KIOCL: The Rise, Fall, and Rebirth of India's Iron Ore Pioneer

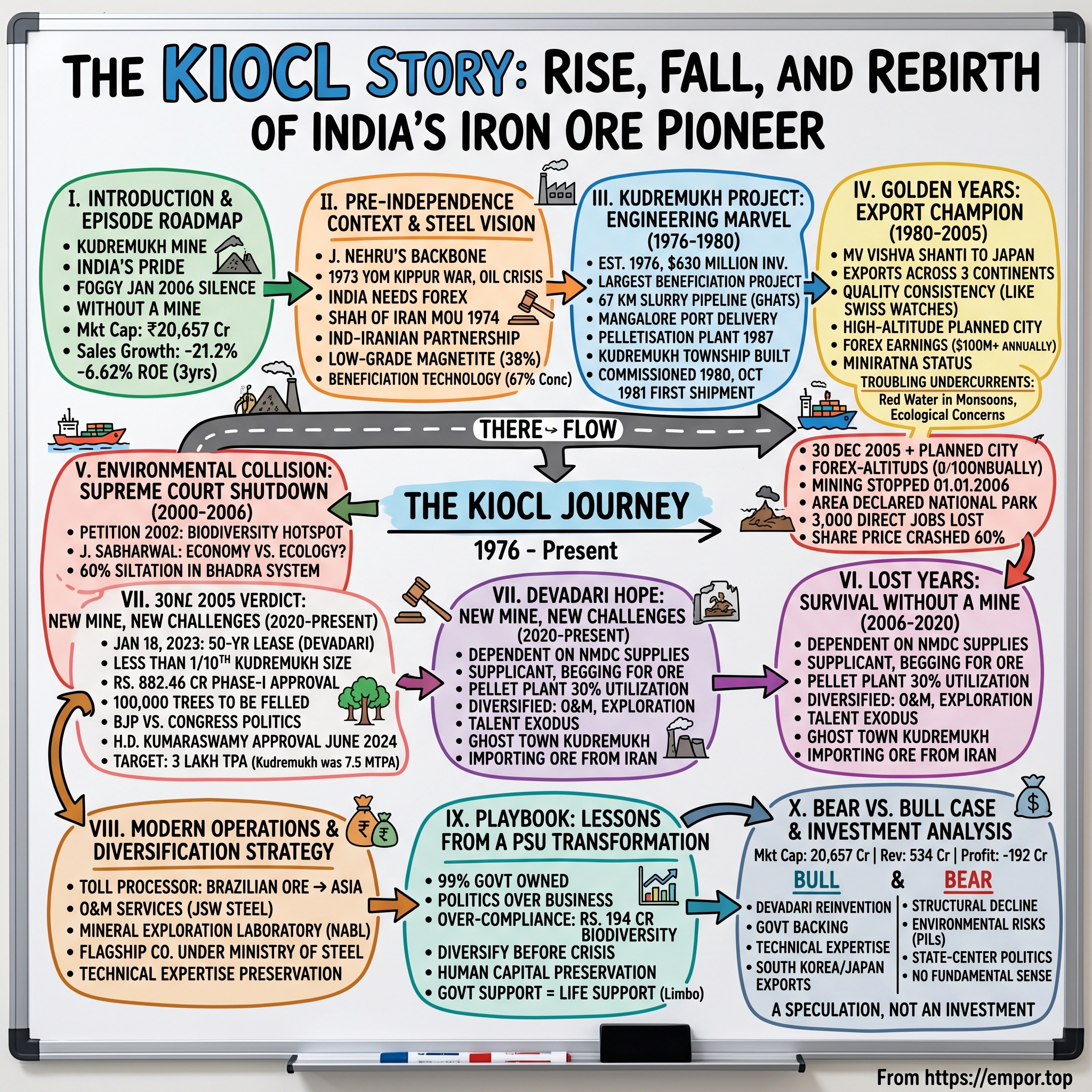

I. Introduction & Episode Roadmap

Picture this: A massive iron ore mine sprawling across 4,605 hectares in Karnataka's Western Ghats, processing 7.5 million tonnes of ore annually, connected by a 67-kilometer slurry pipeline snaking through dense forests to reach the Arabian Sea. For nearly three decades, this was Kudremukh—India's pride in mining engineering and a foreign exchange earning powerhouse. Then, on a foggy January morning in 2006, the excavators fell silent. The Supreme Court had spoken. The mine was dead.

This is the story of KIOCL Limited—formerly the Kudremukh Iron Ore Company—a Government of India enterprise that went from being one of the world's most sophisticated mining operations to a company without a mine, and its desperate fight to be reborn. It's a uniquely Indian tale where industrial ambition collides with environmental activism, where engineering marvels meet ecological concerns, and where a public sector undertaking must reinvent itself or perish. Today, KIOCL trades at a market cap of ₹20,657 crore, a company that once exported iron ore pellets to steel mills across the globe. The central question isn't just about survival—it's about whether a state-owned enterprise, stripped of its core asset by judicial decree, can transform itself from a mining company to something else entirely. This is a story of industrial ambition meeting environmental reality, of Supreme Court judgments reshaping corporate destinies, and of a company that refuses to die even after losing the very mine it was created to operate.

What we'll explore today is how KIOCL went from being a crown jewel of India's public sector—earning precious foreign exchange and showcasing technological prowess—to delivering poor sales growth of -21.2% over the past five years and a return on equity of -6.62% over the last three years. Yet remarkably, this isn't a story of inevitable decline. It's about reinvention, political maneuvering, and the complex dance between development and conservation in modern India.

Over the next few hours, we'll trace KIOCL's journey from its birth as part of an Indo-Iranian partnership through its golden years as an export champion, its shocking shutdown by environmental activists, and its current attempts at resurrection through the controversial Devadari mines. Along the way, we'll uncover lessons about running public sector undertakings, managing environmental risks, and the peculiar challenges of being 99% owned by the Government of India.

II. Pre-Independence Context & India's Steel Vision

The year was 1947. As the British Raj's Union Jack descended for the final time over the Red Fort, independent India inherited an economy that produced less steel than Belgium. Jawaharlal Nehru, standing before the Constituent Assembly, declared steel the backbone of modern industry—without it, his vision of an industrialized India would remain a pipe dream. The Tatas and Birlas had their mills, yes, but private capital alone couldn't build the temples of modern India that Nehru envisioned.

Fast forward to 1973. The Yom Kippur War erupts. Oil prices quadruple overnight. The global economy convulses. But for commodity-rich nations, including iron ore exporters, this crisis becomes opportunity. India, perpetually short of foreign exchange, sees a chance. The Shah of Iran, flush with petrodollars and ambitious to industrialize, needs iron ore for his grand steel projects. India has ore but needs technology and capital. A marriage of convenience beckons. On May 2, 1974, a Memorandum of Understanding was signed between the Government of Iran and India for implementation of the project for production and delivery of iron ore concentrate to National Iran Steel Company. This wasn't just a commercial deal—it was geopolitics wrapped in iron ore. Iran drew up plans for an ambitious domestic steel industry and was looking for a reliable supplier of iron ore. Kudremukh seemed ideal, abundant and just across the sea. Initially Iran agreed to finance the project in the form of US $630 million loan.

The selection of Karnataka's Western Ghats wasn't accidental. Here lay magnetite ore—not the high-grade hematite that Australia and Brazil blessed their steel mills with, but low-grade ore averaging just 38% iron content. Most would have walked away. But Indian engineers saw opportunity where others saw waste. With new beneficiation technology, they could transform this 38% ore into 67% concentrate—world-class material from what others dismissed as dirt.

Consider the audacity: India, still finding its industrial feet three decades after independence, proposed to build one of the world's most sophisticated ore beneficiation plants in virgin forest, accessible only by footpaths used by tribal communities. No roads, no power, no infrastructure—just ambition and Iranian money. The Western Ghats, with rainfall exceeding 6,000mm annually, would challenge every piece of equipment, every construction timeline, every budget projection.

Government of Iran financed for the project to buy back the finished product. However Iran withdrawn from the project due to its internal problem. The 1979 Islamic Revolution would shatter the Shah's steel dreams and leave India holding a half-built mining project with no customer. But by then, the die was cast. Government of India completed the project, transforming what began as an Indo-Iranian partnership into a wholly Indian enterprise—a pattern of resilience that would define KIOCL's journey through triumph and tragedy alike.

III. The Kudremukh Project: Engineering Marvel (1976–1980)

Dawn breaks over the Western Ghats in 1977. Where tigers once prowled undisturbed, bulldozers now carve switchbacks into mountainsides. Engineers from Bangalore, armed with theodolites and slide rules, survey terrain that would make Swiss tunnel builders nervous. The monsoon turns access roads into rivers. Leeches drop from trees onto construction workers. Equipment rusts overnight in humidity that hovers at 95%. This is where India chose to build its most ambitious mining project.

KIOCL was established in 1976 with a planned investment of $630 million. It is the country's largest iron ore project for beneficiation of low grade Iron Ore. But those two sentences hide an engineering saga that deserves its own epic. The project required moving 30 million cubic meters of earth—enough to fill 12,000 Olympic swimming pools. Every piece of heavy equipment had to be transported up mountain roads that didn't exist until workers carved them from cliff faces.

The slurry pipeline alone defied conventional wisdom. A 110 km road through ghats was built, and a slurry pipeline to Mangalore Port was completed and delivered on time, within the estimated cost of US$ 630 million. Think about that—pumping iron ore slurry 67 kilometers through some of India's most ecologically sensitive terrain, crossing 11 rivers, navigating elevation changes of over 900 meters. Engineers had to calculate pressure drops, erosion rates, and pump stations powerful enough to push millions of tonnes of material annually, yet gentle enough not to burst pipes crossing earthquake-prone zones.

The technology transfer component proved equally complex. Indian engineers worked alongside specialists from Canada, Australia, and Germany, absorbing knowledge about magnetic separation, flotation cells, and thickener design. This wasn't just purchasing equipment—it was acquiring the capability to process ore that others considered worthless. The concentrator plant, when completed, could process 7.5 million tonnes of ore annually, extracting iron from rock where nature had scattered it in microscopic particles.

The mine and plant facilities were commissioned in 1980 and the first shipment of concentrate was made in October 1981. A pelletisation plant with a capacity of 3 million tonnes per year was commissioned in 1987 for production of high quality blast furnace and direct reduction grade pellets for export. The speed of execution was remarkable—from virgin forest to operational mine in just four years, during an era without satellite imagery, GPS, or modern project management software.

The human dimension often gets lost in technical achievements. KIOCL built an entire township—Kudremukh—from scratch. Schools, hospitals, markets, recreation centers emerged where only forest existed. Engineers convinced their families to relocate from Bangalore's comfort to a mining camp where the nearest city was four hours away on roads that washed out every monsoon. They created not just a mine but a community, complete with its own cultural programs, sports facilities, and social fabric.

By 1980, as the first ore moved through the concentrator, KIOCL had achieved something remarkable: proving India could execute world-class mining projects without foreign operators. The Kudremukh project became a case study at mining schools worldwide—how to build sophisticated operations in impossible terrain, on time and on budget. What nobody knew then was that this engineering marvel would become the stage for one of India's most bitter environmental battles.

IV. The Golden Years: Export Champion (1980–2005)

October 1981. The cargo ship MV Vishva Shanti departs Mangalore Port, her holds filled with 30,000 tonnes of iron ore concentrate destined for Japan's Nippon Steel. On the dock, KIOCL engineers pop champagne—not imported French, but good Indian sparkling wine. After five years of construction battles with nature, the company had finally joined the global iron ore trade. Within a decade, that single shipment would multiply into a river of exports flowing to steel mills across three continents.

The Company's pellets have been used in blast furnaces of steel mills in Australia, China, Japan, Taiwan, Turkey and a host of other countries. Its pellets have also been used in steel plants of Hungary, Yugoslavia, United States of America, West Germany, Poland, Czechoslovakia, Indonesia and in some of the direct reduction plants in India. The geographic spread tells a story of diplomatic success—KIOCL's pellets crossed both Cold War boundaries and trade barriers. When Chinese mills needed high-quality feed for their blast furnaces, they turned to Kudremukh. When Japanese steelmakers, notoriously quality-obsessed, evaluated global suppliers, KIOCL made the cut.

The 1987 commissioning of the pelletization plant marked KIOCL's evolution from raw material supplier to value-added manufacturer. Pellets commanded premium prices—sometimes double that of concentrate. The technology was sophisticated: iron ore concentrate mixed with bentonite binder, rolled into marble-sized balls, then hardened in a 1,300-degree Celsius furnace. The process required precise chemistry, exact temperatures, and quality control that matched pharmaceutical standards. One bad batch could destroy blast furnace linings worth millions.

KIOCL's pellets earned a reputation for consistency that became its calling card. While Brazilian ore might vary in iron content by 2-3%, Kudremukh pellets maintained tolerances of 0.5%. This reliability mattered when steel mills planned production months in advance. A purchasing manager at Nippon Steel once remarked that KIOCL pellets were like Swiss watches—you could set your furnace by them.

The township of Kudremukh evolved into something extraordinary during these golden years. With 20,000 residents at its peak, it became Karnataka's highest-altitude planned city. The company built India's first computerized school in a mining township, introduced satellite television when most of India still had one state channel, and created recreational facilities that rivaled those in Bangalore. Children who grew up in Kudremukh in the 1990s describe an idyllic existence—mountain air, excellent schools, and a community where everyone knew everyone.

Foreign exchange earnings became KIOCL's contribution to national development. In an era when India desperately needed dollars for oil imports, KIOCL generated over $100 million annually in hard currency. The company achieved Miniratna status, joining the elite tier of profitable public sector undertakings. Its stock became a favorite of institutional investors who saw steady dividends backed by global commodity demand.

But beneath this success lay troubling undercurrents. The rainfall in Kudremukh, one of the highest for any open cast mining operation in the world, with over 60% of total siltation in the Bhadra system being contributed by the mining area which forms less than six percent of the catchment. Environmental activists began documenting red water flowing into streams during monsoons. Tribal communities complained about declining fish catches. Wildlife photographers captured images of elephants crossing mining roads, their ancient migration routes disrupted.

The company's attempts at environmental management—check dams, siltation ponds, reforestation—seemed perpetually inadequate against the Western Ghats' torrential rains. What worked in Australia's dry Pilbara region failed spectacularly in Kudremukh's 6,000mm annual rainfall. By the late 1990s, public interest litigation began winding through courts. The golden years were ending, though few at KIOCL recognized the gathering storm.

V. Environmental Collision: The Supreme Court Shutdown (2000–2006)

The petition arrived at the Supreme Court in 2002, filed by a coalition of environmental groups with a simple, devastating argument: How could India permit large-scale mining in one of the world's 25 biodiversity hotspots? The Western Ghats, older than the Himalayas, harbored species found nowhere else on Earth. The Kudremukh Iron Ore Company, petitioners argued, was slowly killing a global treasure for quarterly profits.

KIOCL's legal team arrived confident. They had environmental clearances dating back to 1976, employment records showing 3,000 direct jobs, export earnings exceeding ₹1,000 crore annually. Their 200-page response documented check dams, water treatment plants, and reforestation programs. They'd planted 1.2 million trees, they argued. They'd won national safety awards. How could success be redefined as failure?

The Supreme Court proceedings revealed a philosophical chasm that would define India's development debates for decades. Justice Y.K. Sabharwal's questions cut to the core: "Can economic benefit justify ecological destruction?" When KIOCL's lawyers cited foreign exchange earnings, the bench responded: "Can we sell our forests for dollars?" The company's environmental compliance certificates seemed to shrink before the court's moral interrogation.

The rainfall in Kudremukh, one of the highest for any open cast mining operation in the world, with over 60% of total siltation in the Bhadra system being contributed by the mining area which forms less than six percent of the catchment. This single statistic became the environmental movement's rallying cry. The Bhadra reservoir, which supplied water to five districts, was filling with mining silt. Activists produced photographs of red streams during monsoons, before-and-after satellite images showing forest degradation, studies documenting declining wildlife populations.

December 30, 2005. The Supreme Court delivered its verdict like a guillotine: KIOCL stopped mining operations at Kudremukh from 01.01.2006 pursuant to Supreme Court's Judgment, as the area was declared National Park. The court gave no transition period, no phased closure. On New Year's Day 2006, one of the world's most productive iron ore mines would simply stop. Forever.

The human cost was immediate and brutal. 3,000 direct employees, 10,000 contract workers, an entire township built around mining—all faced overnight obsolescence. Kudremukh's schools, which had sent students to IITs and medical colleges, would empty. The hospital that had conducted Karnataka's first laparoscopic surgery in a mining town would close. Families that had lived in Kudremukh for two generations would scatter across India, their community atomized by judicial decree.

KIOCL's management scrambled for alternatives. Could they mine underground? No—the ore body geometry made it uneconomical. Could they appeal? The Supreme Court's environmental judgments were historically irreversible. Could they find another mine? Every suitable deposit in Karnataka was either already allocated or similarly environmentally sensitive.

The shutdown's ripple effects spread far beyond Kudremukh. Mangalore Port lost its largest customer. The pellet plant, built for Kudremukh concentrate, sat idle. Share price crashed 60% in three months. International customers who'd relied on KIOCL for decades scrambled for alternatives. The company that had generated thousands of crores in foreign exchange now hemorrhaged money maintaining idle infrastructure.

Yet the environmental movement celebrated. The Western Ghats had been saved, they argued. The Bhadra river would run clear again. Wildlife would return. The precedent was set: India's ecological heritage was not for sale. That this victory came at the cost of thousands of livelihoods was, activists argued, the price of past mistakes. KIOCL had operated for 25 years—wasn't that enough?

VI. The Lost Years: Survival Without a Mine (2006–2020)

January 2006. KIOCL's headquarters in Bangalore resembled a emergency ward after a catastrophe. Executives huddled in crisis meetings that stretched past midnight. How does a mining company survive without a mine? The question wasn't rhetorical—3,000 families depended on the answer. The company's bank accounts held enough cash for perhaps six months of salaries. After that, insolvency loomed.

The immediate pivot seemed obvious: Company dependent on ore from NMDC Limited's supplies from mines in Chhattisgarh state to feed raw materials to its pellet plant. But NMDC, a fellow public sector undertaking, had its own priorities and customers. KIOCL would get ore when available, at prices NMDC determined, in quantities NMDC could spare. From master of its destiny, KIOCL became a supplicant, begging for raw material to keep its pellet plant running.

The numbers told a story of slow strangulation. The company has delivered a poor sales growth of -21.2% over past five years. Company has a low return on equity of -6.62% over last 3 years. Revenue that had exceeded ₹2,000 crore during peak mining years collapsed to under ₹500 crore. The pellet plant, designed for 3.5 million tonnes annual capacity, operated at 30% utilization. Fixed costs remained while revenue evaporated—a death spiral in accounting terms.

Management tried everything. Diversified into operation and maintenance (O&M) services and mineral exploration pertaining to various core areas of expertise. KIOCL engineers, among India's best in mineral processing, became consultants for hire. They operated NMDC's plants, conducted exploration surveys for private companies, provided technical audits for struggling mining operations. The company that once exported to Japan now survived on service contracts worth a few crores.

The talent exodus was devastating. Young engineers, seeing no future, left for Vedanta, Tata Steel, JSW. The Kudremukh township, once vibrant with 20,000 residents, shrank to a ghost town maintained by skeleton crews. The school that had produced merit scholars closed. The hospital that had served three districts reduced to a dispensary. Streets where children once played cricket were reclaimed by jungle.

Political promises came and went like monsoons. Every election brought assurances of new mining leases. The Karnataka government would announce allocations, then retract them under environmental pressure. The central government, KIOCL's 99% owner, made sympathetic noises but took no decisive action. Files moved between ministries—Steel to Environment to Forest to Law—accumulating dust and notations but no approvals.

The company's attempts to secure iron ore became increasingly desperate. The first shipment of 50,000 tonne of iron ore fines from Gol Gohar mines in Iran is expected to arrive in September this year. KIOCL would make pellets from the fines and export them to Iran. We are going to sign an agreement shortly with Gol Gohar mines wherein KIOCL would source one million tonne of iron ore fines every year. The irony was complete—the company created with Iranian financing to export to Iran would now import from Iran to survive.

By 2015, institutional investors had written off KIOCL. The stock that once traded at ₹300 touched ₹45. Analysts stopped coverage—why waste time on a mining company without mines? The Ministry of Steel periodically discussed merging KIOCL with NMDC or Steel Authority of India, essentially admitting defeat. Yet somehow, the company persisted, bleeding but breathing, waiting for salvation that seemed increasingly unlikely.

The preservation of institutional knowledge became an unexpected achievement during these dark years. KIOCL maintained its technical teams, its NABL-accredited laboratories, its engineering expertise. Like a library preserving books through a dark age, the company kept alive capabilities that India had spent decades building. When private miners needed help processing complex ores, they turned to KIOCL. When the government needed mineral exploration in difficult terrain, KIOCL's teams were ready.

VII. The Devadari Hope: New Mine, New Challenges (2020–Present)

January 18, 2023. In a government office in Sandur Taluk, Karnataka, two signatures changed KIOCL's destiny. The Mining Lease deed document executed between Govt. of Karnataka and KIOCL for the grant of a mining lease for Iron Ore and Manganese Ore, over an extent of 388 ha for a period of 50 years in Devadari Range, Sandur Taluk, Ballari District, Karnataka State, has been registered at the Office of Sub-Registrar, Sandur Tq on 18 January 2023 by paying the total amount of Rs. 329.17 crore which includes the stamp duty, cess on stamps and fees for registering documents. After seventeen years without a mine, KIOCL had finally secured new ore reserves. The champagne remained corked—too many false dawns had taught management caution.

The Devadari deposits weren't Kudremukh. Where Kudremukh sprawled across 4,605 hectares with reserves lasting decades, Devadari offered 388 hectares—less than a tenth the size. The ore quality was better, yes, but volumes were limited. KIOCL Limited has received approval from the Finance Minister and Steel Minister for Phase-I of the Devadari Iron Ore Mine project in Bellary District, Karnataka. The project, estimated at Rs. 882.46 crore, includes pre-operative expenditure approval. Nearly 900 crores for a mine that would produce what Kudremukh generated in a few months—the economics were challenging at best.

Political drama erupted immediately. In a letter dated June 21, the Karnataka Forest, Ecology and Environment Ministry directed officials not to transfer forest land to the company. KIOCL had proposed to start operations in 401.5 hectares of forest land in the Devadari forest in the Swamimalai block and 100,000 trees were expected to be felled in the forest area if the company were to go ahead with its mining plan. "There are complaints that KIOCL has failed to implement the directions of the Centrally Empowered Committee (CEC) within the stipulated time, over violations that took place when the company took up mining activity at Kudremukh national forest," the state ministry said.

The political calculus was transparent. The BJP-led central government supported KIOCL. The Congress government in Karnataka opposed it. Environmental groups, emboldened by their Kudremukh victory, mobilized against Devadari. The same arguments resurfaced—biodiversity, water pollution, tribal rights. KIOCL found itself trapped between federal support and state resistance, between economic necessity and environmental activism.

June 2024 brought unexpected relief. H.D. Kumaraswamy, newly appointed as Union Steel Minister, signed his first file approving Devadari operations. Signed the first file after assuming office as Union Minister of Steel. It is related to my home state Karnataka. The first file of KIOCL Limited was… The Karnataka politician understood both local sensitivities and national imperatives. His approval carried political weight that bureaucratic clearances couldn't match.

Yet challenges mounted. The mining involves removing over 99,000 trees, of which 21,259 trees in 293 acres will be cleared in the first five years. Before starting the operations, the KIOCL has pledged to take up afforestation and conserve biodiversity in 808 hectare at the cost of Rs 194 crore," he said. The mining involves removing over 99,000 trees, of which 21,259 trees in 293 acres will be cleared in the first five years. The environmental cost was undeniable. KIOCL promised compensatory afforestation, biodiversity conservation, zero-discharge systems. Whether technology could reconcile mining with conservation remained unproven.

Production targets revealed the mine's limitations. The company has plans to produce around 3 lakh tonnes per annum in 2024-25. KIOCL has plans to produce around 3 lakh tonnes per annum around 2024-25. Three lakh tonnes annually—Kudremukh had produced 7.5 million tonnes. The pellet plant needed 3.5 million tonnes to run efficiently. Devadari would provide less than 10% of requirements. KIOCL would remain dependent on purchased ore, vulnerable to price fluctuations and supply disruptions.

The financial markets responded with characteristic volatility. KIOCL surged 11.63% to Rs 477.60 after the Union steel and and heavy industries minister, H D Kumaraswamy approved the commencement of operations in Devadari iron ore mine in Sandur taluk of Ballari district in Karnataka. Hope drove valuations more than fundamentals. Investors saw any mine as better than no mine, any production preferable to complete dependence.

As 2024 progresses, Devadari remains more promise than reality. Equipment moves into position. Environmental activists file petitions. Politicians make speeches. The ore lies waiting, 100,000 trees standing sentinel over deposits that might save KIOCL or merely postpone its reckoning. The question isn't whether Devadari can replace Kudremukh—it clearly cannot. The question is whether it provides enough breathing room for KIOCL to transform into something beyond a traditional mining company.

VIII. Modern Operations & Diversification Strategy

Walk through KIOCL's Mangalore complex today and you encounter a curious paradox: world-class infrastructure operating at fraction of capacity, like a Formula One track hosting go-karts. KIOCL is having facilities to operate 3.5 MTPA Iron-oxide Pellet Plant, Blast Furnace Unit to manufacture 2.16 lakh tonnes per annum Pig iron at Mangaluru, Karnataka. The pellet plant, designed for 3.5 million tonnes annual production, runs intermittently on whatever ore KIOCL can source. The blast furnace, added as value addition during better days, operates when economics permit—which isn't often.

The transformation into a service provider began as survival instinct but evolved into strategy. The Company has diversified into operation and maintenance (O&M) services and mineral exploration pertaining to its various core areas of expertise. KIOCL engineers, trained on complex beneficiation challenges, became consultants to private miners struggling with low-grade deposits. When JSW Steel needed assessment of siliceous ore at their Bellary operations, they turned to KIOCL. The Company got into regime of providing mineral exploration services to private agencies by securing 5 number of Iron Ore Mine Lease Projects from Lease (for assessment of BHQ / silicious ore) Projects from M/s JSW Steel Limited, Tornagallu, Bellary, Karnataka with Order value Rs 12.27 Crores.

The technical capabilities accumulated over decades found new applications. KIOCL is a flagship company under the Ministry of Steel, GoI, with Miniratna status. The Mineral Exploration Laboratory, originally built to analyze Kudremukh samples, expanded its scope. KIOCL has been a pioneer with over four decades of experience in operating Iron Ore Mining, Beneficiation and Iron–Oxide Pelletisation in the Country. Private companies paid premium prices for KIOCL's expertise in processing complex ores that conventional methods couldn't handle.

The laboratory certification told a story of adaptation. In April 2022, KIOCL's Mineral Exploration Laboratory acquired NABL accreditation—recognition that its testing met international standards. This wasn't just bureaucratic achievement. It meant private companies could use KIOCL's analysis for export documentation, environmental clearances, and quality certification. Each certificate generated revenue, small but steady.

The pellet plant's transformation was more dramatic. Without captive ore, KIOCL became a toll processor—converting others' ore into pellets for a fee. Brazilian miners shipped ore to Mangalore. KIOCL processed it and shipped pellets to China, Japan, South Korea. We are now producing high grade pellets for our customers in Iran, Brazil, China and Japan. We are getting iron ore from Brazil which is converted into pellets and sent back to customers. Besides, we have recently entered South Korea and Japan. We are now exporting one shipment each (50,000 tonnes) every month to these countries. The irony was complete—a company created to mine Indian ore now processed Brazilian ore for Asian markets.

International partnerships revealed both opportunity and desperation. The Iran connection, dormant since 1979, revived as sanctions eased. KIOCL Ltd, owned by India's steel ministry, could sell as much as 2 million tonnes of pellets to Iran to meet substantial local demand, Chairman Malay Chatterjee said. Keyvan Ja'fari Tehrani, head of international affairs at the Iranian Iron Ore Producers and Exporters Association, said a final agreement was yet to be struck. 'The production of pellets in Iran is not sufficient,' Tehrani said, adding there's a need to import between 7 and 8 million tonnes a year. Iran produced 21 million tonnes of iron ore pellets last year while demand reached 28 to 29 million tonnes, he said. Full circle—the company born from Iranian partnership sought salvation through Iranian demand.

Yet financial performance remained dismal. The company has delivered a poor sales growth of -21.2% over past five years. Company has a low return on equity of -6.62% over last 3 years. Service contracts and toll processing couldn't replace mining's margins. The pellet plant needed 70% utilization to break even; it rarely exceeded 40%. Every quarter brought losses, covered by reserves accumulated during golden years—reserves rapidly depleting.

The technical expertise preservation became KIOCL's unexpected legacy. While revenues collapsed and stock price languished, the company maintained capabilities that took decades to build. Young engineers might have fled, but senior technical staff remained, guardians of institutional knowledge. When India's steel production eventually expands toward 300 million tonnes annually, when new mines need beneficiation expertise, when complex ores require processing—KIOCL's knowledge base will matter.

The diversification strategy, born of desperation, contained seeds of transformation. Could KIOCL evolve from mine operator to mining services company? From ore producer to technical consultant? From commodity player to knowledge enterprise? The answers remained unclear, but the questions themselves represented evolution. A company that once defined itself by what it dug from the ground now sought identity in what it knew about digging.

IX. Playbook: Lessons from a PSU Transformation

The boardroom at KIOCL's Bangalore headquarters holds a peculiar artifact: a framed photograph of the last blast at Kudremukh mine, December 31, 2005. Executives pass it daily, a reminder that in the public sector, political decisions can override decades of planning. This image encapsulates the first lesson of the KIOCL playbook: when you're 99% government-owned, you're not really in the business of business—you're in the business of politics.

Promoter Holding: 99.0%. As of March 31, 2024, the Government of India held a 99.03% stake in KIOCL. This ownership structure creates peculiar dynamics. Private companies facing Kudremukh's closure would have declared bankruptcy, liquidated assets, and moved on. KIOCL couldn't die even when it had every reason to. The government wouldn't allow it. Instead, it entered corporate purgatory—alive but not living, existing but not thriving, preserved like a museum piece of industrial ambition.

Managing political and bureaucratic constraints becomes an art form in PSUs. Every decision requires multiple approvals. A private miner deciding to source ore from Brazil would make that call in a boardroom. KIOCL needs clearances from Steel Ministry, Finance Ministry, External Affairs Ministry, and probably three other departments. By the time approvals arrive, market opportunities have vanished. The company operates with one hand tied behind its back while competing against private players using both hands and occasionally their feet.

Environmental compliance evolved from operational consideration to existential threat. The Kudremukh closure taught a harsh lesson: you can have every clearance, follow every rule, win every safety award, and still lose everything if public opinion turns. The new playbook requires over-compliance—not just meeting environmental standards but exceeding them so dramatically that even activists struggle to object. Before starting the operations, the KIOCL has pledged to take up afforestation and conserve biodiversity in 808 hectare at the cost of Rs 194 crore. Spending 194 crores on biodiversity for a 388-hectare mine seems excessive until you remember Kudremukh's fate.

Diversification strategies for single-asset companies require careful calibration. KIOCL's pivot to services made sense theoretically—leverage expertise, minimize capital investment, generate steady revenues. But service contracts worth 12 crores don't replace mining revenues worth 2,000 crores. The math never worked. The lesson: diversification must happen before crisis, not during it. By the time you need alternatives, it's too late to build them.

Building technical expertise as competitive advantage seems obvious until you try maintaining it without operations. KIOCL kept engineers employed for seventeen years without a mine. Private companies would have fired everyone except security guards. But those engineers, expensive and underutilized, preserved capabilities that money can't quickly buy. When India needs to process complex ores, when environmental standards require sophisticated beneficiation, when low-grade deposits become economically viable—KIOCL's expertise will matter. The playbook lesson: in knowledge industries, human capital preservation trumps short-term cost cutting.

Long-term planning in volatile commodity markets requires acknowledging that long-term might not exist. KIOCL planned for Kudremukh to operate until 2025. The Supreme Court had other ideas. Devadari is planned for 50 years. for a period of 50 years in Devadari Range, Sandur Taluk, Ballari District, Karnataka State Will environmental activism, political changes, or judicial intervention cut that short? Probably. The new playbook assumes disruption, plans for discontinuity, and maintains optionality even when options seem theoretical.

The role of government ownership in crisis management proved double-edged. Government support kept KIOCL alive when any private company would have died. But government ownership also prevented radical restructuring, asset sales, or strategic pivots that might have enabled genuine transformation. The company existed in limbo—too important to die, too constrained to thrive. The playbook insight: government ownership provides survival but prevents revival. It's life support, not medicine.

Competition from private miners and global markets exposed KIOCL's structural disadvantages. While JSW Steel or Vedanta could make quick decisions, KIOCL navigated bureaucracy. While Vale could invest billions in expansion, KIOCL begged for budgets. While Chinese companies integrated vertically from mine to steel mill, KIOCL couldn't even secure reliable ore supply. The competitive playbook requires accepting these constraints while finding niches where they matter less—specialized processing, technical services, complex projects where expertise trumps speed.

The ultimate lesson might be the most uncomfortable: some business models become obsolete not through poor management or strategic errors but through societal evolution. India in 1976 needed foreign exchange and accepted environmental costs. India in 2006 valued biodiversity over mining revenue. KIOCL got caught in this transition, a corporate casualty of changing national priorities. The playbook's final page might read: know when your time has passed, and prepare for transformation before transformation is forced upon you.

X. Bear vs. Bull Case & Investment Analysis

The investment case for KIOCL requires first accepting a fundamental reality: Mkt Cap: 20,657 Crore (down -20.0% in 1 year) · Revenue: 534 Cr · Profit: -192 Cr. A company valued at 20,000 crores generating 500 crores in revenue while losing money—the numbers scream value trap. Yet institutional investors hold positions, analysts maintain coverage, and the stock trades actively. The disconnect between market valuation and operational reality defines KIOCL's investment paradox.

The Bull Case: Renaissance Through Reinvention

Bulls see Devadari as the beginning, not the end. Yes, initial production targets are modest—300,000 tonnes annually versus Kudremukh's 7.5 million. But Devadari proves KIOCL can still secure mining rights, navigate environmental clearances, and mobilize capital. The 50-year lease provides time to expand, optimize, and potentially discover additional reserves. If Phase I succeeds, Phase II could follow. If Devadari works, other mines become possible.

The company has delivered a poor sales growth of -21.2% over past five years. Company has a low return on equity of -6.62% over last 3 years. Bulls argue these backward-looking metrics miss the inflection point. The worst is behind us, they claim. KIOCL Limited has received approval from the Finance Minister and Steel Minister for Phase-I of the Devadari Iron Ore Mine project in Bellary District, Karnataka. The project, estimated at Rs. 882.46 crore, represents government commitment to KIOCL's revival. When both Finance and Steel Ministers sign off on nearly 900 crores of investment, it signals political will that transcends party lines.

The technical expertise argument carries weight. India's steel production target of 300 million tonnes by 2030 requires processing increasingly complex, low-grade ores. KIOCL's four decades of beneficiation experience becomes valuable when easy ore deposits exhaust. The company that transformed 38% magnetite into 67% concentrate possesses knowledge that new miners lack. This intellectual property, though intangible, has real value in a resource-constrained future.

International opportunities expand as global steel dynamics shift. Net loss of KIOCL reported to Rs 47.79 crore in the quarter ended December 2024 as against net profit of Rs 39.03 crore during the previous quarter ended December 2023. Sales declined 67.14% to Rs 180.54 crore in the quarter ended December 2024 as against Rs 549.44 crore during the previous quarter ended December 2023. The numbers are terrible, but context matters—iron ore prices crashed globally in 2024. When commodity cycles turn, KIOCL's operational leverage could deliver explosive earnings growth.

The government backing provides ultimate downside protection. With 99% ownership, the Government of India won't let KIOCL fail catastrophically. This implicit guarantee means bankruptcy risk approaches zero. For value investors, this creates an asymmetric bet—limited downside with potential multibagger upside if operations normalize.

The Bear Case: Structural Decline Accelerating

Bears see Devadari as too little, too late. The revenue of KIOCL Ltd for the Mar '25 is ₹ 262.24 crore as compare to the Dec '24 revenue of ₹ 191.22 crore. This represent the growth of 37.14%. The ebitda of KIOCL Ltd for the Mar '25 is ₹ -25.03 crore as compare to the Dec '24 ebitda of ₹ -32.8 crore. The net profit of KIOCL Ltd for the Mar '25 is ₹ -36.86 crore as compare to the Dec '24 net profit of ₹ -47.79 crore. Even with revenue growth, the company can't generate positive EBITDA. Operating leverage works both ways—if you can't make money at 260 crores revenue, how do you profit at any realistic production level?

Environmental risks remain existential. KIOCL had proposed to start operations in 401.5 hectares of forest land in the Devadari forest in the Swamimalai block and 100,000 trees were expected to be felled in the forest area if the company were to go ahead with its mining plan. "There are complaints that KIOCL has failed to implement the directions of the Centrally Empowered Committee (CEC) within the stipulated time, over violations that took place when the company took up mining activity at Kudremukh national forest," the state ministry said. The same forces that killed Kudremukh threaten Devadari. One PIL, one adverse judgment, and KIOCL faces another shutdown.

The competitive position has permanently eroded. While KIOCL struggled without mines, private players like JSW Steel and Vedanta built integrated operations from mine to finished steel. They secured captive ore, developed logistics, and captured margins across the value chain. KIOCL, dependent on purchased ore and third-party customers, operates at the mercy of others' economics.

Political risk compounds operational challenges. In a letter dated June 21, the Karnataka Forest, Ecology and Environment Ministry directed officials not to transfer forest land to the company. State-center politics can halt operations overnight. With Karnataka often governed by parties opposing the central government, KIOCL becomes a political football, kicked between competing agendas.

The valuation makes no fundamental sense. Trading at 12 times book value for a company losing money, with challenged operations and political risks, defies logic. The market cap of 20,000 crores implies expectations that operational reality can't support. When reality reasserts itself, the correction could be brutal.

The Verdict: A Speculation, Not an Investment

KIOCL represents a bet on political will overcoming economic reality. Bulls buy hope—that Devadari succeeds, that steel demand explodes, that environmental concerns fade. Bears see structural decline—a company whose time has passed, preserved artificially by government ownership.

The stock price, volatile and news-driven, reflects this uncertainty. Every ministry approval sends shares soaring. Every environmental objection triggers selling. This isn't investing—it's gambling on regulatory outcomes and political decisions.

For fundamental investors, KIOCL offers a clear lesson: some turnarounds never turn. Some businesses become obsolete not through mismanagement but through societal evolution. India decided biodiversity matters more than iron ore. That decision, irreversible and probably correct, renders KIOCL's business model permanently impaired.

The only rational position might be to watch from the sidelines, studying KIOCL as a cautionary tale about environmental risks, government ownership, and the challenges of resurrecting dead business models. The stock might double or halve—both outcomes seem equally probable and equally disconnected from fundamental value creation.

XI. Epilogue: What Could Have Been Different

Standing at the abandoned Kudremukh township in 2024, you see nature reclaiming human ambition with ruthless efficiency. Vines strangle the school where future engineers learned calculus. The hospital's operating theatre, which once saved lives, shelters bats. The executive guest house where international buyers negotiated pellet contracts hosts termites negotiating wood. This isn't just physical decay—it's a monument to missed opportunities and choices that might have been different.

Could Kudremukh have survived with better environmental management? The question haunts every KIOCL employee who remembers the good years. Modern mining companies operate in equally sensitive environments—Vale in the Amazon, BHP in Australia's outback. They use zero-discharge systems, real-time monitoring, and restoration that sometimes improves on nature. Had KIOCL invested in these technologies in the 1990s, rather than maximizing production, would the Supreme Court have ruled differently?

The answer probably lies in timing. KIOCL operated during an era when environmental compliance meant meeting minimum standards, not exceeding them. The company did what regulations required, nothing more. By the time environmental consciousness evolved, patterns were set, damage documented, and activist narratives established. Kudremukh became a symbol of ecological destruction, fairly or not. Symbols, once created, resist fact-based revision.

Alternative paths proliferate in hindsight. KIOCL could have voluntarily reduced mining areas, creating buffer zones that demonstrated environmental commitment. It could have partnered with conservation groups, funding biodiversity research that generated goodwill. It could have transitioned tribal communities into permanent employees, creating local stakeholders who'd defend operations. Each path not taken seems obvious now, impossible then.

The cost of losing world-class mining assets extends beyond KIOCL's balance sheet. India imports 60% of its coking coal and significant iron ore despite domestic reserves. Every tonne imported drains foreign exchange, creates logistics bottlenecks, and increases steel costs. Kudremukh could have supplied 7.5 million tonnes annually for another two decades. At current prices, that represents $15 billion in avoided imports. The macroeconomic cost of environmental protection, rarely calculated, might exceed environmental benefits.

Lessons for India's mining sector emerge painfully. First, environmental and social license to operate matters more than government permits. Second, investing in beyond-compliance environmental management isn't corporate social responsibility—it's survival. Third, engaging communities as partners, not obstacles, creates defenders when activists attack. Fourth, technical excellence means nothing if social acceptance disappears.

Future PSUs face KIOCL's dilemma magnified. Climate change makes every coal mine controversial. Water scarcity makes every industrial project contested. Urbanization makes every land acquisition political. The playbook that built India's industrial base—government acquires land, PSU develops infrastructure, production begins—no longer works. Future PSUs must be simultaneously profitable, environmental, and social—a trinity that KIOCL never attempted.

What could have been different ultimately becomes what must be different. The next KIOCL—perhaps lithium mining for electric vehicle batteries or rare earth extraction for wind turbines—can't repeat these mistakes. It must design for closure from day one, plan for environmental opposition, and build social capital alongside physical infrastructure. It must assume that today's permit becomes tomorrow's litigation.

The abandoned railway line from Kudremukh to Mangalore, rails rusting in monsoon rain, offers a final metaphor. Infrastructure built for extraction can be reimagined for conservation. The mining roads now serve forest rangers. The slurry pipeline route became a trekking trail. The township's water treatment plant supplies nearby villages. From industrial ambition's corpse, different futures grow.

KIOCL's story isn't finished. Devadari might succeed. New technologies might make low-grade ores valuable. Political winds might shift toward development. But Kudremukh is gone forever, a $630 million investment reduced to ruins that environmental activists celebrate and industry mourns. In those ruins lies a lesson worth more than iron ore: in democracy, social license matters more than mining license, and once lost, it's almost impossible to recover.

The epilogue writes itself daily in KIOCL's struggles, in India's import bills, in environmental victories and industrial defeats. What could have been different? Everything. What was different? Nothing. And in that gap between possibility and reality lies the tragedy of Kudremukh—not just a mine that closed, but a future that never opened.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube