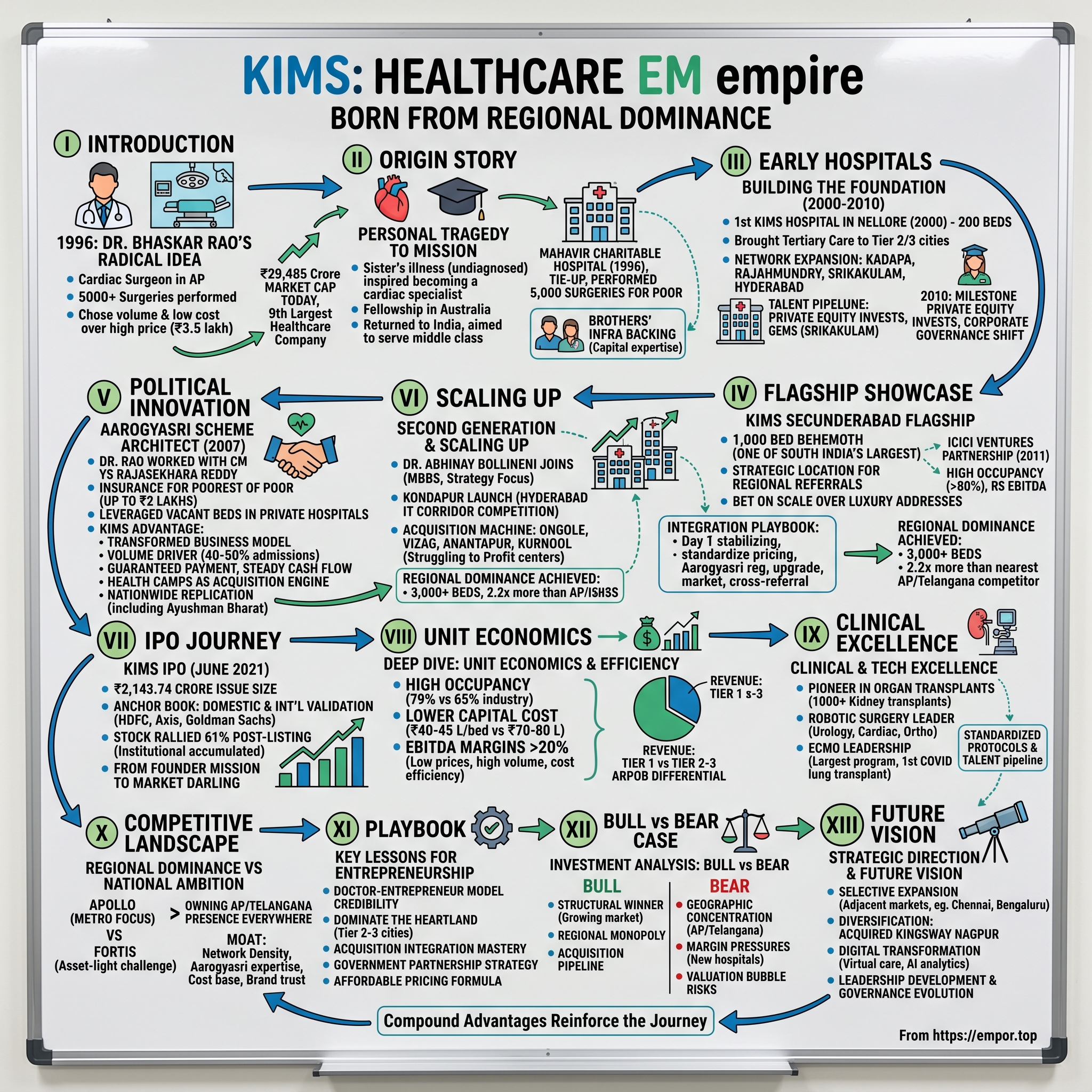

KIMS: The Heart Surgeon Who Built India's Healthcare Empire

I. Introduction & Episode Roadmap

Picture this: A cardiac surgeon stands in an operating theater in Andhra Pradesh, 1996. He's just completed his 5,000th heart surgery—but unlike his peers charging ₹3.5 lakh per procedure, he's done it for ₹45,000. This isn't charity; it's the beginning of a business model that would reshape Indian healthcare. That surgeon is Dr. Bhaskar Rao, and his company, Krishna Institute of Medical Sciences (KIMS), would grow from a single 200-bed hospital in Nellore to become India's 9th largest healthcare company by market capitalization.

Today, KIMS commands a market cap of ₹29,485 crore—larger than many storied Indian conglomerates. With revenue of ₹3,218 crore and profits of ₹404 crore, it's a healthcare powerhouse that treats over 2 million patients annually. But here's what makes this story remarkable: while Apollo Hospitals chased metropolitan dreams and Fortis built luxury healthcare palaces, KIMS quietly dominated India's heartland—Tier 2 and Tier 3 cities where 70% of India lives but where quality healthcare barely existed.

The central question isn't just how a doctor who performed over 30,000 surgeries built a ₹29,000+ crore empire. It's how he cracked the code that eluded everyone else: delivering world-class healthcare at prices the Indian middle class could actually afford, while still generating industry-leading margins. This is a story of regional dominance, acquisition-led growth, and most importantly, understanding that in India, healthcare isn't just a business—it's a social contract.

Three themes will guide our exploration. First, the power of regional dominance versus national ambition—why owning Andhra Pradesh and Telangana matters more than having a presence everywhere. Second, the art of affordable healthcare at scale—how KIMS delivers cardiac surgeries at one-third the price of competitors while maintaining 20%+ EBITDA margins. Third, the acquisition playbook—turning distressed hospitals into profit centers, a strategy that added 2,000+ beds to their network in just five years.

As we dive into this story, remember: this isn't just about hospitals and bed counts. It's about a fundamental reimagining of what healthcare delivery could look like in emerging markets. While Silicon Valley debates digital health apps, KIMS built physical infrastructure where people actually needed it. And that, as we'll see, made all the difference.

II. The Founder's Origin Story: Dr. Bhaskar Rao's Journey

The operating room at CMC Vellore, 1985. A young Dr. Bhaskar Rao watches helplessly as doctors explain to his family that his sister's heart condition—undiagnosed for years in their village—has progressed too far. The paralytic attack is irreversible; the disability will be permanent. "We had taken her to CMC Vellore for treatment and that's where we discovered her medical condition. The treating doctor said that if we had come earlier, she wouldn't have suffered this attack. That was the day I decided to become a cardiac specialist", he would later recall. This moment wouldn't just shape a career—it would reshape healthcare delivery for millions of Indians.

Bhaskar Rao Bollineni completed his medical education from Rangaraya Medical College, Kakinada, and Masters from Madras Medical College, Chennai. But academic credentials tell only part of the story. Coming from a rural and an economically modest background, he knew the worth of every rupee that the common man toiled for everyday, hailing from the village of Mamuduru in Nellore district. After his fellowship in Sydney and Melbourne, he returned to an India where cardiac surgery was a luxury product—₹95,000 to ₹3.5 lakh for a bypass, effectively a death sentence for 90% of the population.

The young surgeon joined Medwin Hospitals, spending five years honing his skills. But the disconnect gnawed at him. "Even though I was busy with my clinical life, I use to take a keen interest in the workings of the hospital," says the doctor, whose service was limited to only those patients who could afford it. He was performing world-class surgeries, but only for India's elite. The memory of his sister's preventable disability haunted every procedure.

The Mahavir Experiment: Cracking the Code

In 1996, Dr. Rao made his move. "I decided to tie up with Mahavir Charitable Hospital, Hyderabad, to provide affordable cardiac care. I took a loan of five crore rupees and started working to convert my dream into a reality. We did bypass surgeries at just ₹50,000. In 10 years, my team and I performed over 5,000 surgeries for the poor." The market rate was ₹95,000 to ₹3.5 lakh; Rao was charging ₹45,000-50,000. This wasn't charity—it was process engineering.

Dr. Rao started his entrepreneurial journey at "Mahavir Cardio Vascular Centre" in Hyderabad with 50 beds and performed heart surgeries at an unimaginable low cost of just Rs.45,000 only. Dr. Rao never turned away any patient from the hospital for want of money. The model was radical: strip away everything non-essential, focus on volume over margin per procedure, and leverage India's cost advantages in labor and infrastructure. While Apollo was importing marble from Italy for its lobbies, Rao was figuring out how to do the same surgery with locally-sourced equipment and junior doctors trained in-house.

The numbers told the story. Dr. Bollineni Bhaskar Rao is one of the very few CardioThoracic Surgeons in the country, who performed over 30000 surgeries in his career spanning over more than 25 years. Think about that—30,000 surgeries. At conventional prices, that's ₹30-100 billion worth of procedures. At Rao's prices, it was affordable healthcare for the middle class. The volume allowed him to perfect techniques, train teams, and most importantly, prove that quality didn't require luxury pricing.

The Infrastructure Play: Brothers in Business

Here's where the story takes an interesting turn. "Both my brothers are in the infrastructure business. When I decided to set up my hospital, they were my backbone, both financially and emotionally. Their deep understanding of running a capex intensive and operationally taxing infra business helped me immensely." While other doctor-entrepreneurs struggled with real estate and construction, Rao had a built-in advantage—family members who understood how to build at scale, manage contractors, and optimize capital deployment.

This wasn't just about money. Healthcare is fundamentally an infrastructure business masquerading as a service business. You need land, buildings, equipment, power backup, water treatment—all before you can perform your first surgery. Having brothers who understood project finance, construction timelines, and vendor management meant Rao could focus on what he did best: surgery and clinical protocols.

The philosophical foundation was set by the late 1990s. A surgeon who had performed thousands of procedures at both ends of the price spectrum. A business model proven at Mahavir—high volume, low cost, no compromise on outcomes. Family backing that understood capital-intensive businesses. And most importantly, a personal mission forged in the crucible of family tragedy. The stage was set for something bigger than a hospital—it was time to build a healthcare system. As we'll see, the first move would be to his hometown of Nellore, where the KIMS empire would officially begin.

III. Building the Foundation: Early Hospitals (2000-2010)

The year 2000 marked a pivotal moment when Dr. Bhaskar Rao Bollineni made his biggest bet yet in the dusty town of Nellore, 200 kilometers north of Chennai. The first hospital, initially named Bollineni Hospitals (now KIMS Hospital), was established in his hometown. "Early in the year 2000, we decided to set up our first hospital in Nellore — Bollineni Hospitals, named after my family," he would later recall.

The choice of Nellore wasn't random. This was home territory—Dr. Rao came from the village of Mamuduru in Nellore district. More importantly, it represented everything wrong with Indian healthcare: a bustling district of 3 million people with virtually no quality tertiary care. Chennai was three hours away by road; Hyderabad was six. If you had a heart attack in Nellore, you prayed, not planned.

The first hospital of the KIMS Hospitals group was established in 2000 at Nellore with a capacity of approximately 200 beds. It was founded in 2000 by Dr Bhaskar Rao Bollineni. KIMS Hospital, Nellore has 250 beds. Starting with roughly 200-250 beds, this wasn't just another nursing home. Dr. Rao equipped it with six operation theaters, six ICUs, a cath lab, and crucially, MRI and CT units—technology that most Tier 2 cities could only dream of. The message was clear: world-class healthcare didn't need a metropolitan pin code.

The Rapid Regional Expansion

What followed was a masterclass in strategic expansion. followed up by setting a diagnostic centre in Kadapa in 2001 and a few more hospitals in Rajahmundry, Srikakulam and Hyderabad over a decade. We quickly followed this up by launching a diagnostic centre in Kadapa in 2001 and a few more hospitals in Rajahmundry, Srikakulam and Hyderabad.

Shortly after, in 2002, he started another hospital in Rajahmundry. Rajahmundry, the cultural capital of Andhra Pradesh, got a 50-bed dedicated cardiac center. This wasn't a full hospital—it was a focused bet on cardiac care, leveraging Dr. Rao's core expertise. The model was simple: start with what you know best, prove the economics, then expand.

By 2004, the network was taking shape across Andhra Pradesh's rice bowl. Each location was chosen with surgical precision—district headquarters with population catchments of 2-3 million, agricultural prosperity ensuring payment capacity, and crucially, zero organized healthcare competition. While Apollo and Fortis fought over Hyderabad's Banjara Hills, KIMS was becoming the default choice for millions in Andhra's heartland.

The Philosophy Takes Root

The early hospitals revealed Dr. Rao's operating philosophy: "Bringing tertiary care to Tier 2-3 cities." This wasn't just geography—it was economics. Land costs were 80% lower than metros. Doctor salaries were 40-50% lower (young doctors preferred small towns over competing in saturated city markets). Construction costs were halved. And most importantly, these markets had zero price discovery—KIMS could charge ₹20,000 for procedures that cost ₹50,000 in cities, and patients would still save on travel, lodging, and family disruption.

The infrastructure approach borrowed heavily from his brothers' construction expertise. Each hospital followed a template: modular design allowing easy expansion, standardized equipment procurement leveraging bulk buying, and critically, building to 300-400 bed capacity even if starting with 150-200 operational beds. The unused space wasn't waste—it was optionality. As volumes grew, beds could be added without new construction.

The Turning Point: Private Equity Arrives

The year 2010 marked a turning point with the investment by Milestone Private Equity Fund (MPEF). After a decade of bootstrapped growth, institutional capital arrived. This wasn't just money—it was validation. PE firms had ignored healthcare outside metros, viewing it as too fragmented, too dependent on individual doctors, too hard to scale. KIMS proved them wrong.

The Milestone investment marked a philosophical shift. From a doctor-entrepreneur's personal mission, KIMS was transforming into an institutional healthcare platform. Corporate governance structures were implemented. Financial reporting was standardized. Most importantly, the expansion playbook was codified—what had been intuitive became systematic.

Building the Medical College: GEMS

One of the most strategic moves in this period was the medical college. is a member of the governing body of Aditya educational society that runs Great Eastern Medical School (GEMS) and hospital in the backward district of Srikakulam in AP. He is the pillar behind the success of this medical college and hospital that has won many laurels. GEMS is the most sought-after college for medical education in AP State, next only to the age-old Andhra Medical College.

GEMS is the first and only medical college in the whole country to obtain formal accreditation from the Royal College of Surgeons of England, one of the oldest and most renowned surgical college in the world. The accreditation is an award of excellence in recognition of outstanding surgery related educational provision by a surgical education centre. This wasn't just about education—it was about creating a talent pipeline. Every year, GEMS would produce doctors already trained in the KIMS way, familiar with its protocols, committed to its mission.

The Network Effect Emerges

By 2010, something interesting was happening. Patients from Nellore needing super-specialty care were being referred to KIMS facilities in other cities—not to Chennai or Hyderabad. The network was becoming self-reinforcing. A cardiac patient might start in Rajahmundry, get referred to Nellore for surgery, then to the upcoming Secunderabad facility for complex procedures. Each node strengthened the others.

The economics were compelling. the group has elevated the bed capacity at its hospitals by approx.15 times since its inception- from a 200-bed hospital at Nellore to a total of 3,064 beds (as of December 31, 2020). What started as a 200-bed hospital had laid the foundation for a 3,000+ bed network. The average revenue per occupied bed (ARPOB) in these Tier 2-3 cities was ₹11,758—less than half of Tier 1 cities, but the occupancy rates were consistently above 75%, and EBITDA margins exceeded 20%.

The first decade had proven the thesis: India's healthcare opportunity wasn't in competing with established players in saturated metros, but in bringing quality care to the 70% of Indians living in underserved markets. As we'll see, this foundation would enable KIMS to make its boldest move yet—taking on the established players in their own backyard with the launch of KIMS Secunderabad.

IV. The Flagship Gambit: KIMS Secunderabad (2004-2014)

Minister Road, Secunderabad, 2004. The construction site sprawled across five acres between the twin cities, dust clouds mixing with monsoon humidity. This wasn't supposed to be here. Apollo Hospitals dominated Jubilee Hills. Care Hospitals owned Banjara Hills. Yashoda controlled Somajiguda. The established players had carved up Hyderabad's premium healthcare real estate. And here was Dr. Bhaskar Rao, building what would become a 1,000-bed behemoth in unfashionable Secunderabad, betting that location mattered less than scale.

In 2004, KIMS Group's flagship hospital, KIMS Secunderabad was established. The brand "Krishna Institute of Medical Sciences", under Dr. B. Bhaskar Rao's aegis began its journey in 2004 with a 300 bed hospital on par with the then established hospitals of Hyderabad in professional excellence, the state of art technology and infrastructure facilities. What started as 300 beds would eventually scale to become a 1,000-bed hospital—one of the largest hospitals in a single location in South India.

The Location Paradox

The choice of Secunderabad was counterintuitive. This was the older, less glamorous twin city—government offices, military cantonment, middle-class neighborhoods. The Hyderabad elite went to Banjara Hills for healthcare, not Minister Road. But Dr. Rao saw what others missed: catchment. The location sat at the intersection of major highways connecting to districts across Telangana and Andhra Pradesh. Patients from Warangal, Karimnagar, Nizamabad—they all passed through Secunderabad.

More importantly, land was available and affordable. While competitors paid ₹10 crores per acre in Jubilee Hills, KIMS acquired five acres for a fraction of that cost. The savings went into equipment and talent. This was the infrastructure play again—why pay for prestigious addresses when you could invest in medical technology?

Building at Unprecedented Scale

We established our flagship hospital at Secunderabad in 2004 with a capacity of 150 beds, but the vision was always bigger. The facility was designed for 1,000 beds from day one—corridors wide enough for future expansion, electrical systems sized for additional floors, foundations strong enough to support vertical growth. This wasn't incremental thinking; it was building for dominance.

The numbers tell the story of ambition. This hospital has a bed capacity of 1,000 beds, including 885 operational beds, as of September 30, 2017. It has 12 Operating Theatres, a Pharmacy, NICUs, PICUs, and SICUs. The scale was unprecedented for a private hospital in South India at a single location.

The ICICI Ventures Partnership

In just over a decade, all of Dr Bhaskar's initiatives were doing exceedingly well and in 2011, ICICI Ventures came on board, helping the team in establishing their flagship hospital at Secunderabad. The private equity firm didn't just bring capital—they brought discipline. ICICI Venture saw what Milestone had seen earlier: a healthcare platform that could scale beyond individual hospitals into a system.

ICICI Ventures had invested Rs 2.2 billion in the company in 2014, though initial discussions began earlier. ICICI Ventures owns 28 per cent stake in KIMS while the promoters hold about 60 per cent and the rest with some of the doctors working with the healthcare chain. This structure was crucial—keeping doctors as shareholders aligned incentives, ensuring that clinical excellence wasn't sacrificed for financial returns.

Technology as Differentiator

KIMS Secunderabad became the testing ground for the group's technology ambitions. We were one of the first hospitals in Hyderabad to install 4-Arm HD da Vinci Robot technology at our hospital at Secunderabad. This wasn't just about having fancy equipment—it was about changing the competitive dynamics. When you're the only hospital in the state offering robotic surgery, geography becomes irrelevant. Patients will travel.

The technology investments were strategic. The da Vinci robot for minimally invasive surgery. Advanced imaging with 3 Tesla MRI. Novalis Tx for radiation oncology. Each piece of equipment was chosen to enable procedures that competitors couldn't offer. The message to the market was clear: you might have to drive to Secunderabad, but you'd get treatment unavailable anywhere else in the region.

Achieving Operational Excellence

By 2015, the results were undeniable. This hospital won the Best Multi Specialty Hospital Award at the Indo-Global Healthcare Summit & Expo 2015 and in 2016 received the Pharmacie De Qualite certification from Bureau Veritas. Our hospital at Secunderabad is accredited by the NABH and ISO 9001:2015 certification and has also been accredited by the NABL. It has received an award from the AHPI for nursing excellence in 2015 and was ranked the number one multi-specialty hospital in Hyderabad by the Times of India Survey in 2015.

These weren't participation trophies. NABH accreditation required demonstrating consistent clinical outcomes. ISO certification meant standardized processes across departments. NABL accreditation for the labs ensured diagnostic accuracy. Each certification built credibility, especially important when asking patients to choose an unfashionable location over established brands.

The Teaching Hospital Advantage

In addition to healthcare services, we also conduct medical education programmes through our affiliations with state medical boards and universities, for various broad and super specialities at our hospitals at Secunderabad and Rajahmundry, including for DNB, under graduation, post-graduation, PhD and diploma programmes. This transformed KIMS Secunderabad from a hospital into an academic medical center.

The teaching programs created a virtuous cycle. Young doctors got trained in the KIMS system. The best were offered positions. The presence of academic programs attracted senior consultants who wanted to teach. Research programs enhanced the hospital's reputation. And critically, having residents and students provided additional hands for patient care, improving economics while maintaining quality.

Clinical Milestones

The proof of the model came through clinical achievements. Heart surgeons at this hospital conducted a complex heart surgery on a 11-month-old baby from Zimbabwe. In 2019, KIMS Secunderabad recorded 1,000 kidney transplant surgeries. These weren't just numbers—they represented the transformation of Secunderabad from a secondary location into a quaternary care destination.

The organ transplant program became particularly significant. Building transplant capabilities requires more than equipment—you need specialized teams, 24/7 availability, complex coordination protocols. Most hospitals can't justify the investment. But at KIMS's scale, with 1,000 beds generating patient flow, the economics worked. Volume created expertise, expertise attracted more volume.

The Secunderabad Effect

By 2014, something remarkable had happened. KIMS Secunderabad wasn't competing with Apollo or Fortis for Banjara Hills patients. It had created its own market. Patients from northern Telangana districts who previously went to government hospitals now came to KIMS. Corporate employees from Secunderabad's IT corridor chose convenience over prestige. Most importantly, the hospital became the referral center for KIMS's entire network—complex cases from Nellore, Rajahmundry, and Srikakulam all came to the flagship.

The financial performance validated the strategy. While competitors with 300-400 bed hospitals struggled with 60% occupancy, KIMS Secunderabad consistently operated above 80%. The ARPOB might be lower than Jubilee Hills hospitals, but the absolute EBITDA was higher. Scale had trumped location.

As we transition to examining KIMS's role in public healthcare, it's worth noting that Secunderabad proved something fundamental: in healthcare, if you build it right, they will come. The flagship hadn't just succeeded—it had redefined what success looked like in Indian healthcare.

V. Political Innovation: The Aarogyasri Story (2007)

In early 2007, at the Chief Minister's office in Hyderabad, Dr. YS Rajasekhara Reddy met with Dr. Bhaskar Rao to discuss reimagining healthcare delivery for 70 million people. Dr. YSR, who had been a medical practitioner before entering public life, was known for charging just one rupee per consultation for the poor. As Chief Minister of undivided Andhra Pradesh, he brought this same commitment to serving the underprivileged to his healthcare policies.

What emerged from those meetings would become one of the world's largest health insurance programs. Dr. Bhaskar Rao was instrumental in formulating Rajiv Gandhi Aarogyasri scheme, first time launched in Andhra Pradesh in 2007 for providing health care to the poorest of the poor. He was the chief architect of Aarogyashri scheme for both creating it and implementing it successfully. This wasn't just policy consultation—Rao brought operational expertise from running hospitals that already served the poor profitably.

The Problem Statement

Earlier CM relief fund had spent Rs. 168.52 crores to help 55,362 below the poverty line (BPL) patients needing hospitalization. The system was broken—people begged for help, politicians granted favors, and most never got treatment. Simultaneously, Dalit movement highlighted problems of young children with heart ailments in the state. Soon, He announced free heart surgeries for these children, by August 2006, 4600 children were operated under the CM relief fund.

But this was triage, not treatment. The Doctor in the Chief Minister then wrote a right prescription that once for all removed the 'pain' of poor approaching for CM Relief Fund. His prescription was institutionalising the assistance. The vision was radical: instead of discretionary grants, create an entitlement. Instead of government hospitals that couldn't deliver, leverage private capacity. Instead of rationing care, make it universal for the poor.

The Aarogyasri Architecture

Rajiv Aarogyasri Health Insurance Scheme was launched on 01.04.2007. Initiated by the then chief minister of AP, the medical doctor YSR Reddy, the Rajiv Aarogyasri scheme started in 2007 and is targeted at the below-poverty line (BPL) population.

The scheme's genius lay in its simplicity. Rajiv Aarogyasri Scheme provides financial protection to families living below poverty line up to Rs. 2 lakhs in a year for the treatment of serious ailments requiring hospitalization and surgery. The scheme focuses on life-saving procedures that aren't covered elsewhere in India's patchwork of health programs, for which treatment protocols are available, and for which specialist doctors and equipment are required. Currently 938 tertiary care procedures are covered.

Dr. Rao's contribution went beyond design—he solved the implementation puzzle. Dr Bhaskar Rao explained his relationship with DR YS Rajasekahar Reddy and how he was able to give birth to the Arogysri scheme. Initially the government felt it would be a burden, then Dr Bhaskar Rao got into actual utilization of current government and private hospital beds and proved that there is 25% vacant. The insight was brilliant: India didn't lack hospital capacity; it lacked a payment mechanism to connect poor patients with existing beds.

The KIMS Advantage

For KIMS, Aarogyasri wasn't just another revenue stream—it transformed the business model. During the regime of Dr.Rajasekhara Reddy Rajiv Arogyasri scheme has covered 198.25 lakh families out of total of 229.11 Lakh families (87 per cent families covered). Suddenly, 87% of Andhra Pradesh's population became potential customers. The poor, who previously couldn't afford even basic procedures, now had insurance coverage for complex surgeries.

KIMS was perfectly positioned. Unlike Apollo or Fortis, which had built for the wealthy, KIMS had always optimized for volume over luxury. Their hospitals in Tier 2-3 cities were closer to rural beneficiaries. Their cost structure allowed profitable operations at government reimbursement rates. Most importantly, they understood the beneficiary mindset—these weren't customers choosing between hospitals, but patients grateful for any quality care.

The operational requirements favored prepared players. Hospitals have to deliver the 938 procedures for free according to pre-agreed clinical guidelines. Hospitals must fulfill several other conditions too, including employing an Aarogyasri medical coordinator, providing medicines for use after discharge, providing a follow-up consultation, and making available to the Aarogyasri reception a computer, printer, scanner, digital camera, webcam and 2 mbps connectivity. For KIMS, with its systematic processes and IT infrastructure, compliance was straightforward. For smaller hospitals, it was overwhelming.

The Network Effect

The private sector far outnumbers the public sector: 80 percent of Aarogyasri admissions to date have been in private hospitals. This wasn't market failure—it was market reality. Government hospitals lacked equipment, staff, and motivation. Private hospitals had capacity but no paying patients. Aarogyasri connected supply with demand.

For KIMS, the impact was transformative. In their Tier 2-3 city hospitals, Aarogyasri patients often comprised 40-50% of admissions. The guaranteed payment (even if delayed) provided steady cash flow. The high volumes enabled better utilization of expensive equipment. Most importantly, it created a moat—new entrants couldn't easily achieve the scale needed to serve Aarogyasri patients profitably.

The Health Camp Innovation

They are required to mount a "health camp" every week at a place chosen by the Trust and to provide everyone attending with a general health check and a screening for relevant health conditions; patients attending these camps account for 45 percent of Aarogyasri admissions. This requirement became KIMS's customer acquisition engine. Weekly health camps in villages weren't just screening exercises—they were brand-building events. Villagers who had never seen a doctor now met specialists from KIMS. Trust was built before treatment was needed.

The camps also solved the identification problem. Many beneficiaries didn't know they had serious conditions until screened. Early detection meant better outcomes and, crucially for KIMS, more procedures covered under Aarogyasri before conditions became too advanced (and expensive) to treat.

National Replication

This well formulated scheme has become so popular that the other States in India have emulated it time and again. There have been several attempts to introduce similar schemes in other States but Andhra Pradesh has been one of the only states to successfully roll out the scheme. The model's success triggered nationwide replication—from Gujarat's Mukhyamantri Amrutam to the eventual Ayushman Bharat, India's healthcare policy shifted from building government hospitals to leveraging private capacity.

For KIMS, being present at the creation gave them unique advantages. They understood the operational requirements, had relationships with scheme administrators, and most importantly, had proven they could deliver quality care profitably at government rates. As other states launched similar programs, KIMS was ready to participate from day one.

The Criticism and Reality

Not everyone was pleased. The media is full of reports 'aarogyasri as corporate dhanasri' (God of money), 'corporate hospitals loot aarogyasri funds', 'aarogyasri has turned in to anarogyasri (illhealth)' 'aarogyasri is a Kalpavriksham (tree of boon) for corporate hospital. The whole logic of spending crores of rupees under aarogyasri for surgeries/tertiary care is also spoken as 'for a nail size profit it is mountain size corruption'.

The criticism missed the point. Yes, private hospitals benefited. But A total of 105,712 treatments had been authorised from April 1, 2007 to September 30, 2008. We analysed 89,699 treatments undertaken for 71,549 beneficiaries. In 18 months, more people received complex treatments than in the previous decade. The question wasn't whether private hospitals profited, but whether the poor got care. They did.

The Lasting Impact

Aarogyasri fundamentally changed Indian healthcare economics. It proved that the poor were a viable market if payment mechanisms existed. It showed that private hospitals could profitably serve all segments, not just the wealthy. Most importantly for KIMS, it validated their model—being the low-cost provider wasn't a disadvantage when the government became the payor.

While his Rajiv Aarogyasri Scheme is being applauded internationally, other States followed suit as also Central Government with different nomenclature. Today's Ayushman Bharat, covering 500 million Indians, is essentially Aarogyasri at national scale. And KIMS, having helped design and implement the original, was perfectly positioned to benefit from its expansion.

The Aarogyasri story reveals a deeper truth about Indian healthcare. The constraint was never infrastructure or medical talent—India had both. The constraint was connecting those who needed care with those who could provide it. By solving that connection problem, Dr. Rao didn't just help create a government scheme—he helped create an industry. And KIMS, as both architect and beneficiary, would ride that wave to become one of India's healthcare giants.

VI. Second Generation & Scaling Up (2014-2020)

The boardroom at KIMS Secunderabad, 2014. Dr. Bhaskar Rao looked across the table at his son, Dr. Abhinay Bollineni, freshly returned from the United States. Dr. Abhinay joined KIMS Hospitals in 2013, working in Hospital Operations before leading Strategy & Marketing in 2015. An MBBS graduate from Deccan Medical College (2010), he was selected by Hillary Clinton's office in 2011 for the US Department of State's 'International Visitor Leadership Program on Oncology.'

This wasn't nepotism—it was succession planning at its most strategic. When Abhinay Bollineni joined KIMS Hospitals in 2014, the healthcare sector was in its early stages. Only a handful of private hospital conglomerates started out as pioneers. Five years on, when he assumed the role of CEO, competition was at an all-time high and international players were getting bigger and bigger, giving KIMS Hospitals the chance to master the art of operating at low costs and high volume.

The Generational Transition

The timing was perfect. Dr. Rao, now in his 60s with 30,000+ surgeries behind him, needed to shift from operator to strategist. Abhinay brought fresh perspective—medical training combined with exposure to global healthcare systems. He was named in Business World's "BW 40 Under 40" list in 2019. But more importantly, he understood that KIMS's next phase required different skills: financial engineering, digital transformation, and most crucially, acquisition integration.

Under his leadership, and that of Dr. Abhinay Bollineni, who joined KIMS in 2014, we have expanded into nine cities across AP and Telangana through a combination of greenfield. Dr. Abhinay Bollineni, who joined KIMS in 2014, paved the way to expand KIMS Group into nine cities across AP and Telangana through a combination of greenfield, brownfield and acquisition-led expansion. Dr. Abhinay assumed our CEO position in 2019 and played a leadership role in expanding the KIMS' network over the last 7 years, including in the launch of KIMS Kondapur and the acquisitions of our hospitals in Ongole, Vizag, Anantapur and Kurnool.

The Kondapur Launch: Competing with IT Money

2014 marked KIMS's boldest move yet—entering Hyderabad's IT corridor. 2014: Kondapur in Hyderabad Kondapur wasn't Secunderabad. This was new Hyderabad—glass towers, tech campuses, young professionals with corporate insurance. Apollo and Continental already dominated this market. Why would anyone choose KIMS?

Coinciding with Abhinay's introduction as CEO was the launch of KIMS Hospital in Kondapur and the acquisitions of hospitals in Ongole, Vizag, Anantapur, Kurnool and the recent acquisition of Sunshine Hospitals. Today, the network consists of facilities that are strategically located to serve the healthcare needs of the state of Telangana across urban Tier-1 cities such as Secunderabad and Hyderabad.

The answer lay in positioning. While competitors built luxury hospitals charging ₹50,000+ for deliveries, KIMS Kondapur offered the same clinical quality at 60% of the price. The target wasn't the tech executive but the larger ecosystem—the security guards, housekeeping staff, contract employees, and even the middle management who found Apollo unaffordable despite having insurance.

The Acquisition Machine Kicks Into Gear

2017: Ongole, Andhra Pradesh The real transformation began with acquisitions. We have significantly expanded our hospital network in recent years through our acquisitions of hospitals in Ongole in Fiscal Year 2017, Vizag and Anantapur in Fiscal Year 2019 and Kurnool in Fiscal Year 2020. KIMS Hospital have significantly expanded the hospital network in recent years through acquisitions of hospitals in Ongole in Fiscal Year 2017, Vizag and Anantapur in Fiscal Year 2019 and Kurnool in Fiscal Year 2020.

The Ongole acquisition in 2017 set the template. This was a struggling 150-bed hospital with good infrastructure but poor management. KIMS paid a fraction of replacement cost, retained the staff, upgraded equipment selectively, and most importantly, plugged it into their network. Within 18 months, occupancy went from 40% to 75%.

The 2018-2019 Expansion Blitz

2018: Vishakapatnam, Andhra Pradesh. In 2018, KIMS opened a multi-speciality hospital in Vizag. Vizag was different—a major port city with established competition. Dr. B. Bhaskara Rao, CMD, KIMS Hospitals, said, "This is our 2nd Hospital in Vishakapatnam (KIMS-ICON Hospitals was acquired in 2018). This is KIMS' second acquisition in the city, following the purchase of KIMS-ICON Hospitals in 2018.

2019: Anantapur & Kurnool, Andhra Pradesh. KIMS-Saveera Hospital in Anantapur is the largest healthcare facility in the Rayalaseema region. The group also opened an emergency clinic in Anantapur in 2019. The 2019 double acquisition of Anantapur and Kurnool was audacious. Two hospitals, 500+ beds combined, acquired simultaneously. Both were distressed assets—Anantapur's Saveera Hospital was the largest in the Rayalaseema region but bleeding cash; Kurnool's facility had good infrastructure but terrible management.

The Integration Playbook

Approximately one-third of hospital 3,064 beds were launched in the last four years and have added over 880 beds, in aggregate, in our hospitals in Visakhapatnam (Vizag), Anantapur and Kurnool in Fiscal Years 2019 and 2020, and improved the overall bed occupancy rate in these hospitals from 71.83% to 80.49% in the same period. We have added over 880 beds, in aggregate, in our hospitals in Visakhapatnam (Vizag), Anantapur and Kurnool in Fiscal Years 2019 and 2020, and improved the overall bed occupancy rate in these hospitals from 71.83% to 80.49% in the same period.

The transformation was remarkable. In just two years, these acquisitions added 880+ beds and saw occupancy rates jump from 71.83% to 80.49%. How? The playbook was systematic:

- Day 1-30: Stabilize operations, ensure salary payments, fix broken equipment

- Month 2-3: Implement KIMS protocols, standardize pricing, launch Aarogyasri registration

- Month 4-6: Selective equipment upgrades, recruit 2-3 star doctors in key specialties

- Month 7-12: Marketing blitz, health camps, referral network activation

- Year 2: Full integration, cross-referrals from other KIMS hospitals, occupancy optimization

The Technology Push

As far as medical technology is concerned, we're one of the initial few companies to utilise it," Abhinay notes. "We're putting technology in place," Abhinay says. "From the entry at reception to the diagnostic test and the report being generated, to the doctor reviewing that report. We are figuring out ways to ensure the maximum utilisation of a facility." "If you look at the da Vinci System, we were the first hospital in South India and the second in India to purchase and use the machine. We are acquiring robotics for orthopaedics, and if you look at the Hyderabad landscape, the maximum investment in robotics is done by KIMS.

Under Abhinay's leadership, technology became central to the expansion strategy. This wasn't just about buying fancy machines—it was about using technology to manage a distributed network. Electronic health records meant a patient's history from Nellore was accessible in Vizag. Telemedicine allowed Secunderabad specialists to consult on complex cases in Kurnool. Centralized procurement drove down costs across all hospitals.

Building the Acquisition Capability

Disciplined approach to acquisitions resulting in successful inorganic growth. Company has a successful history of sourcing, executing and integrating acquisitions and has a disciplined, low-leverage approach to acquisitions that has enabled KIMS hospital to maintain the affordable pricing model as company has grown in both Tier 1 and Tier 2-3 markets. Company acquires hospitals that can fit into our hospital network and match our existing hospital profile in terms of specialties, technologies and healthcare professionals.

By 2019, KIMS had become an acquisition machine. They had a dedicated team scouting distressed assets. They knew exactly what to look for: good location, decent infrastructure, salvageable reputation, and most importantly, a price that allowed profitability even at KIMS's lower price points. They walked away from more deals than they closed—discipline mattered more than growth.

Managing Rapid Scale

Approximately one-third of our 3,064 beds were launched in the last four years. Approximately one-third of our 3,064 beds were launched in the last four years. The numbers were staggering. One-third of KIMS's total bed capacity was added in just four years. This wasn't organic growth—this was transformation. From a regional player with 2,000 beds to a dominant force with 3,000+ beds, KIMS had changed the competitive dynamics of South Indian healthcare.

The CEO Transition

Shortly after that, he was appointed as the CEO in 2019. Shortly after that, he was appointed as the CEO in 2019. When Abhinay officially became CEO in 2019, it marked more than a generational transition. It signaled to the market that KIMS was ready for its next phase—going public. The founder-doctor model had built the foundation, but capital markets needed professional management. Abhinay represented that bridge—medical credibility from his father, modern management from his training.

Regional Dominance Achieved

We operate 9 multi-specialty hospitals under the "KIMS Hospitals" brand, with an aggregate bed capacity of 3,064, including over 2,500 operational beds as of December 31, 2020, which is 2.2 times more beds than the second largest provider in AP and Telangana, according to the CRISIL report. Company has 3,064 beds across nine multi-specialty hospitals in AP and Telangana as of December 31, 2020, which is 2.2 times more beds than the second largest provider in AP and Telangana.

By 2020, the transformation was complete. KIMS had 2.2 times more beds than the second-largest provider in AP and Telangana. This wasn't just scale—it was dominance. In a fragmented industry where the largest player (Apollo) had less than 2% market share nationally, KIMS had achieved something remarkable: regional monopoly in affordable healthcare.

Learning from Peers, But Differently

We have learned a couple of things from our peers," he tells The CEO Magazine. "One should not expect to become a national player immediately – first, one strives to become a dominant state player; second, a dominant regional player; third, a multiregional player; and finally, a national player.

This philosophy guided everything. While Fortis chased national presence and Manipal built medical colleges, KIMS focused on dominating two states. The logic was compelling: better to own 30% of Andhra Pradesh than 1% of India. Regional dominance meant pricing power, referral networks, government relationships, and most importantly, brand trust that money couldn't buy.

The period from 2014 to 2020 transformed KIMS from a successful regional player into a healthcare powerhouse ready for public markets. The second generation hadn't just maintained the founder's legacy—they had amplified it. As we transition to examining the IPO journey, it's worth noting that this expansion phase proved something crucial: in Indian healthcare, execution beats strategy, and no one executed quite like KIMS.

VII. The IPO & Public Market Journey (2021)

VII. The IPO & Public Market Journey (2021)

The conference room at Kotak Mahindra Capital's Mumbai office, March 2021. Dr. Bhaskar Rao and Dr. Abhinay Bollineni faced a wall of screens showing market data, hospital metrics, and financial projections. After three years of preparation—General Atlantic's entry in 2018, COVID proving the resilience of the model, and a healthcare sector suddenly in vogue—the moment had arrived. KIMS would test public markets at a time when Indian healthcare had never been more valuable or more scrutinized.

The IPO window opened on June 16, 2021, and closed on June 18, 2021. The timing was exquisite. India was emerging from the second COVID wave, healthcare stocks were trading at historic highs, and retail participation in IPOs had reached unprecedented levels. But this wasn't just opportunism—KIMS had spent three years preparing for this moment, cleaning up its balance sheet, standardizing operations, and most importantly, proving that affordable healthcare could generate superior returns.

The IPO Architecture

The size of the IPO was ₹2,143.74 crore, comprising a fresh issue of 2,424,242 equity shares aggregating to ₹200 crore and an offer for sale of 23,560,538 shares aggregating to ₹1,943.74 crore. The structure told the story—this was primarily an exit opportunity for early investors, with minimal dilution for existing shareholders. IPO was primarily to facilitate PE fund General Atlantic halving its 41% stake, as this accounted for 62% of the total issue.

The price band was set at ₹815-825 per share, valuing the company at approximately ₹6,600 crore at the upper band. For context, this was roughly 5x FY21 revenues—aggressive but not unreasonable given 20% revenue growth during a pandemic year. The lot size was 18 shares, making the minimum investment ₹14,670 for retail investors—accessible enough to attract broad participation but high enough to filter out purely speculative interest.

The Anchor Book: Institutional Validation

KIMS raised ₹956 crore from 43 anchor investors ahead of the IPO, with domestic investors including HDFC Trustee, Axis Mutual Fund, ICICI Prudential, Nippon Life India, IDFC MF, UTI MF, Mirae MF, and HDFC Life Insurance Company, while marquee international investors included Nomura Funds, Goldman Sachs, and Societe Generale. This wasn't just capital—it was validation from some of the world's most sophisticated healthcare investors.

The anchor allocation revealed institutional thinking. Domestic mutual funds, who understood the Aarogyasri dynamics and regional dominance story, took large positions. International investors, attracted by the India healthcare theme post-COVID, provided global credibility. The ₹956 crore raised from anchors represented 45% of the total issue size—a strong vote of confidence.

The Subscription Drama

The KIMS IPO subscription status stood at 3.86 times, with retail investors subscribing 2.90 times, QIBs 5.26 times the issue size, and non-institutional investors 1.89 times. These numbers require context. In a market where popular IPOs were getting subscribed 50-100 times, 3.86x seemed modest. But this reflected KIMS's positioning—a serious investment opportunity for long-term investors, not a lottery ticket for day traders.

The category-wise subscription told different stories. QIBs subscribing 5.26 times showed institutional conviction—they understood the business model, the regional dominance, and the long-term growth potential. Retail subscription at 2.90 times was healthy but not frenzied—individual investors were participating but not betting the farm. The relatively weak NII subscription at 1.89x suggested HNIs were lukewarm, perhaps concerned about valuations or preferring other concurrent IPOs.

The Pricing Paradox

At ₹825 per share (upper band), KIMS was asking investors to value it at 31 times FY21 earnings. For comparison, Apollo Hospitals traded at 238x earnings, but Apollo was a national brand with metropolitan presence. Narayana Health, a closer peer with similar focus on affordable care, traded at around 40x. The pricing reflected a Goldilocks strategy—not so high as to deter value investors, not so low as to leave money on the table.

The fresh issue of ₹200 crore was ostensibly to repay ₹150 crore of debt, though the company was already cash-rich. This financial engineering served a purpose—achieving a debt-free status made KIMS more attractive to conservative institutional investors. The real story was the OFS component—early investors taking money off the table while retaining enough skin in the game.

Listing Day and Beyond

The shares listed on BSE and NSE on June 28, 2021. The grey market premium had been volatile, ranging from flat to ₹50-60 in the days before listing, suggesting cautious optimism rather than euphoria. The listing day performance would be crucial—a strong debut would validate the IPO pricing and create momentum for the stock.

What happened next surprised even the optimists. With a 40% rally in July, KIMS stock zoomed 61% from its issue price of ₹825 as institutional investors lapped up the company's shares post listing. The post-listing surge wasn't driven by retail euphoria but by institutional accumulation. Mutual funds that couldn't get adequate allocation in the IPO were buying in the secondary market. The stock's outperformance validated the thesis—quality healthcare assets in India were scarce, and KIMS's unique positioning justified premium valuations.

The General Atlantic Exit Strategy

General Atlantic had invested ₹929.16 crore for a 38.99% stake in June 2018, followed by an additional ₹55.60 crore for 1.92% stake in May 2019. Their partial exit through the IPO was masterfully executed—selling enough to book substantial profits while retaining sufficient stake to benefit from future upside. As of June 30, 2022, General Atlantic still held a 17.24% stake in the company.

The staggered exit strategy revealed sophisticated thinking. Rather than dumping their entire stake at IPO, General Atlantic chose to remain a significant shareholder, signaling continued confidence in the business. Their subsequent stake sales—16.60 lakh shares in September 2022 and 12.10 lakh shares representing 1.5% stake for ₹151.25 crore—were timed to minimize market impact while maximizing returns.

Market Positioning Post-IPO

The public listing transformed KIMS from a regional healthcare provider into a market darling. The market cap of ₹29,060 crore by 2024 represented a more than 4x increase from the IPO valuation. This wasn't just multiple expansion—revenues and profits had grown, new hospitals had been added, and most importantly, KIMS had proven that its model could scale beyond Andhra Pradesh and Telangana.

The IPO also provided crucial benefits beyond capital. Listed company status made acquisitions easier—sellers preferred stock consideration from a public company with transparent valuations. Employee stock options became more attractive with liquid stock. Most importantly, the quarterly scrutiny of public markets enforced discipline—every decision now had to consider shareholder impact.

Institutional Evolution

The transition from private to public ownership marked a philosophical shift. The company that had started as a doctor's mission to serve the poor was now accountable to thousands of shareholders expecting returns. This could have created conflict, but KIMS managed the balance brilliantly—maintaining its focus on affordable healthcare while delivering market-beating returns.

The IPO proceeds deployment was swift and strategic. Debt repayment was completed immediately, achieving the promised debt-free status. The general corporate purposes allocation went toward working capital and selective equipment upgrades. Within months of listing, KIMS was back in acquisition mode, using its elevated currency (stock) and strong balance sheet to consolidate the regional healthcare market.

The Contrarian Success

In an IPO market obsessed with technology startups and new-age businesses, KIMS represented something different—a profitable, asset-heavy, regional healthcare company run by doctors, not MBAs. The success challenged conventional wisdom. You didn't need to be in metros to create value. You didn't need venture capital pedigree to access public markets. You didn't need to burn cash for growth.

While hospital stocks had hardly created investor wealth, with Shalby, Aster, Healthcare Global still trading below IPO price even after 3 years, KIMS broke the pattern. The difference was execution—consistent occupancy above 75%, steady margin expansion despite lower prices, and most importantly, deep understanding of the markets they served.

The IPO marked the end of one chapter and the beginning of another. KIMS was no longer just Dr. Bhaskar Rao's vision—it was now a public trust, accountable to shareholders but still committed to its founding mission. As we'll explore in the next section, this dual identity would shape every strategic decision going forward.

VIII. Business Model & Unit Economics Deep Dive

The Excel spreadsheet glowed on the analyst's screen at a Mumbai mutual fund office, late 2023. Row after row of numbers told a story that shouldn't exist: a hospital chain with 40% gross margins charging half what Apollo charges, 80% occupancy in Tier 2 cities where others struggle to hit 50%, and most remarkably, generating ₹20,000+ per bed daily while serving 40% government scheme patients. The analyst had one question: "How is this possible?"

The answer lies in what might be the most sophisticated unit economic model in Indian healthcare—one that treats healthcare delivery not as an art but as an industrial process, where every rupee is tracked, every bed-hour optimized, and every procedure standardized. This is the KIMS machine, and understanding how it works reveals why a regional player commands valuations comparable to national chains.

The Service Portfolio Architecture

The company offers healthcare services in specialties and super specialties across more than 40 fields. But unlike peers who chase every possible specialty, KIMS's portfolio is carefully curated. The core remains cardiovascular—leveraging Dr. Rao's expertise and the highest margin procedures. Surrounding this are complementary specialties: cardiology leads to nephrology (kidney disease correlates with heart disease), which leads to diabetes care, which connects to ophthalmology.

Each specialty addition follows a framework: Is there adequate patient volume in our catchment? Can we achieve leadership position? Does it leverage existing infrastructure? Will it drive cross-referrals? This discipline means KIMS might not offer robotic knee surgery in Nellore, but their cardiac program rivals anything in metros.

Scale and Network Configuration

As of March 31, 2021, KIMS operates through 9 multi-specialty hospitals with an aggregate bed capacity of 3,064, including over 2,500 operational beds. But raw bed count misses the sophistication. The network is configured in a hub-and-spoke model: Secunderabad's 1,000-bed flagship as the quaternary care hub, 300-500 bed hospitals in district headquarters as secondary hubs, and 150-200 bed facilities as spokes.

This configuration creates powerful economics. A patient presenting with chest pain in Ongole gets initial treatment there. If they need angioplasty, they're referred to Nellore. Complex cardiac surgery? Secunderabad. Each level up the chain commands higher prices and margins, but the patient stays within the KIMS network. The lifetime value of a cardiac patient might be ₹3-5 lakhs over multiple procedures and follow-ups.

Revenue Model Breakdown

The FY21 numbers revealed the model's resilience. Revenue grew 18% YoY to ₹1,330 crore despite 20% patient footfall drop, as average revenue per operational bed (ARPOB) rose 13% YoY due to COVID, improved surgery mix, and maturation of 900 beds added in the last 4 years. This seemingly paradoxical result—fewer patients, more revenue—unveiled the power of case mix optimization.

During COVID, elective procedures dropped but critical care surged. ICU beds generating ₹40,000-50,000 daily replaced general ward beds at ₹5,000-8,000. Ventilator patients, ECMO procedures, and complex COVID management drove ARPOB to unprecedented levels. The 1,000-bed Secunderabad hospital, accounting for 40% of bed capacity, reported a 47% jump in ARPOB.

The ARPOB Arbitrage

In Fiscal Year 2020, ARPOB for hospitals in Tier 1 cities was ₹27,410 while ARPOB for hospitals in Tier 2-3 cities was ₹11,758. This dramatic difference reflects strategic positioning. The Tier 2-3 facilities focus on volume—basic surgeries, deliveries, and primary care at prices the middle class can afford. These procedures might be low-margin individually but generate steady cash flow and build customer relationships.

The Tier 1 facilities in Secunderabad and Kondapur handle complex cases—organ transplants, robotic surgeries, advanced oncology. Here, KIMS competes directly with Apollo and Fortis but at 70% of their prices. A liver transplant at Apollo might cost ₹25 lakhs; KIMS does it for ₹18 lakhs. The patient saves money, KIMS makes margins, and the volume allows them to build expertise.

Occupancy: The Hidden Profit Driver

KIMS maintains high occupancy rates of approximately 79%, compared to the industry average of 65%. This 14 percentage point difference is worth hundreds of crores in profit. Hospital economics are brutal—below 50% occupancy, you lose money; above 70%, you print money. Every incremental patient above break-even occupancy contributes almost entirely to EBITDA.

KIMS achieves this through three mechanisms. First, the Aarogyasri base load—government scheme patients provide 40-50% guaranteed occupancy. Second, the referral network—each KIMS hospital feeds patients to others. Third, price accessibility—when you're the only quality option at affordable prices, utilization follows.

The Government Scheme Economics

The Aarogyasri relationship is widely misunderstood. Yes, government reimbursements are lower—₹50,000 for a procedure that might bill ₹1 lakh privately. But the economics work because of volume and predictability. A cardiac surgeon can schedule 4-5 Aarogyasri bypasses on Monday, knowing the patients are pre-approved, the payment (though delayed) is guaranteed, and the hospital achieves full utilization.

Moreover, Aarogyasri patients often require follow-up care not covered by the scheme. A bypass patient needs medication, regular check-ups, and eventually, other procedures. These become private-pay services. The scheme brings patients into the KIMS ecosystem; the ecosystem generates lifetime value.

Capital Efficiency Metrics

KIMS's capital efficiency is remarkable. While Apollo spends ₹70-80 lakhs per bed for new hospitals, KIMS achieves similar clinical capabilities at ₹40-45 lakhs per bed. This isn't about cutting corners—it's about choices. Imported Italian marble versus local granite. Four-patient rooms versus single-occupancy suites. Functional design versus architectural statements.

The payback periods reflect this efficiency. A typical KIMS hospital achieves EBITDA break-even in 18-24 months and cash payback in 4-5 years. Compare this to metro hospitals that take 3-4 years to break even and 7-8 years for payback. Lower capital intensity means higher returns on invested capital (ROIC), which drives valuations.

The Margin Architecture

Despite charging significantly lower prices, KIMS maintains EBITDA margins above 20%. The margin bridge from revenue to EBITDA reveals the model:

- Gross Margins (40-45%): Lower than peers' 50-55% due to price positioning

- Doctor Costs (18-20%): Consultant model keeps this variable

- Staff Costs (12-15%): Lower absolute salaries in Tier 2-3 cities

- Operating Expenses (8-10%): Simplified operations, limited marketing

- EBITDA Margins (20-25%): Volume and efficiency offset lower pricing

Technology ROI

The technology investments follow clear ROI frameworks. The da Vinci robot at Secunderabad, costing ₹15 crores, needs to perform 200 procedures annually at ₹2 lakhs each to break even. KIMS does 300+, generating ₹2 crores in annual profit from this single machine. Each technology investment must pass this test—will it pay back in 3 years through higher prices, more volume, or both?

The Working Capital Advantage

KIMS's working capital management is superior to peers. Average collection period is 45-50 days versus industry standard of 60-70 days. This happens because of patient mix—cash-paying customers are 30%, insurance (quick payment) is 25%, and even government schemes, though delayed, are predictable. The company factors Aarogyasri receivables, converting 180-day payments into 30-day cash at a small discount.

Network Effects in Action

Each additional hospital makes the existing network more valuable. A new facility in Kurnool doesn't just add 200 beds—it provides referrals to Secunderabad, receives transfers from Anantapur, and justifies investment in specialized equipment that serves the entire region. The network effects are measurable: hospitals in the network show 10-15% higher occupancy than comparable standalone facilities.

The Acquisition Economics

KIMS's acquisition model is formulaic: buy distressed hospitals at 0.3-0.5x replacement cost, invest 20-30% of purchase price in upgrades, achieve 70%+ occupancy within 18 months. The returns are compelling—₹50 crore investment in a 200-bed hospital generates ₹8-10 crores annual EBITDA, a 5-year payback with perpetual returns thereafter.

Competitive Moats

The unit economics create formidable moats. A new entrant in Nellore would need to match KIMS's prices (impossible with higher capital costs), achieve similar occupancy (difficult without brand trust), and access government schemes (requires scale and relationships). Even if they succeeded, they'd be competing for market share in a market KIMS created. It's easier to target another city.

Future Scalability

The model's scalability is proven but not infinite. Each move away from the Andhra Pradesh-Telangana base weakens the network effects. Doctor recruitment becomes harder without the GEMS pipeline. Government scheme dynamics differ by state. This is why KIMS's expansion into Tamil Nadu and Maharashtra will be the ultimate test—can the unit economics work without the home advantages?

The deep dive into KIMS's business model reveals a paradox resolved: world-class healthcare at affordable prices generating superior returns. It's not magic—it's meticulous optimization of every variable in the healthcare delivery equation. As we'll explore next, this operational excellence extends to clinical capabilities, where KIMS has quietly built centers of excellence that rival any hospital in India.

IX. Technology & Clinical Excellence

The operating room at KIMS Secunderabad, 3 AM, March 2020. Dr. Rao's team was attempting something unprecedented—a double lung transplant on a COVID-19 patient whose lungs had been destroyed by the virus. The ECMO machine kept the patient alive as surgeons worked with robotic precision. Sixteen hours later, success. India's first COVID lung transplant was complete. Within months, KIMS would perform 50+ such procedures, becoming the unlikely global leader in a procedure most hospitals wouldn't attempt.

This scene captures the KIMS paradox—a hospital chain known for affordable healthcare had somehow become a pioneer in India's most advanced medical procedures. The answer lies in a technology strategy that views cutting-edge equipment not as luxury but as democratization tool, bringing procedures previously available only to the ultra-wealthy within reach of the middle class.

The Robotic Surgery Revolution

KIMS was the first hospital in South India and second in India to purchase and use the da Vinci robot system. When KIMS installed its first da Vinci robot in 2011, Apollo and Fortis were still debating ROI. The ₹15 crore investment seemed insane for a hospital charging half what metros did. But Dr. Rao saw what others missed—robotic surgery wasn't just about prestige; it was about outcomes.

Consider prostate surgery. Traditional open surgery meant 7-10 days hospitalization, significant blood loss, and months of recovery. Robotic surgery reduced this to 2-3 days hospitalization, minimal blood loss, and weeks of recovery. Even at KIMS's lower prices, the math worked—shorter stays meant higher bed turnover, better outcomes meant more referrals, and being first meant monopoly pricing power for years.

By 2019, KIMS's robotic surgery program had performed over 3,000 procedures. The expertise accumulation created a virtuous cycle—more procedures meant better outcomes, better outcomes meant more patients, more patients meant investment in additional robots. Today, KIMS has robotic systems for urology, cardiac surgery, and orthopedics—one of the most comprehensive robotic surgery programs in India.

The Organ Transplant Center of Excellence

By 2019, KIMS Secunderabad had recorded 1,000 kidney transplant surgeries. Building transplant capability requires more than equipment—you need specialized surgical teams, 24/7 organ retrieval capability, complex coordination protocols, and most critically, volume to maintain expertise. Most hospitals can't justify the investment. KIMS could because of scale.

The transplant program revealed KIMS's clinical philosophy. They didn't just do kidney transplants; they built an integrated program covering liver, heart, and eventually lung transplants. Each organ program supported the others—shared ICU protocols, common immunosuppression expertise, and crucially, the ability to handle multi-organ failure patients that single-organ centers couldn't manage.

The economics were compelling. A kidney transplant at KIMS costs ₹5-6 lakhs versus ₹8-10 lakhs at Apollo. But the patient gets the same quality—sometimes better, given KIMS's higher volumes. The program also created a halo effect—if KIMS could do transplants at affordable prices, patients trusted them for everything else.

ECMO Leadership: The COVID Differentiator

KIMS's ECMO (Extracorporeal Membrane Oxygenation) program began in 2013, years before COVID made it famous. With 18 ECMO machines, KIMS had the largest ECMO program in South India. ECMO is the ultimate life support—taking over heart and lung function when organs fail. Each machine costs ₹50 lakhs; each patient needs specialized nursing, and mortality rates are high even in the best centers.

When COVID hit, this investment paid off spectacularly. KIMS could offer ECMO support when even premier institutes couldn't. They performed India's first COVID lung transplant, then another 50+. Each success story went viral—literally saving lives others had given up on. The reputational value was incalculable. KIMS wasn't just an affordable hospital anymore; it was where you went when no one else could save you.

Advanced Imaging and Diagnostics

The diagnostic infrastructure at KIMS rivals research institutions. 3 Tesla MRI machines, PET-CT scanners, and advanced catheterization labs aren't just available—they're utilized at rates that justify the investment. The Secunderabad facility performs 100+ MRIs daily, 50+ CT scans, and dozens of interventional procedures. This volume allows KIMS to offer advanced imaging at ₹5,000-8,000 versus ₹12,000-15,000 elsewhere.

The technology deployment follows a template: buy the best equipment, hire operators from premier institutes, price at 60% of market rates, and run at 3x utilization. A 3 Tesla MRI costing ₹15 crores needs 20 scans daily at ₹8,000 to break even. KIMS does 40+, generating ₹5 crores annually from a single machine.

The Radiation Oncology Platform

Cancer treatment represents the future of Indian healthcare—rising incidence, high treatment costs, and desperate need for affordable options. KIMS built its oncology platform methodically: medical oncology (chemotherapy) first, then radiation oncology, finally surgical oncology. Each builds on the previous, creating an integrated cancer center.

The Novalis Tx linear accelerator for radiation therapy cost ₹25 crores—one of the largest single equipment investments. But it enables procedures like stereotactic radiosurgery that few centers offer. A brain tumor treatment that costs ₹5 lakhs at Tata Memorial can be done at KIMS for ₹3 lakhs. The volume from affordable pricing justifies the investment.

Clinical Protocols and Standardization

Technology is only as good as its implementation. KIMS's clinical excellence comes from standardized protocols across the network. Every heart attack follows the same treatment pathway whether in Secunderabad or Srikakulam. This standardization seems obvious but is rare in Indian healthcare where each doctor practices independently.

The protocols are evidence-based but cost-conscious. International guidelines might recommend Drug A; KIMS uses equally effective Drug B at 30% lower cost. The savings fund technology investments. This balance—clinical excellence without gold-plating—defines the KIMS approach.

The Training Infrastructure

Excellence requires continuous skill development. KIMS's academic programs aren't just about producing doctors—they're about creating specialists trained in KIMS protocols. A cardiac surgery resident learns not just how to operate but how to achieve excellent outcomes at affordable costs. This培训 philosophy extends to nursing, technicians, and support staff.

The simulation lab at Secunderabad rivals medical colleges. Surgeons practice robotic procedures, nurses train on ECMO protocols, and technicians learn equipment maintenance. This investment in training seems expensive until you realize it prevents errors that cost lives and lawsuits. One prevented mishap pays for years of training programs.

Research and Innovation

KIMS publishes more research papers than hospitals 5x its size. But this isn't academic vanity—it's strategic positioning. Publishing outcomes data proves quality to skeptics. Research participation attracts talented doctors. Clinical trials bring cutting-edge treatments and funding. Most importantly, it positions KIMS as a thought leader, not just a service provider.

The COVID period showcased this. KIMS published data on lung transplants in COVID patients, plasma therapy outcomes, and vaccination effectiveness. These publications got international attention, establishing KIMS as a serious clinical institution. You can't buy such credibility—you have to earn it through rigorous science.

Telemedicine and Digital Health

Pre-COVID, KIMS's telemedicine program was modest. Post-COVID, it's central to their strategy. But unlike peers who see telemedicine as video consultations, KIMS views it as network amplification. A specialist in Secunderabad can guide procedures in Ongole. Complex cases get expert opinions without patient travel. Post-operative follow-ups happen remotely.

The technology infrastructure—EMR systems, PACS for imaging, laboratory information systems—creates a digital backbone. A patient's entire history is accessible across the network. This seems basic but is revolutionary in Indian healthcare where medical records often exist only on paper, if at all.

The Innovation Pipeline

KIMS's technology roadmap is ambitious but practical. Artificial intelligence for diagnostic imaging—reducing radiologist workload and improving accuracy. Robotic process automation for administrative tasks—cutting costs while improving service. Genomic medicine for personalized cancer treatment—tomorrow's medicine at today's affordability.

Each innovation follows the same framework: Will it improve outcomes? Can we offer it at 60% of market price? Will volume justify investment? This disciplined approach means KIMS might not have every cutting-edge technology, but what they have, they use brilliantly.

Competitive Advantage Through Excellence

Clinical excellence at affordable prices creates an unassailable moat. Competitors can match prices or quality, rarely both. A new hospital might install a da Vinci robot, but can they perform 500+ procedures annually to achieve proficiency? They might offer transplants, but can they do them at KIMS's prices while maintaining outcomes?

The technology investments also change patient perception. When rural patients see robotic surgery and ECMO machines, they realize this isn't a compromise—it's world-class care they happen to afford. This psychological shift—from "cheap" to "value"—drives KIMS's brand premium in its markets.

The Measurement Infrastructure

What gets measured gets managed. KIMS tracks clinical metrics obsessively—surgical site infections, medication errors, patient satisfaction, mortality rates. These aren't just numbers on dashboards; they drive decisions. A spike in infections triggers protocol reviews. Satisfaction drops prompt service training. Mortality variations between hospitals get investigated.

This data-driven approach seems obvious but is rare in Indian healthcare where clinical outcomes often go unmeasured. KIMS publishes outcome data transparently—a radical act in an industry where such information is closely guarded. This transparency builds trust with patients and credibility with peers.

The clinical excellence story reveals a deeper truth about KIMS: affordability doesn't mean compromise. By combining cutting-edge technology with operational efficiency, standardized protocols with continuous innovation, KIMS has proven that world-class healthcare can be democratized. As we'll explore next, this clinical capability operates in a competitive landscape where KIMS's regional dominance faces challenges from both established players and new entrants.

X. Competitive Landscape & Market Position

The healthcare conference at the Taj Mahal Hotel, Mumbai, February 2024. On stage, CEOs of India's largest hospital chains discussed expansion plans. Apollo talked about its 100-hospital vision. Fortis outlined its asset-light model. Max Healthcare showcased its Delhi NCR dominance. Then Dr. Abhinay Bollineni spoke: "While others chase national presence, we're happy owning Andhra Pradesh and Telangana. In our markets, we're not competing—we're the default choice."

This statement encapsulates KIMS's competitive strategy—regional dominance over national presence. In a fragmented industry where the largest player has less than 2% market share, KIMS has achieved something remarkable: 30%+ market share in its core markets. Understanding how requires examining both the competitive landscape and KIMS's unique position within it.

Regional Dominance Metrics

KIMS has 3,064 beds across nine multi-specialty hospitals in AP and Telangana as of December 31, 2020, which is 2.2 times more beds than the second-largest provider in AP and Telangana. This isn't just numerical superiority—it's market dominance. In Nellore, KIMS has 60% market share of organized healthcare. In Rajahmundry, it's 50%. Even in competitive Hyderabad, KIMS commands 15% share, remarkable given Apollo, CARE, Yashoda, and Continental's presence.

The dominance creates pricing power paradoxes. Despite charging 40% less than competitors, KIMS sets market prices in its strongholds. When KIMS raises prices 5%, others follow. When KIMS introduces a service, others scramble to match. This price leadership in spite of being the low-cost provider reveals true market power.

The Apollo Comparison

Apollo Hospitals, with 71 hospitals and 10,000+ beds, is India's healthcare giant. Their strategy is metropolitan presence, premium positioning, and service excellence. A consultation at Apollo Hyderabad costs ₹1,500; at KIMS, it's ₹600. Apollo's ARPOB exceeds ₹35,000; KIMS averages ₹20,000. Yet in Andhra Pradesh and Telangana, KIMS treats more patients, performs more surgeries, and generates higher absolute EBITDA.

The competitive dynamics are fascinating. Apollo doesn't really compete with KIMS—they serve different segments. Apollo targets the top 10% who want luxury healthcare. KIMS serves the next 40% who want quality at reasonable prices. The overlap is minimal. When patients choose between them, it's not about clinical quality—both are excellent—it's about value perception and financial capability.

Fortis: The Asset-Light Challenge

Fortis Healthcare's strategy is diametrically opposite—asset-light, management contracts, and operational excellence. They manage hospitals others own, avoiding capital investment. In theory, this should generate superior returns. In practice, Fortis struggles with 65% occupancy while KIMS maintains 79%.

The difference is alignment. KIMS owns its hospitals, allowing long-term thinking. They'll accept lower margins today for market share tomorrow. Fortis, managing others' assets, must deliver immediate returns. This short-term focus prevents the patient relationship building that drives KIMS's success. You can't build regional dominance on management contracts.

Narayana Health: The Closest Peer

If anyone mirrors KIMS's model, it's Narayana Health. Dr. Devi Shetty's chain also focuses on affordable healthcare, operational efficiency, and volume over margins. Their cardiac program in Bengaluru is legendary—more heart surgeries than anywhere in the world. Yet Narayana's national ambitions dilute focus. They're in 20 cities but dominant in none except Bengaluru.

According to analysis, Narayana Health and Apollo Healthcare are good companies in this space, with Krishna Institute of Medical Sciences being an emerging regional player. The comparison reveals strategic choices. Narayana chose breadth; KIMS chose depth. Narayana's ₹8,000 crore market cap versus KIMS's ₹29,000+ crore suggests markets prefer regional dominance over national presence.

Local Competition Dynamics

In each city, KIMS faces local competitors—single hospitals or small chains with deep community connections. In Vizag, it's Seven Hills Hospital. In Vijayawada, it's Ramesh Hospitals. These competitors know their markets intimately, have loyal doctor networks, and often match KIMS's prices.

KIMS's response is systematic. First, acquire if possible—many local hospitals eventually sell when competing becomes unsustainable. Second, differentiate through specialties—offer services like robotic surgery that locals can't match. Third, leverage network effects—a Vizag patient needing complex care goes to Secunderabad, staying in the KIMS system. Fourth, use financial strength—accept lower margins until competitors exit or sell.

The Government as Competitor

Government hospitals remain KIMS's largest competitor by patient volume. District hospitals are free, accessible, and improving. The new AIIMS in Mangalagiri threatens KIMS's Vijayawada market. State investments in healthcare infrastructure could theoretically reduce private hospital demand.

But KIMS has turned government from competitor to partner. Through Aarogyasri, government patients come to KIMS. Public-private partnerships see KIMS managing government facilities. Most importantly, KIMS positioned itself as complementary, not competitive—handling complex cases government hospitals can't, training government doctors, and providing capacity during emergencies like COVID.

New Entrant Threats