KRN Heat Exchanger: The Silent Engine of India's Cooling Boom

I. Introduction: The 213x IPO Moment

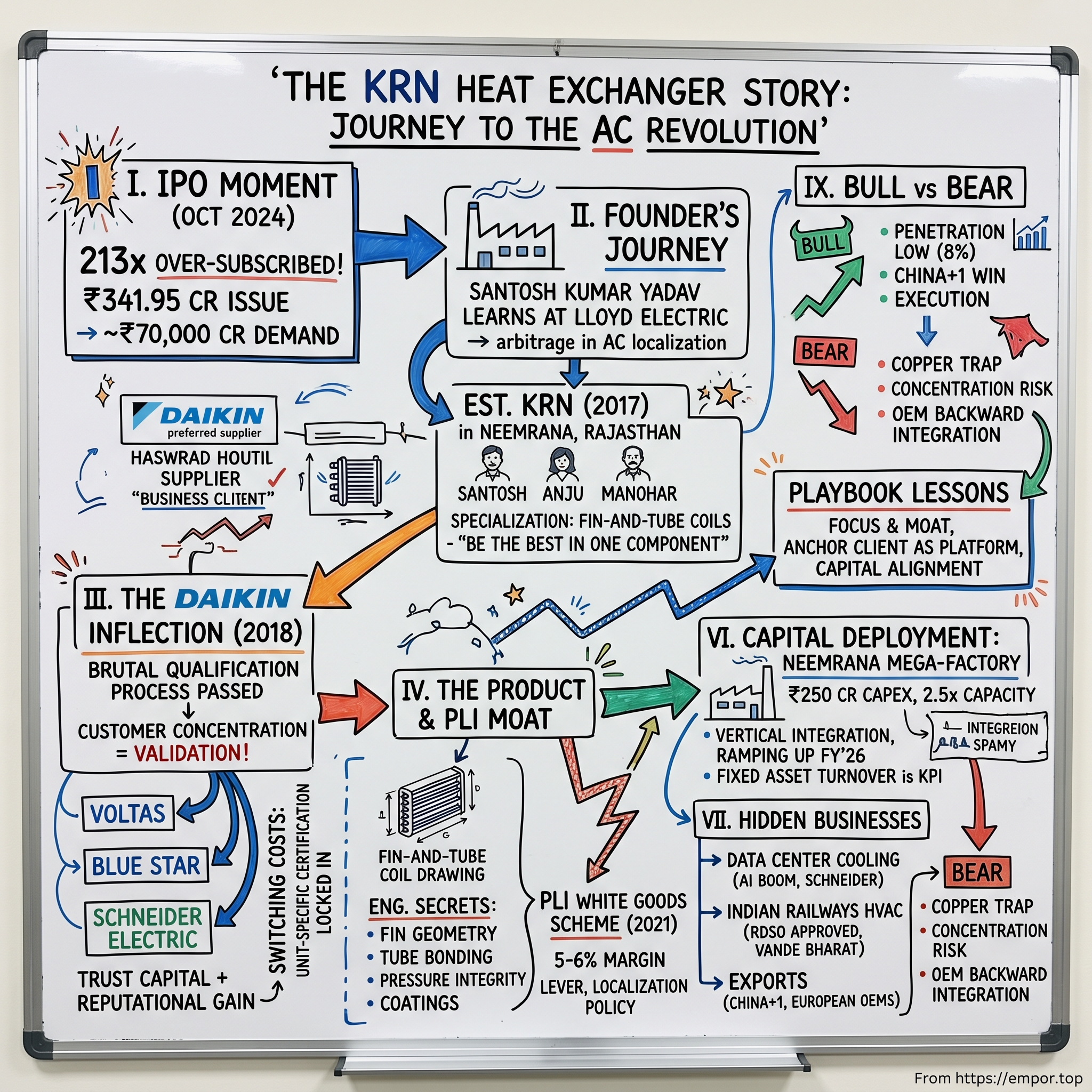

It was the last day of September 2024, and somewhere in a windowless dealing room in Mumbai's Bandra Kurla Complex, a syndicate banker was refreshing his screen with the expression of a man watching a slot machine pay out. The numbers were no longer moving in increments. They were doubling. Tripling. By the time the book closed at 5:00 PM on Friday, September 27, 2024, the initial public offering of a company that almost nobody outside the Indian air-conditioning supply chain had heard of, was sitting on subscription numbers that nearly broke the model. The retail portion was oversubscribed 130 times. The non-institutional investor portion: 424 times. The qualified institutional buyer book: 264 times. Aggregate: 213.41 times.[^1]

The company was called KRN Heat Exchanger & Refrigeration Ltd. The issue size was a modest ₹341.95 crore. The demand was somewhere north of ₹70,000 crore — roughly $8.4 billion in retail-level bids chasing about $40 million worth of paper.[^1] In a market that had grown weary of "story" IPOs from food delivery apps and quick-commerce hopefuls, here was something stranger. An industrial component supplier from a sleepy industrial estate near नीमराना Neemrana, in Rajasthan, was being treated like a tech unicorn. On listing day, October 3, 2024, the stock opened at ₹480 against an issue price of ₹220, a 118% pop, and traded as high as ₹524 before settling.1

The question that hung in the air, both for analysts who covered the consumer durables space and for the army of retail investors watching CNBC-Awaaz on mute in the background, was deceptively simple. Why? Why does an industrial component maker — a business that does not make finished goods, has no brand on a showroom floor, and operates almost entirely in the unglamorous middle of a B2B value chain — command this kind of demand?

The answer, as the next two hours will unpack, is that KRN is a near-perfect case study in the "picks and shovels" trade applied to one of the largest demographic-meets-climate stories of the next decade: the Indian air-conditioning revolution. India's room AC penetration in 2024 was around 8% — about where China was in 1995, and roughly one-tenth of where the US has been for forty years. The runway is, to use a phrase that gets thrown around too liberally on Indian financial television but happens to be correct here, generational.

And while everyone has been busy debating whether Voltas or Blue Star or LG will win the share war for the finished AC unit, KRN quietly positioned itself as the supplier all of them must use. They make heat exchangers — specifically, the fin-and-tube coils that are the literal beating heart of any cooling appliance. Without that coil, the AC outside your window is a fan in a metal box.

Across the next ten chapters, we trace how a first-generation founder from the Rajasthan industrial belt — a former Lloyd Electric executive named संतोष कुमार यादव Santosh Kumar Yadav — built a Tier-1 supplier to companies like डायकिन Daikin, Voltas, Blue Star, and Schneider Electric, in under a decade. We will look at the moat (it is more interesting than it first appears), the customer concentration (which is alarming if you take it at face value, and reassuring if you do not), the new ₹250+ crore mega-factory in Neemrana, and the optionality embedded in two side businesses — डेटा सेंटर data center cooling and भारतीय रेलवे Indian Railways HVAC — that the IPO prospectus barely bothered to mention.

This is not just an IPO story. It is a story about specialization as a strategy, about anchor customers as platforms, and about what happens when a small, focused Indian manufacturer manages to insert itself into the supply chain of a global energy transition. Welcome to KRN.

II. The Founder's Journey: Santosh Kumar Yadav & the Lloyd Legacy

To understand KRN, you have to understand the strange purgatory that the Indian air conditioning industry occupied between roughly 2000 and 2015. The big consumer brand names you would recognize — Voltas, Blue Star, Hitachi, LG — were largely assemblers. They imported coils, compressors, and control boards from China, Thailand, and Malaysia, screwed them into a metal cabinet at a plant in Pune or Sanand, slapped on a BEE star-rating sticker, and shipped them out to dealers. The "Made in India" label was, in many cases, a polite fiction. The high-spec engineering work — heat exchanger design, refrigerant flow optimization, anti-corrosive coating chemistry — happened somewhere along the eastern seaboard of China.

The exception, and it is a critical exception for our story, was Lloyd Electric. Lloyd, before its 2017 acquisition by Havells, was one of the few Indian companies that had attempted vertical integration on heat exchangers — actually owning the coil manufacturing capability rather than buying it off the shelf.[^3] It was, by reputation in the industry, the place where you learned how to make a fin-and-tube coil to global tolerances inside India. And it was, in the early 2010s, where Santosh Kumar Yadav worked.

Santosh is not a Stanford MBA. He is not the kind of founder Indian financial media tends to mythologize. He is, by all accounts, an operations engineer who came up through the shop floor, learned the manufacturing of heat exchangers from the inside, and concluded — sometime in 2016, by his own telling in the Red Herring Prospectus — that there was an enormous arbitrage sitting in plain sight.[^4] India was about to need an order of magnitude more air conditioners. The brands assembling those air conditioners were going to come under pressure to localize their bill of materials, both because of cost and because of policy. And almost nobody in India was set up to make heat exchangers to the spec a डायकिन Daikin or a पैनासॉनिक Panasonic would actually accept.

So in 2017, Santosh Kumar Yadav, along with two co-promoters — अंजू देवी Anju Devi and मनोहर लाल Manohar Lal — incorporated KRN Heat Exchanger & Refrigeration Limited in Alwar district, Rajasthan.[^4] The location was not glamorous. The Neemrana–Alwar industrial belt, hugging the Delhi–Mumbai expressway about 130 kilometers from the capital, was at that point known mainly as the Japanese industrial cluster — Daikin, Nissin Brake, Mitsubishi Electric and others had all set up there following the bilateral Japan-India industrial corridor initiative. That last detail will matter very shortly.

The decision Santosh made in 2017 was, in hindsight, the most important strategic call in the company's history. He did not try to make air conditioners. He did not even try to make compressors. He picked one component — the heat exchanger — and decided to be the best in India at it. In a country whose entrepreneurial culture, fairly or not, tends to glorify the conglomerate, the diversifier, the man with twenty businesses, this was almost contrarian. Acquired.fm listeners will recognize the move instantly: it is Hamilton Helmer-style specialization. You narrow the surface area you are competing on to widen the moat you can build.

The early years were lean. The first plant, KRN-1 in Neemrana, was modest — a fraction of what the company runs today. Headcount was small. Margins were thin. According to the prospectus, the company's revenue from operations in FY2021 was ₹136 crore.[^4] But the cultural DNA — Rajasthani Marwari operational discipline, a frugal engineering culture inherited from Santosh's Lloyd years, and an obsession with passing the qualification audits of finicky Japanese clients — was set in those first eighteen months.

There is one anecdote, repeated in industry circles around Neemrana, that captures the founder's temperament. In KRN's early years, when an OEM auditor flagged a single micro-leak issue on a batch of coils, Santosh reportedly refused to ship the entire batch, eating the loss, even though the customer would likely never have detected the defect in field use. The story may be apocryphal. But the behavior it describes — treating quality as a religion in a country where the cultural temptation in manufacturing has historically been जुगाड़ jugaad (clever workarounds) — is what got KRN onto the Daikin approved-vendor list. And once you are on the Daikin list, as we will see, an entire industry follows.

That obsession is where our next chapter begins.

III. The Daikin Inflection Point & The "Preferred Supplier" Moat

If you were to draw a single vertical line in KRN's history and mark "before" and "after," it would be sometime in 2018, when Daikin Airconditioning India placed its first significant production order for heat exchanger coils at the company's Neemrana plant. To understand why this mattered, you need to understand what Daikin is. ダイキン工業 Daikin Industries, headquartered in Osaka, is the largest air conditioning company in the world by revenue — bigger than Carrier, bigger than Trane, bigger than Mitsubishi Electric's HVAC division.[^5] In India, Daikin was in the middle of an aggressive localization push, building out a new manufacturing campus in श्री सिटी Sri City, Andhra Pradesh, and looking for domestic suppliers who could produce coils to its global specification rather than its India-tolerated specification.

The qualification process — known internally at Daikin as 源流管理 genryū kanri, or "upstream management" of supplier quality — is famously brutal. Multi-week on-site audits. Statistical process control reviews. Salt-spray corrosion testing. Burst-pressure testing of every coil pattern to two and a half times the maximum operating pressure. Sample lots dissected, microsections of brazed joints examined under microscope. If you have spent any time in Japanese automotive supply chain consulting, you know what this looks like. If you have not, imagine a year of being on probation, with your customer's quality engineer essentially living inside your factory.

KRN passed. And here is the part that financial analysts often miss when they look at the customer concentration line item in the company's filings and panic. Yes, Daikin India was approximately 33% of KRN's revenue in FY2024.[^4] On paper, that looks like a textbook concentration risk. In practice, it is the opposite. Once Daikin signs off on you as a coil supplier, every other OEM in the country pays attention. The reputational shorthand is brutal in its simplicity: if you are good enough for Daikin's energy-rating-critical components, you are good enough for everyone else.

The cascade through 2019, 2020, and 2021 was textbook. Voltas — the Tata-group AC market leader — onboarded. Blue Star added KRN as an approved coil supplier for its commercial cooling lineup. Schneider Electric, hunting for an Indian supplier for डेटा सेंटर data center precision cooling units, added KRN. By the time the company filed its DRHP with भारतीय प्रतिभूति और विनिमय बोर्ड SEBI in 2024, the customer roster included nine of the top fifteen room AC and commercial refrigeration brands operating in India.[^4]

What is happening here, in the language of Helmer's 7 Powers, is the construction of cornered resource and switching cost powers simultaneously. The cornered resource is the trust capital — the fact that to qualify a heat exchanger supplier, an OEM has to go through a 9-to-18-month process and put the supplier's coils into the BEE energy efficiency certification documentation. That documentation, once registered, is unit-specific. A 1.5-ton, 5-star inverter AC sold under the Daikin badge is certified at a particular cooling capacity (kW) and a particular Indian Seasonal Energy Efficiency Ratio (ISEER) value, calculated based on the exact thermal performance of the heat exchanger coil inside it. Change the coil — say, switch from KRN to a Chinese alternative — and you have to re-do the certification. Re-doing the certification means re-testing at a Bureau of Energy Efficiency-empaneled lab. Re-testing costs money and, more critically, costs time-to-market in an industry where seasonal demand windows are unforgiving. An OEM that misses the March-to-June pre-summer stocking cycle, because they were re-certifying a model, has effectively missed a year.

This is what makes the 33% Daikin number a feature, not a bug. The longer KRN's coils stay inside Daikin's certified product lineup, the more expensive — in opportunity-cost terms — it becomes for Daikin to ever switch. Customer concentration in a spec-locked supplier relationship is qualitatively different from customer concentration in a price-shopped commodity relationship. KRN is the former. A typical contract textile manufacturer is the latter. Treating them with the same risk discount is a category error.

The other under-appreciated dimension here is geography. KRN's Neemrana plants sit roughly fifteen kilometers from Daikin's North India facility. For a heat exchanger — a physically bulky, fragile-when-handled product with low value density (you cannot really ship coils economically across a thousand kilometers of road) — being inside the customer's logistical radius is itself a moat. The freight math, run on copper-and-aluminum-priced coils through trucking lanes that double their rates every monsoon, simply does not work for a competitor sitting in Gujarat or Tamil Nadu. KRN locked in not just the customer, but the customer's geography.

This is the foundation on which everything else gets built.

IV. The Product: Copper, Aluminum, and the "Fin & Tube" Secret

Pause for a moment and imagine the white indoor unit of an air conditioner mounted high on a living room wall in Pune. Open it up. Behind the front grille and the air filter, you find a wavy, accordion-folded panel of thin aluminum sheets, with thin copper tubes snaking horizontally through them in repeating rows. That panel — about the size of a placemat in a residential unit, and the size of a refrigerator door in a commercial cassette — is the indoor heat exchanger. Outside on your balcony, in the much larger condenser unit, you will find a bigger, vertical version of essentially the same thing. Two heat exchangers, working in concert with a compressor and a small amount of refrigerant gas, are what move heat from inside your home to outside.

The engineering looks deceptively simple. It is not. The reason this is high-stakes manufacturing rather than commodity tinsmithing comes down to four things, and understanding them is the difference between thinking KRN is "just a tube bender" and understanding why Daikin's auditors take this seriously.

First, fin geometry. The corrugated aluminum sheets are not flat — they are stamped with very precisely engineered patterns of louvers, waves, and slits that maximize the air's exposure to the heated metal while minimizing the pressure drop the indoor fan has to overcome. Get the geometry wrong by a fraction of a millimeter and the AC either uses too much energy, makes too much noise, or fails to hit its rated cooling capacity. The press dies that stamp these fins are themselves capital-intensive precision tools — and the variety of fin patterns KRN runs across its OEM customer base is one of the things that gives the company operational leverage. Each fin pattern is essentially a customer-specific tooling investment.

Second, tube-to-fin bonding. The copper tubes have to be expanded mechanically against the aluminum fins to create thermal contact. Too little expansion and you get hot spots and efficiency loss. Too much and you stress the copper, eventually causing micro-cracks that, six months into the warranty, become refrigerant leaks. Hydraulic tube expansion machines, paired with very specific copper-aluminum brazing flux chemistry, are the manufacturing know-how that lives in operator muscle memory more than in any documented process manual.

Third, pressure integrity. Every coil that leaves KRN's plant is helium-leak-tested or nitrogen-pressure-tested to 35–45 bar — well above the typical operating pressure of 18–20 bar for R-32 refrigerant systems. A single pinhole leak the size of a hair, undetected, becomes a field failure that costs the OEM warranty replacement plus reputational damage. The cost of a pressure-test failure caught in-plant is rupees. The cost of a pressure-test failure caught in a customer's living room is hundreds of thousands of rupees.

Fourth, coatings. India is, in many of its coastal cities, brutally corrosive on outdoor HVAC equipment. Salt fog from Mumbai. Sulfur compounds from Vizag refineries. Acid rain in industrial Gujarat. The hydrophilic coatings that get applied to fins, and the more recent "blue fin" anti-corrosion coatings, are themselves specialty chemistries. KRN's mastery of the coating line — the application uniformity, the curing oven temperature profiles, the salt-spray-hour ratings it can certify — is part of why it sits where it does on Daikin's approved-vendor list.[^4]

So this is not commodity work. Now layer on top of it the macro tailwind. India, until recently, imported a meaningful share of its finished heat exchangers and their components from China and Thailand. The आत्मनिर्भर भारत Atmanirbhar Bharat (Self-Reliant India) policy framework, kicked off in 2020, was explicitly aimed at reducing this import dependence in strategic and consumer-durable sectors. Air conditioners, somewhat surprisingly, made the list — partly because finished AC imports were running at over $1 billion annually in the late 2010s, and partly because Delhi wanted to push the entire consumer durables value chain onshore.[^6]

The hammer that the government brought down to drive this localization was the उत्पादन से जुड़ी प्रोत्साहन योजना Production Linked Incentive scheme, or PLI, for White Goods (AC and LED components). Announced in 2021, the scheme offered cash incentives — 4% to 6% of incremental sales over a baseline year, paid out annually over six years — to companies that committed to specific investment thresholds and met domestic value addition criteria.[^6] KRN was selected as a beneficiary in the PLI White Goods scheme cycle.[^6] The economic effect, run through KRN's P&L, is roughly a 5–6% margin lever on every rupee of incremental PLI-eligible sales for the duration of the scheme. On a business doing high-teens EBITDA margins, that is the difference between a good year and a great year.

The deeper point is not the PLI subsidy itself. It is that government policy, OEM localization strategy, and KRN's specialization decision all converged on the same point at the same time. Investors call this kind of alignment "luck." Operators call it "being early." KRN was early.

V. Management Analysis & Shareholding: Skin in the Game

If you pulled up the post-IPO shareholding pattern for KRN as of March 31, 2025, the first thing that would jump out is that the promoter group still owns approximately 70.39% of the company.[^7] In a country whose listed-equity market has been steadily watching promoter holdings get diluted by private equity exits, employee stock plans, and secondary placements, this is a high number. It is also, importantly, structured. Santosh Kumar Yadav personally holds the lion's share, with the balance distributed among the other promoters and a Hindu Undivided Family entity.[^7]

Promoter holding tells you one thing on the surface — alignment. It tells you something more interesting underneath. Look at the FY2025 management compensation disclosures. Santosh Kumar Yadav, as Managing Director, drew a cash compensation that is, by listed-Indian-mid-cap standards, conspicuously modest.[^8] No multi-crore bonuses tied to share price performance. No mysterious "professional fees" routed through related parties. The structure is what investors who have read enough Berkshire Hathaway letters call "wealth through equity" — the founder gets rich if and only if the stock gets richer, and his fixed salary is functionally a stipend rather than a wealth engine.

This is not common. In the broader Indian mid-cap industrial space, the more frequent pattern is the inverse — a managing director extracting a multi-crore annual package backed by performance metrics that are politely described as "subjective," combined with a promoter family that has steadily monetized stock since listing. KRN's setup is structurally cleaner. Whether that holds over the next decade, as the company scales and the founder approaches the typical succession-decision threshold, is the question. But the starting point is favorable.

The leadership team is small and tight-knit, in the way Indian first-generation manufacturing companies tend to be. Anju Devi serves on the board as a promoter director. Manohar Lal Yadav, another co-promoter, is involved in operational oversight. The independent directors, brought on board ahead of the IPO to meet SEBI's listed-company governance norms, include professionals from the financial and audit world. The structure is broadly conventional — what is unconventional is what the management team has chosen not to do. There is no second business line carved off into a related-party entity. There is no real estate "investment arm." There is no over-engineered holding-company structure obscuring the cash flows. This is a company that wants to be read as a single-business operator, and the financials reflect that.

The 2026 ESOP plan, announced earlier this year, is the next inflection.[^8] After running for nearly a decade as a founder-controlled, equity-stingy outfit, KRN announced a Phase-I employee stock option scheme covering eligible managerial and senior engineering staff. The grants are small in aggregate dilution terms — under 2% of the post-issue share capital — but the signal is what matters. To go from a Tier-2 component manufacturer doing ₹300 crore in revenue to a Tier-1 global supplier doing ₹3,000 crore (which is implicitly the long-range ambition), you cannot run the entire company out of the founder's WhatsApp groups. You need a layer of professional engineering management, design talent that can lead the next-generation microchannel coil R&D, and a procurement organization that can hedge copper exposure across the LME forward curve. None of those people will join for a basic salary. They will join for equity. The ESOP plan, in other words, is KRN admitting it needs to grow up — and choosing to align the senior layer's incentives with shareholders rather than with annual bonuses.

On operational discipline, the benchmark that matters is EBITDA margin. KRN exited FY2024 with EBITDA margins in the 19–20% range, and the FY2025 annual report shows margins holding in the high-teens zone despite copper price volatility.2 To put that in industry context: Amber Enterprises, the much larger contract-manufacturing rival, runs consolidated EBITDA margins in the high-single-digits to low-double-digits, because Amber sells a much larger fraction of fully-assembled white-goods units where the value capture per kilogram of metal is lower. Subros, the auto HVAC specialist, operates in roughly the 9–11% band. PG Electroplast, another listed AC contract manufacturer, runs at single-digit EBITDA margins on its core consumer durables segment.

The reason KRN is structurally ahead is that it sells a component where the engineering specification — not just the unit cost — is the basis of competition. Component businesses where the buyer cares about your tolerances earn margin. Component businesses where the buyer cares only about your invoice price earn cost-plus, which is to say, very little.

That margin discipline is what gets translated, in the next chapter, into capacity.

VI. Capital Deployment: The Neemrana Mega-Factory

Of the ₹341.95 crore raised in the October 2024 IPO, the fresh issue component was ₹240 crore — the rest was an offer-for-sale by the promoters.[^1] The use-of-proceeds in the prospectus was clinical: roughly ₹100 crore for capital expenditure into the wholly-owned subsidiary KRN HVAC Products Pvt. Ltd., for the construction of a new manufacturing facility; another tranche for working capital; and a smaller bucket for general corporate purposes.[^4] The headline number that captured analyst attention, and that we want to spend the next several paragraphs unpacking, is the new Neemrana plant.

The factory — physically located in the same industrial belt as KRN's existing two units but designed to operate at a much larger scale — was envisioned as the company's leap from "leading Indian heat exchanger maker" to "global-scale Tier-1 HVAC component supplier." The plant's design capacity is roughly 2.5x the existing combined output, depending on product mix.[^4] More importantly, the facility was designed to manufacture not just the fin-and-tube coils that have been KRN's bread and butter, but also adjacent products that the company has historically had to source from third parties: sheet metal enclosures, header pipes, distributor assemblies, and complete coil sub-assemblies that are one step closer to a finished HVAC unit.

This is vertical integration, but of an unusually well-targeted kind. KRN was not trying to become an air conditioner brand — that would be poor strategy, and Santosh has been explicit in interviews that this is not the ambition. Instead, the company is moving up the value chain by capturing more parts of the cooling unit, while still operating as an OEM supplier. Each additional component KRN can put inside the same delivered sub-assembly is incremental revenue and incremental margin, captured without taking on the brand-marketing cost or the dealer-channel complexity of going downstream. It is, in essence, doing to the OEM's bill-of-materials what 富士康 Foxconn did to Apple's iPhone assembly bill-of-materials in the early 2010s: consolidating supplier count, shortening the customer's procurement workflow, and stickying the relationship by being the single source for an entire sub-system rather than one input.

The capex efficiency question — did they overpay? — is the one investors should ask at every greenfield build-out, because Indian listed-company capex announcements have a long and not-so-proud history of cost overruns and capacity that mysteriously fails to ramp. KRN's filings disclose the new plant's total project cost at roughly ₹250 crore, with the IPO funding the bulk and internal accruals plus modest borrowings filling the rest.[^4] On a cost-per-incremental-coil basis, this benchmarks reasonably against global peers. Chinese heat exchanger plants of similar capacity, built in the 2019–2022 cycle, typically came in at $20–25 million all-in, which is ₹165–210 crore at recent exchange rates — but with the caveat that Chinese plants tended to source automation equipment domestically at significantly lower prices than what KRN paid for largely European-origin tube benders, fin presses, and helium-leak-test stations. Adjusted for the import content, KRN's number is roughly in line, not overpaying by any obvious margin.

The plant commenced commercial production in May 2025, with the BSE intimation disclosing the commencement on May 15, 2025.[^10] The first quarters of FY26 numbers, reflecting the early ramp, started showing operating leverage in the standalone P&L. The May 2026 standalone result — total income of ₹689.95 crore versus the prior comparable period — reflects both the underlying volume growth and the gradual contribution from the new facility as utilization climbed.3

The capex story matters for one specific reason that long-term holders need to internalize. Heat exchanger manufacturing has a particular relationship with fixed asset turnover. Up to a certain plant-level utilization, additional capacity is a margin headwind — depreciation hits the income statement, the plant runs at sub-optimal utilization, and EBITDA percentages compress even as absolute EBITDA may grow. Past the utilization inflection — typically somewhere between 60% and 70% of nameplate — every additional ton of coils shipped is essentially incremental gross margin dropping to the operating line. The Neemrana plant is, in mid-2026, somewhere on the early side of that curve. Where it gets to over the next eight quarters — and how cleanly the fixed-asset-turnover ratio rebuilds — is the single most important operational metric to track. We will come back to this in Chapter IX.

The next chapter is about something the IPO prospectus almost buried, but which may matter more than the residential AC story.

VII. Hidden Businesses: The High-Growth New Frontiers

There is a charming paradox in how Indian companies disclose their growth options. The big, obvious, easy-to-understand business — in KRN's case, residential AC coils for Daikin and Voltas — gets ten pages in the prospectus. The smaller, weirder, faster-growing businesses get half a page each, almost as afterthoughts. For investors, the half-pages are often where the alpha lives.

The first half-page is डेटा सेंटर data center cooling. India had, as of early 2026, roughly 1,000–1,100 MW of operational data center capacity, with another 2,500+ MW in various stages of construction and announcement.[^12] The drivers — डेटा स्थानीयकरण data localization mandates from the RBI for payments and from MeitY for personal data, hyperscaler buildouts from AWS, Microsoft, Google, and a new wave of indigenous AI inference infrastructure — are not a 2026 phenomenon, but the capacity ramp from 2024 onward is unprecedented. Every megawatt of data center IT load requires roughly an equivalent megawatt of cooling capacity, and that cooling is overwhelmingly precision air conditioning — CRAC and CRAH units, in-row coolers, rear-door heat exchangers — supplied by a handful of vendors. Schneider Electric, through its APC brand and its Uniflair precision cooling line, is one of the largest of those vendors. Schneider is also a KRN customer.

The data center play is interesting for two reasons. First, the unit economics of a data center heat exchanger are dramatically more attractive than a residential coil — higher copper content, higher engineering complexity (chilled water versus direct expansion variants, redundant circuiting), and significantly higher per-unit pricing. A 200kW precision cooling unit carries multiples of the BOM value of a 1.5-ton residential split. Second, the data center cycle is procyclical with global hyperscaler capex — meaning when AI capex stays hot, data center buildouts stay hot, and KRN's order book in this segment compounds. The segment is small today as a share of KRN's revenue. The trajectory is the point.

The second half-page is भारतीय रेलवे Indian Railways HVAC. India runs the fourth-largest rail network in the world by route kilometers, and as of the mid-2020s is in the middle of a multi-decade modernization push. The वंदे भारत Vande Bharat semi-high-speed trains, the new generation of AC LHB coaches replacing the legacy ICF fleet, and the upcoming रैपिडएक्स RapidX and various metro systems — all require HVAC systems with very specific shock, vibration, and longevity specifications.[^13] These are not residential AC coils — they are heavy-duty, dual-zone, ruggedized units. They are also, like data center coils, priced and margined very differently from the consumer durables business.

KRN's vendor approval from अनुसंधान अभिकल्प और मानक संगठन RDSO — the Research Designs and Standards Organisation, the technical arm of the Ministry of Indian Railways — was a quietly significant 2024 milestone.[^13] RDSO approvals are notoriously hard to obtain. The qualification process makes Daikin's look quick. But once you are on the approved-vendor list for a specific railway product class, you participate in tenders that flow steadily for decades. This is the kind of slow-burn, low-glamour business line that does not move the stock in any single quarter but, compounded over a decade, can transform the segment mix.

The third half-page is exports. KRN's export revenue grew at roughly a 44% compound annual rate over the FY2021–FY2024 window, off a small base, with the export mix increasingly tilted toward European HVAC OEMs and select North American distributors.[^4] The चीन प्लस वन China-Plus-One phenomenon — global brands diversifying their sourcing footprint away from China for geopolitical, tariff, and supply-chain-resilience reasons — has been talked about endlessly in Indian financial media without producing as many actual revenue wins as the talk would suggest. For KRN, it has been producing wins. The European HVAC market, dominated by names like Carrier, Trane Technologies, Daikin Europe and Mitsubishi Electric Europe, has been hunting for Asian heat exchanger suppliers who can meet European refrigerant-handling standards (F-Gas regulations, low-GWP refrigerant compatibility) without the political and customs friction that comes increasingly attached to Chinese sourcing. KRN, sitting in India, with PLI-subsidized economics and Daikin-approved quality stamps, is well-positioned.

The segment-mix implication of all three of these "side businesses" is the longer-term thesis. KRN as of FY2024 was roughly 90% residential AC coils.[^4] If the data center business compounds at the rates implied by Indian data center capacity additions, if the railway segment moves from sub-5% to mid-double-digits of revenue over the next five years, and if exports continue at the kind of CAGR seen since FY2021, the revenue mix at FY2030 looks quite different from the mix at FY2025. Less seasonal. Less concentrated on a single end-market. More margin-rich, on average. That mix shift, more than any single quarter's growth rate, is the thing patient investors are buying when they buy KRN.

The transition to the strategic-framework chapter is natural here, because all of the above — the customer lock-in, the geographic moat, the capex, the new segments — needs to be stress-tested against an actual analytical framework rather than just narrative momentum.

VIII. Strategic Framework: Hamilton's 7 Powers & Porter's 5 Forces

Hamilton Helmer's 7 Powers framework is, for those who have not read the book, an attempt to taxonomize why a business sustains above-cost-of-capital returns over a long horizon. The seven powers — scale economies, network economies, counter-positioning, switching costs, branding, cornered resource, and process power — are not all equally relevant to every business. For KRN, three of them carry the analytical weight.

The first is switching costs. We have already discussed the BEE certification dynamic — that once an OEM has registered an AC model with a specific heat exchanger inside it, switching coil suppliers means re-registering. But there is a second layer that matters even more. Daikin, Voltas, Blue Star — all the major OEMs — design their entire indoor and outdoor unit chassis around a specific coil geometry. Tube spacing, header positioning, end-plate dimensions, drain-pan integration: all of it is parametrized to the coil supplier's mechanical drawings. Changing supplier means redesigning the unit. Redesigning means re-tooling. Re-tooling means a year of capex and a year of lost time-to-market. The switching cost is not just regulatory — it is mechanical, and far stickier than spreadsheet analysis would suggest.

The second is cornered resource, specifically in the form of trust capital with global OEMs. Daikin, Schneider, Voltas — these are companies whose qualification processes can take 9–18 months. KRN has been through those processes, has the audit trails, has the salt-spray test certificates, has the PPAP (production part approval process) documentation packages cleared. That body of qualification work is, in the strictest sense, a cornered resource — it is not transferable, it cannot be bought, and a new entrant cannot replicate it without spending the same 9–18 months times the number of OEMs.

The third is scale economies, but with a specific application. Heat exchanger manufacturing's largest single variable cost is the metal — copper for tubes, aluminum for fins. Copper alone is typically 40–50% of the bill of materials. The ability to hedge copper exposure — through London Metal Exchange forward contracts, supplier long-term agreements, or backward integration into copper tubing — scales sub-linearly with company size. A KRN running the Neemrana mega-plant can lock in copper at price points and credit terms that a smaller competitor running a single-line facility simply cannot. As the new capacity ramps, this scale advantage compounds.

Now to Porter's 5 Forces, which is the older and more pessimistic of the two frameworks for a reason: it forces you to confront the structural risks.

Bargaining power of buyers is the obvious threat. Daikin, Voltas, Blue Star are not small accounts — each is a multi-billion-rupee customer with sophisticated procurement organizations whose KPI is to grind supplier margins year over year. The "annual price reduction" conversation is a recurring fixture of the relationship. The mitigant — and it is a meaningful one — is that KRN's value addition is high enough, and its customer-specific tooling investment deep enough, that the buyer's practical power to grind margin is bounded. You cannot squeeze a supplier whose component your entire chassis is designed around without risking the supplier dropping you, which means you lose a year of model launches.

Threat of substitutes is structurally low. Cooling is a thermodynamic problem. You move heat by exchanging it across a metal interface. There is no software substitute for a copper-aluminum coil. The only real substitute conversation that matters is microchannel heat exchangers — an alternative geometry using flat multiport tubes, mostly aluminum, eliminating copper. Microchannel has gained share in automotive HVAC and some commercial applications, but in residential split ACs it has limited penetration, mainly because of refrigerant-distribution and frost-management complexities. KRN is reportedly developing microchannel capability — which is the correct strategic posture, but the substitute risk is more an evolutionary than a revolutionary one.

Threat of new entrants is moderate. The capital cost to set up a coil plant is not enormous in absolute terms — a credible greenfield facility runs around ₹150–250 crore. What is enormous, and what protects KRN, is the time cost of customer qualification. A new entrant with a fully built plant in 2026 is, at best, mid-2027 before it gets its first significant Indian OEM order, and 2029 before it is shipping at meaningful scale. By that point KRN has had three years to entrench further, lock in PLI economics, and build the next plant.

Bargaining power of suppliers runs through the copper market. Copper prices, set on the LME, are not negotiable with any individual supplier — they are exogenous. Aluminum less so, but still meaningfully cyclical. The mitigant is contract structure: KRN's OEM contracts increasingly contain copper-price pass-through clauses, with monthly or quarterly resets. The mitigant is imperfect — there is always some lag, some basis risk — but it is real.

Intensity of rivalry is the most fluid of the five forces here. Existing competitors include Lloyd Engineering (the heat exchanger arm of what is now part of Havells), various unlisted Chinese-Indian joint ventures, and some captive in-house coil operations at Voltas and Blue Star. The rivalry is intensifying as the market grows — Lloyd has reportedly been investing in additional capacity. Captive in-house manufacturing by OEMs is the most strategically important rivalry to watch, because if a Voltas or a Daikin decides to backward-integrate fully, KRN's share at that customer caps out. That risk is real but slow-moving, because the capex and management bandwidth required for OEMs to run a coil plant well is high, and the make-versus-buy economics rarely favor making at sub-scale captive volumes.

Net of the framework analysis, the picture is of a business with multiple stacked sources of competitive advantage in a structurally growing end-market, with concrete but manageable risks. Which sets up the bull-bear conversation.

IX. The Bear Case vs. The Bull Case

Let us steelman the bear first, because too many Indian-mid-cap write-ups get accused — fairly — of pre-baked bullishness.

The first bear argument is the copper trap. KRN's bill of materials is roughly half exposed to LME copper prices.4 When copper rallied from $7,000 per ton in 2020 to over $10,000 in early 2024 and again touched fresh highs in early 2026, the working capital impact on every Indian heat exchanger manufacturer was severe. Inventory got revalued upward, accounts payable terms got tighter, and the gap between purchase price and customer billing price (with its contractual lag) widened. KRN's contracts include pass-through clauses, but the lag is typically 30–90 days, and the basis risk between contract reset windows is non-trivial. A sustained copper bull run can compress margins by 200–400 basis points for a quarter or two before pass-throughs catch up. For a stock priced on margin expectations, that compression hits the multiple as well as the earnings.

The second bear argument is customer concentration, taken at face value. Even if we believe — and the earlier analysis suggested we should — that Daikin's 33% revenue share is qualitatively different from generic customer-concentration risk, quantitative tail risks remain. A Daikin India strategic decision to in-source a meaningful portion of its coil requirement (backward integration), or a Daikin global decision to consolidate Asian coil sourcing onto one or two preferred suppliers from a different country, would be material to KRN's near-term P&L regardless of how qualitatively sticky the relationship is. The probability of either is low, but not zero. The mitigant is the customer-base diversification trend visible in the FY2025 disclosures — the share of Daikin in total revenue has been slowly declining as the rest of the book grows faster — but the absolute exposure is still substantial.

The third bear argument is OEM backward integration. Voltas has, in recent years, made noise about deepening its components manufacturing footprint. Blue Star runs limited in-house coil capacity. If a major OEM decides that coils are strategic enough to bring in-house, the addressable market for KRN shrinks at the margin. This is, again, slow-moving and not a 2026 catastrophe — but it is the kind of strategic risk a long-term holder should monitor at every annual day investor meet.

The fourth bear argument is valuation. The stock listed at a 100%+ premium and has, like many of the post-2024 Indian small-cap IPO winners, traded at multiples that price in years of execution.1 Markets can stay enthusiastic for a long time, but the gap between price and earnings power can narrow rapidly when sentiment shifts. This is not a fundamentals risk so much as a path-dependence risk.

Now the bull case.

The first bull argument is the macro tailwind, and it is not a small one. India's residential AC penetration was about 8% in 2024.[^15] China's was 11% in 1995 and is 60%+ today. The US has been at 90%+ for decades. The Indian per-capita income trajectory, the climate trajectory (India has had progressively more brutal summers, with लू heat waves becoming a top-ten public health issue), the urbanization trajectory, and the electrification-of-the-rural-grid trajectory all point in the same direction. The Indian room AC market, which was around 9–10 million units a year in 2023, is widely expected to triple over the next decade. Picks-and-shovels suppliers ride this curve mechanically.

The second bull argument is China-Plus-One. The structural reshoring of global HVAC supply chains away from China — driven by US-China tariff dynamics, European-Chinese trade tensions, and corporate supply-chain-resilience mandates — is a multi-year tailwind for Indian component manufacturers. KRN, with its quality credentials and PLI-subsidized cost economics, is one of the few Indian suppliers that can absorb the demand-pull.

The third bull argument is the data center and railway optionality, which we discussed in Chapter VII. Even modest success in either segment shifts KRN's revenue mix toward higher-margin, less seasonal, more strategic end-markets.

The fourth bull argument is the execution track record. The Neemrana mega-plant came up roughly on time. Operating margins held through a volatile commodity year. The PLI selection went through. The export book grew. These are the operating signals that compound.

The KPIs to actually watch — and the rule from the start of this piece is to keep this list short — are three.

KPI one: Fixed Asset Turnover Ratio. With ₹250 crore of new fixed assets sitting on the balance sheet from the Neemrana mega-plant, the question is how quickly KRN can drive sales through that asset base. The pre-IPO fixed asset turnover, on the older plants, was strong. The post-ramp number for the consolidated business is the single best indicator of whether the capex was well-deployed. Watch this quarterly.

KPI two: Revenue mix outside Daikin and outside residential AC. Specifically, what percentage of revenue comes from data center, railway, and export segments combined. This number, today in the low double digits, is the leading indicator of business diversification. A move from 15% to 30% over the next two years would be a meaningful re-rating signal even before it shows up in EBITDA margins.

KPI three: EBITDA margin trajectory through commodity cycles. Specifically, the ability to maintain margins above 17% even when copper is volatile. This is the test of contract design and procurement discipline. A business that holds margin through bad metal cycles is a business with real pricing power. A business that does not, is a business riding the cycle.

Three numbers. That is the watchlist.

X. Conclusion: Playbook Lessons

Strip away the IPO drama, the 213x oversubscription, the listing-day pop, and the post-listing volatility, and what is left is a relatively straightforward business case study with three lessons that travel well beyond KRN itself.

Lesson one: narrow the focus to widen the moat. In 2017, Santosh Kumar Yadav could have built another AC brand. He could have built a diversified HVAC contract manufacturer. He could have chased the consumer-facing margins of finished products. He did none of those things. He picked one component, became the best in India at making it, and let the rest of the industry come to him. The pattern — the deliberate refusal to diversify in the early years, the specialization-as-strategy bet — is something investors will recognize from the histories of Intel in the early DRAM-to-microprocessor pivot, of ASML in the lithography wars, of 台積電 TSMC in pure-play foundry, and at a much smaller scale, of dozens of Indian mid-cap industrial winners over the past decade. Specialization works because the moat-builder gets to compound learning curves that diversifiers never accumulate.

Lesson two: anchor clients are platforms, not customers. The Daikin relationship is not just a 33% revenue line item. It is the credential that opened every other door in the Indian HVAC industry. It is the spec discipline that forced KRN to operate at world-class quality from year three rather than year ten. It is the geographic anchor that made the Neemrana cluster a natural location to build at. Acquired.fm listeners will hear echoes of this pattern in the early Apple-Foxconn relationship, in the early Samsung Display-Apple OLED relationship, in the early NVIDIA-OpenAI compute relationship. The right first big customer is not a customer; it is a platform you build the rest of the business on top of.

Lesson three: align capital deployment with the macro tailwinds. The PLI scheme, the China-Plus-One supply chain reshoring, the Atmanirbhar Bharat policy push — none of these were invented by KRN. They were exogenous to the company. What KRN did, intelligently, was position its capital allocation to fully ride each of those tailwinds at the moment they emerged. The Neemrana capex was timed to PLI eligibility. The customer-base diversification was timed to China-Plus-One. The product extension into data center and railway HVAC was timed to the relevant infrastructure investment cycles. A founder operating in 2017 could not have foreseen all of these tailwinds with precision. But Santosh built a business that could opportunistically ride each one as it materialized. That optionality is itself a form of strategic foresight.

Where does KRN sit in the broader narrative of what gets called the "Indian century"? It sits, somewhat inconveniently for the headline writers, neither in the marquee places that get the most attention — software exports, fintech, e-commerce — nor in the consumer-brand-building stories that dominate the front pages of business newspapers. It sits in the middle of the industrial supply chain, doing unglamorous engineering work, selling to people who sell to people, far from the consumer's eye. It is a company that does not exist as a name in any household conversation about air conditioning.

And yet, in the next decade, as roughly 100 million Indian households install their first air conditioner, as data center capacity in India multiplies six-fold, as railway HVAC requirements scale with the modernization of the network, and as European and North American HVAC brands continue their slow reshoring of Asian sourcing away from China — a meaningful share of the heat exchangers inside all of that cooling equipment will have rolled off a fin-press line in Neemrana. That is the bet. That is the story. And whatever happens to the stock price quarter to quarter, the underlying industrial reality is one of the more durable picks-and-shovels propositions that the Indian listed equity market currently offers.

The picks-and-shovels merchants in California in 1849 made more money than the gold prospectors. Two centuries on, in a different country, with a different commodity (cool air), the structural setup looks awfully similar.

References

References

-

KRN Heat Exchanger lists at 118% premium over issue price — Moneycontrol, 2024-10-03 ↩↩

-

Annual Report FY 2024-25 — KRN Heat Exchanger Investor Relations ↩

-

KRN Heat Exchanger standalone total income jumps to Rs 689.95 crore — Investing.com, May 2026 ↩

-

Copper and Aluminum Price Trends for HVAC Manufacturers — Reuters, 2026-03-15 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube