Ksolves India: The High-Efficiency Compounding Machine

I. Introduction and Episode Roadmap

Here is a question worth sitting with: How does a tiny, bootstrapped IT consultancy, started in a cramped office in Indirapuram in 2012, turn itself into one of the most capital-efficient listed companies in India — delivering return on capital employed north of 200%, distributing almost all its profits back to shareholders, and compounding revenue at a pace that would make most mid-cap IT firms blush?

The answer is Ksolves India, listed on the NSE under the ticker KSOLVES. And if the name does not ring a bell, that is part of the story. This is not Infosys. This is not TCS. This is not even Happiest Minds or LTIM. Ksolves is a company with roughly 565 employees, generating around 153 crore rupees in trailing twelve-month revenue as of its most recent quarter, and yet it operates with the financial discipline and margin profile of a company ten times its size. It is a study in what happens when a founder refuses to play the game everyone else is playing — the game of scale-at-all-costs, acquire-to-grow, and hoard-cash-for-optionality.

To appreciate how unusual this is, consider the standard metrics of the Indian IT services industry. The largest players — TCS, Infosys, Wipro — generate ROCE in the range of 30% to 60%. These are excellent businesses by any measure. The mid-cap firms — Happiest Minds, Mphasis, Coforge — typically land in the 20% to 40% range. Ksolves, with ROCE figures that have exceeded 170% in recent years and touched 199% in FY24, operates in a different universe. These are not the numbers of a typical IT services company. These are the numbers of a business with a genuinely differentiated model — one that requires very little capital to generate very large profits.

Consider the contrast. India's IT services sector is a 250-billion-dollar export engine that employs over five million people. The playbook is well-documented: build a bench of thousands of engineers, bid for large multi-year contracts, squeeze margins through scale, and use the resulting cash flow to acquire complementary firms. Infosys, Wipro, TCS, HCL — they all followed variations of this template. Even the newer generation of mid-cap IT firms — Happiest Minds, LTIM, Mphasis — have largely adhered to it, using M&A to accelerate growth and diversify their technology offerings.

Ksolves has done almost none of this. It has never made a significant acquisition. It employs fewer people than a single floor of most TCS delivery centers. It does not bid for the massive multi-year outsourcing contracts that dominate the Indian IT landscape. And yet, its return on capital employed exceeds that of virtually every IT company in India, its EBITDA margins rival those of firms many times its size, and it pays out dividends at a rate that would embarrass most mature businesses, let alone a growth-stage technology company.

Instead, it picked narrow, high-complexity technology niches — Salesforce, Apache Big Data tools, Odoo ERP, and increasingly AI — and built deep expertise that commands premium billing rates. It layered a product strategy on top of its services business, launching proprietary applications on the Salesforce AppExchange and the Odoo App Store that serve as both revenue streams and lead generation engines. And it did all of this while remaining essentially bootstrapped, raising a mere four crore rupees in its IPO.

The founder and chairman, Ratan Srivastava, owns about 32% of the company. His co-promoter Deepali Verma holds another 27%. Together, they control nearly 59% of the equity, which means their incentives are perfectly aligned with outside shareholders. There is no agency problem here. When Ksolves pays out 80% or more of its profits as dividends, the promoters are the biggest beneficiaries — and the biggest losers if the business stumbles.

This episode traces the arc from Kartik Solution — the forgettable name under which the business was originally started — to a main-board listed entity that has become a quiet case study in capital allocation, niche positioning, and the art of building product DNA inside a services body. The journey passes through the brutal early years of competing on price in India's red-ocean IT market, the pivotal bet on Salesforce and Big Data, a pandemic-era micro-IPO that was as much about credibility as capital, and the current moment where AI threatens to disrupt the very billing model that made Ksolves rich.

There is a particular irony in the Ksolves story that is worth naming upfront. The Indian IT services industry was built on the insight that talented Indian engineers could deliver enterprise software work at a fraction of the cost of their Western counterparts. That insight created hundreds of billions of dollars in value and transformed India's economy. But within India itself, the same dynamic played out again at a smaller scale: firms in smaller cities like Noida and Indore discovered they could deliver the same quality work as their counterparts in Bangalore and Mumbai, but at lower cost because rent, salaries, and overheads were cheaper. Ksolves is, in effect, applying the Infosys playbook against Infosys — offering enterprise-grade expertise from a leaner, hungrier, more efficient platform.

The question that hangs over everything: Can Ksolves scale to a hundred million dollars in revenue without breaking the model that got it here?

II. History: The Body Shop Trap and the Pivot (2012–2018)

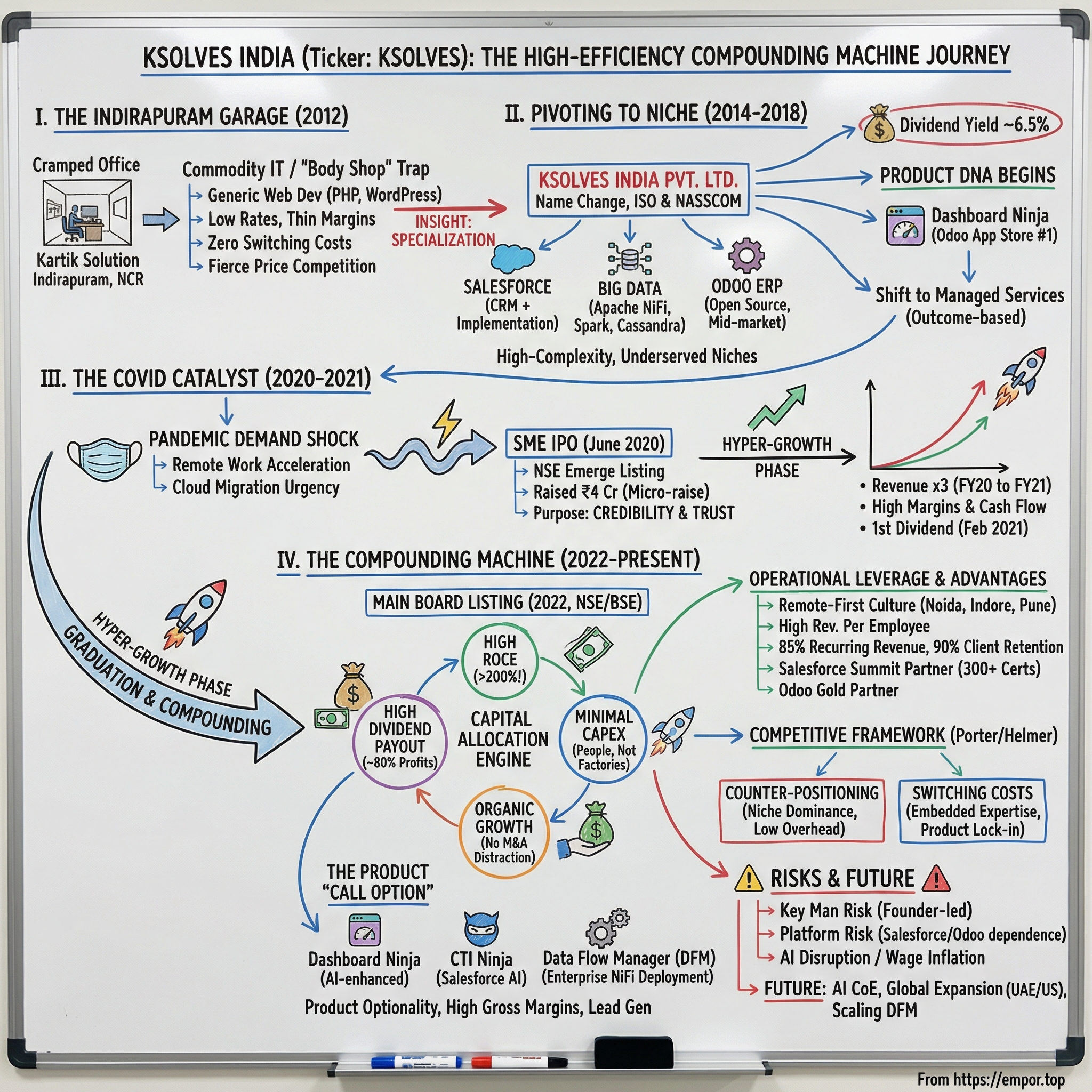

Picture Indirapuram in 2012. A dense, fast-growing suburb on the eastern edge of Delhi-NCR, full of apartment towers rising above narrow lanes, chai stalls operating out of ground-floor garages, and thousands of small commercial offices housing the kinds of businesses that never make the newspapers. This is the India that produces most of its entrepreneurs — not the venture-backed, WeWork-inhabiting, Stanford-educated startup ecosystem of Bangalore, but the scrappy, self-funded, learn-by-doing world of NCR's sprawling suburbs.

Ratan Srivastava had just walked away from a comfortable career at Tech Mahindra, where he had spent four years as a senior software engineer after earlier stints at Birlasoft, HSBC, and Persistent Systems. He had a computer science degree, over a decade of enterprise software experience working on projects for global clients, and the restless conviction that he could build something of his own. The decision was not born of frustration — by all accounts, his corporate career was progressing well. It was born of the observation that sits at the heart of every bootstrapper's origin story: the belief that the value he created for his employers could be captured more directly if he built the business himself.

The venture he started in 2012 was called Kartik Solution — an unregistered, bootstrapped operation run from a small office in Indirapuram with little more than a handful of developers and a dream. The ambition, at that stage, was modest. Srivastava was entering what the Indian IT industry calls the "body shop" model — essentially renting out developer hours to clients who needed software built but did not want to hire full-time engineers. It is the most common entry point for IT entrepreneurs in India, and it is also the most commoditized. Thousands of small firms compete on price, undercutting each other for PHP development, WordPress customization, and generic web projects. The margins are thin, the clients are fickle, and the switching costs are zero.

For the first couple of years, Kartik Solution lived in this world. The work was generic — building websites, customizing WordPress installations, writing basic PHP applications. The clients were small — local businesses, startups with limited budgets, the occasional offshore contract. The billing rates were low — single-digit dollars per hour, barely enough to cover salaries and overhead with anything left over for the founder.

Srivastava was essentially doing the same work he had done at Tech Mahindra, but without the brand, the scale, or the safety net. Anyone who has started a services business in India knows the grind: chasing invoices from clients who are slow to pay, managing cash flow week to week, losing developers to slightly higher offers from the shop next door, and constantly questioning whether the decision to leave a stable corporate paycheck was the right one.

But Srivastava was observing something that would become the foundation of everything Ksolves later built. He noticed that while the market for generic web development was brutally competitive, the market for complex, emerging technology stacks was dramatically underserved. Enterprise clients needed specialists in Apache Cassandra, Apache Spark, Apache NiFi — powerful open-source tools for handling massive datasets — but the talent pool was tiny. Similarly, the Salesforce ecosystem was exploding in the United States, and companies needed implementation partners who understood not just the platform but the business processes it was meant to support. These were not ten-dollar-an-hour PHP jobs. These were high-value engagements where expertise commanded a premium.

This observation contained a profound insight about the economics of IT services. In commodity web development, a client's decision to hire a provider is based almost entirely on price. If one shop charges eight dollars an hour and another charges ten, the client picks the cheaper option because they believe the output is interchangeable. But when a Fortune 500 telecom company needs to design a data pipeline that processes billions of call records per day using Apache NiFi, the decision calculus inverts entirely. The cost of failure — data loss, system downtime, regulatory violations — dwarfs the cost of the consultant. The client is not shopping for the cheapest option; they are shopping for the most capable. And in a market where only a handful of firms have genuine expertise in these complex, mission-critical technologies, the capable provider can charge a substantial premium.

Srivastava saw that the path to building a defensible IT services business was not to be cheaper than the competition but to be more specialized — to develop expertise so deep in a narrow set of technologies that clients would seek Ksolves out rather than the other way around. It was a bet against the prevailing wisdom of the Indian IT industry, which prized breadth of capability and scale of delivery. But it was a bet that the economics of specialization strongly favored.

The first inflection point came in 2014 when Srivastava formally incorporated the business — initially as Keyon Softwares Private Limited on July 17, 2014, then quickly renamed to Ksolves India Private Limited via a special resolution passed on September 27, 2014, with a fresh certificate of incorporation dated October 14, 2014. The name change itself was strategic. "Keyon Softwares" sounded generic and forgettable — one of ten thousand similarly named software shops in NCR. "Ksolves" — a portmanteau suggesting "solutions" — was distinctive, easy to remember, and carried a professional resonance that the original name lacked. For a company whose success depended on winning the trust of American enterprise clients who had never heard of it, the name mattered more than one might think.

The rebirth was more than administrative. It signaled a conscious decision to move up the value chain — to stop competing on price and start competing on capability. The company pursued ISO certification and NASSCOM membership, not as vanity badges but as prerequisites for landing enterprise contracts. In the world of B2B technology services, especially when selling to American and European clients, these certifications are table stakes. Without them, a small Indian firm does not even get invited to the conversation. An ISO 9001 certification tells a prospective client that the firm has documented quality management processes. NASSCOM membership — the industry body that represents India's technology sector — signals that the firm meets minimum standards for financial stability, ethical practices, and data security. For Srivastava, getting these credentials was not about checking boxes. It was about systematically removing the objections that enterprise procurement teams would raise when evaluating a small, unknown firm from Noida.

Between 2014 and 2018, Ksolves methodically built its capabilities in three areas: Salesforce consulting, Big Data engineering, and Odoo ERP implementation. Each of these choices was deliberate. Salesforce was the fastest-growing CRM platform in the world, with an ecosystem of over 150,000 companies using it and a constant need for certified implementation partners. Big Data tools like Spark and NiFi were becoming critical infrastructure for enterprises drowning in data but lacking the internal expertise to process it. And Odoo, the open-source ERP system, was gaining traction as a cost-effective alternative to SAP and Oracle among small and mid-sized businesses.

What made these bets smart was not just the growth of the underlying platforms but the structural economics they created. All three technologies have high switching costs. Once a company has built its sales operations on Salesforce, or its data pipelines on Apache NiFi, ripping those systems out is enormously expensive and risky.

The consultants who built and maintain those systems become deeply embedded in the client's operations. They understand not just the technology but the client's specific business logic, data structures, and organizational workflows. This is the opposite of the body-shop model, where a developer can be swapped out overnight. Ksolves was building relationships that were sticky by nature.

There is a useful way to think about this. In commodity IT services, a provider is like a temporary worker at a factory — easily replaced by anyone with similar basic skills. In niche, platform-specific consulting, a provider is more like a family doctor — someone who knows your medical history, understands your quirks, and whom you trust with critical decisions. You can always switch doctors, but the cost of doing so — the lost history, the risk of misdiagnosis, the time spent rebuilding the relationship — deters you from switching unless something goes seriously wrong.

By 2018, the company had achieved something that most small Indian IT firms never manage: escape velocity from the commodity trap. Revenue was growing from a small base, profitability was improving as the mix shifted toward higher-value work, and the client base was diversifying across industries and geographies. It was still small — but it was differentiated, and increasingly, it was difficult to replicate. The stage was set for the moves that would transform Ksolves from a niche consultancy into a compounding machine.

III. The Salesforce and Big Data Bet (2018–2020)

In the Indian IT services industry, there is a saying that captures the central strategic dilemma: "Generalist equals commodity." The moment a company positions itself as a do-everything, build-anything software shop, it enters a race to the bottom on price. The only escape is specialization — but most founders resist it because specialization feels like voluntarily shrinking your addressable market. Ratan Srivastava leaned into it.

By 2018, Ksolves had made its bets clear. The company would go deep — not wide — into Salesforce, Big Data, and Odoo. To understand why this mattered, it helps to understand what these technologies actually do and why they create such durable competitive advantages for the firms that master them.

Salesforce, for the uninitiated, is the world's dominant customer relationship management platform. Think of it as the central nervous system for a company's sales and marketing operations. Every lead, every customer interaction, every deal in the pipeline flows through Salesforce. But out of the box, Salesforce is like a powerful but unconfigured engine. It needs to be customized, integrated with other systems, and maintained — and that requires specialized consultants who understand both the technology and the business processes. Salesforce certifications are notoriously difficult to earn, and companies that accumulate hundreds of them — as Ksolves eventually did, reaching over 300 — signal a depth of expertise that is genuinely hard to replicate.

Big Data tools like Apache NiFi, Spark, and Cassandra occupy a different but equally sticky niche. These are the plumbing systems that move, process, and store massive volumes of data in real time. To use a non-technical analogy: if a company's data is water, then NiFi is the pipe system that moves it from source to destination, Spark is the treatment plant that processes and transforms it, and Cassandra is the reservoir that stores it at massive scale. Together, they form the invisible infrastructure that allows modern enterprises to function.

Imagine a telecommunications company processing billions of call records per day, or a financial institution running fraud detection algorithms across millions of transactions, or a healthcare system matching patient records across dozens of hospitals in real time. The engineers who design and maintain these systems need to understand distributed computing — the art of making hundreds of computers work together as if they were one — along with data architecture, fault tolerance, and the specific quirks of each tool. It is highly specialized work, and the consequences of getting it wrong — data loss, system downtime, compliance failures — are severe enough that clients are reluctant to change providers. When your entire data infrastructure is built on Apache NiFi and the team that built it leaves, you are not just replacing developers. You are putting your business at risk.

The Odoo play was different in character but equally strategic. Odoo is an open-source ERP system — enterprise resource planning software that manages everything from accounting to inventory to human resources. For those unfamiliar with the ERP landscape, think of it this way: a CRM like Salesforce manages a company's external relationships with customers, while an ERP manages a company's internal operations. Together, they form the complete digital backbone of a modern business.

Odoo competes against behemoths like SAP and Oracle, but at a fraction of the cost, making it attractive to small and mid-sized businesses that need enterprise-grade software without enterprise-grade budgets. SAP implementations can cost millions of dollars and take years to complete. An Odoo implementation can be done in weeks at a fraction of the cost, and the open-source nature of the platform means there are no licensing fees eating into the client's ROI.

The Odoo ecosystem was growing rapidly, and Ksolves positioned itself as a premier implementation partner, eventually earning Odoo Gold Partner status. In September 2025, the company received the ultimate validation: being recognized as the Best ERP Implementation Partner (Odoo) India 2025 at the Odoo Experience event in Brussels — a recognition earned through rigorous evaluation of technical expertise, customer satisfaction, innovation, and business growth across 80-plus countries and 50-plus industries. The award was presented at the Brussels Expo on September 20, 2025, in front of the global Odoo community.

But the real inflection point in this period was not a services win. It was a product launch. In 2018, Ksolves released Dashboard Ninja on the Odoo App Store. Dashboard Ninja is, at its core, a data visualization tool — it allows Odoo users to create dynamic, visually rich dashboards that consolidate key performance indicators from across their business. It sounds simple, but execution matters enormously in enterprise software, and Dashboard Ninja was executed exceptionally well.

Within months, Dashboard Ninja became the number-one application on the entire Odoo App Store — a position it has held as the longest-standing number-one app on the platform. By early 2026, it had powered over 2,550 businesses worldwide, which in the enterprise software world represents significant penetration. The revenue from Dashboard Ninja itself was modest relative to the services business, but its strategic value was enormous. It served as what marketers call a "lead magnet" — a proof of capability that attracted potential services clients. When a mid-sized manufacturer in Germany or a retailer in the United States found Dashboard Ninja on the Odoo App Store, they were not just downloading an app. They were discovering a company that clearly understood the platform at a deep level. Many of those downloads converted into services engagements worth multiples of the product's price.

This was the moment Ksolves began to develop what might be called "product DNA" — the ability to think like a product company even while operating primarily as a services business. Most IT services firms attempt this transition and fail spectacularly. Building products requires a fundamentally different mindset: investing upfront with no guaranteed return, iterating based on user feedback, and maintaining a codebase over years rather than delivering a project and moving on. The fact that Ksolves pulled it off — and did so with a product that achieved market leadership — says something important about the organization's culture and the founder's willingness to invest in long-term strategic assets.

Alongside Dashboard Ninja, Ksolves launched several other products during this period, including Sales League on the Salesforce AppExchange (a gamification tool that uses real-time opportunity data to identify and celebrate top salespeople) and early versions of what would later become their Big Data product portfolio. None of these achieved the same market position as Dashboard Ninja, but collectively they reinforced the company's identity as a firm that builds solutions rather than merely renting out developers.

There is a broader lesson here about how services companies can develop product capabilities without the typical pitfalls. Most IT services firms that attempt product development make the mistake of treating it as a separate business unit — hiring product managers from outside, setting up a separate P&L, and running the product team with different incentives and culture than the services team. This almost always creates friction: the services team resents the product team for consuming resources without generating near-term revenue, while the product team resents the services team for not prioritizing product-related client work. The result is usually organizational dysfunction and mediocre products.

Ksolves avoided this trap by integrating product development into the services culture. The same engineers who build products also work on client projects. The products themselves are designed to solve problems that the services team encounters repeatedly — creating a natural feedback loop where services experience informs product design, and products make the services team more efficient. Dashboard Ninja exists because Ksolves' Odoo consultants kept building custom dashboards for every client and realized the work could be productized. DFM exists because Ksolves' Big Data engineers kept solving the same NiFi deployment challenges and recognized the opportunity for a tool. This bottom-up, practitioner-driven approach to product development is far more likely to produce tools that solve real problems than the top-down, market-research-driven approach that most firms attempt.

The cultural shift was perhaps more important than any individual product. Ksolves was moving from "staff augmentation" — the industry euphemism for renting out developer hours — to "managed services and solutions," where the company owns the outcome rather than just providing labor. To understand why this distinction matters so much, consider what each model looks like from the client's perspective.

In staff augmentation — or time-and-materials billing — the client pays for developer hours. If the project takes longer, the client pays more. If the developer is inefficient, the client bears the cost. The incentive structure is perverse: the service provider actually benefits from inefficiency, and the client has every reason to shop for cheaper developers. Switching costs are minimal because the client is buying a commodity — human hours — rather than a solution.

In managed services and project-based delivery, the dynamic inverts. The provider quotes a price for a defined outcome — build this Salesforce integration, deploy this data pipeline, maintain this ERP system. If the provider's engineers are more efficient, the provider keeps the savings as margin. If they are less efficient, the provider absorbs the cost. The incentive structure aligns: the provider benefits from excellence, the client benefits from predictability, and the switching costs are high because the provider is embedded in the outcome rather than just supplying labor.

Ksolves' transition toward this model was still underway as of early 2026 — management disclosed in the Q4 FY25 earnings call that the shift to project-based delivery required extensive internal training of the sales team, and that some larger deals took six or more months to close due to extended approval cycles. But the directional shift was clear, and the evidence of its impact was visible in the largest single contract of 600,000 dollars, a step-function increase from the previous maximum of roughly 120,000 dollars.

By early 2020, Ksolves was profitable, growing, and increasingly differentiated. The company had built a roster of clients across healthcare, telecom, e-commerce, finance, and logistics. Its revenue was modest but its margins were exceptional. And Ratan Srivastava was about to make the most counterintuitive move of his career — launching an IPO in the middle of a global pandemic.

IV. The Micro-IPO and the Covid Catalyst (2020–2021)

The timing looked insane. In early 2020, India was bracing for what would become its first devastating Covid-19 wave. The stock market had crashed in March and was still finding its footing. Businesses across the country were shutting down. And Ratan Srivastava chose this moment to take Ksolves public. He first converted the company from a private limited to a public limited entity on April 28, 2020 — just weeks after India entered its nationwide lockdown — and then pushed forward with the offering.

The IPO opened on June 23, 2020, on the NSE Emerge platform — the exchange's dedicated marketplace for small and medium enterprises. The terms were almost comically modest by Indian IPO standards: 402,000 equity shares at a face value of ten rupees each, priced at 100 rupees per share, raising a total of approximately four crore rupees. To put that in perspective, four crore rupees was roughly half a million US dollars. Most Series A fundraises in Indian tech were fifty to a hundred times that size. Even by SME IPO standards, it was a micro-raise.

But the purpose was never primarily about capital. Ksolves was already profitable. It did not need the money to fund operations or pay down debt. The IPO served a different, more strategic function: trust. In the world of enterprise B2B sales, particularly when an Indian company is selling to American and European clients, being publicly listed changes the conversation. It means audited financials, regulatory oversight, and a level of transparency that privately held companies cannot match. For a 500-person firm competing against Accenture and Deloitte for Salesforce implementation contracts, the ability to say "we are a listed company on the National Stock Exchange of India" was a powerful credibility signal.

The IPO was modestly subscribed — 1.42 times overall, with non-institutional investors showing more enthusiasm at 2.22 times while retail investors came in below full subscription at 0.62 times. The minimum lot size was 1,200 shares, requiring a retail investment of 120,000 rupees — a high bar that filtered for serious investors rather than speculative punters. The listing on July 6, 2020, was uneventful in the best possible way. Ksolves opened at 101.95 rupees — a 1.95% premium to the issue price — and closed its first day at 106.90 rupees. No dramatic pop, no crash. Just a quiet entrance onto the public stage.

Looking back, the modesty of that listing day is almost poignant. Investors who purchased at the IPO price of 100 rupees and held through to the stock's subsequent peaks would see returns of over fifty times their investment — one of the most dramatic wealth creation stories in the SME IPO segment. But on that July day in 2020, with Covid raging and markets still shell-shocked, nobody was making those projections. The IPO was, in the purest sense, a bet on the character and capability of the founder rather than on any grand financial engineering.

What happened next was anything but quiet. And to understand it, one needs to appreciate the peculiar dynamics of the SME listing platform in India.

NSE Emerge, where Ksolves listed, is the exchange's dedicated marketplace for small and medium enterprises — companies too small for the main board but ambitious enough to seek public capital. The platform has its own rules: higher lot sizes to filter out casual retail investors, lighter disclosure requirements, and a trading environment that is thinly liquidity-constrained. Most companies that list on Emerge never graduate to the main board. Many languish in obscurity, trading a handful of shares per day, their stock prices disconnected from any fundamental reality. The fact that Ksolves was listed here, rather than on the main board where institutional investors and fund managers could easily access it, meant that the stock flew under the radar of most professional investors during its most explosive growth phase. Those who did find it — often through word of mouth in small-cap investor communities or through screening for high-ROCE companies — were rewarded handsomely.

The Covid-19 pandemic, for all its devastation, turned out to be the most powerful demand accelerator the cloud computing and digital transformation industry had ever experienced. Overnight, companies that had been dithering about moving to Salesforce suddenly had no choice — their sales teams were remote, their old systems did not work, and they needed cloud-based solutions immediately. The same was true for data infrastructure: companies needed to process, analyze, and act on data faster than ever, and they needed the Big Data tools that Ksolves specialized in.

Ksolves was positioned almost perfectly for this demand shock. Its entire technology stack — Salesforce, cloud-based ERP, Big Data analytics — was exactly what the market was desperate for. And unlike larger competitors, Ksolves was nimble enough to respond almost instantly. There were no layers of management to approve new project proposals, no committee meetings to debate resource allocation, no bureaucratic approval chains for hiring. Srivastava could say yes to a new client on Monday and have a team assembled by Wednesday. In a market where speed of response was everything, this agility became a competitive weapon.

Revenue accelerated dramatically. In FY20, the company had generated just 10 crore rupees in revenue. In FY21 — the pandemic year — that nearly tripled to 28 crore rupees. The company added clients across geographies, with a particular surge in the United States, which would come to account for the majority of Ksolves' overseas revenue. Margins expanded as the shift to remote work eliminated office-related costs while billing rates held steady or even increased due to the urgency of client needs.

The pandemic also revealed something about Ksolves' organizational DNA that would prove durable. Unlike larger firms where remote work required massive IT infrastructure overhauls, VPN capacity expansions, and months of policy deliberation, Ksolves transitioned almost seamlessly. The company had always operated with a distributed delivery model — engineers working from Noida, Indore, and Pune, collaborating with clients across time zones. The pandemic merely formalized what was already a de facto remote-first culture. This agility — the ability to keep delivering without missing a beat while competitors were scrambling — became its own sales pitch. Several clients who came to Ksolves during the pandemic did so specifically because their existing providers were struggling with the transition to remote work.

By the end of FY21, the company's financial trajectory had shifted from steady growth to rapid compounding — and critically, the new clients that came in during the pandemic were sticky, creating a base of recurring revenue that would fuel growth for years to come.

The financial discipline during this hyper-growth phase is worth noting because it contrasts sharply with the behavior of most companies experiencing a sudden demand surge. Many firms, flush with unexpected revenue, would have hired aggressively ahead of demand, expanded into expensive office space, or made opportunistic acquisitions while their stock price was elevated. Srivastava did none of this. Headcount grew, but in line with revenue — maintaining the per-employee productivity that drives margins. Costs were managed tightly. And the company's first interim dividend — ten rupees per share — was declared in February 2021, barely seven months after listing. The message to shareholders was unmistakable: this company generates more cash than it needs to grow, and the surplus belongs to you.

The SME platform, however, was always meant to be a stepping stone. In 2022, Ksolves graduated from NSE Emerge to the main board of both the NSE and BSE — a transition that most SME-listed companies never achieve. The migration required meeting stringent criteria: minimum paid-up capital of ten crore rupees, market capitalization exceeding 100 crore rupees, a minimum track record of profitability, and compliance with the more demanding disclosure and governance requirements of the main board. The fact that Ksolves met these thresholds within approximately two years of its SME listing spoke to the velocity of its growth and the discipline of its financial management.

For investors, the migration mattered beyond symbolism. Main-board listing opens the stock to a dramatically larger pool of buyers — institutional investors, mutual funds, portfolio management services — many of which are prohibited from investing in SME-listed stocks. It also brings more stringent quarterly disclosure requirements, analyst coverage (however thin for a company of this size), and the psychological validation of being grouped with India's larger listed companies. The main-board listing further enhanced the company's credibility with enterprise clients, creating a virtuous cycle: better clients led to better revenue, which led to better stock performance, which attracted better investors, which led to even better clients. In the business of enterprise IT services, where client confidence in a provider's stability is paramount, being listed on the same exchange as Infosys and TCS — however small by comparison — carried real commercial value.

The speed of this graduation from SME platform to main board deserves emphasis. Most SME-listed companies take five to seven years to meet main board eligibility criteria, if they ever do. Many SME stocks remain thinly traded, poorly covered, and effectively inaccessible to institutional investors for their entire listed life. Ksolves accomplished the transition in roughly two years — a timeline that reflects not just the company's growth trajectory but the quality of its financial management. Meeting the main board's audit, governance, and disclosure requirements is a non-trivial administrative burden for a small company, and the fact that Ksolves navigated it smoothly speaks to the organizational discipline that also drives its operational performance.

It is also worth noting the CMMI Level 3 certification that Ksolves achieved in 2020 — a quality standard for software development processes that is particularly valued in the US defense and government contracting ecosystem. Combined with the listing, the certifications, and the growing Salesforce partnership status, Ksolves was systematically removing every excuse a potential client might have for not working with a smaller firm.

By mid-2022, the stock had multiplied several times from its IPO price, the company had over 150 clients across more than 30 countries, and it was generating the kind of return on capital employed — north of 200% in FY23 — that made financial analysts do a double take. The revenue trajectory tells the story of compounding in miniature: roughly 10 crore rupees in FY20, 28 crore in FY21, 47 crore in FY22, 78 crore in FY23, 109 crore in FY24, and 137 crore in FY25 — a five-year revenue CAGR of 68% and a five-year profit CAGR of 119%. By Q3 FY26, Ksolves posted its highest-ever quarterly revenue of 42.30 crore rupees, growing 12.2% year-on-year. The compounding machine was fully operational.

V. Inside the Machine: Hidden Businesses and Operations

Most analysts who cover Ksolves — and there are not many, given its size — focus on the services revenue. That is understandable: services account for roughly 90% of total revenue, and it is the services business that generates the cash flow, the margins, and the recurring relationships that define the company's financial profile. But to look only at services is to miss what may be the most strategically important part of the business: the product portfolio.

Think of Ksolves' product division as a call option embedded inside a services company. The services business is the cash cow — predictable, high-margin, and growing steadily. The products business is smaller, riskier, and harder to value, but it carries the potential for an entirely different kind of upside.

To quantify the gap: IT services companies in India typically trade at 15 to 30 times earnings, reflecting the linear nature of services revenue — you need more people to generate more revenue, which limits scalability. Enterprise software products, by contrast, can trade at 10 to 20 times revenue — not earnings, but revenue — because software scales without proportional increases in cost. If even one of Ksolves' proprietary products achieves meaningful scale, the company's valuation framework shifts. The products division could be worth more than the services division on a per-rupee-of-revenue basis, even if it remains a fraction of total revenue. This is the "call option" embedded in the stock — and unlike a financial option, it does not expire.

The product portfolio spans three ecosystems. On the Odoo side, Dashboard Ninja remains the crown jewel — the number-one app on the Odoo Store, now enhanced with AI capabilities and available in multiple variants including Sales Dashboard Ninja, Inventory Dashboard Ninja, and POS Dashboard Ninja. Ksolves also offers additional Odoo products including a Transparent Theme and project management tools, building a suite rather than relying on a single product.

On the Salesforce AppExchange, the company has expanded beyond Sales League to include CTI Ninja — an AI-powered call center solution launched in late 2024 or early 2025 that integrates computer telephony with Salesforce, offering features like 24/7 virtual agents, sentiment-aware conversations, and intelligent call routing. There is also Lead Manager Ninja for lead management and CRUD Magic for data operations.

The Salesforce products are strategically important because the AppExchange is one of the most visited enterprise software marketplaces in the world — a kind of App Store for enterprise software, where Salesforce's hundreds of thousands of customers browse for tools to extend the platform's capabilities. Every product listing is a storefront, and every download is a potential services lead. A CFO in Texas who discovers CTI Ninja while searching for call center solutions may end up hiring Ksolves to implement their entire Salesforce environment. The products punch far above their weight as marketing and sales tools — they cost relatively little to build and maintain, but they generate awareness and credibility that would cost millions to achieve through traditional marketing channels.

But the most intriguing product in Ksolves' portfolio may be the newest one: Data Flow Manager, or DFM. This is a tool designed to automate the deployment and management of Apache NiFi data flows — the complex pipelines that move data between systems in large enterprises. NiFi is powerful but notoriously difficult to manage at scale, and DFM aims to simplify the process with a one-click, UI-driven deployment interface, over 500 prebuilt data flows, an AI-powered flow creation assistant, and role-based access controls.

To understand why DFM matters, consider the pain it addresses. Managing NiFi data flows across multiple clusters in a large enterprise is like orchestrating a symphony where every musician is playing from a different score in a different key. Data engineers spend enormous amounts of time manually deploying, testing, and troubleshooting flows. DFM automates much of this work, and crucially, it runs entirely on-premises — no cloud dependency — which matters enormously for clients in regulated industries like banking and healthcare where data sovereignty is non-negotiable.

DFM is in its early stages but the early signals are striking. The company's first customer — a company with 13 billion dollars in revenue — paid approximately 40,000 dollars for 50 nodes in its initial discounted deployment, and according to management, saves roughly 1.3 million dollars annually on flow deployment costs as a result. The pricing model charges approximately 10,000 dollars per node rather than per CPU, making it roughly 16 times more cost-effective than competing solutions.

A second customer was onboarded in mid-2025, and by the Q4 FY25 earnings call, the company had completed 12 product demonstrations to major enterprises including Red Hat, Airtel, and IBM, with positive feedback. With over 9,000 businesses globally using Apache NiFi and no identified competitor offering a comparable UI-based one-click deployment solution, the addressable market is meaningful.

If DFM gains traction, it could become a genuine enterprise software product with recurring revenue characteristics — not just a services lead generator but a standalone business. The fact that its first customer was a 13-billion-dollar-revenue enterprise — not a small startup experimenting with a new tool — suggests that DFM is solving a real, high-stakes problem that large organizations are willing to pay for.

On the services side, the numbers reveal a business that has achieved remarkable consistency. Approximately 78% of revenue comes from overseas clients, predominantly in North America, with growing contributions from Europe, the UAE, and Australia. The company established a wholly-owned subsidiary, Ksolves LLC, in the United States in June 2021, and the board approved the establishment of a 100% subsidiary in the UAE in July 2024, supported by delivery centers in Noida, Indore, and Pune.

Client retention stands at 90%, and 85% of revenue is recurring — meaning it comes from existing clients rather than new logos. These are critically important numbers. In IT services, the cost of acquiring a new client is dramatically higher than the cost of retaining an existing one, and repeat business is typically more profitable because the team already understands the client's systems, processes, and expectations. An 85% recurring revenue rate means Ksolves starts each year with a large base of committed revenue before winning a single new logo.

The top five clients account for about 40% of revenue, and the top ten for roughly 53%, which represents moderate concentration risk but is well within norms for a company of this size. Tellingly, the company now counts 11 clients with over one billion dollars in revenue and seven clients in the 200 million to one billion dollar range — a significant upgrade in client quality from the early days of small web development contracts.

The largest single contract signed as of the Q4 FY25 earnings call was 600,000 dollars, up dramatically from a previous maximum of roughly 120,000 dollars — a signal that the transition from time-and-materials billing to project-based delivery is yielding larger deal sizes. This fivefold increase in maximum contract value is arguably the single most important operational development in recent quarters, because it demonstrates that Ksolves can compete for and win engagements of a size that was previously beyond its reach.

One detail from the financials deserves attention here because it captures the operational leverage of the model. In FY24, Ksolves generated approximately 109 crore rupees in revenue with about 500 employees — roughly 21-22 lakh rupees per employee. For context, the Indian IT services industry average is somewhere around 15-18 lakh rupees per employee for mid-sized firms. The larger players like TCS and Infosys generate higher absolute revenue per employee, but they also carry significantly higher cost structures — global offices, large management hierarchies, marketing budgets, and the overhead of supporting hundreds of thousands of employees. Ksolves achieves competitive per-employee productivity with a fraction of the overhead, and the difference flows straight to the bottom line.

The talent engine is another critical piece of the operational picture, and arguably the one that most determines whether Ksolves can sustain its growth trajectory. With over 565 employees and a 25% headcount increase in 2024, Ksolves faces the same challenge as every Indian IT firm: attracting and retaining skilled engineers in a market where the competition for Salesforce-certified and Big Data-skilled talent is fierce. The company's Big Data practice, led by Technology Head Anil Kushwaha — an eleven-year Ksolves veteran and expert in Apache NiFi, Cassandra, and Spark — includes engineers who hold the prestigious Apache Cassandra DataStax Professional certification. These are not commodity skill sets that can be hired off a job board. They represent years of accumulated expertise in technologies that most engineering graduates have never touched.

The company's approach to talent retention involves a combination of ESOPs — the board granted 268,000 shares to key management, representing roughly 1% of outstanding capital — remote work flexibility across delivery centers in Noida, Indore, and Pune, and what management describes as a "learning culture." That last term could easily be dismissed as corporate jargon, but at Ksolves it carries specific meaning: engineers work across cutting-edge technology stacks rather than being pigeonholed into maintenance work. A developer might work on Salesforce implementation one quarter, Apache NiFi data flows the next, and an AI proof-of-concept after that. This variety is itself a retention mechanism — talented engineers stay because they are constantly learning, not because the company pays more than everyone else.

The establishment of an AI Center of Excellence in 2024, dedicated to training employees in generative AI, large language models, and intelligent automation, is both a talent retention tool and a strategic investment in future capabilities. The company also expanded its partnership ecosystem beyond Salesforce and Odoo to include Red Hat, Adobe, and AWS — each partnership creating new skill development pathways for employees and new revenue opportunities for the business.

The company's partnership ecosystem extends beyond its core technology areas. In 2025, Ksolves became a Red Hat ISV (Independent Software Vendor) Partner, adding another enterprise technology vendor to its alliance portfolio alongside Salesforce, Odoo, Adobe, and AWS. Each partnership serves a dual purpose: it creates new revenue opportunities by connecting Ksolves to the partner's client base, and it provides employees with access to training and certification programs that serve as retention tools.

The Salesforce practice deserves particular attention because of the partnership dynamics involved. Salesforce organizes its partner ecosystem into tiers — Registered, Ridge, Crest, and Summit, in ascending order of prestige and capability. Each tier requires meeting specific thresholds for certifications, customer satisfaction scores, and delivery quality.

In March 2024, Ksolves achieved Salesforce Summit Partner status — the highest tier, previously known as Platinum. This required accumulating over 300 Salesforce certifications across the organization, a significant investment given that each certification requires individual exam preparation and testing. The Summit designation matters for a reason beyond branding: Salesforce actively refers clients to its highest-tier partners, creating a direct channel for deal flow that lower-tier firms cannot access. When a large enterprise approaches Salesforce about a complex implementation and asks for partner recommendations, Summit partners appear at the top of the list.

For a company of Ksolves' size, achieving Summit status is remarkable. The typical Summit partner is a global consulting firm with thousands of Salesforce practitioners. Ksolves achieved it with a focused team where the ratio of certifications to total headcount is unusually high — roughly one certification for every two employees. This concentration of expertise is itself a competitive moat: it means that nearly every project team includes multiple certified specialists, which improves both the quality of delivery and the client's confidence in the team.

VI. Management and Capital Allocation: The Anti-Rollup

In the Indian IT services landscape, the standard playbook for growth-stage companies looks something like this: raise capital, acquire smaller competitors, consolidate billing relationships, cross-sell into the acquired client base, and repeat. Happiest Minds, Sonata Software, Mphasis — the sector is full of companies that have used M&A as a primary growth engine. The logic is straightforward: organic growth in IT services is capped by how quickly you can hire and train engineers, while acquisitions allow you to buy revenue, clients, and capabilities overnight.

Ratan Srivastava looked at this playbook and rejected it entirely.

To understand why, you need to understand the man. Srivastava is an engineer by training and temperament — a computer science graduate who spent the first decade of his career writing code and managing projects at Persistent Systems, Birlasoft, HSBC, and Tech Mahindra. He is not a dealmaker or a financial engineer. He is a builder. In earnings calls and investor presentations, he speaks about technology stacks and client problems with a granularity that suggests he is still deeply involved in the technical strategy of the company, not just the boardroom strategy. When discussing DFM's architecture or the nuances of Apache NiFi deployment challenges, he demonstrates a level of technical fluency that most CEOs of his tenure would have long ago delegated. This is not a founder who has "moved to the business side" — he remains, at his core, a technologist who happens to run a business.

He owns approximately 31.82% of Ksolves, which at the company's current market capitalization represents a holding worth several hundred crore rupees. That stake was not acquired through stock options, secondary purchases, or financial engineering — it represents the equity he built from scratch, starting from a single office in Indirapuram with a handful of developers. When Srivastava announces a dividend, he is writing a check to himself as much as to any outside shareholder. When he decides against an acquisition, he is passing up on empire-building with his own money. This alignment of incentives is rare in public markets, where the trend has been toward lower insider ownership and greater reliance on stock-based compensation.

Deepali Verma, the co-promoter and Whole Time Director, holds another 27.13%. Her background provides the commercial counterweight to Srivastava's technical orientation. She holds a Master of Commerce from Dr. B.R. Ambedkar University in Agra and has over 15 years of experience in sales, marketing, and organizational leadership. At Ksolves, she leads the sales, marketing, and UI/UX teams, and is credited with driving employee engagement, cultural transformation, and workplace design.

In a company where the CEO is focused on technology strategy and high-level client relationships, Verma's role in building the organizational infrastructure — the hiring processes, the cultural norms, the physical and virtual work environments — is arguably just as important to Ksolves' success. The complementarity between Srivastava and Verma — technical depth paired with commercial and organizational acumen — is a common pattern in successful founder-led companies, and the fact that both are deeply invested financially means neither has an incentive to undermine the other.

The CTO, Manish Gurnani, rounds out the senior leadership triangle with a profile that is unusually diverse for a technology executive. Gurnani holds a PGDM in Finance from IIM Lucknow — one of India's premier business schools — and has worked at Bank of America, Tech Mahindra, Infogain, and SDG Software Technologies before founding his own venture, Matreh Technology. He joined Ksolves as a Senior Technology Architect and rose to CTO, where he drives the expansion into AI, machine learning, and Big Data.

His financial training from IIM combined with deep technical expertise gives him a rare ability to evaluate technology investments through both a capability lens and a returns lens. When Gurnani decides to invest engineering resources in Data Flow Manager or the AI Center of Excellence, he is thinking not just about technical feasibility but about the return on that investment relative to alternative uses of the same engineering talent.

The combined promoter holding of approximately 59% is unusually high for a listed Indian IT company and creates what investors call "skin in the game." When management owns a majority of the equity, every strategic decision — every hiring push, every product investment, every dividend declaration — directly affects their personal wealth. This alignment eliminates the classic agency problem where hired managers pursue empire-building or excessive risk-taking because they bear little personal downside.

The capital allocation philosophy that flows from this ownership structure is almost aggressively simple. Ksolves generates high margins — EBITDA margins have ranged from 25% to 40% depending on the quarter, with a stated medium-term target of around 30%. The company operates with minimal capital expenditure because software services require people, not factories. And rather than hoarding the resulting cash flow for acquisitions or building a war chest, management returns the vast majority of it to shareholders through dividends.

The numbers are striking. In FY25, the company declared total dividends of 23.50 rupees per share across three tranches — including a single interim dividend of 8 rupees in October 2024 and 7.50 rupees in March 2025. Through the first three quarters of FY26, the company had already declared cumulative interim dividends of 11 rupees per share across three payments of 1 rupee, 5 rupees, and 5 rupees.

At the current share price, the trailing twelve-month dividend yield sits at approximately 6.5% — extraordinary for a growth company targeting 20% revenue growth. This level of shareholder returns is extremely unusual in the technology sector. Most growth companies argue that they should retain earnings and reinvest for compounding.

Srivastava's counterargument, implicit in his actions, is elegant: Why retain capital when the business generates return on capital employed above 200%? The incremental investment needed to grow 20% annually is small relative to the cash the business produces. The surplus should go back to the people who own the company.

There is a Warren Buffett-esque quality to this approach. Buffett has long argued that the best companies are those that can reinvest earnings at high rates of return, and that companies which cannot do so should return capital to shareholders rather than deploying it in low-return acquisitions or vanity projects. Ksolves may be too small to appear on Berkshire Hathaway's radar, but the capital allocation philosophy would resonate deeply with the Sage of Omaha: earn high returns on invested capital, keep what you need, give back the rest.

The anti-M&A stance reinforces this logic, and it is worth dwelling on because it is so unusual in the Indian IT services landscape. Consider the track record of M&A in mid-cap Indian IT. Happiest Minds acquired PGS Group in 2022 and Macmillan Learning's India operations. Sonata Software acquired Quint Wellington Redwood. Mphasis has made multiple acquisitions to expand its digital capabilities. Each of these deals came with integration costs, earn-out provisions, cultural friction, and the inevitable distraction of senior management attention. Some have worked out well; others have delivered mediocre returns. But all of them consumed capital that could have been returned to shareholders or invested organically.

Acquiring another IT services firm typically costs 15 to 25 times EBITDA, sometimes more for specialized firms with attractive technology capabilities. Integration is risky — culture clashes between the acquiring and acquired teams, client attrition during the transition period, technology incompatibilities between different delivery platforms, and management departures when founders or key leaders cash out are all common. Goodwill write-offs are endemic in the sector.

And even when acquisitions succeed — when integration goes smoothly, clients stay, and cross-selling materializes — the returns on the capital deployed rarely exceed 15-20%.

Compare that to Ksolves' organic growth. Hiring a new Salesforce developer costs the company perhaps a few lakhs in recruitment and training. That developer begins generating revenue within weeks, at billing rates that deliver returns on the investment of several hundred percent.

Building a new product like Data Flow Manager requires a team of engineers working over months, but the capital investment is the opportunity cost of their time — no external funding required. The math is not close. Every rupee invested organically in hiring, training, and product development generates dramatically higher returns than any acquisition could.

The result is a balance sheet that looks almost comically clean for a technology company. The company operates as essentially debt-free, with only minimal working capital borrowings that were largely paid down by September 2025. There is no goodwill, no intangible assets from acquisitions, no earn-out liabilities, no minority interests. Just clean cash generation and clean distribution. In an industry where bloated balance sheets and serial acquisition write-offs are the norm, Ksolves' financial simplicity is its own kind of competitive advantage — it means that every rupee of reported profit is real, tangible cash that can be distributed to shareholders or reinvested at extraordinary returns.

The recent leadership hires tell the story of a company preparing for its next phase of growth. Jerry Huang joined as Vice President — a significant hire given his background as a former Director at Salesforce Australia and Global Head of Salesforce at Infosys. Aseem Kumar, an IIT Kanpur alumnus, was brought in as Director of Program and Operations. Nishant Agrawal, Vice President of Engineering, leads the AI and machine learning expansion. And Darpan Audichya serves as Head of Business Transformation and Consulting, specializing in RFP development and enterprise sales processes. Umang Soni handles the CFO responsibilities.

These hires — particularly Huang's Salesforce pedigree and Kumar's IIT credentials — represent a deliberate upgrade of the leadership bench, addressing the key man risk concern while bringing world-class institutional experience to a company that had previously run lean on senior talent.

The board includes independent directors Varsha Choudhary, Varun Sharma, Sushma Samarth, and Vineet Krishna — providing governance oversight appropriate for a main-board listed company. The company also won the Deloitte Technology Fast 50 India 2024 award in the Data and AI Tech category — received by CTO Manish Gurnani and Business Development Head Kirti Sharma at a ceremony in Bengaluru in December 2024 — and earned the NASSCOM Impact Award 2025, further cementing its reputation beyond the small-cap investor community.

VII. Competitive Advantage and Frameworks

To evaluate Ksolves' competitive position rigorously, it helps to apply two widely used strategic frameworks: Michael Porter's Five Forces and Hamilton Helmer's Seven Powers. These frameworks reveal both the structural challenges Ksolves faces and the specific advantages it has built to navigate them.

It is important to note that these are not theoretical frameworks being applied retrospectively to justify an investment thesis. They are diagnostic tools for understanding whether Ksolves' current competitive position is durable or whether it is a temporary advantage that competitors will eventually erode. The distinction matters because Ksolves' premium valuation relative to other small-cap IT services firms is only justified if its advantages are structural rather than cyclical.

Starting with Porter's Five Forces, the picture is sobering — and that sobriety is precisely what makes Ksolves' performance so impressive.

The rivalry among existing competitors in Indian IT services is intense — perhaps the most competitive services market in the world. Thousands of firms, from giants like TCS with over 600,000 employees and Infosys with over 300,000, down to two-person shops operating out of co-working spaces, compete for the same pool of global clients. Price pressure is relentless at the lower end of the market, and even at the higher end, clients regularly benchmark their providers against alternatives. The large firms compete through scale, brand, and existing relationships. The mid-caps compete through specialization and agility. And the small firms compete on price — often destructively so, driving margins across the industry toward commodity levels.

The threat of new entrants is similarly high. The barriers to starting an IT services company in India are almost nonexistent: a computer science degree, a laptop, and an internet connection. Every year, hundreds of new firms enter the market, many competing on price alone. This constant influx of new competitors keeps pricing pressure high across the industry.

Supplier power — which in this industry means the power of skilled engineers — is also elevated. India produces a large number of computer science graduates each year, but the subset with genuine expertise in niche technologies like Salesforce, Apache NiFi, or generative AI is much smaller. These specialists can command premium salaries and are constantly recruited by competitors. Wage inflation for skilled tech talent in India has run at 8-15% annually in recent years, putting persistent pressure on margins.

Buyer power is moderate to high. Enterprise clients are sophisticated purchasers who run competitive RFPs, benchmark pricing, and often maintain panels of approved vendors that they can rotate. The saving grace for firms like Ksolves is that switching costs increase once a provider is embedded in mission-critical systems.

The threat of substitutes is evolving rapidly. AI-powered coding tools, low-code platforms, and increasingly capable automation are beginning to substitute for some categories of human software development. This is the existential question for the entire IT services industry and one we will address in the bear case.

Given this hostile competitive environment, how does Ksolves survive — let alone thrive? The answer maps neatly onto Hamilton Helmer's Seven Powers framework, which identifies seven durable sources of competitive advantage.

The most relevant power for Ksolves is counter-positioning. This is worth understanding deeply, because it explains how a 565-person company survives and thrives in an industry dominated by firms with hundreds of thousands of employees.

Ksolves occupies a strategic sweet spot that larger competitors cannot easily access. It is small enough to care deeply about deals worth 50,000 to 500,000 dollars — engagements that Accenture, Deloitte, and even mid-sized firms like Happiest Minds would consider too small to pursue.

Think about the math from Accenture's perspective: a 600,000-dollar Salesforce implementation project requires a partner, a project manager, a team lead, and several developers. The fully loaded cost of an Accenture partner's time alone — salary, benefits, office space, support staff — might eat half the project budget. The economics simply do not work for a firm with Accenture's cost structure.

But Ksolves can serve this segment profitably because its cost structure is fundamentally different. Its founders still actively participate in sales and delivery. Its office costs are a fraction of a global consulting firm's. Its hierarchy is flat, its overhead is minimal, and its engineers work from tier-two Indian cities where the cost of living — and therefore salary expectations — are materially lower than in Mumbai or Bangalore.

And yet the quality of output, validated by Summit-level Salesforce partnership and CMMI Level 3 certification, is enterprise-grade. This creates a protected niche where Ksolves can operate with less competitive pressure and higher margins than the headline industry dynamics would suggest.

The second relevant power is switching costs. When Ksolves implements a client's Salesforce environment, builds their data pipelines on Apache NiFi, or deploys their Odoo ERP system, it becomes embedded in the client's core operational infrastructure. These are not discretionary projects that can be paused or reassigned on a whim. They are mission-critical systems that process sales data, manage customer relationships, and move information between enterprise applications.

Replacing the team that built and maintains these systems involves months of knowledge transfer, significant risk of disruption, and the potential for costly errors during the transition. The 90% client retention rate and 85% recurring revenue from existing clients are direct manifestations of these switching costs.

The third power is what Helmer calls cornered resource — in this case, the product DNA culture that Ksolves has cultivated. Most IT services companies in India operate with a purely services mindset: take requirements, build to spec, deliver, and move on to the next project.

Building proprietary products requires a fundamentally different organizational capability — the willingness to invest without guaranteed returns, the discipline to maintain and iterate on a codebase over years, and the product management skills to understand market needs rather than just client specifications. Ksolves has demonstrated this capability repeatedly, from Dashboard Ninja to CTI Ninja to Data Flow Manager. Competitors who have been purely services companies for decades would find it extremely difficult to replicate this dual capability, even if they wanted to.

There is also an emerging element of process power — the operational systems and knowledge that Ksolves has built around its niche technology areas. With 300-plus Salesforce certifications, a dedicated Odoo team of over 100 specialists, and deep expertise in Apache Big Data tools, the company has accumulated institutional knowledge that would take years for a competitor to replicate. This is not just about individual talent — it is about the systems, templates, playbooks, and best practices that enable consistent delivery across hundreds of engagements.

Where Ksolves lacks Helmer's powers is also instructive. It does not have significant scale economies — its cost structure does not benefit from being larger in the way that a semiconductor fab or a cloud platform does. It does not have meaningful network effects — its products are useful regardless of how many other customers use them. And its brand power, while growing, is modest compared to industry leaders. These gaps define the boundaries of Ksolves' competitive position and help explain why the company is better suited to highly profitable niche dominance than to broad market leadership.

The competitive landscape comparison is worth making explicit. Among Indian IT companies with a Salesforce focus, Ksolves competes with firms like Persistent Systems, Zensar Technologies, and dozens of privately held boutique consultancies. Persistent, with revenue exceeding 9,000 crore rupees, operates at a vastly different scale but also in similar technology niches. The key difference is positioning: Persistent pursues larger, multi-year enterprise engagements, while Ksolves thrives in the sub-million-dollar segment where its cost structure and agility give it an edge.

In the Odoo ecosystem, Ksolves competes with firms like Brainvire, Pragmatic Techsoft, and other Indian Gold Partners — but its product portfolio, particularly Dashboard Ninja's market-leading position, gives it a visibility and credibility advantage that pure services competitors lack.

In Big Data and Apache technologies, the competitive set is smaller and more fragmented, which is precisely why Ksolves chose this niche — fewer competitors means less pricing pressure and more room for differentiation.

VIII. Bull vs. Bear Case

The Bull Case

The optimistic thesis for Ksolves rests on three pillars, each independently powerful and collectively compelling.

First, the "Baby LTIMindtree" thesis. LTIMindtree, formed through the merger of L&T Infotech and Mindtree, is a roughly 35,000-crore-rupee revenue IT services company that built its early success on exactly the same strategy Ksolves is executing today: niche specialization, deep technology expertise, and a focus on high-margin engagements. L&T Infotech in its early years was similarly focused on specific technology domains, maintained higher margins than the industry average, and grew organically before eventually using M&A to accelerate its trajectory. The argument is that Ksolves is at an earlier point on the same growth curve, with the potential to scale from its current revenue base of approximately 153 crore rupees to 500 crore or more over the next several years while maintaining its margin superiority.

The math supports the possibility. The Indian IT services industry is enormous — over 250 billion dollars in exports alone, growing at a mid-to-high single-digit rate annually. Ksolves' current revenue is less than 0.01% of this market. Even a tiny increase in market share — from 0.01% to 0.05%, say — would represent a fivefold increase in Ksolves' revenue. The Salesforce ecosystem alone is projected to generate trillions of dollars in economic activity through its partner network by 2028. The Odoo community is one of the fastest-growing enterprise software ecosystems in the world. And the demand for Big Data and AI implementation services is accelerating as enterprises race to build the data foundations required for generative AI deployments. The growth opportunity is not constrained by market size — it is constrained only by Ksolves' ability to hire, train, and deploy talent fast enough to capture it.

Second, the AI and machine learning expansion. Ksolves' investment in an AI Center of Excellence and its growing practice around generative AI, natural language processing, and intelligent automation positions it to ride the next wave of enterprise technology spending. Currently, AI-related work represents a relatively small share of revenue, but billing rates for AI implementations are significantly higher than traditional development work. As enterprises move from AI experimentation to production deployment, the demand for implementation partners with genuine expertise — as opposed to firms that have slapped "AI" on their marketing materials — will be enormous. Ksolves' track record of building deep expertise in emerging technologies suggests it can capture a meaningful share of this demand.

Third, the product optionality. If Data Flow Manager gains traction as an enterprise software product — and the early signs, including a customer with 13 billion dollars in revenue, are promising — it could transform Ksolves' valuation framework. Enterprise software products are valued on recurring revenue multiples that can be 10 to 20 times higher than the earnings multiples applied to IT services companies. Even if the product division remains small relative to services, a successful product with SaaS economics could contribute disproportionately to the company's market value. The dividend policy provides a floor for investor returns while waiting for this optionality to materialize.

The macro environment is also supportive. Global spending on Salesforce ecosystem services continues to grow — Salesforce itself projects that its partner ecosystem will generate over six trillion dollars in economic activity by 2028. The Odoo community is expanding rapidly, with the platform gaining share against SAP and Oracle in the mid-market, driven by the appeal of open-source economics and faster implementation timelines. Enterprise data infrastructure spending is accelerating as companies try to build the data foundations required for AI. And Indian IT services as a sector continues to benefit from the global trend toward outsourcing complex technology work to lower-cost, high-skill markets.

The dividend policy adds an additional layer to the bull case that is often underappreciated. At a trailing twelve-month yield of approximately 6.5%, Ksolves provides a level of income return that is unusual for a growth company. This creates a floor for total shareholder returns — even if the stock price stagnates, investors are receiving a meaningful cash yield. For income-oriented investors who want growth exposure without sacrificing current returns, this combination is rare and valuable.

The Bear Case

The risks to the Ksolves story are real and should not be dismissed by investors who are seduced by the headline return on capital figures.

The most immediate concern is key man risk. Ratan Srivastava is the architect of Ksolves' strategy, the face of the company to major clients, and the decision-maker on technology bets. He and Deepali Verma together control nearly 59% of the equity. The company has built a capable management team around them — Gurnani as CTO, Soni as CFO, Agarwal in engineering — and the hiring of Jerry Huang from Salesforce/Infosys and Aseem Kumar from IIT Kanpur represents a deliberate effort to deepen the leadership bench.

But there is no question that the loss or disengagement of the founder would create significant uncertainty. In a 550-person company, the CEO's involvement in client relationships and strategic decisions is far more concentrated than in a 50,000-person firm. Investors should pay close attention to any changes in promoter activity, health, or engagement.

Platform risk is the second major concern. Ksolves' fortunes are meaningfully tied to the Salesforce and Odoo ecosystems. If Salesforce's growth were to slow materially — due to market saturation, competitive pressure from Microsoft Dynamics or HubSpot, or a shift in enterprise buying patterns — Ksolves' largest practice area would be directly impacted. Similarly, if Odoo were to change its partnership structure, face security concerns, or lose market share, the product and services revenue tied to that ecosystem would be at risk. Concentration in specific technology platforms creates focus and expertise, but it also creates vulnerability to shifts in those platforms' fortunes.

The AI disruption question is perhaps the most intellectually interesting risk. The IT services industry's fundamental value proposition is that skilled engineers can do work that clients either cannot do internally or can do more cheaply through outsourcing. But AI-powered coding assistants — GitHub Copilot, Amazon CodeWhisperer, and their successors — are rapidly improving at tasks that junior and mid-level developers currently perform. If these tools continue to improve at their current pace, the demand for human developers for routine coding tasks could decline significantly. The counter-argument is that AI creates as much work as it displaces — someone needs to implement, customize, and maintain AI systems — but the transition period could be painful for firms whose billing depends on large teams of developers.

There is also a subtler form of AI risk specific to Ksolves' business model. Salesforce itself is aggressively embedding AI into its platform through Einstein AI and Agentforce. If Salesforce's own AI capabilities become good enough to automate significant portions of the implementation and customization work that Ksolves currently performs, the demand for external consultants could decline even if the Salesforce ecosystem continues to grow. The platform's own intelligence could substitute for the consultant's expertise — a scenario where Ksolves' biggest platform partner inadvertently undermines its business model.

Ksolves has taken steps to address this risk by investing in AI capabilities and training its workforce. The company's AI Center of Excellence, the hiring of Nishant Agrawal as VP of Engineering with specific AI/ML expertise, and the integration of AI features into products like Dashboard Ninja with AI and CTI Ninja all suggest awareness.

The counter-positioning argument is also relevant here: Ksolves is well-positioned to become the firm that implements AI for its clients rather than the firm displaced by AI. Someone still needs to configure Salesforce's Einstein, build the data pipelines that feed AI models, and integrate AI outputs into existing business processes.

But execution over the next two to three years will be critical. The gap between "we have an AI Center of Excellence" and "AI represents a meaningful portion of our revenue at premium billing rates" is enormous, and crossing it requires sustained investment, capability building, and client education.