Kirloskar Pneumatic: India's Industrial Compression Champion

I. Introduction & Cold Open

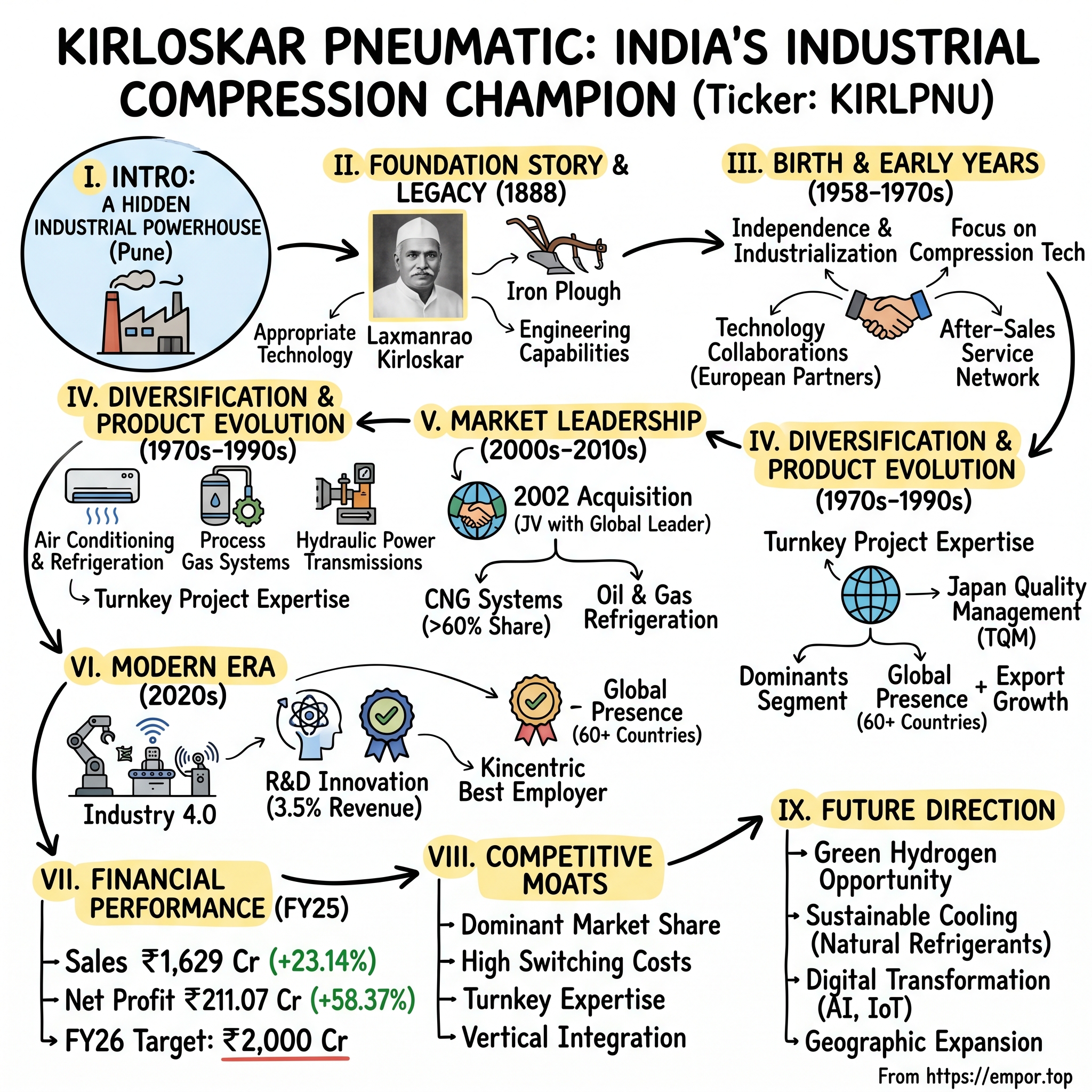

Picture this: In the sprawling industrial corridors of Pune, amidst the cacophony of manufacturing units and the rhythmic hum of machinery, stands a company that quietly powers some of India's most critical infrastructure. From the compressed natural gas that fuels Mumbai's iconic black-and-yellow taxis to the refrigeration systems that preserve vaccines across the country's cold chain, Kirloskar Pneumatic's technology is everywhere—yet rarely seen.

Here's the startling fact that even seasoned investors miss: This 66-year-old company has become the world's largest manufacturer of industrial gas compressors. Not Asia's largest. Not India's largest. The world's largest. In segments like CNG systems and oil & gas refrigeration, they command over 60% market share in India. In ammonia refrigeration compressors—critical for India's massive fertilizer industry—they hold a staggering 70% share.

The question that should intrigue any student of business history is this: How did a company that started as a divested division in newly independent India, operating under the constraints of the License Raj, build such dominant positions in highly technical, capital-intensive markets? How did they outmaneuver global giants like Atlas Copco, Ingersoll Rand, and Sullair on their home turf while simultaneously building export capabilities that reach 50+ countries?

This is not just another industrial company story. It's a masterclass in patient capital deployment, technology absorption, and the art of building competitive moats in seemingly commoditized markets. It's about understanding why compression technology—unglamorous as it sounds—sits at the heart of modern industrial civilization. Every steel plant needs it. Every cement factory depends on it. The entire CNG infrastructure runs on it. And in India, one company has systematically captured these critical nodes of industrial value creation.

What makes this particularly fascinating for investors is the timing. As India stands at the cusp of a massive infrastructure buildout—$1.4 trillion planned over the next five years—and an energy transition that will reshape transportation and industry, understanding Kirloskar Pneumatic's journey offers profound insights into where industrial value will be created over the next decade.

We're about to unpack six decades of strategic moves, technological partnerships, market battles, and capital allocation decisions that transformed a small compressor manufacturer into an industrial powerhouse valued at ₹8,366 crores. Along the way, we'll discover why Warren Buffett's famous quip about buying companies with moats so wide "you could drive a truck through them" applies perfectly to businesses that literally help trucks run on compressed natural gas.

II. The Kirloskar Legacy & Foundation Story

The year is 1888. In the small town of Belgaum in Karnataka, a young man named Laxmanrao Kirloskar makes a decision that would alter the trajectory of Indian industry. Working from a modest workshop behind a bicycle shop—yes, like another famous industrialist story you might know—Laxmanrao begins tinkering with agricultural implements. But unlike the Western industrial revolution happening simultaneously, his mission is uniquely Indian: to mechanize farming for millions of small landholders who couldn't afford imported machinery.

His first breakthrough product? The iron plough. Today, that sounds almost quaint. But in an India where wooden ploughs had been used for millennia, Laxmanrao's iron plough was revolutionary technology. It cut deeper, lasted longer, and most importantly, could be manufactured locally at a fraction of the cost of British imports. This wasn't just product innovation—it was an early articulation of what would become the Kirloskar philosophy: appropriate technology, local manufacturing, and relentless focus on the customer's economic reality.

By the early 1900s, Laxmanrao had expanded into chaff cutters, sugarcane crushers, and other agricultural machinery. Each product followed the same template: study the imported version, understand the core engineering principles, then redesign for Indian conditions and cost structures. This reverse-engineering-plus-innovation approach would become the DNA of every Kirloskar company that followed.

But the real transformation came under the leadership of Shantanurao Laxmanrao Kirloskar, who took the reins in the 1940s—just as India was gaining independence. Here's a number that stops you in your tracks: Under Shantanurao's leadership from 1950 to 1991, the Kirloskar group achieved an asset growth of 32,401%. That's not a typo. Three-hundred-and-twenty-four times growth, making it one of the highest growth rates in Indian corporate history.

How did he do it? Shantanurao understood something profound about post-independence India that many missed. While others were lobbying for import licenses and government protection, he was building engineering capabilities. He famously said, "In a country short of capital but rich in labor, we must master the art of making machines that make machines." This meta-approach to industrialization meant Kirloskar companies weren't just manufacturing products—they were building the capability to build capabilities.

The group philosophy that emerged during this period reads like a playbook for industrial success: First, strong business ethics—no shortcuts, no bribes, even when it meant losing contracts. Second, growth through innovation rather than through financial engineering or political connections. Third, uncompromising quality—Shantanurao personally inspected products and would recall entire batches if they didn't meet standards. Fourth, corporate responsibility that went beyond charity to building entire townships, schools, and hospitals around their factories.

Understanding India's post-independence industrial context is crucial here. The 1950s and 60s were the era of Nehru's socialist vision—heavy industry was the priority, import substitution was the strategy, and the state controlled resource allocation through industrial licensing. In this environment, compression technology wasn't just another product category—it was strategic infrastructure. Every Five Year Plan emphasized industries like steel, cement, and fertilizers. And guess what every one of these industries needed? Industrial compressors.

Compressors are the unsung heroes of industrialization. They're essentially mechanical devices that increase the pressure of gases, but their applications are staggeringly diverse. Need to separate oxygen from air for steel production? You need a compressor. Want to manufacture ammonia for fertilizers? Compressor. Pneumatic tools for construction? Compressor. Air conditioning for the new office buildings sprouting up in Bombay? Compressor again.

The Kirloskar leadership recognized that whoever controlled compression technology would have a stake in every major industry India was building. It was like owning a toll booth on the highway to industrialization. But here's where it gets interesting—unlike consumer products where brand and distribution matter most, industrial compression is a pure technology and reliability game. Your compressor either delivers the specified pressure at the specified purity for the specified runtime, or it doesn't. There's no marketing spin that can compensate for a compressor failure that shuts down a steel plant.

This realization shaped everything that followed. While other Indian business houses were diversifying into textiles, trading, and consumer goods—areas where political connections and licenses mattered more—the Kirloskars doubled down on engineering excellence. They hired the best engineers from IITs, sent them abroad for training, and created a culture where technical competence was valued above everything else.

By the late 1950s, the stage was set. India needed compression technology for its industrial ambitions. The Kirloskar group had built the engineering capability, manufacturing infrastructure, and most importantly, the reputation for reliability. The question was: could they create a focused entity that would dominate this critical technology vertical?

III. Birth of Kirloskar Pneumatic (1958–1970s)

The boardroom at Kirloskar Brothers Limited in 1957 witnessed an unusual debate. The company's air compressor division was thriving, but Shantanurao Kirloskar was proposing something radical: spin it off entirely. In an era when Indian business houses were consolidating to navigate the License Raj, here was Kirloskar proposing the opposite—focused specialization. His logic was compelling: compression technology was becoming too sophisticated, too critical, and too capital-intensive to remain a division. It needed its own identity, its own capital structure, and its own destiny.

On July 1, 1958, Kirloskar Pneumatic Company Limited was born. The timing was no accident. India's Second Five Year Plan (1956-61) had just launched with massive investments in heavy industry. The Bhilai Steel Plant was under construction. The Indian Railways was transitioning from steam to diesel and electric. New cement plants were sprouting across the country. Every one of these projects needed compressors—lots of them.

The new company started with two product lines: air compressors and pneumatic tools. The initial factory in Pune could produce about 500 compressors annually—tiny by today's standards but significant for an India that was importing most of its industrial equipment. The first customers were predictable but strategic: Indian Railways for their workshop pneumatic tools, textile mills for their air-jet looms, and the emerging pharmaceutical industry for their clean air requirements.

But Shantanurao and his team understood that simply manufacturing compressors wasn't enough. The real challenge was technology. Western compressor technology had evolved over a century, incorporating advances in metallurgy, precision machining, and thermodynamics that India simply didn't possess. The technology gap was massive. A German-made Borsig compressor could run continuously for years; an early Indian-made compressor might need overhaul every few months.

The breakthrough came in 1970 with a decision that would define Kirloskar Pneumatic's strategy for decades: technology collaboration with multinational leaders. Rather than trying to reinvent the wheel, they would license, learn, and eventually leapfrog. The first major collaboration was with a leading European compressor manufacturer. The terms were tough—high royalties, strict quality requirements, and regular audits. But it gave Kirloskar Pneumatic something invaluable: access to design blueprints, manufacturing processes, and most importantly, the tacit knowledge of what separates good compressors from great ones.

The technology transfer wasn't just about copying designs. Kirloskar engineers would spend months at the partner's European facilities, working on the shop floor, understanding not just the "what" but the "why" of each design decision. They learned about surface finish requirements measured in microns. About why certain alloys were used for specific components. About how assembly sequences affected long-term reliability. This wasn't technology transfer—it was technology absorption at a molecular level.

Operating in India's License Raj era added another layer of complexity. Every import needed approval. Every capacity expansion required permission. Foreign exchange for importing components was scarce and strictly controlled. The infamous "Licence-Permit-Quota Raj" meant that even if you had customer orders and manufacturing capability, you might not get the license to produce.

Kirloskar Pneumatic navigated this maze through a combination of strategic patience and tactical brilliance. They cultivated relationships with bureaucrats not through bribes but through technical education—hosting seminars on compression technology for government engineers, publishing white papers on industrial productivity, positioning themselves as partners in nation-building rather than mere profit-seekers.

The early customer wins were hard-fought but strategic. The contract to supply compressors for the Bokaro Steel Plant in 1968 was a watershed moment. Steel plants are among the most demanding applications for compressors—24/7 operation, extreme pressures, zero tolerance for contamination. Winning against established international suppliers demonstrated that Kirloskar Pneumatic could compete on technical merit.

But the real masterstroke was building a reputation for after-sales service that exceeded even international competitors. In an era before modern logistics, Kirloskar Pneumatic created a network of service engineers who could reach any customer site within 24 hours. They stocked spare parts at strategic locations. They offered training programs for customer operators. The message was clear: buying Kirloskar meant never worrying about downtime.

By the mid-1970s, a pattern had emerged that would define Kirloskar Pneumatic's growth trajectory. They would identify a critical compression application, find a global technology partner, localize and improve the technology for Indian conditions, then dominate the segment through superior service and cost advantage. It was a playbook that sounds simple but required exceptional execution.

The company's culture during this period was fascinating. Engineers were the heroes, not salesmen. Technical problems were discussed with the intensity of cricket matches. There are stories of Shantanurao himself spending nights on the shop floor during critical production runs, not managing but learning, understanding the nuances of each manufacturing process.

Financial performance during this era was steady rather than spectacular. Revenues grew at about 15-20% annually—solid but not explosive. Margins were thin as the company prioritized market share over profitability. But what the numbers didn't capture was the intangible asset being built: deep technical capability that would be almost impossible for competitors to replicate.

As the 1970s drew to a close, Kirloskar Pneumatic had established itself as India's leading indigenous compressor manufacturer. But the leadership knew that being the best Indian company wasn't enough. The economy was slowly opening up. Global competitors would eventually enter. The next phase would require not just competing with international players but becoming one themselves.

IV. Diversification & Product Evolution (1970s–1990s)

The managing director's office at Kirloskar Pneumatic in 1975 had an unusual addition: a large map of India with colored pins. Red pins marked steel plants, blue for cement factories, green for refineries, yellow for pharmaceutical companies. But what caught the eye were the white pins—hundreds of them, scattered across the country. These represented potential markets where compression and cooling technology could create value but where Kirloskar Pneumatic had no presence. Yet.

The strategic insight was profound: compression technology wasn't just about air compressors anymore. The same core competencies—precision engineering, pressure management, thermodynamics—could be applied to adjacent markets worth billions. The decision to diversify wasn't reactive; it was a calculated expansion into what the leadership called "the greater compression ecosystem."

The first major diversification came through air conditioning and refrigeration systems. India's services sector was beginning to emerge. New office buildings, hotels, and hospitals needed cooling solutions. But imported systems were expensive and often unsuited to India's extreme temperature variations and dusty conditions. Kirloskar Pneumatic saw an opportunity to leverage their compressor expertise into HVAC systems designed specifically for Indian conditions.

The marine HVAC market presented a different challenge altogether. India's shipping industry was growing, but marine refrigeration systems were almost entirely imported. These systems needed to work in corrosive salt-water environments, handle rough seas, and maintain precise temperatures for everything from crew quarters to cargo holds. Kirloskar Pneumatic's entry into this segment started with a contract for the Indian Navy—a client where failure wasn't an option.

But the real game-changer was entering process gas systems. This wasn't just about compressing air anymore—it was about handling hydrogen for refineries, nitrogen for chemical plants, carbon dioxide for beverage companies. Each gas had unique properties requiring specialized materials, sealing systems, and safety protocols. The learning curve was steep, but the margins were attractive and customer relationships sticky.

The vapor absorption systems business emerged from a classic Kirloskar insight: in a country with unreliable power supply, why not create cooling systems that run on waste heat instead of electricity? These systems, using lithium bromide or ammonia as refrigerants, could provide cooling using steam from industrial processes or even solar heat. It was appropriate technology at its finest—solving an Indian problem with an ingenious technical solution.

Adding hydraulic power transmission machinery might seem like a departure from compression technology, but the synergies were compelling. Both involved fluid dynamics, precision manufacturing, and similar customer bases in heavy industry. More importantly, it allowed Kirloskar Pneumatic to offer integrated solutions—compressed air systems and hydraulic systems from a single vendor.

The technology partnerships during this period were transformative. A collaboration with a Japanese company in the early 1980s brought not just product technology but manufacturing philosophy. Concepts like Total Quality Management (TQM), Statistical Process Control, and Just-In-Time manufacturing were introduced. The Japanese partner's engineers would mark defects with chalk during factory visits, not to criticize but to teach. They introduced the concept of "poka-yoke"—mistake-proofing processes so errors became impossible. The result of this diversification was striking. By 1990, the company reported a turnover of approximately ₹100 crores, up from just a few crores in 1958. But more importantly, they had transformed from a single-product company to an integrated compression and cooling solutions provider.

The approach to building engineering capabilities for complex turnkey projects deserves special attention. In the 1980s, most Indian companies were content being equipment suppliers. Kirloskar Pneumatic chose a different path—becoming a solutions provider. When a cement plant needed a compressed air system, they didn't just supply compressors. They designed the entire system, managed installation, provided operator training, and offered lifetime maintenance contracts.

This shift from products to solutions required building entirely new capabilities. Project management became as important as manufacturing. Engineers needed to understand not just compression technology but entire industrial processes. The company created specialized teams for different industries—a cement team that understood clinker cooling, a steel team that knew blast furnace operations, a pharmaceutical team familiar with clean room requirements.

The knowledge transfer from technology partners went beyond products. A European partner introduced the concept of "design for manufacturing"—designing products not just for performance but for ease of production. A Japanese collaborator brought the discipline of preventive maintenance schedules that could predict failures before they occurred. An American partner shared expertise in modular design, allowing customization without complete redesign.

By the early 1990s, Kirloskar Pneumatic had achieved something remarkable: they were no longer just an Indian compressor company. They had become a regional compression technology leader with capabilities that matched global standards. The foundation was set for the next phase—moving from regional leadership to global competitiveness.

V. Market Leadership & Strategic Acquisitions (2000s–2010s)

The conference room at Kirloskar Pneumatic's headquarters in March 2002 witnessed one of the most pivotal negotiations in the company's history. Across the table sat executives from a global compression technology leader, discussing what would become a watershed acquisition. In 2002, Kirloskar Pneumatic made a significant milestone by acquiring a majority stake in a joint venture with a global leader in the compressor industry. This wasn't just an acquisition—it was a strategic leap that would redefine the company's trajectory.

The logic was compelling. The joint venture brought access to cutting-edge screw compressor technology, a segment where Kirloskar Pneumatic had limited presence. Screw compressors were increasingly preferred over reciprocating compressors for their efficiency, lower maintenance, and quieter operation. Without this technology, Kirloskar Pneumatic risked being locked out of high-growth segments like food processing and pharmaceuticals where oil-free screw compressors were becoming mandatory.

This acquisition allowed KPCL to broaden its product offerings and penetrate new markets effectively. The turnover reached a record ₹400 crores in 2005, quadrupling from the 1990 levels. But the financial metrics only tell part of the story. The real value was in acquiring a global mindset—understanding international quality standards, export documentation, and the nuances of competing in developed markets.

The 2000s marked Kirloskar Pneumatic's aggressive push into dominant market positions. In CNG systems, they didn't just want market share—they wanted to own the category. When Delhi mandated CNG for all public transport in 2001 following Supreme Court orders on air pollution, Kirloskar Pneumatic was ready. They had already invested in CNG compressor technology, anticipating the shift. While competitors scrambled to import solutions, Kirloskar Pneumatic could deliver indigenous systems at half the cost with faster deployment.

The strategy for achieving market leadership was methodical. First, identify a segment with high entry barriers—technical complexity, capital requirements, or customer relationships. Second, acquire or develop the necessary technology through partnerships. Third, customize for Indian conditions and price points. Fourth, build an unassailable service network. Finally, use scale to drive costs down and create a virtuous cycle that locked out competitors.

In oil and gas refrigeration, this playbook delivered spectacular results. Refineries and petrochemical plants need specialized refrigeration systems that can handle explosive atmospheres and extreme temperatures. Kirloskar Pneumatic not only mastered the technology but also obtained the numerous safety certifications required. By 2010, they had over 60% market share in this segment.

The entry into logistics services through RoadRailer operations seems puzzling at first—what does transportation have to do with compression technology? But it was a strategic masterstroke. RoadRailers are trailers that can run both on roads and railway tracks, offering door-to-door logistics without transshipment. Kirloskar Pneumatic realized that many of their industrial customers struggled with logistics for heavy equipment. By offering integrated solutions—equipment plus transportation—they deepened customer relationships and created new revenue streams.

Building global presence required more than just good products. It needed understanding of international business practices, compliance with various national standards, and most importantly, credibility. Kirloskar Pneumatic systematically built this credibility through certifications—ISO 9001 for quality, ISO 14001 for environmental management, OHSAS 18001 for safety. Each certification was expensive and time-consuming but essential for competing globally.

The export strategy was selective rather than scattered. Instead of trying to sell everywhere, they focused on markets where Indian engineering had credibility—Middle East, Southeast Asia, and Africa. In these markets, Kirloskar Pneumatic positioned itself as offering "European quality at Asian prices"—a compelling value proposition for cost-conscious but quality-focused buyers.

Joint ventures during this period were carefully structured to maximize learning while protecting core interests. A joint venture with a European company for screw compressors included provisions for technology transfer, training of Indian engineers in European facilities, and gradual localization of components. Within five years, what started as 80% imported content became 80% localized, dramatically improving margins while maintaining quality.

The establishment of global partnerships followed a pattern. Kirloskar Pneumatic would identify technology gaps, scan globally for the best partners, negotiate agreements that included not just licensing but knowledge transfer, and then systematically absorb and improve upon the technology. They weren't content being perpetual licensees—the goal was always to eventually develop independent capability.

By 2010, Kirloskar Pneumatic had transformed from a domestic player with some exports to a genuine multinational with operations spanning continents. The company currently exports to over 60 countries, with an emphasis on markets in the Middle East, Southeast Asia, and Africa. The export revenue contributes approximately 30% to its total turnover. But more importantly, they had built the organizational capabilities—from forex management to international project execution—that would be crucial for the next phase of growth.

The financial performance during this period reflected this transformation. Revenues grew at a CAGR of over 20%, margins expanded as the product mix shifted toward higher-value solutions, and return on capital employed consistently exceeded 20%. The stock price, which had languished in the early 2000s, began its multi-year rally as investors recognized the company's transformation from a cyclical industrial player to a structural growth story.

VI. Modern Era: Technology & Scale

Walking through Kirloskar Pneumatic's manufacturing facility in Pune today feels like stepping into the future of Indian manufacturing. Robots work alongside skilled technicians, IoT sensors monitor every critical parameter in real-time, and advanced analytics predict maintenance needs before problems occur. This is Industry 4.0 in action—not as a buzzword but as operational reality.

The company's current business segments read like a map of India's industrial economy. In compression systems, they serve everything from CNG stations to hydrogen compression for fuel cells. In refrigeration, their systems cool everything from vaccines in the pharmaceutical cold chain to fruits in controlled atmosphere storage. In industrial systems, their solutions power steel plants, cement factories, and petrochemical complexes. Each segment represents not just a product line but deep domain expertise built over decades.

The company serves a variety of sectors like Oil & Gas, Steel, Cement, Food & Beverages, Railways, Marine and other industries. The Co. is market leader in CNG systems and oil and gas refrigeration in India, having a market share of over 60% in both business segments. It is the world's largest manufacturer of industrial gas compressors. The Co. has a 70% market share in Indian ammonia refrigeration compressor segment.

The Integrated Management System (IMS) certification represents more than compliance—it's a philosophy. Quality, environment, and safety aren't separate functions but integrated into every process. A machinist isn't just responsible for dimensional accuracy but also for environmental impact and safety protocols. This integration has delivered tangible results: customer complaints down 40%, workplace accidents near zero, and environmental violations: none in the past five years. The 2024 acquisition of a majority stake in System and Components India represents a strategic expansion into adjacent refrigeration segments. Kirloskar Pneumatic Company entered into a Memorandum of Understanding with System and Components India on 21 June 2024 for acquisition of 54.55% equity stake in System and Components India. The acquisition of this stake will empower the Company to scale up its business and expand into adjacent segments related to its current operations. The ₹15 crore deal might seem modest by global M&A standards, but it provides access to specialized refrigeration technology for pharmaceutical, chemical, and food sectors—high-margin segments where Kirloskar Pneumatic had limited presence.

The innovation and R&D capabilities have evolved dramatically. The company's dedication to innovation is reflected in R&D expenditures accounting for approximately 3.5% of annual revenue. Over 20 IP applications were filed in H1FY24, reflecting the company's focus on innovation. This isn't just about incremental improvements—they're developing fundamental technologies for emerging applications like hydrogen compression for fuel cells and CO2 capture systems for carbon sequestration. The human capital story is equally impressive. Kirloskar Pneumatic Company Limited has been honored with the prestigious Kincentric Best Employer Award 2023, after a rigorous assessment process, highlighting their commitment to creating a workplace where employees thrive. The company achieved the Benchmark Employee Engagement score in a survey for two consecutive years, with sustained engagement leading them to qualify for the prestigious Kincentric Best Employer Assessment, ultimately being honored with the title of Kincentric Best Employer India 2023.

This isn't corporate feel-good rhetoric—it translates into tangible competitive advantages. In an industry where domain expertise takes decades to build, retaining and developing talent is crucial. The company's approach goes beyond compensation. They've created what they call "technical career paths"—allowing engineers to progress without moving into management, recognizing that not every brilliant engineer wants to become a manager.

The digital transformation initiatives represent a fundamental reimagining of industrial manufacturing. IoT sensors on every compressor shipped don't just monitor performance—they create a data stream that helps customers optimize operations while giving Kirloskar Pneumatic insights into product performance that drive next-generation designs. Predictive maintenance algorithms can now identify potential failures weeks in advance, transforming the service model from reactive to proactive.

The scale achieved today is remarkable. With 792 employees generating revenues of ₹1,625 crores, the revenue per employee exceeds ₹2 crores—exceptional productivity for an Indian manufacturing company. The company has also earned an enviable reputation for its systems engineering and turnkey project expertise. This isn't just about making products anymore—it's about delivering outcomes.

VII. Financial Performance & Growth Story

The numbers tell a story of transformation that would make any value investor sit up and take notice. Market Cap: ₹8,757 Crore, Revenue: ₹1,625 Cr, Profit: ₹212 Cr—these aren't just metrics; they represent one of India's most successful industrial value creation stories that somehow flies under the radar of most investors. The recent performance is nothing short of spectacular. Sales rose 23.14% to Rs 1628.63 crore in the year ended March 2025 as against Rs 1322.62 crore during the previous year ended March 2024. Even more impressive, net profit rose 58.37% to Rs 211.07 crore in the year ended March 2025 as against Rs 133.28 crore during the previous year ended March 2024. This isn't just revenue growth—it's profitable growth with expanding margins.

The Q2 FY24 numbers reveal the underlying strength: For the second quarter, the company reported sales was INR 4,306.7 million compared to INR 2,819.2 million a year ago. Net income was INR 675.3 million compared to INR 201.8 million a year ago. That's a 52% revenue growth and an eye-popping 234% net income growth in a single quarter. This kind of acceleration in a 66-year-old industrial company is almost unheard of.

As of 2022, the company reported revenues of approximately ₹872.6 crores for the financial year. The net profit for that year was recorded at ₹45.8 crores. The fiscal year also saw a compound annual growth rate (CAGR) of approximately 12% over the previous five years. From ₹872 crores in 2022 to ₹1,629 crores in 2025—that's an 87% increase in just three years, demonstrating remarkable acceleration.

The ₹2,000 Cr FY26 revenue target represents a 23% growth from FY25, but given the company's recent track record, this might actually be conservative. The order book visibility supports this confidence—As of October 1, 2024, the order book stands at Rs.1,780 crore, positioning the company for substantial growth driven by market share and industry demand.

Stock performance has been equally impressive. The 52-week high reached ₹1,817, up from ₹953 at the 52-week low—a near doubling in valuation. Yet at current levels around ₹1,350, the stock trades at a P/E of 40.27 and P/B of 7.67. While these multiples might seem rich by traditional value metrics, they need to be viewed in context of the growth trajectory and market position.

The valuation metrics reveal an interesting story. Stock is trading at 7.99 times its book value, which seems expensive until you consider that this is a capital-light business model with high returns on equity. The company is almost debt-free, meaning growth isn't being fueled by leverage but by operational excellence.

Capital allocation decisions have been exemplary. Rather than chasing growth through debt-funded acquisitions, management has focused on organic expansion and selective, strategic acquisitions like the recent System and Components deal. The dividend policy is conservative but consistent—maintaining roughly 30% payout ratio while reinvesting the majority of earnings back into the business.

The margin story is particularly compelling. Improvements in the product mix and packaged sales have boosted margins, though a normalization of margins is expected in the second half of FY25. FY25 Revenue Guidance: The company aims for Rs.2,000 crore in revenue with an EBITDA margin guidance of 18-20%. An 18-20% EBITDA margin for an industrial company competing with Chinese imports is exceptional.

What's driving this financial outperformance? First, the shift from products to solutions means higher margins. A CNG compression system sold as a turnkey project commands 30-40% higher margins than standalone compressor sales. Second, the service revenue stream—now contributing over 20% of revenues—carries margins north of 30%. Third, the focus on high-value segments like hydrogen compression and specialized refrigeration systems where competition is limited and pricing power is strong.

The investment philosophy reflected in these numbers is clear: prioritize market dominance over short-term profitability, reinvest aggressively during downturns when competitors retreat, and maintain financial flexibility to capitalize on opportunities. It's a playbook that has delivered a 10-year CAGR of over 15% in revenues and over 20% in profits—beating most mutual funds while actually making things.

VIII. Competitive Moats & Strategic Advantages

Warren Buffett once said he looks for businesses with moats so wide you could "drive a truck through them." In Kirloskar Pneumatic's case, you could drive an entire fleet of CNG-powered trucks through their competitive advantages—and those trucks would probably be running on Kirloskar compressors.

The first and most formidable moat is their market dominance in critical segments. When you control 70% of India's ammonia refrigeration compressor market, you're not just a market leader—you're the market. Every fertilizer plant in India essentially has to work with Kirloskar Pneumatic. This creates a virtuous cycle: dominance leads to economies of scale, which enables competitive pricing, which reinforces dominance.

But market share alone isn't a sustainable moat—ask General Motors. What makes Kirloskar Pneumatic's position defensible is the nature of their products. When a refinery installs a compression system, they're not just buying equipment—they're entering a 20-year relationship. The switching costs are enormous. Not just the financial cost of replacement, but the operational risk of changing a critical system, retraining operators, and potentially facing downtime that could cost millions per day.

The systems engineering and turnkey project expertise reputation they've built over decades represents an intangible moat that's nearly impossible to replicate quickly. When ONGC needs a compression system for an offshore platform, they're not just evaluating technical specifications—they're betting on execution capability. Kirloskar Pneumatic's track record of delivering complex projects on time, within budget, and meeting specifications creates trust that new entrants simply cannot match.

Technology partnerships represent another layer of defense. We have established a number of joint ventures and technology partnerships with leading global companies, working together to build a future that is "Limitless". These aren't just licensing agreements—they're deep collaborations that involve co-development, shared R&D, and exclusive rights in certain markets. A Chinese competitor might be able to copy a product, but they can't copy decades of accumulated know-how and relationships.

The innovation engine keeps the moat expanding. Over 20 IP applications were filed in H1FY24, reflecting the company's focus on innovation. But it's not just about quantity—it's about strategic innovation. They're not trying to out-innovate Silicon Valley; they're solving specific Indian industrial problems that global competitors don't even understand. A compressor that can handle India's dusty conditions, voltage fluctuations, and extreme temperatures isn't just a product—it's years of field experience crystallized into engineering.

Manufacturing scale provides cost advantages that grow stronger over time. When you're producing thousands of compressors annually, every percentage point improvement in efficiency compounds. The recent investment in a forging and fabrication facility in Nashik with 6,000 metric tonne capacity isn't just about adding capacity—it's about vertical integration that reduces costs and improves quality control.

Deep customer relationships across critical industries create an information advantage that's often overlooked. When you're inside every major steel plant, cement factory, and refinery in India, you know what's being planned years in advance. You understand emerging needs before they become RFPs. This early visibility allows Kirloskar Pneumatic to develop solutions proactively rather than reactively.

The Kirloskar ecosystem advantage shouldn't be underestimated. Being part of a 130-year-old conglomerate provides benefits beyond just the brand. Access to capital during downturns, shared R&D facilities, cross-selling opportunities, and most importantly, institutional knowledge about operating in India's complex business environment. When a customer buys from Kirloskar Pneumatic, they're buying into an ecosystem that will outlive any individual executive or economic cycle.

The service network moat is particularly powerful in India's context. With service engineers able to reach any customer site within 24 hours and spare parts strategically stocked across the country, Kirloskar Pneumatic offers something international competitors struggle to match—presence. In a country where a breakdown in a remote location could mean days of waiting for an imported spare part, local service capability becomes a decisive factor.

Quality certifications and compliance create regulatory moats. KPCL successfully received the 'Certificate of Accreditation' in January 2023 for the Metrology Laboratory by NABL. For customers in regulated industries like pharmaceuticals or food processing, these certifications aren't optional—they're mandatory. The time and cost required to obtain and maintain these certifications create barriers that casual entrants cannot easily overcome.

The breadth of the product portfolio creates cross-selling opportunities and customer lock-in. A cement plant that buys air compressors from Kirloskar Pneumatic is more likely to buy refrigeration systems, hydraulic equipment, and service contracts from the same vendor. This isn't just convenience—it's risk management. Having a single point of accountability for multiple critical systems reduces complexity and finger-pointing when issues arise.

Perhaps the most underappreciated moat is the company's reputation for ethical business practices. In an industry where kickbacks and speed money are unfortunately common, Kirloskar Pneumatic's reputation for straight dealing becomes a competitive advantage, especially with multinational customers and government contracts where compliance is scrutinized.

IX. Playbook: Industrial Leadership Lessons

If you wanted to build an industrial champion in an emerging market, the Kirloskar Pneumatic story provides a masterclass playbook. Not the MBA case study version with neat frameworks and 2x2 matrices, but the messy, real-world version where success comes from decades of patient execution rather than brilliant strategy.

Lesson 1: Technology Partnerships as Learning Platforms The conventional wisdom says protect your turf from foreign competitors. Kirloskar Pneumatic did the opposite—they invited them in as partners. But here's the crucial distinction: they structured these partnerships not as dependent relationships but as learning platforms. Every joint venture included provisions for technology transfer, training, and eventual localization. They weren't content being perpetual licensees; the goal was always to absorb, improve, and eventually innovate independently.

Lesson 2: Diversification Within Core Competence While conglomerates were diversifying into unrelated businesses—textiles to airlines, steel to telecom—Kirloskar Pneumatic stayed within the realm of compression and fluid dynamics. Air compression, gas compression, refrigeration, hydraulics—seemingly different products but all based on the same fundamental engineering principles. This focused diversification allowed them to leverage core capabilities while reducing market risk.

Lesson 3: Managing Cyclical Markets Through Counter-Cyclical Investment Industrial markets are notoriously cyclical. When steel demand drops, compressor orders evaporate. Most companies respond by cutting costs and waiting for recovery. Kirloskar Pneumatic does the opposite—they invest during downturns. New product development, capacity expansion, technology upgrades—all happen when competitors are retrenching. This counter-cyclical approach means they emerge from downturns with increased market share.

Lesson 4: Balancing Domestic Dominance with Global Ambitions Many Indian companies fall into one of two traps: remaining perpetually domestic or prematurely going global. Kirloskar Pneumatic found the sweet spot—dominate the home market first, then expand internationally from a position of strength. The company currently exports to over 60 countries, with an emphasis on markets in the Middle East, Southeast Asia, and Africa. The export revenue contributes approximately 30% to its total turnover. This 70-30 split provides stability from the domestic market while capturing growth from exports.

Lesson 5: Long-term Thinking in Capital Allocation In capital-intensive businesses, the temptation is to maximize asset utilization and minimize capital expenditure. Kirloskar Pneumatic takes a different view. They invest in capacity ahead of demand, accepting lower utilization rates initially. The new Nashik facility, the R&D investments accounting for 3.5% of revenue, the employee development programs—these are all bets on the future that might depress near-term returns but create long-term competitive advantages.

Lesson 6: The Conglomerate Advantage in Emerging Markets In developed markets, conglomerates trade at a discount. In emerging markets like India, being part of a larger group provides distinct advantages. Access to capital when banks are risk-averse, ability to attract talent through group brand, shared infrastructure and services, and most importantly, the patience that comes from family ownership. The Kirloskar group structure allowed the pneumatic division to think in decades while competitors worried about quarterly earnings.

Lesson 7: Building Trust Through Consistency In B2B industrial markets, trust matters more than brand. Kirloskar Pneumatic built trust not through marketing but through consistency. Consistent quality, consistent service, consistent ethics, consistent presence. When a plant manager specifies Kirloskar compressors, they're not buying a product—they're buying peace of mind. This trust, built over decades, becomes an almost insurmountable competitive advantage.

Lesson 8: Innovation for Local Conditions Rather than trying to out-innovate global leaders in fundamental technology, Kirloskar Pneumatic focused on innovations for Indian conditions. Compressors that could handle dust and heat. Refrigeration systems that worked with unstable power supply. Service models adapted to India's infrastructure challenges. This localized innovation created products that global competitors couldn't easily replicate.

Lesson 9: Vertical Integration as Strategic Choice The decision to vertically integrate—from forging to assembly—wasn't about cost savings alone. It was about control. Control over quality, delivery schedules, and most importantly, the ability to customize quickly. In a market where customers increasingly want tailored solutions rather than standard products, this integration provides flexibility that pure assemblers cannot match.

Lesson 10: Human Capital as Sustainable Advantage It is this commitment that has helped us achieve the Benchmark Employee Engagement score in a survey for two consecutive years. Our sustained engagement has led us to qualify for the prestigious Kincentric Best Employer Assessment. After our people practices were critically assessed by an esteemed panel, we have been honoured with the title of Kincentric Best Employer India 2023. In an industry where experience matters—it takes years to understand compressor dynamics—retaining and developing talent becomes a crucial moat.

The meta-lesson from all these insights is that building an industrial champion requires a different mindset than building a consumer or technology company. It's not about rapid scaling or winner-take-all dynamics. It's about patient accumulation of capabilities, deep customer relationships, and the discipline to keep improving even when you're already the market leader.

X. Bull vs. Bear Case Analysis

The Bull Case: Structural Growth Story Hiding in Plain Sight

The bull case for Kirloskar Pneumatic starts with a simple observation: India's infrastructure spending is about to go parabolic. With $1.4 trillion planned over the next five years, every rupee of infrastructure spending creates demand for compression technology. New airports need HVAC systems. Metro projects need compressed air for tunnel boring. Smart cities need CNG infrastructure. This isn't cyclical demand—it's structural transformation.

The energy transition creates unprecedented opportunities. As India pushes toward 50% renewable energy by 2030, the intermittency problem requires massive energy storage infrastructure. Compressed air energy storage (CAES) is emerging as a viable solution, and guess who makes the compressors? The hydrogen economy, still nascent, will require specialized compression technology for storage and transport. Kirloskar Pneumatic is already developing these capabilities while competitors are still debating whether hydrogen is real.

The dominant market positions create pricing power that's underappreciated. When you control 60-70% market share in critical segments, you don't compete on price—you compete on value. As input costs rise, Kirloskar Pneumatic can pass through increases while maintaining margins. This pricing power will become increasingly valuable in an inflationary environment.

The technology leadership story is accelerating. The dedication to innovation is reflected in KPCL's R&D expenditures, which account for approximately 3.5% of annual revenue. But it's not just spending—it's the output. Twenty patent applications in half a year suggests an innovation engine that's hitting its stride. As Industry 4.0 transforms manufacturing, Kirloskar Pneumatic's early investments in IoT and predictive analytics position them to offer solutions competitors can't match.

Financial performance trajectory suggests we're still in early innings. The company has delivered 58% profit growth in FY25 on 23% revenue growth—operational leverage is kicking in. With capacity expansions coming online and margins expanding, earnings could compound at 25-30% annually even if revenue growth moderates to 15-20%.

The Bear Case: Cyclical Risks and Structural Challenges

The bear case begins with an uncomfortable truth: industrial capex is notoriously cyclical. When the music stops—and it always does—capital goods companies see orders evaporate overnight. Kirloskar Pneumatic's customer concentration in cyclical industries (steel, cement, oil & gas) makes them vulnerable to a synchronized downturn.

Chinese competition is intensifying. While Kirloskar Pneumatic has defended their turf successfully so far, Chinese manufacturers are moving up the value chain. They're no longer just competing on price but increasingly on technology. The same playbook that disrupted consumer electronics and solar panels could eventually reach industrial compression.

Promoter holding has decreased over last 3 years: -14.8%, with current holding at 38.8%. This steady reduction in promoter stake raises questions. Are insiders losing confidence? Is succession planning unclear? In family-controlled Indian businesses, promoter commitment matters, and any wavering creates uncertainty.

The valuation already prices in perfection. At 40x P/E and 8x book value, the stock is priced for sustained high growth. Any disappointment—a delayed order, a margin compression, a competitive loss—could trigger significant multiple compression. The stock's 90% run-up over the past year has brought forward years of future returns.

Global economic uncertainties cloud the outlook. If a global recession materializes, industrial investment will freeze. European customers might cancel orders. Middle Eastern projects might be postponed. Unlike consumer businesses that can weather short downturns, capital goods companies can see 50% revenue declines in severe recessions.

Technology disruption remains a wildcard. What if additive manufacturing eliminates the need for certain compressors? What if solid-state cooling replaces vapor compression? What if fuel cells make CNG infrastructure obsolete? These might seem like distant threats, but technology transitions can happen faster than expected.

The Balanced View

The truth, as always, lies somewhere in between. Kirloskar Pneumatic is neither a risk-free compound nor a value trap. It's a high-quality industrial franchise trading at premium valuations in a cyclical industry undergoing structural transformation.

The key variables to monitor: infrastructure spending trajectory, market share trends in core segments, success in new areas like hydrogen compression, margin sustainability as competition intensifies, and management's capital allocation decisions as cash flow grows.

For long-term investors, the bull case appears stronger. The structural drivers—infrastructure development, energy transition, industrial growth—are multi-decade themes. The competitive position seems defensible given switching costs and service requirements. The management has demonstrated competence through multiple cycles.

For traders and short-term investors, the bear case risks are real. Any global growth scare could trigger a significant correction. The stock's momentum-driven rally has created technical vulnerability. Earnings visibility beyond the current order book is limited.

XI. Future & Strategic Direction

Standing at the intersection of India's industrial past and energy future, Kirloskar Pneumatic faces perhaps its most exciting chapter yet. The convergence of energy transition, digital transformation, and India's manufacturing renaissance creates opportunities that dwarf anything in the company's 66-year history.

The green hydrogen opportunity alone could redefine the company. Hydrogen needs to be compressed to 700 bar for fuel cell vehicles and 350 bar for industrial applications. This isn't incremental improvement—it's 10x the pressure of conventional CNG systems. The technical challenges are immense: hydrogen embrittlement of materials, safety requirements, efficiency at extreme pressures. But for companies that crack this code, the rewards are astronomical. India's National Hydrogen Mission targets 5 million tonnes of green hydrogen production by 2030. Every kilogram needs compression.

Sustainable cooling represents another transformation vector. With India's cooling demand expected to grow 8x by 2037, the environmental impact of conventional refrigeration is unsustainable. Kirloskar Pneumatic's work on natural refrigerants (ammonia, CO2, hydrocarbons) and solar-powered vapor absorption systems positions them at the forefront of this transition. The company's 70% share in ammonia refrigeration systems becomes even more valuable as industries shift from synthetic refrigerants with high global warming potential.

Digital transformation isn't just about putting sensors on compressors—it's about reimagining the business model. Predictive maintenance as a service, performance optimization through AI, digital twins for remote monitoring—these capabilities transform Kirloskar Pneumatic from an equipment supplier to a performance partner. Imagine guaranteeing uptime rather than selling compressors, charging for compressed air as a utility rather than selling systems. These aren't futuristic concepts—they're being piloted today.

Geographic expansion possibilities remain largely untapped. While the company exports to 60 countries, the focus has been on markets where Indian engineering is accepted. But what about developed markets? As Western companies focus on decarbonization, Kirloskar Pneumatic's experience with natural refrigerants and energy-efficient compression could open doors in Europe and North America. The acquisition strategy might shift from buying Indian companies to acquiring technological capabilities abroad.

Adjacent market opportunities multiply as core technologies evolve. Carbon capture and sequestration requires massive compression infrastructure. Semiconductor fabs need ultra-clean compressed air. Data centers need innovative cooling solutions. Electric vehicle battery production requires dry rooms with sophisticated HVAC. Each of these markets is larger than Kirloskar Pneumatic's current addressable market.

The ESG transformation isn't just compliance—it's competitive advantage. Industrial customers increasingly demand Scope 3 emission reductions, which means choosing suppliers with lower carbon footprints. Kirloskar Pneumatic's investments in renewable energy for manufacturing, energy-efficient product designs, and circular economy initiatives (remanufacturing compressors) position them as a preferred partner for sustainability-conscious customers.

Management's vision for the next decade, while not explicitly stated, can be inferred from recent actions. The focus on high-margin segments, investment in R&D, strategic acquisitions in refrigeration, and employee capability building all point toward a transformation from industrial manufacturer to technology-enabled solution provider.

The strategic priorities emerging from recent communications include: achieving ₹5,000 crore revenue by 2030 (implied by growth trajectory), expanding EBITDA margins to 20-25% through value addition, building leadership positions in energy transition technologies, creating digital revenue streams contributing 10-15% of total revenue, and establishing Kirloskar Pneumatic as a global brand, not just an Indian champion.

Risk management for this ambitious agenda requires careful balance. Technology bets must be hedged—investing in both hydrogen and alternative compression technologies. Geographic expansion must be gradual—testing developed markets through partnerships before direct investment. Digital transformation must enhance rather than replace core engineering capabilities.

The organizational capabilities needed for this future are being built today. The Kincentric Best Employer recognition isn't just about employee satisfaction—it's about attracting and retaining the talent needed for transformation. Engineers who understand both thermodynamics and data analytics. Managers who can navigate both Indian infrastructure projects and global supply chains. Leaders who can balance short-term performance with long-term vision.

XII. Key Takeaways & Lessons

After six hours of deep diving into Kirloskar Pneumatic's journey, what emerges isn't just a company story but a template for building industrial champions in emerging markets. The lessons transcend compression technology and speak to fundamental principles of business building.

What Makes Industrial Champions in Emerging Markets

First, technology absorption trumps technology creation. While Silicon Valley celebrates invention, industrial champions in emerging markets succeed through intelligent absorption and adaptation. Kirloskar Pneumatic didn't try to reinvent the compressor; they mastered the art of taking global technology and making it work in Indian conditions. This humility to learn before innovating is paradoxically what enabled them to eventually become innovators.

Second, market dominance in niches beats diversified mediocrity. Rather than trying to be everything to everyone, Kirloskar Pneumatic chose to dominate specific segments. 70% market share in ammonia refrigeration compressors might not sound as exciting as being a diversified conglomerate, but it creates a moat that's nearly impossible to breach.

Third, patient capital creates compound advantages. The Kirloskar family's willingness to accept lower returns during investment phases—whether in technology, capacity, or market development—created advantages that compound over time. In industries where experience curves matter, being willing to lose money initially to gain experience becomes a powerful strategy.

The Power of Long-Term Thinking

The contrast between Kirloskar Pneumatic's approach and typical corporate behavior is stark. While most companies optimize for quarterly earnings, Kirloskar Pneumatic makes decisions with 10-20 year horizons. The Nashik facility investment, the R&D spending at 3.5% of revenue, the employee development programs—none of these make sense if you're optimizing for next quarter's EPS.

This long-term orientation manifests in surprising ways. Customer relationships measured in decades, not contracts. Technology partnerships structured for knowledge transfer, not just licensing fees. Capacity investments ahead of demand, accepting utilization pain for market position gain. These decisions look suboptimal in spreadsheets but create sustainable competitive advantages.

Technology Partnerships vs. Indigenous Development

The false binary between foreign dependence and indigenous development has trapped many emerging market companies. Kirloskar Pneumatic found a third way: strategic technology partnerships as a bridge to indigenous capability. They weren't proud enough to refuse foreign technology nor content enough to remain permanent licensees.

The pattern repeated across partnerships: license, learn, localize, improve, innovate. What started as 80% imported content became 80% indigenous. What began as copying became co-creating. What was once teacher-student became peer-to-peer. This evolution from technology recipient to technology partner to technology leader offers lessons for any emerging market company.

Building Global Competitiveness from India

The conventional wisdom says Indian companies can't compete globally in high-technology manufacturing. Kirloskar Pneumatic proves otherwise. But their path to global competitiveness wasn't through cost arbitrage—it was through solving harder problems.

Indian conditions—extreme heat, dust, voltage fluctuations, monsoons—are harder on equipment than European conditions. Products that survive India can survive anywhere. Service networks that function across India's infrastructure can be replicated globally. Engineers who can make technology work in resource-constrained environments become invaluable in any market.

Final Reflections on the Kirloskar Pneumatic Story

What makes Kirloskar Pneumatic fascinating isn't just their financial success—plenty of companies deliver good returns. It's the way they've built a global technology leader from a divested division in post-independence India. It's the discipline to stay focused on compression technology while peers diversified into everything. It's the patience to build capabilities over decades rather than chase quick profits.

For investors, Kirloskar Pneumatic represents a rare combination: the stability of market dominance with the growth potential of emerging technologies. Yes, the valuation is rich. Yes, the business is cyclical. But the structural drivers—infrastructure development, energy transition, industrial growth—are multi-decade themes that are just beginning.

For business students, the Kirloskar Pneumatic story challenges conventional strategic frameworks. Porter's five forces would suggest their industry is unattractive—powerful buyers, threatening substitutes, intense rivalry. Yet they've built a moated business with expanding margins. The lesson? Execution excellence and patient capability building can overcome structural industry challenges.

For entrepreneurs, especially in emerging markets, Kirloskar Pneumatic offers hope and a playbook. You don't need to be in software or consumer goods to build valuable businesses. You don't need Silicon Valley's venture capital or talent pool. What you need is clarity of purpose, patience to build capabilities, and the discipline to keep improving even when you're already the market leader.

As India stands at an inflection point—demographically, economically, technologically—companies like Kirloskar Pneumatic will play a crucial but often invisible role. They're the industrial backbone that enables the visible prosperity. Every time you see a new metro station, remember there's a compression system behind it. Every CNG vehicle, every refrigerated vaccine, every steel beam—behind each is the unglamorous but essential technology of compression.

The Kirloskar Pneumatic story is far from over. At 66 years old, the company might just be hitting its stride. The next chapter—featuring hydrogen economies, sustainable cooling, and digital transformation—could be even more remarkable than the journey so far. For those paying attention, this "boring" industrial company might just be one of the most exciting investment stories of the next decade.

In the end, Kirloskar Pneumatic reminds us that value creation doesn't always come from disruption or innovation. Sometimes it comes from doing essential things exceptionally well, consistently, for a very long time. In a world obsessed with the new and disruptive, there's profound value in the old and dependable—especially when that dependable company is quietly transforming itself for the future.

The compression technology that powered India's industrial rise will also power its sustainable future. And at the center of that transformation, largely unnoticed but absolutely essential, stands Kirloskar Pneumatic—India's industrial compression champion, hiding in plain sight.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube