses and walks out with a second, free. To a traditional optician this looks like commercial suicide, because the optician's entire model is high margin on low volume — sell few, charge a lot. Lenskart inverts it. When you own the factory and run it at scale, your gross margin on a pair of glasses can sit around 70%.2 At that structure, the marginal cost of the "free" second pair is low enough that giving it away is a customer-acquisition and volume strategy, not a loss. BOGO simultaneously undercuts every organized competitor on price, doubles the volume flowing through the automated plant (which further lowers unit cost — a flywheel), and still leaves Lenskart with healthy unit economics. The free pair isn't generosity. It's vertical integration showing off.

That cost structure — owning the means of production and turning the savings into an offer rivals can't match — is the platform on which everything else is built. And once you have a manufacturing machine hungry for volume, the logical next move is to go find more demand to feed it. Which is exactly what Lenskart did, on three continents.

V. M&A and Capital Deployment: Benchmarking the Playbook

In June 2022, Lenskart did something that very few Indian consumer startups had ever attempted: it acquired a foreign company larger and more premium than itself in its home segment, in one of the most demanding retail markets on earth. The target was オンデーズ Owndays, a Japanese eyewear chain, and the deal valued Owndays at around $400 million, with Lenskart taking a majority position — buying out shareholders including L Catterton, 三井物産 Mitsui & Co., and others to control roughly 92% of the company.39 For a company that had begun as a contact-lens website in a Delhi basement, buying a 460-store premium chain across 13 markets was a statement of arrival.

Let's benchmark the deal the way an investor should, because the price is the whole story. Owndays operated around 460 stores spread across markets including Japan, Singapore, Taiwan, Thailand, the Philippines, Indonesia, and Malaysia, running at roughly a $250 million annual revenue run-rate.3 At a $400 million enterprise value, Lenskart paid something close to 1.6 times revenue. Hold that next to the comps. Luxury and premium retail brands routinely trade at four to six times revenue; high-growth consumer-tech names in the pre-listing froth of 2021–22 traded at multiples that would make your eyes water. Lenskart bought a profitable, premium, multi-country eyewear operator for less than two times sales. In a year when money was still cheap and consumer multiples were still inflated, that is an unusually disciplined price for a strategic asset.

But the real return on the deal wasn't in the purchase multiple — it was in the synergy that only a vertically integrated buyer could unlock. Owndays, like most eyewear retailers, sourced its product through relatively expensive overseas manufacturing and supply lines. Lenskart owned a 75%-automated factory hungry for volume. By migrating Owndays' manufacturing and supply chain onto Lenskart's Bhiwadi base, Lenskart could structurally lift Owndays' gross margins — taking a premium brand with a strong customer proposition and grafting it onto a low-cost production engine.10 That is the textbook industrial-logic acquisition: buy the demand and the brand, plug it into your own supply, and capture the margin that used to leak to third-party manufacturers. The combined entity vaulted to roughly $650 million in annual revenue and a presence across 13 Asian markets.3

The second deal in the playbook was tiny in dollars and large in intent. In October 2023, Lenskart acquired Tango Eye, a Chennai-based AI computer-vision startup, for an undisclosed sum — reported in the low single-digit millions, around $1.7 million — a company Lenskart already partly owned via a 2020 investment.1112 The strategy here is about converting a capability from rented to owned. Tango Eye's computer vision had been analyzing in-store CCTV to generate footfall analytics, customer heatmaps, and process-compliance checks. By bringing it fully in-house, Lenskart turned a vendor relationship into a proprietary asset it could point in two directions at once: at the retail floor, to understand exactly how customers move through stores and where they linger, and at the factory floor, where the same vision technology can sit on cameras over the lens-edging lines and automate quality control — catching a flawed lens that a human inspector might miss, at machine speed. A retail-analytics tool and a manufacturing-QC tool in one small acquisition.

The third move pushed into a new continent. In July 2025, Lenskart acquired an 80% stake in Meller, a Barcelona-based digital-first eyewear and accessories brand, reportedly for around $47 million.13 Meller is a younger, fashion-led sunglasses-and-watches label with European distribution and brand fluency — exactly the kind of localized beachhead that's hard to build from scratch in Europe and comparatively cheap to buy. Where Owndays bought Asian premium scale and Tango Eye bought a capability, Meller bought a European front door and the local taste-making that goes with it.

Three acquisitions, three different logics — premium scale, proprietary technology, geographic entry — all in service of the same machine. Now let's open the hood on where the money actually lives inside that machine, because the segment dynamics reveal which engine pays the bills and which one is the bet on the future.

VI. The Flywheel & Segment Dynamics: Core India vs. Global

Strip away the geography and the brand names, and Lenskart is really two businesses wearing one logo — and they have very different jobs. Understanding which is the cash generator and which is the growth bet is the single most useful lens for an investor looking at this company.

The first business is Standalone India — the core engine. This is the original Lenskart: the domestic stores, the Indian website, the Bhiwadi factory feeding the home market. In FY24 it drove roughly 58% of consolidated revenue, on the order of ₹3,186 crore, scaling toward ₹4,100 crore-plus in FY25.214 More importantly, this is the mature, profitable part of the company. The Indian standalone operation turned a net profit of around ₹144 crore in FY24, even as the consolidated group — weighed down by international expansion and acquisition integration — sat near breakeven, posting a small consolidated loss of roughly ₹10 crore that year.1514 That gap between a profitable core and a breakeven whole is not a red flag; it's the signature of a company using a mature, cash-generating home market to fund a deliberate, expensive land-grab abroad. India is the wallet. The world is the ambition.

The second business is International Operations — the premium engine, accounting for roughly 42% of revenue (around ₹2,273 crore in FY24), powered chiefly by オンデーズ Owndays across Japan, Singapore, and Taiwan.14 These markets matter for a reason beyond size: their average order values and gross profits per transaction run well above the Indian mass market. A pair of glasses sold in Tokyo or Singapore simply carries more revenue and more margin than the same transaction in a Tier 3 Indian town. As Lenskart migrates Owndays onto its own low-cost manufacturing, those higher-AOV international sales become disproportionately powerful contributors to consolidated profitability — which is the mechanism by which the whole group is expected to cross from breakeven into durable profit. The international segment isn't just bigger AOV for its own sake; it's the lever on group margins.

Sitting underneath both is a quieter, structurally important business that most coverage ignores: Aqualens, the contact-lens play. Here's the problem it solves. Eyeglasses are a terrible product for recurring revenue — a customer buys a pair and then disappears for twelve to twenty-four months. That's a low-frequency, lumpy relationship. Contact lenses are the opposite: a consumable that gets used up and reordered on a predictable cadence, the razor-blade to the eyeglass razor. Lenskart built Aqualens as a private-label contact-lens brand explicitly to capture that recurring, subscription-style demand.16 And the clever part is the go-to-market: rather than fighting purely on medical prescription needs, Aqualens leans on a fashion wedge — coloured lenses and high-oxygen silicone-hydrogel materials aimed at Gen Z and Millennials. ("High-oxygen silicone hydrogel" simply means a newer lens material that lets more oxygen reach the cornea, so lenses are more comfortable to wear longer — a genuine product improvement dressed in fashion appeal.) That fashion angle expands the addressable market beyond people who strictly need correction, and a contact-lens customer, once hooked, has real lifetime value because they keep reordering.

The final piece of the flywheel is Lenskart Gold — a membership program priced in the ₹500–600 a year range that effectively grants permanent BOGO benefits and member pricing.16 Think of it as the Amazon Prime move applied to eyewear. For a few hundred rupees a year, the customer pre-commits to coming back to Lenskart for their next pair and their family's pairs, because the economics only pay off if they do. That converts a fundamentally transactional, low-frequency category into something with a sticky, recurring relationship — and it's the engine behind Lenskart's reported repeat-purchase rates north of 70%. Membership locks the customer in; the factory makes the lock-in affordable; the data makes the next sale easier. The flywheel turns.

A flywheel this integrated raises an obvious question: who actually owns it, and how did the people who built it hold on to it through $1.7 billion of outside capital? That's where the story gets, frankly, a little astonishing.

VII. The Cap Table Masterclass & Current Leadership

There's a grim statistic that haunts venture-backed founders: by the time a hot consumer startup reaches its IPO, having raised round after round from increasingly powerful investors, the founders often own a sliver — single digits, sometimes less. Each financing dilutes them; each marquee investor takes a slice. Lenskart raised over $1.7 billion across its life from a who's-who of global capital — ソフトバンク・ビジョン・ファンド SoftBank Vision Fund, 三井物産 Mitsui & Co., Temasek, ADIA, Premji Invest, Kedaara Capital, Chiratae Ventures, and more.1718 By the iron logic of dilution, the founders should have been left with crumbs. Instead, heading into the public markets, the promoter group still controlled roughly a fifth of the company. In modern venture capital, that is a rare feat.

At the centre is Peyush Bansal — founder, CEO, and managing director — holding around 10.28% of the equity at listing.18 The arc of his career is the arc of the company: the Microsoft engineer who walked away from Seattle, the founder who failed at campus classifieds, the operator who broke the asset-light rule to build stores and factories, and finally the public-company CEO running a multi-country industrial-retail enterprise. What's notable about Bansal is the consistency of the underlying instinct across all those phases — a willingness to take on the hard, physical, capital-heavy version of a problem when the easy, asset-light version doesn't actually serve the customer. That instinct is unfashionable in software and exactly right in eyewear.

Around him sits the same founding team that couldn't make SearchMyCampus work. Neha Bansal, co-founder and executive director, holds roughly 7.5% and directs in-store operations and retail integration — the discipline of making thousands of stores feel like one store.18 Amit Chaudhary, co-founder, oversees global expansion and the supply-chain and logistics backbone that ties Bhiwadi, Hyderabad, Owndays, and Meller into one system. Sumeet Kapahi, co-founder, leads domestic retail expansion and the franchise networks — the FOCO and LITE machinery that blankets India. Four people, one company, eighteen years. We'll skip the non-founder, non-current-executive history here, because the live story is this remarkably durable founding core still holding the wheel.

Now the move that deserves its own paragraph, because it is a small masterclass in conviction and timing. In July 2025, just before filing the draft prospectus, Peyush Bansal bought back 4.27 crore shares — about a 2.5% stake — from early venture investors including Kedaara Capital, Chiratae Ventures, SoftBank, and others, at a secondary price of ₹52 per share, deploying roughly ₹222 crore over a week in mid-to-late July.1920 That price valued Lenskart at around ₹8,700 crore — a dramatic markdown to the ₹70,000-crore-plus valuation the company would target in its IPO weeks later.20 When Lenskart listed in November 2025 and the stock subsequently traded around ₹510, those ₹52 shares represented something close to a tenfold notional gain.121 You can read the optics two ways — and both can be true. The skeptic notes that buying at ₹52 right before marketing an IPO at ₹402 is a spectacular personal trade. The charitable reading, and the one the company leans on, is that a founder voluntarily concentrating his own capital into the business at the eleventh hour is the purest possible signal of skin in the game and alignment with the public shareholders about to come aboard. Either way, it is not the behaviour of someone hedging his bets.

The compensation structure reinforces the alignment story. The founders draw fixed salaries that are modest relative to the company's scale — on the order of ₹6 crore for Peyush and ₹3 crore each for Neha and Amit — with the real upside loaded into long-term ESOPs carrying performance hurdles tied to ambitious valuation targets reaching toward $10 billion.18 In other words, the team gets meaningfully rich only if the public shareholders do too. That's the structure you want to see; whether the targets are met is the open question. Speaking of open questions — why exactly is this business so hard to attack? Let's run it through two frameworks.

VIII. Hamilton's 7 Powers & Porter's 5 Forces

Strategy frameworks are where business analysis usually goes to die in jargon, so let's keep this concrete and ask the only question that matters: if you handed a competitor a billion dollars and told them to kill Lenskart, what exactly would stop them? Hamilton Helmer's 7 Powers gives us a vocabulary for the answer, and Lenskart genuinely holds several of them.

The most obvious is Scale Economies. The Bhiwadi plant — and soon Hyderabad — runs at a volume that drives the per-unit cost of a finished lens below anything a smaller player in India can achieve. This isn't a marketing claim; it's the physics of fixed-cost amortization. A robotic line costs the same whether it makes five million lenses or fifty million, so the more you run through it, the lower the cost of each one — and the more BOGO volume you push, the cheaper your unit cost gets, which lets you push more BOGO volume. A competitor producing a tenth of the volume simply cannot match the cost per lens. Scale here is self-reinforcing.

The subtlest and arguably strongest power is Counter-Positioning. This is the power that incumbents literally cannot copy without destroying themselves. The traditional Indian optician makes high margin on low volume — a few sales a day at fat markups. Lenskart's BOGO-at-scale model makes low margin per unit on enormous volume. For the incumbent optician to match Lenskart's prices, they would have to slash their own margins to the bone and cannibalize the high-margin business that keeps their lights on. They can see exactly what Lenskart is doing and still be unable to respond, because responding kills them faster than ignoring it does. That's textbook counter-positioning, and it's why organized incumbents have struggled to fight back on price.

Third, Switching Costs, engineered deliberately. The Gold membership creates a financial reason to come back; the proprietary app holds your saved prescriptions, your 3D facial map, your purchase and clinical history. Once Lenskart knows your face and your eyes and you've prepaid for member benefits, the friction of starting over with a competitor — re-testing, re-scanning, re-paying — is real. None of it is dramatic on its own, but together it raises the activation energy of leaving.

Fourth, Process Power — the hardest to copy and the slowest to build. This is the accumulated organizational capability of running a vertically integrated, automated supply chain that refills 2,500-plus stores in near real-time based on local demand signals, with computer vision watching both the shop floor and the factory line. You cannot buy this off a shelf; it's built over years of iteration, and it's why even a well-funded new entrant couldn't simply purchase Lenskart's operating capability along with a factory.

Now Porter's Five Forces, quickly, because they tell the same story from the outside in. Threat of new entrants: low. Replicating thousands of phygital stores plus automated factories is a several-hundred-million-dollar, multi-year undertaking — the capital and time barrier is brutal. Bargaining power of buyers: medium. Customers have abundant alternatives in the unorganized sector, which caps pricing power; but the BOGO value proposition is so strong that it neutralizes much of that leverage. Bargaining power of suppliers: low. Through vertical integration, Lenskart is largely its own supplier — it doesn't beg a frame distributor for terms; it owns the line. Competitive rivalry: low-to-medium within organized retail, where Lenskart commands over 41% of the organized market, leaving listed and unlisted peers well behind.2 The pressure that exists comes less from organized rivals and more from the vast, fragmented unorganized sector — which is less a competitor than a conversion opportunity. Let's go look at the actual competitors, because the war-game is instructive.

IX. Competitive Benchmarking: Lenskart vs. The World

If you want to understand a company's moat, watch how its strongest competitor fights — and then notice what that competitor structurally cannot do. In Indian organized eyewear, the strongest competitor carries one of the most trusted names in the country.

The main organized rival is Titan Eye Plus, the eyewear arm of Titan Company, itself part of the Tata Group — and trust is its entire weapon. Titan brings the Tata name, a reputation for clinical precision, and a marketing posture built around heritage and rigor, including an elaborate multi-step eye examination protocol positioned as more thorough than the competition.22 For a certain customer — older, more conservative, brand-loyal to Tata — that proposition genuinely resonates. But look at the scale gap and the structural difference. Titan Eye Plus generated on the order of ₹724 crore in eyewear revenue in FY24 across roughly 950 stores, against Lenskart's standalone India figure of around ₹3,186 crore across roughly 2,000 stores.222 Lenskart is several times larger on a fraction-more store count — meaning far higher productivity per store. And the deeper point is manufacturing: Titan's eyewear is heavily reliant on outsourced production, which means it cannot match Lenskart on raw volume cost or sustain aggressive BOGO-style discounting without bleeding. Titan competes on trust precisely because it cannot win on price. That's not a criticism; it's the constraint that vertical integration imposes on anyone who skipped it.

At the other end sits the luxury incumbent, exemplified by chains like GKB Opticals — a legacy, premium-metro operator built around high-touch service and imported luxury brands (the Cartiers and Guccis of the eyewear world), capturing high average selling prices from affluent urban buyers but, by design, addressing a thin slice of the market. Independently disclosed financials for these privately held luxury chains are limited, but the strategic position is clear regardless of the exact numbers: they win a small, high-ASP premium niche and make no attempt at mass-market volume. They are not really in the same fight as Lenskart; they're harvesting a different, smaller pond. Lenskart's premium ambitions, where it has them, are served by Owndays, not by trying to out-luxury the luxury players.

And then there is the real giant in the room — the one that owns roughly 80% of the entire Indian eyewear market and has no marketing budget at all: the unorganized sector, the hundreds of thousands of neighbourhood opticians. This is simultaneously Lenskart's largest "competitor" and its largest opportunity, and that framing is the whole game. Lenskart doesn't beat the corner optician by being cheaper on every single transaction; it beats them by offering something the fragmented sector structurally cannot — a clean, air-conditioned, tech-enabled store with transparent, fixed pricing, a verifiable eye test, a virtual try-on, a brand you can trust, and a free second pair. Every customer Lenskart converts from the unorganized 80% into a Gold member is a customer pulled out of a fragmented market and locked into a structured, recurring relationship. The competition that matters most isn't a battle against organized peers; it's a decades-long conversion of an entire informal market. Which sets up the obvious question for an investor: what could go right, what could go wrong, and what should you actually watch?

X. The Bull & Bear Cases & KPIs

Every great compounding story is also a list of ways it could break, and a disciplined investor holds both in mind at once. Before the bull and bear cases, let's name the instruments on the dashboard — because for a business this multi-layered, most of the noise is noise, and only a few numbers actually tell you whether the machine is healthy.

The first KPI is Same-Store-Sales Growth (SSSG). With thousands of stores, Lenskart can flatter its top line for years simply by opening new ones. SSSG strips that away and asks the honest question: are the stores that already existed last year selling more this year? It's the truest read on whether the core retail proposition is strengthening or quietly decaying beneath the expansion. The second is the Gold membership renewal rate. The entire recurring-revenue thesis — the conversion of transactional eyewear into a sticky, Prime-like relationship — lives or dies on whether members renew. A high and rising renewal rate validates the lock-in; a sagging one would mean the membership is a discount giveaway rather than a retention engine. The third is consolidated EBITDA margin, the single cleanest measure of whether the expensive international expansion is actually converging toward the profitability of the Indian core. The whole financial story is "profitable India funds breakeven world until the world becomes profitable too" — consolidated EBITDA margin is the needle that tells you if that's happening. Three numbers. Watch those; let the rest be commentary.

Now the bear case, and it's a serious one. The first risk is franchise cannibalization and channel conflict. The same hybrid model that let Lenskart blanket India — company-owned stores alongside FOCO and FOFO franchises — contains a built-in tension. When Lenskart opens a company-owned store too close to an existing franchisee's territory, it can siphon that franchisee's sales, breeding resentment, disputes, and occasionally litigation; regional friction of exactly this kind has surfaced before. As the network densifies, managing the geometry of who-can-open-where without alienating the franchise partners whose capital fuels the expansion becomes a genuine operational and legal challenge. The second bear risk is lower-tier margin compression. Lenskart LITE's push into Tier 4 and Tier 5 India is great for reach, but small-town customers buy cheaper frames and smaller baskets. As the mix shifts toward these lower-ticket sales, average order value can drift down and pressure the rich retail-store economics that the BOGO model depends on. Growth in unit count is not the same as growth in profit, and the deeper Lenskart goes into price-sensitive India, the more that distinction matters.

And the bull case, which is genuinely large. Strip it to one sentence: Lenskart has built a vertically integrated, automated, low-cost eyewear manufacturing-and-retail machine in the country with the lowest costs, and the rest of the world's eyewear is made and sold at structurally higher margins. The Hyderabad export factory, the Owndays platform across Asia, the Meller beachhead in Europe, the Middle East ambitions — these are all expressions of one idea: take the Indian-built cost engine and point it at markets where eyewear has always been more expensive to make and sell. If Lenskart can export even a fraction of its 41% domestic organized-market dominance into Southeast Asia, the Middle East, and beyond, the company stops being an Indian eyewear champion and becomes a global eyewear platform — the kind of generational, $20-billion-plus enterprise that vertical integration occasionally produces when it's executed for a decade without flinching. The bull case isn't that India keeps growing. It's that the whole world starts buying glasses made in Bhiwadi and Hyderabad.

Which raises the largest question of all — not whether Lenskart wins the eyewear market it knows, but what happens when the definition of "eyewear" itself starts to change.

XI. Epilogue & Surprises

Step back from the financials and the frameworks, and the deepest lesson of the Lenskart story is almost old-fashioned. In an era that worshipped the asset-light, capital-efficient, software-only business model, Lenskart's founders concluded that the only way to actually win their market was to do the hard thing — own the factory, own the stores, own the prescription data, own the eye test on the back of a motorcycle. Vertical integration is brutally difficult to execute; it ties up capital, demands operational excellence across manufacturing and retail and logistics simultaneously, and punishes mistakes harshly. But once it's built and scaled, it produces an economic moat that a slick storefront never can. And the second lesson sits right beside it: in emerging markets, for any consumer product with a physical or clinical step in the middle of the purchase, the "phygital" omnichannel model isn't one option among many — it's the mandatory architecture. The customer needs to touch the product and trust the seller, and no amount of digital polish substitutes for a store and a technician.

Then there's the surprise lurking at the edge of the story — the optionality nobody is fully pricing. The world is sliding toward smart glasses, augmented-reality eyewear, and computerized lenses; the face is becoming the next computing surface. Ask who is positioned to distribute that future to hundreds of millions of people, and the answer is uncomfortable for the technology giants: it's the company that already has thousands of stores where customers come to get their faces measured, already holds tens of millions of precise 3D facial maps and prescriptions, already runs the eye tests and the fitting and the after-sales relationship. A smart-glasses maker can build the chip; it cannot easily build the physical channel that puts a correctly-fitted, prescription-accurate device on a customer's face across a continent. Lenskart's unglamorous infrastructure — the stores, the optometrists, the face data, the factories — could turn out to be the default last-mile for an entire category of wearable computing it didn't set out to build.

For now, the verdict the public market is rendering shows up in the ticker. After a wobbly debut in November 2025 — the stock actually listed at a slight discount to its ₹402 issue price before finding its feet — LENSKART.NS traded around ₹510 by mid-2026, valuing the company north of $6 billion and reflecting an investor base that has chosen to see Lenskart not as a retailer but as a profitable, high-growth, vertically integrated consumer-technology platform.1212 Whether it grows into the $10-billion-and-beyond ambitions encoded in its founders' ESOP hurdles, or stumbles on franchise conflict, margin compression, or the sheer difficulty of exporting its model, is the story of the next decade. What's already settled is the lesson of the last one: the company that built the physical infrastructure of a continent's vision did it the hard way, on purpose — and that, far more than any website, is why it's worth what it's worth.

References

-

SoftBank-backed Lenskart wobbles after volatile debut despite oversubscribed IPO — CNBC, 2025-11-10 ↩↩↩

-

Lenskart Solutions Ltd share price & key insights — Screener.in ↩↩↩↩↩↩

-

Lenskart acquires majority stake in eyewear brand Owndays in $400 million deal — TechCrunch, 2022-06-30 ↩↩↩↩

-

Lenskart company profile and history — Lenskart Investor Relations ↩↩

-

How Peyush Bansal Built Lenskart Into An Eyewear Behemoth — Fortune India ↩

-

Lenskart Franchise Models: FOCO vs FOFO Expansion — Franchise India ↩↩

-

Lenskart to Build World's Largest Eyewear Manufacturing Plant in Hyderabad — Asia Manufacturing Review ↩↩

-

Telangana to Host Lenskart's Biggest Manufacturing Unit with ₹1,500 Crore Funding — Elets CIO ↩

-

Lenskart acquires majority stake in Japanese eyewear brand Owndays — Business Standard, 2022-06-30 ↩

-

Why $4.5B Lenskart spent $400M to buy Japanese eyewear brand Owndays — The Ken ↩

-

Lenskart acquires computer vision startup Tango Eye — Business Standard, 2023-10-30 ↩

-

Lenskart acquires AI-driven computer vision startup Tango Eye — YourStory, 2023-10 ↩

-

Lenskart FY25 Revenue, Profit, Market Share & Growth Breakdown — Kotak Neo ↩↩↩

-

Aqualens Contact Lens Growth and Subscription Playbook — The Strategy Story ↩↩

-

Promoter Group Shareholding & Founder Compensation Structure — YourStory ↩↩↩↩

-

Lenskart IPO: Founder Peyush Bansal Buys Back Shares at Discount Before Listing — Angel One ↩

-

Peyush Bansal buys 2.5% stake in Lenskart at 90% discount ahead of IPO — Indian Startup News ↩↩

-

Lenskart share price: Stock lists at nearly 2% discount on NSE — Upstox, 2025-11-10 ↩↩

-

Titan Company Annual Report & Eyewear Division Financials — Titan Company ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube