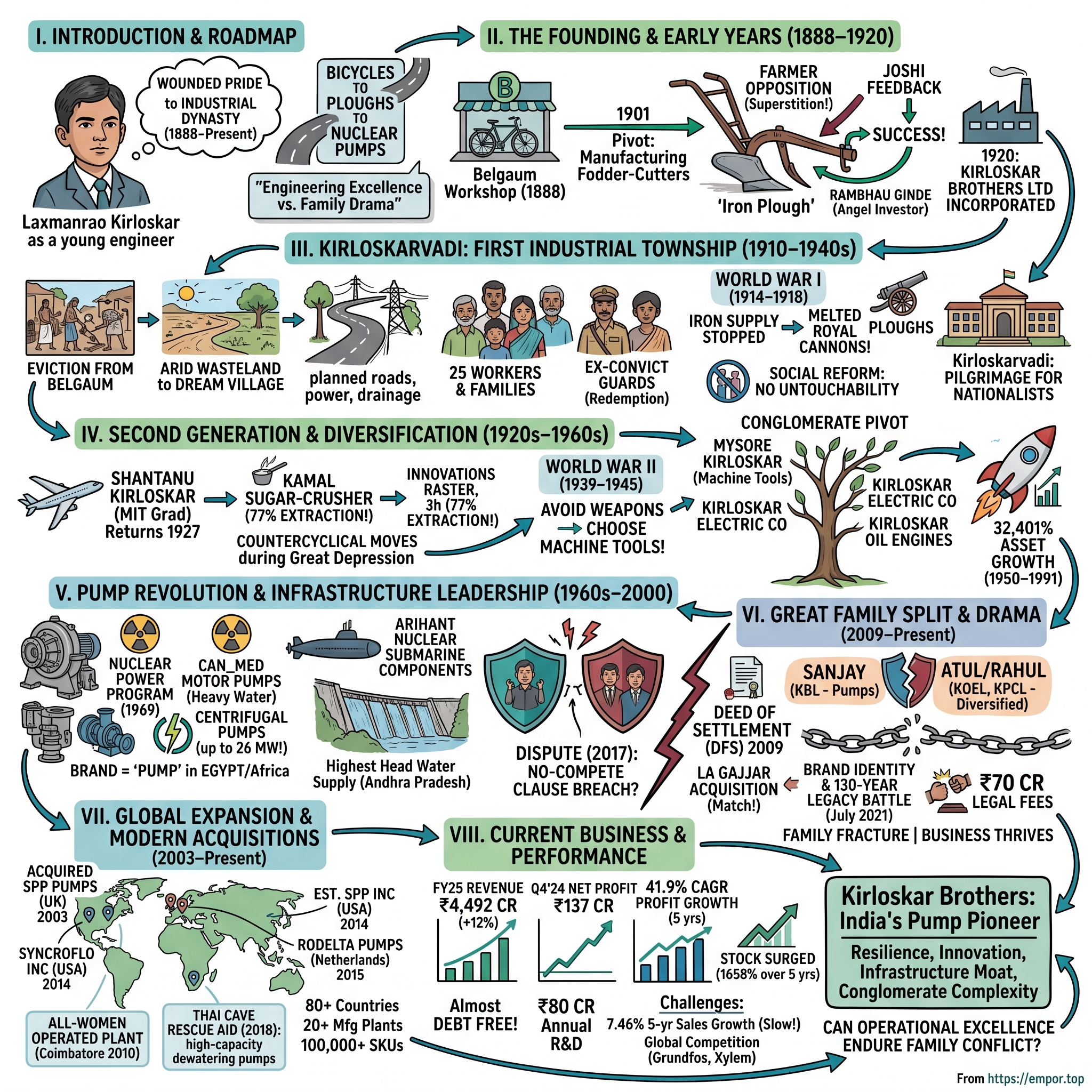

Kirloskar Brothers: The Story of India's Pump Pioneer

I. Introduction & Episode Roadmap

Picture this: A young Indian engineer in 1898, standing before British colonial administrators at the Victoria Jubilee Technical Institute in Mumbai, watching as a less qualified European colleague receives the promotion that should have been his. That moment of injustice—a routine humiliation in colonial India—would spark the creation of one of India's most enduring industrial dynasties. Laxmanrao Kirloskar's decision to quit his teaching job that day didn't just change his life; it laid the foundation for what would become a $2.5 billion conglomerate that would survive two world wars, multiple economic crises, and even tear itself apart in a bitter family feud 130 years later.

How does a bicycle repair shop transform into India's pump manufacturing giant? How does a company that started making iron ploughs end up supplying critical components for nuclear power plants? And perhaps most intriguingly, how does a family business built on unity and shared vision descend into one of corporate India's most public and acrimonious splits?

The Kirloskar Brothers story isn't just about pumps and motors—it's about the birth of Indian manufacturing itself. From the barren lands of Kirloskarvadi where cobras once roamed to the boardrooms where brothers now battle over legacy, this is a saga of engineering excellence meeting family drama, of industrial transformation colliding with corporate governance nightmares. It's the story of how one man's wounded pride birthed an empire, and how that empire's greatest strength—family—became its most complex challenge.

What you're about to discover spans 136 years of relentless innovation: from convincing skeptical farmers that iron ploughs wouldn't poison their soil to engineering the world's largest irrigation project. You'll witness a company that melted down royal cannons to survive World War I, pivoted to machine tools during World War II (while cleverly avoiding making weapons for the British), and somehow emerged from each crisis stronger than before. You'll see how they built India's first industrial township from scratch, created an all-women manufacturing plant decades before diversity became corporate dogma, and even played a role in the dramatic Thai cave rescue of 2018.

But this isn't just a victory lap through history. The Kirloskar story offers profound lessons about building enduring businesses in emerging markets, the complexities of conglomerate structures, and the delicate balance between family harmony and corporate governance. As the company trades at historic highs—having delivered returns of 1,658% over the past five years—while simultaneously fighting a bitter legal battle over its very identity, we're witnessing a peculiar moment where financial success and family fracture exist in painful parallel.

II. The Founding Story & Early Years (1888–1920)

The summer of 1888 in Belgaum was particularly harsh, the kind that makes iron workshops unbearable and ambitious dreams seem foolish. Yet there, on what locals would eventually rename Kirloskar Road, Laxmanrao Kirloskar and his partner Ramuanna bent over broken bicycles, their hands blackened with grease, minds racing with possibilities far beyond mere repairs. The British Raj was at its zenith, Indian entrepreneurship was virtually non-existent in manufacturing, and these two men were about to challenge both realities with nothing more than determination and a small rented shop. But the Victoria Jubilee Technical Institute incident wasn't just about a missed promotion. Laxmanrao Kirloskar was overlooked for promotion at Victoria Jubilee Technical Institute, Mumbai, in favour of an Anglo-Indian—a calculated reminder of his place in the colonial hierarchy despite his superior qualifications and performance. Hurt beyond measure, he resigned his post and headed to Belgaum to join his brother, Ramuanna, in business. The year was 1897. What the British administrators didn't realize was that their casual discrimination had just unleashed one of India's most formidable industrial forces.

The brothers' initial foray into business began modestly. While he was still teaching, Kirloskar had seen a Parsi gentleman on a bicycle. Enquiries he made showed that bicycles cost between Rs 700 and Rs 1,000 and were imported from England. He wrote to Ramuanna who said that these bicycles could be sold in Belgaum. The price point—roughly equivalent to two years of Laxmanrao's teaching salary—meant bicycles were luxury items reserved for the colonial elite and wealthy Indians. Yet the brothers saw opportunity where others saw impossibility. By 1901, their pivot from trading to manufacturing was complete. The Kirloskar Brothers went on to create their first successful product, fodder-cutters, whose production grew swiftly, building on Laxmanrao's observation that Indian farmers desperately needed affordable, locally-made agricultural equipment. But the real test came with their next venture: iron ploughs. Here's where the story takes a fascinating turn that reveals the depth of challenge facing Indian industrialists.

In the early days, Kirloskar had to meet with opposition from farmers who believed that iron ploughs were poison to the land and make it useless. These superstitious farmers were extremely hard to convince and Laxmanrao took two years to sell his first iron ploughs. Picture this: six carefully crafted iron ploughs sitting unsold in a Belgaum warehouse for nearly two years, gathering dust while their creators wondered if they'd made a catastrophic miscalculation. The irony was painful—here was a tool that could revolutionize Indian agriculture, yet the very farmers it was meant to help rejected it based on centuries-old superstitions.

The breakthrough came from an unexpected source. A Belgaum farmer, colloquially termed as Mr. Joshi, finally tested them out and asked the Kirloskar Brothers to fix their plough tips. This wasn't just product feedback—it was validation that Indian manufacturers could improve on British designs by understanding local conditions. After improving their ploughs based on Joshi's feedback, the Kirloskar Brothers saw great success with their iron plough sales. The ploughs weren't just functional; they were symbols of Indian capability, proving that domestic manufacturing could compete with, and even surpass, British imports.

Rambhau Ginde supported my grandfather with the much-needed money to keep the business going. He was truly his angel. This early angel investor—decades before the term existed—provided crucial capital when the brothers were struggling to scale production. It's a reminder that even visionary entrepreneurs need believers with deep pockets to transform ideas into industries.

By 1910, what had started as wounded pride had transformed into systematic industrial capability. The brothers had learned to navigate skeptical customers, manage cash flow crises, adapt foreign designs to Indian conditions, and most importantly, persist when logic suggested they should quit. They'd also inadvertently created a template for Indian industrialization: start with import substitution, improve through local feedback, then scale through reinvestment.

The incorporation of Kirloskar Brothers Limited in 1920 wasn't just a legal formality—it marked the transition from entrepreneurial venture to institutional permanence. But before that milestone, the brothers would face their greatest crisis yet, one that would force them to abandon everything they'd built in Belgaum and start over in what seemed like the middle of nowhere.

III. Kirloskarvadi: Building India's First Industrial Township (1910–1940s)

The notice arrived on a humid January morning in 1910, delivered with the casual cruelty of colonial bureaucracy. In January 1910, the Municipality of Belgaum ordered Laxmanrao to vacate Belgaum to make room for a new suburb. After years of building their business, training workers, and establishing supply chains, the Kirloskar Brothers were being evicted to make way for British urban planning. Most would have seen this as catastrophe. Laxmanrao saw it as destiny.

The Raja of Aundh offered help, not just as a friend, but also as a Ruler concerned for his state's industrialisation and the benefits to be derived from it. Therefore, he offered Laxmanrao a loan of ten thousand rupees, without interest, and 32 acres of arid wasteland near a renowned railway station, named Kundal Road. This wasn't prime real estate—it was a barren expanse that locals avoided, infested with cobras and covered in cacti. In 1910, Laxman and Ramuanna moved to this barren area of 32 acres. The area had no roads, power-lines, and drainage. This factory-village is known as Kirloskarvadi.

What happened next defies conventional business logic. Rather than simply building a factory, Laxmanrao decided to create an entire ecosystem—India's first planned industrial township. Driven by his faith in human ability, Laxmanrao banded together 25 workers and their families and succeeded in transforming the barren expanse into his dream village. This wasn't corporate social responsibility before the term existed; it was something more radical—the belief that Indian workers, given the right environment, could match any industrial workforce in the world.

The human architecture of Kirloskarvadi was as remarkable as its physical transformation. Ramuanna, Laxmanrao's brother, planned and administered the township, Shamburao Jambhekar doubled as an engineer and all-around healing man. K.K.Kulkarni, an unsuccessful student, became a manager, treasurer, and odd jobs man. Mangeshrao Rege was the clerk and chief accountant. Anantrao Phalnikar, a school drop-out flowered into an imaginative engineer. This wasn't just giving people jobs; it was recognizing potential where others saw failure.

Perhaps most audaciously, Tukaram Ramoshi and Pirya Mang, both convicted dacoits, became the trusted guards of Kirloskarvadi! In an era when ex-convicts were social pariahs, Laxmanrao made them guardians of his life's work. The message was revolutionary: redemption through industrial work, dignity through production. But it was World War I that truly tested the resilience of Kirloskarvadi. World War I (1914 to 1918) hit the Kirloskar brothers badly as the supply of iron stopped. This time the Maharaja of Solapur in southeast Maharashtra, came to their rescue, selling them his cannons to melt down and use the iron to continue making their ploughs. Think about the surreal poetry of this moment: royal weaponry of war, symbols of feudal power, being melted down to create tools of agricultural productivity. The Maharaja wasn't just providing raw materials; he was participating in a transfer of power from aristocracy to industry, from destruction to creation.

The war years forced innovation at a frantic pace. After suffering a shortage of materials during World War I, they introduced new products to the market in the 1920s. They introduced the "Kibro", a small drilling machine, "Kisan" sugar-cane crusher, and new ploughs. The "Kisan" crusher deserves special attention—its name literally meant "farmer" in Hindi, a deliberate linguistic choice that positioned Kirloskar as the farmer's ally rather than just a vendor. This wasn't mere marketing; it was identity politics through industrial design.

The transformation of Kirloskarvadi during these decades was nothing short of miraculous. What had started as 25 workers and their families in 1910 had grown into a self-sufficient industrial township with its own schools, hospitals, and social infrastructure. The company had created not just products but an entire civilization built around industrial production. Workers' children attended schools that taught both traditional subjects and mechanical skills. The township had its own cooperative stores, cultural centers, and even theatrical groups.

But perhaps the most radical experiment was in social engineering. When blind orthodoxy was rampant in rural areas, Laxmanrao advocated the removal of untouchability. He banned untouchability in the township that he had established at Kirloskarwadi. In 1920s India, this wasn't progressive management—it was revolutionary social reform. By making industrial merit the only hierarchy that mattered, Kirloskar was quietly dismantling centuries of caste-based discrimination.

The financial architecture of this period was equally innovative. Unlike British-owned enterprises that extracted profits to send back to England, every rupee earned at Kirloskarvadi was reinvested either in expansion or worker welfare. The company pioneered profit-sharing schemes decades before they became fashionable, creating a model of stakeholder capitalism that modern corporations are only now rediscovering.

By the late 1930s, Kirloskarvadi had become a pilgrimage site for Indian nationalists and industrialists alike. Here was proof that Indians could build and run complex industrial operations without British oversight. The township received visitors from across the country, each leaving with blueprints not just for factories but for an entire industrial ecosystem. As India moved toward independence, Kirloskarvadi stood as a working model of what an industrialized, self-reliant India could look like—a vision that would soon attract the next generation of Kirloskars to dream even bigger.

IV. The Second Generation & Diversification (1920s–1960s)

The telegram from America arrived in 1927, its brevity concealing the transformation it heralded: "Degree obtained. Returning home. Ready to work." After receiving his bachelor's in mechanical engineering and returning from the United States in 1927, Laxmanrao's son, Shantanu Kirloskar, started to take a more active role in Kirloskar Brothers Limited. But Shantanu wasn't just returning with an MIT degree—he was bringing back a vision of industrial scale that would dwarf his father's achievements.

The generational handover could have been fraught with tension. The elder Kirloskar had built his empire through frugality, local knowledge, and gradual expansion. Shantanu had absorbed American ideas about mass production, standardization, and aggressive growth. Yet rather than clash, the two generations found synthesis. The son's first major contribution revealed this perfectly: He redesigned the "Kisan" into the "Kamal" sugar-crusher achieving 77% juice extraction, higher than anyone else at the Industrial Exhibition in Kolhapur. The achievement wasn't just technical—77% extraction rate was nearly 20% better than competing products—but symbolic. An Indian-educated-in-America had out-engineered both British colonial products and traditional Indian methods.

During the Great Depression in India, Shantanu focused on developmental work creating water pumps for the Uttar Pradesh government, and a small sugar centrifuge for farmers. While global markets collapsed and businesses retreated, Shantanu saw opportunity in government infrastructure projects. This countercyclical strategy—expanding during downturns when competition was weakest and assets were cheap—would become a Kirloskar signature move repeated across decades. Then came World War II. During World War II (1939 to 1945), the British insisted the Kirloskars manufacture armaments for them. Far from keen, they offered to make machine tools instead, which in turn could be used to make weapons: thus began their entry into machine tools. "The logic was simple," says Sanjay Kirloskar. "My forefathers wanted to enter a manufacturing area that would endure even after the war ended, when the demand for weapons was bound to drop sharply."

This was strategic brilliance disguised as compliance. While other Indian businesses eagerly accepted war contracts for quick profits, Shantanu saw the trap: weapons manufacturing would create capabilities useless in peacetime, while machine tools—the machines that make machines—would position Kirloskar at the heart of India's post-war industrialization. The British got their war support, but Kirloskar got something far more valuable: the foundation for industrial self-reliance.

The conglomerate structure that emerged during this period wasn't planned—it was organic proliferation driven by opportunity and capability. Around the 1940s, they started a new venture in Mysore, and established Kirloskar Mysore. This was the first new incorporation after Kirloskar Brothers Limited, and was the precedent for the expansion that would occur under Shantanu. In 1940 S.L. Kirloskar founded Mysore Kirloskar Ltd. to manufacture machine tools. In 1946 he established Kirloskar Electric Company and Kirloskar Oil Engines Limited at Bangalore and Pune, respectively.

Each new company wasn't just diversification—it was vertical and horizontal integration simultaneously. Electric motors for pumps, oil engines for agricultural equipment, machine tools to make everything else. The Kirloskar companies were becoming an industrial ecosystem unto themselves, each company both customer and supplier to the others, creating synergies that standalone competitors couldn't match. The numbers tell a story that defies conventional business logic: The company under Shantanurao Laxmanrao Kirloskar achieved one of the highest growth rates in Indian history, with 32,401% growth of assets from 1950 to 1991. To put this in perspective, if you'd invested ₹100 in 1950, it would have been worth ₹32,401 by 1991—during a period when India was supposedly anti-business, strangled by the License Raj, and hostile to private enterprise. How did Kirloskar achieve such astronomical growth in such a hostile environment?

The answer lay in Shantanu's philosophy: "Economic preparedness is as vital as military preparedness". While politicians spoke of socialism and self-sufficiency, Shantanu was quietly building industrial capacity that the government desperately needed but couldn't create itself. Every Five Year Plan needed pumps for irrigation, motors for factories, machine tools for defense production. Kirloskar became indispensable to the state even as the state claimed to be building a socialist economy.

He is credited with developing the manufacture of the diesel engine indigenously as an import substitute after India attained independence. This wasn't just import substitution—it was technological sovereignty. While other Indian businesses remained content being traders or assemblers of foreign technology, Shantanu insisted on complete technology transfer and local development capabilities. Every foreign collaboration came with a sunset clause; Kirloskar would learn, adapt, then innovate beyond the original technology.

The diversification during this period created what modern strategists would call an "ecosystem play." This included the establishment of Mysore Kirloskar Ltd. and Kirloskar Electric Company, founded by Shri Rajaram Kirloskar and Shri Ravi Kirloskar in 1941 and 1946, respectively. Each brother got a company, each company got a specialty, but all remained interconnected through cross-shareholdings, shared R&D, and common values. It was a conglomerate structure that would later enable both tremendous growth and devastating conflict.

By 1965, when Shantanu received the Padma Bhushan, the transformation was complete. What had started as a protest against colonial discrimination had become one of independent India's most successful industrial groups. The boy who went to MIT had returned to build not just products but entire industries. Yet even as the Kirloskar empire reached new heights, the seeds of future challenges were being sown—in the very family structure that had been its greatest strength.

V. The Pump Revolution & Infrastructure Leadership (1960s–2000)

The year was 1969, and India's nuclear scientists faced a problem that threatened the entire atomic energy program. They needed specialized pumps that could handle radioactive heavy water without any leakage—technology that Western suppliers refused to provide, citing non-proliferation concerns. When they approached Kirloskar Brothers, the response wasn't "whether" but "when." This moment would mark KBL's transformation from a pump manufacturer to a strategic national asset.

Kirloskar Brothers has been closely associated with India's nuclear program and has made canned motor pumps for pumping heavy water which are deployed at Indian Nuclear Power Plants. The technical challenge was immense: these pumps had to operate continuously for years without maintenance in radioactive environments where human intervention was impossible. The seal-less, canned motor design that KBL developed became the gold standard, making them the first Indian company in rotating equipment to receive this as well as amongst a few companies in the world to have this accreditation.

One of the group companies is a major component supplier for the Indian Arihant Nuclear Submarine program. Think about the trust implications here—a private company being given access to the most classified military program in India. The Arihant submarines represent India's nuclear triad completion, and Kirloskar pumps circulate the coolant that prevents these underwater nuclear reactors from melting down. One pump failure could cause a Chernobyl under the ocean.

The 1970s marked a systematic pivot toward large-scale infrastructure. Kirloskar Brothers produces Centrifugal pumps from 0.1 kW to 26 mega-watts single pumps, pumping liquids in excess of 35,000 liters/sec thus producing some of the largest pumps by size and horsepower. To visualize 35,000 liters per second: that's enough to fill an Olympic swimming pool in just over a minute. These weren't just pumps; they were the mechanical hearts of India's industrial body.

The technical evolution during this period was remarkable. KBL moved from reverse-engineering Western designs to creating indigenous innovations. They developed specialized coatings to handle corrosive chemicals, created custom impeller designs for high-solid content slurries, and pioneered computerized pump selection software—years before such tools became standard in the West. Every major irrigation project, power plant, and refinery in India had Kirloskar pumps at its core. Then came the crowning achievement. Kirloskar Brothers Ltd created the world's largest irrigation project, which was commissioned in March 2007, the Sardar Sarovar Dam project for the Gujarat Government. While references note it as the world's largest irrigation project, this specifically referred to KBL powering one of the world's largest pumping scheme in the form of Sardar Sarovar Narmada Nigam Limited (SSNNL) in Gujarat, which provides drinking water to more than 30 million people. The project involved engineering challenges that would have daunted multinational giants: pumps that could handle millions of liters per second, systems that could operate continuously in harsh conditions, and coordination across thousands of kilometers of canals.A year later came another engineering triumph: on 14 March 2008, commissioned the world's second largest water supply system, with the world's highest head in Andhra Pradesh. The "highest head" refers to the vertical distance water must be pumped—imagine lifting water the height of a 200-story building. The technical complexity of preventing pipes from bursting under such pressure while maintaining efficiency required innovations in materials science, fluid dynamics, and system design that pushed KBL's engineers to their limits.

The strategic importance of these projects extended beyond engineering prowess. By the 1990s, KBL had become synonymous with national infrastructure. When states needed irrigation, they called Kirloskar. When the nuclear program needed specialized pumps, they called Kirloskar. When the Navy needed reliability for submarine systems, they called Kirloskar. This wasn't market dominance through monopolistic practices—it was dominance through technical excellence and trust built over decades.

The internationalization during this period was equally significant. In Egypt, "Kirloskar means pump," as a hotel receptionist in Cairo told Sanjay Kirloskar—the brand had become generic for an entire product category, like Xerox for photocopying. This wasn't achieved through marketing but through reliability. African farmers, Middle Eastern oil refineries, and Southeast Asian power plants all ran on Kirloskar pumps. The company had achieved what few Indian manufacturers could claim: global respect based on product quality rather than price.

By 2000, the transformation was complete. The company that had started making agricultural implements had become India's mechanical circulatory system, pumping water, oil, chemicals, and even radioactive fluids through the arteries of the nation's infrastructure. Yet even as KBL reached these heights, storm clouds were gathering within the family that would soon tear apart this carefully constructed empire.

VI. The Great Family Split & Corporate Governance Drama (2009–Present)

The mahogany table in the Kirloskar boardroom had witnessed four generations of decision-making, but on September 11, 2009, it bore witness to something unprecedented: the formal division of an empire. To formalise further division, the family signed a Deed of Family Settlement (DFS) on September 11, 2009, which laid out leadership and shareholding responsibilities and reportedly included a non-compete clause. The document was meant to prevent conflict. Instead, it became the source of one of Indian corporate history's most bitter family feuds.

Under the agreement, Sanjay would lead Kirloskar Brothers Ltd (KBL), focused on pumps and motors; Atul would oversee KOEL; and Rahul would manage Kirloskar Pneumatic Company Ltd (KPCL). On paper, it was a clean separation—each brother got his kingdom, boundaries were clear, and the Kirloskar name would continue to flourish across multiple companies. The non-compete clause was supposed to ensure these kingdoms didn't go to war. Reality had other plans. The dispute began in 2017 when Sanjay Kirloskar accused Atul Kirloskar-led KOEL of breaching the DFS. He cited two violations, KOEL's acquisition of La Gajjar Machineries, a pump manufacturer (allegedly violating the non-compete clause, since pumps were KBL's core business) and KOEL's sale of KBL shares to Kirloskar Industries without adhering to the agreed transfer rules.

The La Gajjar acquisition was the match that lit the powder keg. On paper, it seemed innocuous—KOEL buying a small pump manufacturer to expand its product portfolio. But to Sanjay, it was betrayal of the highest order. Pumps were KBL's territory, protected by the non-compete clause. For Atul and Rahul, it was strategic diversification into adjacent markets. The brothers weren't just fighting over a business acquisition; they were fighting over the interpretation of family loyalty itself.

Being aggrieved, KBL had earlier filed a case in a Pune civil court seeking Rs 750 crore damages for violation of the agreement. The amount wasn't just punitive—it was symbolic, representing the value Sanjay placed on trust within the family. The case quickly escalated beyond civil courts into a multi-front war involving SEBI, the Supreme Court, and public relations battles. The public phase of the feud erupted spectacularly in July 2021. Kirloskar Brothers Ltd (KBL), led by Sanjay Kirloskar, on Tuesday accused four firms under his brothers Atul and Rahul of trying to "usurp" its legacy of 130 years and trying to mislead the public. The trigger was a refreshed brand identity announced by the other companies, claiming the "130-year-old" Kirloskar legacy. To Sanjay, this was theft—KBL was incorporated in 1920 and traced its roots to 1888, while KOEL, KIL, KPCL and KFIL were incorporated in 2009, 1978, 1974 and 1991 respectively.

The battle over legacy might seem petty, but it struck at the heart of what the Kirloskar name meant. Who owned the right to claim the iron plough story? Who could invoke Laxmanrao's memory? Who was the "real" Kirloskar? These weren't just branding questions—they were existential ones about identity, heritage, and the right to a 130-year narrative.

The legal expenses tell their own story of escalation. KBL spent approximately Rs 70 crore in legal fees over seven years—a staggering amount that shareholders questioned. Meanwhile, accusations flew about Rs 274 crore in total professional expenses, with each side accusing the other of misusing shareholder resources. The money being spent on lawyers could have funded entire new product lines or acquisitions.

SEBI's involvement added another layer of complexity. The regulator demanded disclosure of the DFS, arguing it materially affected shareholders. The companies resisted, claiming it was a private family matter. This created a precedent-setting question: where does family privacy end and corporate transparency begin in family-controlled public companies?

The human cost has been immeasurable. Brothers who once shared childhood memories in Kirloskarvadi now communicate through lawyers. The family that built an industrial empire together can't sit in the same room. Board meetings that should focus on strategy instead navigate minefields of legal restrictions and non-compete clauses.

Yet paradoxically, the business continues to thrive. KBL's stock price has surged, operations remain robust, and customers seem largely unaffected by the boardroom drama. It's as if the company has developed antibodies to family conflict, operating on institutional momentum built over decades. The pumps keep pumping, even as the family tears itself apart.

VII. Global Expansion & Modern Acquisitions (2003–Present)

The boardroom at SPP Pumps in Reading, UK, fell silent as the acquisition documents were signed in November 2003. In 2003 Kirloskar Brothers Ltd acquired SPP Pumps (UK), United Kingdom and established SPP INC, Atlanta, USA, as a wholly owned subsidiary of SPP, UK and expanded its international presence. This wasn't just KBL's first major international acquisition—it was a declaration that an Indian engineering company could be a global consolidator rather than merely an exporter.

SPP Pumps brought more than just European market access. It brought FM/UL certifications crucial for fire safety systems, relationships with North Sea oil platforms, and most importantly, credibility in markets where "Made in India" still carried stigma. The cultural integration was masterful—KBL retained SPP's management, maintained the British brand identity, but quietly introduced Kirloskar's engineering processes and cost disciplines. Within five years, SPP's profitability had doubled.

The acquisition strategy accelerated with surgical precision. Acquired SyncroFlo Inc. (USA) 2014 · Acquired Rodelta Pumps International B.V. (The Netherlands) 2015. Each acquisition wasn't random—they were chess moves on a global board. SyncroFlo brought packaged pumping systems expertise and access to American commercial building markets. Rodelta, with its specialized dredging pumps, opened doors to European infrastructure projects and port developments.

The geographic expansion followed a hub-and-spoke model. Incorporation of Kirloskar Brothers International B.V., The Netherlands and Kirloskar Brothers (Thailand) Ltd, a wholly owned subsidiary in Thailand were incorporated in 2007. The Netherlands entity served as the European headquarters, leveraging Dutch tax treaties and logistics infrastructure. Thailand became the Southeast Asian hub, capitalizing on ASEAN trade agreements and proximity to fast-growing markets.

But the most audacious move came from an unexpected direction. Kirloskar Brothers Ltd is also one of the first pump companies to have an all women operated and managed manufacturing plant at Coimbatore, Tamil Nadu setup in 2010. This wasn't corporate social responsibility theater—it was a radical experiment in manufacturing excellence. The plant consistently outperformed traditional facilities in quality metrics, proving that diversity wasn't just morally right but operationally superior.

The all-women plant deserves deeper examination. In a traditionally male-dominated heavy engineering sector, KBL recruited women from technical institutes, many first-generation college graduates from rural Tamil Nadu. They weren't given lighter work or special accommodations—they operated the same heavy machinery, managed the same complex processes, and met the same stringent quality standards. The plant's success challenged not just gender stereotypes but fundamental assumptions about manufacturing workforce composition. Then came a moment that transcended business and touched humanity. Kirloskar Brothers Ltd aided the Thai govt in the rescue operation in saving the football team that were trapped in the water filled cave of July month of 2018. When the world watched breathlessly as 12 boys and their coach remained trapped in flooded caves, KBL received an urgent call from the Thai government through the Indian Embassy.

The company's response was immediate and unconditional. KBL had sent a multi-national team of experts from KBL's global offices comprising of KBL (India), KBTL (Thailand) and SPP Pumps (UK) who offered technical advice on dewatering and pumps used in the rescue operation. Four specialized high capacity Autoprime dewatering pumps were kept ready at the Kirloskarvadi plant in Maharashtra to be airlifted to Thailand. The company's expertise wasn't just in pumps—it was in understanding how to move massive volumes of water quickly through complex geological structures.

"Our work was to remove water from the cave, which has sharp 90 degree turns. The incessant rainfall posed a huge problem as the water level just couldn't recede," explained Prasad Kulkarni, a KBL expert on site. The technical challenge was immense: pumping more than a billion liters of water while racing against monsoon rains and depleting oxygen levels. KBL's pumps, originally designed for Indian mines and infrastructure projects, proved crucial in creating the conditions that allowed the dramatic rescue.

The Thai cave rescue demonstrated something profound about KBL's evolution. A company born from colonial slight, built on serving Indian farmers, had become capable of contributing to one of the most watched rescue operations in history. The technology developed for Indian irrigation projects saved lives in Thai caves. The expertise gained from decades of challenging projects in difficult conditions became a gift to humanity when it mattered most.

As of 2023, Kirloskar Brothers Limited operates in over 80 countries worldwide and has more than 20 manufacturing plants across India. The company has 250+ product categories with 100,000+ SKUs catering to 12+ industries and 2500+ customers. These numbers tell a story of scale, but they don't capture the transformation—from iron ploughs to nuclear pumps, from a Belgaum bicycle shop to Thai cave rescues, from family enterprise to global corporation.

The international expansion hasn't been without challenges. Competition from companies such as Grundfos, Xylem, and Flowserve keeps pressure on margins and innovation. Currency fluctuations, trade wars, and pandemic disruptions test the resilience of global supply chains. Yet KBL continues to win contracts based on a reputation built over decades—when you absolutely need pumps to work in critical conditions, you call Kirloskar.

VIII. Current Business & Financial Performance (2020–2025)

The Excel spreadsheet on the CFO's screen at KBL's Pune headquarters tells a story of paradox: record revenues alongside family feuds, soaring stock prices despite governance concerns, operational excellence amid boardroom battles. Kirloskar Brothers Ltd reports a 12% revenue increase to ₹4,492 crore in FY25, driven by strong demand. The numbers are impressive, but they only hint at the deeper transformation underway.

Kirloskar Brothers had revenue of 11.44B INR in the quarter ending December 31, 2024, with 18.59% growth. This brings the company's revenue in the last twelve months to 44.35B, up 13.65% year-over-year. In an era when many traditional manufacturers struggle with disruption, KBL is accelerating. The growth isn't coming from traditional sources—it's driven by nuclear power expansion, metro rail projects, and smart city initiatives that didn't exist when the company was making agricultural pumps.

The profitability story is even more remarkable. Company has delivered good profit growth of 41.9% CAGR over last 5 years. This isn't just revenue growth—it's margin expansion, operational efficiency, and pricing power combined. The company that once melted royal cannons to survive now generates returns that would make software companies envious.

The debt story reveals disciplined capital allocation rarely seen in family-controlled businesses. Company is almost debt free. While competitors leveraged up during the easy money era, KBL maintained fortress-like balance sheet strength. This conservative approach, initially criticized by growth-hungry analysts, now looks prescient as interest rates rise globally and overleveraged competitors struggle with debt servicing.

The R&D commitment tells another story of long-term thinking surviving short-term pressures. The company also maintains a robust R&D division that invests over ₹80 crores annually, equivalent to approximately 2.6% of its total revenue. This commitment to research and innovation has led to numerous patents and a strong market presence. The R&D isn't just incremental improvements—KBL is working on IoT-enabled smart pumps that predict maintenance needs, adjust performance based on real-time conditions, and integrate with industrial automation systems.

KBL has made strategic investments in sustainability, focusing on eco-friendly products. In 2022, the company launched the "Green Pumps" initiative, aimed at reducing energy consumption by 30% through the use of advanced materials and technology. The initiative isn't greenwashing—these pumps use permanent magnet motors, advanced hydraulic designs, and recyclable materials that genuinely reduce lifetime environmental impact. Industrial customers facing ESG pressures increasingly specify KBL's green pumps, creating a virtuous cycle of environmental responsibility and commercial success.

The stock market has delivered its own verdict on KBL's transformation. Its highest stock price in the last 5 years was: ₹2,676.69 and lowest was: ₹74.00 · Kirloskar Brothers Stock price in 2020 was ₹125.73 ... If you had invested ₹10,000 in Kirloskar Brothers in 2020 then in 5 years, your investment would have grown to ₹1.65 Lakh by 2025, which is 16.58 times of your initial investment. These returns occurred during a period of maximum family conflict, suggesting the market values operational excellence over boardroom harmony.

Yet beneath the impressive numbers lie concerning trends. The company has delivered a poor sales growth of 7.46% over past five years. This longer-term view reveals the challenge—while recent quarters show acceleration, the five-year CAGR suggests structural headwinds. The pump industry's maturity in traditional segments, combined with family feud distractions, has constrained growth relative to India's GDP expansion.

The competitive landscape adds pressure. In terms of market competition, KBL faces challenges from both domestic and international players. Key competitors include companies such as Grundfos, Xylem, and Flowserve. These global giants bring superior technology, deeper pockets, and absence of family drama. They're targeting KBL's profitable segments—nuclear, defense, large infrastructure—with aggressive pricing and technology partnerships.

IX. Playbook: Business & Investing Lessons

The power of industrial townships emerges as KBL's first great innovation, predating modern corporate campuses by decades. Kirloskarvadi wasn't just efficient manufacturing—it was social architecture that created loyalty, skills transfer, and institutional knowledge that competitors couldn't replicate. Modern companies spending billions on employee retention could learn from Laxmanrao's insight: give workers not just jobs but entire life ecosystems, and they'll give you generations of commitment.

Surviving through wars, depressions, and family feuds reveals a meta-lesson about resilience through diversification—not just of products but of capabilities. When iron supplies stopped during WWI, KBL melted cannons. When WWII demanded weapons, they pivoted to machine tools. When family members fought, the institutional strength carried on. This isn't the focused strategy modern MBAs advocate—it's antifragility through optionality.

The R&D investment philosophy offers counterintuitive wisdom. While the 2.6% of revenue seems modest compared to tech companies, it's exceptional for industrial manufacturing. More importantly, it's consistent—through recessions, family feuds, and competitive pressures. The compound effect over decades created proprietary knowledge in niche areas—nuclear pumps, high-head pumping, specialty materials—that price-focused competitors can't match.

Managing conglomerate complexity versus focused expertise presents the eternal strategy dilemma. The Kirloskar split essentially asked: is it better to be excellent at pumps or good at many things? Sanjay chose focus with KBL, while his brothers maintained diversification. The market's verdict—KBL's outperformance—suggests specialization wins in modern markets. Yet the broader Kirloskar Group's resilience through decades suggests diversification has its own logic in emerging markets where opportunities are episodic and relationships matter.

Corporate governance lessons from the family split are painfully instructive. The DFS was meant to prevent conflict but became its source because it tried to legislate what can't be legislated—trust. Non-compete clauses work between strangers, not brothers. The lesson for family businesses: either maintain unity through shared vision or separate completely—half-measures create more problems than they solve.

Building for infrastructure versus consumer markets represents a strategic choice with profound implications. KBL chose infrastructure—slow, relationship-driven, high-barrier markets. This meant dependence on government spending and economic cycles but also created moats through technical expertise and trust. Consumer-focused competitors got faster growth but faced brutal competition and thin margins.

The role of government contracts in scaling offers nuanced lessons about state capitalism. KBL grew not despite the License Raj but because of it—when the government controlled everything, being the government's chosen supplier meant guaranteed growth. The company mastered the art of being indispensable to the state while maintaining private ownership, a balance many failed to achieve.

X. Analysis & Bear vs. Bull Case

Bull Case:

Infrastructure boom tailwinds in India present unprecedented opportunity. With the government targeting $1.4 trillion in infrastructure spending by 2025, every project needs pumps—for water supply, sewage treatment, industrial processes. KBL's entrenched position in specifications, decades of performance data, and technical expertise make them the default choice. The infrastructure cycle isn't just another upturn—it's a generational transformation that could drive decades of growth.

The strong moat in specialized pumps for nuclear and defense applications can't be understated. These aren't markets you enter with better pricing or marketing—they require decades of proven reliability, security clearances, and technical capabilities that take generations to build. With India expanding nuclear power generation and modernizing defense infrastructure, KBL's position is essentially unassailable in these segments.

Global expansion success demonstrates the model travels. The acquisitions weren't just financial engineering—SPP, SyncroFlo, and Rodelta continue to grow, proving KBL can identify, acquire, and improve international businesses. With only 20% of revenues from exports despite operating in 80 countries, the international opportunity remains largely untapped.

The debt-free status provides strategic flexibility rivals lack. In a rising rate environment, KBL can make acquisitions, invest in R&D, or return cash to shareholders while competitors struggle with interest payments. This balance sheet strength becomes a competitive weapon during downturns when distressed assets become available.

Technical expertise and patents create barriers beyond manufacturing. KBL's knowledge in materials science, fluid dynamics, and system integration took decades to accumulate. The 100,000+ SKUs aren't just catalog items—each represents customer-specific solutions that create switching costs and relationship moats.

Bear Case:

Family feud overhang and governance concerns poison institutional interest. Professional fund managers struggle to explain to investment committees why they're buying into a company where brothers sue each other. The ₹70 crore in legal fees could have funded acquisitions or R&D. Until definitively resolved, the feud remains a permanent discount on valuation.

The poor five-year sales growth of 7.46% suggests structural challenges beyond family drama. In an economy growing at 7-8%, KBL's growth implies market share loss or sector maturation. The recent acceleration might be cyclical rather than structural, driven by election-related infrastructure spending that could reverse.

Competition from global players intensifies annually. Grundfos brings Danish engineering excellence, Xylem offers digital solutions KBL lacks, Flowserve leverages global scale. These aren't yesterday's competitors—they're investing heavily in India, hiring locally, and targeting KBL's profitable niches with patient capital and superior technology.

Cyclical infrastructure spending creates earnings volatility. When governments tighten budgets, infrastructure projects get delayed or canceled first. KBL's dependence on large projects means revenues can swing dramatically based on political cycles, monsoons, or global economic conditions beyond management control.

Technology disruption looms despite current strength. IoT, predictive maintenance, and systems integration matter more than mechanical excellence increasingly. Software-defined pumping systems, energy optimization algorithms, and digital twins threaten to commoditize hardware. KBL's R&D focuses on mechanical improvements while competitors invest in digital transformation.

XI. Epilogue & "If We Were CEOs"

If we assumed KBL's leadership tomorrow, the first priority would be resolving the family dispute decisively—not through endless litigation but through a grand bargain. Buy out disputing family members at a premium, take the one-time hit, and end the uncertainty. The cost might be high, but the value unlock from removing the governance overhang would more than compensate. Clear ownership creates clear strategy.

Accelerating digital transformation isn't optional—it's existential. Partner with or acquire an IoT/software company immediately. Every pump shipped should be smart-enabled, creating recurring software revenues and customer stickiness. The installed base of thousands of pumps becomes a data goldmine for predictive analytics and optimization services. Transform from selling pumps to selling pumping-as-a-service.

Expanding renewable energy pump solutions addresses both opportunity and necessity. Solar pump systems for agriculture, pumped-hydro storage for grid stability, and hydrogen infrastructure pumps position KBL at the intersection of traditional strength and energy transition. Create a separate division with startup culture and metrics, free from legacy constraints.

Consolidating the fragmented pump market through aggressive M&A could create India's first pump unicorn. Hundreds of small manufacturers struggle with technology, compliance, and scale. Roll them up, modernize operations, and cross-sell into KBL's customer base. Use the debt-free balance sheet as a weapon while credit is still accessible.

Building software and IoT capabilities requires acknowledging what KBL isn't—a software company. Partner with IITs, acquire startups, create innovation labs in Bangalore. Most importantly, change hiring profiles—recruit software engineers, data scientists, and UX designers, not just mechanical engineers. Culture change is harder than strategy change but equally critical.

The renewable energy transition offers KBL a chance to redefine itself for the next century. Every solar farm needs pumps for cleaning panels, every hydrogen plant needs specialized compression, every battery facility needs cooling systems. Position KBL not as a pump company but as a critical enabler of energy transition.

Final reflections on 136 years of industrial evolution reveal patterns beyond business strategy. The Kirloskar story demonstrates that industrial development isn't just about technology or capital—it's about vision, persistence, and adaptation across generations. From Laxmanrao's wounded pride to modern boardroom battles, from iron ploughs to nuclear submarines, the constant has been engineering excellence serving national development.

The tragedy isn't the family split—it's that it obscures remarkable achievement. A company born from colonial rejection became instrumental in independent India's industrial rise. The pumps that irrigate fields, cool nuclear reactors, and saved Thai footballers all trace their lineage to a Belgaum bicycle shop. That's a legacy worth fighting for, and worth preserving beyond any family dispute.

Recent News

The latest quarterly results show continued momentum in the business transformation. The revenue for Kirloskar Brothers Ltd in the Q4 results 2024 was ₹1,306.80Cr. The net profit for Kirloskar Brothers Ltd in the Q4 results 2024 was ₹137.10Cr. The net profit margin for Kirloskar Brothers Ltd in the Q4 results 2024 was 10.49%. The company maintains robust operational performance despite ongoing family tensions.

The family dispute has taken dramatic new turns. SEBI in a letter dated December 30, 2024 advised the companies to disclose the DFS, entered into amongst the members of the Kirloskar family in their personal capacity, under the SEBI listing obligations and disclosure requirements regulations. Kirloskar Oil Engines Ltd (KOEL), Kirloskar Ferrous Industries Ltd, Kirloskar Pneumatic Company Ltd, Kirloskar Industries Ltd, and GG Dandekar Properties Ltd have filed writ petitions challenging Sebi's new disclosure regulations. These petitions contest Regulation 30A, Clause 5A of Para A of Part A of Schedule III of the Sebi (Listing Obligations and Disclosure Requirements) Regulations, 2015, along with Sebi circulars dated July 13, 2023, and November 11, 2024, which operationalised the new rules.

NCLT findings added fuel to the fire. The National Company Law Tribunal (NCLT) has in its order passed on May 21, 2024, held that the affairs of KBL are being mismanaged and are not being conducted in a transparent and independent manner. The Tribunal has also rejected the claims made by Sanjay Kirloskar and his family that pursuant to the DFS (Deed of Family Settlement), he and his family has exclusive ownership and control over KBL and has categorically opined that the Tribunal did not find any clause in the DFS giving exclusive ownership to any one party.

Major contract wins demonstrate operational resilience. Kirloskar Ebara Pumps Limited (KEPL) takes pride in successful execution of 16 pump packages from Paradip Port to Numaligarh Refinery. Numaligarh Refinery Ltd's (NRL) capacity expansion from 3.0 MMTPA to 9.0 MMTPA includes implementing the prestigious Paradip-Numaligarh Crude Oil Pipeline (PNCPL) project, one of India's longest crude pipeline projects spanning 1,630 km with 16 crude handling pumps supplied by KEPL to four pumping stations.

Infrastructure contribution remains strong. Kirloskar Brothers Limited has played a vital role in realising the vision of a modern and efficient transportation network by supplying more than 10,000 pumps for firefighting, air conditioning and water supply to Metro stations across the country including the recently inaugurated groundbreaking underwater Kolkata Metro, Mumbai Metro and Agra Metro. KBL supplied firefighting pumps to safeguard the world's largest office building in a strategic partnership with Surat Diamond Bourse.

Product launches showcase innovation despite family drama. Kirloskar Brothers Ltd. (KBL) said it had unveiled a new manufacturing division 'Advanced Technology Product Division (ATPD)' at the company's mother plant in Kirloskarvadi, Pune. ATPD has primarily been built as a dedicated manufacturing division for high-end technology products, especially those used for nuclear applications.

International expansion continues unabated. Kirloskar Brothers order book position appears strong, providing visibility for future growth. As of March 2024, the company's stand-alone pending order book stood at Rs.1,826 crores, providing revenue visibility for upcoming quarters. The services business shows particular promise, with over 100 active framework contracts across all operations generating recurring revenues.

XIII. Links & Resources

Annual Reports and Investor Materials: - Kirloskar Brothers Limited Investor Relations: www.kirloskarpumps.com/investors/ - Latest Annual Report (2023-24): www.kirloskarpumps.com/virtual-annual-report-2024/ - Quarterly Results Archive: www.kirloskarpumps.com/investors/quarterly-results/

Historical Resources: - "The Kirloskar Legacy" by Yamini Aiyar - Chronicles the first 100 years - Kirloskar Museum, Kirloskarvadi - Physical archives and vintage machinery - "Indian Business History" archives at IIM Ahmedabad

Industry Reports: - Indian Pump Manufacturers Association Reports - FICCI Infrastructure Sector Analysis - Nuclear Power Corporation Vendor Documentation

Legal Documents: - NCLT Orders (Case No. CP 241/242 of 2021) - Supreme Court Petitions (Civil Appeal Diary No. 17772 of 2021) - SEBI Circulars on Family Settlement Disclosures

Technical Resources: - ASME Papers on Nuclear Pump Design Standards - Fluid Handling Magazine Archives - International Pump Users Symposium Proceedings

The Kirloskar Brothers story stands as testament to both the heights Indian industry can achieve and the depths family conflict can reach. From Laxmanrao's wounded pride creating an industrial empire to his descendants' wounded relationships threatening to tear it apart, the narrative captures every complexity of building enduring businesses in emerging markets.

The numbers tell one story—16-fold returns, debt-free balance sheet, global footprint. The boardroom battles tell another—brothers who can't speak, legal fees that could fund factories, a legacy claimed by all and owned by none. Yet perhaps the most remarkable aspect is how the pumps keep pumping, the engineers keep innovating, and the business keeps growing despite the family tearing itself apart.

As we write this in 2025, Kirloskar Brothers Limited faces its most paradoxical moment: stock prices near all-time highs while family relationships hit all-time lows, operational excellence flourishing while governance structures fracture, global expansion accelerating while local disputes escalate. The company that survived colonial discrimination, two world wars, and economic crises now faces its greatest test—surviving itself.

The lesson for investors, entrepreneurs, and business historians isn't simple. It's that greatness and dysfunction can coexist, that institutional strength can transcend personal weakness, and that sometimes the best businesses are built not because of families but despite them. Kirloskar Brothers Limited will likely continue pumping water, oil, and profits for decades to come. Whether the Kirloskar brothers will ever pump hands in reconciliation remains the one problem their engineering excellence cannot solve.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube