Kirloskar Oil Engines: The Family Firm Betting Its Second Century on the Data Center Boom

I. Introduction & Episode Roadmap

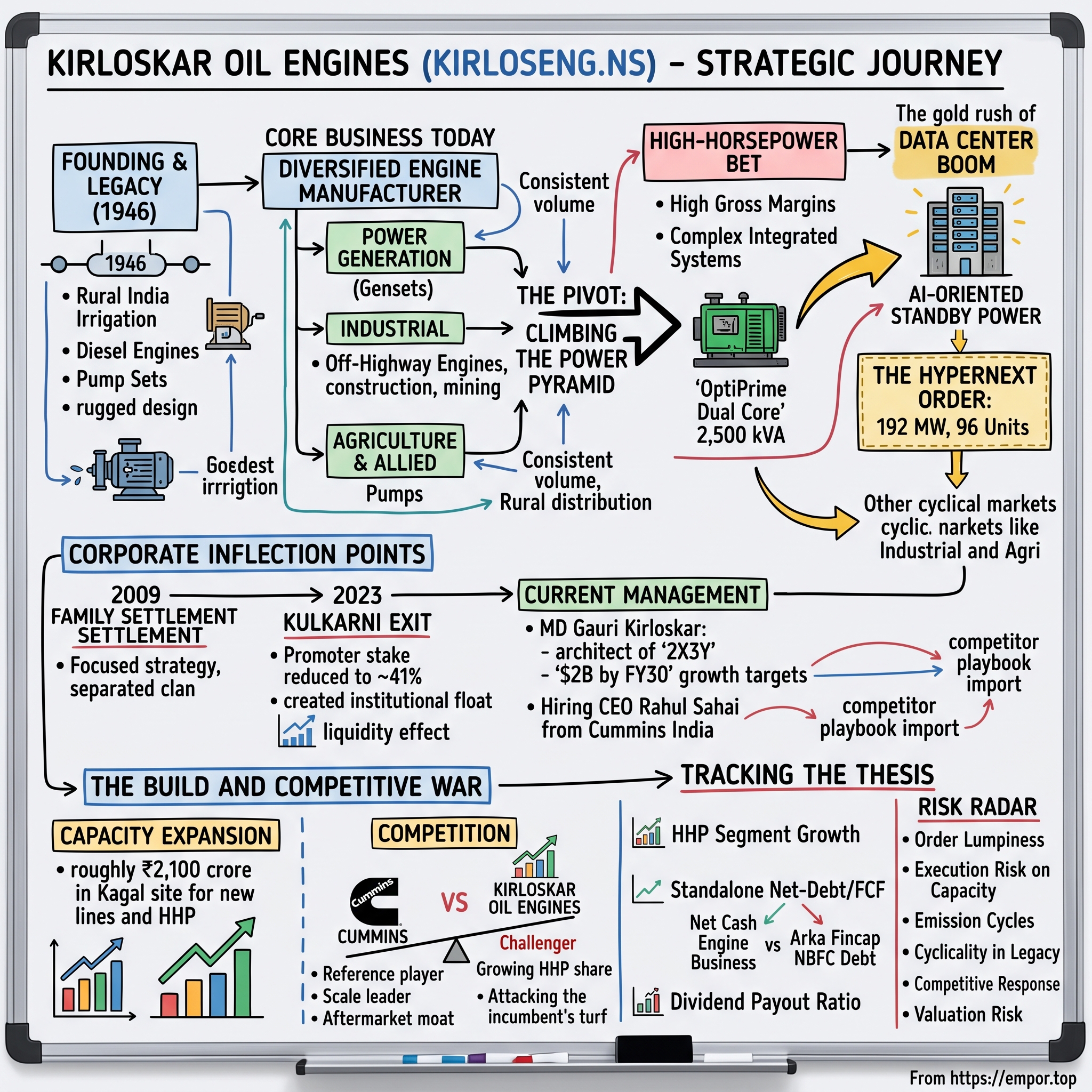

On June 20, 2026, a company that has spent the better part of eight decades building diesel engines to pump water onto Indian farmland issued a stock-exchange filing that read like something out of a Silicon Valley press kit. Kirloskar Oil Engines Limited — ticker KIRLOSENG on the NSE, a name most Indians associate with irrigation pump sets and the reassuring clatter of a backup genset during a power cut — announced that a company called HyperNext had selected it to supply 192 megawatts of standby power: 96 units of its 2,500 kVA "OptiPrime Dual Core" systems, destined to anchor what was described as one of India's first hyperscale, AI-oriented data centers built on an 800-volt DC power architecture.12

The market's reaction was not subtle. The stock slammed into its 20% upper circuit and printed an all-time high within days, as traders reached for the most exciting story available: that a 79-year-old maker of farm and industrial engines had just become an artificial-intelligence infrastructure play.1

Here is the tension that animates this entire story. Kirloskar Oil Engines — KOEL, for short — is still nearly 41% owned by the founding Kirloskar family, one of India's oldest industrial dynasties. Its economic center of gravity remains the diesel engine: the ones that spin irrigation pumps in the monsoon-dependent countryside, the ones bolted into construction equipment, and the gensets that keep factories humming through India's chronic grid unreliability. And yet, on the strength of a single splashy order, the market briefly repriced it as a growth-stock proxy for the data-center capex wave. Is that re-rating earned? Or is one large, undisclosed-value contract being extrapolated into a permanent structural shift?

It is worth pausing on why the market wanted so badly to believe. India in 2026 is in the grip of a data-center gold rush — hyperscalers, colocation operators, and AI-campus builders racing to plant capacity on Indian soil, each facility hungry for uninterruptible power measured not in kilowatts but in tens of megawatts. Any listed company with a plausible claim on that spend gets a hearing. What made KOEL's claim intoxicating was the before-and-after: this was not a new-economy startup but a legacy industrial, the kind of stock that trades on monsoon forecasts and industrial-production prints, suddenly holding a ticket to the most fashionable capex theme in the country. The gap between what the company was and what the order implied is exactly the gap that produces a 20% upper circuit — and exactly the gap a careful investor has to interrogate rather than celebrate.

That question is the spine of everything that follows. To answer it honestly, we have to travel back to a 1946 Pune workshop and, more importantly, to a 2009 family settlement that quietly created the company that trades today. From there: how KOEL actually makes money across Power Generation, Industrial, and Agriculture & Allied; the brutal, cyclical, regulation-whipsawed economics of the Indian engine and genset industry; the 2023 ownership earthquake that finally gave the stock a real free float; the current management team — including a chairman succession and a CEO poached straight from the arch-rival; the high-horsepower bet and the roughly ₹2,100 crore of capacity behind it; the competitive war against Cummins India and a genuinely crowded field; and finally, the bull and bear cases, tested rather than assumed.

Let's start where the engineering did.

II. Origins: From a Pune Workshop to India's Engine Backbone (1946–2000s)

Picture rural India in the middle of the twentieth century: a landscape where the difference between a good harvest and a ruined one often came down to whether a farmer could lift water out of the ground on demand rather than praying to the monsoon. Into that reality stepped the Kirloskars, a Maharashtrian industrial family whose roots trace back to Laxmanrao Kirloskar's turn-of-the-century foundry and the eventual company town of Kirloskarvadi. Kirloskar Oil Engines was founded in 1946 as part of that group, and its early identity was simple and profoundly useful: build diesel engines cheap enough and rugged enough to run irrigation pump sets across a country that desperately needed them.

That founding purpose matters less as history than as genetics. The company built its distribution reach one dusty district at a time, seeding a dealer-and-mechanic network deep into rural and semi-urban India. It learned to make engines that could survive dust, heat, erratic fuel, and owners who would run them for decades. From pump sets it expanded into gensets and industrial engines — a natural adjacency, because the same country that couldn't guarantee water also couldn't guarantee electricity. KOEL, in other words, was built on two of India's most reliable failures: unreliable rain and an unreliable grid.

There is one collaboration from this era that no analyst can afford to treat as trivia, because it turned into KOEL's largest competitor. In 1962, Kirloskar entered a joint venture with America's Cummins Inc. — Kirloskar Cummins Ltd — to build diesel engines in India. It was, for its time, a masterstroke of technology transfer: Cummins brought modern high-horsepower diesel engineering, Kirloskar brought the market and the manufacturing base. The partners eventually parted ways in the 1990s, Cummins took full control, and the entity became what is today Cummins India — now the scale leader of the exact market KOEL is straining to break into.5 Sit with the irony for a moment: the firm that taught Kirloskar the modern craft of the big diesel engine is the one it is now racing to catch at the high end.

This is more than a piquant historical footnote; it is a structural fact about the competitive landscape KOEL inhabits. When a joint venture dissolves and the foreign partner walks away with the crown jewels — the big-engine technology, the brand, the high-margin franchise — the domestic partner is left with the base of the pyramid and the memory of what the top looked like. For thirty years, that is roughly where the two companies stood: Cummins India accumulating the installed base, the consultant relationships, and the reputation at the high-horsepower end, while KOEL harvested volume in pumps, small gensets, and mid-range industrial engines. The current strategy is, in a very real sense, KOEL trying to reverse a divorce settlement from the 1990s — to climb back into the segment its former partner took with it. That framing should stay in the reader's mind through every subsequent section, because it explains both the size of the prize and the difficulty of the climb.

There were other adjacent bets that didn't stick. A 1970s tractor venture with Germany's Deutz-Fahr, housed in a separate entity, was long since wound down and is dormant today — a footnote worth a single sentence, notable only because it shows a group with a periodic appetite for adjacencies that don't always compound.

So what does this ancient history mean for an investor in 2026? Two things, pulling in opposite directions. On one hand, KOEL's engineering know-how and its rural-industrial distribution web are genuine multi-decade assets that a new entrant simply cannot buy off the shelf. On the other, its historical identity — a low-to-mid-horsepower engine maker for farms and small factories — is precisely the identity management is now spending capital to shed. To understand why the company that trades today feels like a different animal from the one founded in 1946, though, you have to understand a family document signed in 2009.

III. The Family Fracture: The 2009 Settlement and What KOEL Became

Family businesses have a particular way of ending an era: not with a hostile takeover, but with a deed. On September 11, 2009, members of the Kirloskar family signed a Deed of Family Settlement that carved the historic conglomerate among branches of the clan. The branch that included Atul and Rahul Kirloskar retained Kirloskar Oil Engines, alongside Kirloskar Pneumatic and Kirloskar Ferrous Industries; other businesses went to other cousins. In the plainest possible terms, this is the true birth certificate of the KOEL that trades today. Everything before it belongs to the broader dynasty; everything after belongs to this company.

But the settlement carries a governance footnote that a neutral observer should weigh rather than wave away. The deed itself was not disclosed to the stock exchanges when it was signed, and it stayed out of public view for years. It resurfaced only when SEBI, India's market regulator, took the position that such a private family agreement imposed indirect restrictions on the listed companies and therefore had to be disclosed — even though the listed entities were not parties to it. Rather than simply comply, several Kirloskar group companies challenged the demand, taking the matter to the Bombay High Court and contesting the constitutional validity of the disclosure amendments SEBI was leaning on. The deed was ultimately disclosed only after a Bombay High Court order dated September 23, 2025 — roughly sixteen years after it was signed.8

How should a story that aspires to independence treat this? Not as a live scandal, and not as ancient irrelevance, but as a dated yellow flag on the promoter group's disclosure instincts. KOEL was not the direct party at fault, and no operating harm to the company has been established. Yet a governance matter that took a decade and a half — and a High Court order — to fully resolve and disclose is a real data point about how this family handles the boundary between private arrangements and public shareholders' right to know. It is the kind of thing that costs nothing when everything is going well and matters enormously in the one year it doesn't. File it, and move on.

There is a broader lesson embedded in this episode that applies far beyond KOEL, and it is worth stating for the long-term investor: in India's promoter-controlled companies, the governance risk you cannot see on the income statement often lives in the family, not the business. A conglomerate divided among cousins can produce years of quiet friction over who controls what, who owes what to whom, and what was privately agreed that public shareholders were never told. None of that necessarily impairs the operating company — KOEL kept building and selling engines throughout — but it does mean the minority shareholder is, to some degree, a passenger in a vehicle whose steering is shared within a family. The clean, unpledged, stable promoter block that KOEL exhibits today (a point we return to) is reassuring precisely because the historical record shows the alternative is possible.

Because with that deed, the modern Kirloskar Oil Engines came into being: a focused engine-and-power company, controlled by one branch of the family, free to chart its own strategy. The rest of this story is about that company — and the first thing to understand about it is how, exactly, it turns engines into cash.

IV. Anatomy of the Business Today: Where the Money Actually Comes From

Strip away the data-center headlines and KOEL is, at heart, a diversified diesel-engine manufacturer that reports across a handful of businesses. Walk them in order of how they touch the world.

Power Generation is the crown jewel and the segment management is most actively reshaping. It spans everything from small backup gensets — the kind that hum to life behind a hospital or an apartment tower during a cut — up through multi-megawatt, high-horsepower systems for large infrastructure and, now, data centers. On the Q3 FY26 call, management flagged that the domestic Power Generation business delivered ₹603 crore in a single quarter, up 44% year over year, driven largely by its retail genset business.3 This is both the legacy volume engine and the vehicle for the entire growth story.

Industrial / Off-Highway Engines sells engines to other manufacturers — construction-equipment, compressor, and material-handling OEMs — with customers spanning global names like Caterpillar and Komatsu and India's own ACE. In Q3 FY26 the domestic industrial business posted its best-ever quarter at ₹390 crore, up 41%, powered by defence, nuclear, and marine demand; construction and mining were softer, which management attributed to OEM customers correcting inventory rather than a demand collapse.3 For the full year FY26, the Industrial segment grew 22% to ₹1,444 crore, with construction up 44% year over year as KOEL's products cleared the new CEV BS-V emission standard.4

Agriculture & Allied is the ancestral business — engines for irrigation pump sets — and it remains economically tethered to monsoon quality and the farm-input cycle. It is lower-growth and lower-glamour, but it is also the deep well of volume and distribution that funded everything else.

Around these sit a Distribution & Aftermarket business — spare parts, service, and annual maintenance contracts, which grew to a record ₹238 crore quarter in Q3 FY263 — and an International book that management is careful to distinguish from mere exports: the ambition is to build genuine local businesses in select geographies rather than just ship engines abroad.4

Now, the numbers that require honesty. There are two very different KOELs depending on which line of the accounts you read, and conflating them is the single easiest way to misjudge this company. On a standalone basis — the core engine business — FY26 net sales were ₹5,604 crore, up 25% from ₹4,481 crore, with EBITDA of ₹737 crore (a 13.1% margin) and net profit from continuing operations of ₹464 crore, up 35%.4 On a consolidated basis, revenue runs higher — toward the ₹7,700 crore range cited in press coverage — because the group also consolidates Arka Fincap, a financial-services (NBFC) subsidiary, and the KOEL Fluid Dynamics pumping business built around the La-Gajjar acquisition.13 The presence of a lending company inside the group is why aggregated data services and standalone filings can show jarringly different revenue, debt, and profit figures for "the same" company. Throughout this story, when the distinction matters — and for leverage, it matters a lot — we will say which KOEL we mean.

A word on that finance subsidiary, because it is easy to miss and impossible to ignore once you see it. Arka Fincap is a non-banking financial company — a lender — that KOEL has built and scaled aggressively: its loan book (AUM) reached ₹7,947 crore in FY26, up from a far smaller base, as it expanded from 34 to 137 branches in a single year and pivoted toward secured retail lending.4 An NBFC inside an engine company is an unusual portfolio choice, and it is the single biggest reason the consolidated financials look so different from the standalone ones: a lender's entire business model is to borrow money and lend it out at a spread, so consolidating Arka drags a large borrowings figure and a chunky revenue line onto the group accounts that have nothing to do with making engines. Whether Arka is brilliant diversification or a distraction — a "diworsification," in the classic critique of conglomerates wandering from their core — is a live question a skeptical investor is entitled to press. For now, it is profitable (FY26 profit after tax of roughly ₹69 crore) and growing, but it complicates the story and the balance sheet in ways this article will keep flagging.4

The honest framing to carry forward: this is still fundamentally a diesel-engine manufacturer selling into cyclical, capex-linked Indian end markets — agriculture, construction, industrial capacity, and backup power — with a finance subsidiary bolted on and a fast-growing high-end sliver. It is not yet a diversified technology company, whatever the June headlines implied. And understanding why it is such a hard business to run well requires understanding the peculiar rhythm that governs the entire industry.

V. The Economics of the Business: Emission Cycles, Distribution, and Why This Is a Hard, Cyclical Trade

Every few years, the Indian engine industry gets shaken by the same force, and it is not demand — it is the regulator. The genset and engine businesses live and die by emission norms, and the transition from the CPCB II standard to the far stricter CPCB IV+ regime forced the entire industry through a multi-year cycle of recertifying products, re-engineering engines, and repricing them upward. Think of it as a mandatory, government-scheduled product refresh that everyone must undergo at once. The predictable pattern: demand gets pulled forward as buyers rush to purchase before a deadline, then digests in a stabilization period afterward. This same rhythm is why KOEL's construction segment, tied to the January 2025 CEV BS-IV to BS-V shift, is a story of customers won and lost on the strength of whose engine clears the new bar — a qualification process management says can take eighteen months per OEM.4 Emission cycles are not a one-off shock here; they are a structural feature of the terrain, and they favor players with the engineering depth and capital to recertify fast.

There is a second, subtler feature of emission cycles that rewards the incumbent and punishes the challenger, and it surfaced in the Q3 call almost in passing. Every norm change forces buyers to re-decide, and re-decisions can go either way — an emission shift is "both an opportunity to acquire customers and a risk of losing them," as management put it regarding the construction segment.4 For a challenger trying to climb, each cycle is a chance to poach a customer who must re-qualify anyway. But for the incumbent with the deepest service network and the most consultant relationships, the same churn is a chance to consolidate the fragmented tail toward organized players. The regulatory rhythm, in other words, is a double-edged sword — and which edge cuts your way depends on whether you already own the relationship or are trying to win it.

Run the business through Porter's Five Forces and the picture sharpens. Buyer power is moderate-to-high, because large industrial and OEM customers can and do multi-source their engines; a data-center developer specifying gensets will happily play Cummins, KOEL, and a Caterpillar-based assembler against one another on price and delivery. Supplier power is moderate — steel, castings, and electronic-control components matter, but are not single-sourced chokeholds, though the electronics content of CPCB IV+-compliant engines has raised the stakes on component sourcing. Barriers to entry are the interesting split: at the high-horsepower end they are genuinely high — engineering complexity, certification, capital intensity, and the need for consultants to approve your product before a data center will touch it — while at the low-horsepower end they are low, and competition is fragmented and brutally price-driven. That split is the whole game: the low end is where KOEL is strong but the economics are thin, and the high end is where the economics are fat but KOEL is the newcomer. Substitution is a slow-burn threat: as the grid becomes more reliable and as renewables-plus-battery storage matures, the economic case for a diesel genset as backup power erodes at the margin — though for a data center that cannot tolerate a millisecond of interruption, diesel standby remains, for now, the trusted default. And rivalry is intense and multi-tiered, running from global majors down to regional assemblers who bolt gensets around Cummins engines.

Now apply Hamilton Helmer's 7 Powers, which asks not "is this a good business" but "what, specifically, keeps competitors from copying you." KOEL's most defensible claim is something close to process power — decades of accumulated engine-manufacturing know-how — married to a scale-economy-flavored distribution and service network that reaches into rural and semi-urban India in a way that would take a rival years and enormous capital to replicate. For the irrigation and low-horsepower genset business, that is a real, if unglamorous, moat. But here is the uncomfortable part: at the high end — the part the market is now paying up for — KOEL has essentially no durable power yet. That is Cummins India's turf, where an installed base, brand trust among consultants, and a dense service network create something much closer to genuine switching costs and scale advantage.

Management's own words are the best evidence check here, and to its credit, the team does not oversell. On the FY26 calls, executives described the high-horsepower business as having gone from "zero market share" a couple of years ago to "approaching double digits" — impressive as a growth rate, but candidly a minority position.34 Even more telling was an exchange on the Q3 call in which an analyst pressed on whether KOEL had actually been losing low-horsepower share to the market leader over the two years since CPCB IV+; managing director Gauri Kirloskar declined to engage, saying she couldn't comment without knowing the source of the analyst's data.3 A good growth-rate story sits on top of a still-small base and, in the legacy segment, a still-contested one. That is not a criticism — it is simply the trade as it actually is.

The cyclicality drivers are worth naming plainly, because they will determine whether any given year looks like a triumph or a stumble regardless of the data-center narrative: monsoon quality and rural income drive Agri & Allied; industrial capex and construction activity drive Industrial engines; and now a brand-new, far less tested driver — hyperscale data-center capex — has been added to the mix. The question of whether KOEL can win in that last category depends entirely on the incumbent it is up against.

VI. Competitive Landscape: Cummins India and the Rest of the Field

If this were a boxing match, the tale of the tape would be lopsided. In one corner, KOEL, with standalone FY26 revenue of ₹5,604 crore.4 In the other, Cummins India, which posted FY25 revenue of ₹10,166 crore — its highest ever, up about 15% year over year — with profit after tax of ₹1,906 crore on domestic sales that alone were ₹8,395 crore.5 Cummins is not just larger; it is the incumbent that KOEL's own management points to when discussing the high-horsepower and data-center opportunity. And Cummins has been riding the same data-center wave, with analysts and its own commentary attributing a surge in orders above 2 megawatts to AI-campus demand and data-center deliveries now making up a meaningful chunk of its power-generation revenue.14 The rival is not asleep; it is arguably the best-positioned player in the country for exactly the prize KOEL is chasing.

But it would be a mistake to imagine this as a two-horse race. Mahindra Powerol, a division of Mahindra & Mahindra, was named India's No. 1 diesel genset manufacturer by volume in FY25 by Frost & Sullivan, with a reported 23.8% share of a roughly 150,000-unit annual market.6 That statistic contains a crucial subtlety: volume leadership and value leadership are entirely different contests. Mahindra wins on units, largely at the lower-horsepower, higher-volume end; the money and the moat in this industry increasingly sit at the high-horsepower end, where the fight is between Cummins and everyone trying to reach it.

Greaves Cotton offers the most instructive contrast. A smaller, more diversified peer with FY25 consolidated revenue around ₹2,900 crore, Greaves made a deliberately different strategic bet — it poured growth capital into electric mobility, to the point that its Greaves Electric Mobility unit approached a quarter of consolidated revenue, rather than doubling down on diesel and gas engines. Two old-line engine makers, two opposite conclusions about where the future lies: Greaves diversifying away from the core, KOEL concentrating harder into the high end of it. Only one can be right for any given investor's thesis, and the market will settle the argument over the next several years.

Round out the field and you see how crowded the ring really is. Jakson Group and Sudhir Power are large genset assemblers built on Cummins engines — both market themselves as leaders, though that self-reported claim should be treated skeptically absent independent data. Wärtsilä and Volvo Penta occupy the higher-end power-plant and industrial-engine space. Force Motors runs a joint venture with Rolls-Royce Power Systems (the MTU brand) in large-format diesel for rail and marine. Ashok Leyland's Power Solutions division fields a commercial-vehicle-derived genset business. The point is not to memorize the roster; it is to internalize that KOEL is a credible, well-capitalized number-two-or-three player charging at the most attractive part of the market against an entrenched, larger, better-capitalized leader.

There is a competitive nuance in that Jakson/Sudhir layer worth dwelling on, because it complicates the simple "KOEL versus Cummins" framing. Many of the assemblers that dominate the genset market do not manufacture the engine at all — they buy the core engine (frequently from Cummins) and integrate it into a packaged genset with an alternator, controls, and an enclosure. This means Cummins wins twice: once through its own branded gensets, and again by selling engines to the very assemblers who compete at the retail level. For KOEL, which manufactures its own engines and increasingly its own integrated systems like OptiPrime, the opportunity is to capture more of that value chain — but the challenge is that it is fighting an engine platform, Cummins, that is embedded across the ecosystem, not just a single rival brand. Displacing an entrenched engine standard is harder than beating a competing product, because it means persuading consultants, assemblers, and end customers to re-standardize around you.

War-game it from Cummins's side for a moment, because a challenger's thesis is only as good as its read on how the incumbent responds. Cummins India is not a sleepy monopolist ripe for disruption; it is a focused, profitable market leader riding the same tailwind, rolling out its own CPCB IV+ high-horsepower products into the data-center surge and generating the cash to defend its turf.514 An incumbent with an installed base, a service moat, and superior scale economics can respond to a challenger in ways that do not show up until it is too late — sharpening service-level agreements, bundling aftermarket, leaning on consultant relationships, and, if it chooses, competing harder on price at exactly the nodes where the challenger is trying to gain a foothold. KOEL's bet is not that Cummins is weak; it is that the market is growing fast enough that a well-executed challenger can take share of the growth even while the incumbent stays dominant. That is a more modest — and more honest — proposition than "KOEL disrupts Cummins," and it is the one the evidence actually supports.

That is the classic challenger setup, and it comes with a classic challenger question: can the challenger take share fast enough, and durably enough, to justify a growth multiple? Part of the answer lies in the company's balance sheet and ownership — and both were reshaped by an event in 2023 that had nothing to do with engines at all.

VII. The Ownership Earthquake: The 2023 Kulkarni Exit

Sometimes the most important thing that happens to a stock isn't an order or a product — it's a decision by a family to walk away. In March 2023, the Kulkarni family, a branch of the founding promoter group, sold its entire stake in Kirloskar Oil Engines. The transaction moved through open-market block deals: roughly 2.56 crore shares, about 17.71% of the company, at an average of ₹322 per share, for a total of about ₹825 crore. The sellers had announced their intention to exit Kirloskar group companies altogether. On the other side of the trade sat a roll-call of serious institutions — Nomura Trust, Société Générale, BNP Paribas Arbitrage, the Regents of the University of California, Max Life Insurance, and DSP Mutual Fund among them.7

Why does a single block deal deserve its own chapter? Because of what it did to the ownership structure. In one stroke, promoter/family holding dropped from roughly 59% in early 2022 to about 41% by mid-2023, and it has stayed essentially flat there since.13 This was not a gradual drift; it was a one-time re-basing of the entire shareholder register. And the consequence is subtle but decisive: it manufactured a free float where one barely existed before.

Here is the mechanism, because it is easy to underrate. A tightly held, illiquid stock is structurally unable to absorb large institutional buying — there simply aren't enough shares available to trade without moving the price violently. The Kulkarni exit dumped nearly a fifth of the company into institutional hands and, in doing so, created the liquidity precondition for everything that followed. Since 2023, institutional ownership has broadened substantially — foreign portfolio investors added to positions into early 2026, mutual-fund ownership rose steadily, and the shareholder base widened from roughly 36,000 holders in 2017 to over 106,000 by 2026.13 When the data-center news hit in June 2026, there was a deep, liquid, institution-friendly float ready to be repriced. Without the 2023 exit, the same news might have produced a thin, jumpy move rather than a sustained re-rating.

There is one more dimension to the Kulkarni exit that deserves a beat, because it speaks to how family-controlled companies actually evolve. When a promoter branch decides to leave entirely — not trim, not diversify, but exit — it removes a potential source of the very intra-family friction the 2009 settlement was meant to resolve. A cleaner cap table, with fewer family branches holding blocking positions, arguably makes the remaining management's job easier: fewer cooks, clearer accountability. The flip side, which a governance-minded investor should hold in tension, is that a large promoter exit at ₹322 per share was also a signal that one branch of the founding family did not see enough future value to stay — and the stock has since traded well above that level.7 Read charitably, the Kulkarnis simply wanted out of Kirloskar companies for their own reasons; read skeptically, insiders sold, and the outside institutions who bought have been the beneficiaries of the re-rating. Both readings can be true at once.

There is a governance grace note here that partially offsets the family-settlement flag from earlier. Since 2023, the remaining Kirloskar promoters — Rahul, Atul, Gauri, and related family members and entities — have held their combined ~41% stake essentially flat, with no confirmed pledging of shares against loans.13 For a family-controlled Indian company, an unpledged, stable promoter block is a quietly reassuring signal: the family is neither cashing out nor borrowing against the business. It is a clean, if unspectacular, marker of alignment — and it raises the natural next question of what this management has actually done with capital when it has deployed it.

VIII. Disciplined but Modest: KOEL's M&A and Capital Deployment Record

Every management team that promises transformation invites the same audit: show us your track record with other people's money. KOEL's M&A history is best described as disciplined, modest, and — importantly — mostly unproven at scale.

The most substantial deal is La-Gajjar Machineries, the Ahmedabad-based pump-and-machinery maker. KOEL acquired a 76% stake in 2017 (reported at roughly 7.9x EBITDA) and bought out the remaining 24% in 2022 to take full ownership.11 La-Gajjar has since been folded into the group's KOEL Fluid Dynamics pumping business, which management describes as its B2C fluid-dynamics platform spanning water and agricultural pumps.34 It is a genuine, adjacent bolt-on that fits the distribution logic of the core business. But a fair analyst has to note what the public record does not provide: a clean benchmark against comparable industrial-machinery deal multiples. Whether KOEL paid a smart price or an average one is, honestly, unresolved — so treat the "was it cheap" question as open rather than assuming the answer.

The international record is smaller and more experimental than transformational, and management is refreshingly plain about that. KOEL took a 51% stake in a small US generator maker (Engines LPG LLC, doing business as Wildcat Power Gen) in November 2023 — a business whose post-acquisition revenue was reported at under $1 million with a net loss. It incorporated a UAE subsidiary, Kirloskar International ME FZE, in January 2025, tied to a small planned South African acquisition that management framed on the Q3 call as a modest, market-by-market capability build rather than a landmark deal.3 And a 2010-era joint-venture MOU with US-based Axial Vector Energy Corporation for novel engine technology appears to have quietly lapsed without ever reaching mass production — a useful, sobering data point on follow-through when this group makes early-stage technology bets.

The candid framing, which the company itself essentially endorses: none of this international activity is currently material to consolidated revenue or profit. It is optionality and market-development spend — planting seeds in the US, the Middle East, and Africa to see which take root — not a second engine of growth. Inflating it into more than that would be exactly the kind of promotion this analysis is meant to avoid.

One newer seedling is worth a sentence because it is strategically interesting even while being financially tiny: Kirloskar Advanced Systems Private Limited, incorporated in early 2026 with modest capital, positioned around defence and railway systems-integration work. It ties to the Indian Navy's ₹270 crore "Make-I" contract, awarded in April 2025, for an indigenous 6-megawatt marine diesel engine, with a prototype targeted for 2028.12 It is genuine optionality riding India's defence-indigenization push — and it is minuscule against a company doing thousands of crores in annual revenue. Size it as a footnote, not a pillar.

What all of this reveals is a management culture that deploys capital cautiously and incrementally. Whether that same culture can execute the far larger, far bolder high-horsepower capacity bet is the real test — and to judge that, you have to meet the people now making the decisions.

IX. Current Management: A Family Succession, and an Outsider Hired From the Rival

The changing of the guard at KOEL happened on a calendar date: March 31, 2026, the day Atul Kirloskar retired as Chairman after 43 years with the company, having reached the mandatory retirement age of 70. His cousin Rahul Kirloskar, previously a non-executive director, took the chairman's seat effective April 1, 2026.10 The continuity is deliberate; this is a family handing the gavel within the family. But the more consequential figure for the strategy is not the chairman.

Gauri Kirloskar — Atul's daughter — is the executive who has actually driven KOEL's acceleration. Managing Director since 2014 (with the MD title formalized in 2022, and a fresh three-year term approved in 2025 with a striking 99.6% shareholder vote), she added the Vice-Chairperson title alongside the recent succession.4 Her background is not the usual family-scion résumé, and it matters to the story: a finance and M&A career at Merrill Lynch, followed by a stint in Pearson's corporate-strategy group, before she returned to India in 2010. She is the architect of the internal "2X3Y" ambition — the drive to roughly double revenue over three years, escaping the low-single-digit growth of the prior decade — and of the newer public target of reaching $2 billion in revenue by FY30.4

It is worth lingering on what that background implies about how she runs the company, because it is unusual among Indian promoter-heirs. Someone who spent formative years in investment banking and corporate strategy tends to think in portfolios, returns on capital, and probability-weighted outcomes rather than in the operational instincts of a lifer who came up through the shop floor. That shows in KOEL's recent posture: the willingness to set an explicit, quantified multi-year revenue target and hold the organization to it; the framing of businesses around "complex products, aftermarket, and international" as the profitable-growth vectors; the incubation of a financial-services arm, Arka Fincap, as a separate value-creation vehicle; and the readiness to hire senior outside talent, including from the direct competitor. It is a more capital-markets-literate way of running a family engineering firm than the sector's norm — which is a genuine asset when the strategy is working and a source of scrutiny when the numbers are asked to justify the ambition.

That $2 billion goal deserves to be tested, not repeated. On the Q4 FY26 call, an analyst noted bluntly that hitting it implies roughly tripling from current levels and asked what capex that requires. Management confirmed the goal and pointed to the capacity build underway, but declined to break down how much of the $2 billion is expected to come from data centers specifically, calling parts of the question internal.4 The target is a stretch ambition backed by real early progress — revenue genuinely did accelerate into the mid-20s-percent range in FY26 — but it remains a promise about FY30, and the discipline is to track delivery against it rather than to score it as already achieved.

Now the hire that tells you the most about competitive intent. In a move that would make any war-gamer sit up, KOEL appointed Rahul Sahai as CEO effective January 1, 2025 — and Sahai came from years at Cummins India, where he worked in distribution, channel strategy, and marketing.9 Read that again: the company chasing Cummins in high-horsepower engines hired one of Cummins's own India executives to help run the chase. This is not investor-day rhetoric about "closing the gap"; it is a concrete, testable action. A firm that wanted to out-distribute and out-service the market leader went and bought a piece of that leader's playbook. On the FY26 calls, Sahai fielded the pointed questions — on construction inventory corrections, on why channel checks kept surfacing multinational names instead of KOEL's, on international market entry — with the measured, sometimes deflecting precision of someone who knows exactly how the incumbent thinks.34

Why does the provenance of the hire matter so much? Because in this industry the moat is not the engine block — it is distribution and service. A data-center operator does not buy a genset the way it buys a laptop; it buys a decades-long relationship, a promise that when the grid fails at 3 a.m. a technician will be on-site fast, and a track record that consultants will sign off on. That is precisely the muscle Cummins spent decades building and KOEL historically lacked at the high end. Hiring someone who built or ran pieces of the incumbent's channel is the single most direct way to import that capability rather than grow it slowly. It is also, notably, consistent with how management describes the internal work: on the Q3 call, KOEL's CHRO detailed a deliberate program to retrain frontline sales teams — and even the sales teams of its genset-OEM partners — because high-horsepower products "are way too more technical in nature" and must be explained and witnessed by consultants before they win, a fundamentally different sale from selling a pump-set engine.3 The Sahai hire and the capability-building program are two expressions of the same recognition: to win the high end, KOEL must sell differently, not just build differently.

A fair-minded skeptic should still ask the counter-question: does one executive move the needle at a company this size, and is a channel-and-marketing background the right pedigree to close an engineering-and-service gap? A single hire is a signal of intent, not a guarantee of capability transfer; corporate history is littered with star executives who could not replicate a rival's advantage inside a different culture. The honest verdict is that the hire raises the probability KOEL executes, without proving it will — which is exactly how leading indicators are supposed to be weighed.

On incentives and pay: the combined family promoter stake sits around 41%, split so that no single family member holds more than roughly 12%.13 Gauri Kirloskar's disclosed compensation has ranged from roughly ₹5 crore to ₹9 crore across recent years, weighted toward commission and variable pay rather than fixed salary, with no ESOP component reported for her specifically.13 That is moderately incentive-aligned — her wealth rides on the family shareholding more than on option grants — but it is worth flagging that Indian listed companies disclose only summary remuneration, so precision here is genuinely limited.

The capital-allocation credibility test is where a skeptic should lean in, and where the standalone-versus-consolidated distinction from earlier earns its keep. Two facts are often cited as a bearish pair: the dividend payout ratio has declined steadily even as profits have grown (from roughly a third of earnings in FY22 toward the low teens on a trailing basis by FY26), while consolidated borrowings have ballooned toward the multi-thousand-crore range.13 The dividend compression is real and defensible — a company funding a large growth build reasonably retains more earnings — but shareholders should watch whether returns keep shrinking. The debt figure, however, needs the reconciliation this article promised: the bulk of consolidated borrowings sits inside Arka Fincap, the lending subsidiary, for which borrowing is the business model — an NBFC funds its loan book with debt by definition, and Arka's AUM alone was ₹7,947 crore at FY26.4 The core engine business, by contrast, ended FY26 in a net cash position of ₹552 crore on a standalone basis.4 So the honest read is not "an overlevered manufacturer," but "a net-cash engine maker that also consolidates a finance company." That is a materially different — and more benign — picture than the raw consolidated debt number suggests, and getting it right is exactly the kind of second-layer diligence that separates signal from headline.

Where management is least satisfying is on quantifying the data-center story, and they have been consistent in that reticence across calls — which brings us to the bet itself.

X. The Big Bet: High-Horsepower Engines and the Data Center Gold Rush

Here is the narrative the market fell in love with, told straight. Two-plus years ago, KOEL's high-horsepower (HHP) segment barely existed — "zero market share," in management's own phrasing. Then it caught fire. In Q3 FY26, the HHP segment grew 235% year over year; over the first nine months of the fiscal year, it grew 132%.3 By the close of FY26, management described HHP share as "approaching double digits."4 Both halves of that sentence must be held together at once: this is genuinely fast growth, off a genuinely small base. A number can triple and still be a minority sliver — and that is precisely the situation.

The capstone, of course, was the June 2026 HyperNext order: 192 MW across 96 units of the 2,500 kVA "OptiPrime Dual Core" system, for a hyperscale, AI-oriented data center built on 800-volt DC architecture, described by multiple outlets as among the largest standby-power deployments for a hyperscale facility in India.12 A word on the technology, in plain terms: a data center cannot tolerate even a flicker of lost power, so it needs enormous banks of standby generators that can shoulder the entire load the instant the grid fails. The "OptiPrime Dual Core" approach packs multiple engine cores into one integrated system to deliver more power in less floor space — floor space being scarce and expensive in a data center. The 800VDC detail signals a next-generation, AI-optimized facility design. It is a real, marquee win. It is also, notably, a contract whose exact rupee value was not disclosed in any source found — a fact the market cheerfully ignored, and one an honest analyst should not.1

It is worth understanding why an order like this validates KOEL's strategy in a way that revenue alone would not. Recall from the Q3 call that KOEL's high-speed single engine units top out around 1,500 kVA, while the company also makes engines that reach 10 megawatts.3 A 2,500 kVA solution therefore is not a single engine — it is the OptiPrime multi-core architecture, precisely the kind of "complex product" management has repeatedly said is its chosen path to profitable growth.3 Winning a hyperscale customer with such a system means clearing the consultant-approval gauntlet, proving the integration works at scale, and earning a reference customer — the credential that opens the next data-center door. In a business where the first sale is the hardest, a marquee win is worth more than its rupee value, because it converts KOEL from an aspirant the consultants have to be talked into to an incumbent they have already witnessed. That is the genuine strategic content of the HyperNext order, over and above whatever it eventually contributes to the top line.

But keep the counterweight firmly in view: a single order, however prestigious, is a data point, not a trend. Data-center demand is famously lumpy — a facility is built in phases, orders arrive in bursts, and a quarter with a HyperNext-scale win can be followed by a quarter with none. This is why order lumpiness sits near the top of the risk radar later in this piece, and why the market's instinct to annualize one order into a permanent growth rate is exactly the instinct to resist.

Behind the order sits the capacity to fulfill it, and this is where the capital gets committed. KOEL earmarked roughly ₹700 crore to expand its existing Kagal (Kolhapur) plant — enhancing and adding lines for about 50,000 engines a year, targeted online by around April 2027.4 Then, in May 2026, it approved a further roughly ₹1,400 crore for an entirely new building at the same Kagal site, adding about 20,000 high-horsepower engines a year over the following two years.4 That is roughly ₹2,100 crore of multi-year capital commitment. Management was careful on the Q4 call to explain why the second tranche costs twice as much for fewer engines — it includes a whole new building and completely new lines and equipment, and it is skewed toward larger, higher-horsepower machines.4 Crucially, management also stated the capacity is for the whole company's use, not dedicated solely to data centers — a caveat that tempers the cleanest "pure AI-infrastructure play" version of the story.4

Pause on the economics that these buildings are meant to produce, because capacity only matters if it earns a return. On the Q4 call, an analyst did the arithmetic out loud: reaching the $2 billion FY30 goal implies roughly tripling revenue, which implies the gross block climbing from around ₹1,900–2,000 crore toward perhaps ₹4,000 crore-plus once the ₹700 crore and ₹1,400 crore tranches land — and he asked, reasonably, what asset turn to expect on all that new plant.4 Management's reluctance to hand over a clean asset-turn number is understandable but leaves investors to triangulate. The bullish mechanism is straightforward: high-horsepower engines carry richer gross margins than the legacy low-horsepower volume business, so as HHP grows into the mix, blended margins should rise — management confirmed gross margin was flat around 35% but "should improve" as HHP scales.3 The bearish mechanism is equally straightforward: new capacity is a fixed cost that must be filled to earn its return, and a project-driven, lumpy data-center order book is a riskier way to fill a plant than the steady, predictable pull of pump-set and small-genset demand. Build a factory for a boom, and you are exposed if the boom arrives in fits and starts. That is the fundamental trade the ₹2,100 crore commits KOEL to.

The sell-side reaction functions as a useful real-time credibility check, cutting both ways. Bullish houses moved quickly — the HyperNext news drew upgrades and higher targets, with the thesis often framed as a narrowing valuation discount to Cummins India as KOEL's portfolio expands into the high end.14 But at least one independent voice flagged the obvious risk: after the rally, the stock traded at a rich multiple (reported around the high-40s times trailing earnings) that leaves little room for operational error, alongside the working-capital strain and lumpy, unpredictable order timing that a capital-intensive, project-driven build inevitably brings.14

And then there is the tell that recurs across every earnings call: management will not quantify the data-center contribution. Pressed directly on the Q4 FY26 call for the data-center share of Power Generation revenue, CEO Rahul Sahai called it "premature" to give out those contributions — and when the analyst pushed for even a single-versus-double-digit hint, offered only that the company "certainly sight[s] for double digit as far as contribution is concerned."4 That is aspiration, not disclosure. It may reflect genuine commercial sensitivity, or an order book too lumpy to characterize, or simply a base too small to advertise. Whatever the reason, the correct way to size this whole segment is: real, growing fast, strategically central to the stock's story — and thinly disclosed on exact economics. Not a foregone conclusion. Which sets up the argument the whole article has been building toward.

XI. Bull vs. Bear: The Investment Case, Tested

Let's put both cases on the table and stress them, rather than picking a side.

The bull case is genuinely attractive. A multi-decade engine manufacturer with real engineering and distribution assets is finally aiming its capital at the fastest-growing, highest-margin part of its own industry — high-horsepower gensets — at the exact moment India's data-center buildout is accelerating. This is not a slide-deck ambition: management has demonstrably grown HHP share from near-zero, hired a Cummins veteran to run the chase, and landed a marquee 192 MW order as tangible proof of concept.13 The 2023 ownership event created the liquidity and institutional interest needed to sustain a re-rating. And the balance-sheet fear is overstated once you strip Arka Fincap out: the core business is net cash, giving it room to fund the ₹2,100 crore build without existential leverage.4 Gross margins should structurally improve as the higher-margin HHP mix rises — management said as much, noting margins were flat at ~35% but should climb as HHP grows.3

The bear case is equally coherent. By revenue, this is still mostly a cyclical, low-to-mid-horsepower diesel-engine and irrigation-pump business exposed to monsoons and industrial capex, now wearing a growth-stock multiple earned on the strength of one large, undisclosed-value order and a capacity plan that is not yet built. The incumbent it must beat — Cummins India — is roughly twice its size, is the reference player in data-center gensets, and is itself surging on the same wave; there is no evidence it intends to cede the high ground.514 Management's persistent refusal to quantify the data-center contribution means shareholders are being asked to trust an unproven execution story on qualitative language. And an exchange on the Q3 call — where an analyst suggested KOEL had lost low-horsepower share to the leader over the CPCB IV+ transition, and management declined to rebut it — is a reminder that share can move against KOEL, too.3

Fold in the frameworks. Through Porter, the attractive high end has high entry barriers that today protect the incumbent more than the challenger; through Helmer's 7 Powers, KOEL's real powers (process know-how, distribution) live in the legacy business, while it is still building — not yet holding — power at the high end. That asymmetry is the crux: KOEL is spending to acquire, in data centers, the kind of durable advantage it already enjoys in pump sets.

The skeptical-investor stress test asks the sharpest version of the question. No activist campaign exists at KOEL as of mid-2026, but a hard-nosed long/short analyst would frame it thus: after a decade of unremarkable growth, is the recent acceleration a durable structural shift in end-market mix, or a cyclical, order-driven spike — juiced by the CPCB IV+ replacement wave and a handful of large wins — that the market has already extrapolated into a permanent re-rating versus Cummins? The most honest answer available is management's own hedged, non-quantified language on the FY26 calls. When the people closest to the data say it is "premature" to size the data-center contribution, that is itself information about how firm the ground really is.4

One more strand belongs in a complete bear-and-bull assessment: the quality of disclosure itself, treated as an analytical fact rather than a complaint. Across two earnings calls, management repeatedly declined to break out HHP revenue, declined to quantify the data-center contribution, and declined to detail capex beyond what board disclosures forced into the open.34 A generous reading is that this is ordinary commercial discretion — you do not hand rivals your segment economics, and you do not annualize a lumpy order book you cannot yet forecast. A less generous reading is that a company enjoying a growth-stock re-rating on the strength of a data-center narrative is conspicuously unwilling to put numbers behind that narrative. The tell that tilts toward the generous reading is consistency: management has been uniformly reticent, on good metrics and ambiguous ones alike, rather than trumpeting the flattering figures and hiding the rest. Selective disclosure is a red flag; uniform reticence is merely frustrating. Investors should nonetheless treat the eventual arrival of hard data-center numbers as the moment the thesis becomes truly testable — and the continued absence of them as a reason to keep the position sized for uncertainty.

Stated as plainly as possible — the why win / why not. KOEL wins from here if its high-horsepower product line and new Kagal capacity let it take durable share from Cummins in data centers and large infrastructure gensets, while its legacy Agri and Industrial businesses hold steady and its margin mix genuinely improves. It does not win if the data-center opportunity proves lumpier and more contested than the current pipeline suggests — leaving a company that has committed ₹2,100 crore of capacity and compressed its dividend to chase a high-margin base that stays stubbornly small. Both paths are live. The next several quarters of data will discriminate between them — which is why what you measure matters as much as what you believe.

XII. KPIs and Risk Radar to Track Going Forward

Resist the urge to track everything; three metrics carry the thesis.

First, high-horsepower / Power Generation growth and any hard data-center disclosure. This is the entire basis of the re-rating. The single most important thing to watch is whether management ever converts its qualitative "sight for double digit" language into an actual, reported data-center revenue contribution — and whether HHP growth rates stay high as the base grows. A triple-digit growth rate off a tiny base is easy; sustaining strong growth once HHP is a meaningful chunk of revenue is the real test.4

Second, the core (standalone) net-debt and free-cash-flow trajectory as the ₹2,100 crore capex deploys. The engine business entered this build net cash; the question is whether it stays disciplined as the spending peaks in FY27–FY28.4 Watch standalone free cash flow, not the consolidated debt figure that Arka Fincap's lending book inflates — conflating the two is the most common analytical error on this name.

Third, the dividend payout ratio and broader capital-allocation discipline as a read on whether growth investment is quietly crowding out shareholder returns for longer than the payoff justifies.13

On the risk radar, with mechanisms rather than labels: order lumpiness and customer concentration in a nascent data-center order book means a few large wins or losses can swing the entire growth narrative — the HyperNext order is thrilling precisely because it is big, which is also why its absence in a future quarter would sting. Execution risk on a multi-year build spanning new buildings and equipment at Kagal is real; capacity that slips from a 2027–2028 target reprices the growth runway. Emission-cycle risk recurs whenever the next CPCB norm change disrupts certification timelines, as prior cycles have. Cyclicality in Agri and Industrial — monsoons, rural income, construction and mining capex — can mask or offset HHP gains in any given year. Competitive response from a well-capitalized Cummins defending its data-center turf is close to a certainty, not a tail risk. And valuation risk: after the rally, the multiple leaves limited room for a miss, so even good-but-not-great execution could disappoint.14

These are the dials. Now the lessons the whole saga teaches.

XIII. Playbook: Business & Investing Lessons

Lesson one: in a family-controlled industrial company, an ownership event can matter as much to a stock as any operating decision. The 2023 Kulkarni exit changed no engine, won no order, and improved no margin — yet by creating a real free float and institutional access, it was arguably a precondition for the 2026 re-rating.7 Free float and liquidity are not plumbing details; they are what allow a good operating story to actually express itself in the price.

Lesson two: a single headline order can be real evidence of strategic progress and still be a poor basis for extrapolating a permanent structural shift. The HyperNext win is genuine proof the strategy is working; it is not proof the strategy has won. The discipline — for management and investors alike — is holding those two ideas apart. Markets routinely collapse them, and the gap between "working" and "won" is where both large gains and large disappointments live.1

Lesson three: hiring key talent directly from your most important competitor is a more credible marker of competitive intent than any amount of investor-day rhetoric. Poaching a Cummins India executive to run the chase is a concrete, testable signal that KOEL is serious about the high end.9 But a leading indicator is not a result — it tells you where the company is aiming, not whether it will hit.

Lesson four: rising leverage during a growth-investment phase is not automatically a red flag — but you must read the balance sheet correctly first. In KOEL's case, the scary consolidated debt number largely belongs to a finance subsidiary, while the engine business is net cash.4 The broader principle cuts both ways: growth capex raises the bar for what "success" must look like, and the honest move is to track whether the payoff — segment revenue, margin, share — actually materializes on the timeline management implied.

XIV. Epilogue & What to Watch

Kirloskar Oil Engines enters the second half of 2026 as a company whose story is, fittingly for an engine maker, running hot and cold at once. The near-term checkpoints are concrete: delivery and revenue recognition on the HyperNext order; progress on the ₹700 crore and ₹1,400 crore Kagal expansions, both targeted to come online across 2027–2028; and — the one that would change the conversation most — whether management finally puts a number on the data-center contribution instead of calling it "premature."4

Watch the next several earnings calls for two specific things. First, whether high-horsepower growth rates moderate as the base grows — a natural, healthy deceleration that the market may nonetheless punish if it has priced perpetual triple digits. Second, whether the promised "double-digit" data-center contribution to Power Generation actually shows up in disclosed figures, or remains an aspiration deferred another quarter.4

The final framing is the one worth holding onto. This is less the story of a single transformative deal than of a harder, slower question: whether a century-old family engineering business can out-execute a larger, entrenched rival in the one segment of its industry that actually matters to its future valuation. The company has real assets, a credible plan, a marquee proof point, and a management team that — to its credit — mostly refuses to oversell. It also has a still-small high-end base, a formidable incumbent, and a valuation that has already assumed a good deal of the win. The data so far is, genuinely and simultaneously, promising and thin. Which of those two words wins out is what the next several years will decide.

References

-

Kirloskar Oil Engines share price zooms 20% to hit record high on HyperNext order — Business Standard, 2026-06-22 ↩↩↩↩↩↩

-

Kirloskar Oil Engines shares zoom 19% to hit record high — Business Today, 2026-06-22 ↩↩

-

KOEL Q3 FY26 Investor Call Transcript (PDF) — Kirloskar Oil Engines, 2026-02-12 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

KOEL Q4 FY26 Investor Call Transcript (PDF) — Kirloskar Oil Engines, 2026-05-14 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Cummins India posts FY25 annual revenue at Rs 10,166 crore — Indian Chemical News, 2025 ↩↩↩↩

-

Mahindra Powerol announced as India's No. 1 genset manufacturer in FY25 by Frost & Sullivan — Business Today, 2025-05-27 ↩

-

Kirloskar Oil Engines' promoter entities sell 17.71% stake for Rs 825 cr — Business Standard, 2023-03-08 ↩↩↩

-

BSE sends notice to Kirloskar companies for not disclosing settlement deed — RegStreet Law, 2025 ↩

-

Kirloskar Oil Engines Limited appoints Rahul Sahai as CEO effective January 1, 2025 — MarketScreener, 2024 ↩↩

-

Kirloskar Oil Engines appoints Rahul Kirloskar as Chairman, Atul Kirloskar steps down — Business Upturn, 2026-03 ↩

-

Kirloskar Oil Engines soars on consolidating stake in La-Gajjar Machineries — Business Standard, 2022-09-22 ↩

-

Kirloskar Oil Engines bags Rs 270 crore order from Defence Ministry — Angel One, 2025-04 ↩

-

Kirloskar Oil Engines Ltd — consolidated financials and shareholding trend — Screener.in ↩↩↩↩↩↩↩↩

-

Expanding portfolio may bridge Kirloskar Oil's valuation gap with Cummins India — Business Standard, 2026-06-22 ↩↩↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube