Kay Cee Energy & Infra Limited: Powering the Rajasthan Corridor and the SME Capital Craze

I. Introduction & Episode Roadmap

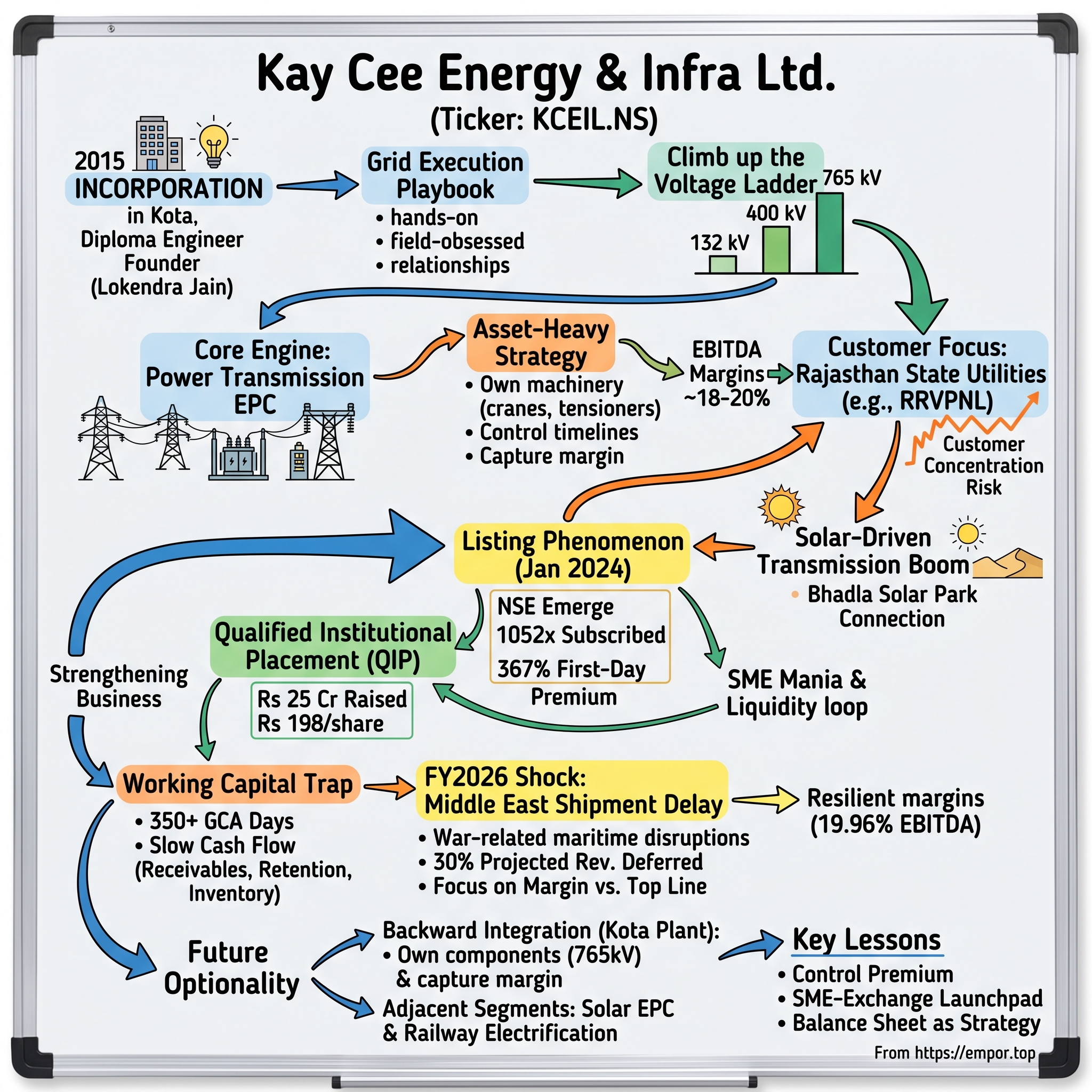

On the morning of January 5, 2024, brokers watching the National Stock Exchange's SME platform, NSE Emerge, saw something that looked less like a market and more like a lottery draw. A tiny electrical contractor from Kota, Rajasthan — a company most institutional investors had never heard of and could not, by regulation, easily buy — opened for trading at ₹252 per share against an issue price of ₹54. That was a first-day premium of roughly 367%, a near-quadrupling before most of India had finished its morning chai.2

Rewind three days. The company, Kay Cee Energy & Infra Limited (KCEIL), had closed a ₹15.93 crore initial public offering that was subscribed an almost absurd 1,052 times on aggregate.1[^2] Retail investors put in bids at 1,311 times their allotted quota; the high-net-worth non-institutional category bid 1,669 times theirs.[^3] Stack those bids up and the public had pledged well over ₹11,000 crore chasing a sliver of stock worth about ₹16 crore — a demand-to-supply ratio that tells you almost nothing about the company and almost everything about the mania then gripping India's micro-cap market.

Here is the puzzle this episode unpacks. How does a regional electrical contractor — founded in 2015 by a diploma engineer, executing power-transmission projects almost entirely inside one Indian state — command that kind of frenzied appetite? How did it go from stringing 132 kV lines to commissioning extra-high-voltage substations rated up to 765 kV? And how, just fifteen months after listing at ₹54, did the same company place stock with qualified institutions at ₹198 — nearly four times its IPO price — in its first-ever Qualified Institutional Placement?7

The answers sit at the intersection of two very different stories. One is a genuine operating story: a founder with three decades of grid experience, an unfashionable "asset-heavy" execution model that produced EBITDA margins near 18–20%, and a front-row seat to Rajasthan's solar-driven transmission boom. The other is a capital-markets story: the SME-IPO gold rush of 2023–24, in which liquidity and speculation re-rated micro-caps to valuations their cash flows could not yet justify.

The map for the next two hours: the genesis of founder Lokendra Jain and his diploma-engineer's playbook; the engineering economics of extra-high-voltage grid EPC and why owning your own machinery matters; the customer concentration and order book that define the growth runway; the listing phenomenon and the QIP re-rating; the brutal working-capital arithmetic that makes infrastructure revenue a "mirage" without cash discipline; the Middle East shipping delay that deferred nearly a third of FY2026's projected revenue; the backward-integration bet in Kota; and finally a hard-nosed bull-versus-bear stress test using Porter and Helmer. Throughout, one discipline: separating what management claims from what the evidence proves. Let's start where every good origin story starts — with the founder and the field.

II. The Genesis: Lokendra Jain & The Diploma Engineer's Playbook

Picture the Rajasthan grid in the late 1990s and 2000s: a sprawling, thirsty state — geographically India's largest — dotted with substations that had to push power across vast semi-arid distances to towns, mines, and irrigation pumps. The glamorous end of this business belonged to national giants. Larsen & Toubro, KEC International, and Kalpataru Projects bid the marquee transmission packages, mobilized armies of engineers, and moved on. But beneath them lay a fragmented layer of regional execution — the actual bolting of towers, stringing of conductors, and commissioning of switchgear — carried out by small, often under-capitalized local contractors who lived or died on their relationships with the state utility.

Into this layer walked Lokendra Jain. He was not an IIT-minted executive parachuting in from a metro. He held a diploma in electrical engineering, and he spent the better part of three decades on Rajasthan's grid — surveying line routes across scrubland, supervising tower foundations, and standing under live-line tension where a miscalculation is not a spreadsheet error but a fatality. CRISIL, in its rating rationale, credits the promoters with "three decades" of experience in EPC and extra-high-voltage transmission — a cornered-resource-style asset we will return to.3 That experience is the hidden capital of this company: not a patent, not a factory, but a mental map of how Rajasthan's power bureaucracy actually awards, inspects, and — crucially — pays.

The diploma detail is not a throwaway; it is a clue to the kind of company this is. A diploma engineer in India is a practitioner, trained on the shop floor and the field rather than the lecture theatre — the person who knows how the equipment actually behaves, not merely how it is supposed to behave on paper. Founders of this stripe tend to build companies in their own image: hands-on, execution-obsessed, distrustful of anything they cannot personally inspect. That temperament is the psychological root of the asset-heavy model we will examine — a founder who has spent thirty years watching rented cranes arrive late and subcontractors cut corners is exactly the kind of person who decides, against conventional financial advice, to own the machinery and control the crew himself. The strategy and the biography are the same fact viewed from two angles.

The flip side of a founder-embodied company is the governance question a careful investor must hold open. When the competitive edge, the key relationships, and the operating judgment all reside in one promoter and his family, the company inherits both his strengths and his mortality. Succession, the depth of the professional bench beneath him, and the independence of the board are not abstractions in a business like this; they are the difference between a durable franchise and a one-generation contractor. KCEIL has not yet had to answer these questions in public, which is itself worth noting: the institutionalization that a QIP begins on the shareholder register has to be matched by institutionalization of management depth, and that is a slower, less visible process.

KCEIL was incorporated in 2015 in Kota, the industrial and coaching-classes hub of southeastern Rajasthan, as Kay Cee Energy & Infra Private Limited.3 Its opening premise was unromantic and specific: hitch itself to the capex cycle of Rajasthan Rajya Vidyut Prasaran Nigam Limited (RRVPNL), the state transmission utility, and the distribution companies (DISCOMs) beneath it. That meant winning tenders, executing on time, and — the part that separates survivors from casualties in this business — collecting on retention money and security deposits without going broke while you wait.

It helps to appreciate what "starting" a transmission-EPC company in 2015 actually demanded, because it explains why so few of KCEIL's peers ever cleared the runway. A first-time contractor faces a chicken-and-egg wall: you cannot win a meaningful transmission package without a pre-qualification record, and you cannot build a record without first winning packages. The way through is to start small — sub-transmission and lower-voltage jobs where the eligibility bar is low — deliver flawlessly, and use each completed project as a rung to reach for the next voltage class. Every rung requires more working capital than the last, because bigger projects mean bigger retention withholdings and longer payment cycles. So the early history of a company like KCEIL is really a story of a founder repeatedly betting the firm's thin cash reserves on the next-larger project, trusting that a state utility would eventually pay. Most contractors who try this either stall at a voltage ceiling they cannot technically clear, or run out of cash financing the growth. KCEIL did neither, and that survival — more than any single contract — is the quiet achievement of its first eight years.

There is a cultural dimension worth naming, too. Kota is not a power-sector capital; it is a city best known for its coaching institutes and its chemical industry. A grid contractor headquartered there, rather than in a metro, is inherently a local, relationship-run operation. That geography is not incidental to the strategy — it is the strategy. Being physically embedded in Rajasthan, with machinery parked in Kota and a promoter who has spent his career among the state's power engineers, is precisely what lets KCEIL mobilize faster and price more tightly on local tenders than a national firm running its Rajasthan work from a distant regional office.

The eight years between incorporation and IPO are the part of the story that never makes the headlines, and they are the part that matters most. This was a slow climb up the voltage ladder. A contractor's credibility in transmission is measured almost literally in kilovolts: the ability to execute a 400 kV or 765 kV project is a pre-qualification gate that shuts out the vast majority of small players. KCEIL moved from lower-voltage 132 kV work toward the complex 400 kV and 765 kV class of substations and lines — each step unlocking bigger, higher-margin, less-crowded tenders. Along the way, by the company's own account, it collected the kind of trophy that carries real weight with a state utility: an "Excellent Construction Work" recognition from RRVPNL, the sort of preferred-vendor signal that helps a regional contractor keep winning repeat work.10 Self-reported awards deserve a light discount — they are marketing as much as evidence — but the independently verifiable version of the same claim is more persuasive: CRISIL cites "repeat business from existing customers" and new customer additions as a rating strength, which is what genuine execution credibility actually looks like on paper.34

For an investor, the takeaway from the genesis years is not the awards; it is the nature of the moat being built. It was not a technology edge. It was accumulated, relationship-dense, jurisdiction-specific execution credibility — deep but narrow. That depth is exactly why KCEIL could later bid 765 kV work; the narrowness is exactly why over 90% of its revenue would remain trapped inside one state's budget. Hold that tension in mind, because it defines everything that follows. First, though, we need to understand what these projects actually are — and why the way KCEIL chose to build them is the real engine of its margins.

III. The Core Engine: Power Transmission EPC & The "In-House" Playbook

Start with a simple mental picture. When a giant solar park in the Rajasthan desert generates a gigawatt of electricity at midday, that power is useless unless it can be lifted to extremely high voltage, carried hundreds of kilometres on transmission lines, stepped back down, and fed into the grid where people actually live. The machinery that does the lifting and stepping is the extra-high-voltage (EHV) substation; the wires that do the carrying are EHV transmission lines. KCEIL builds both, end to end — engineering, procurement, and construction, or EPC.

It is tempting to imagine this as glorified electrical wiring. It is not. Building a 400 kV substation is closer to assembling a small, unforgiving industrial plant. It involves land surveying and geotechnical work; pouring tower and equipment foundations that must hold under decades of wind and thermal load; erecting steel structures; stringing heavy conductors under precisely controlled mechanical tension (get it wrong and the line either sags into the ground or snaps); and then the delicate part — installing and testing transformers, switchgear, circuit breakers, and the SCADA automation systems that let a control room miles away open and close the grid. At 765 kV — the top of the Indian transmission pyramid — the tolerances tighten and the roster of contractors qualified to bid shrinks dramatically. That shrinking list is itself the barrier to entry: you cannot bid a 765 kV package without a track record of having safely built one, which is a wonderfully circular moat for whoever got there first.

A useful analogy: think of voltage classes the way you'd think of pilot licences. A private licence lets you fly a small propeller plane; it does not let you captain a wide-body jet. Each higher rating requires demonstrated hours on progressively larger, less forgiving aircraft, and the airline will not hand you the jet until you have proven you can fly it. Transmission works the same way. The 132 kV job is the propeller plane; the 765 kV substation is the wide-body. And just as a fatal error at altitude ends careers, a safety lapse on a live extra-high-voltage line ends a contractor's eligibility — utilities weight safety records heavily in pre-qualification, so a single serious incident can lock a firm out of the bids that matter most. This is why KCEIL's climb up the voltage ladder over its first decade was not a formality but the entire competitive point: each rung it cleared removed a slice of the field it would ever have to compete against again.

Why does a small contractor even attempt the harder voltage classes rather than staying comfortable in the crowded lower rungs? Because that is where the pricing lives. The 132 kV tender attracts dozens of eligible bidders and gets competed down to razor margins; the 765 kV package attracts a handful, and the winner keeps more of the value. Moving up the voltage ladder is, in effect, moving away from commoditized competition toward something closer to an oligopoly of the technically qualified. It is the closest thing this tender-driven industry offers to pricing power — and it is why an ambitious contractor is always trying to climb.

Now the strategic choice that defines KCEIL. The default playbook for a small EPC contractor is asset-light: win the tender, then rent the cranes, hire the tensioning rigs, lease the transport fleet, buy or borrow the testing kits, and subcontract most of the labour. It is capital-efficient and keeps the balance sheet clean. It is also, in this business, a quiet trap. When your critical equipment belongs to someone else, you are last in the queue when a crane is scarce, you pay a spread on every rented machine, and you lose control of the one variable a utility punishes hardest — time. Miss a milestone and liquidated-damages clauses start eating your margin.

KCEIL went the other way. It bought and maintained its own fleet — heavy construction machinery, specialized hydraulic tensioners for stringing, emergency restoration equipment, and its own suite of testing instruments. This is the asset-heavy counter-strategy, and it is the load-bearing wall of the entire investment thesis. Owning the critical path buys three things: control over timelines, bargaining power over the subcontractors and suppliers who no longer hold you hostage, and the captured margin that would otherwise leak out as rental spreads.

Consider what the rental spread actually costs an asset-light competitor. A firm that rents a hydraulic tensioner pays a daily rate that must cover the owner's capital cost, maintenance, transport, and profit — every day the machine sits on site, whether it is running or idle between milestones. Multiply that across cranes, transport, and testing rigs over a multi-year project, and the leakage is not trivial; it is a structural haircut to margin. When KCEIL owns the same equipment, that entire spread — including the profit an equipment lessor would have earned — stays inside the company. The machine still depreciates and still needs maintenance, so ownership is not free; but on a fleet kept reasonably utilized across a dense cluster of nearby Rajasthan projects, the owned-asset math beats the rental math. Utilization is the hinge. The asset-heavy model rewards a contractor with enough local project density to keep its machines busy, and punishes one whose fleet sits idle — another reason KCEIL's regional concentration and its margin profile are two sides of the same design choice.

There is a subtler benefit that rarely shows up in the numbers: schedule control as a bargaining chip. A contractor who controls its own equipment and can credibly promise a completion date has leverage in negotiations with a utility and with its own subcontractors. It can sequence work to hit high-value milestones early, accelerating billing. An asset-light rival, dependent on whenever the rental crane becomes available, is forever managing around someone else's calendar. In a business where time is money in the most literal, liquidated-damages sense, owning the clock is worth more than the balance-sheet purists concede.

Does the evidence support the claim? Largely, yes — with a caveat. KCEIL's operating margins have run at a level that genuinely stands out for a micro-cap contractor: roughly 19.9% in FY2024, 17.79% in FY2025, and back near 19.96% (EBITDA) in FY2026.359 For context, large-cap benchmark KEC International — a national leader with vastly greater scale — has historically operated in the high-single-digit to low-double-digit EBITDA range, the structural reality of a competitive, tender-driven industry.12 KCEIL earning high-teens-to-20% margins at a fraction of the scale is the anomaly the asset-heavy story is meant to explain, and it is a reasonable explanation. The caveat, which CRISIL itself flags: margin sustainability "amid competitive pressures remains monitorable."3 Owning machinery protects margins; it does not repeal the gravity of a lowest-bidder tender market. A dip from ~20% to ~18% and back is not noise to wave away — it is the industry pulling on the leash. The asset-heavy model is a genuine edge, but it is a margin cushion, not a margin fortress.

That cushion, though, only matters if there is work to win. And KCEIL's work came overwhelmingly from one place — which is both the source of its efficiency and the sharpest point of its risk.

IV. Customer Dynamics, Regional Concentration, and the Order Book

There is a reason a Kota-based contractor could grow this fast this decade, and its name is Bhadla. The Bhadla Solar Park in Rajasthan's Jodhpur district is one of the largest solar installations on Earth, and it is only the most famous node in a state that has become India's undisputed solar capital. Sun-drenched, sparsely populated, and blessed with cheap land, Rajasthan has attracted gigawatts of renewable generation. But solar power has a geography problem: it is generated in remote deserts and consumed in distant cities, and it is intermittent, spiking at noon and vanishing at dusk. Absorbing it requires a massive, unglamorous build-out of exactly what KCEIL sells — EHV substations and transmission lines to collect, step up, and evacuate all that midday electricity into the national grid.

So KCEIL was not merely operating in a good state; it was sitting at the physical chokepoint of a structural boom. The company's fortunes are wired directly to Rajasthan's grid-expansion capex, which is in turn wired to India's renewable-energy ambitions. When the tailwind is this strong, concentration can look like brilliance.

It is worth dwelling on the physics of why renewables demand so much transmission, because it is the whole macro thesis in one idea. A conventional thermal plant is built near demand and runs steadily around the clock, so it needs relatively little new long-distance grid. Solar and wind are the opposite: they are built wherever the sun and wind are best — often hundreds of kilometres from cities — and they generate in variable, weather-dependent bursts. To make that power useful, you must move it far and absorb its swings, which means far more transmission line per unit of generation than the old thermal grid ever required. India's renewable build-out is therefore not just a generation story; it is, underneath, a transmission story of at least equal size. Every gigawatt of desert solar implies a corresponding build-out of the substations and EHV lines that evacuate it — the exact product KCEIL sells. That is the deepest reason the bull case has real structural support and not merely a cyclical one: the grid must be built for the energy transition to happen at all, and Rajasthan is where a disproportionate share of it gets built.

The problem is that concentration is symmetrical — it cuts both ways. Historically, the overwhelming majority of KCEIL's revenue has come from within Rajasthan's borders, and the customer roster reads like a directory of the state's power sector: the transmission utility RRVPNL and distribution companies such as Jaipur Vidyut Vitran Nigam and Ajmer Vidyut Vitran Nigam, alongside a handful of large private players like Sterlite Power. This is client concentration layered on top of geographic concentration, and it means KCEIL's growth, cash flow, and even survival are hostage to the budgetary rhythm and political weather of a single state government. CRISIL names this plainly, citing "dependence on the timing of government/PSU expenditure" as a core weakness.3 A fiscal squeeze in Jaipur is not a footnote for this company; it is an existential variable.

Which brings us to the metric investors should actually watch: the order book. This is the contracted, not-yet-executed work that gives an EPC contractor its revenue visibility. As of September 30, 2025, KCEIL's order book stood at roughly ₹575 crore, executable over the next 18–24 months per CRISIL.3 Set that against FY2026 revenue of ₹165.59 crore and you get a book-to-bill ratio comfortably above 3x — meaning the company entered the year with something like three years of visible revenue already signed.35 For a business this small, that is a genuinely healthy runway, and it is the single strongest piece of evidence in the bull case.

To appreciate how much the book has grown, rewind to the CRISIL data points. The order book was around ₹532 crore as of September 2024 and ₹575 crore a year later, even as the company billed well over ₹150 crore of revenue in between.34 A book that stays large while you execute against it means new wins are replacing completed work faster than you can burn it down — evidence that KCEIL is not just harvesting a one-time bulge of contracts but continuously replenishing its pipeline. For a contractor, a flat-to-growing book during a high-execution year is a healthier sign than a shrinking one, because it shows the tender-winning engine is keeping pace with the delivery engine.

But a book-to-bill ratio is a headline, not an X-ray. The question a skeptical investor should press is one of quality, not just quantity. An order book stuffed with high-margin substation installation and specialized supply is worth far more than the same rupee value of low-margin cable-laying or generic civil work. KCEIL does not disclose a clean margin-weighted breakdown of its book, so this remains a partial blind spot — and blind spots in an order book are where future margin disappointments hide. The visibility is real; the composition is a "trust but verify." A fat order book also means very little if the cash it generates takes a year to come home — a problem we will meet in full force shortly. But first, the event that put this company on every retail trader's screen.

V. The Listing Phenomenon & Capital Allocation

To understand January 2024, you have to understand the fever. Through 2023, India's SME IPO platforms — NSE Emerge and BSE SME — had turned into the hottest casino in the country's equity market. Retail and HNI investors, flush with post-pandemic liquidity and chasing the guaranteed-looking pop of listing-day gains, were subscribing tiny issues hundreds or thousands of times over. Into this fever stepped KCEIL, with an offer almost comically small relative to the demand it would attract.

The mechanics were modest. The IPO opened on December 28, 2023 and closed on January 2, 2024, offering 29.5 lakh fresh equity shares of ₹10 face value in a price band of ₹51–54, to raise ₹15.93 crore.1 The proceeds were earmarked not for some transformational acquisition but for the unglamorous lifeblood of an EPC business — incremental working capital and general corporate purposes — a tell we will decode in the next section. The book ran by GYR Capital Advisors.

Step back and consider what the SME-IPO structure does to incentives, because it explains the mania better than any single company can. NSE Emerge and BSE SME were created to give small companies — too tiny for the main board's rigorous requirements — a regulated path to public capital. The trade-off is lighter disclosure, larger minimum lot sizes intended to keep out the smallest retail punters, and far thinner float. That thin float is the accelerant. When only a handful of crores of stock will ever trade, and demand is running hundreds of times oversubscribed, the listing-day price is set by whoever is most desperate to own a scarce thing — not by any sober estimate of value. Through 2023 and into 2024, a self-reinforcing loop took hold: listing pops drew in more speculative money, which drove subscription multiples higher, which produced bigger pops. KCEIL was not the cause of that loop; it was one of its most vivid symptoms. An investor reading the 1,052-times headline should hear it as a data point about market psychology in that window, and mentally quarantine it from any judgment about the underlying contractor.

It is also worth noting who could and could not participate. Because SME issues carry large lot sizes and are pitched at sophisticated investors, the frenzy was dominated by retail traders willing to lock up cash for a few days chasing a listing gain, and by HNIs deploying leverage to amplify their allotments — which is exactly why the HNI category, at 1,669 times, ran even hotter than retail.[^3] The institutions that would later anchor the QIP were largely absent from the IPO. That sequencing — retail frenzy first, institutions later — is itself the SME life cycle in miniature.

Then the fever spoke. The issue was subscribed 1,052 times overall, with the HNI/NII book at 1,669 times, retail at 1,311 times, and even the qualified-institutional slice at nearly 128 times.[^2][^3] On listing day, January 5, 2024, the stock opened at ₹252 — a roughly 367% premium — handing anyone lucky enough to receive an allotment a near-quadruple overnight.2 It is worth stating plainly what this did and did not mean. It did not mean the market had carefully appraised KCEIL's discounted cash flows and found ₹252 fair. It meant that when you offer ₹16 crore of stock to a market bidding ₹11,000 crore, price discovery breaks and scarcity does the pricing. The subscription number is a fact about liquidity and speculative appetite in Indian micro-caps in early 2024 — not a verdict on the business.

Here is where management did something genuinely shrewd, and where the capital-markets story gets interesting. A less disciplined promoter might have treated a re-rated stock as a personal ATM. Instead, KCEIL used its inflated currency to strengthen the actual business. In April 2025 — just fifteen months after listing — the company executed its first Qualified Institutional Placement, the QIP being the mechanism by which a listed Indian company sells shares directly to institutions. It raised ₹25.03 crore by issuing 12.64 lakh shares at ₹198 each, drawing domestic and international qualified institutional buyers.78

Sit with the arithmetic for a moment. Shares that were issued to the public at ₹54 in January 2024 were placed with institutions at ₹198 in April 2025 — roughly a 266% higher price in fifteen months. Whatever one thinks of the valuation, the capital-allocation logic is sound: raise equity when your currency is expensive, use it to fund the working capital the business structurally consumes, and pull institutional shareholders onto the register in the process, nudging the company from a retail-frenzy stock toward something institutions can own. The QIP added roughly ₹25 crore of permanent capital precisely when the balance sheet needed cushioning; net worth was set to climb from about ₹61.69 crore in March 2025 to over ₹112 crore by March 2026, helped by both the placement and retained profit.3

Compare this behaviour to the two failure modes that plague newly-listed promoters, because the contrast is where credibility is earned. The first failure mode is the promoter who sells his own shares into the post-listing pop — cashing out personally while public shareholders hold the bag. The second is the one who lets a re-rated stock go to his head and blows the proceeds on an ego-driven acquisition or an unrelated "diversification." KCEIL did neither. It issued new shares (non-dilutive to the extent it funded genuine growth rather than cashing out insiders) and routed the money into the working capital the business demonstrably needs to grow. That is a boring, correct use of an over-valued currency — and boring correctness in capital allocation is exactly what a long-term investor should want to see from a founder-run micro-cap. The QIP is the single best piece of evidence in the file that this management thinks like operators building a company rather than promoters monetizing a listing.

The counterpoint an activist would raise: a QIP is still dilution, and a business that must periodically issue equity to fund its own growth is quietly telling you that its return on incremental capital, after accounting for the shares printed to fund it, may be lower than the headline profit growth suggests. Issuing stock at ₹198 is smart if that stock is genuinely worth ₹198; it is value-destructive for existing holders if it is not. The capital allocation is defensible; whether it compounds value per share depends entirely on the price at which the equity is raised versus its intrinsic worth — a question the market, not management, will ultimately answer.

But notice the word that keeps recurring — working capital. Both the IPO and the QIP existed, at bottom, to feed the same hungry mouth. Why does a profitable, high-margin company with a three-year order book keep needing to raise cash? The answer is the least glamorous and most important part of this entire story.

VI. The Working Capital Trap: Gross Current Assets and Cash Flows

Here is the paradox at the dark heart of Indian infrastructure investing: a company can grow revenue smartly, earn 20% margins, report rising profits — and still generate little or no actual cash. Revenue growth in EPC can be a mirage, and the desert it shimmers over is the working-capital cycle. To see how it swallows a contractor, you have to follow a single rupee of a KCEIL project from billing to bank account.

The key gauge is Gross Current Assets (GCA) days — a measure of how long capital stays locked up in the business before it recycles into cash. For KCEIL, GCA days have run at a punishing 359 days as of March 2025, down from an even more extreme 439 days a year earlier, and CRISIL expects the number to hover in the 350–360 range.34 Translate that from the spreadsheet: it takes KCEIL roughly a full calendar year to convert the capital it deploys back into cash. For every rupee of growth, the company must pre-fund about a year of that rupee sitting in receivables, inventory, and retention.

Three forces drive that year-long lock-up. First, the retention-money penalty. State utilities typically withhold a slice of every billing milestone — often around 10% — as security, releasing it only after the project is commissioned and a defect-liability period has passed, sometimes 12 to 24 months later. That retention is real, earned money the contractor cannot touch. Second, debtor days: even the portion that is billable takes about 96 days to actually arrive, gated by the fiscal releases of cash-strapped state entities.3 Third, inventory, running near 99 days, because an asset-heavy contractor stocks components and equipment to keep projects moving.3 Add them up and you have a business that is, in effect, extending a year-long interest-bearing loan to the government of Rajasthan on every project it wins.

Here is the counterintuitive trap that catches inexperienced investors in this sector: faster growth makes the cash problem worse, not better. Because every new rupee of revenue must be pre-funded for roughly a year before it converts to cash, a contractor growing revenue 40% or 50% is simultaneously sinking ever-larger sums into receivables, retention, and inventory. The profit-and-loss statement shows a booming, profitable company; the cash-flow statement shows money pouring out the door. This is why a growing EPC firm can post record profits and still need to raise equity — the growth itself is the cash drain. The mirage is not that the profits are fake; it is that profits and cash generation have decoupled, and only one of them pays the bills. An analyst who reads only the income statement of a fast-growing contractor is reading half the story, and the more flattering half.

This also reframes what "success" looks like for KCEIL year to year. A slower-growth year in which cash actually comes home can be healthier for the balance sheet than a blockbuster-growth year that has to be financed. It is a genuinely different mental model from the software or consumer businesses most investors cut their teeth on, where growth is nearly costless and cash-generative. In infrastructure, growth is expensive to carry, and the discipline that matters is not how fast you grow but whether you can fund the growth without permanently diluting owners or over-levering the balance sheet.

How does KCEIL survive this squeeze? Partly by playing the same game in reverse — stretching its own payable days to roughly 176, effectively passing a chunk of the financing strain down to its own suppliers and subcontractors.3 That narrows the net working-capital cycle to around 183 days, which is the difference between an uncomfortable business and an unviable one.3 But stretching payables has limits; lean too hard and suppliers demand cash upfront or walk. The residual gap has to be plugged with external capital — which is exactly why the recurring pattern in EPC of this type is thin or negative operating cash flow even in profitable years, and why the funding lifelines matter so much.

This structural cash hunger is also where the risk radar should point most sharply, because it defines KCEIL's single greatest vulnerability: refinancing and liquidity risk. A business utilizing its working-capital lines at around 91% has limited headroom, and its ability to keep growing depends on those lines being renewed and expanded on reasonable terms.3 In a benign credit environment, that is routine. But should interest rates spike, should banks tighten lending to the contracting sector after some unrelated blow-up, or should a large receivable from a state utility go unusually slow, the same leverage that funds growth becomes a squeeze. This is not a hypothetical unique to KCEIL — it is the failure mode that has ended countless infrastructure contractors, who did not go bankrupt because they were unprofitable but because they ran out of the short-term financing that bridges the gap between doing the work and getting paid. The company's improving credit metrics widen the margin of safety, but they do not eliminate the dependency; a leveraged working-capital model is only ever as safe as the credit taps that feed it.

Two lifelines stand out. The April 2025 QIP injected permanent equity into the cycle. And in February 2026, CRISIL reaffirmed KCEIL's rating at BBB-/Stable/A3 while noting that the rated bank facilities had been enhanced to ₹125 crore, more than double the ₹60 crore rated a year earlier.34 That expansion of bank lines — utilized at around 91% over the preceding year — is not a trophy; it is oxygen.3 It is the credit system extending KCEIL enough rope to keep pre-funding its growth. The rating trajectory itself tells a real story of improving creditworthiness: CRISIL had rated the company at the sub-investment-grade BB+/A4+ as recently as January 2025 before upgrading it into the BBB- investment-grade band, with gearing improving toward 0.45–0.5x and interest coverage strengthening past 5.7x.34 That is genuine balance-sheet progress. But the underlying truth is unchanged and structural: this is a business whose growth must be continuously financed, which means the bear case — periodic dilution — is not a bug someone can fix, it is the operating model. Keep that in view, because the very next chapter shows what happens when the machine hits a shock it did not budget for.

VII. The Middle East Shipment Delay: A Case Study in Execution Risk

Every growth story eventually meets the year the plan doesn't survive contact with reality. For KCEIL, that year was FY2026 — and the culprit came not from a Rajasthan tender room but from a shipping lane thousands of kilometres away.

Start with the headline numbers, because they are not a disaster — they are a disappointment, which is a more instructive thing. KCEIL reported FY2026 revenue of ₹165.59 crore, up only about 8% over FY2025's ₹152.72 crore, with EBITDA margin near 19.96% and profit after tax of ₹18.78 crore, an 11.34% net margin.5611 A profitable, high-margin year. But set it against expectations and the miss is stark. CRISIL, as late as February 2026, had modeled FY2026 revenue at roughly ₹230 crore.3 The company had entered the year with momentum that made even that look conservative: first-half FY2026 revenue had exploded to ₹83 crore from ₹38 crore a year earlier, a 119% jump.3 For revenue to finish at ₹165.59 crore, the second half had to shrink — H2 FY2026 came in around ₹81.57 crore, actually below the prior year's second half.5 Something broke in the back half of the year.

On the post-results commentary accompanying the FY2026 numbers, management's framing is itself a data point worth reading closely. Jain's stated emphasis — discipline over aggression, margin over top line — is the language of a team choosing to be judged on profitability rather than growth optics.5 That is a defensible posture, and the numbers corroborate it rather than contradict it: had management been chasing the guided top line, the honest expectation would be a visible margin sag as the company took on lower-quality billing to fill the gap, and no such sag appears — EBITDA margin actually held near its 20% high in the second half.56 When management's words and the margin line tell the same story, credibility rises; when they diverge, that is the tell. Here they aligned.

That something was the Emergency Restoration System (ERS). Picture a cyclone or flood that topples a high-voltage transmission tower and cuts power to a region. You cannot wait months to rebuild a permanent lattice tower. Instead, crews deploy an ERS — a lightweight, modular, quickly-erected temporary structure that bypasses the damaged section and restores power in days. It is a specialized, high-margin niche, and for KCEIL it was a meaningful chunk of FY2026's plan. The catch: critical ERS components were sourced through supply chains that ran through the Middle East. When geopolitical tensions and war-related maritime disruptions snarled shipping in the region, those components — worth an estimated ₹50–60 crore of revenue — got stuck in transit and could not be delivered and recognized within the fiscal year.57 Roughly 30% of the year's projected top line simply slid into the next period.

Now the part that actually matters for judging this management team: how did they handle it? The instructive contrast is with the promotional playbook, in which a miss gets buried under vague talk of "macro headwinds" and "challenging conditions." KCEIL did the opposite. Managing Director Lokendra Jain named the cause specifically — delays in ERS shipments "arising from the escalation of geopolitical tensions and war-related disruptions in the Middle East" — and quantified the deferred revenue rather than obscuring it.56 More tellingly, management framed the choice as deliberate: it "remained focused on maintaining operational discipline, protecting margins, and ensuring prudent project execution rather than pursuing aggressive revenue growth at the cost of profitability."5 The evidence backs the claim — margins held near 20% through the miss, exactly what you would expect if the company refused to chase low-margin billing to paper over the top-line gap.

There is a harder question underneath the ERS story, and an independent analyst has to ask it: was the FY2026 shortfall entirely a shipping problem, or was the original target simply too ambitious? Recall the expectations gap. CRISIL modeled roughly ₹230 crore of FY2026 revenue, and internal aspirations ran higher still, yet the company landed at ₹165.59 crore.35 The deferred ERS shipments account for an estimated ₹50–60 crore of that gap — meaningful, but not the whole distance between aspiration and outcome.57 The most probable reading is that FY2026 combined a genuine external shock with a starting target that had been set during the euphoria of a 119%-growth first half. Both things can be true: the shipping delay was real and well-explained, and the guidance was optimistic. For an investor, the lesson is to discount forward-looking targets from a management riding a hot first half, and to weight the audited full-year result over the mid-year run-rate.

An independent analyst should still give real credit here for candour and margin discipline — and keep both eyes open. Specific, quantified explanations are a genuine marker of management credibility, far better than blame-shifting; a promotional team would have folded the miss into vague "industry headwinds." But candour about a miss is not the same as not missing. The revenue is deferred, not lost — provided those shipments actually arrive and get executed in FY2027. If they slip again, "deferred" quietly becomes "impaired," and a one-year timing story becomes a two-year credibility problem. The right posture is to bank the honesty, then watch FY2027 for the catch-up revenue to actually show up, and to test whether management's future targets are calibrated to audited reality or to peak-momentum optimism. Execution risk, it turns out, is the tax you pay for a global supply chain feeding a local order book — and it is a useful reminder as we turn to KCEIL's plan to control more of that chain itself.

VIII. Future Optionality: Backward Integration & Adjacent Segments

If the ERS delay taught KCEIL anything, it was the cost of depending on suppliers you don't control — and the company's most consequential strategic bet is a direct answer to that lesson. In Kota, KCEIL has been building a manufacturing facility to make in-house the very components it currently buys from third parties.

The strategic logic is a natural extension of the asset-heavy philosophy already discussed: if owning your cranes and tensioners buys control, owning your component supply buys more of it. The planned product portfolio runs up the technical ladder — connectors rated to 765 kV, substation hardware, bird-flight diverters, transmission structures, and electrical control panels.10 The implications, if it works, are threefold. KCEIL would capture the supplier's margin that currently leaks out of every project; it would compress lead times and reduce its exposure to exactly the kind of shipping shock that just cost it a strong FY2026; and it would open an entirely new revenue line — selling components business-to-business to other EPC contractors and utilities, turning a pure-play service contractor into an integrated manufacturer.

That is the bull framing, and it is coherent. The independent framing is more cautious. Backward integration is one of the most seductive strategies in industrials and one of the most frequently disappointing. It converts a variable cost into a fixed asset that must be kept utilized; it demands manufacturing skills distinct from project-execution skills; and it can tip into "diworsification" if the plant ends up subscale or if selling to competitors proves harder than selling to yourself. The margin-capture math is real, but so is the execution risk, and the facility's contribution should be treated as unproven optionality until the plant is commissioned and its output shows up in the numbers — not as a margin uplift to underwrite today.

Alongside the Kota plant sit two diversification vectors aimed squarely at KCEIL's concentration problem. The first is Solar EPC — a logical adjacency given the company already builds the transmission infrastructure that solar parks depend on, and reflected in its consolidation of a renewable-energy joint venture, Suryavayu Renewable and Energy Solutions Private Limited.3 The second is Railway Electrification — undertaking EHV cabling and transmission-line crossings for Indian Railways, a customer whose budget cycle is set in New Delhi rather than Jaipur, and therefore a genuine diversifier away from state DISCOM dependence. Both are sensible on paper. Both are also, for now, aspirations rather than track records; the honest label is optionality, not yet a second engine.

The diversification logic deserves a skeptic's scrutiny, because "adjacent" is one of the most abused words in strategy. Solar EPC sounds close to transmission EPC, but it is a distinct, ferociously price-competitive business with its own crowded field of established players; being good at building substations does not automatically make you cost-competitive at bolting down solar modules. Railway electrification is closer to KCEIL's core skill set — it is still high-voltage, structure-heavy work — but it means competing for a new customer's tenders against incumbents who already hold Indian Railways pre-qualifications. In both cases KCEIL would start again near the bottom of a fresh pre-qualification ladder, which is precisely the slow, capital-hungry climb it spent a decade completing in Rajasthan transmission. Diversification reduces concentration risk, but it does so by trading a hard-won position of local strength for a beginner's position in an adjacent market. That can be the right trade — concentration is a genuine vulnerability — but it is not a free one, and the returns will lag the rhetoric. Whether any of these bets pays off will be decided by execution — which is the natural pivot to what the last twelve years actually teach us.

IX. Playbook: Business & Investing Lessons

Step back from the quarter-to-quarter and three broader lessons emerge from the KCEIL story — the kind of transferable pattern-recognition that outlives any single company.

The "control premium" of the asset-heavy model. Conventional finance worships capital efficiency: rent, don't buy; subcontract, don't own; keep the balance sheet light and the returns on capital high. KCEIL is a live counter-example in a specific context. In a highly regulated, high-penalty utility sector, where missing a milestone triggers liquidated damages and where a scarce crane can idle an entire project, owning the critical path can be worth more than the capital it ties up. Control over quality and time becomes the ultimate margin protector — and KCEIL's high-teens-to-20% operating margins, well above what asset-light micro-peers typically manage, are the evidence.35 The lesson is not "asset-heavy always wins"; it is that capital efficiency and operational control are a genuine trade-off, and the right side of it depends on how brutally your industry punishes lost time.

The SME-exchange life cycle. Platforms like NSE Emerge are a remarkable innovation — cheap equity fuel for companies too small for the main board. But they are a launchpad, not a destination. The micro-cap contractor space has a high mortality rate; the ones that survive are those that use the SME listing to institutionalize fast — raising follow-on capital through instruments like a QIP, pulling institutional investors onto the register, tightening disclosure, and ultimately migrating toward the main board. KCEIL's arc from a ₹16 crore SME IPO to a ₹25 crore institutional placement in fifteen months is a near-textbook execution of this transition.17 The listing was not the achievement; the use of the listing was.

The regional-dominance trap. Specializing in one grid corridor is what made KCEIL efficient — faster mobilization, denser relationships, real regulatory leverage inside Rajasthan. It is also what makes it fragile. The same concentration that produces the margins produces the single-point-of-failure risk: a state budget freeze, a political shift, or a delayed DISCOM payment cycle can stall the whole company at once. There is no diversified portfolio to cushion the blow. Regional dominance and regional dependence are the same coin; you cannot own one side without the other. The Solar EPC and railway pushes are, at their core, an attempt to buy back some of that lost optionality — and their success or failure is one of the most important things to watch.

A fourth lesson runs underneath the other three: in government-dependent infrastructure, the balance sheet is the strategy. A contractor's ability to win and hold larger work is gated not only by its technical pre-qualifications but by its financial ones — utilities screen bidders for solvency, net worth, and the capacity to post bank guarantees and absorb long payment cycles. This creates a compounding advantage for the contractor who can access capital: a stronger balance sheet qualifies you for bigger tenders, which generate the profits and the credit history that further strengthen the balance sheet. KCEIL's climb up the CRISIL rating ladder, from sub-investment-grade to the BBB- band, and its enhanced bank lines are not merely financial housekeeping — they are competitive weapons that widen the set of tenders it can credibly pursue.34 In this industry, cheap and reliable access to capital is itself a moat-adjacent advantage, and it is one of the more durable things KCEIL has built.

These lessons set up the final question every investor actually cares about: from here, does KCEIL win, and what would break the case? Time to war-game it.

X. Analysis: Hamilton Helmer's 7 Powers & Bull vs. Bear Case

Let's put KCEIL on the analytical dissecting table, using two frameworks that cut through narrative to structure.

Hamilton Helmer's 7 Powers. The exercise here is to ask which durable advantages KCEIL actually possesses, versus which it merely aspires to.

The strongest by far is Cornered Resource — but with an asterisk. Lokendra Jain's three decades of hands-on EHV experience and his personal, relationship-dense network inside Rajasthan's power bureaucracy is a genuinely scarce asset that competitors cannot quickly replicate.3 The asterisk is that this resource is embodied in a person and a promoter family, which makes it a key-man risk as much as a moat; a cornered resource that walks out the door is a fragile one.

Scale Economies are weak nationally but real locally. KCEIL will never out-scale L&T or KEC. But inside Rajasthan, owning a machinery fleet stationed in Kota lets it mobilize to a rural project faster and cheaper than a national player parachuting equipment across the country. It is a local density advantage, not a global scale one — meaningful within the corridor, invisible outside it.

Switching Costs are low, and this is the uncomfortable truth the bull case must swallow. Utility tenders are typically awarded to the lowest eligible bidder; the client has little loyalty and every incentive to shop on price. What partially substitutes for switching costs is the pre-qualification barrier at the 400 kV and 765 kV level — a practical filter that keeps the smallest entrants out of the highest-margin work. That is a barrier to entry, not a switching cost, and the distinction matters: it protects the category KCEIL competes in, not KCEIL's specific position within it.

The remaining powers — Network Economies, Branding, Counter-Positioning, Process Power, Cornered supply beyond the founder — are essentially absent. This is, stripped of romance, a competitive, tender-driven contracting business. Acknowledging that is the beginning of honest analysis, not the end of the investment case.

Porter's Five Forces sharpens the same picture. Bargaining power of buyers is very high — state utilities dictate payment terms, milestones, and the retention conditions that create the working-capital trap. Rivalry is intense, fought against regional SME peers such as Viviana Power Tech and others, and against large-cap giants on the bigger packages.[^15] Threat of new entrants is low-to-moderate, held down by the technical pre-qualification gates. Supplier power just demonstrated itself vividly in the ERS delay — which is precisely the force the Kota plant is meant to neutralize. Threat of substitutes is low; there is no alternative to physically building the grid. Net picture: a business with a defensible niche but structurally weak pricing power, at the mercy of powerful buyers and its own cash cycle.

The peer comparison is worth making explicit, because it locates KCEIL on the industry map. At the top sit the national heavyweights — KEC International, Kalpataru, L&T's transmission arm — firms with multi-billion-rupee order books, international footprints, and the balance sheets to absorb working-capital swings that would sink a micro-cap.12 Their trade-off is that scale and diversification come with the diluted margins of a business that competes everywhere against everyone; a KEC operates in the high-single-digit-to-low-double-digit EBITDA range, structurally below KCEIL's high teens.12 At KCEIL's own weight class sit the SME-listed specialists — Viviana Power Tech and similar names — competing for regional packages with comparable asset intensity and comparable concentration risks.[^15] KCEIL's distinctiveness within that peer set is the combination of unusually high margins, a fast-improving credit profile, and a promoter with genuine 765 kV-class credentials. What it emphatically is not is a category-defining moat business; it is a well-run specialist in a fragmented, competitive trade, and it should be valued as such rather than as the next national champion.

There is a myth-versus-reality worth puncturing here. The bullish retail narrative frames KCEIL as a "multibagger EPC play riding India's power capex" — as though the sector tailwind alone guarantees compounding returns. The reality is more sober: the tailwind is real and durable, but it lifts the entire crowded field, not KCEIL uniquely. A rising grid-capex tide floats every eligible bidder, and in a lowest-price tender market, an industry-wide boom can compress margins even as volumes rise, because more capacity chases the same tenders. The macro tailwind is necessary for the bull case but nowhere near sufficient; what has to carry the case is company-specific execution — margin defense, cash discipline, and the voltage-ladder position — not the sector story that any promoter in the space can recite.

The three KPIs that actually matter. Ignore the noise and track these: 1. Order book-to-bill ratio. Above roughly 2.5–3x sustains the high-growth expectation; a slide signals the runway shortening.3 2. Gross Current Asset (GCA) days. The tell for whether growth is being funded by real cash or by permanently locking capital into receivables and retention. Watch whether it holds near 350 or drifts back toward the 439-day extreme of FY2024.34 3. Core EBITDA margin. The single number that will reveal whether the asset-heavy model and the Kota backward-integration bet are expanding profitability toward and beyond 20%, or whether tender competition is grinding it down.5

The bull case. India is in the early innings of a multi-decade grid modernization to connect renewable energy, and Rajasthan is the epicenter. KCEIL is a profitable, promoter-led, increasingly credit-worthy vehicle sitting at that geographic heart, with a three-year order book, industry-leading margins, an improving balance sheet, and genuine optionality in backward integration and adjacent segments. If even part of the diversification works, a regional contractor becomes a broader grid-infrastructure platform.

The bear case. This is a working-capital sponge that structurally consumes cash and therefore requires periodic equity dilution — the QIP is not a one-off but a preview. Its margins, while high, are not fortified against relentless tender competition, and CRISIL itself flags their sustainability as monitorable.3 Its revenue is dangerously concentrated in one state and a handful of government-linked clients, leaving it exposed to any fiscal wobble in Rajasthan. And the FY2026 miss showed how a single external shock can vaporize a third of a year's revenue. An activist skeptic would press hardest on three things: the recurring need to raise capital to fund growth (is return-on-equity real once you account for the dilution?), the key-man dependence on a promoter family, and the opacity of the order book's margin composition. None of these is disqualifying; all of them are unresolved.

The honest synthesis is that KCEIL's edge is real but narrow, cyclical, and partly unproven — a good operator riding a powerful tailwind, not a fortress. Whether it wins from here depends less on the macro (the grid build-out is close to certain) and more on execution: converting deferred revenue, funding growth without value-destructive dilution, and proving that the manufacturing and diversification bets are expansion rather than distraction.

XI. Outro & Epilogue

Strip this story to its spine and it is really about two transformations happening at once. The first is operational: a diploma engineer's field expertise, compounded over three decades and hardwired into one state's grid, scaling from 132 kV contracts to 765 kV substations on the back of an unfashionable, control-obsessed, asset-heavy model. The second is financial: a family-run private contractor becoming an institutionally-backed public company — through a frenzied SME IPO that priced on scarcity rather than fundamentals, and a shrewd QIP that turned an inflated stock into permanent working capital.

The two transformations are not fully reconciled, and that is the honest place to end. The operating business is genuinely good — high margins, a real niche, a strong tailwind, improving credit. The financial reality is genuinely demanding — a cash-hungry cycle that must be continuously fed, a concentration risk that no order book can hedge, and a valuation history driven as much by micro-cap mania as by discounted cash flows.

The larger lesson is about the macro-reality of infrastructure investing in emerging markets. Building the physical backbone of a developing economy is a business of thin cash flows, patient capital, powerful government buyers, and long feedback loops — where a strong order book and a real profit margin can still coexist with negative operating cash flow and periodic dilution. KCEIL is a clean, small-scale specimen of that entire pattern.

It is also a reminder that a good business and a good stock are different questions, held apart most sharply in micro-caps. The operating company can be genuinely well-run — as the margins, the credit-rating trajectory, and the disciplined capital allocation suggest KCEIL's is — while the shares carry all the volatility, thin liquidity, and mispricing risk that a 1,052-times-subscribed SME listing implies. The two frenzies that opened this story, the operational climb up the voltage ladder and the speculative climb of the share price, will not always move together, and an investor's job is to keep them mentally separate: to judge the business on its order book, its cash conversion, and its margins, and to judge the price on its own terms.

Whether KCEIL graduates from a regional contractor into a durable grid-infrastructure platform will be written not in press releases but in three unglamorous numbers — its order book, its GCA days, and its core margin — quarter after quarter, as the Rajasthan sun keeps generating power that someone has to carry to the grid.

References

-

Kay Cee Energy & Infra IPO Subscribed 1,061 Times on Final Day — Business Standard, 2024-01-02 ↩↩↩

-

Kay Cee Energy & Infra SME IPO Listing: Shares Debut at Massive Premium — Moneycontrol, 2024-01-05 ↩↩

-

Kay Cee Energy & Infra Limited — Rating Rationale (Crisil BBB-/Stable/A3) — CRISIL Ratings, 2026-02-06 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Kay Cee Energy & Infra Limited — Rating Rationale (Crisil BB+/Stable/A4+) — CRISIL Ratings, 2025-01-17 ↩↩↩↩↩↩↩

-

Kay Cee Energy & Infra Limited Announces H2 & FY26 Results — The Tribune, 2026-05-16 ↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Kay Cee Energy & Infra Limited Announces H2 & FY26 Results — Webindia123, 2026-05-16 ↩↩↩

-

Kay Cee Energy & Infra Raises Rs 2,500 Lakhs in QIP, Allots Shares — Entrepreneur India, 2025-04-25 ↩↩↩↩↩

-

Kay Cee Energy & Infra Limited Raises Rs 2,502.72 Lakhs via QIP — Business Standard, 2025-04-25 ↩

-

Kay Cee Energy & Infra Ltd — Financial Metrics and Overview — Screener.in ↩

-

Kay Cee Energy Reports Resilient Financial Results Amid Industry Challenges — Devdiscourse, 2026-05-16 ↩

-

KEC International Limited — Financial Metrics (Peer Benchmark) — Screener.in ↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube