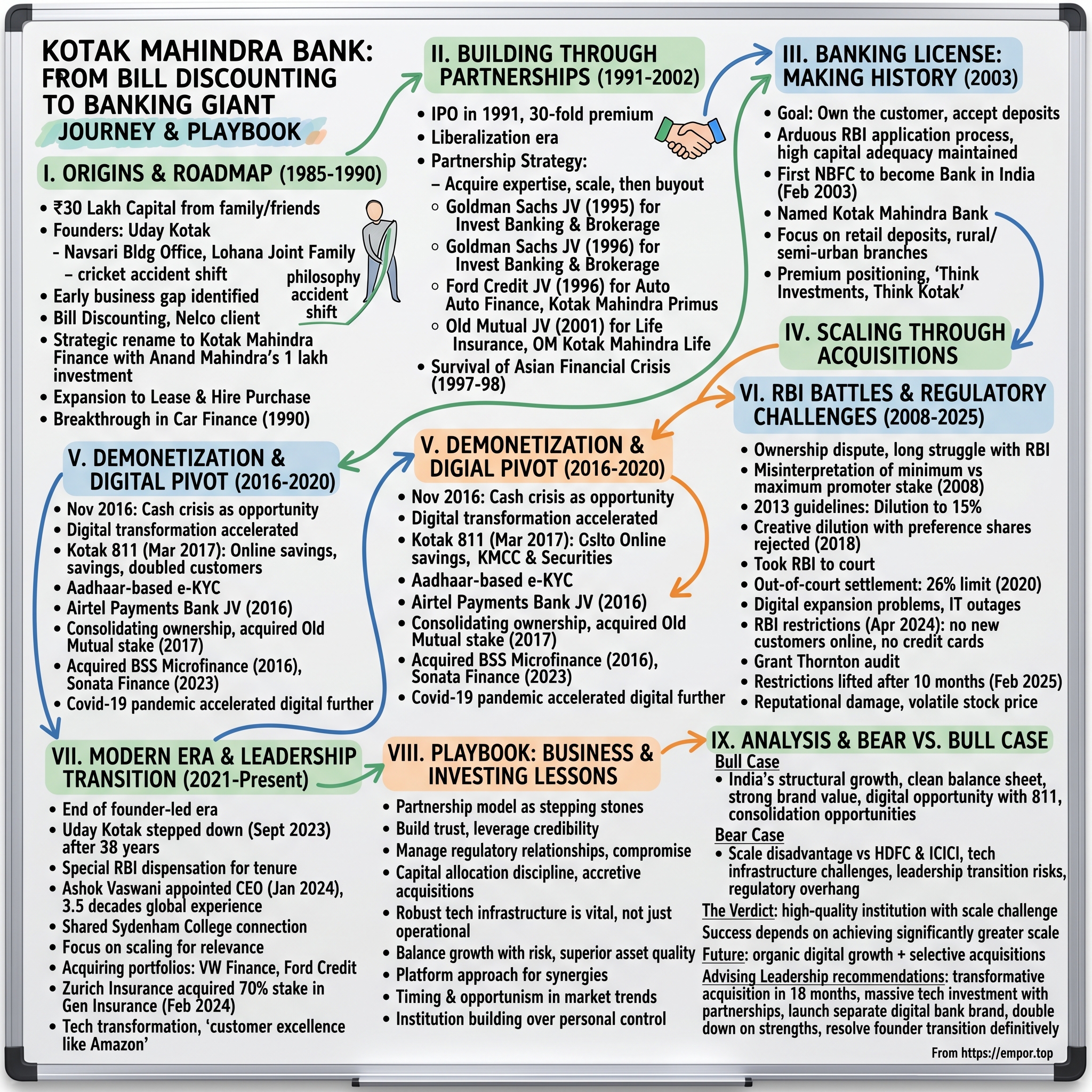

Kotak Mahindra Bank: From Bill Discounting to Banking Giant

I. Introduction & Episode Roadmap

In the pantheon of Indian banking, few stories capture the entrepreneurial spirit quite like that of Kotak Mahindra Bank—a financial institution that began with just ₹30 lakh in borrowed capital and evolved into India's third-largest private sector bank by market capitalization. In 1985, Uday Kotak founded Kotak Capital Management Finance Limited as a financial services company with a loan of ₹30 lakh from family and friends. This is the remarkable journey of how a middle-class Gujarati entrepreneur transformed a small bill discounting operation into a banking powerhouse worth over ₹3.5 lakh crore today.

The story of Kotak Mahindra Bank is fundamentally the story of India's financial liberalization itself. When Uday Kotak started his journey in the mid-1980s, India was still a closed economy operating under the License Raj, where interest rate spreads exceeded 10% and financial markets were riddled with inefficiencies. Foreign banks were restricted, private banks were non-existent, and the entire financial system was dominated by public sector institutions that moved at a glacial pace. In this environment, a young chartered accountant saw opportunity where others saw obstacles.

What makes the Kotak story particularly compelling is its timing and transformation. In February 2003, Kotak Mahindra Finance received a banking licence from the Reserve Bank of India, becoming India's first non-banking finance company to be converted into a bank. This unprecedented conversion marked a watershed moment in Indian banking history, demonstrating that with the right governance, risk management, and strategic vision, even a non-banking financial company could earn the trust required to accept public deposits.

The central question that drives this narrative is deceptively simple yet profoundly complex: How did a middle-class entrepreneur with no banking pedigree build India's most valuable private bank? The answer lies not in a single masterstroke but in a series of calculated risks, strategic partnerships, timely exits, and most importantly, an unwavering commitment to trust and governance in an industry where credibility is currency.

This episode will trace the arc of Kotak Mahindra Bank through several distinct phases: the scrappy startup years of bill discounting and car financing; the partnership era with global giants like Goldman Sachs and Ford Credit; the historic banking license and transformation; the scaling through strategic acquisitions including the landmark ING Vysya merger; the digital pivot post-demonetization; ongoing regulatory battles; and finally, the leadership transition from founder to professional management. Along the way, we'll unpack the playbook that enabled a three-person operation in a 300-square-foot office to become a financial conglomerate employing over 100,000 people today.

II. Origins: The Cotton Trader's Son & Early Days (1985-1990)

The story of Kotak Mahindra Bank begins not in the boardrooms of Bombay but in the crowded lanes of a Gujarati joint family household where 60 members lived under one roof. So, the concept of living with family, cousins, uncles, aunts, how do you make sure that you live together at the same time you pursue your own goals and interests, Kotak would later reflect, describing his upbringing as "capitalism at work, socialism at home"—a philosophy that would profoundly shape his approach to business.

Born on March 15, 1959, into an upper-middle-class Lohana family engaged in cotton trading, Uday Kotak seemed destined for a conventional business career. He attended Hindi Vidya Bhavan for his schooling, earned his B.Com from Sydenham College of Commerce and Economics, and completed his MBA from the prestigious Jamnalal Bajaj Institute of Management Studies. But fate had other plans.

In September 1979, he (Kotak) was playing cricket in the Kanga League. For those not familiar with the Kanga League, it (the league matches) is played during the monsoon season with adverse weather conditions. After a blow to his head, the banker had to take a break and lost a semester. The incident was far more serious than initially described. During a Kanga League match at Azad Maidan, he was hit on the head by the ball while running between the wickets. He collapsed. An immediate operation stopped the brain hemorrhage. It saved his life but rendered him bedridden for months.

This near-death experience at age 20 fundamentally altered Kotak's trajectory. His dreams of becoming a professional cricketer—he had been coached by the legendary Ramakant Achrekar, who also mentored Sachin Tendulkar—were definitively over. If it weren't for a cricket accident that almost killed him, Uday Kotak probably wouldn't be the world's richest banker. A ball that hit him in the head and led to an emergency surgery pushed a 20-year-old Kotak to abandon his dream of becoming a professional player.

After recovering, Kotak was set to join Hindustan Unilever following his MBA, a prestigious placement that would have guaranteed a comfortable corporate career. But something didn't sit right. He wasn't keen on working with his extended family in their traditional business, yet he also didn't want the predictability of corporate employment. In early 1985, with his father's blessing and a small 300-square-foot office space in the Navsari building, Kotak decided to chart his own path.

Kotak Mahindra Bank founder Uday Kotak has said that the bank was a bootstrapped start-up back in 1985 which began operations with a modest sum of Rs 30 lakh. The initial capital came from family and friends, but the business model was ingenious in its simplicity. Kotak identified a gap in the market: companies like Nelco, a Tata subsidiary, needed working capital but found bank lending processes cumbersome and expensive. Meanwhile, there were entities with surplus funds earning suboptimal returns. Kotak positioned himself as the intermediary, borrowing at one rate and lending at another, earning the spread with minimal capital investment.

The bill discounting business was unglamorous but profitable. In those pre-liberalization days, with interest rates highly regulated and credit markets inefficient, there were numerous arbitrage opportunities for those willing to do the legwork. Kotak would personally visit clients, understand their cash flow cycles, and structure financing solutions that banks wouldn't touch. Starting a business was relatively the easy part. The important turning points in the journey from say 1985 to 2023, which is roughly 38 years, were 1992 when you saw a significant challenge to India's financial sector. You saw the famous securities scandal and we survived that. We lived through that and came out completely unscathed.

The transformative moment came in 1986. In 1986, Anand Mahindra and his father Harish Mahindra invested ₹1 lakh in the company which was subsequently renamed Kotak Mahindra Finance. This wasn't just about the money—though the capital was welcome. The Mahindra name brought instant credibility to a fledgling financial services firm. Anand Mahindra, who would later become chairman of the Mahindra Group, was then a young Harvard Business School graduate looking to make strategic investments. He saw in Uday Kotak not just a competent financial professional but an entrepreneur with the hunger and discipline to build something substantial.

The partnership was formalized with Anand Mahindra taking a small equity stake, and more importantly, lending his family name to the venture. "As far as I'm concerned, becoming the world's richest banker is only a proxy for Uday being one of the world's smartest bankers," said Anand Mahindra, the chairman of Mahindra Group in Mumbai, whose tie up with Kotak back in 1986 led to the firm's name. The newly christened Kotak Mahindra Finance Limited now had the pedigree to approach larger clients and more sophisticated transactions.

By 1987, the company had ventured into lease and hire purchase activities, recognizing that India's growing middle class needed financing solutions for consumer durables and equipment. But the real breakthrough came in 1990 when Kotak made a prescient bet on car financing. 1990: Expanded its operations to provide auto finance. This was a significant move as it catered to a rapidly growing automobile sector in India.

The timing was perfect. India was on the cusp of economic liberalization, and car ownership was about to explode from a luxury to an aspiration for the emerging middle class. While established banks were slow to recognize this opportunity, viewing car loans as risky retail exposure, Kotak dove in headfirst. The company developed proprietary credit assessment models, built relationships with auto dealers, and most importantly, understood that in a country where a car was often a family's second-largest purchase after a home, the emotional and social dimensions of ownership were as important as the financial ones.

By 1991, Kotak Mahindra Finance had grown confident enough to go public, listing on the stock exchanges at a time when the Indian capital markets were still nascent. The IPO was a resounding success—shares listed at ₹1,300-1,400 against an issue price of just ₹45, a nearly 30-fold premium that validated the market's faith in Kotak's business model and execution capabilities.

But 1992 would bring the first major test. The Harshad Mehta securities scam rocked India's financial markets, taking down numerous financial institutions in its wake. The bill discounting market, where Kotak had cut his teeth, was particularly affected. Yet Kotak Mahindra Finance emerged unscathed, having avoided the temptation of easy money that had lured many competitors into questionable practices. You then saw the significant Asian crisis and the NBFC crisis which happened between 1997-98 all the way up to 2002-2003. At that stage we were a non-bank financial company. There were more than 4,000 NBFCs, and barely I think around 20 survived. You then then came to the conclusion that if you did the right thing, which was within the law of the land, it always worked for you.

This early brush with crisis would establish a pattern that would define Kotak's entire career: conservative when others were aggressive, opportunistic when others were fearful, and always, always focused on the long-term sustainability of the business over short-term gains. As the 1990s began, Kotak Mahindra Finance was no longer just a bill discounting shop—it was emerging as a serious player in India's financial services sector, ready to capitalize on the liberalization wave that was about to transform the Indian economy.

III. Building Through Partnerships (1991-2002)

The 1990s marked a pivotal transformation for Kotak Mahindra Finance—from a domestic financial services firm to an institution with global ambitions and partnerships. This was the decade when Uday Kotak perfected what would become his signature strategy: partnering with global giants to acquire expertise, scaling the business, and then buying them out at the right moment to maintain control.

The liberalization of 1991 had opened India's doors to foreign investment, and Kotak was among the first to recognize that partnerships with international financial institutions could provide not just capital but invaluable expertise in sophisticated financial products and risk management systems. His approach was pragmatic: "I'm a great believer that it is important for Indian companies to learn and implement and really thereafter execute well," he would later reflect.

On July 25, 1995, Goldman Sachs announced an equity joint venture in the form of a 28 percent stake in a new investment bank, Kotak Mahindra Capital, being formed by Kotak Mahindra Finance Ltd., a leading financial services company in India, with an option to increase its stake to 40 percent within three years. Goldman Sachs also acquired a similar stake in Kotak Securities, a Bombay Stock Exchange brokerage firm.

The Goldman Sachs partnership was transformative. The joint venture with Kotak Mahindra Finance Ltd. followed the opening of India's stock markets to direct foreign investment just two years earlier. The deal was the result of three years of joint efforts in research and investment banking between the two firms on an informal basis. For Kotak, this wasn't just about the Goldman Sachs brand—though that certainly helped win mandates. It was about learning how a world-class investment bank operated, understanding global best practices in underwriting, M&A advisory, and capital markets.

The partnership structure was carefully crafted. In the same year, Kotak Mahindra Finance hived off its investment banking division into a new company, Kotak Mahindra Capital, started in partnership with Goldman Sachs. Goldman Sachs took a 25% stake in both Kotak Mahindra Capital Company (for investment banking) and Kotak Securities (for broking), with Kotak retaining majority control. This ensured that while Kotak benefited from Goldman's expertise and global network, he never ceded control of the strategic direction.

Simultaneously, Kotak was building another crucial partnership in the auto finance business. In 1996, the company formed Kotak Mahindra Primus (later renamed Kotak Mahindra Prime) as a 60:40 joint venture with Ford Credit International. In 1996, the car finance business was hived off into a separate company, namely Kotak Mahindra Primus Ltd and Ford Credit took a 40% stake in Kotak Mahindra Primus. This partnership brought sophisticated auto financing expertise, risk assessment models, and importantly, a relationship with Ford Motor Company that would help Kotak finance Ford vehicles across India.

The late 1990s saw Kotak systematically building a financial services conglomerate. In 1998, Kotak Mahindra Finance started its mutual fund arm called Kotak Mahindra AMC. Each vertical was carefully chosen to complement the others—investment banking brought corporate relationships, securities broking provided distribution, mutual funds offered fee-based income, and car financing delivered steady interest income.

The Asian Financial Crisis of 1997-98 provided both a test and an opportunity. While numerous NBFCs collapsed—the number dropped from over 4,000 to barely 20 survivors—Kotak Mahindra not only survived but thrived. The company had deliberately shrunk its balance sheet during the crisis, choosing safety over growth. This conservative approach, while criticized by some as overly cautious, proved prescient when competitors began falling like dominoes.

In 2001, recognizing the massive opportunity in life insurance following sector liberalization, OM Kotak Mahindra Life Insurance was established as a 74:26 joint venture between Kotak Mahindra Finance and Old Mutual. Old Mutual, a 150-year-old South African financial services group with extensive insurance expertise, brought technical know-how in product design, actuarial capabilities, and distribution strategies.

The partnership strategy was yielding impressive results. By 2002, Kotak Mahindra Finance had transformed from a single-product NBFC into a diversified financial services group with presence across investment banking, securities broking, mutual funds, car financing, and life insurance. Each partnership had served its purpose—providing expertise, credibility, and capital at crucial junctures.

But Kotak was already thinking ahead. He understood that while partnerships were valuable for learning and scaling, ultimate value creation would come from full ownership. "Our joint venture partnership with Goldman Sachs, with Ford Credit, with Old Mutual in the life insurance business. I'm a great believer that it is important for Indian companies to learn and implement and really thereafter execute well."

What distinguished Kotak's approach to partnerships was his clarity about their lifecycle. Unlike many Indian entrepreneurs who either became overly dependent on foreign partners or engaged in acrimonious battles for control, Kotak viewed partnerships as stepping stones. He would later articulate this philosophy: enter partnerships for specific capabilities, absorb the learning, scale the business, and when the time is right, buy out the partner to capture full value.

The partnerships also served another crucial purpose—they provided external validation of Kotak's governance standards and business practices. Having Goldman Sachs as a partner meant adhering to international compliance standards. Ford Credit's involvement meant implementing rigorous risk management systems. Old Mutual's partnership brought insurance best practices. Each partnership raised the bar for the entire organization.

As 2002 drew to a close, Kotak Mahindra Finance stood at a crossroads. It had built a successful NBFC with diverse business lines and blue-chip partnerships. But Uday Kotak harbored a bigger ambition. The Reserve Bank of India had begun discussing the possibility of allowing well-run NBFCs to convert into banks. For Kotak, who believed that "ultimately one needs to own the customer," this represented the ultimate opportunity—the chance to transform from a lender who depended on banks for funding to a bank that could accept public deposits.

The application process would be arduous, the regulatory scrutiny intense, and the challenges of transformation immense. But Kotak had spent the past decade preparing for exactly this moment. The partnerships had provided the expertise, the various crises had proven the risk management capabilities, and most importantly, the track record had established the trust. The stage was set for Kotak Mahindra Finance to attempt something no Indian NBFC had done before—become a bank.

IV. The Banking License: Making History (2003)

The year 2003 would mark the most significant transformation in the Kotak Mahindra story—the metamorphosis from a non-banking financial company to a commercial bank. In February 2003, Kotak Mahindra Finance received a banking licence from the Reserve Bank of India, becoming India's first non-banking finance company to be converted into a bank. Kotak Mahindra Finance was then renamed Kotak Mahindra Bank.

The context for this historic transformation requires understanding the regulatory environment of early 2000s India. The Indian banking sector was undergoing significant stress. Global Trust Bank was teetering on the edge of collapse, several cooperative banks had failed, and the Reserve Bank of India was deeply skeptical about expanding the banking sector. The memory of bank failures was fresh, and the RBI's primary concern was protecting depositors' money.

Yet, there was also recognition that India's banking sector needed fresh blood. Public sector banks, while stable, were often inefficient and slow to innovate. The few private banks that existed—HDFC Bank and ICICI Bank being the prominent ones—had demonstrated that well-run private institutions could serve customers better while maintaining stability. The RBI, under Governor Bimal Jalan, was cautiously open to expanding the private banking sector, but only to institutions that met the highest standards of governance and financial strength.

For Kotak, the journey toward a banking license had begun years earlier. "I have always believed an institution is more important than an individual, and institutions must go on forever," he would later say, articulating the philosophy that would convince regulators. The NBFC had deliberately maintained higher capital adequacy ratios than required, implemented systems and processes that exceeded regulatory requirements, and most importantly, had survived multiple financial crises without a blemish.

The application process was grueling. The RBI's scrutiny covered every aspect of the business—from the quality of assets to the sophistication of risk management systems, from the independence of board members to the sustainability of the business model. There were numerous rounds of meetings, presentations, and clarifications. The RBI was particularly concerned about whether an NBFC, accustomed to wholesale lending and car financing, could build the retail liability franchise that was essential for a bank.

A critical factor in the RBI's decision was the ownership structure. At the time, Uday Kotak had a 56% stake in the company while Anand Mahindra held a 5% stake. While the high promoter holding would later become a contentious issue, at the time of licensing, it was seen as ensuring "skin in the game"—the promoters had everything to lose if the bank failed, ensuring aligned interests with depositors.

The regulatory approval came with conditions. The newly formed bank would need to meet priority sector lending requirements, set up rural and semi-urban branches, and most importantly, build a deposit franchise quickly. The RBI was clear: this was not just a license to continue the existing NBFC business with a banking wrapper, but a responsibility to serve the broader financial inclusion agenda.

On March 22, 2003, Kotak Mahindra Bank formally came into existence. In February 2003, the company was given the license to carry on banking business by the Reserve Bank of India (RBI). This approval created banking history since Kotak Mahindra Finance Ltd is the first non-banking finance company in India to convert them into a bank as Kotak Mahindra Bank Ltd.

The immediate challenges were immense. Building a deposit franchise from scratch was perhaps the most daunting. Unlike HDFC Bank, which had inherited a deposit base from HDFC, or ICICI Bank, which had the ICICI brand, Kotak Mahindra Bank had to convince depositors to trust a newly converted NBFC with their savings. The bank launched with just a handful of branches, primarily in Mumbai and other major cities.

The technology infrastructure posed another challenge. As an NBFC, Kotak Mahindra Finance had operated with relatively simple systems adequate for lending operations. As a bank, it needed robust core banking systems, ATM networks, and the ability to handle millions of transactions daily. The bank invested heavily in technology, choosing Finacle as its core banking platform and building one of the most modern technology infrastructures among Indian banks.

The competitive landscape was formidable. ICICI Bank and HDFC Bank had a decade's head start and were already well-established. Foreign banks like Citibank and Standard Chartered dominated the premium segment. Public sector banks controlled the mass market. Kotak Mahindra Bank needed to find its niche—affluent urban Indians who valued service and were willing to pay for quality.

The strategy was deliberate and focused. Rather than trying to be everything to everyone, Kotak Mahindra Bank positioned itself as a premium bank for discerning customers. Minimum balance requirements were kept high, branches were located in affluent neighborhoods, and the service model emphasized relationship banking over transactional banking. The tagline "Think Investments, Think Kotak" positioned the bank as a wealth creator, not just a place to park money.

The existing businesses provided crucial synergies. Investment banking clients became corporate banking customers. Car loan customers were cross-sold savings accounts. The securities broking business provided a ready distribution network for third-party products. The mutual fund and life insurance businesses created additional touchpoints with customers. This integrated model, where various businesses reinforced each other, would become a key competitive advantage.

By the end of 2003, the transformation was well underway. The bank had opened 29 branches, launched Internet banking, and more importantly, had begun building a deposit franchise. The CASA (Current Account Savings Account) ratio, a key metric for banks, was improving steadily. The market responded positively—Kotak Mahindra Bank's stock price rose significantly, validating the transformation strategy.

The psychological impact of becoming a bank cannot be overstated. For Uday Kotak, it represented the culmination of an 18-year journey from a small bill discounting firm to a full-fledged bank. For employees, it meant working for an institution that could now compete with the best in the industry. For customers, it meant access to a full suite of banking services from an institution they had learned to trust.

But perhaps most significantly, the banking license represented a platform for future growth. As a bank, Kotak Mahindra could access low-cost deposits, expand into new businesses, and most importantly, control its own destiny. The transformation from NBFC to bank wasn't just a regulatory change—it was the foundation for building one of India's most valuable financial institutions.

Looking back, the banking license was both an ending and a beginning. It was the end of Kotak Mahindra's journey as an NBFC, but the beginning of its journey to become one of India's most valuable private sector banks. The real work of building a banking franchise had just begun.

V. Scaling Through Strategic Acquisitions (2004-2015)

With the banking license secured and the initial transformation complete, Kotak Mahindra Bank entered its next phase: aggressive but calculated expansion through strategic acquisitions. This period would see Uday Kotak perfect his playbook of buying out partners at opportune moments and making transformative acquisitions that would catapult the bank from a niche player to a major force in Indian banking.

The first move came in 2005. In 2005, Kotak Mahindra Bank acquired Ford Credit's 40% stake in Kotak Mahindra Primus, making it a wholly owned subsidiary of the group. Kotak Mahindra Primus was subsequently renamed as Kotak Mahindra Prime. The timing was strategic. Ford Credit was reassessing its global strategy and looking to exit non-core markets. For Kotak, full ownership of the car financing business meant complete control over a highly profitable vertical that was generating substantial returns.

The following year brought an even more significant transaction. In 2006, Kotak Mahindra Bank bought out Goldman Sachs' 25% stake in Kotak Mahindra Capital for ₹210 crore (US$46.35 million) and 25% in Kotak Securities for ₹123 crore (US$27.15 million), turning both companies into its wholly owned subsidiaries. The total consideration of ₹333 crore seemed substantial at the time, but it would prove to be a bargain. The joint venture lasted until March 2006, when Kotak Mahindra bought out Goldman Sachs' stake in both ventures for US$70 million as both banks sought to pursue independently the growing investment banking market in India.

The Goldman Sachs exit was particularly symbolic. After 11 years of partnership, both parties recognized that their interests were diverging. Goldman wanted to establish its own presence in the booming Indian market, while Kotak wanted full control of businesses that were becoming increasingly central to the bank's strategy. The parting was amicable, with both sides acknowledging the value created through the partnership. For Kotak, it meant that two of its most profitable businesses—investment banking and securities broking—were now fully under its control.

These buyouts demonstrated Kotak's strategic acumen. He had partnered with global giants when he needed their expertise and credibility, learned from them, built the businesses, and then bought them out when the valuations were still reasonable. The partnerships had served their purpose, and now it was time to capture the full value of these businesses.

But the most transformative acquisition was yet to come. By 2014, Kotak Mahindra Bank had grown substantially but still lacked the scale to compete with the largest private sector banks. HDFC Bank and ICICI Bank were several times larger, and even newer entrants like Axis Bank had greater reach. Kotak needed a game-changing acquisition to achieve scale, and he found it in ING Vysya Bank.

In 2014, Kotak Mahindra Bank announced the acquisition of ING Vysya Bank in a deal valued at ₹15,000 crore (US$2.34 billion). With the merger completed in 2015, Kotak Mahindra Bank had almost 40,000 employees, and the number of branches reached 1,261. This was not just an acquisition—it was a merger that would fundamentally transform Kotak Mahindra Bank's scale and reach.

ING Vysya Bank brought several strategic advantages. First, it provided immediate scale—the combined entity would have assets of over ₹2 lakh crore, making it the fourth-largest private sector bank in India. Second, it brought geographical diversification. While Kotak was strong in western and northern India, ING Vysya had a significant presence in southern India, particularly in Karnataka, Andhra Pradesh, and Tamil Nadu. Third, it brought a strong SME banking franchise, complementing Kotak's strength in affluent retail and corporate banking.

The merger structure was elegant—an all-stock deal where ING Vysya shareholders received 725 Kotak shares for every 1,000 ING Vysya shares held. The proposed merger is an all-stock merger. 1000 shares of Rs.10 each of ING Vysya will receive 725 shares of Rs.5 each of Kotak Mahindra Bank. This exchange ratio indicates an implied price of Rs.790 for each ING Vysya share based on the average closing price of Kotak shares during one month to November 19, 2014, which is a 16% premium to a like measure of ING Vysya market price.

The regulatory approval process was smooth, with the RBI approving the merger in March 2015. Vysya and Kotak announced their intention to merge their respective businesses on 20 November 2014. On 31 March 2015 the Reserve Bank of India has approved this transaction with effect from 1 April 2015. The integration, however, was complex. The two banks had different cultures, systems, and processes. ING Vysya was an 80-year-old institution with its own legacy and way of doing business. Kotak Mahindra Bank was younger, more aggressive, and entrepreneurial.

Uday Kotak personally led the integration effort, emphasizing that no ING Vysya employee would lose their job due to the merger. The employees of ING Vysya will also be at the benefit as Mr.Kotak has announced that there will be no drastic job cuts post-merger. Employees are the major concern in the service industry. As the employees will be satisfied, there will be no post-merger difficulties. This commitment to protecting employees helped smooth the integration process and maintain morale during a potentially turbulent period.

The merger also had an important side benefit—it helped Kotak comply with RBI regulations on promoter shareholding. The deal will also help Uday Kotak reduce the promoter's stake in Kotak Bank, in line with the road map given by the Reserve Bank of India. After the merger, promoter shareholding in Kotak Bank will come down from 40 per cent to 34 per cent. The dilution through fresh equity issuance for the merger naturally reduced Uday Kotak's percentage holding, though this would remain a contentious issue with the regulator for years to come.

After the merger, ING Group, which controlled ING Vysya Bank, obtained a 6.5% stake in Kotak Mahindra Bank. ING became the second-largest shareholder, and while they had a lock-in period, their presence provided additional international credibility to the combined entity.

By 2015, the transformation was complete. What had started as a small NBFC with a handful of employees had become one of India's largest private sector banks with over 40,000 employees, 1,261 branches, and a presence across all major business lines. The acquisition strategy had worked brilliantly—each buyout and acquisition had been timed perfectly, executed flawlessly, and integrated successfully.

The period from 2004 to 2015 demonstrated Uday Kotak's evolution from entrepreneur to institution builder. He had shown the ability not just to grow organically but to execute complex M&A transactions, integrate diverse businesses, and create value through consolidation. The ING Vysya merger, in particular, showed that Kotak Mahindra Bank could execute large-scale transformative transactions that would typically be the preserve of much larger institutions.

As 2015 ended, Kotak Mahindra Bank stood transformed. It was no longer a niche player but a serious contender in Indian banking. The foundation was now in place for the next phase of growth—one that would be driven not by acquisitions but by digital transformation and innovation. The timing would prove fortuitous, as India was about to undergo a digital revolution that would fundamentally change banking forever.

VI. The Demonetization Moment & Digital Pivot (2016-2020)

November 8, 2016, would go down as one of the most dramatic moments in Indian economic history. When Prime Minister Narendra Modi announced the demonetization of ₹500 and ₹1,000 notes, effectively removing 86% of currency in circulation overnight, it sent shockwaves through the economy. For Kotak Mahindra Bank, this crisis would become an extraordinary opportunity to accelerate its digital transformation and double its customer base in record time.

While other banks scrambled to manage the chaos of currency exchange and endless queues, Uday Kotak saw a different opportunity. He recognized that demonetization would fundamentally alter Indian consumers' relationship with cash and digital payments. More importantly, it would create an urgent need for bank accounts as the government pushed for a transition to formal banking channels. Within four months of the announcement, Kotak Mahindra Bank would launch one of the most successful digital banking products in Indian history.

In March 2017, Kotak Mahindra Bank launched an online savings account called Kotak 811, named after the date Prime Minister Narendra Modi had announced demonetisation in the previous year (8 November), which according to Uday Kotak was "the day that changed India." Kotak 811 helped the bank double its number of customers by September 2018.

The development of Kotak 811 was a masterclass in rapid innovation. The bank assembled a cross-functional team that worked round the clock to create a completely digital account opening process. Using Aadhaar-based e-KYC, customers could open an account in minutes without visiting a branch or submitting physical documents. The account had zero balance requirements, making it accessible to millions who had previously been excluded from formal banking due to minimum balance constraints.

On 8th November 2016, the announcement of demonetization, sent citizens and banks scrambling towards a more digitalized India. Kotak Mahindra took quick action and in just four months, launched its 811 mobile app getting everything down from online banking, shopping, travel bookings to mobile recharge.

The marketing strategy for 811 was equally innovative. The bank leveraged digital channels extensively, using social media, online advertising, and influencer marketing to reach younger, digitally-savvy consumers. The name itself—811—was brilliant marketing, immediately connecting the product to the transformative moment of demonetization while being easy to remember. The tagline "Banking that keeps up with you" positioned it as a modern, mobile-first banking solution for the new India.

The numbers were staggering. The lender operates Kotak811, a digital offering that has emerged as its strongest customer acquisition tool in recent years. Kotak811, which allows onboarding of customers digitally and within "three minutes" without paperwork, serves nearly 20 million customers. By December 2023, 811 accounted for 72% of new savings accounts opened at the bank. The platform wasn't just acquiring customers; it was acquiring them at a fraction of the traditional cost, with digital onboarding costing less than one-tenth of branch-based acquisition.

But 811 was more than just an account opening platform. It became a comprehensive digital ecosystem offering everything from investments to insurance, bill payments to shopping. The bank integrated e-commerce capabilities through its Kaymall platform, allowing customers to shop from partners like Flipkart directly through the app. This strategy of embedding financial services into lifestyle activities was ahead of its time, predating the super-app strategies that would later become popular.

The digital transformation extended beyond 811. In 2016, Kotak made another strategic move into the payments space. In 2016, Bharti Airtel and Kotak Mahindra Bank started an 80:20 joint venture called Airtel Payments Bank. While this partnership would eventually be unwound—In 2021, Kotak Mahindra Bank sold its 8.57% stake in Airtel Payments Bank to Bharti Enterprises for ₹295 crore (US$39.81 million)—it demonstrated Kotak's willingness to experiment with new models and partnerships in the digital space.

The period also saw significant activity in consolidating ownership of existing businesses. In April 2017, Kotak Mahindra Bank acquired Old Mutual's 26% stake in Kotak Mahindra Old Mutual Life Insurance for ₹1,292 crore (US$198.4 million), making the life insurance company its wholly owned subsidiary. This acquisition was strategic—life insurance was becoming increasingly digital, and full ownership would allow better integration with the bank's digital platforms.

The microfinance sector presented another opportunity for digital-led expansion. In 2016, Kotak Mahindra Bank acquired BSS Microfinance for ₹139.2 crore (US$20.72 million). This was followed by In 2023, Kotak Mahindra Bank acquired microfinancier Sonata Finance for ₹537 crore (US$64 million). These acquisitions gave Kotak access to millions of underbanked customers who could be gradually brought into the formal banking system through digital channels.

The bank also capitalized on the fintech partnership trend. Rather than viewing fintech companies as threats, Kotak partnered with them to enhance its digital capabilities. The bank became a preferred banking partner for numerous fintech startups, providing them with banking infrastructure while benefiting from their innovation and customer acquisition capabilities. Companies like KredX and Rupeek relied on Kotak for their banking needs, creating a symbiotic relationship that enhanced both parties' capabilities.

The digital push wasn't without challenges. The rapid scaling of digital channels put pressure on the bank's IT infrastructure. System outages became more frequent as transaction volumes soared. The bank's core banking system, while modern by Indian standards, struggled to keep pace with the exponential growth in digital transactions. These infrastructure challenges would later attract regulatory scrutiny, but for the moment, the focus remained on growth.

Competition in the digital space was intensifying. New-age fintech companies like Paytm and PhonePe were acquiring customers at unprecedented rates. Traditional banks like HDFC and ICICI were also investing heavily in digital transformation. Kotak's response was to focus on quality over quantity—while others chased customer numbers, Kotak focused on acquiring profitable customers who would use multiple products.

The COVID-19 pandemic in 2020 accelerated digital adoption dramatically. With branches closed and physical interactions limited, digital channels became the primary mode of banking. Kotak's early investments in digital infrastructure paid off handsomely. While other banks struggled to scale their digital operations, Kotak was able to seamlessly serve customers through its digital channels.

The bank also demonstrated its commitment to national causes during the pandemic. In 2020, Kotak pledged to donate ₹50 crore to the PM CARES Fund to fight against the COVID-19 pandemic in India. This gesture, while philanthropic, also reinforced the bank's image as a responsible corporate citizen.

By the end of 2020, Kotak Mahindra Bank's digital transformation was largely complete. The bank had successfully pivoted from a branch-led model to a digital-first approach. Over 90% of transactions were happening through digital channels. The 811 platform had emerged as one of India's most successful digital banking initiatives. The customer base had more than doubled since demonetization.

But success brought scrutiny. The rapid digital expansion had exposed weaknesses in the bank's IT infrastructure and risk management systems. The Reserve Bank of India was watching closely, concerned about the systemic risks posed by rapid digitalization without adequate controls. The stage was being set for a confrontation between the regulator and the bank that would define the next phase of Kotak's journey.

The digital pivot of 2016-2020 had transformed Kotak Mahindra Bank from a traditional bank with digital capabilities to a digital bank with physical presence. It had demonstrated the ability to innovate rapidly, scale efficiently, and compete with both traditional banks and new-age fintech companies. But it had also created new vulnerabilities that would soon be exposed, leading to one of the most challenging periods in the bank's history.

VII. RBI Battles & Regulatory Challenges

The relationship between Kotak Mahindra Bank and the Reserve Bank of India has been one of the most complex and contentious in Indian banking history. What began as a regulatory blessing—the first NBFC to receive a banking license—evolved into a decades-long struggle over ownership, control, and compliance that would test Uday Kotak's diplomatic skills and the bank's institutional resilience.

The roots of the conflict trace back to the original banking license in 2003. When Kotak Mahindra became the first NBFC-turned-bank, the central bank had some rules on promoters shareholding limits. As per RBI, promoters needed to hold at least 49% of the bank's paid-up capital for a period of five years. The idea behind this mandate was to ensure that promoters had skin in the banking game.

Initially, this wasn't a problem. At the time, Uday Kotak had a 56% stake in the company while Anand Mahindra held a 5% stake. Kotak was well above the minimum requirement. But in 2008, the relationship took its first adversarial turn. The twist in the 'Kotak vs RBI' story comes in 2008. The central bank asked Kotak about "not reducing the shareholding to 49% as prescribed even after five years. It also asked the bank to show its plan to reduce it further to 10%.

The confusion stemmed from differing interpretations of the regulations. Kotak Mahindra Bank argued that the 49% was a minimum requirement, not a maximum. The RBI, however, had evolved its thinking on bank ownership, now viewing concentrated promoter holdings as a governance risk. This fundamental disagreement would color the relationship for the next decade.

In 2013, the RBI issued new banking license guidelines that dramatically changed the landscape. To comply with the 2013 guidelines, the promoter group had to trim down its stake in Kotak Mahindra Bank from 44.96 percent in 2013 to 15 percent by 2015. The central bank mandated that promoters reduce their stake to 15% within a specified timeframe. For Uday Kotak, who still held around 40% of the bank, this meant a massive dilution.

The bank's response was creative—perhaps too creative for the RBI's comfort. In 2018, Kotak Mahindra Bank announced it would issue preference shares to reduce the promoter's stake. The bank said it would do so not by selling equity shares, but by issuing non-cumulative preference shares – an instrument that allows investors to receive dividends on profits before they are distributed among common shareholders. Since preference shares don't carry voting rights, Kotak argued this met the spirit of the regulation by reducing his control while maintaining economic interest.

The RBI rejected this interpretation forcefully. In August 2018, they made it clear that the dilution had to be through equity shares, not preference shares. This led to an unprecedented move—In December 2018, the Kotak Mahindra Bank took the Reserve Bank to court over the matter. A private bank taking the central bank to court was almost unheard of in Indian banking.

The legal battle was as much about principle as percentages. Kotak argued that the RBI was changing rules retrospectively and that preference shares were a legitimate form of capital. The RBI countered that the regulations were clear and that concentrated ownership posed systemic risks. Behind the legal arguments lay a deeper tension about regulatory authority and institutional autonomy.

When the RBI asked the bank to reduce its promoter holding to 49%, Kotak Mahindra Bank simply declassified Anand Mahindra and his family as a promoter in 2009. The bank claimed that Mahindra had diluted his stake significantly and that he shouldn't be a promoter anymore. That meant the promoter shareholding would automatically drop to 48.50% in the books. It would be in line with what the RBI wanted. But the RBI was having none of that. They said that the only way that Anand Mahindra would be a non-promoter was if the bank actually dropped 'Mahindra' from its name. And well, we all know that didn't happen.

The standoff continued until January 2020, when both parties agreed to an out-of-court settlement. The central bank accepted Kotak Mahindra Bank's proposal to reduce promoter stake to only 26 percent within six months, relaxing its insistence on cutting it to 15 percent. In January 2020, the central bank relented, agreeing to the private bank's proposal in an out-of-court settlement.

"The settlement was more or less a win for the bank's promoter, Uday Kotak and his demands," Hazari wrote. While Kotak had to reduce his stake, the 26% threshold was significantly higher than the 15% originally mandated. In June 2020, Uday Kotak sold 56 million shares held by him in the bank for Rs 6,900 crore through a block deal, in an effort to reduce his stake from 28.93% to 26.1%.

But the regulatory challenges were far from over. Even as the ownership issue was being resolved, new problems were emerging. The bank's rapid digital expansion had exposed weaknesses in its IT infrastructure. System outages were becoming frequent, and the RBI was growing concerned about operational risks.

The situation came to a head in April 2024. On 24th April 2024, the Reserve Bank of India (RBI) ordered Kotak Mahindra Bank to stop onboarding new customers online and through mobile banking. The main reason behind these restrictions by RBI is Kotak Mahindra Bank's red flags about serious data security concerns and flawed IT infrastructure.

The Reserve Bank of India (RBI) on April 24 barred Kotak Mahindra Bank from issuing fresh credit cards and onboarding new customers through online and mobile banking channels over "serious shortcomings" in the bank's information technology (IT) infrastructure. These are said to have led to frequent outages, including a major disruption on April 15, 2024. According to a press release from the RBI, "these actions are necessitated based on significant concerns arising out of the Reserve Bank's IT examination of the bank for 2022 and 2023 and the continued failure on part of the bank to address these concerns in a comprehensive and timely manner".

The timing was particularly painful. Ashok Vaswani had just taken over as CEO in January 2024, succeeding Uday Kotak. The restrictions were imposed shortly after Ashok Vaswani assumed the role of managing director and CEO on January 1, 2024. The new leadership was immediately thrust into crisis management mode.

The restrictions were severe. The bank couldn't onboard new customers digitally or issue new credit cards—a massive blow for an institution that had built its growth strategy around digital acquisition. The 811 platform, which had been the crown jewel of the digital strategy, was effectively neutered. Credit card issuance, a high-margin business, was frozen.

The bank responded with a comprehensive remediation program. To resolve these issues, Kotak Mahindra Bank implemented several remedial measures, including appointing Grant Thornton Bharat as an external auditor to identify and fix gaps in its IT systems. Technology teams were expanded, systems were upgraded, and new controls were implemented. The bank worked closely with the RBI to address each concern systematically.

After ten months of intensive work, relief finally came. The Reserve Bank of India (RBI) has lifted restrictions on Kotak Mahindra Bank, allowing it to onboard new customers via online and mobile banking from February 12. The central bank also permitted the lender to issue fresh credit cards. The lifting of restrictions validated the remediation efforts but also served as a warning about the importance of robust IT infrastructure in modern banking.

The regulatory battles had extracted a significant toll. Beyond the direct business impact—credit card numbers had dropped from over 6 million to 5 million during the restriction period—there was reputational damage. The bank's stock price had been volatile, and questions were raised about governance and risk management.

Yet, these challenges also demonstrated institutional resilience. The bank had stood up to the regulator when it believed it was right, compromised when necessary, and ultimately addressed deficiencies when identified. The ability to navigate complex regulatory relationships while maintaining business momentum would become a defining characteristic of the institution.

The regulatory saga also highlighted a broader tension in Indian banking—the balance between entrepreneurial drive and regulatory compliance, between innovation and stability, between founder control and institutional governance. Kotak Mahindra Bank had become the test case for these tensions, and its experiences would shape regulatory thinking for years to come.

VIII. Modern Era & Leadership Transition (2021-Present)

The transition from founder-led to professionally managed is perhaps the most critical test for any institution. For Kotak Mahindra Bank, this transition began in earnest in 2023 when Uday Kotak, after 38 years at the helm, stepped down as CEO, marking the end of an era and the beginning of a new chapter under professional management.

The seeds of transition had been planted earlier. The RBI's regulations on CEO tenure had made it clear that Kotak's time as chief executive was limited. According to the RBI rules 2021, the MD and CEOs or whole-time director (WTD) are allowed to continue for up to 15 years. Having already served well beyond this period, Kotak's continuation had required special dispensation. By 2023, it was clear that a succession plan needed to be executed.

On September 1, 2023, Uday Kotak stepped down as Managing Director and CEO, about four months before his extended term was to end. Vaswani will succeed Uday Kotak, who has quit as the MD of the bank in September this year. Uday Kotak was set to retire from his executive role in December but it was cut short by around four months. Kotak's exit from the bank was said to be due to personal reasons.

The choice of successor was carefully considered. Mumbai-headquartered Kotak Mahindra Bank on Saturday announced that the Reserve Bank of India (RBI) has approved the appointment of Ashok Vaswani as the Managing Director and Chief Executive Officer of the bank for a period of three years, likely from January 1, 2024. Vaswani brought impeccable credentials—over three and a half decades of global banking experience, including senior roles at Citigroup and Barclays. Both these stints had Vaswani leverage forward-leaning technology with a vision to deliver strong bottom-line growth apart from building and growing businesses at scale, building result-oriented teams, and establishing transformational partnerships, compliance and industrial strength across Corporate and Consumer businesses. He has also headed divisions such as personal and corporate banking, retail banking, and retail and business banking during his stint at Barclays. He was also the CEO of Barclays Africa from October 2011-September 2012 and the CEO of the bank's Cards Europe from February-October 2010.

Interestingly, Vaswani and Kotak shared a connection beyond banking. Ashok Vaswani also happens to be Uday Kotak's junior from Sydenham College. Both were chartered accountants who had taken unconventional paths to banking leadership. Kotak's endorsement was unequivocal: "I am delighted that the RBI has approved our recommendation, Ashok Vaswani, as the next CEO of Kotak Mahindra Bank. I am proud that we bring a 'Global Indian' home to build Kotak and India of tomorrow".

The transition period was carefully managed. Kotak remained on the board as a non-executive director, providing continuity and guidance without interfering in operational matters. Vaswani, a graduate of the same Mumbai college attended by Kotak, will benefit from the support and mentorship of the bank's founder, Kotak, who is still on the board. This unique advantage sets him apart from many new CEOs who took the helm at other private banks such as HDFC Bank, ICICI Bank, Axis Bank, and IndusInd Bank, where the start CEOs made an exit after retirement or otherwise.

Vaswani inherited a bank at an inflection point. The immediate challenge was dealing with the RBI restrictions on digital onboarding and credit card issuance that had been imposed in April 2024. But beyond the immediate crisis, there were strategic questions about the bank's future direction. How would it compete with larger rivals who had achieved greater scale? How would it differentiate itself in an increasingly digital and commoditized banking market?

The new CEO's initial pronouncements provided clues to his strategy. "The challenge in the (Kotak) story from here on is how we scale. Scale not just for the sake of it but the scale for relevance," said Vaswani. While explaining the 'scale' remark, Vaswani mentioned that the bank has a very wide platform. "The challenge is really going to be the identification of those areas where we want to have and create a disproportionate impact and grow aggressively to scale the business."

Under Vaswani's leadership, the bank continued its acquisition strategy, though with a different focus. In 2021, Kotak Mahindra Group acquired the vehicle financing portfolio of Volkswagen Finance India and passenger vehicle financing portfolio of Ford Credit India. In 2022, it acquired the agriculture and healthcare equipment financing portfolio of DLL India. These portfolio acquisitions provided immediate scale in specific segments without the complexity of full mergers.

The most significant transaction of the modern era came in 2024. In February 2024, Zurich Insurance Group announced its acquisition of a 70% stake in Kotak Mahindra General Insurance for ₹5,560 crore (US$660 million). Zurich acquires 70% of Kotak General Insurance, becoming the first foreign insurer to enter India since the FDI rules were amended to allow up to 74% foreign ownership in 2021. Zurich and Kotak will jointly build a leading general insurer in India, bringing together Zurich's global insurance leadership and scale with Kotak's local expertise and reach.

This transaction was strategic on multiple levels. It brought significant capital to the general insurance business, provided access to Zurich's global expertise and products, and importantly, allowed Kotak Mahindra Bank to focus on its core banking operations while maintaining a stake in the insurance business. The deal valued the general insurance business at approximately ₹8,000 crore, validating the value creation in this subsidiary.

The technology transformation initiated under Uday Kotak continued under new leadership. Before exiting, Uday Kotak had initiated a new strategy and put together a team to guide the bank's transformation into a tech-savvy institution by focusing on building customer excellence similar to that of Amazon. The new strategy has three main parts. First, it wants to make the customer experience as good as Amazon's. Second, it's all about making things better for employees by giving them the right tools and systems. And third, there's a big focus on getting more work done efficiently.

The lifting of RBI restrictions in February 2025 marked a crucial milestone for the new leadership. The Reserve Bank of India (RBI) has lifted restrictions on Kotak Mahindra Bank, allowing it to onboard new customers via online and mobile banking from February 12. The central bank also permitted the lender to issue fresh credit cards. This restoration of full business capabilities came after intensive remediation efforts, including comprehensive IT system upgrades and external audits.

The modern era also saw evolution in the bank's market positioning. While maintaining its premium positioning, there was recognition that scale required broader market participation. The 811 platform was enhanced to serve not just urban millennials but also tier-2 and tier-3 city customers. The SME banking franchise, strengthened through the ING Vysya acquisition, became a key growth driver.

Financial performance remained robust despite the challenges. As of December 2023, the bank operated 1,869 branches and 3,239 ATMs, including branches in GIFT City and DIFC (Dubai). The international presence, though limited, signaled ambitions beyond domestic banking. Asset quality remained among the best in the industry, with net NPAs below 1%, validating the conservative underwriting culture instilled by the founder.

The cultural transition was perhaps the most delicate aspect. Kotak Mahindra Bank had been synonymous with Uday Kotak for nearly four decades. Employees, customers, and investors had to adjust to new leadership. Vaswani's approach was to respect the legacy while bringing his own vision. He emphasized continuity in values—trust, conservatism, customer focus—while pushing for greater scale and efficiency.

Looking ahead, the bank faces both opportunities and challenges. The Indian banking sector is undergoing rapid consolidation, creating opportunities for acquisition. Digital banking is becoming the primary channel for customer interaction, requiring continuous technology investment. Competition from both traditional banks and fintech companies is intensifying. Regulatory requirements are becoming more stringent.

Yet, the foundation laid over four decades provides significant advantages. The bank has one of the strongest brands in Indian banking, a diversified business model spanning retail, corporate, and investment banking, a proven track record of successful acquisitions and integrations, and importantly, a culture of compliance and conservatism that has helped it navigate multiple crises.

The transition from founder to professional management is still in its early stages. While Uday Kotak's presence on the board provides continuity, the true test will come when the bank faces its next major crisis or opportunity without his executive leadership. Early signs are encouraging—the successful resolution of RBI restrictions, continued business growth, and maintained financial discipline suggest the institution has successfully transcended its founder.

IX. Playbook: Business & Investing Lessons

The Kotak Mahindra story offers a masterclass in building a financial institution in an emerging market. The playbook that emerges from nearly four decades of navigation through India's complex financial landscape provides lessons that extend far beyond banking. Let's deconstruct the key strategies and principles that enabled a three-person startup to become one of Asia's most valuable banks.

The Partnership Playbook: Strategic Entry and Exit

Perhaps no aspect of Kotak's strategy has been more distinctive than his approach to partnerships. "Our joint venture partnership with Goldman Sachs, with Ford Credit, with Old Mutual in the life insurance business. I'm a great believer that it is important for Indian companies to learn and implement and really thereafter execute well."

The pattern was consistent: identify a capability gap, find the best global partner with that expertise, structure a joint venture that maintains control, absorb the knowledge and build the business, and finally, buy out the partner when the learning is complete and valuations are reasonable. Each partnership—Goldman Sachs for investment banking, Ford Credit for auto financing, Old Mutual for life insurance—followed this template.

What made this approach successful was Kotak's clarity about the lifecycle of partnerships. Unlike many Indian entrepreneurs who either became overly dependent on foreign partners or engaged in acrimonious battles for control, Kotak viewed partnerships as stepping stones. The joint venture lasted until March 2006, when Kotak Mahindra bought out Goldman Sachs' stake in both ventures for US$70 million as both banks sought to pursue independently the growing investment banking market in India. The parting was amicable, with both sides having achieved their objectives.

Building Trust in Financial Services

In financial services, trust is the ultimate currency. Kotak understood this from day one. The decision to partner with the Mahindra family in 1986 wasn't just about capital—it was about borrowing credibility. The Mahindra name opened doors and provided assurance to customers and regulators alike.

This focus on trust manifested in multiple ways. The bank maintained higher capital adequacy ratios than required, even when it meant slower growth. It avoided the temptations that felled competitors—the stock market excesses of 1992, the NBFC exuberance of the late 1990s, the real estate bubble of the 2000s. At that stage we were a non-bank financial company. There were more than 4,000 NBFCs, and barely I think around 20 survived. You then then came to the conclusion that if you did the right thing, which was within the law of the land, it always worked for you.

Managing Regulatory Relationships

The complex relationship with the RBI offers crucial lessons in managing regulatory relationships in highly regulated industries. While Kotak was willing to challenge the regulator when he believed the bank was right—even taking the unprecedented step of going to court—he also knew when to compromise.

The preference shares controversy illustrated this balance. When the RBI rejected the bank's interpretation, rather than prolonging the battle, Kotak negotiated a settlement that, while requiring dilution, was still favorable compared to original requirements. The central bank accepted Kotak Mahindra Bank's proposal to reduce promoter stake to only 26 percent within six months, relaxing its insistence on cutting it to 15 percent.

The key insight is that regulatory relationships are long-term games. Short-term victories that damage regulatory trust are pyrrhic. The bank's eventual compliance with RBI directives, even when disagreeing with them, maintained the relationship that was essential for long-term success.

Capital Allocation Discipline

One of the most underappreciated aspects of Kotak's success has been capital allocation discipline. Every major acquisition was accretive, every partnership was structured to ensure value capture, and every exit was timed to maximize returns. The ING Vysya acquisition, while the largest, followed the same disciplined approach—an all-stock deal that provided immediate scale without straining capital.

The decision to sell 70% of the general insurance business to Zurich for ₹5,560 crore exemplified this discipline. Rather than trying to build a subscale insurance business with massive capital requirements, Kotak chose to partner with a global leader while retaining significant upside through the 30% stake.

The Importance of Technology Infrastructure

The RBI restrictions of 2024 provided a costly lesson in the importance of robust technology infrastructure. The main reason behind these restrictions by RBI is Kotak Mahindra Bank's red flags about serious data security concerns and flawed IT infrastructure. The bank's rapid digital expansion had outpaced its infrastructure capabilities, leading to frequent outages and regulatory action.

The lesson is clear: in modern banking, technology infrastructure is not just an operational necessity but a regulatory requirement and competitive differentiator. The bank's response—comprehensive remediation including external audits and significant investment—showed that this lesson was learned, albeit painfully.

Balancing Growth with Risk Management

Throughout its history, Kotak Mahindra Bank has demonstrated that sustainable growth comes from balancing aggression with conservatism. The bank was aggressive in pursuing opportunities—whether the car financing boom of the 1990s or the digital revolution post-demonetization—but conservative in underwriting and risk management.

This balance is reflected in the bank's consistently superior asset quality. Even through multiple economic cycles and crises, the bank maintained NPAs well below industry averages. This wasn't luck but the result of institutional discipline in credit underwriting, even when it meant sacrificing growth.

The Platform Approach

Rather than viewing different businesses as separate silos, Kotak built an integrated platform where each business reinforced the others. Investment banking brought corporate relationships that became commercial banking clients. Car loans customers were cross-sold savings accounts and insurance. The securities broking business provided distribution for mutual funds and wealth management.

This platform approach created multiple competitive advantages: customer acquisition costs were amortized across products, relationships were deeper and stickier, and the bank could offer comprehensive solutions rather than individual products. The 811 platform represented the digital evolution of this strategy, creating a single interface for all financial needs.

Timing and Opportunism

Perhaps the most important lesson is about timing. Every major move—from starting car financing in 1990 to launching 811 after demonetization—was perfectly timed to capitalize on structural changes in the Indian economy. This wasn't luck but the result of deep understanding of India's economic evolution and the patience to wait for the right moment.

The banking license application in 2003 came just as the RBI was open to NBFC conversions. The ING Vysya acquisition happened when ING was looking to exit and valuations were reasonable. The digital push coincided with India's smartphone revolution and demonetization. Each move captured a wave rather than trying to create one.

Institution Building Over Personal Wealth

"I have always believed an institution is more important than an individual, and institutions must go on forever. Individuals may come and go." This philosophy, articulated consistently throughout Kotak's tenure, explains many strategic decisions. The willingness to dilute shareholding, bring in professional management, and eventually step down as CEO all reflected prioritizing institutional sustainability over personal control.

The successful transition to professional management under Ashok Vaswani validates this approach. The institution has transcended its founder, a rare achievement in Indian business where many enterprises struggle to survive leadership transitions.

X. Analysis & Bear vs. Bull Case

As we evaluate Kotak Mahindra Bank's position today and its prospects for tomorrow, we find an institution at a fascinating inflection point. The bank has successfully navigated its founder transition, resolved its immediate regulatory challenges, and maintained its financial strength. Yet it faces intensifying competition, technology challenges, and the perpetual question of whether it can achieve the scale necessary to compete with India's banking giants.

Competitive Positioning

In the Indian private banking landscape, Kotak Mahindra Bank occupies a unique position. With a market capitalization of over ₹3.5 lakh crore, it ranks as the third most valuable private bank, behind HDFC Bank and ICICI Bank but ahead of Axis Bank. However, in terms of assets and branch network, it remains significantly smaller than the top two, creating both a challenge and an opportunity.

The bank's strengths lie in its niche dominance. In investment banking, Kotak consistently ranks among the top three. In wealth management for affluent Indians, it has built a formidable franchise. The 811 platform has established it as a leader in digital account opening. In asset quality, it consistently outperforms peers with NPAs below 2%.

Yet the competitive landscape is evolving rapidly. HDFC Bank's merger with HDFC Ltd has created a behemoth with assets exceeding ₹20 lakh crore. ICICI Bank has successfully transformed from a corporate bank to a retail powerhouse. New-age fintech companies are attacking profitable niches like payments and consumer lending. Foreign banks, while retreating from retail, are competing aggressively for the affluent segment that Kotak has traditionally dominated.

Financial Metrics Deep Dive

The numbers tell a story of quality over quantity. The bank's Return on Equity (ROE) has consistently ranged between 12-14%, respectable though not exceptional. The Net Interest Margin (NIM) at around 5% is among the highest in the industry, reflecting the bank's pricing power and affluent customer base. The cost-to-income ratio around 50% shows operational efficiency, though there's room for improvement through greater scale.

The CASA ratio—the proportion of low-cost current and savings deposits—at approximately 48% is healthy but not exceptional. This metric is crucial because it determines funding costs and therefore profitability. The bank's focus on affluent customers means higher average balances but also more rate-sensitive deposits.

Asset quality remains a standout. Gross NPAs at 1.73% and net NPAs at 0.34% are among the best in the industry. This reflects not just conservative underwriting but also the bank's focus on secured lending (home loans, car loans) and affluent customers who have lower default rates.

The Bull Case

The optimistic view of Kotak Mahindra Bank rests on several pillars:

First, India's structural growth story. With GDP expected to grow at 6-7% annually and financial services growing at 1.5-2x GDP, even maintaining market share would deliver substantial growth. The bank's presence in high-growth segments like wealth management and investment banking positions it well to capture disproportionate value.

Second, the franchise value. The Kotak brand stands for trust and quality in Indian banking. This is not easily replicable and provides pricing power. The bank can charge premium pricing for products and services, maintaining superior margins even in a competitive market.

Third, the digital opportunity. With restrictions lifted, the 811 platform can resume its growth trajectory. Digital acquisition costs are a fraction of physical, and the bank has demonstrated the ability to innovate rapidly. The younger demographic being acquired through digital channels provides a long runway for growth.

Fourth, consolidation opportunities. Indian banking is ripe for consolidation, with several smaller private banks and even some PSU banks potential targets. Under Vaswani's leadership, with his emphasis on scale, a transformative acquisition is possible. The successful integration of ING Vysya provides confidence in execution capabilities.

Fifth, the clean balance sheet. Unlike peers who are still dealing with legacy corporate lending issues, Kotak's balance sheet is clean. This provides flexibility to grow aggressively when opportunities arise without being constrained by past mistakes.

The Bear Case

The pessimistic view highlights several structural challenges:

First, the scale disadvantage. Despite four decades of growth, Kotak remains subscale compared to HDFC Bank and ICICI Bank. In banking, scale provides advantages in technology investments, product development, and negotiating power. The question is whether Kotak can achieve necessary scale organically or whether it needs another transformative acquisition.

Second, technology infrastructure challenges. The RBI restrictions exposed serious deficiencies in IT systems. While these have been addressed, the episode raises questions about whether the bank has the technology DNA to compete in an increasingly digital world. Building robust, scalable technology infrastructure requires massive investments that are easier to amortize over a larger base.

Third, leadership transition risks. While Vaswani brings impressive credentials, he's still new to the institution. The real test will come during the next crisis or when major strategic decisions need to be made. The founder's presence on the board provides continuity but could also create confusion about ultimate authority.

Fourth, regulatory overhang. The history of regulatory challenges suggests a complicated relationship with the RBI. While current issues are resolved, the bank seems to attract regulatory scrutiny. Any future lapses could result in restrictions that impact growth.

Fifth, market saturation in core segments. The affluent banking segment that Kotak has traditionally dominated is becoming increasingly competitive. Every bank is chasing the same high-value customers. Meanwhile, expanding into mass market segments would dilute margins and increase risks.

Technology and Infrastructure Investment Needs

The April 2024 RBI restrictions highlighted a critical weakness—technology infrastructure hadn't kept pace with business growth. Kotak Mahindra Bank's computer systems have been deficient for a while, as found by the RBI's audit for two years. While remediation efforts have addressed immediate concerns, the bank needs massive investments to build world-class technology infrastructure.

The challenge is not just about preventing outages but building capabilities for the future. Real-time payments, AI-based credit decisioning, blockchain for trade finance, and open banking APIs all require sophisticated technology stacks. The bank is competing not just with other banks but with technology companies entering financial services.

Regulatory Relationships and Compliance Costs

The adversarial history with the RBI has implications beyond immediate restrictions. It means the bank operates under greater scrutiny, requiring higher compliance costs. Every new product or initiative likely faces greater regulatory examination. While this ensures robustness, it also slows innovation and increases costs.

The broader regulatory environment is also becoming more complex. Data protection regulations, cybersecurity requirements, and ESG mandates all add to compliance burden. For a bank of Kotak's size, these costs are proportionally higher than for larger competitors who can spread them over a bigger base.

Growth Opportunities

Despite challenges, significant growth opportunities exist:

Wealth management is expected to grow at 15-20% annually as India creates more millionaires. Kotak's strong franchise in this segment positions it well. The partnership with Zurich in general insurance opens new opportunities for cross-selling and product innovation. The SME banking franchise, strengthened through ING Vysya acquisition, has significant room to grow as India's economy formalizes.

Digital banking for the mass market through 811 remains underpenetrated. With less than 20 million customers, there's room to scale to 50-100 million over time. International expansion, while nascent, offers long-term potential. The presence in GIFT City and Dubai signals ambitions beyond domestic banking.

The Verdict

The balanced view suggests Kotak Mahindra Bank is a high-quality institution facing a scale challenge. It has the brand, culture, and financial strength to succeed but needs to achieve significantly greater scale to compete effectively with larger rivals. The path forward likely requires a combination of organic growth through digital channels, selective acquisitions to build scale in specific segments, massive technology investments to build competitive capabilities, careful navigation of regulatory relationships, and most importantly, successful execution of the leadership transition.

The next few years under Vaswani's leadership will be crucial. If the bank can successfully scale while maintaining its quality culture, it could emerge as a true challenger to the duopoly of HDFC Bank and ICICI Bank. If it fails to achieve scale, it risks being relegated to a profitable but ultimately niche player in Indian banking.

XI. Epilogue & "What Would We Do?"

As we reach the conclusion of the Kotak Mahindra Bank story, we're left contemplating a fundamental question: What is the legacy of Uday Kotak, and can the institution he built truly transcend its founder to become India's answer to JP Morgan?

The Uday Kotak Legacy: Institution Builder vs. Entrepreneur

Uday Kotak represents a unique figure in Indian business—an entrepreneur who successfully transformed into an institution builder. "If you go back to the history of successful financial institutions, whether it's a JP Morgan or a Goldman Sachs or Morgan Stanley or a Merrill Lynch, which is now of course part of Bank of America, all these were family names started by individuals and families. And there was enough ability to be creative and at the same time within the framework."

Unlike many first-generation entrepreneurs who struggle to let go, Kotak systematically reduced his ownership, brought in professional management, and ultimately stepped down from executive responsibilities. His philosophy was clear: "I have always believed an institution is more important than an individual, and institutions must go on forever. Individuals may come and go. That is a core philosophy I deeply believe in, and that's what we are really working on."

The legacy is multifaceted. Kotak proved that an Indian entrepreneur without business lineage or political connections could build a world-class financial institution. He demonstrated that patient capital and conservative risk management could create more value than aggressive growth. Most importantly, he showed that Indian institutions could maintain global governance standards while operating in a challenging emerging market environment.