Knowledge Realty Trust: The Architects of India's Silicon Valley

I. Introduction & The "Knowledge" Thesis

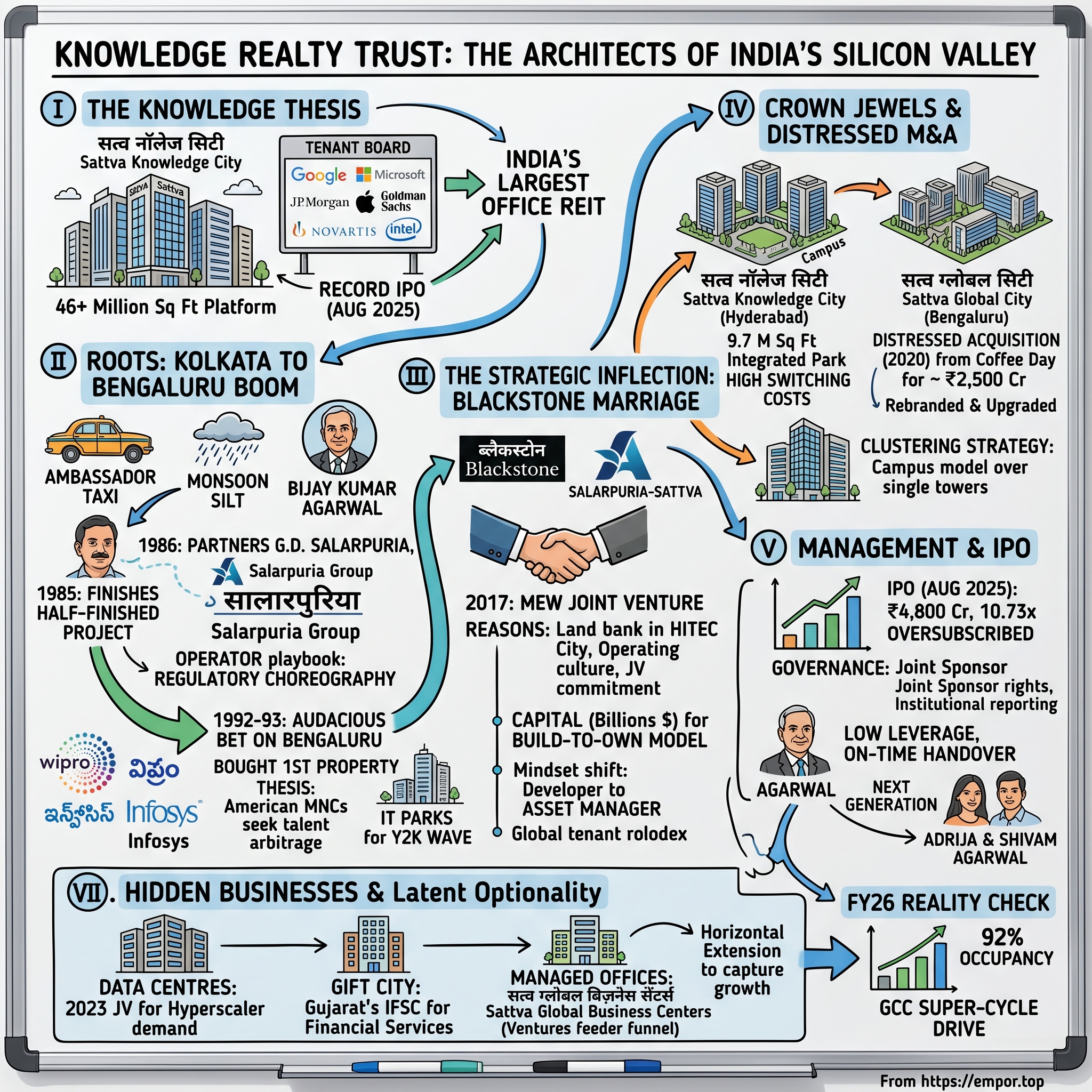

It is a humid May morning in 2026 in హైదరాబాద్ Hyderabad's HITEC City, and the eight-lane Outer Ring Road is already at a crawl. Air-conditioned shuttle buses inch toward a cluster of glass towers that, from a distance, look like any other Indian office park — sandstone-coloured podiums, mirrored facades, neat rows of palm trees. Then you notice the lobby tenant boards: Google, Microsoft, JP Morgan, Apple, Goldman Sachs, Novartis, Intel.1 On a single 30-acre parcel, more than fifty thousand engineers and analysts file in to write code for products that will be used by half the planet by sundown.

The building they walk into is owned by an entity most retail investors had never heard of two years ago — सत्व नॉलेज सिटी Sattva Knowledge City, the flagship of नॉलेज रियल्टी ट्रस्ट Knowledge Realty Trust (KRT.BO), India's newest and now its largest office REIT.

That is the through-line of this episode. How did a small Marwari-Bengali construction firm founded in कोलकाता Kolkata in the mid-1980s end up as the institutional landlord to the most valuable companies on earth? How did a partnership with ब्लैकस्टोन Blackstone — the firm that pioneered the modern office REIT in the United States — turn a regional developer into a 46-million-square-foot platform across six Indian cities?2 And what does the August 2025 IPO, the most subscribed REIT IPO in Indian history,3 tell us about how global capital wants to play the भारत में जीसीसी India GCC story for the next decade?

The asset under the microscope is simple to describe and hard to replicate. Knowledge Realty Trust owns 29 Grade-A office assets totalling roughly 46.3 million square feet, anchored by बेंगलुरु Bengaluru, Hyderabad, and मुंबई Mumbai, with the balance in Pune, चेन्नई Chennai, and a small footprint in गुरुग्राम Gurugram.1 About 95.6 percent of the portfolio's gross asset value sits in the top three cities — the same micro-markets where Apple's first India retail store, Google's largest engineering campus outside Mountain View, and Goldman Sachs's biggest non-US back office all live.2

The episode that follows is a story in five movements. The Salarpuria-Sattva origin story in Kolkata and the audacious 1992 bet on Bengaluru. The 2017 Blackstone joint venture that turned a builder into an asset manager. The opportunistic 2020 acquisition of Global Village Tech Park from a dead founder's estate. The 2025 listing that finally crystallised value. And the 2026 reality check — a market trying to figure out what a 92-percent-occupied, 46-million-square-foot Indian office REIT is worth in a world of hybrid work, falling interest rates, and an unstoppable wave of Global Capability Centres.

Pour yourself something cold. This one is going to take a while.

II. Roots: From Kolkata to the Bengaluru Boom

Picture Kolkata in 1985. The Hooghly is grey with monsoon silt, ambassador taxis honk through धर्मतला Dharmatala, and a thin twenty-something from a small Marwari trading family named Bijay Kumar Agarwal steps off a train and walks into a finance corporation job. Within months, the corporation's books reveal a familiar Indian small-business tragedy: a builder has defaulted on a half-finished residential project, and the finance company must either take possession or write it off. The corporation hands the keys to its newest hire, a young man who has never poured a foundation in his life, and tells him: finish the building.4

He finishes it. Then he finishes another. Somewhere along the way, the project meets a wiry, soft-spoken Marwari patriarch named G.D. Salarpuria, a Kolkata businessman who in 1986 had registered a modest construction outfit called the सालारपुरिया Salarpuria Group.5 Salarpuria saw in Agarwal what mentors always see in protégés — a willingness to do unglamorous work, an instinct for closing, and an unusual comfort with the slow, paper-heavy grind of Indian real estate development. The two of them stitched together a partnership that would define Indian commercial real estate for the next four decades. Salarpuria was the patient chairman, the man who held title and credibility; Agarwal was the operator, the one who showed up at the municipal office at 7 a.m. and stayed at the construction site until 9 p.m.

The accident of geography mattered enormously. Kolkata in the 1980s was a dying commercial city — its industrial base had collapsed, capital was fleeing for बंबई Bombay, and the state government's relationship with private enterprise was openly hostile. A construction company born in Kolkata in 1986 was, on paper, a terrible business. But Salarpuria and Agarwal made the move that defines the entire subsequent story: they got on a plane to Bengaluru in 1993 and bought their first piece of property there, a parcel that would become a building called Money Chambers.4 India had liberalised in 1991. Bangalore, sleepy and pensioner-filled, was about to become the back office of the world.

It is hard, from 2026, to convey how non-obvious this bet was at the time. In 1993, Bengaluru's tech industry was effectively विप्रो Wipro and इन्फोसिस Infosys — two homegrown software firms working out of converted bungalows. The city had no flyovers, no metro, no airport worth the name. Multinational tenants were a rounding error. Salarpuria-Sattva's instinct was that the city's tropical climate, English-speaking talent base, and accidentally well-run public university system would attract American companies looking to arbitrage their software engineering costs. It was a thesis that took ten years to play out and then compounded for the next thirty.

By the mid-1990s, the firm was building the first wave of बेंगलुरु Bengaluru IT parks — small Grade-B campuses, mostly leased to Indian software services companies preparing for the Y2K wave of outsourcing work. The buildings were unremarkable; the relationships were not. Agarwal learned, in those years, how to navigate the byzantine layers of Karnataka land conversion permissions, BBMP approvals, BESCOM power connections, and pollution-control consents that strangled most foreign developers. The Salarpuria operating playbook was less about architecture and more about regulatory choreography.

In 2003, G.D. Salarpuria died at the age of 74,6 leaving Agarwal effectively in charge of a firm whose founder had been its public face for eighteen years. The transition could have gone badly. Indian family-owned developers have a famous habit of fragmenting at exactly this moment, with second-generation heirs squabbling over land banks. It did not. Agarwal had spent two decades earning the trust of the Salarpuria family, and by the time the rebrand to सालारपुरिया सत्व Salarpuria Sattva was complete, he held the operating reins without question. He has held them ever since.

Two things about that era still matter for KRT investors today. First, the firm internalised an obsession with land. Every Salarpuria-Sattva tower built between 1995 and 2015 sat on freehold or long-lease land that the firm had bought directly, often years before the building was conceived. The cornered-resource power that KRT now enjoys in HITEC City and अउटर रिंग रोड बेंगलुरु ORR Bengaluru was acquired one parcel at a time, in transactions invisible to the market. Second, Agarwal built the firm with very little external equity. By 2015, Salarpuria-Sattva had completed roughly 15 million square feet and held 30 million more in various stages of development — but it had done so almost entirely on developer-style project debt, not patient institutional capital.4 That was the constraint a partnership with Blackstone was about to solve.

III. The Strategic Inflection: The Blackstone Marriage

In late 2017, two delegations met at the ओबरॉय Oberoi hotel in मुंबई Mumbai. On one side, partners from ब्लैकस्टोन ग्रुप Blackstone Group's real estate team, fresh off launching India's first listed REIT-precursor structures and looking for an operating partner outside their existing relationship with the एम्बेसी ग्रुप Embassy Group. On the other, Bijay Agarwal and a small team from Salarpuria-Sattva. The meeting, in the recollection of one former Blackstone India executive, was unusual in one respect: Agarwal did not pitch. He listened.

The conventional view at the time was that Blackstone — which had already built India's office market essentially single-handedly between 2012 and 2017 — would extend its existing Embassy partnership across the country. Embassy was bigger, more international, and had Mumbai-quality investor optics. Salarpuria-Sattva was a Bengaluru regional player with a Kolkata back office and a chairman who did not give interviews. Why did Blackstone pick the underdog?

Three reasons, as far as the public record allows reconstruction. First, the land. Salarpuria-Sattva had quietly assembled, over fifteen years, a portfolio of contiguous land parcels in HITEC City that no other developer could replicate. Hyderabad was about to become the most important office market in India — partly because of Telangana's pro-business government, partly because Bengaluru had simply run out of land — and Salarpuria-Sattva's HITEC City position was the single best land bank in the city. Second, the operating culture. Agarwal had a reputation as a "closer" — a developer who finished what he started, on time, with a tenant rent roll already signed. In Indian real estate, that was rarer than it should have been. Third, the alignment. Where Embassy had its own listed REIT ambitions and competing interests, Salarpuria-Sattva was prepared to make the joint venture the primary vehicle for its commercial portfolio.

The joint venture was structured as a series of asset-level transactions over the following years rather than a single platform deal. Blackstone contributed capital — billions of dollars of it — in exchange for majority economic interests in specific buildings. Salarpuria-Sattva contributed land, in-flight developments, and the entire local execution machine. The brand on the buildings stayed Sattva; the institutional ownership behind the brand became Blackstone. By 2024, the JV controlled roughly 48 million square feet across the country and had become, by gross asset value, the largest commercial real estate platform in India.7

The strategic shift this enabled is the whole reason KRT exists. Indian developers, almost without exception, run a "build-to-sell" model: assemble land, finance construction with expensive bank debt, lease the building, sell the asset to an investor, recycle the cash into the next land parcel. The model produces lumpy returns, mediocre quality (because the developer has no incentive to over-build), and tenants who get treated like one-night stands. Blackstone's capital let Salarpuria-Sattva flip into a "build-to-own" model, where the same firm developed the building, kept it on its balance sheet, and earned a multi-decade stream of rent and capital appreciation. The mindset shift — from developer to asset manager — is the single most important business change in this episode.

It also changed how Agarwal ran the company. The reporting cadence tightened. Building specifications crept upward — Knowledge City Towers, completed under the new regime, were built to LEED Platinum standards with district cooling and on-site sewage treatment, the kind of capex a build-to-sell developer would never have spent. Tenant retention became the operating KPI rather than units sold per quarter. Agarwal, who had spent twenty years building like a developer, now started thinking like a landlord.

Blackstone, for its part, brought something Salarpuria-Sattva could not have bought at any price: a global tenant rolodex. When the firm's New York office partners called their counterparts at JP Morgan or Goldman Sachs or माइक्रोसॉफ्ट Microsoft, they were calling people who already leased Blackstone buildings in eight other countries. Walking those relationships into a HITEC City pre-lease conversation accelerated the leasing cycle by years. The collaboration also gave Salarpuria-Sattva access to Blackstone's leasing analytics, its capital markets desk, and — eventually — its REIT structuring expertise.

By 2024, the JV had outgrown its private-market clothes. The portfolio was generating predictable cash flow, tenant concentration was diversified, and Indian REIT regulation had matured enough to support a sixth listing. The question stopped being whether the platform would list and became when.

IV. The "Crown Jewels" and Distressed M&A

The clearest way to understand what Knowledge Realty Trust actually owns is to walk through its two most important assets, because everything else in the portfolio is, at some level, a variation on these two patterns.

The first is सत्व नॉलेज सिटी Sattva Knowledge City itself, in Hyderabad's HITEC City. Built on roughly 30 acres of contiguous land assembled over years, the campus today is a 9.7-million-square-foot integrated business park with five mega towers, structured parking for thousands of cars, and an in-campus retail and food court that operates more like a small town centre than a commercial leasing amenity.8 Walk through it on a weekday and the tenant directory reads like a Bay Area corporate park's: Microsoft R&D, Google India, Apple, Goldman Sachs, JP Morgan Chase, Novartis, Intel, Siemens EDA, VMware, Hyundai Transys, Dun & Bradstreet, OakNorth Analytics.1

The economic logic of an asset like Sattva Knowledge City is worth pausing on, because it explains the entire KRT investment thesis. A single 50,000-employee tenant — say, a top-five global investment bank that has consolidated its India back office into 1.4 million square feet at Knowledge City — does not just sign a lease. It builds out a custom trading floor, brings in $80 million of internal capex, trains its talent on the local labour market, integrates with the neighbouring food courts and metro stations, and embeds itself into a recruiting flywheel where every Indian engineer's resume already lists "HITEC City" as the desired location. To move out, the tenant must rebuild all of that somewhere else. Switching costs in commercial real estate are usually thought of as moderate. In a Knowledge City context, they are very high — and that is the whole game.

The second crown jewel arrived through one of the more remarkable distressed transactions in recent Indian corporate history. In July 2019, the founder of कैफे कॉफी डे Café Coffee Day (Coffee Day Enterprises), V.G. Siddhartha, died by suicide off a bridge near मंगलुरु Mangaluru, leaving behind a tangle of personal guarantees, related-party loans, and a non-core commercial real estate holding called Global Village Tech Park in राजराजेश्वरी नगर Rajarajeshwari Nagar, on Bengaluru's southwest edge.

Global Village was no ordinary asset. The 90-acre campus housed a who's-who of Bengaluru's tech tenant base — including एक्सेंचर Accenture, माइंडट्री Mindtree, टेक महिंद्रा Tech Mahindra, and नोकिया Nokia — but had been pledged as collateral in a way that left the Coffee Day estate desperate for liquidity. The Coffee Day board, looking to settle creditor claims, approved the sale on September 17, 2019, valuing the property at roughly ₹2,700 crore.9

Six months later, in March 2020 — with the country effectively shutting down for the first Covid lockdown — a consortium of Blackstone (80 percent) and Salarpuria-Sattva (20 percent) closed the acquisition for approximately ₹2,500 crore.10 The payment was structured in three tranches: roughly ₹300 crore at closing, ₹1,700 crore in a second tranche, and the balance by year-end 2020.9 Almost every other potential bidder had pulled out as Covid uncertainty froze the office market. Blackstone and Sattva, looking at a fully-leased Grade-A asset with an in-place rent roll, kept their offer on the table and walked away with one of the lowest entry prices per square foot for a comparable Bengaluru campus in the last decade.

Did they overpay? On the day of closing, the headlines suggested they had: who wants to own offices in March 2020? With six years of hindsight, the answer is unambiguous. The campus was rebranded as सत्व ग्लोबल सिटी Sattva Global City, capex was poured into upgrading the common areas to Knowledge City standards, and the rent roll re-leased at substantial mark-to-market increases as Bengaluru's office market roared back through 2022 and 2023. The asset's contribution to KRT's gross asset value at IPO was several multiples of the acquisition price.

The Global City deal is important not just for the IRR. It tells you something durable about how the platform operates. Salarpuria-Sattva and Blackstone are willing to underwrite distressed assets at moments of maximum dislocation, on the strength of a long-term tenant thesis, and they have the balance sheet to actually close. In an Indian commercial real estate industry full of developers chasing the next residential tower launch, that is a genuinely different posture.

A second pattern visible across the portfolio is the deliberate clustering strategy. KRT does not, as a rule, own one tower in a city. It owns campuses — multi-building complexes on the same or adjacent parcels, where the operator can offer tenants the option to expand from 200,000 to 400,000 to 1 million square feet without ever leaving the parking lot. That clustering effect is what allows KRT to retain tenants through expansion cycles that would normally send them to a competitor.

By the time the firm started filing for its IPO in early 2025, it had aggregated 29 office assets totalling 46.3 million square feet, with an occupancy rate of 91.4 percent at filing.1 Roughly 95 percent of the portfolio's value was concentrated in Bengaluru, Hyderabad, and Mumbai — the three Indian markets where rent growth had structurally outpaced every other commercial real estate sub-sector for five years running.

V. Management: The Agarwal Dynasty and Blackstone Oversight

Bijay Agarwal does not give many interviews. The handful he has given over the last decade have a consistent character: short, technical, low on the personal-brand theatrics that Indian real estate moguls often indulge in. He is, by reputation, the kind of CEO who knows the rent roll of every tower he owns and can recite from memory which floor of which building a particular tenant occupies. People who have negotiated against him describe a man who prefers silence to pitches and who, when he does speak, is almost always closer to a "yes" than the room had assumed.

Agarwal's operating philosophy, distilled from years of interviews and the few profiles that exist of him, has three pillars.11 First, never overpromise on delivery dates. The firm's reputation for hitting handover dates with Fortune 500 tenants is the central marketing asset of the platform; missing one would damage the next ten lease negotiations. Second, never leverage to a level that prevents the next opportunistic acquisition. This is why Salarpuria-Sattva, despite being a developer in a developer-debt industry, has historically run lower leverage than its peers. Third, never split the operating company from the brand. Even after the Blackstone JV, the buildings carry the Sattva name. That brand equity, Agarwal has argued, is what wins tenant renewals.

The next generation is starting to appear. Agarwal's daughter Adrija Agarwal and son Shivam Agarwal have taken on visible roles inside the broader Sattva ecosystem, with Adrija driving strategy and सत्व ग्लोबल बिज़नेस सेंटर्स Sattva Global Business Centers — the firm's managed-office and flexible-workspace platform — and Shivam working on the residential and hospitality verticals that sit outside the REIT. The careful separation matters: the listed REIT contains the stabilised office portfolio; the family vehicle retains the development pipeline and the more exotic adjacencies.

The governance architecture of the REIT is where the Blackstone relationship really matters. Blackstone holds a 55 percent unit-holder stake in KRT, with Sattva holding 45 percent at listing.7 The investment management arm and asset management oversight are structured around joint sponsor rights, with Blackstone bringing the institutional reporting templates that REIT investors globally have come to expect. Quarterly reporting cadence, sustainability disclosures, tenant concentration breakdowns, weighted average lease expiry tracking — none of these are revolutionary for a US or Singapore listed REIT, but in the Indian office market they represent a quantum leap from the opacity that family-run developers had operated under for decades.

There is a phrase in Indian institutional real estate circles for what happens when a family-run developer accepts Blackstone capital: it is called "the Blackstone standard." Sleeves get rolled up; auditors get changed; the next round of capex gets approved by an investment committee that asks unromantic questions about cap rates and hold-period IRRs rather than which architect the chairman likes. KRT has been through this process completely. The result is a REIT that, on paper, looks less like a typical Indian property platform and more like a सिंगापुर Singapore-listed S-REIT — which is, of course, exactly the comparable foreign institutional investors were trained to underwrite.

The incentive structure is worth a paragraph. The REIT's management fees are split such that the sponsor (Sattva-Blackstone, jointly) earns base management fees on assets under management and performance fees tied to distributable cash flow growth. Because Blackstone holds 55 percent of the units, every rupee Sattva extracts from the REIT in management fees is, in some sense, coming out of Blackstone's pocket. That alignment is the structural reason KRT's expense ratios at listing came in tighter than several peer REITs.

The hardest question about the management story is succession. Agarwal is in his early sixties. Adrija and Shivam are visibly being groomed. But the Blackstone relationship is built on the personal trust between Agarwal and Blackstone's India real estate leadership, much of which has itself rotated through the firm's global offices over the years. The succession question is not whether Sattva can survive without Agarwal — the firm has institutional depth — but whether the next chapter preserves the operating culture that made the JV work in the first place.

For now, that question is unresolved. The relevant fact for investors is that the alignment between sponsor and unit-holders is unusually tight, that the governance overlay is unusually international, and that the management team has earned credibility on the one thing that matters most in real estate: they ship buildings on time.

VI. Hidden Businesses: Data Centres, GIFT City, and Managed Offices

A casual look at the KRT prospectus would suggest the REIT is a pure-play office story. That is true today. It is unlikely to be true in five years, and the seeds of what comes next are already visible in the broader Sattva ecosystem.

Start with data centres. Beginning in 2023, Sattva began publicly discussing a joint venture aimed at developing specialised data centre infrastructure in India, leveraging the same land bank advantages that had made the office platform successful.12 Indian data centre demand has been accelerating for two reasons: regulatory localisation requirements that force global cloud providers to host Indian customer data inside the country, and the absolute explosion of generative-AI compute demand that has every major hyperscaler scrambling for power-adjacent land. Sattva's land parcels — particularly in नवी मुंबई Navi Mumbai, चेन्नई Chennai, and Hyderabad — are unusually well-suited to data centre conversion because the firm acquired them when grid power, water, and fibre were available cheaply.

The REIT structure itself is well-suited to data centres in the long run. Hyperscale tenants like अमेज़न वेब सर्विसेज़ Amazon Web Services or गूगल क्लाउड Google Cloud sign 15- to 20-year triple-net leases that look, financially, exactly like investment-grade bond cash flows. That is the kind of contract a REIT investor will pay a premium multiple for. As of this episode's recording, the data centre assets sit outside the listed REIT, in the broader Sattva-Blackstone vehicle — but the explicit playbook articulated in the DRHP is that stabilised data centre cash flows would be candidates for eventual contribution into KRT.7

The second hidden business is the firm's exposure to गिफ्ट सिटी GIFT City in Gujarat — India's only operational International Financial Services Centre. GIFT City has spent the better part of a decade trying to attract financial services firms with regulatory carve-outs, tax holidays, and dollar-denominated transaction privileges, with mixed early results. The last two years have changed the picture. Global insurance reinsurers, foreign banks setting up resolution-and-recovery offices, and a handful of hedge fund administrators have started taking serious space in GIFT City, and the long-awaited inflection in tenant demand may finally be arriving. Sattva's early-mover position in commercial development in GIFT City does not yet contribute meaningfully to KRT's cash flow, but the option value is real.

The third — and most operationally interesting — adjacency is the managed-office business, branded as Sattva Global Business Centers. This is, in effect, a captive flex-office and co-working operator that sits inside the larger Sattva tech parks. Where a वीवर्क WeWork might sign a lease for 100,000 square feet inside a Knowledge City tower and then sub-let to startups, Sattva runs the same model under its own brand. The economic effect is twofold. First, it lets the platform capture the higher per-square-foot revenue that flex office commands without giving up margin to an intermediary. Second, and more strategically, it creates a feeder funnel: a thirty-person startup that takes a managed office in Sattva Global City today is the most natural tenant for a 30,000-square-foot direct lease in three years. The platform is, quietly, building a venture-style tenant acquisition pipeline.

None of these businesses are large today. None of them show up as material line items in the FY26 results. But together they represent the firm's answer to the most uncomfortable question facing any pure-play office REIT in 2026: where does growth come from once the Indian Grade-A office market hits saturation in the top three cities? The answer, in KRT's case, is that the platform is set up to extend horizontally — into data centres, into flex, into financial-services-zone-adjacent assets — without needing to acquire new land from scratch. That latent optionality is harder to value than the in-place rent roll, but it is real.

The investor takeaway is that the headline KRT story is a stabilised office REIT, but the embedded story — visible mostly through the sponsor pipeline — is a multi-asset Indian commercial real estate platform in formation. Whether that broader platform ever fully arrives inside the listed REIT vehicle, rather than remaining at the sponsor level, is one of the more interesting capital allocation questions in Indian REITs over the next five years.

VII. Playbook: Analysis and Frameworks

Step back from the asset-by-asset narrative and ask the analytical question: what kind of business is Knowledge Realty Trust, really? The clearest way to answer is through Hamilton Helmer's 7 Powers framework, because the most durable advantages here cluster around two of Helmer's seven, and the absence of others is just as informative.

The first and most important power is Cornered Resource. KRT's land positions in HITEC City, ORR Bengaluru, and Mumbai's पवई Powai and गोरेगांव Goregaon corridors are functionally impossible to replicate. The parcels were assembled over fifteen-plus years, often before the surrounding micro-market matured, and at price points that no developer entering today could match. To build a competing 9.7-million-square-foot integrated campus in HITEC City in 2026, a hypothetical entrant would need to (a) find contiguous 30-acre land, (b) navigate clearances that now take twice as long as they did a decade ago, and (c) underwrite a multi-year construction period during which the existing incumbents would lock down the marginal tenant. The land bank is, in effect, a moat that widens every year.

The second power is Switching Costs, and this is the under-appreciated one. Office leases superficially look like commodity contracts — a square footage, a rent per foot, a lock-in. They are not. A 1.4-million-square-foot tenant who has installed redundant power, built secure floors, embedded biometric access, and recruited a workforce that lives within a 15-kilometre radius of the campus is not going to move for a 5 percent rent reduction at a competitor. The operating cost of relocation, the productivity hit during transition, the talent attrition during the move — these are real and they are large. The clustering effect compounds the lock-in: a tenant who has 200,000 feet in one Sattva tower and the option to expand into 200,000 more in the adjacent tower has switching costs an order of magnitude higher than a tenant in a standalone building.

The third power, Scale Economies, applies in a softer form. Operating a 46-million-square-foot portfolio under one set of facility-management contracts, one set of utility purchasing agreements, and one centralised security and cleaning organisation produces real per-square-foot cost advantages over a 5-million-square-foot competitor. The savings are not enormous in absolute terms — perhaps 50 to 100 basis points of NOI margin — but at REIT-level multiples, those basis points compound into meaningful equity value.

The remaining four powers — Counter-Positioning, Network Economies, Branding, and Process Power — apply weakly or not at all to KRT. This is fine. A REIT does not need all seven powers. It needs the two it has, applied relentlessly.

Now flip to Porter's Five Forces. The Bargaining Power of Tenants is structurally high in commercial real estate, because tenants always have the option to take space at a competing building. But in KRT's case, the cornered-resource and switching-cost powers above mean that the realised bargaining power is much lower than it looks on paper. A Fortune 500 tenant negotiating a renewal on its existing Knowledge City floors is not going to walk away over a 10 percent rent increase, because the alternative is a multi-year, multi-million-dollar relocation.

The Threat of Substitutes is the question every office REIT investor has been asking since 2020: does hybrid work permanently shrink demand for Grade-A office space? The Indian answer, six years into the post-Covid era, looks meaningfully different from the American one. Indian office demand has not contracted; it has actually accelerated, driven by the Global Capability Centre wave (more on that in the next section). Indian engineers, on average, work from offices significantly more days per week than their American counterparts, partly because of cultural preferences, partly because home work environments in Indian metros are often genuinely inferior. The hybrid-work substitution risk for KRT is real but is dwarfed by the structural tailwind of GCC formation.

The Threat of New Entrants is moderate. Developing a competing campus is hard, as noted, but capital can flow into Indian commercial real estate from many directions — Singapore sovereign funds, US pension money, Indian insurance company allocations. What protects KRT is not the absence of capital; it is the absence of land. Capital can be raised in months; a 30-acre HITEC City parcel cannot be assembled in a decade.

The Rivalry Among Existing Competitors is the most interesting force, because KRT does not really compete with the other Indian REITs on an asset-by-asset basis. एम्बेसी ऑफिस पार्क्स Embassy Office Parks REIT, with roughly 51 million square feet, is the largest by absolute size, but its portfolio is concentrated in different micro-markets within Bengaluru.13 माइंडस्पेस Mindspace Business Parks REIT, at roughly 34 million square feet, overlaps in Hyderabad and Mumbai but is smaller in Bengaluru.13 ब्रुकफील्ड Brookfield India Real Estate Trust is the only fully institutionally managed REIT and skews to NCR. In practice, the listed Indian REITs compete more for institutional capital than for individual tenants, and the relevant comparison for KRT is less a fight for a specific tenant and more a fight for a specific basis point of foreign portfolio investor allocation.

The Bargaining Power of Suppliers — construction firms, materials suppliers, facility managers — is low. Indian construction is a buyer's market.

Putting the analytical frameworks together, KRT looks like a high-quality cornered-resource business with meaningful switching costs, operating in an industry where the most important strategic risk (hybrid work) is structurally smaller in its geography than in the global comparables.

VIII. The IPO and the Bull vs. Bear Case

The numbers around the IPO itself are worth getting right. Sattva and Blackstone filed the Draft Red Herring Prospectus with SEBI in March 2025, initially targeting a ₹6,200 crore issue.7 By the time the offering came to market, the size had been recalibrated to ₹4,800 crore, with the IPO opening for subscription from August 5 to August 7, 2025 in a price band of ₹95 to ₹100 per unit.14 The book was oversubscribed 10.73 times — the most subscribed REIT IPO in Indian history.3 Units listed on August 18, 2025, opening at ₹103 on the NSE and ₹104 on the BSE, a modest premium that reflected the discipline of the underwriters' price band rather than tepid demand.14

Anchor investors took roughly ₹1,620 crore of the deal before the public window opened, with foreign institutional investors taking the bulk and a meaningful Indian mutual fund allocation rounding out the book.14 The unit-holder register at listing was a mix of long-only sovereign wealth funds, global REIT specialists, and Indian institutional buyers — exactly the kind of patient capital base a long-duration income asset needs.

The bull case for KRT rests on three pillars, each of which has compounded since listing.

The first is the GCC supercycle. Global Capability Centres — captive offshore offices that multinational corporations operate to handle engineering, finance, analytics, and increasingly AI/ML work — have become the single largest source of net new Grade-A office demand in India. JLL's research suggests that GCC-led leasing has been the dominant driver of Indian office absorption over the last several years, with the centre count growing into the high hundreds.15 Every new GCC is, by definition, a multi-thousand-employee organisation that takes hundreds of thousands of square feet of premium office space. KRT's portfolio is concentrated in the exact three cities where this demand is most pronounced.

The second pillar is supply constraint. The pipeline of new Grade-A office completions in core Bengaluru and Hyderabad has not kept pace with absorption, partly because land approvals have become harder, partly because the pandemic delayed several speculative projects, and partly because the surviving developers are more disciplined about pre-leasing thresholds. The result is that effective rents in KRT's core micro-markets have inflected upward — a tailwind for any landlord with rent escalation clauses built into existing leases.

The third pillar is the interest rate cycle. REITs, as a yield-sensitive asset class, benefit when policy rates decline. The RBI's monetary stance over 2025 and into 2026 has been gradually accommodative, and the term structure of Indian rates has shifted in a way that improves the relative attractiveness of REIT distributions.

The bear case is, as ever, the mirror image. Concentration risk is real — roughly 95 percent of KRT's gross asset value sits in three cities, and within those cities, a handful of micro-markets dominate.2 A single regulatory event in Telangana, or a single major employer's decision to relocate, could meaningfully affect Hyderabad rents. Tenant concentration is similarly elevated; the top ten tenants represent a substantial share of in-place rent, and although each is investment-grade, a global investment bank's cost-cutting decision can ripple through Indian back-office space planning quickly.

Hybrid work remains a slow-burn risk. Even if Indian office attendance is structurally higher than American, the global headquarters making the seat-allocation decisions are increasingly run by executives who themselves work hybrid. Three- or four-day return-to-office norms become embedded in capacity planning, and over a five-year horizon, even a 10 percent reduction in seat density assumptions reduces the trajectory of office demand growth.

The "shadow supply" risk is the under-discussed one. The other listed Indian REITs — Embassy, Mindspace, Brookfield — are themselves capable of acquiring new buildings and contributing them into their own listed vehicles, increasing aggregate listed-REIT supply and competing for the same FII allocation that KRT depends on. The Nifty REITs index has crossed ₹1.6 trillion in market cap, but that is still a thin float relative to the size of foreign capital that might want to own Indian commercial real estate over the next decade.13

The early results have given the bulls more to work with than the bears. For the quarter ended March 31, 2026 — Q4 FY26 — KRT reported net operating income of ₹1,053 crore, up 14 percent year-on-year.16 Full-year FY26 NOI grew 18 percent to ₹4,048.4 crore, and the board declared a Q4 distribution of ₹1.616 per unit, taking the FY26 cumulative distribution to ₹4.74 per unit and the total distribution since the August 2025 listing to approximately ₹2,102 crore.17 Q4 FY26 gross leasing came in at 1.1 million square feet, taking cumulative FY26 leasing to 3.5 million square feet and portfolio occupancy to 92 percent.17 The Q4 FY26 portfolio valuation report pegged total market value at ₹67,411 crore.18 The first three quarters as a listed REIT have, by any reasonable measure, hit or exceeded the underwriting case.

A brief myth-versus-reality digression is worth a paragraph. The consensus narrative around Indian REITs has been that they are a "bond-substitute" yield product unsuited to capital appreciation. The reality, looking at the 2025 and early-2026 returns across the listed Indian REIT complex, is that unit prices have meaningfully outperformed broader equity indices on a total-return basis, driven by NOI growth that has surprised to the upside. KRT, as the newest and largest of the listed REITs, has been the most pronounced beneficiary of this re-rating.

The KPIs to watch for KRT, narrowed to three, are: (1) portfolio occupancy — the single best leading indicator of NOI direction and the cleanest measure of whether the leasing engine is keeping pace with new completions; (2) re-leasing spreads on lease renewals, which tells investors whether the cornered-resource and switching-cost story is translating into real rent pricing power; and (3) distribution per unit growth, which is, in the end, the only number that determines whether unit-holders are getting paid for owning the trust.

IX. Conclusion and Final Reflections

The Knowledge Realty Trust story is, at one level, the most boring kind of business story: a regional construction firm assembled good land, partnered with patient global capital, built better buildings than its competitors, attracted sticky tenants, and eventually packaged the stabilised cash flow into a listed yield vehicle. There is no transformational technology pivot, no founder cult, no death-defying turnaround. It is a forty-year compounding story, executed quietly, by people most of the country has never heard of.

But the broader significance is harder to miss. Without realising it, India spent the last thirty years building the physical substrate of the global knowledge economy. Every customer service call routed to Bengaluru, every credit risk model run out of Hyderabad, every iPhone supply chain managed out of Mumbai — all of it sits inside buildings that someone had to design, finance, build, and operate. Salarpuria-Sattva, in partnership with Blackstone, ended up owning a disproportionate share of those buildings, and KRT is the financial instrument that lets ordinary investors participate in the resulting cash flow.

What comes next is the more interesting question. Sattva's next chapter is visibly tilted toward extension — into data centres for the AI buildout, into managed offices for the startup demand wave, into Mumbai and Pune for geographic diversification, into a possible "knowledge-hospitality" crossover where the platform layers branded extended-stay residences and conference infrastructure on top of its existing tech park footprint. None of these are guaranteed to compound at the rate that the office business has, but the same operating playbook — cornered land, patient capital, institutional governance — is portable across all of them.

The Agarwal succession is the open variable. So is the path of the rupee, the durability of the GCC story, and the question of how many more REITs the Indian market can absorb without compressing the multiple that KRT enjoys. The answers to those questions will determine whether KRT is, in 2036, a 100-million-square-foot platform with a Singapore-listed dual share class and a serious data centre business, or simply a high-quality Indian office REIT that did its job for unit-holders.

Either outcome would, by the standards of how this story began in a half-built Kolkata residential project four decades ago, count as a remarkable second act for the protégé who finished the building no one else wanted to touch.

References

References

-

Knowledge Realty Trust REIT IPO 2025: Full Investor Guide — Share.Market ↩↩↩↩

-

Knowledge Realty Trust REIT IPO: India's Largest Office REIT — ForgeUp News, 2025 ↩↩↩

-

Sattva–Blackstone-backed Knowledge Realty Trust sets record as India's most subscribed REIT IPO — Torbit Realty, 2025 ↩↩

-

Story of Bijay Agarwal, MD, Salarpuria Sattva Group — YourStory, 2013-10 ↩↩↩

-

Salarpuria Group emerges as a force to reckon with — Business India ↩

-

India's largest REIT IPO: Blackstone, Sattva Developers file DRHP with SEBI — Business Standard, 2025-03-07 ↩↩↩↩

-

Blackstone Group and Salarpuria Sattva jointly acquired Global Village Tech Park for ₹2,500 crore — RealtyNXT, 2020-03-16 ↩

-

Bijay Agarwal, MD Salarpuria Group — Salarpuria Sattva Official ↩

-

Blackstone-Sattva REIT to raise ₹4,800 crore via IPO in August 2025 — Business Standard, 2025-06-17 ↩

-

Embassy REIT, Mindspace, Brookfield: Best Indian REIT for 2026 — Terranexxus ↩↩↩

-

Knowledge Realty Trust REIT IPO Lists at 3% Premium; Strong Market Debut — Torus Digital, 2025 ↩↩↩

-

Knowledge Realty Trust posts 14% growth in Q4 FY26 NOI at ₹1,053 crore — Business Standard, 2026-05-13 ↩

-

Knowledge Realty Trust delivers strong Q4 FY26 results — ForPressRelease, 2026 ↩↩

-

Knowledge Realty Trust Q4FY26 Portfolio Market Value at INR 674,111 Mn — Scanx ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube