KFINTECH: India's Financial Infrastructure Powerhouse

I. Introduction & Episode Thesis

Picture this: Every morning, before India's stock markets open, a nondescript building in Hyderabad processes millions of transactions that will determine the financial futures of countless Indians. No flashy trading floors, no celebrity fund managers—just servers humming quietly as they reconcile mutual fund purchases, process dividend payments, and maintain shareholder records for some of India's largest corporations. This is KFin Technologies, and despite its low profile, it touches more Indian investment accounts than perhaps any other company in the country.

With a market capitalization of ₹19,201 crores, KFINTECH operates as the invisible backbone of India's capital markets. The company processes transactions for 26 of India's 51 mutual fund houses, maintains records for nearly 8,000 corporations, and manages pension accounts for millions of Indians. Yet most investors have never heard of it. This anonymity is both its weakness and its greatest strength.

The paradox at the heart of KFINTECH's story is compelling: How does a back-office services company—essentially doing the unglamorous work of record-keeping and transaction processing—become so indispensable that India's largest financial institutions can't function without it? More intriguingly, how did this company survive when its parent, the once-mighty Karvy Group, collapsed in one of India's most spectacular financial frauds?

This is a story of transformation unlike any in Indian corporate history. It's about building critical infrastructure when no one else would, surviving a parent company scandal that should have been fatal, and emerging stronger under private equity ownership. It's about General Atlantic's most audacious India bet—taking a tainted asset and turning it into a public market darling. And ultimately, it's about whether you can build a lasting moat in what seems like commodity financial plumbing.

The journey from Karvy's chaotic empire to today's technology-driven powerhouse reveals fundamental truths about India's financial evolution. As the country undergoes massive financialization—with mutual fund assets growing at 20% annually and retail participation exploding—KFINTECH sits at the center of this transformation. Every SIP (Systematic Investment Plan) registration, every IPO application, every dividend payment flows through systems that KFINTECH built and maintains.

But here's what makes this story truly fascinating: In an era where every financial services company claims to be a "fintech," KFINTECH actually is one—and has been since 1984, long before the term existed. While others talk about disruption, KFINTECH quietly processes 70% of India's mutual fund transactions. While startups promise to revolutionize financial infrastructure, KFINTECH already runs it.

The big question we'll explore: Can you build a defensible moat in financial plumbing? The answer, as we'll see, depends on understanding that in financial services, trust isn't just important—it's everything. And trust, once broken, is almost impossible to rebuild. Unless, of course, you completely reinvent yourself.

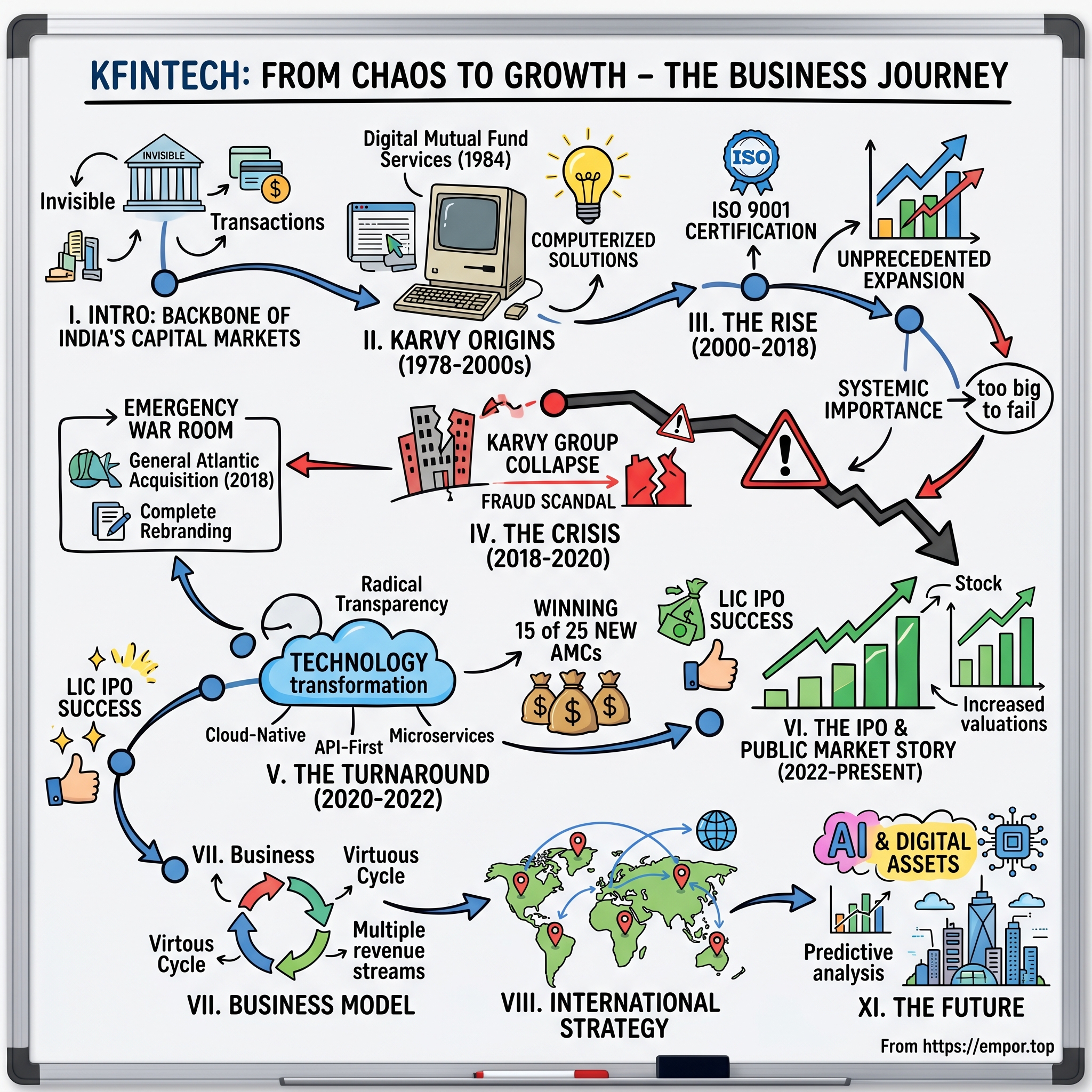

II. The Karvy Origins: Building in the License Raj Era (1978–2000s)

The year was 1983, and Hyderabad was far from India's technology capital. The city's claim to fame was still the Charminar and biryani, not bytes and bandwidth. In a modest office in Somajiguda, three chartered accountants—C. Parthasarathy, M. Yugandhar, and MS Ramakrishna—pooled together ₹1.5 lakh to start what they called Karvy Consultants. The name itself was an acronym drawn from their surnames, a practice common among partnership firms of that era. None of them could have imagined they were laying the foundation for what would become India's financial infrastructure backbone.

Parthasarathy, the driving force among the three, had a vision that extended beyond traditional accounting. Having worked with various businesses in Hyderabad, he noticed a pattern: Indian companies were drowning in paperwork, especially when it came to managing shareholder records. The 1980s were the twilight years of India's License Raj, where every business decision required multiple approvals, and documentation was king. But Parthasarathy saw opportunity where others saw drudgery.

The firm's initial services were mundane—auditing, taxation, and company law consultancy. But 1984 marked a pivotal turn. While the world watched Indira Gandhi's assassination and Rajiv Gandhi's ascension, Karvy quietly launched something revolutionary for its time: digital mutual fund services. This wasn't Silicon Valley-style innovation with venture capital and press releases. This was three accountants in Hyderabad convincing mutual fund companies that computers could manage investor records better than ledger books.

To understand how radical this was, consider the context. In 1984, India had exactly six mutual funds, all government-owned. Personal computers were exotic imports that cost more than most Indians earned in a year. The idea of using computers for financial services was so foreign that Karvy's founders had to first educate potential clients on what computers could do. Parthasarathy would later recall carrying a computer to client meetings—not a laptop, but an actual desktop computer—just to demonstrate that these machines were real and could actually store and process data.

The timing was fortuitous. India's capital markets were about to undergo seismic changes. The Rajiv Gandhi government, despite its political troubles, was quietly liberalizing the economy. New private sector mutual funds were being contemplated. The Bombay Stock Exchange was modernizing. Foreign institutional investors were knocking on India's doors. Someone would need to manage the paperwork—or rather, the digital work—for this emerging market economy.

Karvy's breakthrough came through a combination of persistence and being in the right place. When Unit Trust of India (UTI), then India's only mutual fund, needed help managing its expanding investor base, Karvy was one of the few firms that could offer computerized solutions. The contract wasn't large, but it established credibility. More importantly, it gave Karvy access to UTI's processes, allowing them to understand the intricate workflows of mutual fund operations.

By the late 1980s, Karvy had evolved from a services firm to an infrastructure company. They weren't just processing transactions; they were building the rails on which transactions would run. When India's capital markets exploded in the 1991 liberalization, Karvy was perfectly positioned. As new mutual funds launched, they needed someone to manage investor records, process applications, handle redemptions, and distribute dividends. The manual alternative was hiring hundreds of clerks. Karvy offered computers and expertise.

The Registrar and Transfer Agent (RTA) business model that Karvy pioneered in India was elegantly simple yet powerful. Mutual funds and companies would outsource their investor record-keeping to Karvy, paying per transaction or per folio. For the clients, it meant converting a fixed cost (maintaining an in-house team) to a variable cost. For Karvy, it meant building a business with tremendous operating leverage—the same infrastructure could serve multiple clients with minimal incremental cost.

But Parthasarathy's ambitions extended beyond just RTA services. Through the 1990s, Karvy aggressively expanded into every corner of India's financial markets. Stock broking, depository services, portfolio management, distribution—if it involved financial transactions, Karvy wanted a piece of it. The company established offices across India, often in tier-2 and tier-3 cities where no other financial services firm would go. By 2000, Karvy had over 300 offices, making it one of India's largest financial services networks.

This expansion wasn't without controversy. Old-timers in India's financial markets viewed Karvy with suspicion. Here was a Hyderabad-based firm, backed by no major business house, rapidly capturing market share in businesses traditionally dominated by Mumbai's established players. The aggressive growth, funded largely by debt and internal accruals, raised eyebrows. But as long as the business kept growing and clients kept coming, the questions remained muted.

The international expansion began in the late 1990s, initially following the Indian diaspora. Karvy set up offices in Dubai and New York, primarily to serve NRIs (Non-Resident Indians) who wanted to invest in Indian markets. But Parthasarathy had bigger dreams—he wanted Karvy to become a global financial services player, competing with the likes of Computershare and DST Systems.

By 2000, Karvy employed over 5,000 people and processed millions of transactions annually. The three chartered accountants who started with ₹1.5 lakh had built an empire. But empires, as history repeatedly shows, contain the seeds of their own destruction. The very ambition and aggressive expansion that made Karvy successful would eventually lead to its downfall. For now, though, the future looked limitless.

III. The Rise: Becoming India's Financial Backbone (2000–2018)

The new millennium opened with the dot-com crash, but for Karvy, it was the beginning of an unprecedented expansion. While technology stocks were cratering globally, C. Parthasarathy saw opportunity in the rubble. "When everyone is selling, that's when infrastructure becomes cheap," he told his leadership team in a 2001 strategy meeting. He was right. Karvy went on an acquisition and hiring spree, picking up technology talent and assets at fraction of their boom-time valuations.

The masterstroke came in 2003 when Karvy became the first Indian financial services company to achieve ISO 9001:2000 certification for its entire operations. This wasn't just a certificate to hang on the wall—it was a signal to global funds entering India that Karvy operated at international standards. When Franklin Templeton wanted to expand its Indian operations, they chose Karvy as their RTA partner specifically because of these process certifications. Others followed.

By 2005, Karvy had become a force in every vertical of the Indian securities market. The numbers were staggering: managing 16 million investor accounts, processing 500,000 transactions daily, maintaining records for 1,200 listed companies. The company had grown to more than 30,000 employees, spanning 900 offices in about 400 cities and towns. No other financial services company, not even the banks, had this kind of reach into India's hinterlands.

The mutual fund boom of 2003-2008 transformed Karvy from a large player to an indispensable institution. As India's equity markets soared and retail participation exploded, mutual fund assets under management grew from ₹1 lakh crore to over ₹5 lakh crores. Every one of those investments needed to be processed, recorded, and serviced. Karvy was processing nearly 40% of all mutual fund transactions in India. On peak days during NFO (New Fund Offer) seasons, Karvy's systems would process over 2 million applications in 24 hours.

The technology infrastructure Karvy built during this period was remarkable for its scale and sophistication. While competitors relied on manual processes supplemented by basic databases, Karvy invested heavily in automated workflow systems, real-time processing capabilities, and what they called "straight-through processing"—transactions that required no human intervention from initiation to completion. The company was spending ₹100 crores annually on technology by 2007, more than most Indian IT services companies of similar size.

But technology alone didn't explain Karvy's dominance. The real moat was the intricate knowledge of India's Byzantine financial regulations and the relationships with regulators. When SEBI (Securities and Exchange Board of India) wanted to introduce new investor protection measures, they consulted Karvy. When the Ministry of Finance needed data on retail participation in markets, Karvy provided it. This proximity to power and policy-making gave Karvy an insurmountable advantage.

The international expansion accelerated after 2008. While the global financial crisis devastated Western markets, it paradoxically strengthened Karvy's position. As global asset managers looked to cut costs, outsourcing to India became attractive. Karvy set up operations in Malaysia, Hong Kong, and the Philippines, not to serve Indian investors, but to provide back-office services to global funds. By 2010, Karvy was processing transactions for 76 global asset managers across Southeast Asia.

The most audacious move came in 2012 when Karvy entered the U.S. mortgage services market. This seemed bizarre—what did a Hyderabad-based financial services company know about American mortgages? But Parthasarathy had identified an opportunity: U.S. banks needed help with the massive documentation and compliance requirements following the 2008 crisis. Karvy acquired a small mortgage services firm in Texas and built it into a $50 million revenue business within three years.

The transformation of India's capital markets during this period cannot be overstated, and Karvy was at the center of it all. The introduction of demat accounts eliminated physical share certificates. The launch of National Stock Exchange brought electronic trading. The mutual fund industry's systematic investment plans (SIPs) democratized equity investing. Each of these innovations required massive backend infrastructure, and Karvy provided it.

Consider the SIP revolution. In 2000, India had fewer than 100,000 SIP accounts. By 2018, there were over 25 million, contributing ₹8,000 crores monthly to mutual funds. Each SIP required monthly bank debits, NAV calculations, unit allocations, and statement generation. Karvy automated this entire chain, processing millions of SIP transactions with 99.9% accuracy. When fund houses launched daily SIPs or trigger-based investment plans, Karvy's systems could handle them without modification.

The corporate registry business grew equally dramatically. As India's IPO market boomed, every newly listed company needed a registrar to maintain shareholder records. Karvy became the preferred choice, eventually managing records for over 7,000 companies. When Reliance Industries wanted to distribute bonus shares to its 3 million shareholders, Karvy executed it in 48 hours. When Coal India conducted the world's largest IPO in 2010, Karvy processed 1.5 million applications.

By 2015, Karvy had achieved something remarkable: it had become too big to fail in Indian capital markets. If Karvy's systems went down, mutual fund investors couldn't redeem their investments, companies couldn't pay dividends, and IPOs couldn't be processed. This systemic importance gave Karvy enormous pricing power and made client switching nearly impossible. The switching costs weren't just financial—they were operational, regulatory, and reputational.

The culture within Karvy during these growth years was unique. Unlike Mumbai's financial firms with their maritime club pretensions, Karvy maintained its middle-class Hyderabad ethos. Employees called Parthasarathy "CP Sir," meetings started with Sanskrit shlokas, and the company cafeteria served authentic Andhra meals. This culture attracted talented professionals from India's tier-2 cities who felt excluded from Mumbai's elite financial circles.

But success bred complacency, and complacency bred risk-taking. As Karvy's core RTA business matured, growth slowed. To maintain the aggressive expansion that investors expected, Parthasarathy pushed into riskier ventures. Karvy Stock Broking began proprietary trading. Karvy Capital started lending against shares. Karvy Realty entered property development. Each business seemed logical individually, but collectively they created a web of related-party transactions and conflicts of interest.

The warning signs were visible to those who looked closely. Audit reports mentioned "significant related party transactions." Employees whispered about funds being moved between entities. Competitors spread rumors about aggressive accounting. But as long as the core business performed and clients remained satisfied, these concerns were dismissed as jealousy from rivals who had been outmaneuvered.

By early 2018, Karvy looked unstoppable. The company was valued at over ₹8,000 crores in private transactions. International private equity firms were circling, seeing opportunity in India's under-penetrated financial markets. Parthasarathy was featured on magazine covers as a visionary entrepreneur who built a financial empire from nothing. The three chartered accountants from Hyderabad had seemingly achieved the impossible.

But beneath the surface, the foundation was cracking. The aggressive expansion had been funded by debt—lots of it. The various group companies had cross-guaranteed each other's borrowings. Most dangerously, Karvy Stock Broking had begun using client securities for its own financing needs. It was a house of cards waiting for the slightest breeze. That breeze would soon become a hurricane.

IV. The Crisis & General Atlantic Acquisition (2018–2020)

November 2018 should have been a moment of triumph for C. Parthasarathy. After months of negotiations, General Atlantic, one of the world's most prestigious private equity firms, had agreed to acquire an 83.5% stake in Karvy's RTA and corporate registry business for ₹2,100 crores. The valuation implied that the business Parthasarathy had built from ₹1.5 lakhs was now worth over ₹2,500 crores. Champagne was ordered for the signing ceremony at the Taj Krishna hotel in Hyderabad. But even as the deal was being celebrated, a catastrophe was brewing in another part of the Karvy empire.

The first signs of trouble emerged quietly. In September 2019, HDFC Bank froze accounts belonging to Karvy Stock Broking Limited (KSBL) over non-payment of loans. This should have been manageable—a temporary liquidity issue in one group company. But when SEBI investigators began probing, they uncovered something far more sinister. KSBL had pledged securities belonging to its clients—worth over ₹2,300 crores—as collateral for its own loans. These weren't authorized transactions; clients had no idea their shares were being used this way.

The scandal unraveled with stunning speed. On November 22, 2019, SEBI issued an ex-parte order prohibiting KSBL from taking new clients. By November 25, the National Stock Exchange suspended KSBL's trading membership. Within a week, criminal cases were filed, Parthasarathy was arrested, and the Karvy name became synonymous with fraud. The very brand that had taken 36 years to build was destroyed in 36 hours.

For General Atlantic, this was a nightmare scenario. They had just paid ₹2,100 crores for a business whose brand was now toxic. GA's India head, Shantanu Rastogi, flew down from Mumbai to Hyderabad for emergency meetings. The situation was dire: clients were panicking, employees were resigning, and regulators were threatening to cancel licenses. The investment that was supposed to showcase GA's India strategy was turning into a reputational disaster.

But General Atlantic didn't panic. Instead, they executed one of the most remarkable crisis management operations in private equity history. Within 48 hours of the scandal breaking, GA's crisis team had set up a war room in Hyderabad. Their first priority: ring-fence the RTA business from the broking scandal. They immediately filed regulatory submissions clarifying that the RTA business—now wholly owned by GA—had no connection to the fraudulent broking operations.

The human drama inside Karvy's offices during those weeks was intense. Employees arrived at work not knowing if they still had jobs. Clients called demanding immediate transfer of their accounts. Competitors circled like vultures, openly poaching staff and clients. In the Hyderabad headquarters, where 5,000 employees worked, security guards were posted to prevent data theft. IT teams worked round the clock to ensure systems remained operational despite the chaos.

General Atlantic's next move was bold: complete rebranding. By December 2019, less than a month after the scandal, they announced that Karvy Computershare would be renamed KFin Technologies. This wasn't just a cosmetic change. Every single touchpoint—from office signage to email domains to employee ID cards—had to be changed. The operation cost ₹50 crores and required updating millions of customer records. But it was essential to distance the business from the tainted Karvy brand.

The appointment of leadership was crucial. GA brought in Sreekanth Nadella, a veteran technology executive who had previously worked at Cognizant and Oracle, as CEO. More significantly, they appointed M.V. Nair, the respected former Chairman of Union Bank of India, as non-executive Chairman. Nair's reputation for integrity was unimpeachable—exactly what was needed to restore confidence. "My first task," Nair told the board, "is to ensure that not a single investor loses trust in our operations."

Client retention became an existential battle. Every major mutual fund client held emergency board meetings to discuss whether to continue with KFin. Franklin Templeton, one of the largest clients, sent a team to audit KFin's operations. HDFC Mutual Fund demanded daily reports on operational metrics. Some smaller AMCs began the process of transitioning to competitors. Nadella and his team spent 18-hour days in client meetings, demonstrating that operations were unaffected and that GA's ownership meant stronger governance.

The employee morale crisis was equally severe. Of the 30,000 employees in the broader Karvy group, only 8,000 were part of the business acquired by GA. The rest faced uncertain futures as other Karvy businesses collapsed. Even for those in KFin, the stigma was real. "I stopped mentioning where I worked at social gatherings," one senior manager recalled. "The Karvy name had become shameful." GA responded with town halls, retention bonuses for key employees, and a clear communication that KFin was a new company with new values.

Regulatory management required delicate handling. SEBI, RBI, and other regulators were understandably skeptical. Why should they trust an entity that emerged from the Karvy scandal? GA's approach was radical transparency. They invited regulators to inspect operations, shared technology architecture, and implemented governance standards that exceeded regulatory requirements. When SEBI asked for additional compliance measures, KFin implemented them immediately, no questions asked.

The financial engineering to separate KFin from Karvy was complex. The businesses were intertwined through hundreds of contracts, shared services agreements, and technology licenses. Each had to be unwound or renegotiated. The Karvy group's creditors initially tried to claim that KFin's assets could be used to satisfy Karvy's debts. GA's legal team fought these claims aggressively, establishing clear boundaries between the entities.

Through this crisis, KFin's operations never faltered—a remarkable achievement. Not a single mutual fund NAV was delayed. No dividend payment was missed. No IPO processing was disrupted. This operational excellence during chaos became KFin's strongest selling point. As Nadella told clients: "We kept the lights on when everything around us was falling apart. That's the resilience you're buying."

By mid-2020, the immediate crisis had passed, but the transformation was just beginning. GA had stabilized the patient, but major surgery was still required. The technology infrastructure needed modernization. The organizational culture needed reformation. The business model needed evolution. Most importantly, trust needed to be rebuilt—not just restored to pre-crisis levels, but elevated to new heights.

The crisis had cost General Atlantic dearly—not just financially but reputationally. Their ₹2,100 crore investment was worth significantly less given the brand damage and client losses. Additional investments in rebranding, technology, and retention had added hundreds of crores to the bill. Some GA limited partners questioned whether the investment could ever recover. But Rastogi remained confident: "Crisis creates opportunity. The Indian financial services market is too important, and this business is too strategic to fail."

As 2020 ended, KFin had survived but was far from thriving. Revenue had declined 15% as some clients left. Margins were compressed due to retention costs and emergency investments. The company that had once commanded premium valuations was now viewed skeptically. But in the ruins of the Karvy empire, something new was being built. The question was whether General Atlantic could transform a crisis acquisition into a crown jewel.

V. The Turnaround: From Karvy to KFINTECH (2020–2022)

The transformation of KFin Technologies under General Atlantic's ownership represents one of the most successful turnarounds in Indian corporate history. When Sreekanth Nadella convened his first leadership meeting in January 2020, he opened with a stark message: "Forget everything you knew about how Karvy operated. We're building a new company." What followed was 24 months of relentless execution that would culminate in one of India's most successful IPOs.

The cultural transformation began immediately. Karvy had operated as a family-controlled business where decisions flowed from Parthasarathy's office. KFin would be different. Nadella instituted what he called "radical transparency"—every major decision would be documented, every process would be standardized, and every transaction would be auditable. The old practice of verbal approvals and relationship-based deals was dead. "Trust through transparency" became the new mantra, printed on office walls and repeated in every meeting.

The technology transformation was equally dramatic. Karvy's systems, while functional, were a patchwork of applications built over decades. Some modules still ran on COBOL. Customer data was fragmented across multiple databases. Integration between systems required manual intervention. General Atlantic committed ₹500 crores for a complete technology overhaul. But this wasn't just about modernization—it was about building competitive advantage.

The new technology architecture was cloud-native, API-first, and built for scale. Instead of monolithic applications, KFin adopted a microservices architecture where each function—be it NAV calculation or dividend processing—operated as an independent service. This meant new features could be deployed without affecting existing operations. When a mutual fund wanted a custom reporting format, KFin could deliver it in days, not months.

The masterstroke was the development of what KFin called the "Digital Ecosystem Platform." This wasn't just about digitizing existing processes; it was about reimagining how financial services infrastructure should work. The platform allowed mutual funds to offer their investors mobile apps, robo-advisory services, and automated financial planning tools—all powered by KFin's backend. For AMCs lacking technical capabilities, KFin became their technology partner, not just their operations vendor.

Client acquisition strategy underwent a fundamental shift. Under Karvy, the approach was relationship-driven—Parthasarathy would personally call CEOs to win business. Under GA's ownership, KFin adopted a solutions-based selling approach. When approaching new AMCs, KFin didn't just offer RTA services; they presented a complete digital transformation roadmap. This resonated particularly with new fund houses that wanted to launch with digital-first strategies.

The success was immediate and dramatic. Between 2020 and 2022, KFin became the de-facto choice for new AMCs, winning 15 of the 25 newly launched fund houses. When Navi Mutual Fund, backed by Flipkart founder Sachin Bansal, needed an RTA partner, they chose KFin specifically for its technology capabilities. When WhiteOak Capital wanted to launch with a completely digital onboarding process, KFin built it for them in six weeks.

The international business, which had stagnated during the crisis, was revitalized with a new strategy. Instead of trying to compete globally, KFin focused on markets with large Indian diaspora populations and similar regulatory frameworks. The company established operations in GIFT City, India's international financial services center, positioning itself as the gateway for global funds entering India. Partnerships were struck with technology providers in Singapore and Hong Kong, extending KFin's reach without heavy capital investment.

But the real coup came in the pension sector. In 2021, the Pension Fund Regulatory and Development Authority (PFRDA) appointed KFin as India's second Central Record Keeping Agency (CRA) for the National Pension System. This broke NSDL's monopoly and gave KFin access to India's rapidly growing pension market. The appointment was significant not just for the business opportunity but for what it represented—regulatory confidence in KFin's governance and capabilities.

The IPO services business saw explosive growth. As India's IPO market boomed in 2021-2022, KFin positioned itself as the technology-enabled alternative to traditional registrars. When Zomato went public in a ₹9,375 crore IPO, KFin processed 4.8 million applications in 72 hours. When Paytm launched India's largest IPO at ₹18,300 crores, KFin's systems handled the complexity without breaking a sweat. But the crown jewel was the LIC IPO.

The Life Insurance Corporation of India's IPO in May 2022 was India's largest ever, raising ₹21,000 crores. With 7.35 million applications, it was also the most complex. KFin was chosen as the registrar, beating established competitors. The successful execution—processing all applications, managing the allotment, and crediting shares to millions of demat accounts within regulatory timelines—established KFin as India's premier IPO registrar. "If we can handle LIC, we can handle anything," became the sales pitch.

Employee morale, devastated during the crisis, was rebuilt through a combination of performance incentives and cultural initiatives. GA introduced employee stock options, something unheard of in the Karvy era. Town halls became regular, with Nadella answering unscripted questions from employees. A whistleblower hotline was established, reporting directly to the board. The message was clear: the old culture of fear and favoritism was gone.

The financial performance during this period validated the transformation. Revenue grew from ₹558 crores in FY2020 to ₹721 crores in FY2022. More importantly, EBITDA margins expanded from 31% to 38% as technology investments drove operational efficiency. The company that was valued at ₹2,100 crores during GA's acquisition was now generating ₹220 crores in annual profit. The return on equity exceeded 25%, among the highest in India's financial services sector.

Risk management, an afterthought in the Karvy era, became central to operations. A Chief Risk Officer was appointed, reporting directly to the board. Every process was mapped for operational risk. Disaster recovery sites were established. Cybersecurity investments increased five-fold. When RBI conducted a surprise audit in 2021, they found zero compliance violations—a remarkable achievement for a company emerging from scandal.

The brand rehabilitation was complete by early 2022. The Karvy name had been completely erased—from office buildings, from legal documents, from public memory. KFin Technologies was now seen as a General Atlantic portfolio company, backed by global capital and governance standards. When customers were surveyed, over 90% expressed satisfaction with services. The transformation from pariah to partner was complete.

As KFin prepared for its IPO in 2022, the contrast with the crisis years was stark. The company that couldn't retain clients was now winning new business at record rates. The organization that employees were ashamed to work for was now featured in "Best Places to Work" lists. The brand that regulators viewed with suspicion was now their trusted partner. General Atlantic had achieved what seemed impossible: they had taken a toxic asset and transformed it into a crown jewel.

VI. The IPO & Public Market Story (2022–Present)

The morning of December 29, 2022, marked a moment of vindication for General Atlantic and the entire KFin Technologies team. The shares were set to list on BSE and NSE on Thursday, December 29, 2022, exactly four years after the Karvy scandal had erupted. The IPO, which opened on December 19, 2022, and closed on December 21, 2022, was entirely an offer for sale of 4.10 crore shares worth ₹1,500 crores, priced at ₹366 per share, at the upper end of the price band.

The subscription numbers told a story of restored confidence. KFin had raised ₹675 crores from anchor investors on December 16, 2022, with marquee global institutions participating. The public portion saw steady demand across all categories—institutional investors who had shunned anything associated with Karvy were now backing KFin with conviction. This wasn't just capital raising; it was a public referendum on the transformation.

For Sreekanth Nadella and his team, the IPO represented more than a liquidity event for General Atlantic. It was the culmination of a grueling turnaround that many thought impossible. "We're not celebrating an exit," Nadella told employees at a pre-listing town hall. "We're celebrating a new beginning. Being public means higher scrutiny, greater transparency, and bigger opportunities."

KFintech made its stock market debut on December 29, 2022, and was trading 198 percent higher than its issue price of Rs 366 per share within months, a remarkable performance that validated investor confidence in the transformation story. The market capitalization that started at ₹6,133 crores on listing day would eventually soar to over ₹19,000 crores, making early investors substantial returns.

General Atlantic's exit strategy was masterfully executed. Rather than dumping shares immediately post-listing, they adopted a staged approach. The initial OFS (Offer for Sale) allowed them to recover their initial investment while retaining significant ownership to benefit from future growth. By 2024, promoter holding had decreased to 22.9%, as GA gradually reduced its stake at increasingly higher valuations.

The post-IPO performance validated every strategic decision made during the crisis years. Revenue growth accelerated as the company won new mandates from mutual funds launching digital-first strategies. The pension business, barely existent during the Karvy era, became a significant contributor. International operations, which many had written off, started generating meaningful profits.

But the real validation came from operational metrics. Customer churn, which spiked during the crisis, fell to historic lows. Employee attrition, a chronic problem in the technology services sector, dropped below industry averages. Net promoter scores from clients reached levels typically associated with consumer brands, not B2B service providers. The company that couldn't retain clients was now their preferred partner.

Since July 2024, in just 13 trading days, KFin Tech's share price rallied 56 percent after the company reported strong performance across segments in the June quarter. This wasn't speculative fervor—it was recognition of fundamental business strength. Margins were expanding, new products were gaining traction, and the competitive position was strengthening.

The regulatory relationships, carefully rebuilt after the crisis, became a strategic advantage. When SEBI introduced new compliance requirements for mutual funds, KFin was ready with solutions before competitors knew what hit them. When PFRDA wanted to modernize pension infrastructure, KFin got the mandate. The company that regulators once viewed with suspicion was now their trusted partner for market development.

The technology investments made during the turnaround started paying dividends—literally. The microservices architecture allowed KFin to launch new products in weeks, not months. The API-first approach meant clients could integrate KFin services into their own applications seamlessly. The cloud infrastructure provided scalability without capital expenditure. While competitors struggled with legacy systems, KFin operated like a technology company that happened to be in financial services.

The cultural transformation proved equally valuable. The command-and-control structure of the Karvy era had given way to empowered teams making rapid decisions. Innovation, once stifled by hierarchy, flourished in the new environment. Engineers who previously just maintained systems were now building products. Operations staff who merely processed transactions were now consulting with clients on process optimization.

Market dynamics post-IPO favored KFin's positioning. India's mutual fund penetration remained below 15%, suggesting massive growth potential. The SIP book was growing at 30% annually, creating recurring revenue streams. New asset classes—AIFs, InvITs, REITs—needed infrastructure providers. International markets were opening up to Indian service providers. Every trend pointed toward sustained growth.

The competitive landscape had also evolved favorably. While CAMS remained the market leader in mutual fund RTA services, KFin's technology-first approach resonated with new-age fund houses. The duopoly structure meant rational pricing and high barriers to entry. New competitors faced the chicken-and-egg problem: they needed scale to be profitable, but couldn't achieve scale without massive investments.

The stock trading at 13.7 times book value might seem expensive, but investors were paying for the platform's optionality. The infrastructure built for mutual funds could serve any asset class. The technology developed for India could be deployed globally. The relationships with financial institutions could unlock adjacencies. This wasn't just an RTA company anymore—it was a financial technology platform with multiple growth vectors.

International expansion accelerated post-IPO. The Southeast Asian operations, particularly in Malaysia and the Philippines, gained critical mass. The GIFT City operations positioned KFin as the gateway for global funds entering India. The mortgage services business in the U.S., while small, demonstrated the platform's versatility. Each international success de-risked the India concentration and opened new markets.

For General Atlantic, the KFin investment became a case study in private equity excellence. They had acquired a distressed asset, navigated a existential crisis, executed a complete transformation, and achieved a successful public market exit. The returns—while not publicly disclosed—were rumored to exceed 3x in INR terms despite the crisis years. More importantly, they had created lasting value, not just financial engineering.

The leadership team that had navigated the crisis remained largely intact post-IPO, a rarity in private equity exits. Nadella continued as CEO, building on the foundation laid during the turnaround. The senior management, having proven themselves during the crisis, were now equity holders with skin in the game. This continuity provided stability and institutional knowledge that money couldn't buy.

As 2023 progressed, KFin's public market story evolved from turnaround to growth. In Q1FY25, profit after tax jumped 56.9% year-on-year to Rs 68.07 crore, aided by 30.9% broad-based revenue growth, with international and other investor solutions revenue up 56.6% YoY and VAS revenue up 49.6% YoY, while EBITDA grew 41.5% with margins improving 315 bps to 42.0%. These weren't the metrics of a mature infrastructure company—they were the growth rates of a technology platform hitting its stride.

The IPO had achieved what seemed impossible in 2019: it had transformed KFin from a scandal-tainted subsidiary into a respected public company. The market had validated the transformation with its wallet. Regulators had endorsed it with new licenses. Clients had confirmed it with renewed contracts. Employees had embraced it with their commitment. The journey from crisis to credibility was complete, but the story was far from over.

VII. The Business Model: Network Effects in Financial Infrastructure

To understand KFin Technologies' moat, imagine trying to switch your email provider, but multiply the complexity by a thousand. Every mutual fund transaction, every dividend payment, every shareholder record is embedded in KFin's systems. The switching costs aren't just financial—they're operational, regulatory, reputational, and existential. This is the genius of financial infrastructure: once embedded, displacement becomes almost impossible.

KFin Technologies serves over 90 million investor accounts spread over 1,300 issuers including banks, PSUs, and mutual funds, serving the mission-critical needs of asset managers with clients spanning mutual funds, AIFs (alternative investments), pension, wealth managers, and corporates in India and abroad. But these numbers only hint at the true scope of the platform. Every one of those accounts generates multiple transactions monthly—SIP debits, redemption requests, dividend credits, statement generations. The volume creates a data moat that competitors simply cannot replicate.

The duopoly structure with CAMS is often misunderstood as a weakness, but it's actually KFin's greatest strategic advantage. In a monopoly, regulatory pressure would force price reductions and market opening. In a fragmented market, price wars would destroy margins. But in a duopoly, both players maintain rational pricing while the market grows rapidly enough to satisfy both. It's the Visa-Mastercard playbook, executed in Indian financial infrastructure.

The revenue model is elegantly diversified across three streams, each with different growth drivers and margin profiles. Transaction fees, charged per mutual fund purchase or redemption, benefit from market volatility and investor activity. Asset-based fees, calculated as basis points on assets under management, provide steady recurring revenue that grows with market appreciation. Platform fees, charged for technology services and value-added solutions, offer the highest margins and fastest growth.

KFintech provides SaaS-based end-to-end transaction management, channel management, compliance solutions, data analytics, and various other digital services to asset managers across segments, as well as outsourcing services for global players. This isn't just processing—it's the entire technology stack that mutual funds need to operate. When a new AMC launches in India, they essentially get a fund-in-a-box solution from KFin: investor onboarding, transaction processing, compliance reporting, distribution management, all delivered through APIs and white-labeled interfaces.

The technology moat deserves special attention. KFin processes over 10 lakh (1 million) transactions daily with 99.9% accuracy. Building this capability would require not just hundreds of crores in technology investment, but years of operational learning. Every edge case, every regulatory nuance, every integration challenge has been solved and encoded into KFin's platform. A new entrant would need to recreate decades of accumulated knowledge.

Consider the complexity of a simple SIP transaction. The investor's bank account must be debited on a specific date. The amount must be converted to mutual fund units based on that day's NAV. The units must be allocated to the investor's folio. The transaction must be reported to the AMC, the distributor, the investor, and regulators. Tax implications must be calculated. If any step fails, the entire chain must be reversed. KFin does this millions of times monthly, flawlessly.

The corporate registry business adds another layer of stickiness. As the #1 corporate registrar in India serving nearly 600 listed and 3,000+ unlisted corporates, KFin maintains cap tables, processes corporate actions, manages dividend distributions, and handles shareholder communications. Switching registrars requires shareholder approval, regulatory filings, and operational risk that most boards won't accept. Once KFin becomes a company's registrar, the relationship typically lasts decades.

Network effects manifest in multiple ways. Every new mutual fund that joins KFin's platform makes it more valuable for distributors who need single-point integration. Every new distributor makes it more attractive for mutual funds. Every new corporate client provides more data for analytics products. Every new international client makes the platform more attractive for global asset managers. It's a virtuous cycle that strengthens with scale.

The data advantage is perhaps the most underappreciated aspect of KFin's moat. With visibility into transaction patterns across hundreds of financial institutions, KFin can identify trends before anyone else. Which pin codes are seeing increased SIP adoption? Which age groups are switching from regular to direct plans? Which corporate actions trigger the most investor queries? This intelligence is invaluable for product development and risk management.

The platform's extensibility into new asset classes demonstrates the power of the infrastructure. The same systems that process mutual fund transactions can handle pension contributions, insurance premiums, alternative investment subscriptions, even cryptocurrency holdings. The marginal cost of adding a new asset class is minimal, but the revenue opportunity is substantial. Every new financial product in India becomes a potential revenue stream for KFin.

Managing Rs 13 lac crores of AUM and serving over 300 AIF schemes launched by 100+ fund managers, KFin has become the default infrastructure for India's alternative investment industry. As wealthy Indians diversify beyond mutual funds into private equity, venture capital, and real estate funds, KFin processes the subscriptions, maintains investor records, and manages distributions. The AIF segment, while smaller than mutual funds, offers higher margins due to complexity.

The international expansion strategy leverages the same platform economics. KFin has emerged as the transaction processing platform of choice in South East Asia with 23 mutual funds and pension manager clients in Malaysia alone. The technology and processes developed for India work with minor modifications in other emerging markets. The marginal cost of serving a Malaysian mutual fund is minimal when the core platform already exists.

Regulatory compliance, often viewed as a cost center, becomes a revenue opportunity for KFin. Every new SEBI circular, every RBI guideline, every tax law change requires system modifications across the financial industry. KFin implements these changes once and deploys them across all clients. Smaller players must make the same investments but spread them across fewer clients. This regulatory complexity becomes a barrier to entry that strengthens with time.

The pricing power inherent in this model is remarkable but must be exercised carefully. KFin could theoretically raise prices significantly given the switching costs, but doing so would invite regulatory scrutiny and encourage new entrants. Instead, the company maintains reasonable pricing while expanding wallet share through new services. A client paying ₹1 crore for RTA services might pay another ₹50 lakhs for analytics, ₹30 lakhs for digital solutions, and ₹20 lakhs for compliance tools.

Operating leverage in this business is extraordinary. The fixed costs—technology infrastructure, regulatory compliance, core operations—are largely constant regardless of transaction volumes. But revenue scales linearly with volumes. This means that as India's financial markets grow, margins naturally expand. During the bull market of 2021-2022, KFin's EBITDA margins expanded by over 500 basis points without any structural changes.

The competitive dynamics with CAMS deserve deeper analysis. While they compete for new clients, both benefit from market growth and have found ways to coexist profitably. CAMS focuses more on traditional fund houses and retail distribution. KFin targets digital-first AMCs and institutional channels. CAMS emphasizes operational excellence. KFin prioritizes technology innovation. This differentiation allows both to maintain pricing discipline while serving different client needs.

The threat of disruption from blockchain or distributed ledger technology is often raised but misunderstood. While blockchain could theoretically replace centralized registries, the reality is more complex. Regulatory approval would take years. Existing investors would need education and migration. The cost savings are unclear given the need for governance and compliance layers. Most importantly, KFin could itself adopt blockchain technology if it proves superior. The infrastructure provider doesn't care about the underlying technology—it cares about providing reliable service.

As India's financial markets mature, the infrastructure requirements become more sophisticated, not less. Real-time settlement, fractional investing, cross-border transactions, embedded finance—each innovation requires robust backend systems. KFin's position at the center of these flows means it benefits regardless of which trends dominate. The platform that enables innovation captures value from all innovations.

The business model's resilience was proven during COVID-19. While transaction volumes initially dropped, the shift to digital channels accelerated adoption of KFin's technology solutions. SIP registrations moved entirely online. Investor onboarding became video-based. Document processing went paperless. Each change made KFin more essential, not less. The pandemic that could have been a crisis became a catalyst for digital transformation.

Looking ahead, the business model's evolution toward higher-value services is clear. Basic transaction processing will remain the foundation, but growth will come from analytics, advisory tools, and embedded finance solutions. The company that started as a record keeper is becoming an intelligence platform. The data flowing through KFin's systems, properly analyzed and packaged, is worth more than the transaction fees themselves.

VIII. International Expansion & Platform Strategy

The conference room at KFin's Hyderabad headquarters has a world map with pins marking their international presence—Malaysia, Singapore, Hong Kong, Philippines, Thailand, Canada, and the United States. Each pin represents not just a geographic expansion but a strategic bet that the infrastructure model perfected in India can be replicated globally. The early results suggest this bet is paying off handsomely.

The international strategy began with a simple insight: emerging markets face the same financial infrastructure challenges India faced two decades ago. Growing middle classes, nascent capital markets, regulatory evolution, digital transformation—the playbook KFin developed for India applies with local modifications. But unlike Western infrastructure providers who approach these markets with expensive, over-engineered solutions, KFin offers battle-tested systems at emerging market price points.

International and other investor solutions revenue was up by 56.6% year-on-year in recent quarters, validating the expansion strategy. But the numbers tell only part of the story. In Malaysia, KFin didn't just win clients—it transformed how the industry operates. When Malaysian mutual funds were struggling with paper-based processes, KFin introduced straight-through processing that reduced transaction times from days to minutes.

The Philippines expansion showcased KFin's ability to navigate complex regulatory environments. The country's securities regulations were fragmented across multiple agencies, each with different requirements. KFin's team spent months mapping these requirements, building relationships with regulators, and creating a compliance framework that satisfied all stakeholders. This patient approach paid off when they won the mandate to service the country's largest asset manager.

Singapore became the hub for Southeast Asian operations, but not in the traditional sense. Instead of building expensive infrastructure in the city-state, KFin created a hybrid model. Client-facing teams and relationship managers operated from Singapore, while transaction processing happened in Hyderabad. This delivered Singapore-level service quality at India-level costs—a compelling proposition for cost-conscious Asian asset managers.

The Hong Kong operations revealed an unexpected opportunity: Chinese asset managers looking to expand internationally needed infrastructure support for their offshore funds. KFin's platform, already configured for multi-currency and multi-jurisdiction operations, was perfectly suited. While Western providers charged millions for similar services, KFin could deliver at a fraction of the cost while maintaining institutional quality.

Thailand presented a different challenge—entrenched local competitors with deep government relationships. KFin's approach was clever: instead of competing head-on, they partnered with local banks to provide white-labeled infrastructure. The banks maintained client relationships while KFin powered the backend. This partnership model, refined in Thailand, became the template for entering other protected markets.

The GIFT City operations deserve special attention. India's international financial services center was designed to rival Singapore and Dubai, but lacked critical infrastructure. KFin established operations there early, becoming the preferred partner for international funds setting up India-focused vehicles. When global private equity funds wanted to raise India-dedicated funds from international investors, KFin provided the entire infrastructure—from investor onboarding to regulatory reporting.

But the boldest international move was entering the U.S. mortgage services market. This seemed like a departure from the core business, but the logic was sound. Post-2008 financial crisis, U.S. banks faced massive compliance requirements for mortgage documentation. They needed high-quality, low-cost processing—exactly what KFin offered. The acquisition of a small Texas-based mortgage servicer gave KFin the necessary licenses and local knowledge.

The U.S. operations grew from processing 10,000 mortgages monthly to over 100,000 within three years. The margins were lower than Indian operations, but the volumes were massive. More importantly, it established KFin's credentials in the world's largest financial market. When American asset managers evaluated KFin for their Asian operations, the U.S. presence provided credibility that no amount of marketing could achieve.

Canada became another surprising success story. The country's large Indian diaspora wanted to invest in Indian mutual funds but faced operational challenges. KFin created specialized NRI (Non-Resident Indian) services that simplified cross-border investing. This wasn't just about processing transactions—it involved navigating tax treaties, managing currency conversions, and ensuring compliance with both Canadian and Indian regulations.

The technology platform strategy for international markets was sophisticated. Instead of creating country-specific systems, KFin built a configurable platform that could be customized through parameters rather than code changes. Need to comply with Malaysian language requirements? Configure the parameter. Hong Kong tax calculations? Another parameter. This approach meant new market entry required weeks, not months of development.

The data insights from international operations created unexpected value. By processing transactions across multiple markets, KFin could identify cross-border trends before others. When Malaysian investors started buying Singapore REITs, KFin saw it first. When Hong Kong money began flowing into Indian markets, KFin knew the magnitude. This intelligence became valuable not just for clients but for regulators and policymakers.

Competition with global players like Computershare and State Street revealed KFin's unique advantages. These giants had legacy systems built for developed markets—expensive to operate and slow to change. KFin's cloud-native platform could deliver new features in weeks while they took months. When a Philippines mutual fund wanted mobile-first onboarding, KFin delivered in six weeks. Computershare quoted six months.

The partnership strategy with global technology providers multiplied KFin's reach. Instead of competing with companies like FIS and Temenos, KFin integrated with them. A global bank using Temenos for core banking could use KFin for fund administration. An asset manager on FIS for portfolio management could use KFin for investor services. These partnerships made KFin complementary rather than competitive.

The regulatory arbitrage opportunity was substantial. Many international financial regulations were modeled on developed market frameworks but implemented in emerging market contexts. KFin's experience navigating India's complex regulations—often more stringent than Western standards—made other markets seem simple by comparison. When Singapore introduced new fund regulations, KFin was compliant on day one while competitors scrambled.

Cultural advantages played a surprising role in international success. KFin's Indian heritage resonated in Asian markets where Western providers were seen as arrogant and expensive. The company's willingness to customize solutions, provide 24/7 support, and maintain reasonable pricing won over clients tired of being treated as second-tier by global giants. The same humility that characterized the domestic business became a competitive advantage internationally.

The international expansion also strengthened the domestic moat. Every global client added credibility with Indian regulators. Every international regulatory approval made SEBI more comfortable with KFin's governance. Every cross-border transaction processed built expertise that benefited Indian clients. The international business wasn't just about growth—it was about building a stronger core.

Looking ahead, the international platform strategy is evolving toward managed services. Instead of just processing transactions, KFin increasingly manages entire operations for global asset managers. A European fund wanting Asian exposure doesn't need to build local infrastructure—KFin provides everything from fund administration to investor services. This full-stack approach commands premium pricing and creates deeper client relationships.

The vision is ambitious but achievable: become the AWS of financial services infrastructure for emerging markets. Just as Amazon Web Services democratized computing infrastructure, KFin aims to democratize financial infrastructure. A startup mutual fund in Vietnam should be able to launch as easily as one in Mumbai. A pension fund in Africa should access the same technology as one in Singapore. This platform vision, if executed successfully, could make KFin a global infrastructure powerhouse.

IX. Playbook: Lessons in Crisis, Transformation & Scale

The KFin story offers a masterclass in crisis management, private equity transformation, and platform scaling. Each phase of the journey—from scandal to salvation to success—provides lessons that extend far beyond financial services. This is the playbook for turning disaster into opportunity, distrust into credibility, and infrastructure into innovation.

Lesson 1: Speed is Survival in Crisis Management

When the Karvy scandal broke, General Atlantic had hours, not weeks, to respond. Their 48-hour war room setup and immediate ring-fencing of the RTA business saved the company. The lesson is clear: in crisis, speed matters more than perfection. GA's team made decisions with 70% information that competitors would have debated for months. They understood that a good decision made immediately beats a perfect decision made too late.

The rebranding to KFin Technologies within 30 days was operationally complex but psychologically essential. Every day the Karvy name remained was another day of reputational damage. The ₹50 crore cost seemed excessive, but compared to losing clients worth hundreds of crores annually, it was a bargain. The lesson: when your brand becomes toxic, don't try to rehabilitate it—replace it entirely and immediately.

Lesson 2: Leadership Signaling in Turnarounds

The appointment of M.V. Nair as Chairman sent a powerful signal. Here was a banker of impeccable reputation, someone who had nothing to gain from association with a tainted company unless he believed in its transformation. This wasn't just about governance—it was about borrowing credibility when you have none. Every turnaround needs a figure whose personal reputation can bridge the trust deficit.

Sreekanth Nadella's appointment as CEO was equally strategic. As an outsider to the Karvy system but an insider to Indian financial services, he could drive change without being seen as naive. His technology background signaled the company's future direction. His operational experience meant he could execute, not just strategize. The lesson: in transformation, your leadership appointments are your strategy announcements.

Lesson 3: The PE Playbook - More Than Financial Engineering

General Atlantic's approach went beyond typical private equity financial engineering. They invested in technology when the company was bleeding clients. They paid retention bonuses when cash was tight. They hired senior talent when the future was uncertain. This patient capital approach—investing for long-term value creation rather than short-term cash extraction—is what separated successful transformation from asset stripping.

The governance changes were foundational, not cosmetic. Independent directors with real power. Audit committees with external members. Whistleblower hotlines reporting to the board. Technology committees overseeing investments. These structures created accountability that outlasted GA's ownership. The lesson: sustainable transformation requires institutional change, not just operational improvement.

Lesson 4: Building Trust in a Trust Business

Financial infrastructure is ultimately a trust business. You're asking clients to hand over their most sensitive data and critical operations. Once trust breaks, rebuilding it requires radical transparency. KFin's approach—inviting regulators to inspect operations, sharing technology architecture with clients, publishing operational metrics daily—went beyond industry norms. They understood that in trust businesses, transparency isn't a nice-to-have; it's existential.

The operational excellence during crisis became the foundation for trust rebuilding. Not missing a single NAV calculation or dividend payment while the company imploded around them proved competence under pressure. The lesson: in crisis, maintaining operational excellence is your most powerful marketing tool. Every successful transaction is a vote of confidence.

Lesson 5: Technology as Transformation Catalyst

The ₹500 crore technology investment during turnaround seemed excessive for a company in crisis. But this investment transformed KFin from a services company to a technology company. The cloud-native architecture, microservices approach, and API-first strategy weren't just modernization—they were differentiation. While competitors remained on legacy systems, KFin could innovate at startup speed with enterprise reliability.

The platform approach—building once and deploying many times—created operating leverage that traditional service models couldn't match. Every new feature benefited all clients. Every bug fix improved the entire platform. Every security enhancement protected everyone. This network effect in improvement meant the platform got better faster than any single-tenant solution could.

Lesson 6: Operating Leverage in Platform Businesses

KFin's business model demonstrates the power of operating leverage in platform businesses. The fixed costs—technology infrastructure, regulatory compliance, core operations—remain relatively constant. But revenue scales with volume. This means that growth translates directly to margin expansion. During India's mutual fund boom, KFin's margins expanded naturally without cost cutting or price increases.

The key insight is that infrastructure businesses are scale games. The first transaction costs crores to process (when you amortize all fixed costs). The millionth transaction costs paise. This economics means that market share isn't just about revenue—it's about unit economics. The lesson: in platform businesses, scale isn't everything; it's the only thing.

Lesson 7: The Power of Regulatory Relationships

KFin's relationship with regulators evolved from suspicion to partnership. This didn't happen through lobbying or influence peddling. It happened through consistent delivery, proactive compliance, and genuine contribution to market development. When SEBI needed data for policy making, KFin provided it. When PFRDA wanted to modernize pension infrastructure, KFin invested in it.

The lesson is that in regulated industries, regulators are stakeholders, not adversaries. The companies that thrive are those that align their interests with regulatory objectives. KFin understood that helping regulators achieve their goals—market development, investor protection, systemic stability—created opportunities for business growth.

Lesson 8: Why Financial Infrastructure is the Ultimate Sticky Business

The switching costs in financial infrastructure create natural moats. But KFin went beyond relying on switching costs. They made themselves indispensable through continuous innovation. Every new feature, every new service, every new integration made switching harder and less attractive. The lesson: stickiness isn't just about making leaving hard; it's about making staying valuable.

The data accumulation over time creates another moat. Twenty years of transaction history, investor behavior patterns, and operational knowledge can't be replicated. New entrants can build better technology, but they can't recreate history. This temporal moat—the advantage that comes from simply being there longer—is underappreciated in infrastructure businesses.

Lesson 9: The Network Effects in B2B Platforms

KFin demonstrates that network effects aren't limited to consumer platforms. Every mutual fund that joins makes the platform more valuable for distributors. Every distributor makes it more attractive for funds. Every corporate client adds to the data intelligence. Every international client enhances global credibility. These reinforcing loops create competitive advantages that strengthen over time.

The key is identifying and nurturing these network effects. KFin deliberately built features that enhanced network value—unified distributor interfaces, cross-client analytics, shared compliance modules. The lesson: in B2B platforms, network effects are less obvious but equally powerful. The winners are those who architect their platforms to maximize these effects.

Lesson 10: The Transformation Mindset

Perhaps the most important lesson is about organizational mindset during transformation. KFin succeeded because it embraced radical change rather than incremental improvement. Old ways of working weren't modified; they were eliminated. Legacy systems weren't upgraded; they were replaced. The culture wasn't evolved; it was revolutionized.

This required courage from leadership and faith from employees. Many comfortable with the old ways left. Those who stayed had to relearn their jobs. But this creative destruction was necessary. The lesson: transformation isn't about making the existing better; it's about creating something entirely new. Half-measures don't work in turnarounds.

The playbook that emerges from KFin's journey is both specific and universal. Specific in its application to financial services and infrastructure businesses. Universal in its lessons about crisis management, transformation, and platform building. It shows that even the most dire situations—a parent company scandal, regulatory scrutiny, client exodus—can be overcome with the right approach.

X. Bull vs. Bear Case & Competitive Analysis

The investment case for KFINTECH splits sharply between believers who see a multi-decade compounder and skeptics who worry about valuation, competition, and technological disruption. With the stock trading at 56.2x P/E and 13.7 times book value, the market is clearly pricing in significant future growth. Whether that optimism is justified depends on your view of India's financial future and KFin's ability to capture it.

The Bull Case: Riding India's Financialization Wave

The bulls start with a simple observation: India's mutual fund penetration is still only 15% of households, compared to over 50% in developed markets. With a young population, rising incomes, and increasing financial awareness, the runway for growth extends decades. Every percentage point increase in penetration means millions of new investors, billions in new assets, and substantial revenue growth for infrastructure providers like KFin.

The SIP revolution is just beginning. Monthly SIP flows have grown from ₹1,000 crores in 2014 to over ₹20,000 crores today, and still represent less than 5% of household savings. As Indians shift from physical assets (gold, real estate) to financial assets, the systematic investment habit will only strengthen. KFin processes the majority of these transactions, earning fees on each one. The beauty of SIPs is their stickiness—once started, they typically continue for years, creating predictable, recurring revenue streams.

The IPO pipeline provides another growth vector. India is witnessing unprecedented startup creation and wealth generation. Every unicorn will eventually need to go public. Every public listing needs a registrar. As the #1 corporate registrar in India, KFin is positioned to capture the lion's share of this business. The LIC IPO success demonstrated their ability to handle complexity at scale—a capability competitors struggle to match.

New asset classes offer massive expansion opportunities. Alternative Investment Funds (AIFs) are growing at 40% annually as wealthy Indians diversify portfolios. REITs and InvITs are just beginning to gain traction. Cryptocurrency regulation, when it comes, will require institutional infrastructure. Each new asset class needs the same services KFin provides to mutual funds—investor onboarding, transaction processing, record keeping, compliance reporting. The platform built for one asset class extends naturally to others.

The pension opportunity is particularly compelling. As one of the two players providing central recordkeeping services for the National Pension System, KFin has privileged access to India's retirement savings market. With only 5% of Indians having formal retirement savings (versus 40%+ in developed markets), the growth potential is enormous. The government's push for pension coverage, combined with tax incentives, could trigger explosive growth similar to the 401(k) revolution in the United States.

International expansion multiplies the opportunity. If KFin can capture even 5% of the Southeast Asian market, it would double their current revenue. The success in Malaysia and Philippines proves the model travels. As emerging markets develop capital markets, they need exactly what KFin offers—proven infrastructure at reasonable costs. The global TAM (Total Addressable Market) is 20x the Indian opportunity.

Technology leadership creates competitive advantages that compound over time. While CAMS remains larger, KFin is recognized as the technology leader. New-age fund houses prefer KFin's API-first approach. Digital distribution platforms integrate more easily with KFin's systems. As financial services increasingly become technology services, KFin's positioning strengthens. The recent AI and analytics initiatives could create entirely new revenue streams from the data flowing through their platform.

The operating leverage inherent in the model means margins expand naturally with growth. EBITDA margins improved 315 bps to 42.0% in recent quarters without major cost cutting. As volumes grow, fixed costs get spread over more transactions, driving margin expansion. This isn't a business that needs to choose between growth and profitability—growth creates profitability.

Management quality under the new regime inspires confidence. The successful navigation of the Karvy crisis demonstrated exceptional execution under pressure. The technology transformation showed strategic vision. The international expansion proved ambitious thinking. With General Atlantic's continued involvement and an experienced leadership team, execution risk appears manageable.

The valuation, while optically expensive, may be reasonable given the growth trajectory. The stock has rallied 56% in just 13 trading days after strong results, suggesting the market sees acceleration ahead. If KFin can maintain 20%+ revenue growth and 25%+ profit growth—achievable given the market dynamics—the current valuation could prove conservative in hindsight.

The Bear Case: Priced for Perfection in an Uncertain World

The bears start with valuation. At 56x earnings, KFin is priced as if nothing can go wrong. Any disappointment—a regulatory change, a major client loss, a technology glitch—could trigger a significant correction. The stock has already captured much of the optimism about India's financial future. Where's the margin of safety?

The duopoly with CAMS might not last forever. SEBI has historically been skeptical of concentrated market structures. If regulators decide to encourage more competition—through licensing requirements, price caps, or forced interoperability—the economics could deteriorate rapidly. The mutual fund industry faced similar regulatory pressure on fees; the infrastructure providers could be next.

Technology disruption remains a real threat. Blockchain and distributed ledger technology could eventually eliminate the need for centralized registrars. While implementation challenges exist today, technology moves fast. A government-backed blockchain initiative or a well-funded startup with revolutionary technology could disrupt the entire industry. KFin's legacy infrastructure, however modernized, might become obsolete.

Client concentration risk is material. The top 10 clients contribute over 40% of revenue. Losing even one major mutual fund house would impact earnings significantly. As these clients grow larger, their negotiating power increases. They might demand price reductions, bring services in-house, or collaborate to create an industry-owned utility. The switching costs that protect KFin today could motivate clients to find alternatives tomorrow.

The international expansion, while promising, faces execution challenges. Competing with global giants like Computershare and State Street requires sustained investment. Regulatory requirements vary significantly across markets. Cultural differences matter more in financial services than technology. The mortgage services business in the U.S., while growing, operates at much lower margins than the core Indian business. International expansion might dilute returns rather than enhance them.

Market cyclicality could impact growth. The mutual fund industry is inherently cyclical. Bear markets reduce assets under management, decrease transaction volumes, and delay IPOs. While KFin survived COVID-19, a prolonged market downturn could pressure revenues and margins. The high fixed cost base means downturns impact profitability disproportionately.

The intrinsic value calculations raise concerns. At an intrinsic value of ₹900.81 versus the current price of ₹1,120, the stock appears 20% overvalued. This suggests the market is pricing in extremely optimistic assumptions about future growth. Any deviation from these assumptions could lead to valuation compression.

Competition from CAMS remains formidable. Despite KFin's technology advantages, CAMS maintains dominant market share in mutual fund assets. CAMS has also modernized its technology stack and expanded internationally. The comfortable duopoly of today could become a fierce battle for market share tomorrow, pressuring margins and increasing customer acquisition costs.

Regulatory risks extend beyond market structure. Data privacy regulations are tightening globally. Cybersecurity requirements are increasing. Cross-border data transfer restrictions could impact international operations. Each new regulation increases compliance costs and operational complexity. The regulatory moat that protects KFin also constrains its flexibility.

Key person risk deserves consideration. While the leadership team is strong, the departure of critical executives could impact execution. The technology transformation was led by specific individuals whose loss would be felt. The relationships with regulators and major clients often depend on personal connections that can't be easily transferred.

Competitive Analysis: The CAMS Comparison

The KFin-CAMS rivalry defines India's financial infrastructure landscape. CAMS, with 68% market share in mutual fund assets, remains the dominant player. But market share alone doesn't tell the full story. KFin's 33.5% share in equity mutual funds—the fastest-growing segment—suggests momentum is shifting. The two companies have evolved different strategies that could lead to divergent outcomes.

CAMS focuses on operational excellence and relationship depth. Their longer history (established 1993) provides deeper client relationships and institutional knowledge. They maintain higher margins through operational efficiency rather than technology innovation. Their conservative approach appeals to traditional fund houses that prioritize stability over innovation.

KFin emphasizes technology innovation and platform expansion. Their modern architecture enables faster product development and easier integration. They target new-age fund houses and digital distribution channels. Their international expansion is more aggressive, and their asset class diversification broader. They're building a platform; CAMS is optimizing a service.