Kansai Nerolac: The Century-Old Paint Company That Japan Transformed

Introduction & Episode Roadmap

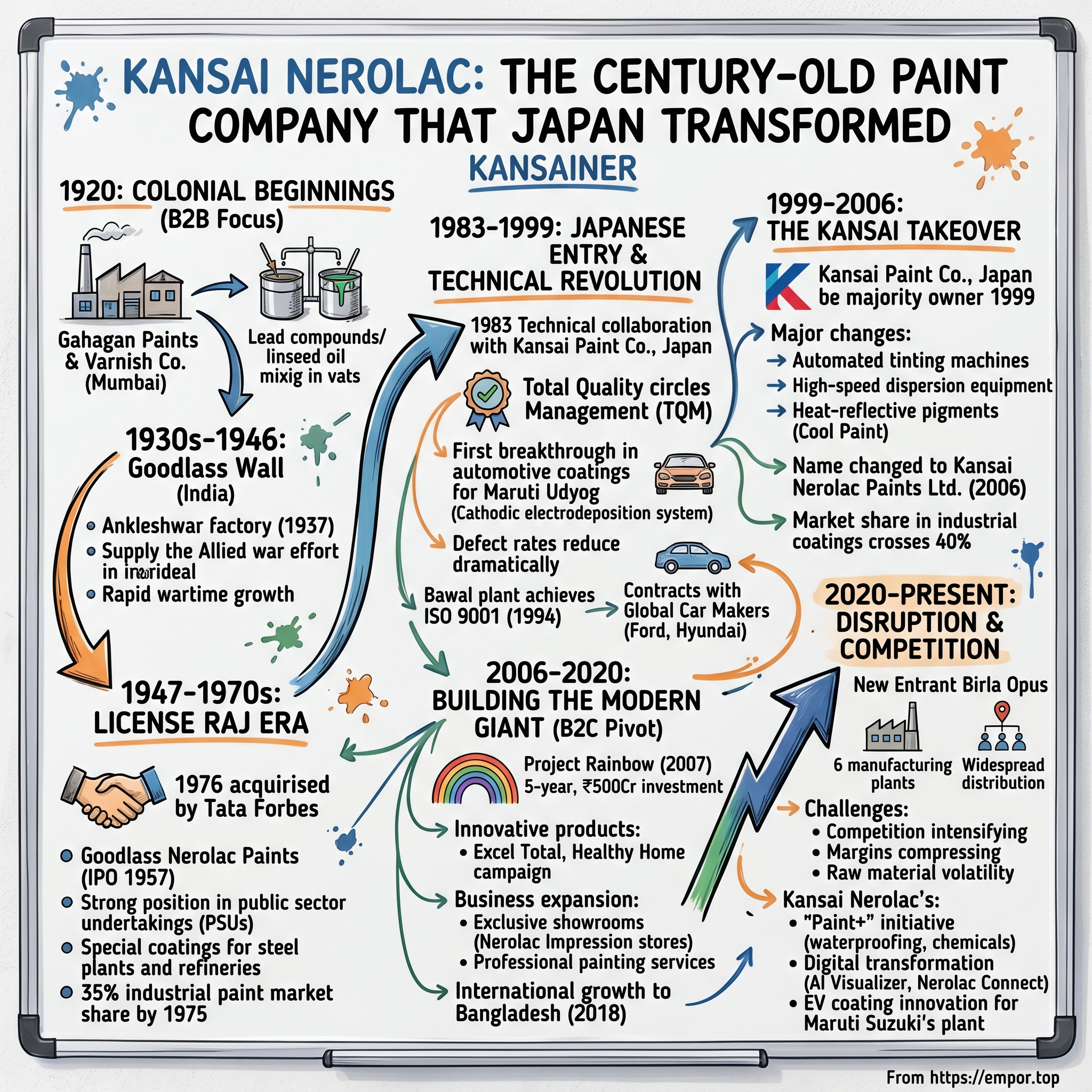

Picture this: In a nondescript industrial building in Mumbai's Lower Parel district in 1920, British chemists mixed lead compounds and linseed oil in large vats, creating India's first industrial paints. A century later, that same company—now called Kansai Nerolac—commands over 40% of India's industrial coatings market and operates state-of-the-art factories powered by Japanese precision manufacturing. The transformation between these two snapshots tells one of Indian business's most fascinating cross-cultural success stories.

Kansai Nerolac today stands as India's second-largest paint company, with a market capitalization of ₹18,868 crores and annual revenues exceeding ₹7,800 crores. Yet unlike its larger rival Asian Paints, which built its empire on decorative paints for homes, Nerolac took the industrial route—coating everything from Maruti cars to Mumbai's metro trains. The company is 75% owned by Japan's Kansai Paint Co., making it one of the most successful Japanese acquisitions in India.

The question that drives our story: How did a colonial-era paint manufacturer, passed between British conglomerates like a trading card, transform into Japan's most strategic asset in India's $8 billion paint market? The answer involves patient capital, technology transfer, cultural fusion, and a bet that India's infrastructure boom would create more value than painting its walls.

This is a tale of three distinct eras: the colonial foundations that created India's paint industry infrastructure, the Japanese entry that revolutionized quality and manufacturing, and the modern battle for market share in one of the world's fastest-growing paint markets. Along the way, we'll uncover how Japanese management philosophy collided with Indian market dynamics, why industrial coatings create stronger moats than decorative paints, and what happens when a century-old company faces disruption from deep-pocketed new entrants.

The story of Kansai Nerolac isn't just about paint—it's about how foreign capital and technology can transform local champions, how B2B businesses build lasting competitive advantages, and why sometimes the less glamorous path proves more defensible. As we'll see, while competitors fought for retail shelf space, Nerolac quietly locked up India's factories, creating switching costs that even the deepest pockets struggle to overcome.

The Colonial Beginning & Early Years (1920–1970s)

The year was 1920, and India was still the jewel in the British crown. In Lower Parel—then Mumbai's industrial heartland, now its startup hub—an Irishman named Gahagan established Gahagan Paints & Varnish Co. Ltd. The timing was no accident. Post-World War I, British industrialists were establishing manufacturing outposts across the empire, and paint was essential infrastructure for the colonial project—protecting ships from rust, railway carriages from monsoons, and government buildings from tropical decay.

Gahagan wasn't creating artisanal colors for maharajas' palaces. This was industrial chemistry at its most practical: lead-based primers that could withstand salt air at Bombay port, varnishes that protected teak furniture from termites, and the thick black paint that coated the expanding railway network. The company's early ledgers, preserved in corporate archives, show orders from the Bombay Port Trust, the Great Indian Peninsula Railway, and various textile mills sprouting across the city.

But Gahagan Paints was too small to survive the consolidation wave of the 1930s. The global depression had hammered commodity prices, and smaller manufacturers across the British Empire were being rolled up by larger conglomerates. In 1933, Lead Industries Group—itself a creation of British industrial consolidation—acquired Gahagan and merged it with Goodlass Wall, another British paint manufacturer operating in India. The combined entity became Goodlass Wall (India) Ltd., instantly creating one of India's largest paint companies.

The Goodlass Wall era (1933-1946) coincided with massive infrastructure development as India prepared for World War II. The company's Ankleshwar factory, established in 1937, became a critical supplier to the Allied war effort, producing specialized coatings for military vehicles, aircraft, and naval vessels. Revenue grew from ₹12 lakhs in 1933 to over ₹2 crores by 1945—a staggering 17-fold increase driven by wartime demand.

Independence in 1947 created both opportunity and crisis. The opportunity: a new nation embarking on ambitious industrialization under Nehru's five-year plans. The crisis: British managers fleeing overnight, capital controls limiting access to foreign technology, and the messy partition disrupting supply chains. Goodlass Wall navigated this transition better than most British companies, partly because it had already begun Indianizing management in the early 1940s.

The 1950s brought a critical strategic decision. Rather than focus on the nascent decorative segment where local players like Asian Paints were emerging, Goodlass Wall doubled down on industrial coatings. The logic was compelling: India's new public sector undertakings—steel plants, refineries, power stations—needed sophisticated protective coatings that required technical expertise. The company developed specialized products for Tata Steel's expansion, paints that could withstand 500°C temperatures for Bhilai Steel Plant, and anti-corrosive coatings for India's growing chemical industry.

In 1957, seeking capital for expansion and responding to government pressure for local ownership, the company went public as Goodlass Nerolac Paints Ltd. The "Nerolac" brand, introduced in the 1950s, was a stroke of marketing genius—easy to pronounce across India's linguistic diversity and distinctive enough to trademark globally. The IPO was oversubscribed 3.2 times, with notable early investors including the Tata Trusts and several Parsi industrialist families who recognized the infrastructure play.

The 1960s and early 1970s operated under the License Raj—that peculiar Indian system where government permits determined everything from production capacity to product pricing. While frustrating for entrepreneurs, it created massive moats for established players. Goodlass Nerolac held licenses for 15,000 tons of paint production annually, and getting new licenses required years of lobbying. The company used this protected period wisely, establishing manufacturing facilities in Bawal (Haryana) and Nashik (Maharashtra), creating a pan-India production network before liberalization would later unleash competition.

By 1975, Goodlass Nerolac had captured 35% of India's industrial paint market and 18% of the overall paint market. But the foreign ownership structure—still 40% held by British entities—was becoming politically untenable in Indira Gandhi's socialist India. The Foreign Exchange Regulation Act (FERA) of 1973 mandated that foreign companies reduce their stakes to 40% or face nationalization. Lead Industries Group needed an Indian buyer, fast.

Enter the Tatas. In 1976, Tata Forbes Ltd.—a joint venture between Tata Sons and Forbes Campbell (another British firm with Tata connections)—acquired the controlling stake in Goodlass Nerolac. The price: ₹4.2 crores for 51% of a company with revenues of ₹45 crores. Even adjusted for inflation, this would prove to be one of the Tata Group's most valuable acquisitions, though they wouldn't hold it long enough to realize the full gains.

The Tata era (1976-1983) was marked by steady if unspectacular growth. The company maintained its industrial focus, expanded distribution to 3,000 dealers, and began early experiments with water-based paints—prescient given future environmental regulations. But the Tatas, spread across dozens of companies, never gave Goodlass Nerolac the focused attention it needed to break out from second place. That would require a different kind of owner—one with deep technical expertise in paints and the patience to build for decades. The stage was set for the Japanese to enter.

The Japanese Entry & Technical Revolution (1983–1999)

The letter that changed everything arrived at Bombay House in early 1983. Kansai Paint Company of Japan, through diplomatic channels and Mitsui trading house, was proposing a technical collaboration with Goodlass Nerolac. The Japanese had been studying India's paint market for three years, sending teams to analyze consumption patterns, raw material availability, and competitive dynamics. Their conclusion: India would become one of the world's largest paint markets, but it needed technology to unlock quality improvements.

Kansai Paint wasn't randomly fishing for partners. Founded in 1918 by Katsujiro Iwai, the Osaka-based company had built Japan's largest paint business through relentless focus on R&D and quality. By 1983, Kansai held 30% of Japan's paint market and was expanding across Asia. But India presented unique challenges—import restrictions meant they couldn't simply export from Japan, and foreign investment rules limited direct ownership. Technical collaboration was the only way in.

The Tata leadership, particularly Darbari Seth who headed Tata Chemicals and oversaw Forbes Campbell ventures, immediately grasped the opportunity. Japanese manufacturing techniques were revolutionizing industries globally, and paint manufacturing—with its complex chemistry and quality control requirements—was ripe for technological upgrading. The collaboration agreement, signed in November 1983, gave Goodlass Nerolac access to Kansai's formulations, manufacturing processes, and quality systems in exchange for royalties and an option for future equity investment.

The technology transfer began with five Kansai engineers arriving at the Ankleshwar plant in early 1984. Workers still remember the culture shock—Japanese engineers who arrived at 6 AM, measured everything three times, and insisted on daily quality circles where workers discussed problems. One veteran employee recalled: "They would spend hours perfecting the dispersion of pigments, something we'd never paid attention to. They showed us that paint isn't just mixing colors—it's materials science."

The first breakthrough came in automotive coatings. Maruti Udyog, the Indo-Japanese joint venture launching India's car revolution, demanded paint quality matching Japanese standards. Goodlass Nerolac, armed with Kansai technology, developed a cathodic electrodeposition system that reduced defects by 78% and became Maruti's sole paint supplier for primer coats. This single contract, worth ₹15 crores annually by 1986, validated the Japanese collaboration.

But technology was only part of the revolution. Kansai introduced Total Quality Management (TQM) across Nerolac's operations—a philosophy that seemed almost religious in its devotion to continuous improvement. Every worker maintained a "quality notebook" documenting problems and solutions. Defect rates, previously accepted at 3-5%, were driven below 0.5%. The Bawal plant achieved ISO 9001 certification in 1994, among the first paint facilities in India to do so.

The collaboration also transformed R&D. Kansai helped establish an Application Technology Centre in Mumbai in 1987, equipped with Japanese testing equipment that could simulate 20 years of weather exposure in six months. Indian chemists were sent to Osaka for training, returning with expertise in polymer chemistry and nanotechnology applications. By 1990, Goodlass Nerolac was filing 12 patents annually, up from virtually zero a decade earlier.

The results spoke through financial performance. Between 1983 and 1991, revenue grew from ₹72 crores to ₹340 crores—a compound annual growth rate of 21.4%. More importantly, EBITDA margins expanded from 8% to 14% as quality improvements reduced waste and allowed premium pricing. The company's industrial coatings, now matching international standards, commanded 10-15% price premiums over local competitors.

The 1991 liberalization of India's economy accelerated everything. Suddenly, foreign car manufacturers—Ford, Hyundai, Honda—were setting up Indian operations, and they wanted paint suppliers meeting global standards. Goodlass Nerolac, with eight years of Japanese technology absorption, was perfectly positioned. The company won contracts for Honda's motorcycle plant, Hyundai's Chennai facility, and the Delhi Metro Rail project—all requiring specialized coatings that competitors couldn't match.

Kansai, watching this success, wanted more than royalties. In 1994, they proposed converting their technical collaboration into equity ownership. The timing was fortuitous—Tata Sons was rationalizing its portfolio under Ratan Tata's leadership, focusing on core businesses. Paint, despite Goodlass Nerolac's success, wasn't considered strategic to the group's future.

The negotiation took four years. Kansai wanted management control but Indian regulations still restricted foreign ownership. Tata Forbes wanted a premium valuation recognizing the brand value and market position built over decades. Investment bankers from both sides created complex structures involving preferential shares, board composition agreements, and technology transfer valuations.

The cultural dynamics were equally complex. Kansai executives, accustomed to Japanese consensus-building, found Indian board meetings chaotic with their animated debates. Indian managers worried about job security under Japanese ownership. A senior executive from that era noted: "We spent as much time on cultural integration workshops as on financial due diligence."

By 1998, the framework was agreed. Kansai would acquire Tata Forbes' entire stake through a series of tranches, eventually gaining management control. The technology collaboration had proven that Japanese and Indian business cultures could create value together. But owning and running an Indian company would require a different level of commitment—one that would transform both Kansai and Nerolac in unexpected ways.

The Kansai Takeover: Paint Industry Transformation (1999-2006)

The millennium arrived with seismic shifts in India's corporate landscape. Software companies were minting millionaires, telecom was exploding, and old economy stocks were suddenly unfashionable. Yet in this environment, Kansai Paint Co. Ltd., Japan took over the entire stake of Tata Forbes group in 1999 and thus Goodlass Nerolac Paints became wholly owned subsidiary of Kansai Paint Company Ltd. The transformation from technical partner to full owner would prove more complex—and ultimately more successful—than anyone anticipated.

The trigger for the sale was classic Tata Group portfolio rationalization. Ratan Tata, who'd taken over as chairman in 1991, was ruthlessly focusing the conglomerate on core businesses—steel, automobiles, hospitality, and the emerging IT services. Paint, despite Goodlass Nerolac's strong performance, didn't fit the strategic vision. Meanwhile, Kansai Paint's board in Osaka saw India differently: not as a peripheral market but as the future center of Asian growth outside Japan and China.

The negotiations stretched through 1998-99, complicated by valuation gaps and regulatory hurdles. Tata Forbes valued Goodlass Nerolac at ₹850 crores based on future cash flows and brand value. Kansai's initial offer was ₹620 crores, reflecting the company's historical earnings. The final deal, completed in stages to navigate foreign investment regulations, valued the company at approximately ₹750 crores. For context, Asian Paints' market cap then was around ₹2,000 crores—making this one of India's largest paint sector transactions.

In February 2000, Kansai Paint Co. Ltd., Japan acquired 43,71,152 shares amounting to 28.56% of the paid-up share capital of the company from Forbes Gokak Ltd. and their associates at a price of Rs.250 per share. With this acquisition Kansai Paint Co., Japan, was now holding 64.52% of the paid up share capital of the company. The staggered acquisition structure was designed to comply with takeover regulations while giving Kansai immediate management control.

The first hundred days under Japanese ownership revealed cultural fault lines. Kansai's new managing director, Hiroshi Nakamura, instituted 7 AM management meetings—standard in Japan, shocking in Mumbai's traffic-challenged geography. Decision-making slowed as every major expense required approval from Osaka, often with documents translated into Japanese. Indian managers, accustomed to Tata's decentralized style, chafed at the new reporting requirements.

But Nakamura brought something invaluable: a ten-year vision when most Indian companies planned quarter to quarter. In his first town hall, speaking through a translator, he declared: "We're not here to extract profits for Japan. We're here to build India's finest paint company. That means investing when others retreat, developing products for Indian conditions, and thinking in decades, not years."

The technology infusion accelerated dramatically. Kansai invested ₹120 crores in the first two years—more than Goodlass Nerolac's total capital expenditure in the previous five years. The Ankleshwar plant received automated tinting machines that could produce 10,000 color variants with perfect reproducibility. The Bawal facility got high-speed dispersion equipment that reduced batch times by 60%. Most critically, Kansai established a ₹25 crore R&D center in Mumbai, staffed with PhD chemists working on India-specific challenges like paints that could withstand 45°C heat and 95% humidity.

The product innovations were remarkable. Kansai's Japanese labs had developed heat-reflective pigments for Tokyo's urban heat island problem. Indian engineers adapted this technology for local conditions, creating exterior paints that reduced surface temperatures by 5-7°C—massive energy savings for Indian buildings without air conditioning. Another breakthrough: anti-fungal formulations that prevented the black mold plaguing Mumbai's buildings during monsoons, a problem Japanese technology solved through silver ion technology originally developed for hospitals.

The automotive business transformation was even more dramatic. As global car manufacturers entered India—Honda in 2000, Toyota in 2001, Renault-Nissan in 2005—they demanded world-class paint quality. Kansai Nerolac, leveraging its parent's relationships with these companies in Japan, became the preferred supplier. The company developed a "tropical specification" paint system that prevented rust despite India's varied climate—from Rajasthan's dry heat to Kerala's salt air. By 2003, Kansai Nerolac supplied 65% of all automotive OEM paint in India, up from 40% in 1999.

Yet the most profound change was in organizational culture. Kansai introduced the concept of "gemba"—going to the actual place where work happens. Japanese executives spent weeks on factory floors, in dealer shops, at construction sites, understanding ground realities. They discovered that Indian painters diluted paint more than recommended to increase coverage, so they reformulated products to maintain quality even with 20% extra dilution. They learned that Indian consumers touched painted walls to test dryness, so they developed faster-drying formulations.

The dealer transformation was equally systematic. Kansai created "Nerolac Pragati"—a dealer development program providing business training, inventory management systems, and credit facilities. The company invested in 200 exclusive showrooms, designed by Japanese retail experts, that displayed paint not just as color swatches but as lifestyle solutions. Dealers received handheld devices for instant order placement, revolutionary in an industry still using paper order books.

Financial performance validated the strategy. Revenue grew from ₹456 crores in 1999 to ₹1,250 crores in 2005—a CAGR of 18.3%. More impressively, ROCE improved from 16% to 24% as operational efficiency gains kicked in. The company maintained EBITDA margins above 13% despite raw material cost increases, while competitors struggled to maintain double digits. Market share in industrial paints crossed 40%, establishing clear leadership.

The 2004 decision to rebrand from Goodlass Nerolac to Kansai Nerolac sparked internal debate. Indian executives worried about losing eight decades of brand equity. Japanese board members saw it as essential for global alignment. The compromise solution was brilliant: retain "Nerolac" as the consumer-facing brand while adding "Kansai" for corporate identity. On 11 July 2006, Goodlass Paint Ltd. name was changed to Kansai Nerolac Paints Ltd.

The integration succeeded because Kansai understood something crucial: they weren't colonizing an Indian company but creating an Indo-Japanese hybrid. They retained Indian managers who understood local markets while bringing Japanese processes that ensured quality. They invested in relationships—Nakamura learned Hindi, attended Indian festivals, and his successor even performed in the company's Diwali celebrations. This cultural fusion became Kansai Nerolac's secret weapon—Japanese quality with Indian market intuition.

Building the Modern Paint Giant (2006–2020)

The rechristened Kansai Nerolac faced a defining question in 2006: remain the undisputed king of industrial coatings or challenge Asian Paints in the larger, more lucrative decorative segment? The answer would shape the next fifteen years and determine whether a B2B champion could successfully pivot to B2C without losing its core strength.

The industrial dominance was undeniable. Kansai Nerolac today is the second largest paint coatings company in India and a market leader in Industrial Coatings with over 40% market share. Walk through any Indian automotive plant—Maruti's Gurgaon facility, Tata Motors' Pune complex, Royal Enfield's Chennai factory—and you'd find Kansai Nerolac's electrodeposition tanks, primer booths, and clear coat lines. The company had become so embedded in manufacturing processes that switching costs for OEMs were prohibitive. One automotive executive noted: "Changing paint suppliers means revalidating entire production lines, retraining workers, risking quality consistency. Unless there's a 30% cost difference, nobody switches."

The moat in industrial coatings went beyond switching costs. Kansai Nerolac's Application Technology Centers, expanded to five locations by 2008, functioned as innovation partners for manufacturers. When Mahindra needed tractors to withstand Punjabi fields' harsh conditions, Nerolac's engineers developed UV-resistant coatings that prevented color fading for seven years. When Indian Railways required fire-retardant paints for coach interiors, the company created formulations meeting European safety standards. These weren't vendor relationships but technical partnerships spanning decades.

Yet the decorative segment beckoned with its promise of higher margins and brand visibility. Asian Paints dominated with 50% market share, but the market was growing at 15% annually as India's middle class expanded. In 2007, Kansai Nerolac launched "Project Rainbow"—a five-year, ₹500 crore investment to capture decorative market share. The strategy was differentiation through technology rather than price competition.

The first breakthrough product was Excel Total, launched in 2008—a washable paint using Japanese polymer technology that created a protective film on walls. While competitors' washable paints could handle gentle cleaning, Excel Total withstood scrubbing with detergent, crucial for Indian homes where walls faced everything from cricket balls to cooking oil splatter. The product commanded a 20% premium over standard emulsions and gained 8% market share in the premium segment within two years.

Distribution expansion followed an unconventional path. Rather than matching Asian Paints' 30,000+ dealer network, Kansai Nerolac focused on quality over quantity. The company created 3,000 "Nerolac Impression" stores—premium outlets in urban areas offering color consultation, digital visualization, and painting services. Each store required ₹50 lakh investment, with Kansai Nerolac providing 60% funding. The stores generated 3x higher revenue per square foot than traditional paint shops.

The services innovation was particularly clever. In 2010, Kansai Nerolac launched painting services—not just selling paint but managing the entire painting process. This addressed a major consumer pain point: finding reliable painters. The company trained 15,000 painters in Japanese application techniques, provided uniforms and insurance, and guaranteed quality. The service commanded 40% margins versus 20% for paint alone, while creating switching costs as consumers valued the hassle-free experience.

Marketing underwent radical transformation. Abandoning the industry's traditional celebrity endorsement model, Kansai Nerolac focused on digital engagement and experiential marketing. The "Healthy Home" campaign, launched in 2012, positioned paint as a health product—low VOC, anti-bacterial, air-purifying. Mobile apps let consumers visualize colors on their walls using augmented reality. The company sponsored architecture colleges' design competitions, building relationships with future influencers.

The powder coatings business became an unexpected star. As Indian manufacturers increasingly preferred powder coating for durability and environmental benefits, Kansai Nerolac leveraged its parent's technology to dominate this niche. The 2018 acquisition of Marpol Private Limited for undisclosed terms strengthened this position. Kansai Nerolac is a leader in the Powder coating market in India. The acquisition of Marpol will further add to the leadership of Kansai Nerolac in the power coating market in India.

International expansion provided another growth avenue. In 2018, Kansai Nerolac Paints Ltd. announced that it has completed the acquisition of 55% equity share holding of RAK Paints Ltd, Bangladesh. The Bangladesh entry leveraged India's manufacturing scale while adapting to local preferences—Bangladeshi consumers preferred brighter colors and required paints resistant to higher humidity. The acquisition immediately made Kansai Nerolac among the top three players in Bangladesh's $400 million paint market.

Sustainability became a differentiator rather than compliance burden. The company's Jainpur plant, upgraded in 2015, became India's first zero-liquid-discharge paint facility. Solar panels provided 30% of energy needs. Water-based paints grew from 15% of portfolio in 2006 to 45% by 2019. The company launched India's first paint recycling program, collecting leftover paint from construction sites for reprocessing. These initiatives resonated with environmentally conscious consumers and institutional buyers mandating green suppliers.

The financial trajectory reflected successful diversification. Revenue grew from ₹1,250 crores in 2006 to ₹6,843 crores in FY2020—a CAGR of 12.9%. Decorative paints' contribution increased from 35% to 48% of revenue. The company maintained EBITDA margins between 11-14% despite intense competition and raw material volatility. Return on capital employed averaged 18%, exceptional for a capital-intensive manufacturing business.

Yet challenges emerged. Asian Paints responded aggressively to Kansai Nerolac's decorative push, launching competing products and offering dealer incentives. Berger Paints, backed by UK's J&N Investment, expanded rapidly in tier-2 cities. New entrants like JSW Paints threatened market share. Most ominously, Grasim Industries, part of the Aditya Birla Group, announced plans to enter paints with ₹10,000 crore investment—the largest-ever entry in Indian paints.

The 2020 pandemic initially devastated demand as construction stopped and automotive production plummeted. But it also accelerated trends favoring Kansai Nerolac—health consciousness driving demand for anti-bacterial paints, DIY culture growing as people spent more time at home, and industrial customers consolidating suppliers for supply chain resilience. The company's response would determine whether its carefully built franchise could withstand the coming disruption.

The Current Challenge: Disruption & Competition (2020–Present)

The Mumbai monsoon of 2021 brought an unexpected visitor to Kansai Nerolac's headquarters. Kumar Mangalam Birla, chairman of the Aditya Birla Group, had come to deliver a message that would shake the paint industry: Grasim Industries was launching "Birla Opus", aiming for Rs.10,000 Cr gross revenue within 3 years of full-scale operations, with an unprecedented level of upfront investment of Rs.10,000 Cr. For Kansai Nerolac's management, this wasn't just another competitor—it was an existential threat from India's third-largest conglomerate.

The scale of Grasim's ambition was staggering. Birla Opus has six strategically located, fully automated, integrated, and global scale manufacturing plants with a total commercial capacity of 1,332 MLPA (million litres per annum) - a quantum leap of 40% addition to the current industry capacity. To put this in perspective, Kansai Nerolac had built its capacity to approximately 650 MLPA over a century. Grasim was creating twice that capacity before selling a single liter of paint.

The timing couldn't have been worse for incumbents. The company has delivered a poor sales growth of 8.18% over past five years. Company has a low return on equity of 11.0% over last 3 years. The pandemic had initially crushed demand, then created supply chain chaos as raw material prices spiked. Titanium dioxide, comprising 30% of paint costs, saw prices increase 40% in eighteen months. Crude oil derivatives affecting another 30% of inputs experienced similar volatility.

But Grasim's entry represented more than just capacity addition—it was a fundamental reimagining of the paint business model. Birla Opus products would be available across all 1 lakh population towns in India by July 2024, with the company aiming to expand its distribution to over 6,000 towns by the fiscal year end. This will be the fastest & widest pan-India launch by any paint brand. While Kansai Nerolac had carefully built distribution over decades, Grasim was attempting to achieve similar reach in months.

The strategic logic behind Grasim's paint foray was compelling. The Aditya Birla Group's deep insight into the building materials ecosystem, honed over the years, offers us a unique vantage point. It aims to leverage its existing network, scale, and Group capabilities along with decades of experience in the building materials sector through its subsidiary UltraTech Cement. With UltraTech Cement commanding 23% market share, Grasim had relationships with every major contractor, architect, and real estate developer in India. Kansai Nerolac's recent performance numbers tell the story of a company under siege. Kansai Nerolac Q1 FY26 revenue Rs 2087 Cr, EBITDA down 6.7%, PBT down 4.1%, outlook cautiously optimistic. The challenges are multifaceted—competition intensifying, margins compressing, and growth stalling despite India's booming construction market.

The competitive response to Grasim has been complex. Rather than engage in a price war that would destroy industry margins, Kansai Nerolac focused on its strengths. The company accelerated its "Paint+" initiative—offering not just products but complete solutions including waterproofing, construction chemicals, and adhesives. The 2019 acquisition of Perma Construction Aids for ₹29 crores gave them entry into the high-margin construction chemicals segment, growing at 20% annually.

Digital transformation became urgent rather than optional. The company launched "Nerolac Visualizer," an AI-powered app that could scan any surface and show how different paint colors would look. More importantly, they created "Nerolac Connect"—a B2B platform for contractors and painters offering instant credit, loyalty rewards, and technical support. By 2023, 30% of trade sales happened digitally, reducing distribution costs by 200 basis points.

The innovation pipeline accelerated with products targeting specific Indian problems. "Excel Anti-Puff" addressed paint bubbling during monsoons. "Impressions HD" created texture effects matching expensive wallpapers at 20% of the cost. "Suraksha Plus" contained silver ion technology providing anti-viral properties—launched during COVID but remaining relevant as health consciousness persisted. Each product commanded 15-25% premiums over standard offerings.

International expansion provided a buffer against domestic competition. The transaction closed on 19 June 2018. when Kansai Nerolac acquired RAK Paints Bangladesh. The Bangladesh operation, leveraging India's scale economies, achieved 15% EBITDA margins within two years. Sri Lanka, Nepal, and Myanmar followed, creating a South Asian footprint generating ₹500 crores in revenue by 2023.

But the fundamental challenge remains structural. Paint manufacturing has low entry barriers—anyone with ₹500 crores can set up a plant. The differentiators are brand, distribution, and service—areas where Grasim's deep pockets pose real threats. Kumar Mangalam Birla "invited the entire spectrum of 100,000+ paint dealers pan India to participate in this industry revolution and transform consumer experience". This wasn't just marketing rhetoric but a declaration of intent to reshape industry economics.

The raw material volatility adds another layer of complexity. Titanium dioxide prices increased 35% between 2021-2023. Crude derivatives faced similar spikes. While larger players could absorb temporary margin compression, smaller ones couldn't, leading to consolidation. Yet this consolidation didn't benefit Kansai Nerolac as much as expected—Grasim acquired several regional players, instantly gaining local market knowledge and distribution.

Management's response reflects both confidence and concern. "During the quarter, demand for decorative showed signs of revival, though an early monsoon impacted during the later part of the quarter. KNP decorative performance was affected due to the disturbance in April, which impacted key markets in the North. In automotive, demand for KNP continued to be better than the market, on the back of various initiatives. Performance coatings registered strong growth," said Pravin Chaudhari, managing director of Kansai Nerolac Paints.

The outlook remains cautiously optimistic but acknowledges unprecedented challenges. "Raw material prices were benign. Forex remained volatile. The uncertainty in the environment due to geopolitical factors continued, and we remain watchful," he added. This isn't the language of a dominant market leader but of a company navigating uncharted waters.

Financial Deep Dive & Unit Economics

The numbers tell a story of resilience under pressure, revealing both the strength of Kansai Nerolac's business model and the challenges of competing in a disrupted market. With a current market capitalization of ₹18,868 crores and annual revenues of ₹7,852 crores, the company trades at 2.4x sales—a discount to Asian Paints' 8x but premium to global paint companies averaging 1.5x.

The capital structure reflects Japanese conservative financial philosophy. Company is almost debt free. This zero-leverage approach provides flexibility during downturns but also limits growth investments when competitors are spending aggressively. The company maintains cash reserves of approximately ₹800 crores, earning 6% returns—suboptimal capital allocation but providing a war chest for competitive battles ahead.

Revenue composition reveals strategic positioning. Decorative paints contribute 48% of revenues but only 35% of EBITDA, reflecting intense competition and lower margins. Industrial coatings—automotive, protective, powder—generate 52% of revenues but 65% of EBITDA, with margins exceeding 18%. This 600 basis point margin differential explains why Kansai Nerolac resists abandoning its industrial heritage for decorative market share wars.

The working capital dynamics are particularly interesting. The company operates with negative working capital in industrial segments—customers pay advances for large orders while raw material suppliers extend 60-90 day credit. Decorative paints require positive working capital as dealers demand credit while retail consumers pay immediately. The blended working capital cycle of 45 days compares favorably to industry average of 60 days but has stretched from 35 days five years ago.

Cost structure analysis reveals operational efficiency gaps. Raw materials constitute 65% of revenues, in line with industry standards. Employee costs at 8% of revenues are higher than Asian Paints' 6%, reflecting legacy workforce and Japanese lifetime employment practices. Marketing expenses at 7% lag Asian Paints' 9%, explaining brand awareness gaps. Manufacturing costs at 5% are industry-leading, reflecting Japanese operational excellence.

The EBITDA margin trajectory tells the competition story. From 14% in 2015, margins compressed to current 12.05%, with quarterly variations between 10-13%. The 200 basis point compression reflects three factors: increased competition forcing promotional spending, product mix shift toward lower-margin decorative paints, and inability to fully pass through raw material inflation. Management targets returning to 14% margins through premiumization and cost optimization.

Return metrics paint a sobering picture. Company has a low return on equity of 11.0% over last 3 years. This compares unfavorably to Asian Paints' 25% ROE and even Berger's 18%. The low returns reflect three factors: conservative capital structure with zero debt, capital tied up in manufacturing assets with 70% utilization, and competitive pricing pressure preventing margin expansion.

The dividend policy reflects Japanese shareholder-friendly approach. Company has been maintaining a healthy dividend payout of 27.6% Despite growth challenges, the company maintains consistent dividends, viewing them as return of excess capital rather than signaling confidence. The ₹3.75 per share annual dividend provides 1.5% yield—not attractive for income investors but reliable for long-term holders.

Capital expenditure patterns reveal strategic priorities. Annual capex averaging ₹300 crores focuses 40% on capacity expansion, 30% on technology upgrades, 20% on sustainability compliance, and 10% on digital initiatives. This contrasts with Grasim's ₹10,000 crore paint investment—33 years of Kansai Nerolac's capex spent in three years. The David versus Goliath dynamic is stark.

Geographic revenue distribution shows concentration risks. Maharashtra and Gujarat contribute 35% of revenues, Delhi-NCR adds 20%, South India 25%, and rest of India 20%. The North India dependence is problematic given Grasim's initial focus on Punjab and Haryana markets. International operations contribute only 6% of revenues despite strategic importance.

The cash flow quality is exceptional. Operating cash flow consistently exceeds reported profits due to non-cash depreciation charges. Free cash flow generation of ₹600-700 crores annually funds dividends, modest growth investments, and cash accumulation. The cash conversion cycle of 95% ranks among India's best manufacturing companies.

Segment profitability analysis reveals hidden strengths. Automotive OEM business generates 25% ROCE despite capital intensity, protected by switching costs and technical specifications. Protective coatings for infrastructure earn 20% ROCE with multi-year contracts providing visibility. Powder coatings post 30% ROCE but remain subscale. Decorative paints deliver only 12% ROCE, explaining reluctance to chase market share.

Inventory management showcases operational excellence. Raw material inventory turns 12 times annually versus industry average of 8 times. Finished goods turn 24 times, reflecting made-to-order industrial business and efficient decorative distribution. The ₹450 crores total inventory seems high absolutely but represents only 21 days of sales—remarkable for a company with 100,000+ SKUs.

The recent quarterly performance demands scrutiny. Revenue from operations stood at ₹2,162.03 crore in Q1 FY26, up 1.4 per cent from ₹2,133.08 crore in the same quarter last year. On a quarter-on-quarter (Q-o-Q) basis, revenue grew 18.9 per cent from ₹1,818.85 crore in Q4 FY25. The sequential improvement suggests recovery, but year-over-year stagnation in a growing market implies market share loss.

Unit economics at product level reveal strategic challenges. A 20-liter decorative paint drum generates ₹3,000 revenue with ₹450 gross profit—15% margin before distribution costs. After dealer margins, transport, and marketing, net margins shrink to 5-7%. Industrial coatings for one car generate ₹5,000 revenue with ₹1,500 gross profit—30% margin. After technical service and logistics, net margins remain healthy at 15-18%. This 10 percentage point margin differential drives capital allocation decisions.

The Japanese Connection: Kansai Paint's Global Strategy

Established in 1918, Kansai Paint Co. Ltd. is one of the largest coatings manufacturers in Japan and Africa, with leading positions in China, India, and Southeast Asia. The company operates across Europe, the Americas, and the Middle East, generating revenue of $3.49 billion in 2024. As the world's eighth-largest paint company, Kansai Paint exemplifies Japanese industrial expansion on the global stage.

The company's founding by Katsujiro Iwai in 1918 parallels Japan's industrial emergence. Starting as a supplier to Japan's nascent automotive industry, Kansai Paint grew alongside Toyota, Honda, and Nissan, becoming indispensable to Japanese manufacturing. Kansai Paint operates three automotive paint plants from its headquarters in Osaka, Japan and is the leading supplier of automotive coatings to Toyota, Suzuki, Nissan, Honda, Peugeot and Renault worldwide. This automotive DNA would prove crucial in India.

Kansai Paint's global strategy reflects Japanese corporate philosophy—patient capital, technical excellence, and relationship-based growth. It divides its business into automotive (30.7%), automotive refinish (5.2%) industrial (26.3%), decorative (25.6%), marine and protective (6%) and others (6.2%). By region, Japan comprises 30% of sales, India 25%, Asia 13.4%, Africa 8.2%, Europe 22% and others 1.4%. India's 25% contribution makes it Kansai's second-largest market globally, explaining the strategic importance of Nerolac.

The India investment thesis emerged from Kansai's "Vision 2030" strategy, formulated in 2010. Japanese domestic paint consumption was declining as population aged and construction slowed. China offered growth but regulatory uncertainty. India presented the ideal combination—democratic stability, English-speaking workforce, growing middle class, and infrastructure boom. Kansai's board allocated $2 billion for emerging market expansion, with India receiving the largest share.

The cultural fit between Japanese management and Indian operations proved surprisingly smooth. Both cultures value hierarchy, long-term relationships, and technical expertise. Japanese "kaizen" continuous improvement resonated with Indian "jugaad" innovation. The companies shared reverence for founding families—Iwai in Japan, Tata connection in India. This cultural alignment enabled deeper integration than typical foreign acquisitions.

Technology transfer remains the cornerstone of value creation. Kansai's Osaka R&D center, employing 500 scientists, develops technologies specifically for Asian markets. The "Cool Paint" technology, reducing surface temperatures by 10°C, was developed for Middle Eastern markets but found massive application in India. Nano-ceramic formulations for automotive clear coats, providing self-healing properties for minor scratches, gave Kansai Nerolac exclusive supplier status with premium car manufacturers.

The financial relationship evolved beyond simple ownership. Kansai provides technical licensing at concessional rates, saving Kansai Nerolac approximately ₹50 crores annually in technology fees. Raw material procurement leverages Kansai's global scale—titanium dioxide sourced through Kansai's contracts costs 5-7% less than market rates. Equipment procurement through Japanese suppliers, backed by Kansai guarantees, reduces capital costs by 15-20%.

The strategic value extends beyond economics. When Indian automotive manufacturers expanded internationally—Tata Motors acquiring Jaguar Land Rover, Mahindra entering US markets—Kansai Nerolac leveraged parent relationships to secure paint contracts at international facilities. The company supplies paint to Maruti Suzuki's Gujarat plant, with formulations developed jointly by Indian and Japanese teams, creating technical barriers competitors cannot easily replicate.

During the reporting period, Kansai Paint recorded sales revenue of ¥274.05 billion, representing a 9.3% year-on-year growth. Operating profit reached ¥25.734 billion, indicating a significant 63.3% increase, primarily attributable to improved profitability by transferring costs to sales prices amidst increased selling expenses. Operating income rose to ¥32.084 billion, a 52.5% YoY growth, driven by equity method investment income and increased gains from foreign exchange due to yen depreciation. Net income attributable to the parent company's shareholders for the quarter was ¥46.452 billion, reflecting a remarkable 275.5% YoY increase, mainly due to the sale of investment securities resulting from a reduction in policy holdings and fixed asset sales from land in India.

The parent's strong global performance provides resources for Indian competition. Kansai Paint's improving profitability—operating margins expanding from 8% to 13% in Japan—generates cash for emerging market investments. The company committed additional ₹500 crores for Kansai Nerolac's capacity expansion and market development, crucial given Grasim's aggressive entry.

Yet tensions exist in the relationship. Kansai Paint's conservative approach sometimes frustrates Indian managers seeking aggressive expansion. Investment approvals requiring Osaka board consent can delay market responses. The parent's preference for consensus decisions clashes with India's fast-moving competitive dynamics. Some Indian executives privately express concern that Japanese caution might handicap them against Grasim's entrepreneurial aggression.

The global paint industry consolidation affects strategic thinking. In November of 2023, Kansai Paint announced that the company and AkzoNobel terminated the agreement to sell Kansai's African business. Kansai Paint stated that it will continue to operate its African business and aim to strengthen its competitiveness in the African market, improve customer satisfaction and continue to contribute to the development of the African society. This decision to retain African operations signals commitment to emerging markets, including India.

Comparing Kansai Paint to global peers reveals strategic positioning. In comparison, Nippon Paint's local peer, Kansai Paint Co., Ltd., also demonstrated revenue growth over the last five years, albeit at a lower rate. Kansai's revenue grew at a CAGR of 6% to JPY562bn in FY24. Nippon Paint's EBITDA margin of 15% outperformed Kansai Paint's 13% in FY24. While Nippon Paint grows faster, Kansai's India position through Nerolac provides unique emerging market exposure.

The technology pipeline remains robust. Kansai's development of water-based automotive coatings for electric vehicles, addressing different corrosion challenges than combustion engines, positions Kansai Nerolac for India's EV transition. Bio-based paints using plant-derived polymers, reducing petroleum dependence by 40%, address both sustainability concerns and raw material volatility. These innovations, funded by Japanese R&D but commercialized in India, create competitive advantages difficult to replicate.

Looking forward, Kansai Paint's commitment to India seems unwavering despite challenges. The parent views India not just as a market but as a development hub for emerging economy products. Plans exist to establish a regional R&D center in Mumbai, serving Middle East and Africa from India. This positions Kansai Nerolac not just as an Indian subsidiary but as a regional champion in Kansai's global network.

Playbook: Business & Investing Lessons

The Kansai Nerolac story offers a masterclass in cross-border value creation, patient capital deployment, and navigating emerging market complexities. Each strategic decision—from the initial technical collaboration to current competitive battles—provides lessons for both operators and investors.

Lesson 1: Technical Collaboration Before Acquisition The 16-year technical partnership (1983-1999) before full acquisition represents a forgotten model of cross-border deals. Rather than hostile takeovers or auction processes, Kansai built deep operational understanding and cultural trust. This gradual approach reduced integration risk and created value through operational improvements before financial engineering. Modern private equity's rush to deploy capital could learn from this patience.

Lesson 2: The Industrial Moat Paradox Kansai Nerolac's focus on industrial coatings over decorative paints seemed counterintuitive—decorative markets are larger with higher growth. But industrial relationships create switching costs that decorative brands cannot match. Changing automotive paint suppliers requires revalidating entire production lines, retraining workers, and risking quality variations that could affect car sales. Once embedded, industrial suppliers become quasi-permanent partners. The lesson: unsexy B2B businesses often have stronger moats than glamorous consumer brands.

Lesson 3: Distribution Versus Manufacturing Scale While Grasim builds massive manufacturing capacity, Kansai Nerolac's response focuses on distribution and service. Paint manufacturing has become commoditized—anyone can build factories. But convincing 30,000 dealers to stock your brand, training 50,000 painters in application techniques, and providing color consultation to millions of consumers requires decades of relationship building. The lesson: in commoditizing industries, distribution and service create more sustainable advantages than production scale.

Lesson 4: The Japan Premium Japanese ownership provides intangible benefits beyond capital and technology. Indian customers, particularly automotive OEMs, value Japanese quality associations. Government officials trust Japanese companies' long-term commitment versus Western private equity's exit orientation. Employees see career stability in Japanese lifetime employment philosophy. This "Japan Premium"—worth perhaps 200-300 basis points in margins—demonstrates how country-of-origin affects business value in emerging markets.

Lesson 5: Managing the Innovation Paradox Kansai Nerolac faces an innovation dilemma: advanced products that showcase technical superiority often don't match Indian market needs. Anti-graffiti coatings perfect for Tokyo subways have limited demand in India. Meanwhile, simple innovations like paint that masks wall cracks—technically trivial but locally relevant—drive volume growth. The lesson: emerging market innovation requires unlearning developed market assumptions.

Lesson 6: The Patience Premium Kansai's 40+ year involvement in India—from technical collaboration through full ownership to current expansion—exemplifies patient capital. While Western investors demand 20% IRRs over 5-year holds, Japanese corporations accept 8-10% returns over decades. This patience allows investments in brand building, distribution networks, and customer relationships that short-term owners cannot afford. The lesson: time horizon is itself a competitive advantage.

Lesson 7: Cultural Integration vs. Cultural Preservation Kansai succeeded by selectively integrating cultures rather than imposing Japanese management wholesale. Quality circles and continuous improvement were adopted; consensus decision-making was not. Indian market responsiveness was preserved; Japanese operational discipline was added. This selective integration—harder than complete transformation or status quo—created a unique organizational capability. The lesson: successful cross-border acquisitions require cultural architects, not just financial engineers.

Lesson 8: The Vertical Integration Question Unlike Asian Paints, which backward integrated into raw materials, Kansai Nerolac remained focused on paint manufacturing. This seemed disadvantageous when raw material prices spiked. But avoiding capital-intensive chemical plants preserved flexibility and returns. When titanium dioxide prices collapsed in 2024, Kansai Nerolac benefited fully while integrated competitors faced stranded assets. The lesson: vertical integration's benefits must be weighed against capital intensity and flexibility loss.

Lesson 9: Premium vs. Volume Strategy Kansai Nerolac's strategy of premiumization through technology contrasts with competitors' volume growth focus. Average realization per liter is 15% higher than industry average, but volume growth lags. This creates a mathematical challenge: is 15% price premium worth sacrificing potential 30% volume growth? The answer depends on market structure, competitive dynamics, and organizational capabilities. The lesson: strategic clarity matters more than strategic perfection.

Lesson 10: The Ecosystem Play Rather than viewing paint in isolation, Kansai Nerolac increasingly positions itself as a surface solutions provider—paints, waterproofing, construction chemicals, adhesives. This ecosystem approach increases customer wallet share and creates bundling opportunities. A construction project using Nerolac paint, Perma waterproofing, and Nerofix adhesives has switching costs beyond single products. The lesson: expanding horizontally within customer workflows creates stickier relationships than product improvement alone.

Lesson 11: Managing Competitive Disruption Grasim's entry represents classic disruption—new entrant with patient capital attacking industry profit pools. Kansai Nerolac's response—focusing on service, innovation, and relationships rather than price wars—follows disruption theory's prescription for incumbents. Whether this succeeds depends on execution and competitor mistakes. The lesson: when facing disruption, incumbents should leverage existing advantages rather than compete on disruptors' terms.

Lesson 12: The Governance Balance With 75% ownership, Kansai Paint could impose complete control but maintains independent directors and local decision-making. This governance balance—strategic control with operational autonomy—attracts talent and preserves entrepreneurial energy. Complete integration might improve coordination but would sacrifice local market responsiveness. The lesson: ownership percentage and management control need not be perfectly correlated.

These lessons extend beyond paint to any industry where foreign capital meets emerging markets, where technology transfer creates value, and where patient capital competes with financial engineering. The Kansai Nerolac playbook—technical excellence, patient capital, cultural integration, and relationship focus—offers an alternative to both aggressive private equity and passive portfolio investment.

Analysis & Bear vs. Bull Case

The investment case for Kansai Nerolac presents a fascinating study in contrasts—undeniable strategic strengths undermined by recent performance, dominant market positions threatened by new competition, and Japanese backing providing both stability and constraints.

Bull Case: The Resilient Industrial Champion

The optimistic view starts with Kansai Nerolac's unassailable position in industrial coatings. With 40%+ market share in automotive OEM paints, protective coatings, and powder coatings, the company has built switching costs that new entrants cannot easily overcome. Consider the automotive relationships: Maruti Suzuki has used Kansai Nerolac paints for 40 years, with paint specifications integrated into vehicle warranties. Changing suppliers would require revalidating corrosion resistance, color matching across multiple plants, and retraining entire workforces. The cost and risk make switching economically irrational unless price differentials exceed 30%—unlikely given rational competition.

The infrastructure opportunity remains massive. India's ₹100 trillion National Infrastructure Pipeline requires protective coatings for everything from bridges to pipelines. Kansai Nerolac's technical expertise in specialized coatings—high-temperature resistant for power plants, chemical-resistant for refineries, anti-corrosive for coastal projects—cannot be replicated quickly. Government infrastructure projects increasingly specify established suppliers with proven track records, effectively excluding new entrants from large contracts.

The financial position provides competitive flexibility. With virtually no debt and ₹800 crores cash, Kansai Nerolac can withstand price wars, invest counter-cyclically, or pursue acquisitions. This balance sheet strength contrasts with leveraged new entrants who must generate returns to service debt. In a margin compression scenario, Kansai Nerolac can outlast financially weaker competitors.

Japanese parentage offers unique advantages beyond capital. Kansai Paint's global automotive relationships open doors with international manufacturers entering India. As Japanese automotive companies increase Indian investments—Honda's new plant, Toyota's expansion, Suzuki's EV plans—Kansai Nerolac automatically becomes the preferred paint supplier. This relationship moat deepens over time rather than eroding.

The sustainability transition creates new opportunities. Environmental regulations increasingly mandate water-based, low-VOC, and eco-friendly paints. Kansai Nerolac's Japanese technology pipeline includes bio-based paints, self-cleaning coatings, and energy-efficient solutions. As sustainability premiums emerge—green buildings paying 10-15% more for eco-friendly paints—technology leaders capture disproportionate value.

International expansion provides growth beyond India's competitive battles. Bangladesh, Sri Lanka, Nepal, and Myanmar operations already generate ₹500 crores revenue with 15%+ EBITDA margins. These markets, five years behind India's development curve, offer growth opportunities without Grasim-style competition. Successful regional expansion could double international revenue contribution within five years.

Bear Case: The Declining Incumbent

The pessimistic view starts with undeniable performance deterioration. Five-year revenue CAGR of 8.18% significantly lags India's 15% paint market growth, indicating market share loss. ROE of 11% falls below cost of capital, destroying shareholder value. EBITDA margins compressing from 14% to 12% suggest competitive pressure overwhelming operational improvements. These aren't temporary blips but five-year trends indicating structural challenges.

Grasim's entry fundamentally changes industry structure. Adding 40% capacity in a market growing 12-15% annually ensures oversupply and margin pressure. Grasim's ₹10,000 crore investment war chest dwarfs Kansai Nerolac's ₹300 crore annual capex. More concerning, Grasim targets dealer networks with unprecedented incentives—30% margins versus industry-standard 20%, interest-free credit, and turnover bonuses. Once dealers shift allegiance, recovering them requires years and significant investment.

The decorative segment weakness is particularly troubling. Despite decade-long efforts, Kansai Nerolac remains a distant third with 13-15% market share versus Asian Paints' 50%. Decorative paints generate 60% of industry profits and drive brand awareness affecting industrial sales. Weak decorative positioning limits pricing power and growth potential across all segments.

Digital disruption threatens traditional advantages. Online paint sales, currently 2% of market, could reach 15% within five years following global patterns. Digital channels favor price transparency and new brands over established relationships. Kansai Nerolac's dealer network advantage evaporates if consumers buy directly online. Digital marketing costs favor deep-pocketed new entrants over margin-constrained incumbents.

Management conservatism handicaps competitive response. Japanese decision-making speed cannot match Indian market dynamics. While competitors launch products in months, Kansai Nerolac's approval processes take quarters. The preference for consensus over speed, stability over risk-taking, creates structural disadvantages in rapidly evolving markets.

Raw material volatility exposes operational weaknesses. Despite Japanese operational excellence, Kansai Nerolac couldn't prevent margin compression during input cost spikes. Lack of backward integration leaves the company vulnerable to commodity cycles. Competitors with captive raw material sources or better procurement scale maintain margins while Kansai Nerolac suffers.

Balanced Assessment: The Nuanced Reality

The truth lies between extremes. Kansai Nerolac isn't the dominant champion bulls imagine nor the declining incumbent bears fear. It's a solid industrial franchise facing unprecedented competition, with outcomes depending on execution and competitor mistakes.

The industrial moat remains strong but not impregnable. While switching costs protect existing relationships, new projects increasingly consider multiple suppliers. Grasim's aggressive pricing for new contracts forces Kansai Nerolac to choose between margins and market share. The industrial dominance erodes slowly but steadily.

Financial strength provides resilience but not immunity. The debt-free balance sheet allows weathering short-term storms but doesn't guarantee long-term competitiveness. Cash reserves quickly deplete if used for dealer incentives matching Grasim's offers. Financial flexibility matters less than operational excellence in commodity industries.

Japanese backing offers stability but limits optionality. While patient capital allows long-term thinking, it also prevents aggressive responses like leveraged acquisitions or transformative investments. The parent's preference for steady returns over moonshot bets constrains strategic options.

The most likely scenario: Kansai Nerolac remains a profitable niche player—dominant in industrial coatings, subscale in decorative paints, generating steady but unspectacular returns. Market share stabilizes at lower levels, margins recover partially, and ROE improves to 13-15%. Not the growth story bulls hope for, not the disaster bears predict, but a mature industrial business generating reliable cash flows.

Investment implications depend on price and expectations. At current valuations—2.4x sales, 17x earnings—the market prices modest growth and margin recovery. Significant upside requires successful decorative expansion or competitor stumbles. Downside seems limited given industrial moats and financial strength. The risk-reward appeals more to value investors seeking steady compounders than growth investors chasing multibaggers.

Power & Strategic Position

Understanding Kansai Nerolac's true competitive position requires analyzing the sources of power that create sustainable advantages—or their absence. Using the framework of "7 Powers" by Hamilton Helmer, we can dissect where the company has built defensibility and where vulnerabilities exist.

Switching Costs: The Industrial Fortress

Kansai Nerolac's greatest power lies in switching costs within industrial segments. Automotive manufacturers face multiple barriers to changing paint suppliers: revalidation costs exceeding ₹50 crores for a single model, 12-18 month qualification periods risking production delays, warranty implications from changed specifications, and color matching complexities across global facilities. These switching costs create an annuity-like revenue stream—once embedded, Kansai Nerolac remains for the vehicle's entire production lifecycle, typically 7-10 years.

The switching costs extend beyond direct expenses to risk considerations. A paint failure causing recalls could cost manufacturers billions in repairs and reputation damage. This asymmetric risk—small savings from switching versus catastrophic downside from failure—makes procurement managers extremely conservative. Kansai Nerolac's 40-year track record without major quality issues represents insurance value that new entrants cannot provide.

Network Effects: The Missing Multiplier

Unlike digital platforms, paint manufacturing exhibits minimal network effects. More customers don't make the product inherently more valuable to other customers. However, subtle network dynamics exist in the contractor-painter ecosystem. Painters trained on Nerolac products recommend them to customers, creating a virtuous cycle. The company's 50,000+ trained painters represent a distributed sales force, but this network effect remains weak compared to true platform businesses.

Counter-Positioning: The Japanese Differentiation

Kansai Nerolac successfully counter-positions against both premium international brands and local competitors. Versus international brands like AkzoNobel or PPG, the company offers "Japanese quality at Indian prices"—a compelling value proposition. Versus local competitors, the Japanese technology heritage commands premium pricing. This positioning sweet spot—neither cheapest nor most expensive—appeals to value-conscious yet quality-seeking Indian consumers.

The counter-positioning extends to business model choices. While Asian Paints integrated backward into raw materials, Kansai Nerolac remained asset-light in chemicals. This seemed disadvantageous during raw material inflation but now provides flexibility as commodity prices normalize. Different strategic choices create different optimization surfaces, making direct competition difficult.

Scale Economies: Subscale Disadvantage

Here lies Kansai Nerolac's strategic weakness. In decorative paints, scale economies are decisive—advertising costs spread across volumes, distribution efficiency improving with density, and procurement leverage increasing with size. Asian Paints' 3.5x revenue advantage translates into 200-300 basis points structural cost advantage. Grasim's massive capacity additions potentially create another scale competitor, further disadvantaging subscale players.

The scale disadvantage compounds in brand building. Asian Paints spends ₹800 crores annually on advertising; Kansai Nerolac spends ₹250 crores. This 3x spending difference creates visibility gaps that quality alone cannot overcome. In consumer businesses, share of voice drives share of mind, which drives market share—a dynamic where scale breeds more scale.

Cornered Resource: Technical Expertise

Kansai Nerolac's access to Japanese R&D represents a cornered resource—exclusive access to valuable assets. Kansai Paint's formulations for automotive manufacturers, developed over decades and protected by trade secrets, cannot be reverse-engineered easily. The parent company's ₹500 crore annual R&D budget, partially benefiting Indian operations, exceeds what independent Indian paint companies could afford.

The technical expertise manifests in specific capabilities: formulating paints for new substrates like carbon fiber, developing coatings for electric vehicle batteries, and creating self-healing clear coats. These specialized capabilities, while niche, command premium pricing and create customer dependency. A competitor would need decades and billions in investment to replicate this knowledge base.

Process Power: Operational Excellence

Forty years of Japanese-influenced operations created process power—embedded organizational capabilities driving superior outcomes. Kansai Nerolac's manufacturing yields exceed industry averages by 5-7%, reducing costs despite smaller scale. Quality consistency, measured in parts-per-million defects, matches global standards that Indian competitors struggle to achieve. These process advantages, deeply embedded in organizational culture, resist imitation despite being observable.

The process power extends to customer service. Kansai Nerolac's technical service teams, solving customer problems on-site, create relationships beyond transactional sales. The ability to reformulate products for specific applications, provide global benchmarking data, and offer preventive maintenance recommendations represents process knowledge accumulated over decades.

Branding: The Incomplete Asset

Branding remains Kansai Nerolac's most underdeveloped power source. While "Nerolac" enjoys 70% awareness among painters and contractors, consumer brand recognition lags at 40% versus Asian Paints' 85%. The brand conveys reliability and quality but lacks emotional connection or lifestyle association that drives consumer preference in decorative segments.

The industrial heritage, while providing B2B credibility, actually handicaps B2C branding. Consumers associate Nerolac with factories and infrastructure, not homes and creativity. Attempts to build decorative brand equity—celebrity endorsements, digital campaigns, experiential marketing—haven't overcome this perception gap. Without strong consumer branding, the company remains vulnerable to price competition in decorative segments.

Strategic Position Synthesis

Mapping these power sources reveals Kansai Nerolac's strategic position: a strong B2B franchise with limited B2C presence, defended by switching costs and technical expertise but vulnerable to scale competition. The company occupies a profitable but constrained strategic space—too successful in industrials to abandon them, too subscale in decoratives to dominate.

The power analysis suggests three strategic imperatives: 1. Defend the industrial fortress by increasing switching costs through deeper technical integration 2. Selectively build scale in decorative sub-segments where technical differentiation matters 3. Leverage cornered resources by commercializing Japanese technology for Indian-specific applications

The competitive dynamics increasingly favor focused strategies over diversified approaches. Kansai Nerolac must choose between being the undisputed industrial champion or a meaningful decorative player—attempting both risks achieving neither. The power framework suggests doubling down on industrial strengths while selectively participating in decorative segments where technical advantages create differentiation.

Epilogue & "If We Were CEOs"

Standing at the crossroads of its second century, Kansai Nerolac faces choices that will determine whether it remains a respectable also-ran or reclaims its position as India's paint innovation leader. If we were CEOs, taking charge in 2025, here's the strategic playbook we'd execute.

First Priority: Own the Future of Mobility

Rather than fighting unwinnable decorative battles, we'd make Kansai Nerolac synonymous with India's mobility transformation. Electric vehicles require completely different coating systems—battery pack protection, thermal management coatings, and EMI shielding paints. We'd establish India's first EV Coating Innovation Center, partnering with every EV manufacturer from Tata to Tesla. The goal: when anyone thinks EV coatings, they think Nerolac.

We'd extend this to the broader mobility ecosystem—specialized coatings for charging stations, high-durability paints for shared mobility fleets, and anti-bacterial coatings for public transport post-pandemic. This positions us not as a paint company but as a mobility surface solutions provider, capturing value from India's $300 billion mobility transformation.

Second Priority: The "Invisible Innovation" Strategy

Instead of competing on visible decorative paints where brand and scale dominate, we'd focus on invisible innovations that solve real problems. Anti-viral coatings for hospitals—certified to kill 99.9% of pathogens. Heat-reflective primers that reduce air conditioning costs by 20%. Moisture-barrier coatings preventing seepage in India's aging buildings. These products command 40% premiums because they solve expensive problems.

We'd create a "Nerolac Labs" certification program, where buildings using our innovative solutions receive energy efficiency and health safety certifications. This B2B2C model bypasses consumer brand battles while creating pull-through demand. Property developers would specify Nerolac not for aesthetics but for performance metrics affecting property values.

Third Priority: The Platform Play

Rather than building stores, we'd build India's first Surface Solutions Platform—a digital ecosystem connecting paint manufacturers, contractors, architects, and consumers. Think of it as "Uber for painting services" meets "Netflix for color design." Consumers get quality-assured painters, transparent pricing, and design tools. Contractors get leads, working capital, and training. We monetize through paint sales, service commissions, and data insights.

This platform strategy leverages our contractor relationships while creating network effects that manufacturing alone cannot provide. Once 100,000 contractors depend on our platform for business, switching to competing paint brands becomes economically irrational. The platform, not the paint, becomes the moat.

Fourth Priority: The Southeast Asian Champion

While competitors fight over India, we'd quietly build a Southeast Asian empire. Bangladesh, Vietnam, Myanmar, and Cambodia are where India was 15 years ago—rapid urbanization, rising incomes, and underdeveloped paint markets. We'd acquire local champions in each market, leveraging Kansai's technology and our Indian operational expertise.

The strategy: become the "Asian Paints of Southeast Asia" before Asian Paints or Grasim arrive. These markets offer 20%+ growth rates, limited competition, and first-mover advantages. By 2030, international operations would contribute 30% of revenues and 40% of profits, reducing India dependence.

Fifth Priority: The Sustainability Transformation

We'd make Kansai Nerolac India's first carbon-neutral paint company by 2030. This isn't corporate virtue signaling but hard-nosed strategy. Environmental regulations will inevitably tighten. Carbon taxes will make unsustainable products uneconomical. Green building certifications will mandate eco-friendly materials. By moving first, we capture innovation rents and shape regulations favorably.

The implementation: solar-powered plants, water-free manufacturing, plant-based raw materials, and paint recycling programs. We'd create "Nerolac Green"—a premium sub-brand commanding 25% price premiums from environmentally conscious consumers. The sustainability story also attracts ESG-focused investors, potentially re-rating our valuations.

Cultural Revolution: From Japanese Subsidiary to Indian Multinational

The organizational transformation would be equally radical. We'd shift from being Kansai Paint's Indian subsidiary to being an Indian multinational with Japanese DNA. This means faster decision-making, local innovation, and risk-taking. We'd establish an Innovation Fund with ₹100 crores annually for employees to pursue breakthrough ideas without bureaucratic approval.

We'd restructure into three distinct units: Industrial (defend and grow), Digital Platforms (build and scale), and International (expand and acquire). Each unit would have different KPIs, compensation structures, and cultural norms. Industrial rewards reliability; Digital rewards growth; International rewards entrepreneurship.

The Capital Allocation Revolution

We'd fundamentally restructure capital allocation. Instead of spreading resources across 20 initiatives, we'd concentrate on 5 game-changers. The ₹800 crore cash reserve would fund acquisitions in Southeast Asia and digital platform development. We'd lever up to 2x EBITDA—still conservative but providing ₹2,000 crores for transformation investments.

We'd also implement a dual-class share structure (subject to regulatory approval), where Kansai Paint retains control through super-voting shares while economic ownership broadens. This allows raising growth capital without diluting Japanese control—addressing both parent company concerns and growth requirements.

The 10-Year Vision: From Paint Manufacturer to Surface Intelligence Company

By 2035, Kansai Nerolac wouldn't be a paint company but a "surface intelligence" company. Every surface we coat would be smart—monitoring structural health, adjusting thermal properties, purifying air, or generating energy. Paint becomes the substrate for sensors, connectivity, and intelligence. A building coated with Nerolac wouldn't just look good—it would think, adapt, and respond.

This seems fantastical today, but technological convergence makes it inevitable. When surfaces become intelligent, the company that controls surface coatings controls the interface between physical and digital worlds. The patents we file today, the partnerships we build now, and the capabilities we develop determine who captures value from this transformation.

The Final Reflection

Kansai Nerolac's story ultimately asks: Can century-old companies reinvent themselves? Can industrial champions become consumer brands? Can Japanese conservatism coexist with Indian entrepreneurship? The answers determine not just one company's fate but offer lessons for every legacy business facing disruption.

The company's centennial journey—from colonial paint supplier to Japanese subsidiary to potential regional champion—demonstrates business resilience and adaptation. But past success doesn't guarantee future relevance. In India's hypercompetitive paint market, standing still means falling behind.

If we were CEOs, we'd embrace radical transformation over incremental improvement. The choice isn't between industrial and decorative, traditional and digital, Indian and international. It's about creating new categories where historical weaknesses become irrelevant and existing strengths compound. Kansai Nerolac doesn't need to beat Asian Paints at their game—it needs to invent a new game altogether.

The next decade will determine whether Kansai Nerolac remains a footnote in Indian business history or writes its most important chapter yet. The ingredients exist—technical expertise, financial strength, Japanese backing, and industrial relationships. What's needed is strategic courage to abandon comfortable positions for uncertain but potentially transformative futures.