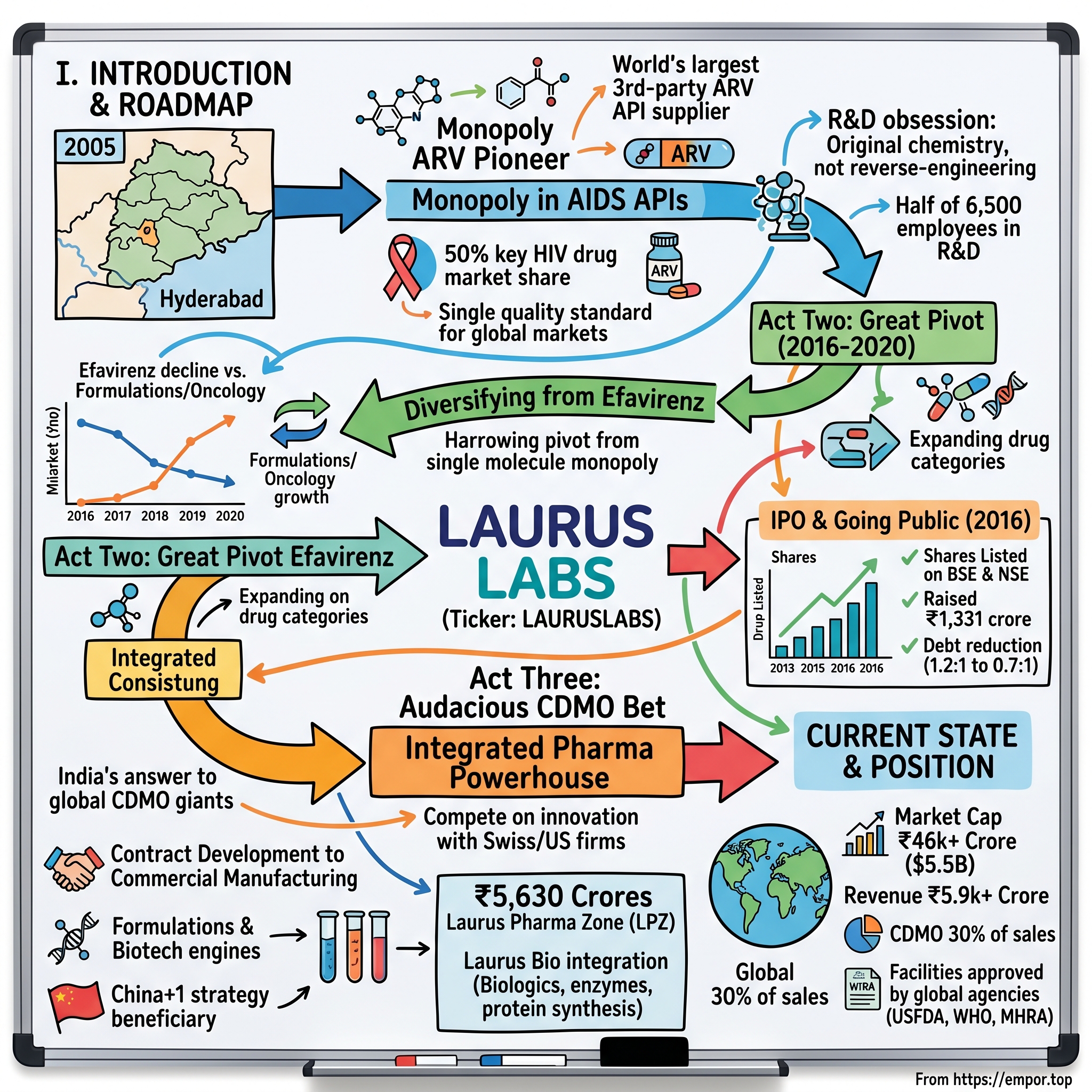

Laurus Labs: From ARV Pioneer to Integrated Pharma Powerhouse

I. Introduction & Episode Roadmap

Picture this: It's 2005 in Hyderabad, the pharmaceutical capital of India. A former CTO who just watched his previous company get acquired for $550 million decides to bet everything on a radical idea—build a pharma company that treats African AIDS patients with the same quality standards as American cancer patients. No shortcuts. No "good enough for emerging markets." Just world-class chemistry at prices the developing world could afford.

That man was Dr. Satyanarayana Chava, and his company, Laurus Labs, would go on to become the world's largest third-party supplier of antiretroviral APIs, commanding 50% of the global market for key HIV drugs. Today, with a market cap north of ₹46,000 crore ($5.5 billion), Laurus has transformed from that single-minded API startup into an integrated pharmaceutical powerhouse spanning drug discovery to commercial manufacturing.

But here's what makes this story remarkable: Unlike the typical Indian pharma playbook of reverse-engineering expired patents and racing to the bottom on price, Laurus built its empire on original chemistry. Half of its 6,500 employees work in R&D. The company holds over 300 patents. And in an industry where "Made in India" often meant "cheaper alternative," Laurus supplies ingredients to 9 of the 10 largest generic pharmaceutical companies globally.

This is a story of three distinct acts. Act One: How a chemistry-obsessed founder built a monopoly in AIDS drugs by solving synthesis problems others couldn't crack. Act Two: The harrowing pivot away from that very monopoly when the market shifted overnight. Act Three: The audacious bet on becoming India's answer to the global CDMO giants, competing not with Chinese manufacturers on price, but with Swiss and American firms on innovation.

Along the way, we'll explore how Laurus navigated the labyrinth of global health funding, why private equity giants like Warburg Pincus and Eight Roads backed a company dependent on donor-funded programs, and how a firm that once derived 50% of revenue from a single molecule diversified into one of India's most promising contract development stories.

We'll also wrestle with the fundamental tension at the heart of Laurus: Can a company built on serving humanity's most vulnerable populations generate venture-scale returns? And what happens when your biggest customer isn't a corporation, but the collective conscience of the developed world?

II. The Founder's Journey & Early Days (2005–2010)

The conference room at Matrix Laboratories buzzed with celebration in early 2006. Mylan, the American generic giant, had just agreed to acquire the company for $736 million—one of the largest pharma deals in Indian history. For most executives, this would be the crowning achievement of a career. But Dr. Satyanarayana Chava, Matrix's Chief Technology Officer, saw it differently. As his colleagues toasted with champagne, Chava was already sketching molecular structures on a napkin, plotting his next move.

"I realized during the acquisition that we were selling molecules, not solving problems," Chava would later recall. The Indian pharma industry had perfected the art of the fast follower—wait for patents to expire, reverse-engineer the synthesis, race to market. It was profitable, predictable, and utterly uninspiring for a chemist who'd spent years pushing the boundaries of what was possible in a lab.

By November 2005, even before the Matrix deal closed, Chava had incorporated Laurus Labs with his own capital—no venture funding, no corporate backing, just personal savings and an almost messianic belief that Indian pharma could compete on innovation, not just cost. The name itself was revealing: Laurus, from the Latin for laurel, the crown of victory in ancient Rome. This wasn't meant to be another contract manufacturer. This was meant to be a champion.

The timing seemed almost suicidal. The API (Active Pharmaceutical Ingredient) market was brutally commoditized. Chinese manufacturers were dumping products at prices that barely covered raw materials. Indian players were locked in a race to the bottom. Why would anyone start an API company in 2005?

But Chava saw something others missed. The global fight against HIV/AIDS was at an inflection point. The World Health Organization had just launched its "3 by 5" initiative—getting 3 million people on antiretroviral therapy by 2005. PEPFAR, the U.S. President's Emergency Plan for AIDS Relief, was deploying billions in funding. The Clinton Foundation was negotiating bulk purchases. The demand for affordable ARVs was about to explode, but the chemistry was wickedly complex.

Take Efavirenz, the backbone of first-line HIV therapy. The standard synthesis required expensive catalysts, generated toxic waste, and yielded barely 60% of theoretical output. Most Indian firms looked at it and saw a low-margin commodity. Chava saw a chemistry puzzle worth solving.

He assembled a team that would become legendary in Indian pharma circles—not MBAs or sales executives, but hardcore synthetic chemists recruited from the country's top institutes. The early Laurus office in Hyderabad's IDA Jeedimetla looked more like an academic research lab than a commercial operation. Whiteboards covered in reaction mechanisms. Dog-eared copies of the Journal of Organic Chemistry. And a culture that was downright peculiar by Indian corporate standards.

"From day one, we decided on a single quality standard," explains a former early employee. "Whether the API was going to Switzerland or Swaziland, it would be manufactured to the same specifications." This wasn't just idealism—it was strategy. While competitors maintained different quality tiers (premium for regulated markets, "good enough" for Africa), Laurus bet that eventually, the world would demand uniform quality. They were building for a future that hadn't arrived yet.

The R&D intensity was almost absurd for a startup. By 2007, with barely 100 employees, 55 were working in research. The company was filing patents not on the molecules themselves—those were generic—but on novel synthetic routes that could slash production costs by 30-40%. One early breakthrough: a new Efavirenz synthesis that eliminated two steps, improved yield to 85%, and reduced solvent use by half.

Corporate governance was another anomaly. While most Indian pharma companies were run as extended family businesses, Chava instituted independent directors, audit committees, and transparency standards from the start. "We knew we'd need institutional capital eventually," he'd say. "Better to build the governance before you need it than scramble when investors show up."

By 2010, Laurus had achieved something remarkable: Despite being just five years old, it had become a critical supplier to the global ARV supply chain. The company wasn't the largest—that was still the domain of Cipla and Aurobindo. But for certain key intermediates, especially for Efavirenz, Laurus had developed chemistry so elegant, so cost-effective, that even competitors were buying from them.

Revenue had grown from essentially zero to over ₹400 crore. The company was profitable, cash-flow positive, and had attracted attention from an unexpected source: Eight Roads Ventures, Fidelity's venture capital arm, which saw in Laurus something that transcended the typical Indian pharma story. This wasn't just about making drugs cheaper—it was about reimagining how drugs could be made.

III. The ARV Dominance Story (2010–2016)

The email arrived at 3 AM Hyderabad time in March 2011. The Clinton Health Access Initiative needed an urgent quote for 10 million doses of Efavirenz. Not in six months. Not in three months. In six weeks. The global ARV supply chain was in crisis—a major supplier had failed FDA inspection, creating a massive shortage just as African treatment programs were scaling up.

Dr. Chava called an emergency meeting at 6 AM. "This is our moment," he told his team. While competitors scrambled to expand capacity—a process that typically took 12-18 months in pharma—Laurus had a secret weapon. They'd been quietly building modular production units, designed to scale rapidly. Think of it as the pharma equivalent of cloud computing: instead of one massive plant, multiple smaller units that could be brought online as needed.

Within 72 hours, Laurus had committed to the order. Within six weeks, they delivered. That single contract established Laurus as the go-to crisis solver in the ARV supply chain. When things went wrong—and in the chaotic world of global health procurement, things always went wrong—Laurus could deliver. Eight Roads' investment in 2011 marked a turning point. The Fidelity-backed venture firm wasn't looking for another generic pharma play—they'd seen hundreds of those. What intrigued them was Laurus's chemistry-first approach. "Most Indian pharma companies are marketing organizations that happen to manufacture," an Eight Roads partner would later observe. "Laurus was a chemistry company that happened to sell drugs."

The numbers by 2014 were staggering. Laurus had built dominant market share through novel chemistry which made for cheaper, more scalable production processes. Efavirenz API, that molecule Chava had obsessed over since the early days, now constituted 50% of company revenues. The company commanded a 50% global market share in Efavirenz API. To put that in perspective: half of all HIV patients globally taking Efavirenz-based regimens were consuming a drug with Laurus ingredients.

But here's what made this dominance remarkable—and precarious. The entire global ARV market was essentially a monopsony, with purchasing dominated by a handful of organizations: PEPFAR, the Global Fund, Clinton Health Access Initiative, and Médecins Sans Frontières. These weren't traditional customers optimizing for features or brand. They had one metric: cost per patient-year of treatment. Every dollar saved meant another patient who could access life-saving therapy.

Laurus thrived in this environment because they'd cracked the code on process chemistry. Take their Tenofovir synthesis, another key ARV. The standard process required a particularly nasty phosphorylation step that generated significant hazardous waste. Laurus developed an enzymatic alternative that not only eliminated the waste but improved yield by 20%. The cost savings were passed directly to buyers, making Laurus the preferred supplier for cost-conscious global health programs. In 2014, Warburg Pincus made a landmark investment, acquiring a 32% stake for approximately ₹550 crore. Warburg acquired a minority stake in Laurus Labs for about Rs 550 crore, picking up a 32.29 per cent effective stake. The private equity giant's investment thesis was crystal clear: "Through a positive combination of technical depth, relentless execution and highest level of corporate governance, the team at Laurus Labs has built a market-leading pharmaceutical company in a short span of time".

What Warburg saw that others missed was the defensibility of Laurus's position. Yes, the ARV market was concentrated and donor-dependent. But Laurus had built such deep process expertise that switching costs for buyers were astronomical. When you're supplying APIs for drugs keeping millions alive, you don't switch suppliers to save 2%. The regulatory re-qualification alone would take years.

By 2015, Laurus was supplying APIs to 9 of the 10 largest generic pharmaceutical companies globally. Names like Teva, Mylan, and Cipla were dependent on Laurus for their ARV formulations. The company had become the Intel Inside of the global AIDS treatment ecosystem—invisible to patients but indispensable to the industry.

The manufacturing footprint had expanded dramatically. Eight plants across Visakhapatnam, Hyderabad, and Bangalore, all built to global regulatory standards. FDA inspections came and went without major observations—remarkable for an Indian manufacturer in an era when regulatory actions were decimating competitors.

But beneath the success, a strategic tension was building. Efavirenz, that wonder molecule that built the empire, was showing its age. Newer ARVs like Dolutegravir promised better efficacy with fewer side effects. The WHO was preparing to shift its treatment guidelines. When that happened, demand for Efavirenz would crater almost overnight.

"We knew by 2014 that we had maybe 24 months before the market shifted," a senior executive would later reveal. "The question wasn't if, but when. And more importantly, what next?"

The answer to that question would transform Laurus from an API supplier into something far more ambitious. But first, they needed capital. Public market capital. It was time for an IPO.

IV. The IPO & Going Public (2016)

The roadshow kicked off on a humid Mumbai morning in November 2016. Dr. Chava, typically more comfortable in a lab coat than a suit, stood before a room of skeptical fund managers at the Taj Mahal Palace hotel. The first question came fast: "You derive 50% of revenue from one molecule that's about to be obsoleted. Why should we invest?"

It was the elephant in every room, the question that had dogged the IPO preparations for months. Laurus was attempting something audacious—going public at the exact moment its core product faced extinction. The bankers had suggested waiting, pivoting first, then approaching markets. Chava disagreed. "Markets reward transparency," he'd argued. "We'll tell them exactly what we're doing. "The IPO structure was aggressive: bidding from December 6, 2016 to December 8, 2016, priced at ₹428 per share (with a price band of ₹426-428), raising ₹300 crore fresh issue and ₹1,031 crore offer for sale, total ₹1,331 crore. The offer for sale component was telling—existing investors, including Warburg Pincus and Eight Roads, were taking money off the table. Aptuit, an early investor, was exiting completely.

At IPO, Laurus presented three distinct business lines. Generic APIs dominated at 90% of revenue, with ARVs alone accounting for 61%. Generic FDFs (Finished Dosage Forms) were nascent but growing. And Synthesis—their contract development and manufacturing services—represented the future, though it contributed less than 5% of revenue at the time.

The roadshow pitch was audacious in its honesty. "We know Efavirenz is going away," Chava would tell investors. "The WHO is shifting to Dolutegravir-based regimens. Our Efavirenz revenues will decline 40-50% over the next two years. But here's what you're really buying: the capability to do complex chemistry at scale. Today it's ARVs. Tomorrow it's oncology. Eventually, it's proprietary molecules for Big Pharma."

The market was skeptical but intrigued. The subscription data told the story: QIBs (Qualified Institutional Buyers) subscribed 100% by day two—they understood the transformation thesis. Retail investors were more cautious, subscribing less than 2x. The grey market premium was modest, suggesting expectations were measured.

The shares listed on BSE and NSE on December 19, 2016. The opening trade was at ₹442, a modest 3.3% premium to the issue price. Not a blockbuster debut, but solid enough. More importantly, it gave Laurus the currency—both literal and figurative—to execute its transformation.

The IPO proceeds were immediately deployed. ₹225 crore went to debt reduction, bringing the debt-to-equity ratio from 1.2:1 to 0.7:1. The rest funded capacity expansion, particularly in the formulations business. Laurus was now a public company, with quarterly earnings calls, analyst scrutiny, and the relentless pressure to deliver growth even as its core product faced obsolescence.

"Going public during a crisis is actually liberating," Chava would later reflect. "There's no room for complacency. The market knows your biggest product is dying. Every quarter, you have to show them the future is being built."

And build they did. But the transformation that followed would test every assumption about what an Indian pharma company could become.

V. The Great Transformation: From API to Integrated Pharma (2016–2020)

The numbers on the whiteboard in Laurus's strategy room in January 2017 were sobering. Efavirenz revenues: ₹1,100 crore in FY2016. Projected for FY2020: ₹400 crore. The WHO had officially recommended Dolutegravir as first-line therapy. Countries were switching their treatment protocols. The clock was ticking.

But here's what outsiders missed: Laurus had been preparing for this moment since 2014. While publicly they were the Efavirenz company, internally they'd been building capabilities across the pharmaceutical value chain. The transformation wouldn't just be about finding new molecules to replace Efavirenz—it would be about reimagining what kind of company Laurus could be.

The first pillar was formulations. Laurus Labs is a research-driven pharmaceutical and biotechnology company that recognized APIs were becoming commoditized. The real value—and margins—lay in finished dosage forms. But building a formulations business from scratch typically took a decade. Laurus needed to move faster.

Their approach was counterintuitive. Instead of building massive plants and hoping for orders, they started with small, flexible units designed for quick changeovers. Think of it as the pharmaceutical equivalent of lean manufacturing. A single line could produce ARVs one month, oncology drugs the next. The capital efficiency was remarkable—₹100 crore invested in formulations capacity could generate ₹300 crore in revenue, versus ₹150 crore for traditional API plants.

The formulations growth was explosive: from ₹5 crore in FY2019 to ₹825 crore in FY2021. This wasn't organic growth—this was a step function change. The key was leveraging existing customer relationships. Companies that bought Laurus APIs were offered an integrated solution: "We'll make the API and the finished tablet. One vendor, one quality standard, simplified supply chain."

The second pillar was diversification within APIs. As Efavirenz declined, Laurus doubled down on other complex molecules. Dolutegravir itself became a major product—ironic, given it was cannibalizing Efavirenz. But Laurus had learned from the Efavirenz experience. Instead of betting everything on one molecule, they built a portfolio: antiretrovirals, yes, but also oncology APIs, cardiovascular drugs, and Hepatitis C treatments.

The oncology bet was particularly strategic. These were high-potent APIs (HPAPIs) requiring specialized handling facilities and expertise. Most Indian companies avoided them—too complex, too capital-intensive, too risky. Laurus saw opportunity. They built one of India's largest HPAPI facilities, capable of handling compounds so potent that exposure to micrograms could be lethal.

"We realized that complexity is a moat," explained the head of strategy. "Anyone can make simple molecules. But when you need containment systems, specialized analytical methods, and deep process understanding, the field narrows dramatically."

The third pillar—and the most ambitious—was the CDMO (Contract Development and Manufacturing Organization) business. This wasn't just contract manufacturing of generics. This was partnering with innovator companies to develop and manufacture their proprietary molecules from clinical trials through commercial launch.

The CDMO opportunity was massive. Global pharma companies were increasingly outsourcing manufacturing, especially for complex small molecules. India had the talent and cost advantage, but most Indian companies lacked the quality systems and regulatory track record to win these contracts. Laurus had both.

By FY2020, the transformation was tangible. ARV API contribution had dropped from over 50% to 25% of revenues. The company had successfully navigated the Dolutegravir transition, with the new molecule more than offsetting Efavirenz declines. Total revenues had grown from ₹2,292 crore in FY2019 to ₹4,800 crore in FY2020, despite the Efavirenz headwind.

But the real achievement was margins. Gross margins expanded from 45% to over 50% as the product mix shifted toward higher-value formulations and CDMO services. The company that had once been dangerously dependent on a single molecule had become genuinely diversified.

The pandemic year of 2020 provided an unexpected catalyst. Supply chain disruptions exposed the vulnerability of single-source dependencies. Global pharma companies scrambled to diversify away from China. Laurus, with its expanded capacity and proven track record, was perfectly positioned. CDMO inquiries tripled. New projects were signed at unprecedented pace.

The transformation was complete. Or so it seemed. But Chava and his team were already planning the next evolution—one that would take Laurus beyond traditional pharmaceuticals into the cutting edge of biotechnology.

VI. The CDMO Revolution & New Growth Engines (2020–Present)

The conference call in March 2021 started like any other quarterly earnings discussion. Analysts asked about API pricing, formulation volumes, the usual metrics. Then Dr. Chava dropped a bombshell: "We're acquiring Richcore Lifesciences for ₹246 crore. We're entering biotechnology."

The silence on the line was palpable. Laurus, the small-molecule chemistry specialist, was buying a fermentation-based biotech company? It seemed like a radical departure. But for those who understood Chava's vision, it was the logical next step.

"The future of pharmaceuticals isn't just chemical synthesis," Chava explained to skeptical analysts. "It's biological manufacturing—enzymes, proteins, cell therapies. We can either watch that future happen or help build it. "Richcore, renamed to Laurus Bio after the ₹246.7 crore acquisition, wasn't just any biotech company. It had advanced R&D and manufacturing facilities developing biotech products critical for biological drugs manufacturing. More importantly, it brought fermentation capabilities—a completely different technology platform from chemical synthesis.

"Chemistry and biology converging," as the Richcore founder Subramani Ramachandrappa put it. The synergies were immediate. Laurus's chemical expertise could be combined with Richcore's biological capabilities to create novel manufacturing processes. Think of it as building bridges between two scientific worlds that had traditionally operated in silos.

But the real story of 2020-2024 was the CDMO explosion. Laurus offers integrated CMO and CDMO services to Global Innovators from Clinical phase drug development to commercial manufacturing. The numbers were staggering: CDMO segment reaching 19% of revenue in FY22, with 50 ongoing projects and 4 Big Pharma clients. By Q1 FY26, CDMO reached 30% of sales.

The transformation wasn't just about adding capabilities—it was about changing the entire value proposition. Instead of competing on cost with Chinese manufacturers, Laurus was now competing on innovation with Western CDMOs. The margin story reflected this: gross margins upgraded from 45% to 55-60%.

"We stopped thinking of ourselves as an Indian company competing globally," explained the head of CDMO business. "We became a global company that happened to be based in India."

The client list read like a who's who of Big Pharma. Names weren't disclosed for confidentiality, but the nature of projects spoke volumes: Phase III clinical manufacturing for an oncology blockbuster, commercial production of a complex cardiovascular drug, development of a novel synthesis for a CNS molecule. These weren't generic projects—these were proprietary molecules with patent protection and pricing power.

The capex commitment was massive: ₹2,800 crore investment over FY22-24. New facilities were coming online at breakneck pace. A state-of-the-art CDMO facility in Vizag. An expanded fermentation unit for Laurus Bio. And most ambitiously, a gene therapy and ADC (Antibody-Drug Conjugate) facility in Hyderabad—technologies at the absolute cutting edge of pharmaceutical innovation. The biotechnology expansion continued to accelerate. Laurus Bio's CDMO services now span from cell line development to protein synthesis, including cutting-edge areas like antibody-drug conjugates (ADCs), mRNA vaccines, and plasmid DNA. The company was building capabilities not just for today's drugs but for tomorrow's—gene therapies, CAR-T cell treatments, technologies that were still in clinical trials but represented the future of medicine.

The global context was crucial. The pandemic had exposed the vulnerability of pharmaceutical supply chains concentrated in China. The U.S. BIOSECURE Act was pushing American companies to diversify suppliers. Europe was implementing similar policies. India, with its strong regulatory track record and cost advantages, was perfectly positioned—and Laurus, with its integrated capabilities from development to commercial manufacturing, was perhaps the best-positioned Indian company.

"We're not competing with other Indian CDMOs anymore," Chava told investors in 2023. "Our competition is Lonza, Catalent, Samsung Biologics. And on certain parameters—speed, flexibility, cost—we're winning."

The evidence was in the numbers. By Q1 FY26, CDMO had reached 30% of sales. The company was working on over 70 active projects, including 10 commercial molecules. Client retention was over 95%. And most tellingly, average project size had grown from $2 million to over $10 million, indicating deeper, more strategic partnerships.

The capex continued: a new R&D facility at IKP Knowledge Park in Hyderabad operational in 2024, microbial fermentation facility expansion in Vizag, and investments in continuous flow technologies and green chemistry platforms. Each investment wasn't just about capacity—it was about capability, building the infrastructure for the next generation of pharmaceutical manufacturing.

VII. Current State & Market Position

The analyst conference room at the Trident Hotel in Mumbai was packed in July 2024. Laurus had just announced Q1 FY26 results: 31% revenue growth, CDMO at 30% of sales, gross margins at 59%. But the number that caught everyone's attention was different: 531.77 acres. The Government of Andhra Pradesh has allotted 531.77 acres of land in IP Rambilli Phase-II of Anakapalli District to Laurus for establishment of Laurus Pharma Zone (LPZ). The Company has projected ₹5,630 Crores of investment and to provide employment to 6,350 people in three phases over a period of eight years. With this allotment, the Company has secured an important component for future expansion of its business i.e., land parcel.

This wasn't just a land allocation. It was validation of Laurus's transformation from a single-product API company to a pharmaceutical powerhouse worthy of its own industrial zone. The scale was breathtaking—531 acres is larger than many industrial parks that house dozens of companies. Laurus would have it all to itself.

The current numbers tell the story of a company that has successfully navigated one of the most difficult pivots in pharmaceutical history. Market cap of ₹46,476 crore, revenue of ₹5,929 crore, profit of ₹507 crore. But beneath these headline numbers lies a more complex narrative.

Generic API remains 46% of revenue in 9M FY25, with the company maintaining its position as the world's leading third-party supplier of antiretroviral APIs. Its portfolio includes antiretrovirals, oncology, steroids, hormones, and cardiovascular APIs, serving global generic pharmaceutical companies.

The scale of operations has reached global standards. Laurus employs 6500+ people, including around 1050+ scientists at more than 11 facilities approved by global agencies USFDA, WHO-Geneva, Japan-PDMA, UK-MHRA, EMA, TGA etc. The regulatory track record is particularly impressive—multiple FDA inspections with zero or minimal observations, a rarity for Indian pharmaceutical companies.

But the real story is in the business mix evolution. CDMO, which barely existed five years ago, now represents 30% of sales with margins substantially higher than the traditional API business. The formulations business, growing at 50% year-over-year, is becoming a meaningful contributor. And Laurus Bio, though still small, represents optionality on the future of biotechnology.

The global context remains favorable. The pharmaceutical industry continues to outsource more manufacturing, driven by cost pressures and the need for specialized capabilities. The China+1 strategy has accelerated post-pandemic, with Western companies actively seeking to diversify supply chains. India, with its established pharmaceutical ecosystem and regulatory credibility, is the natural beneficiary.

Yet challenges remain. Company has a low return on equity of 10.5% over last 3 years—a reflection of the heavy capex requirements and the transition period as new businesses scale. The ARV market, while stable, faces ongoing pricing pressure and dependency on donor funding that can be unpredictable.

Competition is intensifying. Other Indian companies like Divi's, Syngene, and Biocon Biologics are expanding CDMO capabilities. Chinese companies, despite geopolitical headwinds, remain formidable competitors on cost. And the entry barriers that once protected Laurus's ARV franchise are less relevant in the CDMO space where relationships and track record matter more than process chemistry.

The management challenge is equally daunting. Running an integrated pharmaceutical company spanning APIs, formulations, CDMO services, and biotechnology requires different skill sets, cultures, and operational models. The company that once prided itself on focus—"we do one thing exceptionally well"—now needs to excel at multiple things simultaneously.

"We're not the same company we were five years ago," Chava acknowledged in a recent investor call. "The complexity has increased exponentially. But so has the opportunity."

VIII. Playbook: Business & Investing Lessons

The Laurus story offers a masterclass in industrial transformation, but the lessons extend far beyond pharmaceuticals. This is fundamentally about how a founder-led company in a commoditized industry can create sustainable competitive advantages through technical excellence and strategic pivots.

The Power of Founder-Led Execution in Complex Industries

Dr. Chava's journey illuminates a critical truth: in industries where technical depth matters, founder-CEOs with domain expertise possess an almost unfair advantage. Unlike professional managers who might optimize for quarterly earnings, Chava could make decade-long bets on chemistry platforms because he understood the science intimately. When the Efavirenz market was collapsing, he didn't panic or financial-engineer his way out—he went back to the lab and built new capabilities.

This isn't just about having skin in the game. It's about having the technical conviction to see opportunities where others see only risk. When Laurus acquired Richcore for biotechnology, most investors were skeptical. A chemical synthesis company buying a fermentation platform? But Chava saw what they didn't: the convergence of small and large molecule manufacturing, the synergies in quality systems, the shared customer base. That's the kind of insight you only get from decades in the trenches.

R&D as Competitive Moat

With around 1050+ scientists at more than 11 facilities, Laurus has built something rare in Indian pharma: genuine research capability, not just reverse-engineering expertise. But here's the counterintuitive lesson: the moat isn't in the R&D spend itself (4-5% of revenues, respectable but not exceptional). It's in the culture of technical problem-solving that permeates the entire organization.

When a customer comes with a complex molecule, Laurus doesn't just quote a price. They redesign the synthesis, eliminate steps, improve yields, reduce environmental impact. This consultative approach transforms vendor relationships into partnerships. It's why client retention exceeds 95% and why average project values have quintupled.

The real insight: in commoditized industries, the only sustainable differentiation is continuous innovation. Not moonshot innovation—incremental, practical, customer-focused innovation that compounds over time.

Managing Concentration Risk: The ARV Dependency Journey

The Efavirenz story is a case study in both the perils and opportunities of concentration risk. At its peak, one molecule generated 50% of revenues. Most MBA programs would cite this as a textbook failure of diversification. Yet it was precisely this concentration that funded Laurus's transformation.

The lesson isn't to avoid concentration—it's to use periods of dominance to fund diversification. Laurus didn't wait for the Efavirenz decline to start building new capabilities. They began investing in formulations and CDMO while Efavirenz was still growing. The cash flow from the monopoly product funded the experiments that would eventually replace it.

But there's a deeper insight here about market dynamics. In Winner-Take-All markets (which many B2B markets are), it's often better to dominate a niche than to be subscale in multiple segments. Laurus's Efavirenz dominance gave them economies of scale, customer relationships, and credibility that they could leverage into adjacent areas.

Quality as Non-Negotiable

The "single quality standard" philosophy—same specifications whether selling to Switzerland or Swaziland—seemed economically irrational in 2005. Why over-engineer for price-sensitive emerging markets? But this decision proved prescient in multiple ways.

First, it simplified operations dramatically. No separate production lines, no inventory complexity, no risk of mix-ups. Second, it built trust with global health organizations who knew Laurus wouldn't compromise quality for African patients. Third, and most importantly, it positioned Laurus perfectly when regulatory standards globally converged upward.

The broader lesson: in regulated industries, racing to the top on quality is often more profitable long-term than racing to the bottom on price. Quality is a platform that enables everything else—customer trust, regulatory approvals, premium pricing, market access.

Capital Allocation in Pharma

The ₹2,800 crore capex commitment over FY22-24 represents a massive bet on manufacturing capacity. In an industry increasingly moving to asset-light models, why is Laurus doubling down on steel and concrete?

The answer reveals sophisticated thinking about competitive dynamics. In CDMO, customers aren't just buying capacity—they're buying reliability, confidentiality, and speed. Having dedicated assets means Laurus can guarantee supply, protect intellectual property, and scale rapidly. The capital intensity that might seem like a disadvantage is actually a barrier to entry.

But notice what Laurus didn't do: they didn't build massive, single-purpose plants. Instead, they built modular, flexible facilities that can be reconfigured as demand shifts. This is real options theory applied to industrial strategy—pay a premium for flexibility because the value of being able to pivot exceeds the cost of efficiency loss.

The CDMO Opportunity: Riding the China+1 Wave

The geopolitical tailwinds are obvious, but Laurus's CDMO strategy reveals nuanced understanding of global pharmaceutical dynamics. They're not trying to compete with Chinese manufacturers on cost for simple molecules. Instead, they're targeting complex chemistries, regulated markets, and proprietary molecules where IP protection and regulatory compliance matter more than absolute cost.

The insight: in global supply chains, the winner isn't always the cheapest—it's the most reliable. Laurus's investment in quality systems, regulatory affairs, and customer relationships is building switching costs that transcend price competition.

Navigating Regulatory Complexity

With operations spanning multiple geographies and therapeutic areas, Laurus faces a regulatory maze that would paralyze most companies. FDA, EMA, WHO, PMDA—each with different standards, inspection protocols, and documentation requirements. How do you manage this without drowning in compliance costs?

Laurus's approach: treat regulatory excellence as a revenue driver, not a cost center. Every successful inspection is a sales tool. Every approval is a competitive moat. The company that can navigate regulatory complexity faster and more reliably can charge premium prices and win more business.

The broader principle: in highly regulated industries, regulatory capability is as important as technical capability. It's not enough to make great products—you need to prove they're great, repeatedly, to skeptical regulators worldwide.

IX. Analysis & Bear vs. Bull Case

The investment case for Laurus Labs hinges on a fundamental question: Is this a cyclical recovery story in a structurally challenged industry, or a genuine transformation into a higher-quality business model? The answer determines whether the stock's 98% run-up over the past year is the beginning of a multi-year rerating or a peak to sell into.

Bull Case: The Structural Transformation Thesis

The bulls see Laurus as an Indian Lonza in the making—a world-class CDMO player that happens to be based in India rather than an Indian company trying to go global. The evidence is compelling.

First, the CDMO momentum is undeniable. In Q1 FY26, Laurus Labs CDMO revenue more than doubled year-on-year to Rs 522 crore, driven by a 130% increase in small molecules revenue. This isn't just cyclical recovery—it's structural share gain in a market growing at 7-8% annually. With gross margins at 59%, these aren't commodity contracts but strategic partnerships with pricing power.

The addressable market is massive and expanding. The global CDMO market, valued at $217 billion, is expected to grow to $350 billion by 2030. India's share, currently at 5%, could double as Western companies diversify from China. If Laurus captures even a tiny slice of this incremental opportunity, revenues could triple.

The regulatory track record provides a powerful moat. The USFDA conducted the inspection from 9 September 2024 to 13 September 2024. The inspection concluded with zero 483 observations by the US drug regulator. Laurus Labs' API manufacturing facility, located at DS-1, IKP Knowledge Park, Genome Valley, Shameerpet, Telangana is instrumental in developing active pharmaceutical ingredients. In an industry where a single FDA warning letter can destroy years of business development, Laurus's clean track record is gold.

The diversification is finally bearing fruit. ARV dependency, once an existential risk, is now manageable at 25% of revenues. The formulations business is scaling rapidly with 50% growth. Laurus Bio, while nascent, provides optionality on the $50 billion biologics CDMO market. This isn't a one-trick pony anymore—it's a diversified pharmaceutical platform.

Management execution has been exceptional. They called the Efavirenz decline correctly, pivoted successfully, and are now capturing the CDMO opportunity. The capital allocation has been disciplined—no expensive acquisitions, no unrelated diversification, just steady investment in core capabilities. With the founder still at the helm and deeply invested, alignment with shareholders is clear.

The valuation remains reasonable despite the recent run-up. At 10.4x book value and with ROE poised to expand as new capacity comes online, Laurus trades at a discount to global CDMO peers like Lonza (15x book) and Catalent (12x book). As the business mix shifts toward higher-margin CDMO and formulations, multiple expansion seems likely.

Bear Case: The Execution Risk Scenario

The bears see a company juggling too many balls, with execution risk mounting as complexity increases.

The low return on equity of 10.5% over last 3 years is concerning. Despite massive capex and operational improvements, the company isn't generating returns that exceed its cost of capital. This suggests either structural challenges in the business model or execution issues that management hasn't acknowledged.

The CDMO business, while growing, lacks visibility. Unlike established players with multi-year contracts and transparent pipelines, Laurus provides limited disclosure on project duration, customer concentration, or pipeline conversion. The 130% growth could be from a low base rather than sustainable momentum. What happens when these projects complete? Is there enough pipeline to sustain growth?

Competition is intensifying everywhere. In APIs, Chinese companies are regaining share as customers balance supply chain diversification with cost pressures. In CDMO, every Indian pharma company is chasing the same opportunity—Divi's, Syngene, Piramal, Jubilant. In formulations, Laurus lacks the scale and distribution to compete with established players. Being subscale in multiple segments is a recipe for mediocrity.

The ARV franchise, while smaller as a percentage of revenue, remains vulnerable. ARV revenues advanced 17% to Rs 647 crore during the period under review, but this growth comes from a low base after years of decline. PEPFAR funding remains uncertain, with potential budget cuts under discussion in Washington. A sudden reduction in donor funding could impact 25% of revenues overnight.

The capex requirements are staggering. ₹5,630 crore for the new Pharma Zone, ongoing investments in biotechnology, new facilities for CDMO—the capital intensity shows no signs of abating. This will pressure returns for years, and any execution delays or cost overruns could destroy value. Meanwhile, competitors are adopting asset-light models that generate higher returns with less risk.

Laurus Bio remains unproven. The biotechnology bet, while strategically sound, is financially questionable. although the bio-segment saw a 33% decline in Q1 FY26 revenues. The fermentation platform requires different expertise, customers, and economics than small molecule chemistry. Success is far from assured, and the investment could prove a costly distraction.

The Verdict: Asymmetric Risk-Reward

The truth, as always, lies somewhere between the extremes. Laurus is neither the next Lonza nor a value trap. It's a company in transition, with genuine competitive advantages but significant execution challenges.

The bull case rests on CDMO becoming a sustained growth driver, margins expanding as mix improves, and management executing on the ambitious capex plan. If this happens, the stock could double from here as multiples rerate to global peers.

The bear case sees execution stumbles, competition eroding margins, and returns remaining suppressed by ongoing capex needs. In this scenario, the stock could correct 30-40% as growth disappoints and multiples compress.

For investors, the key monitorables are clear: CDMO revenue growth and margin trajectory, ROE improvement as new capacity comes online, successful FDA inspections for new facilities, and Laurus Bio achieving commercial scale. The next 12-18 months will determine whether this transformation story has legs or whether Laurus remains a perpetual "tomorrow" story.

X. The Future: What's Next for Laurus

Standing in the newly constructed R&D facility at IKP Knowledge Park in Hyderabad, you can feel the ambition. Scientists huddle over benchtops synthesizing molecules that won't reach patients for a decade. Engineers optimize continuous flow reactors that could revolutionize manufacturing economics. And in a corner, a small team works on something that would have seemed like science fiction just years ago: using artificial intelligence to predict synthesis routes.

This is Laurus Labs in 2025—no longer just executing on yesterday's molecules but inventing tomorrow's manufacturing. The company that built its fortune on ARVs is now positioning itself at the intersection of chemistry, biology, and computation. The question isn't whether Laurus can grow—it's whether it can become something fundamentally different: India's first truly innovative pharmaceutical company.

The Immediate Horizon: Execution, Execution, Execution

The next 24 months are about turning blueprints into reality. The 531-acre Pharma Zone isn't just another manufacturing site—it's intended to be an integrated pharmaceutical city. API plants feeding formulation units. Quality control labs serving multiple facilities. Warehouses with direct access to ports. The economics are compelling: vertical integration could improve gross margins by 500-1000 basis points while reducing working capital needs.

But the real game-changer is speed. In pharmaceuticals, time-to-market can determine whether a drug generates $1 billion or $100 million in revenues. By co-locating development and manufacturing, Laurus can compress timelines from years to months. A Big Pharma client needs to scale up a Phase III molecule? Laurus can go from kilograms to metric tons without changing sites, teams, or even time zones.

The CDMO pipeline is particularly exciting. While Laurus doesn't disclose specific molecules for confidentiality reasons, industry sources suggest they're working on several potential blockbusters in oncology and CNS. If even one of these molecules succeeds commercially, it could generate $50-100 million in annual revenues for Laurus—at 40%+ EBITDA margins.

The Biologics Wild Card

Laurus Bio represents the biggest swing for the fences. The microbial fermentation platform, while currently subscale, has potential applications that extend far beyond traditional pharmaceuticals. Sustainable chemicals using engineered bacteria. Novel food ingredients through precision fermentation. Industrial enzymes that could replace harsh chemical processes.

The CAR-T therapy development is even more audacious. The company is making strides in CAR-T therapies with NexCAR19, targeting cancer treatment through innovative cell therapy solutions. If successful, this would position Laurus at the absolute cutting edge of cancer treatment. The market opportunity is enormous—CAR-T therapies command prices exceeding $400,000 per treatment—but so are the technical and regulatory challenges.

The strategic logic is sound: as the line between small and large molecules blurs, companies need capabilities in both. A CDMO that can offer integrated solutions—small molecule API, biological drug substance, and finished formulation—has significant competitive advantages. But execution risk is high, and success is far from guaranteed.

AI and Automation: The Productivity Revolution

Less visible but potentially more impactful is Laurus's investment in artificial intelligence and automation. The company is deploying machine learning models to predict reaction outcomes, optimize process parameters, and identify potential impurities before they occur. Early results suggest 20-30% reduction in development timelines and 15-20% improvement in yields.

Automation is equally transformative. New facilities feature automated material handling, continuous manufacturing, and real-time quality monitoring. The goal isn't just cost reduction—it's consistency, safety, and speed. A fully automated plant can run 24/7 with minimal human intervention, reducing contamination risk and improving output quality.

This technological edge could prove decisive in winning CDMO contracts. When a Big Pharma company is choosing a manufacturing partner for a $5 billion drug, they care less about saving 10% on costs than ensuring 100% reliability. Laurus's investment in Industry 4.0 technologies positions them as a partner for the future, not just a low-cost alternative.

Geographic Expansion: Beyond India

While Laurus has subsidiaries in the U.S. and Europe, these are primarily sales offices. The next phase involves establishing physical presence in key markets. Not manufacturing—that remains in India for cost advantages—but development centers, regulatory affairs offices, and customer-facing laboratories.

The U.S. market is particularly critical. Despite being a major supplier to American companies, Laurus has limited direct presence. Establishing a U.S. innovation center would enable closer collaboration with biotech clients, faster regulatory submissions, and better understanding of market needs. It's the difference between being a vendor and being a partner.

China presents a different opportunity. Despite geopolitical tensions, China remains the world's second-largest pharmaceutical market. Laurus's strong regulatory track record and non-Chinese origin could position them as an attractive partner for multinational companies serving Chinese patients. It's contrarian, but potentially lucrative.

The Consolidation Play

As the Indian pharmaceutical industry matures, consolidation seems inevitable. Laurus, with its strong balance sheet and proven integration capabilities, could be an acquirer. The targets wouldn't be large generic companies—that's not Laurus's game. Instead, look for specialized capabilities: a peptide manufacturer, an ADC specialist, a cell therapy platform.

The Richcore acquisition provides the template: buy technological capability, not just capacity. Integrate the science while maintaining entrepreneurial culture. Leverage Laurus's scale and regulatory expertise to accelerate growth. Done right, strategic acquisitions could add new platforms faster than organic development.

There's also the possibility that Laurus itself becomes an acquisition target. Global CDMOs are looking for emerging market presence. Big Pharma companies want to secure supply chains. At the right price, Laurus could provide instant access to India's pharmaceutical ecosystem. The founder's 27.6% stake makes hostile takeovers impossible, but a friendly deal at a premium isn't out of the question.

Key Milestones to Watch

For investors tracking the Laurus story, several upcoming milestones will prove critical:

-

Pharma Zone Development (2025-2029): Is construction on schedule and on budget? Early delays or cost overruns would signal execution challenges.

-

CDMO Client Wins (Ongoing): Announcements of new Big Pharma partnerships or expansions of existing relationships would validate the strategy.

-

Laurus Bio Scale-Up (2025-2026): Can the biotechnology division achieve $100 million in revenues? This would prove the platform's commercial viability.

-

Regulatory Inspections (Ongoing): Any FDA observations or warning letters would be devastating for the CDMO business.

-

ROE Improvement (FY26-27): As new capacity comes online, returns should expand. ROE reaching 15%+ would justify premium valuations.

-

Geographic Expansion (2026-2027): Establishment of U.S. or European innovation centers would signal evolution from manufacturer to innovation partner.

The Trillion-Rupee Question

Can Laurus Labs become India's answer to global CDMO giants? The opportunity certainly exists. India's pharmaceutical industry, already worth $50 billion, is expected to reach $130 billion by 2030. The CDMO segment could grow even faster as global companies diversify supply chains and Indian companies move up the value chain.

Laurus has the ingredients: technical expertise, regulatory track record, customer relationships, and ambitious management. But ingredients don't make a dish—execution does. The next five years will require flawless operational performance, strategic customer wins, and successful technology integration.

The biggest risk might be ambition itself. In trying to be everything—API supplier, formulation manufacturer, CDMO partner, biotechnology innovator—Laurus could lose focus and become mediocre at everything. The history of Indian pharma is littered with companies that tried to do too much too fast.

Yet there's something different about Laurus. Maybe it's the founder's technical background, the culture of innovation, or simply good timing. But this feels like a company at an inflection point, ready to transcend its origins and become something greater.

The next chapter of the Laurus story is being written in laboratories and boardrooms, in FDA inspection reports and customer contracts. It's a story about whether an Indian company can compete globally not just on cost but on innovation. Whether chemistry and biology can converge to create new therapeutic possibilities. Whether a company built on serving humanity's most vulnerable can also generate exceptional returns.

For investors, customers, and competitors, one thing is clear: Laurus Labs is no longer just an ARV supplier from Hyderabad. It's a pharmaceutical force with global ambitions and the capabilities to achieve them. The only question is how far they can go.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube