Landmark Cars: The Luxury Gatekeeper of India

I. Introduction: The Retailer to the Riches

Picture a Saturday afternoon in the leafy diplomatic enclave of Ahmedabad's Sindhu Bhavan Road. A glass-fronted showroom catches the harsh Gujarati sun, and parked just inside the polished granite floor is a Mercedes-Benz GLE, its three-pointed star glinting under custom lighting that costs more per square foot than the average Indian home. A family walks in. The father, a third-generation textile baron, has just sold a parcel of land in Gandhinagar for a sum that would have been unthinkable to his grandfather. He is not really shopping. He is, in the parlance of luxury retail, "manifesting." And the salesperson — wearing a sharp navy blazer with a small embroidered logo that reads "Group Landmark" — knows exactly what to do.

This is the front line of Indian premiumization. And the company that owns this floor, and roughly two hundred and ninety-six others like it across twenty-two Indian cities1, is the subject of today's deep dive.

Most automotive business stories obsess over the manufacturer. We talk about Elon Musk's tweets, about टाटा मोटर्स Tata Motors' EV strategy, about मारुति सुजुकी Maruti Suzuki's seemingly eternal grip on the Indian small-car market. What we rarely talk about is the boring, capital-intensive, fragmented, family-dominated business of actually selling those cars to actual people. Dealerships. Showrooms. Service bays. The unglamorous middle of the automotive value chain — the part where the OEM (Original Equipment Manufacturer) hands off the metal and someone else has to hand it to a customer, and then keep that customer happy for the next decade through warranty claims, oil changes, brake pad replacements, and the occasional warranty dispute over a malfunctioning infotainment screen.

In India, this middle layer is dominated by what bankers politely call "promoter-led entities" — meaning, family businesses run out of a back office above the showroom, often by the second or third generation of a Marwari, Gujarati, or Punjabi trading family. They are notoriously hard to consolidate. They are sentimental about their relationships with manufacturers. They mark up service hours the way Mumbai cab drivers used to mark up airport meters. And most of them have no idea what their actual return on capital employed looks like, because they have never been forced to compute it.

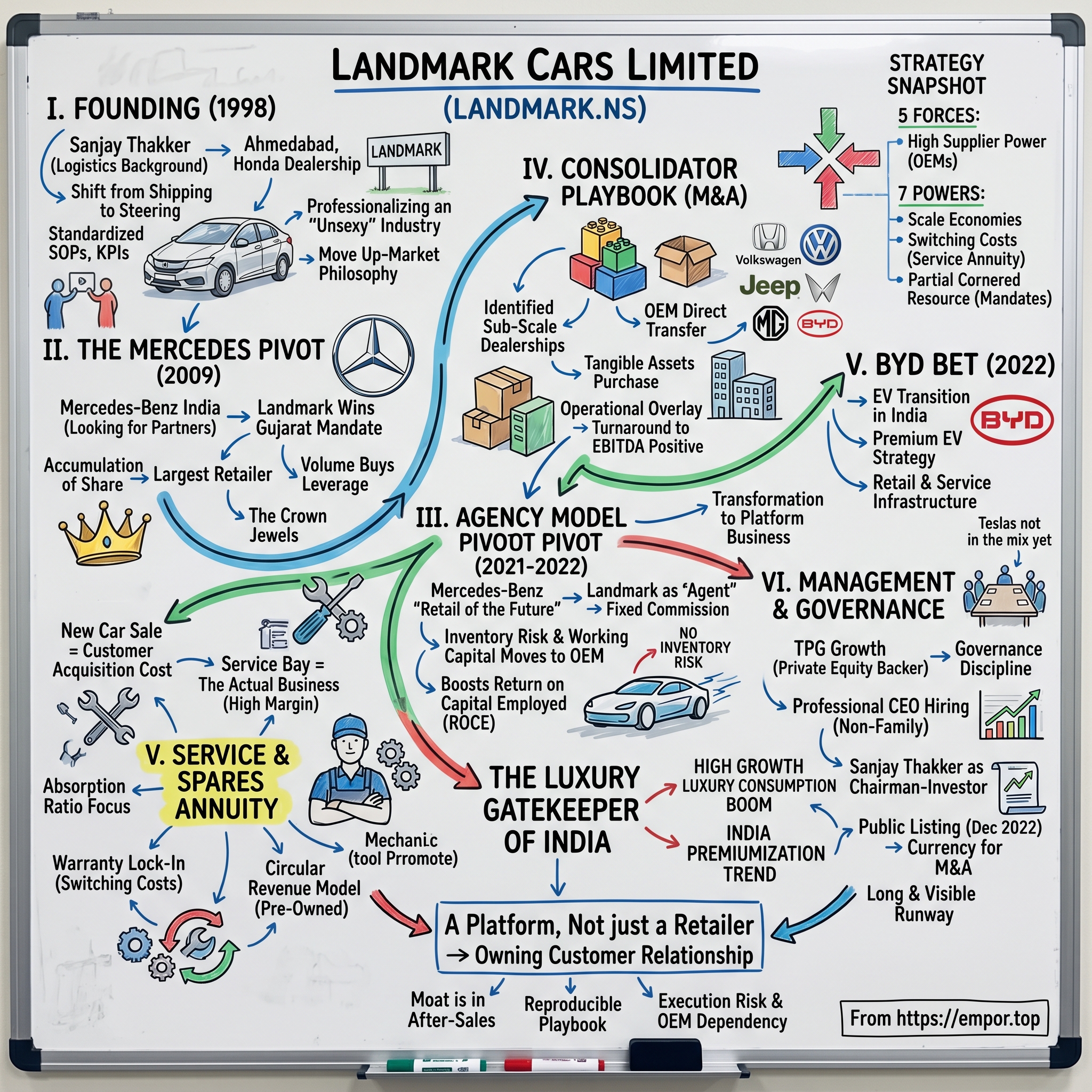

Landmark Cars Limited — symbol LANDMARK.NS, listed on the NSE since December 20222 — is the company that decided to professionalize this mess. Founded by सञ्जय ठक्कर Sanjay Thakker in 1998 with a single Honda dealership in Ahmedabad, Landmark today is the largest Mercedes-Benz retailer in India by volume, accounting for between fifteen and twenty percent of Mercedes' Indian sales depending on the quarter3. It also retails Honda, Volkswagen, Jeep, Renault, Ashok Leyland trucks, BYD electric vehicles, MG, and Mahindra — a portfolio that reads less like a dealership and more like a venture fund of automotive brands.

The thesis is elegant: India is undergoing a once-in-a-generation luxury consumption boom. The number of dollar-millionaire households grew at roughly twelve to fourteen percent compound annually through the late 2010s and 2020s[^4]. Luxury car sales in India crossed fifty thousand units for the first time in calendar 2023[^5]. Yet luxury car penetration in India remains under one percent of total auto sales, versus roughly ten percent in China and twelve percent in Germany. The runway is, as the bankers say, "long and visible."

Landmark's bet is that someone has to operate the physical infrastructure that converts that aspiration into a transaction. Someone has to own the real estate, train the technicians, stock the genuine spare parts, finance the floor plan inventory, and absorb the working capital cycle. That someone, if it is rolled up properly, is not a small business — it is a platform. And platforms, even unsexy ones with grease stains on the floor, can compound capital for a very long time.

Today we are going to dissect that platform. We are going to trace it from a single Honda showroom in 1998 to the agency-model pivot of 2021, through the BYD pivot of 2022, the IPO of 2022, and the consolidator playbook that has defined the years since. We will look at how Sanjay Thakker thinks about capital, why Mercedes-Benz chose him to take inventory risk off its books, and what the bear case looks like when an OEM decides to go direct-to-consumer. Buckle up.

II. Founding & The Shift from Shipping to Steering

Before there was a Landmark, there was a ship. Several ships, actually. The Thakker family's roots in Gujarat trace back through the classic colonial-era trading enterprises of the Arabian Sea — the freight-forwarding, customs-clearing, port-agent businesses that had quietly powered Gujarati mercantile life since the days when Bombay was still spelled with two B's. Sanjay Thakker grew up in this world. His family ran a logistics and shipping operation, the kind where the assets were dhows and warehouses and trust networks rather than spreadsheets and showrooms.

If you wanted to write the screenplay version of what happened next, you would open on a young Sanjay in the early 1990s, post-liberalization India crackling around him, watching the country open up to foreign direct investment and to imported consumer goods. The 1991 reforms had effectively un-locked the gates. Suddenly, Suzuki was no longer the only foreign carmaker allowed to operate. होंडा Honda came in. ह्युंडई Hyundai followed. By the mid-1990s, a generation of Indian entrepreneurs realized that the real arbitrage was not in manufacturing — that was capital-heavy and politically fraught — but in distribution.

In 1998, Sanjay Thakker took out a Honda dealership in Ahmedabad and called it Landmark Honda[^6]. The name was not particularly inspired. It was simply meant to suggest scale and permanence in a market where most dealerships were named after the proprietor's deceased grandfather. The first showroom was, by all accounts, an unremarkable structure on a service road off SG Highway, with the kind of fluorescent lighting and white-tiled flooring that you would see in any mid-1990s Indian commercial establishment.

But Thakker was doing something subtly different from his peers. The standard Indian dealership in 1998 was, fundamentally, a margin shop. The proprietor would buy the car from the manufacturer at a wholesale price, mark it up, sell it to a customer who he probably knew personally, and pocket the difference. Service was an afterthought, run by a chief mechanic who had been with the family since forever and who maintained his own informal economy of side-jobs. There were no SOPs. There were no KPIs. There was, in many cases, no general ledger that would have passed a Big Four audit.

Thakker imported, from his shipping background, a different mental model. Shipping was a fixed-asset business with brutal working-capital dynamics — you had to think about utilization, about turnaround time, about the cost of carry. He started running his Honda dealership the same way. What was the dwell time on a sold car between invoice and delivery? What was the throughput of the service bay per technician per shift? What percentage of customers came back for their second service interval, and what was the gross margin on each? In an industry where most peers could not have told you their service absorption ratio if you offered them a free Mercedes, Sanjay Thakker was building dashboards.

The realization that crystallized Landmark's eventual strategy came somewhere between 2002 and 2005, as Honda's India product mix evolved. Mass-market cars were a brutal business — razor-thin margins, fierce competition between dealers in the same city, and a customer who would walk for a five-thousand-rupee discount. The real money, Thakker concluded, was in the aspirational tier. The customer who bought a luxury sedan did not haggle the same way. He cared about ambiance, about the espresso in the lounge, about being recognized by name. And critically, he came back for service. The lifetime value of a luxury customer dwarfed the mass-market equivalent, often by a multiple of five to seven on a discounted-cash-flow basis.

This was the philosophical foundation: move up-market, professionalize operations, and treat each dealership not as a standalone shop but as a node in an integrated retail platform. Hire managers from outside the family. Tie their compensation to operational metrics. Centralize procurement, finance, HR, and IT. Treat the OEMs as suppliers rather than as deities. It sounds obvious in hindsight. In the Indian auto retail context of 2005, it was heretical.

By the late 2000s, the foundation was set. Landmark had a clean balance sheet, a decent Honda relationship, and a management philosophy that was about to be tested by the most important phone call in the company's history.

III. The Mercedes Pivot & The Crown Jewels

That phone call came in 2008, in the immediate aftermath of the global financial crisis, when मर्सिडीज़-बेन्ज़ इंडिया Mercedes-Benz India was looking for partners willing to plant the three-pointed star in markets that Mumbai and Delhi-based dealers had largely ignored. Ahmedabad. Surat. Vadodara. The diamond-cutting and textile fortunes of Gujarat. These were not Tier-2 cities in any economic sense — there was enough wealth concentrated in Surat alone to support a small Swiss canton — but they were Tier-2 in the luxury-retail sense, meaning that German automotive executives in Pune had to be persuaded that they existed.

Sanjay Thakker had been quietly courting Stuttgart for years. He understood that Mercedes' India strategy needed a different kind of partner: someone who could explain to a third-generation diamantaire in Surat why the S-Class was worth twice the BMW 7-Series sitting in Mumbai, someone who could navigate the local political economy, and crucially someone who could run a dealership to German operational standards. Mercedes signed Landmark for the Gujarat mandate around 2009, and the relationship has since expanded into West Bengal, Maharashtra, Madhya Pradesh, and beyond[^7].

What followed over the next decade was a slow, deliberate accumulation of share. While other Mercedes dealers in India operated one or two showrooms in a single state, Landmark built out a multi-state network, eventually becoming the largest Mercedes-Benz partner in the country and accounting for roughly fifteen to twenty percent of brand sales depending on quarterly mix3. The reason this matters, strategically, is that volume buys you leverage with the OEM. Mercedes-Benz India simply could not afford for Landmark to fail or to defect. The dependence ran both ways — and Sanjay Thakker, having watched the shipping industry, understood exactly how to use a counterparty's dependence as a strategic asset.

Then came the move that genuinely re-rated the business. In late 2021, Mercedes-Benz India announced its "Retail of the Future" initiative — the formal shift to what is technically called the agency model[^8]. To understand why this mattered, you have to understand the old model. Traditionally, a Mercedes dealership in India worked like this: Mercedes-Benz invoiced the car to the dealer, the dealer financed it through working-capital loans (often at rates north of nine percent annually), the dealer held the inventory on his balance sheet, and the dealer took the markup when the car was eventually sold. If the car sat unsold, the dealer ate the interest cost. If the customer demanded a discount, the dealer ate that too. Dealers, in effect, were sub-contracted balance sheets for the OEM.

Under the agency model, Mercedes-Benz India retained ownership of inventory all the way until retail sale. The dealer — now technically an "agent" — was paid a fixed commission per vehicle sold, plus performance incentives, plus the lucrative service-and-spares revenue stream. Inventory risk, price discounting risk, and floor-plan financing all migrated to the OEM's books.

For an Indian listed company, the implications were transformative. Landmark's working capital intensity in the new-car Mercedes business collapsed almost overnight. Inventory days dropped sharply on the Mercedes piece. The return on capital employed in that segment surged because the denominator shrank faster than the numerator. The company was now, effectively, running a high-ROE service-and-commission engine rather than a capital-heavy distribution business. The trade-off was that absolute gross profit per car was lower under the agency model than under the old margin model — but the capital you no longer had to deploy could be redirected into acquisitions, new brands, and the service network. For a long-term compounder thesis, this was, to use the technical term, beautiful.

The Mercedes agency model has not been without its frictions, and we will return to those in the bear case. The journalistic chronicle of luxury dealers grumbling about reduced autonomy is well-documented[^9]. But from a structural-strategy standpoint, Landmark emerged on the other side of the 2021 transition as something different from the dealer it had been in 2019. It had been transformed, voluntarily, from a margin business into a platform business. And the timing — heading into a once-in-a-generation Indian luxury boom — could not have been better.

IV. The Consolidator Playbook: M&A and Capital Deployment

If the Mercedes relationship was the crown jewel, the M&A playbook was the engine that turned Landmark from a Mercedes proxy into a multi-brand retail platform. To understand how Sanjay Thakker thinks about acquisitions, you have to picture him not as a car guy but as a private-equity operator who happens to be in the dealership business. He looks at a failing dealership the way a vulture-debt investor looks at a distressed bond: where is the option value, what is the cost basis, and how quickly can I get to mid-teens EBITDA margins through operational improvement?

The Landmark M&A pattern, repeated dozens of times over the past decade, runs roughly like this. Step one: identify a sub-scale or struggling dealership in a target geography — typically one where Landmark already has a Mercedes or Honda presence and can layer in another brand without doubling fixed costs. Step two: negotiate directly with the OEM rather than with the incumbent dealer. The OEM (let's say Jeep, or Volkswagen, or Renault) cares about its retail footprint and its brand experience; if the existing dealer is underperforming, the OEM is often willing to transfer the mandate to Landmark, with Landmark paying the outgoing operator only for tangible assets — the spare parts inventory, the workshop equipment, and the lease deposit on the showroom.

Step three is the operational overlay. Landmark drops in its standard playbook: centralized accounting, the proprietary DMS (dealer management system) that tracks everything from showroom footfall to technician productivity, retraining of service staff to OEM specifications, and renegotiation of supplier contracts. Step four — and this is the key financial output — bring the acquired dealership from cash-burn or break-even to mid-single-digit EBITDA margins within twelve to eighteen months. This is the same playbook that American multi-brand dealer groups like AutoNation and Penske Automotive ran in the United States in the 1990s, professionalizing what had been a fragmented family-owned industry. Sanjay Thakker has, in the parlance of Indian capital markets, basically Indianized the Penske model.

A concrete example: the Jeep dealership acquisition in Madhya Pradesh, announced in November 20234. Jeep, owned by Stellantis, had struggled in India after the initial novelty of the Compass faded. Landmark stepped in, took over the dealership rights, and within roughly a year had repositioned the showroom under the Landmark operational standard. The pattern repeated for Volkswagen in select geographies, where the Volkswagen-Skoda passenger car business in India had struggled with dealer profitability for the better part of a decade5. Landmark's pitch to Volkswagen was effectively: "Your dealers are losing money because they cannot operate at our scale. Let us take the underperforming markets, we will give you better customer experience, and you will get higher throughput per showroom."

The acquisition of Renault dealerships followed a similar logic. Renault has, candidly, struggled in India since the post-Kwid era, and its dealer network has been in periodic stress. For Landmark, this represents an option value play — pay a modest amount for the showroom rights and the spare parts inventory, run it lean, and either turn it around or use the real estate and customer database to seed a different brand. If Renault recovers in India (a not-impossible scenario as it leans into electric), the option value pays off. If not, the downside is bounded by the asset purchase price.

What is striking is what Landmark does not do. It does not chase Maruti dealerships, where the margins are too thin and the brand experience is commoditized. It does not bid for mass-market two-wheelers. It does not enter geographies where it lacks an existing Mercedes or Honda anchor. The discipline around what it does not acquire is, arguably, more important than the discipline around what it does. Indian conglomerates have a long and unhappy history of "diworsification" — the Peter Lynch coinage for diversifying into businesses you do not understand. Landmark has so far avoided this trap, though the BYD bet that we will discuss shortly is in its own way a test of that discipline.

The financing of all this M&A has been the second elegant part. Landmark went public in December 2022, with shares listing on the NSE and BSE on December 23, 20222. The IPO raised roughly five hundred and fifty-two crore rupees through a combination of fresh issue and offer for sale[^12]. The fresh-issue piece gave Landmark a war chest to fund the acquisition pipeline; the offer-for-sale portion gave existing investors, including the private equity backer TPG, a partial liquidity event[^13]. The IPO priced into a tepid market — listing day was unremarkable — but the strategic effect was achieved: Landmark now had public-market currency to pursue larger consolidation, and a board structure that imposed governance discipline on the acquisition playbook. The next test was whether the consolidator could keep finding things worth consolidating.

V. The "Hidden" Business: The Service & Spares Annuity

Here is the dirty secret of automotive retail that almost no consumer ever thinks about: the new car sale is, at best, a break-even transaction. In some cases, particularly for entry-level mass-market cars, the dealer actually loses money on the new car sale — competitive discounting, OEM volume targets that force you to push inventory at month-end, and the relentless pressure from customers who have access to online price discovery. The new car sale is, in a meaningful sense, just the customer acquisition cost. The actual business — the part where the dealer's economics work — happens over the next ten years, in the service bay.

Walk behind any Landmark Mercedes showroom in India, past the glass-walled customer lounge with the cappuccino machine, through the discreet "Authorized Personnel Only" door, and you find yourself in a different building entirely. Long, brightly lit service bays. Hydraulic lifts. Imported diagnostic equipment from Stuttgart connected directly to Mercedes-Benz's global servers. Trained technicians in clean blue uniforms. This is where Landmark makes its money. The service-and-spares segment, by Landmark's own disclosures, contributed a disproportionate share of gross profit relative to its revenue contribution — meaning the gross margin on a Mercedes brake-pad replacement is multiples of the gross margin on a new C-Class sale6.

The reason is structural, and worth dwelling on, because it underpins the entire thesis. Once you buy a Mercedes-Benz from Landmark, you are effectively locked into the Landmark service network for the warranty period, which typically runs three to five years. Taking your S-Class to an unorganized garage in Lower Parel during the warranty period voids the warranty. Even after the warranty expires, the resale value of a Mercedes is materially affected by whether it has a complete authorized service history — Mercedes-certified pre-owned vehicles command premium prices in part because the service log can be verified end-to-end. This creates a switching cost that is, in Hamilton Helmer's framework, almost a textbook example: the customer is locked in not by contract but by economics.

The annuity nature of this business cannot be overstated. A Mercedes owner in India typically spends between five and eight percent of the original vehicle cost annually on service, parts, insurance renewals, and accessories at the authorized dealership over the ownership cycle. For a fifty-lakh-rupee E-Class, that is somewhere between two and a half and four lakh rupees per year of post-sale revenue, with much higher gross margins than the new car sale itself. Multiply that across the installed base — Landmark has cumulatively delivered tens of thousands of Mercedes vehicles over the past decade and a half — and you start to see why the after-sales business is not just "supportive" of the new car business. It is the business.

This dynamic is what makes the next strategic move so important: the partnership with 比亚迪 BYD. In 2022, Landmark announced a partnership to become a major retail partner for BYD in India, opening showrooms in cities including Noida and Gurugram[^15]. BYD, the Shenzhen-based EV giant, is one of the global heavyweights of electric vehicle manufacturing — by global volumes it has alternated with टेस्ला Tesla for the title of the world's largest EV maker. In India, BYD's strategy has been to enter through the premium and commercial segments first (with vehicles like the Atto 3 and the Seal), before potentially expanding downmarket as Indian EV adoption scales.

For Landmark, BYD is a bet on three things simultaneously. First, that the EV transition in India will be real and durable, not just a Delhi-air-pollution policy story. Second, that the premium EV segment specifically will scale, because that is where Landmark's existing customer base sits and where the service-network advantage matters most. Third, that BYD specifically — and not, say, Tesla or Hyundai's Ioniq line — will be the dominant premium EV brand in India over the next decade. That third bet is the most contestable, but the contractual structure is favorable: Landmark is not betting capital on BYD vehicles directly; it is operating the retail and service infrastructure, which means the option value is positively asymmetric.

Layered on top of all of this is the pre-owned business, branded Landmark Select. Indian luxury car ownership patterns increasingly mirror European ones: the first owner trades in after three or four years, the second owner buys a certified pre-owned vehicle through the authorized dealer network, and Landmark captures margin on both transactions plus continued service revenue. The pre-owned vehicle, in this model, is not a one-time sale — it is a renewed annuity, a refresh of the customer relationship. It also helps the dealer manage trade-in flow, set residual values, and capture customers who cannot afford a new Mercedes but who can afford a three-year-old one. The economics, while not as fat as service, are meaningfully better than new-car retail. As the Indian luxury fleet ages — and remember, the absolute installed base of luxury cars in India is still very small relative to mature markets — this circular revenue model has runway to compound for years.

VI. Management, Shareholding, and the "Anti-Family" Office

There is a moment that Landmark insiders sometimes reference when they want to explain the company's culture, and it concerns a CEO recruitment process around 2014. The candidate was an experienced auto retail executive, not a member of the Thakker family, not a Gujarati, not anyone who had grown up in the family-business ecosystem. He was being interviewed to run one of Landmark's brand verticals. At the end of the conversation, he asked Sanjay Thakker the question that every outside hire asks at an Indian family business: "Will I actually have autonomy, or will I be reporting to your brother-in-law?" Thakker's reply, by all accounts, was a flat one: "We do not employ relatives in operating roles. You will report to me, and to the board." The candidate took the job.

That story may be apocryphal — corporate cultural lore often is — but the structural reality is verifiable from the company's disclosures and proxy filings. Landmark Cars Limited has, deliberately, hired professional non-family CEOs to run individual brand verticals. The Mercedes vertical, the Honda vertical, the truck vertical, the EV vertical: each has its own operational leadership, with Sanjay Thakker functioning more as a chairman-investor than as an executive operator. In an Indian auto retail industry where the typical structure is "promoter is the boss, and the brother handles service," this is genuinely unusual.

Sanjay Thakker himself is worth a closer look. He is now in his late fifties, soft-spoken in public appearances, more comfortable in investor conferences than in glossy magazine profiles. He has consistently described his own model as treating Landmark less as a "company" and more as a "portfolio of high-yield assets." Each dealership, in his framing, is an asset with a known cost of capital, a measurable return profile, and a defined operational benchmark. If a dealership cannot achieve the target return after the operational overlay, you either fix it within a defined timeframe or you exit. It is a discipline that owes more to private equity than to traditional Indian family business culture, and it is the single most important cultural factor in understanding why Landmark looks different from its peers.

The shareholding structure reflects this private-equity-flavored DNA. Promoter holding sat in the mid-forties percentage range post-IPO, with the balance spread between institutional investors, public shareholders, and the residual stakes of pre-IPO backers7. The most consequential institutional backer was टीपीजी ग्रोथ TPG Growth, the U.S. private equity firm that had invested in Landmark in 2017 as a pre-IPO partner. TPG's involvement mattered for several reasons. It brought governance discipline — quarterly board meetings with actual investor scrutiny, audit committees that functioned as audit committees, related-party transaction reviews that were not just box-ticking exercises. It also brought a strategic template, since TPG had seen multi-brand auto retail consolidation play out in other markets.

TPG's exit, completed in stages around 2023, was itself a marker of the company's maturation[^17]. Private equity exits typically happen when the asset has been "de-risked" — meaning the operating model is proven, the management team is in place, and the public market has accepted the equity story. The TPG exit signaled, in effect, that the consolidator playbook was now reproducible without private-equity hand-holding. The shares were absorbed by domestic institutional investors and mutual funds, broadening the float and improving the liquidity profile of the stock.

The incentive structure inside Landmark is, again, worth pausing on. Most Indian dealerships pay their branch managers a salary plus a sales commission. Landmark pays its branch managers on a metric called the absorption ratio — the percentage of a dealership's fixed costs (rent, salaries, utilities, depreciation) that is covered by gross profit from the service and spares business alone. A well-run Landmark dealership might run at an absorption ratio of seventy to ninety percent, meaning that even if the dealership sold zero new cars in a given month, the service business alone would cover most of the overhead. The new car sale, in that framework, becomes the upside, not the survival mechanism.

This is a different mental model than the one used by most Indian auto retailers, and it has cultural implications. Branch managers are incentivized to invest in service capacity, technician training, and customer retention, because those drive their bonus. They are not incentivized to push aggressive new-car discounts at month-end to hit volume targets, because volume targets are not what they are paid on. The structural effect, compounded across dozens of dealerships, is a company that behaves more like an annuity-management business than like a typical auto retailer. Whether the public markets fully price this distinction is, of course, the open question that drives the equity story.

VII. Strategy Analysis: Hamilton's 7 Powers & Porter's 5 Forces

Time to put Landmark on the strategic chessboard. The framework worth using here is the one popularized by Hamilton Helmer in his 2016 book 7 Powers, which identifies seven distinct sources of durable competitive advantage. Most companies, if they are lucky, have one. Landmark, on close inspection, can be argued to have parts of three.

The first is Scale Economies. Landmark operates roughly two hundred and ninety-six outlets across seventeen brands and twenty-two cities as of the most recent annual disclosure1. This scale matters because the dealership business has substantial fixed costs that can be spread across a larger revenue base: a centralized accounting and HR function, an enterprise-grade dealer management system, a corporate-level relationship with multiple OEMs that allows for cross-brand negotiation, and centralized procurement of consumables. A single-showroom dealer in Indore cannot replicate any of these. A multi-showroom group might replicate one or two. Only a national-scale platform can replicate all of them. The math of scale economies in this business is, frankly, brutal for sub-scale competitors.

The second power is Switching Costs, which we have discussed extensively. The Mercedes owner who has bought a car through Landmark and has had it serviced at a Landmark workshop for five years faces real economic friction in switching to a different service provider — warranty risk, resale-value risk, parts-authenticity risk, and the inertia of an established customer relationship. These switching costs are not contractual, but they are deeply economic, and they compound over the ownership cycle. The CFO of Landmark probably looks at the installed-base service-revenue annuity the way the CFO of a SaaS company looks at net revenue retention.

The third power is partial Cornered Resource: the exclusive dealership mandates from Mercedes-Benz and BYD in specific high-growth geographies. A dealership mandate is, in legal terms, a license — it can be revoked, modified, or transferred at the OEM's discretion. So it is not a cornered resource in the purest sense, the way a patent or a mining concession would be. But in practical terms, once a multi-state Mercedes mandate has been operating for fifteen years and the dealer accounts for a meaningful percentage of national brand volume, the cost of switching for the OEM is also substantial. The mandate is, effectively, a soft cornered resource — defensible in the medium term, vulnerable in the long term, and worth a meaningful share-of-profit premium.

What Landmark does not have, candidly, is Branding in the Helmer sense (the Hermès / Rolex / Apple kind of brand pricing power), Network Economies (the dealership business is not a network in the Helmer technical sense), Counter-Positioning (the strategy is reproducible by another well-funded consolidator), or Process Power at the Toyota Production System level (the operational overlay is good, but not yet legendary). And Cornered Resource is partial, as discussed.

Now flip to Michael Porter's 1979 framework — the Five Forces. The most material force, by some distance, is the bargaining power of suppliers, meaning the OEMs. This is the existential force for any auto retailer. Mercedes-Benz, in particular, has demonstrated through the agency-model transition that it can unilaterally restructure the economic relationship with its dealers — moving inventory risk back onto the OEM, but also potentially moving pricing power back onto the OEM in ways that compress dealer margins over time. The bargaining power of the supplier here is roughly the same as the bargaining power of Apple over a small independent Apple reseller: theoretically constrained by contract, practically dominant.

The threat of new entrants in luxury auto retail is moderate. The capital requirements are meaningful, the OEM mandates are not freely available, and the operational expertise is hard to replicate. But there are well-funded competitors — Auto Hangar, Silver Arrows, Trans Car India in the Mercedes ecosystem, and conglomerate-backed groups like the TVS Group in BMW retail. Landmark is not unchallenged; it is the leader in a competitive field.

The threat of substitutes is the philosophically interesting one. The substitute for buying a luxury car is, increasingly, not buying a different car — it is choosing not to own a car at all, instead using shared mobility, premium ride-hailing, or chauffeur-on-demand services. For the price of a new S-Class plus five years of fuel and service, you could in theory ride business-class on Uber for a very long time. But the luxury car purchase in India is, importantly, not primarily a transportation purchase. It is a status purchase, a wealth-display purchase, a self-actualization purchase. To the extent that the symbolic function dominates, substitution risk from shared mobility is structurally limited.

The bargaining power of buyers — meaning the end customer — is moderate. In the luxury segment, customers do shop around between dealers, but the differences between Landmark's offering and a competitor's are perceptible (showroom experience, service quality, after-sale relationship). Customers are not price-takers; they have alternatives. But they are also not in a strong position to demand structural concessions.

The intensity of competitive rivalry within the auto-retail industry is high, but the fragmentation works in Landmark's favor as the consolidator. In a fragmented industry, the largest player with the best operational systems wins disproportionate share over time, because the small players cannot match the cost-per-transaction or the customer experience. The dealership industry in India looks, in this respect, like the U.S. dealership industry looked in 1990 — fragmented, family-owned, and primed for consolidation.

Net-net: the strategic position is defensible in the medium term, with the OEM dependency being the single most material structural risk.

VIII. The Bear vs. Bull Case

Every long-form thesis deserves an honest steel-manning of both sides. Let us start with the bull case, because it is the more emotionally appealing one and we should get it out of our system before turning to the bear case with a clear head.

The Bull Case. India is undergoing a structural premiumization shift across every consumer category — apparel, hospitality, real estate, financial services, and yes, automobiles. The number of dollar-millionaire households in India has been growing at a low double-digit compound annual rate for over a decade and is projected to continue compounding for at least another decade[^4]. Luxury car sales in India crossed fifty thousand units in calendar 2023 and continued growing into 2024 and 2025[^5]. Yet luxury car penetration in India is still under one percent of total auto sales, versus roughly ten percent in China and twelve percent in mature European markets. The absolute size of the addressable market could plausibly triple over the next decade just from penetration normalization.

Within that growing pie, Landmark is the largest and most professionalized retail platform — the kind of business that compounds share organically because it operates better than the competitors. The agency-model transition with Mercedes has structurally reduced the working-capital intensity of the largest brand vertical, releasing capital that can be redeployed into M&A. The BYD partnership positions the company for the EV transition without requiring it to take principal risk on the vehicles themselves. The pre-owned and service-spares annuity provides a cushion against new-car cyclicality. And the management team, having proven that the playbook is reproducible, has the platform and the public-market currency to scale.

Layered on this, Hamilton Helmer's 7 Powers view gives Landmark exposure to Scale Economies, Switching Costs, and partial Cornered Resource — three of the seven powers, which is more than most listed Indian companies can credibly claim. The Porter Five Forces picture is one of moderate-to-favorable competitive dynamics, with the consolidator role exploiting fragmentation. And the company's KPIs, on which more in a moment, point to a business that is improving structurally rather than cyclically.

A holistic competitive-comparison view sharpens the bull case. Among the listed Indian auto-retail and adjacent comps, Landmark is one of very few pure-play luxury-tilted multi-brand retailers. Competitors like Auto Hangar (unlisted) and Silver Arrows (unlisted) are single-OEM or single-region exposures. Conglomerate-backed players have other businesses diluting the focus. Landmark's pure-play structure means investors get a clean expression of the Indian premiumization thesis without conglomerate discount or unrelated business drag.

The Bear Case. Now the harder side. The single most material risk is OEM disintermediation. The agency-model shift that benefited Landmark on inventory risk is the same shift that, taken further, could undermine the dealer's role entirely. If Mercedes-Benz India decides over the next five years to move toward a direct-to-consumer e-commerce model — selling cars through a corporate website and using dealers purely as fulfillment and service centers — the gross profit on the new-car transaction would compress meaningfully. We have seen versions of this play out internationally; Tesla famously bypasses dealerships entirely, and other OEMs have been studying that template[^18]. India is unlikely to go all the way to a Tesla model in the near term, but the structural direction of travel is unfavorable for traditional dealer economics.

The second material risk is mandate concentration. If Mercedes-Benz India decided, for whatever reason — strategic, governance, or commercial — to reduce Landmark's mandate footprint, the impact on revenue and profit would be severe. Mercedes-Benz contributes a disproportionate share of group profit, and the loss of mandate in even one state would be a meaningful event. This is the cornered-resource fragility we discussed earlier.

The third risk is cyclicality. Luxury car sales in India are far more cyclical than mass-market sales, because they are correlated with household wealth effects (stock market performance, real estate appreciation, business cycle peaks). A protracted Indian equity bear market or a sharp economic slowdown would compress new-car volumes substantially. The service-and-spares annuity provides some cushion, but it is not immune to a multi-year demand depression.

The fourth risk, and worth flagging carefully, is execution risk on M&A. The consolidator playbook works beautifully on paper, and Landmark has executed it well to date. But every additional acquisition is a fresh integration challenge, with the typical risks: cultural mismatch with the acquired dealer team, unexpected liabilities (warranty claims, tax exposures, employment disputes), and the simple math that as the platform gets bigger, each marginal acquisition adds proportionally less. The risk of overpaying or of botched integration grows non-linearly.

A second-layer-diligence aside: investors should pay attention to credit-rating actions on Landmark's debt, working capital trends on the non-agency-model parts of the business (the brands that have not migrated to agency model still carry inventory risk), any related-party transaction disclosures in the annual report, and any management-team departures from key brand verticals. These are the operational tells that often precede the headline numbers.

The two or three KPIs worth tracking obsessively for this business: first, same-store throughput growth at mature dealerships — meaning new cars sold per existing showroom on a year-over-year basis. Second, service revenue mix as a percentage of total revenue — a rising mix indicates the annuity business is compounding faster than new-car cyclicality. Third, absorption ratio at the consolidated level, which captures whether the company is generating enough recurring revenue to cover its fixed-cost base. These three metrics, tracked over multiple quarters, will tell investors more about the underlying business than the headline revenue and EPS prints ever will.

A brief myth-versus-reality check, since several narratives float around in the Indian financial media around this name. Myth one: "Landmark is just a Mercedes proxy." Reality: Mercedes is the largest single contributor, but the brand portfolio is genuinely diversified across seventeen brands. Myth two: "The agency model destroyed dealer economics." Reality: the agency model compressed margin per car but expanded return on capital employed by collapsing inventory; the net effect on enterprise value is positive, not negative. Myth three: "The BYD bet is a bet on Chinese EVs in India." Reality: it is a bet on Landmark's retail infrastructure being valuable to whichever premium EV brand wins in India; if BYD stumbles, the showrooms and service bays are convertible.

IX. Conclusion & Final Reflections

The most underappreciated truth in the public-markets investing canon is that the best businesses are often not the ones that invent the product, but the ones that own the customer relationship. The chip industry has its Taiwan Semiconductor. The hospitality industry has its booking platforms. The luxury fashion industry has its multi-brand retailers and its outlet operators. And the Indian luxury automotive industry, by patient and disciplined accumulation, has its Landmark Cars.

The Mercedes engineer in Stuttgart cares about the car. The customer in Surat cares about the experience. The dealer who sits between them — if he runs it right — captures a disproportionate share of the lifetime economic relationship. That has been the historical pattern in mature automotive markets globally, from the United States to Germany to Japan. India is at the early innings of that same evolution, and Landmark has positioned itself to be the platform on which that evolution plays out.

What Sanjay Thakker has built, in essence, is the same business that the great American multi-brand dealer groups built between 1990 and 2010, but optimized for the structural realities of the Indian market: a different luxury demand curve, a different mix of OEM relationships, and a different service-revenue annuity profile. Whether the multi-decade compounding case plays out in Landmark the way it did in AutoNation or Penske is, of course, the question that the next decade of quarterly results will answer.

The lesson for founders and operators watching this story is simple, and worth stating directly: you do not have to build the product to build a billion-dollar business. You can build the platform that delivers the product. The branding, the financing, the logistics, the after-sales service, and the customer relationship — these are not commodity activities. They are themselves the value chain, and they can be a moat if you operate them with discipline.

The lesson for long-term fundamental investors is more nuanced. Landmark is not a perfect business. It is exposed to OEM disintermediation, to luxury cyclicality, and to the M&A execution risk that all consolidators face. It does not have the kind of pricing power that a true consumer brand has, and it never will. But it sits at a specific intersection of structural tailwinds — Indian premiumization, EV transition, organized-retail penetration, the consolidation of a fragmented industry — that may not come along again in this generation. The question, as always, is whether the price you pay leaves enough margin of safety for the future you cannot foresee.

And the final reflection, the one that captures the spirit of the business, comes back to where we started: the Saturday afternoon in the Ahmedabad showroom, the textile baron and his family, the silent salesperson in the navy blazer. India's luxury consumption story is, fundamentally, a story about a country becoming richer faster than its institutions can keep up with. Landmark is one of the institutions that is keeping up. It is building, slowly and unspectacularly, the retail infrastructure for the next generation of Indian wealth.

The cars will change. The brands will rotate. The technology will shift from internal combustion to electric. But somewhere on a service road off SG Highway in Ahmedabad, somewhere on a Sunday in Surat, somewhere in a service bay in Pune, a Landmark technician will be running diagnostics on a luxury vehicle owned by a customer who would not, frankly, trust anyone else to do it. That is the business. That is the moat. And that, in the end, is the whole thesis.

References

References

-

Landmark Cars IPO: Why this is a bet on India's rising affluence — Moneycontrol, 2022-12-13 ↩↩

-

How Landmark Cars is consolidating the fragmented dealership market — Forbes India, 2023-01-20 ↩↩

-

Landmark Cars acquires Jeep dealership in Madhya Pradesh — Business Standard, 2023-11-05 ↩

-

Landmark Cars Q4 FY24 Investor Presentation — Group Landmark ↩

-

Landmark Cars Financial Results and Shareholding — NSE India ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube