KNR Constructions: The Execution Machine of Indian Infrastructure

I. Introduction & The "Infratech" Alpha

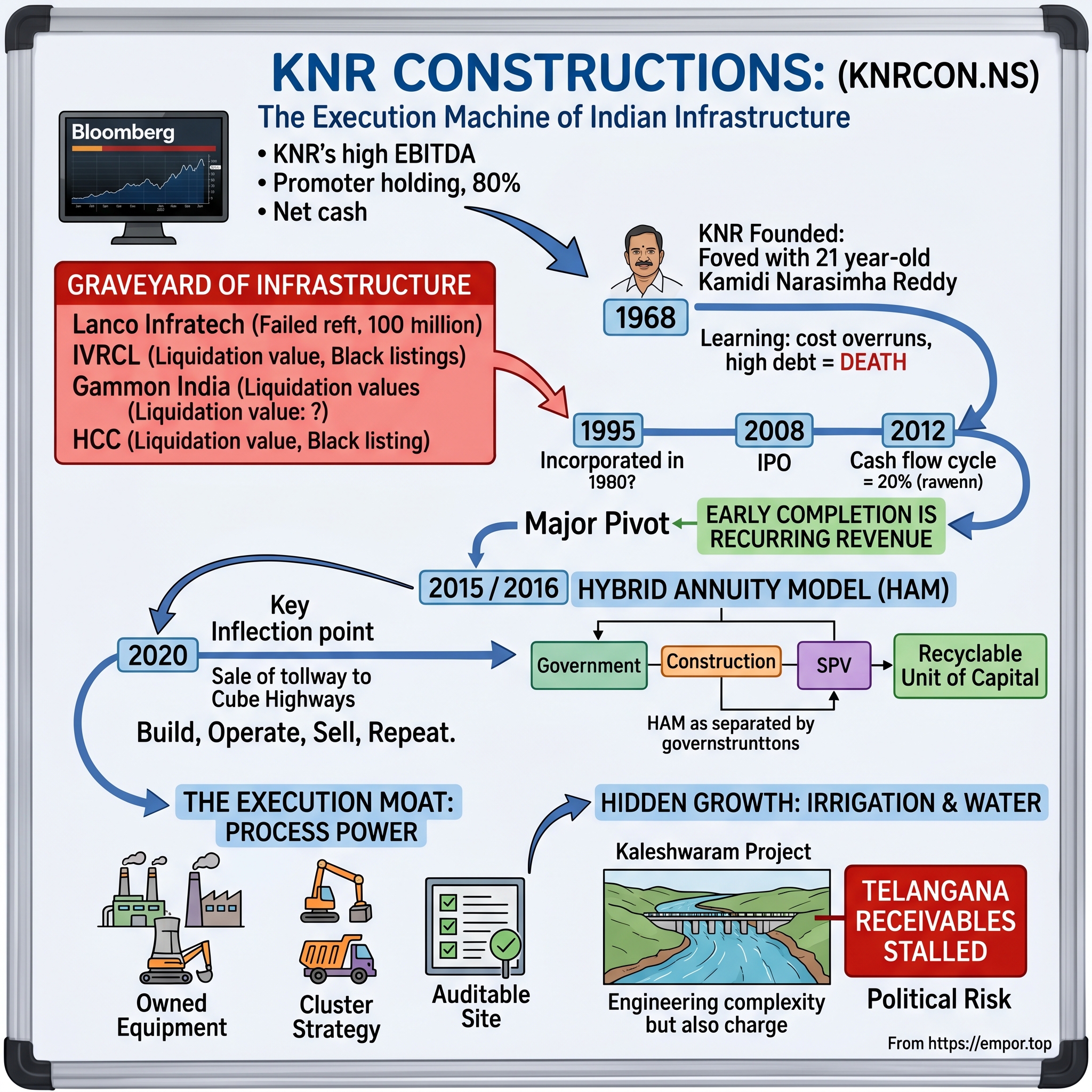

Picture a Bloomberg screen on any given Monday in 2024.

You scroll past the usual suspects — the Nifty 50 heavyweights, the IT majors with their familiar 25% operating margins, the consumer-staples darlings trading at 60 times earnings. Then your eyes catch a peculiar name from the dusty mid-cap construction shelf: केएनआर कंस्ट्रक्शंस लिमिटेड KNR Constructions Limited.

EBITDA margin pushing 24%[^1]. Net cash on the standalone balance sheet1. Promoter holding north of 50%. A thirty-year compounding story buried inside a sector famous for blowing itself up every cycle.

Now, here is the strange part.

Indian infrastructure is supposed to be a graveyard. The 2008–2012 boom produced household names — आईवीआरसीएल IVRCL, लांको Lanco Infratech, गैमन Gammon India, एचसीसी Hindustan Construction Company — that today are either liquidated, in resolution, or trading as penny-stock zombies.

Lanco Infratech alone went into liquidation in 2018 with creditors admitting roughly ₹54,258 crore of claims, a number large enough to make a Wall Street default look quaint2. IVRCL, the company that once won the Hyderabad outer ring road, ended up blacklisted by state water boards for shoddy execution3. The carnage was sector-wide and indiscriminate.

And yet, headquartered in Hyderabad, run by a 78-year-old founder who started life as a sub-contractor in 1968, sits a road builder that has compounded operating margins of more than 20% through that entire carnage, owns its own fleet of yellow steel, and refuses — refuses — to put net debt on its standalone books4. The investing community has slowly started treating it like the polite cousin nobody invited to the wedding, but who quietly bought a duplex in Bandra while everyone else was leveraging up to buy power plants.

That is the puzzle of this episode. Why does the public market afford KNR multiples that look more like a Asian Paints-adjacent compounder than a लार्सन एंड टुब्रो Larsen & Toubro-adjacent EPC vendor? Why has a regional southern roads contractor managed to do what a generation of larger, better-funded peers could not — survive two full infra cycles without a write-down, without a debt restructuring, and without a single quarter of cash-flow negative operations in its core EPC vertical[^6]?

The roadmap of this story runs from a small partnership called M/s K. Narasimha Reddy & Co. doing sub-contract work for larger civil firms in the early 1980s, through a 1997 reorganization into a private limited entity, through a 2008 IPO that almost no one in Mumbai noticed5, to a 2020 sale of a Kerala toll road to Cube Highways that turned the company permanently net-cash and reshaped what investors thought a roads business could look like6. And it ends — for now — with a roughly ₹5,000 crore order book heavily tilted toward Telangana irrigation and Hybrid Annuity Model roads, a balance sheet wrestling with stalled state-government payments, and a stock that the market still cannot decide whether to value as a builder or a quasi-financial asset recycler[^9].

The "Infratech" framing — borrowed from the way sell-side analysts have started bracketing companies like KNR alongside the digital-economy compounders — captures something genuine. KNR's revenue does not grow exponentially the way a SaaS business might. Its margin structure, however, behaves more like a software company in its consistency. Through FY20 to FY24, while the average BSE Capital Goods constituent saw EBITDA margins swing between roughly 9% in the trough quarters and 14% in the peaks, KNR's quarterly EBITDA margins barely moved out of the 20–25% band[^1]9. That stability of margin profile, in an industry whose customer is a monopsony government and whose primary input is volatile commodity-priced material, is the analytical anomaly that has earned KNR its multiple premium.

It is also worth setting one piece of context up front for the international or generalist reader. India's infrastructure boom is not optional. As of 2026, the country has crossed a nominal GDP of roughly $4 ट्रिलियन $4 trillion, but its road density, irrigation coverage, and urban transit infrastructure still trail comparable middle-income peers by a wide margin. The government's पंच साल योजना capital expenditure envelope on physical infrastructure has, since FY16, grown at a CAGR comfortably north of 15%, driven by NHAI's award pipeline, the भारतमाला Bharatmala Pariyojana, and the जल जीवन मिशन Jal Jeevan Mission water infrastructure programme10. A contractor that survives this decade with discipline intact is by definition leveraged to a multi-decade tailwind. Whether that contractor is KNR specifically — versus one of the four or five other listed mid-cap survivors — is the entire investment debate.

This is the story of how one family in Telangana built something that the Indian infrastructure ecosystem was, structurally, not supposed to permit.

II. Roots & The Founder's Ethos

To understand KNR, you have to understand a particular kind of South Indian engineering hustle that does not get written about in business schools.

In 1968 — the year इंदिरा गांधी Indira Gandhi was midway through her first term and the Indian construction industry was almost entirely a public-sector affair dominated by सीपीडब्ल्यूडी CPWD and the state PWDs — a young man named Kamidi Narasimha Reddy, with a Bachelor of Arts from काकतीय विश्वविद्यालय Kakatiya University in Warangal, started taking sub-contract work for larger civil contractors7.

He was 21 years old. He had no engineering degree.

The choice of being a sub-contractor was not romantic. It was the only door open.

In that era, government tenders required pre-qualifications a first-generation entrepreneur from a non-metro family simply could not assemble. So Narasimha Reddy did what hundreds of would-be builders across the Deccan did: he found someone with the license, supplied the labor, the supervision, and the on-site sweat, and learned the craft from the bottom up.

For eleven years he worked this way. He read soil reports he was not invited to read. He watched larger contractors miss deadlines and pay penalties. He developed, by the late 1970s, a near-religious conviction that the single biggest leak in Indian construction was time.

In 1979 he formalized his outfit as a partnership, M/s K. Narasimha Reddy & Co.5, and began bidding on small civil and mechanical contracts in his own name. The 1980s were a slog — flyovers in आंध्र प्रदेश Andhra Pradesh, irrigation channels for कृष्णा Krishna basin schemes, sub-contract packages for the larger national contractors. The firm survived. More importantly, it built a reputation among district engineers in Telangana and Andhra for one thing: KNR finished early. Not on time — early.

By the early 1990s, India was opening up. मनमोहन सिंह Manmohan Singh had delivered his 1991 budget, the राष्ट्रीय राजमार्ग प्राधिकरण National Highways Authority of India (NHAI) had been constituted in 1988 and was beginning to find its institutional feet, and the conversation around private participation in highways was no longer fringe. Narasimha Reddy and his core team decided the partnership had outgrown its skin. On July 11, 1995 they incorporated KNR Constructions Limited; the certificate of commencement followed on August 9, 19955. Two years later, in 1997, the new company absorbed the assets and liabilities of the original partnership firm — a clean, tidy succession that, in hindsight, said a great deal about how the family thought about long-term structure5.

The contrast with peers was already visible. Look at the cohort of southern infrastructure companies that came up in the same window — Lanco started in 1986 as a small civil contractor before pivoting hard into power; IVRCL incorporated in 1987 and chased water and EPC across half the country; गायत्री Gayatri Projects, मधुकोन Madhucon, नवयुग Navayuga, सोमा Soma Enterprises — all swung for diversification. They built roads, then bought thermal plants, then bid for ports, then leveraged the holdco to seed real estate arms. The 2008–2012 यूपीए UPA-era capex boom was, for them, an irresistible buffet.

KNR sat out the buffet. The discipline came directly from Narasimha Reddy. According to the founder's public profile, he had over 55 years of roads and infrastructure experience as of the FY24 annual report, and the bulk of that experience had been spent watching contractors die from three things: cost overruns, leveraged BOT bets, and state-government payment delays7. He had a near-allergic response to all three. The "Southern Fortress" the company built through the 1990s and 2000s — projects clustered tightly across Andhra Pradesh, Telangana, Karnataka, and Tamil Nadu — was less about strategic genius than about a deep mistrust of taking yellow metal across unfamiliar geographies.

The 2006 award of the company's first BOT project in कर्नाटक Karnataka — a road package valued at ₹4,420 million — was the inflection from sub-scale civil contractor to project developer5. It was deliberately small. Other firms in the cohort were already bidding for ₹1,000+ crore BOT-Toll packages with debt-equity ratios that, in retrospect, were structurally suicidal. KNR's first BOT was sized to be losable. The founder's bias, even in moments of obvious opportunity, was always to ask what happens if traffic comes in 20% below the consultant's projection — and to walk away from any bid where that scenario broke the equity.

This temperament had a cultural ancestor that is worth naming. Telugu business families in the post-Independence era — the రెడ్డి Reddy, నాయుడు Naidu, and చౌదరి Chowdary agricultural-and-trading lineages that produced the cohort of South Indian industrialists in pharma, infrastructure, and aquaculture — tended to hold a particular view of debt and family wealth. The bias was toward intergenerational preservation, not single-generation maximization. You can hear it in the way రామోజీ రావు Ramoji Rao ran Margadarsi, in the way నందమూరి తారక రామారావు N. T. Rama Rao's political-business descendants thought about capital, and in the way Narasimha Reddy organized KNR. It is not unique to the Telugu commercial diaspora — Marwari and Gujarati family firms display similar instincts — but it explains a great deal about why KNR survived 2012 when many peers from outside that cultural orbit did not.

The 2008 IPO marked the company's debut as a public entity. The offering was priced at ₹170 per share, raised approximately ₹134 crores, and listed on February 18, 2008 — almost exactly at the cyclical peak before the global financial crisis hammered Indian mid-caps5. The post-listing experience for early KNR shareholders was, by any honest reading, painful. The stock spent the entirety of 2008 and most of 2009 below issue price, recovered tentatively through the 2010–2011 period as infrastructure stocks broadly rallied on UPA capex enthusiasm, and then ground sideways through the 2012–2014 stress cycle. Anyone who bought KNR at the IPO and held through that decade earned moderate but unspectacular returns; the genuinely outsize compounding happened only from FY15 onward, once the HAM regime began to mature and the early-completion bonus economics started showing up consistently in the P&L.

This delayed market recognition is itself revealing. The Indian public markets in 2008–2014 had limited patience for companies that refused to grow their order book aggressively. Analysts wanted top-line headline growth; KNR refused to deliver it at the cost of margin or bid quality. The result was a thin sell-side following, a low free-float liquidity profile, and a multiple compression that, in hindsight, marked one of the better buying opportunities in the Indian mid-cap universe. The lesson, if one wants to draw a portable one, is that disciplined family-run firms in cyclical sectors typically trade at a discount during their first half-cycle as a public entity and rerate sharply once a single multi-cycle compounding cohort of returns becomes undeniable.

Why does this matter for an investor today? Because the culture set in those decades is the asset. The man who refused to bid for projects he could not personally inspect by car is still on the board, still the Managing Director. The next section is about what that culture, applied with industrial discipline, actually produces on the ground.

III. The Execution Moat: "Early Completion" as a Business Strategy

There is a clause in most NHAI EPC contracts that almost nobody outside the industry talks about. It is called the early completion bonus. If a contractor finishes a stretch of national highway meaningfully ahead of the scheduled completion date, NHAI pays a one-time premium — often calculated as a fraction of the toll or annuity value that the road generates in the months saved. The clause exists because the government's bigger pain is not budget overruns; it is the political cost of incomplete roads at ribbon-cutting time. For most contractors, the bonus is a theoretical line item. For KNR, it has been a recurring revenue stream.

The economic logic of the bonus is worth pausing on. A 60-kilometre national highway, once operational, can generate annuity or toll cash flows in the tens of crores annually. Even a six-month early completion saves the government roughly that much in foregone economic productivity, while accelerating the same amount of cash flow to the developer side. NHAI's bonus structure typically captures somewhere in the range of 2–4% of contract value for meaningfully early completion — small as a fraction, but enormous as a contributor to project IRR when the developer's equity in the project may only be 15% of contract value. For a contractor who finishes early on a meaningful share of projects across a decade, this bonus stream compounds into a margin differentiator that simply cannot be matched by a contractor who finishes on time.

Consider the texture of how KNR runs a site.

The standard industry approach to a 60-kilometre EPC road project is to mobilize a single asphalt plant, sometimes two, sequence the work in long linear segments, and pray that monsoon, land acquisition, and utility shifting do not eat the schedule.

KNR's approach, refined over more than 9,100 lane kilometres of executed roads across 12 Indian states[^11], is the opposite. They establish multiple asphalt plants and crusher units along the alignment, attack the road in parallel from several fronts simultaneously, and pre-position equipment for the dirtiest parts of the job before the monsoon hits.

It costs more on day one. It saves a year on day three hundred.

This is Hamilton Helmer's Process Power — the seventh of his 7 Powers — in textbook form. Process Power requires that a company's way of doing things is opaque to outsiders and hysteretic, meaning it can only be acquired through long, patient evolution.

You cannot reverse-engineer KNR's execution by buying its equipment list. You can buy the same Volvo pavers and Caterpillar graders. What you cannot buy is the muscle memory of district managers who have run forty similar projects, the supplier base in नागपुर Nagpur and विशाखापत्तनम Visakhapatnam who answer KNR's call before others, and the workforce that knows where the boss likes the camp set up.

The second pillar is the cluster strategy.

Anyone who has watched a roads contractor try to operate in eight states at once knows the brutal truth — yellow metal is heavy, slow, and expensive to move. A single concrete batching plant requires a low-bed trailer, road permits across state lines, and weeks of redeployment.

KNR's response, from the late 2000s onward, was to bid almost exclusively for projects within tight geographic clusters. Andhra Pradesh and Telangana share a workforce pool. Karnataka projects feed off the same Bangalore supplier base. When KNR moves into Madhya Pradesh or Maharashtra, it does so in clusters of two or three contiguous packages — never one orphan project that would force a sub-scale local establishment8.

This is Helmer's Scale Economies operating at the regional level rather than the national.

The third pillar is ownership of equipment.

In the post-2012 cleanup, the surviving major contractors split into two philosophical camps. One camp, exemplified by some of the listed pure-EPC players, leased aggressively — they wanted asset-light return on capital and were willing to pay a rental premium for it.

The other camp, KNR being the most ideologically pure example, doubled down on owning. KNR's fixed-asset base relative to revenue is meaningfully heavier than the lease-heavy peers, but the company's argument is straightforward: owned equipment means schedule certainty, no last-minute lessor games, and the ability to bid for early-completion bonuses with confidence[^1].

In a sector where execution risk is the single largest determinant of return on capital, the calculus is hard to argue with.

The fourth, less-discussed pillar is what one could call the "auditable site." Anyone who has spent time on Indian construction sites knows that the variance between contractor cultures is enormous — some sites are visibly well-organized, with material laid out in straight rows, machinery in maintained sheds, daily progress boards painted on the supervisor's hut, while other sites look like a riot scene. KNR's sites are, by long-running anecdotal account from sector consultants and rating agency visits, in the first category. CRISIL's rating commentary has repeatedly cited the company's project monitoring and cost control systems as differentiating factors, alongside the financial conservatism that drove the investment-grade rating with stable outlook through cycles that compressed peer ratings[^20]. Process Power, again, is not a single thing — it is the cumulative effect of a thousand small decisions about how a site is organized.

The result of these pillars compounds in margin. While the BSE Capital Goods index averaged operating margins in the low double digits through FY20–FY24, KNR consistently delivered EBITDA margins above 20%, and in FY24 specifically the figure crossed 24%[^1]9. To put that in industrial context: KNR earns construction margins that resemble ब्रिटानिया Britannia Industries earning biscuit margins. It earns these in a regulated, capital-intensive, government-customer business that, in the textbook, should produce mid-single-digit returns at best.

A simple analogy may help the non-industry reader. Imagine a contractor as a chef running a high-end restaurant where the menu is decided by the customer, the ingredient prices are decided by the commodity market, and the diner has the legal right to deduct from the bill for any imperfection. The only variables the chef controls are speed and operational efficiency. Most chefs in that scenario would either go bankrupt or produce mediocre food. KNR's answer has been to staff its kitchen with the same team for two decades, to own its ovens rather than rent them, to source ingredients from a tight network of suppliers who answer the phone first, and to consistently serve dishes ahead of the diner's expected time. The diner — NHAI — has, predictably, become a repeat customer.

For investors, this is the foundation of the entire thesis. Everything that comes later — the capital recycling story, the irrigation pivot, the net-cash balance sheet — is downstream of the simple, boring fact that this company finishes roads earlier than anyone else.

IV. Inflection Point 1: The HAM Revolution & Capital Deployment

In late 2015, the Indian roads sector was a corpse.

The previous private-investment vehicle — बीओटी BOT (Build-Operate-Transfer) — had imploded. Banks were sitting on ₹3 लाख करोड़ ₹3 lakh crore of stressed infrastructure exposure, much of it BOT toll roads where traffic had simply failed to materialize against the wildly optimistic IRRs that bidders had sold to bank consortiums.

The मोदी Modi government's Ministry of Road Transport & Highways needed a new model. What they came up with — formally introduced in January 2016 — was the Hybrid Annuity Model (HAM)10.

For a long-term investor in Indian infrastructure, understanding HAM is not optional. So a brief explanation, in the spirit of Acquired's "let me explain this like you are smart but not in the industry" tradition. Under pure BOT-Toll, the developer fronted the entire capital, borrowed against the future toll stream, and prayed traffic showed up. Under HAM, the government funds 40% of project cost during construction, the developer arranges the remaining 60% as a mix of equity and debt, and the developer is paid back semi-annual annuities over a 15-year operating period along with interest on the outstanding balance, plus inflation-linked O&M payments10. Toll risk sits with the government. Construction risk sits with the developer. It is, effectively, a quasi-fixed-income asset for the developer once the road is operational.

Why was this model so transformative? Because it untangled the three different types of risk that the BOT-Toll regime had bundled together — construction risk, traffic risk, and interest-rate risk — and let each sit with the party best able to bear it. The government, with sovereign borrowing costs and a long-term planning horizon, was the natural bearer of traffic risk. The developer, with execution capability, was the natural bearer of construction risk. The capital markets, through SPV-level debt with explicit semi-annual annuity cash flows, were the natural bearer of interest-rate risk. The result was a financing structure that, for the first time in Indian roads history, could be priced sensibly by lenders and equity investors alike. The pace of HAM awards from FY16 onward — eventually exceeding 100 packages per fiscal year at peak — vindicated the design.

What makes HAM particularly relevant for a company like KNR is that it splits the value chain into three pieces: a construction project (where KNR's margins shine), an SPV-level project debt structure (which sits off the parent balance sheet), and an operational annuity asset (which has clear, predictable cash flows and can be sold to long-duration capital providers — pension funds, infra trusts, sovereign wealth). Each piece can be optimized independently. And critically, the operational asset becomes a recyclable unit of capital.

KNR did not rush in.

While more aggressive peers scooped up early HAM packages in 2016 and 2017 — sometimes at IRRs that, in retrospect, look like charity to NHAI — KNR's bid discipline kept it relatively measured[^9]. The company allowed competitors to set the price floor, then bid for clusters within its execution comfort zone.

By FY19–FY20, KNR had built a portfolio of HAM road assets across Telangana, Tamil Nadu, and Kerala that were either operational or nearing completion.

The discipline is hard to overstate.

Through 2017 and 2018, NHAI was awarding HAM packages at a frantic pace — at peak award months, more than 30 packages would clear in a single quarter — and the bidder pool included both surviving listed contractors and a long tail of private firms hungry to deploy restructured capital.

The IRR compression was visible in the public bid sheets: equity IRRs implied by winning bids were running in the 13–14% zone for projects in tougher geographies, and in some single-bidder situations, even lower.

KNR's response, articulated in successive annual reports and analyst calls, was to walk away from sub-15% IRRs and let competitors absorb the order book bloat[^9]8. The result in the short term was a slower order book growth than peers. The result in the medium term was that, when working capital tightened in 2019–2020, KNR was not the firm having difficult conversations with its banks.

Then came the move that, more than anything else in the last decade, defines what kind of company KNR really is.

In January 2020, the company signed a Share Purchase Agreement with Cube Highways, the I Squared Capital-backed roads platform, to sell 100% of KNR Walayar Tollways Private Limited, the SPV operating the Walayar–Vadakkanchery section of NH-544 in Kerala11. The deal closed in September 20206.

The asset was a BOT-Toll, not a HAM, but it set the template. The headline number was modest in macro terms — the stock jumped 11% on announcement day, suggesting the market priced the transaction comfortably above book12 — but the strategic implication was enormous.

It is worth pausing on who Cube Highways is, because the identity of the buyer matters as much as the identity of the seller.

Cube Highways was created in 2014 as a roads platform sponsored by I Squared Capital, the global infrastructure private equity firm based in Miami, with أبو ظبي للاستثمار Abu Dhabi Investment Authority (ADIA) and the International Finance Corporation as additional investors.

By the time it engaged with KNR, Cube had become India's largest dedicated road asset platform by lane kilometres, focused on aggregating operational toll-road SPVs from EPC contractors and from NHAI's own TOT (Toll-Operate-Transfer) auctions.

The thesis was straightforward: long-duration capital pricing 11–13% IRRs would happily acquire seasoned road assets at valuations attractive to the original developer, who needed to recycle equity to bid for the next round of HAM. The KNR–Cube transaction was a textbook execution of that thesis.

It also marked the moment that the Indian roads sector finally produced a genuine secondary market for operating assets — something the country had lacked for the entire BOT-Toll era.

KNR had just proven that it could build a road, operate it for a few years to seasoning, sell it for an attractive equity IRR, and redeploy the cash either into new HAM bids or back to the parent's net-cash position. This is the "Build-Operate-Sell-Repeat" engine that, when you squint, looks much more like a private-equity infrastructure platform than a traditional EPC contractor. Subsequent transactions across FY22–FY24 — the sales and asset-monetization commentary in management presentations — were variations on the same theme, with management guiding for further HAM SPV monetization through partnership with long-duration capital[^9].

The benchmarking question — did they overpay for the underlying HAM IRRs in the first place? — gets at the heart of capital allocation discipline. Internal management commentary and sell-side reconstructions of project IRRs put KNR's equity IRRs on HAM projects in the mid-to-high teens, comfortably above the 12–14% that the marginal HAM bidder is rumored to clear[^17]. That spread is not magic. It comes from the early-completion bonuses (which compress the construction window and front-load returns), from the lower-than-peer construction cost (the cluster and ownership advantages from the previous section), and from a willingness to walk away from projects where the bid sheet does not work.

The capital recycling story has continued into the most recent fiscal year. The company has, through FY25 management commentary, signaled additional HAM SPV monetization conversations, with timelines guided toward a near-term closing15[^9]. The deeper structural point is that the Indian infrastructure ecosystem in 2026 contains, for the first time, a deep pool of long-duration capital — InvITs (Infrastructure Investment Trusts) governed by SEBI regulations, sovereign-wealth aligned platforms like Cube, and private credit funds — willing to buy operational road assets at reasonable multiples. KNR, as one of the earliest disciplined recyclers, is positioned as a preferred counterparty in that market.

The takeaway for a long-term investor is that KNR turned a procurement reform — HAM — that was designed to bail out lenders into a capital-recycling flywheel for a single contractor. The next question is whether the company that built that flywheel has the leadership to keep it spinning. That brings us to the next generation.

V. Current Management: The Next Generation & Incentives

The founder is still the Managing Director.

That is the first thing to understand about KNR's management structure, and arguably the second and third things too. Kamidi Narasimha Reddy, now in his late seventies, continues as MD and the largest single shareholder of the company, with a personal stake reported around the 30% mark[^18].

Collectively, the promoter group holds slightly above 50%[^9]. By the standards of large-cap Indian corporates that have shed promoter ownership through repeated equity raises, that figure is striking — and by the standards of the highly leveraged infra peers who diluted their way through 2010–2018, it is almost unrecognizable.

But the day-to-day face of the modern KNR is increasingly Kamidi Jalandhar Reddy, the founder's son and the company's Executive Director.

He came to the business by a path that is itself characteristic. He holds a Bachelor's degree in Computer Engineering from बैंगलोर विश्वविद्यालय Bangalore University, started his career inside KNR as a project manager, and was elevated to Executive Director in 1997 — the same year the partnership-to-company reorganization took effect13.

As of the FY24 disclosures he carried close to three decades of experience inside the firm, with direct responsibility for tendering, bidding, and project execution13.

That biographical detail is more than HR trivia.

A son who runs tendering inherits the single most consequential function in an EPC business — the bid sheet. In infrastructure, you do not lose money in execution. You lose money in the moment you decide to bid ₹100 करोड़ ₹100 crore for a project that should have been bid at ₹110 करोड़.

The fact that the family member with the decision rights on bidding came up through site work, not through finance or M&A, is one of the structural reasons KNR has avoided the bid-vanity trap that took out so many competitors during the post-Bharatmala boom.

The incentive architecture compounds this. With the founder family holding roughly half the equity, the marginal benefit of "winning the award" against the marginal cost of "losing money on the contract" is internalized directly into the same balance sheet. There is no agent-principal gap between management and shareholders because they are, to a very real extent, the same entity. The company has publicly resisted bidding for projects where land acquisition is incomplete, where right-of-way is more than 60% encumbered, or where the customer is a state government with a poor payment track record. In a sector where the order book is treated as the supreme KPI, KNR has consistently said it would rather have a smaller order book and collectible cash flows[^9].

This is what the sell-side has, half-affectionately, called "the Auditor's Construction Company." KNR's annual reports read like accountant prose. There is no glossy diversification narrative, no "becoming a logistics and clean-energy and data-centre player" buzzword section. There is a roads vertical, an irrigation vertical, an asset-monetization update, a balance sheet that is obsessively reconciled, and a CRISIL rating that reflects the conservatism — investment-grade with stable outlook, year after year, through cycles that ate the credit of larger peers[^20].

The auditor analogy holds even at the operational reporting level. The Q4 FY24 investor presentation, for instance, is one of the most numbers-dense documents in the Indian mid-cap universe — bid-pipeline tables, SPV-level execution status, equipment fleet ageing, package-wise revenue contribution[^11]. Compare it to the glossy presentations of some EPC peers that emphasize award announcements and order book milestones while burying execution detail, and the cultural difference is visible on every page. Investors who read the full presentation, rather than just the headline slides, are rewarded with a fidelity of disclosure that is genuinely unusual for the sector.

Compensation and capital allocation discipline reinforce each other. Director compensation at KNR has historically been modest by comparable mid-cap standards, and the family draws the bulk of its economic reward from dividends and equity appreciation rather than salary or stock options. There is no employee stock option program of the kind that has, in some peer firms, created the kind of dilution that quietly erodes long-term per-share value. The buy-side analyst's worst nightmare in family-run Indian businesses — related-party transactions used to siphon value from minority shareholders — has not, on any public reading of the company's audited related-party disclosures, been a material concern at KNR[^1][^20].

There is, of course, the obvious question that follows from a founder-led, founder-owned, family-managed company in its third decade. What happens when the 78-year-old founder steps back? The mitigant is structural — the son is already running execution and bidding, the board has independent directors who chair audit and risk, and the systems are well-documented enough that institutional memory does not sit in a single person's head. But honest investors should not pretend the key-man risk is zero. It is the single most material qualitative overhang on the company. Family-business successions in India have a mixed record — for every बजाज Bajaj or मुरुगप्पा Murugappa where multi-generational stewardship has worked, there is a बिड़ला Birla group disagreement or a रेड्डी Reddy Labs boardroom dispute that has destroyed shareholder value during the transition. The fact that the successor has been running execution since 1997 is the strongest possible mitigant, but it is not, by itself, immunity.

The next section, however, makes clear why this management has been worth holding through any such transition. Because while the market was busy looking at KNR's roads order book, something quieter — and arguably more interesting — was happening on the irrigation side.

VI. Inflection Point 2: The "Hidden" Growth — Irrigation & Water

If you flew over northern Telangana in 2018, you would have seen a strange thing — perhaps the most ambitious civil engineering project India had attempted in a generation.

The कलेश्वरम Kaleshwaram Lift Irrigation Project was lifting water from the गोदावरी Godavari River against gravity through a chain of pumping stations, tunnels, and reservoirs that, in scale, dwarfed anything the post-1947 Indian state had built. The price tag would eventually balloon past ₹1 लाख करोड़ ₹1 lakh crore.

The political stakes for then–Chief Minister के. चंद्रशेखर राव K. Chandrashekar Rao were existential. And among the contractors mobilized to build pieces of it was KNR.

To grasp the technical complexity of Kaleshwaram, consider that the project lifts water through a series of pump houses against a cumulative head of more than 600 metres, across one of the highest concentrations of pumping infrastructure ever assembled in a single irrigation project globally.

The pumps installed at the deepest underground pumping station — at Ramadugu — were among the largest single-stage vertical pumps in the world at the time of commissioning. Building this required not just civil engineering but precision electromechanical integration, deep-shaft excavation through Deccan basalt, and water-management hydraulics that few Indian contractors had ever attempted at this scale.

The contractors who were pre-qualified to bid for Kaleshwaram packages were a narrow set, and the contractors who actually executed without major schedule slippage were narrower still. KNR was on both lists.

This pivot — from a pure roads-and-highways player to a serious irrigation and water management contractor — happened quietly.

Through FY20–FY24, the share of irrigation in the order book climbed from a single-digit afterthought to a meaningful pillar. By the March 2025 balance sheet date, irrigation projects constituted ₹2,490.7 crore of an approximately ₹5,051.8 crore order book — almost a 50:50 split with roads when measured at that specific cut-off[^9].

The longer-term mix has roads at roughly 70–75% of the order book and irrigation at the balance; March 2025 was a moment where major road orders had been executed faster than they had been replenished, distorting the snapshot upward in irrigation share[^1][^9].

The strategic logic for the irrigation pivot is multi-layered. First, technical complexity. Lift irrigation involves heavy mechanical, electrical, and civil scope all in one package — pumping stations require precision concrete and structural steel; tunnels through Deccan trap basalt require specialized boring; barrages require deep foundation expertise. The technical pre-qualifications to bid for these packages are brutal, and most of the listed mid-cap EPC names cannot meet them. This narrows the competitive field — which is exactly what a contractor obsessed with margin should want.

Second, margin profile. While the company does not publish vertical-level EBITDA, sell-side reconstructions and management commentary suggest irrigation has run at higher margins than highways through the cycle, primarily because of the lower bidder count and the technical premium[^17]. Third, geographic concentration. KNR's deepest relationships are with the Telangana and Andhra Pradesh state governments. Irrigation, unlike highways, is a state subject. The customer set sits in capitals where KNR has been delivering for decades.

There is, however, a sharp and material risk inside this story that has played out in the last 24 months — and any honest investor view must engage with it head on. The same Telangana state that awarded the irrigation work has, since the change of government in late 2023, slowed payments dramatically. Reports through 2025 placed KNR's outstanding receivables from the Telangana government — across Kaleshwaram Packages 3 and 4 — at roughly ₹1,350 crore, split between ₹758 crore of certified receivables and ₹720 crore of unbilled work14. Collections on those specific packages had been effectively stalled since March 2023 on one package and March 2024 on the other, with KNR continuing to execute work out of pocket to remain contractually compliant14. The consequence is visible in the consolidated debt line, which moved from ₹1,202 crore at March 2025 to roughly ₹2,121 crore by September 2025 — an increase driven entirely by working capital absorption against stalled state-government dues15.

The political backdrop matters here. Kaleshwaram had been the signature project of the previous तेलंगाना राष्ट्र समिति BRS government under K. Chandrashekar Rao, and the new कांग्रेस Congress government that took power in December 2023 ordered judicial and technical reviews of the project even as it continued to be physically operational. For contractors mid-execution, this kind of political churn translates almost directly into a payment freeze, regardless of contractual obligation. The standard contractor response in this scenario — slowing or stopping execution — would have triggered penalty clauses and reputational damage. KNR's response was to keep executing, absorbing the working capital cost as a cost of preserving the franchise. The decision is defensible in long-term franchise-preservation terms; the short-term P&L impact is undeniable15.

This is the underbelly of the irrigation thesis, and it tells you something important about the sector. State-government counterparties carry political risk that no contractor, however operationally excellent, can fully hedge. The mitigants here are partial — the standalone parent still operates with effectively zero net debt, the debt is parked at SPV and project levels, and the receivables are not impaired (they are stuck, not lost) — but the working capital absorption is real, and it is the reason the stock spent much of 2025 in a frustrating sideways range15.

Worth noting as a counterweight to the irrigation drama is the continued roads order book accumulation through early 2026. The company announced two material HAM awards in close succession — a ₹2,163.07 crore four-lane elevated corridor along the East Coast Road in Tamil Nadu in February 2026, and a ₹1,734 crore HAM project for four-laning of the NH-167 from Gudebellur to Mahabubnagar in Telangana in March 202614. Together they restore meaningful order book visibility and demonstrate that, even amid the Telangana payment drama, the company's relationship with NHAI and its bidding discipline remain intact. The Tamil Nadu award in particular is meaningful because it geographically diversifies the order book somewhat further from the Telangana concentration — a structural positive for the medium-term risk profile.

For long-term investors, this is the single most important operational line to track. Irrigation gives KNR margin and competitive differentiation. It also gives KNR a customer concentration that, when politics turn, can compress cash flow for multiple quarters. The capital recycling engine that worked so beautifully on the roads side has not yet been tested in the same way for irrigation, and arguably cannot be — irrigation projects are EPC-only, with no operating annuity to monetize. The next section pulls the threads together into a strategic framework.

VII. Porter's 5 Forces & Hamilton's 7 Powers Analysis

So we have a company that builds roads early, that pivoted into irrigation for margin, that recycles HAM assets for cash, and that refuses to put debt on its parent balance sheet.

The question for an investor is: which of these are durable structural advantages, and which are simply the residue of a great management team that may or may not persist?

The two best frameworks for cutting through that question are Michael Porter's Five Forces and Hamilton Helmer's 7 Powers. Run KNR through both and the picture sharpens considerably.

Start with the 7 Powers, because that is where KNR is most differentiated.

Process Power is the strongest. The "KNR Way" of execution — multiple plant deployment, owned equipment fleet, pre-monsoon front-loading, cluster project density — is not codifiable in a manual. It exists in the heads and hands of a workforce that has been together for two decades, and in the supplier and sub-contractor relationships across South India that other contractors cannot simply buy. The early-completion bonus stream is the financial signature of this power[^1].

Cornered Resource, while weaker than Process Power, is real. KNR's relationship with NHAI — built across more than 9,100 lane kilometres of execution[^11] — gives it a technical pre-qualification footprint that few mid-cap contractors can match. The same is true on the irrigation side with the Telangana state water resources department. These pre-qualifications are not legally exclusive, but they materially compress the competitive bidder set for the most complex packages.

Scale Economies operate at the regional, not the national, level. Within Telangana, Andhra Pradesh, Karnataka, and Tamil Nadu, KNR has unit costs that competitors moving in from outside the region cannot match — because of the cluster strategy and the local supplier base. Outside that footprint, the company is at parity or worse with regional incumbents. This is why management has been deliberate about expansion into Madhya Pradesh and Maharashtra in clusters rather than one-off bids.

The other 7 Powers — Switching Costs, Network Economies, Branding, Counter-Positioning — are largely absent. Roads are commoditized at handover. There are no switching costs for NHAI. There is no network. And there is no contrarian business model that incumbent peers cannot copy if they choose to.

Now overlay Porter's 5 Forces.

Threat of New Entrants is genuinely high in the abstract — building roads requires equipment and labor, and India has both in abundance. But the effective threat at KNR's scale and project complexity is moderated by pre-qualification thresholds, by working capital requirements that crush sub-scale entrants, and by the brutal Darwinian lesson of 2012 that scared off a generation of would-be empire builders. The marginal new entrant in HAM today is more likely a refugee from another stressed peer than a greenfield startup.

Bargaining Power of Buyers is the single most important force in this analysis, and it is extreme.

NHAI and the state governments are monopsony customers. They write the contract, they certify the work, they release the payment. The contractor has, in theory, almost no leverage.

KNR's answer to this — its only answer — has been "Execution Alpha." If you deliver early, with quality, and from a fortress balance sheet, the customer has reason to give you the benefit of the doubt on disputes and to invite you back to the next bid. This is not a moat. It is a daily renegotiation of a moat.

The Telangana receivables saga of 2024–2025 shows exactly how thin the protection is when political cycles change14.

Bargaining Power of Suppliers is moderate. Steel and cement are commoditized; bitumen pricing has been volatile but pass-through clauses in modern HAM contracts mitigate this substantially.

Threat of Substitutes is low — there is no substitute for a road or an irrigation channel. The threat is more about who builds it (private capex versus government-funded) and that pendulum has, under the current NDA government, swung hard toward government-financed HAM and EPC for the better part of a decade10.

Industry Rivalry is intense among the surviving listed mid-caps — दिलीप बिल्डकॉन Dilip Buildcon, पीएनसी Infratech, एचजी इन्फ्रा HG Infra, अशोका बिल्डकॉन Ashoka Buildcon, जीआर इन्फ्राप्रोजेक्ट्स G R Infraprojects, and केएनआर KNR — but the rivalry is more about bid discipline than about price wars, because each of these players has, post-2012, internalized the lesson that an aggressive bid is a guaranteed loss.

A useful mental experiment: imagine the marginal new mid-cap contractor trying to displace KNR on a Telangana road bid. They would need (a) a comparable owned equipment fleet, requiring ₹500+ crore of capex; (b) a comparable supplier ecosystem in the Hyderabad-Vijayawada corridor, which takes years of relationship-building; (c) project managers with the demonstrated track record needed to clear NHAI pre-qualification thresholds; and (d) a balance sheet clean enough to underwrite the working capital cycle. Each of these takes years to build, and the marginal new entrant who tries to compress the timeline will almost certainly underprice the bid and bleed cash on execution. This is what economists call a "sunk-cost moat" — not unbreachable, but expensive enough to deter the marginal challenger.

The "myth vs reality" check is also worth doing explicitly. The market narrative on KNR oscillates between two extreme framings. The bull framing is "Indian roads compounder with infrastructure-trust optionality." The bear framing, especially after Telangana headlines, is "regional state-government EPC with growing working capital risk." The reality is somewhere structurally in between, and it has been since the company went public in 2008. The execution moat is real and durable. The customer concentration is also real, and not declining. The capital recycling engine is functional but lumpy. Anyone valuing KNR purely on one of the two extreme narratives is going to be regularly wrong-footed by quarterly reality.

The synthesis is uncomfortable for a true believer. KNR has real but narrow powers — execution-led process advantages in a sector defined by extreme customer bargaining power. The defensibility is genuine, but it must be re-earned every project. That is why the playbook the company has built around capital recycling matters so much.

VIII. The Playbook: Lessons for Builders

The KNR playbook can be summarized in three lines that, if a junior contractor wrote them on a wall, would represent a meaningful upgrade in survival probability through the next infrastructure cycle.

Line one: Build, Operate, Sell, Repeat.

The capital recycling philosophy is what separates KNR from peers who, after the BOT collapse, swung between two equally bad poles — either bidding for nothing and watching the order book wither, or bidding for everything and watching the balance sheet bloat.

KNR's third path was to bid selectively for HAM and BOT assets where the IRR worked, build them to specification, operate them through enough seasoning to attract long-duration buyers, and then sell. The Cube Highways transaction in 2020 was the proof-of-concept116.

Management has signaled additional monetization through FY26, conditional on market timing and buyer availability[^9]. This is the playbook of a Macquarie-style asset manager wrapped inside an EPC contractor.

Line two: Stay in the lane.

The temptation for any successful South Indian builder in the 2005–2012 window was to diversify into power, real estate, or ports. The cautionary tales — लांको Lanco into power, गायत्री Gayatri into power, गैमन Gammon into ports — are well documented.

KNR did none of it. There is no real estate arm. There is no power arm. There is no ports arm.

The only adjacent vertical is irrigation, which sits squarely within civil engineering competency and uses largely overlapping equipment and crews. This kind of focus is what veteran fund manager रॉबर्ट विल्सन Robert Wilson would have called the discipline of doing one thing extremely well. It is also, not coincidentally, what the public market is willing to pay a margin premium for.

Line three: In a high-interest-rate country, no debt is competitive advantage.

The Indian repo rate has spent the better part of the post-2014 era at 5.5–6.5%, with corporate borrowing rates for mid-cap infrastructure names running comfortably north of 10%10. For a contractor running on roughly 10–11% EBITDA margins post-tax, a single turn of leverage destroys nearly half the equity return.

KNR's near-religious refusal to put net debt on the standalone parent is not a vanity. It is a structural advantage that, in periods of liquidity stress (2013, 2018, 2020), turned every working capital squeeze into an opportunity to win contracts from over-leveraged competitors who could not bid14.

A fourth, implicit line in the playbook deserves explicit mention: trust the long arc. KNR's management has, over the past two decades, repeatedly chosen short-term order book restraint over long-term franchise dilution. They sat out the 2007–2012 BOT euphoria. They sat out the early 2017 HAM gold rush. They have, by all public indication, declined to participate in opportunistic foreign infrastructure bids that some peers have chased. This pattern of restraint is, paradoxically, what creates the optionality to act decisively when genuine opportunities appear — the 2020 Cube Highways monetization being the clearest example. Patient capital allocation is hard to copy because it requires watching peers grow faster than you for years at a time. Most management teams, accountable to quarterly P&L, cannot stomach that. KNR's family-owned structure removes the agency cost that punishes patience.

The combination of these lines produces something rare. KNR's return on capital employed has run consistently in the high teens to low twenties through the cycle — a number that would be respectable for a branded consumer company and is, frankly, extraordinary for a roads contractor9. The price the market pays for this is, naturally, a multiple premium versus the peer set. The question for an investor is whether that premium is sustainable as the next leg of the story unfolds.

IX. Analysis: The Bull & Bear Case

The bull case for KNR rests on three pillars that, individually, look attractive and, together, look like a thesis.

First, the Indian government's infrastructure capex cycle remains in its multi-year upswing. The गति शक्ति Gati Shakti master plan, the भारतमाला Bharatmala Pariyojana, and the steady drumbeat of केंद्रीय बजट Union Budget allocations to roads and irrigation have, since 2019, anchored a sustained order pipeline for the qualified mid-cap contractor cohort10. Even with some volatility in awarding pace, the secular direction is unambiguous.

Second, the irrigation vertical — assuming Telangana receivables eventually clear — opens a genuinely new TAM for KNR at higher technical complexity and likely higher margin than roads. The market has not yet learned to value KNR as a water management business. When it does, the multiple rerating could be significant[^9][^17].

Third, the capital recycling engine, once peers replicate it, will face more competition for buyer attention — but KNR has the first-mover relationship with long-duration capital (Cube Highways, the various infrastructure investment trusts, sovereign wealth platforms looking at India) and a track record that derisks the next monetization116. The standalone parent already runs with effectively zero net debt; further monetization simply compounds optionality.

A reasonable bull also looks at peer comparisons.

Stacked against Dilip Buildcon (which has spent the better part of the last cycle deleveraging and recovering from execution challenges), PNC Infratech (a closer peer in disciplined bid behavior), G R Infraprojects (another quality operator with a strong North India footprint), and HG Infra Engineering (the fastest-growing of the cohort but with a less developed monetization track), KNR has the longest cycle-tested franchise in the South, the highest promoter ownership, and arguably the cleanest balance sheet relative to size[^1].

None of these peers has, as of mid-2025, monetized HAM assets at the depth that KNR has demonstrated.

A deeper peer-level comparison adds nuance.

दिलीप बिल्डकॉन Dilip Buildcon, headquartered in Bhopal, is the largest pure roads contractor in India by order book at various points in the cycle, but its working capital intensity has historically been meaningfully higher than KNR's, and its expansion into mining and metro projects diluted the focus that made it a darling in 2017.

पीएनसी इन्फ्राटेक PNC Infratech, based in Agra, runs a disciplined bid book and a comparable family-owned structure, with strong North Indian execution; the company has been increasingly competing for the same HAM packages as KNR in the central states, though its margin profile typically tracks 200–300 basis points below KNR's.

जीआर इन्फ्राप्रोजेक्ट्स G R Infraprojects, the Udaipur-headquartered firm that went public in 2021, has perhaps the best North-Indian geographic franchise and the cleanest capital structure of the cohort outside KNR.

एचजी इन्फ्रा HG Infra Engineering is the youngest and most growth-oriented; its margins have been the most cyclically variable.

The collective takeaway is that the listed mid-cap Indian roads space is, in 2026, a club of roughly five disciplined survivors — each with regional anchor strengths, all increasingly competing for the same national HAM and EPC packages.

The implication for KNR is twofold. First, the regional moat in South India is real but not permanent — peers from outside the region are increasingly bidding for Telangana and Karnataka projects, and KNR will need to defend its home turf even as it expands geographically. Second, the capital recycling track record gives KNR an edge in winning future HAM bids where lenders and equity partners ask the question, "Can this developer actually monetize the asset?" Five-year-ago, that question had no good answer for any Indian contractor. Today, it has at least one credible answer — and KNR is one of the names on the short list.

The bear case is, however, neither short nor frivolous.

Geographic concentration remains the single biggest structural risk. Telangana and Andhra Pradesh together account for the majority of KNR's order book and an even larger share of its irrigation backlog. The change in Telangana government in late 2023 has, as discussed, produced a ₹1,350 crore working capital absorption that the company is still working through. A similar political shift in Andhra Pradesh, or a sustained slowdown in Telangana awards, would meaningfully compress order book replenishment14.

Regulatory shifts in HAM are a second material concern. The HAM model is not a constitutional right. Any future ministry that wanted to swing back toward pure BOT-Toll, or further toward pure EPC, would change the economics of the entire monetization engine that KNR has built. Recent commentary out of NHAI suggesting a shift toward more EPC at the expense of HAM in some corridors has spooked sector multiples periodically10.

Key-man risk deserves explicit acknowledgment. The founder is 78. The succession is in place and tested, but is, as in any family-led firm, untested in the specific moment when the patriarch steps fully back.

Cyclical earnings volatility is visible even in the most recent quarters. Q4 FY25 saw revenue down 35% year-on-year and PAT down 62%, reflecting a combination of irrigation execution slowdown, working capital constraint, and lumpiness in order book completion timing16. Investors who view KNR as a smooth compounder will be tested by quarters like that.

There is also a second-layer diligence overlay worth noting. CRISIL's most recent rating action retained the investment-grade rating but with commentary on the working capital absorption from state-government receivables[^20]. The auditor's report on the FY24 accounts did not raise emphasis-of-matter or going-concern flags, but the increase in trade receivables and contract assets as a percentage of revenue from FY23 to FY24 — a single-digit-percentage move that nonetheless represented several hundred crores in absolute cash terms — was noted in financial commentary9. This is not a red flag of the kind that preceded the IVRCL-era collapses; it is, however, the kind of working-capital build that investors should monitor against the FY25 and FY26 collections.

Equally worth flagging: the company has, through public disclosure, no material 13F-style concentration of foreign institutional ownership in the way that some Indian large-caps do. The shareholder register is dominated by the promoter family, followed by Indian mutual funds and a tail of FPIs holding modest stakes. This shareholder structure is generally favorable to long-term holders — it means there is no single 5%+ institutional holder whose redemption could create forced-selling pressure — but it also means that the stock can trade with relatively thin liquidity during periods of stress, amplifying near-term volatility.

Porter and Helmer in summary: the powers are real but narrow, the buyer concentration is extreme, the rivalry is disciplined but persistent, and the entry barriers — while higher than the headlines suggest — are not insurmountable for a well-capitalized refugee from a stressed peer. The investment case is not "KNR has an unassailable moat." It is "KNR has the best operational and capital allocation culture in a structurally challenging sector, and that culture has compounded value for two decades."

For long-term investors, three KPIs matter more than any other to track this story going forward. First, the standalone net debt position, because the moment that turns persistently negative — meaning, the parent takes on debt that does not look working-capital-temporary — the entire capital allocation thesis is in question1. Second, the EBITDA margin on the EPC business, because that is the single most direct measure of whether the execution moat is intact[^1]9. Third, the Telangana receivables balance, because that single line item will, more than any other, determine the cash flow trajectory of FY26 and FY2714. None of these are calculations — they are line items in the quarterly disclosure that an investor can read and judge.

X. Epilogue

There is a tempting analogy that gets made about KNR by sell-side analysts who want to convey the company's character to a generalist audience. It goes: "KNR is the Toyota of Indian construction." The phrasing is meant to evoke the quiet, methodical, process-obsessed discipline that Toyota brought to automotive manufacturing in the 1970s — the Kaizen culture, the supplier integration, the relentless focus on operational excellence over financial engineering.

The analogy is imperfect — Toyota had branding, scale economies, and network effects that KNR will never have in roads. But it captures something true about the temperamental difference between this company and its competitors. While the sector spent the post-2008 decade swinging between euphoria and despair, KNR was running a multi-decade compounding experiment in which the variable being maximized was not order book or revenue, but the survival probability of the franchise itself.

That experiment is now in its fourth decade. The founder who started as a 21-year-old sub-contractor in 1968 is still on the board. The son who came up through site execution is running the day-to-day. The balance sheet at the parent level remains structurally net cash. The execution culture continues to deliver early completion bonuses on roads and complex packages on irrigation. The capital recycling engine has been demonstrated and is, as of 2026, being run for a second iteration.

The Indian infrastructure landscape itself is at a fascinating juncture. The country has spent the last decade building the kind of physical backbone — highways, ports, irrigation networks, urban metros — that countries like Japan and Korea built in their high-growth phases of the 1960s and 1970s. The next decade will be about whether that backbone is operated, maintained, and renewed efficiently enough to support the GDP growth ambitions of a country that, as of 2026, has crossed $4 ट्रिलियन $4 trillion in nominal output. The mid-cap contractor cohort that survives this transition — KNR among them — will, almost by definition, be a beneficiary of compounding government capex.

But the deeper lesson of the KNR story, for the long-term investor, is not about which contractor wins the next NHAI bid. It is about what discipline looks like in a sector that has historically rewarded the opposite of discipline. It is about how a family that started in a Hyderabad workshop in 1979 built a company that, in 2026, is still owned, still run, and still — improbably — finishing roads ahead of schedule. It is, in short, about how to build something that lasts in an industry that does not usually let things last.

Whether the market will continue to pay a premium for that discipline through the next cycle is, of course, the unanswerable question that every long-term investor in KNR has to make peace with. The historical answer is yes. The forward-looking answer, as always, sits in the order book, the receivables ledger, and the quiet, methodical decisions made every quarter inside an unassuming office in Hyderabad by a 78-year-old founder and his son.

The legacy of K. Narasimha Reddy, when the time comes to write it, will not be a single landmark project. There is no बांद्रा-वर्ली Bandra-Worli Sea Link with his name on it, no signature dam or bridge that became a tourist photograph. The legacy is, instead, an institutional one: the demonstration that a contractor in the Indian infrastructure sector — a sector that has, structurally, destroyed more capital than almost any other in the post-liberalization economy — could be built and run with the temperament of a long-only family endowment rather than the temperament of a casino. That demonstration, if it persists through the next generation and through the next major political cycle, will outlast any individual project the company has ever built.

The broader Indian infrastructure narrative is at a moment of genuine inflection. The Gati Shakti programme continues to drive integrated planning across road, rail, port, and waterway projects. The Jal Jeevan Mission is reshaping the rural water infrastructure landscape. The राष्ट्रीय अवसंरचना पाइपलाइन National Infrastructure Pipeline envisages a multi-trillion-rupee envelope of public and private capex through the rest of the decade. The contractors who survive this decade in a position to underwrite this opportunity will not be the loudest or the most diversified. They will be the ones who, like KNR, built their balance sheet discipline a cycle earlier than the moment required it.

In the end, the most accurate description of KNR may not be "the Toyota of Indian construction." It may simply be "the company that did the math, refused to forget the math, and let everyone else find out the hard way." For long-term fundamental investors trying to find compounding stories in inefficient public markets, that is a description worth paying attention to — not because it guarantees the future, but because, over thirty years, it has consistently described the past.

References

References

-

KNR Constructions Investor Relations — KNR Constructions ↩↩↩

-

Lanco Infratech and lessons from a failed group resolution of troubled debt — Business Standard, 2020-10-23 ↩

-

Kolkata flyover collapse: IVRCL has faced allegations of negligence in the past too — Business Standard, 2016-04-01 ↩

-

The Execution Machine: A Deep Dive into KNR — Moneycontrol, 2023-11-15 ↩↩

-

KNR Constructions IPO Date, Price, GMP, Review, Details — Chittorgarh ↩↩↩↩↩↩

-

Cube Highways Acquires KNR Walayar Tollways — BusinessWire, 2020-09-29 ↩↩↩↩

-

KNR Constructions: The Quiet Performer in the Infra Space — Business Standard, 2022-05-18 ↩↩

-

KNR Constructions 2023-24 Annual Report Analysis — Equitymaster ↩↩↩↩↩

-

NHAI's Hybrid Annuity Model (HAM) Explained — Ministry of Road Transport & Highways ↩↩↩↩↩↩↩

-

Cube Highways to Acquire KNR Walayar Tollways — BusinessWire, 2020-01-09 ↩↩↩

-

KNR Constructions up 11% as it sells entire stake in KNR Walayar Tollways — Business Standard, 2020-01-10 ↩

-

KNR Constructions update — Substack research note by Srikanth Thangellamudi, 2025 ↩↩↩↩↩↩

-

KNR Constructions Ltd Q4FY25 Result Update — Axis Direct, 2025-06-02 ↩↩↩↩

-

KNR Constructions slides as Q4 PAT slumps 61% YoY to Rs 248 cr — Business Standard, 2025-05-30 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube