Kiri Industries: The Great DyStar Gambit

I. Introduction & Episode Roadmap

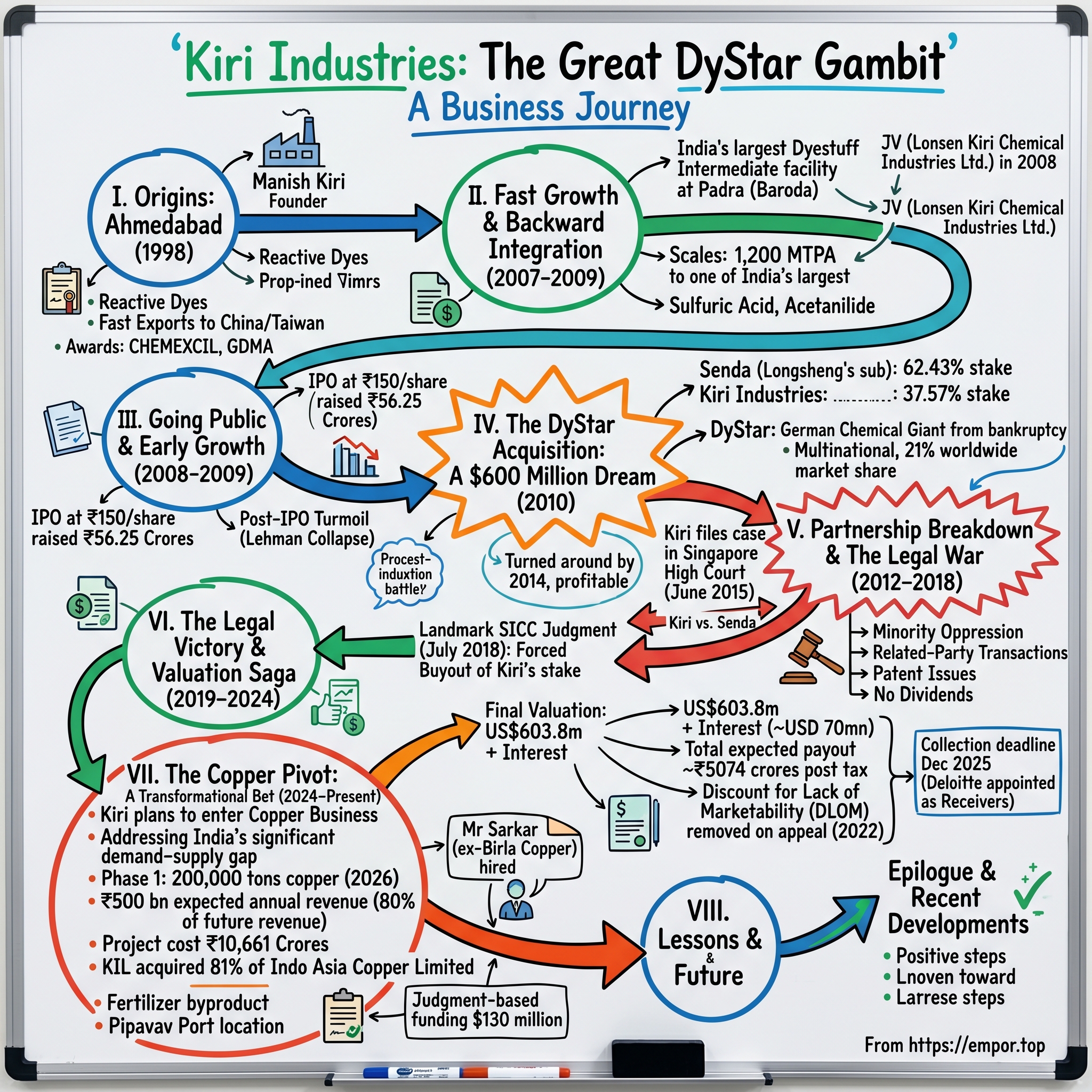

Picture this: A chemical dyes company from Gujarat with a market capitalization of around ₹3,400 crore has a legal claim worth over ₹5,000 crore. It sounds like a financial impossibility, yet this is precisely the situation facing Kiri Industries Limited (KIL), one of the largest manufacturer and exporter of wide range of Dyes, Intermediates and Chemicals from India, a winner of several CHEMEXCIL and GDMA performance awards.

The story we're about to unpack isn't your typical Indian corporate saga. It's a tale that spans continents, involves decade-long legal battles in Singapore's most sophisticated commercial courts, and culminates in one of the most audacious business pivots in recent memory—from textile dyes to copper smelting. This is the story of how a family business from Ahmedabad ended up in the center of a global corporate drama worth hundreds of millions of dollars, and how it's now betting its entire future on India's infrastructure supercycle.

What makes this particularly fascinating is the asymmetry at play here. Kiri Industries, a company that trades at an EV of 2700Cr is therefore expecting to receive a cash inflow of 5000 Cr by June next year. When the market values a company at less than the cash it's about to receive, you know there's either extreme skepticism or a remarkable opportunity—possibly both.

Over the next several hours, we'll trace Kiri's journey from its humble beginnings in 1998 to its current crossroads. We'll examine how a minority stake acquisition in 2010 turned into a legal quagmire, why Singapore's courts matter more than Indian ones in this case, and what a copper plant in Gujarat has to do with any of this. Along the way, we'll extract lessons about cross-border joint ventures, the value of patient capital, and what happens when David takes on Goliath in international arbitration.

Buckle up. This isn't just a business story—it's a masterclass in special situations investing, wrapped in a cautionary tale about partnership risk, delivered through the lens of one of the most unusual corporate transformations you'll encounter.

II. Origins: From Family Business to Dyes Empire (1998–2007)

The monsoon of 1998 brought more than rain to Ahmedabad. It was the year Manish Kiri started his family business, becoming the founder Promoter and Chairman & Managing Director of the Company, holding a degree in Bachelors of Engineering (Electronics & Communication) from Gujarat University and also a Masters Degree in Business Management. Like many Gujarat entrepreneurs before him, Kiri didn't start with grand ambitions of global domination. He started with a simple manufacturing unit in Vatva.

The company came into being in 1998 with the setting up of Dyes manufacturing unit at Vatva, Ahmedabad, incorporated as Kiri Dyes and Chemicals Private Limited with an initial capacity of 1200 MTPA. The choice of reactive dyes wasn't accidental—these synthetic organic compounds that bond chemically with cotton fibers represented the cutting edge of textile chemistry. While competitors were selling commodity products, Kiri focused on the science.

The early wins came fast. The Company started to export the products to China and Taiwan from the year 1999. Think about that for a moment—an Indian chemical company successfully exporting to China at the turn of the millennium, when the narrative was entirely about Chinese products flooding Indian markets. This contrarian move would define Kiri's trajectory.

Recognition followed performance. The company was awarded by CHEMEXCIL for outstanding export performance for the year 1999-2000 and again in the year 1998-1999. These weren't participation trophies—CHEMEXCIL (Chemical Export Promotion Council) awards were the industry's gold standard, given to companies demonstrating exceptional export growth and quality standards.

The company was given Two star Export house rating in the year 2004, a designation that opened doors to preferential treatment in government schemes and enhanced credibility with international buyers. By the mid-2000s, Kiri wasn't just surviving; it was building the foundation for something much larger.

The real transformation began in 2007. In 2007, KIL embarked upon two stage backward integration by setting up India's largest Dyestuff intermediate manufacturing facility and largest basic chemicals facility at Padra (Baroda, Gujarat). This wasn't incremental expansion—it was a complete reimagining of what an Indian dyes company could be.

Backward integration in the chemical industry is like owning the entire supply chain from farm to table in the food business. Instead of buying expensive intermediates from other suppliers (often importing them), Kiri would make them in-house. The Padra facility wasn't just large; it was strategically located near the Dahej chemical zone, providing access to raw materials, ports, and a skilled workforce familiar with chemical manufacturing.

He embarked upon a plan of fast growth and spearheaded the company's growth by establishing a large economy of scale manufacturing facilities and backward integration into manufacturing of intermediates and basic chemicals, being the force behind the formation of Company's JV (Lonsen Kiri Chemical Industries Ltd.), in 2008.

The numbers tell the story of ambition meeting execution. From a 1,200 MTPA initial capacity to becoming one of India's largest integrated dyes manufacturers in less than a decade. Subsequently the management in 2005 and 2007 started backward integration into Vinyl Sulphone and H-acid—the building blocks of reactive dyes that most Indian companies were content to import.

What's remarkable about this phase is how methodical it was. Each expansion built on the previous one. Each backward integration step reduced dependency on imports and improved margins. Each award and recognition opened new markets. This wasn't the story of a company stumbling into success—it was engineered growth, calculated and deliberate.

By 2007, Kiri had transformed from a small Vatva unit into a vertically integrated chemical conglomerate with facilities across Gujarat. The company that started with a modest vision of making dyes was now thinking bigger—much bigger. The stage was set for the next act: going public and going global.

The reactive dyes market Kiri had chosen to focus on was experiencing a fundamental shift. Environmental regulations in China were tightening, creating opportunities for Indian manufacturers. Global fashion brands were demanding more sustainable and traceable supply chains. Kiri, with its integrated facilities and quality certifications, was perfectly positioned to capture this shift.

But Manish Kiri understood something crucial: in the commodity chemicals business, scale is survival. The backward integration wasn't just about margins—it was about building a moat. When you control your raw materials, you control your destiny. This philosophy would soon be tested on a much larger stage.

III. Going Public & Early Growth (2008–2009)

March 25, 2008, should have been a day of celebration. The shares got listed on BSE, NSE on April 22, 2008, after the IPO opened on March 25, 2008 and closed on April 2, 2008, priced at ₹150 per share. For a company that began just a decade earlier in a small manufacturing unit, this was the pinnacle of achievement—or so it seemed.

The timing, in hindsight, was almost tragically perfect. The IPO raised ₹56.25 crores through the allotment of 3750053 equity shares of Rs. 10/- each at an issue price of Rs. 150/- per equity share (including premium of Rs. 140/- per equity share), with the company raising Rs. 7069.06 Lakhs comprising Rs. 5625 Lakhs through IPO and Rs. 1444.06 lakhs through Pre IPO placement. Within months, Lehman Brothers would collapse, and the global financial system would teeter on the brink. But Kiri, flush with IPO proceeds and undeterred by global headwinds, was about to make moves that would define its next decade.

The post-IPO period saw Kiri double down on expansion rather than retreat. While global markets were in turmoil, the company was executing on ambitious plans that seemed almost reckless in the context of 2008-2009. The Joint Venture with Well Prospering Limited, a Hong Kong based subsidiary Company of Zhejiang Longsheng Group Co. Ltd. of China, was formed during the year 2009 as Lonsen Kiri Chemical Industries Ltd, with a plant to manufacture Dyestuff with the installed capacity of 50000 TPA envisaged, opening a plant with installed capacity of 36000 TPA of Reactive Dyes in Gujarat on 19th July, 2009.

This partnership with Longsheng wasn't just another joint venture—it was a meeting of titans. Longsheng was already a giant in the global dyes industry, and for them to partner with a relatively small Indian player was significant. The 36,000 TPA facility represented one of the largest single reactive dyes plants in India at the time.

The strategic logic was compelling. Longsheng brought global market access and technical expertise. Kiri brought local manufacturing capabilities, knowledge of Indian markets, and most importantly, the infrastructure from its backward integration. Together, they could serve both Chinese and Indian markets while competing globally. It was, on paper, the perfect marriage.

But Kiri wasn't done. During the year 2010, the Company commenced commercial production of its backward integration plant for manufacturing of basic chemicals i.e. Sulphuric Acid, Oleum and Chloro Sulphonic Acid with a combined capacity of 500 MT/day. These aren't glamorous products—they're the industrial workhorses that make modern chemistry possible. Sulphuric acid is often called the "king of chemicals" because of its importance in manufacturing processes.

The scale of ambition here deserves emphasis. A 500 MT/day capacity for basic chemicals meant Kiri was now playing in the big leagues. This wasn't just about serving internal requirements anymore—the company was becoming a significant supplier of basic chemicals to other industries. It commenced 3.5 MW co-generation steam based power plant at Village Dudhwada, Vadodara, and commercial production of Acetanilide, with installed capacity of 12000 MTPA at Village Dudhwada, District Vadodara, which is used in manufacturing of Vinyl Sulphone.

The integration was becoming almost fractal in its complexity. Power generation to reduce energy costs. Acetanilide production to feed into Vinyl Sulphone manufacturing. Vinyl Sulphone to produce reactive dyes. Reactive dyes to serve global textile markets. Each piece connected to the next, creating a self-reinforcing ecosystem.

What's particularly impressive about this period is the financial discipline. Despite the aggressive expansion, the company maintained its focus on profitability and cash generation. The backward integration wasn't just about control—it was about margins. By producing their own intermediates and basic chemicals, Kiri could maintain profitability even when dyes prices were under pressure.

The relationship with Longsheng was deepening too. What started as a joint venture for manufacturing was evolving into something more strategic. Both companies were beginning to see opportunities beyond just the Indian plant. There were whispers in the industry about distressed assets in Europe—companies that had dominated the global dyes industry for decades but were now struggling in the post-2008 environment.

By late 2009, Kiri had transformed from a newly public company into a fully integrated chemical conglomerate. The company now had modern manufacturing facilities, a strong balance sheet, a powerful Chinese partner, and most importantly, ambition that extended far beyond Indian shores. The foundation was set for what would become the defining moment in Kiri's history—a moment that would either catapult them into the global elite or entangle them in a web of litigation that would last over a decade.

The stage was set for the DyStar acquisition, a move so audacious that even today, market participants struggle to fully comprehend its implications.

IV. The DyStar Acquisition: A $600 Million Dream (2010)

February 4, 2010, marked a watershed moment not just for Kiri, but for the entire global dyes industry. On 4th February, 2010, Kiri Industries Limited (KIL) acquired DyStar Group, through SPV Kiri Holding Singapore Pvt Ltd, considered to be a historical development in the global Dyes industry. But to understand why this acquisition was so significant, we need to understand what DyStar represented.

DyStar wasn't just another dyes company. The company was founded in 1995 as a joint venture between Hoechst AG and Bayer Textile Dyes. In 2000, the textile dyes business from BASF was also integrated into it. Think about that—three of Germany's chemical giants had combined their textile dyes businesses into this entity. DyStar was, quite literally, the repository of over a century of German chemical engineering excellence.

By 2009, however, DyStar was in trouble. The DyStar group was a major player in the international dye industry and was based in Germany. It experienced financial difficulties in 2009 and insolvency administrators were appointed. The global financial crisis had devastated demand, and the company's high-cost European manufacturing base was struggling to compete with Asian producers.

Enter Kiri and Longsheng. In March 2010, Kiri industries (37.57% stake) formed a JV with China-based Longsheng group (62.43% stake) and acquired German-based DyStar from bankruptcy proceedings. The JV was based out of Singapore and raised about 100 million euro (Debt to equity of 65:35) to fund the acquisition. For Kiri, this represented an investment of roughly 100 crores—a massive bet for a company that had just gone public two years earlier.

The strategic rationale was compelling. DyStar, a multinational German Company having worldwide market share of around 21%, would instantly transform Kiri from an Indian player into a global force. DyStar brought with it cutting-edge technology, prestigious customers, global manufacturing facilities, and most importantly, a portfolio of patents and intellectual property that had taken decades to develop.

The structure of the deal reveals much about the dynamics at play. Kiri held 37.57% while Senda (Longsheng's subsidiary) held 62.43%. On the surface, this made sense—Longsheng was the larger company with deeper pockets. But this minority position would later become the source of Kiri's greatest challenge and, paradoxically, its potential windfall.

The early years validated the acquisition thesis brilliantly. DyStar struggled until 2013. But since then it was turned around successfully and now consistently generates profit from 2014. In FY'2016, DyStar reported around 450 Cr of profits and Kiri's 37.37% stake will give 170 cr. The turnaround was remarkable—from insolvency to profitability in just four years.

What drove this transformation? First, the Asian partners brought crucial cost advantages. Manufacturing could be shifted to lower-cost facilities in Asia while maintaining DyStar's premium brand and customer relationships. Second, the booming textile industry in Asia provided ready markets for DyStar's products. Third, environmental regulations in China were creating opportunities for companies with cleaner production technologies—exactly what DyStar offered.

The acquisition of Dystar, a multinational German Company having worldwide market share of around 21% has changed the dynamics, making KIL now a Global Conglomerate and a total textile solution provider. Kiri was no longer just selling dyes; it was providing complete color solutions to global fashion brands, automotive manufacturers, and technical textile producers.

The numbers were staggering. DyStar operated manufacturing facilities across the globe, employed thousands of people, and served customers in over 50 countries. For a company that had started just 12 years earlier in a small unit in Vatva, this was a quantum leap. Kiri's management, led by Manish Kiri, was now sitting in board meetings with executives who had run some of the world's largest chemical companies.

But beneath the surface, tensions were brewing. Being minority shareholder, Kiri could not able to access the cash generated or intellectual property rights. Longsheng group also rejected IPO listing of DyStar. Since, JV entity was registered in Singapore, Kiri filed litigation to enforce the minority rights. Either Majority shareholder should buyout the minority shareholder or the company has to be liquidated and assets distributed between them. Through this Kiri can realize the market value of its minority stake in DyStar.

The seeds of the future conflict were embedded in the structure itself. Kiri had put up roughly 37.57% of the equity but had no real control over DyStar's operations, dividend policy, or strategic direction. As DyStar became increasingly profitable, this lack of control became increasingly frustrating. The German company that Kiri had helped rescue from bankruptcy was now generating hundreds of crores in profits, but Kiri couldn't access its share of the cash.

What started as a dream partnership was slowly morphing into a nightmare of corporate governance. The very success of the turnaround was becoming the source of conflict. Longsheng, through its majority control, could direct DyStar's business toward its own interests. Kiri, despite its substantial investment and contribution to the turnaround, was effectively a silent partner in a increasingly valuable asset.

By 2013, it was clear that the DyStar acquisition had been both Kiri's greatest triumph and its greatest challenge. The company had achieved its goal of becoming a global player, but at what cost? The stage was set for one of the most complex and protracted legal battles in the history of India-China business relations.

V. Partnership Breakdown & The Legal War (2012–2018)

The breakdown didn't happen overnight. Like many partnership failures, it began with small disagreements that metastasized into fundamental conflicts about control, value, and fairness. By 2015, what had started as strategic differences had evolved into full-scale corporate warfare.

June 2015 - Kiri files a case in the High Court of Singapore against Longsheng and Dystar, in an effort to enforce it's rights as a minority shareholder arising from matters relating to governance and intellectual property rights. The choice of Singapore wasn't accidental—the joint venture was structured through Singapore, giving the island nation's courts jurisdiction over the dispute.

The allegations Kiri made were explosive. They painted a picture of systematic oppression designed to extract value from DyStar for Longsheng's benefit while freezing out the minority shareholder. The litany of complaints included related-party transactions where DyStar was allegedly forced to buy raw materials from Longsheng at above-market prices, patent assignments where DyStar's valuable intellectual property was transferred to Longsheng entities, and a deliberate suppression of dividends despite DyStar's strong profitability.

But Longsheng had its own narrative. Evidence showing DyStar would have been commercially justified concluding in 2013 that Kiri was unreliable supplier, with DyStar's preference of Lonsen Kiri over Kiri being result of Kiri's supply reliability issues. From Longsheng's perspective, they were the ones who had provided the majority of the capital, taken the bigger risk, and driven the turnaround. Kiri was simply an opportunistic minority shareholder trying to extract value it hadn't earned.

The Singapore International Commercial Court (SICC) became the arena for this corporate gladiatorial contest. This court case has been hailed as a landmark judgement in Singapore due to its complexity, and atypically long timeline. The final judgement (which I spent hours skimming through), is hundreds of pages long.

What made this case particularly complex was the international nature of the dispute. Evidence had to be gathered from multiple jurisdictions. Witnesses included German executives, Chinese directors, Indian managers, and Singaporean administrators. The court had to untangle a web of inter-company transactions spanning continents and involving dozens of subsidiaries.

January 2018 - After 3 long years, recording of all evidence is finally completed. Three years just to gather and present evidence—this gives you a sense of the scale and complexity of the litigation. Both sides had deployed armies of lawyers, forensic accountants, and industry experts. The legal fees alone were running into tens of millions of dollars.

Then came the landmark judgment. The Singapore International Commercial Court ("the Court") has released its judgment in Suit Nos. 3 and 4 of 2017 on 3rd July, 2018. The Court has found that Senda committed numerous acts of minority oppression against KIL.

The court's findings were devastating for Senda. In 2017, the suit was transferred to the SICC due to its international elements and in 2018, the court issued its judgement for the case, stating they accepted most of the instances of commercial unfairness raised by Kiri. The SICC found evidence of a pattern of behavior designed to benefit the majority shareholder at the expense of the minority.

The remedy was equally dramatic. The court was pleased to direct Senda to purchase KIL's 37.57% shareholding in DyStar, based on a valuation to be assessed. This wasn't just a slap on the wrist—it was a forced buyout, the corporate equivalent of a divorce decree.

But the court went further. The Court also directed that KIL's shareholding be valued as at the date of this judgment and shall take into consideration and incorporate all of the following: (i) the Special Incentive Payment made by DyStar to Ruan, challenged by KIL; (ii) the Longsheng Fees for year 2015 and 2016 challenged by KIL; (iii) the licence fees that Longsheng has obtained from the Patent, which according to KIL had a huge value; (iv) the benefit that Longsheng has obtained from its commercial use of the Patent for its own production; and (v) the loss to DyStar, directly or by impact through subsidiaries, from the Related Party Loans, the Cash-pooling Agreement.

These weren't just technical accounting adjustments. Each represented a finding that Senda had extracted value from DyStar improperly. The patent issue was particularly significant—intellectual property developed by DyStar had allegedly been used by Longsheng for its own benefit without proper compensation.

The court was pleased to dismiss all the claims and counterclaims against Mr. Pravin Kiri, Mr. Manish Kiri, Mr. Amitava Mukherjee (KIL's nominated director on DyStar Board) and Kiri International Mauritius Pvt. Ltd. ("KIPL"). This personal vindication was crucial—the Kiri family and their nominated directors had been accused of various improprieties, and the court's dismissal of these claims was a complete exoneration.

The 2018 judgment was a stunning victory for Kiri, but it was also just the beginning of a new phase of the battle. Senda would appeal, arguing that the SICC had overreached, that the findings of oppression were not supported by evidence, and that the remedy of a forced buyout was inappropriate.

Meanwhile, the business implications were profound. DyStar continued to operate and generate profits, but now it was effectively a company in limbo—profitable but paralyzed, valuable but contested. The very success that should have been celebrated was now just another point of contention in the valuation battle to come.

What the 2018 judgment really represented was a vindication of minority shareholder rights in cross-border joint ventures. The SICC had sent a clear message: majority control doesn't mean carte blanche to exploit minority shareholders. Even in complex international structures, courts would protect the legitimate interests of minority investors.

For Kiri, this was more than just a legal victory—it was an existential validation. The company had bet everything on being right, had spent millions on legal fees, and had endured years of uncertainty. Now, the only question was: how much was their stake actually worth?

VI. The Valuation Saga & Legal Marathon (2019–2024)

If the liability phase was complex, the valuation phase was byzantine. How do you value a 37.57% stake in a company when the majority shareholder has allegedly suppressed its value? What discounts, if any, should apply? And how do you account for benefits improperly extracted? These questions would consume the next five years.

The first major development came with the valuation judgment. Based on the above, we adjudge the final valuation of Kiri's shares to be US$481.6m for the purposes of the buy-out order. This initial valuation, delivered on June 21, 2021, adjudged the value of Kiri's shareholding to be US$481.6m, represented a massive win for Kiri—but it wasn't the end of the story.

The valuation process itself was extraordinary in its thoroughness. We found DyStar's equity value as at the valuation date to be US$1,636m, subject to the nine adjustments. Think about that—DyStar, the company acquired from bankruptcy for roughly 100 million euros in 2010, was now valued at over $1.6 billion. This represented a spectacular return on investment, even accounting for the years of litigation.

But then came the battle over discounts. The SICC held that a DLOM (Discount for Lack of Marketability) of 19% should apply to the valuation of Kiri's shareholding in DyStar. The SICC was of the opinion that a DLOM should apply as a starting point where a private company was being valued unless exceptional circumstances could be shown.

This 19% discount was crushing—it would reduce Kiri's payout by nearly $100 million. The rationale was that shares in a private company are inherently less valuable than public shares because they can't be easily sold. But Kiri argued this was absurd in the context of a forced buyout resulting from oppression. Why should the oppressor benefit from a discount?

The appeals flew thick and fast. Both sides challenged various aspects of the valuation. Then came a crucial victory for Kiri. On 6 July 2022, the Singapore Court of Appeal in Kiri Industries Ltd v Senda International Capital Ltd & Anor allowed Kiri's appeal that a DLOM should not apply to the valuation of Kiri's shareholding. This is the first time the Singapore court has clarified and authoritatively decided the law on the applicability of a DLOM where a minority shareholder's shares are valued pursuant to a buyout order made in a minority oppression action. As the Court of Appeal observed in the judgment, there was "a lack of a clear path of principle on the existing state of the authorities" in this area of law.

This was more than just a win for Kiri—it was a landmark decision that would influence minority oppression cases globally. The Court of Appeal agreed with Kiri's submissions that the reprehensible conduct on the part of Senda, and the fact that Senda would gain total control of DyStar as a result of the buyout order, should not enable Senda to gain the benefit of a discount. The effect of the Court of Appeal's judgment is that the value of Kiri's shareholding in DyStar would increase by at least 19%.

There was also the matter of interest. Kiri had made extensive submissions on the under disclosure by Senda on the quantities of products that Longsheng had produced using the O288 Patent. However, in calculating the notional licence fee, the SICC had relied on figures put forth by Senda because there was no evidence on exactly how severe the under-disclosure by Senda was. The Court of Appeal considered that this issue could not be disposed of simply on the application of a burden of proof, where that burden operated to the disadvantage of Kiri because of the apparent under-disclosure of Senda.

By 2023, the final number was crystallizing. The SICC increased Kiri's share valuation to USD 603.8 million from an earlier judgement of USD 481.6 million, acknowledging the extent of oppression suffered by the Indian dye company as a result of Senda International Capital's actions. This represented an increase of over $120 million from the initial valuation—a testament to the value of persistence in litigation.

But Senda still wasn't paying. Despite the court orders, despite the appeals being dismissed, the money wasn't flowing to Kiri. This led to the next phase: enforcement. The court appointed Matthew Stuart Becker, Lim Loo Khoon and Tan Wei Cheong of Deloitte & Touche LLP as Receivers to conduct the sale and take all necessary steps in this regard before 31st December 2025. DyStar and Senda were directed by the court to cooperate and render all assistance that the Receivers may require for completing the sale. Earlier, the same court had ordered Senda International to buy out the minority shareholding of 37.57% held by Kiri Industries in DyStar at the price of US$ 603.8 million but Senda International could not materialize it.

The appointment of receivers was a nuclear option. The court was essentially saying: if you won't buy out Kiri voluntarily, we'll sell the entire company and give Kiri its share. This finally brought Senda to the table.

Singapore, 5 June 2025 – DyStar announced that Zhejiang Longsheng Group Co., Ltd has entered into a Share Purchase Agreement to acquire 37.57% of issued shares in DyStar Global Holdings (Singapore) Pte. Ltd., previously held by Kiri Industries Limited. As controlling shareholder with 62.43% of DyStar, Zhejiang Longsheng Group's strategic acquisition of the outstanding shares will result in DyStar becoming a wholly owned subsidiary. This transaction resolves the long-standing litigation with Kiri Industries, thereby avoiding a full sale of DyStar. The total consideration is valued at USD 696.5478 million, subject to adjustments on or after the closing date.

The final number—$696.5 million—was even higher than the court-ordered amount, likely including interest and other adjustments. In 2025, Supreme Court of Singapore awarded Interest of 5.33% on USD 603.80 Mn from September 2023 till payment (USD 70mn roughly). Also legal fees would be reimbursed to the tune of USD 10mn. Total payout post tax is expected to be ~5074 crores.

The timeline for receipt became clearer. Non-binding offers are expected by November 2024, with binding offers due by January 2025. The sale is projected to conclude by March-June 2025. After nearly a decade of litigation, Kiri was finally going to see the money.

But what made this saga truly remarkable wasn't just the amount—it was what it represented. A relatively small Indian company had taken on a Chinese giant in Singaporean courts and won. They had persevered through years of litigation, millions in legal fees, and constant uncertainty. The DyStar case would go down in history as one of the most significant minority oppression victories ever.

The implications extended far beyond Kiri. The case established important precedents for minority shareholder rights in cross-border joint ventures. It showed that patient capital and determination could prevail against seemingly insurmountable odds. And it demonstrated that even in complex international disputes, justice—albeit slow and expensive—was possible.

VII. The Copper Pivot: From Dyes to Metals (2024–Present)

While the legal battles raged in Singapore, something extraordinary was brewing in the boardrooms of Ahmedabad. Kiri's management, led by Manish Kiri, was contemplating a transformation so radical that it would make the DyStar acquisition look conservative by comparison. They were planning to enter the copper business.

The logic, when you first hear it, seems almost absurd. What does a dyes company know about smelting copper? But dig deeper, and a compelling narrative emerges. India imports nearly 95% of its copper requirements. The country's infrastructure boom, electric vehicle transition, and renewable energy push are all copper-intensive. Kiri plans to address India's significant demand-supply gap in copper, which is expected to triple by 2030. The company aims to reduce reliance on imports while capitalising on domestic demand.

The scale of ambition is breathtaking. The first phase of the copper project, set to begin operations by 2026, will produce 200,000 tons of copper, expanding to 500,000 tons by 2027. This project, with an estimated cost of Rs 80 bn, is expected to generate over Rs 500 bn in annual revenue once fully operational, contributing to more than 80% of the company's future revenue.

Let's put those numbers in perspective. ₹500 billion in annual revenue. Kiri's current annual revenue is less than ₹1,000 crore. They're talking about a 50x increase in top line. This isn't expansion; it's metamorphosis.

The project structure reveals careful planning. The new project, estimated at INR 10,661.00 crores, is already underway with a 36-month completion target. KIL has infused INR 1,036.00 crores as equity, with the remaining following a 70:30 debt-equity ratio. The 70:30 debt-equity ratio is aggressive but not reckless, especially considering the cash infusion from DyStar.

To lead this transformation, Kiri brought in serious talent. The company would be led by Mr Sarkar who is ex Birla Copper and who used to sit in Hindalco board and has extensive experience in this area. This isn't a case of chemical engineers trying to figure out metallurgy—they've hired people who've actually run copper operations at scale.

The subsidiary structure is already in place. Kiri Industries Limited has informed to the exchanges that it is acquiring 81% Equity stake of Indo Asia Copper Limited. Accordingly, Indo Asia Copper Limited become a wholly owned subsidiary of the Company. The prospective intent is for manufacturing of Copper & allied products as well as Fertilizers.

The fertilizer angle is particularly clever. The remaining fertiliser production will complement copper operations as a byproduct, with a planned capacity of 1 m tons for DAP and NPK fertilizers. Copper smelting produces sulfuric acid as a byproduct, which is a key input for fertilizer production. It's the same backward integration philosophy that served Kiri well in dyes, applied to an entirely new industry.

Location matters in the copper business, and Kiri has chosen wisely. KIL is developing a copper project at Pipavav Port, providing direct access to imported copper concentrate and efficient logistics for finished products. The Gujarat location also provides access to industrial consumers and established chemical industry infrastructure.

The funding strategy is perhaps the most interesting aspect. The DyStar sale proceeds, anticipated by March 2025, will play a pivotal role in funding these projects. About Rs 30 bn will be allocated to the copper project, while the remaining funds will strengthen working capital and reduce debt.

But Kiri isn't waiting for the DyStar money. Kiri has taken a $130 million loan, called judgment-based funding, to start its planned capex without waiting for the DyStar sale cash. This is sophisticated financial engineering—using the legal judgment as collateral to access capital immediately.

The promoter commitment is unmistakable. The promoters of Kiri Industries have applied for warrants worth ₹492 Cr in October, which, when converted over the next 18 months, will increase their shareholding from the current 27% to 41%. The company has already received ₹250 Cr and an additional ₹60 Cr recently from this arrangement.

When promoters are putting in nearly ₹500 crore of their own money, it's a strong signal of confidence. This isn't a pivot born of desperation; it's a calculated bet on India's infrastructure future.

The international dimension is already emerging. India's Kiri Industries Limited (KIL) is exploring a major investment in the Philippines to develop an integrated copper smelting, refining, and fertilizer production facility. The project is being discussed with Makilala Mining Company, Inc. (MMCI). The expression of interest was conveyed during a meeting between President Ferdinand R. Marcos Jr. and KIL Chairman and Managing Director Manish Kiri.

The ambition here is staggering. From a dyes company in Gujarat to potentially operating copper smelters in the Philippines. It's the kind of transformation that business school case studies are made of—if it works.

But there are legitimate concerns. Historically, the company has not been the best allocator of capital. The dyes business, despite all the backward integration and expansion, never really generated spectacular returns. Kiri's dyes business has been struggling. It hasn't seen much growth in the last 10 years and continues to face challenges, such as weak demand, underutilized capacity, and rising raw material costs.

The execution risk is enormous. They've brought in experienced people, like a former board member from Hindalco, to help lead it. However, since this is a much bigger investment than what Kiri's done in the past, it'll be important to watch how well they can handle the project (eg- sourcing copper concentrates which seems to be having a very tight supply currently).

Yet, there's something audacious and admirable about this pivot. Rather than simply returning the DyStar proceeds to shareholders or making small incremental investments, Kiri is swinging for the fences. They're betting that India's copper demand will explode, that their execution will be flawless, and that the commodity cycle will be favorable.

Whether this transforms into India's next industrial giant or becomes a cautionary tale of overreach remains to be seen. But one thing is certain: Kiri Industries is not content to remain a dyes company with a legal windfall. They're using that windfall to attempt something transformational.

VIII. Financial Engineering & Special Situations

The Kiri story offers a masterclass in financial engineering and special situations investing. The current market dynamics are particularly fascinating. Total payout post tax is expected to be ~5074 crores. Currently the Mcap of the company is below the total amount of cash expected to receive post tax.

This is the kind of situation that makes value investors salivate and efficient market theorists scratch their heads. How can a company trade for less than the cash it's about to receive? The answer lies in the intersection of complexity, uncertainty, and market psychology.

First, there's the warrant issuance to promoters. The promoters of Kiri Industries have applied for warrants worth ₹492 Cr in October, which, when converted over the next 18 months, will increase their shareholding from the current 27% to 41%. This is dilutive to existing shareholders, but it also signals massive confidence from insiders who know the business best.

The pricing of these warrants is crucial. They're essentially buying shares at current prices, betting that the combination of DyStar proceeds and copper project success will drive the stock much higher. It's the ultimate insider vote of confidence.

Then there's the judgment-based funding. Kiri has taken a $130 million loan, called judgment-based funding, to start its planned capex without waiting for the DyStar sale cash. This is a relatively rare form of financing where lenders provide capital against a legal judgment. The fact that sophisticated lenders were willing to provide this funding suggests strong confidence in the eventual collection of the DyStar proceeds.

The capital allocation framework going forward is intriguing. The company plans to invest half of the DyStar sale proceeds into the copper project. This leaves roughly ₹2,500 crore for other purposes—debt reduction, working capital, and potentially, shareholder returns.

The market's skepticism is understandable but possibly overdone. The concerns include execution risk on the copper project, the history of capital allocation at Kiri, the timeline uncertainty for DyStar proceeds, and the dilution from warrant conversion. Each of these is valid, but the current valuation seems to price in a worst-case scenario.

Consider the bear case: Even if the copper project fails completely, Kiri would still receive ₹5,000+ crore from DyStar. Even accounting for taxes and warrant dilution, the cash per share would exceed the current stock price. This creates an asymmetric risk-reward proposition.

The timeline dynamics are particularly important for investors. As per Singapore Supreme court its expected that the hard deadline is December 2025, though the sale is expected to close in few months. This suggests cash receipt sometime between March and June 2025, creating a specific catalyst timeline.

The Q1 FY26 performance provides some comfort on the base business. Kiri Industries Limited (KIL) reported 8% YoY growth in standalone revenue to Rs. 181.00 crores for Q1 FY26. EBITDA improved to Rs. 17.30 crores, and the company turned profitable with Rs. 7.20 crores PAT. While the dyes business isn't setting the world on fire, it's not collapsing either.

The special situation dynamics here are textbook: - Legal complexity that limits institutional participation - Timeline uncertainty that creates impatience - Corporate action (copper pivot) that changes the narrative - Insider buying that signals confidence - Valuation disconnect that creates opportunity

For patient investors who can navigate the complexity, Kiri represents a fascinating risk-reward proposition. The downside appears limited by the DyStar proceeds, while the upside—if the copper project succeeds—could be multiples of the current price.

The key is understanding that this is really two bets in one: a near-term special situation (DyStar proceeds) and a long-term transformation story (copper). The market is struggling to price both simultaneously, creating the opportunity.

What's particularly interesting is how the company is using financial engineering to bridge the timing gap. Rather than waiting for DyStar money to start the copper project, they're using judgment-based funding to begin immediately. This accelerates the transformation timeline and could position them to capture the copper cycle upturn.

The governance improvements post-litigation are also noteworthy. Having fought a decade-long battle over minority rights, Kiri's management is acutely aware of corporate governance importance. The transparency in communication, regular investor calls, and detailed disclosures suggest a company that has learned from its experiences.

IX. Playbook: Lessons from the Kiri Story

The Kiri saga offers a treasure trove of lessons for investors, entrepreneurs, and anyone interested in cross-border business. Let's extract the key insights that transcend this specific situation.

Lesson 1: Partnership Risk in Cross-Border JVs

The DyStar experience illustrates a fundamental truth: minority positions in cross-border joint ventures are inherently vulnerable. Being minority shareholder, Kiri could not able to access the cash generated or intellectual property rights. The protection mechanisms that work in domestic contexts often fail when partners are from different jurisdictions with different business cultures.

The key learning isn't to avoid such partnerships but to structure them carefully. Explicit deadlock provisions, mandatory dividend policies, and clear exit mechanisms should be negotiated upfront. The cost of good legal advice at the beginning pales in comparison to a decade of litigation.

Lesson 2: The Value of Patient Capital in Legal Disputes

Kiri's willingness to pursue litigation for nearly a decade is remarkable. Many companies would have settled for cents on the dollar rather than endure the uncertainty and expense. But "We are delighted with how our suits have progressed through Singapore's courts to achieve a just outcome," said Manish Kiri.

The patience paid off spectacularly. From an initial investment of ₹100 crore to a payout of ₹5,000+ crore—a 50x return, albeit over 15 years. The lesson: when you have a strong legal case and the financial capacity to pursue it, patience can be enormously valuable.

Lesson 3: Pivoting from Commodity Chemicals to Strategic Metals

The copper pivot represents a bold recognition that the dyes business, despite all efforts, had limited growth potential. Rather than throwing good money after bad, management chose radical transformation. This requires intellectual humility—admitting that your core business isn't working—and courage to try something completely different.

The timing of the pivot is particularly astute. India's infrastructure boom, the global energy transition, and China's potential supply constraints create a favorable backdrop for copper production. Sometimes, the best strategy is to abandon a difficult battlefield for a more promising one.

Lesson 4: Managing Stakeholder Expectations During Transformation

Kiri's communication strategy during this transformation has been exemplary. Regular investor calls, detailed presentations, and clear timelines help manage expectations. Investors and analysts will likely seek more details on the execution plan for the new project and strategies to turnaround the core dyes and chemicals business during the upcoming meeting.

The lesson: radical transformations require radical transparency. Stakeholders need to understand not just what you're doing, but why you're doing it and how you plan to execute.

Lesson 5: The Role of Jurisdiction in International Disputes

The choice of Singapore for the joint venture structure proved crucial. As the Court of Appeal observed in the judgment, there was "a lack of a clear path of principle on the existing state of the authorities" in this area of law. Singapore's SICC provided a sophisticated, neutral forum for resolving the dispute.

Singapore's legal system offered several advantages: common law tradition familiar to both parties, sophisticated commercial courts with international expertise, enforceability of judgments globally, and a reputation for fairness and efficiency. The lesson: in international ventures, the choice of jurisdiction is as important as the choice of partner.

Lesson 6: Special Situations Investing Opportunities

The current Kiri situation exemplifies classic special situations characteristics: complexity that limits competition, a defined catalyst (cash receipt), and valuation disconnect from intrinsic value. Kiri Industries, a company that trades at an EV of 2700Cr is therefore expecting to receive a cash inflow of 5000 Cr by June next year, an amount almost twice the value that it is currently trading at.

These situations require specialized skills—legal analysis, patience, and comfort with uncertainty. But for those with these capabilities, they offer some of the best risk-reward opportunities in public markets.

Lesson 7: The Importance of Bringing in Domain Expertise

Kiri's approach to the copper project—hiring experienced professionals from established players—shows maturity. They've brought in experienced people, like a former board member from Hindalco, to help lead it. The recognition that they don't know what they don't know is crucial for successful diversification.

Lesson 8: Using Financial Innovation to Accelerate Strategy

The judgment-based funding is particularly innovative. Rather than waiting for cash to arrive, Kiri used the legal judgment as collateral to access capital immediately. This type of financial engineering can be the difference between capturing an opportunity and missing it.

Lesson 9: The Power of Aligned Incentives

The promoter warrant subscription aligns management incentives with transformation success. By increasing their stake at current prices, promoters are betting their own capital on the strategy. This skin in the game provides comfort to minority shareholders.

Lesson 10: Learning from Crisis

Perhaps the most important lesson is how crisis can catalyze transformation. The DyStar litigation, while painful, ultimately provided both the capital and the impetus for radical change. Sometimes, the worst thing that happens to you becomes the best thing that happens to you—if you respond correctly.

X. Bear vs. Bull Case

Bear Case: The Skeptic's View

The bear case for Kiri starts with execution risk. The new investment projects are in sectors where the company has no prior experience, posing potential execution risks. Copper smelting is a completely different business from dyes manufacturing. It requires different skills, different relationships, and different capital allocation frameworks. The history of conglomerates attempting unrelated diversification is littered with failures.

The capital allocation track record raises red flags. Historically, the company has not been the best allocator of capital. Despite years of investment in backward integration and capacity expansion, the dyes business never generated exceptional returns. Why should we expect better results in copper?

The copper market itself presents challenges. There is an oversupply of smelting capacity of copper globally and domestically (with Kutch Copper's first unit having already come online and to be ramped up to more than the current entire capacity India has). Entering a market with oversupply rarely ends well for new entrants.

China dependency remains a concern. Copper prices are significantly influenced by Chinese demand, which is slowing as their property market struggles. A significant downturn in Chinese demand could devastate copper prices just as Kiri's project comes online.

The legal settlement, while likely, isn't guaranteed. Judgment on Senda's appeal to overturn the priority payment to Kiri has to be closely monitored too. Any unfavorable outcome here could lead to uncertainty on the expected receipt. Courts can surprise, and international enforcement can be complex.

Timeline delays are almost certain in projects of this scale. The copper project could face environmental clearances, land acquisition issues, technology transfer problems, or simple execution delays. Each delay increases costs and pushes back revenue generation.

The dilution from warrant conversion is substantial. Adding ₹492 crore worth of shares will significantly dilute existing shareholders, especially if the stock price doesn't appreciate meaningfully before conversion.

Bull Case: The Optimist's View

The bull case starts with simple math. Total payout post tax is expected to be ~5074 crores. Currently the Mcap of the company is below the total amount of cash expected to receive post tax. Even if everything else goes wrong, the company is trading below its near-term cash receipt.

India's copper deficit is structural and growing. India's significant demand-supply gap in copper, which is expected to triple by 2030. Electric vehicles, renewable energy, and infrastructure development all require massive amounts of copper. This isn't a cyclical opportunity; it's a secular growth story.

Management skin in the game is unprecedented. The promoters of Kiri Industries have applied for warrants worth ₹492 Cr in October. The company has already received ₹250 Cr and an additional ₹60 Cr recently. When promoters bet this much of their own money, they're seeing something the market isn't.

The copper project economics are compelling. Expected to generate over Rs 500 bn in annual revenue once fully operational. Even at modest margins, this translates to enormous profit potential. The fertilizer byproduct provides additional revenue streams and natural hedging.

The execution team is proven. Mr Sarkar who is ex Birla Copper and who used to sit in Hindalco board brings decades of relevant experience. This isn't amateurs trying to figure out metallurgy; it's industry veterans executing a familiar playbook.

Infrastructure location advantages are significant. The Pipavav port location provides logistics advantages that established players don't have. In commodity businesses, logistics costs can be the difference between profit and loss.

The Singapore legal system's track record suggests collection is highly likely. "...the honouring of the buyout agreement by Senda is essential in fostering trust between Indian and Chinese businesses". The reputational cost to Chinese businesses of not honoring a Singapore court judgment would be enormous.

Potential for special dividends post-settlement could provide near-term catalysts. With ₹5,000 crore coming in and only ₹3,000 crore needed for the copper project, substantial capital could be returned to shareholders.

The transformation multiple potential is enormous. If the copper project succeeds, Kiri could trade at industrial multiples rather than chemical company multiples. The re-rating potential from successful execution could be 5-10x current valuations.

Recent operational improvements suggest management is executing. The company turned profitable with Rs. 7.20 crores PAT. While small, this shows the base business is stabilizing even as transformation proceeds.

XI. Epilogue & Recent Developments

As we record this in late 2024, Kiri Industries stands at the most crucial juncture in its history. The company that began in a small Vatva unit making dyes is now preparing to receive one of the largest legal settlements in Indian corporate history while simultaneously attempting one of the most ambitious industrial transformations ever attempted by an Indian mid-cap company.

The recent developments paint a picture of accelerating momentum. The DyStar sale agreement for $696.00 million is progressing as planned. This isn't theoretical anymore—real money is about to change hands. The appointment of Deloitte as receivers has professionalized the sale process, removing the emotion and ensuring maximum value realization.

Q1 FY26 performance: Standalone business turnaround with revenue growing 8% YoY to Rs. 181.00 crores. The company turned profitable with Rs. 7.20 crores PAT. While the dyes business won't drive the future, its stabilization provides a platform for transformation.

The copper project milestones are being hit. Construction work has commenced with a targeted completion timeline of 36 months, starting from October 1. This means by October 2027, Kiri could be producing copper—transforming from a chemical company to a metals producer in just three years.

The international expansion continues with the meeting between President Ferdinand R. Marcos Jr. and KIL Chairman and Managing Director Manish Kiri signaling serious interest in Philippines operations. This suggests ambitions beyond just the Indian market.

What makes this moment particularly fascinating is the convergence of catalysts. The DyStar money provides the capital. The copper deficit provides the opportunity. The experienced team provides the capability. The promoter commitment provides the alignment. All the pieces are falling into place for either spectacular success or spectacular failure.

The surprises from our research are numerous. The sheer persistence in pursuing the DyStar case for nearly a decade. The audacity of the copper pivot. The sophistication of the financial engineering. The transformation from a family business to a potential industrial giant. Each element alone would be remarkable; together, they create one of the most interesting corporate stories in India today.

Looking ahead to the next five years, the scenarios diverge dramatically. In the bull case, Kiri becomes a major copper producer, generates ₹500 billion in revenue, and trades at a market cap of ₹50,000+ crore. In the bear case, the copper project struggles, capital is destroyed, and the company remains a subscale chemical producer trading at depressed multiples.

What's certain is that Kiri Industries won't be the same company five years from now. The DyStar settlement ensures significant cash infusion. The copper project ensures fundamental transformation. Whether that transformation creates or destroys value remains to be seen, but it certainly won't be boring.

The broader implications of the Kiri story extend beyond one company. It's a template for how Indian companies can fight for their rights in international ventures. It's a case study in how legal victories can fund business transformation. It's an example of how special situations can create extraordinary investment opportunities. And it's a reminder that in business, as in life, the biggest risks often come from not taking enough risk.

As we close this episode, Kiri Industries remains a live experiment in corporate transformation. The company that started making dyes in Ahmedabad may end up as one of India's major copper producers. Or it may serve as a cautionary tale about the perils of unrelated diversification. Either way, it's a story worth following, and one that will influence how we think about special situations, corporate transformation, and the value of patient capital for years to come.

The Kiri story is far from over. In fact, the most interesting chapters may just be beginning. The settlement money will arrive. The copper plant will be built. The transformation will be attempted. Whether it succeeds or fails, the lessons will be valuable, the drama will be compelling, and the implications will ripple through Indian corporate landscape for years to come.

For investors, entrepreneurs, and students of business, Kiri Industries represents a masterclass in navigating complexity, pursuing justice, and attempting transformation. It's a reminder that in the intersection of legal victories, operational transformation, and financial engineering, extraordinary opportunities can emerge—for those brave enough to pursue them and patient enough to see them through.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube